Abstract

Aims

Assessing the value of single or short-term therapies (SSTs) within traditional cost-effectiveness analyses (CEAs) has been a topic of discussion as the number of SSTs increases, particularly regarding the effect of discounting on valuation. To quantify the impact of discounting in economic evaluations, a CEA of a hypothetical SST and equivalent chronic therapy was conducted using standard methods.

Materials and methods

A lifetime Markov model was developed for a hypothetical chronic, progressive disease that could be treated with an SST, chronic therapy, or no novel treatment, termed standard of care (SoC). Incremental cost-effectiveness ratios (ICERs) with quality-adjusted life years (QALYs) comparing SST vs. SoC and an equivalent chronic therapy vs. SoC were assessed from a payer perspective. Both treatments had equal benefits and undiscounted lifetime costs; 3% discounting was applied to costs/benefits in the base case, and the impact of discounting was assessed.

Results

In the base case example, both the SST and equivalent chronic therapy vs. SoC had ICERs of $86,000/QALY without discounting. With 3% discounting, the ICER for the SST increased by 116% ($186,000/QALY) while the ICER for the chronic therapy increased by 10% ($95,000/QALY) despite equal clinical benefit. In scenario analyses, the ICER of the SST was consistently higher than the equivalent chronic therapy across a range of assumptions/inputs. Varying the cost/benefit discount rates had a greater impact on the SST. Differences in the ICERs between the therapies increased with increasing life expectancy/time horizon.

Limitations

The simple model structure may not be reflective of acute or more complex diseases. Also, the scenario of perfect equivalency in efficacy and lifetime costs is hypothetical.

Conclusions

This quantitative assessment showed the extent to which SST CEAs are highly sensitive to discounting, resulting in worse value assessments for SSTs than equivalent chronic therapies.

Introduction

Single or short-term therapies (SSTs), including gene therapies, may offer substantial health gains as they have the potential to provide lifetime benefits from a single treatment. By 2025, between 10 and 20 gene therapy products are estimated to be approved by the United States (US) Food and Drug Administration (FDA) each yearCitation1. In anticipation of the growing number of SSTs, efforts to comprehensively determine the value of these novel therapies are underway.

Cost-effectiveness analysis (CEA) is a commonly applied approach to estimate the value of a therapy in terms of the incremental costs and health benefits compared to an alternative therapy or other standard of care (SoC). These assessments not only guide health policy, but also inform health resource allocationCitation2,Citation3. While CEAs can also evaluate health services and procedures, a substantial majority assess therapies, specifically chronic therapiesCitation4, as there are not as many SSTs currently available. There are numerous challenges with using the traditional CEA framework to assess SSTs, including evaluation of clinical effectiveness, uncertainties around long term durability, accommodation of up-front treatment costs, and the potential application of additional aspects of valueCitation5–9. Previous studies have also suggested that the application of equivalent discount rates to both costs and benefits, as recommended by most guidelines and typical of the majority of CEAsCitation10, is a potential bias against SSTs given their up-front costs and potential long-term benefitsCitation11–13. As a result, there is ongoing discussion regarding whether traditional CEA methods, including standard discounting, should be adapted for SSTsCitation5,Citation14,Citation15.

Although the potential impact of discounting on the economic evaluation of SSTs has been describedCitation11,Citation12, it has yet to be quantified and compared to that of chronic therapies because of complexities in typical disease-specific models, the few SSTs currently available, and the underlying differences in treatment costs and benefits for those few diseases in which both SSTs and chronic therapies are approved. Thus, a disease-agnostic model was constructed to quantitatively assess the potential impact of discounting on an SST vs. a theoretically equivalent chronic therapy with the same clinical benefit using a traditional CEA. The model offers the opportunity to isolate the impact of discounting without potential confounding factors, such as unequal treatment benefits, differing costs/utilities, and varying health states across different diseases.

Methods

This study assessed the long-term costs and clinical benefits of two hypothetical treatments vs. SoC for a long-term chronic, progressive disease. The primary outcome was the incremental cost per QALY (ICER).

Model structure

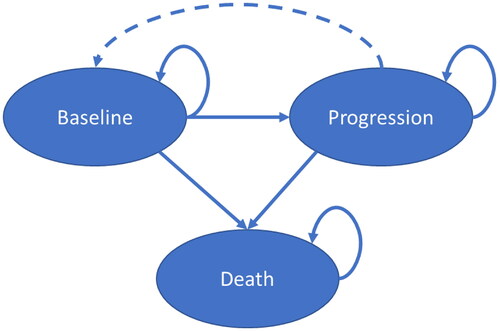

This study used a de novo disease-agnostic Markov model developed in Microsoft Excel to simulate the effect of SSTs and chronic therapies for a homogenous cohort. The model assessed a hypothetical chronic, progressive disease using three health states: baseline, progression, and death (). With treatment, patients could transition from progression to baseline, reflecting one benefit of treatment. While a three-state model is relatively simple, it has been used in CEAs for numerous treatments, including those for COVID-19, HIV, obesity, and cancerCitation16–24.

Figure 1. Model structure. Patients can only transition from progression back to baseline with treatment.

Treatment costs and efficacy

Two hypothetical treatments were assessed: an SST and a clinically-equivalent chronic therapy. The SST treatment cost was the average wholesale acquisition cost of FDA-approved gene-based therapies at the time of the analysis ($1,500,000)Citation25,Citation26. It was assumed the SST was given one time at the start of the analysis. The cost of chronic therapy, administered continuously in the baseline and progression states, amortized the undiscounted SST treatment costs over the patients’ lifetime ($54,000/year in the base case).

Both hypothetical treatments increased survival and improved utility by slowing disease progression and permitting a return to the baseline state. Hazard ratios (HRs) for nonfatal events ranged from 0.45 to 0.85, with a base case value of 0.65 (). For context, a meta-analysis of statin clinical trials showed a range of HRs from 0.52 to 0.94 for nonfatal myocardial infarction, with an overall value of 0.71Citation27. HRs for fatal events ranged from 0.60 to 0.98. This is similar to all-cause mortality HRs for neoadjuvant chemoradiotherapy and surgery for esophageal carcinoma (range, 0.40 to 0.96; overall, 0.81)Citation28.

Table 1. Input values.

Transition probabilities, direct medical costs, and utilities

Annual transition probabilities, direct medical costs, and utilities were selected from appropriate ranges (intentionally chosen not to represent any specific disease) based on expert opinion (). Specifically, annual transition probabilities ranged from 2% to 25% in the base case. For context, these transition probabilities were similar to those reported for secondary, progressive multiple sclerosis (range, 0.2% to 35%)Citation29 and Alzheimer’s disease (range, 2% to 42%)Citation30. All-cause mortality risk was estimated based on US Center for Disease Control and Prevention life tablesCitation31.

The direct medical costs for the progression state in the base case analysis was $100,000/year. This is similar to patients diagnosed with spinal muscular atrophy (SMA) by their first birthday ($112,644/year)Citation32. The direct medical costs ranged up to $200,000/year in scenario analyses, which is between the direct medical costs of urea cycle disorder ($140,044/year)Citation33 and hemophilia A ($614,886/year)Citation34.

Utility values ranged from 1.0 (perfect health) to 0.05. For context, a review of 1,000 published utility values showed a wide range of estimates across health states, with an overall range from 1.0 to −0.12Citation35. Specifically, health state utilities for breast cancer ranged from 0.16 to 0.99 while those for severe angina ranged from 0.354 to 0.707. The wide range of estimates reflect variations in disease severity, country, instrument, tariffs, and rater (proxy vs. self).

Other inputs and assumptions

The study assessed a 5-year-old over a lifetime horizon, reflecting a disease with pediatric onset and allowing for substantial health gains. The model used annual cycles with half-cycle corrections. A discount rate of 3% per annum was applied to costs and benefits in the base case. This discounting rate was based on the standard practice in the USCitation36 and reflects the economic concept that current costs (and health benefits) have greater value than those in the future. A US payer perspective was adopted. Results were rounded to the nearest $1,000.

Sensitivity and scenario analyses

Numerous sensitivity and scenario analyses were performed to evaluate the impact of the inputs on the results. To account for model uncertainty, probabilistic sensitivity analysis (PSA) was conducted. Input values were sampled from uniform distributions (). Although uniform distributions are atypical in a disease-specific CEA, a uniform distribution was used to ensure the analyses covered a wide range of inputs and did not over-sample values closer to the base case assumptions. SST treatment costs, HRs, transition probabilities, direct medical costs, and utilities were varied in 1,000 scenarios. For each SST cost, the equivalent chronic treatment’s annual costs were calculated by amortizing the undiscounted SST cost over the patients’ lifetime.

In scenario analyses, the values used for discount rates for costs and benefits were disassociated to examine the impact of differential discounting. Discount values ranged from 0% to 5%, where the benefit discount rate was never higher than that for costs. HRs were also varied to see how the ICERs changed with varying health gains. To ensure consistency, the relationship between the HRs was maintained and the SST cost remained at $1,500,000. The chronic costs varied based on the patients’ overall survival by amortizing the undiscounted SST cost over the patients’ lifetime.

Additional scenarios were performed to evaluate those assessed in a study by Pearson et al.Citation15, which examined the maximum “value-based” price of hypothetical potential cures for hypothetical diseases of varying severity. In that analysis, the “value-based” price was determined without discounting, simply stating the hypothetical treatment benefits (QALYs gained and annual cost offsets by replacing SoC). The first scenario analyzed a fatal disease in a 5-year-old, who would have died in 10 years with SoC. The hypothetical cure would add 50 undiscounted QALYs through increased survival. The second scenario evaluated a hypothetical cure for a nonfatal disease in a 15-year-old who would gain 0.2 QALYs per year in improved utility over 50 yearsCitation15. The inputs in this study’s disease-agnostic model were adjusted to recreate the undiscounted results (Supplemental Table 1). Using the disease-agnostic model and standard 3% discounting, the maximum “value-based” price of the SST and an equivalent chronic therapy were calculated, assuming the same $100,000/QALY cost-effectiveness threshold as in the original analysis.

Results

Base case analysis

The results for the base case scenario comparing SST vs. SoC and the equivalent chronic therapy vs. SoC are shown in . By design, clinical benefits gained due to treatment were equal for both therapies, as were lifetime undiscounted incremental costs. Without discounting, the ICER was $86,000/QALY for both the SST and chronic therapy vs. SoC. When a 3% discount rate was applied to both costs and benefits, chronic therapy had an ICER of $95,000/QALY, 10% higher than when no discounting was applied. For the chronic therapy, discounting substantially reduced the incremental costs by 50% and QALYs gained by 54%. Overall, discounting costs and benefits resulted in a relatively small impact on the ICER for the chronic therapy.

Table 2. Impact of discounting and timing of treatment for the base case.

In contrast to a chronic therapy, the treatment cost of an SST is incurred up-front whereby discounting has no effect on the value included in the analysis. Indeed, discounting had a nominal impact on total incremental costs of the SST vs. SoC (−2%; ). On the other hand, QALYs gained were reduced by 54% when 3% discounting was applied (by definition equivalent to the chronic therapy analysis). Thus, the net impact of discounting both costs and benefits for the SST resulted in a much higher ICER than the chronic therapy. In the base case, the ICER of an equivalent SST vs. SoC was $186,000/QALY, above standard cost-effectiveness thresholds and almost double that of the equivalent chronic therapy. The ICER with 3% discounting was 116% higher than without discounting.

Probabilistic sensitivity analysis

Of the 1,000 PSA scenarios analyzed, the ICER for the SST was always higher than that for the equivalent chronic therapy, although the magnitude of the difference varied. When the chronic therapy was within the standard cost-effectiveness threshold of $150,000/QALY, the equivalent SST was above the threshold in 52% of the iterations.

Impact of varying discount rates on ICER per QALY

The ICER of the chronic therapy ranged from $86,000 to $104,000 when applying equal discount rates for costs and health benefits (). Use of the same discount rate for costs and benefits had a much larger impact on the ICER of the SST, ranging from $86,000 to $282,000. Furthermore, the ICERs of both the SST and the equivalent chronic therapy were noticeably impacted by variations in only the benefit discount rate. However, increasing the cost discount rate noticeably improved the ICER of the chronic therapy, but had a negligible impact on the ICER result for the SST.

Table 3. Impact of varying discount rates on ICER per QALY.

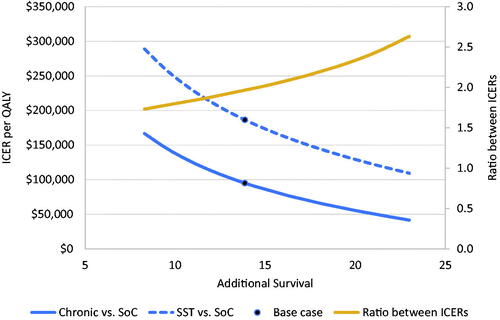

Impact of varying treatment efficacy

shows the impact of varying treatment efficacy on the ICER of each therapy. Variation in HRs yielded 8 to 23 undiscounted life years gained. With an increased survival of 8 and 23 years, the ICER of the SST was $289,000 and $109,000, respectively, and the ICER of the chronic therapy was $167,000 and $41,000, respectively. For every treatment efficacy analyzed, the ICER of the SST was higher than that for the equivalent chronic therapy. As treatment benefits increased, the ratio between the ICERs also increased, ranging from 1.73:1 to 2.63:1 with 8 to 23 life years gained, respectively.

Figure 2. ICER per QALY for both hypothetical therapies with varying survival gains. Gold line represents the difference in value. Abbreviations. ICER, incremental cost-effectiveness ratio; QALY, quality-adjusted life year; SoC, standard of care; SST, single or short-term therapy.

Impact of discounting on “value-based” price

Additional scenarios were performed using the disease-agnostic model to evaluate two previously described hypothetical SSTs for diseases of varying severityCitation15. In the first scenario (a hypothetical cure that increased survival for a fatal disease), Pearson et al.Citation15 showed a maximum “value-based” price of $7,000,000. In contrast, using the disease-agnostic model and 3% discounting of costs and benefits, the maximum “value-based” price for the SST was $3,300,000 (). The price for the equivalent chronic therapy was $120,000/year, which is lower than the SoC cost due to the increase in survival and the relatively short period for cost offsets.

Table 4. Impact of discounting on “value-based” pricing.

In the second scenario (a hypothetical cure that increased utility for a nonfatal disease), the maximum “value-based” price was $11,000,000 in Pearson et al.Citation15. Using the disease-agnostic model and 3% discounting of costs and benefit, the maximum “value-based” price was $5,300,000 for the SST and $220,000/year for the equivalent chronic therapy (). Thus, discounting has a substantial impact on the overall value assessments of the SSTs, reducing the “value-based” price by more than 50% in both scenarios.

Discussion

As the number of SSTs under development continues to increase, it is important to understand how these therapies fit within a traditional CEA framework, historically designed to evaluate chronic therapiesCitation4. The present study demonstrated that the ICER of an SST is consistently higher than that of an equivalent chronic therapy, which aligns with a recent International Society for Pharmacoeconomics and Outcomes Research (ISPOR) panel reportCitation7. In the base case analysis, the ICER of the SST was nearly double the ICER of the equivalent chronic therapy. This discrepancy is noteworthy as the ICERs of the two therapies without discounting were equivalent by design. Furthermore, although the ICER of the chronic therapy was within the standard cost-effectiveness threshold, the equivalent ICER of the SST noticeably exceeded the threshold. The ICER of the SST was consistently higher than that of the equivalent chronic therapy across a range of inputs (costs, risks, utilities, and hazard ratios), with many scenarios where the chronic therapy was within standard cost-effectiveness thresholds, but the equivalent SST was not. Moreover, the discrepancy between the ICERs increased with greater health benefits. Thus, although the SST and chronic therapy had projected exactly the same treatment benefits, the CEA results suggest that the two treatments have different values. This inadvertently suggests that chronic therapies provide greater value than SSTs despite equivalent benefits and costs.

The model developed in this study allowed for the direct comparison of ICERs of equivalent SSTs and chronic therapies to quantify the impact of discounting on SST valuations compared to those of chronic therapies offering the same benefits. This study has quantified the impact of discounting on the valuation of treatments with one-time administration. With the increasing number of SSTs available, a few CEAs have considered the incremental value of the SST over an available chronic therapyCitation37–39 although these therapies were inherently different in the benefits provided and the lifetime treatment costsCitation37–39. The model used a hypothetical pediatric patient over a lifetime horizon; therefore, further studies are necessary to evaluate the impact of these treatments as a function of age.

The sensitivity of SSTs to discounting described in this study is supported by real-world examples. For example, in an assessment of onasemnogene abeparvovec (a gene therapy for SMA) vs. best supportive care, the base case ICER was £177,061/QALY with 3.5% discounting of costs and benefits, compared to £99,423/QALY (45% lower) without discountingCitation40. In contrast, the ICER for nusinersen (a chronic SMA therapy) vs. best supportive care was only improved by 15% without discountingCitation40. In another assessment of betibeglogene autotemcel (a gene therapy for beta-thalassemia), removing the 3% discount rate improved the ICER from $95,000/QALY to dominating SoCCitation41. Similarly, reducing the discount rate from 3% to 1.5% for tisagenlecleucel, a chimeric antigen receptor T-cell (CAR-T) therapy, improved the ICER by approximately 20%Citation42. The impact of discounting on SSTs is also similar to that observed with preventative interventions, where costs are incurred upfront but benefits may be obtained in the futureCitation43. Analysis of the human papillomavirus 16/18 vaccine, used to prevent cervical cancer, showed a five-fold increase in QALYs gained without the 3% discount rateCitation44. It should be noted that some SSTs provide value due to cost offsets and have limited, if any, QALYs gained, such as valoctocogene roxaparvovec, a gene therapy approved to treat hemophilia ACitation45. The evaluations of these SSTs will be negligibly influenced by the selected benefit discount rate.

While discounting future costs is largely accepted as a best practice in various economic modeling, discounting of health benefits is more controversial. Specific points of controversy include choice of discount model (e.g. constant vs. hyperbolic), discount rate height, and equal discounting of costs and benefitsCitation46. Furthermore, discounting treats both delayed and prolonged benefits the same (e.g. an additional year of life 5 years from now is valued the same whether it was the first life year gained due to treatment or the fifth). Postma et al.Citation47 highlighted the dependence of future health gains on prior survival as support for changes to the constant and equal discounting of benefits over time. However, most current CEA guidelines in various countries recommend discounting costs and benefits equally with rates varying from 0% to 5%Citation46. The use of equal discounting has been influenced by two arguments: the consistency argument proposed by Weinstein and StasonCitation48 and the postponement dilemma described by Keeler and CretinCitation49. Using differential discounting with a higher rate for costs than benefits, Keller and Cretin showed that a therapy’s cost-effectiveness would improve each year that it is postponed and theorized that decision makers would ultimately postpone the intervention indefinitelyCitation49. However, indefinite postponing does not occur in practiceCitation46,Citation50,Citation51.

Because equal discounting negatively impacts therapies with upfront costs and sustained health benefitsCitation52, arguments in favor of differential discounting with lower rates for benefits are increasing in recent yearsCitation47,Citation51–54. For example, the Zorginstituut Nederland recommends discounting costs at 4% and benefits at 1.5%Citation43. John et al.Citation52 suggest the benefit discount rate should be 0.3% to 1.5% lower than the cost discount rate in Germany. Nonetheless, the majority of CEAs performed in the US continue to use 3% discounting for both costs and benefitsCitation2.

The growing pipeline of SSTs has prompted questions about their affordability. However, it is important that CEAs are undertaken without adjustments for budget impact concernsCitation55, to ensure that value and affordability are not conflated. Without discounting, the Pearson publicationCitation15 estimated potential “value-based” prices of $7,000,000 for a hypothetical new cure for a fatal disease in a 5-year-old patient and $11,000,000 for a hypothetical new cure for a nonfatal disease in a 15-year-old. Acknowledging the hardship this might cause health care budgets from a budget impact perspective, numerous proposals were suggested to reduce the value assessment of SSTsCitation5,Citation14,Citation15. Recent assessments by the Institute for Clinical and Economic Review for SSTs have included scenario analyses based on these proposals, including accrediting 50% of the shared savings back to the healthcare system and capping the annual cost offsets included in the analysisCitation41,Citation45,Citation56. This study, however, shows the value assessment for both hypothetical SSTs are substantially impacted by discounting, which was not considered in the original analysis. Application of the proposed adjustments to the CEA in Pearson et al.Citation15 would further reduce the valuation of the SSTs. Therefore, any studies aimed at informing methodological or policy changes to address the valuation of SSTs should be performed in a manner similar to a traditional CEA, including discounting.

The purpose of CEA is to determine a therapy’s value to inform resource allocationCitation57, and leveraging a standard approach allows for relative valuation across a range of diseases and treatmentsCitation58. Thus, it is reasonable to consider modifying approaches when assessing SSTsCitation5,Citation14,Citation15 in a standardized mannerCitation10 rather than ad hoc adjustments, which have been applied on a case-by-case basis, including for mifamurtideCitation59. Mifamurtide is indicated for a rare type of osteosarcoma and administered over 36 weeks with potential benefits lasting a lifetime, making it SST-likeCitation59. NICE found the CEA was substantially sensitive to the benefit discount rateCitation60. Specifically, all benefits would be discounted away after 22 years with the standard UK 3.5% discount rate compared to 49 years with a 1.5% rateCitation61. Ultimately, the 1.5% benefit discount rate was used given the curative potential of the therapy and the expected sustained benefitCitation60.

SSTs may have other unique elements of value that should be considered but are not generally included in traditional CEAs. For example, CEAs do not consider potential patient or caregiver preference for the convenience of an SST. Current studies are underway to evaluate patient preferences for gene therapies and gain insight on other elements of potential valueCitation62–64. In patients with hemophilia A, dosing frequency/durability of treatment was viewed as the most important gene therapy attribute even over efficacy (i.e. effect on annual bleeding) and safety uncertaintiesCitation65. In patients with SMA or their caregivers, preference was given to one-time administration over repeat intrathecal injectionsCitation63 although this burden did not get quantified in a recent CEACitation65. While some CEAs include non-adherence for chronic therapies, it is not considered consistently; therefore, the relative value of SSTs in terms of adherence will likely be muted. Additionally, CEAs omit other recurring costs associated with chronic therapies, such as continuous provider visits to refill prescriptions, travel for treatments, and processing prescription coverage and pre-authorizations. Not including these characteristics and costs can diminish the relative valuation of SSTs relative to chronic therapies. Furthermore, while discounting generally incorporates loss of exclusivityCitation66, this does not apply to SSTs and many chronic therapies have real price increases beyond inflation (e.g. price increases outpaced inflation for nearly half of Medicare-covered drugs in 2020)Citation67, which are not included in most CEAs.

Universal adjustments to CEAs ideally would allow for comparisons to those that have been previously completed, as updating prior CEAs would be prohibitively time-consuming. Instead of ad hoc adjustments for some SSTs, it is worth discussing a few modifications to the traditional CEA framework to ensure fair assessments of SSTs. First, payment-over-time options, which are aimed at addressing affordabilityCitation67, would reduce the discrepancy between SSTs and chronic therapies observed in this study. Most options currently under consideration in the US consider a 3- or 5-year horizon, given approximately 20% of patients switch health plans annuallyCitation68. Thus, most pay-over-time options would have a nominal effect on the valuation of an SST as this is a transient period of time within most lifetime models. Second, a lower discount rate for benefits could be applied, which would partially mitigate the discrepancies seen between SSTs and chronic therapies. Third, a normalization factor (i.e. ratio of discounted life years to undiscounted life years for treated patients over the full model horizon) may be applied to SSTs, which would effectively assess an SST like an equivalent chronic therapy; however, such an approach has yet to be established. Finally, assessing broader elements of value not generally captured within most CEAs, including those described in the ISPOR value flowerCitation69, may be even more important for capturing the full value obtained with SSTs. Ultimately, further research is needed to fully understand the CEA of SSTs within the traditional framework and to examine the impact of potential modifications. Based on the findings of this study, it is recommended that any modifications to the CEA framework for SSTs be universal rather than case-by-case adjustments based on the results of a particular therapy’s CEA.

The present study is limited by the model structure may not be reflective of acute or more complex diseases. However, three-state Markov models have been used in a variety of diseasesCitation16–24. In addition, inputs were selected without regards to specific diseases or treatments. While this strengthens the generalizability, application of these insights to a particular therapy or disease would require the development of a disease-specific model. Also, the hypothetical scenario of perfectly equivalent SST and chronic therapies is unrealistic as there are no known examples of two therapies (one SST and one chronic therapy) with the same efficacy and lifetime costs. Furthermore, as with all therapies, there are uncertainties around durability of treatment effect that necessitate extrapolation to a lifetime horizon; however, currently approved gene therapies have shown long-term durability up to 7.5 yearsCitation70,Citation71. Finally, the model assumed that chronic therapy costs do not decline due to going off-patent.

Conclusions

Although there has been previous discussion on the appropriate use of discounting in evaluations of SSTsCitation11–13, this study is the first, to the authors’ knowledge, that quantitatively demonstrates the impact of discounting of SSTs due solely to one-time administration without the idiosyncrasies of disease or treatment-specific inputs. Compared with chronic therapies with equal treatment costs and benefits, SSTs consistently had higher ICERs vs. SoC due to discounting of treatment benefits and these differences increased with increasing health benefits. This study suggests that value frameworks may need to be adapted for the evaluation of SSTs to ensure equitable assessments relative to chronic therapies.

Transparency

Declaration of funding

This work was supported by Sarepta Therapeutics, Inc. who designed and funded the analysis. Writing and editorial support was funded by Sarepta Therapeutics, Inc. Open access fees were funded by Sarepta Therapeutics, Inc.

Declaration of financial/other relationships

ACK, LES, KLG are employees of Sarepta Therapeutics, Inc. and may own stock/options in the company. DCM has served as a consultant to Sarepta Therapeutics, Inc. Peer reviewers on this manuscript have no relevant financial or other relationships to disclose.

Author contributions

All authors had full access to the data and analyzed and interpreted the data. ACK and LES wrote the original draft. All authors edited, reviewed, and approved the final manuscript for submission.

Supplemental Material

Download MS Word (13.8 KB)Acknowledgements

The authors thank Marjet Heitzer, PhD of 360 Medical Writing for providing medical writing and editorial support.

Data availability statement

Qualified researchers may request access to the data that support the findings of this study from Sarepta Therapeutics Inc., by contacting [email protected].

References

- FDA Press Release. Statement from FDA Commissioner Scott Gottlieb, M.D. and Peter Marks, M.D., Ph.D., Director of the Center for Biologics Evaluation and Research on new policies to advance development of safe and effective cell and gene therapies; [accessed 2022 Jul 14]. Available from: https://www.fda.gov/news-events/press-announcements/statement-fda-commissioner-scott-gottlieb-md-and-peter-marks-md-phd-director-center-biologics

- Institute for Clinical and Economic Review. 2020-2023 value assessment framework; [accessed 2022 Jul 27]. Available from: https://icer.org/wp-content/uploads/2020/10/ICER_2020_2023_VAF_013120-4.pdf

- National Institute of Health and Care Excellence. The guidelines manual. Process and methods [PMG6]; 2012 [accessed 2022 Oct 16]. Available from: https://www.nice.org.uk/process/pmg6/chapter/assessing-cost-effectiveness

- Neumann PJ, Ollendorf DA. Why so few value assessments on health services and procedures, and what should be done?; 2022 [accessed 2023 Feb 16]. Available from: https://www.healthaffairs.org/content/forefront/why-so-few-value-assessments-health-services-and-procedures-and-should-done

- Institute for Clinical and Economic Review. Adapted value assessment methods for high-impact “single and short-term therapies” (SSTs); [accessed 2022 Jul 13]. Available from: https://icer.org/wp-content/uploads/2020/10/ICER_SST_FinalAdaptations_111219.pdf

- National Institute for Health and Care Excellence. Interim process and methods of the Highly Specialised Technologies Programme updated to reflect 2017 changes; [accessed 2022 Jul 17]. Available from: https://www.nice.org.uk/media/default/about/what-we-do/nice-guidance/nice-highly-specialised-technologies-guidance/hst-interim-methods-process-guide-may-17.pdf

- Henderson N. ISPOR Issue Panel roundup: are our HTA methods fit for purpose for gene therapies?; [accessed 2022 Jul 13]. Available from: https://www.ohe.org/news/ispor-issue-panel-roundup-are-our-hta-methods-fit-purpose-gene-therapies

- Taylor C, Jan S, Thompson K. Funding therapies for rare diseases: an ethical dilemma with a potential solution. Aust Health Rev. 2018;42(1):117–119.

- Aballea S, Thokagevistk K, Velikanova R, et al. Health economic evaluation of gene replacement therapies: methodological issues and recommendations. J Mark Access Health Policy. 2020;8(1):1822666.

- Williams AO, Rojanasarot S, McGovern AM, et al. A systematic review of discounting in national health economic evaluation guidelines: healthcare value implications. J Comp Eff Res. 2023;12(2):e220167.

- Drummond MF, Neumann PJ, Sullivan SD, et al. Analytic considerations in applying a general economic evaluation reference case to gene therapy. Value Health. 2019;22(6):661–668.

- Jonsson B, Hampson G, Michaels J, et al. Advanced therapy medicinal products and health technology assessment principles and practices for value-based and sustainable healthcare. Eur J Health Econ. 2019;20(3):427–438.

- Clay E, Pochopien M, Aballea S, et al. Differentiating discount rates in cost-effectiveness evaluations in the context of gene therapies. Value Health. 2018;21:s363.

- Chapman RH, Kumar VM, Whittington MD, et al. Does cost-effectiveness analysis overvalue potential cures? Exploring alternative methods for applying a "shared savings" approach to cost offsets. Value Health. 2021;24(6):839–845.

- Pearson SD, Ollendorf DA, Chapman RH. New cost-effectiveness methods to determine value-based prices for potential cures: what are the options? Value Health. 2019;22(6):656–660.

- Bullement A, Knowles ES, DasMahapatra P, et al. Cost-Effectiveness analysis of rFVIIIFc versus contemporary rFVIII treatments for patients with severe hemophilia a without inhibitors in the United States. Pharmacoecon Open. 2021;5(4):625–633.

- Calamia M, McBride A, Abraham I. Economic evaluation of polatuzumab-bendamustine-rituximab vs. tafasitamab-lenalidomide in transplant-ineligible R/R DLBCL. J Med Econ. 2021;24(sup1):14–24.

- Cao Y, Zhao L, Zhang T, et al. Cost-Effectiveness analysis of adding daratumumab to bortezomib, melphalan, and prednisone for untreated multiple myeloma. Front Pharmacol. 2021;12:608685.

- Chakraborty H, Hossain A, Latif MAHM. A three-state continuous time Markov chain model for HIV disease burden. J Applied Stat. 2019;46(9):1671–1688.

- Chen TA, Baranowski T, Moreno JP, et al. Obesity status transitions across the elementary years: use of Markov chain modelling. Pediatr Obes. 2016;11(2):88–94.

- Li N, Zheng H, Huang Y, et al. Cost-effectiveness analysis of olaparib maintenance treatment for germline BRCA-mutated metastatic pancreatic cancer. Front Pharmacol. 2021;12:632818.

- Lin S, Luo S, Gu D, et al. First-line durvalumab in addition to etoposide and platinum for extensive-stage small cell lung cancer: a U.S.-based cost-effectiveness analysis. Oncologist. 2021;26(11):e2013–e2020.

- Sheinson D, Dang J, Shah A, et al. A cost-effectiveness framework for COVID-19 treatments for hospitalized patients in the United States. Adv Ther. 2021;38(4):1811–1831.

- Institute for Clinical and Economic Review. Cognitive and mind-body therapies for chronic low back and neck pain: effectiveness and value; 2017 Nov 6 [accessed 2022 Aug 23]. Available from: https://icer.org/wp-content/uploads/2020/10/CTAF_LBNP_Final_Evidence_Report_110617.pdf

- Novartis Press Release. AveXis announces innovative Zolgensma® gene therapy access programs for US payers and families; [accessed 2022 Jul 13]. Available from: https://www.novartis.com/news/media-releases/avexis-announces-innovative-zolgensma-gene-therapy-access-programs-us-payers-and-families

- Harper M. Spark therapeutics sets price of blindness- treating gene therapy at $850,000; [accessed 2022 Jul 13]. Available from: https://www.forbes.com/sites/matthewherper/2018/01/03/spark-therapeutics-sets-price-of-blindness-curing-gene-therapy-at-850000/?sh=38d1e92b7dc3

- , Baigent C, Blackwell L, Emberson J, et al. Efficacy and safety of more intensive lowering of LDL cholesterol: a meta-analysis of data from 170,000 participants in 26 randomised trials. Lancet. 2010;376(9753):1670–1681.

- Gebski V, Burmeister B, Smithers BM, et al. Survival benefits from neoadjuvant chemoradiotherapy or chemotherapy in oesophageal carcinoma: a meta-analysis. Lancet Oncol. 2007;8(3):226–234.

- Institute for Clinical and Economic Review. Siponimod for the treatment of secondary progressive multiple sclerosis: effectiveness and value; [accessed 2022 Aug 23]. Available from: https://icer.org/wp-content/uploads/2020/10/ICER_MS_Final_Evidence_Report_062019.pdf

- Potashman M, Buessing M, Levitchi Benea M, et al. Estimating progression rates across the spectrum of Alzheimer’s disease for amyloid-positive individuals using national Alzheimer’s coordinating center data. Neurol Ther. 2021;10(2):941–953.

- Arias E, Xu JQ. United States life tables, 2018. National vital statistics reports. vol. 69. Hyattsville (MD): National Center for Health Statistics; 2020.

- Armstrong EP, Malone DC, Yeh WS, et al. The economic burden of spinal muscular atrophy. J Med Econ. 2016;19(8):822–826.

- Tisdale A, Cutillo CM, Nathan R, et al. The IDeaS initiative: pilot study to assess the impact of rare diseases on patients and healthcare systems. Orphanet J Rare Dis. 2021;16(1):429.

- Burke T, Asghar S, O'Hara J, et al. Clinical, humanistic, and economic burden of severe hemophilia B in the United States: results from the CHESS US and CHESS US + population surveys. Orphanet J Rare Dis. 2021;16(1):143.

- Tengs TO, Wallace A. One thousand health-related quality-of-life estimates. Med Care. 2000;38(6):583–637.

- Neumann PJ, Sanders GD, Russell LB, et al. editors. Cost-effectiveness in health and medicine. 2nd ed. Oxford: Oxford University Press; 2016.

- Kansal AR, Reifsnider OS, Brand SB, et al. Economic evaluation of betibeglogene autotemcel (beti-cel) gene addition therapy in transfusion-dependent beta-thalassemia. J Mark Access Health Policy. 2021;9(1):1922028.

- Machin N, Ragni MV, Smith KJ. Gene therapy in hemophilia A: a cost-effectiveness analysis. Blood Adv. 2018;2(14):1792–1798.

- Malone DC, Dean R, Arjunji R, et al. Cost-effectiveness analysis of using onasemnogene abeparvocec (AVXS-101) in spinal muscular atrophy type 1 patients. J Mark Access Health Policy. 2019;7(1):1601484.

- National Institute for Health and Care Excellence. Onasemnogene abeparvovec for treating spinal muscular atrophy; [accessed 2022 Jul 31]. Available from: https://www.nice.org.uk/guidance/hst15/documents/committee-papers

- Institute for Clinical and Economic Review. Betibeglogene autotemcel for beta thalassemia: effectiveness and value. Final evidence report; 2022 Jul 19 [accessed 2022 Jul 28]. Available from: https://icer.org/wp-content/uploads/2021/11/ICER_Beta-Thalassemia_Final-Report_071922.pdf

- Whittington MD, McQueen RB, Ollendorf DA, et al. Long-term survival and value of chimeric antigen receptor T-cell therapy for pediatric patients with relapsed or refractory leukemia. JAMA Pediatr. 2018;172(12):1161–1168.

- Zorginstituut Nederland. Guideline for economic evaluations in healthcare; 2016 [accessed 2022 Jul 14]. Available from: https://english.zorginstituutnederland.nl/binaries/zinl-eng/documenten/reports/2016/06/16/guideline-for-economic-evaluations-in-healthcare/Guideline+for+economic+evaluations+in+healthcare.pdf

- Westra TA, Parouty M, Brouwer WB, et al. On discounting of health gains from human papillomavirus vaccination: effects of different approaches. Value Health. 2012;15(3):562–567.

- Institute for Clinical and Economic Review. Valoctocogene roxaparvovec and emicizumab for hemophilia A without inhibitors: effectiveness and Value; 2020 Oct 16; [accessed 2022 Aug 20]. Available from: https://icer.org/wp-content/uploads/2020/10/ICER_Hemophilia-A_Evidence-Report_102620.pdf

- Attema AE, Brouwer WBF, Claxton K. Discounting in economic evaluations. Pharmacoeconomics. 2018;36(7):745–758.

- Postma MJ, Parouty M, Westra TA. Accumulating evidence for the case of differential discounting. Expert Rev Clin Pharmacol. 2013;6(1):1–3.

- Weinstein MC, Stason WB. Foundations of cost-effectiveness analysis for health and medical practices. N Engl J Med. 1977;296(13):716–721.

- Keeler EB, Cretin S. Discounting of life-saving and other nonmonetary effects. Management Sci. 1983;29(3):300–306.

- College voor zorgverzekeringen, Diemen. Guidelines for pharmacoeconomic research, updated version; 2006 Mar [accessed 2022 Jul 13]. Available from: https://heatinformatics.com/sites/default/files/images-videosFileContent/Netherlands%20CVZ%20Pharmacoeconomics%202006.pdf

- Brouwer WB, Niessen LW, Postma MJ, et al. Need for differential discounting of costs and health effects in cost effectiveness analyses. Br Med J. 2005;331(7514):446–448.

- John J, Koerber F, Schad M. Differential discounting in the economic evaluation of healthcare programs. Cost Eff Resour Alloc. 2019;17:29.

- Nord E. Discounting future health benefits: the poverty of consistency arguments. Health Econ. 2011;20(1):16–26.

- Paulden M, O'Mahony JF, McCabe C. Discounting the recommendations of the second panel on cost-effectiveness in health and medicine. Pharmacoeconomics. 2017;35(1):5–13.

- Mauskopf JA, Sullivan SD, Annemans L, et al. Principles of good practice for budget impact analysis: report of the ISPOR task force on good research practices–budget impact analysis. Value Health. 2007;10(5):336–347.

- Institute for Clinical and Economic Review. Gene therapy for hemophilia B and an update on gene therapy for hemophilia A: effectiveness and value. Final evidence report; [accessed 2023 Mar 8]. Available from: https://icer.org/wp-content/uploads/2022/05/ICER_Hemophilia_Final_Report_12222022.pdf

- Drummond M, Brixner D, Gold M, et al. Toward a consensus on the QALY. Value Health. 2009;12 Suppl 1:s31–s35.

- Jamison DT, Breman JG, Measham AR, et al., editors. Priorities in health. Washington (DC): The International Bank for Reconstruction and Development/The World Bank; 2006. Chapter 3, Cost-effectiveness analysis; [accessed 2022 Aug 1]. Available from: https://www.ncbi.nlm.nih.gov/books/NBK10253/

- MEPACT® (mifamurtide) Prescribing Information; [accessed 2022 Aug 1]. Available from: https://www.takeda.com/siteassets/system/hcps/mepact-prescribing-information.pdf

- National Institute for Health and Care Excellence; [accessed 2022 Jul 13]. Available from: https://www.nice.org.uk/guidance/ta235/resources/mifamurtide-for-the-treatment-of-osteosarcoma-pdf-82600372273093

- Ralston S, Floyd D, Ratcliffe M. Differential discouting: capturing the value of living longer and better. Value Health. 2013;16(7):A467.

- Monnette A, Chen E, Hong D, et al. Treatment preference among patients with spinal muscular atrophy (SMA): a discrete choice experiment. Orphanet J Rare Dis. 2021;16(1):36.

- van Overbeeke E, Hauber B, Michelsen S, et al. Patient preferences for gene therapy in haemophilia: results from the PAVING threshold technique survey. Haemophilia. 2021;27(6):957–966.

- Witkop M, Morgan G, O'Hara J, et al. Patient preferences and priorities for haemophilia gene therapy in the US: a discrete choice experiment. Haemophilia. 2021;27(5):769–782.

- Institute for Clinical and Economic Review. Spinraza® and Zolgensma® for spinal muscular atrophy: effectiveness and value; [accessed 2021 Jul 13]. Available from: https://icer.org/wp-content/uploads/2020/10/ICER_SMA_Final_Evidence_Report_110220.pdf

- Hoyle M. Future drug prices and cost-effectiveness analyses. Pharmacoeconomics. 2008;26(7):589–602.

- Cubanski J, Neuman T. Prices increased faster than inflation for half of all drugs covered by Medicare in 2020; [accessed 2022 Jul 13]. Available from: https://www.kff.org/medicare/issue-brief/prices-increased-faster-than-inflation-for-half-of-all-drugs-covered-by-medicare-in-2020/

- Schmickel B, Perry K, Sanchez H, et al. Exploring the truth of reimbursement challenges for cell and gene therapies; [accessed 2022 Aug 1]. Available from: https://trinitylifesciences.com/wp-content/uploads/2021/05/Trinity_Reimbursement_Challenges-6.10.19-1.pdf

- Lakdawalla DN, Doshi JA, Garrison LP, Jr., et al. Defining elements of value in health Care-A health economics approach: an ISPOR special task force report [3]. Value Health. 2018;21(2):131–139.

- Leroy BP, Fischer MD, Flannery JG, et al. Gene therapy for inherited retinal disease: long-term durability of effect. Ophthalmic Res. 2023;66:179–196.

- Mendell JR, Wigderson M, Alecu I, et al. Long-term follow-up of onasemnogene abeparvovec gene therapy in symptomatic patients with spinal muscular atrophy type 1. Abstract presented at the 2023 MDA Clinical & Scientific Conference, Dallas, TX; 2023 Mar 19–22.

- Institute for Clinical and Economic Review. Anti B-cell maturation antigen CAR T-cell and antibody drug conjugate therapy for heavily pre-treated relapsed and refractory multiple myeloma final report; [accessed 2022 Jul 13]. Available from: https://icer.org/wp-content/uploads/2020/10/ICER_Multiple-Myeloma_Final-Report_Update_070921.pdf

- Pickard AS, Law EH, Jiang R, et al. United States valuation of EQ-5D-5L health states using an international protocol. Value Health. 2019;22(8):931–941.