ABSTRACT

This article investigates the differences in the application and impact of digital technologies between manufacturing subsidiaries and lead companies, the principal orchestrators of global automotive value chains. Utilising a dataset of 10 in-depth interviews with automotive industry actors, we analyse headquarters–subsidiary differences in the patterns of digitalisation-driven upgrading. A theoretical framework is offered that explains why the significant upgrading achievements of manufacturing subsidiaries deploying industry 4.0 technologies will not reduce the gap between lead companies and manufacturing subsidiaries in terms of value generation. We show that the concept of ‘industry 4.0’ is much narrower than that of ‘digitalisation’ and transition to smart factories is only part of the digital transformation story. Industry 4.0 technologies contribute to the upgrading of operations, and enable subsidiaries to take on production-related knowledge-intensive assignments (functional upgrading). Conversely, digitalisation serves lead companies’ strategic differentiation efforts, and facilitates achieving competitive advantage: the latter are crucial for value capture.

Introduction

The digital transformation of manufacturing is expected to pose formidable challenges to ‘factory economies’ (Baldwin, Citation2013), i.e. to countries specialising in labour-intensive activities, where economic upgrading has, so far, been driven by efficiency-seeking foreign direct investment (FDI). Digitalisation-driven labour-saving process innovations are projected to result in massive unemployment (Brynjolfsson & McAfee, Citation2014; Ford, Citation2015; Frey & Osborne, Citation2017; LaGrandeur & Hughes, Citation2017), in particular in factory economies (Frey, Osborne, & Holmes, Citation2016) and in countries that fail to bring forth the necessary social, economic and institutional innovations that would facilitate their societies’ adaptation (Stevens & Marchant, Citation2017; UNCTAD, Citation2018).

Moreover, the digitalisation of manufacturing may result in a reconfiguration of the geographical organisation of production, for example, by prompting value chain orchestrators to move production back to home countries or close to end markets (Brettel, Friederichsen, Keller, & Rosenberg, Citation2014; Dachs, Kinkel, & Jäger, Citation2017; Sasson & Johnson, Citation2016; Strange & Zucchella, Citation2017). Consequences may be devastating for factory economies, where production relocation-driven value generation has been the main engine of growth and upgrading.

Contesting gloomy predictions about technological unemployment and calling the arguments about the looming backshoring of production into question, some scholars argue that digital transformation (hereafter DT) gives unprecedented opportunities for FDI hosting factory economies to increase the knowledge-intensity of their contribution to, and their overall share in, global value chain-level value added.

One of the key propositions is that DT will bring about capital deepening in factory economies. As a result of the path dependence of offshoring practices (Lewin, Massini, & Peeters, Citation2009), lead companies’ existing manufacturing units will be upgraded by advanced technologies (Szalavetz, Citation2017). This requires large-scale investments in tangible and intangible capital, and will lead to the upgrading of human work input, allowing for specialisation in higher-end activities (compared to the activity mix of pre-DT years).

Other scholars maintain that instead of backshoring, DT will rather contribute to the decentralisation of increasingly advanced activities within organisations. Advanced manufacturing displays important colocation synergies with R&D. Production necessitates close interactions with product and process-related research and development (Pisano & Shih, Citation2012; Tassey, Citation2014). Consequently, the upgrading of low-cost manufacturing units will be intensified by the relocation of advanced tasks, including engineering, design and software development (Lewin et al., Citation2009; Linares-Navarro, Pedersen, & Pla-Barber, Citation2014).

This article argues that assessments need to move beyond the usual dichotomy of DT ‘opening new upgrading opportunities for factory economies’ versus ‘nullifying factory economies’ past upgrading achievements’. This dichotomous view considers upgrading a black box, which limits the scope of the analysis of implications. The patterns of digitalisation-driven upgrading require detailed scrutiny to obtain insights enabling predictions about eventual DT-driven changes in the distribution of actors’ contribution to value added.

Accordingly, the point of departure of this article is that indeed, the digitalisation of manufacturing intensifies the upgrading of technology-adopting factory economy actors. We argue, however, that transition to smart connected factories is only part of the DT story. DT triggers the upgrading also of lead companies in global value chains (GVCs). More importantly, the patterns of upgrading differ across value chain actors, which may be one of the explanatory factors of the widely observed increases in global inequalities in the digital era (Allen, Citation2017).

To develop these arguments, we employed a two-stage investigation with linked stages. In the first stage we conducted interviews at a sample of high-flying manufacturing subsidiaries, pioneers in digitalisation, to explore the changes the deployment of digital technologies produced in their activities and identify the specifics of their upgrading.

To better capture the relative importance of investments in smart factory solutions, in the second stage, we explored the changes digitalisation engenders in the activities and specialisation of the headquarters (HQ). The evaluations of the managers interviewed regarding corporate-level digital strategy have been contrasted with findings from secondary source information about the digital strategy of the parent companies. This approach allowed us to reveal key HQ–subsidiary differences both in terms of the purpose of digital technology implementation and in the patterns of upgrading.

The specific context of the research is the Hungarian automotive industry, a sector dominated by foreign-controlled, export-oriented manufacturing units: subsidiaries of global original equipment manufacturers and of their global suppliers (Pavlínek, Citation2017). With nearly continuous large-scale investment inflows in the past quarter of a century, the transport equipment industry has been the main driver of growth, employment and export in Hungary, accounting for 30.2% of manufacturing production, 16.5% of manufacturing employment and 37.1% of manufacturing export in 2016.Footnote1 The automotive industry is a good choice to investigate the impact of DT, also because this industry is a forerunner in adopting digital technologies.

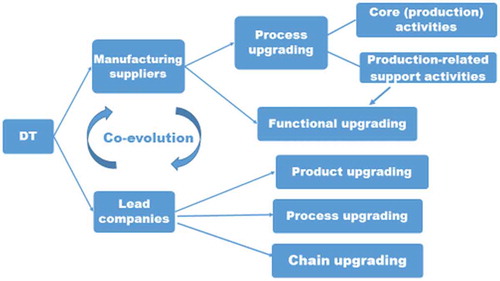

Our study contributes to research on the impact of DT in two ways. First, we move beyond the ‘opportunity or threat’ dichotomy regarding the impact of DT. We acknowledge the value addition and upgrading opportunities DT offers to manufacturing subsidiaries in factory economies, and open the black box of upgrading by elaborating on its specifics. Second, we present DT-driven upgrading in a co-evolutionary framework (Figure 1) and demonstrate that the upgrading of manufacturing suppliers is paralleled by similar upward shifts in lead companies’ specialisation.

The article proceeds as follows. First, some background information is provided on DT in the context of the theory of disruptive innovation. We then turn to summarise the theoretical framework closest related to the subject of our research: GVCs and upgrading. Next, we outline the proposed model of DT-driven upgrading. We then present the research method and introduce the sample of companies interviewed. This is followed by a section where we report and discuss our findings. In the concluding section, the findings are synthesised, implications discussed, limitations revealed and future research directions suggested.

Digital transformation as a series of disruptive innovations?

The integration of digital technologies, such as the Internet of Things (IoT), cloud computing, additive manufacturing, artificial intelligence, big data analytics and virtualisation technologies in manufacturing operations and in business functions supporting manufacturing, together with the digital reinvention of business are expected to profoundly transform global value adding activities, and result in spectacular improvements in technology adopters’ performance indicators. The DT of industries driven by these technology enablers is referred to as the fourth industrial revolution, or industry 4.0 for short (Kagermann, Helbig, Hellinger, & Wahlster, Citation2013; Manyika et al., Citation2013).

Some scholars refer to cyber-physical production systems (CPPS) as the epitome of the digital transformation of manufacturing (see survey by Monostori et al., Citation2016). CPPS are industrial production systems monitored, controlled, coordinated and connected by technological solutions that integrate recent research and development outcomes of computer science, information and communication technologies, and manufacturing science and technology. CPPS provide large amounts of data about their own ongoing operations. These data are processed in real time, by big data analytics solutions, which allows for managing complexity, boosting operational excellence, optimising resource use, and increasing the productivity of both manufacturing operations and – even more importantly – of production-related auxiliary functional activities (Colledani et al., Citation2014).

Examples of these latter include process planning, production scheduling, inventory management, energy management, quality control and maintenance. For instance, when processing production data, analytics solutions identify patterns that accompany production disturbances, such as tool breakage, equipment degradation or failure. This allows for developing predictions regarding the disturbances that are bound to emerge. In this way, big data analytics solutions prevent disturbances from materialising (Lee, Bagheri, & Jin, Citation2016). Big data analytics solutions are indispensable also for achieving a balanced load of the available resources, at a time when production plants manufacture a large variety of products, multiple processes are going on at the same time, and the portfolio of manufactured products may change several times, even in a single day, necessitating a fast reconfiguration of the system.

Another smart functionality enabled by DT, is virtualisation. For example, the optimal design (from the perspective of in-plant logistics) of the plant, or of the assembly line, is identified through simulation-based experimentation, which helps to eliminate bottlenecks in the production process (Duflou et al., Citation2012). Computer-based digital models (digital twins) are also used for product development. Virtual modelling, simulation and analysis of product properties (geometry, crack resistance, thermal behaviour) assist product developers’ work, and allow for shorter time to market.

Altogether, digital solutions in manufacturing improve the excellence of products and production, enhance productivity, contribute to resource optimisation, and allow for faster and more substantiated (data-supported) decision-making (Brettel et al., Citation2014; Tolio, Sacco, Terkaj, & Urgo, Citation2013).

The expected transformational impact of digital technologies explains why observers tend to refer to these digital novelties as ‘disruptive innovations’ – a common misinterpretation. The term was coined first by Clayton Christensen (Citation1997) and has rapidly achieved sweeping popularity (see review by Yu & Hang, Citation2010). In an effort to refine the excessively broadly-used original term, Christensen and Raynor (Citation2003) differentiated between low-end disruption and new market disruption. The former refers to a process in which challengers originally gain a foothold in low-end market segments, ignored by incumbents, introducing low-cost products, the quality of which is inferior to the original, high-performance ones. Disruptors gradually dethrone incumbents through improving their products incrementally and acquiring also mainstream market customers. The latter term refers to innovations offering new value propositions, which turns the non-consumers of these goods or services into consumers (Christensen, Raynor, & McDonald, Citation2015).

The features that constitute the definition of disruptive innovation do not apply, however, to most of the digital solutions integrated in manufacturing operations and in business functions supporting manufacturing. Neither do they apply to digitally enhanced products or services. Digital solutions are neither low-cost, low-performance product-service systems, nor are they targeting niche markets.Footnote2 Most of them definitely offer new value propositions, but rarelyFootnote3 attract new customer segments as a result, as would be the case in new-market-type disruptive innovations. Digital technology providers target mainstream manufacturing customers, and digital solutions can be classified as competence-enhancing (Tushman & Anderson, Citation1986) for technology adopters. Digitally enhanced products, e.g. vehicles and components, such as tyre monitoring systems, represent ‘sustaining innovation’ offering higher value to mainstream customers.

Altogether, despite the definitive transformational impact of digital technologies and irrespective of the fundamental changes digitalisation prompted in a number of industries, these developments and the technologies enabling them cannot be labelled as ‘disruptive’ in the original Christensenian sense. Digital technologies and solutions are rather radical, transformational innovations, turning several industries upside down and, indeed, often dismantling incumbents, but not necessarily disrupting them.

Following these side-remarks, we now turn to the theoretical framework closest related to the subject of our research, GVCs and upgrading.

Global value chains and upgrading

Our research is informed by the GVC approach, used to investigate: (a) the global composition of value adding activities of geographically dispersed, networked and functionally integrated economic actors (Dicken, Citation2003; Gereffi, Citation1999; Gereffi & Fernandez-Stark, Citation2016); (b) the governance of these activities; and (c) the global distribution of value added (Gereffi, Humphrey, & Sturgeon, Citation2005).

According to the commonly cited definition, GVCs describe the full range of tangible and intangible activities, undertaken by inter-firm networks on a global scale, to bring a product or service from its conception to its end use and beyond (adapted from Gereffi & Fernandez-Stark, Citation2016). The GVC framework of analysis is used to highlight the changes in the global organisation of activities and in the composition of value added, driven by technological progress, corporate strategies, regulations, market trends and transformation of power relations (Cattaneo, Gereffi, & Staritz, Citation2010; Dicken, Citation2003).

In addition to the above-listed dimensions (specialisation, geographic scope and governance of networked actors), another core concept of the analysis of GVC dynamics is upgrading (Gereffi & Fernandez-Stark, Citation2016). Upgrading is defined as specialising in higher value adding activities within GVCs than before, e.g. by extending the scope and the knowledge-intensity of activities (cf. Ponte & Ewert, Citation2009; Sass & Szalavetz, Citation2013). In the Humphrey and Schmitz (Citation2002) classification, upgrading may refer to (better) products, (improved, more efficient) processes, higher-skill functions and/or to shifting to (new and technologically more advanced) sectors or value chains. Barrientos, Gereffi, and Rossi (Citation2011) underline that each type of upgrading embodies a capital dimension and a labour dimension. Consequently, upgrading can be conceptualised as a move from low-skilled, labour-intensive work to medium-skilled and then to high-skilled, technology-intensive and further, to knowledge-intensive activities. This move is driven by the given actors’ dynamic acquisition of competitive advantage (Giuliani, Pietrobelli, & Rabellotti, Citation2005), as they enhance existing and/or develop new capabilities.

As argued by Coe and Yeung (Citation2015) upgrading needs to be conceived as a co-evolutionary process. For example, as upgraded factory economy suppliers become capable of taking on more complex and higher value-added activities along the value chain, lead firms re-engineer their organisational strategy and focus on even higher value activities, such as new product and market development, to capture more value.

One of the key factors accounting for the dynamic, evolutionary character of GVCs is technological progress. New technological solutions may transform the existing organisation of value activities, industry architectures, GVC structures and power relations (Gereffi et al., Citation2005). In the context of our research, for example, the DT of manufacturing operations and of support functions is expected to have a transformational impact on all dimensions of GVCs, e.g. specialisation, geographic scope, governance and upgrading (Manyika et al., Citation2013; Rehnberg & Ponte, Citation2018).

The transformational impact of digital technologies on the aforementioned dimensions of GVCs has received considerable and increasing scholarly attention (e.g. Dachs et al., Citation2017; Porter & Heppelmann, Citation2014; Rehnberg & Ponte, Citation2018; Vendrell-Herrero, Bustinza, Parry, & Georgantzis, Citation2017).

The classical reference to be used as a point of departure for assessing the impact of DT on upgrading is Gereffi et al. (Citation2005). According to these authors, the three most important variables that determine how GVCs change and how they are governed are the complexity of transactions, the ability to codify transactions and suppliers’ capabilities. Association between upgrading and the first and third variables is strongly positive. Conversely, codification reduces the specialised knowledge-intensity of transactions and thus works against upgrading.

DT acts upon each of the above variables. On one hand, digital technology deployment adds to the complexity of the production system, and thus, requires superior capabilities to operate it (ElMaraghy, ElMaraghy, Tomiyama, & Monostori, Citation2012). On the other hand, advanced computing solutions can effectively address continuously increasing complexity by enhancing operational transparency and offering real-time monitoring and control solutions. Further, by turning data and information into knowledge that can substantiate decisions, DT facilitates lead firms’ quest to codify transactions and convert specialised and tacit knowledge-intensive activities into standardised, repetitive and low-knowledge ones (Cano-Kollmann, Cantwell, Hannigan, Mudambi, & Song, Citation2016).

At the same time, as argued by labour economists (e.g. Autor, Citation2015), DT creates new kinds of technological and organisational problems to be addressed by new high-skilled, specialised and labour-intensive tasks, often performed in new occupations. The balance of DT’s contradictory effects on upgrading is influenced, among others, by management choices, cultural factors, the specifics of production technology and the role of the plant within the global company and the value chain (Hirsch-Kreinsen, Citation2016; Krzywdzinski, Citation2017).

While these arguments elucidate some factors influencing the upgrading of manufacturing suppliers, they do not clarify some important specifics of upgrading. It remains obscure, for example, whether DT-driven upgrading impinges only on manufacturing suppliers’ core (production) activities or DT also influences the value added of production supporting activities? Accordingly, it remains to be explored whether DT is associated only with process upgrading or if it also induces manufacturing suppliers’ functional upgrading?

Further, although the co-evolutionary nature of upgrading is a widely shared view in the GVC literature (e.g. Gereffi et al., Citation2005; Sturgeon & Lee, Citation2001), the questions regarding whether and how the DT-driven upgrading of manufacturing suppliers is paralleled by similar upward shifts in lead companies’ specialisation have, so far, received little attention.Footnote4

To address these research gaps, we propose a model of DT-driven upgrading, where upgrading is presented as a co-evolutionary process and the particular features of upgrading differ across value chain actors.

Digital transformation-driven upgrading: factory economy actors versus lead companies

The point of departure of the proposed model is that the digitalisation of manufacturing brings about spectacular improvements in technology adopters’ operational performance, for instance in overall equipment effectiveness, operational excellence, cycle time and resource efficiency. Overall, the primary and most conspicuous benefit of digitalisation, at least at manufacturing companies, is an increasingly efficient transformation of inputs into outputs, i.e. process upgrading. Our review of the industry 4.0 literature reveals that digitalisation enhances the efficiency of both the core and the production-related auxiliary functional activities: they simultaneously contribute to process upgrading. In our framework, the enhanced efficiency of production supporting activities propels and enables manufacturing suppliers’ functional upgrading: it allows for the take up by suppliers of additional, high value adding functional tasks.

In contrast to process upgrading and functional upgrading at manufacturing suppliers, digital technology is used at lead companies, among others, to enhance and support new product development (to facilitate product upgrading).

Digital solutions increase the efficiency also of other lead company-specific core activities, such as planning, optimising, monitoring and controlling the supply chain (e.g. through big data analytics, virtualisation and by creating real-time transparency of the state of affairs along the whole value chain – cf. Xu & Duan, Citation2018), and developing new business concepts and new markets (e.g. by leveraging big data to understand and anticipate customer value).

In this article we define process upgrading in a broader-than-the-usual manner, as technology deployment and/or innovation aimed at performing core activities (and not just production) more efficiently than before. This definition makes it evident that digital technologies induce process upgrading also at lead companies.

In addition to the above-listed types of upgrading at lead companies,Footnote5 DT also engenders chain upgrading, defined as applying the competences acquired in the process of the DT of automotive industry, to shift to new activities (new sectors), for example, through inventing digital technology-enabled new business models and shifting to connected-car-related digital services.

provides a graphic summary of our arguments.

Figure 1. A co-evolutionary framework of DT-driven upgrading.

There is a large body of literature on DT-driven business model innovation in the automotive industry (e.g. Burmeister, Lüttgens, & Piller, Citation2016; Gissler, Oertel, Knackfuß, & Kupferschmidt, Citation2015; Hanelt, Piccinini, Gregory, Hildebrandt, & Kolbe, Citation2015; Kaiser, Stocker, & Viscusi, Citation2017, see also: Teece & Linden, Citation2017). These authors maintain that business model innovation generates significant new revenue opportunities. Altogether, industry analysts conjecture that digitalisation bears significant additional profit potential. Returns are however uneven across activities and value chain stages: digitalisation of customer experience, marketing and after sales services will account for the lion’s share of the expected total additional profit (Gissler et al., Citation2015). The digital technologies-enabled optimisation of existing business processes, such as supply chain management and R&D, will also account for a large albeit relatively smaller part of the expected total additional profit. In the longer run, however, the profit potential of new business models and that of connected car services will grow exponentially.

The resulting redistribution of revenue pools may culminate in an unprecedentedly skewed and concentrated structure of value capture along the transformed automotive value chain (Iansiti & Lakhani, Citation2017). Consequently, it seems safe to predict that manufacturing suppliers’ DT-driven upgrading will not diminish the gap between lead companies and manufacturing subsidiaries in terms of value generation and contribution to total value added.

Research method and sample

Since this research was intended to (a) explore the patterns of DT-driven changes in the activities of manufacturing subsidiaries, and (b) assess the relative importance of these changes compared to the overall transformation of activities along the value chain, a qualitative approach based on multiple case studies was considered the most appropriate method of investigation (Eisenhardt, Citation1989; Yin, Citation2014).Footnote6 As detailed below, the means and modes of data collection and analysis were determined in accordance with the methodological prescriptions by Gibbert, Ruigrok, and Wicki (Citation2008).

As mentioned earlier, Hungary, a factory economy specialised in the automotive industry, was selected for the context of our empirical investigations. Efficiency-seeking FDI inflows, leveraging labour-cost differences combined with a relatively skilled local labour force, have grown at nearly a geometric rate since the early transition years (Sass & Kalotay, Citation2012). Specialisation in and the concentration of the automotive industry has been increasing continuously, even after the crisis (Rechnitzer, Hausmann, & Tóth, Citation2017), making Hungary particularly exposed to the radical technological and business model changes the industry is currently experiencing.

We applied the method of purposeful sampling (Patton, Citation1990), and chose companies representing illuminative cases from the point of view of implementing cyber-physical systems and other smart factory technologies. Drawing on the author’s collection of business press articlesFootnote7 on digital forerunners in Hungary, we identified the companies to be included. Our sample consists of 10 large, export-oriented companies, subsidiaries of global corporations in the automotive industry. Automotive companies have a higher-than-the average degree of industry 4.0 maturity, since quality, safety and product traceability requirements have long required computerisation, automation, implementation of sensors, and access to and storage of a variety of production data. Automotive industry actors are pioneers also in the most recent wave of digital transformation.

presents the basic characteristics of the firms in the sample. Companies were selected for inclusion if they displayed a higher-than-elementary maturity level in the operations and technology dimensions. For assessing the maturity of the contacted firms, we relied on a narrow version of Schumacher, Erol, and Sihn’s (Citation2016) maturity model. These authors evaluate industry 4.0 readiness of organisations in nine dimensions, for instance strategy, products, operations, technology, leadership and culture, and define five levels for each dimension. For the purpose of this study, i.e. for selecting information-rich cases from the local population of automotive subsidiaries, we considered only the operations and technology dimensions, though our interviews have also revealed some information about the leadership and strategy dimensions.

Table 1. Overview of sample firm characteristics.

Industry 4.0 readiness was deemed of a higher-than-elementary level, if production was digitally supported, not just IT-enabled (McLaughlin, Citation2017), and if production data were extracted, analysed, and the given company’s production system and enterprise system, i.e. its manufacturing operations and business processes were, at least to some extent, integrated.Footnote8

Sample companies display some heterogeneity with respect to the sophistication of digital technologies implemented, but are systematically increasing the scope of digital applications employed. Production is semi-automated across the sample, i.e. processing itself is fully automated, or industrial robotics solutions are deployed, but manual workers load and discharge the machinery. Collaborative robots have been implemented in five companies (half of the sample). Although key performance indicators are visualised only in some firms, most of them are making efforts to make shop-floor management (more and more) paperless. The most advanced firms in the sample have implemented intelligent production monitoring and digital production control solutions. They have invested in algorithms-based production scheduling and in digital quality control solutions. Some of them have automated in-plant transportation and material handling.

Altogether, our sample consists of ‘high-flying’, successful companies, operating in an industry that is a digital forerunner, which makes the results hard to generalise. It needs to be mentioned here that the aim of this study was analytical rather than statistical generalisation. Notwithstanding, we tried to compensate for this limitation using systematic cross-case analysis and also conducting interviews with industry experts (see below).

Our data collection was guided by an interview protocol (see Appendix), consisting of open-ended questions regarding the specifics of the new technologies/solutions deployed. Respondents were asked to specify the functional activities, where the new digital solutions were used (e.g. core production versus production support activities). We also inquired about the drivers and motivations of investment, and asked whether technology deployment fulfilled the related expectations. We asked the managers to specify in which dimensions and functional areas the expected improvements have become manifested. Another topic discussed with the managers interviewed was whether technology deployment has made HQ delegate any new tasks to the subsidiary, or whether it has resulted in the creation of new occupations.

To better capture the relative importance of investments in smart factory solutions at local manufacturing sites, we inquired whether our respondents perceive any differences between the parent company and the Hungarian subsidiary, in terms of the purpose of investing in digital technologies. In the second stage of the research, we complemented these latter data with information gained from secondary sources (see below) about parent companies’ digital strategy.

Interviews were made between January and March 2018, and lasted between 45 and 90 minutes. To ensure the validity and reliability of the data, interview results were triangulated, employing multiple data sources, such as press releases, corporate websites, business press articles, company reports, notes to the financial statement and parent companies’ annual reports. In addition to conducting interviews with corporate officials, we consulted two representatives of the Hungarian Metalworkers’ FederationFootnote9 and a professional from the Association of the Hungarian Automotive Component Manufacturers.

To identify upgrading, we analysed data on the dimensions of performance improvement where the beneficial impact of digital technology deployment has been observed. In accordance with the literature (e.g. Humphrey & Schmitz, Citation2002; Navas-Alemán, Citation2011), upgrading was evaluated considering changes in actors’ value adding capability.

Consequently, we operationalised process upgrading not simply as the implementation of new technological solutions, new production machinery, or new organisational and management methods (such as automation of in-plant logistics or shifting to simulation-based decision-making), but rather through notions referring to the resulting performance improvement, e.g. productivity, overall equipment effectiveness, operational excellence, cycle time and resource efficiency. Since the exact value of (and changes in) these variables were considered confidential by the companies interviewed, we obtained information only about whether improvements in the production system have had a beneficial impact on these variables or not. Conversely, the impacts of digitalisation on functional upgrading were operationalised through new (kinds of) jobs at subsidiary level and/or new tasks delegated by HQ to the subsidiary.

Internal validity was ensured by asking our respondents, again and again, to confirm whether the observed changes were indeed related to the deployment of digital technologies, or were rather business-as-usual developments. The first draft of this article with preliminary conclusions was sent to all our respondents for comments and feedback and some minor misunderstandings have been corrected.

Digital transformation: smart factories

Driven by diverse operational motivations, such as production quality, productivity, process efficiency, flexibility and transparency,Footnote10 the surveyed firms have gradually increased investment in digital solutions. Since new digital manufacturing technologies can be deployed step-wise, i.e. they can be added to the existing production systems without jeopardising their functionality (Szalavetz, Citation2017), transition to a higher level of industry 4.0 maturity can be achieved in a gradual manner.

Investments in the most advanced manufacturing technologies have added to the heterogeneity of sample companies’ production systems. These production systems were characterised by the coexistence of old and new-vintage machinery. Different information technology (IT) solutions were controlling individual sub-systems and functional activities.

Consequently, investments in DT were intended to achieve the harmonisation of the heterogeneous IT legacy systems, and the interconnection of IT applications supporting different operational activities that had been deployed in an isolated manner. Another objective, considered by our informants as the very essence of DT, was the digital interconnection of core (manufacturing) and support activities, e.g. manufacturing with maintenance and CNC programming, or production planning with inventory management and logistics. As the following interview excerpt demonstrates, interconnection lies at the heart of DT.

You may wonder why robotisation, or the automation of warehouse picking are mentioned last in my list. As a matter of fact, these spectacular industry 4.0 solutions are far less important from the point of view of overall production quality and efficiency than the interconnection of core and support activities. Now, operators do not have to ‘walk up’ to the line supervisor or to the maintenance staff to ask for help. They needn’t ‘go and look for someone’ responsible for CNC programming, if they notice a problem. They simply give a signal on a display, and specify the problem selecting among the standard menu items, and help arrives immediately. As you see, interconnection improves efficiency.

The collection of data about various product and process parameters has long been achieved at the surveyed companies. For instance, newer vintages of production equipment are already capable of collecting and storing data about their activities. Consequently, major development efforts have been dedicated to the upgrading of the manufacturing execution systemFootnote11 and to developing the analytics of the obtained data. Advanced analytics solutions ensured transparency, for instance, real-time information about the state of production, and allowed for data-driven decision-making.

Regarding this latter purpose, some companies have already started to invest in implementing artificial intelligence solutions, for example, to identify the correlation between processing parameters and product quality, perform a root-cause analysis of production disturbances and/or develop predictive analytics solutions to avoid machine failures.

Furthermore, the companies in the sample gradually implemented a variety of other industry 4.0 solutions (see summary in and details in Appendix Table A1). They automated selected activities, for instance production control and in-plant transportation through shopping cart-based driverless transport systems, and invested in advanced quality inspection supporting solutions, such as 3D scanners and optical measurement of the geometry and shape of automotive components.

Table 2. Purpose of sample firms’ investments in digital technologies.

Paperless shop-floor management systems and smart operator assistance solutions were also among the usual investment targets. Examples of these latter include ‘screwdriver’ applications that signal if screws haven’t been tightened sufficiently, or tracking devices that optimise and guide manual inventory picking activities. A variety of smart, poka yoke (mistake proof) solutions (Shingo, Citation1986) have been deployed to guide assembly operators mounting components. Some workers (e.g. the maintenance staff) in selected companies receive instructions and notifications directly on their displays. One company reported about the pilot implementation of smart watches on the shop floor. These smart wearables assist workers assembling complex configurations, since they contain situation-specific work instructions about the necessary components to be assembled in the given car. Smart wearable technology also served as a notification system in case of process malfunctions or any other problems.

The deployment of advanced manufacturing technology resulted in the upgrading of the surveyed companies. The beneficial impacts of DT were manifested in the improvement of indicators, such as defect ratio, cycle time, throughput, overall equipment effectiveness, size of product backlog, work in progress, reliability (e.g. mean time between failures, number of rework orders) and maintenance costs. Moreover, several respondents underlined that their companies are undertaking just the groundwork for future, more significant performance improvements.

Although the automation of selected manual processes and the implementation of collaborative robots and automated guided (driverless) vehicles have significantly improved the productivity of core processes, the overall improvements in the aforementioned indicators have been driven mainly by the improved performance of production support tasks. Accordingly, an important finding that crystallised from the interviews was that process upgrading was driven mainly by the improved efficiency of non-production activities.

Our informants emphasised that technology adoption involves more and/or broader responsibilities, because it saves time for employees at all skill levels to engage in higher quality and higher value adding work. For example, in functional occupations, such as logistics, quality, maintenance, engineering, design or management, a substantial share of total working time used to be spent on collecting information and analysing data. Due to digitalisation, the time requirement of these activities was dramatically reduced. Moreover, functional officers have been freed from a variety of time-consuming activities, such as documentation, reporting and other administrative tasks, inasmuch as these have been automated.

Simulation software has dramatically improved the productivity of knowledge-intensive activities, such as layout planning, process planning, commissioning, new product development and validation of design.

Previously we tested and validated the design sent by HQ. Our feedback was a yes or no answer: accepting the given design or asking for modification and pointing to problems. Using this simulation software, validation process became much quicker. We have time to experiment with our own ideas, try, say, five alternatives instead of one, and identify the best solution.

These latter developments can already be associated with functional upgrading. Altogether, productivity improvement allowed white-collar employees to take on new tasks or dedicate more time to higher value adding activities, for instance, to contribute their expertise to ongoing process development efforts.

Other manifestations of functional upgrading, for instance, the creation of new kinds of jobs, such as robot programmers or data security analysts, or the broadening of existing job descriptions (for example, sensor integration, sensor calibration, robotic path planning) were mentioned by more than two-thirds of the companies in the sample. In some cases, old job categories were renamed to reflect their broadened responsibility requirements, for instance, in one company, automation engineers were renamed as ‘industry 4.0 engineers’.

One of the most conspicuous manifestations of functional upgrading was the expansion of the local R&D departments and the delegation of additional R&D tasks to the subsidiaries interviewed. Subsidiary engineers and researchers were entrusted with new tasks such as software development (e.g. development of the manufacturing execution system), sensor development, component development in the field of vehicle safety, analysis of production technology malfunctions, PLC programming, virtual commissioning. The relation between this latter expression of upgrading and the adoption of advanced digital technologies was, however, deemed ambiguous by the respondents. The expansion of R&D assignments was rather ascribed to the ongoing expansion and organic development of the subsidiary.

Digital transformation: digital business

When asked about their perceptions, whether there was any difference between HQ and subsidiary in the purpose of industry 4.0 technology deployment, the managers interviewed proved highly knowledgeable about the digital strategy of their global corporations.

The main focus of HQ is autonomous driving and connected car solutions development. That’s where R&D resources are concentrated.

Advanced digital technologies are used to design and develop electric vehicles. A further key component of our owner’s digital strategy is referred to as mobility services, you know, the pay-per-use business model. Of course, considerable resources are dedicated also to expanding the portfolio of our digital services.

Data security, new apps in the navigation and entertainment systems, development of drivers’ assistance systems: software, software and again, software! Our global owner does not label itself an automotive company any more. You know what it says it is? A software company!

One of the main pillars of our digital strategy is to build a digital marketing platform that helps us develop personalised customer relations and accompany our customers after the sale of the vehicle.

These interview findings have been triangulated, reviewing secondary-source information on parent companies’ digitalisation strategy. Press releases, corporate websites, business press articles and parent companies’ annual reports have been reviewed for data on the main strategic directions of DT. Results are summarised in and detailed in .

Table 3. Purpose of digitalisation at HQ.

The reviewed data indicate that one of the key strategic purposes of lead companies’ digital transformation is additional revenue generation through new product development and/or digital enhancement of existing products, servitisation as new growth strategy and business model innovation. Lead companies leverage digital transformation, combining the physical components of their business and the new digital solutions. This is referred to as ‘investments in connected and autonomous technology’.

Leveraging digital technologies, lead companies propose new business models, enter new business fields and apply new service delivery methods. In turn, this requires investments in R&D and corporate infrastructure, for instance, in corporate cloud solutions and enterprise-specific databases. It also necessitates the expansion of companies’ ecosystems by forging new strategic alliances and investing corporate venture capital in digital technology-based startups.

Furthermore, lead companies integrate digital technologies in their business processes to enhance the efficiency thereof. Examples include investments in business intelligence to obtain accurate information about customers and enable data-driven decision-making. Digital technologies enhance the efficiency of coordination, e.g. through organisational and across-value-chain integration.

Part of lead companies’ resources is used to transform corporate culture, enhance and find out new ways of intra-corporation communication and collaboration. These purposes are also achieved by relying on a variety of digital tools.

Discussion

The empirical evidence reviewed earlier highlights that manufacturing subsidiaries and lead companies are poles apart regarding the specifics and the motives of using digital technologies. Moreover, the patterns of digitalisation-triggered upgrading are also completely different at the two parties.

One of the most conspicuous signs of DT at HQ level is global companies’ quest to forge ahead in the new product development race. In the current turbulent phase of the industry life cycle that precedes the emergence of a new dominant design, HQs use digital technologies for product upgrading and new product development, making massive investments in electric vehicle, autonomous and connected car technologies.

Additionally, as the automotive industry turns into a digital business, the global company owners of the surveyed subsidiaries concentrate their efforts on the services side of the automotive product-service system. Recognising that value has migrated from traditional vehicle manufacturing to smart digital services and solutions, the HQs of the companies in the sample focus on developing solutions that enhance driving experience and the safety of driving, such as drivers’ assistance systems, navigation and infotainment.

In short, vehicles are considered ‘platforms’, and global companies use digital technologies for developing platform-based digital services.

By contrast, digitalisation at manufacturing subsidiary level refers to investments in smart factory solutions to enhance the excellence and reduce the costs of manufacturing the ‘platform’ (the car).

Regarding upgrading, the collected evidence indicates that digitalisation has, indeed, offered upgrading opportunities for factory economy actors, in terms of both process upgrading and functional upgrading.

Moreover, the data obtained from in-depth interviews and from secondary sources indicate a co-evolutionary pattern of DT-driven upgrading, where DT presents upgrading opportunities also for lead companies.

Digital technologies support not only lead companies’ product upgrading efforts but also a number of other lead company-specific core activities, such as supply chain management and value chain coordination, R&D and knowledge management, customer engagement and new market development. The digitisation of these activities enabled significant efficiency improvement, hence these developments can be referred to as process upgrading (of lead companies’ core processes).

The kind of lead company upgrading that is the most relevant for the digital era is chain upgrading, i.e. inventing digital technology-enabled new business models, such as car sharing and shifting to platform-based connected and mobility services. According to industry analysts (e.g. KPMG, Citation2017; McKinsey & Company, Citation2016), automotive industry actors’ shifting focus, in terms of servitisation and new business models, will secure new revenue streams and allow for capturing more value than in traditional unit sales-based business models.

Altogether, the reviewed HQ–subsidiary differences in the application and impacts of digital technologies suggest that the smart factory concept and all the related investments comprise only a fragment of automotive companies’ digitalisation efforts. This finding is far from trivial, since it highlights that the concept of ‘industry 4.0’ is much narrower than that of ‘digitalisation’. Industry 4.0 technologies contribute to the upgrading of operations, and enable subsidiaries’ functional upgrading, i.e. their taking on production-related knowledge-intensive assignments. By contrast, digitalisation serves lead companies’ strategic differentiation efforts, and contributes to achieving competitive advantage: these latter are crucial for value capture.

Conclusion

The purpose of this article was to explore the changes digital technologies engender in the activities of value chain actors, and identify the specifics of upgrading. We presented DT-driven upgrading in a co-evolutionary framework and demonstrated that the upgrading of manufacturing suppliers is paralleled by similar upward shifts in lead companies’ specialisation.

We argued that although DT presents non-negligible additional value adding opportunities for actors specialising in manufacturing activities, these changes are dwarfed by the ones lead companies experienced. We opened the black box of DT-driven upgrading and showed that in the case of manufacturing subsidiaries, value generation was enhanced mainly through process efficiency, i.e. higher productivity and reduced costs. In turn, this opened up new opportunities for subsidiaries’ functional upgrading, i.e. to generating additional value by taking on new, knowledge-intensive activities.

In the case of lead companies, digital technologies supported product upgrading and allowed for significant improvements in the efficiency of lead company-specific business processes (they induced process upgrading in the field of supply chain management, coordination, R&D, knowledge management and customer engagement). However, according to interview information and the reviewed secondary source documents, the kind of DT-driven upgrading that triggered the most spectacular growth in lead companies’ revenues and operating margins can be referred to as chain upgrading, manifested in servitisation and new business model introduction.

This led us to conclude that manufacturing subsidiaries and lead companies are poles apart regarding the specifics of digitalisation-induced upgrading. We also hypothesise that manufacturing suppliers’ DT-driven upgrading will not diminish the gap between lead companies and manufacturing subsidiaries in terms of value generation.

Our findings have important policy implications. On one hand, FDI promotion policy needs to lay even more emphasis on qualitative aspects (cf. Szent-Iványi, Citation2017), provide a wide range of investment aftercare services to stimulate digitalisation-driven upgrading and promote workforce adaptation through ‘education 4.0’. On the other hand, these findings make it obvious that FDI promotion is not the only means of fostering factory economy actors’ upgrading and increased value capture. Digitalisation offers unprecedented opportunities for technology-based start-ups inventing smart solutions to be integrated in vehicles.Footnote12 Consequently, much greater attention needs to be paid to the promotion of indigenous, technology-based entrepreneurship than before.

This study is not without limitations. The main limitations are the small size and the industry-specific character of the sample. The generalisation of the results is limited also because highly successful companies have been selected and only the aspects of upgrading considered. Our focus on upgrading does not preclude potential DT-driven downgrading effects; this aspect needs to be considered by further research. Further research is needed also to reveal whether the patterns of, and the HQ–subsidiary differences in, DT-induced upgrading are similar across other industries and countries hosting efficiency-seeking FDI in manufacturing.

Acknowledgments

Research support by the European Trade Union Institute is gratefully acknowledged.

Disclosure statement

No potential conflict of interest was reported by the author.

Notes

1. Source: Author’s calculations from Central Statistical Office data.

2. There are of course exceptions, but mainly outside the realm of manufacturing, for example in retail, financial services, healthcare and so forth.

3. The technology of cloud computing, enabling ubiquitous, on-demand network access to a shared pool of computing resources, is an exception, since it minimises the costs of using computer resources and attracts thereby new customers benefiting from advanced applications they could not afford otherwise.

4. One exception is the large and rapidly growing literature on DT-driven business model innovation, e.g. Burmeister et al. (Citation2016).

5. From the perspective of lead companies, DT-driven functional upgrading also makes sense: it can be interpreted as the DT-enabled backshoring/insourcing of previously offshored/outsourced activities. This issue is, however, only indirectly relevant for the subject of this research, hence its detailed discussion is beyond the scope of this paper.

6. The impact of DT on upgrading, production restructuring and the organisation of work was studied using a similar interview-based approach by Butollo and Lüthje (Citation2017) in China. Krzywdzinski (Citation2017) interviewed German automotive suppliers and compared DT-driven changes in the nature of work and in companies’ labour-use strategies with the results of similar interviews at Polish, Czech, Slovakian and Hungarian automotive plants.

7. Two magazines and their websites proved particularly useful for identifying information-rich cases: Techmonitor (www.techmonitor.hu) and Gyártástrend (www.gyartastrend.hu). Both of them focus on and report new technological solutions across a variety of industries and introduce among others, Hungarian use cases of the given solutions. Moreover, since 2015, Gyártástrend organises an annual ‘Factory of the Year’ competition, including, among others a category of ‘Industry 4.0’. The yearly shortlists of winners in this category were also used as a source of information for sample selection.

8. In this vein, we decided to exclude one company following the interview (and looked for a new one, instead), since it was deemed insufficiently mature to be included. This company has adopted some digital solutions, specifically, it implemented automation and some robotic solutions, and invested in an enterprise resource planning solution, but failed to collect and analyse production data.

9. The Federation represents workers’ interests in the metal, automotive, mechanical engineering, electronics and ICT industries.

10. Some of these motivations are interdependent. For example, increased transparency allows rapid reaction to process anomalies, which improves process efficiency. The real-time measurement and visualisation of process parameters improve not only transparency and, thus, enable data-driven decision-making, but also allow for process optimisation, e.g. through the reduction of internal transport or of work in progress. In this vein, transparency contributes to process efficiency improvement.

11. Manufacturing execution systems are software packages used to manage factory floor material flows, track and optimise labour and machine capacity, provide real-time information about inventory and orders, and optimise production activities.

12. Although the number of parts is bound to diminish with electrification, the automotive industry is and has always been a particularly good example of the multi-invention context exhibited by today’s products (Teece & Linden, Citation2017). Digitalisation will further increase the number of functions ‘computers on four wheels’ fulfil.

References

- Allen, J. P. (2017). Technology and inequality: Concentrated wealth in a digital world. Cham: Springer.

- Autor, D. H. (2015). Why are there still so many jobs? The history and future of workplace automation. The Journal of Economic Perspectives, 29(3), 3–30.

- Baldwin, R. (2013). Trade and industrialization after globalization's second unbundling: How building and joining a supply chain are different and why it matters. In R. C. Feentsra, & A. M. Taylor (Eds.), Globalization in an age of crisis: Multilateral economic cooperation in the twenty-first century (pp. 165–212). Chicago: University of Chicago Press.

- Barrientos, S., Gereffi, G., & Rossi, A. (2011). Economic and social upgrading in global production networks: A new paradigm for a changing world. International Labour Review, 150(3‐4), 319–340.

- Brettel, M., Friederichsen, N., Keller, M., & Rosenberg, M. (2014). How virtualization, decentralization and network building change the manufacturing landscape: An industry 4.0 perspective. International Journal of Mechanical, Industrial Science and Engineering, 8(1), 37–44.

- Brynjolfsson, E., & McAfee, A. (2014). The second machine age: Work, progress, and prosperity in a time of brilliant technologies. New York, NY; London: WW Norton & Company.

- Burmeister, C., Lüttgens, D., & Piller, F. T. (2016). Business model innovation for industrie 4.0: Why the industrial internet mandates a new perspective on innovation. Die Unternehmung, 70(2), 124–152.

- Butollo, F., & Lüthje, B. (2017). ‘Made in china 2025’: Intelligent Manufacturing and Work. In K. Briken, S. Chillas, M. Krzywdzinski, & A. Marks (Eds.), The new digital workplace. How new technologies revolutionise work (pp. 42–61). London: Palgrave MacMillan International Higher Education.

- Cano-Kollmann, M., Cantwell, J., Hannigan, T. J., Mudambi, R., & Song, J. (2016). Knowledge connectivity: An agenda for innovation research in international business. Journal of International Business Studies, 47(3), 255–262.

- Cattaneo, O., Gereffi, G., & Staritz, C. (Eds.). (2010). Global value chains in a postcrisis world: A development perspective. Washington, DC: World Bank Publications.

- Christensen, C. (1997). The innovator’s dilemma: When new technologies cause great firms to fail. Boston, MA: Harvard Business School Press.

- Christensen, C. M., Raynor, M., & McDonald, R. (2015). What is Disruptive innovation? Twenty years after the introduction of the theory we revisit what it does – And doesn’t – Explain. Harvard Business Review, 93(12), 44–53.

- Christensen, C. M., & Raynor, M. E. (2003). The innovator’s solution: Creating and sustaining successful growth. Boston, MA: Harvard Business School Press.

- Coe, N. M., & Yeung, H. W. C. (2015). Global production networks: Theorizing economic development in an interconnected world. New York, NY: Oxford University Press.

- Colledani, M., Tolio, T., Fischer, A., Iung, B., Lanza, G., Schmitt, R., & Váncza, J. (2014). Design and management of manufacturing systems for production quality. CIRP Annals-Manufacturing Technology, 63(2), 773–796.

- Dachs, B., Kinkel, S., & Jäger, A. (2017). Bringing it all back home? Backshoring of manufacturing activities and the adoption of Industry 4.0 technologies. MPRA Paper No. 83167.

- Dicken, P. (2003). Global shift: Reshaping the global economic map in the 21st century. Thousand Oaks, CA: Sage.

- Duflou, J. R., Sutherland, J. W., Dornfeld, D., Herrmann, C., Jeswiet, J., Hauschield, M., … Kellens, K. (2012). Towards energy and resource efficient manufacturing: A processes and systems approach. CIRP Annals-Manufacturing Technology, 61 (2), 587–609.

- Eisenhardt, K.M. (1989). Building theories from case study research. Academy of Management Review, 14(4), 532–550.

- ElMaraghy, W., ElMaraghy, H., Tomiyama, T., & Monostori, L. (2012). Complexity in engineering design and manufacturing. CIRP Annals-Manufacturing Technology, 61(2), 793–814.

- Ford, M. (2015). Rise of the Robots: Technology and the threat of a jobless future. New York: Basic Books.

- Frey, C. B., & Osborne, M. A. (2017). The future of employment: How susceptible are jobs to computerisation? Technological Forecasting and Social Change, 114, 254–280.

- Frey, C. B., Osborne, M. A., & Holmes, C. (2016). Technology at Work v2.0. The future is not what it used to be. Oxford Martin School & Citi GPS Report. https://www.oxfordmartin.ox.ac.uk/downloads/reports/Citi_GPS_Technology_Work_2.pdf

- Gereffi, G. (1999). International trade and industrial upgrading in the apparel commodity chain. Journal of International Economics, 48(1), 37–70.

- Gereffi, G., & Fernandez-Stark, K. (2016). Global value chain analysis: A primer (2nd ed.). Duke Center on Globalization, Governance & Competitiveness (CGGC), Duke University, Durham, NC. Retrieved from https://dukespace.lib.duke.edu/dspace/bitstream/handle/10161/12488/2016-07-28_GVC%20Primer%202016_2nd%20edition.pdf?sequence=1_1

- Gereffi, G., Humphrey, J., & Sturgeon, T. (2005). The governance of global value chains. Review of International Political Economy, 12(1), 78–104.

- Gibbert, M., Ruigrok, W., & Wicki, B. (2008). What passes as a rigorous case study? Strategic Management Journal, 29(13), 1465–1474.

- Gissler, A., Oertel, C., Knackfuß, C., & Kupferschmidt, F. (2015). Are you ready for pole position? Driving digitization in the auto industry. Retrieved from https://www.accenture.com/t00010101T000000__w__/es-es/_acnmedia/PDF-10/Accenture-Strategy-Driving-Digitization-Auto-Industry-1.pdf

- Giuliani, E., Pietrobelli, C., & Rabellotti, R. (2005). Upgrading in global value chains: Lessons from Latin American clusters. World Development, 33(4), 549–573.

- Hanelt, A., Piccinini, E., Gregory, R. W., Hildebrandt, B., & Kolbe, L. M. (2015). Digital transformation of primarily physical industries. Exploring the impact of digital trends on business models of automobile manufacturers. In Proceedings of the 12. International Conference on Wirtschaftsinformatik (pp. 1313–1327). Universität Osnabrück.

- Hirsch-Kreinsen, H. (2016). Digitization of industrial work: Development paths and prospects. Journal for Labour Market Research, 49(1), 1–14.

- Humphrey, J., & Schmitz, H. (2002). How does insertion in global value chains affect upgrading in industrial clusters?. Regional Studies, 36(9), 1017–1027.

- Iansiti, M., & Lakhani, K. R. (2017). Managing our hub economy. Harvard Business Review, 95(5), 84–92.

- Kagermann, H., Helbig, J., Hellinger, A., & Wahlster, W. (2013). Recommendations for Implementing the strategic initiative INDUSTRIE 4.0: securing the future of German manufacturing industry; final report of the Industrie 4.0 working group. Forschungsunion.

- Kaiser, C., Stocker, A., & Viscusi, G. (2017). Digital vehicle ecosystems and new business models: An overview of digitalization perspectives. Paper presented at Platform Economy & Business Models workshop at i-KNOW ’17 October 11–12, 2017, Graz, Austria.

- KPMG. (2017). Global automotive executive survey 2017. Retrieved from https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2017/01/global-automotive-executive-survey-2017.pdf

- Krzywdzinski, M. (2017). Automation, skill requirements and labour‐use strategies: High‐wage and low‐wage approaches to high‐tech manufacturing in the automotive industry. New Technology, Work and Employment, 32(3), 247–267.

- LaGrandeur, K., & Hughes, J. J. (Eds.). (2017). Surviving the machine age: Intelligent technology and the transformation of human work. Cham: Springer.

- Lee, J., Bagheri, B., & Jin, C. (2016). Introduction to cyber manufacturing. Manufacturing Letters, 8, 11–15.

- Lewin, A. Y., Massini, S., & Peeters, C. (2009). Why are companies offshoring innovation? The emerging global race for talent. Journal of International Business Studies, 40(6), 901–925.

- Linares-Navarro, E., Pedersen, T., & Pla-Barber, J. (2014). Fine slicing of the value chain and offshoring of essential activities: Empirical evidence from European multinationals. Journal of Business Economics and Management, 15(1), 111–134.

- Manyika, J., Chui, M., Bughin, J., Dobbs, R., Bisson, P., & Marrs, A. (2013). Disruptive technologies: Advances that will transform life, business, and the global economy. San Francisco, CA: McKinsey Global Institute.

- McKinsey & Company. (2016). Automotive revolution – Perspective towards 2030. Retrieved from https://www.mckinsey.com/~/media/mckinsey/industries/high%20tech/our%20insights/disruptive%20trends%20that%20will%20transform%20the%20auto%20industry/auto%202030%20report%20jan%202016.ashx

- McLaughlin, S. A. (2017). Dynamic capabilities: Taking an emerging technology perspective. International Journal of Manufacturing Technology and Management, 31(1–3), 62–81.

- Monostori, L., Kádár, B., Bauernhansl, T., Kondoh, S., Kumara, S., Reinhart, G., ... Ueda, K. (2016). Cyber-physical systems in manufacturing. Cirp Annals, 65(2), 621–641.

- Navas-Alemán, L. (2011). The impact of operating in multiple value chains for upgrading: The case of the Brazilian furniture and footwear industries. World Development, 39(8), 1386–1397.

- Patton, M. Q. (1990). Qualitative evaluation and research methods. Newbury Park, CA.: Sage Publications.

- Pavlínek, P. (2017). Dependent growth. Foreign Investment and the development of the automotive industry in East-Central Europe. Cham: Springer.

- Pisano, G. P., & Shih, W. C. (2012). Does America really need manufacturing? Yes, when production is closely tied to innovation. Harvard Business Review, 90(3), 94–102.

- Ponte, S., & Ewert, J. (2009). Which way is ‘up’ in upgrading? Trajectories of change in the value chain for South African wine. World Development, 37(10), 1637–1650.

- Porter, M. E., & Heppelmann, J. E. (2014). How smart, connected products are transforming competition. Harvard Business Review, 92(11), 64–88.

- Rechnitzer, J., Hausmann, R., & Tóth, T. (2017). Insight into the Hungarian automotive industry in international comparison. Financial and Economic Review, 16(1), 119–142.

- Rehnberg, M., & Ponte, S. (2018). From smiling to smirking? 3D printing, upgrading and the restructuring of global value chains. Global Networks, 18(1), 57–80.

- Sass, M., & Kalotay, K. (2012). Inward FDI in Hungary and its policy context. New York: Vale Columbia Center on Sustainable International Investment. Retrieved from http://ccsi.columbia.edu/publications/test-fdi-profiles-page/

- Sass, M., & Szalavetz, A. (2013). Crisis and upgrading: The case of the Hungarian automotive and electronics sectors. Europe-Asia Studies, 65(3), 489–507.

- Sasson, A., & Johnson, J. C. (2016). The 3D printing order: Variability, supercenters and supply chain reconfigurations. International Journal of Physical Distribution & Logistics Management, 46(1), 82–94.

- Schumacher, A., Erol, S., & Sihn, W. (2016). A maturity model for assessing industry 4.0 readiness and maturity of manufacturing enterprises. Procedia CIRP, 52, 161–166.

- Shingo, S. (1986). Zero quality control: Source inspection and the poka-yoke system. Portland, Oregon: Productivity Press.

- Stevens, Y. A., & Marchant, G. E. (2017). Policy solutions to technological unemployment. In LaGrandeur & Hughes (Eds.), Surviving the Machine Age: Intelligent Technology and the Transformation of Human Work. (pp. 117–130). Cham: Springer.

- Strange, R., & Zucchella, A. (2017). Industry 4.0, global value chains and international business. Multinational Business Review, 25(3), 174–184.

- Sturgeon, T., & Lee, J. R. (2001, June). Industry co-evolution and the rise of a shared supply-base for electronics manufacturing. Paper Presented at Nelson and Winter Conference, Aalborg.

- Szalavetz, A. (2017). Industry 4.0 in ‘factory economies’. In B. Galgóczi & J. Drahokoupil (Eds.), Condemned to be left behind? Can Central Eastern Europe emerge from its low-wage FDI-based growth model? (pp. 123–142). Brussels: ETUI.

- Szent-Iványi, B. (2017). Investment promotion in the Visegrad four countries: Post-FDI challenges. In B. Galgóczi & J. Drahokoupil (Eds.), Condemned to be left behind? Can Central Eastern Europe emerge from its low-wage FDI-based growth model? (pp. 171–187). Brussels: ETUI.

- Tassey, G. (2014). Competing in advanced manufacturing: The need for improved growth models and policies. The Journal of Economic Perspectives, 28(1), 27–48.

- Teece, D. J., & Linden, G. (2017). Business models, value capture, and the digital enterprise. Journal of Organization Design, 6(1), 8.

- Tolio, T., Sacco, M., Terkaj, W., & Urgo, M. (2013). Virtual factory: An integrated framework for manufacturing systems design and analysis. Procedia CIRP, 7, 25–30.

- Tushman, M. L., & Anderson, P. (1986). Technological discontinuities and organizational environments. Administrative Science Quarterly, 31(3), 439–465.

- UNCTAD. (2018, March 19). Building digital competencies to benefit from existing and emerging technologies, with a special focus on gender and youth dimension. Retrieved from http://unctad.org/meetings/en/SessionalDocuments/ecn162018d3_en.pdf

- Vendrell-Herrero, F., Bustinza, O. F., Parry, G., & Georgantzis, N. (2017). Servitization, digitization and supply chain interdependency. Industrial Marketing Management, 60, 69–81.

- Xu, L. D., & Duan, L. (2018). Big data for cyber physical systems in industry 4.0: A survey. Enterprise Information Systems, 1–22. doi:10.1080/17517575.2018.1442934

- Yin, R. K. (2014). Case study research: Design and methods (5th ed.). Thousand Oaks, CA: Sage.

- Yu, D., & Hang, C. C. (2010). A reflective review of disruptive innovation theory. International Journal of Management Reviews, 12(4), 435–452.

Appendix.

Interview protocol

0. Basic facts: products, turnover (2016), share of exports, employment.

1. Adoption of industry 4.0 technologies

Have you deployed

new kinds of factory automation/robotisation solutions, or any collaborative robots?

cyber-physical systems, i.e. data extraction solutions?

any kind of workforce augmenting solutions? Please specify!

any kind of business process automation solutions (e.g. order management, reporting, production scheduling, remote maintenance etc.) Please give examples, which processes/tasks/activities have become automated, and why?

any Web 2.0-type knowledge sharing solution? (among workers/among subsidiaries)

business intelligence and analytics solutions (decision support software in production planning, process optimisation, predictive maintenance, workforce analytics, etc.)?

What happens with the extracted data? Are they just stored, or transferred to headquarters, or are they analysed on-site?

2. Please describe the motivations of deploying these technological solutions

(E.g. operational excellence, cost cutting, optimisation and process efficiency solution to labour shortage problems, transparency, flexibility)

3. Which activities and business functions were transformed as a result of digital technologies?

How did the activities/responsibilities of operators, technicians, process engineers, maintenance staff, logistics staff, quality control staff, etc. change? Please give some real-world examples!

Are there any new kinds of jobs (new job categories) related to the new technologies? Please specify!

4. Has the deployment of industry 4.0 technology fulfilled the related expectations? Please specify!

5. Impact of digital technology deployment on subsidiary performance

What are the major impacts of industry 4.0 technology deployment on subsidiary performance? (E.g. reduction of faults; reduced costs; increased flexibility; improved productivity? increased production volume? reduced cycle time?)

Are there any new, subsidiary-specific capabilities, developed as a result of the deployment of advanced manufacturing technologies?

Were there any new activities offshored to your company? If yes, was relocation enabled by the deployment of advanced technologies or was it driven by other factors?

6. Impact of digital technology deployment on mother company strategy

Can you tell me some words about the digital strategy of your mother company? What are the strategic focus areas?

Do you perceive any differences between the headquarters and the subsidiary in the purpose of industry 4.0 technology deployment?

Table A1. Investment in digital technologies.

Table A2. Components* of HQ digitalisation strategy.