ABSTRACT

After two decades of meagre results in post-Soviet regionalism, the Eurasian Economic Union (EAEU) is the first gleam of hope. However, research on the EAEU is mostly Russia-centred and focused on trade issues, which leaves the small states’ perspectives and developmental aspects, such as the EAEU’s industrial cooperation agenda, understudied. The small states might disproportionately benefit from a shift towards developmental regionalism, but there are also many challenges associated with this issue. Thus, this paper examines Armenia’s and Belarus’ industrial development prospects in the framework of the EAEU. Based on Regulation Theory, the paper triangulates data from national, supranational and international organisations, official EAEU documents and reports with insights from 10 expert interviews with policy makers, policy advisers and management consultants. The paper identifies diverging (and sometimes conflicting) interests regarding the relevance and concrete arrangement of industrial cooperation, which has particular implications for smaller member states like Armenia and Belarus.

1. Introduction

After the dissolution of the Soviet Union, the post-Soviet space witnessed several attempts at reintegration through regionalism. The first and most widely-known initiative was the Commonwealth of Independent States (CIS) in 1991, which was followed by many others (Libman & Vinokurov, Citation2018). Wirminghaus (Citation2012, p. 25) invokes 39 different regional integration initiatives between 1991 and 2010, which led to the creation of 36 organisations. As the sheer number testifies, those political projects were not always competing, but sometimes overlapping, and they encompassed different fields of cooperation. For example, after its creation in 2000, the Eurasian Economic Community (EurAsEc)Footnote1 comprised Belarus, Kazakhstan, Kyrgyzstan, Russia and Tajikistan. In the same period, the Collective Security Treaty Organisation (CSTO), with a focus on security cooperation, had exactly the same member states, plus Armenia (Molchanov, Citation2018). However, there is one feature that this range of organisations had in common until approximately 2010: they largely failed to accomplish their commitments. Scholars provide different explanations for this phenomenon. Wirminghaus (Citation2012) points to neorealist approaches in order to explain the motives for cooperation (forming alliances to counter the power of other groups of states) and the reasons for failure (the ultimate prioritisation of national interests). Furthermore, as do Libman and Obydenkova (Citation2018b), Wirminghaus mentions the authoritarian political structures in the CIS countries as the main obstacle to successful regionalism in Eurasia.

After a myriad of slowly advancing, overlapping and partially competing regional integration projects (Libman & Obydenkova, Citation2018b, pp. 156–157), in 2007 three countries inside the EurAsEC – Belarus, Kazakhstan and the Russian Federation – agreed to create a customs union (CU). This initiative to strengthen the trade ties among the post-socialist states finally came into force in 2011 (Molchanov, Citation2016, p. 119; Obydenkova & Libman, Citation2012, p. 379). It was the first example of successful post-Soviet regionalism, meaning that the members formally and to a very large degree realised their commitment (Libman & Vinokurov, Citation2018). Subsequently, the national authorities of the EurAsEc countries and their supranational organ, the 2012-founded Eurasian Economic Commission (EEC), took several steps to intensify cooperation; for instance, they coordinated their national industrial policies to promote structural change in the manufacturing sector.Footnote2 On 1 January 2015, they further intensified cooperation by founding the Eurasian Economic Union (EAEU), which Armenia joined on January 2 and Kyrgyzstan on August 6 of the same year.

While the creation of a customs union is typical for trade-centred, ‘open’ or ‘new’ regionalism, the additional inclusion of the industrial sphere provides the integration process with a developmental dimension. According to regional economic integration theory this could be particularly beneficial for the industrial development of the smaller member states, because the access to a larger market bears the potential to reap economies of scale (Balassa, Citation1961/1973, p. 160). However, it has also been argued that the benefits of cooperation might be distributed unequally among the partners, which is even more likely when the asymmetries are big – as is the case in the Eurasian Economic Union (Sloan, Citation1971, pp. 151–152; Vinokurov & Libman, Citation2012, pp. 174–175). For the Eurasian Economic Union, the small states’ perspective on such developmental issues is still understudied. Thus, this paper examines the Armenian and Belarusian industrial development prospects in the industrial cooperation framework of the EAEU. Which opportunities and challenges actually prevail? This paper contributes to the more general debate on the Eurasian economic integration process by analysing the industrial cooperation initiative in the framework of the EAEU from an Armenian and Belarusian perspective. The article deals with these two countries, because they are both under the influence of two competing regional initiatives, the European Union’s Eastern Partnership and the EAEU (Vieira & Vasilyan, Citation2018). This has specific implications for their industrial development options (differing from those of Kazakhstan and Kyrgyzstan).

In the theoretical realm, the investigation draws on Regulation Theory. Methodologically, the paper builds on macroeconomic data from national, supranational and international organisations, official documents and reports. I combine these sources with the insights from 10 expert interviews (see list in the Appendix), conducted with politicians, policy advisers, business representatives and researchers, coming mostly from Armenia and Belarus, who were either involved in industrial policy making, or were policy advisers or researchers that studied topics which are relevant for the successful implementation of industrial policy, e.g., institutional issues or macroeconomic policy.

After outlining the theoretical framework, the paper introduces the orientation and evolution of industrial cooperation in the EAEU. The next chapters analyse the prevailing mechanisms of accumulation and regulation in Armenia and Belarus, with particular emphasis on features related to manufacturing. Based on the country-specific findings, the paper focuses on opportunities and challenges for industrial cooperation from the small states’ perspective. After summarising the results of the investigation, the conclusion will also illustrate alternatives and complements to the current industrial cooperation initiative.

2. The political economy of regional integration

In the theoretical realm, the paper draws on Regulation Theory, which originated in the 1970s in France and focused on explaining the crisis of Fordism (Becker, Citation2013, pp. 31–33). However, the theoretical approach has also been used to examine regional integration projects in the semi-periphery (Becker, Citation2006). A regulationist analysis departs from the basic features of capital accumulation. Based on Aglietta’s work, Joachim Becker (Citation2006, pp. 12–16) distinguishes three axes of accumulation, which define in their interplay the accumulation regime. The first – and most basic – axis investigates whether accumulation is predominantly driven by investment in the productive or financial sector of the economy. However, for semi-peripheral countries with a strong reliance on raw materials, Jäger and Leubolt (Citation2014) suggest introducing ‘resource-based’ accumulation as a third category. The second axis examines whether accumulation is extensive or intensive, and thus, whether the surplus creation depends on the expansion of production capabilities or on the increase of productivity (e.g., through technological innovation). Finally, the third axis differentiates between an orientation towards the domestic market (intraversion) or towards the regional or world market (extraversion). Extraversion is active if the focus lies on exports or passive if high dependency on imports of goods, capital and/or remittances prevails (Aglietta, Citation2015; Becker, Citation2013). The dominant forms of accumulation set up a corridor of options for industrial development. Industrial policy as state intervention promoting structural change aspires to shift accumulation into a more productive and intensive direction. Whether it prefers an inward or outward-oriented strategy depends on the specific historical and socio-spatial context.

As capitalist accumulation is a crisis-ridden process, the stabilisation of an accumulation regime requires specific economic and social policies, as well as legal and social norms. These are the outcome of social struggles among different actors. Regulation Theory captures them in four structural forms of regulation, which attempt to mediate the prevailing conflicts and constitute as a whole the mode of regulation. The most important structural form related to industrial development is the regulation of competition among different capital groups and economic sectors, but also among (groups of) workers. Furthermore, the rules for foreign direct investment (FDI) play a central role in this field, because they determine the scope of action for national and foreign capital.

The other three structural forms of regulation also influence industrial policy making. Second is that of monetary restriction, which encompasses macroeconomic policy and lending conditions. For example, the exchange rate is crucial for ensuring competitiveness and, thus, can thwart industrial development if it is overvalued. Furthermore, the access to cheap credit and loans is a decisive factor for industrial development. Third, the wage relation is concerned with the regulation of the industrial relations between employers and workers. Industrial policy influences the wage relation, because it aims at modifying the structure of an economy, which also affects the labour market. Lastly, the ecological restriction sets the accumulation process natural limits, because industrial production relies on the extraction and/or import of (scarce) resources in order to process them. Finally, the state is one of the main institutions upholding regulation and is therefore present in all structural forms (for the theoretical basis see Becker, Citation2013, pp. 24–56; Sablowski, Citation2013, pp. 88–97). Hence, the effectiveness of industrial policy measures partially depends on the functional interplay of the structural forms of regulation. Therefore, industrial policy making needs to accurately consider them as framework conditions.

While Regulation Theory in most cases uses the nation state as the central unit of analysis, some scholars, for example, Becker (Citation2006), have applied it to regional integration schemes, for instance, to the EU, the Common Market of the South (MERCOSUR) and the Southern African Development Community (SADC). From a regulationist perspective, the (partial) expansion of the space of accumulation to the regional scale equates to what theories of regional integration call (bottom-up) ‘regionalisation’, while the creation of forms of regulation on the regional scale would be state-led (top-down) ‘regionalism’ (Vinokurov & Libman, Citation2012, pp. 44–56). In the former case, regional integration is mostly a market-driven process, in which private economic actors play an important role, whereas in the latter case states coordinate the process of deepening cooperation and exchange. In this context, the scales to which the single forms of regulation apply can vary (Becker, Citation2009, p. 101), which implies that they can stall each other. For example, regulations adequate for the national accumulation strategy might hamper regional industrial policy. It becomes even more complicated, when the integrating states follow different – or even competing – accumulation strategies. This can hamper the implementation of specific joint industrial policy measures, and will impede the emergence of a congruent regional development strategy (Becker, Citation2006, pp. 11, 22).

From a neoclassical perspective, regional economic integration increases the welfare of the participating nations, because it raises the efficiency of their economies by generating more trade creation than trade diversion (Viner, Citation1950/2014, p. 55). In addition to these static effects of integration, Bela Balassa specified possible dynamic effects, which he expected due to the increase of the market size. The larger market would allow the exploitation of internal economies, leading to increased productivity, particularly for manufactured goods (due to increasing returns to scale). Moreover, it would also promote external economies, which favour, inter alia, specialisation in the industrial sector and ‘induced technological change’. Small states would particularly benefit from the abolition of trade barriers, as their small markets seriously restrict industrial development opportunities (Balassa, Citation1961/1973, pp. 120–162). This is a trade-centred approach to regional economic integration, although it encompasses particular assumptions on how industries would develop, particularly in manufacturing (Balassa, Citation1961/1973, pp. 173–183).

Other, moderately liberal scholars such as Friedrich List favoured a more development-centred approach to regionalism (Becker, Citation2006, pp. 21–22). From this perspective, states should actively promote their industrial development in the regional bloc – on the single country level and jointly. For (semi-)peripheral countries, scholars developed, based on List’s legacy, the concept of ‘developmental regionalism’ for economic catch-up (Gordon, Citation1961, pp. 245–250; Sloan, Citation1971, p. 140). Development-centred regionalism would serve ‘not only to expand trade but also to encourage the emergence of new industries, to help diversify national economies, and to increase the region’s bargaining power with developed nations’ (Sloan, Citation1971, p. 143; Gordon, Citation1961, pp. 247–248). Thus, the concept aspires to shift the accumulation of a particular (sub-)region towards more productive, intensive and – at least partially – intraverted accumulation (in order to decrease external dependence). However, also among (semi-) peripheral countries, large asymmetries may exist, which can cause the largest economy to reap most of the benefits (Sloan, Citation1971, pp. 151–152).

Based on these assumptions, this paper interprets the EAEU’s industrial cooperation initiative as a (possible) developmental aspect of the Eurasian integration process and examines the associated opportunities and challenges from the perspective of two small member states – Armenia and Belarus.

3. Industrial cooperation in the EAEU

3.1 Antecedents

All EAEU member states formerly belonged to the Union of Soviet Socialist Republics (USSR), the centrally planned economy of which was closely integrated through production chains traversing different republics (Libman & Obydenkova, Citation2014, p. 173). Their level of industrial output was very high. In 1975, this output represented 64.7% of the total output of the USSR, while in 1980 it still amounted to 63.6% (Yarashevich, Citation2014a, p. 20). For our topic, this has two important implications. First, the Soviet republics had achieved a considerable level of industrialisation, but they fell short of global competitiveness, which is still a problem in the industrial sphere. Second, while some of the production chains broke apart, a significant share of the economic ties survived the transition period and still condition economic development opportunities (Libman & Obydenkova, Citation2014). Hence, we are currently witnessing a process of reintegration amid new circumstances (Libman & Obydenkova, Citation2014; Yarashevich, Citation2014a).

When the USSR dissolved in 1991 and the transition to capitalism followed, a process of primitive accumulation with strong capital concentration set in, which has very negatively affected the industrial sphere of the former Soviet republics (Becker, Citation2018; Jaitner, Citation2015, pp. 520–521). Mass privatisations in the transition economies created a new oligarchic elite, showing rent-seeking behaviour. At the same time, strategic companies fell into foreign ownership. This entailed a new distribution of power in most of the ex-Soviet republics. Oligarchs and foreign investors were mainly interested in natural resources and financial assets, not in the (non-competitive) manufacturing enterprises (Yarashevich, Citation2019, pp. 427–428). The mixture of a reduced tax revenue of the states, disinvestment in the industrial sector, and the restructuring of the industrial capacities led to serious de-industrialisation (Becker, Citation2018; Chasovsky & Katrovsky, Citation2015, p. 16). The remaining industrial base was characterised by outdated machinery and equipment and was to a large degree uncompetitive on the world market. Belarus is the huge exception among the current EAEU members, because it never witnessed large-scale privatisations with the subsequent rise of a new oligarchy. This is one of the reasons why it could preserve a relevant share of its Soviet industrial base (Yarashevich, Citation2014a, p. 54), albeit lacking modernisation (see below). Additionally, with the dissolution of the Soviet Union, many of the institutions implementing industrial policy or dedicated to research and development (R&D) activities became obsolete and significant part of them disappeared. Thus, along with industrial capacities, a substantial part of industrial and innovation capabilities faded away. However, in the 2000s, a global trend to rehabilitate industrial policy after decades of neoliberalism (Andreoni & Chang, Citation2016b; Cimoli et al., Citation2008; Rodrik, Citation2004, Citation2008; Stiglitz et al., Citation2013) coincided with the Soviet legacy of industrial planning.

3.2 Main documents and evolution of industrial cooperation

From the very start, the official documents of the Eurasian integration process were concerned with industrial development. When the customs union between Belarus, Kazakhstan and Russia commenced operation in 2011, and the creation of the Single Economic Space was prepared, the national rules for the provision of industrial subsidies were harmonised. In May 2013, the parties agreed on the coordination of national industrial policies (Eurasian Economic Commission (EEC), Citation2018, p. 39). Furthermore, they defined 19 priority industries that they planned to jointly promote within the newly established single economic space (Sidorsky, Citation2013, p. 26). Article 92 of the founding treaty on the EAEU explicitly discussed ‘industrial policy and cooperation’, while Article 93 defined the legal basis for industrial subsidies (EEC, Citation2018, pp. 42–51). Only a few months later, in September 2015, the five member states approved the ‘Main Directions on Industrial Cooperation’ (EEC, Citation2015b). This was followed by the document ‘EAEU Industrial Policy: From its creation to the first results’ (EEC, Citation2015a), which readopted and slightly modified the 19 priority sectors mentioned above. Notably, several manufacturing sectors associated with extractivism were added to the later version (printed in bold, ). Finally, in 2018, ‘Industrial Policy in the Eurasian Economic Union: Three Years of Integration’ (EEC, Citation2018) summarised the achievements and challenges of the first three years of industrial cooperation.

Table 1. Industrial priority sectors in 2013 and 2018

The Main Directions formulated the following goals for industrial policy in the EAEU: a) to increase the growth rates and the output of industries; b) to promote cooperation, for example, creating new joint value chains through the development and implementation of joint protectionist measures; c) to increase the share of EAEU products in the common market; d) to develop new competitive and export-oriented manufacturing activities in order to increase exports towards third countries, supported by joint trading and service networks; e) to achieve technological upgrading in existing sectors and to build up new innovative sectors; f) to eliminate trade barriers for industrial products in the EAEU; and g) to attract investments and funding options for companies of the industrial sector (EEC, Citation2015a, pp. 41–56).

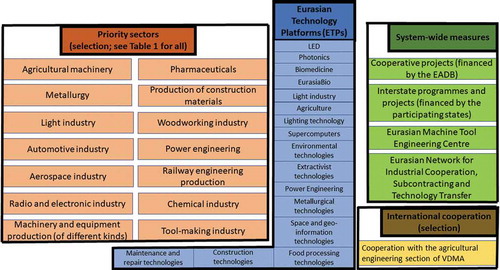

As of 2020, the industrial cooperation matrix of the EAEU has four main components (see ), which are in the following stages:

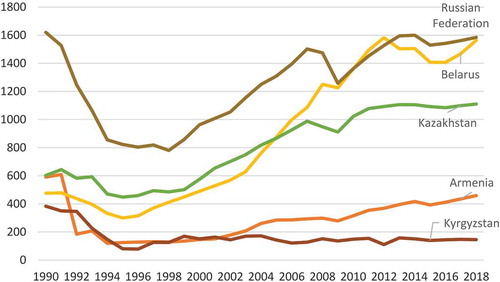

Figure 1. MVA per capita (constant 2010 USD), 1990–2018

Figure 2. The EAEU’s industrial cooperation

(1) In 2015, 19 priority sectors for industrial cooperation were defined (see ; EEC, Citation2015a, pp. 62–65). According to the EEC, the preparatory works with respect to regulatory and legal terms in 14 sectors have advanced considerably in the meantime and will soon allow for the implementation of the first projects (see ; EEC, Citation2018, pp. 56–78). The implementation of concrete projects can take the form of the options listed among 2), 3) and 4).

(2) The cooperation in science, technology and innovation relies on the Eurasian Technology Platforms (ETPs), of which some are directly allotted to a priority sector. For example, the ETP ‘Space and geo-information technologies’ belongs to the priority sector ‘Space industry’. The ETPs strive to promote the interaction between scientific, industrial and government entities in order to develop and introduce cutting-edge technology into production processes (EEC, Citation2020a, p. 75). In 2018, the EEC (Citation2018, p. 82) stated that eight cooperative projects connected to the ETPs were identified as mature enough for the investment stage (to apply for a loan by the Eurasian Development Bank), while 37 needed more detailed elaboration, and a further 85 involving R&D required venture financing. According to the EEC, ‘[a]t the moment, we are seeing the transition from selection to the implementation of such projects and interstate programs’ (EEC, Citation2020a, pp. 74–76).

(3) The so-called ‘system-wide’ (horizontal) measures encompass cooperative projects and interstate projects or programmes. While the former might receive funding from the Eurasian Development Bank, the latters’ budget comes directly from the participating member states. A working group of the EEC has identified cooperative projects with great integration potential and contacted potential participants. At the same time, business representatives can approach the Commission with proposals (EEC, Citation2018, p. 44, Citation2020b, p. 52). The most advanced interstate programme is in the space industry, where the member states plan to jointly develop space and geo-information technologies and to ultimately build satellites together. In September 2018, the Russian Federation, Kazakhstan and Belarus signed an agreement for developing the project (EEC, Citation2018, pp. 61–62, Citation2020a, pp. 76–77, Interview 6, 2018, para. 16). Regarding the other projects, the author could not identify any that would be close to launching.

Furthermore, the Commission and the EAEU member states had agreed in 2015 to found a Eurasian Machine Tool Engineering Centre and a Eurasian network of industrial cooperation and subcontracting. The Engineering Centre was to be based at the MSTU Stankin in Moscow (EEC, Citation2020a, p. 71). According to more recent sources, it has been created (EEC, Citation2020b, p. 52) and ‘now it is starting to work’ (EEC, Citation2020a, p. 72). However, at the website of MSTU Stankin, the latest news with respect to the Engineering Centre is from 9 July 2019 and the author could not find any evidence that the Centre is actually in operation. The Eurasian network of industrial cooperation and subcontracting, in turn, merged with the projected Eurasian technology transfer network (ETTN) to become the Eurasian Network for Industrial Cooperation, Subcontracting and Technology Transfer. Under www.eurasianindustry.org, the EEC created a digital platform to collect information on industrial activities and to connect industrial enterprises. It is online and displayed, on 11 May 2020, 6003 registered enterprises (EEC, Citation2018, p. 103). According to the EEC (Citation2020a, pp. 78–79), this is still the pilot project. It is planned to launch the network in 2021.

(4) Finally, industrial cooperation also has an international dimension. The aim is to integrate domestic (Eurasian) production into global value chains (GVCs). Currently, the Commission, together with the agricultural engineering section of VDMA, the German Mechanical Engineering Industry Association, attempts to create new production facilities in the EAEU’s territory. In 2018, the EAEU started a pilot project to become a supplier of a German equipment division; of US company John Deere, the world leader in agricultural engineering (EEC, Citation2020b, pp. 50 Interview 6, 2018, para. 17).

Overall, the EAEU’s industrial cooperation initiative appears to be an extension to the region of the Russian industrial policy, which also draws on top-down policies in the form of priority sectors and technology platforms (United Nations Industrial Development Organization (UNIDO), Citation2017, pp. 147–161). This might be explained by the huge asymmetries prevailing in the EAEU, with Russia accounting for more than 87% of the EAEU’s industrial output and 85% of the gross value added industrial output, while Belarus’ share amounts to 5.0% and 3.7%, and Armenia’s only to 0.3% and 0.4%, respectively (EEC, Citation2015b, p. 11). Thus, the question arises as to what extent the regional industrial development strategy fits the needs of the smaller member countries. In this context, we will deal now with the cases of Armenia and Belarus by first analysing their national modes of accumulation and regulation before outlining the related opportunities and challenges.

4. The small states’ perspective

4.1 Armenia’s industrial development prospects

Several peculiar features characterise Armenia’s economic structure and condition to some extent its growth prospects, particularly in manufacturing. Armenia is a small country with a reduced market size, which is further aggravated by its landlocked position and the geopolitical isolation of the country – due to border conflicts with Azerbaijan and Turkey (Hartwell, Citation2016, p. 58; Ter-Matevosyan et al., Citation2017, pp. 344–345). After the end of the Soviet Union, Armenia was among the ex-republics which most consequently implemented the ‘shock therapy’ of sudden and far-reaching trade and market liberalisation. This led to a massive fall of output (Chobanyan & Leigh, Citation2006, p. 148), with a steep decline of MVA per capita between 1990 and 1992 (see ). The MVA per capita in real terms (measured at constant 2010 US dollar exchange rates) needed about 10 years to again reach the level of 1992, which was already only a third of the value of 1990. Even today, Armenia’s MVA per capita is still below the level of 1990. This number becomes even more remarkable if we consider that the population decreased from 3.5 Million in 1990 to 2.9 Million in 2018 (UNIDO, Citation2020).

Productive vs. financialised accumulation

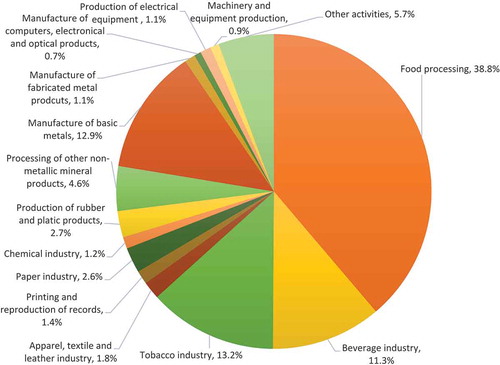

The Armenian accumulation process is import-driven. In 2018, the industrial sector was responsible for 18.4% of GDP, witnessing a continuous increase from 16% in 2014. The contribution of industry to GDP, value added amounted even to 20.5% in 2018 (National Statistical Service of Armenia (Armstat), Citation2019, pp. 267, 271). In the Armenian industrial sector, mining and quarrying held a share of 15.5% in 2018, while manufacturing accounted for 69.8% of industrial activities. Food processing (38.8%), the tobacco industry (13.2%), manufacturing of basic metals (12.9%) and the beverage industry (11.3%) were the biggest manufacturing branches in 2018 (see in the Appendix; Armstat, Citation2019, pp. 270–271). According to UNIDO’s Competitive Industrial Performance Index (CIP) for 2019, in 2017 79.0% of Armenia’s manufacturing was resource-based, while low-tech (7.7%), medium-tech (10.9%) and high-tech (2.3%) manufacturing fell far behind (UNIDO, Citation2019a, p. 8). Furthermore, only 13.8% of the economically active population in 2018 worked in the industrial sector. Considering only manufacturing, it was 10.2% of the total workforce (Armstat, Citation2019, p. 73).

Extensive vs. intensive

Armenia inherited a large but inefficient industrial sector from the Soviet period. Privatisation and restructuring during the 1990s decimated industry, but did not resolve the problems of low productivity and lack of modernisation. Currently, the share of outdated machinery and equipment is estimated at 80% (EEC, Citation2018, p. 65; United Nations Economic Commission for Europe (UNECE), Citation2014, p. 43). In 2011, the government approved the national ‘Strategy of Export-oriented Industrial Policy of the Republic of Armenia’, selecting 11 industrial branches which had potential for export orientation and job creation. While most of those had existed since Soviet times and exploited the current comparative advantage, the authorities decided to newly develop the pharmaceutical and biotechnology sector (Interview 3, 2018, para. 44–57). The Ministry of Economy is responsible for the implementation of the industrial policy strategy, which broadly aims to promote industrial upgrading, to create new labour-intensive industries, and to develop more knowledge-intensive activities. The targeted industries were metal mining, metallurgical production, food production, production of precious stones and jewellery, machinery and equipment production, pharmaceutical production, and textile production (EEC, Citation2015b, pp. 26–28; UNIDO, Citation2017, pp. 164–167). Overall, the industrial policy strategy points to the attempt to promote intensive accumulation in manufacturing.

According to the World Economic Forum, Armenia was, in the first half of the 2010s, at the border between a factor-driven and an efficiency-driven economy, which means that it was moving from competing based on its factor endowments (cheap wages) to competing based on increasing resource efficiency, that is, labour productivity (UNECE, Citation2014, p. 6). In this context, innovation policy becomes a crucial component of industrial policy. The accumulation of knowledge and technological capabilities become the main target of the so-called ‘national system of innovation and production’ (Cimoli et al., Citation2008), which is comprised of a network of institutions that are related to the innovative performance of national firms. Intensive growth is thus a ‘process of continuous technological innovation, industrial upgrading and economic diversification’ (Stiglitz et al., Citation2013, p. 10).

During Soviet times, Armenia was an important science hub of applied research, for example, in the fields of physics, astrophysics, computer science and information technologies, as well as biotechnology. As the R&D sector was closely integrated with the Soviet industrial structure, the volume of researchers, research institutes and R&D funding shrank dramatically after 1991. The number of researchers declined from 25,344 in 1991 to 4,452 in 2018, while the number of research institutes nearly halved from 124 to 63 in 2018 (Armstat, Citation2019, pp. 164–165; UNECE, Citation2014, p. 15). In the USSR, Armenia spent more than 2.5% of its GDP on R&D, while in 2018 the share was barely 0.2% (UNECE, Citation2014, pp. 15, 49; World Bank, Citation2019). Thus, while Armenia has a strong tradition in this field, it has been considerably weakened during the past 30 years.

Intraversion vs. extraversion

The Armenian economy shows strong characteristics of passive extraversion, expressing itself in the high dependence on the import of capital and goods, thus causing a chronically negative trade balance (−13.16% in 2017). Armenia depends on the inflow of FDI and remittances, the latter surpassing the former in quantity since 2010. In 2017, they made up 13.32% of the Armenian GDP (United Nations Conference on Trade and Development (UNCTAD), Citation2017). According to Armstat (Citation2019, pp. 496, 498), Russia was Armenia’s main export and import partner in 2018 (see ). However, the sum of exports going to EU countries was higher than the sum going to CIS countries in 2017. In detail, Armenia exports to the other CIS countries (mainly Russia) exhibit a higher value added than those to the EU, which are mostly unprocessed raw materials. This highlights the importance of the Eurasian Common Market for Armenia and shows potential for industrial cooperation (Armstat, Citation2019, pp. 470–484; for an overview according to SITC categories see Yarashevich, Citation2019, p. 414).

Table 2. Main trading partners of Armenia (2018)

Competition

There exist several dividing lines between different interest groups and capital factions in Armenia. While the most powerful capital group is that of trading capital, which correlates with the import-driven accumulation pattern, industrial capital is far weaker (Interview 10, 2019, para. 74). Part of the business community is oriented towards the EU and another part towards Russia/EAEUFootnote3 (Vasilyan, Citation2017, p. 42). The alignment depends on the import or export orientation and the field of economic activity of the respective business people. Industrial capital is markedly oriented towards Russia/the EAEU, because this is its major export market, and it could also have a potential interest in increased industrial cooperation. However, Armenia exhibits ‘abundant monopolies in various import and export sectors’ (Ter-Matevosyan et al., Citation2017, p. 350), the owners of which have close relations with the political elites (Ter-Matevosyan et al., Citation2017, pp. 348–352; Vasilyan, Citation2017, p. 34). They would only support industrial cooperation if their influence was not curbed (Interview 10, 2019, para. 28). Finally, Russia plays a relevant role in the sphere of competition. According to Armstat (Citation2019, p. 536), the biggest holder of net stocks of foreign total investment in Armenia was by far Russia, with 1,015,592.5 million drams at the end of 2018, of which 842,494.6 million drams are FDI (Armstat, Citation2019, pp. 531–532). However, the Russian investments are mostly not greenfield investments, but acquisitions of existing enterprises, mostly related to energy and infrastructure (Vasilyan, Citation2017, pp. 36, Interview 10, 2019, para. 32–36). Arguably, industrial cooperation favouring industrial development in Armenia would require that Russia changes or at least broadens its investment pattern.

Monetary restriction

The macroeconomic environment can be very discouraging for the industrial development of a country (Becker, Citation2009, p. 105), which is currently the case for Armenia. The monetary policy aims at keeping inflation low in order to control the level of public debt. Furthermore, the overvalued exchange rate strengthens Armenia’s import position, which favours import-oriented capital groups as well as remittance receivers, but it impedes industrial exports and therefore intensifies the problem of low competitiveness (Interview 10, 2019, para. 18, 22–26). In addition, interest rates are quite high (in order to attract foreign capital), which complicates borrowing money for productive investments (Central Bank of Armenia, Citation2019; Chobanyan & Leigh, Citation2006, p. 152). Thus, the macroeconomic sphere currently leaves lots of space for improving the conditions for developing manufacturing.

Wage relation

During the Soviet period, Armenia was famous for its high-skilled workers and strong education system. From the 1990s onwards, Armenia has exploited the relatively low wages of its highly-qualified workforce as a competitive advantage (Chobanyan & Leigh, Citation2006, p. 151). However, in combination with high unemployment, the low remuneration has also been an incentive for labour migration (UNECE, Citation2014). Interviewee 1 (2017, para. 28) compared labour migration to a ‘life jacket’ that ‘helps the national economies to float, it helps people to survive. But, on the other hand, it’s a brain drain. Highly qualified people leave the country as the first ones and then people with some qualifications also leave.’ Thus, while securing the possibility of work migration to the Russian labour market was one of Armenia’s main interests in joining the EAEU, the constant outflow of labour migrants also complicates the local accumulation of the capabilities necessary for industrial development. Eventually, successful reindustrialisation would create high-quality jobs (Andreoni & Chang, Citation2016a) and, thus, could contribute to the reduction of unemployment and poverty in Armenia (Interview 2, 2018, para. 44).

Ecological restriction

As Armenia has only few specific mineral reserves, and only 17.5% of the land is agriculturally arable (Chobanyan & Leigh, Citation2006, p. 153), many raw materials for industrial production need to be imported. Furthermore, Armenia depends on Russia in the energy domain. On the one hand, Armenia receives Russian gas and oil at preferential prices (Vasilyan, Citation2017, p. 37). On the other hand, Russia uses this energy-dependency to increase its influence in Armenia. For example, Armenia sold the 20% state share of ArmRusGazArd to Russia to get the 300 Mio. national debt waived, before it joined the CU. Furthermore, since 2006, Russia has had exclusive control over 75% of the Iran-Armenian gas pipeline (Ter-Matevosyan et al., Citation2017, pp. 349–350). The strong dependence on foreign energy resources is a serious constraint for industrialisation efforts.

4.2 Belarus’ industrial development prospects

Belarus is one of the few former Soviet republics that did not experience severe de-industrialisation after the dissolution of the Soviet Union and where central economic activities remained under state control. The state sector is estimated to still account for 60 to 70% of all economic activities (Becker, Citation2018; Yarashevich, Citation2014b, pp. 1707–1708). The reason for this is that Belarus was reluctant to implement structural reforms in the transition period. The MVA per capita in real terms (measured at constant 2010 US dollar exchange rates) of Belarus fell from 1990 until 1995, but steadily increased from 1996 onwards, recovering to the level of 1990 in the year 2000. In the past 20 years an impressive growth of MVA took place. In 2018, the MVA per capita were three times as high as in 1990 (UNIDO, Citation2020).

Productive vs. financialised accumulation

The Belarusian economy is oriented towards productive accumulation. As mentioned before, Belarus inherited a solid manufacturing base from Soviet times. This placed it in a good starting position when the USSR dissolved (Bell & Bell, Citation2015; for a more critical position regarding the Soviet industrial legacy, see Bonatti & Haiduk, Citation2014). In the transition phase, Belarus could avoid extensive privatisation (as took place in many other republics), because of its growth performance during the previous two decades (still forming part of the Soviet Union). When Lukashenka came to power in 1994, only 13% of the state-owned enterprises (SOEs) had been privatised (Bell & Bell, Citation2015, p. 156). Up to the present day, the Belarusian state dominates the economy and controls the biggest manufacturing enterprises (UNIDO, Citation2017, p. 167). In 2017, according to UNIDO’s Competitive Industrial Performance Index (CIP) for 2019, 44.6% of Belarus’ manufacturing was resource-based, 15.6% low-tech, 36.5% medium-tech and 3.3% high-tech. With these features Belarus belongs to the ‘Industrialized Economies’ and is the only EAEU member apart of Russia that forms part of the ‘Upper Middle’ CIP quintile (UNIDO, Citation2019b, p. 8). In 2018, 23.7% of the economically active population worked in the industrial sector, and 20.2% if we consider only manufacturing (National Statistical Committee of the Republic of Belarus (Belstat), Citation2019b, p. 76).

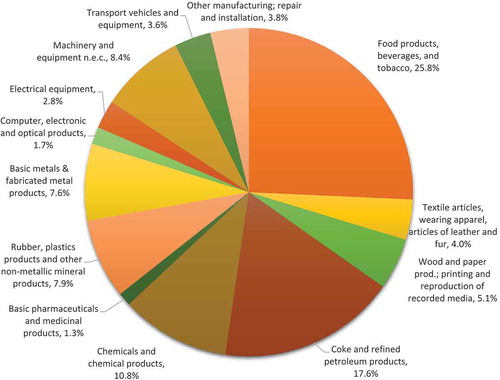

In 2018, the industrial sector accounted for 26.1% of the Belarusian GDP (Belstat, Citation2019a, p. 33). Manufacturing was responsible for 88.6% of total industrial production in 2018 (Belstat, Citation2019a, p. 42). According to the Competitive Industrial Performance Index for 2017, 44.6% of Belarusian manufacturing was resource-based (UNIDO, Citation2019b, p. 8). The high resource-based manufacturing share is extraordinary for a resource-poor country such as Belarus. The reason is that Belarus receives crude oil from Russia on preferential prices that it processes and (partly) re-exports (Libman & Obydenkova, Citation2018a, p. 1053). Belarus has a quite diversified manufacturing sector with food, beverages & tobacco manufacturing (25.8%), coke and refined petroleum products (17.6%), chemicals and chemical products (10.8%), rubber and plastic products (7.9%), and basic and fabricated metals (7.6%) holding the biggest shares (see in the Appendix; Belstat, Citation2019a, p. 42). Thus, manufacturing is the backbone of the Belarusian economy.

Intensive vs. extensive

There exists a productivity gap between the SOEs and the companies of the private sector. This is the outcome of structural reforms reluctantly undertaken in the transition period, which helped to preserve the old industrial structure, characterised by low efficiency and insufficient modernisation (Dobrinsky et al., Citation2016, pp. 51, 78). The EEC (Citation2018, p. 65) estimates the share of outdated machinery and equipment in Belarus to be 78% of the total. The Belarusian authorities have mentioned the need to modernise and to become more efficient in several industrial policy documents that attempt to set the agenda for intensive accumulation in order to decrease the gap in labour productivity with the EU countries, to modernise the productive capacities, and to expand the high-tech sector (EEC, Citation2015b, pp. 32–33; Gotovsky, Citation2015; UNIDO, Citation2017, pp. 167–171). To this end, Belarus also created six free economic zones, the Chinese-Belarus industrial park ‘Great Stone’, and the Belarusian High Technology Park (Dobrinsky et al., Citation2016, pp. 86–87). Thus, the national industrial policy aims at promoting a knowledge-based, innovative industrial development. Thereby, it builds on its Soviet legacy, having ‘preserved engineering competencies in large enterprises, capabilities in the research and development (R&D) sector and a skilled labour force’ (UNECE, Citation2011, xvi). Currently, the third State Programme for Innovative Development (SPID) (2016–2020) is in place, which seeks to modernise the Belarusian industry and to increase international competitiveness (UNECE, Citation2017, p. 22). However, Belarus has been criticised for focusing exclusively on marketable technological innovation and for ‘selling’ pure industrial modernisation initiatives as innovation projects (UNECE, Citation2017, pp. 23–24). Hence, Belarus can contribute to technological modernisation, innovation and upgrading at the EAEU level, but needs, in parallel, to transform its own production structure.

Intraversion vs. extraversion

While Belarus attempts to implement a coherent national development strategy and protects the local production in strategic sectors against foreign competition (Interview 5, 2018), the size of the country makes an exclusive inward-orientation impossible. In 2018, 62.5% of total industrial production was exported (Belstat, Citation2019a, p. 40). Of all commodity exports, in 2018 the largest groups were mineral products (25.8%), machinery and equipment (16.4%), chemical products and rubber (19.0%), as well as food products and agricultural raw materials (15.4%) (Belstat, Citation2019b, p. 376). As was the case during Soviet times, Russia is by far Belarus’ biggest trading partner. In 2018, 38.4% of all goods exported from Belarus went to Russia, while 58.9% of imports came from Russia (see ; Belstat, Citation2019a, p. 61). The manufactured high value-added products go to the CIS countries (mainly to Russia), while raw materials are exported to non-CIS countries (mainly to Europe; Yarashevich, Citation2019, p. 414). Thus, in this sphere rests the potential for cooperation in order to intensify the productive integration of the EAEU economies, which would also imply increasing the trade of intermediate goods within Eurasian supply chains.

Table 3. Main trading partners of Belarus (2018)

Competition

The state is still dominant in the economy, particularly in the industrial sector, and foreign capital, as well as private enterprises, is still subject to many restrictions. SOEs are often subsidised, even if they are not efficient and/or competitive in their current state (UNIDO, Citation2017, pp. 167–168). Bonatti and Haiduk (Citation2014, p. 3) describe the Belarusian industrial structure as ‘the coexistence of a viable private sector of small and medium-sized enterprises with a bunch of unreformed industrial giants.’ They argue that in the current setting, ‘well-performing enterprises are subject to heavy taxation and other extraction measures. A relatively small but viable private sector is often playing the role of donor for the state sector’ (Bonatti & Haiduk, Citation2014, p. 5). However, it is not only the political opposition and foreign actors who argue in favour of loosening the strict regulations for competition in Belarus. There is also a wing in the state authorities that favours such a solution,Footnote4 which would allow the attraction of larger FDI flows from EU countries and – possibly – the insertion of Belarusian firms into EU value chains. While the positive effects of FDI attraction for industrial development are widely recognised (Warwick, Citation2013, p. 37), the stronger orientation towards Europe would make serious restructuring of the manufacturing sector inevitable (Interview 5, 2018, para. 24), which would come at a social cost. Currently, the inflows of Russian FDI (60% of the total) allow Belarus to preserve its current industrial structure without restructuring measures (Dobrinsky et al., Citation2016, p. 82).

Monetary restriction

Since 1996, the Belarusian authorities have extensively used macroeconomic policy to support their development model. With regard to industrial development, so-called ‘directed lending’ was of particular relevance. Through this mechanism, state-owned banks supported SOEs with loans at preferential terms. The state would bear the interest rate differential. While this mechanism granted the SOEs quite stable access to financial resources, it also caused macroeconomic imbalances (Dobrinsky et al., Citation2016, p. 95; see also Korosteleva & Lawson, Citation2010). For the period between 1996 and 2002, multiple exchange rates existed, and then, in 2003, a currency peg to the dollar was introduced, which in 2014 could no longer be sustained. As early as from 2007/8 onwards, the Belarusian authorities had increasingly relied on active external borrowings to relieve the pressure on the currency market. The result was a sharp rise in external debts. The contradictions of the monetary policy measures led to three currency crises (in 2009, 2011 and 2014–2015) and Belarus had to accept IMF loans in 2009 and 2011, and a loan from the EurAsEc anti-crisis fund in 2011 to promote recovery. As they were conditional loans, Belarus had to adopt structural reforms regarding liberalisation, privatisation and macroeconomic stabilisation, but was reluctant to implement them (Bell & Bell, Citation2015, pp. 157–158; Dobrinsky et al., Citation2016, Executive Summary; Korosteleva & Lawson, Citation2010, pp. 37–41). Hence, the macroeconomic policy in Belarus generally benefitted manufacturing, but repeatedly reached the limits of stability in the past 10 years.

Wage relation

The centralised, authoritarian state structures in Belarus also allow for a strict control of the wage relation. The central means for this are SOEs, which are obliged to implement uniform tariff increases (Yarashevich, Citation2014b, p. 1711). Notably, the wage targets set by the government also influence the private sector, as it needs to offer competitive wages in order to attract skilled workers (Dobrinsky et al., Citation2016, p. 27). On the one hand, due to the wage and output targets, domestic demand has been stable (Bell & Bell, Citation2015, pp. 156–157). Thence, it has been stated that Lukashenka has established a ‘social contract’ with the population, prioritising the interests of non-entrepreneurial groups (Yarashevich, Citation2014b, p. 1717). Bonatti and Haiduk (Citation2014, p. 7) term it the ‘exchange of political loyalty for guaranteed employment and periodic increases in real incomes and wages.’ Currently, it is exactly the trade of industrial goods and the cooperation in manufacturing in the EAEU (particularly with Russia) that allows Belarus to preserve the labour-intensive industries that are vital for the continuity of the social contract, as restructuring would cause a steep rise in unemployment (Yarashevich, Citation2014a, p. 38).

Ecological restriction

Currently, the Belarusian economy is quite resource-intensive, which the Belarusian industrial policy aims to reduce for economic and ecological reasons (UNIDO, Citation2017, pp. 167–168). As Belarus is a resource-poor country, many of the inputs for its huge manufacturing sector need to be imported (Yarashevich, Citation2014a, p. 36). However, the most important feature is the reliance on Russian oil and gas at preferential prices (Dobrinsky et al., Citation2016, p. 10). The refining and re-exporting of Russian oil allows for the cross-financing of the rather ineffective industrial sector and the share of those fuel exports is quite impressive: in 2017, they made up about a quarter of total merchandise exports (Yarashevich, Citation2019, p. 432). Thus, the Russian ‘energy subsidies’ are crucial for maintaining the current Belarusian economic structure. However, during the past years, particularly since the end of the commodity boom in 2014, the conditions of the energy supplies have become increasingly contested between Russia and Belarus. This is why the Belarusian authorities adjudge a common market for oil and gas to be a prerequisite for the creation of a common electric power market (all envisioned for 2025) and joint industrial policy (Volnistaya, Citation2018).

4.3 The opportunities and challenges of industrial cooperation for Armenia and Belarus

Looking at the industrial cooperation initiative from an Armenian and Belarusian perspective, the results are quite moderate. Comparing the 19 priority sectors to the current industrial production and export structure of Armenia (see , and above), it is obvious that the priority sectors were not tailored to Armenia’s needs (unsurprisingly, as they were mostly set in 2013; Sidorsky, Citation2013, p. 26). As a concrete cooperation partner, Armenia is only mentioned once in all sectoral proposals, namely, in the chapter on aircraft engineering, where Russia considers drawing on Armenian enterprises for the production of avionic elements (EEC, Citation2018, p. 64). Furthermore, Armenia is involved in the creation of seven to eight ETPs (Interview 3, 2018, para. 9). Belarus is involved with several enterprises in the recently-launched space project. Moreover, Belarusian enterprises are also under consideration for the supply of Russian aircraft companies with avionic components (EEC, Citation2018, pp. 62–64). Another project in which Belarus has taken part is the international cooperation with VDMA and John Deere in the field of agricultural engineering (Interview 6, 2018, para. 17). Nevertheless, although the results are still moderate, industrial cooperation can open opportunities for both countries.

Armenia’s options are predominantly related to knowledge-driven activities. As pointed out above, Armenia has a strong tradition in science and research. Thus, the ETPs could become a way to become part of a regional innovation network and to regain the country’s former position as a science hub. In this role, Armenia could aim at creating ‘a vibrant innovation process based on imitation and the introduction of new-to-the market products and technologies’ (UNECE, Citation2014, p. 7), targeting the CIS/EAEU market. However, there is a long way to go, as currently the industry-science linkages are weak (UNECE, Citation2014) and many of the old relations were cut. In this context, Interviewee 7 (2018, para. 48) pointed to the need to revive them: ‘ [I]n order to make more active these ties in research and education (…), they need to be developed, so that our students, the researchers trust each other, the way that they say: “Hey, they are better than I am, so I’ll go and study over there”. But in this case, we don’t have the perception that they know something that we don’t know.’ Against this background, seasonal labour migration can open up interesting opportunities. In the best-case scenario this could lead to knowledge transfer and ‘brain circulation’ instead of ‘brain drain’ (Hartwell, Citation2016, p. 64). For instance, Interviewee 2 (2018, para. 20) reported that

we are just starting a project with Belarus to send them around 300 people to work in the construction sector in one of the companies being very strong in construction. And they need welders, bricklayers, cement mixers, etc. (…) When you have an agreement and you are sure that your labour force can be exported to work and they will also have social protection programmes in these countries, it is very important. Because we see that after these projects, they will come back with new knowledge, with new skills, having them developed in those countries. So, it is important.

Another opportunity for Armenia is the possible localisation of EAEU enterprises in its territory and/or the integration of suppliers into EAEU (Russian) value chains. This would be particularly helpful to counter high unemployment. For the first scenario, the signature of the Free Trade Agreement between the EAEU and Iran might compensate somewhat for the lack of borders between Armenia and the other member states. As Interviewee 2 (2018, para. 4) pointed out, Armenia could not only turn into a relevant trade corridor, but other EAEU countries might also establish their assembly plants in Armenia in order to export to Iran. Industrial cooperation in the EAEU could strategically exploit this potential. The other opportunity lies in the targeted integration of Armenian SMEs of the skills-based and knowledge-based sectors into regional value chains. However, to achieve this objective the formation of clusters would be helpful, ‘because SMEs in developing countries are typically too small in size and limited in resources to compete in global industries.’ (Gereffi & Lee, Citation2016, p. 27). Usually, SMEs in countries like Armenia do not have the scale or scope to climb to the upper rungs of a GVC, but they can still improve their efficiency and the working conditions of their employees (Gereffi & Lee, Citation2016, pp. 27–28). However, such a strategy would need a long-term strategic approach to industrial policy, which would require a shift in priorities in Armenian politics and society.

For Belarus, the projected industrial cooperation is of greater significance, and a far more strategic endeavour. The reason is first and foremost the existence of close ties between the Belarusian and Russian economies, which materialise in cross-border value chains and intensive trade relations. The Russian market is of particular relevance when it comes to industrial exports, which are mostly not competitive on the world market. Therefore, some experts have stated that the relationship with Russia has hampered the modernisation and restructuring of Belarusian industry (Interview 5, 2018, para. 8; Interview 8, 2018, para. 16). While this is a legitimate objection, and certainly true under the current circumstances, it is not carved into stone: ‘[I]f Russia gets serious about modernisation through industrialisation (…), Belarusian manufacturers, with their easy market access and great deal of experience, could gain significant benefits, either through increased exports of machinery and equipment, or through closer industrial cooperation’ (Yarashevich, Citation2014a, p. 38). The reason for this is that Belarus has a very diversified manufacturing sector, but relies on exporting a great share of its industrial goods due to the small size of the domestic market. For example, Belarus is strong in sectors such as agricultural engineering as well as transportation and lifting equipment, and has started developing electric cars (all sectors of the EAEU’s industrial cooperation). Furthermore, the successful evolution of the industrial cooperation initiative would also increase the intra-industry trade in manufacturing branches of the EAEU (Dudin et al., Citation2016, p. 643). A stronger integration into EAEU (Russian) value chains would allow Belarus to upscale the production of intermediate goods. Conversely, Russian suppliers might become part of Belarusian VCs. For instance, the EEC has identified 37 cooperative projects that are feasible in the sectors of ferrous and non-ferrous metallurgy, which could strengthen cross-border VCs (EEC, Citation2018, p. 58). Finally, the involvement of other countries in the industrial cooperation initiative softens the very asymmetric relation Belarus has with Russia in the framework of the Union State, which is a bilateral cooperation project between Russia and Belarus that started in 1996 and has evolved through several stages since then.

However, while opportunities do exist, also challenges arise that relate to differing national accumulation patterns and the resulting development strategies. Armenia (and Kyrgyzstan) are characterised by import-driven passive extraversion, supported by a regime of macroeconomic regulation detrimental to industrial development. Belarus features strong productive accumulation with an intraverted development strategy for the overall economy, but with active extraversion regarding the manufacturing sector. Russia and Kazakhstan, in contrast, follow a resource-based accumulation model in which the development of manufacturing is subordinated to other strategic interests related to commodity extraction and exports (Becker, Citation2018). Since the financial and economic crisis of 2008/9, the struggle for controlling the raw material rent in the Russian elite has intensified (Yakovlev, Citation2014), a tendency that the end of the commodity boom in 2014 further spurred. Hence, while debates on the Russian development model and the potential of industrial policy returned to the political and academic discourse in Russia (Chasovsky & Katrovsky, Citation2015; Jaitner, Citation2015; Simachev et al., Citation2014, Citation2018), the idea of whether to resort to industrial policy or not is still ‘heavily disputed’ (Interview 9, 2018, para. 8). Thus, while Russia (and Kazakhstan) could theoretically draw on a (currently squeezed) raw material rent in order to finance industrial endeavours, the social relations of forces currently obstruct this from happening in a consistent way.

The reluctance of Russia to mobilise palpable resources for the development of the EAEU (Molchanov, Citation2016) also affects the sphere of industrial cooperation. The so-called cooperative projects can apply for funding at the Eurasian development bank (EDB). However, the bank’s investment portfolio is rather limited (Interview 1, 2017, para. 32), amounting to 4.1 billion US dollar as of 1 April 2020. Thus, Russia’s dominant position in the EAEU would require that it pays a relevant share of the costs of productive integration (Interview 6, 2018, para. 36), directly and indirectly through the EDB (to which it contributes the biggest share of the budget). However, it currently does not seem that the different factions of the Russian elite can agree to bear the costs of integration (Jaitner, Citation2015). In this context, it becomes obvious that industrial policy implementation presupposes a (relatively stable) coalition of different actors, because it is always a question of distribution, namely of how much of the (scarce) public resources should be invested in the manufacturing sector (Andreoni & Chang, Citation2016b). And, after all, the moderate willingness to invest in industrial policy stands in stark contrast to the very broad industrial cooperation agenda, encompassing 19 priority sectors and 16 ETPs. It is evident that so many sectors were included in order to avoid conflict over the selection of targeted sectors. However, while mitigating disputes in the beginning, this further weakens the prospects of successful implementation.

Another challenge relates to the fact that – while most of EAEU countries are under authoritarian rule – the national leaders argue the case for different forms of regulation in the regional integration project. This problem becomes particularly obvious with respect to the conflicting ideas about the industrial cooperation of Russia and Belarus. For Belarus, an important element of common industrial policy would be to coordinate the production volumes of a specific good, as explained by Interviewee 1 (2017, para. 10):

[T]hey [Belarus] would perhaps be most interested in a coordinated or synchronised industrial policy with Russia in order to avoid overproduction, (…). In their understanding, synchronising industrial policy equals being in agreement on the volumes of production, sharing production, so to say. ‘Russia should produce 10,000 and we will produce 12,000 tractors. Okay? Okay!’.

This conception of industrial policy is a legacy of Soviet times that makes sense from the perspective of Belarus, which has still extensive planning elements in the economy.

In some cases, Russia and Belarus even managed to agree on the horizontal integration of plants producing the same product, for example, trucks. However, problems appeared when the Russian and Belarusian representatives disagreed on how to handle horizontal specialisation, that is, reducing the product variety in the affiliated plants (in order to maximise the opportunities of large-scale production) and compensating for it through complementary intra-industry trade. For example, in the framework of the Union State it was planned to integrate two truck-producing plants, Belarusian MAZ and Russian KAMAZ, into a common holding in order to conquer Asian markets. However, as the Russian business side planned to rationalise the production in Belarus by scaling down plants and the connected social infrastructure, the Belarusian authorities cancelled the deal. ‘And, after that the political reaction of our president was to throw out those businessmen and there was not established any holding between KAMAZ and MAZ. Because the Russian business wanted to close practically the whole enterprise of MAZ in Minsk; from 20,000 of workers they wanted to keep only 5,000 ’ (Interview 4, 2018, para. 30). The already-mentioned social contract prevailing in Belarus entails that the authorities aspire to maintain the level of unemployment as low as possible. Therefore, they seek to avoid drastic measures of restructuring, because it would threaten social stability and weaken their political base. However, this brings about a trade-off with the rationalisation of production that efficient industrial cooperation on the regional scale arguably would require (Gordon, Citation1961, p. 145).

Russia’s commitment to industrial cooperation is fundamental for the success of the joint project, due to its economic weight in the EAEU. Obviously, the other member countries need to engage, too, but it is the largest and technologically most advanced country and has to pull the others with it (if the chosen reindustrialisation and modernisation strategy targets the region). ‘Russia is the one who has to try to develop and try to become at least the technological leader of the region. In this case only, we have the chance to develop [jointly]’ (Interview 7, 2018, para. 32). In order to make this scenario beneficial for the other EAEU members, inter alia, the number of cross-border supply chains would need to increase. However, this can only work if the persisting non-tariff trade barriers in the Eurasian common market are drastically reduced (Vakulchuk & Knobel, Citation2018) and if Russia’s import substitution strategy becomes more inclusive towards regional partners (Volnistaya, Citation2018).

Russia’s (selective) promotion of import substitution policies following the Western sanctions had ambiguous effects for the smaller EAEU countries. On the one hand, it stimulated them to develop new industries and products. For example, Armenia set up mozzarella production to substitute the unavailable Italian cheese on the Russian market. ‘[W]e started to do that, because this was a market where we could export our goods to. This way it did stimulate the production process in Armenia. And, right now, the Armenian mozzarella became even very famous inside Armenia’ (Interview 7, 2018, para. 20). For Belarus, on the other hand, the results were less positive, which is due to the fact that Russia’s import substitution programme targets sectors in which Belarus has been a major exporter to the Russian market, e.g., machine building, agricultural machinery, food processing, woodworking etc. (Interview 5, 2018, para. 12). In the past years, Russia has repeatedly used non-tariff trade barriers, for example, licences or phytosanitary standards, against other EAEU members, although the common market should allow for the free movement of goods. For instance, Belarusian dairy products would suddenly not comply with the phytosanitary standards of the Russian market anymore, when Russia decided to develop a proper dairy industry (Interview 4, 2018, para. 32–36). Another example is that Belarusian companies from one day to the next were not certified as suppliers for Russian firms anymore. ‘This is why no foreign investor thinks that localisation is fair and in case of doubt you prefer to do it in Russia’ (Interview 5, 2018, para. 14). Hence, import substitution policies can aggravate the problem of non-tariff trade barriers and, thus, hamper the industrial development of the smaller states. Therefore, the EEC worked on a solution to let enterprises from the other EAEU countries benefit from the Russian strategy, too (Interview 6, 2018, para. 19). Future research will have to verify whether this has worked out.

5. Conclusion

Regional economic integration can take the form of regionalisation, which is a bottom-up process increasing the ties among formal and informal actors in a specific territory (not bound to the nation state), while regionalism is a state-led top-down initiative to integrate the region (e.g., the EAEU). From the perspective of Regulation Theory, an example of the first is the (partial) expansion of capital accumulation to the region, while regionalism constitutes the member states’ joint attempt to formally regulate those processes. An aspect of such regulation concerning primarily the field of competition is common industrial policy or industrial cooperation, as the EAEU calls it. In 2015, the EAEU launched its industrial cooperation initiative, which has four main components: the promotion of 19 priority sectors, the development of Eurasian Technology Platforms, system-wide measures – such as cooperative or interstate projects, the creation of a Eurasian Engineering Centre and of a Eurasian Network for Industrial Cooperation, Subcontracting and Technology Transfer – and international cooperation projects. While the preparatory works for implementing those projects and institutions have advanced, the results are still very moderate. Thus, we are currently not witnessing a transition of the EAEU towards developmental regionalism.

In a sense, the elements of industrial cooperation are the expansion of Russian national industrial policy instruments to the regional scale (e.g., priority sectors and technology platforms). In theory, this industrial cooperation could be beneficial for Armenia and Belarus, if the cooperation in R&D, the increased attraction of FDI in manufacturing, and the possibility to enter GVCs as a country or as a group (see international cooperation) works out. For Armenia, the focus on technology, R&D and innovation activities could be helpful in order to regain its position as science hub of the region and to connect labour migration with ‘brain circulation’. Furthermore, the opportunity to further integrate local firms into Russian-headed GVCs exists, as well as the possibility of localisation of enterprises of other EAEU countries in Armenia in order to export to the Middle East, e.g., Iran. Belarus could benefit from coordinated horizontal specialisation in manufacturing, considering that the industrial structures in the territory of the EAEU duplicate each other to some extent, which is not always efficient. The strategic geographic position of Belarus could convert it into the ‘window to Europe’ of the EAEU, which might incentivise the integration of (West-)Russian firms into Belarus-headed GVCs and might promote the localisation of enterprises of other EAEU countries in Belarus.

However, there are several major challenges associated with industrial cooperation. First, the success of implementation depends on the political will of Russia, because the huge asymmetries in the bloc require that Russia finances a relevant share of the industrial cooperation projects. Second, despite numerous proclamations that Russia would include the smaller countries into its import substitution strategy, the prevailing non-tariff trade barriers (NTBs) against EAEU competitors remain high (Vakulchuk & Knobel, Citation2018). These are especially harmful for competitive enterprises (e.g., the Belarusian dairy industry) from the small countries. Thus, for economic actors from the small states, a focus on conquering niche markets that Russian enterprises do not dominate might be recommendable. At the same time, the removal of the NTBs needs to be accelerated, as they constitute a huge barrier to successful vertical and horizontal specialisation in the bloc, and thus restrict the industrial development prospects of the small states. This issue cannot solely be resolved through the improvement of the EAEU’s competition policy framework, as it is also a reflection of the existing power asymmetries. In any case, for the small states an exclusive concentration on deepening their integration within the EAEU entails the risk of increasing their dependence on Russia. Therefore, they should simultaneously promote ties with other countries and regions.

For Armenian policymakers, it might be worth studying in detail the catch-up experience of countries such as Korea, particularly when it comes to building up local production capacities through GVC involvement (Lee et al., Citation2018), and successfully promoting economic and social upgrading (Gereffi & Lee, Citation2016). Particularly with respect to technological learning, firms from EU countries, China and Korea could become relevant partners. GVCs headed by firms based outside of Eurasia can play an important role, if political leaders have a long-term strategy that seeks to transit ‘from participation in the GVC to creation of local value chains and innovation systems’ (Lee et al., Citation2018, p. 437). The participation in extra-regional GVCs does not necessarily conflict with (potential) regional industrial cooperation, but it would decrease Armenia’s dependence on Russia in the industrial realm.

While in Armenia the social coalition supporting industrial policymaking is very weak, and industrial cooperation was not one of the major interests for joining the EAEU (Eder, Citation2017), for Belarus industrial development is a key concern. Due to the active extraversion of the manufacturing sector (export reliance) and the social contract between the Belarusian leadership and society, Lukashenka needs to proceed carefully with the modernisation of the industrial sector (Bonatti & Haiduk, Citation2014, p. 7). Thus, a sudden opening to the West, including the (subordinated) insertion into EU value chains, is currently not an option. Therefore, it could be argued that the EAEU indirectly stabilises authoritarian rule in Belarus (Libman & Obydenkova, Citation2018a, p. 1058). However, regarding the question of industrial cooperation, it is more important that the Russian and Belarusian modes of regulation significantly diverge. The Belarusian authorities see the EAEU as a chance to maintain the current accumulation strategy while pursuing a ‘soft’ strategy of modernisation. This limits the social costs of rationalisation to the minimum, but makes horizontal specialisation less efficient. Russia, by contrast, has shown fewer concerns for the social effects of restructuring. This has already led to big disagreements; for instance, Belarus cancelled the envisioned cooperation between MAZ and KAMAZ. Hence, considering the differing national modes of regulation and the conflicting policy visions in the regional bloc, the small countries should not ultimately rely on regional industrial cooperation, but instead develop sound national industrial strategies that regional policies can complement (in the event that they materialise).

Regulation Theory has proven to be an adequate approach with which to analyse the opportunities of and obstacles to common industrial policy in the EAEU. The identification of the specific national forms of accumulation and the corresponding forms of regulation allows for the determination of the prevailing interests and options related to industrial policy on the regional level. For different reasons, the interest in industrial cooperation on the regional level is moderate in Russia, Kazakhstan, Armenia and Kyrgyzstan. While the former two follow resource-based accumulation strategies and the interest groups of the extractivist sector are the most powerful, in the latter two countries the import-driven accumulation patterns and the dominance of trading capital are detrimental to industrial development. The most broadly-shared interest in industrial cooperation has Belarus, because the Belarusian economy has a productive orientation with a strong manufacturing sector. However, the Belarusian authorities envision a different kind of industrial cooperation than other EAEU countries (namely, more in the tradition of Soviet planning). Thus, while accumulation and regulation have partially expanded to the region, those factors have so far inhibited the emergence of a common regional development strategy. In view of the diverging (and sometimes conflicting) interests, it is unlikely that this will happen anytime soon.

Acknowledgments

The author thanks the special issue editors, the two anonymous reviewers, as well as Brigitte Aulenbacher, Joachim Becker and Michael Windisch for valuable comments on earlier drafts.

This work was kindly supported under the Marietta Blau Grant, funded by the Austrian Ministry of Education, Research and Science (BMBWF) and administered by the Austrian Agency for International Mobility and Cooperation in Education, Science and Research (OeAD), as well as by the Land Oberösterreich under the Programm des Landes Oberösterreich zur Förderung von “Forschung, Lehre und Internationalisierung”.

Disclosure statement

No potential conflict of interest was reported by the author.

Notes

1. The Eurasian Economic Community existed between 2000 and 2014. It consisted of Belarus, Kazakhstan, Kyrgyzstan, Russia and Tajikistan. On January 1 2015, it was merged into the Eurasian Economic Union (EAEU).

2. Industrial policy is a form of state intervention in the economy. For the purpose of the paper, the narrow definition of industrial policy fits best, namely encompassing policies that aim at promoting structural change in the manufacturing sector. They can be either horizontal or vertical (although in practice, combinations frequently appear). Horizontal industrial policies aim at providing framework conditions, which allow industries to become or remain competitive, e.g., subsidies for research and development. Vertical or selective industrial policy, on the contrary, tackles specific sectors, enterprises and/or value chains. It can either be strategic, e.g., supporting the most competitive enterprises of a branch (‘picking winners’) or defensive (reacting to a changing economic environment) (Warwick, Citation2013).

3. The EAEU has developed in competition with the EU’s ‘Eastern Partnership’ (EaP), which had nearly won over Armenia, when it suddenly withdrew from signing the already-negotiated Association Agreement with the EU in 2013 and opted for the affiliation to the EAEU instead (Eder, Citation2017, p. 46). However, in November 2017 Armenia signed the ‘Comprehensive and Enhanced Partnership Agreement’ (CEPA) with the EU (Vieira & Vasilyan, Citation2018, p. 472), which can be interpreted as a ‘light version’ of the originally envisioned DCFTA.

4. An interviewee requested to cite this information without any reference to him/her.

References

- Aglietta, M. (2015). A theory of capitalist regulation: The US experience. Verso.

- Andreoni, A., & Chang, H. ‑. J. (2016a). Bringing production and employment back into development: Alice Amsden’s legacy for a new developmentalist Agenda. SOAS eprints. https://eprints.soas.ac.uk/23186/1/Andreoni_23186.pdf

- Andreoni, A., & Chang, H. ‑. J. (2016b). Industrial policy and the future of manufacturing. Economia E Politica Industriale, 43(4), 491–502. https://doi.org/10.1007/s40812-016-0057-2

- Balassa, B. (1973/1961). The theory of economic integration (3rd ed.). George Allen & Unwin Ltd.

- Becker, J. (2006). Metamorphosen der regionalen Integration. Austrian Journal of Development Studies, 22(2), 11–44. https://doi.org/10.20446/JEP-2414-3197-22-2-11

- Becker, J. (2009). Regulationstheorie. In J. Becker, A. Grisold, G. Mikl-Horke, R. Pirker, & H. Rauchenschwandtner (Eds.), Heterodoxe Ökonomie (pp. 89–117). Metropolis.

- Becker, J. (2013). Regulationstheorie: Ursprünge und Entwicklungstendenzen. In R. Atzmüller, J. Becker, U. Brand, L. Oberndorfer, V. Redak, & T. Sablowski (Eds.), Fit für die Krise?: Perspektiven der Regulationstheorie (pp. 24–56). Westfälisches Dampfboot.