Abstract

Drawing on the sociology of expectations and sociology of conventions, this paper explores issues of worth and value in the bioeconomy, and the promissory character of contemporary capitalism. Arguing that the literature on biocapital has paid insufficient attention to geographical differentiation in capital accumulation strategies, this paper situates the consumer genomics firm 23andme in the entrepreneurial culture of Silicon Valley. The paper suggests that in Silicon Valley the relationship between moral worth and economic value is mediated through the concept of disruptive innovation, which functions as both ideological construct and a set of commercial practices utilized by the founders of start-up firms and the venture capitalists who invest in them. Analyzing 23andme’s status as a “unicorn” firm, the paper describes how the recent increase in private investment capital in Silicon Valley has led to a new model of business development for start-ups and considers its implications for corporate governance.

Introduction

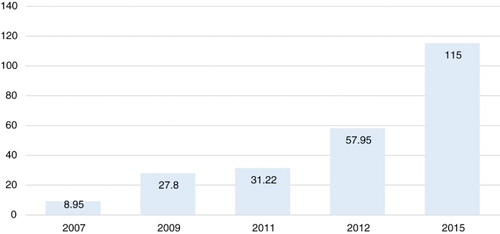

In 2007, the Silicon Valley consumer genomics firm 23andme launched with a bold mission to revolutionize healthcare and biomedical research. From the outset the firm’s ambitions were global in scale: co-founder Anne Wojcicki declared that 23andme aimed to become “the world’s trusted source of personal genetic information” (23andme Citation2008). These grand ambitions were underpinned by investment funding from leading players in Silicon Valley, each of them global leaders in their respective sectors: the venture capital (VC) firm New Enterprise Associates, the biopharmaceutical firm Genentech, and the Internet search firm Google. Like other start-up firms (including its rivals in the nascent consumer genomics market), 23andme was heavily dependent on continued injections of private capital as it sought to build a market for its products and services, and measured by the amount of private capital the firm has raised, 23andme has been highly successful. It raised $240M in a series of five financing rounds between 2007 and 2015 (see ), and by 2015 had achieved “unicorn” status, a term used to describe privately held firms valued at over $1 Billion. To put this achievement in perspective, of the 22 diagnostics firms listed on the NASDAQ only two raised more than $100M when they floated as public companies, that is, 23andme has raised more money in the private capital markets than its counterparts have been able to raise by going public.

Figure 1. 23andme funding rounds 2007-15. Total raised $240.92M. Data source: CrunchBase.

This financial success was achieved despite longstanding uncertainty about the firm’s commercial viability, public controversy about the ethics of consumer genomics, professional critique of the scientific validity of genetic risk scores offered by the firm and its rivals (Mihaescu et al. Citation2009), and then regulatory censure by the US Government. The US Food and Drug Administration (FDA) closed down the health-related aspects of 23andme’s business in 2013 (see Curnutte Citation2017). Two years later, when the FDA took regulatory action against Theranos, another high-profile Silicon Valley diagnostics firm, some media commentators suggested that the regulatory problems encountered by the two firms exemplified a broader crisis in the corporate culture of Silicon Valley. These critics pointed to failures in corporate governance, media complicity in promotional hype and a lack of due diligence on the part of investors, all fueling a dangerous new investment bubble underpinned by the ideology of disruptive innovation (McDermid Citation2016).

How to explain 23andme’s success in attracting financial investment despite the seemingly toxic combination of commercial underperformance and regulatory scandal? Given the importance of personal networks in securing VC finance, it was helpful that 23andme was, from the outset, enmeshed in the Silicon Valley establishment, most notably through co-founder (and current CEO) Anne Wojcicki’s marriage to Sergey Brin, the co-founder of Google. Google invested $3.9M in Series A and then $2.6M in Series B, but in addition Brin provided a start-up loan of $2.6M ahead of the Series A round, and a further $10M ahead of the Series B financing round (Rao Citation2009). However, the power of personal networks is not the focus of this paper, which is concerned instead with issues of worth and value in the bioeconomy, and what Paul Martin (Citation2015) has called “the promissory character of contemporary capitalism”. This paper suggests that in Silicon Valley the relationship between moral worth and economic value is mediated through the concept of disruptive innovation, which functions as both ideological construct and a set of commercial practices utilized by the founders of start-up firms and the venture capitalists who invest in them.

In addressing matters of political economy, this paper takes an approach hitherto neglected in the literature on consumer genomics, a puzzling oversight given that in recent years a growing body of scholarly work has argued that the emergence of commercial biotechnology has generated a new form of capitalism: biocapitalism (for an overview of this literature, see Helmreich Citation2008). Attempts to characterize a distinct form of biocapital are consistent with a long tradition of middle-range theory in political economy that addresses the “specific forms and mediations of capitalist processes, such as the nature of institutions, or new forms of organization such as post-Fordism” (Sayer Citation1995, 10). This paper offers two original contributions to the scholarship on biocapital. Firstly, by suggesting that as an attempt to understand sectoral differentiation, this literature has been too ready to generalize using data on the biotech therapeutics sector and has failed to understand the distinctive dynamics of the diagnostics sector. However, its more substantive contribution is to argue for a greater focus on geographical rather than sectoral differentiation (Sheppard Citation2013). I locate 23andme in its geographical setting of Silicon Valley, identifying the ways in which firm might be characterized as typical of the distinctive local culture of entrepreneurialism that has developed in the area since the 1980s.

I begin by situating this paper’s conceptual framework in the broader social science literature about the bioeconomy. By way of descriptive context, I then outline the role of VC in the financing of high-technology start-ups, the growth of Silicon Valley as a geographic cluster for high-tech firms and the key features of Silicon Valley disruption. I then move on to describe how 23andme modeled itself as a disruptive firm and to discuss how that strategy may have helped attract investment funding.

Conceptual framework

In addressing VC’s role in consumer genomics, this paper is a contribution to a small body of work in critical political economy that has explored the relationship between financialization and the biotechnology sector. The bioeconomy has been described as a Ponzi scheme (Mirowski Citation2011), a boondoggle (Lazonick and Tulum Citation2011), and a sector “underpinned by a rentier regime in which financial asset values are more important than revenues from the sale of biotechnology commodities” (Birch and Tyfield Citation2013). These papers share a common interest in understanding biotechnology as just one example of an industrial sector where financialization is reshaping capitalist accumulation strategies. However, Birch and Tyfield went further by offering a critique of scholarship that has sought to characterize biocapital as a distinct new form of capitalism. Offering critical support to Birch and Tyfield’s argument, Paul Martin (Citation2015) has sought to extend his work on the sociology of expectations by exploring how “the promissory is transformed into the real and the role of VCs, market analysts and public exchanges in this process” (440).

Martin draws on the argument advanced by Moreira and Palladino (Citation2005) that in contemporary biomedicine the subjectivity of the patient is “shaped by two, seemingly incommensurable, organizational logics, the ‘regime of truth’ and ‘the regime of hope’” (55). Martin adopts this dual regime framework but shifts the unit of analysis from the self to the firm. Drawing on his survey of the emergent neurotech sector, he describes how start-up firms transition from a regime of hope to a regime of truth. Martin distinguishes between start-up firms “who have no products on the market or in late stage development, and are poorly integrated into the pharmaceutical industry.” Such firms belong to the “‘regime of hope’ … a speculative market based on promissory assets that cannot be traded in any established market” (434). Martin contrasts this group with a second set of firms which have “products on the market, significant sales and profits, a relatively large number of products in late stage development and who are well-integrated into the pharmaceutical industry” (437.) These firms belong to a “‘regime of truth’ … belonging to a real economy with tangible assets that are traded in established financial and technology markets” (437). Start-up firms begin in the regime of hope, and then, in the course of developing and bringing to market a portfolio of products, they move into the regime of truth. Although firms transition from the regime of hope to the regime of truth, the two regimes are “linked and entangled” and some firms “occupy intermediary positions between them” (437). In this paper, I suggest that unicorn firms like 23andme are located in this liminal space straddling the regimes of hope and truth, and that the growing number of unicorns signals an expansion in the capacity of this liminal space.

By focusing on the political economy of biotech commercialization and the dynamics of firm development, Martin expands the institutional complexity of the regime of truth. Moreira and Palladino focused on the evaluation of clinical trial data by regulatory agencies and Health Technology Assessment bodies but Martin’s truth regime encompasses a variety of other actors, domains and evaluative mechanisms such as the consumer market and the financial markets that trade shares in public firms. Flotation as a public company through an initial Public Offering (IPO) is a critical entry point into a regime of truth in which information about the firm’s financial performance, revenue streams, profits and share price become public knowledge and subject to critical scrutiny by market analysts.

This paper seeks to build on Martin’s account by addressing some potential weaknesses in his conceptual framework. Firstly, the dichotomy between regimes of hope and truth rests on a characterization of public stock markets as governed by the rational calculation of value, thus ignoring the vulnerability of institutional investors to the irrational exuberance of technology bubbles. Similarly, its characterization of the valuation process used by angel and venture investors is limited to describing “various options-based valuation models and judgements about the quality of management” (438). This is inconsistent with Martin’s characterization of these investors as part of the regime of hope because it downplays the extent to which a range of non-financial values help to establish the worth of a firm at this early stage in its development.

To understand the values and valuation processes that underpin the practice of disruptive innovation, I draw on David Stark’s (Citation2009) work on innovation and entrepreneurship, in which he explores the “evaluative principles” that determine how worth/value is established in the contemporary economy and in particular, how moral judgments and rational calculations of economic value are interpenetrated. His concept of evaluative principles is an elaboration of the sociology of conventions framework developed by Boltanski and Thévenot (Citation1991) that describes how multiple “orders of worth” operate within a single social domain. Stark defines entrepreneurship as “the ability to keep multiple evaluative principles in play and to exploit the resulting friction of their interplay” (6).

A second problem with Martin’s framework is that its model of how firm growth, product development, and financial investment are interlinked is based on the biopharmaceutical sector, and pays no attention to the diagnostics sector. The development of novel therapeutics proceeds along a well-defined sequential pathway of pre-clinical and clinical phases of development and, as Martin explains, progress through these stages provides crucial signals to investors that may trigger new funding rounds, public flotation or even firm acquisition. However, diagnostics firms face lower regulatory hurdles and have products on the market far faster than therapeutics firms, and their product development process has no equivalent formal regulatory definition of pre-clinical/clinical development stages. This has implications for the transition from the regime of hope to the regime of truth – diagnostics firms generally float on a public stock market at a point when they are already selling products, whereas for therapeutics firms it is sufficient to have moved a candidate drug through the first stages of clinical development.

Martin’s focus on therapeutic rather than diagnostic innovation is replicated in the broader literature on biotech finance referenced earlier. By redressing this imbalance, this paper offers new insights into the political economy of biomedical innovation. Moreover, by characterizing 23andme as a Silicon Valley start-up, the paper will offer a different approach to understanding the bioeconomy, by locating firms in geographical, as well as sectoral context. Such an approach draws on a rich tradition of scholarship in political economy that seeks to understand how capitalism is socially embedded as a moral economy, and to delineate the variety of forms that capitalism in different locales, “distinguished partly according to their cultural legacies and forms of embedding” (Sayer Citation2004).

The regime of VC

A critical dimension of 23andme’s embedding in Silicon Valley entrepreneurial culture is the firm’s relationship to VC investors. High-tech start-up firms require support from investors as they move from R&D to commercialization of products. Investment proceeds through a series of stages with initial investments from family, friends or angel investors and subsequent funding generally coming from VC firms or through commercial alliances with larger firms (the latter is a common pattern in the biopharmaceutical sector). Inadequate finance is a common cause of firm failure and US firms enjoy a competitive advantage as a consequence of the much larger domestic VC sector, for instance, US biopharmaceutical firms generally receive far larger VC investments than their European rivals (Hogarth and Salter Citation2010). Venture capitalists are active investors providing guidance to the firms they invest in, often taking a position on the board and exercising authority in key decisions such as the composition of the senior management team, bringing in new executives or removing some of the original start-up founders.

Venture capitalists hope for a return of investment (ROI) of between 500 and 1000% within five years, but they know that around one-third of investments will make no return at all, and a further third only a modest ROI. When investors evaluate a start-up firm, they need to assess three key areas: the science/technology, the business model and the management team. Weakness in any one of these areas could have a negative impact on the potential for a significant return on investment (Shapin Citation2008).

There are well-established financial techniques that investors can use as part of the due diligence process when evaluating a prospective firm’s business model, including some that are specific to the biotech sector (Keegan Citation2008), but a recent survey of VC firms (Gompers et al. Citation2016) found that almost half often make investment decisions based on gut instinct and that 17% of early-stage investors use no financial metrics. Such speculative valuation practices, reliant on tacit knowledge, hunches and the VC’s instinctive “feel for the game” are integral to VC operations in Silicon Valley (Shapin Citation2008), and the area is thus fertile ground for the growth of what Martin terms promissory capitalism.

Valley values and the corruption of disruption

Silicon Valley is the name given to the southern region of the San Francisco Bay Area that became the base for the US semiconductor industry in the early 1970s, and has subsequently established a global reputation as the spiritual home of high-tech entrepreneurship. It remains a major center for the US computer hardware industry, including giant multinational corporations like Apple, but its growth has been driven by diversification: the 1980s saw the emergence of leading biopharmaceutical firms such as Genentech, and in the 1990s dotcom boom, software firms like Google. Silicon Valley thus boasts a world-leading position in the two pillars of the contemporary knowledge-based economy: information technology and biotechnology.

Policy-makers across the globe who aspire to compete in the knowledge-based economy have looked to Silicon Valley as a model and have sought to emulate this innovation eco-system (Casper Citation2006). The organizational infrastructure that provides the region’s competitive advantage is multi-faceted, including generous state funding, leading higher education institutions, and a strong private capital market.

The Valley is home to a panoply of large VC firms like Mohr Davidow whose growth since the 1970s has been bound up with that of the high-tech firms they have supported with private capital and strategic guidance. Silicon Valley is the center of US VC – nearly 50% of all US VC investments are tied up in the area’s firms (Gupta and Wang Citation2016). However, traditional VC firms are no longer the only investors powering the growth of Silicon Valley start-ups: successful dotcom entrepreneurs like Elon Musk and Peter Thiel have put their money to work by diversifying into VC. Google Ventures (GVs) exemplify this trend. Established by the search engine firm in 2009, GV has $2 billion under management and in 2012 it increased its annual investment to $300M.

The massive growth in private capital has led to a new model of business development for high-tech start-ups in Silicon Valley. Traditionally, start-ups have used private finance as a staging post on the path to flotation as a public company, but a growing number of firms are now existing indefinitely supported by private finance. The most successful of these firms are so-called unicorns – firms that have yet to float as public companies but that are already valued at over $1Bn. Unicorns are a predominantly US phenomenon – 64% of them are US-based – and they are most commonly found in Silicon Valley – 39% of the world’s unicorns are located there (Tellis Citation2016).

Venture capitalists may also be operating with a different business model. A report on the unicorn phenomenon by SharesPost (Citation2016) describes how VC firms used to operate on the basis that one-third of firms would provide no ROI, another third would only return the initial investment and the remaining third would provide the real profit for the VCs. However, in the new model a small proportion, perhaps 2% of firms, will provide the bulk of the profit, the true “home runs”. Significantly for our interest in processes of valuation and worth, it is precisely in relation to these potential “home run” investments that established techniques for calculating the potential ROI are least useful.

Demand for a radically new innovation can only be perceived demand; market surveys and statistics of projected consumption are “images” or “visions” (or “forecasts”) of future sales, to be revised as real purchases do or do not take place.

In Silicon Valley, the promissory capitalism of start-up financing draws heavily on the rhetoric of disruption to signal a set of ideals and practices that resonate with the established Silicon Valley value system. As noted earlier, given Silicon Valley’s reliance on high-tech industry and financial speculation as drivers of economic growth, the area is exceptional in its exemplification of post-industrial capitalism, but the Valley has also been home to a distinctive brand of neoliberal ideology that celebrates the region’s culture of high-tech entrepreneurship. Two decades ago, Barbrook and Cameron (Citation1996) described the earliest manifestation of this belief system as the “Californian ideology”, a fusion of the counter-cultural radicalism of San Francisco with the high-tech entrepreneurship of Silicon Valley, that

… promiscuously combines the freewheeling spirit of the hippies and the entrepreneurial zeal of the yuppies. This amalgamation of opposites has been achieved through a profound faith in the emancipatory potential of the new information technologies. (45)

Hiding beneath this glossy veneer of disruption-talk is the same old gospel of individualism, small government, and market fundamentalism that we associate with Randian characters. For Silicon Valley and its idols, innovation is the new selfishness.

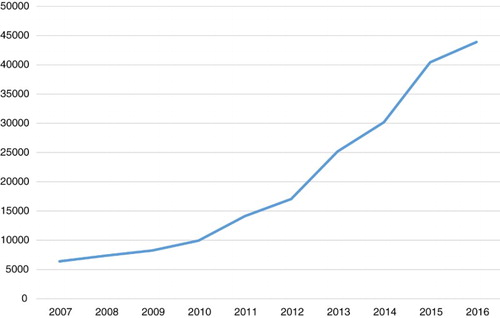

Figure 2. Media publications including both the words “disrupt*” and “innovation” 2007–2016. Source: FACTIVA, search 13/12/2016.

The insight that disruptive innovation is now a signifier that has floated free of its original conceptual mooring is a starting point for this paper. In defining the Silicon Valley approach to disruption, this paper suggests there are five key components:

A compelling vision of socially beneficial market transformation communicated by a passionate CEO;

A belief in the transformative power of information technology (especially the Internet);

Regulatory arbitrage as a form of competitive advantage frequently defended as a means to deliver consumer value by disrupting entrenched market incumbents;

The ambition for global growth and market dominance;

A willingness to rapidly adapt business models in response to changing conditions.

23andme – the business of disruption

Vision – making the world a better place.

In his discussions with Silicon Valley VCs, the historian Steven Shapin (Citation2008) was told that start-up founders need more than a desire for wealth, because avarice alone will not fortify against the inevitable setbacks that entrepreneurs experience: “The guy who wants to do it for money? He’s going to bail on you when the going gets tough … You need people who want to change the world” (295). Gompers et al.’ (Citation2016) survey of venture capitalists found that when they evaluate a start-up’s management team, VCs rate passion as an important quality, and that this attribute is especially favored by VCs in California.

The public pronouncements of 23andme’s CEO Anne Wojcicki’s establish her as exactly the kind of passionate, committed visionary that venture capitalists want to invest in. From the firm’s launch, the founders of 23andme presented themselves as disruptive agents of change seeking to challenge the biomedical establishment. Fast Company magazine named Anne Wojcicki “America’s Most Daring CEO.” In 2015, she described herself as “A rebel fighting the system” (Pollack Citation2015). The concept of disruption was routinely invoked to signal the scale of the firm’s ambitions. In 2012, a feature in Fortune magazine reported that “Wojcicki uses the word disrupt a lot; and she has some big audacious hopes for her company … ” (Benner Citation2012). In 2013, the firm was listed in the TV business news channel CNBC’s inaugural Disruptor 50 list, a roll-call of the top private, venture-backed companies, “disrupting the status quo in ten traditional industries.”

The founders of 23andme wanted to transform healthcare by refocusing it on the goal of disease prevention to radically extend life expectancy. As Wojcicki said in 2013: “My goal isn’t to just minimize the chance of getting sick. I want to live a healthy life at 100” (Brady Citation2013). For 23andme, this emphasis on preventive healthcare meant that genetic risk assessment was at the heart of its technoscientific vision.

The most important thing I want to know as a consumer is am I at risk of something? … Genetics is all about what you are at risk for, and the only way I can know how to prevent a disease is if I know what I am at risk for, and then I need to know what to do to try to prevent it … . (Wojcicki Citation2011)

… It made me frustrated that medicine didn’t focus more on prevention … decisions in our healthcare system are not being made in the best interests of the patient, but rather on optimising revenue. Bone-marrow transplants are profitable for doctors, for example, but checking someone out for melanoma doesn’t make them any money. (Wojcicki in Teeman Citation2012)

… you can’t just trust that somebody is going to do the right thing for you. If you want to have the best health outcome, you need to be in charge of your health … It’s your job to manage your health. (Wojcicki in Pollack Citation2014)

Digital disruption

Alongside a vision of market-based consumerization, the founders of 23andme promote the transformative power of the Internet as a mechanism for collection, curation and dissemination of big data (see Saukko Citation2017). This vision of digital disruption is part of the origin myth of 23andme, recounted in countless news reports, interviews, and personal profiles and briefly summarized by this account from the Washington Post:

As a young analyst on Wall Street, Wojcicki had been frustrated by how a country with such wealth could fail to provide even the most basic medical needs to its citizens. By 2006, she had the connections to do something about it.

Wojcicki had moved to California to be with her then-boyfriend Brin and grew convinced that Silicon Valley, with its wonky algorithms and expertise in big data, could help.

For Wojcicki and her peers, disease wasn’t an inevitable part of the human experience. It was more like a math problem. “I think this is something the Valley can solve for,” Wojcicki said. (Eunjung Cha Citation2014)

Regulatory arbitrage – Silicon Valley is from Mars, the FDA is from Venus

The idea of digital disruption is inextricably linked to the third characteristic of Silicon Valley disruption: regulatory arbitrage. Dotcom disruptors like AirBnB and Uber exploit the potential for regulatory arbitrage offered by the ambiguous novelty of their market function – is Uber a taxi firm or a software business? Disruption is thus often bound up with a critique of government regulation and a logic of regulatory incommensurability. Disruptor firms suggest that since the way they operate is radically different to the practices of market incumbents, then existing regulations may be inappropriate, and serve only to protect the market incumbents from the full brunt of unfettered market competition. Disruptor firms shift tactically from flouting the law to lobbying for legislative change depending on the logic of local circumstance:

Lessons from regulated industries show that disruptors can topple the incumbents in these industries by first innovating outside of the reach of regulators; as the up-starts accumulate a sufficient number of customers, regulators cave ex post facto to the new reality in reaction to the innovator’s success. (Horn Citation2016)

The potential for 23andme to exploit ambiguity about whether it was a software firm or a healthcare firm could have been attractive to investors hoping for an opportunity to work in the healthcare system without the added costs of regulatory compliance. A 2006 article in Business 2.0 (a magazine that aspired to be the trade journal of the New Economy) highlighted precisely this possibility in a feature that surveyed business opportunities in consumer healthcare such as the nascent consumer genomics sector. The article concluded with a list of recommendations for entrepeneurs, including the suggestion that they run their businesses on the Internet in order to avoid unnecessary regulatory complications:

Stay clear of services that require you to spend a lot of quality time with the FDA. So consider dropping that plan for a high-tech hospital and think instead about a service that delivers hospital-quality health information to consumers, such as WebMD’s. (Alsever et al. Citation2006)

“‘It’s simply your information,’ she insists. In part, this distinction is to make sure the company doesn’t run afoul of the Food and Drug Administration, which strictly regulates diagnostic testing for disease but has been slow to respond to the more transformational aspects of genomics. (Goetz Citation2007)

In the wake of the FDA’s 2013 shutdown of 23andme’s health reports, some pointed to the ideology of disruption as the source of a lax attitude to regulatory compliance. In October 2016, the cover story in the San Francisco Business Times was entitled “Why are so many start-ups behaving badly, and can anything be done about it?” The story cited both Theranos and 23andme as examples of biotech start-ups failing in regulatory compliance, and quoted one venture capitalist who suggested that the logic of disruption might be a contributory factor:

Some people may think that being a disruptor means you can break the law, but I don’t … In health care, where patient safety and security are paramount, it is a red flag when founders want to go at odds with the FDA. (Julia Papanek quoted in McDermid Citation2016)

The idea of a West Coast/East Coast culture clash between Silicon Valley and the FDA belies the obvious fact that there are many successful biotechnology firms in the Valley who have successfully navigated the FDA’s regulatory pathways. The argument only makes sense if Silicon Valley is being used as a synonym for the tech sector. As Wojcicki indicates, much of the perceived cultural clash is about the pace that software firms operate at. Consider this Wojcicki quotation from 2014, discussing the use of 23andme’s database as a research resource for academics and pharmaceutical firms:

We’re in the beta phase. It’s a challenging build because you want to answer a lot of questions and it’s a lot of data, and you also have to protect privacy. (Hof Citation2014)

This beta testing model was an important part of how 23andme responded to its critics – the firm’s approach was to suggest that they were engaged in a long-term, iterative process of developing their service through dialogue with users and experts.

As we continue to respond to feedback from customers and scholars in the scientific, medical, and ELSI communities, 23andMe becomes as much a reflection of its users and critics as of the people at 23andMe. (Hsu et al. Citation2009)

When you try new things, you will make mistakes … The best thing you can do is to understand how you quickly recover. (Hof Citation2014)

The FDA said it plans to regulate software companies as medical devices. If you get your genome done, you can ship it off to Canada or China or other places in the world and get an interpretation. So how do you regulate information? That’s one of the issues. I’m not sure you can hold it back. (Hof Citation2014)

Market dominance

As, the economist Ann Pettifor (Citation2015) has remarked, firms like AirBnB and Uber have “monopolistic aspirations”. The growth of such firms is driven by network effects that act as a barrier to market entry. Characterizing the rise of such dotcom disruptors as a new era of “platform capitalism”, Srnicek argues that “a tendency towards monopolization is built into the DNA of platforms” (Srnicek Citation2017). The generous VC funding offered to such firms is spurred by the hope of achieving the kind of monopoly or market dominance that has characterized the most successful dotcom firms like Google and Amazon. Peter Thiel, a leading Silicon Valley VC investor, is candid about the commercial allure of monopolies:

… capitalism and competition are opposites. Capitalism is premised on the accumulation of capital, but under perfect competition, all profits get competed away. The lesson for entrepreneurs is clear: If you want to create and capture lasting value, don’t build an undifferentiated commodity business. (Thiel Citation2014)

… to get a syndicate of investors willing to open their wallets to one particular company, it needs to demonstrate that it essentially has few, if any, competitors … companies today must present products with disruptive potential, rather than incremental improvements to existing technology, in order to get noticed. (Fong Citation2012)

There’s still a lot of redundancy in this industry because of competition. Part of my goal is to eliminate some of that commodity competition … Traditionally when you talk to people who have Parkinson’s or Alzheimer’s, they’ll talk about how they’re in five or six studies and they’ve been sequenced by each study. That’s just fat in the system. Just have a single data set that then you can share. You can make the entire system more efficient … We have so much information about humanity that we almost become the ultimate epidemiological company with genetic information that can be used for research. (Hof Citation2014)

Pivoting to profit?

This uncertainty about the firm’s business model brings us to the final of our five characteristics of disruptor firms: the willingness to rapidly adapt business models in the light of changing circumstances. 23andme has been forced to adapt in response to FDA intervention and because of longstanding doubts about its commercial viability. When 23andme launched, the journalist David Hamilton suggested the firm would not to be able to create a sustainable business from consumer sales alone because the margins were too thin (Hamilton Citation2007). A 2010 article by Andrew Pollack reported that market uptake was slow – 23andme had only 3500 customers and at least 25% of those had received the test for free or at the discount price of $25 (Pollack Citation2010). Even within the firm, uncertainty about the business model has been an issue since its launch. In 2007, Anne Wojcicki stated:

It’s really too early to specify how we might monetize and derive value from the information we’re aggregating. We’ve thought about a lot of different ways to monetize it, but we’re not ready to talk about them. (Wojcicki in Hamilton Citation2007)

23andme has two core assets: its expertise in curating and communicating genomic science, and its growing database of customers who are willing to allow their data to be used for genomic research and/or to participate actively in research projects (by providing further data). Since its inception the firm has developed multiple revenue streams: customer sales, federal research grants and contract research for pharmaceutical firms. Following the FDA’s regulatory intervention, there was a growth in research activity as 23andme received multiple research grants from NIH and industry investment from pharmaceutical firms seeking to exploit their database. In 2015, 23andme struck deals with Genentech and Pfizer providing them with access to the firm’s database in return for “upfront payments and a cut of revenue from new drugs development” (Bercovici Citation2015). 23andme subsequently established its own drug development unit.

These developments were followed by a new financing round in which the firm raised $115M, nearly as much as the cumulative total it raised in the first four financing rounds. It was in this investment round that 23andme was valued at just over $1Billion, and the firm joined the growing band of Silicon Valley unicorns. Yet when the firm announced its intentions to move into drug development not everyone was convinced. Andrew Pollack at the New York Times cited the failures of older genomics firms like Celera and deCODE which had attempted to straddle diagnostics and drug development but failed (Pollack Citation2015). Furthermore, there seemed to be continued confusion within 23andme about its business model: Anne Wojcicki stated that the firm’s main revenue stream would be R&D for pharma firms (Anonymous Citation2013) but Andy Page stated “We always were and always will be a consumer company first, but doing research is a close second” (quoted in Lash Citation2015). According to one industry executive, the tension between the two business models continues to slow progress on FDA approval: “23andme have great research scientists, but they are terrible at product development” (Anonymous Citation2017).

Discussion – between hope and truth in unicorn valley

The case of 23andme sheds new light on the practice of promissory capitalism and the “complex entanglements of hope and truth at the different stages of company development and market formation” (Martin Citation2015, 439). Martin’s regime of truth has, in effect, three evaluative domains in which hopes are tested: the consumer market, the regulatory regime and the public stock market.

With regard to the consumer market, the hope articulated by 23andme was that within five to ten years “it will be standard for individuals to have access to their genetic information” (Wojcicki quoted in Dubner Citation2009). In October 2015, 23andme declined to reveal customer numbers to the New York Times (Pollack Citation2015), but according to Anthony Regalado (Citation2016), the firm had 1.2 million customers by June 2016. Given this failure to establish consumer genomics as a “standard” consumer good routinely accessed by a significant portion of the population, the firm’s quest for commercial viability has pivoted towards greater emphasis on the business-to-business market of pharmaceutical R&D services. Its subsequent pivot towards drug development has, according to the CEO, only served to further defer the goal of profitability (Pollack Citation2015). In effect, the firm has moved the evaluative goalposts, placing it in a liminal position between the regime of hope and the regime of truth.

23andme’s promise to disrupt healthcare by a shift towards preventive medicine is undermined by this change in business models. Anne Wojcicki continues to offer a social critique of the ways in which financial incentives in healthcare are skewed to treatment not prevention, yet her firm’s business model is now based on providing pharmaceutical R&D services and developing its own novel therapeutics. This apparent disjuncture offers an insight into how disruption functions as rhetorical strategy across separate evaluative principles. 23andme’s investors want the firm’s CEO to communicate passionately her compelling vision of the social value of consumer genomics, and they need the firm establish a sustainable business model that will generate a significant return on investment. Since these are two separate evaluative principles, then contradictions between them are not necessarily matters of concern for investors.

The encounter with the FDA was also part of 23andme’s partial transition to the regime of truth, challenging its disruptor strategy of regulatory arbitrage by forcing closure on the ambiguity about whether the firm was simply an Internet-based research business, generating its own data and sharing the fruits of the broader genomic research enterprise with the public, or a consumer healthcare service. The bolder the firm’s claims that genetic risk assessment was a preventive health strategy that could transform medicine, the harder it became to argue that it should not be regulated as a healthcare product. Such was the logic of the FDA (Citation2013), which drew attention to the gradual expansion of 23andme’s marketing claims in the warning letter that led to closure of the firm’s health-related testing service in the USA in 2013.

The disruptor practice of regulatory arbitrage has been abandoned in favor of a dual strategy of compliance and lobbying for regulatory reform. The recent success of this strategy notwithstanding, it should be noted that the risk gene tests which have been FDA-approved are all for single genes; the polygenic risk scores that were a core part of 23andme’s health testing service, but that had attracted much scientific criticism, remain firmly in the regime of hope. The reasons for the regulatory exemption for future risk tests that accompanied the recent FDA clearance are unclear, but it may demonstrate the value of the established disruptor tactic of switching from regulatory arbitrage to lobbying for regulatory reform. Perhaps the exemption also signals an accommodation between the software industry’s beta testing mode of iterative, flexible innovation and the more linear, sequential approach to product development enforced by the FDA, thus demonstrating Stark’s contention that successful entrepreneurship entails harnessing the creative friction generated by the “rivalry of evaluative principles” (6).

The FDA’s (Citation2013) action against 23andme raises important issues about corporate governance in unicorn firms. Had the firm been public at the time when FDA shut down its health reports in November 2013, its share price would have plummeted and Anne Wojcicki would likely have come under intense pressure to resign as CEO. Further pressure might have come from investor scrutiny of the firm’s commercial performance – in her 2015 interview with the New York Times Wojcicki revealed that the firm was not yet profitable (Pollack Citation2015). At this point, the firm had been operating for eight years and had raised $240M in VC finance. In the traditional trajectory of a diagnostics start-up, 23andme’s investors would have already pushed for a liquidity event to generate a return on their investment, either through acquisition by a larger firm or via an IPO. Either option would have meant that the firm would have been subject to intense external scrutiny of its assets, business model, and management team. Flotation would have opened the firm to publication of quarterly financial reports that would have been subject to expert assessment by stock market analysts.

23andme has been able to attract such huge investments but still remain a private firm because of the massive increase in private capital available for start-ups in Silicon Valley. Marc Andressen, one of Silicon Valley’s leading venture capitalists, was reported in the New York Times describing the stark divergence between how investors now behave towards the chief executives of public firms and private firms: “‘They tell the public C.E.O., ‘Give us the money back this quarter,’ and they tell the private C.E.O., ‘No problem, go for 10 years’” (Manjoo Citation2015). It is perhaps unsurprising that Wojcicki has publicly stated that she wishes to keep the firm private for the time being (Wojcicki Citation2016).

How does the growth in private capital affect the relationship between regimes of hope and truth in the bioeconomy? There is now much discussion about whether rapid growth in the number of unicorn firms signals that Silicon Valley has become embroiled in another investment bubble. Industry analysts report that some unicorn firms are stuck in pre-IPO because there is “a large unresolved disparity between public and private market valuations” of the firms’ commercial worth (Renaissance Capital Citation2015). Gompers et al.’ (Citation2016) survey of venture capitalists found that 91% thought that unicorns were over-valued, an opinion shared by those who had invested in unicorns and those who had not.

To return to Paul Martin’s model, it seems that by reducing firms’ reliance on public flotation as a source of investment finance, the era of unicorn finance has expanded the liminal space between the regimes of hope and truth. That liminal space is not confined geographically to Silicon Valley, but the region’s abundant private capital and its distinctive style of disruptive entrepreneurship are critical components in this new mode of promissory capitalism. Understanding how this regime of accumulation functions requires attention to the multiple evaluative principles at play, and the ways in which they intersect. Given the growing concerns that the rise in unicorn firms signals an unsustainable and potentially destructive investment bubble, there is a pressing need for further scrutiny of the rationalities that underpin VC valuation processes.

This paper has argued that research on the bioeconomy should pay greater attention to processes of geographical differentiation. Future work might usefully interrogate these dynamics in comparative perspective, broadening out to encompass other high-tech clusters in the USA, Europe and Asia-Pacific. At the sectoral level, there is considerable scope for more explicit comparison of diagnostics and therapeutics firms. Finally, this paper suggests that a fruitful area for further research in the sociology of expectations would be the role of charismatic leadership in start-up firms. Such research might examine the performativity of corporate values and their embodiment in the person of the CEO, the media’s role in the promotion of entrepreneur as celebrity, and the role these business leaders play in managing their firms’ transition from the regime of hope to the regime of truth.

Disclosure statement

No potential conflict of interest was reported by the author.

Notes

1. The disruptors gain market entry not by offering a superior product but by exploiting the fact that incumbents in mature markets tend to focus on their most demanding and profitable customers, neglecting the needs of other parts of the market. Once that market has developed disruptors then move upmarket, targeting the incumbents’ mainstream customers.

References

- 23andme. 2008. “TIME Magazine Names 23andMe’s Personal Genome Service 2008 Invention of the Year.” Press release, October 30. https://mediacenter.23andme.com/press-releases/time-magazine-names-23andmes-personal-genome-service-2008-invention-of-the-year/.

- Alsever, J., S. Durst, J. Borzo, and S. S. R. Datta. 2006. “The Patient Knows Best.” Business 2.0, November 9. http://money.cnn.com/magazines/business2/business2_archive/2006/10/01/8387104/index.htm.

- Anonymous. 2013. “How 23andMe Disrupts Health Care with DNA.” BioBox Bloomberg, November 26. https://www.bloomberg.com/news/videos/b/ee8c5651-9fdc-4fea-bf01-2d9e574fc75d.

- Anonymous. 2017. Personal Communication with US Diagnostics Industry Executive. March.

- Barbrook, R., and A. Cameron. 1996. “The Californian Ideology.” Science as Culture 6 (1): 44–72. doi: 10.1080/09505439609526455

- Benner, K. 2012. “23andme Wants to Change the Face of Health Care.” Fortune, December.

- Bercovici, J. 2015. “The Billion-Dollar Company That Not Even the Feds Could Stop.” Inc., October. https://www.inc.com/magazine/201510/jeff-bercovici/the-dna-whisperer.html.

- Birch, K., and D. Tyfield. 2013. “Theorizing the Bioeconomy: Biovalue, Biocapital, Bioeconomics or … What?” Science, Technology, & Human Values 38 (3): 299–327. doi: 10.1177/0162243912442398

- Boltanski, L., and L. Thévenot. 1991. On Justification. Economies of Worth. Princeton, NJ: Princeton University Press.

- Brady, D. 2013. “23andme Wants to Take Its Tests Mass-market.” Bloomberg, September 30. https://www.bloomberg.com/news/articles/2013-09-30/23andme-wants-to-take-its-dna-tests-mass-market.

- Casper, S. 2006. “Exporting the Silicon Valley to Europe: How Useful Is Comparative Institutional Theory?.” In Innovation, Science, and Institutional Change: A Research Handbook, edited by Jerald Hage and Marius Meeus, 483–504. Oxford: Oxford University Press.

- Christensen, C. M. 1997. The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail. Boston, MA: Harvard Business School Press.

- Christensen, C. M., M. Raynor, and R. McDonald. 2015. “What Is Disruptive Innovation?” Harvard Business Review, December. https://hbr.org/2015/12/what-is-disruptive-innovation.

- Crow, D. 2015. “Theranos Exemplifies Clash of New Versus Old In-vitro Test Models.” Financial Times, December 15.

- Curnutte, M. 2017. “Regulatory Controls for Direct-to-Consumer Genetic Tests: A Case Study on How the FDA Exercised its Authority.” New Genetics and Society. doi:10.1080/14636778.2017.1354690.

- Dorfman, R. 2013. “Falling Prices and Unfair Competition in Consumer Genomics.” Nature Biotechnology 31 (9): 785–786. doi: 10.1038/nbt.2693

- Dubner, J. 2009. “Genetics Entrepreneur Anne Wojcicki Answers Your Questions.” Freakonomics Blog, August 12. http://freakonomics.com/2009/08/12/genetics-entrepreneur-anne-wojcicki-answers-your-questions/.

- Eunjung Cha, A. 2014. “23andMe Co-founder Anne Wojcicki’s Washington Charm Offensive.” Washington Post, June 27.

- FDA. 2013. Warning Letter to Anne Wojcicki, 23andme. Department of Health and Human Services, November 22. https://www.fda.gov/iceci/enforcementactions/warningletters/2013/ucm376296.htm.

- Fong, T. 2012. Difficult VC Funding Market Extends to ‘Omics, MDx. GenomeWeb Aug 20.

- Goetz, T. 2007. “23andme Will Decode Your DNA for $1,000. Welcome to the Age of Genomics.” Wired, November 17.

- Gompers, P., W. Gornall, S. Kaplan, and I. Strebulaev. 2016. “How Do Venture Capitalists Make Decisions?” Stanford University Graduate School of Business Research Paper No. 16–33.

- Green, K. 1991. “Shaping Technologies and Shaping Markets: Creating Demand for Biotechnology.” Technology Analysis & Strategic Management 3 (1): 57–76. doi: 10.1080/09537329108524032

- Gupta, A., and H. Wang. 2016. “The Reason Silicon Valley Beat Out Boston for VC Dominance.” Harvard Business Review, November 16. https://hbr.org/2016/11/the-reason-silicon-valley-beat-out-boston-for-vc-dominance.

- Hamilton, D. 2007. “23andme: Will the Personal-Genomics Company Need Big Pharma to Make Money?” VenutreBeat, November 19.

- Helmreich, S. 2008. “Species of Biocapital.” Science as Culture 17 (4): 463–478. doi: 10.1080/09505430802519256

- Hof, R. 2014. “‘We Are Going For Change’: A Conversation with 23andMe CEO Anne Wojcicki.” Forbes, August 15. http://www.forbes.com/sites/roberthof/2014/08/15/we-are-going-for-change-a-conversation-with-23andme-ceo-anne-wojcicki/#5af96b275477.

- Hogarth, S., and B. Salter. 2010. “Regenerative Medicine in Europe: Global Competition and Innovation Governance.” Regenerative Medicine 5 (6): 971–985. doi: 10.2217/rme.10.81

- Horn, M. 2016. “Uber, Disruptive Innovation, and Regulated Markets.” Christensen Institute Blog, June 16. http://www.christenseninstitute.org/blog/uber-disruptive-innovation-and-regulated-markets/.

- Hsu, A. R., J. L. Mountain, A. Wojcicki, and L. Avey. 2009. “A Pragmatic Consideration of Ethical Issues Relating to Personal Genomics.” The American Journal of Bioethics 9 (6–7): 1–2. doi: 10.1080/15265160902966795. doi: 10.1080/15265160902966795

- Keegan, K. 2008. Biotechnology Valuation: An Introductory Guide. Chichester: Wiley.

- King, A., and B. Baatartogtokh. 2015. “How Useful Is the Theory of Disruptive Innovation?” MIT Sloan Management Review, September. http://sloanreview.mit.edu/article/how-useful-is-the-theory-of-disruptive-innovation/.

- Langreth, R., and M. Herper. 2008. “States Crack Down on Online Gene Tests.” Forbes, April 18. http://www.forbes.com/2008/04/17/genes-regulation-testing-biz-cx_mh_bl_0418genes_print.html.

- Lash, A. 2015. “23andme Adds On: More About the Gene-Test Maker’s Drug R&D Ambitions.” Xconomy, March 12. http://www.xconomy.com/san-francisco/2015/03/12/23andme-adds-on-more-about-the-gene-test-makers-drug-rd-ambitions/?utm_source=related-content&utm_medium=link&utm_campaign=related-content.

- Lazonick, W., and Ö Tulum. 2011. “US Biopharmaceutical Finance and the Sustainability of the Biotech Business Model.” Research Policy 40: 1170–1187. doi: 10.1016/j.respol.2011.05.021

- Lowe, F. 2008. “Google Wife Targets World DNA Domination.” Daily Telegraph, January 25.

- Manjoo, F. 2015. “As More Tech Start-Ups Stay Private, So Does the Money.” New York Times, July 1.

- Martin, P. 2015. “Commercialising Neurofutures: Promissory Economies, Value Creation and the Making of a New Industry.” BioSocieties 10 (4): 422–443. doi: 10.1057/biosoc.2014.40

- McCray, W. P. 2012. “California Dreamin’: Visioneering the Technological Future.” In Minds and Matters: Technology in California and the West, edited by Volker Janssen, 347–378. Berkeley: University of California Press.

- McDermid, R. 2016. “Why Are So Many Startups Behaving Badly, and Can Anything Be Done About It?” San Francisco Business Times, October 6. http://www.bizjournals.com/sanfrancisco/news/2016/10/06/startup-ethics-ipo-zenefits-theranos-lending-club.html.

- Mihaescu, R., M. Van Hoek, E. J. G. Sijbrands, A. Uitterlinden, J. C. M. Witteman, A. Hofman, C. M. Van Duijn, and A. C. J. W. Janssens. 2009. “Evaluation of Risk Prediction Updates from Commercial Genome-wide Scans.” Genetics in Medicine 11 (8): 588–594. doi: 10.1097/GIM.0b013e3181b13a4f

- Mirowski, P. 2011. Science-mart: Privatizing American Science. Cambridge, MA: Harvard University Press.

- Moreira, T., and P. Palladino. 2005. “Between Truth and Hope: On Parkinson’s Disease, Neurotransplantation and the Production of the ‘Self’.” History of the Human Sciences 18 (3): 55–82. doi: 10.1177/0952695105059306

- Morozov, E. 2013a. “The Meme Hustler: Tim O’Reilly’s Crazy Talk.” The Baffler, April. http://thebaffler.com/salvos/the-meme-hustler.

- Morozov, E. 2013b. To Save Everything Click Here. New York, NY: Public Affairs.

- Murphy, E. 2013. “Inside 23andme Founder Anne Wojcicki’s $99 DNA Revolution.” Fast Company, October.

- Pettifor, A. 2015. “Is Capitalism ‘Mutating’ into an Infotech Utopia?” Open Economy, November 6. https://www.opendemocracy.net/ann-pettifor/is-capitalism-mutating-into-infotech-utopia.

- Pollack, A. 2010. “Gene-testing Companies: Too Little Too Soon for Success.” International Herald Tribune, March 20.

- Pollack, A. 2010. “Outlook Uncertain.” New York Times, March 20.

- Pollack, N. 2014. “23andme Wants to Reveal Health Risks Using Your DNA.” Wired, December 2.

- Pollack, A. 2015. “23andMe Will Resume Giving Users Health Data.” New York Times, October 21.

- Rao, L. 2009. “All in the Family: Sergey Brin Loans 23andme $10 Million and Google Ponies up $2.6 Million.” Techcrunch, June 18. https://techcrunch.com/2009/06/18/all-in-the-family-sergey-brin-loans-23andme-10-million-and-google-ponies-up-26-million/.

- Regalado, A. 2016. “23andMe Sells Data for Drug Search.” MIT Technology Review June 21. https://www.technologyreview.com/s/601506/23andme-sells-data-for-drug-search/.

- Renaissance Capital. 2015. “2015 US IP Annual Review.” http://www.renaissancecapital.com/news/renaissance-capitals-2015-us-ipo-annual-review-37648.html.

- Saukko, P. 2017. “Shifting Metaphors in Direct-to-Consumer Genetic Testing: From Genes as Information to Genes as Big Data.” New Genetics and Society. doi:10.1080/14636778.2017.1354691.

- Sayer, A. 1995. Radical Political Economy: A Critique. Oxford: Blackwell.

- Sayer, A. 2004. “Moral Economy.” Department of Sociology, Lancaster University. http://www.comp.lancs.ac.uk/sociology/papers/sayer-moral-economy.pdf.

- Shapin, S. 2008. The Scientific Life: A Moral History of a Late Modern Vocation. Chicago, IL: University of Chicago Press.

- SharesPost. 2016. “Zero to One Billion: Demistifying the Unicorn.” SharesPost. Accessed May 9, 2017. http://sharespost.com/insights/research-reports/zero-to-one-billion-landing/.

- Sheppard, E. 2013. “Rethinking Capitalism from a Geographical Perspective.” Archives of the Association of Economic Geographers 59 (4): 394–418.

- Simons, K. 2009. “Two Roads to Riches: The (In)frequency of Strongly Disruptive Technological Change.” Department of Economics, Rensselaer Polytechnic Institute, November 9. http://homepages.rpi.edu/~simonk/pdf/tworoads.pdf.

- Srnicek, N. 2017. Platform Capitalism. Cambridge: Polity Press.

- Stark, D. 2009. The Sense of Dissonance: Accounts of Worth in Economic Life. Princeton, NJ: Princeton University Press.

- Teeman, T. 2012. “‘He Cooks. I Clean’; The Simple Life of the Google Power Couple.” The Times, February 4.

- Tellis, G. 2016. Startup Index of Nations, Cities: Startups Worth $1 Billion or More (‘Unicorns’). Center for Global Innovation, USC Marshall School of Business. https://www.marshall.usc.edu/sites/default/files/PDF/Unicorn-Index-Report-GT17.pdf.

- Thiel, P. 2014. “Competition Is For Losers.” Wall Street Journal, September 12.

- Wojcicki, A. 2011. “A Conversation with Anne Wojcicki.” Web2.0 Summit, October 19. https://www.youtube.com/watch?v = hYs85Q13Trk.

- Wojcicki, A. 2016. Interview by Kara Swisher, Recode Decode, Podcast audio, April 4. http://www.recode.net/2016/4/4/11585828/23andme-anne-wojcicki-genomics-theranos-alex-rodriguez.