ABSTRACT

Energy and climate policies may have significant economy-wide impacts, which are regularly assessed based on quantitative energy-environment-economy models. These tend to vary in their conclusions on the scale and direction of the likely macroeconomic impacts of a low-carbon transition. This paper traces the characteristic discrepancies in models’ outcomes to their origins in different macro-economic theories, most importantly their treatment of technological innovation and finance. We comprehensively analyse the relevant branches of macro-innovation theory and group them into two classes: ‘Equilibrium’ and ‘Non-equilibrium’. While both approaches are rigorous and self-consistent, they frequently yield opposite conclusions for the economic impacts of low-carbon policies. We show that model outcomes are mainly determined by their representations of monetary and finance dimensions, and their interactions with investment, innovation and technological change. Improving these in all modelling approaches is crucial for strengthening the evidence base for policy making and gaining a more consistent picture of the macroeconomic impacts of achieving emissions reductions objectives. The paper contributes towards the ongoing effort of enhancing the transparency and understanding of sophisticated model mechanisms applied to energy and climate policy analysis. It helps tackle the overall ‘black box’ critique, much-cited in policy circles and elsewhere.

Key policy insights

Quantitative models commissioned by policy-makers to assess the macroeconomic impacts of climate policy generate contradictory outcomes and interpretations.

The source of the differences in model outcomes originates primarily from assumptions on the workings of the financial sector and the nature of money, and of how these interact with processes of low-carbon energy innovation and technological change.

Representations of innovation and technological change are incomplete in energy-economy-environment models, leading to limitations in the assessment of the impacts of climate-related policies.

All modelling studies should state clearly their underpinning theoretical school and their treatment of finance and innovation.

A strong recommendation is given for modellers of energy-economy systems to improve their representations of money and finance.

1. Introduction

Climate and energy targets could be met via different pathways and combinations of supply-side and demand-side technological and socioeconomic options. Significant debate exists on strategies for achieving an efficient and cost-effective sustainable energy transition (Edenhofer et al., Citation2010; IPCC, Citation2014b; Kriegler et al., Citation2014; Nordhaus, Citation2010; Nordhaus, Citation2015; Rogelj et al., Citation2015; Rogelj et al., Citation2018; Stern, Citation2007). Macro-models are used extensively in this context to inform policy-making, notably through the Intergovernmental Panel on Climate Change (IPCC) process (IPCC, Citation2014b), and in national, European and international policy-making.Footnote1

Following the recent context of economic instability in many countries across the globe, it is of primary importance to determine whether climate policies will hinder or boost economic growth, lead to unsustainable debt levels, generate economic opportunity or impose an economic burden (Mercure, Pollitt, Bassi, Viñuales, & Edwards, Citation2016b; Stern, Citation2007; Stern, Citation2015).Footnote2 Innovation as a driver of economic activity is a recurrent theme in current discourses on economic development (BIS, Citation2011; European Commission, Citation2017; OECD, Citation2015), as well as public and private aggregate debt (Mazzucato, Citation2018; McLeay, Radia, & Thomas, Citation2014b, Citation2014a), This particularly relates to low-carbon and energy innovation, which could either fuel future prosperity or become an economic burden, its scale being sufficiently large to influence the macroeconomy.

Energy-economy-environment (E3) models are typically designed to inform policy-makers on technology or economic scenarios for achieving low-carbon transformations. However, they do not currently address in the required detail some of the key features of low-carbon innovation, including the necessary investment and finance of technology transitions, leaving unanswered questions for actual policy application (Grubb, Hourcade, & Neuhoff, Citation2014; Mercure et al., Citation2016b; Pollitt & Mercure, Citation2018). As we show here, consensus has never been reached over how to treat innovation and technological change, and financing, in basic economic theory. Since underlying model assumptions on such theory determine model outcomes and policy recommendations, results are often opposite for different models (see e.g. Cambridge Econometrics, Citation2013, Citation2015; Carbon Trust, Citation2005; Edenhofer et al., Citation2010). This is an issue that has been debated for many years (Grubb, Carraro, & Schellnhuber, Citation2006; Grubb, Edmonds, Ten Brink, & Morrison, Citation1993; Grubb, Köhler, & Anderson, Citation2002) While there is an ongoing debate on how to improve the realism of technological change and agent behaviour by using model experiments (Holtz et al., Citation2015; Li & Strachan, Citation2017; Li, Trutnevyte, & Strachan, Citation2015; McCollum et al., Citation2017; McCollum et al., Citation2018a; Pettifor, Wilson, McCollum, & Edelenbosch, Citation2017; Trutnevyte, Citation2016), none of these experiments challenge representations of investment, money and finance.

This problem reflects partly the underestimation of the role of finance and money on the real economy (Guttmann, Citation2016; Minsky, Citation1986; Monasterolo & Raberto, Citation2018), including stranded assets (McGlade & Ekins, Citation2015; Mercure et al., Citation2018b) or assets at risk from climate change and climate policy (Bank of England, Citation2015; Battiston, Mandel, Monasterolo, Schütze, & Visentin, Citation2017; Campiglio et al., Citation2018; Carney, Citation2015), and partly the difficulty in modelling energy-related innovation, technological change and the effectiveness of policy instruments (Mercure et al., Citation2016b). Few of the current E3 models (e.g. as in GEA, Citation2012; IPCC, Citation2014b; Kriegler et al., Citation2014) have representations of the financial sector, its relevance for a large scale decarbonization transition and its impact on the macroeconomy. This is a major shortcoming because such a transition will require large-scale investment in non-traditional sectors (Pollitt & Mercure, Citation2018) and put at risk existing investment and assets (Bank of England, Citation2015; Battiston et al., Citation2017; Carney, Citation2015; Mercure et al., Citation2018b). It also requires a much better understanding of the complex behaviour of agents and their response to policy incentives than what currently exists in the community (Knobloch & Mercure, Citation2016). While the need for a more explicit representation of the financial sector in macroeconomic models has been widely discussed after the 2007 global financial crisis (e.g. for Dynamic Stochastic General Equilibrium (DSGE) models as they are used by central banks), such a discussion in the context of climate policy has yet to take place.

In this paper, we review current modelling methodologies for assessing energy and climate policies. We provide a critical comparative analysis of various approaches to modelling policy-induced energy innovation and technological change, in order to better inform policy-makers and users of modelling results. We aim to answer important climate and energy policy questions: can policy and governance accelerate rates of low-carbon technology substitution, innovation and energy efficiency changes? Will this help or hinder economic development? And, do models accurately capture the impacts of investment that result from the use of chosen policy instruments?

For this purpose, we identify features and factors in theory and models that result in particular modelling outcomes. This requires looking at their underlying theoretical basis and methodological assumptions: how do we currently understand innovation? Several reviews on the representation of energy-related innovation in E3 models have been written (Baccianti & Löschel, Citation2014; Clarke, Weyant, & Edmonds, Citation2008; Gillingham, Newell, & Pizer, Citation2008; Grubb et al., Citation2002; Hall & Buckley, Citation2016; Köhler, Grubb, Popp, & Edenhofer, Citation2006; Löschel, Citation2002; Popp, Citation2006). However, none of these reviews cover the theoretical underpinnings of the various existing implementations, especially with regards to finance. Furthermore, many analyses have been made on how innovation may be induced by prices or policy (Acemoglu, Aghion, Bursztyn, & Hemous, Citation2012; Goulder & Schneider, Citation1999; Goulder, Hafstead, & Williams, Citation2016; Nordhaus, Citation2014; Popp, Citation2002), going back to Nordhaus (Citation1973) and Hicks (Citation1932), but again, these do not cover the role of money and finance in technological change. We note that the various model families have not converged at all to our knowledge over the years. It is also correct to say that nearly no attention has been given to representations of money and finance in models, particularly in the field of energy-economy modelling (Grubb et al., Citation1993; Grubb et al., Citation2002; Grubb et al., Citation2006), as computational experiments with finance have been made outside of the field (Battiston et al., Citation2016; Haldane & Turrell, Citation2018).

In Section two, we review how innovation and finance are addressed in recent economic theory and models. Section three shows how different underlying theories imply different perspectives on the macro-economic effects of policies, how this can be considered in policy-making, and under which conditions models could converge. Section four concludes and proposes a research agenda covering key gaps in the future energy-environment-economy modelling of low-carbon transitions. The Supplementary Material (SM) provides more information on the models used in this work.

2. Materials and methods: innovation in economic theory and models

2.1. Technology and innovation in economic theory

Economic theory can be roughly grouped into two different schools, each with different perspectives on innovation and the macroeconomy: equilibrium economics and non-equilibrium economics.

The equilibrium economics school explains finance, innovation and productivity change based on Post-Walrasian neoclassical economics (Acemoglu, Citation2002; Aghion, Howitt, Brant-Collett, & García-Peñalosa, Citation1998; Arrow, Citation1962; Romer, Citation1986; Solow, Citation1986). The central assumption is that prices coordinate the actions of all agents that adjust so as to equilibrate the markets for production factors (labour, capital/finance, knowledge, etc). The decisions of representative agents (usually one per economic activity) ensure that, given technology and resource constraints and market imperfections (labour unemployment), all remaining factors are always fully employed in the most efficient way, determining the state of the economy. This underpins most models used to assess energy-economy issues in the climate change community (e.g. Capros et al., Citation2014; Clarke et al., Citation2014; Kriegler et al., Citation2014; Kriegler et al., Citation2015a; Nordhaus, Citation2017).

In the non-equilibrium economics school, the economy is seen as being in perpetual dynamical change. At its heart is Schumpeter’s foundational workFootnote3 on the role of the entrepreneur and of the enabling financial institutions (Schumpeter, Citation1934, Citation1939, Citation2014), and Keynes’ analysis of investment and macroeconomic dynamics (Keynes, Citation1936), which has been extended by the ‘Post-Keynesians’ into a comprehensive theory of macroeconomics (e.g. Lavoie, Citation2014). Models that focus on money and finance follow this theoretical underpinning (e.g. Bovari, Giraud, & Mc Isaac, Citation2018; Dafermos, Nikolaidi, & Galanis, Citation2017; Lamperti, Dosi, Napoletano, Roventini, & Sapio, Citation2018; Mercure, Pollitt, Edwards, Holden, & Vinuales, Citation2018a; Monasterolo & Raberto, Citation2018).

We summarize here how economic development and productivity change is understood to take place for both schools. A more extensive review of the treatment of innovation throughout the history of economic thought is given in (Mercure et al., Citation2016a).

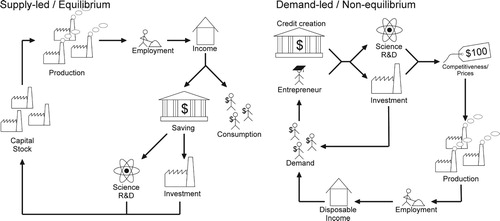

The basic view of the equilibrium school is one of optimal allocation of scarce economic resources given technology at each point in time, and of optimal capital accumulation over time ( left):

Firms produce by fully using all available production factors (full employment of capital)Footnote4 to meet the demand for their products, given the technology options and households’ preferences for consumption.

Firms decide on investment that maximizes their net present value, and seek financing from the capital market, which the interest rate clears.

Firms’ revenues from selling products are paid out to households, according to their provision of labour and capital ownership to the production process. Based on an intertemporal utility maximization, households choose how to allocate this income between consumption (of various goods) and saving.Footnote5

Savings are used to finance firms’ investments. Investment accumulation defines the capital stock available for production, which includes: physical production facilities (e.g. new factories, replacement of retired machinery, etc.), and investments into knowledge stock (e.g. technical progress, R&D).

The increased amount of capital, labour (population) and their improved factor productivity (resulting from R&D expenditure) expand the production frontier, which allows higher volumes of production.

Figure 1. Contrasting representations of economic growth in the Post-Keynesian/Post-Schumpeterian (non-equilibrium) schools to the neoclassical (equilibrium) school.

Meanwhile, the non-equilibrium school contends that economic development takes place through entrepreneurial activity and the creation of purchasing power by banks ( right):

Entrepreneurs sense where potential demand is not satisfied and see potential applications for their ideas. They apply to financial institutions to finance their innovative improvements to the existing capital stock. Banks offer loans and create deposits, based on entrepreneurs’ credit-worthiness and the expected profitability of the investment project.

Bank-funded investment in new capital involves R&D expenditure in various connected technologies and sectors, which increases their productivity.

Productivity improvements reduce production costs. This can result in a mixture of (1) profits for the entrepreneurs and (2) price reductions in consumer markets. Both result in higher income for households, higher demand for the new products, and/or (3) reduced imports, and/or (4) increased exports.

Higher income leads to higher effective demand (for all products) and higher saving.

Higher demand and profits incentivise firms to re-invest in R&D and to expand their capital stock.

These two representations are radically different in their key principles and lead to contrasting approaches when implemented quantitatively, with opposite directions in the flow of information:

In the equilibrium school, a representative agent maximizes utility by allocating fixed resources between possible uses, so that the methodology is generally tied to constrained optimization (optimization henceforth; every point in time is optimal and in a steady state within its context). In this perspective, the economy is driven by its ability to produce (supply-led).

In the non-equilibrium school, the state of the economy at every time step primarily depends on its states in previous time steps and expectations of the future and financial resources are unconstrained, so that the methodology is generally tied to dynamical systems simulations (simulation henceforth). In that perspective, the economy is driven by demand (demand-led). These are independent traditions of mathematics research, often pursued independently from one another.

While the simulation/optimization terminology may be neither exhaustive nor always exact,Footnote6 in practice it classifies effectively the methodology used in most contemporary models, and captures a marked methodological division that reinforces theoretical differences and perceptions for policy-making.Footnote7

The theoretical difference between the schools has at its heart a difference in the treatment of risk and uncertainty in investment and finance (Fontana, Citation2008; Keynes, Citation1921).Footnote8 Keynes describes risk as quantifiable probabilities of outcomes of an action (e.g. investment), while uncertainty is unquantifiable. In Post-Keynesian theory, it is assumed that investment takes place under fundamental uncertainty, which makes it impossible for agents to reliably estimate the likelihood of return on investment. Keynesian theory assumes that due to lack of detailed information, it is not possible for agents to devise a strategy that fully uses reliably all resources, as opposed to neoclassical theory, in which even under uncertainty, agents would find ways through markets to coordinate the use of all resources. For example, in the non-equilibrium school, under uncertainty over variations of demand, the investor plans for spare production capacity, so that he/she can respond to sudden demand changes (Fontana, Citation2008; Lavoie, Citation2014). This implies that investment depends on investor and bank confidence in markets, and drives income and employment (or unemployment) of resources.

Meanwhile, in pure equilibrium theory in its most basic form, income determines investment through the propensity to save. Since demand can be relied upon and be foreseen (probabilistically), capital is optimally planned and used. Thus, capital accumulation determines production, and the theory functions the other way around. Therefore, the different direction of economic causality in equilibrium and non-equilibrium theory is a consequence of their respective treatments of risk and uncertainty.

A difference in philosophical interpretation also arises: in basic equilibrium theory, agents behave in a way that leads to maximal utility for all. This therefore identifies a normative or aspirational scenario, and deviations, ascribed to real-world effects and policy decisions, are discussed as distortions or frictions. Meanwhile, in non-equilibrium theory, no scenario is deemed more aspirational than any other; each scenario describes the economy in a different trajectory, and scenarios diverge from one another over time.

2.2. Technology and innovation in contemporary low-carbon transition models

2.2.1. Taxonomy of theories and models used for informing climate policy and beyond

We list representations of money, innovation, technology, methodology and the source of economic change in ten schools and research areas in economics, grouped into equilibrium and non-equilibrium (). This list is not exhaustive, but represents the main contemporary currents of economic thought.

Table 1. Schools of economic thought.

We furthermore classify current macroeconomic and macro-sectoral economic models along the categories of general equilibrium, partial equilibrium, macro-econometric, systems dynamics and agent-based (). Within each of these classifications, sub-categories exist. We provide a taxonomy of approaches according to the types of assumptions adopted for the structure of technological change, its representation at the micro and macro levels, and their representation of the entrepreneur at both levels.

Table 2. Types of macro-models and summary of their assumptions regarding energy-related innovation and investment behaviour.

We have classified the main methodologies in terms of their representation of energy-related innovation, and representation of agents, at the micro and macro levels. Here ‘micro’ and ‘macro’ are used to refer to the level of aggregation: ‘micro’ means for example distinguishing individual technologies (e.g. solar PV), while macro means modelling aggregates at the sectoral or economy-wide level (e.g. the electricity or automotive sectors as a whole). Innovation indicates representations of cost-reducing or productivity-enhancing activity, while agents refer to representations of decision-making and behaviour (e.g. investment decisions).

Representations of endogenous innovation and induced/endogenous technological change (ITC/ETC) were explored extensively a decade ago, and applied to energy and climate policy (see IMCP, Edenhofer, Kemfert, Lessmann, Grubb, & Koehler, Citation2006). The result was that, according to the models, the capital costs and hence investment requirements to roll out technological change become less over time if learning-by-doing and technological progress are allowed to take place endogenously in those models.

The change towards ITC/ETC has been crucial: in earlier neoclassical models with inter-temporal optimization, the representative agent was optimizing utility over a trend of productivity predetermined with certainty. This had the perverse effect that the representative agent could anticipate future gains in efficiency and so postpone investing in low-carbon energy if this was not cost-optimal. The presence of so-called back-stop technologiesFootnote9 also had the same effect, promising future solutions that would appear with certainty once made economical. This in general meant that pre-ETC model results were to a great extent determined by exogenous assumptions (Grubb et al., Citation2002). With ITC/ETC, results emerged regarding the clustering of different possible types of optimal path-dependent states of the energy system, whether high or low-carbon (Gritsevskyi & Nakićenovic, Citation2000).

Exogenous productivity has been equally problematic in Post-Keynesian / Post-Schumpeterian simulation models. For example, if the efficiency of new energy-using technology did not endogenously respond to a change in prices, models would predict continuous slowdowns of energy-based service demand (e.g. transport, energy intensive goods, and perhaps economic growth) in scenarios of increasing energy prices, something not observed in reality (Grubb et al., Citation2014, p. 209; Grubb et al., Citation2018). In reality, price rises incentivise investment in higher efficiency and faster technological turnover, while price falls do not imply technology regression (though they may encourage behaviour that uses more energy, see Grubb et al., Citation2014).Footnote10

However, at the time of these modelling innovations, there was no consensus on the meaning of economic costs, an ongoing issue (see Grubb et al., Citation2014, ch. 11). Indeed, in some studies, costs are identified with total energy system costs, in other cases with additional investment costs, and yet in other cases, with changes in GDP or changes in (conceptualized) utility or welfare (which is still the case, see e.g. IPCC, Citation2014b, ch. 6).

Many contemporary models now feature representations of some degree of ETC/ITC in principle, although it is not always clear to which degree these mechanisms are relied upon in studies, as they are not always reported, an issue that can lead to ambiguity for interpretation.Footnote11 These representations can be radically different, tracing back again to basic economic theory, namely the neoclassical, Post-Keynesian and Post-Schumpeterian schools of thought.

2.2.2. Innovation and technological change in macro-economic models

Consistent with the underlying philosophical assumptions about flows of causality in economic systems, the two theoretical paradigms discussed in Section 2.1 embody the following, opposite, directions of causation with respect to the treatment of innovation and technological change:

In the equilibrium/supply-led paradigm, the representative household chooses between consuming its income now or in the future (i.e. to save). The financial resources made available by saving in the present are exhausted in investment, increasing (with certainty) the production capacity and productivity for supplying consumption in the future, through the accumulation of physical capital and knowledge. Capital resources in each year are finite, and are allocated to their most efficient use (that provides the highest rate of return). Because in deterministic equilibrium models investment outcomes are known with certainty, only the efficient portfolios are selected (technology risk-returns relationships are exogenously specified).

In the non-equilibrium/demand-led paradigm, the entrepreneur decides under fundamental uncertainty whether to borrow funds for investing in production capital, R&D and technology. When banks agree to offer loans, money is created in the form of deposits (the finance for investment), and saving and investment both increase equally. Since investment is not constrained by households’ savings, this increases debt and income simultaneously (unless the economy is operating at full employment). Individual investments may or may not lead to their intended productivity improvements and profit; at the aggregate level, however, they all contribute to an increasing body of knowledge. Economic growth can be driven by increasing debt (although not indefinitely). The clustering of innovation leads to economic cycles.

In computational implementations, the current model zoology is not so clear-cut, and many models are hybrid (e.g. IMACLIM (CIRED, Citation2018) and GEM-E3 (E3MLab, Citation2018a), see the SM for details). In particular, when equilibrium models feature elements that cannot be changed even when it would be optimal to change them (e.g. physical capital with long lifetimes, sticky prices), solutions are ‘sub-optimal’ and models deviate from ‘aspirational’ efficient markets towards descriptions that more closely reflect real-world ‘imperfections’. Furthermore, the representative agent can be given limited foresight (often called the ‘myopic mode’, relaxing the constraints of rational expectations). Finally, if a financial sector is introduced, savings can be borrowed from abroad and repaid in the future (e.g. in GEM-E3-FIT).

A similar division of paradigms also exists in the bottom-up technology modelling literature: an optimization versus simulation methodological divide, with a large number of partial equilibrium cost-optimization models of technology being in use and forming the most common model type. Furthermore, the adoption and diffusion of innovations are processes that are not modelled very well in the community: energy models are found to produce typically pessimistic outcomes in comparison to observed diffusion trends (Wilson, Grubler, Bauer, Krey, & Riahi, Citation2013). This points to a clear need to improve this representation, which is currently addressed in ongoing research initiatives (McCollum et al., Citation2017; McCollum et al., Citation2018a; Mercure et al., Citation2016b).

2.3. The role of money and finance in current macro-models

A transition to a decarbonized energy system requires significant amounts of investment in energy R&D, supply chains, infrastructure and physical capital, which could substantially exceed what might have been invested in this sector in an otherwise business as usual scenario. Even in contexts favourable for entrepreneurs to invest in low-carbon technology, they require access to funds in order for the transition to take place (Pollitt & Mercure, Citation2018). Such investments could, in principle, displace other (arguably more productive) investments, a detrimental crowding-out effect. A debate also exists as to whether government or other finance of innovation in the early stages of the innovation chain crowds-out or crowds-in other private finance in later stages (Hottenrott & Rexhäuser, Citation2015; Mazzucato, Citation2011; Mazzucato & Semieniuk, Citation2017, Citation2018; Popp & Newell, Citation2012).

In the context of this work, we use a general meaning of ‘crowding-out’: when an agent (government, firms, individuals) borrow(s) significant amounts of funds in order to invest into productive capital, this demand could (under certain conditions) divert funds that otherwise would have been used elsewhere in the economy, by bidding upwards the price of finance (the interest rate), i.e. pricing out competing projects. Crowding-out can also apply to physical capital or labour, in which cases prices or wages clear the respective markets.

The potential extent of ‘crowding-out’ depends on the amounts of funds available in the economy, and the degree to which crowding-out is assumed to take place in the model is determinant for model results.

This subject is once more fundamental to economic theory, where we again have the same two paradigms, (a) equilibrium and (b) non-equilibrium, this time with a focus on money. For policy contexts favourable for entrepreneurs to invest significant amounts of funds into low-carbon ventures (e.g. due to carbon pricing), outcomes will differ.

In the equilibrium/supply-led paradigm, investment is determined by saving, which is a fixed proportion of income. Entrepreneurs compete for this restricted finite amount made available through financial markets/institutions. Demand for money by different sectors at the same time is cleared by the rate of interest, i.e. some entrepreneurs are outbid by the willingness to pay of others, and are thus crowded-out. Money is a commodity in a finite quantity chosen by the central bank; if the central bank prints more money, the value of money decreases proportionally (the neutrality of money). Thus equilibrium models need not have any representation of money or inflation, but only of relative prices. In the climate policy context, low-carbon investments promoted by policy crowd out other investments key to the economy. This leads to underinvestment in other key sectors for growth, leading to less productive use of capital, a higher cost of capital and hence overall high costs to the economy.

In the non-equilibrium/demand-led paradigm, investment is unrestricted and determined only by the willingness of entrepreneurs to invest and the willingness of banks to lend (unless funds are re-invested profits), determined by the perception by banks of the credit-worthiness of entrepreneurs. Banks are not solely intermediaries, but have a balance sheet and strategy. Banks borrow from each other, to diversify risk, and to/from the central bank, to gain reserves necessary to underwrite their lending activities (they minimise/optimise the risk and return of their balance sheet, constrained by financial regulation). Money, whether in paper form, or in commercial bank accounts, is a form of asset-liability pair, between two entities, the bank (debtor) and the owner (creditor). Thus all forms of money are financial instruments that can be created or destroyed by financial institutions (Lavoie, Citation2014; McLeay, Radia, & Thomas, Citation2014a; Schumpeter, Citation2014). Money creation is thus not constrained by savings, but only limited by the supply of credible lucrative ventures (in the prevailing context). In times of economic optimism with high returns on investment, banks expand lending, leading to growth and prosperity; in times of high perceived risk of default, financial institutions restrict lending, leading to economic recession. Thus GDP can increase in periods of optimism, high borrowing and investment, while it can slump in periods of pessimism, credit rationing and low confidence.

In line with those perspectives, equilibrium models take the premise that banks only play the role of intermediary between creditors and lenders, and that their role as money creators is neglected. Current non-equilibrium models, when they lack explicit representations of the financial sector, assume the allocation of finance ‘on demand’ by banks exogenously (i.e. how much money is created) according to how much investment is required. Notwithstanding the overwhelming role that money and finance play in driving low-carbon transitions, the modelling literature that provides a satisfactory representation of such monetary elements is extremely scarce.

3. Results: implications of model choice for climate-related policy-making and macro-economic effects

3.1. Model outcomes and policy implications by model type

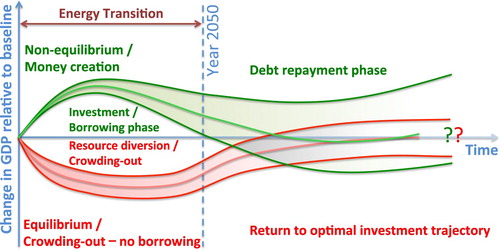

We present our key result and message in , based on work using state-of-the-art models from both sides of the theoretical spectrum. In the case of equilibrium models (red curves), with crowding-out of investment, an investment-intensive energy transition displaces resources that would have been used more productively elsewhere in the economy, leading to a sub-optimal equilibrium at lower GDP in the short run.Footnote12 As the transition completes itself and high carbon equipment becomes replaced by low-carbon technology, this displacement ceases and investment returns to normal (undistorted) purposes. In the long-run, with learning-by-doing, productivity increases, while lower operational expenses (e.g. fuel costs) may be incurred, and GDP recovers, or may even be improved above the baseline due to improved productivity and trade balance.

Figure 2. Illustration of GDP changes, relative to a baseline, of a policy-driven sustainability transition for the two groups of modelling schools of thought, equilibrium and non-equilibrium, in the current state-of-the-art. In this hypothetical example, a sustainability transition is financed (self-financed or via borrowing) from time zero until the vertical dashed line, after which low-carbon finance stops (figure co-designed by the authors). It is to be noted that for equilibrium models, recovery post-transition is strongly related to innovation processes such as productivity change, which mitigate the negative effects. However, even without representations of learning-by-doing and innovation, equilibrium models may still display a recovery post-transition due to processes such as reductions in fossil-fuel imports. Meanwhile, without representations of debt burdens, non-equilibrium models would not likely display a convergence post-transition.

We note that a reverse ‘crowding-out’ effect can also arise in equilibrium in cases where policy forces the shutdown of an economic sector (e.g. oil and gas during decarbonization). In the equilibrium case, this frees-up capital, which, with optimal allocation, increases the capital available for investment in other sectors, thereby compensating for the output loss. Thus, the effect goes both ways.

In the case of non-equilibrium models without crowding-out (green curves), an investment-intensive energy transition programme is predicted to create additional employment and to boost GDP in the short to medium run, due to a boost in employment stemming from higher investment (which is not offset by the impact of higher interest rates since financing is assumed to be abundant). It is followed by a possible reduction in macro-economic gains or even decline in the long run as debts are paid back, depending on debt servicing conditions. This is due to money being created by banks for investment in the early phase, which funds construction and results in activity across the economy, but also increases the debt burden, which remains in the longer term. For similar reasons as in equilibrium models, long-lasting productivity increases typically remain in the long run, following cumulative investments in better technology and equipment. These can offset the burden of debt repayment.

The ‘reverse crowding-out’ effect observed in equilibrium models also does not occur in non-equilibrium models. In the latter, losses of market share in particular sectors means that related capital and investment opportunities are truly lost and not replaced, leading to job and income losses despite the aggregate possible positive impact of investment-led growth in other sectors. This means that rapid structural change instead leads to stranded capital, for example stranded fossil fuel assets (Mercure et al., Citation2018b), which do not arise in equilibrium models.

This explains why models of different classes exhibit essentially opposite outcomes for the macroeconomics of an energy sustainability transition (i.e. GDP and employment). Uncertainty also behaves differently: in equilibrium, due to the use of optimization, uncertainty of solutions is linearly related to the uncertainty in parameters, as it primarily represents the gradient of the optimization function in the vicinity of the optimal point. In contrast, non-equilibrium models are strongly path-dependent. This means that uncertainty on parameters accumulates over simulation time, as path-dependence generates alternate scenarios that diverge from each other, differing minimally in the short run but becoming significantly different in the long run. As such, model outcomes in the far future are more uncertain than those in the near future.Footnote13 This property is standard for complex systems, and arises for example strongly in climate models.

3.2. Is a convergence of models possible?

To move beyond conceptual arguments about different economic paradigms and the models that result, the authors have worked together in enhancing two models based on these different fundamental perspectives – equilibrium (GEM-E3)Footnote14 and non-equilibrium (E3ME,Footnote15 see the SM for details on both models) – and focused on how to represent the crucial processes of innovation and finance applied to climate change mitigation. The collaboration was facilitated by the fact that both models already had an advanced treatment of induced innovation, and have been given similar parameterization inputs. We focus here on the representation of finance, which we argue is the more fundamental reason for persistent differences in the magnitude and direction of model results.

These two models make explicit the mark-up faced by borrowers over a ‘benchmark’ interest rate, where the mark-up is intended to capture the risks that are specific to the project / industry sector / country. One such risk is the capacity of borrowers to service additional debt, and the models construct estimates of the existing debt carried by each industry (or other institutional sector) based on the history of previous investment and assumptions for how that investment was financed. The models differ in their determination of the benchmark interest rate, reflecting their respective origins in the equilibrium (GEM-E3-FIT) and non-equilibrium (E3ME-FTT) traditions.

In both models, the developments allow financial constraints to be explored explicitly in scenarios. For example, a scenario of rapid decarbonization in power generation would be associated with a higher rate of investment and a higher level of debt carried by the firms undertaking the investment. This will have the effect of making the power generation sector a riskier prospect for lenders, reflected in a higher cost of capital and a higher price ultimately passed through to consumers. This can be mitigated by policy, for example through some form of public underwriting of the higher risk (transferring the risk, and the cost to taxpayers).

In summary, in equilibrium models, the factor limiting the total amount of borrowing is the interest rate, which clears the market. In non-equilibrium theory, credit-worthiness is what ultimately determines the confidence of banks to invest.

Based on a comparison of preliminary results from the models E3ME-FTT and GEM-E3-FIT, incorporating the developments described above, the two models appear to converge in their outcomes. As discussions and debates intensify regarding investment levels required in the context of the low-carbon transition (IPCC, Citation2018a; McCollum et al., Citation2018b), it is possible that improving the representations of money and finance in both model types could bring much needed coherence and clarity in the macroeconomic messages conveyed to energy and climate policy makers.

3.3. Clarifying the purpose of models: normative or positive?

The use or not of an optimizing representative agent or social planner construct, as a model representation of human populations, raises questions as to the nature, purpose and methodology of models deployed in climate policy making, which appear to be confused: are they normative (identifying best configurations or strategies in order to make recommendations, i.e. what agents ought to do) or positive (describing observed reality, i.e. what agents are observed to do)? By definition, an economic allocation identified by systems optimization is the best possible allocation (under certain chosen criteria and constraints, and according to existing knowledge). The finding that an optimal resource allocation is not achieved due to frictions and market failures, ultimately reflects a normative philosophy of science. Meanwhile, allocations that are identified and described because they are considered likely to arise, whether good or bad, reflect a descriptive scientific approach. The science philosophy question debated here concerns what the research question is, whether agents are understood to behave in such a way that optimal outcomes are realized in scenarios, and whether those scenarios are in themselves recommendations or descriptions of reality. Unfortunately, there exists a deep lack of clarity in the position of modellers on that question in the field.

Scenarios calculated using normative optimization models are by definition ‘possible/plausible’, but they are not necessarily ‘likely’. Specifically, it is not possible to determine the likelihood of optimal scenarios occurring in reality, simply because, even if agents were inclined to contribute to an optimal economic allocation, they would have no way of finding out, individually, which strategies would make the correct contribution (Kirman, Citation1992). The degree of control and coordination necessary exceeds the capacity of law-makers. Naturally, what is analysed in optimization scenarios are the differences from the optimum, not the optimum itself, while in descriptive models, it is differences from current trajectory that are analysed. Thus, when dealing with optimal scenarios, the difference between the ‘baseline’ (no intervention) trajectory and an optimal situation (albeit with market failures) is sometimes blurred. If not treated carefully, the interpretation of optimization results could pre-determine the result, in that any market distortion of the baseline scenario would automatically lead, by construction, to a detrimental performance outcome, even though it corrects market failures (for instance, its impact on GDP).

Furthermore, a danger exists in interpreting the results of optimization models – inherently normative – in a descriptive philosophy. For example, cost-optimization and pure representative agent equilibrium models offer the attractive but potentially misleading suggestion that pricing policies are the best way to correct market failures such as climate change, since agents, when assumed to behave optimally, always find the best possible use of resources according to prices. Indeed, many such models equate ‘marginal/social cost of carbon’ (what the models produce from a constraint or externality) with ‘carbon price’ (the assumed policy instrument). However, policy practice has shown that pricing is usually not the only policy lever to be known to work: while pricing policies do offer incentives to correct market failures, their likelihood of achieving actual normative objectives is not as clear as basic equilibrium theory would suggest.Footnote16 Finding out whether carbon pricing is likely to reach its stated objective requires studying how agents take decisions, including how they take account of such incentives (Knobloch & Mercure, Citation2016). The distinction between normative and descriptive approaches to science is not frequently identified, but it is crucial if one is to understand the meaning of model results. Ultimately, the danger lies in the interpretation of model results in terms of causality between intervention and outcome.

The normative/descriptive paradigms are reflected in model behaviour. In optimization-based models, allocations at each point in time modelled are in equilibrium steady states, and thus only change when exogenous variables change, as for example, population, regulations, trade agreements, the price of carbon, technology costs or taxation. The converse is that configurations do not change unless an external parameter changes (e.g. the price of an internalized externality). This has the result that, for climate change mitigation, additional emissions abatement only takes place when the (shadow) price of carbon increases.Footnote17 Low-carbon technology diffusion stops if the (real) price of carbon or other incentives becomes constant.Footnote18 In the scenario database of the IPCC’s Fifth Assessment Report (AR5), this leads some models to report very high carbon prices, up to $10,000/tCO2 or more (IPCC, Citation2014a, Citation2018b), that are required to abate the last remaining sources of emissions in the marginal abatement cost curve. However, in a largely decarbonized world, as carbon markets decline in relevance, and older socio-technical and industrial systems based on fossil fuels are abandoned and replaced by newer innovative low-carbon systems, it is not clear how, in reality, the carbon price would behave (Vogt-Schilb, Meunier, & Hallegatte, Citation2018).

In a non-equilibrium perspective, model states typically evolve without end even if the policy context does not change, in part pre-conditioned by their history, momentum and inertia. Thus, technological change does not solely take place when relative prices change, but instead, happens continuously, since the methodology does not involve searching for a steady state. In this paradigm, taxes create incentives to re-orient an ever-changing system towards a new course.Footnote19 Indeed, the system may be permanently altered and the policies which drove the transition to a new path may then become either embedded, or redundant (or possibly both). Unchanging but significant policies are not in this case equivalent to zero incentive.

This difference in model behaviour matches a divide within the policy sphere as well. The world of climate policy is divided along two lines of thought. On the one hand, in the equilibrium paradigm, policy-makers see carbon pricing as a tool for re-allocating scarce funds to fix a market failure, climate change, focusing on the marginal abatement cost and social cost of carbon. As a result, it is generally argued that linking or merging carbon markets increases market efficiency.

In the non-equilibrium perspective, energy and climate policy-makers see the carbon price as a signal instrument to incentivise faster economy-wide innovation and low-carbon technological change. The experienced and expected future price of carbon must be sufficiently high to communicate the current and future value of the low-carbon investment to firms (including R&D), but it is not the only policy available. Regulation can play an important role, allowing a lower carbon tax, using for instance technology or sectoral policies, including both ‘push’, and ‘pull’ policies such as the combination of R&D, feed-in tariffs and regulatory changes which have driven the revolution in renewable energy technologies. It is then argued that different national innovation systems, facing different contexts, are likely to require different magnitudes of incentives (e.g. what creates an incentive for R&D, innovation and investment in China is not the same as in Germany), and thus carbon markets should not necessarily be linked internationally to accelerate decarbonization.

4. Discussion and policy implications

Innovation is one of the determining factors in the long run costs of climate change mitigation, a finding that may also be relevant for other major structural economic transformation processes. Climate policies that stimulate innovation have a plausible prospect of yielding economic benefits, but are also as likely to generate economic challenges. In fact, climate policies may well be found to generate both at the same time (for instance, see Mercure et al., Citation2018b), depending on sectors and regions, the net effect depending on contextual policy design and mode of implementation.

Climate and energy policy assessment often involves the use of large complex multi-sectoral computational economic, energy technology and environmental models, to carry out quantitative analysis. However, innovation, and the financing requirements of capital-intensive systems transformations, remains generally not well represented in models deployed for informing climate and low-carbon energy innovation policy planning. Furthermore, long-run models that do not explicitly include endogenous innovation have a higher chance of yielding potentially erroneous results which could become quickly outdated (notably technology costs).

The outcomes of these models are tied to their assumptions and theoretical underpinnings. In order to overcome the much-referenced ‘black-box’ critique, it is therefore crucial to lay out these assumptions and theoretical details in a way that makes understanding the results as easy as possible. Since estimates of economic impacts of policies tend to have an important impact on the political economy of climate policy, greater attention to the theories, empirics and modelling of finance is required, in both equilibrium and non-equilibrium types of models. This paper contributes towards this effort of improving the transparency of sophisticated model mechanisms and the drivers of their outcomes, when applied in assessing climate and energy policy impacts.

Depending on the model choice, model results imply that the structural characteristic of the climate change mitigation problem may or may not be one of burden-sharing to deliver a global public good. Instead, they could rather point towards the challenge of crafting smart domestic policies combined with international mechanisms for accelerating low-carbon technology and policy diffusion, and for reducing the cost of capital by cementing policy commitments in international agreements. Ultimately, with further development, models may over time depart from the standard framing of climate policy as a prisoner’s dilemma, replacing it by another type of game with rules based on the consequences of financing low-carbon innovation and structural change.

The observed differences between the models in their treatment of innovation, money and finance reflect the lack of consensus among economists and social scientists. While both approaches are theoretically rigorous and self-consistent, it is important for policy-makers to have some insight into this state of conflicting knowledge. It needs to be recognized by both the policy and modelling communities that this schism exists, that representations are incomplete, and therefore that further research is critically needed in order to further our ability to effectively inform climate policy-making. Otherwise, model types can be chosen solely according to whether their results support or not particular political platforms. In this context, it is reasonable to make the recommendation that, in the interests of transparency for policy-makers and researchers, all modelling studies should state clearly their underpinning theoretical school and their treatment of finance and innovation, whether they use learning-curves, or represent finance explicitly, something not usually currently done.

Finally, and most importantly, it emerges from our study that developing representations of the monetary and financial sectors is crucial in models used for studying the economic impacts of energy system transformations and emissions reductions. Model differences completely hinge on whether crowding-out of financial resources takes place or not, which thus needs empirical verification. In addition to this, improving representations of behavioural features in agent decision-making (e.g. technology adoption, bank lending) can improve the accuracy of models to assess the effectiveness of proposed policies. It is thus imperative that in existing science-policy interfaces, in which policy-makers routinely commission modelling studies, strong incentives are given to modellers to improve their representations of money and finance. We argue that this is critical in order to clarify model outcomes with respect to policy proposals, and attempt to reduce model uncertainty, the robustness of results, and spur a conciliatory methodological dialogue.

Our explanation of the theoretical and methodological origins of model differences can help policy-makers and policy-analysts understand what broad mechanisms the models have and have not taken into account when interpreting the results of empirical policy analyses. Our analysis may also help shape the future direction of research and development in theory and models that are used for the analysis of energy and climate policies. Our analysis could in fact be generalized to the macroeconomic impacts of any type of technological transition (notably, the on-going transition towards automation and artificial intelligence). We trust that the knowledge reviewed here can help not only build a new research agenda, but also, shape the direction of enquiry in climate policy assessment.

Supplemental Material

Download MS Word (1.1 MB)Acknowledgement

The original study was published by the European Commission (more details are available at the link http://ec.europa.eu/energy/en/data-analysis/energy-modelling). J.-F.M. and F.K. conducted the analysis and wrote the text, with support from H.P., L.P., R.L. and S.S. R. L. coordinated the project, with S.S. The authors thank J. Canton from the European Commission for guidance, T. Barker, M. Grubb, and J. Köhler for their role as peer reviewers for the European Commission study, and S. Sharpe (UK BEIS) for informative discussions.

Disclosure statement

No potential conflict of interest was reported by the authors.

ORCID

Jean-Francois Mercure http://orcid.org/0000-0003-2620-9200

S. Serban Scrieciu http://orcid.org/0000-0003-1709-9708

Additional information

Funding

Notes

1. See, for instance, the several macro-modelling studies commissioned by the Directorate-General for Climate Action or the Directorate-General for Energy at the European Commission that have fed into the impact assessments underpinning their 2020, 2030 and 2050 EU climate and energy strategies. E.g. see http://ec.europa.eu/clima/policies/strategies/2020/studies_en.htm and http://ec.europa.eu/clima/policies/strategies/2030/documentation_en.htm

2. See Rogelj, McCollum, Reisinger, Meinshausen, & Riahi, (Citation2013); Clarke et al., (Citation2014); Kriegler et al., (Citation2015a); Kriegler et al., (Citation2015b); McCollum et al., (Citation2018b) for recent engineering estimates of mitigation costs/investment.

3. Schumpeter’s telling representation of innovation has resurfaced in various forms throughout modern economics, for example in Endogenous Growth Theory (Aghion et al., Citation1998), Evolutionary Economics (Freeman & Louçã, Citation2001), Sustainability Transitions Theory (Geels, Citation2002), Energy Technology Innovation Systems (Hekkert et al., Citation2007; Grubler & Wilson, Citation2013), directed clean innovation (Acemoglu, Citation2002; Acemoglu et al., Citation2012), and ‘planetary economics’ (Grubb et al., Citation2014).

4. This reflects a standard assumption in textbook models. Contemporary equilibrium theory can allow for partial employment, market imperfections, oligopolisitic competition (Dixon & Jorgenson, Citation2013).

5. We note the distinction between saving (the action of not spending a fraction of income) and savings (a certain amount of accumulated wealth). Here we use the verb saving, which implies a yearly flow of income not spent on consumption.

6. For instance, Goodwin's (Citation1982) model could be classified as Marxian although it uses some optimal conditions to yield a closed-form.

7. We avoid the orthodox/heterodox terminology as it is applied to too many issues in economics (values, methods, traditions and ideology) and is thus insufficiently precise for our purposes, and it is only used by a small subset of practitioners. We use the equilibrium/non-equilibrium, optimisation/simulation and the demand-led/supply-led terminologies to refer to, respectively, the theoretical, methodological and flow of information aspects.

8. Note that DSGE models do attempt to integrate uncertainty to macroeconomic modelling (Christiano, Eichenbaum, & Trabandt, Citation2018). However, the uncertainty addressed is that which concerns the modeller’s knowledge, not the modelled agent’s knowledge and expectations, since the rational expectations assumption prevents systematic errors in agent predictions, making the predictions of agents the same as the model’s itself, on average. DSGE models possess the constraints discussed in this paper in the ‘equilibrium’ sections (see also Pesaran & Smith, Citation1995).

9. A backstop technology is a hypothetical future technology that, assuming the consumer is willing to pay a high enough price, could provide infinite amounts of clean energy (e.g. solar photovoltaic or nuclear fusion).

10. Jorgenson and Wilcoxen (Citation1993) found, using a CGE model, that the oil price shocks of the 70’ suppressed total factor productivity growth temporarily. This result, however, is fully dependent on the assumption of crowding-out discussed below, as the dynamics involve changes in savings, originating from changes in consumption, that are forced by model construction to generate equal changes in investment. Without crowding-out, lower (higher) consumption would not be directly linked to higher (lower) investment.

11. ETC/ITC generates difficulties when introduced in optimisation algorithms, and therefore, it is known that such features, although available, are sometimes (or potentially often) switched off in order for modellers to improve model stability and/or reduce computational time (as inferred from our private communications with modellers). Thus, while nearly all model descriptions and papers claim or have claimed representations of learning curves, it is currently not possible to know when they are used and when not.

12. Unless, for instance, if the baseline initially included distortions that were then removed in a mitigation scenario.

13. Lower apparent uncertainty bounds in equilibrium models should not be understood as better treatment of real-world uncertainty, but rather, as the uncertainty that can be represented in optimisation algorithms, which are not strongly path-dependent. I.e. increasing uncertainty bounds stem from path-dependence. Path-dependence is typically generated by processes with increasing returns such as learning-by-doing, diffusion dynamics etc (Arthur, Ermoliev, & Kaniovski, Citation1987; Arthur, Citation1989; Gritsevskyi & Nakićenovic, Citation2000).

14. GEM-E3-FIT: General Equilibrium Model for Energy Economy & Environment with Financial and Technical progress modules.

15. E3ME-FTT: Energy-Economy-Environment Macro-Econometric model with Future Technology Transformations.

16. Notably, most optimisation models assume and require the application of a carbon price to all sources of carbon emissions, including those in which other policy instruments are currently used and for which no plans currently exist in most countries to use emissions trading or carbon taxes (e.g. personal mobility, household heating, agriculture). The assumed effectiveness of a carbon price to reduce emissions in consumer-based sectors is at best conjectural, and not informed by extensive behavioural research.

17. With the exception of policy instruments involving setting standards which optimisation models reflect by reducing the menu of technological choices, eliminating those polluting technologies that do not meet the standards imposed. In this case emission reductions can still occur as a response to setting standards without changes in the carbon price.

18. In models without non-convexities, technology composition is a unique function of the carbon price.

19. Diffusion is not a simple function of the carbon price or other incentives: increasing the carbon price does not always incentivise the same number of agents deciding to purchase a particular durable good; it depends on history. But also, due to inertia in diffusion, an unchanging (real) carbon price/tax signal can sustain low-carbon technology diffusion.

Related Research Data

References

- Acemoglu, D. (2002). Directed technical change. The Review of Economic Studies, 69(4), 781–809.

- Acemoglu, D., Aghion, P., Bursztyn, L., & Hemous, D. (2012). The environment and directed technical change. American Economic Review, 102(1), 131–166.

- Aghion, P., Howitt, P., Brant-Collett, M., & García-Peñalosa, C. (1998). Endogenous growth theory. Cambridge: MIT press.

- Anthoff, D., & Tol, R. S. J. (2014). Climate framework for uncertianty, negotiation and distribution.

- Arrow, K. (1962). Economic welfare and the allocation of resources for invention. In The rate and direction of inventive activity: Economic and social factors (pp. 609–626). Princeton, NJ: Princeton Legacy Press.

- Arthur, W. B. (1989). Competing technologies, increasing returns, and lock-in by historical events. The Economic Journal, 99(394), 116–131.

- Arthur, W. B., Ermoliev, Y. M., & Kaniovski, Y. M. (1987). Path-dependent processes and the emergence of macro-structure. European Journal of Operational Research, 30(3), 294–303.

- Baccianti, C., & Löschel, A. (2014). The role of product and process innovation in CGE models of environmental policy. WWWforEurope Working Paper

- Bank of England. (2015). The impact of climate change on the UK insurance sector.

- Battiston, S., Farmer, J. D., Flache, A., Garlaschelli, D., Haldane, A. G., Heesterbeek, H., … Scheffer, M. (2016). Complexity theory and financial regulation. Science, 351(6275), 818–819.

- Battiston, S., Mandel, A., Monasterolo, I., Schütze, F., & Visentin, G. (2017). A climate stress-test of the financial system. Nature Climate Change, 7(4), 283–288.

- BIS. (2011). Innovation and research strategy for growth. UK Department for Business, Innovation and Skills.

- Bouwman, A. F., Kram and, T., et al. (2006). ). Integrated modelling of global environmental change. An overview of IMAGE 2.4.

- Bovari, E., Giraud, G., & Mc Isaac, F. (2018). Coping with collapse: A stock-flow consistent monetary macrodynamics of global warming. Ecological Economics, 147, 383–398.

- Cambridge Econometrics. (2013). Employment effects of selected scenarios from the energy roadmap 2050. Cambridge Econometrics.

- Cambridge Econometrics. (2015). Assessing the employment and social impact of energy efficiency. Cambridge Econometrics.

- Campiglio, E., Dafermos, Y., Monnin, P., Ryan-Collins, J., Schotten, G., & Tanaka, M. (2018). Climate change challenges for central banks and financial regulators. Nature Climate Change, 8(6), 462–468.

- Capros, P., Paroussos, L., Fragkos, P., Tsani, S., Boitier, B., Wagner, F., … Bollen, J. (2014). Description of models and scenarios used to assess European decarbonisation pathways. Energy Strategy Reviews, 2(3-4), 220–230.

- Carbon Trust. (2005). The UK climate change programme: Potential evolution for business and the public sector. London: Carbon Trust.

- Carney, M. (2015). Breaking the tragedy of the horizon—climate change and financial stability. Bank of England.

- Christiano, L. J., Eichenbaum, M. S., & Trabandt, M. (2018). On DSGE models. Journal of Economic Perspectives, 32(3), 113–140.

- CIRED. (2018). The IMACLIM model. Retrieved from http://www2.centre-cired.fr/Recherches/Methodes-et-outils/Modelisation-prospective/article/Prospective-modeling?lang=en

- Clarke, L., Jiang, K., Akimoto, K., Babiker, M., Blanford, G., Fisher-Vanden, K., … Löschel, A. (2014). Chapter 6: Assessing transformation pathways, in climate change 2017. Working Group III, Fifth Assessment Report of the Intergovernmental Panel on Climate Change.

- Clarke, L., Weyant, J., & Edmonds, J. (2008). On the sources of technological change: What do the models assume? Energy Economics, 30(2), 409–424.

- Dafermos, Y., Nikolaidi, M., & Galanis, G. (2017). A stock-flow-fund ecological macroeconomic model. Ecological Economics, 131, 191–207.

- DG ECFIN. (2015). The QUEST III model.

- Dixon, P. B., & Jorgenson, D. W. (2013). Handbook of computable general equilibrium modeling. Oxford: Newnes.

- Domencich, T. A., & McFadden, D. (1975). Urban travel demand-a behavioral analysis.

- E3MLab. (2018a). The GEM-E3 model. Retrieved from http://www.e3mlab.eu/e3mlab/index.php?option=com_content&view=category&id=36%3Agem-e3&Itemid=71&layout=default&lang=en

- E3MLab. (2018b). The PRIMES model. Retrieved from http://www.e3mlab.eu/e3mlab/index.php?option=com_content&view=category&id=35%3Aprimes&Itemid=80&layout=default&lang=en

- Edenhofer, O., Kemfert, C., Lessmann, K., Grubb, M., & Koehler, J. (2006). Technological change: Exploring its implicaton for the economics of stabilisation. Insights from the Innovation Modelling Comparison Project. Endogenous Technological Change and the Economics of Atmospheric Stabilisation. The Energy Journal Special 35.

- Edenhofer, O., Knopf, B., Barker, T., Baumstark, L., Bellevrat, E., Chateau, B., … Kypreos, S. (2010). The economics of low stabilization: Model comparison of mitigation strategies and costs. The Energy Journal, 31(1), 11–48.

- European Commission. (2017). The economic rationale for public R&I funding and its impact. European Commission.

- Fontana, G. (2008). Money, uncertainty and time. Abingdon: Routledge.

- Freeman, C., & Louçã, F. (2001). As time goes by: From the industrial revolutions to the information revolution. Oxford: Oxford University Press.

- GEA. (2012). Global energy assessment—toward a sustainable future. Cambridge: Cambridge University Press and the International Institute for Applied Systems Analysis.

- Geels, F. W. (2002). Technological transitions as evolutionary reconfiguration processes: A multi-level perspective and a case-study. Research Policy, 31(8), 1257–1274.

- Gillingham, K., Newell, R. G., & Pizer, W. A. (2008). Modeling endogenous technological change for climate policy analysis. Energy Economics, 30(6), 2734–2753.

- Giraud, G., Mc Isaac, F., Bovari, E., & Zatsepina, E. (2016). Coping with the collapse: A stock-flow consistent monetary macrodynamics of global warming.

- Goodwin, R. M. (1982). A growth cycle. In Essays in economic dynamics (pp. 165–170). London: Palgrave Macmillan.

- Goulder, L. H., Hafstead, M. A., & Williams III, R. C. (2016). General equilibrium impacts of a federal clean energy standard. American Economic Journal: Economic Policy, 8(2), 186–218.

- Goulder, L. H., & Schneider, S. H. (1999). Induced technological change and the attractiveness of CO2 abatement policies. Resource and Energy Economics, 21(3-4), 211–253.

- Gritsevskyi, A., & Nakićenovic, N. (2000). Modeling uncertainty of induced technological change. Energy Policy, 28(13), 907–921.

- Grubb, M., Bashmakov, I., Drummond, P., Myshak, A., Hughes, N., Biancardi, A., … Lowe, R. (2018). An exploration of energy cost, ranges, limits and adjustment process. UCL Institute for Sustainable Resources. Retrieved from http://discovery.ucl.ac.uk/10047775/1/An%20exploration%20of%20energy%20cost%2C%20ranges%2C%20limits%20and%20adjustment%20process.pdf

- Grubb, M., Carraro, C., & Schellnhuber, J. (2006). Endogenous technological change and the economics of Atmospheric Stabilisation. The Energy Journal, 27(1), 1–16.

- Grubb, M., Edmonds, J., Ten Brink, P., & Morrison, M. (1993). The costs of limiting fossil-fuel CO2 emissions: A survey and analysis. Annual Review of Energy and the Environment, 18(1), 397–478.

- Grubb, M., Hourcade, J.-C., & Neuhoff, K. (2014). Planetary economics. Abingdon: Routledge.

- Grubb, M., Köhler, J., & Anderson, D. (2002). Induced technical change in energy and environmental modeling: Analytic approaches and policy implications. Annual Review of Energy and the Environment, 27(1), 271–308.

- Grubler, A., & Wilson, C. (2013). Energy technology innovation. Cambridge: Cambridge University Press.

- Guttmann, R. (2016). Finance-led capitalism: Shadow banking, re-regulation, and the future of global markets. London: Palgrave Macmillan.

- Haldane, A. G., & Turrell, A. E. (2018). An interdisciplinary model for macroeconomics. Oxford Review of Economic Policy, 34(1-2), 219–251.

- Hall, L. M., & Buckley, A. R. (2016). A review of energy systems models in the UK: Prevalent usage and categorisation. Applied Energy, 169, 607–628.

- Hekkert, M. P., Suurs, R. A., Negro, S. O., Kuhlmann, S., & Smits, R. E. (2007). Functions of innovation systems: A new approach for analysing technological change. Technological Forecasting and Social Change, 74(4), 413–432.

- Hicks, J. (1932). The theory of wages. London: Palgrave Macmillan.

- Holtz, G., Alkemade, F., de Haan, F., Köhler, J., Trutnevyte, E., Luthe, T., … Kwakkel, J. (2015). Prospects of modelling societal transitions: Position paper of an emerging community. Environmental Innovation and Societal Transitions, 17, 41–58.

- Hottenrott, H., & Rexhäuser, S. (2015). Policy-induced environmental technology and inventive efforts: Is there a crowding out? Industry and Innovation, 22(5), 375–401.

- IEA/ETSAP. (2016). The TIMES model.

- IIASA. (2014). The MESSAGE model.

- IPCC. (2014a). AR5 scenarios database.

- IPCC. (2014b). Mitigation of climate change. Contribution of Working group III to the Fifth assessment report of the Intergovernmental Panel on climate change. Cambridge: Cambridge University Press.

- IPCC. (2018a). Global warming of 1.5°C: An IPCC special report on the impacts of global warming of 1.5 °C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty. IPCC.

- IPCC. (2018b). SR15 scenarios database.

- Jorgenson, D. W., & Wilcoxen, P. J. (1993). Energy prices, productivity, and economic growth. Annual Review of Energy and the Environment, 18(1), 343–395.

- Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica: Journal of the Econometric Society, 47, 263–291.

- Keen, S. (1995). Finance and economic breakdown: Modeling minsky’s “financial instability hypothesis”. Journal of Post Keynesian Economics, 17(4), 607–635.

- Keynes, J. M. (1921). A treatise on probability courier corporation. London: Macmillan & Co.

- Keynes, J. M. (1936). General theory of employment, interest and money. London: Macmillan & Co.

- Kirman, A. P. (1992). Whom or what does the representative individual represent? The Journal of Economic Perspectives, 6(2), 117–136.

- Knobloch, F., & Mercure, J.-F. (2016). The behavioural aspect of green technology investments: A general positive model in the context of heterogeneous agents. Environmental Innovation and Societal Transitions, 21, 39–55.

- Köhler, J., Grubb, M., Popp, D., & Edenhofer, O. (2006). The transition to endogenous technical change in climate-economy models: A technical overview to the innovation modeling comparison project. The Energy Journal, 1, 17–55.

- Köhler, J., Whitmarsh, L., Nykvist, B., Schilperoord, M., Bergman, N., & Haxeltine, A. (2009). A transitions model for sustainable mobility. Ecological Economics, 68(12), 2985–2995.

- Kriegler, E., Petermann, N., Krey, V., Schwanitz, V. J., Luderer, G., Ashina, S., … Méjean, A. (2015a). Diagnostic indicators for integrated assessment models of climate policy. Technological Forecasting and Social Change, 90, 45–61.

- Kriegler, E., Riahi, K., Bauer, N., Schwanitz, V. J., Petermann, N., Bosetti, V., … Rao, S. (2015b). Making or breaking climate targets: The AMPERE study on staged accession scenarios for climate policy. Technological Forecasting and Social Change, 90, 24–44.

- Kriegler, E., Weyant, J. P., Blanford, G. J., Krey, V., Clarke, L., Edmonds, J., … Richels, R. (2014). The role of technology for achieving climate policy objectives: Overview of the EMF 27 study on global technology and climate policy strategies. Climatic Change, 123(3-4), 353–367.

- Lamperti, F., Dosi, G., Napoletano, M., Roventini, A., & Sapio, A. (2018). Faraway, so close: Coupled climate and economic dynamics in an agent-based integrated assessment model. Ecological Economics, 150, 315–339.

- Lavoie, M. (2014). Post-Keynesian economics: New foundations. Cheltenham: Edward Elgar Publishing.

- Li, F. G., & Strachan, N. (2017). Modelling energy transitions for climate targets under landscape and actor inertia. Environmental Innovation and Societal Transitions, 24, 106–129.

- Li, F. G., Trutnevyte, E., & Strachan, N. (2015). A review of socio-technical energy transition (STET) models. Technological Forecasting and Social Change, 100, 290–305.

- Löschel, A. (2002). Technological change in economic models of environmental policy: A survey. Ecological Economics, 43(2-3), 105–126.

- Lutz, C., Meyer, B., & Wolter, M. I. (2009). The global multisector/multicountry 3-E model GINFORS. A description of the model and a baseline forecast for global energy demand and CO2 emissions. International Journal of Global Environmental Issues, 10(1-2), 25–45.

- Mazzucato, M. (2011). The entrepreneurial state. Soundings, 49(49), 131–142.

- Mazzucato, M. (2018). The value of everything: Making and taking in the global economy. London: Penguin.

- Mazzucato, M., & Semieniuk, G. (2017). Public financing of innovation: New questions. Oxford Review of Economic Policy, 33(1), 24–48.

- Mazzucato, M., & Semieniuk, G. (2018). Financing renewable energy: Who is financing what and why it matters. Technological Forecasting and Social Change, 127, 8–22.

- McCollum, D. L., Wilson, C., Bevione, M., Carrara, S., Edelenbosch, O. Y., Emmerling, J., … Krey, V. (2018a). Interaction of consumer preferences and climate policies in the global transition to low-carbon vehicles. Nature Energy, 3(8), 664–673.

- McCollum, D. L., Wilson, C., Pettifor, H., Ramea, K., Krey, V., Riahi, K., … Fujisawa, S. (2017). Improving the behavioral realism of global integrated assessment models: An application to consumers’ vehicle choices. Transportation Research Part D: Transport and Environment, 55, 322–342.

- McCollum, D. L., Zhou, W., Bertram, C., de Boer, H.-S., Bosetti, V., Busch, S., … Fay, M. (2018b). Energy investment needs for fulfilling the Paris agreement and achieving the sustainable development goals. Nature Energy, 3(7), 589.

- McGlade, C., & Ekins, P. (2015). The geographical distribution of fossil fuels unused when limiting global warming to 2°C. Nature, 517(7533), 187–190.

- McLeay, M., Radia, A., & Thomas, R. (2014a). Money creation in the modern economy.

- McLeay, M., Radia, A., & Thomas, R. (2014b). Money in the modern economy: An introduction.

- Mercure, J., Knobloch, F., Pollitt, H., Lewney, R., Rademakers, K., Eichler, L., … Paroussos, L. (2016a). Policy-induced energy technological innovation and finance for low-carbon economic growth. Study on the macroeconomics of energy and climate policies.

- Mercure, J.-F., Pollitt, H., Bassi, A. M., Viñuales, J. E., & Edwards, N. R. (2016b). Modelling complex systems of heterogeneous agents to better design sustainability transitions policy. Global Environmental Change, 37, 102–115.

- Mercure, J.-F., Pollitt, H., Chewpreecha, U., Salas, P., Foley, A. M., Holden, P. B., & Edwards, N. R. (2014). The dynamics of technology diffusion and the impacts of climate policy instruments in the decarbonisation of the global electricity sector. Energy Policy, 73, 686–700.

- Mercure, J.-F., Pollitt, H., Edwards, N. R., Holden, P. B., & Vinuales, J. E. (2018a). Environmental impact assessment for climate change policy with the simulation-based integrated assessment model E3ME-FTT-GENIE. Energy Strategy Reviews, 20, 195–208. doi: 10.1016/j.esr.2018.03.003

- Mercure, J.-F., Pollitt, H., Sognnaes, I. B., Lam, A., Salas, P., Holden, P. B., … Viñuales, J. E. (2018b). Macroeconomic impact of stranded fossil fuel assets. Nature Climate Change, 8, 588–593. doi: 10.1038/s41558-018-0182-1

- Minsky, H. P. (1986). Stabilizing an unstable economy. New York, NY: McGraw Hill.

- Monasterolo, I., & Raberto, M. (2018). The EIRIN flow-of-funds behavioural model of green fiscal policies and green sovereign bonds. Ecological Economics, 144, 228–243.

- NIES. (2012). Asia-pacific integrated model.

- Nordhaus, W. (2013). The DICE-2013R Model.

- Nordhaus, W. (2015). Climate clubs: Overcoming free-riding in international climate policy. American Economic Review, 105(4), 1339–1370.

- Nordhaus, W. D. (1973). Some skeptical thoughts on the theory of induced innovation. The Quarterly Journal of Economics, 87, 208–219.

- Nordhaus, W. D. (2010). Economic aspects of global warming in a post-Copenhagen environment. Proceedings of the National Academy of Sciences, 107(26), 11721–11726.

- Nordhaus, W. D. (2014). The perils of the learning model for modeling endogenous technological change. The Energy Journal, 35(1), 1–13.

- Nordhaus, W. D. (2017). Revisiting the social cost of carbon. Proceedings of the National Academy of Sciences, 114(7), 1518–1523.

- OECD. (2015). System innovation: Synthesis report. OECD.

- Pesaran, M. H., & Smith, R. (1995). The role of theory in econometrics. Journal of Econometrics, 67(1), 61–79.

- Pettifor, H., Wilson, C., McCollum, D., & Edelenbosch, O. (2017). Modelling social influence and cultural variation in global low-carbon vehicle transitions. Global Environmental Change, 47, 76–87.

- PIK. (2016). The REMIND model.

- PNNL. (2017). The GCAM Model.