ABSTRACT

Policy makers in a number of nations are currently developing carbon capture and storage (CCS) as an industrial decarbonisation solution, linking capture potential in industry clusters to domestic or overseas offshore storage capacity. However, the design, focus and timeframe for policy support are proving challenging in countries like the UK, where industry actors are concerned about the competitiveness implications of additional operational capital costs, while government aims to offer only transitory policy support. Policy-facing research is required to understand the drivers, nature and extent of potential competitiveness loss from adopting carbon capture in specific industry and country contexts, along with the impacts of policy decisions in other countries and of possible future technology improvements. We consider the case of the UK chemicals industry, using an economy-wide computable general equilibrium (CGE) model. This highlights how macroeconomic and sectoral impacts of concern under regional, industry and climate policy agendas depend on domestic and export demand responses to changing industry prices. A crucial question is whether capture costs are similarly reflected in international prices. We identify a risk of policy commitment to ‘polluter pays’ having sustained negative outcomes for capture firms, along with offshoring/leakage of jobs and GDP, and associated emissions, as demand shifts to lower cost overseas production. However, such costs could be reduced, and some capture industry gains realised, if competitors in other nations ultimately follow in bearing similar costs and particularly if ‘early mover’ action enables firms to make efficiency gains and build comparative advantage in operational carbon capture.

Key policy insights

A ‘polluter pays’ approach to industrial carbon capture risks triggering potential ‘offshoring’ of manufacturing activity in all timeframes where increased operational costs reduce the relative competitiveness of capture firms.

A border tax risks worse industry and wider economy outcomes, where domestic production is intensive in imports of the commodity in question.

Transitory policy support should focus on enabling capture firms to build efficiency in using carbon capture equipment while sustaining competitiveness and jobs within regional industry clusters.

Opportunities should be explored to develop comparative advantage where policy activity involves ‘early mover’ action on carbon capture.

1. Introduction

In 2019, the UK was the first G7 nation to legislate for a 2050 ‘net zero carbon’ target for territorial greenhouse gas (GHG) emissions (UK Legislation, Citation2019).Footnote1 The Climate Change Committee (CCC, Citation2019, Citation2020) has advised on a range of areas where deep emissions reductions are required. This includes the particularly challenging area of industrial decarbonisation, where the UK is currently deploying carbon capture and storage (CCS), linking capture potential in regional manufacturing clusters with off-shore storage capacity (BEIS, Citation2018, Citation2021a, Citation2021b). CCS is an interesting case with potential wider lessons for other decarbonisation approaches that may involve substantial new capital/equipment requirements in both investment and operational stages, including where carbon capture may be involved in switching to low carbon fuels (e.g. ‘blue’ hydrogen).

However, as in most nations, the UK policy context is not solely a climate one. ‘Green growth’ – i.e. combining decarbonisation with continued economic growth – is a central element in the government's Industrial Strategy with a key role for CCS in reducing emissions while sustaining activity in regional manufacturing clusters (BEIS, Citation2017, Citation2018; HM Government, Citation2020; HM Treasury, Citation2021). Here, UK Government plans involve delivering one net zero and four low carbon regional clusters by 2030/2040 (BEIS, Citation2019), with significant policy action to date centred on supporting the deployment of CCS (BEIS, Citation2021b).

The challenge is complicated by the UK Government's apparent commitment to a new regional policy agenda, referred to politically as ‘levelling up’ (PMO, Citation2021), and linked commitments to the 2021 Just Transition Declaration signed at COP 26 in Glasgow, which focusses on the need for ‘green growth’ involving decent work and continued/growing economic prosperity with emphasis on sustainable work for people in local areas.Footnote2 Here, concern lies in sustaining industries that support substantial employment and income generation through complex regional and interregional supply chains, while introducing carbon capture costs that generate risks for industry competitiveness. Risks are exacerbated where the UK is an ‘early mover’ in CCS; the UK Government (HM Treasury, Citation2021, p. 85) stated its intention to become ‘a world-leader in technology to capture and store harmful emissions away from the atmosphere’ prior to the launch of CCS policy action, mainly focussed on developing transport and storage capacity, later the same year (BEIS, Citation2021b). Reducing these risks will involve industry being able to exploit 'early mover' status to build comparative advantage in operational capture.

In short, the UK has become an early and vigorous promoter and adopter of CCS. In developing UK business models for CCS, the UK Government (BEIS, Citation2020) recognises the challenges to industry competitiveness from engaging in capture activity which, at the very least, will require firms to install and operate additional capital equipment to produce the same level of output, thereby affecting capital efficiency.Footnote3 A time-limited subsidy regime has been proposed in the form of an ‘Industrial Capture Contract’ (ICC) (BEIS, Citation2020, p. 58), aiming to offset capture-driven price increases until it becomes a ‘competitive solution’. However, the conditions for subsidy implementation, evolution and ultimate withdrawal are not yet clear.

We aim to inform the policy discourse through a better understanding of differences in how the position of UK production sectors in domestic and international markets can influence the potential economy-wide impacts of introducing carbon capture as a decarbonisation solution. Our analysis focusses not only on whether carbon capture can become a competitive solution, but also the importance of industry having the ability to exploit 'early mover' status to develop comparative advantage. We explore the outcomes of the UK unilaterally introducing carbon capture and how said outcomes are affected by capture costs being reflected in international prices, with and without the presence of first mover advantages for UK industries, or if the UK Government employs mechanisms to bridge the prices of domestic and imported goods of specific industries. We build on an economy-wide computable general equilibrium (CGE) approach developed Turner et al. (Citation2021), focussing on the UK chemicals industry as an example of a heavily traded industry servicing both domestic and complex international supply chains, where the capital efficiency implications of operating additional carbon capture equipment trigger competitiveness challenges.

Beyond the specific case of the UK, the type of questions and issues we address here contribute to the broader literature focussing on investigating and understanding the economy-wide implications of carbon policies and overlapping regulations (see for example Böhringer et al., Citation2016; Corradini et al., Citation2018; Delarue & Van den Bergh, Citation2016; Wu et al., Citation2020). We address a key gap around the limited discussion and evidence on cases like carbon capture that involve operational capital/equipment requirements, and where this is the source of international competitiveness challenges that generate tensions between domestic and international climate policy ambitions, priorities, and regulations.

2. Model

We employ UKENVI, a multi-sector economy-wide computable general equilibrium (CGE) model of the UK, calibrated on a social accounting matrix (SAM) incorporating the 2016 UK input-output, IO tables (the most recent analytical IO data published by the Office for National Statistics, ONS).Footnote4 We treat these data as reflecting the real economy in the effective policy base year of 2021. We aggregate to 34 broader industries producing 34 commodity outputs (see our SAM database for details – in Section 4 elucidates sector typesFootnote5). This includes the single ‘chemical’ industry identified in the UK IO. Here we provide a brief overview of the most relevant characteristics and assumptions of the UKENVI model (detailed in Katris & Turner, Citation2021).

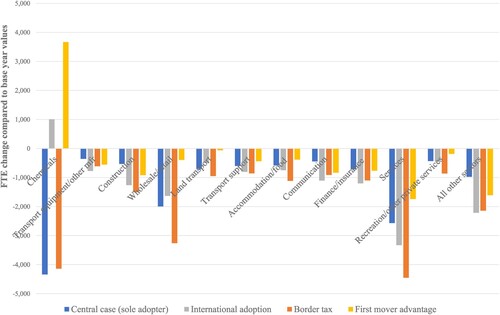

Figure 1. 2050 changes (relative to 2016 base year) in sectoral employment – comparing across cases as to how capital efficiency losses associated with carbon capture uptake are reflected in international prices.

2.1. Production

Each sector produces output at minimum costs using a nested production function (of a constant elasticity of substitution, CES, form). Each industry combines imported and domestically produced commodities (governed by an Armington, Citation1969, function). Energy commodities combine through various levels of an energy nest, then with non-energy intermediate commodities. The composite (produced) intermediate good then combines with a value-added combination of labour and capital to produce total output (Alabi et al., Citation2020, illustrate). Within the value-added nest, an efficiency parameter on the use of capital is the key element within the UK chemicals industry in introducing the capital efficiency shock associated with carbon capture (where more capital is required to produce a given level of output).

2.2. Labour market

The labour force (sum of employed and unemployed workers) is fixed over time.Footnote6 We do not model skills or sector-specific competencies, so we assume perfect mobility between sectors. The real take-home wage is determined by an econometrically parameterized bargaining function, with power shifting between firms and workers depending on changes in the unemployment rate (Blanchflower and Oswald, Citation2009). Long-run conditions do not require that labour demand matches labour supply, with a pool of unemployed labour from the outset. Thus, there can be long-run overall job gains or losses.

2.3. Savings and investment

Domestic savings rates are given as an exogenous share of household income. Investment is forward-looking, depending on exogenous depreciation and interest rates, set in extra-regional markets, and quadratic adjustment costs. Thus, in each sector, the actual capital stock gradually adjusts to its desired level, which is a function of sectoral output and relative input prices. Specifically, we follow Hayashi’s (Citation1982) treatment of investment, meaning that producers anticipate demands and prices across all timeframes, determining the optimal investment pattern to maximize the value of the firms. In the long-run, equilibrium gross investment in each sector just covers depreciation.

2.4. Trade

UK exports to an exogenous rest of the world (ROW) region are sensitive to changes in relative domestic and foreign prices. Domestically produced commodities and foreign imports are also assumed to be imperfect substitutes. In both production and consumption, this is specified through an Armington (Citation1969) assumption governing substitution between domestic production and imports for each commodity identified. The initial price of foreign commodities effectively gives the model numeraire, and this price is fixed in all timeframes in our central case scenarios. Our scenarios focus on introducing exogenous shocks to the price of foreign chemicals in imports and exports, but we also provide sensitivity analyses around trade elasticity values.

2.5. Household consumption

Household expenditure is determined after deducting taxes and savings from household income (assuming a fixed savings rate). In our scenarios, the key drivers of changes in household real incomes and purchasing power are earnings from employment and taxes paid to government. Note that household income also includes income from capital from firms, linked to the other value-added generated and transfers from government, which are fixed in real terms with nominal values adjusted for changes in the consumer price index (CPI). Households consume goods and services from each of the sectors in the model using a nested consumption function (i.e. in a similar manner to that in production) and are, therefore, sensitive to relative price changes between domestic outputs and imports.

2.6. Government

Government demand for goods and services is fixed in nominal terms, with real expenditures adjusting to economy-wide price changes. The public budget is determined by a range of endogenous revenue sources and does not need to balance in the scenarios modelled here, allowing accumulation of public surpluses or deficits to inform wider fiscal modelling of decarbonisation actions.

3. Simulation strategy

UK CCS policy prioritises decarbonising the nation's regional industrial clusters. We study the collective UK chemicals industry as a dominant presence in several of these clusters: Grangemouth in Scotland; and Runcorn, Teeside and Humberside in North England, where these English sites are the focus of the current ‘Phase 1’ CCS roll-out, focussed on transport and storage capacity – see BEIS (Citation2021b). Crucially, there are significant downstream links between the UK chemicals industry and other UK sectors, such as ‘Rubber/plastic’ and ‘Construction’, meaning that any impacts on the price of chemicals will spill across the entire economy, given that approximately 68% of the intermediate use of chemicals is covered by the UK chemicals industry (and 32% is imported). Here, we focus specifically on the capture element of CCS, where UK policy is still being formulated (see also BEIS, Citation2020).

We assume a single ‘end-of-pipe’ technology treatment of CCS as adopted in studies such as Li et al. (Citation2017) and Thepkun et al. (Citation2013), so that carbon capture introduces increased equipment requirements to produce a given level of output. Building on Turner et al.'s (Citation2021) Scottish CGE work, and informed by engagement with UK chemical industry actors, we impose a 30% capital efficiency reduction in the chemicals sector, introduced evenly over a 10-year period.Footnote7 We compare all results to the 2016 SAM database values, which are taken to represent the real economy if nothing else changes. This allows us to isolate and understand the impacts of introducing carbon capture without the additional complexity of how any other potential changes – such as projected economic growth, changes in technology or other policy interventions – may impact outcomes. Moreover, we do not consider any other CCS costs here, such as any fees associated with using transport and storage services, the provision and use of which raise separate policy issues (BEIS, Citation2020). Assuming that the introduction of CCS removes all of the sector's emissions (10,956 kilotonnes in the base year), then the direct impact on total UK CO2 emissions will be a reduction of 4.1%.

While the UK plans to encourage the initial adoption of CCS via a (as yet loosely defined) subsidy known as an ‘Industrial Capture Contract’ (BEIS, Citation2020, p. 58), the clear intention is to move to a ‘polluter pays’ scenario over the mid-to-long term. However, competitiveness impacts and risks of offshoring both production and associated carbon will remain a central concern if the timeframes for any policy support provided do not focus on ensuring capture firms can compete on a level international playing field. This could involve tailoring support to enable efficiency and/or expertise to build in operational capture. This may be a key route to exploring 'early mover' status in developing comparative advantage. Thus, we build out a ‘polluter pays’ case under different assumptions regarding the relative international situation and report sectoral and economy-wide outcomes with focus on key mid-century (2050) timeframes.

In our central case, we assume the UK chemicals industry is a sole adopter to investigate the nature of impacts driven by competitiveness loss triggered by reduced capital efficiency in the domestic chemicals industry. Here, we follow Turner et al. (Citation2021) in assuming that all Armington import and export price elasticities both equal to 2 in all sectors (consistent with previous UK CGE studies – e.g. Turner, Citation2009; Lecca et al., Citation2014). Given the importance of trade responses in governing the extent of competitiveness loss associated with any given price increase – where the UK chemicals industry exports 41% of its output in the base year – we draw on systematic sensitivity analysis varying the trade elasticities that directly govern the international competitiveness loss of the UK chemicals industry.

We then develop three basic scenarios considering how long-run outcomes may change if the relative international situation were to shift. First, we consider how industry and macroeconomic outcomes may change if competing overseas chemicals prices change in line with the long-run price increase that we observe for the UK chemicals industry in our central case. We then consider a case that represents a price adjustment regime, such as a ‘border tax adjustment’ that involves exogenously imposing a price increase on imports of foreign chemicals that matches the cumulative, or price multiplier, impact of efficiency loss in the UK sector (6.9%). Finally, we consider the impacts of the UK chemicals industry potentially gaining a first mover advantage in global chemicals production with capture through technological leadership (Lieberman & Montgomery, Citation1998). This manifests in the form of a smaller, yet illustrative, capital efficiency reduction (15% rather than 30%, where later movers experience the latter) where (as in other scenarios), UK chemicals reach the 15% capital efficiency reduction, in equal increments, over a 10-year period.

4. Results

4.1. Central/default case

The second and third data columns of report the key macroeconomic and chemicals industry impacts of the 30% reduction in capital efficiency in the chemicals sector using the central case/default values for all parameters. We report results for 2030 and 2050 as significant timeframes for UK policy: the government's aim is to have operationalised four main regional CCS clusters by 2030 and to have reached net zero by 2050 (HM Treasury, Citation2021; UK Legislation, Citation2019). In modelling terms, during the first 10 periods (taken to be years) to 2030 the constantly falling chemical industry capital efficiency replicates the gradual introduction of CCS. By 2050 (30 periods) the model is very close to its new long-run equilibrium.

Table 1. Percentage changes (relative to 2016 baseline) in key macroeconomic and industry indicators following the introduction of carbon capture – central and alternative cases regarding how associated capital effiency losses are reflected in international prices (all with default trade elasticities).

In both timeframes, there is a negative impact on aggregate economic activity as measured by GDP, total employment and household expenditure. This is unsurprising given that carbon capture increases the cost requirements of the chemicals sector. This triggers a substantial reduction in the competitiveness of the chemicals sector as its output price increases, by 5.02% in 2030 (completion of industry-wide capture uptake). Over time, as its capital stock increases, the industry price adjusts. By 2050 it reaches a sustained 4.38% increase, which causes chemicals exports to fall and imports to rise, by 8.21% and 5.47% respectively. This is accompanied by chemical sector output and employment reductions of 6.03% and 4.79%. Using the base year figures in the first data column, the employment change equates to a reduction of 4,337 full time equivalent (FTE) jobs. Chemical industry investment rises by 22.16%, but this is set against the 30% gross increase in investment required to fully offset the efficiency loss at constant output.

Negative upstream supply chain impacts interact with the overall CPI effects of increased production costs in chemicals and its downstream supply chain to trigger an economy-wide contraction. The consequence is a final 0.12% GDP reduction or just over £2 billion of which over £1 billion is in the chemicals industry. Emissions will fall in all sectors that contract, including the chemicals industry, so that less than the initial 10,956 kilotonnes will be captured. However, imports of chemicals and other goods and services rise, and this offshoring involves carbon leakage that will increase emissions overseas. The economic contraction also reduces UK Government revenue from taxation, while increasing the total government spending: government spending is fixed in real terms so must adjust for the CPI increase. The net outcome is to increase the government budget deficit by £0.59 billion per annum by 2050.

Moreover, the GDP reduction is associated with a 0.05% contraction in total employment (14,248 UK jobs, 4,337 in the chemical industry). The first case (bar) in shows the distribution of employment losses across all sectors in this central case. Here, our assumption that real wage adjustment takes place in an imperfectly competitive labour market means that, in the absence of any driver of expansion/increased labour demand elsewhere in the economy, those who lose their jobs become unemployed (with the unemployment rate rising by 0.86% by 2030 and 0.92% by 2050). That is, despite some downward adjustment in the real wage, this is not sufficient to maintain the pre-shock employment rate.

The only sectors that grow/gain employment are those where government spending is concentrated, where real expenditure has to rise to maintain per capital spending as nominal prices increase (reflected in the CPI, which rises by 0.05% by 2050). The decrease in employment is a key driver (alongside other factors, such as the increase in the cost of living given by the CPI) with a 0.05% drop in total UK (real) household consumption (£651million), which drives losses particularly in service sectors. The only component of GDP that rises is investment, where this is focussed on replacing less productive capital stock.

The central case results reflect the findings of Turner et al. (Citation2021); the ‘polluter pays’ outcomes suggest that, in the case of carbon capture, the UK Government should not expect to deliver decarbonisation without policy design involving a wider perspective on mitigating industry and wider economy costs. Here, the jobs and GDP losses reported in and are in fact directly or indirectly associated with offshoring of production to meet continued consumption demands both at home and abroad. This is clearly not consistent with UK regional and economic policy objectives, the sustainability of local employment opportunities emphasised in the UK's commitment to the 2021 Just Transition Declaration, or the spirit of global climate change agreements.

Specifically, emissions reduction through carbon capture in UK chemicals is accompanied by offshoring of some of the nation's consumption/use of chemicals, together with associated jobs and incomes, which triggers further losses across the economy. Similarly, an industrial strategy based on sustaining growth in currently emissions intensive industries is ill-served by a sector that declines with the introduction of carbon capture.

4.2. Sensitivity of central case results to varying parameters governing the trade response

However, the size of these negative sectoral impacts of the ‘polluter pays’ simulations depends on key parameters of the model and what we assume about the price of foreign chemicals. Taking the former first, there is currently a real paucity of appropriate data to inform specification of trade elasticities in CGE models (though key insights are provided in studies such as Bajzik et al., Citation2020; Clements et al., Citation2021; Feenstra et al., Citation2018). Thus, we consider how results are impacted across a range of values for import and export elasticities, with focus on those applying to the chemical industry, specifically imports of chemicals and UK chemicals industry exports, value-added and employment. Discussion of full sensitivity results is provided in the Supplementary Materials. Here, several key observations can be made.

First, no combination of trade parameters totally mitigates the fall in UK chemical exports driven by adoption of carbon capture as modelled here, though these would be reduced from more than 8% in to around 2% or less if the export price response were inelastic (i.e. demand falling less than proportionately relative to the price rise). However, (as discussed in Section 5) current evidence (e.g. European Commission, Citation2018) suggests that the UK chemical industry is more vulnerable to relatively price-sensitive export demand.

Second, greater export price elasticities magnify the negative impact of the associated competitiveness loss in domestic production, with the 8.21% loss in chemical industry exports growing by 50% to around 12% if we increase the assumed export elasticity proportionately. On the other hand, if the import elasticity on chemicals were higher, export losses may be reduced to some extent (up to 1% under our central assumption regarding export elasticities). This is simply because the UK chemicals sector is itself a heavy user of chemicals as intermediate inputs, some of which are supplied from abroad. Thus, while it does constitute some extent of offshoring, the impact of increase in the price of UK chemicals on industry competitiveness, reflected in the reduction in export demand, would be moderated to some (albeit limited) extent if (lower cost) imports from overseas competitors were regarded as more acceptable substitutes.

Third, while the negative impact on the sector’s value-added under the default parameters (−9.64% in ) is proportionately larger than the corresponding trade figures, this figure is less responsive to changes in the trade elasticities but remains negative in all cases.

Fourth, employment outcomes, which are perhaps of greatest political concern (or, at least, public visibility), particularly in the context of regional policy and ‘just transition’ agendas, are determined by what happens to chemical industry value-added (which drives the derived demand for labour) and increased labour intensity in response to capital efficiency loss. Our sensitivity analysis reflects this, with the reduction in chemical industry employment tracking but always being smaller than changes in value-added outcomes as trade responses increase or decrease.

4.3. Reflecting capture costs in international prices

To this point, we have simulated the impact of the introduction of carbon capture in the chemicals sector assuming that the UK is, at least initially, the sole adopter. However, if other countries are committed to deep decarbonisation in chemicals production, they may follow in introducing carbon capture with the same sort of cost implications. Referring again to , the final three columns report results for the 2050 timeframe for three additional scenarios where alternative assumptions are made about the behaviour of other countries, the UK Government and future technology.

The reference results are the standard long-run ‘polluter pays’ figures for 2050 in the third data column of (Scenario 1). In the fourth data column we increase the foreign price of chemicals by 6.9% (Scenario 2). This matches the price increase in the UK. Implicitly we are assuming that the rest of the world has adopted CCS. In data column five we report the result of the UK imposing a border tax on chemicals that solely increases the cost of chemical imports by 6.9% (Scenario 3). Then, in the final column, we present the outcome of other countries introducing CCS, with a price penalty of 6.9% (as in Scenario 2) but with the UK having a lower, 15%, capital efficiency reduction as a result of learning by doing and an early adopter status (Scenario 4).

Where all countries adopt carbon capture, so that the foreign price of chemicals also increases by 6.9% (Scenario 2) we see that the adverse effects on UK chemicals exports are removed. Now the reduction in industry exports is marginal (−0.02%), reflecting domestic price pressures.Footnote8 There is still a small reduction in output (0.88%), but this now comes from reduced domestic demand given the price increase (which, in our single national model, captures domestic drivers not reflected in external prices). However, despite the 0.05% rise in the nominal wage, substitution in favour of labour as the effective cost of capital increases is sufficient to bring about a marginal (1.11%, 1,008 jobs) increase in sectoral employment. The impact on aggregate economic activity is only to mitigate macroeconomic losses very slightly, with GDP still falling by −0.10% and total UK employment by −0.04%/13,018 jobs.

However, note (from ) that there is a mixed picture as to whether employment losses increase or decrease, given the greater increase in the CPI set against a smaller reduction in real household spending (given the more limited total employment loss) and total export demand. Nonetheless, the pure supply-side efficiency aspects of capture clearly still dominate in the aggregate impacts.

Where industries in other countries fail to adopt CCS, a border tax could be introduced, levelling the playing field for domestic producers in the UK market (Scenario 3). In this case, the chemical import price is increased by 6.9% but the price of foreign chemicals in UK export markets is held constant. This has a counterintuitive impact on the output of UK chemicals when compared to the reference simulation (Scenario 1). In Scenario 1 chemical output falls by −6.03%; with the imposition of a border tax, the corresponding reduction is even higher at −6.48%.

This shows the key role that imported chemicals play as intermediate inputs in the UK domestic production of chemicals, reflecting the importance of international supply chain activity in this industry. Raising chemical import prices means that Scenario 1 change in domestic chemicals price increases from 4.38% in Scenario 1 to 6.86% in Scenario 3. This makes UK chemicals even more uncompetitive in foreign markets, with chemical exports now 12.42% lower than the base year value. This further loss of competitiveness in export markets more than outweighs any advantage in the domestic market. However, impacts on chemicals employment and value-added (decreasing by −4.58% and −9.45% respectively in Scenario 3) are less negative than the corresponding Scenario 1 values (−4.79% and −9.64%). This is for two reasons: first, because of some substitution away from intermediates towards value-added; and second, due to a greater decrease in the nominal wage (−0.08% compared to −0.06%).

However, the impact of the border tax on most other sectors (see for employment) is negative so that the 0.15% decline in GDP is over 30% greater than in Scenario 1 (−0.12%), with total UK exports falling by 0.45%. This has a further negative impact on all measures of aggregate activity: investment, employment, real wages and household expenditure, while it exacerbates the budget deficit, which is now almost £1 billion.

Finally, we report results from a simulation in which other countries adopt carbon capture, but the UK, as an early adopter, has an advantage. In this case, we assume that the price of foreign chemicals reflects the 30% increase in capital requirements for CCS but that the UK has benefitted from a learning curve and has reduced the capital efficiency loss to 15%. In this case, there is a positive stimulus to the chemicals sector whose output and employment increase by 2.79% and 4.05% respectively, driven by a 5.17% increase in exports as UK chemicals are now price competitive in foreign markets with the 4.24% price increase for UK chemicals below the 6.9% increase in the price of foreign chemicals.

Although the chemicals sector expands, with a gain of 3,665 FTE jobs, the rest of the economy still shows a slight overall contraction, with a total net loss of 4,216 jobs, albeit with the ‘comparative advantage’ being the ‘least worst’ outcome for employment in most sectors (see final bar in ). Basically, increased domestic and imported chemical prices drive the CPI up by 0.11%, reducing the competitiveness in the whole economy. While there is a 0.01% increase in household consumption generated by increased capital incomes, the 0.05% drop in exports leads to small contractions in GDP (−0.03%/£488 million), employment (0.01%/4,216 jobs) and real earnings, whereas the government budget deficit is restricted to approximately £0.30 billion (from £0.59 billion in our central case).

Moving early in carbon capture to secure comparative advantage, thus, acts to mitigate sustained losses in clustered chemical industry activity. This potentially reduces the tension between adopting a ‘polluter pays’ model and regional ‘levelling up’ concerns and improves ‘just transition’ outcomes in terms of the sustainability of work for people in local areas/regional economies. It also provides perhaps the most useful and effective focus and motivation for time-limited public policy support of industry capture. While the outcome is still one characterised by the absence of any wider expansionary driver, and net economy job losses do exceed regional industry gains, regional industry outcomes are more likely to bring alignment across regional, industry and climate policy concerns.

5. Discussion

Our applied example is the UK chemicals industry, a currently emissions-intensive activity with heavy presence across the UK's regional industry clusters, where there is clearly policy focus on sustaining industry and supply chain jobs via CCS (BEIS, Citation2018). The additional operational capital costs involved in adopting carbon capture under ‘polluter pays’ causes increased output prices in capture firms. Our results suggest that this drives negative impacts on activity and employment for the chemicals industry, primarily driven by offshoring, triggering a process of contraction across the wider economy associated with reduced demands and higher consumption prices and consequent impacts on real income generation.

Our sensitivity analysis demonstrates that the extent of industry offshoring will be exacerbated by a more price-sensitive domestic and overseas trade response to competitiveness loss in UK chemicals. Such outcomes are problematic for a government wishing to take a leading role in pursuing mid-century ‘net zero’ goals, where offshoring of emissions intensive activities may reduce territorial emissions, but not necessarily the global emissions that drive climate change. Moreover, leakage of jobs, investment and emissions is not consistent with the UK Industry Strategy or linked Industrial Decarbonisation Strategy (BEIS, Citation2017, Citation2021a), where the current UK approach to regional policy focusses on the very regions where the currently emissions-intensive industry clusters are located (PMO, Citation2021). Crucially, such competitiveness challenges are not limited to the UK: the success of global net zero (and ‘just transition’) commitments depend on individual nations both decarbonising at home and limiting emissions embedded in trade flows.

Going forward, our sensitivity analysis implies that determining the specific nature and magnitude of potential losses at industry and wider economy levels requires understanding of what the trade elasticities underpinning import and export demand responses are actually likely to be, and how these may evolve over time. Such knowledge will be crucial in determining appropriate levels of policy support, for example, through the proposed UK Industrial Capture Contract (BEIS, Citation2020), and how this should adjust over time.

However, while the UK Government, like many others around the world, utilises CGE methods in applied policy analyses presented (e.g. see HMRC/HMT, Citation2014), there is a real paucity of econometric data to inform the specification of trade elasticities.Footnote9 On the other hand, consideration of systematic sensitivity analysis outcomes such as summarised here (and expanded in the Supplementary Materials) can usefully be set in the context of discussion and consideration of those factors which drive higher trade elasticities – such as whether firms sell ‘process outputs’ into complex global supply chains – together with policy intelligence on sectors at most risk from carbon leakage (European Commission, Citation2018; Welsch, Citation2008). Chemicals is an example identified in both cases. Generally, different price elasticities can be used to reflect varying international market conditions for chemicals. The question is whether final consumers would be prepared to pay a premium price for ‘green products’, which would suggest a new product differentiation and lower elasticities where more costly inputs are involved in supply chains. In the current context, this would imply that lower elasticities may represent widespread international adoption of carbon capture and/or developed markets for ‘green products’. On the other hand, higher elasticities represent conditions where this is not the case and the UK industry, as an early mover is, thus, more exposed to competitiveness loss in selling ‘process’ outputs into global supply chains where competitors are not bearing similar costs.

We have also highlighted a crucial issue in terms of the extent to which the notion of ‘carbon markets’ fully accounts for both explicit and implicit carbon prices. Ultimately, the former will largely be determined by the UK's post-Brexit approach to carbon pricing (HMT, Citation2021). The latter is likely to depend on issues such as the geographic and temporal adoption of zero carbon legislation. This will be reflected in the increasing cost of production in nations where competing industry/supply chain activities are located, due to their internalisation of carbon cost and/or the deployment and uptake of carbon capture (even as a transitory solution). Moreover, the challenge is made more complex where competitors in currently emissions-intensive sectors such as chemicals production are located not only in close trading blocks such as the EU, but increasingly on the Asian continent in particular.

Here we have focussed, in the context of our single nation CGE model, on some initial treatments of how carbon capture with homogenous costs impacts may be reflected across international chemical industry markets. While simplistic (with quantitative outcomes dependent on the applied scenarios for the current production and output structure of the UK chemicals industry), our analysis provides some useful initial insights. For example, there is extensive discussion in the literature regarding the potential role of ‘border carbon adjustment’ mechanisms – such as that now agreed by the Council of the European UnionFootnote10 – aimed at reducing carbon embedded in trade flows and enabling individual nations to internalise carbon costs (see, for example, Branger & Quirion, Citation2014; Dissou & Eyland, Citation2011; Droege, Citation2011; Evans et al., Citation2021; Monjon & Quirion, Citation2011). However, our scenario involving the introduction of a tax on imports of chemicals to the UK to offset the price impacts of domestic capture costs leads to the worst outcomes for the home industry and economy due to the complex direct and indirect (supply chain) chemicals import intensity of UK production and consumption.

We note that it is important to stress that our simulations have been constructed on the assumption of a given technology where carbon capture is judged to involve a 30% reduction in capital efficiency in production, introduced to a production function that reflects current substitution possibilities between inputs. Off-line experimentations have demonstrated that there may not be much impact on outcomes from production technologies becoming flexible (e.g. greater substitutability of labour for capital). On the other hand, our simulations have taken a first step in demonstrating that any technical progress that increases the efficiency (reduces the inefficiency) of capture equipment could give the UK a competitive advantage, potentially enabling domestic capture industries to grow while limiting the wider economy costs of higher production and consumption prices.

6. Conclusions

Our simulations involve introducing carbon capture in the UK chemicals industry, where this imposes capital efficiency losses under a ‘polluter pays’ funding approach. The results show that the economic outcomes, both for the whole economy and the chemicals sector itself, depend on interaction between price sensitivity of trade in chemicals, the policy reaction of other countries and future technology possibilities.

One fundamental insight is that the relative industry competitiveness impacts of carbon capture depend crucially on the actual price sensitivity of domestic and export demands. On the one hand, the relevant elasticities are highly contested in the literature, with the implication that scenario simulation analyses cannot precisely inform policy analysis such as those that will be required in designing the proposed UK Industrial Capture Contract over different timeframes and under different conditions. On the other hand, the outcomes of systematic sensitivity analyses in future research could be very useful in considering the potential industry and wider economy implications of successful policy actions to reduce trade sensitivities. This will be particularly the case if future development of economy-wide scenario simulations can further extend to consider issues such as supporting ‘green market’ development and/or ‘levelling playing fields’ through border carbon adjustments and/or promoting international adoption of tested carbon capture approaches.

In this regard, an important contribution of this paper has been to establish what some of the key drivers of industry and wider economy impacts may be, if international prices reflect policy interventions to offset changes in relative prices associated with uptake of a costly decarbonisation approach such as carbon capture, or if competitors in other nations follow suit in uptake. Moreover, in focussing on capital efficiency challenges, insights drawn will be relevant in other industrial decarbonisation contexts, both in the UK and elsewhere, such as fuel switching; this will potentially initially involve the decarbonisation of natural gas prior to fuel use (which larger firms, for example in the chemicals industry, may do on site, thus similarly requiring carbon capture in production processes).

Crucially, we identified that outcomes may be considerably improved if capture industries can be supported in ‘learning by doing’ to increase efficiency in the operation of carbon capture equipment (or reduce wider capital efficiency losses associated with increased equipment needs). Such focus may be the best one for the type of transitory public support that policy decision makers, including those in the UK, are ideally aiming for in designing competitive ‘polluter pays’ approaches going forward.

More generally, a key contribution of this paper is to establish several important research needs to support policy development, within the UK and beyond, if climate policy actions involving additional costs in production activities are to deliver outcomes that are consistent both with (domestic and international) climate ambitions, and with national development goals (cutting across industrial strategies and internal ‘levelling up’, which link to the UK's commitment to international ‘just transition’ agendas, with focus on the sustainability of local employment). These needs extend from further developing economy-wide simulation frameworks to cope with more comprehensive scenarios (e.g. around evolving economic conditions and policy actions, evolution of carbon prices, and fuller costs of CCS), to ensuring analytical tools are effectively informed by econometric and other statistical evidence.

Supplemental Material

Download MS Word (75.7 KB)Acknowledgements

We are grateful to members of the UK Chemical Industries Association for input informing industry scenarios.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The model used in this study is calibrated using a 2016 UK Social Accounting Matrix (SAM), publicly available at: https://doi.org/10.15129/ad64a94c-152d-4ec7-a3a5-4e4a13576a3a.

Additional information

Funding

Notes

1 ‘Net zero’ is the central political response to the 1.5°C warming target of the 2015 COP21 Paris Agreement (UNFCCC, Citation2015), recommitted via the COP26 Glasgow Pact (UNFCCC, Citation2021).

2 See the UNFCCC Just Transition Declaration and list of signatories at https://ukcop26.org/supporting-the-conditions-for-a-just-transition-internationally/.

3 The challenge is not limited to simply investing in capture equipment, as studies that recommend investment subsidies as an appropriate mechanism to incentivise participation in CCS systems often suggest, e.g. Groenenberg and Coninck (Citation2008).

4 The UK analytical input-output tables can be accessed at https://www.ons.gov.uk/economy/nationalaccounts/supplyandusetables/datasets/ukinputoutputanalyticaltablesindustrybyindustry.

5 The SAM database is available at https://doi.org/10.15129/ad64a94c-152d-4ec7-a3a5-4e4a13576a3a.

6 The base level of the unemployment rate is 5%, in line with ONS data.

7 Note that the Turner et al. (Citation2021) analysis assumes a greater, 50%, reduction in capital efficiency associated with carbon capture. This is associated with the generally older state of production capital in the Scottish element of the UK chemicals industry, where new equipment needs rather than retrofits for carbon capture may be required.

8 This is an effect that reflects our national model setting, not the exogenously imposed import price.

9 Challenges relate to mapping/detail of industry sectors (Alexeeva-Talebi et al., Citation2012) and inconsistency of trade specifications (Dixon et al., Citation2016) across econometric and CGE datasets.

10 See the May 2022 press release of the Council of the European Union (2022) at https://www.consilium.europa.eu/en/press/press-releases/2022/03/15/carbon-border-adjustment-mechanism-cbam-council-agrees-its-negotiating-mandate/

References

- Alabi, O., Turner, K., Figus, G., Katris, A., & Calvillo, C. (2020). Can spending to upgrade electricity networks to support electric vehicles (EVs) roll-outs unlock value in the wider economy? Energy Policy, 138, 111–117. https://doi.org/10.1016/j.enpol.2019.111117

- Alexeeva-Talebi, V., Böhringer, C., Löschel, A., & Voigt, S. (2012). The value-added of sectoral disaggregation: Implications on competitive consequences of climate change policies. Energy Economics, 34(2), S127–S142. https://doi.org/10.1016/j.eneco.2012.10.001

- Armington, P S. (1969). A theory of demand for products distinguished by place of production. Staff Papers - International Monetary Fund, 16, 159–178.

- Bajzik, J., Havranek, T., Irsova, Z., & Schwarz, J. (2020). Estimating the Armington elasticity: The importance of study design and publication bias. Journal of International Economics, 127, 103383. https://doi.org/10.1016/j.jinteco.2020.103383

- Blanchflower, D. G., & Oswald, A. J. (2009). The wage curve. Europe. Revue Litteraire Mensuelle, 92, 215–235.

- Böhringer, C., Keller, A., Bortolamedi, M., & Seyffarth, A. R. (2016). Good things do not always come in threes: On the excess cost of overlapping regulation in EU climate policy. Energy Policy, 94, 502–508. https://doi.org/10.1016/j.enpol.2015.12.034

- Branger, F., & Quirion, P. (2014). Would border carbon adjustments prevent carbon leakage and heavy industry competitiveness losses? Insights from a meta-analysis of recent economic studies. Ecological Economics, 99, 29–39. https://doi.org/10.1016/j.ecolecon.2013.12.010

- Business Energy & Industrial Strategy (BEIS) (Department for). (2017). Industrial Strategy: Building a Britain fit for the future. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/664563/industrial-strategy-white-paper-web-ready-version.pdf

- Business Energy & Industrial Strategy (BEIS) (Department for). (2018). The UK carbon capture, usage and storage (CCUS) deployment pathway: An action plan. https://www.gov.uk/government/publications/the-uk-carbon-capture-usage-and-storage-ccus-deployment-pathway-an-action-plan

- Business Energy & Industrial Strategy (BEIS) (Department for). (2019). What is the Industrial Clusters Mission? https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/803086/industrial-clusters-mission-infographic-2019.pdf

- Business Energy & Industrial Strategy (BEIS) (Department for). (2020). An update on business models for carbon capture, usage and storage. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/946561/ccus-business-models-commercial-update.pdf

- Business Energy & Industrial Strategy (BEIS) (Department for). (2021a). Industrial decarbonisation strategy. https://www.gov.uk/government/publications/industrial-decarbonisation-strategy

- Business Energy & Industrial Strategy (BEIS) (Department for). (2021b). Cluster sequencing for carbon capture usage and storage deployment: Phase-1. https://www.gov.uk/government/publications/cluster-sequencing-for-carbon-capture-usage-and-storage-ccus-deployment-phase-1-expressions-of-interest

- Clements, K. W., Mariano, M. J. M., & Verikios, G. (2021). Foreign-domestic substitution, import penetration and CGE modelling. Applied Economics, 53(35), 4080–4099. https://doi.org/10.1080/00036846.2021.1897072

- Climate Change Committee (CCC). (2019). Net zero - The UK’s contribution to stopping global warming. https://www.theccc.org.uk/publication/net-zero-the-uks-contribution-to-stopping-global-warming/

- Climate Change Committee (CCC). (2020). Reducing UK emissions: 2020 Progress Report to Parliament. https://www.theccc.org.uk/publication/reducing-uk-emissions-2020-progress-report-to-parliament/

- Corradini, M., Costantini, V., Markandya, A., Paglialunga, E., & Sforna, G. (2018). A dynamic assessment of instrument interaction and timing alternatives in the EU low-carbon policy mix design. Energy Policy, 120, 73–84. https://doi.org/10.1016/j.enpol.2018.04.068

- Delarue, E., & Van den Bergh, K. (2016). Carbon mitigation in the electric power sector under cap-and-trade and renewables policies. Energy Policy, 92, 34–44. https://doi.org/10.1016/j.enpol.2016.01.028

- Dissou, Y., & Eyland, T. (2011). Carbon control policies, competitiveness, and border tax adjustments. Energy Economics, 33(3), 556–564. https://doi.org/10.1016/j.eneco.2011.01.003

- Dixon, P., Jerie, M., & Rimmer, M. (2016). Modern trade theory for CGE modelling: The Armington. Krugman and Melitz Models. Journal of Global Economic Analysis, 1(1), 1–110. https://doi.org/10.21642/JGEA.010101AF

- Droege, S. (2011). Using border measures to address carbon flows. Climate Policy, 11(5), 1191–1201. https://doi.org/10.21642/JGEA.010101AF

- European Commission. (2018). Preliminary Carbon Leakage List, 2021-2030. Official Journal of the European Union, C 162. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ:C:2018:162:FULL&from=EN

- Evans, S., Mehling, M. A., Ritz, R. A., & Sammon, P. (2021). Border carbon adjustments and industrial competitiveness in a European Green Deal. Climate Policy, 21(3), 307–317. DOI: 10.1080/14693062.2020.1856637

- Feenstra, R. C., Luck, P., Obstfeld, M., & Russ, K. N. (2018). In search of the Armington elasticity. Review of Economics and Statistics, 100(1), 135–150. https://doi.org/10.1162/REST_a_00696

- Groenenberg, H., & de Coninck, H. (2008). Effective EU and Member State policies for stimulating CCS. International Journal of Greenhouse Gas Control, 2(4), 653–664. https://doi.org/10.1016/j.ijggc.2008.04.003

- Hayashi, F. (1982). Tobin’s marginal q and average q: A neoclassical interpretation. Econometrica: Journal of the Econometric Society, 50(1), 213–224. https://doi.org/10.2307/1912538

- HM Government. (2020). The Ten Point Plan for a Green Industrial Revolution. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/936567/10_POINT_PLAN_BOOKLET.pdf

- HMRC/HMT. (2014). Analysis of the dynamic effects of fuel duty reductions. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/303233/Analysis_of_the_dynamic_effects_of_fuel_duty_reductions.pdf

- HM Treasury. (2021). Build back better: Our plan for growth, March 2021. https://www.gov.uk/government/publications/build-back-better-our-plan-for-growth

- Katris, A., & Turner, K. (2021). Can different approaches to funding household energy efficiency deliver on economic and social policy objectives? ECO and alternatives in the UK. Energy Policy, 155, 112375. https://doi.org/10.1016/j.enpol.2021.112375

- Lecca, P., Mcgregor, P. G., Swales, J. K., & Turner, K. (2014). The added value from a general equilibrium analysis of increased efficiency in household energy use. Ecological Economics, 100, 51–62.

- Li, W., Jia, Z., & Zhang, H. (2017). The impact of electric vehicles and CCS in the context of emission trading scheme in China: A CGE-based analysis. Energy, 119, 800–816. https://doi.org/10.1016/j.energy.2016.11.059

- Lieberman, M. B., & Montgomery, D. B. (1998). First-mover (dis) advantages: Retrospective and link with the resource-based view. Strategic Management Journal, 19(12), 1111–1125. https://doi.org/10.1002/(SICI)1097-0266(1998120)19:12%3C1111::AID-SMJ21%3E3.0.CO;2-W

- Monjon, S., & Quirion, P. (2011). A border adjustment for the EU ETS: Reconciling WTO rules and capacity to tackle carbon leakage. Climate Policy, 11(5), 1212–1225. https://doi.org/10.1080/14693062.2011.601907

- Prime Minister’s Office (PMO). (2021). The Queen’s speech 2021. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/986770/Queen_s_Speech_2021_-_Background_Briefing_Notes..pdf

- Thepkun, P., Limmeechokchai, B., Fujimori, S., Masui, T., & Shrestha, R. M. (2013). Thailand’s Low-carbon scenario 2050: The AIM/CGE analyses of CO2 mitigation measures. Energy Policy, 62, 561–572. https://doi.org/10.1016/j.enpol.2013.07.037

- Turner, K. (2009). Negative rebound and disinvestment effects in response to an improvement in energy efficiency in the UK economy. Energy Economics, 31(5), 648–666.

- Turner, K., Race, J., Alabi, O., Katris, A., & Swales, J. K. (2021). Policy options for funding carbon capture in regional industrial clusters: What are the impacts and trade-offs involved in compensating industry competitiveness loss? Ecological Economics, 184, 106978. https://doi.org/10.1016/j.ecolecon.2021.106978

- UK Legislation. (2019). UK Climate Change Act 2050 Amendment (2019). https://www.legislation.gov.uk/ukdsi/2019/9780111187654/pdfs/ukdsiem_9780111187654_en.pdf

- United Nations Framework Convention on Climate Change, UNFCCC. (2015). Paris Agreement. https://unfccc.int/sites/default/files/english_paris_agreement.pdf

- United Nations Framework Convention on Climate Change, UNFCCC. (2021). Glasgow Climate Pact. https://unfccc.int/sites/default/files/resource/cop26_auv_2f_cover_decision.pdf

- Welsch, H. (2008). Armington elasticities for energy policy modeling: Evidence from four European countries. Energy Economics, 30(5), 2252–2264. https://doi.org/10.1016/j.eneco.2007.07.007

- Wu, J., Fan, Y., Timilsina, G., Xia, Y., & Guo, R. (2020). Understanding the economic impact of interacting carbon pricing and renewable energy policy in China. Regional Environmental Change, 20(3), 1–11. https://doi.org/10.1007/s10113-020-01663-0