ABSTRACT

Formal deliberations for the new collective quantified goal on climate finance began at COP26 in Glasgow. This Perspectives article aims to inform this process by discussing the potential size and nature of is post-2025 target. We argue that the climate finance system around the current target to mobilise US$100 billion per year to support developing countries has been fraught with difficulties, and that it would be ineffective to simply increase the climate finance target without addressing these difficulties. Therefore, we identify and discuss five priority elements for negotiations: the relation to Article 2.1(c) of the Paris Agreement; the adaptation-mitigation balance; financial instruments; mobilising private finance; and ‘new and additional’ finance. To increase transparency, accountability, and trust in climate finance under the UNFCCC and to simultaneously allow for the mobilisation of finance at scale, we suggest setting a sub-target for grants. In combination with additional (sub)target(s), this could define an overall new collective quantified goal that is better suited to serve the challenging dual role of mobilising finance at scale and transferring resources to developing countries.

Key policy insights

Ambiguous definitions of climate finance and the US$100 billion target allow for multiple interpretations, reducing transparency and trust between countries.

Climate finance targets can be interpreted in a dual and sometimes contrasting way: mobilising investment at scale and transferring resources from developed to developing countries. Recognising this duality may help to find common ground for a post-2025 climate finance target.

Increasing the climate finance target may prove ineffective without further clarity on private finance mobilisation, the relation to Art. 2.1(c), and other priority elements.

More detailed assessments of needs, priorities, costs, and support are needed to inform the post-2025 target and assess climate finance provision effectiveness.

A sub-target for grants could increase accountability, trust, and transparency, and target the needs of the most vulnerable developing countries.

Negotiations on the post-2025 climate finance target could also consider additional aspects such as access to and prioritisation of finance, and loss and damage.

1. Setting climate finance targets

Climate finance has always been a central issue at the UN climate negotiations. The support to developing countries for mitigation (e.g. promoting renewable energy or low-carbon transport) and adaptation (e.g. making the agricultural and water sector climate resilient to physical climate impacts) is key to building and maintaining trust (Ciplet et al., Citation2015). Such financial support for climate action currently occupies the majority of public funding for implementing international environmental agreements (Pickering et al., Citation2017).

For all its failures, the 2009 UN climate conference in Copenhagen was a watershed moment for climate finance. For the first time, developed countries collectively pledged specific amounts of climate finance to support developing countries with climate change adaptation and mitigation activities, providing US$30 billion for the period 2010–2012 and mobilising US$100 billion annually by 2020 (UNFCCC, Citation2009). These numbers were confirmed in the Cancun Agreements in 2010 (UNFCCC, Citation2010), along with criteria that the US$100 billion needs to be ‘new and additional’, ‘balanced’ between mitigation and adaptation, and that the private sector would be considered a source of climate finance (Pauw, Citation2017).

Since the UN climate negotiations in Copenhagen, the scaling up, tracking, and accounting of climate finance flows towards the agreed US$100 billion per year have become a priority for many different institutions engaged in international climate policy (Iro, Citation2014; Bodnar et al., Citation2015), including provider and recipient countries, climate funds, civil society, and development banks and agencies (Pickering et al., Citation2017). In Paris in 2015, developed countries signalled their intention to continue this collective goal to mobilise climate finance through 2025, and to establish a new collective quantified goal from a floor of US$100 billion per year prior to the 2025 UN climate conference (UNFCCC, Citation2015b, Decision 1/CP.21, paragraph 53). It was agreed that in setting a new climate finance target, the needs and priorities of developing countries’ will be taken into account (ibid). Indeed, the financing needs of developing countries have increased significantly for both mitigation and adaptation since the UN climate conference in 2009 (Sanderson & O’Neill, Citation2020; UNEP, Citation2021a).

Deliberations for the post-2025 finance target started at COP26 in Glasgow. Some countries already put forward a number. For example, ahead of the COP, the South African environment minister suggested US$750 billion per year by 2030 (Timperley, Citation2021) and the Group of Like Minded Developing Countries together with the African Group of Negotiators suggested a commitment by developed countries to mobilise jointly at least USD 1.3 trillion per year by 2030 (LMDC & AGN, Citation2021). However, negotiations about the size of the target and its characteristics have not formally started and decisions in Glasgow were process-related only. It was decided to establish an ad hoc work programme from 2022 to 2024, to hold four technical expert dialogues per year, to convene high-level ministerial dialogues, and to end deliberations by setting the new collective quantified goal in 2024 (UNFCCC, Citation2021, Dec. CMA.3). The decisions also invite external input (ibid.)

This Perspective article aims to inform the negotiations towards a new collective quantified goal that is meaningful in that it effectively supports the implementation of the UNFCCC and the Paris Agreement in a transparent way.

First, we look back at how climate finance has functioned and identify a number of difficulties that hamper it. Second, in the context of these difficulties and the evolution of the UN climate negotiations since the US$100 billion target was first set in 2009, we identify and discuss five priority elements that should be negotiated to reach a meaningful new collective quantified goal. Third, we suggest using these negotiations as an opportunity to consider other aspects of the climate finance system, including access to finance and loss and damage. We conclude by providing suggestions for setting a new collective quantified goal.

The climate finance experts co-authoring this article are long-term followers of the UNFCCC process but currently do not formally represent any party to the UNFCCC. The authors have different backgrounds and perspectives, and are both from and working in a wide range of developing and developed countries.

2. Taking stock: the US$100 billion pledge by 2020

Despite persistent efforts by the UNFCCC in particular, no universally agreed modalities to account for international climate finance under the UNFCCC exist, giving rise to multiple accounting practices (Weikmans & Roberts, Citation2019). Ambiguous definitions of climate finance and the set targets mean that it is not clear how much finance was mobilised exactly. However, it is clear that developed countries did not meet the US$100 billion goal in 2020 (COP26 presidency, Citation2021; OECD, Citation2022).

The most prominent international accounting practices that focus on the US$100 billion goal compile the mandatory biennial reporting by Annex II countries (here considered to represent ‘developed countries’) on financial support they provide and mobilise to non-Annex II countries. This relies on self-reporting, which has led to conflicting views on the accuracy and relevance of the data (Weikmans et al., Citation2017; Weikmans & Roberts, Citation2019). For example, the Standing Committee on Finance (Standing Committee on Finance, Citation2021b) and the OECD (OECD, Citation2020) used self-reported amounts to estimate total climate finance flows at respectively US$74.1Footnote1 and US$74.8 billion per year for 2017–2018 (OECD, Citation2020; Standing Committee on Finance, Citation2021b).Footnote2 However, Oxfam estimated that only US$19–22.5 billion in public finance specifically targeted climate action per year in 2017–2018 (Oxfam, Citation2020).

Roberts et al. (Citation2021) explain this large difference through several key differences in accounting. First, most developed countries count all financial instruments (i.e. loans, grants, equity, insurance) at face value in their reporting to the UNFCCC. This is the requirement by the UNFCCC, with reporting in grant-equivalent values being voluntary only (UNFCCC, Citation2018, Dec. 18/CMA.1). The latter can be prohibitively complex where multiple financial instruments and financiers are combined, but reporting at face value does not distinguish between an investment that consists of a full grant and one that is financed through a (concessional) loan. While this face value accounting practice may reflect an investment well, it is a bad measure for the distributional (or transfer) aspect (i.e. grant equivalent) that comes with instruments such as loans. That explains the much lower estimates of aggregate climate finance by Oxfam (Citation2020), which focused on the net financial transfer to developing countries by counting only the grant equivalence of loans.

Second, the long-standing issue of what qualifies as ‘new and additional’ finance has not been resolved. The 1992 Convention states that climate finance should be new and additional. This concept was never defined because of a lack of agreement, leaving it to countries to indicate how they determined what resources are new and additional (UNFCCC, Citation2018). The result is that countries continue to define it in different ways. In combination with countries’ efforts to mainstream climate change into development cooperation, this causes the risk that development assistance is diverted towards climate finance. For example, when support previously allocated for education and health goes to areas that count as climate finance, this would reallocate rather than increase funding (Roberts et al., Citation2021). Only two countries (Norway and Sweden) described their climate finance as amounting to flows that exceed the target of 0.7 per cent of GNI for overall development finance (Standing Committee on Finance, Citation2021b), putting their definition of ‘new and additional’ amongst the most stringent.

A third accounting issue relates to private finance mobilisation. The Cancun Agreements were the first international environmental agreement whose implementation explicitly depends in part on the mobilisation of private finance (Pauw, Citation2017). Developing countries have often opposed private finance, especially for adaptation, noting that public finance can be better targeted to areas of need (Khan et al., Citation2019). On the other hand, the mobilisation of private finance has the potential to increase the total impact of climate finance substantially. While there is progress in developing rigorous methodologies to measure mobilised private finance, data continues to be incomplete and contested (OECD, Citation2020; Oxfam, Citation2020).

Together, these three accounting issues create ambiguity around targets for climate finance and make it difficult to agree on whether targets are met. Nakhooda et al. (Citation2013) already pointed at diverging approaches on what ‘counts’ as climate finance when they analysed whether developed countries met their US$30 billion target for 2010–2012. While self-reported climate finance by provider countries were estimated to exceed the US$30 billion target by US$5 billion, 80 per cent of the amount was also reported as ODA, putting in question whether the funds were ‘new and additional’ (ibid). Furthermore, only 16 per cent was spent on adaptation (assessed at face value) (ibid). The US$100 billion target was missed in 2020, even by developed countries’ own accounting. According to the OECD, US$83.3 billion was mobilised by the end of 2020 (OECD, Citation2022).

These different accounting approaches taken from different perspectives on the US$100 billion target illustrate the dual role that is interpreted into the target. On the one hand it is about mobilising large-scale investments as such, including from the private sector. On the other hand, it is about transferring resources from developed to developing countries to increase equity among countries in addressing the climate crisis (Rübbelke, Citation2011; Morgan & Waskow, Citation2014; Pauw et al., Citation2020). These two roles can be conflicting, and they need to be spelled out more clearly to increase transparency, establish trust, and reach an agreement on a post-2025 target, as we will further explain in the next two sections.

3. Priority elements to determine a new finance target

The size of the current US$100 billion target was a political compromise (Chhetri et al., Citation2020). New collective quantified goal will also be a political compromise, but at least there is an opportunity to base it on vast experience, new insights around needs, and to link the size of the target to the characteristics of climate finance.

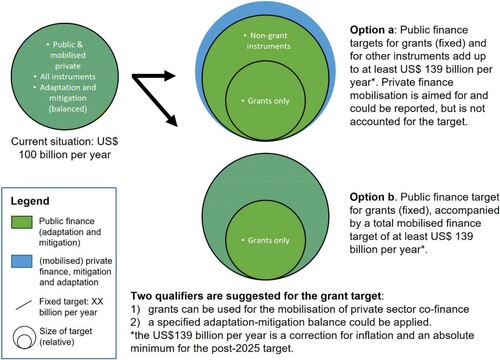

At a minimum, the target should be corrected for inflation. This would imply that the post-2025 target is at least US$139 billion per year (see ). That number is based on an extrapolation up to 2025 of the average inflation rate between 2009 and 2021 of 1,021 per cent (U.S. Bureau of Labour Statistics, Citation2021), assuming that buying power remains at least constant.

Figure 1. Options for new collective quantified goal (source: own compilation).

The target should also be anchored to the ‘needs’ by developing countries to implement the Convention and the Paris Agreement (UNFCCC, Citation2009, Citation2015a; Standing Committee on Finance, Citation2021a). While UNFCCC language has been consistent on the importance of these needs, the financial component of these needs was neither well understood when the US$100 billion target was set (UNFCCC, Citation2007) nor is the current understanding adequate to form the basis of a quantitative needs-based goal setting.

For example, in its first report on the determination of the needs of developing countries, the Standing Committee on Finance (SCF) analysed country submissions to the UNFCCC and concluded that most needs are not expressed in financial terms (Standing Committee on Finance, Citation2021a). The SCF identified 6,690 needs in National Communications of 149 countries, of which only 1,137 needs are expressed in financial terms by 46 countries, adding up to US$8.9 trillion. Similarly, in Nationally Determined Contributions (NDCs), 1,782 out of 4,274 needs are expressed in financial terms in 78 out of 153 assessed, cumulatively amounting to US$5,8-5,9 trillion up to 2030. However, 89% of these ‘costed needs’ do not indicate a possible finance source (Standing Committee on Finance, Citation2021a). Another study on needs expressed in NDCs found that the costs of implementing all conditional ambitions of developing countries could be as high as US$ 4.1 trillion for the period 2020–2030 (Pauw et al., Citation2020). However, this number has strong limitations. First, the precision of the cost estimates varies, and it is sometimes unclear how realistic they are. Second, it is often not clear whether countries’ contributions are partly or fully conditional upon support. Third, the current NDCs are insufficiently ambitious to meet the goals of the Paris Agreement. Finally, the current number of climate finance recipient countries outnumbers the countries with conditional NDCs. For example, only 83% of the countries that have received support for mitigation in 2013–2016 make their NDC conditional on mitigation finance (ibid). More detailed assessments of needs and priorities of developing countries and the relation between needs, costs, and required support would help the work towards the post-2025 target and the effectiveness of climate finance provision.

The size of the post-2025 target should also be understood in the context of the instruments and sources of finance used. Under the current US$100 billion target, and if accounting principles at face value are used, provider countries have a high degree of flexibility in terms of instruments used, focus (adaptation/mitigation), and whether or not to use public funds to mobilise private climate finance. This flexibility, however, decouples the target from the transfer of resources from developed to developing countries, making the actual amounts being transferred unclear.

A more clearly structured target, for example through sub-targets, could guide the choice of instruments (e.g. grants versus loans or other financial instruments), the adaptation-mitigation focus, or the share of funds targeting the mobilisation of private finance. This may also increase trust, in particular when designed in anticipation of or accompanied with clear accounting principles. However, accountability towards sub-targets can also be counterproductive, making the system rigid and increasing the complexity of meeting targets. For instance, the Green Climate Fund (GCF) Secretariat identified trade-offs between increasing adaptation finance and increasing private finance mobilisation (Grüning et al., Citation2020; GCF, Citation2021). Aiming to meet both targets might cause lower amounts of climate finance flows when adaptation projects that do not mobilise private sector finance are put on hold.

Against this background, we, as a group of long-term climate finance experts, identify and discuss below a non-exhaustive list of elements that we deem as the priorities of new collective quantified goal. We argue that simply increasing the climate finance target will be ineffective unless these priority elements are further developed and integrated in new collective quantified goal.

3.1 Relation to art. 2.1(c)

Climate finance under the UNFCCC never aimed to fully prevent dangerous climate change or to make all people, economies, and ecosystems resilient to its impacts. That would require a shift in investment in the order of trillions of US dollars. This is what the third long-term goal, or art. 2.1(c) of the Paris Agreement, is about; the climate consistency of finance flows adds a new definition, scope, and scale to what is required in finance and related policymaking. It sets a purpose for all Parties and their implementation of the Paris Agreement, which will have far-reaching implications for countries and for the private sector (Zamarioli et al., Citation2021). The goal of art. 2.1(c) functions as a reminder of the central role of the financial system’s structures and processes for achieving climate objectives. This larger financial system engages actors, such as central banks, commercial banks, and institutional investors, more strongly than the current climate finance support to developing countries does. While climate finance (art. 9 of the Paris Agreement) should continue to be fundamental on its own to address developing countries’ needs and priorities to mitigate and adapt, it can act in complementarity with art. 2.1(c). The post-2025 target for climate finance needs to take art. 2.1(c) into account. On the one hand, public climate finance can be used to support developing countries to shift financial flows by supporting, for instance, the creation of sustainable classification systems that define climate-consistent investments; the advancing of macro and micro-prudential regulation by central banks; or the implementation of fiscal incentives for climate-related action in the financial sector (Zamarioli et al., Citation2021). On the other hand, the re-allocation of all finance worldwide towards low-carbon and resilient investments potentially reduces the mitigation and adaptation financing gaps in developing countries, freeing up public finance under the post-2025 target towards other priority needs that are less attractive for the market.

3.2 Adaptation-mitigation balance

The difference between adaptation and mitigation is not always straightforward and some types of investments can address both (e.g. nature-based solutions, such as forestry and housing insulation). However, since the Copenhagen Accord, parties have promised that climate finance will aim to ‘balance’ these two – again a concept that has not been further defined. While both mitigation and adaptation finance are currently underfunded (Bhattacharya et al., Citation2020; UNEP, Citation2021b; Kreibiehl et al., Citation2022), recipient countries are often particularly vulnerable to climate change and perceive adaptation finance as a vehicle to enhance fairness in the UN climate negotiations (Rübbelke, Citation2011; Pickering et al., Citation2015). However, only 23.9% of the total climate finance at face value was adaptation finance in the period from 2016 to 2020, according to the OECD, though the trend was upwards in 2019 and 2020 (OECD Citation2022). One of the outcomes of the UN climate conference in Glasgow was that developed countries are urged to ‘at least double their collective provision of climate finance for adaptation to developing country Parties from 2019 levels by 2025’ (UNFCCC, 2021 Dec CMA.3 §18).

In any new collective quantified goal, more adaptation finance could be secured by including an aim for a certain split (e.g. 50:50) on mitigation-adaptation, or by setting the current share of 25% as a minimum. In this context, finance to avert, minimise, and address loss and damage could also be discussed. It has no reliable or adequate funding source (Roberts et al., Citation2017; Gewirtzman et al., Citation2018), but the outcome of COP26 in Glasgow indicates that such financing is likely to remain a priority for many developing countries in the coming years (Schalatek & Roberts, Citation2021). The G7 Climate, Energy, and Environment Ministers also emphasise enhanced support regarding averting, minimising, and addressing loss and damage in their Communique ahead of 2022 G7 summit (G7, Citation2022).

Any clarification on the adaptation-mitigation balance will reduce developed countries’ flexibility in implementing their climate finance commitments. It is important to stress that adaptation projects mobilise less public and private co-finance (Cui et al., Citation2020; Grüning et al., Citation2020). A higher adaptation finance target could therefore imply less overall climate finance and a larger finance gap.

3.3 Financial instruments

An important function of climate finance is to transfer resources from richer developed countries with high (historical) emissions to poorer developing countries that suffer most from the climate crisis and that need support for an economic transition. Developing countries therefore tend to prefer grants over loans in cases of similar face value, with similar tendency towards instruments with a higher grant. According to the OECD (OECD, Citation2021), the grant share of climate finance was only 21% in 2019 (up from 16 per cent in 2018).

Non-grant instruments have advantages and disadvantages. For example, advantages of (concessional) loans and guarantees are that they can have higher impact compared to grants, as they typically mobilise more co-finance from the private sector (Bhattacharya et al., Citation2020). Also, repaid loans can be re-invested in new projects thus stretching the impact of limited public climate finance. However a disadvantage of non-grant instruments is that they can add to countries’ debt levels and curtail their development (Oxfam, Citation2020), thereby reducing their resilience.

New collective quantified goal needs to balance a necessary transfer of resources to developing countries with the need to scale up investments and to maximise impact, precisely to reflect the two roles of the target that were discussed above.

3.4 Mobilising private finance

Measurement and reporting of mobilised private finance continues to be complex and difficult (Standing Committee on Finance, Citation2021b). In the period from 2013 to 2019, mobilised private finance is estimated to have varied between 18 and 27 per cent of total climate finance under the UNFCCC on an annual basis (OECD, Citation2021). More private finance was likely mobilised but not accounted for because it happened indirectly, for example through policy reform, or because data was confidential. Leverage ratios vary strongly between climate finance sources, mitigation versus adaptation projects, and emerging versus lower-income recipient countries (Cui et al., Citation2020; Grüning et al., Citation2020). More research is hence needed to identify implications of these different market contexts for new collective quantified goal. Given the need to shift finance flows in the context of art. 2.1(c), the goal to mobilise private climate finance through the targeted use of public climate finance should become more central in the future, regardless of whether such private finance is accounted for or not as part of the post-2025 target.

For the post-2025 target, it is therefore important to identify whether it is necessary to differentiate with high precision what financing volume can be attributed to which mobilising activity and how to account for this or, instead, if the debate could be focused on shifting private finance flows more generally in relation to art. 2.1(c). In case the focus is on the former, varying leverage ratios and their implications should be considered in more detail, and a coherent accounting system would be necessary.

3.5 ‘New and additional’ finance

Research suggests that climate finance flows have not been ‘new and additional’ as promised since the 1992 UNFCCC (Nakhooda et al., Citation2013; Roberts et al., Citation2021). Concern exists about a possible decline in aid budgets or diversion of essential aid away from important development priorities, e.g. education or public health. This is one reason why Oxfam (Oxfam, Citation2020) argues that developed countries should commit to ensure that future increases of climate finance qualifying as ODA form part of an overall aid budget that is increasing at least at the same rate as climate finance.

However, even if climate finance and ODA can be accounted for separately, the relevance of the concept of ‘new and additional’ finance is fading because the baseline against which it can be measured will change. Art. 2.1(c) sets a global direction for all finance flows – thus including development finance – to at least cease investments in activities that harm mitigation and/or adaptation objectives (Cochran & Pauthier, Citation2019; Jachnik et al., Citation2019). Among possible implications for the post-2025 target, this desired mainstreaming of climate considerations might make it more challenging to separate climate-consistent ODA with ODA provided as – and counted towards – climate finance. Under new collective quantified goal, a stronger articulation of what climate finance is and how it relates to ODA might be required, adjusted to a system of monitoring and accounting climate-consistent finance flows that still needs to be developed.

3.6 Additional aspects

Further to considering the above priorities, the discussion on new collective quantified goal might also be a good opportunity to discuss additional aspects. One example is the reporting on climate finance provision by additional Parties. Except for the removal of Turkey from this list in 2001, the list of countries that are required to provide climate finance under the UNFCCC has not changed since 1992. In line with the Paris Agreement, ‘other Parties’ have also provided climate finance in practice (UNFCCC, Citation2015b). For example, China reported South-South cooperation in 100 countries between 2011 and 2015 in its first Biennial Update Report, although the amount remains unclear. On a multilateral level, 23 ‘other Parties’ pledged to contribute US$354 million to the GCF up to 2022. ‘Other Parties’ refers to countries outside of the group of traditional providers of climate finance, listed on Annex II of the Convention (1992). New collective quantified goal could be accompanied by a decision to require ‘other Parties’ to report on the climate finance that they provide to and mobilise in developing countries. The list of climate finance provider countries could also be extended over time, based on indicators such as emissions (historical and/or per capita), GNI per capita, or climate change vulnerability.

Although it relates to climate finance effectiveness rather than its mobilisation, the prioritisation of climate finance recipients can also be considered in the negotiations. Currently, the majority of climate finance does not reach the countries most in need (Savvidou et al., Citation2021), much less the most vulnerable and at risk communities on the ground (Remling & Persson, Citation2014; Soanes et al., Citation2017). The Paris Agreement prioritises LDCs and SIDS for climate finance and capacity building, and the LDCs for technology transfer (Pauw et al., Citation2019). Further specification of priority recipient countries and considerations of countries’ absorptive capacities could, for example, help to steer grants and adaptation finance to areas of greatest need and/or greatest impact.

Similarly, access to climate finance by the most vulnerable countries hardly relates to climate finance mobilisation, but the negotiations on new collective quantified goal could be used to ensure the need for improvement. Despite readiness support, hurdles to access finance are still high. For example, although allowing direct access for entities from developing countries, the GCF’s accreditation requirements can be particularly stringent before those entities can apply for any funding (Fonta et al., Citation2018). In addition, long lag times in proposal development and approval severely limit the funding that is reaching projects the ground (Chaudhury, Citation2020).

The priorities and aspects above were carefully determined and considered by the authors, but our list is not necessarily exhaustive and other experts might prioritise other issues. For example, newer issues on the international political agenda could also be usefully considered when determining a new collective quantified goal, including: the COVID-19 pandemic and related economic stimulus and recovery spending (Corfee-Morlot et al., Citation2022); the opportunity to make debt-for-climate swaps (Widge, Citation2021); and the need to avert, minimise, and address loss and damage, which has otherwise no reliable source of funding (Mechler & Deubelli, Citation2021).

4. Outlook

In this Perspective article, we have briefly taken stock of the functioning of climate finance under the UNFCCC so far in the context of the 2020 US$100 billion per year target. Based on our experience with the topic to date, we identified six priority elements for setting the new collective quantified goal for climate finance for the post-2025 period. As a final step, this outlook provides our four suggestions moving forward.

First, given the existing difficulties related to accountability, measurement, and trust, we conclude that simply increasing the target would be ineffective to significantly improve climate finance. We demonstrated that the current target embeds a dual role: mobilising investment at scale and transferring resources from developed to developing countries. We believe both are crucial, and this dual role should be spelled out more clearly. It should also be addressed by including a transparent transfer of resources from developed countries to developing countries to address their needs.

Second, in this context we suggest including a collective minimum grant target, either in absolute terms or as an increase compared to the current share. In order to also maintain flexibility in climate finance provision and increase impact, such grants can also be used for the mobilisation of private sector co-finance. Another qualifier could specify the adaptation-mitigation balance for public finance. This might be necessary because it continues to be difficult to mobilise private co-finance for adaptation projects (see ).

A target on grants could be accompanied by at least one additional target. Several options are possible, such as a total public finance target (, option a) and a total mobilised finance target (option b). Together, these specify the full size of a post-2025 target of at least US$139 billion per year (a correction for inflation). It must be kept in mind, however, that accountability towards sub-targets can also make a system rigid and increase the complexity of meeting targets.

Third, as countries implement Article 2.1(c), decarbonisation of the real economy should speed up and resilience should increase. That should reduce the financing gap and free-up some of the limited public climate finance for supporting critical climate needs that will not be addressed in a timely way through the market. A share of new collective quantified goal can also be used to support countries with the implementation of Article 2.1(c). At the same time, however, some measures related to the financial sector, such as the inclusion of climate risks into investments’ decision-making, may also reduce capital inflows and increase the cost of capital in countries with higher climate risks (Buhr et al., Citation2018; Beirne et al., Citation2020; Zamarioli et al., Citation2021). For a post-2025 target that addresses the needs and priorities of developing countries, it will be crucial to track whether overall finance flows are made consistent with low-carbon and climate resilient pathways and to clarify the role of Art. 2.1(c) alongside climate finance, in particular at the UNFCCC negotiations.

Fourth, the negotiations on new collective quantified goal are also a good opportunity to discuss some shortcomings of the current system of climate finance provision. For example, it would be an option to invite more climate finance providers to the table; to discuss a further prioritisation of climate finance allocation to particular countries or needs, including loss and damage; and/or to improve access to finance by the most vulnerable countries. The latter are not directly related to the size of the target per se, but they are central to the effectiveness of climate finance.

Finally, it is essential that the internationally agreed climate finance tracking and accounting rules are updated to respond to the changes incurred by new collective quantified goal. This is key to ensure transparency and increase trust, not just for the high-level political agenda, but also for those who are to be supported.

Acknowledgements

We thank two autonomous reviewers and the team of Climate Policy editors for their excellent comments and suggestions. We are thankful for the financial support of the German Federal Ministry of Economic Cooperation and Development (BMZ) for this research. The research was done independently, BMZ had no role in the preparation, analysis or writing of this article or its outcomes.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 Average for 2017-2018 for UNFCCC funds, multilateral climate funds, climate-specific finance through bilateral, regional and other channels, MDB climate finance attributed to developed countries, and mobilised private climate finance through both multilateral, bilateral and regional channels.

2 These numbers are supplemented by data from the OECD DAC and Export Credit Group statistics and complementary reporting to the OECD. The most recent numbers by the OECD (OECD, Citation2021) indicate that US$ 79.6 billion was mobilised in 2019.

References

- Beirne, J., Renzhi, N., & Volz, U. (2020). Feeling the heat: climate risks and the cost of sovereign borrowing. 1160. doi:10.1007/978-1-349-67278-3_116.

- Bhattacharya, A., Calland, R. Averchenkova, A., Gonzalez, L., Martinez-Diazand, L. van Rooij, J. (2020). Delivering on the $100 Billion Climate Finance Commitment and Transforming Climate Finance.

- Bodnar, P., Brown, J., & Nakhooda, S. (2015). What Counts: Tools to Help Define and Understand Progress Towards the $100 Billion Climate Finance Commitment. Available at: http://www.wri.org/publication/what-counts-tools-help-define-and-understand-progress-towards-100-billion-climate

- Buhr, B., Volz, U., Donovan, C., Kling, G., Lo, Y. C., Murinde, V., & Pullin, N. (2018). Climate change and the cost of capital in developing countries. London.

- Chaudhury, A. (2020). Role of intermediaries in shaping climate finance in developing countries-lessons from the green climate fund. Sustainability (Switzerland), 12(14), 5507. https://doi.org/10.3390/SU12145507

- Chhetri, R. P., Dransfeld, B., Harmeling, S., Köhler, M., & Nettersheim, C. (2020). Options for the post-2025 climate finance goal.

- Ciplet, D., Roberts, J. T., & Khan, M. (2015). Power in a warming world: The new global politics of climate change and the remaking of environmental inequality. MIT Press.

- Cochran, I., & Pauthier, A. (2019). A Framework for Alignment with the Paris Agreement : Why, What and How for Financial Institutions? Paris, France. Available at: https://www.i4ce.org/download/framework-alignment-with-paris-agreement-why-what-and-how-for-financial-institutions/

- COP26 presidency. (2021). Climate Finance Delivery Plan: Meeting the Us $ 100 Billion Goal. London, UK. Available at: https://ukcop26.org/cop26-goals/finance/

- Corfee-Morlot, J., Depledge, J., & Winkler, H. (2022). COVID-19 recovery and climate policy. Climate Policy [Preprint], 21(10), 1249–1256. http://doi.org/10.1080/14693062.2021.2001148

- Cui, L., Sun, Y., Song, M., & Zhu, L. (2020). Co-financing in the green climate fund: Lessons from the global environment facility. Climate Policy, 20(1), 95–108. https://doi.org/10.1080/14693062.2019.1690968

- Fonta, W. M., Ayuk, E. T., & van Huysen, T. (2018). Africa and the green climate fund: Current challenges and future opportunities. Climate Policy, 18(9), 1210–1225. https://doi.org/10.1080/14693062.2018.1459447

- G7. (2022). G7 Climate, Energy and Environment Ministers ‘ Communiqué I . Joint Action: Advancing the Climate, Energy and Environment Agenda Together’. Berlin, Germany, pp. 1–39. Available at: https://www.bmwk.de/Redaktion/DE/Downloads/G/g7-konferenz-klima-energie-umweltminister-05-2022-abschlusskommunique.pdf?__blob = publicationFile&v = 14

- GCF. (2021). Report on the activities of the Secretariat. Songdo, South Korea.

- Gewirtzman, J., Natson, S., Richards, J.-A., Hoffmeister, V., Durand, A., Weikmans, R., Huq, S., & Roberts, J. T. (2018). Financing loss and damage: Reviewing options under the Warsaw international mechanism. Climate Policy, 18(8), 1076–1086. https://doi.org/10.1080/14693062.2018.1450724

- Grüning, C., Pauw, W. P., & Zamarioli, L. H. (2020). Mobilising public and private co-finance. Frankfurt am Main.

- Iro, A. (2014). Monitoring, Reporting and Verifying Climate Finance: international state of play and future perspectives. Bonn, Germany. Available at: http://star-www.giz.de/fetch/5r2w5X001P00geBi0Q/giz2014-0363en-climate-finance.pdf

- Jachnik, R., Mirabile, M., & Dobrinevski, A. (2019). Tracking Finance Flows Towards Assessing Their Consistency with Climate Objectives, OECD Environment Working Papers. Available at: http://doi.org/10.1787/82cc3a4c-en

- Khan, M., Robinson, S.-a., Weikmans, R., Ciplet, D., & Roberts, J. T. (2019). Twenty-five years of adaptation finance through a climate justice lens. Climatic Change, 161(2), 251–269. https://doi.org/10.1007/s10584-019-02563-x

- Kreibiehl, S., Yong Jung, T., Battiston, S., Carvajal, P. E., Clapp, C., Dasgupta, D., Dube, N., Jachnik, R., Morita, K., Samargandi, N., & Williams, M., (2022). Climate change 2022: Mitigation of climate change. Contribution of working group III to the sixth assessment report of the intergovernmental panel on climate change. In J. Shukla et al. (Ed.), IPCC WG III contribution to the sixth assessment report. Cambridge University Press.

- LMDC & AGN. (2021). Conference Room Paper: Group of Like Minded Developing Countries and the African Group of Negotiators. Available at: https://unfccc.int/sites/default/files/resource/3_11_21_ Joint_CPR_New Goal.pdf

- Mechler, R., & Deubelli, T. M. (2021). Finance for loss and damage: A comprehensive risk analytical approach. Current Opinion in Environmental Sustainability, 50, 185–196. https://doi.org/10.1016/j.cosust.2021.03.012

- Morgan, J., & Waskow, D. (2014). A new look at climate equity in the UNFCCC. Climate Policy, 14(1), 17–22. https://doi.org/10.1080/14693062.2014.848096

- Nakhooda, S., Fransen, T., Kuramochi, T., Caravani, A., Prizzon, A., Noriko, S., Tilley, H., Halimanjaya, A., & Welham, B., (2013). Mobilising International climate finance: Lessons from the Fast-Start Finance Period. London, UK.

- OECD. (2020). Climate Finance Provided and Mobilised by Developed Countries in 2013-18, Climate Finance Provided and Mobilised by Developed Countries in 2013-18.

- OECD. (2021). Climate Finance Provided and Mobilised by Developed Countries Aggregate trends updated with 2019 data, OECD publishing. Paris, France. Available at: https://www.oecd.org/env/climate-finance-provided-and-mobilised-by-developed-countries-aggregate-trends-updated-with-2019-data-03590fb7-en.htm?

- OECD (2022). Aggregate trends of climate finance provided and mobilised by developed countries in 2013-2020. https://www.oecd.org/climate-change/finance-usd-100-billion-goal

- Oxfam. (2020). Climate Finance Shadow Report 2020 Global Cooperation on Climate Change. Oxford, UK.

- Pauw, W. P. (2017). From public to private climate change adaptation finance adapting finance or financing adaptation? Utrecht University.

- Pauw, W. P., Castro, P., Pickering, & J., Bhasin, S. (2020). Conditional nationally determined contributions in the Paris Agreement: Foothold for equity or Achilles heel? Climate Policy, 20(4), 468–484. https://doi.org/10.1080/14693062.2019.1635874

- Pauw, W. P., Mbeva, K., & van Asselt, H. (2019). Subtle differentiation of countries’ responsibilities under the Paris Agreement’. Palgrave Communications, 5(1), 1–7. https://doi.org/10.1057/s41599-019-0298-6

- Pickering, J., Betzold, C., & Skovgaard, J. (2017). Special issue: Managing fragmentation and complexity in the emerging system of international climate finance. International Environmental Agreements: Politics, Law and Economics, 17(1), 1–16. https://doi.org/10.1007/s10784-016-9349-2

- Pickering, J., Jotzo, F., & Wood, P. J. (2015). Sharing the global climate finance effort fairly with limited coordination. Global Environmental Politics, 15(4), 39–62. https://doi.org/10.1162/GLEP

- Remling, E., & Persson, Å. (2014). ‘Climate and Development Who is adaptation for? Vulnerability and adaptation benefits in proposals approved by the UNFCCC Adaptation Fund’. doi:10.1080/17565529.2014.886992.

- Roberts, J. T., Natson, S., Hoffmeister, V., Durand, A., Weikmans, R., Gewirtzman, J., & Huq, S. (2017). How will we pay for loss and damage? Ethics, Policy and Environment, 20(2), 208–226. https://doi.org/10.1080/21550085.2017.1342963

- Roberts, J. T., Weikmans, R., Robinson, S.-a., Ciplet, D., Khan, M., & Falzon, D. (2021). Rebooting a failed promise of climate finance. Nature Climate Change [Preprint], 11(3), 180–182. https://doi.org/10.1038/s41558-021-00990-2

- Rübbelke, D. T. G. (2011). International support of climate change policies in developing countries: Strategic, moral and fairness aspects. Ecological Economics, 70(8), 1470–1480. https://doi.org/10.1016/j.ecolecon.2011.03.007

- Sanderson, B. M., & O’Neill, B. C. (2020). Assessing the costs of historical inaction on climate change. Scientific Reports, 10(1), 1–12. https://doi.org/10.1038/s41598-020-66275-4

- Savvidou, G., Atteridge, A., Omari-Motsumi, K., & Trisos, C. H. (2021). Quantifying international public finance for climate change adaptation in Africa. Climate Policy, 21(8), 1020–1036. https://doi.org/10.1080/14693062.2021.1978053

- Schalatek, L., & Roberts, E. (2021). Deferred not defeated: the outcome on Loss and Damage finance at COP26 and next steps, Heinrich Boell Stiftung. Available at: https://us.boell.org/en/2021/12/16/deferred-not-defeated-outcome-loss-anddamage-finance-cop26-and-next-steps

- Soanes, M., Rai, N., Steele, P., Shakya, C., & MacGregor, J. (2017). Delivering real change: Getting international climate finance to the local level. Available at: http://www.jstor.org/stable/resrep02711

- Standing Committee on Finance. (2021a). First report on the determination of the needs of developing country Parties related to implementing the Convention and the Paris Agreement. Bonn, Germany.

- Standing Committee on Finance. (2021b). Fourth Biennial Assessment and Overview of Climate Finance Flows. Bonn, Germany.

- Timperley, J. (2021). The broken $100-billion promise of climate finance - And how to fix it. Nature, 598(7881), 400–402. https://doi.org/10.1038/d41586-021-02846-3

- U.S. Bureau of Labour Statistics. (2021). CPI Inflation Calculator. Available at: https://www.bls.gov/data/inflation_calculator.htm

- UNEP. (2021a). Adaptation Gap report 2020. Nairobi.

- UNEP. (2021b). Adaptation Gap Report 2021: The gathering storm – Adapting to climate change in a post-pandemic world, Endocrinologist. Nairobi: UNEP. doi:10.1097/00019616-199403000-00001.

- UNFCCC. (2007). Investment and Financial Flows to Address Climate Change, United Nations Framework Convention on Climate Change.

- UNFCCC. (2009). Report of the Conference of the Parties on its fifteenth session, held in Copenhagen from 7 to 19 December 2009, UNFCCC. Bonn, Germany.

- UNFCCC. (2010). Framework Convention on Climate Change Conference of the Parties session, held in Cancun from 29 November to Part Two : Action taken by the Conference of the Parties The Cancun Agreements : Outcome of the work of the Ad Hoc Working Group on Long-term Coo. Bonn, Germany.

- UNFCCC. (2015a). Paris Agreement.

- UNFCCC. (2015b). Report of the Conference of the Parties on its twenty-first session, held in Paris from 30 November to 13 December 2015 Addendum Contents Part two: Action taken by the Conference of the Parties at its twenty-first session, Decision 1/CP.21 Adoption of the Paris Agreement. Bonn, Germany.

- UNFCCC. (2018). Report of the Conference of the Parties serving as the meeting of the Parties to the Paris Agreement on the third part of its first session, held in Katowice from 2 to 15 December 2018. Bonn, Germany.

- UNFCCC. (2021). Decision 9/CMA.3 New collective quantified goal on climate finance. UN doc FCCC/PA/CMA/2021/10/Add.3.

- Weikmans, R., Timmons Roberts, J., Baum, J., Bustos, M. C., & Durand, A. (2017). Assessing the credibility of how climate adaptation aid projects are categorised. Development in Practice, 27(4), 458–471. https://doi.org/10.1080/09614524.2017.1307325

- Weikmans, R., & Roberts, J. T. (2019). The international climate finance accounting muddle: Is there hope on the horizon? Climate and Development, 11(2), 97–111. https://doi.org/10.1080/17565529.2017.1410087

- Widge, V. (2021). Opinion: Debt-for-climate swaps — are they really a good idea, and what are the challenges?, Devex. Available at: https://www.devex.com/news/opinion-debt-for-climate-swaps-are-they-really-a-good-idea-and-what-are-the-challenges-98842

- Zamarioli, L. H., Pauw, W. P., & Chenet, H. (2021). The climate consistency goal and the transformation of global finance. Nature Climate Change, 11(7), 578–583. https://doi.org/10.1038/s41558-021-01083-w