ABSTRACT

Several major economies have already committed to achieving a carbon-neutral economy by 2050, in accordance with the Paris Agreement. The banking system in all countries has a key role to play in supporting the transition to a low-carbon economy, and academia has been researching the prudential regulation tools that will enable the incorporation of climate risk management into banking. However, no studies to date have attempted to systematize research on Climate-related Prudential Regulation Tools. This study conducts a systematic review of the English-language peer-reviewed literature produced on this topic in the period since the 2007–2008 financial crisis, revealing the state of the art and the research gaps. The thematic synthesis carried out in this study shows the experience of some countries in the implementation of these tools and the advancement of academic knowledge in this field. These findings can serve as a reference for the further development of a harmonized international framework to address climate risk in banking.

Key Policy Insights

Central banks are considering sustainable and responsible investment (SRI) in their agenda to align national financial systems towards internationally-agreed climate goals.

The academic research community is also investigating how to integrate climate risk into the prudential regulation tools available to financial regulators.

A concentration of research in developed countries, mainly in Europe, and a significant increase in the publication of studies has been observed in recent years.

Scientific research has focused on five prudential regulatory tools: disclosure requirements, climate-related stress testing, differentiated capital requirements, targeted refinancing lines, and green finance guides and frameworks.

Research gaps identified include green bubble, double materiality, interaction between policies, compound risks, banking governance, and small and medium-size enterprize (SME) banking. They are cross-cutting issues that could increase the body of knowledge on climate-related prudential regulation tools.

1. Introduction

Rockström et al. (Citation2009) identified nine planetary boundaries, three of which – climate change, the rate of biodiversity loss, and the rate of interference with the nitrogen cycle – have already occurred. It is thus clear that the planet is in the midst of a climate emergency (UNEP, Citation2021). To address this problem, one of the goals set by the Paris Agreement is to limit the temperature increase to a maximum of 2°C above pre-industrial levels, and where possible to 1.5°C (United Nations, Citation2015). Achieving this depends on the political will to transition to a low-carbon economy, replacing polluting sources of energy with renewable sources (Peake & Ekins, Citation2017).

Some progress has been made in the energy shift. An example of this is the reform of the European Emissions Trading Scheme, EU ETS (EU Parliament, Citation2018), which is designed to encourage the private sector to take an interest in green industries (Campiglio, Citation2016). There are also the commitments by both the European Community and the United States to reach carbon neutrality by 2050 (Biden, Citation2021; European Commission, Citation2019), and for China to reach this milestone by 2060 (Jinping, Citation2020). Other countries submit reports on their Nationally Determined Contributions (NDCs) to present their plans for achieving the reduction in greenhouse gas emissions required for compliance with the Paris Agreement.

The increase in the price of emission allowances under the EU ETS scheme may accelerate the transition away from coal and hydrocarbon-based power plants and boost investment in new renewable energy plants (Victoria et al., Citation2020). This is expected to have an impact on the financial sector, with banks becoming increasingly exposed to climate risks through stranded assets; that is, the loans they granted to build infrastructure for generating energy from polluting sources (Caldecott et al., Citation2016; Carney, Citation2015; Scott Cato & Fletcher, Citation2020). Moreover, the physical impact of climate change can affect some customers’ ability to pay, leading to default.

Scholars such as Schoenmaker and Van Tilburg (Citation2016) and Campiglio et al. (Citation2018) point out that the primary responsibility for establishing climate policies lies with governments. One of their powers is the regulation of fiscal policy, and in particular the implementation of carbon taxes to penalize economic activities that generate greenhouse gases. Such policies are intended to promote the development of renewable energies supporting the transition to a low-carbon economy. However, given the slow pace of government action – and in order to maintain the stability of the financial system – it has been suggested that central banks and financial regulators should have access to prudential regulation tools that can incorporate climate risks.

In practice, a limit to the power of central banks has been observed in some countries. Dikau and Volz (Citation2021) report that only 12% of the 135 central banks they analyze have explicit mandates related to sustainability. The US Federal Reserve has a limited legal framework to address environmental considerations (Skinner, Citation2021). Thus, it makes sense to integrate environmental, social, and governance (ESG) criteria in the policy frameworks of central banks because they can promote caution and financial stability, even without an explicit mandate related to sustainability (Campiglio et al., Citation2018; Dikau & Volz, Citation2021; Sartzetakis, Citation2021).

Recent research has examined the prudential regulatory tools available to central banks and financial regulators, in order to analyze how banks can use them to mitigate climate risks and take advantage of the opportunities that arise. D’orazio and Popoyan (Citation2020) analyze the implementation of some of these tools and conclude that the countries leading their adoption are also vulnerable to climate change, including not only low – and middle-income countries but also developed economies such as Japan, France, the United Kingdom, South Korea and The Netherlands. It is clear that each nation will need to consider the use of these tools in relation to its specific circumstances (Durrani et al., Citation2020).

A number of systematic reviews have analyzed the relationship between the environment and finance from different perspectives, such as sustainability (Rezende et al., Citation2016), low-carbon innovation (Polzin, Citation2017), socially responsible investment (Widyawati, Citation2020), sustainable investing (Talan & Sharma, Citation2019), sustainable banking (Nájera-Sánchez, Citation2020), ESG investing (Daugaard, Citation2020), green finance (Akomea-Frimpong et al., Citation2022), and environmental risks and risk management in the financial sector (Breitenstein et al., Citation2021). However, no studies to date have attempted to systematize the aggregate results of the research being carried out on Climate-related Prudential Regulation Tools.

This paper seeks to fill this research gap by conducting a systematic review of this issue in the context of sustainable and responsible investment (SRI). In so doing, we aim to answer the following research questions:

What lines of research explore prudential regulatory tools that incorporate climate risk into banking?

Which of these research lines have attracted the greatest scientific interest and could help to develop a harmonized approach to climate risk management in banking?

The rest of the paper is structured as follows: Section 2 presents the background to SRI; Section 3 details the methodology used; Section 4 presents the results obtained; Section 5 discusses the thematic synthesis; and Section 6 presents the conclusions.

2. Sustainable and responsible investment, SRI

Sustainability is a concept that has migrated from the field of development economics to business management. Current stakeholder theory is challenging the assumptions of classical economics, in particular the theory of the firm, according to which the social responsibility of business is to increase profits (Friedman, Citation1970). Indeed, there has been a growing belief in recent years that companies have a wider responsibility to not only deliver a good financial performance but also to make a positive contribution to society (Business Roundtable, Citation2019; Fink, Citation2018).

Sustainability criteria have been mainstreamed in the financial sector through a number of initiatives. These include the Equator Principles (2003), Global Compact (2004), Principles for Responsible Investment (2005), Principles for Responsible Banking (2019), and Net-Zero Banking Alliance (2021). The aim of these initiatives is to mobilize resources for activities that contribute to the sustainability of the planetary system, while taking fiduciary duty into account (Galaz et al., Citation2018).

The paradigm of sustainable finance implies a shift in the approach to investment, from ‘socially responsible investment’ to ‘sustainable investment.’ The first approach primarily considers the social responsibility of banking and precludes activities that violate human rights or are socially unacceptable. The second, in addition to taking social issues into account, incorporates environmental and corporate governance criteria – together referred to as ESG criteria – into the decision-making process (Hill, Citation2020, p. 13). Semantically, the term ‘Sustainable and Responsible Investment’ is replacing the term ‘Socially Responsible Investment,’ while keeping the acronym SRI (Capelle-Blancard & Monjon, Citation2012).

Currently, terms such as ‘Ethical Investing,’ ‘Impact Investing,’ ‘Green Investing,’ and ‘ESG Investing’ are used interchangeably to refer to sustainable investing, which can give rise to confusion (Daugaard, Citation2020). For the sake of clarity, this paper aligns with the definitions provided by the Global Sustainable Investing Alliance and Eurosif, together with that of Giamporcaro and Pretorius (Citation2012). These authors define the term SRI as sustainable and responsible investment that meets any of the following investment criteria: negative screening, ESG integration, corporate engagement, norms-based screening, positive/best in class screening, sustainability themed investing, and impact/community investing (Global Sustainable Investment Alliance, Citation2021).

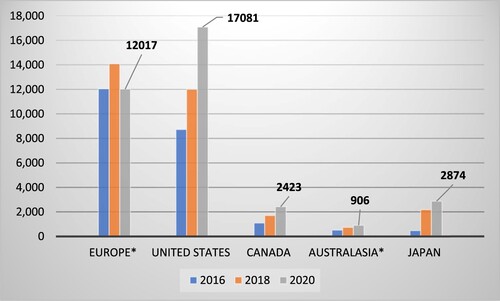

SRI is proving popular with investors (Capasso et al., Citation2020; Cui & Huang, Citation2018; Ferrero-Ferrero et al., Citation2016; Lee et al., Citation2016; Morningstar, Citation2018; Velte, Citation2017), which explains the creation of ESG and sustainable investment indices in recent decades (Talan & Sharma, Citation2019). As an indication of the success of SRI, it now accounts for USD 35.3 trillion (2020), which is equivalent to 36% of all assets under management in five major markets, as shown in (Global Sustainable Investment Alliance, Citation2021).

Figure 1. SRI investment growth in 5 major markets (billion USD). Source: Authors’ own elaboration based on information from Global Sustainable Investment Alliance (Citation2021). Note: According to that report, in 2020, European countries include: Austria, Belgium, Bulgaria, Denmark, France, Germany, Greece, Italy, Spain, The Netherlands, Poland, Portugal, Slovenia, Sweden, the United Kingdom, Norway, Switzerland, and Liechtenstein, while Australasian countries include Australia and New Zealand.

Financial regulators have also added this type of investment to their agendas for consideration. This is because an accelerated progression of climate change involving the manifestation of physical risks or a disorderly transition to a low-carbon economy could well have destabilizing effects on the financial system (Financial Stability Board, Citation2020). Accordingly, the need for a green reform of the financial sector (World Bank Group, Citation2020) is being proposed to prevent the emergence of a carbon bubble (Weizig et al., Citation2014). In 2019, the Network for Greening the Financial System (NGFS), which was created to discuss progress on the Paris Agreement and brings together the major central banks and financial regulators, presented a set of recommendations aimed at raising awareness and capacity building, assessing climate-related risks, setting appropriate governance, requiring transparency, and considering applying capital measures in line with Basel Pillars I and II (NGFS, Citation2019).

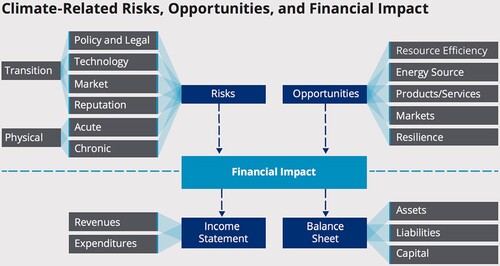

Climate risks remain under discussion, as there are still no standardized methods or frameworks to properly manage them. Nor is there a consensus on the types of risks. While some authors generally point to physical and transition risks, others also include liability and reputational risks (Palm-Steyerberg, Citation2019). As a starting point, the initiative of the Task Force on Climate-Related Financial Disclosures (TCFD) can be used. Under this framework, climate risks are incorporated into traditional risk categories, considering the opportunities for banks, and determining their financial impact ().

Figure 2. Risks, Opportunities and the Financial Impact of Climate Risks. Source: Taken with permission from Task Force on Climate-Related Financial Disclosures. Final Report (TCFD, Citation2017).

3. Methodology

To conduct this study, we performed a systematic literature review, a methodology that is becoming increasingly prominent in the field of social policy (Bryman, Citation2016, p. 98). We used the SALSA framework (Grant & Booth, Citation2009) and its adaptation for the Social Sciences, the ReSiste-CSH framework (Codina, Citation2018), which involves four phases: search, evaluation, analysis, and synthesis.

The search phase was conducted using Scopus and Web of Science databases and only peer-reviewed publications were considered. The search spanned the period from 2008 to May 2022. After several trial and error tests, we established the following search equation:

(‘bank’ OR ‘banking system’ OR ‘financial system’ OR ‘financial institution’ OR ‘commercial bank’ OR ‘central bank’ OR ‘financial regulator’ OR ‘financial supervisor’ OR ‘bank regulator’ OR ‘bank supervisor’ OR ‘banking regulator’ OR ‘banking supervisor’) AND (‘climate risk’ OR ‘physical risk’ OR ‘transition risk’ OR ‘climate change’ OR ‘low carbon’ OR ‘decarbonization’ OR ‘climate’) AND (‘regulation’ OR ‘framework’ OR ‘assessment’ OR ‘methodology’ OR ‘tool’ OR ‘approach’)

Subsequently, in the evaluation phase, duplicates and publications not related to the research questions were excluded. Mendeley software was used as the bibliographic manager.

The following phases, analysis and synthesis, were conducted using the method for thematic synthesis proposed by Thomas and Harden (Citation2008) and adapted for the scope of this work. Although those authors suggest line-by-line coding to establish the descriptive and analytical themes, in our case, the descriptive themes were assigned a priori. To do this, we used the framework proposed by Dikau and Volz (Citation2018), who categorize climate-related prudential regulation tools into five groups, as shown in . Thus, to facilitate the descriptive synthesis, each document under analysis was classified into one of these groups of tools, depending on its main contribution. Finally, from the coding of each research paper, common patterns of research gaps were extracted, and an analytical synthesis was then carried out. This final analysis goes beyond the explicit content of the texts, since it is the reviewers’ interpretation that generates new constructs, explanations and hypotheses (Thomas & Harden, Citation2008).

Table 1. Types of green prudential regulation tools and instruments.

To present the results, bibliometric analysis tools were used. They allow the extraction of quantitative information or can be used to produce standardized metrics from written texts to detect research trends, scientific output in different fields, or patterns of scientific connection (Ellegaard & Wallin, Citation2015). On the one hand, the ‘analyze search results’ function of Scopus was used to summarize academic production by year, the concentration of research by country of affiliation and source of funding, and to categorize by area of study. On the other hand, the software VosViewer (van Eck & Waltman, Citation2010) v. 1.6.18 was used to create a map of the most cited documents and thereby visualize their networks and connections.

4. Results

After applying the method described above, the final database contains 70 records, divided among the categories summarized in . There are far more articles (64) than book chapters (6). Regarding the type of approach, there are slightly more empirical studies (38) that apply a qualitative or quantitative approach than there are theoretical documents (32), which instead analyze the implications for public policies or make conceptual proposals.

Table 2. Summary of database records.

Below, we detail the most relevant results of the Scopus data analysis applied to these records and organized in different blocks.

4.1. Evolution of academic research by year

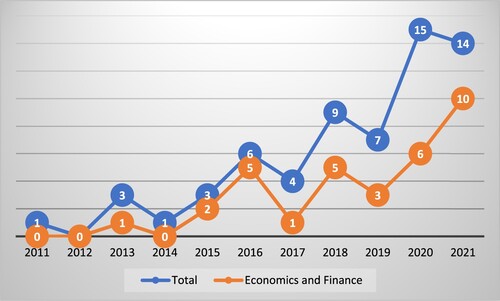

shows the gradual growth in academic interest in this subject. Up until 2015, there were fewer than four publications per year. However, from 2016 onwards, the number of records gradually increases, reaching 15 publications in 2020. The publishing of academic articles in journals indexed in the area of Economics and Finance also reflects this growing trend. Ten papers were produced during the year 2021 alone, underscoring the scientific interest in the subject.

Figure 3. Evolution of published research (2011–2021) by number of documents per year. Source: ‘Analyze search results’ tool of Scopus database.

4.2. Concentration of documents by country of location of the research centres

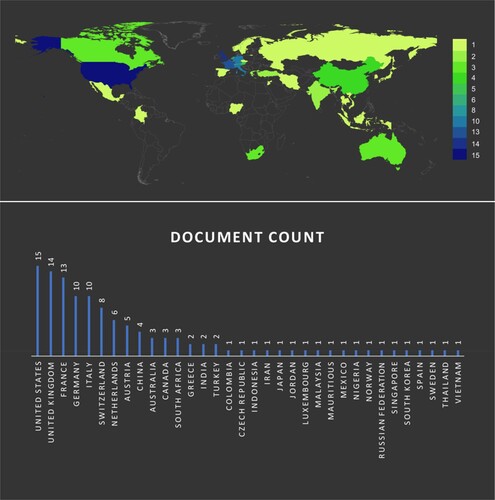

In terms of the number of documents by country of location of the research centres, shows that production is concentrated mainly in the United States (15); the United Kingdom (14); France, Germany, and Italy each with 13 papers; Switzerland (6); The Netherlands (5); China (4); and Australia, Canada, and South Africa each with 3 papers.

Figure 4. Concentration of documents by country of location of research centres. Note: This figure shows the number of documents by country. Source: ‘Analyze search results’ tool of Scopus database.

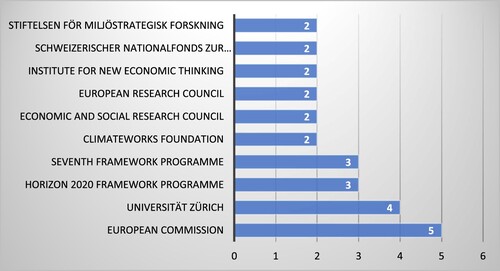

4.3. Concentration of research documents by source of funding

shows the number of research projects by the main sources of funding, revealing a clear predominance of research funds from organizations within Europe.

Figure 5. Concentration of research documents by the main source of funding. Note: The figure shows number of documents per 10 main sources of funding. Source: ‘Analyze search results’ tool of Scopus database.

4.4. Categorization of research by area of study

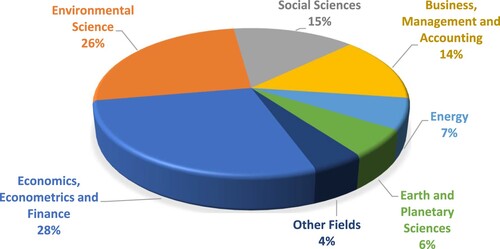

shows how the areas of study are categorized, according to the indexing of the Scopus database. The result shows that 43% of the research papers have been published in journals indexed in the categories of Environmental Science, Energy, Earth and Planetary Sciences, and Other Fields. This evidence supports the rationale for including the Environmental Sciences filter to reduce systemic error.

Figure 6. Categorization of research by area of study in percentages. Source: ‘Analyze search results’ tool of Scopus database.

4.5. Most cited research documents

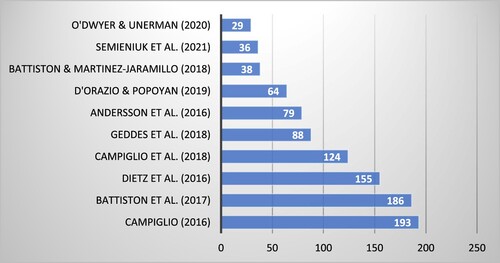

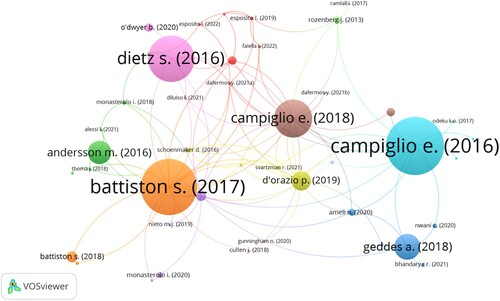

As we can see in , the most cited articles are those of Campiglio (Citation2016), Battiston et al. (Citation2017), Dietz et al. (Citation2016), and Campiglio et al. (Citation2018). The network map in visualizes the interrelationships among those articles and their closeness with other documents.

Figure 7. Most cited documents. Note: The figure shows the number of citations received by the 10 most cited documents. Source: Scopus database.

Figure 8. Network map of the most cited research documents. Note: This figure shows the most cited documents and their proximity based on the network of common citations with other documents. Source: Scopus database and VosViewer software.

4.6. Thematic synthesis

In order to group by thematic lines, it was first necessary to compile information on the adoption of green prudential frameworks by country, as shown in , and categorize each document according to the framework of Dikau and Volz (Citation2018), as summarized in .

Table 3. Adoption of green prudential frameworks by country.

Table 4. Categorization of prudential regulatory tools.

5. Discussion

5.1. State of the art

shows a classification of the empirical and theoretical approaches used in the documents included in this review. The fact that articles substantially outnumber book chapters suggests that this line of research is still in its early stage. This is consistent with , which depicts a growing trend in the publication of documents on the subject of study from 2016 on; the rise thus follows the 2015 Paris Agreement, where the call for climate financing by governments and private entities, particularly banks, helped raise environmental awareness.

The production of documents on the subject of study comes from both developed countries and emerging economies such as China, India, South Africa, Mexico, Colombia, Russia, and Iraq, according to . Results do not reveal any author affiliations with academic centres located in other countries of South America, Africa, Eastern Europe, the Middle East, or Central Asia. One possible explanation for this is the limited availability of research funds in developing countries. Conversely, in developed economies, part of the research has been carried out using public funds (governments and development organizations) or private funds (universities and foundations), as shown in .

Regarding the field of study, confirms that not all the research is published in journals or books indexed in Economics and Finance, but also in those related to Business Administration, Social Sciences, and Natural Sciences. This is an important finding because limiting the search to Economics and Finance may lead to the omission of relevant documents. Some authors of the documents under review come from different branches of science or work in multidisciplinary groups, in which case it is reasonable for their work to be published in related journals. The most cited documents presented in and can be considered as seminal articles on the subject of study.

In relation to the countries where some of these tools are already being implemented, they include both developing countries and more advanced economies, as can be seen in . According to the categorization of publications based on the Dikau and Volz (Citation2018) framework, as shown in , the most commonly referenced documents address the following tools: disclosure requirements, climate-related stress testing, differentiated capital requirements, green refinancing lines, and green finance guidelines or methodologies. The fact that there is no conclusive evidence on these tools points to an ongoing academic debate. We thus present a summary of the main advances in knowledge that can help guide further study on these tools:

Disclosure Requirements. Andersson et al. (Citation2016) suggest the carbon footprint report can be improved using a decarbonized index, while Burnett and Schellhorn (Citation2016) propose the use of a multi-criteria ranking. Instruments for measuring financed emissions (Bimha & Nhamo, Citation2013) and credit carbon intensity (Faiella & Lavecchia, Citation2022) have also been proposed. A general framework for climate risk disclosure is found in the work of Thomä et al. (Citation2018). Successful experiences with and the potential offered by this regulation tool are discussed by de Bruin et al. (Citation2020) and O’Dwyer and Unerman (Citation2020), while criticisms and limitations are raised by Kılıç and Kuzey (Citation2019), Ameli et al. (Citation2020), and Gunningham (Citation2020). Recent studies question the so-called ‘Wall Street Consensus,’ which has encouraged banks to disclose climate risks, but without achieving the necessary transformation to counteract the climate crisis and reverse the dynamics of environmental injustice in the Global South (Dafermos & Nikolaidi, Citation2021). They also highlight the need for standardized metrics to improve interpretation of and comparison between reports (Bingler & Colesanti Senni, Citation2022).

Climate-related Stress Testing. Georgopoulou et al. (Citation2015) put forward a methodological framework to quantify physical and transition risks. Dietz et al. (Citation2016) propose the use of Integrated Assessment Models (IAM) to estimate climate-VaR. The work of Battiston et al. (Citation2017) is also a benchmark for climate-related stress testing. The benefits and implications of these tests are discussed by Battiston and Martinez-Jaramillo (Citation2018) and Monasterolo (Citation2020). Based on Battiston et al. (Citation2017), Monasterolo et al. (Citation2018) analyze the energy portfolio of two Chinese banks, and Roncoroni et al. (Citation2021) evaluate the losses in the Mexican financial system. Other methodologies include those developed by Lamperti et al. (Citation2019), who use an agent-based model (Dystopian Schumpeter meeting Keynes model); Hayne et al. (Citation2019) for late and improvised transition scenarios; Turnbull and Habahbeh (Citation2020) to estimate the financial impact of climate risks; Semieniuk et al. (Citation2021), who propose a framework of transition risk generation channels; Vermeulen et al. (Citation2021) for analyzing the energy transition; and Alessi et al. (Citation2021), who propose the use of the marginal expected shortfall methodology.

Differentiated capital requirements. In his pioneering work, Campiglio (Citation2016) proposes a financing strategy to promote low-carbon investments based on the differentiation of capital requirements according to the destination of the credit. Along these lines, Cullen (Citation2018) suggests increasing the weight for assets high in carbon to penalize investments that contribute to climate risk. Subsequently, the use of a green supporting factor (GSF), or a brown penalizing factor (BPF) as a climate risk differential for risk-weighted assets, has been discussed by several authors, such as Thomä and Gibhardt (Citation2019), who show that the BPF has greater potential than the GSF when it comes to discouraging lending to high-carbon projects; Dafermos and Nikolaidi (Citation2021), who propose a combination of a green fiscal policy and a BPF; or Diluiso et al. (Citation2021), who also justify the use of a BPF to counteract the fall in the price of fossil fuels given the materialization of the transition risk. The combination of a GSF and a BPF is conceptually developed by Esposito et al. (Citation2019) and Esposito et al. (Citation2021), and an empirical analysis is presented by Esposito et al. (Citation2022).

Targeted refinancing lines. Some potential ways for central banks to promote the transition to a low-carbon economy include the issuance of carbon certificates (Hourcade & Shukla, Citation2013; Rozenberg et al., Citation2013), the creation of climate remediation assets (CRAs) (Hourcade, Citation2015), or carbon assets (Espagne & Aglietta, Citation2016). Another scheme is suggested by Ramlall (Citation2017), who proposes the development of a Central Bank Carbon Dioxide Emissions Internalizing Fund, which could be used by countries to reduce carbon dioxide emissions from economic activities. Other authors have carried out an evaluation of incentives for green projects, such as those promoted by the Asian Development Bank to boost green energy (Delina, Citation2011), green financial products in Latin America (Mejia-Escobar et al., Citation2020), or financing of renewable energy in Germany (D’Orazio & Löwenstein, Citation2022). For his part, Odeku (Citation2017) warns that a radical acceleration of sustainable investment by banks is necessary to tackle climate change, and Sawyer (Citation2020) argues there is a need to consider a restructuring of the financial sector that accounts for stakeholder value, to respond to the long-term horizon required for sustainable investments.

Green finance guides or methodologies. Some studies analyze the different climate-related prudential regulation tools to determine their advantages, disadvantages, and implementation recommendations (Bhandary et al., Citation2021; Campiglio et al., Citation2018; D’Orazio & Popoyan, Citation2019; Feridun & Güngör, Citation2020; Schoenmaker & Van Tilburg, Citation2016; Svartzman et al., Citation2021). Other studies are more specific, such as analyses of financial policies in China (Li & Hu, Citation2014); tools for energy transition in Asia (Anbumozhi et al., Citation2018; Wang et al., Citation2020); tools that can foster green financing in Russia (Andreeva et al., Citation2018); and the need to consider a green taxonomy for Malaysia (Keshminder et al., Citation2022). Regarding the methodological approaches, Nieto (Citation2019) proposes an analytical framework for the regulatory treatment of climate risks, while Chenet et al. (Citation2021) present a macroprudential framework using the precautionary principle.

5.2. Research gaps

Some cross-cutting issues that have been identified from our work and that could increase the body of knowledge on climate-related prudential regulation tools are discussed below:

Green bubble. The introduction of a differentiated interest rate for environmental projects or a green supporting factor to encourage green financing has been questioned because it could generate a ‘green bubble’ (Alessi et al., Citation2021; Chenet et al., Citation2021; Dunz et al., Citation2021; D’Orazio, Citation2021). However, there is no empirical evidence that this type of investment is more or less risky than traditional investments. There is thus a need for studies related to the green bubble to prove or disprove the risk inherent to green investments.

Double materiality. Analysis of climate risks has focused on their impact on the economy and finances. However, the feedback in the opposite direction, i.e. how the financial investment decisions contribute to the acceleration of climate change, has not yet been analyzed in depth (Gourdel et al., Citation2021). This dynamic is called the ‘double materiality’ of climate risks. As Le Quang and Scialom (Citation2022) point out, if finances do not redirect financial flows to an ecological reconversion, they are participating in global warming and in so doing amplifying the associated risks; hence the importance of analyzing this dynamic.

Interaction between policies. Some of the tools analyzed have been developed in methodological proposals that are currently being considered by financial regulators. However, independent implementation without proper analysis can increase systemic risk. In this regard, some authors highlight the need to model the interactions between the different climate policies in force (monetary, fiscal, prudential) in the financial systems of each country (Battiston et al., Citation2021; Chenet et al., Citation2021; D’Orazio, Citation2021; Le Quang & Scialom, Citation2022; Svartzman et al., Citation2021). Furthermore, provided there are no conflicts between policies, the impact of a set of policies can outweigh that of a single policy, thus maximizing financial mobilization (Howlett, Citation2014 and Schmidt & Sewerin, Citation2019; cited in Bhandary et al., Citation2021).

Compound risks. Climate change risks are characterized by their nonlinearity of impacts, deep uncertainties, forward-looking nature, complexity, endogeneity, and circularity (Monasterolo, Citation2020). Unlike other types of risk, the analysis of climate risk is generally based on future rather than historical scenarios, which gives rise to even greater complexity. The COVID-19 pandemic has generated new challenges for the economy, including inflationary pressure. Added to this is the war in Ukraine, which is driving up the price of fuel and food. For this reason, some sustainable finance forums have warned of the need to analyze the dynamics of these ‘compound risks’ that threaten financial stability.

SME banking. In the case of the European Union, the current legislation on sustainable finance is focused on large commercial banks, meaning a substantial part of the financial system, including SMEs and local banks, is not covered (Komarnicka & Komarnicki, Citation2022). In fact, some macro prudential tools apply only to systemically important banks. This is a market failure, because it does not contribute to the climate mobilization of the financial system as a whole, and fails to harness existing synergies. For this reason, research is needed to shed light on experiences and propose ways of including climate risk in SME banking.

Bank governance. One reason why banks fail to take climate change into account is short-term thinking, which is driven by incentive structures and management's evaluation of annual results (Gunningham, Citation2020). Alignment with long-term climate objectives does not yet form part of banks’ common practice. Accordingly, some studies have highlighted a need to understand how institutional dynamics can affect climate-related financial policies (Baer et al., Citation2021). Therefore, a review of bank governance could help improve the supervision scheme under Basel Pillar II.

6. Conclusions

The thematic synthesis carried out in this study shows that the scientific research has focused on five prudential regulatory tools: disclosure requirements, climate-related stress testing, differentiated capital requirements, targeted refinancing lines, and green finance guides and frameworks. There is also evidence of research gaps on cross-cutting issues such as the green bubble, double materiality, interaction between policies, compound risks, banking governance, and SME banking.

When comparing this work with other systematic reviews in the field of sustainable finance, a number of common patterns can be observed. The clearest pattern observed is a concentration of research in developed countries, mainly in Europe (Akomea-Frimpong et al., Citation2022; Daugaard, Citation2020; Nájera-Sánchez, Citation2020; Rezende et al., Citation2016; Talan & Sharma, Citation2019). Moreover, a significant increase in the publication of studies has also been observed in recent years, in line with what has been noted in the other reviews, reflecting the growing interest in research into sustainable finance.

The practical utility of this study is that it identifies the state of the art and the research gaps relating to climate-related prudential regulation tools. On the one hand, the final database of documents included in this systematic review is categorized according to the framework of Dikau and Volz (Citation2018), and a list is compiled of the countries where some of these tools are being implemented. It is thus possible with the results here to identify the body of scientific knowledge about emerging tools in this field. On the other hand, the research gaps identified may give rise to new studies that enable solutions to address existing discrepancies and thus to help improve existing models and frameworks.

Regarding the limitations of this study, the analysis is limited to conducting a systematic review, in order to avoid bias in the research process. Only English-language peer-reviewed publications have been used, thus maintaining focus on academic research and objectivity; however, many other types of reports and documents that are being produced, such as books by academic publishers, institutional reports, working papers, and banking supervision reports (i.e. various forms of grey literature) were left out. Given the growing interest in this area of research, all these complementary discursive domains could be added in further research, for example, to examine specific prudential regulation tools. Likewise, experience of voluntary and mandatory implementation in some countries or regions can also serve as a reference for new studies.

Standardizing the use of these prudential regulatory tools is still a subject of discussion. The lack of conclusive evidence on this topic has led to a divergence in performance criteria both in the academic community and among financial regulators. Care should be taken to prevent the emergence of new risks or financial bubbles. However, it is also necessary to rapidly build up a body of knowledge on the drivers and outcomes of climate change risks, and to speed up the development of a harmonized international framework to include climate risks in banking.

Acknowledgements

Research funding for this project was provided by the Universitat Jaume (UJI-B2021-18). We sincerely thank all the anonymous reviewers for the insightful comments offered.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Correction Statement

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

References

- Akomea-Frimpong, I., Adeabah, D., Ofosu, D., & Tenakwah, E. J. (2022). A review of studies on green finance of banks, research gaps and future directions. Journal of Sustainable Finance & Investment, 12, 1241–1264. https://doi.org/10.1080/20430795.2020.1870202

- Alessi, L., Ossola, E., & Panzica, R. (2021). What greenium matters in the stock market? The role of greenhouse gas emissions and environmental disclosures. Journal of Financial Stability, 54, 100869. https://doi.org/10.1016/j.jfs.2021.100869

- Ameli, N., Drummond, P., Bisaro, A., Grubb, M., & Chenet, H. (2020). Climate finance and disclosure for institutional investors: Why transparency is not enough. Climatic Change, 160(4), 565–589. https://doi.org/10.1007/s10584-019-02542-2

- Anbumozhi, V., Kimura, F., & Kalirajan, K. (2018). Unlocking the potentials of private financing for accelerated low-carbon energy transition: An overview. In Financing for Low-carbon Energy Transition: Unlocking the Potential of Private Capital. https://doi.org/10.1007/978-981-10-8582-6_1

- Andersson, M., Bolton, P., & Samama, F. (2016). Hedging climate risk. Financial Analysts Journal, 72(3), 13–32. https://doi.org/10.2469/faj.v72.n3.4

- Andreeva, O. V., Vovchenko, N. G., Ivanova, O. B., & Kostoglodova, E. D. (2018). Green finance: Trends and financial regulation prospects. In Contemporary Studies in Economic and Financial Analysis (Vol. 100). https://doi.org/10.1108/S1569-375920180000100003

- Baer, M., Campiglio, E., & Deyris, J. (2021). It takes two to dance: Institutional dynamics and climate-related financial policies. Ecological Economics, 190, 107210. https://doi.org/10.1016/j.ecolecon.2021.107210

- Battiston, S., Dafermos, Y., & Monasterolo, I. (2021). Climate risks and financial stability. Journal of Financial Stability, 54, 100867. https://doi.org/10.1016/j.jfs.2021.100867

- Battiston, S., Mandel, A., Monasterolo, I., Schütze, F., & Visentin, G. (2017). A climate stress-test of the financial system. Nature Climate Change, 7(4), 283–288. https://doi.org/10.1038/nclimate3255

- Battiston, S., & Martinez-Jaramillo, S. (2018). Financial networks and stress testing: Challenges and new research avenues for systemic risk analysis and financial stability implications. Journal of Financial Stability, 35, 6–16. https://doi.org/10.1016/j.jfs.2018.03.010

- Bhandary, R. R., Gallagher, K. S., & Zhang, F. (2021). Climate finance policy in practice: A review of the evidence. Climate Policy, 21(4), 529–545. https://doi.org/10.1080/14693062.2020.1871313

- Biden, J. (2021). Remarks by President Biden at the Virtual Leaders Summit on Climate Opening Session. https://www.whitehouse.gov/briefing-room/speeches-remarks/2021/04/22/remarks-by-president-biden-at-the-virtual-leaders-summit-on-climate-opening-session/

- Bimha, A., & Nhamo, G. (2013). Conceptual framework for carbon footprinting in the South African banking sector. Banks and Bank Systems, 8(4), 19–33. http://businessperspectives.org/journals_free/bbs/2013/BBS_en_2013_04_Bimha.pdf

- Bingler, J. A., & Colesanti Senni, C. (2022). Taming the green swan: A criteria-based analysis to improve the understanding of climate-related financial risk assessment tools. Climate Policy, 22(3), 356–370. https://doi.org/10.1080/14693062.2022.2032569

- Breitenstein, M., Nguyen, D. K., & Walther, T. (2021). Environmental hazards and risk management in the financial sector: A systematic literature review. Journal of Economic Surveys, 35(2), 512–538. https://doi.org/10.1111/joes.12411

- Bryman, A. (2016). Social research methods (5th Edition). Oxford University Press.

- Burnett, A., & Schellhorn, C. (2016). Leadership performance of financial firms on climate change action. Banks and Bank Systems, 11(2), 103–109. https://doi.org/10.21511/bbs.11(2).2016.10

- Business Roundtable. (2019). Statement on the Purpose of a Corporation. https://s3.amazonaws.com/brt.org/BRT-StatementonthePurposeofaCorporationOctober2020.pdf

- Caldecott, B., Harnett, E., Cojoianu, T., Kok, I., & Pfeiffer, A. (2016). Stranded Assets: A Climate Risk Challenge. https://lpdd.org/wp-content/uploads/2020/03/Stranded-Assets-A-Climate-Risk-Challenge.pdf

- Campiglio, E. (2016). Beyond carbon pricing: The role of banking and monetary policy in financing the transition to a low-carbon economy. Ecological Economics, 121, 220–230. https://doi.org/10.1016/j.ecolecon.2015.03.020

- Campiglio, E., Dafermos, Y., Monnin, P., Ryan-Collins, J., Schotten, G., & Tanaka, M. (2018). Climate change challenges for central banks and financial regulators. Nature Climate Change, 8(6), 462–468. https://doi.org/10.1038/s41558-018-0175-0

- Capasso, G., Gianfrate, G., & Spinelli, M. (2020). Climate change and credit risk. Journal of Cleaner Production, 266, 121634. https://doi.org/10.1016/j.jclepro.2020.121634

- Capelle-Blancard, G., & Monjon, S. (2012). Trends in the literature on socially responsible investment: Looking for the keys under the lamppost. Business Ethics: A European Review, 21(3), 239–250. https://doi.org/10.1111/j.1467-8608.2012.01658.x

- Carney, M. (2015). Breaking the tragedy of the horizon - climate change and financial stability - speech by Mark Carney. https://www.bankofengland.co.uk/speech/2015/breaking-the-tragedy-of-the-horizon-climate-change-and-financial-stability

- Chenet, H., Ryan-Collins, J., & van Lerven, F. (2021). Finance, climate-change and radical uncertainty: Towards a precautionary approach to financial policy. Ecological Economics, 183, 106957. https://doi.org/10.1016/j.ecolecon.2021.106957

- Codina, L. (2018). Revisiones bibliográficas sistematizadas: procedimientos generales y Framework para ciencias humanas y sociales. Universitat Pompeu Fabra.

- Cui, L., & Huang, Y. (2018). Exploring the schemes for green climate fund financing: International lessons. World Development, 101, 173–187. https://doi.org/10.1016/j.worlddev.2017.08.009

- Cullen, J. (2018). After ‘HLEG’: EU banks, climate change abatement and the precautionary principle. Cambridge Yearbook of European Legal Studies, 20, 61–87. https://doi.org/10.1017/cel.2018.7

- Dafermos, Y., & Nikolaidi, M. (2021). How can green differentiated capital requirements affect climate risks? A dynamic macrofinancial analysis. Journal of Financial Stability, 54, 100871. https://doi.org/10.1016/j.jfs.2021.100871

- Dafermos, Y., Gabor, D., & Michell, J. (2021). The Wall Street Consensus in pandemic times: what does it mean for climate-aligned development? Canadian Journal of Development Studies, 42(1-2), 238–251. https://doi.org/10.1080/02255189.2020.1865137

- Daugaard, D. (2020). Emerging new themes in environmental, social and governance investing: A systematic literature review. Accounting & Finance, 60(2), 1501–1530. https://doi.org/10.1111/acfi.12479

- de Bruin, K., Hubert, R., Evain, J., Clapp, C., Dahl, M. S., Bolt, J., & Sillmann, J. (2020). Climate change management. In Climate Change Management, 135–156. https://doi.org/10.1007/978-3-030-36875-3_8

- Delina, L. L. (2011). Asian development bank’s support for clean energy. Climate Policy, 11(6), 1350–1366. https://doi.org/10.1080/14693062.2011.579288

- Dietz, S., Bowen, A., Dixon, C., & Gradwell, P. (2016). ‘Climate value at risk’ of global financial assets. Nature Climate Change, 6(7), 676–679. https://doi.org/10.1038/nclimate2972

- Dikau, S., & Volz, U. (2018). ADBI Working Paper Series Central banking, climate change and green finance. Asian Development Bank Institute. https://www.adb.org/publications/central-banking-climate-change-and-green-

- Dikau, S., & Volz, U. (2021). Central bank mandates, sustainability objectives and the promotion of green finance. Ecological Economics, 184, 107022. https://doi.org/10.1016/j.ecolecon.2021.107022

- Diluiso, F., Annicchiarico, B., Kalkuhl, M., & Minx, J. C. (2021). Climate actions and macro-financial stability: The role of central banks. Journal of Environmental Economics and Management, 110, 102548. https://doi.org/10.1016/j.jeem.2021.102548

- D’Orazio, P. (2021). Towards a post-pandemic policy framework to manage climate-related financial risks and resilience. Climate Policy, 21(10), 1368–1382. https://doi.org/10.1080/14693062.2021.1975623

- D’Orazio, P., & Löwenstein, P. (2022). Mobilising investments in renewable energy in Germany: Which role for public investment banks? Journal of Sustainable Finance & Investment, 12, 451–474. https://doi.org/10.1080/20430795.2020.1777062

- D’Orazio, P., & Popoyan, L. (2019). Fostering green investments and tackling climate-related financial risks: Which role for macroprudential policies? Ecological Economics, 160, 25–37. https://doi.org/10.1016/j.ecolecon.2019.01.029

- D’orazio, P., & Popoyan, L. (2020). Taking up the climate change challenge: a new perspective on central banking. https://www.econstor.eu/handle/10419/228158

- Dunz, N., Naqvi, A., & Monasterolo, I. (2021). Climate sentiments, transition risk, and financial stability in a stock-flow consistent model. Journal of Financial Stability, 54, 100872. https://doi.org/10.1016/j.jfs.2021.100872

- Durrani, A., Rosmin, M., & Volz, U. (2020). The role of central banks in scaling up sustainable finance – what do monetary authorities in the Asia-pacific region think? Journal of Sustainable Finance & Investment, 10(2), 92–112. https://doi.org/10.1080/20430795.2020.1715095

- Dusík, J., & Bond, A. (2022). Environmental assessments and sustainable finance frameworks: will the EU Taxonomy change the mindset over the contribution of EIA to sustainable development? Impact Assessment and Project Appraisal, 40(2), 90–98. https://doi.org/10.1080/14615517.2022.2027609

- Ellegaard, O., & Wallin, J. A. (2015). The bibliometric analysis of scholarly production: How great is the impact? Scientometrics, 105(3), 1809–1831. https://doi.org/10.1007/s11192-015-1645-z

- Espagne, E., & Aglietta, M. (2016). Financing energy and low-carbon investment in Europe: Public guarantees and the ECB. In Handbook of Research on Green Economic Development Initiatives and Strategies. https://doi.org/10.4018/978-1-5225-0440-5.ch007

- Esposito, L., Mastromatteo, G., & Molocchi, A. (2019). Environment – risk-weighted assets: Allowing banking supervision and green economy to meet for good. Journal of Sustainable Finance & Investment, 9(1), 68–86. https://doi.org/10.1080/20430795.2018.1540171

- Esposito, L., Mastromatteo, G., & Molocchi, A. (2021). Extending ‘environment-risk weighted assets’: EU taxonomy and banking supervision. Journal of Sustainable Finance & Investment, 11, 214–232. https://doi.org/10.1080/20430795.2020.1724863

- Esposito, L., Mastromatteo, G., Molocchi, A., Brambilla, P. C., Carvalho, M. L., Girardi, P., Marmiroli, B., & Mela, G. (2022). Green mortgages, EU taxonomy and environment risk weighted assets: A Key link for the transition. Sustainability, 14, 1633. https://doi.org/10.3390/su14031633

- EU Parliament. (2018). Directiva (UE) 2018/410.

- European Commission. (2019). The European Green Deal. https://eur-lex.europa.eu/resource.html?uri = cellar:b828d165-1c22-11ea-8c1f-01aa75ed71a1.0002.02/DOC_1&format = PDF

- Faiella, I., & Lavecchia, L. (2022). The carbon content of Italian loans. Journal of Sustainable Finance & Investment, 12, 939–957. https://doi.org/10.1080/20430795.2020.1814076

- Feridun, M., & Güngör, H. (2020). Climate-related prudential risks in the banking sector: A review of the emerging regulatory and supervisory practices. Sustainability, 12, 5325. https://doi.org/10.3390/su12135325

- Ferrero-Ferrero, I., Fernández-Izquierdo, M., & Muñoz-Torres, M. J. (2016). The effect of environmental, social and governance consistency on economic results. Sustainability, 8(10), 1005. https://doi.org/10.3390/su8101005

- Financial Stability Board. (2020). The Implications of Climate Change for Financial Stability. https://www.fsb.org/wp-content/uploads/P231120.pdf

- Fink, L. (2018). A Sense of Purpose. https://corpgov.law.harvard.edu/2018/01/17/a-sense-of-purpose/

- Friedman, M. (1970). The social responsibility of business is to increase its profits. New York Times Magazine. https://www.nytimes.com/1970/09/13/archives/a-friedman-doctrine-the-social-responsibility-of-business-is-to.html

- Galaz, V., Crona, B., Dauriach, A., Scholtens, B., & Steffen, W. (2018). Finance and the Earth system – exploring the links between financial actors and non-linear changes in the climate system. Global Environmental Change, 53, 296–302. https://doi.org/10.1016/j.gloenvcha.2018.09.008

- Geddes, A., Schmidt, T. S., & Steffen, B. (2018). The multiple roles of state investment banks in low-carbon energy finance: An analysis of Australia, the UK and Germany. Energy Policy, 115, 158–170. https://doi.org/10.1016/j.enpol.2018.01.009

- Georgopoulou, E., Mirasgedis, S., Sarafidis, Y., Hontou, V., Gakis, N., Lalas, D., Xenoyianni, F., Kakavoulis, N., Dimopoulos, D., & Zavras, V. (2015). A methodological framework and tool for assessing the climate change related risks in the banking sector. Journal of Environmental Planning and Management, 58(5), 874–897. https://doi.org/10.1080/09640568.2014.899489

- Giamporcaro, S., & Pretorius, L. (2012). Sustainable and responsible investment (SRI) in South Africa: A limited adoption of environmental criteria. Investment Analysts Journal, 41(1), 1–19. https://doi.org/10.1080/10293523.2012.11082541

- Gibon, T., Popescu, I-Ş, Hitaj, C., Petucco, C., & Benetto, E. (2020). Shades of green: Life cycle assessment of renewable energy projects financed through green bonds. Environmental Research Letters, 15, 104045. https://doi.org/10.1088/1748-9326/abaa0c

- Global Sustainable Investment Alliance. (2021). Global Sustainable Investment Review 2020. https://www.gsi-alliance.org/wp-content/uploads/2021/08/GSIR-20201.pdf

- Gourdel, R., Monasterolo, I., Dunz, N., Mazzocchetti, A., & Parisi, L. (2021). Assessing the double materiality of climate risks in the EU economy and banking sector. SSRN Electronic Journal, https://doi.org/10.2139/ssrn.3939895

- Grant, M. J., & Booth, A. (2009). A typology of reviews: An analysis of 14 review types and associated methodologies. Health Information & Libraries Journal, 26(2), 91–108. https://doi.org/10.1111/j.1471-1842.2009.00848.x

- Gunningham, N. (2020). A quiet revolution: Central banks, financial regulators, and climate finance. Sustainability, 12(22), 9596–9522. https://doi.org/10.3390/su12229596

- Hayne, M., Ralite, S., Thomä, J., & Koopman, D. (2019). Factoring transition risks into regulatory stress-tests: The case for a standardized framework for climate stress testing and measuring impact tolerance to abrupt late and sudden economic decarbonization. ACRN Journal of Finance and Risk Perspectives, 8(1), 206–222. https://doi.org/10.35944/jofrp.2019.8.1.013

- Hill, J. (2020). Environmental, Social, and Governance (ESG) investing. In J. Hill (Ed.), Elsevier.

- Hourcade, J.-C., & Shukla, P. (2013). Triggering the low-carbon transition in the aftermath of the global financial crisis. Climate Policy, 13(SUPPL.1), 22–35. https://doi.org/10.1080/14693062.2012.751687

- Hourcade, J. C. (2015). Harnessing the animal spirits of finance for a low-carbon transition. Geneva Reports on the World Economy, 2015-Novem, 497–514.

- Howlett, M. (2014). From the ‘old’ to the ‘new’ policy design: Design thinking beyond markets and collaborative governance. Policy Sciences, 47(3), 187–207. https://doi.org/10.1007/s11077-014-9199-0

- Jinping, X. (2020). Statement by H.E. Xi Jinping President of the People’s Republic of China At the General Debate of the 75th Session of The United Nations General Assembly. https://www.fmprc.gov.cn/mfa_eng/zxxx_662805/t1817098.shtml

- Kaium Masud, M. A., Mi Bae, S., & Kim, J. D. (2017). Analysis of environmental accounting and reporting practices of listed banking companies in Bangladesh. Sustainability, 9, 1717. https://doi.org/10.3390/su9101717

- Keshminder, J. S., Abdullah, M. S., & Mardi, M. (2022). Green sukuk – Malaysia surviving the bumpy road: Performance, challenges and reconciled issuance framework. Qualitative Research in Financial Markets, 14(1), 76–94. https://doi.org/10.1108/QRFM-04-2021-0049

- Kılıç, M., & Kuzey, C. (2019). Determinants of climate change disclosures in the Turkish banking industry. International Journal of Bank Marketing, 37(3), 901–926. https://doi.org/10.1108/IJBM-08-2018-0206

- Komarnicka, A., & Komarnicki, M. (2022). Challenges in the EU Banking Sector as Exemplified by Poland in View of Legislative Changes Related to Climate Crisis.

- Lamperti, F., Bosetti, V., Roventini, A., & Tavoni, M. (2019). The public costs of climate-induced financial instability. Nature Climate Change, 9(11), 829–833. https://doi.org/10.1038/s41558-019-0607-5

- Lee, K.-H., Cin, B. C., & Lee, E. Y. (2016). Environmental responsibility and firm performance: The application of an environmental, social and governance model. Business Strategy and the Environment, 25(1), 40–53. https://doi.org/10.1002/bse.1855

- Le Quang, G., & Scialom, L. (2022). Better safe than sorry: Macroprudential policy, COVID 19 and climate change. International Economics, 172, 403–413. https://doi.org/10.1016/j.inteco.2021.07.002

- Li, W., & Hu, M. (2014). An overview of the environmental finance policies in China: Retrofitting an integrated mechanism for environmental management. Frontiers of Environmental Science & Engineering, 8(3), 316–328. https://doi.org/10.1007/s11783-014-0625-5

- Mejia-Escobar, J. C., González-Ruiz, J. D., & Duque-Grisales, E. (2020). Sustainable financial products in the Latin America banking industry: Current status and insights. Sustainability, 12(14), 5648. https://doi.org/10.3390/su12145648

- Monasterolo, I. (2020). Climate change and the financial system. Annual Review of Resource Economics, 12(1), 299–320. https://doi.org/10.1146/annurev-resource-110119-031134

- Monasterolo, I., Zheng, J. I., & Battiston, S. (2018). Climate transition risk and development finance: A carbon risk assessment of China’s overseas energy portfolios. China & World Economy, 26(6), 116–142. https://doi.org/10.1111/cwe.12264

- Morningstar. (2018). Sustainable funds U.S. landscape report. Morningstar Research. https://www.morningstar.com/lp/sustainable-funds-landscape-report1

- Nájera-Sánchez, J. J. (2020). A systematic review of sustainable banking through a co-word analysis. Sustainability, 12, 278. https://doi.org/10.3390/su12010278

- Neisen, M., Bruhn, B., & Lienland, D. (2022). ESG rating as input for a sustainability capital buffer. Journal of Risk Management in Financial Institutions, 15(1), 72–84. https://www.eticanews.it/wp-content/uploads/2022/03/Paper-PWC-Pillar-1.pdf

- NGFS. (2019). A call for action Climate change as a source of financial risk. https://www.banque-france.fr/sites/default/files/media/2019/04/17/ngfs_first_comprehensive_report_-_17042019_0.pdf

- Nieto, M. J. (2019). Banks, climate risk and financial stability. Journal of Financial Regulation and Compliance, 27(2), 243–262. https://doi.org/10.1108/JFRC-03-2018-0043

- Nwani, C., & Omoke, P. C. (2020). Does bank credit to the private sector promote low-carbon development in Brazil? An extended STIRPAT analysis using dynamic ARDL simulations. Environmental Science and Pollution Research, 27(25), 31408–31426. https://doi.org/10.1007/s11356-020-09415-7

- Odeku, K. O. (2017). The intrinsic role of the banks in decarbonizing the economy. Banks and Bank Systems, 12(4), 44–55. https://doi.org/10.21511/bbs.12(4).2017.04

- O’Dwyer, B., & Unerman, J. (2020). Shifting the focus of sustainability accounting from impacts to risks and dependencies: Researching the transformative potential of TCFD reporting. Accounting, Auditing & Accountability Journal, 33(5), 1113–1141. https://doi.org/10.1108/AAAJ-02-2020-4445

- Palm-Steyerberg, I. (2019). Climate change and fit and proper-testing in the Dutch financial sector. Law and Financial Markets Review, 13(1), 17–29. https://doi.org/10.1080/17521440.2019.1565127

- Peake, S., & Ekins, P. (2017). Exploring the financial and investment implications of the Paris Agreement. Climate Policy, 17(7), 832–852. https://doi.org/10.1080/14693062.2016.1258633

- Polzin, F. (2017). Mobilizing private finance for low-carbon innovation – A systematic review of barriers and solutions. Renewable and Sustainable Energy Reviews, 77, 525–535. https://doi.org/10.1016/j.rser.2017.04.007

- Purkayastha, D., & Sarkar, R. (2021). Getting financial markets to work for climate finance. The Journal of Structured Finance, 27(2), 27–41. https://doi.org/10.3905/jsf.2021.1.122

- Ramlall, I. (2017). Internalizing CO 2 emissions via central banks’ financials: Evidence from the world. Renewable and Sustainable Energy Reviews, 72, 549–559. https://doi.org/10.1016/j.rser.2017.01.083

- Rezende, C., Amorim Sobreiro, V., Kimura, H., & Luiz de Moraes Barboza, F. (2016). A systematic review of literature about finance and sustainability. Journal of Sustainable Finance & Investment, 6(2), 112–147. https://doi.org/10.1080/20430795.2016.1177438

- Rockström, J., Steffen, W., Noone, K., Persson, Å, Chapin, F. S., Lambin, E. F., Lenton, T. M., Scheffer, M., Folke, C., Schellnhuber, H. J., Crutzen, P., & Foley, J. A. (2009). A safe operating space for humanity. Nature, 461(7263), 472–475. https://doi.org/10.1038/461472a

- Roncoroni, A., Battiston, S., Escobar-Farfán, L. O. L., & Martinez-Jaramillo, S. (2021). Climate risk and financial stability in the network of banks and investment funds. Journal of Financial Stability, 54, 100870. https://doi.org/10.1016/j.jfs.2021.100870

- Rozenberg, J., Hallegatte, S., Perrissin-Fabert, B., & Hourcade, J.-C. (2013). Funding low-carbon investments in the absence of a carbon tax. Climate Policy, 13(1), 134–141. https://doi.org/10.1080/14693062.2012.691222

- Sartzetakis, E. S. (2021). Green bonds as an instrument to finance low carbon transition. Economic Change and Restructuring, 54, 755–779. https://doi.org/10.1007/s10644-020-09266-9

- Sawyer, M. (2020). Financialisation, industrial strategy and the challenges of climate change and environmental degradation. International Review of Applied Economics, https://doi.org/10.4324/9780429425547

- Schmidt, T. S., & Sewerin, S. (2019). Measuring the temporal dynamics of policy mixes – An empirical analysis of renewable energy policy mixes’ balance and design features in nine countries. Research Policy, 48, 103557. https://doi.org/10.1016/j.respol.2018.03.012

- Schoenmaker, D., & Van Tilburg, R. (2016). What role for financial supervisors in addressing environmental risks? Comparative Economic Studies, 58(3), 317–334. https://doi.org/10.1057/ces.2016.11

- Scott Cato, M., & Fletcher, C. (2020). Introducing sell-by dates for stranded assets: Ensuring an orderly transition to a sustainable economy. Journal of Sustainable Finance & Investment, 10(4), 335–348. https://doi.org/10.1080/20430795.2019.1687206

- Semieniuk, G., Campiglio, E., Mercure, J.-F., Volz, U., & Edwards, N. R. (2021). Low-carbon transition risks for finance. WIRES Climate Change, 12(1), https://doi.org/10.1002/wcc.678

- Skinner, C. P. (2021). Central banks and climate change. Vanderbilt Law Review, 74(5), 1301–1364. https://vanderbiltlawreview.org/lawreview/category/volumes/vol-74/vol-74-5-2/

- Svartzman, R., Bolton, P., Despres, M., Pereira Da Silva, L. A., & Samama, F. (2021). Central banks, financial stability and policy coordination in the age of climate uncertainty: A three-layered analytical and operational framework. Climate Policy, 21(4), 563–580. https://doi.org/10.1080/14693062.2020.1862743

- Talan, G., & Sharma, G. D. (2019). Doing well by doing good: A systematic review and research agenda for sustainable investment. Sustainability, 11, 353. https://doi.org/10.3390/su11020353

- TCFD. (2017). Final Report. Recommendations of the Task Force on Climate-Related Financial Disclosures. https://assets.bbhub.io/company/sites/60/2020/10/FINAL-2017-TCFD-Report-11052018.pdf

- Thomas, J., & Harden, A. (2008). Methods for the thematic synthesis of qualitative research in systematic reviews. BMC Medical Research Methodology, 8(1). https://doi.org/10.1186/1471-2288-8-45

- Thomä, J., Dupré, S., & Hayne, M. (2018). A taxonomy of climate accounting principles for financial portfolios. Sustainability, 10(2), 328. https://doi.org/10.3390/su10020328

- Thomä, J., & Gibhardt, K. (2019). Quantifying the potential impact of a green supporting factor or brown penalty on European banks and lending. Journal of Financial Regulation and Compliance, 27(3), 380–394. https://doi.org/10.1108/JFRC-03-2018-0038

- Trabacchi, C., Buchner, B., Smallridge, D., Netto, M., Gomes, J. J., & Serra, L. (2015). The role of national development banks in catalyzing international climate finance: Empirical evidences from Latin America. In Handbook of Climate Change Adaptation, 657–683. https://doi.org/10.1007/978-3-642-38670-1_61

- Tu, C. A., Rasoulinezhad, E., & Sarker, T. (2020). Investigating solutions for the development of a green bond market: Evidence from analytic hierarchy process. Finance Research Letters, 34, 101457. https://doi.org/10.1016/j.frl.2020.101457

- Turnbull, S. M., & Habahbeh, L. (2020). A framework to analyze the financial effects of climate change. The Journal of Risk, 23(2), 105–146. https://doi.org/10.21314/JOR.2020.448

- UNEP. (2021). Making Peace with Nature: A scientific blueprint to tackle the climate, biodiversity and pollution emergencies. https://www.unep.org/resources/making-peace-nature

- United Nations. (2015). Paris Agreement. https://unfccc.int/sites/default/files/english_paris_agreement.pdf

- van Eck, N. J., & Waltman, L. (2010). Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics, 84(2), 523–538. https://doi.org/10.1007/s11192-009-0146-3

- Velte, P. (2017). Does ESG performance have an impact on financial performance? Evidence from Germany. Journal of Global Responsibility, 8(2), 169–178. https://doi.org/10.1108/JGR-11-2016-0029

- Vermeulen, R., Schets, E., Lohuis, M., Kölbl, B., Jansen, D.-J., & Heeringa, W. (2021). The heat is on: A framework for measuring financial stress under disruptive energy transition scenarios. Ecological Economics, 190, 107205. https://doi.org/10.1016/j.ecolecon.2021.107205

- Victoria, M., Zhu, K., Brown, T., Andresen, G. B., & Greiner, M. (2020). Early decarbonisation of the European energy system pays off. Nature Communications, 11(1), https://doi.org/10.1038/s41467-020-20015-4

- Wang, Y., Lei, X., Long, R., & Zhao, J. (2020). Green credit, financial constraint, and capital investment: Evidence from China’s energy-intensive enterprises. Environmental Management, 66(6), 1059–1071. https://doi.org/10.1007/s00267-020-01346-w

- Weizig, F., Kuepper, B., van Gelder, J., & van Tilburg, R. (2014). The Price of Doing Too Little Too Late. The impact of the carbon bubble on the EU financial system. https://gef.eu/wp-content/uploads/2017/01/The_Price_of_Doing_Too_Little_Too_Late_.pdf

- Widyawati, L. (2020). A systematic literature review of socially responsible investment and environmental social governance metrics. Business Strategy and the Environment, 29(2), 619–637. https://doi.org/10.1002/bse.2393

- Wong, C. M. L. (2021). Temporality and systemic risk: The case of green bonds. Journal of Risk Research, 24(1), 110–120. https://doi.org/10.1080/13669877.2020.1843067

- World Bank Group. (2020). Transformative Climate Finance: a new approach for climate finance to achieve low-carbon resilient development in developing countries. https://openknowledge.worldbank.org/bitstream/handle/10986/33917/149752.pdf

- Yuan, F., & Gallagher, K. P. (2018). Greening development lending in the Americas: Trends and determinants. Ecological Economics, 154, 189–200. https://doi.org/10.1016/j.ecolecon.2018.07.009