?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This study examines the impact of capital market on the relationship between energy consumption and carbon emissions. By employing a system Generalised Methods of Moments (GMM) for a sample of 138 developing countries over the period, 1990–2020, we find a U-shaped reverse relationship between renewable energy consumption and carbon emissions. The study reveals that beyond a threshold of 71.03, renewable energy consumption tends to increase carbon emissions. Similarly, the initial levels of carbon emissions reduce the use of renewable energy but beyond a 2.5 level of carbon emissions, renewable energy consumption begins to increase. We find that both the stock market and bond market reduce carbon emissions and enhance the levels of renewable energy consumption. We provide evidence to support that the capital market enhances the negative impact of renewable energy consumption on carbon emissions, while the corporate bond market magnifies the reductive effect of carbon emissions on renewable energy consumption.

1. Introduction

The growing concern about scarce energy sources and the attendant focus on green economy has sparked the interest of researchers and policymakers to understand the association of energy usage and carbon emissions. The increasing global demand for energy has been the reason for the increase in environmental pollution, which has contributed to global warming and energy crisis (Krishnan, Kandasamy, and Subbiah Citation2021; Moodley, Citation2021). For that matter, policies that shape the use of renewable energy sources and environmental emissions are important for achieving sustainable development (see Haldar and Sethi Citation2023; Haldar et al. Citation2023; Houssam et al. Citation2023). For instance, policymakers have put finance firmly at the centre of the debate on environmental degradation and renewable energy consumption (Wang and Ma Citation2022; Zakari, Adedoyin, and Bekun Citation2021; OECD Citation2021; Zhou et al. Citation2019; De Haas and Popov Citation2016). Similar initiatives to fund projects that save energy and reduce carbon emissions are being developed by many other industrialised and developing countries. However, the interest in the development of the capital market has been revealed by the limited understanding of the impact of the capital market in shaping the relationship between renewable energy consumption and carbon emissions.

The motivation of the study stems from the recent debates on how renewable energy consumption and carbon emissions (CO2) are linked to each other (Appiah et al. Citation2019; Chontanawat Citation2020); the non-linear relationship that exists between them (Waqih et al. Citation2019; Szetela et al. Citation2022); and the role of the capital market in the energy-emission nexus. Based on these concepts, we argue that the relationship between renewable energy consumption and carbon emissions should not be one way, rather, it should be: (1) bidirectional; (2) non-linear; and (3) conditioned on the role played by the capital market.

First, persistent global environmental challenges have paved the way for recent studies to explain the unidirectional energy-emission nexus (Mukhtarov et al. Citation2023; Feng Citation2022; Ekwueme, Zoaka, and Alola Citation2021; Soava et al. Citation2018; Joo, Kim, and Yoo Citation2015); and explore the importance of carbon emissions in contributing to the share of renewable energy in the energy mix (Katsampoxakis et al. Citation2022; Anwar et al. Citation2021; Nathaniel, Anyanwu, and Shah Citation2020; Li et al. Citation2020; Balsalobre-Lorente and Leitão Citation2020; Ikram et al. Citation2020), fewer studies have focused on the bidirectional energy-emission nexus (Mukhtarov et al. Citation2023; Haldar and Sethi Citation2021; Chontanawat Citation2020; Irandoust Citation2016). For instance, a study by Mukhtarov et al. (Citation2023) shows how renewable energy consumption reduces CO2 emissions in oil-rich economies, while in the long run, emissions of carbon were found to increase with a reduction in the consumption of renewable energy in South Africa (Ekwueme, Zoaka, and Alola Citation2021) and in Sweden and Norway (Irandoust Citation2016). In addition, recent studies have focused on: the role of governance and renewable energy in alleviating poverty in sub-Saharan Africa (Haldar et al. Citation2023); the importance of green technology and renewable energy in achieving the target of carbon-neutrality for emerging countries (Behera and Dash, Citation2017); the role of institutional quality in moderating the impact of energy consumption on CO2 emission (Haldar and Sethi Citation2021); the effects of ICT, innovation, electricity consumption and renewable power generation on economic growth in the emerging economies (Haldar et al. Citation2023); as well as the relationship between energy consumption, industrialisation, urbanisation and economic growth (Sahoo and Sethi Citation2022). However, a peculiar feature of those studies is that, they ignore the empirical examination of the bidirectional and the non-linearity nexus between renewable energy consumption and carbon emissions in developing economies.

Second, we argue from the perspective of the environmental Kuznets curve (EKC) hypothesis (see Haldar and Sethi Citation2021), which postulates a non-linear energy-emission nexus, and explains that energy is a non-monotonic function of emissions. The literature provides extensive review surveys on the linear relationship between renewable energy consumption and carbon emissions but the results are inconclusive (Mukhtarov et al. Citation2023; Feng Citation2022; Hasnisah, Azlina, and Taib Citation2019). While studies have found a positive relationship between CO2 emissions and energy (Hasnisah, Azlina, and Taib Citation2019; Ozturk Citation2010); others have shown a negative impact of renewable energy consumption on carbon emissions (Mukhtarov et al. Citation2023; Feng Citation2022; Shafiei and Salim Citation2014; Menyah and Wolde-Rufael Citation2010); and a previous study by Pata (Citation2018) has shown that renewable energy has no impact on carbon emissions. These diverse views in the literature could be associated with the differences in the use of renewable sources of energy (EIA Citation2017), and that the energy-emission nexus may not be direct but may exhibit indirect relationship. Depending on the state of the economy and the measurement of energy sources, this indirect relationship can take both a U-shaped pattern and an interaction pattern. On one hand, we argue, based on the U-shaped relationship, that renewable energy consumption reduces carbon emissions until it reaches a certain threshold level and then begins to increase carbon emissions (Alharthi, Dogan, and Taskin Citation2021; Waqih et al. Citation2019). Our approach differs from the above studies in the sense that we extend their models by empirically estimating the threshold level at which the impact of renewable energy consumption on CO2 emissions changes – as well as the reverse. On the other hand, extant literature has explained that, an increasing level of environmental degradation should bring about the adoption of financial reforms that makes financial institutions and government more likely to channel resources and investments into reducing carbon emissions in order to achieve the goal 7 (ensure access to affordable, reliable, sustainable and modern energy for all) and goal 13 (take urgent action to combat climate change and its impact) of the sustainable development goals (Wu et al. Citation2022). Hence, the need to examine the role of the capital market in explaining the energy-emissions nexus.

It is evident that the capital market contributes significantly to development research policies and helps to achieve sustainable development goals in developing countries. In view of that, a number of studies have discovered that the capital market (i.e. stock market) (Paramati, Ummalla, and Apergis Citation2016; Citation2018; Abbasi & Riaz, Citation2016) and financial development (Xiong et al. Citation2020; Danish-Baloch & Suad, Citation2018; Destek & Sarkodie, Citation2019; Sarkodie & Strezov, Citation2019) have a significant effect on carbon emissions and/or environmental degradation. In addition, previous studies have shown that financial development is important in renewable energy production (Xu et al. Citation2021; Destek and Sarkodie, Citation2019; Sarkodie & Strezov, Citation2019; Katircioğlu & Taşpinar, Citation2017), and that the capital market has no connection in reducing emissions in MENA countries (Xu et al. Citation2021). However, these studies produce mixed results due to the measure of financial development that does not capture the independent measure of the capital market (i.e. stock market and bond market). The current study fills in the gap by employing different measures of capital market to examine their impacts on renewable energy consumption and carbon emissions. In addition, the discussions above explain that a strong capital market creates the necessary financing environment or investment opportunities for institutions, investors and governments to moderate the energy-emission nexus, but what is not known is the extent to which the capital market can contribute to the energy-emissions nexus. In this context, the need of a well-developed capital market has been identified as an important channel that provides efficient funding and investments to promote environmentally friendly projects and ultimately help to reduce emissions. This unique role has stirred up development activities, research and policy interests in examining the role of the capital market and in explaining the impact of renewable energy consumption on carbon emissions. We expect that initial levels of renewable energy should reduce carbon emissions while the reduction effect should be magnified at increasing levels of capital market.

Finally, the aforementioned studies have the advantage of using different methods and approaches to explore these concepts. However, little or no study has been devoted to examining the bidirectional and non-linear energy-emission relationship, as well as the role of the capital market in influencing the energy-emissions nexus from the developing economies’ context. In addition, most of them were based primarily in single countries and specific regions in the world, while neglecting the context of developing economies. Our study differs from the previous studies by making novel contributions to a growing body of literature on the energy-emissons nexus. Prior to examining how the capital market can impact the relationship in both ways, we provide empirical contributions to the literature by analysing the bidirectional relationship, as well as the non-linear U-shaped relationship and threshold level at which renewable energy consumption and carbon emissions impact each other. The unique novelty of the study is that it sheds light on the role of the capital market in moderating the renewable energy consumption and carbon emissions nexus in developing countries. Developing economies provide an interesting case study for our empirical experiment because policymakers in this context are now viewing the capital market as an important funding tool to achieve economic development and to meet the sustainable development goals. Therefore, the emerging development of the capital market can be helpful in enhancing the two-way relationship between renewable energy consumption and carbon emissions in developing economies. Our findings show that a bidirectional relationship exists between energy and emissions. It shows that renewable energy consumption reduces carbon emissions to a certain level, and beyond that level carbon emission increases. Similar results are true for the reverse relationship. We find that the capital market enhances the negative impact of renewable energy consumption on carbon emissions while corporate bond market magnifies the reductive effect of carbon emissions on renewable energy consumption.

The rest of the paper is organised into an overview, literature review, methodology, empirical results and discussions, and conclusion and policy implication sections.

2. Literature review: theories, empirics and hypotheses development

It is evident that climate change is one of the most severe problems of the modern world. It is without doubt that the consumption of energy, in the previous decades, has become one of the significant factors that contribute to the changing climate. Given the global warming problem, scarce renewable energy sources and the fight for a green economy, the complex relationship between renewable energy consumption and environmental degradation has become a growing concern in the literature. In addition, researchers are finding it interesting to consider the role of the capital market in shaping the impact of energy consumption on environmental degradation. The literature review section has been divided into various sections to provide clarity regarding the nexus among the variables used in the study.

2.1. Bidirectional nexus between renewable energy consumption and carbon emissions

A number of studies have investigated the impact of renewable energy consumption on carbon emissions. The first kind of studies show that there is a unidirectional relationship between carbon emissions and renewable energy consumption (Haldar and Sethi Citation2021). However, the results are mixed. For instance, some studies argue for a positive energy-emissions nexus, where carbon emissions are important to climate change and therefore one key strategy can be to increase the share of renewable energy in the energy mix (Anwar et al. Citation2021; Balsalobre-Lorente and Leitão Citation2020; Ikram et al. Citation2020; Nathaniel, Anyanwu, and Shah Citation2020; Li et al. Citation2020; Fan et al., Citation2023; Hasnisah, Azlina, and Taib Citation2019; Soava et al. Citation2018; Ozturk Citation2010), while others argue for a negative energy-emissions nexus, where carbon emissions could increase the risk of negative repercussions (Feng Citation2022; Menyah and Wolde-Rufael Citation2010; Shafiei and Salim Citation2014). In addition green technology, renewable energy consumption, urbanisation and corruption-control significantly mitigate carbon emission in both the short-run and the long-run (see Behera and Dash, Citation2017). Haldar and Sethi (Citation2023) show that renewable energy consumption reduces carbon emissions significantly in the long-run. The second kind of studies argue that there is a bidirectional long-term and short-term relationship between environmental degradation and economic growth (Sahoo and Sethi Citation2022; Chontanawat Citation2020; Irandoust Citation2016; Arouri et al., Citation2012; Odhiambo, Citation2012; Soytas & Sari, Citation2009) and also between energy consumption and carbon emissions (Alharthi, Dogan, and Taskin Citation2021; Chontanawat Citation2020; Waqih et al. Citation2019). However, the above-mentioned studies have not empirically tested the bidirectional relationship between renewable energy consumption and carbon emissions in the context of developing economies. Based on this, we formulate the following hypothesis:

H1: There is a positive but bidirectional relationship between renewable energy consumption and carbon emissions.

2.2. Theoretical framework

Several studies have employed the Environmental Kuznets Curve (EKC) hypothesis to investigate the relationship between renewable energy consumption and carbon emissions in a growth model (see Haldar and Sethi Citation2023). This section provides the debate on the EKC hypothesis and how it has been used to explain the concepts of renewable energy consumption and carbon emissions.

2.2.1. Environmental Kuznets Curve Hypothesis

It has been argued that an increase in per capita income increases the level of pollution and after a certain period of time, pollution decreases along with increasing economic growth making an inverted U-shaped (Grossman and Krueger, Citation1995). Following the theoretical argument in the literature, previous studies extended their argument to test the EKC hypothesis on the relationship between renewable energy consumption, emissions of carbons and economic growth. Given the prevailing debate on the relationship between energy consumption and carbon emissions, the current study draws inspiration from the EKC to explain the inverse U-shaped energy-emission nexus. It has been proven in the literature that the linkages between energy consumption and carbon emissions are not only bidirectional (Arouri et al. Citation2012; Odhiambo, Citation2012), but non-linear (Ozturk Citation2010; Chang et al., Citation2010; Omri, Citation2013). From the theoretical perspective, the EKC hypothesis induces a non-linear relationship between renewable energy consumption and carbon emissions, which confirms that renewable energy consumption has a non-monotonic function with carbon emissions (Menyah and Wolde-Rufael Citation2010). Alharthi, Dogan, and Taskin (Citation2021) applied the quantile methodology on a dataset from MENA countries over the period 1990–2015 to analyse the factors that determine CO2 emissions. They provide evidence that renewable energy consumption reduces the level of carbon emissions and that the impact increases at higher quantiles. Further, non-renewable energy consumption increases carbon emissions while its magnitude reduces with higher quantiles (Bun and Windmeijer Citation2010). Haldar and Sethi (Citation2021) confirm the EKC hypothesis and provide evidence to support that the combined influence of institutional quality on the relationship between energy consumption and carbon emissions is significant and negative. However, empirical studies have not tested the threshold level at which the impact of carbon emissions on renewable energy consumption changes. Thus, the current study formulates the following hypothesis:

H2: Renewable energy consumption reduces carbon emissions up to a certain threshold and then begins to increase carbon emissions at an increasing level of renewable energy consumption and vice versa

2.2.2. Renewable energy consumption, capital market and carbon emissions

The energy-emission nexus and its interrelationship with other economic indicators have been intensively debated over the recent decades (Taha et al. Citation2023; Haldar and Sethi Citation2023; Citation2021; Houssam et al. Citation2023; Dash, Dash, and Sethi Citation2022; Padilla et al. Citation2022; Mohanty and Sethi Citation2022). For instance, Haldar and Sethi (Citation2023) employed the panel ARDL and 3SLS estimations to investigate the effect of renewable energy, innovation and governance on climate change and economic growth. They found that both renewable energy and corruption control are beneficial to the economy and the environment, leading to a sustainable economic growth in emerging Asia. Mohanty and Sethi (Citation2022) investigated the role of outward foreign direct investment (FDI) in the relationship between energy consumption and environmental quality in BRICS countries. They reveal that EKC hypothesis induces a greater positive impact of outward FDI and energy consumption on environmental quality. They confirm that an inverted U-shaped linkage exists between energy consumption and environmental quality when outward FDI is interacted. However, the impact of capital market in the energy-emission nexus is still developing. For instance, Akadiri, Adebayo, and Adebayo (Citation2021) have argued that finance is an important factor in coordinating and allocating resources in various fields and it is a major driver of the increase in carbon emissions, which limits regional green development to some extent. As a result, new financial instruments and policies are required to boost investment, encourage energy savings, improve environmental benefits and achieve sustainable development goals. Given the importance of financial development, significant progress has been made in the financial sector to ensure that growth in the economy does not adversely affect the natural environment and energy consumption (Khan, Yu, and Sharif Citation2021). The theoretical literature asserts that a well-functioning capital market improves projects and investments in the energy sector and also helps to reduce environmental degradation (Sinha, Shahbaz, and Sengupta Citation2018; Al-mulali et al., Citation2015; Tang & Tan, Citation2015; Shahbaz et al., Citation2012). This claim could also mean that a well-developed capital market may moderate the relationship between renewable energy consumption and carbon emissions, and therefore, an empirical understanding in establishing the impact of the capital market on the energy-emission nexus will be beneficial to policymakers and researchers.

2.2.3. Impact of capital market on the nexus between renewable energy consumption and carbon emissions

Recent studies have shown the importance of the capital market in revamping the financial and economic systems, and thus, helping to achieve the sustainable development goals (Haldar and Sethi Citation2023; Haldar et al. Citation2023; Houssam et al. Citation2023). Empirically, Sahoo and Sethi (Citation2022) employed different methodological estimations to examine the relationship between energy consumption, industrialisation, urbanisation, economic growth and financial development in India from 1980 to 2017. They found that financial development negatively affects energy consumption. Khan, Khan, and Binh (Citation2020) employ various estimation techniques to examine the heterogeneity of renewable energy consumption, CO2 emission and financial development using a panel of 192 countries. They found that renewable energy consumption has a negative effect on carbon emissions while financial development has a positive effect on carbon emissions. Xu et al. (Citation2021) show that a well-developed financial market tends to reduce carbon emissions and also results in the use of less renewable energy (Xu et al. Citation2021). Evidence has been uncovered that financial development is important in reducing carbon emission and energy consumption to a more manageable level in China (Xu et al. Citation2021) but has no significant impact on carbon emissions in MENA region (Wu et al. Citation2022). In the case of China, the net effect is lower carbon emissions per unit of GDP. An opposing view by Ji and El-Halwagi (Citation2020) asserted that the financial sector in China is positively associated with carbon emissions. Haldar and Sethi (Citation2021) analysed an interaction between institutional quality, renewable energy and CO2 emissions – and found that institutional quality is important in moderating the negative effect of renewable energy consumption on CO2 emissions. Although, a few empirical studies are available on the effect of capital market on environmental degradation and renewable energy consumption (Paramati, Alam, and Apergis Citation2018; Abbasi & Riaz, Citation2016; Wang et al. Citation2015), none of them investigates the role of the capital market (both stocks and bond market) impact on the relationship between renewable energy consumption and carbon emissions in developing economies.

Based on the theoretical and empirical reviews, we formulate the following hypotheses:

H3: Capital market plays an important moderating role in shaping the reverse causality between renewable energy consumption and carbon emissions.

3. Methodology

The study examines the bidirectional and non-linear impact of renewable energy consumption on carbon emissions. We also examine the moderating impact of the capital market on the energy-emission nexus. The study utilises a panel data from 1990 to 2020 on 138 developing countries. The selection of countries and the study period is based on data availability. The study utilises the dynamic System Generalised Method of Moment (GMM) by following recent studies by Khan et al. (Citation2023), Jiang and Khan (Citation2023), Mirziyoyeva and Salahodjaev (Citation2022), and Sheraz et al. (Citation2022). This is because the model has the ability to determine short- and long-run values of coefficients and it makes it possible to choose which explanatory variables are potentially endogenous or exogenous (see Hayakawa Citation2015; Bun and Windmeijer Citation2010). The robustness of the use of the dynamic System GMM is further explained later in this section.

3.1. Model specification and measurements

In this study, we show a bidirectional and a U-shaped linkage between renewable energy consumption and the carbon emissions as proven by the EKC in many regions and countries (see Dhahri & Omri, Citation2020; Khan, Khan, and Binh Citation2020; Citation2022; Gaies et al. Citation2019; Arouri et al. Citation2012; Odhiambo, Citation2012). We specify the simultaneous and dynamic relationships using the dynamic Systemic GMM estimations. The empirical models can be summarised as follows:

(1)

(1)

(2)

(2) where subscript j denotes cross-sectional dimension (country specifics), j = 1, … , M;

denotes the time series dimension (time),

= 1, … , T.

are the constant terms in the models;

represent the coefficient of the lag of the dependent variables in Equations (1) and 2 respectively (i.e. carbon emissions and renewable energy consumption);

and

represent the coefficients of renewable energy consumption and carbon emissions respectively;

represent the coefficients of the squared terms of the respective variables in the equations;

represent the coefficients of capital market indicators in the equations;

k = 5, … , N, represent the regression coefficient parameters for vector C (control variables) to be estimated in the two-equation models;

the idiosyncratic error terms for Equations (1) and (2) respectively, which controls for unit-specific residual

in the models for the jth country at period t.

In the above equations, the key variables included in this study are renewable energy consumption, carbon emissions (see, recent studies of Khan, Khan, and Binh (Citation2020; Citation2021), and capital market indicators (see, Paramati, Alam, and Apergis Citation2018; Mu, Phelps, and Stotsky Citation2013).

In Equation (1), CO2 is the dependent variable, which is measured as carbon emissions expressed in terms of metric tons per capita and has been used in the studies of Szetela et al. (Citation2022), Ekwueme, Zoaka, and Alola (Citation2021), Joo, Kim, and Yoo (Citation2015), etc. Data on carbon dioxide emission were obtained from the World Development Indicator of the World Bank. Higher values suggest a greater level of carbon dioxide emissions.

In Equation (2), renewable energy consumption is the dependent variable, which is measured as the percent of total energy consumption that is renewable. This has been used in the studies of Haldar and Sethi (Citation2023; Citation2021), Mohanty and Sethi (Citation2022), Szetela et al. (Citation2022), Ekwueme, Zoaka, and Alola (Citation2021), Khan, Yu, and Sharif (Citation2021; Citation2020), and Joo, Kim, and Yoo (Citation2015). Data on renewable energy consumption were obtained from the World Development Indicator of the World Bank. Higher values suggest greater use of renewable energy mix.

In both equations, we introduce the capital market indicators because the role of the financial sector in promoting economic development cannot be overemphasised (see Akadiri, Adebayo, and Adebayo Citation2021; Khan, Yu, and Sharif Citation2021). We decompose capital market into two indicators, namely: (1) stock market development and (2) bond market development. Stock market development is measured as the market capitalisation of listed domestic companies as a percent of GDP. Bond market development is measured as the corporate bond issuance volume as a percent GDP. These have been defined so that higher values indicate greater capital market (see Adelegan and Radzewicz-Bak Citation2009; Mu, Phelps, and Stotsky Citation2013; and Paramati, Alam, and Apergis Citation2018). Data on the capital market were obtained from the World Development Indicators.

In both equations, C is a vector of control variables, which are described in .Footnote1

3.1.1 Bidirectional relationship and non-linear relationship

Equations (1) and (2) estimate bidirectional and non-linear relationships between carbon emissionsFootnote2 and renewable energy consumption. In terms of the bidirectional relationship, we expect a negative bi-causal effect between carbon emissions and renewable energy consumption. This is because countries with greater carbon emissions have lesser incentives to use renewable energy and vice versa.

Following the EKC relationship, we extend the estimations by introducing the square term of renewable energy to observe the level of renewable energy consumption required to change the level of impact on carbon emissions (Equation (1)). We also introduce the square term of carbon emissions to observe the level of carbon emissions required to change the level of impact on renewable energy consumption (Equation (2)). In both equations, we expect a non-linear U-shaped energy-emission nexus (see Haldar and Sethi Citation2021). This means that, in Equation (1), renewable energy worsens in the early stages of carbon emissions until it reaches a turning point after which it increases with greater emissions. Similarly, in Equation (2), carbon emission reduces at the initial levels of renewable energy consumption until it reaches a turning point after which it rises with an additional increase in renewable energy. Thus, we estimate the threshold point at which carbon emissions (renewable energy consumption) begin to increase renewable energy consumption (carbon emissions).

In both equations, we introduce the capital market indicators to observe their impact on renewable energy consumption and carbon emissions. In Equation (1), we expect the capital market indicators to reduce carbon emissions (negative impact) and improve environmental degradation, which is consistent with the work of Paramati et al. (Citation2016) while in Equation (2), we expect capital market to increase the level of renewable energy consumption.

3.2. Interactions

To capture possible unobserved heterogeneity, and to analyse the impact of the capital market in moderating the interrelationship between renewable energy consumption and carbon emissions, we expand Equations (1) and (2) by estimating the following models which include the interaction terms:

(3)

(3)

(4)

(4) where

and

are the coefficient parameters and

is the unobserved country-specific effect assumed to be independent and identically distributed,

represent other control variables and

is the stochastic component defined as

.

Following Brambor et al. (Citation2006), we compute the marginal effects of renewable energy consumption and carbon emissions in Equations (3) and (4) respectively. The marginal effects tell us how the capital market affects the interrelationship between renewable energy consumption and carbon emissions.

We compute the marginal effect from Equations (3) and (4) as follows:

(5)

(5)

(6)

(6) From Equations (5) and (6), we expect

to moderate the impact of renewable energy consumption on carbon emissions, and the reverse.

3.3 Estimation technique

To enhance reliability, efficiency and accuracy of the result, the study employs a number of techniques. First, the study screens for outliers in order to reduce the biases caused by outliers. Hence, no evidence of outliers was identified. Second, normality of each variable is assessed by using SWILK normality test. Third, the study employs the Pearson’s correlation to screen for multicollinearity and realizes the absence of multicollinearity (Allison, Citation2012). This was conducted to avoid spurious results. Similarly, cross-sectional dependence is tested using the Pesaran (Citation2015) approach because our panel is unbalanced. With a null hypothesis of weak cross-sectional dependence, the Pesaran (Citation2015) results fail to reject the null hypothesis of weak cross-sectional dependence, implying that the severity of and the presence of cross-sectional dependence can be ignored for the models.

4. Empirical results and discussions

The results are presented based on the dynamic System GMM estimations. shows the descriptive statistics of the variables while shows the correlation coefficient matrix of the variables (see Appendix).

We begin by presenting the results on the bidirectional and non-linear impact of renewable energy consumption and carbon emissions. In we find that renewable energy consumption has a negative effect on carbon emissions. This affirms the findings of Haldar and Sethi (Citation2021) who reveal that renewable energy consumption reduces emissions significantly in the long run. This means countries that develop and promote the use of renewable energy are able to reduce the levels of carbon emissions. This supports the works of Shafiei and Salim (Citation2014) and Sinha, Shahbaz, and Sengupta (Citation2018), who found that an increase in the consumption of renewable energy reduces carbon emissions in OECD countries. This is true because the utilisation of clean energy has not yet reached the desired level to increase carbon emissions. However, we observe a positive and significant coefficient of the square term of renewable energy consumption. This is suggestive of a U-shaped relationship between renewable energy consumption and carbon emission. Our results agree with the argument by Bhujabal, Sethi, and Padhan (Citation2021), who document that an increase in a per capita income increases the level of pollution and after a certain period of time, pollution decreases along with an increasing level of economic growth – leading to an inverted U-shaped. Our results can be explained, based on the EKC hypothesis that the initial levels of renewable energy reduce the levels of carbon emissions but additional level of the use of renewable energy leads to environmental degradation. Renewable energy consumption is costly and thus, increasing the level of renewable energy consumption (as a result of growing income) will reduce CO2 emissions, but beyond a certain point, an increase in the use of renewable energy consumption will increase economic activity and produce more emissions. Based on the EKC hypothesis, more economic activities inexorably hurt the environment, and the demand for a good-quality environment will increase as income increases (Grossman and Krueger Citation1991; Pandey and Rastogi Citation2019). Thus, as economic activities expand, the demand for renewable energy sources will increase, causing pollution and deterioration of the environment.

Table 1. Effect of renewable energy consumption and capital market on carbon emission.

For policy implication, we estimate the threshold point above which the use of renewable energy may not yield a desirable outcome for the environment. For instance, in models 1, the threshold level is 71.03.Footnote4 This means that carbon emission is reducing to 71.03 of renewable energy consumption, but beyond this point, carbon emission will increase. The implication is that policymakers that control the level of renewable energy to an optimal threshold level are able to reduce carbon emissions that may not be detrimental to the environment.

In , the capital market has a negative impact on carbon emission. In model 1, stock market capitalisation to GDP has a negative and significant relationship with carbon emission. This supports the results of Sadorsky (Citation2011) and implies that countries that develop their stock market are able to attract more business activities by accessing equity financing. The significant growth in business may contribute to making renewable energy efficient and hence reduce carbon emissions. In relation to the bond market, model 2 shows that corporate bond issuance to GDP has a negative and significant relationship with carbon emission. This implies that countries that provide more capital from the corporate bond market are able to support sustainable environmental projects and help to reduce environmental degradation.

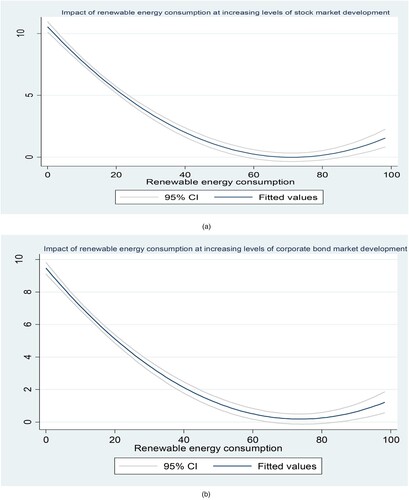

Given the important role that the capital markets play in developing economies, we interact renewable energy consumption with the two measures of capital market separately and estimate the overall impact (see ). Consistent with Brambor et al. (Citation2006), there is a need to compute the overall effect or marginal effects of the interactions between renewable energy consumption and capital market, to give a meaningful economic interpretation. As was found in , generally, the coefficient of renewable energy consumption is negative and significant (i.e. the unconditional effect). Further, we observe that the coefficient of the interaction term between energy consumption and the stock market is significant and negative at 1% (see model 4). Thus, the conditional effect of renewable energy consumption is negative and significant. For instance, in model 4, the marginal effect of renewable energy consumption is −0.1511[−0.144 + (−0.000141*stock market capitalisation to GDP)], when stock market capitalisation to GDP assumes an average of 50.546 (see (model 4)). This suggests that the negative impact of renewable energy consumption on carbon emission is enhanced when countries increase their stock market activities (see (a)). Therefore, countries that develop their stock market have the incentives to increase funding sources for the investments in renewable energy projects which in turn leads to further reduction in the level of carbon emissions. However, the overall marginal effect of renewable energy consumption on carbon emissions is less negative and significant when interacted with the bond market indicator (see model 5, and (b)). The implication is that countries that develop their bond market are able to increase debt financing sources for investments in order to induce a less reductive effect of renewable energy consumption on carbon emission. The results are consistent with the work of Mohanty and Sethi (Citation2022) who investigated the role of outward foreign direct investment (FDI) in the relationship between energy consumption and environmental quality in BRICS countries. They reveal that EKC hypothesis aids in improving the impact of energy consumption on environmental quality at increasing levels of outward FDI.

Figure 1. (a) Effect of renewable energy consumption on carbon emissions at levels of stock market capitalization influence of renewable energy consumption on carbon emissions at levels of stock market development.

Table 2. System dynamic GMM estimation: interaction effect of renewable energy consumption, capital market and carbon emissions.

For a proper interpretation of the results (Brambor et al., Citation2006), it is apparent from (a and b) that the impact of renewable energy consumption on carbon emissions decreases significantly at higher levels of capital market indicators. The implication is that in developing the capital market, governments tend to enforce actions and regulations necessary for investing in renewable energy projects that can minimise the deterioration of the environment.

The significant control variables have their expected signs.

In , carbon emission has a negative and significant relationship with renewable energy consumption (see model 6). This means that countries with more carbon emissions use less renewable sources of energy. This is true because higher emission of carbons leads to greater deterioration of the environment, which induces policies that focus more on improving the environment and reducing developments in renewable energy. However, we observe that the coefficient of the square term of carbon emission is positive. The estimated threshold suggests that initial increase in the level of carbon emissions suggests less use of renewable energy consumption up to 2.5 thresholdFootnote5 level of carbon emissions and beyond this threshold, renewable energy consumption begin to increase (see models 6–8). We observe that stock market capitalisation of GDP has a positive and significant relationship with renewable energy consumption. Similarly, corporate bond market indicators positively affect renewable energy consumption. This means countries that develop their capital markets have the capacity to invest their proceeds into renewable energy sources or projects may in turn generate greater investment opportunities that cause an increase in the overall use of renewable energy. This is consistent with the findings of Xu et al. (Citation2021) who provide evidence that financial development is important in reducing carbon emission and energy consumption to a more manageable level in China. Similarly, our results are in line with the findings of Sahoo and Sethi (Citation2022) who found that financial development negatively affects energy consumption.

Table 3. System dynamic GMM Estimation: Impact of carbon emission and capital market on renewable energy.

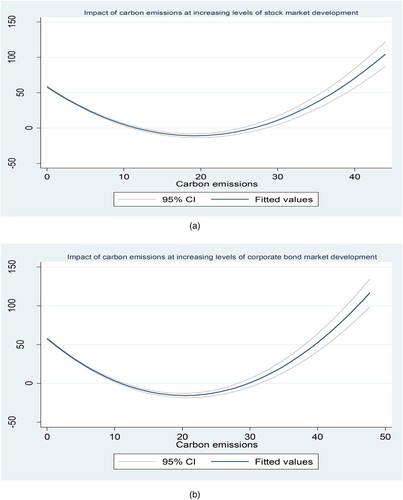

In , we examine the interactive effect of carbon emission and capital market on renewable energy. To give a meaningful economic interpretation, we estimate the marginal effect of carbon emission on renewable energy when interacted with the capital market indicators. In model 9, we observe that stock market has no joint effect on renewable energy consumption. However, in model 10, the net effect or marginal impact of carbon emission is more negative than the unconditional effect of carbon emissions (see (a and b)). This suggests that an increase in the level of corporate bond market development leads to a greater reductive effect of carbon emissions on renewable energy consumption.

Figure 2. (a) Effect of carbon emissions on renewable energy consumption at levels of stock market capitalisation influence of carbon emissions on renewable energy consumption at levels of stock market development; (b) Effect of carbon emissions on renewable energy consumption at levels of bond market issuance influence of carbon emissions on renewable energy consumption at levels of bond market development.

Table 4. System dynamic GMM Estimation: interaction effect of carbon emission and capital market on renewable energy.

It can be observed that stock market does not have any significant effect on the emissions-energy nexus but the bond market has a significant effect on the emissions-energy nexus. This is because corporate bond markets could capture green bonds that are targeted at renewable energy but stock investors in developing countries may probably invest in other sectors of the economy and reduce their involvement in renewable energy investments. Hence, the need to improve stock market development in developing economies is important to improve on the nexus between emissions and renewable energy.

In general, our results confirm the argument of Haldar and Sethi (Citation2021), who confirm that institutional quality moderates energy consumption and strengthen its effectiveness in abating carbon emissions through the EKC hypothesis. Thus, institutional quality, in this case, a strong capital market is important in moderating the nexus between renewable energy consumption and carbon emissions in the presence of the EKC hypothesis.

5. Conclusions and policy implications

Given the important role that the capital market plays in the economy, this study aims to examine the impact of the capital market on the relationship between energy consumption and carbon emissions in developing countries. We test our argument on a sample of 138 developing countries, over the period, 1990–2020, using a two-step dynamic System Generalised Methods of Moments, with collapsed instruments and Windmeijer robust standard errors. The study confirms the existence of a bidirectional energy-emission nexus and finds an evidence to support a ‘U-shaped’ relationship between renewable energy consumption and carbon emission. It reveals that carbon emission is reducing to 71.03 threshold of renewable energy consumption, but beyond this threshold point, carbon emission tends to increase. Similarly, the initial level of carbon emissions reduces the use of renewable energy but beyond a 2.5 threshold of carbon emissions, renewable energy consumption begins to increase. The study finds that the capital market (i.e. stock market and bond market) significantly reduces carbon emissions and also enhance the levels of renewable energy consumption. The study provides evidence to support that the capital market (i.e. both the stock and bond markets) enhances the negative impact of renewable energy consumption on carbon emissions. It also shows that bond market magnifies the reductive effect of carbon emissions on renewable energy consumption.

The major implication from our work is that renewable energy consumption and carbon emissions do matter for sustainable growth of every economy. In terms of the kind of relationship that exists between renewable energy consumption and carbon emissions, our results are in line with Soava et al. (Citation2018), who provided evidence that renewable energy consumption supports growth and the relationship is bidirectional. Athough, our model did not test this empirically, we do recognise that our bidirectional energy-emission nexus is important for the achievement of sustainable economic growth, as evident in the studies of Simionescu, Păuna, and Diaconescu (Citation2020), Ntanos et al. (Citation2018) and Bilan et al. (Citation2019). The implication is that future studies should explore how the bicausality of renewable energy consumption and carbon emissions contribute to sustainable economic growth. Although, our results did not test the influence of renewable energy and carbon emissions on economic growth, we explain that the interrelationships between renewable energy and carbon emissions are not direct but it is nonlinear and conditioned on the capital market. The implication is that policymakers and researchers should leverage this opportunity to explore how the energy-emission nexus is influenced by the capital market to yield a sustainable economic growth in the developing economies.

Considering our findings, developing economies should focus on policies that promote the efficient use of renewable energy sources to prevent environmental deterioration. The policies should come up with measures for determining the optimal level of the use of renewable energy that may yield a desirable outcome of carbon emissions. This is particularly crucial for higher carbon-emitting countries. In addition, policymakers should prioritise the promotion of investment activities in the capital market in order to increase the consumption of renewable energy sources and reduce carbon emissions. Policymakers in the region should implement policies and enforce actions that strengthen the corporate bond market in order to yield a desirable outcome in the emission-energy framework.

5.1. Limitation and future recommendation

The study is limited to only developing economies. It was not able to collect data on various sources of renewable energy and indicators of the environment, social and governance from developing economies perspective. Acquiring this data was very difficult because some are not available publicly as a secondary source. Future research is required to explore this study (including data extension) to other regions in the world to reveal how applicable this model fits the other parts of the world.

Declarations

Availability of data and materials

The datasets used and/or analysed during the current study are available (with corresponding author) on reasonable request.

Citation for available data

databank.worldbank.org/reports.aspx?source = global-financial-development databank.worldbank.org/source/world-development-indicators

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 See Appendix 1.

2 https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Glossary:Carbon_dioxide_emissions

3 The use of higher lags of the respondent variable as instruments hinges critically on the assumption of no autocorrelation in the initial disturbance term.

4 From equation 1: . From ,

5 From equation 2: . From :

References

- Abbasi, F., and K. Riaz. 2016. “CO2 Emissions and Financial Development in an Emerging Economy: An Augmented VAR Approach.” Energy Policy 90: 102–114.

- Adelegan, J., and B. Radzewicz-Bak. 2009. What Determines Bond Market Development in Sub-Saharan Africa, IMF Working Paper No. 09/213. Inter-national Monetary Fund, Washington.

- Aggarwal, R., and J. W. Goodell. 2009. “Markets and Institutions in Financial Intermediation: National Characteristics as Determinants.” Journal of Banking & Finance 33 (10): 1770–1780.

- Akadiri, S. S., T. S. Adebayo, and S. Adebayo. 2021. “Asymmetric Nexus Among Financial Globalization, Non-Renewable Energy, Renewable Energy Use, Economic Growth, and Carbon Emissions: Impact on Environmental Sustainability Targets in India.” Environmental Science and Pollution Research 29: 16311–16323. https://doi.org/10.1007/s11356-021-16849-0.

- Al-Mulali, U., I. Ozturk, and H. H. Lean. 2015. “The Influence of Economic Growth, Urbanization, Trade Openness, Financial Development, and Renewable Energy on Pollution in Europe.” Natural Hazards 79: 621–644.

- Alharthi, M., E. Dogan, and D. Taskin. 2021. “Analysis of CO2 Emissions and Energy Consumption by Sources in MENA Countries: Evidence from Quantile Regressions.” Environmental Science and Pollution Research 28: 38901–38908. https://doi.org/10.1007/s11356-021-13356-0.

- Allison, P. D. 2012. Logistic Regression using SAS: Theory and Application. SAS Institute.

- Anwar, A., M. Siddique, E. Dogan, and A. Sharif. 2021. “The Moderating Role of Renewable and non-Renewable Energy in Environment-Income Nexus for ASEAN Countries: Evidence from Method of Moments Quantile Regression.” Renewable Energy 164: 956–967. https://doi.org/10.1016/j.renene.2020.09.128.

- Appiah, K., J. Du, M. Yeboah, and R. Appiah. 2019. “Causal Correlation Between Energy use and Carbon Emissions in Selected Emerging Economies—Panel Model Approach.” Environmental Science and Pollution Research 26 (8): 7896–7912. https://doi.org/10.1007/s11356-019-04140-2.

- Arellano, M., and S. Bond. 1991. “Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations.” The Review of Economic Studies 58 (2): 277–297. https://doi.org/10.2307/2297968.

- Arouri, M. E. H., A. B. Youssef, H. M'henni, & H. Rault. 2012. “Energy Consumption, Economic Growth and CO2 Emissions in Middle East and North African Countries.” Energy Policy 45: 342–349.

- Balsalobre-Lorente, D., and N. C. Leitão. 2020. “The Role of Tourism, Trade, Renewable Energy use and Carbon Dioxide Emissions on Economic Growth: Evidence of Tourism-led Growth Hypothesis in EU-28.” Environmental Science and Pollution Research 27 (36): 45883–45896. https://doi.org/10.1007/s11356-020-10375-1.

- Baum, A., C. Checherita-Westphal, and P. Rother. 2013. “Debt and Growth: New Evidence for the Euro Area.” Journal of International Money and Finance 32: 809–821.

- Behera, S. R., and D. P. Dash. 2017. “The Effect of Urbanization, Energy Consumption, and Foreign Direct Investment on the Carbon Dioxide Emission in the SSEA (South and Southeast Asian) Region.” Renewable and Sustainable Energy Reviews 70: 96–106.

- Bhujabal, P., N. Sethi, and P. C. Padhan. 2021. “ICT, Foreign Direct Investment and Environmental Pollution in Major Asia Pacific Countries.” Environmental Science and Pollution Research 28 (31): 42649–42669. https://doi.org/10.1007/s11356-021-13619-w.

- Bilan, Y., D. Streimikiene, T. Vasylieva, O. Lyulyov, T. Pimonenko, and A. Pavlyk. 2019. “Linking Between Renewable Energy, CO2 Emissions, and Economic Growth: Challenges for Candidates and Potential Candidates for the EU Membership.” Sustainability 11 (6): 1528. https://doi.org/10.3390/su11061528.

- Blundell, R., and S. Bond. 2000. “GMM Estimation with Persistent Panel Data: An Application to Production Functions.” Econometric Reviews 19 (3): 321–340.

- Brambor, T., W. R. Clark, and M. Golder. 2006. “Understanding Interaction Models: Improving Empirical Analyses.” Political Analysis 14 (1): 63–82.

- Bun, M. J., and F. Windmeijer. 2010. “The Weak Instrument Problem of the System GMM Estimator in Dynamic Panel Data Models.” The Econometrics Journal 13 (1): 95–126. https://doi.org/10.1111/j.1368-423X.2009.00299.x.

- Chang, Y., R. J. Ries, and Y. Wang. 2010. “The Embodied Energy and Environmental Emissions of Construction Projects in China: An Economic Input–Output LCA Model.” Energy Policy 38 (11): 6597–6603.

- Chontanawat, J. 2020. “Relationship Between Energy Consumption, CO2 Emission and Economic Growth in ASEAN: Cointegration and Causality Model.” Energy Reports 6: 660–665. https://doi.org/10.1016/j.egyr.2019.09.046.

- Danish-Baloch, M. A., and S. Suad. 2018. “Modeling the Impact of Transport Energy Consumption on CO2 Emission in Pakistan: Evidence from ARDL Approach.” Environmental Science and Pollution Research 25: 9461–9473.

- Dash, D. P., A. K. Dash, and N. Sethi. 2022. “Designing Hydro-Energy led Economic Growth for Pollution Abatement: Evidence from BRICS.” Environmental Science and Pollution Research 29 (21): 31252–31269. https://doi.org/10.1007/s11356-021-17890-9.

- De Haas, R., and A. Popov. 2016. Working Paper Series-Finance and carbon emissions-No 2318/September 2019.

- Destek, M. A., and S. A. Sarkodie. 2019. “Investigation of Environmental Kuznets Curve for Ecological Footprint: The Role of Energy and Financial Development.” Science of the Total Environment 650: 2483–2489.

- Dhahri, S., and A. Omri. 2020. “Does Foreign Capital Really Matter for the Host Country Agricultural Production? Evidence from Developing Countries.” Review of World Economics 156: 153–181.

- Ekwueme, D. C., J. D. Zoaka, and A. A. Alola. 2021. “Carbon Emission Effect of Renewable Energy Utilization, Fiscal Development, and Foreign Direct Investment in South Africa.” Environmental Science and Pollution Research 28 (31): 41821–41833. https://doi.org/10.1007/s11356-021-13510-8.

- Energy Information Agency (EIA). 2017. How much of the U.S. carbon dioxide emissions are associated with electricity generation?

- Fan, A., J. Yan, Y. Xiong, Y. Shu, X. Fan, Y. Wang, …, J. Chen. 2023. “Characteristics of Real-World Ship Energy Consumption and Emissions Based on Onboard Testing.” Marine Pollution Bulletin 194: 115411.

- Feng, H. 2022. “The Impact of Renewable Energy on Carbon Neutrality for the Sustainable Environment: Role of Green Finance and Technology Innovations.” Frontiers In Environmental Science 10.

- Gaies, B., O. Kaabia, R. Ayadi, K. Guesmi, and I. Abid. 2019. “Financial Development and Energy Consumption: Is the MENA Region Different.” Energy Policy 135: 111000.

- Grossman, G., and A. B. Krueger. 1991. Environmental Impacts of a North American Free Trade Agreement; National Bureau of Economic Research 1991. Working Paper 3914. Cambridge, MA, USA: NBER, 1991.

- Grossman, G. M., and A. B. Krueger. 1995. “Economic Growth and the Environment.” The Quarterly Journal of Economics 110 (2): 353–377.

- Haldar, A., and N. Sethi. 2021. “Effect of Institutional Quality and Renewable Energy Consumption on CO2 Emissions−an Empirical Investigation for Developing Countries.” Environmental Science and Pollution Research 28 (12): 15485–15503. https://doi.org/10.1007/s11356-020-11532-2.

- Haldar, A., and N. Sethi. 2023. “The Effects of Renewable Energy, Innovation, and Governance on Climate Change and Economic Growth—Investigating the Opportunities and Challenges for Emerging Asia.” Asian Economics Letters 4 (2), https://doi.org/10.46557/001c.73683.

- Haldar, A., N. Sethi, P. K. Jena, and P. C. Padhan. 2023. “Towards Achieving Sustainable Development Goal 7 in sub-Saharan Africa: Role of Governance and Renewable Energy.” Sustainable Development.

- Haldar, A., S. Sucharita, D. P. Dash, N. Sethi, and P. C. Padhan. 2023. “The Effects of ICT, Electricity Consumption, Innovation and Renewable Power Generation on Economic Growth: An Income Level Analysis for the Emerging Economies.” Journal of Cleaner Production 384: 135607. https://doi.org/10.1016/j.jclepro.2022.135607.

- Hasnisah, A., A. A. Azlina, and C. M. I. C. Taib. 2019. “The Impact of Renewable Energy Consumption on Carbon Dioxide Emissions: Empirical Evidence from Developing Countries in Asia.” International Journal of Energy Economics and Policy 9 (3): 135. https://doi.org/10.32479/ijeep.7535.

- Hayakawa, K. 2015. “The Asymptotic Properties Of The System Gmm Estimator In Dynamic Panel Data Models When Bothnandtare Large.” Econometric Theory 31 (3): 647–667. https://doi.org/10.1017/S0266466614000449.

- Houssam, N., D. M. Ibrahiem, S. Sucharita, K. M. El-Aasar, R. R. Esily, and N. Sethi. 2023. “Assessing the Role of Green Economy on Sustainable Development in Developing Countries.” Heliyon 1–5. https://doi.org/10.1016/j.heliyon.2023.e17306

- Ikram, M., Q. Zhang, R. Sroufe, and S. Z. A. Shah. 2020. “Towards a Sustainable Environment: The Nexus Between ISO 14001, Renewable Energy Consumption, Access to Electricity, Agriculture and CO2 Emissions in SAARC Countries.” Sustainable Production and Consumption 22: 218–230. https://doi.org/10.1016/j.spc.2020.03.011.

- Im, K. S., M. H. Pesaran, and Y. Shin. 2003. “Testing for Unit Roots in Heterogeneous Panels.” Journal of Econometrics 115 (1): 53–74.

- Irandoust, M. 2016. “The Renewable Energy-Growth Nexus with Carbon Emissions and Technological Innovation: Evidence from the Nordic Countries.” Ecological Indicators 69: 118–125. https://doi.org/10.1016/j.ecolind.2016.03.051.

- Ji, C., and M. M. El-Halwagi. 2020. “A Data-Driven Study of IMO Compliant Fuel Emissions with Consideration of Black Carbon Aerosols.” Ocean Engineering 218: 108241.

- Jiang, Y., and H. Khan. 2023. “The Relationship Between Renewable Energy Consumption, Technological Innovations, and Carbon Dioxide Emission: Evidence from two-Step System GMM.” Environmental Science and Pollution Research 30 (2): 4187–4202. https://doi.org/10.1007/s11356-022-22391-4.

- Joo, Y. J., C. S. Kim, and S. H. Yoo. 2015. “Energy Consumption, Co2Emission, and Economic Growth: Evidence from Chile.” International Journal of Green Energy 12 (5): 543–550. https://doi.org/10.1080/15435075.2013.834822.

- Katircioğlu, S. T., and N. Taşpinar. 2017. “Testing the Moderating Role of Financial Development in an Environmental Kuznets Curve: Empirical Evidence from Turkey.” Renewable and Sustainable Energy Reviews 68: 572–586.

- Katsampoxakis, I., A. Christopoulos, P. Kalantonis, and V. Nastas. 2022. “Crude oil Price Shocks and European Stock Markets During the Covid-19 Period.” Energies 15 (11): 4090. https://doi.org/10.3390/en15114090.

- Khan, S. A. R., D. I. Godil, Z. Yu, F. Abbas, M. A. Shamim. 2022. “Adoption of Renewable Energy Sources, low-Carbon Initiatives, and Advanced Logistical Infrastructure—an Step Toward Integrated Global Progress.” Sustainable Development 30 (1): 275–288. https://doi.org/10.1002/sd.2243.

- Khan, H., I. Khan, and T. T. Binh. 2020. “The Heterogeneity of Renewable Energy Consumption, Carbon Emission and Financial Development in the Globe: A Panel Quantile Regression Approach.” Energy Reports 6: 859–867.

- Khan, H., L. Weili, I. Khan, and J. Zhang. 2023. “The Nexus Between Natural Resources, Renewable Energy Consumption, Economic Growth, and Carbon Dioxide Emission in BRI Countries.” Environmental Science and Pollution Research 30 (13): 36692–36709. https://doi.org/10.1007/s11356-022-24193-0.

- Khan, S. A. R., Z. Yu, and A. Sharif. 2021. “No Silver Bullet for De-Carbonization: Preparing for Tomorrow, Today.” Resources Policy 71: 101942. https://doi.org/10.1016/j.resourpol.2020.101942. resourpol.2020.101942.

- Krishnan, S. K., S. Kandasamy, and K. Subbiah. 2021. “Fabrication of Microbial Fuel Cells with Nanoelectrodes for Enhanced Bioenergy Production.” In Nanomaterials, 677–687. Academic Press. Application in Biofuels and Bioenergy Production System. https://doi.org/10.1016/B978-0-12-822401-4.00003-9

- Li, Z. Z., R. Y. M. Li, M. Y. Malik, M. Murshed, Z. Khan, and M. Umar. 2020. “Determinants of Carbon Emission in China: How Good is Green Investment?” Sustain Prod Consumption 27: 392–401.

- Menyah, K., and Y. Wolde-Rufael. 2010. “Energy Consumption, Pollutant Emissions and Economic Growth in South Africa.” Energy Economics 32 (6): 1374–1382. https://doi.org/10.1016/j.eneco.2010.08.002.

- Mirziyoyeva, Z., and R. Salahodjaev. 2022. “Renewable Energy and CO2 Emissions Intensity in the top Carbon Intense Countries.” Renewable Energy 192: 507–512. https://doi.org/10.1016/j.renene.2022.04.137.

- Mohanty, S., and N. Sethi. 2022. “The Energy Consumption-Environmental Quality Nexus in BRICS Countries: The Role of Outward Foreign Direct Investment.” Environmental Science and Pollution Research 29 (13): 19714–19730. https://doi.org/10.1007/s11356-021-17180-4.

- Moodley, P. 2021. “Sustainable Biofuels: Opportunities and Challenges.” Sustainable Biofuels 1: 1–20. https://doi.org/10.1016/B978-0-12-820297-5.00003-7

- Mu, Y., P. Phelps, and J. G. Stotsky. 2013. “Bond Markets in Africa.” Review of Development Finance 3: 121–135. https://doi.org/10.1016/j.rdf.2013.07.001.

- Mukhtarov, S., F. Aliyev, J. Aliyev, and R. Ajayi. 2023. “Renewable Energy Consumption and Carbon Emissions: Evidence from an Oil-Rich Economy.” Sustainability 15 (1): 134. https://doi.org/10.3390/su15010134.

- Nathaniel, S., O. Anyanwu, and M. Shah. 2020. “Renewable Energy, Urbanization, and Ecological Footprint in the Middle East and North Africa Region.” Environmental Science and Pollution Research 27 (13): 14601–14613. https://doi.org/10.1007/s11356-020-08017-7.

- Ntanos, S., M. Skordoulis, G. Kyriakopoulos, G. Arabatzis, M. Chalikias, S. Galatsidas, A. Batzios, and A. Katsarou. 2018. “Renewable Energy and Economic Growth.” Evidence from European Countries. Sustainability 10 (8): 2626.

- Odhiambo, N. M. 2012. “Economic Growth and Carbon Emissions in South Africa: An Empirical Investigation.” Journal of Applied Business Research (JABR) 28 (1): 37–46.

- OECD. 2021. Financial Markets and Climate Transition: Opportunities, Challenges and Policy Implications, OECD Paris, https://www.oecd.org/finance/Financial-Markets-and-Climate-Transition-Opportunities-challenges-and-policy-implications.htm.

- Omri, A. 2013. “CO2 Emissions, Energy Consumption and Economic Growth Nexus in MENA Countries: Evidence from Simultaneous Equations Models.” Energy Economics 40: 657–664.

- Ozturk, I. 2010. “A Literature Survey on Energy–Growth Nexus.” Energy Policy 38 (1): 340–349. https://doi.org/10.1016/j.enpol.2009.09.024.

- Padilla, M. A. E., L. Sugiharti, H. Rohmawati, and N. Sethi. 2022. “Nexus Between Technological Innovation, Renewable Energy, and Human Capital on the Environmental Sustainability in Emerging Asian Economies: A Panel Quantile Regression Approach.” Energies 15(7).

- Pandey, K. K., and H. Rastogi. 2019. “Effect of Energy Consumption & Economic Growth on Environmental Degradation in India: A Time Series Modelling.” Energy Procedia 158: 4232–4237. https://doi.org/10.1016/j.egypro.2019.01.804.

- Paramati, S. R., M. S. Alam, and N. Apergis. 2018. “The Role of Stock Markets on Environmental Degradation: A Comparative Study of Developed and Emerging Market Economies Across the Globe.” Emerging Markets Review 35: 19–30. https://doi.org/10.1016/j.ememar.2017.12.004.

- Paramati, S. R., M. Ummalla, and N. Apergis. 2016. “The Effect of Foreign Direct Investment and Stock Market Growth on Clean Energy Use Across a Panel of Emerging Market Economies.” Energy Economics 56: 29–41. https://doi.org/10.1016/j.eneco.2016.02.008.

- Pata, U. K. 2018. “Renewable Energy Consumption, Urbanization, Financial Development, Income and CO2 Emissions in Turkey: Testing EKC Hypothesis with Structural Breaks.” Journal of Cleaner Production 187: 770–779.

- Pesaran, M. H. 2015. “Testing Weak Cross-Sectional Dependence in Large Panels.” Econometric Reviews 34 (6-10): 1089–1117.

- Sadorsky, P. 2011. “Financial Development and Energy Consumption in Central and Eastern European Frontier Economies.” Energy Policy 39 (2): 999–1006.

- Sahoo, M., and N. Sethi. 2022. “The Dynamic Impact of Urbanization, Structural Transformation, and Technological Innovation on Ecological Footprint and PM2.5: Evidence from Newly Industrialized Countries.” Environment, Development and Sustainability 24 (3): 4244–4277. https://doi.org/10.1007/s10668-021-01614-7.

- Sarkodie, S. A., and V. Strezov. 2019. “Effect of Foreign Direct Investments, Economic Development and Energy Consumption on Greenhouse Gas Emissions in Developing Countries.” Science of the Total Environment 646: 862–871.

- Shafiei, S., and R. A. Salim. 2014. “Non-renewable and Renewable Energy Consumption and CO2 Emissions in OECD Countries: A Comparative Analysis.” Energy Policy 66: 547–556. https://doi.org/10.1016/j.enpol.2013.10.064.

- Shahbaz, M., H. H. Lean, and M. S. Shabbir. 2012. “Environmental Kuznets Curve Hypothesis in Pakistan: Cointegration and Granger Causality.” Renewable and Sustainable Energy Reviews 16 (5): 2947–2953.

- Sheraz, M., X. Deyi, M. Z. Mumtaz, and A. Ullah. 2022. “Exploring the Dynamic Relationship Between Financial Development, Renewable Energy, and Carbon Emissions: A new Evidence from Belt and Road Countries.” Environmental Science and Pollution Research 29 (10): 14930–14947. https://doi.org/10.1007/s11356-021-16641-0.

- Simionescu, M., C. B. Păuna, and T. Diaconescu. 2020. “Renewable Energy and Economic Performance in the Context of the European Green Deal.” Energies 13 (23): 6440. https://doi.org/10.3390/en13236440.

- Sinha, A., M. Shahbaz, and T. Sengupta. 2018. “Renewable Energy Policies and Contradictions in Causality: A Case of Next 11 Countries.” Journal of Cleaner Production 197: 73–84. https://doi.org/10.1016/j.jclepro.2018.06.219.

- Soava, G., A. Mehedintu, M. Sterpu, and M. Raduteanu. 2018. “Impact of Renewable Energy Consumption on Economic Growth: Evidence from European Union Countries.” Technological and Economic Development of Economy 24 (3): 914–932. https://doi.org/10.3846/tede.2018.1426.

- Soytas, U., and R. Sari. 2009. “Energy Consumption, Economic Growth, and Carbon Emissions: Challenges Faced by an EU Candidate Member.” Ecological Economics 68 (6): 1667–1675.

- Szetela, B., A. Majewska, P. Jamroz, B. Djalilov, and R. Salahodjaev. 2022. “Renewable Energy and CO2 Emissions in Top Natural Resource Rents Depending Countries: The Role of Governance.” Frontiers in Energy Research 242.

- Taha, A., M. Aydin, T. T. Lasisi, F. V. Bekun, and N. Sethi. 2023. “Toward a Sustainable Growth Path in Arab Economies: An Extension of Classical Growth Model.” Financial Innovation 9 (1): 1–24. https://doi.org/10.1186/s40854-022-00426-6.

- Tang, C. F., and B. W. Tan. 2015. “The Impact of Energy Consumption, Income and Foreign Direct Investment on Carbon Dioxide Emissions in Vietnam.” Energy 79: 447–454.

- Wang, J., and Y. Ma. 2022. “How Does Green Finance Affect CO2 Emissions? Heterogeneous and Mediation Effects Analysis.” Frontiers in Environmental Science 817.

- Wang, C., L. Zhang, Y. Chang, and M. Pang. 2015. “Biomass Direct-Fired Power Generation System in China: An Integrated Energy, GHG Emissions, and Economic Evaluation for Salix.” Energy Policy 84: 155–165.

- Waqih, M. A. U., N. A. Bhutto, N. H. Ghumro, S. Kumar, and M. A. Salam. 2019 April. “Rising Environmental Degradation and Impact of Foreign Direct Investment: An Empirical Evidence from SAARC Region.” Journal of Environmental Management 243: 472–480.

- Wu, B., A. Monfort, C. Jin, and X. Shen. 2022. “Substantial Response or Impression Management? Compliance Strategies for Sustainable Development Responsibility in Family Firms.” Technological Forecasting and Social Change 174: 121214. https://doi.org/10.1016/j.techfore.2021.121214.

- Xiong, Q.-M., Z. Chen, J.-T. Huang, M. Zhang, H. Song, X.-F. Hou, et al. 2020. “Preparation, Structure and Mechanical Properties of Sialon Ceramics by Transition Metal-Catalyzed Nitriding Reaction.” Rare Metals 39: 589–596. https://doi.org/10.1007/s12598-020-01385-6.

- Xu, Y., H. Zhang, F. Yang, L. Tong, D. Yan, Y. Yang, et al. 2021. “Experimental Investigation of Pneumatic Motor for Transport Application.” Renewable Energy 179: 517–527. https://doi.org/10.1016/j.renene.2021.07.072.

- Zakari, A., F. F. Adedoyin, and F. V. Bekun. 2021. “The Effect of Energy Consumption on the Environment in the OECD Countries: Economic Policy Uncertainty Perspectives.” Environmental Science and Pollution Research 28 (37): 52295–52305. https://doi.org/10.1007/s11356-021-14463-8.

- Zhou, Y., Z. Fang, N. Li, X. Wu, Y. Du, and Z. Liu. 2019. “How Does Financial Development Affect Reductions in Carbon Emissions in High-Energy Industries?—A Perspective on Technological Progress.” International Journal of Environmental Research and Public Health 16 (17): 3018. https://doi.org/10.3390/ijerph16173018.

Appendix A

Table A1. Measurement of control variables.

Table A2. Descriptive statistics

Table A3. Pairwise correlations