?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The paper examines if COVID-19 crisis has brought changes in companies’ approach on corporate reporting, with focus on annual reports. The research method is based on text mining techniques in order to build measures of readability and tone of uncertainty of annual reports, given the information published by the companies listed on four stock exchanges from Europe, namely the Bucharest Stock Exchange, ATHEX Stock Exchange, IBEX-35, and WIG-20 between 2017–2020. Findings emphasize, through text mining, multivariate analysis, and topic modeling, that the analyzed reports are less extensive in times of pandemic and tend to become more generic. Among firms’ financial performance metrics considered in our models, we found that there is a significant association only between annual reports textual characteristics and respectively, firm size, price earnings ratio and accruals reported. We prove as well significant stock exchange effects and industry effects. Our results show a slight decrease in annual reports readability, while the tone of uncertainty is more prominent within firms listed on less mature stock exchanges.

1. Introduction

The novel coronavirus caused a vast economic decline worldwide. This new context has seriously affected the daily businesses and operations of companies and highlighted the need for better communication and disclosure policies with shareholders and other stakeholders. In this sense, the annual report remains one of the main drivers of communication that companies have with their interested parties regarding the company’s performance and, most important, the company’s ability to continue as a going concern in an environment marked by uncertainty.

As noted by Leuz and Wysocki (Citation2016), disclosures represent an ideal tool for reduction of information asymmetry between managers and firms’ shareholders and stakeholders. However, benefits of higher financial transparency is strongly conditioned by the nature of the disclosures and the content. Instead, under the premises of integrated or sustainability reporting frameworks, managers have started using annual report as powerful marketing tools for the firms they lead, with the scope of signaling positive effects on the market and having benefits, such as lower cost of capital (Christensen, Hail, and Leuz Citation2019).

In times of crisis, annual reports become even more important, as they represent the main tool for managers to communicate financial results to shareholders and stakeholders as well. However, the focus is oriented toward risk management disclosure and presentation of macroeconomic context that might affect forward-looking information. Those directions lead to a change in the tone of annual reports, which is expected to be more negative, showing that accounting estimated reported is highly affected by external factors, and less by managers’ ability (Oskouei and Sureshjani Citation2021).

Furthermore, managers could choose to prepare obfuscated annual reports, to hide as much as possible potential future evolutions of financial performance, to avoid transmitting any negative signal to the market, as during COVID-19 pandemic period shares liquidity has become significantly volatile (Hatmanu and Cautisanu Citation2021). Moreover, capital markets’ systemic impact of COVID-19 becomes globally contagious, especially under uncertain conditions, when news attention negative impact on financial markets is higher than investors’ rational expectation (Engelhardt et al. Citation2020).

Our aim in this paper is to bring some insights on the changes in the annual reports characteristics, determined by the current COVID-19 pandemic crisis. In this context, the focus of our paper is the analysis of firm-specific financial determinants on annual reports readability and tone of uncertainty of entities listed on four stock exchanges, including Bucharest Stock Exchange (BSE) and ATHEX, two stock exchanges that recorded the highest growth in the world, considering the evolution of stock markets in 87 countries with available data (Wall Street Citation2019). According to the ranking published by FTSE Russell in September 2020, Romania and Greece are included in the emerging markets category. In order to compare the data, we included in the study the stock exchanges from Spain and Poland, respectively the entities listed on IBEX-35 and WIG −20, classified by FTSE Russell among the developed stock markets (FTSE Citation2020).

Our article comes with additional insights within the literature. It adds empirical evidence on the area of analysis of readability of annual reports and sentiment analysis, for annual reports made public by firms listed on European capital markets. To our knowledge, only Lang and Stice-Lawrence (Citation2015) analyzed another sample of European companies. It also fills in the gap on the literature by analysis annual reports, as most of the literature is limited to the 10-K disclosure analysis published by American companies. The article is the first to analyze the effect of COVID-19 on annual reports. Only Wang and Xing (Citation2020) analyzed the effect of COVID-19 on corporate conference calls and management announcements. Nonetheless, as of our knowledge, it is the first study that addresses the problem of topic modeling on annual reports disclosed by firms listed in the four European capital markets considered in the study, to arise issues related to the risk of generic disclosures, in the context of actual COVID-19 pandemic.

This paper is structured as follows: Section 2 presents the literature review and the hypothesis development, testing the ways in which corporate disclosures are influenced by the novel coronavirus context; Section 3 presents the research methodology, Section 4 discusses the results obtained, and Section 5 summarizes the main findings, conclusions, and avenues for future research directions.

2. Literature Review

The pandemic and its effects represent a topic of great interest because many view the COVID-19 outbreak as an unprecedented event that the world has witnessed since the inception of the stock markets. COVID-19 affected the activity of companies from all business sectors, being considered an event similar to the financial crisis that began in 2008 (Wang and Xing Citation2020). Much has been written about the crisis, authors providing insights and perspectives, most agreeing that in uncertain times some accounting techniques used in financial reporting led to its deepening. Hence, in this novel coronavirus crisis it is interesting to study how firm’s financial reports are elaborated and released into the market, to mitigate the negative impact of a pandemic on firm’s performance before shareholders and stakeholders.

Overall, the literature shows that over time, the length of annual reports has increased (Dyer, Lang, and Stice-Laurence Citation2017; Lang and Stice-Lawrence Citation2015). Those premises lead to changes in the length of the annual reports, because of complexity of models used for accounting estimates (Lim, Chalmers, and Hanlon Citation2018).

In the current context, telling the story of COVID-19 through annual reports implies more professional judgments, that lead to lengthier annual reports, aimed to describe properly postulates, assumptions, and methods used in accounting estimation and financial reporting. Gould and Arnold (Citation2020) stated that some companies tend to report financial effects of the pandemic through interim financial statements first, which involves a greater use of accounting estimates. Therefore, we believe that these new elements that need to be highlighted in the annual reports, given the current pandemic context, will require more robust and detailed corporate disclosures and the first hypothesis that will be tested will be H1: in the context of COVID-19 pandemic restrictions, firms’ financial characteristics determine significant changes in the length of annual reports.

However, as noted by Dyer, Lang, and Stice-Laurence (Citation2017), the literature underlines a trend of increasing length of annual reports, in parallel with deterioration of readability and increase of tone of ambiguity.

Researchers highlight that performing entities disclose readable reports in order to impress (Li Citation2008). Moreover, there are studies that show a positive correlation between managerial ability and annual reports readability, especially in case of firms reporting positive profitability (Hasan Citation2020). There are also studies that show readability and complexity of annual reports are significantly driven by the accounting standards (Dyer, Lang, and Stice-Laurence Citation2017). The increase in innate component (common complexity) of reporting complexity (readability) is mainly driven by accounting regulation (Dyer, Lang, and Stice-Laurence Citation2017; Efretuei Citation2020), while the increase of obfuscation (uncommon complexity) is more associated to management choice that depends mainly on capital markets incentives (Li Citation2008; Loughran and McDonald Citation2013; Miller Citation2010) and investors disclosure choices. Through more complex and less readable disclosures, managers tend to hide poor performance, by amplifying annual reports obfuscation (Li Citation2008; Lo, Ramos, and Rogo Citation2017), with impact on firms’ cost of capital (Ertugrul et al. Citation2017).

Therefore, we believe that the readability of the annual and interim reports is influenced by the COVID-19 pandemic and the second hypothesis that will be tested will be H2: in the context of COVID-19 pandemic restrictions, firms’ financial characteristics determine significant changes in the readability of annual reports.

Given the importance of making accurate disclosures, reporting in times of uncertainty represents a major challenge. Considering that COVID-19 pandemic negatively impacted companies around the world, the approach by which the “bad news” are disclosed into the market through annual and interim reports represents a topic of great interest. The way the information is presented and structured is essential to ensure significant impact on investors’ decision, especially through the lens of impression managements techniques, as some strategies are aimed to obfuscate bad news, while most of them are designed to emphasize good news (Merkl-Davies and Brennan Citation2017).

The tone of the discourse used when preparing annual reports is also important, as behavioral theories show that negative words have a higher impact compared with the positive words (Tetlock, Saar-Tsechansky, and Macskassy Citation2008). Consequently, the positive bag-of-words are preferred by managers when preparing annual reports. However, there is little evidence on studying the tone of uncertainty of annual reports in the literature, as researchers focus more on either the use of dichotomous positive versus negative predefined lists of words (Loughran and McDonalld Citation2016), or the use of ambiguous words (Dyer, Lang, and Stice-Laurence Citation2017; Ertugrul et al. Citation2017).

Loughran and McDonald (Citation2011) have shown that managers present information on a more positive tone in the annual reports, which is more likely associated with negative stock returns. Davis et al. (Citation2015) noted as well that managers have incentives to set-up their optimistic or pessimistic tone on corporate communication of firms’ results, especially when these information are more sensitive to stock prices, reflecting that the tone of disclosures became negative only after the financial crisis from 2008. However, Wang and Xing (Citation2020) have shown, referring to annual reports related to the COVID-19 pandemic period, that low level of uncertainty tone in the earnings announcements has been made by the management.

Therefore, we believe that now, more than ever, in this uncertain times generated by the COVID-19 pandemic, managers should avoid negative or ambiguous words when reporting the consequences of the global pandemic through annual statements and the third hypothesis that will be tested will be H3: the novel coronavirus created a context marked by uncertainty that has a significant influence on disclosure tone of the annual reports.

Efretuei (Citation2020) has shown that the tone of uncertainty of annual reports is negatively related to the corresponding readability, showing that managers prefer to amplify the obfuscation information, by using more words related to uncertainty and ambiguity, describing an increasing trend of this negative relation overtime. In the actual context of COVID-19 pandemic crisis, the issue of information asymmetry, through its components of moral hazard and adverse selection that arise, is highly condoned by industry-specific and domestic institutional framework as well.

Over time, economies have become increasingly interconnected and interdependent, which has exacerbated the crisis. In this context, it is vital that the information transmitted by companies into the market to be transparent and real so that the business environment could mitigate the negative impact of a pandemic on firm’s performance.

3. Methodology Research

3.1. Sample Data

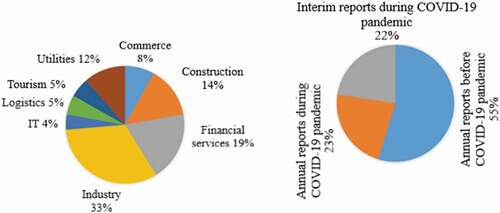

Our research methodology is similar to Lang and Stice-Lawrence (Citation2015). The focus of the paper is the analysis of firm-specific determinants in annual and interim reports readability and keywords frequency, considering the period between 2017 and the first quarter of 2020, as depicted in .

Figure 1. Sample distribution per sector and per nature of report.

In order to emphasize local specifics of institutional and cultural framework, we used a sample that consists of firms listed on different European capital markets, respectively the Romanian capital market (BSE), Greek capital market (ATHEX), the Spanish capital market (IBEX-35), and Polish capital market (WIG-20), as depicted in .

Table 1. Sample distribution on capital markets and years

Annual reports and interim reports were downloaded manually from firm’s websites, or capital markets websites where they are listed. Overall, we included in our analysis 524 observations, controlling for industry effects and capital markets effects as well. The data are split into two main groups, namely data related to period before COVID-19 crisis, concerning period 2017 to 2018, and respectively data related to period during COVID-19 crisis, concerning period 2019–2020.

3.2. Variables Definition

The data used in econometric models estimated in our study consist of some key financial performance indicators and several characteristics of the annual reports, as described in , determined based on annual reports and output generated running text mining procedures.

Table 2. Variables definition

3.3. Construction of the Linear Regression Models

The regression model used to test the hypotheses related to annual reports characteristics has the following configuration:

where represents the financial measures of firms’ characteristics, respectively ROA, Leverage, Accruals and Size, Growth and PER as defined in , while

reflects each of the dependent variables defined in , respectively, Length, Readability and Uncertainty.

Estimation of the econometric models is made using the OLS method. However, in order to control for potential implications of probability distribution of independent variables, we estimate the econometric models looking for firm financial drivers using the quantile regression method as well, with focus on 1st quantile estimates, 2nd quantile estimates, and respectively 3rd quantile estimates (Wooldridge Citation2010).

For reliability purpose, we proceed to results triangulation, by using an alternative measure of readability of annual reports, considering the Flesch reading ease score, which is determined based on formula . A higher

score means better readability of annual reports. Therefore, this alternative measure of document readability is the opposite of the main readability measure of our study, which consists of number of words per sentence.

To illustrate specifics of each area of activity on financial disclosures characteristics, we control our model for fixed effects as well, as described in econometric model below:

where reflects the fixed/random specific effects of each area of activity analyzed. Additionally, we look for impact of corporate governance metrics that describe better firms’ institutional particularities designed to look for the quality of financial reports.

3.4. Entropy Analysis of Annual Reports

In order to measure how uniform extracted topics are addressed in annual reports and if there is a pattern related to industry specific, or capital markets specific, we proceed to Latent Dirichlet Analysis (LDA), in order to extract distinct topics addressed in a text. After performing LDA for different number of topics extracted, we have decided on the extraction of 45 topics from the corpus analyzed, as the value of perplexity score tends to increase less (Hofmann and Klinkenberg Citation2014).

Each topic extracted from the corpus is characterized by a set of performance metrics. The essential metric considered in our study is the distribution of topics, based on topics coherence obtained for each annual report. The coherence of a topic is the measure whether the words in a topic tend to co-occur together. The larger the value topic coherence the lower the indication that words co-occur in different topics simultaneously. Once determined each topic coherence per each annual report, we calculate the Shannon entropy score, using the relation below:

where is the proportion (coherence metric) from the document that topic

is addressed in annual report disclosed by firm

for year

. The interpretation of this score is that the higher the entropy of an annual report, the more uniformly are addressed in the annual report all topics extracted from the corpus running the LDA. Instead, the lower the score of entropy is, the more attention is given in the annual report to only few topics extracted from the corpus analyzed.

Different extensions of the LDA procedure are used as well to directly link the stock prices with topics addressed in the corporate communications, so that stock returns or firm profitability can be explained easily by related topics extracted from the corpus analyzed (Li et al. Citation2020).

Our approach is similar with Dyer, Lang, and Stice-Laurence (Citation2017) that have explained the length of the first three topics by firms’ financial characteristics and annual reports textual characteristic as well. However, in this study we do not focus on explaining length of topics extracted from annual reports, but rather on justifying annual reports readability by the diversity of topics addressed.

4. Results and Discussion

4.1. Descriptive Statistics

In we summarize the descriptive statistics for the sample analyzed, considering two separate panels of data, respectively. Panel A that consists of data analyzed related to period 2017 to 2018 and Panel B including data analyzed related to period 2019 to 2020. We observe that there is spread in the practice of financial disclosures, as the interval of variation for either the number of pages (length), or the level of understanding of financial disclosures (readability) is high, especially in case of readability score.

Table 3. Descriptive statistics

Instead, the standard deviation is relatively small in case of the number of pages of financial disclosures, which means that there is only a slight spread on the practice of financial reporting along capital markets or different areas of activity. In average, the annual reports have about pages, in case of annual reports related to Panel A. On the other side, annual reports related to Panel B record significant decrease to an average of 98 pages. Similar but slight changes are observed in case of reports readability, as the average number of 13.31 words per sentence corresponding to Panel A annual reports decrease to the number 12.77 words per sentence, in case of Panel B annual reports, but with higher deviation between reports analyzed.

The results in show a small percentage of words reflecting the sentiment of uncertainty, as the average on Panel A related annual reports is about 7.2%, while for Panel B annual reports is slightly higher, respectively 8.4%, which show managers avoid, as much as possible, words that lead to unclear or uncertain messages transmitted to shareholders and stakeholders as well. However, the slight increase highlights the systemic effect of COVID-19 pandemic on business operations and financial disclosures as well.

Related to firms’ characteristics summarized in , notable results for our purpose concern the changes determined by COVID-19 pandemic. The statistics show that firms suffer from negative effects of COVID-19 pandemic, through a decrease of profitability, a decrease of financial leverage and a decrease of firms’ market value. On the other side, the high standard deviation of the growth variable shows that some firms are less affected than other, either because of their specific of activity that has benefit from COVID-19 pandemic, such as IT sector (Efretuei Citation2020), or because of business models short-term reorientation that implied also a slight increase on firms’ assets, leading to changes on production capacity. Nonetheless, we observe a significant decrease of accruals once the COVID-19 pandemic crisis has started, suggesting us less earnings management.

Our results are similar with Jiang, Pittman, and Saffar (Citation2019) who show that in times of crisis, described by high uncertainty on policy making, firms’ disclosures become lengthier, less readable and with a more prominent uncertainty tone on discourse, in order to avoid compliance costs or litigation costs (Christensen, Hail, and Leuz Citation2019).

In , we observe slight changes, especially related to the length of the annual reports that seem to be lower, or to the readability of the annual reports that seem to deteriorate in time, especially in case of IBEX-35 listed entities. It seems that the more mature the capital markets are, the higher the readability of annual reports is, in parallel with a lower uncertainty tone of discourse. The highest score of annual reports readability is found within entities listed on IBEX-35 capital market, considered as a developed capital market, with a high level of value and investor segmentation. The highest tone of uncertainty is observed within entities listed on BSE capital market, which is more related to cultural dimension of the corporate reporting, rather than capital markets incentives.

Figure 2. Marginal means conditioned by COVID-19 pandemic effects.

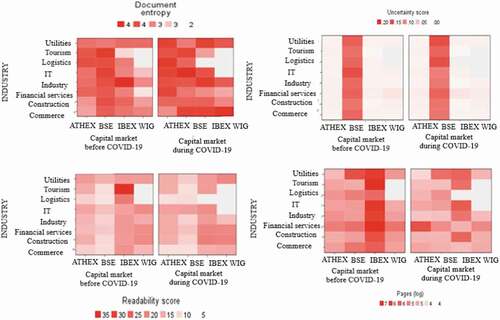

Additionally, in we observe that higher coherence of topics seems to appear in case of annual reported after COVID-19 pandemic, which show topics addressed in annual reports are equally weighted, suggesting a more general approach considered, with less focus on specific topics, similar with the concern Dyer, Lang, and Stice-Laurence (Citation2017) have highlighted. Overall, we observe higher entropy of firms’ annual reports operating in industry area, IT, commerce, and utilities.

4.2. Correlation Analysis

In we provide the correlations between disclosure characteristics and firms’ financial performances. The results show unanimously that firms size represents essential factor for the length and the readability of annual reports, as business strategy related to more complex business models asks for more complex annual reports (Lim, Chalmers, and Hanlon Citation2018). Instead, the correlation between firm size and the annual reports tone of uncertainty is significantly negative, showing that annual reports disclosed by big firms show lower tone of uncertainty.

Table 4. Pearson correlation matrix

We observe a significant positive correlation as well between readability of annual reports and firms’ leverage, and a significant negative correlation between annual reports tone of uncertainty and firms’ leverage, related to period during COVID-19 pandemics. Those correlations suggest to us that, in times of crisis, annual reports disclosed by firms with higher debt focus more on less uncertain information disclosed and try to transmit a more comprehensive message to the creditors.

We highlight in a slight positive correlation between firms’ profitability and the length of annual reports and their readability, for the period before COVID-19 pandemic. Firms’ profitability is negatively correlated with annual reports tone of uncertainty. Like Loughran and McDonald (Citation2011), our results suggest that managers prefer to focus their annual reports on good news, rather than bad news. However, readability of annual reports published during the COVID-19 pandemic is less influenced by firms’ profitability.

Instead, we see a low statistically significant positive correlation between price earnings ratio and the length of the annual reports, only in case of period related to COVID-19 pandemic, which suggest that managers are slightly sensitive to capital markets in times of crisis.

4.3. Assessing Firm-level Determinants of Financial Disclosures

In we provide evidence on the association between measures of annual reports and respectively firms’ financial performance indicators. We addressed the existence of heteroscedasticity in our models, by performing the Modified Breusch-Pagan test. Model 1 estimates are not heteroscedastic, as their is less than the threshold of 1%, reason why we estimate the model using the White-Huber standard errors regression procedure, to ensure efficient regression coefficients estimates, concerning standard errors (Wooldridge Citation2010).

Table 5. Multivariate analysis on financial drivers of annual reports textual measures

All models estimated in are statistically significant, as their level of significance () is lower than the acceptable level of 1%. Instead, we observe a relatively low

adjusted, varying between 13.3% in case of model 4 to 51.9% valid for model 3.

Based on Haussmann test results, summarized in , we consider the models with industry fixed effects more relevant for our analysis in case of our models, except for model 4 and model 5, as their (Lee et al., Lee Citation2019). For model 4 and model 5 we have performed the Lagrange Multiplier (LM) test to check if random effects regression model is more relevant than the fixed effects or the pooled regression model. Based on statistics provided in , we observe that the models look for random effects (

), which shows that the specific of each firms’ business model and management related corporate reporting policy approach is more relevant than the industry-specific effect (Lee Citation2019).

Firm size effect is significant for the readability, the length, and the uncertainty tone of the annual reports, no matter the panel data analyzed. The results show that the more complex is the firm’s business model, the less readable the annual reports will be. Our results are similar with Dempsey et al. (Citation2012) results, who have confirmed a positive association as well between firm size and readability of annual reports.

The results also highlight that the higher the firm size, the lower the uncertainty tone of the annual report will be, suggesting that issuers illustrate in the annual reports less information about the uncertain economic perspectives. The COVID-19 pandemic has affected annual reports, as our results show slight changes in the readability and tone of uncertainty of annual reports, reflecting an increase in readability and a less pronounced tone of uncertainty in case of larger firms.

Managers’ sensitivity to capital markets is visible according to our results only on the tone of uncertainty of annual reports, described by the PER (price earnings ratio) coefficients, which differs on the panels analyzed. While during the period of COVID-19 pandemic, higher stock price earnings ratio determines more pronounced tone of uncertainty of annual reports (), during the period before the COVID-19 pandemic, higher PER determines more positive tone of annual reports (

). The results show that managers would like to emphasize better the positive financial results in conditions of crisis, showing the results are obtained in terms of significant negative constraints, such as the negative economic effects of COVID-19 pandemic.

Our results show as well a negative association between the tone of uncertainty and the level of accruals reported (), for the period prior to COVID-19 pandemic. This result reveals that the lower the accruals are reported, the higher is the uncertainty tone of annual report, as there is less evidence of earnings management, because managers might explain poor financial performance referring to negative shocks on economic environment. However, the marginal effect on the tone of uncertainty on annual reports is relatively small, suggesting that managers prefer to refer less to economic environment uncertainty on annual reports, as negative information has a higher impact compared with the positive words (Tetlock, Saar-Tsechansky, and Macskassy Citation2008).

Our results show as well, a positive association between the level of accruals and the readability of annual reports (), valid for period before COVID-19 pandemic. In our study, higher readability score indicates less readable reports according to our readability score definition. The results we obtained suggest that, managers reporting higher level of accruals present the information through less readable reports. Those results confirm again the relation of substitution between accruals quality and disclosures quality, as lower accruals suggest higher earnings quality, positively related with higher readability of annual reports (Jaafar and Hussainey Citation2012).

The results describe as well a positive association between firms’ profitability and the length of annual reports (), but only in case of reports published during COVID-19 pandemic. Our results highlight that higher profitability means less readable annual reports. The results suggest that managers might use less readable discourse in preparing annual reports, to hide information about earnings management that has led to higher firm’s profitability, similar to Davis et al. (Citation2015), Lang and Stice-Lawrence (Citation2015).

Nonetheless, for the period during COVID-19 pandemic, we confirm a negative statistically significant association between the tone of annual reports and the rate of growth in sales (). This result provides us with evidence that the higher the level of growth in sales, the lower the tone of uncertainty in annual reports. As noted by Davis et al. (Citation2015), managers have incentives to set-up their optimistic or pessimistic tone on corporate communication of firms’ results, especially when this information is more sensitive to stock prices, such as the increase in sales.

4.4. Robustness Analysis Controlling for Distribution Values Effect

In we provide summary statistics of the quantile regression estimation models, for the period before the ongoing COVID-19 pandemic. The results confirm once again that there is a positive association between annual reports readability and firm size. The higher the firms size, the lower the annual reports readability. The result implies that firms of larger size involve more complex business models which are hardly to be reflected in sufficiently readable disclosures.

Table 6. Quantile analysis on financial drivers for period before COVID-19 pandemic

We obtain robust results as well for the association between the tone of uncertainty of annual reports and firm size. These results show that firms of larger size do not focus on emphasizing the uncertainty of economic environment when presenting annual results, probably because of their higher power of negotiation with the creditors and the other stakeholders.

We get robust results as well related to the association between readability of annual reports and the level of firms’ reported accruals, which show that the higher the accruals, the less readable annual reports are. We observe that estimated regression coefficients increase from one percentile to another (). The results show that firms of smaller size tend to be more precise on reporting, in order to explain better accounting estimates reported and avoid any future litigation cost, or capital market penalization.

Robust results are obtained also concerning the association between the uncertainty tone of annual reports and the level of accruals, showing higher level of accruals determines lower tone of uncertainty of annual reports, with the aim to transmit positive signal to investors, that should not warn investors of inaccurate earnings quality. In association with the results related to readability of annual reports, we observe that higher level of accruals determine managers to prepare obfuscated annual reports, but in a more positive tone that would likely determine less concerns for investors. Otherwise, higher investors’ concerns would determine them to do further investigation and put additional pressure on firms’ management team.

In we provide summary statistics of the quantile regression estimation models, for the period before current COVID-19 pandemic started. The results look robust, compared with the estimates obtained using OLS method, but only related to firm size positive marginal effect on the readability of annual reports and firm size negative effect on the tone of uncertainty of annual reports.

Table 7. Quantile analysis on financial drivers for period after COVID-19 pandemic

The results from quantile regression show robustness for the marginal effect of firm size on readability of annual reports, no matter the percentile estimate. Instead, the negative impact of firm size on the tone of uncertainty of annual reports is statistically significant only for 1st and 2nd percentile, suggesting that only in case of annual reports with less pessimistic tone the firm size matters.

4.5. Robustness Analysis Controlling for Corporate Governance Implications

The main purpose of this analysis is to check if the entropy score of annual reports improves our regression models , as annual reports readability is not influenced only by managers’ preferences reflected in firms’ financials, but also depends on the managers ability to present a clear, concise and coherent message with focus only on the key aspects of the business model (Hasan Citation2020).

In we provide the statistics for models estimation, triangulating our results by using an alternative for readability score, respectively the Flesch readability ease score, presenting in parallel results for both measures of readability of annual reports. Additionally, we control for annual reports entropy and firms’ corporate governance framework as well.

Table 8. Control variables effect on annual reports readability score

We observe the negative association between annual reports readability and their entropy score is statistically significant only for models estimated for period before COVID-19 pandemic (). The results show that the higher the entropy score of annual reports, the lower is their readability, meaning that if annual reports address multiple topics, the readability is significantly affected as there is no clear orientation of the financial reporting discourse. It seems that managers prefer to follow a standard approach on corporate reporting, looking especially for compliance with generally accepted reporting standards, such the GRI standards, rather than providing relevant information which could reflect better the impact of particularities of firms’ business model on financial performance.

Robust results are again confirmed related to the positive association between readability of annual reports and firm size as well, no matter the period analyzed and if corporate governance control variables are included in the estimated models.

Instead, the Flesch reading ease score is statistically affected only by firms’ corporate governance score. This measure of readability is more sensitive to the complexity of the words used, rather than the number of words used per sentence. Our results could suggest that there isn’t a pattern on how managers try to prepare obfuscated annual reports using fog words, meaning there isn’t a systematic preoccupation of managers to select fog words just to reduce the readability of annual reports.

However, it seems more effective mechanisms of corporate governance lead to less readable annual reports, with a higher marginal effect on the period of COVID-19 pandemic. Higher corporate governance score shows more mature and effective governance mechanisms. The results show that annual reports are less readable because of longer sentences, but not because of the use of complex words. Corroborated, the results suggest us that management is highly accountable for financial performance, which makes them to obfuscate annual reports. As TOP management incentive plans often consist of equity compensation, they are interested to stimulate attractiveness of the stocks on the capital markets. A root-cause could be that corporate governance mechanisms are effective more in the area of management accountability, but less effective in the area of shareholders or board of director’s oversight.

Instead, same results can suggest as well that strategic shareholders as well can put pressure on preparers inside the firm on how to prepare financial statements, as the use of fewer complex words is conditioned by higher stock market returns.

Industry effects are confirmed along all estimated models that control for effect of financial performance on annual reports readability score, based on Hausman test, for which the p value is less than 5%. Our results are similar with Efretuei (Citation2020) who have underlined the effects of the specific of several areas of activity, such as financial services, technology, tourism, or utilities. Our results show in significant negative fixed effects in case of firms operating in commerce, or logistics. Instead, we observe positive fixed effects in case of firms operating in financial services, logistics or tourism area. These results show that annual reports are less readable in case of firms operating in commerce or logistics area, while firms operating in financial services area seem to be more concise and clearer.

Figure 3. Fixed effects of industry on estimated models.

Additionally, we observe from a temporal perspective that the COVID-19 pandemic has changed drastically firms’ approach on corporate reporting for firms operating in tourism, or financial services, leading to significantly less readable annual reports. Instead, in case of firms operating in IT and communications, the change in the readability of annual reports is even higher, as it goes from a positive value to a negative value, suggesting higher level of readability of annual reports. Therefore, those firms can be used for benchmark for the other firms, with the limitation of some basic constraints, such as the business model complexity, and corporate governance mechanisms.

5. Conclusions

This paper discussed the impact of firms’ financial drivers on annual reports characteristics, respectively the length of the annual report, the level of readability, and the degree of negative tone reflected on analyzed annual reports. The analysis is designed to highlight how the current COVID-19 pandemic affects annual reports and how managers use them to emphasize or to hide firms’ financial results.

Through multivariate analysis and text mining techniques, our paper reveals that the analyzed reports are less extensive in content and less readable. The results show increase in obfuscate information, especially in times of pandemic. However, the results are affected as well by industry fixed effects, as COVID-19 pandemic has affected distinctly the areas of economic activity. Firm size and accruals reported determine a significant positive marginal effect on annual reports readability, while firm size, accruals, and price earnings ratio determine a negative association with the tone of uncertainty of annual reports, especially during the period prior to COVID-19 pandemics. Nonetheless, we underline that users of financial reports should be more careful on annual reports discourse, including the tone preparers use, as this could be already a sign of potential obfuscation on financial reporting.

Finally, we conclude that the lack of a common reporting framework in pandemic conditions to build a disclosure index strictly related to the size of COVID-19 presentations in the report represents one of the main limitations of our research. Future research can empirically investigate the breakdown of a composite ESG score index to understand the extent to which annual reports readability is influenced by financial information vs. non-financial information. Future research can also empirically investigate the correlation analysis of financial and non-financial indicators with the characteristics of the annual reports, for the pre and post COVID-19 period.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Christensen, H. B., L. Hail, and C. Leuz 2019. Economic analysis of widespread adoption of CSR and sustainability reporting standards. Working paper.

- Davis, A. K., W. Ge, D. Matsumoto, and J. L. Zhang. 2015. The effect of manager-specific optimism on the tone of earnings conference calls. Review of Accounting Studies 20 (2):639–73. doi:https://doi.org/10.1007/s11142-014-9309-4.

- Dempsey, S. J., D. M. Harrison, K. F. Luchtenberg, and M. Seiler. 2012. Financial opacity and firm performance: The readability of REIT annual reports. The Journal of Real Estate Finance and Economics 45 (2):450–70. doi:https://doi.org/10.1007/s11146-010-9263-2.

- Dyer, T., M. Lang, and L. Stice-Laurence. 2017. The evolution of 10-K textual disclosure: Evidence from latent dirichlet allocation. Journal of Accounting and Economics 64 (2–3):2–3. doi:https://doi.org/10.1016/j.jacceco.2017.07.002.

- Efretuei, E. 2020. Year and industry-level accounting narrative analysis: Readability and tone variation. Journal of Emerging Technologies in Accounting. doi:https://doi.org/10.2308/JETA-18-12-21-26.

- Engelhardt, N., M. Krause, D. Neukirchen, and P. Posch. 2020. What drives stocks during the Corona-Crash? News attention vs. rational expectation. Sustainability 12 (12):5014. doi:https://doi.org/10.3390/su12125014.

- Ertugrul, M., J. Lei, J. Qiu, and C. Wan. 2017. Annual report readability, tone ambiguity, and the cost of borrowing. Journal of Financial and Quantitative Analysis 52 (2):811–36. doi:https://doi.org/10.1017/S0022109017000187.

- Francis, J., R. LaFond, P. Olsson, and K. Schipper. 2005. The market pricing of accruals quality. Journal of Accounting and Economics 39 (2):295–327. doi:https://doi.org/10.1016/j.jacceco.2004.06.003.

- FTSE Classification of Equity Markets. September 2020.

- Gould, S., and C. Arnold 2020. The financial reporting implications of COVID-19.

- Hasan, M. M. 2020. Readability of narrative disclosures in 10-K reports: Does managerial ability matter? European Accounting Review 29 (1):147–68. doi:https://doi.org/10.1080/09638180.2018.1528169.

- Hatmanu, M., and C. Cautisanu. 2021. The impact of COVID-19 pandemic on stock market: Evidence from Romania. International Journal of Environmental Research and Public Health 18 (17):9315. doi:https://doi.org/10.3390/ijerph18179315.

- Hofmann, M., and R. Klinkenberg. 2014. RapidMiner: Data mining use cases and business analytics applications. London: CRC Press.

- Jaafar, M. S., and K. Hussainey. 2012. Accruals quality visa-vis disclosure quality: Substitutes or complements? British Accounting Review 44 (1):36–46. doi:https://doi.org/10.1016/j.bar.2011.12.004.

- Jiang, L., J. Pittman, and W. Saffar. 2019. Policy uncertainty and textual disclosure. SSRN Paper.

- Lang, M. H., and L. Stice-Lawrence. 2015. Textual analysis and international financial reporting: Large sample evidence. Journal of Accounting & Economics 60 (2):110–35. doi:https://doi.org/10.1016/j.jacceco.2015.09.002.

- Lee, F. C. 2019. Financial econometrics, mathematics ans statistics. New York, NY 10013, U.S.A: Springer.

- Leuz, C., and P. Wysocki. 2016. The economics of disclosure and financial reporting regulation: Evidence and suggestions for future research. Accounting Research 54:525–622.

- Li, F. 2008. Annual report readability, current earnings, and earnings persistence. Journal of Accounting and Economics 45 (2–3):221–47. doi:https://doi.org/10.1016/j.jacceco.2008.02.003.

- Li, J., G. Li, X. Zhu, and Y. Yao. 2020. Identifying the influential factors of commodity futures prices through a new text mining approach. Quantitative Finance 20 (12):1967–81. doi:https://doi.org/10.1080/14697688.2020.1814008.

- Lim, E. K. Y., K. Chalmers, and D. Hanlon. 2018. The influence of business strategy on annual report readability. Journal of Accounting and Public Policy 37 (1):65–81. doi:https://doi.org/10.1016/j.jaccpubpol.2018.01.003.

- Lo, K., F. Ramos, and R. Rogo. 2017. Earnings management and annual report readability. Journal of Accounting and Economics 63 (1):1–25. doi:https://doi.org/10.1016/j.jacceco.2016.09.002.

- Loughran, T., and B. McDonald. 2011. When is a liability not a liability? Textual analysis, dictionaries, and 10-Ks. The Journal of Finance LXVI (I):35–65.

- Loughran, T., and B. McDonald. 2013. IPO first-day returns, offer price revisions, volatility, and form S-1 language. Journal of Financial Economics 109 (2):307–26. doi:https://doi.org/10.1016/j.jfineco.2013.02.017.

- Loughran, T., and B. McDonalld. 2016. Textual analysis in accounting and finance: A survey. Journal of Accounting Research 54:4. doi:https://doi.org/10.1111/1475-679X.12123.

- Merkl-Davies, D. M., and N. M. Brennan. 2017. A theoretical framework of external accounting communication: Research perspectives, traditions, and theories. Accounting, Auditing & Accountability Journal 30 (2):433–69. doi:https://doi.org/10.1108/AAAJ-04-2015-2039.

- Miller, B. P. 2010. The effects of reporting complexity on small and large investor trading. The Accounting Review 85 (6):2107–43. doi:https://doi.org/10.2308/accr.00000001.

- Oskouei, Z. H., and Z. H. Sureshjani. 2021. Studying the relationship between managerial ability and real earnings management in economic and financial crisis conditions. International Journal of Finance & Economics 26 (3):4574–89. doi:https://doi.org/10.1002/ijfe.2031.

- Tetlock, P. C., M. Saar-Tsechansky, and S. Macskassy. 2008. More than words: Quantifying language to measure firms’ fundamentals. The Journal of Finance 63 (3):1437–67. doi:https://doi.org/10.1111/j.1540-6261.2008.01362.x.

- Wall Street. 2019. Bucharest Stock Exchange, the Highest Increase in the World in 2019.

- Wang, V., and B. Xing. 2020. Battling uncertainty: Corporate disclosures of COVID-19 in earnings conference calls and annual reports. SSRN Papers.

- Wooldridge, J. M. 2010. Econometric analysis of cross section and panel data. USA: The Mit Press.