?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The main aim of this paper is to examine the non-linear relationship between financial performance and level of dividends for a recent period and an international sample. Subsidiary, we have included some firm characteristics to revisit their influence over the level of dividends paid. Using both GMM and Quantile Regression, we found that there is a non-linear relationship between the level of dividends paid and financial performance. Among the dividend theories, the signaling effect theory, the lifecycle theory, and the catering theory of dividends are supported through our results.

1. Introduction

The magnitude of dividend policy is a hot topic of study in corporate finance given that managers and security analysts spend much time with this decision. A consensus has not yet been found regarding dividend predictability and therefore is considered one of the few unsolved problems in financial economics. In the literature, the fact that firms that pay dividends tend to be rewarded by markets with higher valuations is a departure from rationality which needs further study.

Dividend policies are influenced by several factors, which could mainly be grouped into three categories: firm characteristics, market characteristics, and substitute forms of payout (a synthesis of previous findings could be seen in Denis and Stepanyan (Citation2009); Frankfurter, Wood, and Wansley (Citation2003)). Starting with Lintner (Citation1956), continuing with Miller and Modigliani (Citation1961), Elton and Gruber (Citation1970), and Black (Citation1976), more and more hypotheses have been proposed about the factors influencing companies’ dividend policies. Researchers found new links that go beyond financial performance indicators and focus on corporate governance factors, political factors, and factors related to the company’s management.

If there is a consensus on the issue of dividend policies, it is that in recent years, there has been a growing interest in this subject. According to Pinto et al. (Citation2020), 768 articles on dividend policies have been published so far, and the distribution of this figure has increased from 1–6 articles per year between 1968 and 2000 to 82 articles in 2016. The average annual increase in the number of indexed articles on this topic is 21%. Since 2010, research has diversified into several areas. Some authors focus on multidisciplinary research seeking influences in the sociocultural area, while other authors focus on the area of corporate governance and public perception of the company, all in close correlation with classical financial and non-financial indicators. Lee and Wang (Citation2022) studied extra variables such as climate risk impact and CEO entrenchment and their impact on financial indicators.

Non-linear relationships are common in economic theory, and such relationships are also frequently tested empirically. For instance, in corporate policy, dividends are a function of financial performance, and financial performance depends on sales and costs and thus must exhibit a maximum. Prior literature suggests the potential non-linearities between dividends and earnings (Grullon et al. Citation2005), firm performance (Anderson and Reeb Citation2003), and financial decision (Shaddady Citation2022).

The purpose of this research is to analyze the dividend theories for a new, more recent international dataset, using a non-linear hypothesis and endogenous empirical models. The main hypothesis of the research is that there is a non-linear relation between the level of dividends paid by firms and financial performance.

The contribution of this article is that while others tested the non-linear relation between the level of dividends paid and company age, level of indebtedness we try to find the non-linear relation between the level of dividends paid and financial performance measured through ROA. We also introduce two composite financial indicators in the dividend dilemma, namely the capital maintenance ratio and the debt holder monitoring indicator. Using both GMM estimations and quantile regressions, the results suggest a non-linear, inverse normally distributed nexus with performance. In addition, the coefficients for certain controls support several dividend theories, such as signaling effect theory, lifecycle theory, and catering theory of dividends.

The paper is structured as follows: the following section summarizes empirical considerations regarding the dividend theories. The third section describes the data collection, measurement, and methodological framework. The empirical results are provided in section four, followed by a robustness section, whie the last section concludes.

2. Literature Review

The first researchers to address the issue of dividend policies were Lintner (Citation1956), Miller and Modigliani (Citation1961), Elton and Gruber (Citation1970), Black (Citation1976), and Rozeff (Citation1982) who built empirical models and tested numerous econometric models to explain the behavior of companies regarding dividend policies. Lintner (Citation1956) opened the discussion by writing an article about the signaling effect of dividends, about how company managers adjust the percentage of dividend distribution according to investors’ expectations and the company’s goals.

Miller and Modigliani (Citation1961) contradicted Lintner (Citation1956) and argued for the irrelevance of dividends, saying it does not matter in the long run if a company does not pay dividends because the growth of the value of stocks as a result of profit reinvestment will offset the impact of not paying dividends.

Although there is a lot of the literature on company dividend policies, the actual motivation for paying dividends is still unclear. Black (Citation1976) described the situation of this lack of consensus on dividend policies as a puzzle, noting that the more we look at the issue of dividends, the more it resembles a puzzle whose pieces do not fit. Even though more than 4 decades have passed since Black’s statement, his observation is still valid today. Brealey and Myers (Citation2003) described the issue of dividend policies as one of the top 10 unresolved issues in finance. In the context of emerging markets, studies have shown that these markets tend to behave much differently from emerging markets due to factors, such as political, social, and financial instability.

More recent trends in research on the topic of dividend policies approach the area of corporate governance and its impact on the capacity of the firm to pay dividends. Authors such as Gyapong et al. (Citation2021) studied the impact of the diversity of the board on the payment of dividends, especially in companies that have problems with the agency cost. They found that an ethnically diverse board involved closer monitoring of the company’s resources and directors with respect to the company’s shareholders, bringing in cash flow available for distribution as dividends by reducing the costs of the parent–agent conflict. Benlemlih (Citation2019) conducted a similar study on a sample of 3,100 US companies from 1991 to 2012 concluding that when companies have a developed CSR dimension, the level of dividends paid is more consistent than in the case of companies that do not allocate resources to CSR. Usually, the implementation of CSR policies in emerging countries comes with a compliance cost, its benefits being seen only with the passage of time. This hypothesis is confirmed by Aziz, Hossain, and Lamb (Citation2021), who found that the effect of ESG policy tightness on the economic environment is negative in the short term but positive in the long term.

Pinto et al. (Citation2020) conducted a bibliometric analysis on the literature regarding the topic of dividend policies on the 2000–2015 timeframe. In order to extend the analysis performed by Pinto, we performed a bibliometric analysis focused on the 2015–2021 timeframe and several remarks could be drawn up (Mihancea, Pirtea, and Botoc Citation2021). First, empirical analysis (Fixed effects) is the most encountered research methodology, and therefore, we decided to examine further with empirical methods like GMM which was less used. Second, in terms of factors analyzed, financial variables are predominating, but there is an emergence of independent variables in the field of corporate governance and ESG. Life cycle theory and signaling effect theory represent over 50% of the influences found on the level of dividends paid. However, new factors of influence appear, such as corporate governance, the diversity of the board, and the independence of the board, which have not been analyzed until recently.

Third, we found that most authors suggest a positive relationship with financial performance, like Akhibe and Madura (Citation1996) and Boehme and Sorescu (Citation2001) but limited papers approached the empirical analysis by looking for a non-linear relation, and there was none approaching the non-linear relation between the level of dividends paid and financial performance. This gap from previous findings motivates our empirical work on which we intend to build with different models and variables, both financial and non-financial.

The hypothesis that there is a non-linear relationship between the level of dividends paid and financial performance comes from the cost of opportunity of paying dividends instead of reallocating free cash flow to areas which need investment. According to Huwei, Qiming, and Lee (Citation2022), manufacturing companies started to invest in innovation activities on the road to digital transformation. The agency cost problem is highlighted by Lee et al. (Citation2022) where CEO entrenchment regarding the choice of debt maturity affects the financial performance of the firm. Choosing to pay dividends and taking on supplementary debt to fund the investment needs of the firm has a negative impact on the financial performance of the company due to interest costs. Executives use dividend smoothing to improve company valuation, as shown by Liu and Chen (Citation2014) and Fukuda (Citation2000) who studied the signaling effect of dividend policies. All these factors collude toward a non-linear relationship where more dividend payments will eventually hinder the evolution of the financial performance of the firm.

There are several authors who analyzed the dividend theories in the non-linear hypothesis, such as Fliers (Citation2019) who found a non-linear relationship between the level of dividends paid and the unused capacity for indebtedness of a company. Tamimi, Takhatei, and Malchi (Citation2014) found a non-linear relationship between the level of dividends paid and the age of the company and the degree of indebtedness. Mbulawa et al. (Citation2020) also found a non-linear relationship between the level of dividends paid and the age of the company but only in times of hyperinflation on a sample of firms listed on the Zimbabwe Stock Exchange.

The research hypotheses designed for our empirical work are as follows:

H1:

The financial performance effect on the level of dividends paid is non-linear.

and

H2:

Firm characteristics (size and debt holder monitoring) affect the level of dividends.

3. Methodology, Research Hypothesis, and Data Collection

The data have been collected from the Compustat Global database, with an initial sample of 486,803 observations and 45,112 companies with several gaps. The selected period is from 2006 to 2021. The database provides information on the identification of companies, such as stock exchange identification symbol, year of establishment, and others, as well as financial indicators. We required dividend data for the entire period, therefore the final database includes 5056 companies and 60,103 firm observations, from 59 countries. There are variations in terms of frequencies for certain countries and sectors (see Annex 1) which motivate us to perform a robustness check in the following sections.

The dependent variable used in the empirical analysis is the natural logarithm of dividends paid by companies in a financial year (DIV). The reason we have introduced the level of dividends paid to the detriment of the dividend payout ratio is to avoid spurious correlation because Earnings is the numerator of ROA – the proxy for variable of interest – and Assets is used as a proxy for size.

The independent variables used are mostly financial variables, some being classical analysis tools, others being more recent, introduced especially in the empirical model to see if they have an influence on the way companies pay dividends.

Out of these independent variables, ROA and its square are the independent variables of interest, while the others are treated as independent variables of controls (). We are aware that no single measure is perfect, but we select ROA because (i) ROE is sensitive to changes in capital structure, (ii) it is not affected by special items, and (iii) market performance is sensitive to stock market efficiency.

Table 1. Summary of independent variables.

The econometric methodology used to conduct the empirical research is to apply linear regressions with fixed effects (FE), random effects (RE), and the Generalized Method of Moments (GMM) in order to tackle the endogeneity issue.

The model has the following general form:

where:

Y – represents the dependent variable – DIV

X – represents the independent variable of interest – ROA

Z – represents the independent variables of control – AUN, AUO, DHM, RETL, SIZE, CR, and CMR.

u – represents the standard error.

Throughout the econometric models selected, we will treat the model in its extended form as follows:

The preliminary analysis of the raw dataset shows the existence of outliers for ROA, ROA2, RETL, CR, and CMR and therefore have been winorized accordingly. The descriptive statistics can be seen in and can notice that on average companies are paying dividends and have low financial performance ():

Table 2. Descriptive statistics of the data sample.

In order to ensure there are no autocorrelation issues, we performed an autocorrelation test which showed that there are no autocorrelation issues in the dataset ().

Table 3. Correlation matrix.

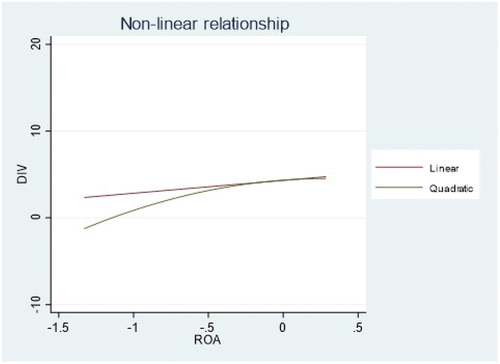

Regarding the functional form between the financial performance and the level of dividends paid, the plot analysis indicates potential non-linearities, the correlation between ROA and dividends paid having initially an upward trend followed by a slower growth before reaching an upper level. This fact is highlighted in :

Figure 1. The non-linear relationship between DIV and ROA.

In addition, the U-test proposed by Lind and Mehlum (Citation2010) rejects the null hypothesis and hence confirms the existence of a non-linear relation between financial performance and dividends paid.

4. The Results of the Empirical Analysis

The research strategy comprises four econometric models, namely an OLS regression, a random effects regression, a fixed effects regression, and a GMM model. The role of the OLS regression is to show the sign and the level of significance of the independent variables on a classic model, as simple as OLS.

Panel models suffer from econometric interferences caused by the correlation between fixed effects and the prior values of the dependent variable. Nerlove (Citation1967) and Nickell (Citation1981) observed this phenomenon in the case of OLS regression models and established that the severity of the interference is reduced after T = 30 periods, but this is not helping on Compustat database-derived models because they usually hold maximum 15 years of historical data. On datasets of less than 30 periods (years), GMM models are recommended because they solve the endogeneity issues which, according to Ketokivi and McIntosh (Citation2017), can be so severe that coefficients can have different signs.

GMM models use the lags of the dependent variables as instruments to control the endogeneity of the variables and produce consistent results under endogeneity conditions. According to Wintoki et al. (Citation2012) and Schultz, Tan, and Walsh (Citation2010), two lags are enough to capture the effect of prior values upon the dependent variable in the econometric model, which is the reason why we used two lags in the model.

presents the OLS model, the regressions with random effects and fixed effects and the GMM model, where DIV is the dependent variable, ROA is the independent variable of interest, and AUN, AUO, DHM, RETL, SIZE, CR, and CMR are independent control variables.

Table 4. Results of the empirical analysis.

The results in column (1) are related to the OLS regression and suggest a strong positive relationship between the company’s financial performance measured by ROA and its squared value and the level of dividends paid, significant at the level (p < 1%). AUN has a strong negative and significant effect at the level (p < 1%) of dividends paid, as it is very likely that there will be material errors that hide a precarious financial situation of the company. Similar result is obtained in the case of the auditors’ opinion, which has a negative effect on the level of dividends paid, with a level of significance (p < 1%). One interpretation of this result may be that management covers potentially reserved opinions by paying more substantial dividends to reassure investors. The DHM variable has a strong negative impact, being significant at the level (p < 1%).

This result highlights the fact that a large share of total debt liabilities to financial institutions erodes the profit available for distribution and further erodes the cash flow available for payment to shareholders because in addition to interest affecting the company’s profit there is a negative impact on the cash flow of the company by paying the principal on the contracted loans. The size of the company, SIZE, has a strong positive impact on the level of dividends paid, with a level of significance of p < 1%, confirming the dividend theory of the company’s life cycle. Mature companies, which are on a plateau in terms of growth through new opportunities that require investment, can afford to pay more substantial dividends as opposed to young companies that allocate capital for investment.

Current liquidity, as measured by the independent variable CR, has a negative and significant influence at the level (p < 1%) on dividends paid by companies, which rejects the dividend theory of available cash flows. The level of liquidity along with the financial performance of the company plays a decisive role in the distribution of dividends in any company. CMR has a positive and significant impact at the level (p < 1%) which rejects the initial hypothesis that supposed the existence of a negative relationship between the degree of maintenance of the productive capital of the company. Thus, capital maintenance involves the acquisition of new tangible and intangible assets to replace the used ones, which brings additional expense with depreciation, reducing the profit and significantly affecting the company’s liquidity level at the time of the acquisition of the asset, indirectly reducing the company’s ability to pay dividends. RETL, the share of the retained earnings in total liabilities, has a negative impact on the level of dividends paid by the company, in line with life cycle theory.

For the fixed effects regression, suggested by the Hausman test as superior to random effects, the financial performance measured by ROA and its squared value has a strong positive impact with a significant level (p < 1%) on the level of dividends paid, similarly to the result obtained in the OLS regression.

In column 4, we turn to the GMM-System estimation proposed by Arrelano and Bond to control endogeneity issue. To get consistent estimation, it is important to determine what variables are endogenous and how many lags to include as internal instruments. The results of specific tests suggest that ROA, AUN, DHM, RETL, and CR are likely to be endogenous, and all remaining variables should be treated as exogenous. Consequently, we use as instruments only lagged t-2 and earlier for endogenous variables, as well as for dependent variables. Furthermore, we use the orthogonal option to maximize sample size, we use the collapse option to avoid instrument proliferation, and we use two-step estimation with robust option to trigger Windmeijer correction of standard errors. The results for variables of interest still suggest a positive and non-linear relationship between firm performance and dividends.

We are aware of the limits of GMM system and difference estimation (i.e., incorrect estimates in some cases when forward-orthogonal deviations are combined with standard instruments), and therefore we include GMM estimation of linear (dynamic) panel data model (DPDGMM) proposed by Kripfganz (Citation2020) which can incorporate additional non-linear moment conditions. The coefficient for the ROA variable (β1) is positive and for its square (β2) is positive too. Thus, the results do not reject the research hypothesis, suggesting the existence of a non-linear relation between firm performance and level of dividends, for all methods considered.

5. Robustness Check

A first robustness check is related to country and GIC sector distribution. Given that 38% of firm-observations are for the USA and 29% are for Japan, we split the sample into three sub-samples (i.e., USA firms, Japan firms, and firms from other countries). Furthermore, we split the initial sample into other two sub-samples, one for the Industrials GIC sector, i.e., 20, which counts for 21% of firm observations and one for the remaining GIC sectors.

The results for the DPDGMM method are reported in where several remarks can be considered. First, for the USA as well as for Japan firms, the non-linear hypothesis is rejected. Second, for firms from other countries included in our sample, the non-linear hypothesis is not rejected since both ROA and its square coefficient are statistically significant. Such results could be explained by differences in stage of growth as previous findings suggest that dividend payouts are less affected by firm characteristics in countries with a high uncertainty avoidance index compared with countries with a low uncertainty avoidance index (Chang, Chang, and Dutta Citation2020). Third, the non-linear relationship is robust to the GIC sector.

Table 5. Robustness check for country and industry level.

Our results complement previous findings for the non-relationship models by validating an existing non-linear, inverse normally distributed nexus with performance. Shaddady (Citation2022) found a non-linear inverted U-shaped relation between the financial structure decision and dividend payouts for Saudi Arabia’s firms. For American companies, Grullon et al. (Citation2005) show that dividend changes are uncorrelated with future earnings changes when one controls for the well-known non-linearities in the earnings process.

The dynamic nature of our dividend model is confirmed by the significance of the coefficient for the first lag of the dividend, which is robust for all sub-samples considered and in line with bird-in-hand theory. From the controls, the most robust variable is SIZE which is positively associated with dividend for all sub-samples, in line with life cycle theory.

The second robustness analysis deals with the estimation method. In this respect, we examine the non-linear relation with quantile regression models given that is likely to provide a more comprehensive picture of the relationship between firm performance and dividends. provides the results for the relevant quantiles.

Table 6. Robustness check – coefficient estimates from quantile regressions.

Regarding ROA and its square, the sign and significance are consistent with OLS, whereas the sign indicates for both that the relationship is concave upward with a slight slope for square. This suggests that the positive effect is more pronounced for firms at the lower performance quantiles than firms at the higher quantiles. Such results are in line with life cycle theory: as firms grow and become mature, their capacity to deliver performance will be limited, and dividends follow a smoother path than performance.

6. Conclusions

The aim of this article was to examine the non-linear relationship between firm performance and the level of dividends paid for a sample of international companies. Subsequently, it was of interest if for a recent period levels of dividend are influenced by other firm characteristics, either representatives like size or compound financial indicators like debt holders monitoring.

For our panel data, we address the heterogeneity issue by estimating Quantile Regression and alternatively the endogeneity issue by estimating GMM methods. The results suggest a non-linear and inverse normally distributed nexus with performance, in line with signaling theory. Sensitive different results (i.e., monotonic relation) are reported for individual USA and Japan sub-samples whereas GIC sector sub-samples are robust. From an economic perspective, such non-linear models suggest that investors might perceive psychological threshold to upward movements in financial performance, and when the threshold is reached, new dividend-based investors might enter the market. An alternative interpretation is related to the market model which suggests that non-linearity is due to the uncertainty attached to the quality of the manager.

From controls, the size of the companies is a robust determinant that positively influences the level of dividends, in line with life cycle theory. On the other hand, debt holder monitoring is negatively associated with the level of dividends, which suggests that management finances investment targets hierarchically according to pecking order theory. Among the remaining controls, the statistically significant coefficients show that some of the classical dividend theories are still relevant.

The policy implications of our results are significant for stakeholders, such as institutional investors, banks, and private investors, because they need to know the factors that drive dividend policies in order to allocate their financial resources in their share portfolio suited to their investing objectives. A better understanding of the dividend policy topic should lead to better yields for investors across their portfolios. For instance, it might be used for redesigning triggered strategies followed by private investors participating in portfolio schemes who commit themselves to buying or selling when their financial performance reaches a predetermined level.

Our analysis could highlight new directions of research that may yield new influence factors on the level of dividends paid. One of these new directions of research is the integration of ESG variables in the empirical analysis, in order to analyze the impact of these factors on dividends.

Disclosure Statement

No potential conflict of interest was reported by the author(s).

References

- Akhibe, A., and J. Madura. 1996. Dividend policy and corporate performance. Journal of Business Finance & Accounting 23 (9–10):1267–87. doi:10.1111/1468-5957.00079.

- Anderson, R. C., and D. M. Reeb. 2003. Founding‐family ownership and firm performance: Evidence from the S&P 500. The Journal of Finance 58 (3):1301–28. doi:10.1111/1540-6261.00567.

- Aziz, N., B. Hossain, and L. Lamb. 2021. Does green policy pay dividends? Environmental Economics and Policy Studies 24 (2):147–72. doi:10.1007/s10018-021-00317-7.

- Benlemlih, M. 2019. Corporate social responsibility and dividend policy. Research in International Business and Finance 47:114–38. doi:10.1016/j.ribaf.2018.07.005.

- Black, F. 1976. The dividend puzzle. The Journal of Portfolio Management 2 (2):5–8. doi:10.3905/jpm.1976.408558.

- Boehme, R. D., and S. M. Sorescu. 2001. The long-run performance following dividend initiations and resumptions: Underreaction or product of chance? The Journal of Finance 57 (2):871–900. doi:10.1111/1540-6261.00445.

- Brealey, R. A., and S. C. Myers. 2003. Principles of corporate finance. International Edition, 7th ed. New York: McGraw-Hill.

- Chang, M., B. Chang, and S. Dutta. 2020. National culture, firm characteristics, and dividend policy. Emerging Markets Finance and Trade 56 (1):149–63. doi:10.1080/1540496X.2019.1627518.

- Denis, D., and G. Stepanyan. 2009. Factors influencing dividends. Dividends and Dividend Policy 55–69.

- Elton, E. J., and M. J. Gruber. 1970. Marginal stockholder tax rates and the clientele effect. The Review of Economics and Statistics 52 (1):68–74. doi:10.2307/1927599.

- Fliers, P. T. 2019. What is the relation between financial flexibility and dividend smoothing? Journal of International Money and Finance 92:98–111. doi:10.1016/j.jimonfin.2018.12.009.

- Frankfurter, G., B. G. Wood, and J. Wansley. 2003. Dividend policy: Theory and practice. Elsevier.

- Fukuda, A. 2000. Dividend changes and earnings performance in Japan. Pacific-Basin Finance Journal 8 (1):53–66. doi:10.1016/S0927-538X(99)00024-4.

- Grullon, G., R. Michaely, S. Benartzi, and R. H. Thaler. 2005. Dividend changes do not signal changes in future profitability. The Journal of Business 78 (5):1659–82. doi:10.1086/431438.

- Gyapong, E., A. Ahmed, C. G. Ntim, and M. Nadeem. 2021. Board gender diversity and dividend policy in Australian listed firms: The effect of ownership concentration. Asia Pacific Journal of Management 38 (2):603–43. doi:10.1007/s10490-019-09672-2.

- Huwei, W., Z. Qiming, and C. Lee. 2022. Digitalization, competition strategy and corporate innovation: Evidence from Chinese manufacturing listed companies. International Review of Financial Analysis 82:102166. doi:10.1016/j.irfa.2022.102166.

- Ketokivi, M., and C. N. McIntosh. 2017. Addressing the endogeneity dilemma in operations management research: Theoretical, empirical, and pragmatic considerations. Journal of Operations Management 52 (1):1–14. doi:10.1016/j.jom.2017.05.001.

- Kripfganz, S. 2020. XTDPDGMM: Stata module to perform the generalized method moments of linear dynamic panel models.

- Lee, C., and C. Wang. 2022. Liquidation threat: Behavior of CEO entrenchment. Finance Research Letters 47:102949. doi:10.1016/j.frl.2022.102949.

- Lee, C., C. Wang, B. Thinh, and Z. Xu. 2022. Climate risk and bank liquidity creation: International evidence. International Review of Financial Analysis 82:102198. doi:10.1016/j.irfa.2022.102198.

- Lind, J. T., and H. Mehlum. 2010. With or without U? The appropriate test for a U‐shaped relationship. Oxford Bulletin of Economics and Statistics 72 (1):109–18. doi:10.1111/j.1468-0084.2009.00569.x.

- Lintner, J. 1956. Distribution of incomes of corporations among dividends retained earnings, and taxes. The American Economic Review 46 (2):97–113.

- Liu, C., and A. Chen. 2014. Do firms use dividend changes to signal future profitability? A simultaneous equation analysis. International Review of Financial Analysis 37:194–207. doi:10.1016/j.irfa.2014.12.001.

- Mbulawa, S., N. F. Okurut, M. M. Ntsosa, and N. Sinha. 2020. Determinants of corporate dividend policy under hyperinflation and dollarization by firms in Zimbabwe. Journal of Applied Finance & Banking 10 (2):1–24. doi:10.25103/ijbesar.133.06.

- Mihancea, E. A., M. G. Pirtea, and F. C. Botoc. 2021. Bibliometric analysis on the recent trends in dividend policy research. Ovidius University Annals, Economic Sciences Series (2):1051–59.

- Miller, M., and F. Modigliani. 1961. Dividend policy, growth, and the valuation of shares. The Journal of Business 34 (4):411–33. doi:10.1086/294442.

- Nerlove, M. 1967. Experimental evidence on the estimation of dynamic economic relations from a time series of cross sections. The Economic Studies Quarterly 18:42–74. doi:10.11398/ECONOMICS1950.18.3_42.

- Nickell, S. 1981. Biases in dynamic models with fixed effects. Econometrica 49:1417–26. doi:10.2307/1911408.

- Pinto, G., S. Rastogi, S. Kadam, and A. Sharma. 2020. Bibliometric study on dividend policy. Qualitative Research in Financial Markets 12 (1):72–95. doi:10.1108/QRFM-11-2018-0118.

- Rozeff, M. S. 1982. Growth, beta and agency costs as determinants of dividend payout ratios. Journal of Financial Research 5 (3):249–59. doi:10.1111/j.1475-6803.1982.tb00299.x.

- Schultz, E. L., D. T. Tan, and K. D. Walsh. 2010. Endogeneity and the corporate governance - performance relation’. Australian Journal of Management 35 (2):145–63. doi:10.1177/0312896210370079.

- Shaddady, A. 2022. The effect of the financial structure decision and governance mechanism on shareholders’ wealth: Nonlinearity evidence from a petroleum‐based economy. Asia‐pacific Journal of Financial Studies 1–37. doi:10.1111/ajfs.12400.

- Tamimi, M., N. Takhatei, and F. Malchi. 2014. Relationship between firm age and financial leverage with dividend policy. Asian Journal of Finance & Accounting 6 (2):53. doi:10.5296/ajfa.v6i2.5910.

- Wintoki, M., L. Babajide, S. James, and J. M. Netter. 2012. Endogeneity and the dynamics of internal corporate governance. Journal of Financial Economics 105 (3):581–606. doi:10.1016/j.jfineco.2012.03.005.