Abstract

Based on a review of both interdisciplinary and policy literature pertaining to the intertwined issues of global economic recovery and sustainability, this article derives a framework of transformational adaptation organized around four objectives. First, we prospect the emergence of a green financing system to integrate international capital markets that sets priorities for climate financing and encourages progress toward the United Nations Sustainable Development Goals (SDGs) to foster energy sustainability in concert with the development of Industry 4.0 on a global scale. Second, this article articulates the imperative of embracing developing economies under a green recovery framework. Third, we point out the recent advancement in cost efficiency of clean energy technologies that rationalize financial decisions for the replacement of fossil fuels. Finally, the study reveals the clustering of green financing institutions as globally distributed hubs for redirecting investments into sustainable infrastructures consistent with the goal of mitigating climate change as advocated in the Paris Agreement. We identify the main challenges that constrain this transformational adaptation, particularly timely technology transfer of advanced clean energy technologies across the globe.

Introduction

The Paris Agreement, based on the United Nations Framework Convention on Climate Change (UNFCCC), was originally signed by 196 countries in 2015 and aims to address climate risk through reduction of greenhouse-gas emissions on a global scale. Rapid globalization reliant on the conventional economic development model driven by ever-escalating consumer-based market demand as the basis for economic growth is the challenge to sustainability of the global ecosystem. Unpredictably, the recent COVID-19 crisis has drastically slowed down the global economy, resulting in financial stress for many business entities (Gates Citation2020; IMF Citation2020). At the same time, a substantial reduction in utilization of transportation as well as consumption of energy has been documented (IEA Citation2020). In the first quarter of 2020, the world’s energy demand declined by 3.8%; in particular, weekly energy demand reportedly dropped by an average of 25% for countries in full lockdown and 18% for countries in partial lockdown (IEA Citation2020). Air quality reportedly improved noticeably around the globe (AGU Citation2020).

The ongoing crisis triggered by the pandemic reflects vulnerabilities in stable employment within the service economy and continued reliance on fossil fuels affected by various storage and distribution problems (Farmbrough Citation2020; Kucik and Leister Citation2020). For economic recovery, there is a growing consensus that the world needs to rebuild its economy with a focus on resilience through a green recovery framework that enhances social, environmental, and economic sustainability under a reformed financial system (de Vries Citation2019; Di Marco, et al. Citation2020; IISD Citation2020a). There is also a compelling need for humanity to mitigate and develop strategies for adapting to the risks associated with ecosystem instability arising from the threat of climate change (Kinney Citation2018; Leal Filho, Nagy, and Ayal Citation2020). Particularly in terms of human health, there have been studies documenting the relationship between exposure to air pollution and ecological vulnerability to adverse human outcomes, such as infection risks and death rates related to COVID-19 (Acharya and Porwal Citation2020; Wu et al. Citation2020).

In light of these concerns, international institutions have encouraged governments around the world to formulate economic stimulus to promote development toward a more sustainable economy instead of continuing to rely on a model that generates more unwanted emissions and other pollutants that adversely affect human health (IISD Citation2020b; United Nations Citation2020a, Citation2020b). Moreover, prioritization of an economic recovery model that facilitates the development of Industry 4.0 and is energized by investments in infrastructure for clean and sustainable energy would enable healthier and smarter cities around the world (Foxon Citation2018; Farmbrough Citation2020; Lom, Pribyl, and Svitek Citation2016; UNIDO Citation2020). Under Industry 4.0, new technologies would revolutionize existing value chains from the design phase to the end-of-life phase with waste minimization embedded in the process (Ribeiro et al. Citation2020). These responses will remain prominent in the evolution of a resilient social and healthcare system capable of dealing with future pandemic and public health crises instigated by climate change (Leal Filho, Nagy, and Ayal Citation2019; EUTEG Citation2020). A recent study also suggests that such an initiative could trigger transitional, and even transformational, adaptation toward sustainable development (Loginova and Batterbury Citation2019). For business enterprises around the world to become more sustainable, it will be necessary for them to undergo systemic transformation that is harmonious with the ecosystem through broader stakeholder engagement beyond the focus on shareholders (Waddock Citation2020). However, a concerted framework to examine the key components of such an ecosystem on a global scale for implementation toward sustainability has not yet been developed.

In addition to the ongoing initiatives by developed nations to foster such an ecosystem, the world needs to prioritize the developing economies and regions in a strategic policy framework for economic recovery plans that foster sustainability. Most nations in the world fall into the category of developing countries and have substantially greater populations than the developed ones. For instance, only 16.3% of the global population lives in what are generally regarded to be developed countries (United Nations Citation2020b). The least developed countries are concentrated on the African continent and have been particularly vulnerable to the adverse impacts of climate change. As a consequence, continuing migration from developing to developed countries has resulted in enormous social and economic challenges. A concerted approach to engaging the developing economies and regions in the impending transformational adaptation for economic recovery through technology transfer is a desirable and promising pathway for sustainable development. This article contributes to the existing literature by articulating a framework to link the underlying components and key attributes of the global ecosystem.

In the next section, we develop a conceptual framework for this transformational adaptation based on an interdisciplinary literature review of the intertwined issues, including the emergence of Industry 4.0, access to clean energy, adoption of clean energy technologies (i.e., renewable energy and electric vehicles that are emission-free), and the advent of a green finance system on a global scale. The third section proposes a framework based on these relevant components and the fourth section discusses the ongoing development of green financial hubs that are crucial to the developing economies and regions in seeking capital for financing and investing into sustainable infrastructures. The conclusion describes the main challenges and outlines opportunities for further studies.

Method: conceptual framework development

Interdisciplinary literature review

Prior studies suggest that different regions of the world could experience three main types of adaptation: incremental, transitional, and transformational pathways toward sustainable development (Pelling Citation2011; Loginova and Batterbury Citation2019). While transformational adaptation could create long-term and intergenerational changes, it is envisaged to contest the status quo of economic and social systems. Embracing the United Nations Sustainable Development Goals (SDGs) as the global initiative, this study looks into pertinent industrial advancement, technological innovation, and evolving green finance practices as intertwined components of an emerging global ecosystem (Leach et al. Citation2018; de Vries Citation2019; Waddock Citation2020). These components are substantiated by the following interdisciplinary literature review on their relevance to this conceptual framework.

Advancing toward sustainable industries: Industry 4.0 and beyond

Since the first Industrial Revolution nearly 200 years ago, there have been waves of change associated with upgrading manufacturing technologies to improve efficiency and financial returns under a market-based economy. Adverse environmental impacts have followed. As pertinent technologies have been transferred continually from developed to developing economies over time, similar concerns over environmental damage remain (Ashford and Hall Citation2019). Nevertheless, with the advancement of computing technologies, Internet, big data analytics, and other related applications, there is expectation for an upcoming cleaner and more intelligent industrial development. Earlier studies have already revealed that creative destruction would be possible through diffusion of new technologies and changes in industrial structure over an extended period (Perez Citation1983; Freeman and Perez Citation1998; Freeman and Louca Citation2001; Dewick, Green, and Miozzo Citation2004; Dewick et al. Citation2006). More recently, this transition has come to be referred to as Industry 4.0. (Bonilla et al. Citation2018; Lopes de Sousa Jabbour et al. Citation2018; Tseng et al. Citation2018).

Such an innovative approach through adoption of new technologies under Industry 4.0 could reduce ecological impacts by effective alignment with the SDGs (Oláh et al Citation2020). Cleaner production, as well as reduced environmental impacts over the entire life cycle of products, is expected from outcomes of more advanced production processes that facilitate environmental sustainability under such digitized operations (Ghobakhlooab Citation2020; Ribeiro et al. Citation2020). In early Citation2021, the European Commission released its policy document on the prospect of Industry 5.0 that embraces sustainable, human-centric, and resilient industrial developments to complement the existing Industry 4.0 paradigm by further emphasizing research and innovation (EC Citation2021).

Access to sustainable levels of clean energy on a global basis and for the developing countries

For economic recovery based on the principles of environmental sustainability and human health, the framework of the SDGs should be referenced as the base (United Nations Citation2020a). This current approach embraces SDG 7 that advocates advancing universal energy access and in particular meeting the needs of clean energy solutions for a very large proportion of the global population in the developing economies that presently have limited access to electricity (Nathwani and Kammen Citation2019). Energy access is a powerful multiplier of virtually all of the SDGs. Energy services are intricately linked to the provision of adequate health and educational services that depend on a reliable infrastructure. The delivery of clean water and irrigation for agriculture, the capacity to transport produce to markets without spoilage, the ability to cook with cleaner energy sources, the reduction of drudgery and burden on women for critical household tasks, and the economic empowerment of individuals through labor-saving devices all rely on affordable energy services. It is estimated by the World Bank that only about 35% of people in developing countries have access to the Internet in comparison with 80% in the advanced economies (World Bank Citation2020). In fact, broadband Internet access is considered to be the foundation for development of smart infrastructure for Industry 4.0. Universal energy access can be within reach but requires rapid diffusion of clean energy options.

Energy access is defined by the International Energy Agency (IEA) as “a household having reliable and affordable access to both clean cooking facilities, and to electricity, which is enough to supply a bundle of energy services initially, and then an increasing level of electricity overtime to reach the regional average” (IEA Citation2011) Energy access is one key pathway to reduction of endemic global inequality but it will require radical progress in the development of scientific and technological solutions to deliver a reduction of costs by an order of magnitude. Low-cost energy from renewable sources delivers high-value impacts on life quality especially for people in the developing economies who are seeking fundamental improvement in their livelihoods and access to other basic infrastructures.Footnote1

If the energy poor are to be drawn into the mainstream of global economic well-being, then access to low-cost energy is a fundamental requirement. Energy poverty remains a barrier to economic well-being for such a large proportion of humanity that the rationale for action now is compelling.Footnote2 To reach universal access at full 24 × 7 grid power would require investments amounting to an estimated US$50 billion annually or US$500 billion over ten years (World Bank Citation2017).Footnote3 This is a high-level approximation that translates to a commitment at a level of about US$50 per person per year over the course of a decade. Investments on this scale provide an anchor to consider the level of funding appropriate to bring to fruition an operational concept of a global extension service linked to a network of Energy Access Innovation Centers (EAICs) for facilitating technology transfer (Nathwani and Kammen Citation2019). With respect to the concept of a network of EAICs on a global scale, four domain areas of inquiry and research are identified as (1) generation, devices, and advanced materials, (2) micro-grids for dispersed power, (3) information and communications technology (ICT) for energy-system convergence, and (4) environmental and human dimensions of energy-system transitions (Nathwani and Kammen Citation2019). Its design goal is to create a convergence of solutions for Industry 4.0 that is applicable to the objective of meeting the requirements of affordable energy for universal access. Despite conventional concerns about the overall funding requirements, recent improvement in cost effectiveness of clean energy would make this vision achievable.

Adoption of clean energy technologies as a viable business decision

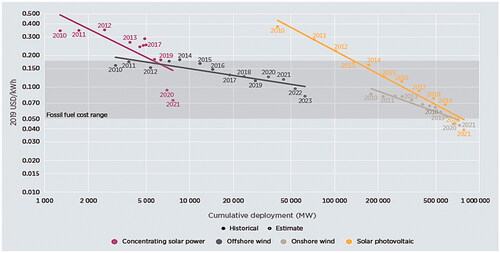

After decades of research and development and extensive adoption of clean energy technologies, namely solar photovoltaics (PV) and wind turbines, the cost structures have experienced significant favorable improvement. According to the International Renewable Energy Agency (IRENA Citation2020), newly installed renewable power capacity has become less expensive than power generation reliant on fossil fuels. summarizes the continuous decline in the cost per kilowatt hour (kWh) generated by various sources of energy from 2010 and suggests such costs from onshore wind and solar photovoltaics have already become more cost effective in comparison to fossil fuels in 2020. In fact, greater than half of the renewable energy installed in 2019 is reportedly cheaper than new coal-powered generating facilities (IRENA Citation2020). This trend is expected to continue in the coming years with improved economics and advancement of renewable energy technologies.

Figure 1. Improvement in cost effectiveness of wind and solar technologies (Source: IRENA Citation2020).

The costs of both solar and wind-power equipment have continued to decline over the last decade. Based on the report by IRENA (Citation2020), solar PV experienced the largest cost decline between 2010 and 2019 of 82% whereas concentrating solar power (CSP) dropped about 47%. In terms of electricity costs, utility-scale solar PV experienced a decline of 13% on an annual basis, resulting in US$0.068 per kWh in 2019 (IRENA Citation2020). For onshore and offshore wind equipment, its cost dropped about 9% annually whereas the related electricity costs were US$0.053 per kWh and US$0.115 per kWh, respectively, for the more recent projects (IRENA Citation2020).

IRENA (Citation2020) further estimates that replacing 500 gigawatts (GW) of coal-powered utility plants with solar and wind-power facilities could reduce the cost of such a power system by approximately US$23 billion per annum. More importantly, the replacement of legacy power-generating facilities reliant on fossil fuels would cut emissions of carbon dioxide by about 1.8 gigatonnes (GTs) (IRENA Citation2020). In fact, due to continuing aging and depreciation of existing coal-fired power generating facilities, they are expected to be costlier to operate than the utility-scale solar PV facilities. Continuing cost reductions would drive the need for aligning short-term economic needs with medium- and long-term sustainable development goals.

It is envisaged that renewable energy installations could form a key component of economic stimulus packages for the post-pandemic recovery since renewable power has become a low-cost decarbonization solution. The financial challenge of retiring legacy assets based on fossil fuels could now be dealt with through issuing green bonds from a green financial system. This recovery approach would also address the enduring concerns over energy security due to reliance on importation of fossil fuels from foreign countries.Footnote4

Emerging global green financial system that embraces risks and returns

In order to finance such a drastic transformation in various industrial sectors toward a new economy that is driven by intelligence and sustainability principles, much market-based capital would need to be allocated into pertinent tangible and intangible assets. Over the last decade, there has been growing international interest in development of a complementary green and sustainable financial system as examined in recent studies (Ng Citation2018; Dikau, Robins, and Täger Citation2019; Ng and Leung Citation2020; United Nations Citation2020a). The international capital market has advocated for this initiative by actively developing standards for sustainable investment opportunities through redesigning debt and equity instruments taking into account potential risks and returns.

First, a set of global standards for issuing green bonds has been proposed with increasing recognition of the risks related to climate change by the international lenders in making their financial decisions (CBI Citation2020a, Citation2020b). Second, equity investors and financial regulators have demanded extended disclosures on the performance of companies and their alignment with the SDGs (Adams Citation2020). A significant development was formation of the Network for Greening the Financial System (NGFS) in 2017 by a group of central banks and financial regulatory institutions to share best practices on environmental and climate-risk exposures within the global financial sector to support the transition toward a sustainable economy (NGFS Citation2020).Footnote5 Furthermore, various stock exchanges around the world now require integrated disclosures on environmental, social and governance (ESG) performance of the listed companies as such information is considered pertinent to their investment risks (Fitch Ratings Citation2020). These disclosures are expected to reduce information asymmetry within an emerging sustainable financial system when making long-term investment decisions.Footnote6

Such a convergence of interest in building a sustainable financial system that embraces both debt and equity markets is reinforced by the global efforts to tackle climate change as growing numbers of societal stakeholders have expressed grave concern about the deteriorating environment (Charnock and Thomson Citation2019). There are emerging financial regulatory measures for dealing with disclosures about the risks pertinent to climate change (TCFD Citation2020). It is anticipated that enormous capital investments would have to be allocated into clean and sustainable energy for a low-carbon economy over the coming decade through the global financial system that accounts for the risk of unsustainability (Charnock and Thomson Citation2019).

Green bonds as a long-term financial instrument for issuing debt has gained momentum in recent years to scale up green financing in different developing regions (Azhgaliyeva and Liddle Citation2020). According to the CBI (Citation2021), the total amount of green bond issuance around the world in compliance with international standards reported an approximate increase of 8.7% from 2019 to US$290 billion in 2020. The top three green bond-issuing countries are the United States, Germany and France; others come mainly from the advanced economies (see ).Footnote7 The United States alone raised US$52 billion or about 18% of the global amount. In the meantime, there has been growth in the number of other countries that participate in green bond issuances including Chile, Ecuador, Greece, India, Kenya, Panama, Russia, Saudi Arabia, Singapore and Ukraine. Funding raised from green bonds is typically allocated into financing low-carbon assets, namely renewable energy facilities, green building, and low-carbon public transportation projects.

Table 1. Top green bond issuing countries in 2020.

As mentioned above, stock exchanges around the world have in recent years started playing a noticeable role in facilitating the development of the green bond market, providing liquidity and market access while imposing regulatory and compliance measures on the fundraising entities. provides a list of the stock exchanges that have launched a dedicated green bond trading exchange or sustainable bond section, suggesting that a growing number of regional stock exchanges attached to developing economies have set up facilities to support the trading of green bonds (CBI Citation2020c).

Table 2. Global stock exchanges for green bonds.

Framework of an ecosystem

Alignment with the SDGs

In light of the disruption caused by the recent global pandemic, the SDGs have become more relevant than ever given their role as synergistic targets for different countries around the world to pursue health and energy sustainability. The linkage between health and energy sustainability is progressively recognized as a significant consideration in sustainable economic development (Yuen and Ng Citation2019). As described by SDG 7, “Lack of access to energy may hamper efforts to contain COVID-19 across many parts of the world. Energy services are key to preventing disease and fighting pandemics – from powering healthcare facilities and supplying clean water for essential hygiene, to enabling communications and IT services that connect people while maintaining social distancing.” It is fundamentally critical for the world to invest more decisively into renewable and sustainable energy that empowers the revitalization of an economy that is aligned with a healthy environment.

Framework of global green financing system to integrate energy sustainability and Industry 4.0 through technology transfer

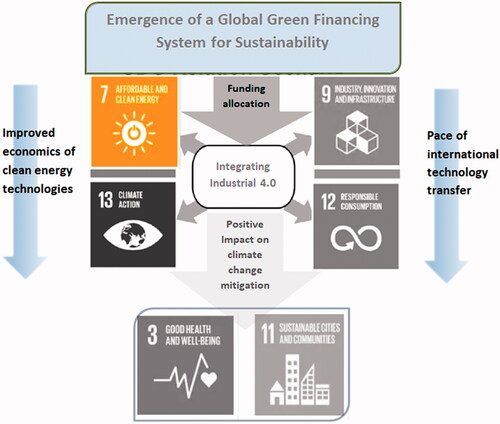

As illustrated in , the emergence of a global financial system is evidenced by the rapid development of green bonds, ESG investments, and pertinent regional stock exchanges for the secondary exchange of green investments. Affordable and clean energy is considered an integral component for Industry 4.0 that is synergistic with the development of infrastructures that in turn enhance responsible consumption and production. These concerted climate actions result in strong emphases on health and sustainability for the future cities.

Figure 2. Framework of Global Green Financing System to Integrate Energy Sustainability and Industry 4.0 for SDGs. Source: Adapted from United Nations (Citation2020a) by the authors.

In fact, the Fourth Industrial Revolution is expected to foster urban renewal among major cities through an interdisciplinary perspective on how to integrate advanced technologies and innovative industrial solutions for better quality of life by reducing the overall carbon footprints (UNIDO Citation2020). Such a transformed industrial model is directly relevant to mitigating a pandemic situation as well. There are recent studies that point out the significant role of Industry 4.0 technologies, Internet of Things, and various advanced applications, such as artificial intelligence, in combating the ongoing COVID-19 crisis (Javaid et al. Citation2020; Singh et al. Citation2020). It becomes crucial for the world to invest in energy sustainability and complementary infrastructure in pursuing the SDGs since they are a key foundation of Industry 4.0 while preparing for the arrival of Industry 5.0 under the principle of sustainability (EC Citation2021).

However, the success of these positive developments hinges on the pace of adoption of advanced clean energy via technology transfer across borders, especially into the developing economies. While the ongoing improvement in cost effectiveness of clean energy technologies is expected to accelerate such adoption, international technology transfer could be constrained by concerns over intellectual property and viability of business opportunities (Bozeman Citation2000; Ciborowski and Skrodzka Citation2020). The absence of complementary policies for international technology transfer could also impede the pertinent initiatives.

Prioritizing assets for climate-change mitigation

Development of clean and sustainable energy has over the past three decades gradually been considered by public stakeholders as critical to mitigate the emission of greenhouse gases that cause climate change (Ng and Nathwani Citation2010, Citation2018). In particular, significantly reducing the use of fossil fuels in power generation and transportation would drastically reduce greenhouse-gas emissions which would in turn be instrumental to the development of healthy and smart cities of the future.Footnote8 In financing these large-scale infrastructure projects that are vital to environmental sustainability, green bonds have long been advocated as an “instrument where the proceeds will be exclusively applied to finance or re-finance, in part or in full, new or/and existing eligible green projects” (ICMA Citation2016).

While the green bond standard developed in the financial services sector to date has a wide range of clean and sustainable energy projects that are qualified as financeable by green bonds for a meaningful reduction of carbon footprints, there are other complementary and viable assets being considered as eligible for enhancing health and energy sustainability and tackling climate-change challenges through mitigation (Sarkis et al. Citation2020). In particular, infrastructures for various clean energy and green transport projects, including manufacturing facilities and charging stations for electric vehicles, are collectively strategic to reducing the emission of greenhouse gases by diminishing the consumption of fossil fuels at a large scale. These infrastructures need to be identified as priority assets to be financed and invested in for regional and global sustainability (Ou Citation2019; Kumar and Kumar Citation2020; Wu et al. Citation2021).

Refined taxonomy by the climate bond initiatives for Industry 4.0

In addition, information and communication technologies (ICTs) are actively considered to be critical assets for Industry 4.0 and need to be included as climate-change compatible and financeable and therefore categorized in the near future as certifiable (CBI Citation2020a). For instance, there have already been green bond issuances by some European companies to finance the development of smart grid and green data-center infrastructures that would improve energy efficiency and reduce carbon footprints with material effect.Footnote9 The latest taxonomy of CBI (Citation2020a) has identified green buildings and health facilities as complementary assets for development of a sustainable economy as well as healthy and smart cities.

highlights that the taxonomy considered certified or certifiable assets for green bond financing are pertinent to development of Industry 4.0. Under this taxonomy, international technology transfer to the developing economies for energy sustainability, including those technologies related to clean energies, intelligent smart grids and electric vehicles (EVs), becomes financeable under the Climate Bond Initiative (CBI Citation2020a). This green financing opportunity could overcome the constraints in much needed technology transfer for sustainable economic development (Bozeman Citation2000; Ciborowski and Skrodzka Citation2020).

Table 3. Climate-financing taxonomy pertinent to energy sustainability and Industry 4.0.

Discussion

Pursuing common goals for the world

The proposed strategic recovery framework articulates the long-term plausibility of meeting specific SDGs and is meant to stipulate a systematic approach for an economic recovery model. However, this conceptual approach requires harmonized global political leadership, concerted structural reforms in international financial market, and intensified engagement with regional and local stakeholders. Clear goals and objectives for sustainability are desirable for the world to swiftly mitigate the spreading sustainability risks under the current trajectory. depicts the pertinent goals, objectives, means, and incentives for stakeholders.

Table 4. Clear common goals and objectives in recovery.

The advantage of this strategic recovery framework based on accelerated efforts for Industry 4.0 through energy sustainability is its design to tackle climate-change issues while synergistically revitalizing an economy rebuilt upon concerted sustainability initiatives and industry innovation. The outcomes are potentially reduced greenhouse-gas emissions and a less polluted environment – in short, a more livable and healthier Earth. Nevertheless, the main challenge remains ongoing differences in policy priorities or ideology among major economies of the world, as well as between advanced and developing economies in terms of a model for social and economic development.

An emerging ecosystem within such a framework provides common ground among nations to articulate the goals and objectives for economic recovery that could benefit their stakeholders. The international capital market that facilitates vast amounts of private and public capital could play a catalytic role in building a value consensus on policy and standards for financing energy sustainability alongside Industry 4.0 on a global scale. Through an integrated capital market that enables transparent financial and non-financial disclosures on sustainable development targets, it would facilitate nurturing champion cases of environmentally and socially responsible firms for scalable economic growth under a new era of sustainable industrial development.

Market-based green financing for the developing economies

From the perspective of climate policy, one can no longer underestimate the growing significance of market-based green financing institutions for both advanced nations and developing economies. The deployment of such green financial instruments is clearly on the rise. As compiled in , there are now five main clusters of developing economies or regions which have issued green bonds and most of them contain at least a stock-exchange institution positioned to provide infrastructure for green bond exchange, except for the Arctic and the Middle East regions. Leveraging the emerging global green financing system, there will be potentially more public-private collaboration that is corroborated by the surging interest in ESG equity investing among stakeholders. The significance of institutional innovation for the emergence of a global green financing system, comprising green debt and ESG equities, is seen as increasingly relevant among the regulated firms under such a system (DiMaggio and Powell Citation1983; North Citation1991; Ng Citation2018).

Table 5. Green financing institutions for developing economies or regions.

Foreseeable opportunities and challenges in transformation

The improving economics in the overall costs of adoption of clean energy technologies provide an opportunity to attract more private funding to support the movement to replace fossil fuels with renewable energy. By enabling viable investment returns and attractive economic incentives for private business investors, institutional investors that control vast amounts of money in private equity and pension funds are now attracted to these investment opportunities with relatively lower risk than the unclean options. For instance, BlackRock – the world’s largest financial institution in terms of asset management – has declared that it is “committed to making sustainability a key component of the way BlackRock manages risk, constructs portfolios, designs products, and engages with companies” (BlackRock Citation2020). Recognizing the concerns over climate change in societies and from clients, Larry Fink, the firm’s chairman and CEO, recently noted that “we know that climate risk is investment risk, but we also believe the climate transition presents a historic investment opportunity” (Fink Citation2021).

The quintessential challenge to this transformational adaptation is to create sustainable improvements for quality of life without undermining the basis for investments. First, there should be scientific oversight to ensure that the circular economy is effectually engaged by the investment community seeking sustainable investment opportunities (Dewick et al. Citation2020). Second, achieving the twin goals of meeting greenhouse gas-reduction targets for climate change and the provision of universal energy access – affordable and accessible to a very large proportion of the global population inclusive of the developing economies – will require massive investment. This could be facilitated by the emerging system of green finance and active participation of private investors incentivized by the improved economics of investing in large-scale renewable energy projects and other related opportunities.

Ensuring that cross-border investment on such a scale and in light of rapid expansion of emerging knowledge and advancement of renewable energy technologies also requires a unique emphasis on matching innovative business solutions with an in-depth understanding of the local context that can be facilitated in a systematic manner through regional green financing hubs (Fagerberg Citation2018). In order to enable timely adoption of new technologies among the developing nations, there is a need to build up the absorptive capacity of human capital through collaborative efforts in training and development as well as in the context of technology transfer (Cohen and Levinthal Citation1990; Denicolai, Ramirez, and Tidd Citation2016; Schweisfurth and Raasch Citation2018).

While a market-based sustainable financial system has been gradually embraced by the international capital market and pertinent financial institutions with growing interest in ESG investing, effective implementation around the world necessitates collaboration through respective national development planning aligned with these global development goals (Chimhowu, Hulme, and Munro Citation2019; Liang and Liu Citation2020). Institutional innovation for sustainability depends on a complementary partnership between state planning and market-based mechanisms (Ng Citation2018; Fu and Ng Citation2020). Public-private partnerships on a global scale could unlock the full potential of resources and capital to the emerging sustainable financial system and thereby into strategic assets for sustainability.

The international capital market today appears to be continuing to pursue short-term returns through various hedge-fund operations despite the pandemic crisis. Such a misalignment between the needs for augmented investments into health and energy sustainability and myopic profit-seeking is likely to remain unless there are determined policy and regulatory measures as well as corporate governance dedicated to sustainability. Nonetheless, the unprecedented economic disruption caused by the recent pandemic suggests intrinsic linkage between sustainability risk and revitalization of the economy. The reactive movement of financial markets to news about progress in research and development for COVID-19 vaccines reveals that the world’s financiers have become more sensitive than ever to potential solutions to the economic recovery that hinge on viable solutions to human health and sustainability. A transparent and reliable green financial system would facilitate effective flow of information through public disclosures on sustainability performance.

Conclusion

We have argued that there is an underlying opportunity for humanity to tackle the economic turmoil instigated by the pandemic and to invest in progress toward the SDGs that can be supported by the emerging green finance hubs situated in various developing economies and regions as the economic driver of this emerging ecosystem for transformational adaptation (Loginova and Batterbury Citation2019; Waddock Citation2020). Based on an interdisciplinary literature review, this article has sought to advance three objectives. First, it outlines prospects for the emergence of a green financing system to integrate with international capital markets to set priorities for climate financing for the SDGs while fostering energy sustainability in concert with the ongoing development of Industry 4.0 on a global scale. Second, we have articulated the imperative of embracing the developing economies under a green recovery framework. Third, the foregoing discussion has pointed out that recent advances in the cost effectiveness of clean energy technologies encourages financial decisions for the replacement of fossil fuels. Finally, we describe how the clustering of green financing institutions as distributed hubs can be utilized for redirecting investments into sustainable infrastructures to mitigate climate change as advocated in the Paris Agreement.

With respect to future studies, it is crucial to examine the following three main challenges as extensions of this review. First, there should be careful evaluation on the efficacy of allocating funds raised from these green financing hubs into “green” projects aiming to reduce greenhouse-gas emissions from both developed and developing economies in order to meet the SDGs. For instance, we encourage further study of the effectiveness of funding in reducing pollution and improving air quality in order to avoid “greenwashing.”

Second, with the emergence of regional green financing hubs and related institutions under the influence of NGFS, there is likely to be heterogeneity in performance and efficacy among these regulatory institutions owing to their respective policy measures and compliance requirements (DiMaggio and Powell Citation1983; North Citation1991; Ng and Leung Citation2020). Development of a global standard for sustainability reporting by corporations seems increasingly inevitable as demanded by stakeholders of the financial services sector (IFRS Citation2020).

Finally, timely technology transfer of clean energy technologies from advanced to developing economies and regions is crucial for deployment on a global scale. Such initiatives could be facilitated by complementary policy for international collaboration and capacity building to leverage the emerging practices associated with Industry 4.0 while preparing for the arrival of Industry 5.0 instigated by a consensus for global sustainability (Ciborowski and Skrodzka Citation2020; EC Citation2021).

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1 For instance, access to improved energy services is considered critical for alleviating poverty, inducing economic growth, and enhancing gender equity in the utilization of resources in Africa (Uhunamure, Nethengwe, and Tinarwo Citation2019). The ongoing rural installation of renewable energy facilities has been fostered by governments in Africa as part of an effort to provide reliable and affordable electricity to local residents and businesses (IEA Citation2019).

2 The importance of energy access has been recognized by several organizations including the United Nation’s Sustainable Energy 4 ALL (SE4ALL) program, the World Energy Council, the World Bank, numerous nongovernmental organizations, and many charitable foundations. It is also comprehensively documented in the Global Energy Assessment (GEA Citation2012). Although progress at the global level has been tangible, it has been slow and insufficient in scale and scope to address basic human needs of a large portion of humanity. Massive diffusion of new technologies that can provide energy services at much lower cost is a necessary building block to help make a difference in the lives of many who have little.

3 The World Bank’s Access Investment Model provides detailed bottom-up estimates of the cost of reaching universal access in countries with large electricity-access deficits. These countries reflect differences in population and geography as well as local unit costs, and they can be used to provide a global estimate of access investment needs (IEA/World Bank Citation2017; IEA Citation2011).

4 Asian nations such as China, Japan, and South Korea should be able to improve their energy security when adopting more locally installed renewable energy for their domestic economic development and to reduce reliance on foreign imports (Choi Citation2009).

5 As of 2020, NGFS has over 70 members from various countries around the world and represents financial regulatory institutions that have oversight over three quarters of the global systemically important banks and two thirds of highly significant international insurers (NGFS Citation2020).

6 For instance, Bloomberg (Citation2020), a global financial intelligence provider, has started offering a range of ESG analytics, indices, research, and news that its customers and others can use to evaluate assets and report on sustainability performance. It provides analytics to support decision making on ESG investing, portfolio optimization, impact investing, and corporate strategic risk management. Bloomberg (Citation2020) compiles ESG data on companies around the world that are active in the sustainable debt and equity markets through a database of green bonds, green loans, social bonds, and sustainability bonds. For examining ESG-related risks and opportunities, a company’s historical ESG performance is based on independently assessed third-party ESG scores. This collection of data is considered increasingly relevant for investors to perform in-depth analyses of performance by assessing carbon emissions and exposure to the SDGs as well as forecasting and monitoring the impact of natural disasters – including storm, wildfire, and other extreme weather incidents – that can undermine the value of company assets.

7 Certain discrepancies exist between China’s green bond guidelines and the international standards advanced by the Climate Bonds Initiative in terms of eligibility of green projects and disclosures. The international framework focuses more on climate-change mitigation and adaptation while China’s procedures tend to emphasize environmental issues such as “greenhouse gases and pollution reduction, resource conservation as well as ecological protection” (CBI Citation2020b). Under such a practice, the domestic guidelines in China allow the use of proceeds from green bond issuances for general corporate operating expenses. According to the report by CBI (Citation2020b), about 57% of the green bonds issued in China comply with both Chinese and international standards, while the remaining share is aligned only with domestic standards.

8 Annual investment in low-carbon energy has increased rapidly and now annually exceeds US$600 billion according to a 2019 report from the IEA. See pp. 31 at https://www.iea.org/wei2019.

9 E.ON successfully raised €1.5 billion in green bonds in 2019 (https://www.eon.com/en/about-us/media/press-release/2019/2019-08-21-eon-successfully-raises-green-bonds.html). In addition, Ficolo issued €20 million in green bonds for its Helsinki data-center expansion (https://data-economy.com/ficolo-issues-e20m-green-bond-for-its-helsinki-data-centre-expansion/).

References

- Adams, C. 2020. “Sustainable Development Goal Disclosure (SDGD) Recommendations: Feedback on the Consultation Responses, ACCA, IIRC and WBA.” https://www.dur.ac.uk/research/directory/staff/?mode=pdetail&pdetail=128343

- Acharya, R., and A. Porwal. 2020. “A Vulnerability Index for the Management of and Response to the COVID-19 Epidemic in India: An Ecological Study.” The Lancet Global Health 8 (9): e1142–1151. doi:10.1016/S2214-109X(20)30300-4.

- American Geophysical Union (AGU). 2020. “COVID-19 Lockdowns Significantly Impacting Global Air Quality.” ScienceDaily, May 11. https://www.sciencedaily.com/releases/2020/05/200511124444.htm.

- Ashford, N., and R. Hall. 2019. Technology, Globalization, and Sustainable Development: Transforming the Industrial State. London: Routledge.

- Azhgaliyeva, A., and B. Liddle. 2020. “Introduction to the Special Issue: Scaling up Green Finance in Asia.” Journal of Sustainable Finance & Investment 10 (2): 83–91. doi:10.1080/20430795.2020.1736491.

- BlackRock. 2020. Our 2020 Sustainability Actions. New York: BlackRock. https://www.blackrock.com/hk/en/about-us/our-2020-sustainability-actions.

- Bloomberg. 2020. Bloomberg for Sustainable Finance Analysis. New York: Bloomberg. https://www.bloomberg.com/professional/solution/sustainable-finance/.

- Bonilla, S., H. Silva, M. Terra da Silva, R. Franco Gonçalves, and J. Sacomano. 2018. “Industry 4.0 and Sustainability Implications: A Scenario-Based Analysis of the Impacts and Challenges.” Sustainability 10 (10): 3740. doi:10.3390/su10103740.

- Bozeman, B. 2000. “Technology Transfer and Public Policy: A Review of Research and Theory.” Research Policy 29 (4–5): 627–655. doi:10.1016/S0048-7333(99)00093-1.

- Charnock, R., and I. Thomson. 2019. “A Pressing Need to Engage with the Intergovernmental Panel on Climate Change: The Role of SEA Scholars in Syntheses of Social Science Climate Research.” Social and Environmental Accountability Journal 39 (3): 192–199. doi:10.1080/0969160X.2019.1677258.

- Chimhowu, A., D. Hulme, and L. Munro. 2019. “The ‘New’ National Development Planning and Global Development Goals: Processes and Partnerships.” World Development 120: 76–89. doi:10.1016/j.worlddev.2019.03.013.

- Choi, H. 2009. “Fueling Crisis or Cooperation? The Geopolitics of Energy Security in Northeast Asia.” Asian Affairs: An American Review 36 (1): 3–27. doi:10.3200/AAFS.36.1.3-28.

- Ciborowski, R., and I. Skrodzka. 2020. “International Technology Transfer and Innovative Changes Adjustment in EU.” Empirical Economics 59 (3): 1351–1371. doi:10.1007/s00181-019-01683-8.

- Climate Bonds Initiative (CBI). 2021. Sustainable Debt: Global State of the Market 2020. London: CBI. https://www.climatebonds.net/files/reports/cbi_sd_sotm_2020_04d.pdf.

- Climate Bonds Initiative (CBI). 2020a. Climate Bond Taxonomy. London: CBI. https://www.climatebonds.net/files/files/CBI-Taxonomy-Sep18.pdf.

- Climate Bonds Initiative (CBI). 2020b. China Green Bond Market 2019 Research Report. London: CBI. https://www.climatebonds.net/resources/reports/china-green-bond-market-2019-research-report.

- Climate Bonds Initiative (CBI). 2020c. Green Stock Exchange. London: CBI. https://www.climatebonds.net.

- Climate Bonds Initiative (CBI). 2020d. Green Bonds Global State of the Market 2019. London: CBI. https://www.climatebonds.net/resources/reports/green-bonds-global-state-market-2019.

- Cohen, W., and D. Levinthal. 1990. “Absorptive Capacity: A New Perspective on Learning and Innovation.” Administrative Science Quarterly 35 (1): 128–152. doi:10.2307/2393553.

- de Vries, B. 2019. “Inequality, SDG10 and the Financial System.” Global Sustainability 2 (e9): 1–2. doi:10.1017/sus.2019.6.

- Denicolai, S., M. Ramirez, and J. Tidd. 2016. “Overcoming the False Dichotomy between Internal R&D and External Knowledge Acquisition: Absorptive Capacity Dynamics over Time.” Technological Forecasting and Social Change 104: 57–65. doi:10.1016/j.techfore.2015.11.025.

- Dewick, P., K. Green, and M. Miozzo. 2004. “Technological Change, Industrial Structure and the Environment.” Futures 36 (3): 267–293. doi:10.1016/S0016-3287(03)00157-5.

- Dewick, P., K. Green, T. Fleetwood, and M. Miozzo. 2006. “Modelling Creative Destruction: Technological Diffusion and Industrial Structure Change to 2050.” Technological Forecasting and Social Change 73 (9): 1084–1106. doi:10.1016/j.techfore.2006.04.002.

- Dewick, P., M. Bengtsson, M. Cohen, J. Sarkis, and P. Schröder. 2020. “Circular Economy Finance: Clear Winner or Risky Proposition?” Journal of Industrial Ecology 24 (6): 1192–1200. doi:10.1111/jiec.13025.

- DiMaggio, P., and P. Powell. 1983. “The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields.” American Sociological Review 48 (2): 147–160. doi:10.2307/2095101.

- Di Marco, M., M. Baker, P. Daszak, P. De Barro, E. Eskew, C. Godde, T. Harwood, et al. 2020. “Opinion: Sustainable Development Must Account for Pandemic Risk.” Proceedings of the National Academy of Sciences of the United States of America 117 (8): 3888–3892. doi:10.1073/pnas.2001655117.

- Dikau, S., N. Robins, and M. Täger. 2019. “Building a Sustainable Financial System: The State of Practice and Future Priorities.” Revista de Estabilidad Financiera 37. https://www.bde.es/f/webbde/GAP/Secciones/Publicaciones/InformesBoletinesRevistas/RevistaEstabilidadFinanciera/19/noviembre/Building_sustainable_financial.pdf

- European Commission (EC). 2021. Industry 5.0: Towards a Sustainable, Human-Centric and Resilient European Industry. Brussels: European Commission. https://ec.europa.eu/info/publications/industry-50_en.

- European Union Technical Expert Group (EUTEG). 2020. Statement of the EU Technical Expert Group on Sustainable Finance. Brussels: EUTEC. https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/200426-sustainable-finance-teg-statement-recovery_en.pdf.

- Fagerberg, J. 2018. “Mobilizing Innovation for Sustainability Transitions: A Comment on Transformative Innovation Policy.” Research Policy 47 (9): 1568–1576. doi:10.1016/j.respol.2018.08.012.

- Farmbrough, H. 2020. “Why the Coronavirus Pandemic Is Creating a Surge in Renewable Energy?” Forbes, May 5. https://www.forbes.com/sites/heatherfarmbrough/2020/05/05/why-the-coronavirus-pandemic-is-creating-a-surge-in-renewable-energy/#44c10d9534b4

- Fink, L. 2021. “Larry Fink’s 2021 Letter to CEOs.” New York: BlackRock. https://www.blackrock.com/corporate/investor-relations/larry-fink-ceo-letter

- Fitch Ratings 2020. “ESG in Credit.” https://your.fitch.group/rs/732-CKH-767/images/Fitch%20Ratings%20-%20ESG%20In%20Credit%202020.pdf.

- Fu, J., and A. Ng, eds. 2020. Sustainable Energy and Green Finance for a Low-Carbon Economy: Perspectives from the Greater Bay Area of China. Cham: Springer.

- Freeman, C., and C. Perez. 1998. “Structural Crises of Adjustment, Business Cycles and Investment Behaviour.” In Technical Change and Economic Theory, edited by G. Dosi, C. Freeman, R. Nelson, G. Silverberg, and L. Soete, 38–66. London: Pinter.

- Freeman, C., and F. Louca. 2001. As Time Goes by: From the Industrial Revolutions to the Information Revolution. Oxford: Oxford University Press.

- Foxon, T. 2018. Energy and Economic Growth: Why We Need a New Pathway to Prosperity. London: Routledge.

- Gates, B. 2020. “Responding to COVID-19 – A Once-in-a-Century Pandemic?” The New England Journal of Medicine 382 (18): 1677–1679. doi:10.1056/NEJMp2003762.

- Ghobakhloo, M. 2020. “Industry 4.0, Digitization, and Opportunities for Sustainability.” Journal of Cleaner Production 252: 119869. doi:10.1016/j.jclepro.2019.119869.

- Global Energy Assessment (GEA). 2012. Global Energy Assessment: Toward a Sustainable Future. Laxenburg: International Institute for Applied Systems Analysis and Cambridge: Cambridge University Press.

- International Capital Market Association (ICMA). 2016. Green Bond Principles 2016: Voluntary Process Guidelines for Issuing Green Bonds. Zurich: ICMA. http://www.icmagroup.org/Regulatory-Policy-and-Market-Practice/green-bonds/green-bond-principles.

- International Energy Agency (IEA). 2011. “Energy Access for All, Financing Access for the Poor.” World Energy Outlook. Paris: IEA. https://iea.blob.core.windows.net/assets/cc401107-a401-40cb-b6ce-c9832bb88d85/WorldEnergyOutlook2011.pdf

- International Energy Agency/World Bank. 2017. Global Tracking Framework 2017: Progress towards Sustainable Energy. Paris: IEA. https://trackingsdg7.esmap.org/data/files/download-documents/eegp17-01_gtf_full_report_for_web_0516.pdf.

- International Energy Agency (IEA). 2019. Africa Energy Outlook 2019. Paris: IEA. https://africacheck.org/wp-content/uploads/2019/12/Africa_Energy_Outlook_2019.pdf.

- International Energy Agency (IEA). 2020. Global Energy Review 2020. Paris: IEA. https://www.iea.org/reports/global-energy-review-2020.

- International Financial Reporting Standards (IFRS). 2020. Consultation Paper on Sustainability Reporting. London: IFRS. https://www.ifrs.org/news-and-events/2020/09/ifrs-foundation-trustees-consult-on-global-approach-to-sustainability-reporting/.

- International Institute for Sustainable Development (IISD). 2020a. Three Ways the Coronavirus is Shaping Sustainable Development. Winnipeg: IISD. https://www.iisd.org/library/coronavirus-shaping-sustainable-development.

- International Institute for Sustainable Development (IISD). 2020b. Could the COVID-19 Pandemic Give the 2020 Environmental Agenda a Much-Needed Boost? Winnipeg: IISD. https://www.iisd.org/blog/covid-19-environmental-agenda.

- International Monetary Fund (IMF). 2020. World Economic Outlook: The Great Lockdown. Washington, DC: IMF. https://www.imf.org/en/Publications/WEO/Issues/2020/04/14/weo-april-2020/.

- International Renewable Energy Agency (IRENA). 2020. Renewable Power Generation Costs in 2019. Abu Dhabi: IRENA. https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2020/Jun/IRENA_Power_Generation_Costs_2019.pdf.

- Javaid, M., A. Haleem, R. Vaishya, S. Bahl, R. Suman, and A. Vaish. 2020. “Industry 4.0 Technologies and Their Applications in Fighting COVID-19 Pandemic.” Diabetes & Metabolic Syndrome 14 (4): 419–422. doi:10.1016/j.dsx.2020.04.032.

- Kinney, P. 2018. “Interactions of Climate Change, Air Pollution, and Human Health.” Current Environmental Health Reports 5 (1): 179–186. doi:10.1007/s40572-018-0188-x.

- Kucik, J., and J. Leister. 2020. “The Pandemic is Exposing the Vulnerabilities of the U.S. Service Economy.” The Washington Post, April 22. https://www.washingtonpost.com/politics/2020/04/22/pandemic-is-exposing-vulnerabilities-us-service-economy/

- Kumar, R., and A. Kumar. 2020. “Adoption of Electric Vehicles: A Literature Review and Prospects for Sustainability.” Journal of Cleaner Production 253: 119911. doi:10.1016/j.jclepro.2019.119911.

- Leach, M., B. Reyers, X. Bai, E. Brondizio, C. Cook, S. Díaz, G. Espindola, M. Scobie, M. Stafford-Smith, and S. Subramanian. 2018. “Equity and Sustainability in the Anthropocene: A Social-Ecological Systems Perspective on Their Intertwined Futures.” Global Sustainability 1 (e13): 1–13. doi:10.1017/sus.2018.12.

- Leal Filho, W., G. Nagy, and D. Ayal. 2020. “Viewpoint: Climate Change, Health and Pandemics – A Wake-up Call from COVID-19.” International Journal of Climate Change Strategies and Management 12 (4): 533–535. doi:10.1108/IJCCSM-08-2020-212.

- Leal Filho, W., S. Scheday, J. Boenecke, A. Gogoi, A. Maharaj, and S. Korovou. 2019. “Climate Change, Health and Mosquito-Borne Diseases: Trends and Implications to the Pacific Region.” International Journal of Environmental Research and Public Health 16 (24): 5114. doi:10.3390/ijerph16245114.

- Loginova, J., and S. Batterbury. 2019. “Incremental, Transitional and Transformational Adaptation to Climate Change in Resource Extraction Regions.” Global Sustainability 2 (e17): 1–12. doi:10.1017/sus.2019.14.

- Liang, C., and B. Liu. 2020. “Challenge or Opportunity of Climate Financial Fragmentation: Evidence from China-Initiated Cooperation with Emerging Multilateral Institutions.” International Journal of Climate Change Strategies and Management 12 (3): 289–303. doi:10.1108/IJCCSM-07-2019-0048.

- Lom, M., O. Pribyl, and M. Svitek. 2016. “Industry 4.0 as a Part of Smart Cities.” 2016 Smart Cities Symposium Prague, Prague, May 26–27. doi:10.1109/SCSP.2016.7501015.

- Lopes de Sousa Jabbour, A., C. Jabbour, M. Godinho Filho, and D. Roubaud. 2018. “Industry 4.0 and the Circular Economy: A Proposed Research Agenda and Original Roadmap for Sustainable Operations.” Annals of Operations Research 270 (1–2): 273–286. doi:10.1007/s10479-018-2772-8.

- Nathwani, J., and D. Kammen. 2019. “Affordable Energy for Humanity: A Global Movement to Support Universal Clean Energy Access.” Proceedings of the IEEE 107 (9): 1780–1789. doi:10.1109/JPROC.2019.2918758.

- Network for Greening the Financial System (NGFS). 2020. Overview of Environmental Risk Analysis by Financial Institutions. Paris: NGFS. https://www.ngfs.net/en/liste-chronologique/ngfs-publications.

- Ng, A. 2018. “From Sustainability Accounting to a Green Financing System: Institutional Legitimacy and Market Heterogeneity in a Global Financial Centre.” Journal of Cleaner Production 195: 585–592. doi:10.1016/j.jclepro.2018.05.250.

- Ng, A., and J. Nathwani. 2010. “Sustainable Energy Policy for Asia: Mitigating Systemic Hurdles in a Highly Dense City.” Renewable and Sustainable Energy Reviews 14 (3): 1118–1123. doi:10.1016/j.rser.2009.11.002.

- Ng, A., and J. Nathwani. 2018. “Sustainable Energy Infrastructure for Asia: Policy Framework for Responsible Financing and Investment.” In Routledge Handbook of Energy in Asia, edited by S. Bhattacharyya, 284–295. London: Routledge.

- Ng, A., and T. Leung. 2020. “Relevance of SEA to a Global Financial Centre under One Country Two Systems: Engaging Stakeholders for Sustainability and Climate Change.” Social and Environmental Accountability Journal 40 (2): 140–148. doi:10.1080/0969160X.2020.1776625.

- North, D. 1991. “Institutions.” Journal of Economic Perspectives 5 (1): 97–112. doi:10.1257/jep.5.1.97.

- Oláh, J., N. Aburumman, J. Popp, M. Khan, H. Haddad, and N. Kitukutha. 2020. “Impact of Industry 4.0 on Environmental Sustainability.” Sustainability 12 (11): 4674. doi:10.3390/su12114674.

- Ou, S., X. Hao, Z. Lin, H. Wang, J. Bouchard, X. He, S. Przesmitzki, et al. 2019. “Light-Duty Plug-in Electric Vehicles in China: An Overview on the Market and Its Comparisons to the United States.” Renewable and Sustainable Energy Reviews 112: 747–761. doi:10.1016/j.rser.2019.06.021.

- Pelling, M. 2011. Adaptation to Climate Change: From Resilience to Transformation. London: Routledge.

- Perez, C. 1983. “Structural Change and the Assimilation of New Technologies in the Economic and Social System.” Futures 15 (5): 357–375. doi:10.1016/0016-3287(83)90050-2.

- Ribeiro, I., F. Matos, C. Jacinto, H. Salman, G. Cardeal, H. Carvalho, R. Godina, and P. Peças. 2020. “Framework for Life Cycle Sustainability Assessment of Additive Manufacturing.” Sustainability 2 (3): 929. doi:10.3390/su12030929.

- Sarkis, J., M. Cohen, P. Dewick, and P. Schroder. 2020. “A Brave New World: Lessons from the COVID-19 Pandemic for Transitioning to Sustainable Supply and Production.” Resources, Conservation, and Recycling 159: 104894. doi:10.1016/j.resconrec.2020.104894.

- Schweisfurth, T., and C. Raasch. 2018. “Absorptive Capacity for Need Knowledge: Antecedents and Effects for Employee Innovativeness.” Research Policy 47 (4): 687–699. doi:10.1016/j.respol.2018.01.017.

- Singh, R., M. Javaid, A. Haleem, and R. Suman. 2020. “Internet of Things (IoT) Applications to Fight against COVID-19 Pandemic.” Diabetes & Metabolic Syndrome 14 (4): 521–524. doi:10.1016/j.dsx.2020.04.041.

- Task Force on Climate-related Financial Disclosures (TCFD). 2020. Final Report: Recommendations of the Task Force on Climate-Related Financial Disclosures. New York: TCFD. https://www.fsb-tcfd.org/publications/final-recommendations-report/.

- Tseng, M., R. Tan, A. Chiu, C. Chien, and T. Kuo. 2018. “Circular Economy Meets Industry 4.0: Can Big Data Drive Industrial Symbiosis?” Resources, Conservation and Recycling 131: 146–147. doi:10.1016/j.resconrec.2017.12.028.

- Thompson, S. 1986. “Biotechnology – Shape of Things to Come or False Promise?” Futures 18 (4): 514–525. doi:10.1016/0016-3287(86)90076-5.

- Uhunamure, S., N. Nethengwe, and D. Tinarwo. 2019. “Correlating the Factors Influencing Household Decisions on Adoption and Utilisation of Biogas Technology in South Africa.” Renewable and Sustainable Energy Reviews 107: 264–273. doi:10.1016/j.rser.2019.03.006.

- United Nations Industrial Development Organization (UNIDO). 2020. Bridge for Cities 4.0: Connecting Cities through the New Industrial Revolution. Vienna: UNIDO. https://www.unido.org/unido-industry-40/.

- United Nations. 2020a. Sustainable Development Goals. New York: United Nations. https://www.un.org/sustainabledevelopment/goal-of-the-month/.

- United Nations. 2020b. Sustainable Development Goals. New York: United Nations. https://www.un.org/sustainabledevelopment/energy/.

- United Nations. 2020b. World Population Prospects 2019. New York: United Nations. https://population.un.org/wpp/Download/Standard/Population/.

- Waddock, S. 2020. “Achieving Sustainability Requires Systemic Business Transformation.” Global Sustainability 3 (e12): 1–12. doi:10.1017/sus.2020.9.

- World Bank. 2017. State of Electricity Access Report (SEAR). Washington, DC: World Bank. https://documents.worldbank.org/en/publication/documents-reports/documentdetail/364571494517675149/full-report.

- World Bank. 2020. Connecting for Inclusion: Broadband Access for All. Washington, DC: World Bank. https://www.worldbank.org/en/topic/digitaldevelopment/brief/connecting-for-inclusion-broadband-access-for-all/.

- Wu, Y., A. Ng, Z. Yu, J. Huang, K. Meng, and Z. Dong. 2021. “A Review of Evolutionary Policy Incentives for Sustainable Development of Electric Vehicles in China: Strategic Implications.” Energy Policy 148 (Part B): 111983. doi:10.1016/j.enpol.2020.111983.

- Wu, X., R. Nethery, B. Sabath, D. Braun, and F. Dominici. 2020. “Exposure to Air Pollution and COVID-19 Mortality in the United States: A Nationwide Cross-Sectional Study.” Science Advances 6 (45):abd4049. doi:10.1101/2020.04.05.20054502/.

- Yuen, P., and A. Ng. 2019. “Healthcare Financing and Sustainability.” In Good Health and Well-Being: Encyclopedia of the UN Sustainable Development Goals, edited by W. Leal Filho, T. Wall, A. Azul, L. Brandli, and P. Gökcin Özuyar. Cham, Switzerland: Springer.