Abstract

This paper presents an empirical investigation of the effectiveness of the institutional frameworks of monetary policy in achieving and maintaining price stability. The institutional frameworks considered are central bank independence (CBI), inflation targeting (IT), currency boards (CB) and monetary unions (MU). Against the vast literature that argues for the price stabilizing effects of each of these institutions, the empirical evidence presented here suggests that countries that have adopted the IT and CB regimes have, on average, been associated with lower inflation rates than others during the past decade. This finding is robust to various control variables, while governance appears to be a substitute to formal mechanisms.

Keywords:

Notes

1. See Lin and Rosenblatt (Citation2012).

2. See the Appendix for the list of countries and their monetary institutions.

3. See Neyapti (Citation2010) for a review of this literature.

4. See, for example, Posen (Citation1995) and Neyapti (Citation2003) for the case of CBI.

5. The data are compiled from the World Bank Development Indicators online.

6. An alternative could be to use the logs (or even the levels) of inflation, which does not alter the results reported below.

7. The criteria list in Cukierman et al. (Citation1992) covers, in broad terms, the objective, chief executive officer, lending and policy formulation of the central bank. Grilli et al. (Citation1991) distinguish between the economic and political aspects of CBI.

8. See http://www.imf.org/external/np/mfd/er/2008/eng/0408.html, where it is stated that ‘a monetary regime based on an explicit legislative commitment to exchange domestic currency for a specified foreign currency at a fixed exchange rate, combined with restrictions on the issuing authority to ensure the fulfillment of its legal obligation’.

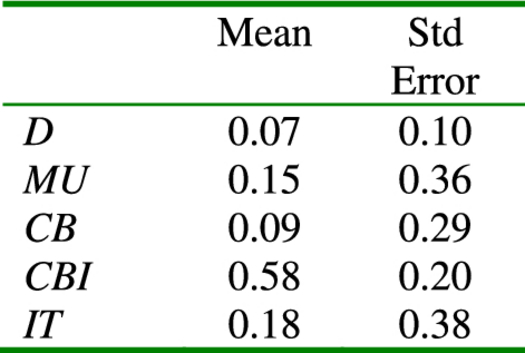

9. The descriptive statistics of D and the monetary institutions subject to this study are as follows:

10. DC takes the value of 1 for countries that IMF classifies as the advanced economies. Source: World Economic Outlook, Sept. 2011.

11. Posen (Citation1995), for example, asserts that it is not CBI but financial opposition to inflation (foi) that explains low inflation. Likewise, Berdiev at al. (2012) argue that the choice of exchange rate regime is endogenous to political and institutional factors.

12. We do not use a dummy for transition economies since countries that were in transition in the 1990s are included in the list of developing countries in the 2000s.

13. Column IIIa reports results with a zero constraint for the CBI values that are lower than 0.6. A similar reporting can be found in Cukierman et al. (2002) for liberalization index (CLI).

14. Angola, Belarus, Congo and Zimbabwe all had more than 100% inflation at least in one year during the 2000s. Zimbabwe remains to be the only one with a high inflation rate as of 2006.

15. The first of these accounts for the fact that CB is mostly effective for small countries and effective implementation of the IT regime requires CBI.

16. Governance indices are provided by Kaufman et al. (2008), based on surveys that report six different measures of the quality of political stability; control of corruption; rule of law; voice and accountability; government effectiveness; and regulatory quality.

17. Small country and developed country dummies are dropped to focus on the effects of structural variables. When included, their coefficients are observed to be insignificant.

18. In Canada, Japan and United Kingdom, for example, CBI is 0.63, 0.44 and 0.69, respectively; whereas the level of gov, representing informal institutional quality is all above 0.8.

19. Data are based on Leaven and Valencia (Citation2008).

20. The coefficient of variation is measured as standard deviation divided by the sample mean, which is a measure of variation that is comparable across.

21. These regressions are available from the author upon request.