Abstract

This paper compares and analyzes the relations between the biogas development and the national policy frameworks for biogas solutions in eight European countries. The policy frameworks are compared using a biogas policy model, comprising five dimensions: type of policy; administrative area; administrative level; targeted part of the value chain; and continuity and change over time. The studied countries show examples of both increasing and stagnating biogas production, all of which can be associated with changes in national policy frameworks. Many different policy tools—particularly economic instruments—have proven successful for stimulating biogas production, but changing a well-functioning framework risks impeding the development. Therefore, predictability and relevance for targeted actors are key in policymaking. Targeting specific parts of the value chain can however be required to integrate all the benefits of biogas solutions, such as agricultural methane emissions reduction. Moreover, it can be challenging to design policies and policy instruments that are both effective and sustainable over time, without needs for modifications or adjustments. Finally, biogas policies and policy instruments that are effective in one country would not necessarily lead to the same outcome in another country, as they are dependent on the broader context and policy and economic framework.

Introduction

Systems for production and use of biogas, biomethane and digestate—often denoted biogas solutions (see, e.g. [Citation1–4])—have the potential to address many societal challenges, including renewable energy production, waste management and nutrient recycling [Citation5]. Consequently, biogas solutions can contribute to many of the UN sustainable development goals (see, e.g. [Citation5–7]). Over the last decades, the interest for biogas has grown rapidly in many countries [Citation8]. Motivated by concerns over climate change, unemployment, rural development and energy import dependence, biogas and other biofuels have been increasingly promoted all over Europe (see, e.g. [Citation9, Citation10]). The number of biogas initiatives has increased and diversified. Previously, biogas solutions were mainly connected to waste and wastewater management [Citation8], but have now become parts of the developments of renewable electricity and heat (see, e.g. [Citation11, Citation12]), renewable vehicle fuels (see, e.g. [Citation13, Citation14]) and sustainable agriculture (see, e.g. [Citation15, Citation16]).

In EU-28, the biogas production doubled from 93 to 187 TWh between 2008 and 2016 [Citation17, Citation18]. Kampman et al. [Citation19] estimated another doubling to be possible until 2030, but even larger increases may be possible in many individual member states. Realizing the estimated potentials will, however, require the combined efforts of many different actors, who need to work for strengthening the drivers and removing the barriers for increased production and use of biogas. In fact, the biogas production in the EU-28 only increased by 3% from 2016 to 2019 [Citation20]. In connection with renewable fuels, several studies have emphasized policy coherence (see, e.g. [Citation21, Citation22]), stability and continuity (see, e.g. [Citation19, Citation23, Citation24]) as central factors for policies to be effective in areas that require large investments over a long time period.

The development of biogas solutions in different European countries have largely been driven by initiatives and regulations at national and regional levels. This has resulted in a great variety of outcomes in terms of both production and consumption of biogas. In several large countries such as Germany, Italy and France, the biogas development has been dominated by the agricultural sector and biogas is primarily used for electricity and heat production, while in countries like Sweden, Switzerland and Finland, most of the production is based on municipal waste streams such as sewage and organic waste [Citation8]. Transport is dominating the use of biogas in Sweden [Citation25], and this area of application is gaining increasing attention in several other countries [Citation8].

Until recently, biogas solutions have not been given much independent attention in EU policies and strategies. Biogas solutions are only very briefly mentioned in the Waste Directive [Citation26, Citation27] and the EU Bioeconomy Strategy [Citation28]. They are indirectly affected by particularly the Renewable Energy Directive [Citation29, Citation30] and the Landfill Directive [Citation31], and investment in biogas plants have been supported within the Common Agricultural Policy and the underlying fund for rural development [Citation32, Citation33], but there have not been any major initiatives directed towards biogas development, nor any observable development toward a common biogas policy. This has, however, begun to change. In three new strategies developed under the European Green Deal in 2020, biogas solutions play a central role. In the EU Methane Strategy [Citation34], the development of efficient biogas solutions are viewed as important for decreasing the methane emissions from agriculture, waste and energy sectors. The Energy System Integration Strategy [Citation35] pronounces the mobilization of waste resources for energy production and substitution of fossil gas by renewable gases. Together with the ‘From Farm to Fork’-strategy [Citation36] it also encourages the development of circular energy communities in connection with agriculture. These strategies are being followed up by more concrete policies, which will provide new frameworks for biogas in Europe and importantly stimulate the development of biogas systems. For example, in December 2021, the European commission presented the proposal of an EU framework to decarbonize gas markets, which sets rules that will facilitate biomethane integration in the gas networks all over Europe together with a legislative proposal to reduce methane emissions in the energy sector [Citation37].

The fact that biogas solutions can provide multiple benefits within several sectors and contribute to solving many of the current sustainability challenges can be regarded as an advantage, but the many functions and externalities also make biogas solutions complex to evaluate. Nevzorova and Kutcherov [Citation38] argued that the development of biogas as an energy resource is impeded by technical, economic, market, institutional, socio-cultural as well as environmental factors. Moreover, the fact that the policies influencing biogas solutions are found in numerous policy areas and that every country has developed its own policy framework have resulted in a very complex ‘policy landscape’, which is difficult to overview and evaluate [Citation39]. This also make policy coherence, stability and continuity extra challenging, which may impede the growth of biogas solutions.

Several efforts have been made to describe the biogas development and the biogas policy landscape in European countries, including reports within the projects Biogas Action [Citation40], BIOSURF [Citation41], Record Biomap [Citation42], SYSTEMIC [Citation23], REGATRACE [Citation43] and GreenGasGrids [Citation44]. While the observations of these reports differ in some respects, they all bear witness of the diversity of biogas developments between different countries as well as of the width and the complexity of policies influencing biogas. There has however been a lack of common understanding of the dimensions of biogas policies and how they influence the production and use of biogas.

As a response to this challenge, we have presented a model [Citation39] for describing the different dimensions of policies influencing biogas solutions in the EU, and how they can be categorized, in a generic way. This model was developed in response to the challenge of defining the relationship between biogas policies and biogas development. It is unique in its way of describing the multidimensional characteristics of biogas policies. In this article, we use this model to compare the biogas developments in eight European countries, and particularly to analyze the relations between the national biogas policy frameworks and the biogas production development. The fact that all countries included in the comparison abide by the same international (EU) framework allows us to focus the analysis on the national level. Thus, this study aims to investigate how policies and policy instruments have influenced the development of biogas solutions in Europe, while also demonstrating how the new policy model can be used in a comparative analysis.

Methods

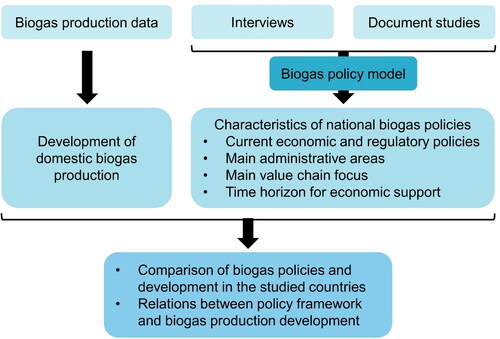

The analysis comprised a quantitative comparison of domestic biogas production and development in recent years, as well as a qualitative comparison of national biogas policies and policy development (). Information on national biogas policies was collected through policy documents and interviews with representatives for the biogas sector in the studied countries. Their biogas policies and development were analyzed using the model by Gustafsson and Anderberg [Citation39]. Together with data on domestic biogas production, this was then used to compare the development in the studied countries, and to analyze the relations between policy framework and biogas production development.

Figure 1. Description of methods and outputs of the study.

Selection of countries

The selection of countries for this analysis was based upon the information obtained from overviews and from our earlier studies [Citation39, Citation45]. The selection was done with the ambition to include as much diversity as possible in the study. Variation was particularly sought concerning production and feedstock used, areas of use, recent development of biogas production, and degree of market maturity. All the selected countries were, however, required to have an established production of biogas and some recent development in biogas policies. They were also required to be implementing EU regulations and directives. The number of countries was limited to eight for practical reasons and avoid too much overlap and similarities. provides an overview of the selected countries including motivations for their inclusion in the study.

Table 1. List of studied countries and motivation for selection.

Data collection

Quantitative data on biogas production in the studied countries was collected from the official statistics database of the European Commission, Eurostat, using 2019 as reference year. Newer data was made available during the process, but was not included in the analysis as it was marked ‘provisional’ in the Eurostat database. Older data from the same source was used in analysis of development over periods of 5, 10 and 20 years.

Interviews and document studies

Interviews were conducted with representatives for national biogas associations, one from each of the studies countries. The interviews were done in a semi-structured way, following a fixed set of questions with additional follow-up questions when needed. All interviews were done either via recorded video meetings or, if the respondents were not available for video call, in written form. The interview transcripts and written answers were then analyzed, and complementary follow-up questions were asked if needed. The interviewees were offered anonymity in connection with publication. When citing interview responses that were given in another language than English, these quotes have been translated by the authors. The interview form is found in Appendix.

The interviews were with help from the interviewees and their respective organizations complemented by inventories of policy documents from the studied countries, as well as data on domestic production and use of biogas. The interviewees were also consulted for interpretation and, in some cases, translation of policy documents. Documents analyzed in the study included national biogas and energy plans and legal texts on support for biogas as well as technical reports on domestic biogas development and policy. The EU database on renewable energy policies, RES LEGAL Europe [Citation46], was also used as a source of information on national policies and support schemes.

Analysis

The policy situation and biogas development in the studied countries were analyzed using the model proposed by Gustafsson and Anderberg [Citation39]. The model divides biogas policies into five dimensions: type of policy; administrative area; administrative level; targeted part of the value chain; and temporal change and continuity. The types of policies are further categorized according to two dimensions: regulatory, economic or voluntary, and encouraging or enforcing. Administrative areas could include energy, environment, waste, water, agriculture, transport, economy and construction. Administrative level refers to whether the policies exist on a local/regional, national, EU or global level. Targeted part of the value chain describes how the policies interact with the biogas system, and whether they are directed to production, distribution or use of biogas, biomethane or biofertilizer. Finally, temporal change and continuity describes how stable or predictable the policies are over time. A more detailed presentation of the model and its dimensions is given in the article by Gustafsson and Anderberg [Citation39]. shows an example of how the policy landscape for biogas can be illustrated using this model.

Figure 2. Comprehensive illustration of the dimensions in the implemented policy model. Based on the work of Gustafsson and Anderberg [Citation39].

![Figure 2. Comprehensive illustration of the dimensions in the implemented policy model. Based on the work of Gustafsson and Anderberg [Citation39].](/cms/asset/9009152a-0947-458b-b043-f999f430ec48/tbfu_a_2034380_f0002_c.jpg)

Results and analysis

Biogas production and development

There are large differences between the studied countries in terms of total production of biogas and the basic characteristics of their biogas sectors and their development (). Germany has a much larger total production than all the other countries; in fact, the biogas production in Germany is larger than in the other seven countries combined. Italy has the second largest production, approximately 1/5 of the German production. However, related to the population size, the differences are less dramatic. The biogas production per capita of both Denmark and the Czech Republic is more than half of the German per capita production. Sweden, Norway and France have the lowest per capita production, less than 1/5 of that in Germany ().

Figure 3. Annual biogas production per capita in the studied countries. Calculated from [Citation20] and [Citation47].

![Figure 3. Annual biogas production per capita in the studied countries. Calculated from [Citation20] and [Citation47].](/cms/asset/a52b87b0-dd92-49ca-8c69-4123be90b985/tbfu_a_2034380_f0003_c.jpg)

Table 2. Comparison of biogas production and some fundamental conditions for biogas solutions in the studied countries.

There are also distinct differences between the different countries in terms of how biogas is produced and used (). In Denmark, France, Italy, the Czech Republic and Germany, biogas production is primarily taking place within the agricultural sector. In the two former countries, manure and crop residues are the dominating substrates, while in the latter, energy crops play an important role. In Sweden, Finland and Norway, biogas production is primarily connected to treatment of urban and industrial organic waste and sewage sludge, while only a very small part of the production is based on agricultural substrates. Sweden and Germany are both relatively well-developed when it comes to anaerobic treatment of wastewater, producing 70–90 kWh/capita of biogas from sewage sludge (calculated from [Citation20, Citation47]). Some development in biogas from wastewater treatment could be expected in Czech Republic, Finland, Norway and Denmark (currently producing 40–50 kWh/capita) and particularly in France and Italy (10 kWh/capita). In many of the studied countries, the use of biogas for producing electricity and heat has been prioritized, but in Sweden, Norway and Finland, an increasing share of the biogas produced has been upgraded for use in the transport sector. This is also viewed as an interesting future option in some other countries. Italy and Germany both have introduced a large number of compressed natural gas fueling stations [Citation48].

All countries except Norway, Sweden and Finland have nationwide gas grids. According to the interviewees, natural gas is regarded as a bridge for the biogas development rather than a competitor, partly because of the infrastructure but also as it can be used as a backup to ensure supply for biomethane customers:

“We see the natural gas as a bridge as it could be blended with biomethane and distributed through the NG [natural gas] pipelines.” [Citation49]

“[Natural gas] is indeed a ‘bridge for biogas’” [Citation50]

“It has been important/…/in that natural gas has been necessary as a backup for the supply.” [Citation51]

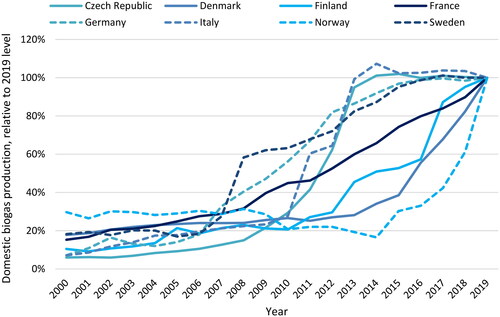

The biogas production in the studied countries show quite different development paths (). In Germany, Italy, Sweden, and the Czech Republic, there has been a rather slow development in recent years, following a dramatic expansion around ten years ago, while biogas production has recently increased rapidly in Norway, Denmark and Finland. France is the only country that has had a very stable continuous production growth, without either quick expansion or stagnation.

Figure 4. Development of domestic biogas production in the studied countries. The production level for each year is plotted relative to the 2019 level in the respective country.

Putting on a raster of national biogas policy development, there appears to be a clear connection between policy and biogas production. In Germany, Italy and the Czech Republic, periods of fast growth have been halted by changes in the respective support systems, making it less attractive to invest in biogas production. In the case of Germany, the European Biogas Association (EBA) criticized the 2014 amendments of the national Renewable Energy Act (Erneuerbare Energie-Gesetz, EEG), in which large-scale biogas plants were no longer eligible for new production support contracts [Citation53]. Further changes in the EEG made in 2017 have led to a net decrease in the number of biogas plants in Germany [Citation54].

Comparative analysis of policy frameworks

The comparison of the studied countries according to the five-dimensional policy model is summarized in and elaborated in the following sections. The summary in focuses on the national level and therefore it does not include the ‘administrative level’ dimension.

Table 3. Comparison of biogas policies in the studied countries, based on the model by Gustafsson and Anderberg [Citation39].

Administrative level

Even though policies that directly or indirectly concern biogas solutions are found at different administrative levels—from international treaties and goals to local investment decisions—the national level has so far been the dominating the policy arena for biogas development. The international climate politics have encouraged renewable fuels such as biogas. The biogas sector in all the studied countries is influenced by EU directives and regulations on renewable energy, climate change mitigation, waste management, wastewater treatment and environmental protection, and national regulations must be in line with EU legislation. This is to a dominating extent also the case for Norway, which is not a member of EU, but closely associated via the EEA Agreement and take full part in the Internal market of the EU [Citation55].

In the EU, several policy areas—particularly climate and environment, waste, and rural development—have been supportive to biogas solutions. For example, EU rural development funds have long been able to provide investment support for agriculturally based biogas plants [Citation32, Citation33]. Depending on which areas that are in focus and which tools that are used in different countries, some overarching EU regulations may also be of importance for national biogas policies. General EU ordinances on governmental subsidies or public procurement are fundamental, and EU energy and environmental regulations may support or interfere with national systems. As an example, EU’s efforts to avoid using crops for energy production, which during the recent decades has been integrated in all relevant EU policies, has in Germany (in 2016) led to abolition of support for energy crops and introduction of a maize cap for biogas plants which is decreased every year (2018: 50%; 2021: 44%) [Citation56].

However, the biogas development in the EU countries has so far largely been driven and regulated at the national level. Due to different preconditions in terms of energy systems and agricultural systems, infrastructure, motivations for biogas development and political traditions, there can be large differences in terms of laws, rules and support systems for biogas in different countries. Also in federal states such as Germany and Austria, where states have far-reaching competencies on, e.g. waste and water issues, the national level has dominated the regulation of biogas solutions, due to particular responsibilities in relation to energy, transport and regional development policies [Citation56, Citation57].

The national legislation and policy set the frames for local and regional policies. Within their level, regions can cooperate and influence each other’s actions, as well as receive support for various projects directly from EU programmes. The regional and local levels are central for implementation of policies from higher levels. No matter if biogas production is based on agricultural waste, sewage sludge or organic household waste, it is normally based on local resources. Local preconditions, and regional strategies and investments, have often led to large differences between different regions. In Sweden, regional and local policy networks—often with cities, public transport and waste companies as central actors—have been important for establishing local biogas transport systems in several regions [Citation58].

Administrative areas

Due to their cross-sectoral characteristics, biogas solutions are influenced by policies within several administrative areas. On the national level, biogas solutions are usually handled by two or more ministries or other governmental bodies, with different areas of responsibility and focus. In the countries covered in this survey, five administrative areas were identified as the most relevant ones: Environment and Climate; Energy; Agriculture, Forestry and Regional Development; Economy and Finance; and Infrastructure and Transport ().

Ministries and agencies of Environment and Climate are involved in biogas governance in all the studied countries, mainly in relation to organic waste management, handling of digestate and nutrient recycling. The environmental aspects of biogas solutions have a particularly strong position in France, where biogas policies often depart from nutrient recycling and sustainable ecosystems [Citation59]. In Finland, the link between biogas and nutrient recycling is expressed through the fusion of the national associations for biogas and organic waste treatment to the Finnish Biocycle and Biogas Association [Citation60]. In Sweden, the Ministry of Environment is responsible for the regulations for investment support [Citation61], which is administered by the Environmental Protection Agency together with the County Administrative Boards [Citation62].

Energy is an administrative area that is naturally associated with biogas solutions through its responsibilities for the production and distribution of electricity and heat as well as development of renewable energy. Biogas has held a central position in renewable electricity production plans in Germany (2000–2017) [Citation54], Italy (2008–2017) [Citation63] and Czech Republic (2005–2013) [Citation49]. Since a large share of the biogas producers in these countries are contracted to produce electricity, electricity production continues to be important even though the respective national plans have changed. Denmark and France have an increasing focus on injection of biomethane into the gas grid. France has taken on a national goal that 10% of the natural gas used should be renewable by 2030 [Citation64], and it is deemed possible to even achieve 30% [Citation65]. Denmark reached a 20% share of biomethane in the gas grid in 2020 [Citation66], and has decided an end date to natural gas and oil extraction projects in the North Sea [Citation67].

The agricultural sector is central for the biogas production in countries like Germany, Italy, France, Czech Republic and Denmark, where a large share of the production comes from agricultural substrates. Moreover, it is increasingly important in Sweden, Norway and Finland, where biogas production from agricultural substrates is hitherto less developed. In terms of administration, Agriculture is often associated with Forestry and Regional Development. The biogas policies in the agricultural area are mainly on nutrient recycling and use of digestate, but also on valorization of agricultural waste and reduction of methane emissions from manure management. In addition, regional and rural development is a recurrent theme and a motive for bioenergy supporting policies in many policy documents, especially on EU level. Economic support for anaerobic digestion of manure is offered in France [Citation23], Germany [Citation68], Italy [Citation69], Norway [Citation51] and Sweden [Citation70], and is being investigated to be introduced in Finland [Citation71, Citation72].

Different types of economic instruments employed to stimulate biogas solutions are in some way linked to the area of Economy and Finance, whether they come in the form of feed-in-premiums (FiP), feed-in-tariffs (FiT) or tax exemption. The practical administration and implementation of such instruments, however, are often handled below ministry level. For example, in Sweden, the investment support for biogas plants is administered by the Environmental Protection Agency [Citation62] and the methane reduction support by the Board of Agriculture [Citation73]. On the other hand, in Germany, the Ministry of Economic Affairs is responsible for the national directive on renewable energy production, EEG [Citation74].

Lastly, in countries where biomethane is used as a vehicle fuel (Sweden, Finland, Norway), important policies are often connected to the area of Transport and Infrastructure. While Infrastructure can also refer to distribution of biogas and biomethane, natural gas grid issues may belong to other administrative areas such as Energy. In Denmark, conditions for gas grid injection are handled by the Ministry of Industry, Business and Financial Affairs [Citation75].

Targeted part of the value chain

Policies for stimulating development of biogas can target different parts of the value chain: production, distribution and use of biogas and biofertilizer. Which part of the value chain that is targeted depends on its purpose, and sometimes which administrative area it has evolved from. In all the studied countries, there have been investment programmes often connected to wastewater treatment, rural development and climate mitigation, which during different time periods have provided financial support for developing biogas production. These programmes have been essential for building up production capacity. In most of the countries, economic incentives for stimulation of the biogas production are directed to the producers (). However, in Sweden as well as in Norway and Finland, biogas subsidies have targeted the use, to guarantee attractive prices for the consumers.

While it can be sufficient to concentrate the efforts to either production or use to affect the whole value chain, that is not always the case. Without targeted and effective incentives for certain types of production and substrates, some of the many benefits of biogas may not be realized. An example of such directed policies are the manure digestion premiums, which have been introduced for reducing methane emissions from agriculture. Currently, there are such premiums in France [Citation78], Germany [Citation79], Sweden [Citation70] and Norway [Citation80], and introducing them are under consideration in Finland [Citation72]. In Sweden and Norway, the manure digestion premium is the only instrument that so far has been directed toward production of biogas.

Policy instrument types

In most of the countries, the producers receive payment according to a fixed FiT, when delivering gas or biogas-produced electricity and heat to the gas, heat or electricity networks or industry (). The received FiTs are often diversified for different producers according to scale-of-production or sector but are fixed for a certain producer over a defined long-term period. In France, the fixed prices are higher for small producers and somewhat higher for gas from sewage treatment and agriculture than for gas produced from urban waste and landfills [Citation78]. Producer support in the form of rather generous FiTs that have been guaranteed over a long time-period have created strong incentives for expanding the biogas production. This type of system created a very fast production growth in particularly Germany, Italy, and the Czech Republic and more recently in Denmark. However, such a system that is built on direct payments to an expanding production without limitations of producers and production may, if effectual, lead to rapidly increasing costs that are difficult to handle in government budgets. In Germany, Italy, the Czech Republic and Denmark, the support systems have been reformed in order to reduce and make the budgetary expenses more foreseeable. In Italy, the support system for biogas introduced in 2008 was changed in 2013, resulting in less favorable conditions for new biogas plant investments [Citation63]. In 2018, a new support system was introduced, only rewarding biomethane production for road transport [Citation69]. Meanwhile, many existing biogas plants are still contracted—under the former support system—to produce electricity [Citation69]. In Czech Republic, the FiT and FiP for electricity and heat from biogas were terminated at the end of 2013, making new biogas projects economically unattractive [Citation46, Citation49]. The German support system for renewable energy production (EEG) has been revised several times since it was first introduced in 2000. In the 2021 update of the EEG, only small biogas plants using a large share of biowaste or manure receive a FiT, while larger producers are assigned to a tender process where they have to make bids for the level of support they need [Citation54]. Similar tender systems are being introduced in Denmark [Citation75] and Finland [Citation72]. The French FiTs for electricity from biogas have been lower than what could previously be seen in Germany and Italy, and the system has not gone through any radical changes thus far [Citation50, Citation82].

In Sweden, Norway and Finland, the biogas development has dominantly been targeted via tax exemption. Since tax exemptions does not involve government spending, it does not create budgetary complications like fixed tariffs without strict limitations in time and amounts have tended to do. Between 2008 and 2014, the biogas production and the use of biogas as transport fuel in Sweden expanded radically, but this expansion was interrupted by a combination of changed car taxation, low oil prices and uncertainty concerning the support system. The main instrument for stimulating biogas development in Sweden has up to now been tax exemption when sold as transport fuel, which is the dominating use of biogas in the country, while no production support exists besides manure digestion premium. This kind of support for biogas development has however needed approval by the EU commission, which until 2020 was only granted for short time periods, up to three years. This made the support system very shortsighted, provisionary and unstable. In 2020, the tax exemption for biogas, biomethane and biopropane was approved for 2021–2030, which made the consumption support much more stable and foreseeable over the long-term. In the last five years, the use of biogas has strongly increased in Sweden; however, this has not resulted in a corresponding increase of biogas production in Sweden, but in increasing imports from Denmark [Citation25]. Denmark introduced investment support for biogas plants and a FiP for injection of biomethane into the gas grid in 2012 [Citation83]. Combined with the tax exemption for biogas implemented in Sweden, this has made Danish biogas very competitive on the Swedish market [Citation81]. This also makes it more attractive for Danish producers and distributors to sell the gas to Sweden than to sell it in Denmark.

In addition to tax exemption for use of biogas and investment support for new plants, Finnish biogas producers can receive economic support for electricity or heat production [Citation72]. In Norway, biogas is exempt from both taxes and road fees, and the ban on landfill of organic waste in issued 2009 has encouraged municipalities to invest in anaerobic digestion plants [Citation51].

The levels of economic support vary substantially between the countries, but also within the support system of each country, depending on how the biogas is produced and what it is used for. In , support for electricity or heat production from biogas has been converted to the equivalent support per MWh biogas, assuming an efficiency of 35% (in line with, e.g. [Citation43, Citation84]). In absolute numbers, Italy, Germany and France have or have had relatively large subsidies for biogas. The real value of the subsidies is of course dependent on the investment and production costs in the respective country, as well as the level of energy prices. Westlund et al. [Citation81] found that the cost of producing biomethane in Sweden is on average 90 €/MWh. Based on their findings, they argued that an additional premium for all biogas production of 20–45 €/MWh would be required to make biomethane competitive against natural gas. Similarly, Eyl-Mazzega and Mathieu [Citation85] indicated a production cost of 80–100 €/MWh for biomethane from monocrops in Italy, with potential for reductions through technology development. According to EU state aid regulations, subsidies for renewable energy are not allowed to be higher than the cost discrepancy compared to the fossil alternative [Citation86]. Higher subsidies can therefore be given to biogas from substrates that are more expensive to collect and to treat. This is the case, e.g. for manure, which renders higher subsidies for biogas producers in many of the studied countries. Moreover, biomethane from manure and other forms of bio-waste qualifies as an advanced biofuel, which is prioritized in EU goals on renewable transports [Citation29], making these substrates more attractive particularly for vehicle fuel production.

Temporal dynamics

In most of the countries, the support measures have been introduced with a very long time horizon. The FiTs have been fixed for new producers and production facilities for an extensive time period, often 20 years (). This has provided foreseeable incomes and pay-back times and minimized the risks for new investments, which have made the investments very attractive. However, such systems bind up future state budgets and decrease the room for new initiatives for a long time. In countries such as Germany, Italy, the Czech republic and Denmark, generous FiTs that were guaranteed for decades accelerated the development but also made the costs explode, which led to that the systems or FiTs were reformed toward less attractive support levels. Sometimes the time periods of guaranteed price levels were shortened, and in Germany the access to the system was restricted by introduction of a tender system, where producers have to apply for contracts of delivering certain amounts [Citation54]. These reforms have, however, not changed the fixed rates for those already in the system that can go on producing under the same terms for many years to come. In Denmark, that most recently reformed its support system, the last contracts signed under the old system are valid into the 2040s [Citation76]. France has the same kind of time frame as the above-mentioned countries, but have not experienced the same dramatic changes during the last 20 years.

Sweden and Norway have traditions of much shorter time horizons in policy and support systems than other European countries. To some extent, the possibility of changing or updating the economic and institutional conditions on an annual basis makes the policy landscape less predictable, even though in many cases the policies tend to be prolonged or only moderately altered. Countries that have sacrificed flexibility for predictability seem to have achieved a higher biogas production per capita. However, by tying a large share of their biogas producers to long-term contracts for electricity or heat production, they have made a possible transition to using biogas in other sectors, such as road transport, much more complicated.

When it comes to the temporal dynamics of non-economic policies, there seems to be relatively short time horizons even in countries where long-term financial support is implemented, such as Finland, Italy and Czech Republic:

“I would say that the biggest problem has been that there has been a lot of uncertainty regarding the development of the whole sector.” [Citation72]

“Unfortunately, there is not a clear strategy for the next five or ten years. We have to wait and to understand what the new government would like to do.” [Citation69]

“There are no specific targets for biogas. Our government sees the future of carbon free country in further use of nuclear energy.” [Citation49]

Strategies and goals, unlike many energy production support systems, are not regulated through a contract between the government and the biogas companies, which allows them to be changed or replaced with shorter notice. Moreover, changes in regulatory policies can induce changes in economic policies, which are usually formed as part of a broader strategy.

Discussion

In many of the studied countries, there seem to be distinct connections between changes in biogas production development and changes in the national policy framework for biogas. The Czech Republic experienced a rapid growth in biogas production following the introduction of a favorable feed-in tariff system, but this growth stagnated as soon as the tariff was reduced. Germany and Italy grew to become the two top biogas-producing countries in Europe, much because of appealing FiT systems. However, these developments decelerated after the FiT systems changed or were replaced by other support systems. In Denmark, the biogas production has increased strongly upon the implementation of a FiP for biomethane. Meanwhile, as Sweden failed to maintain the competitiveness of its domestic biogas against imported biogas, partly due to a support system that seemed short-sighted and unpredictable, the Swedish biogas production stagnated despite a steadily increasing demand. The trade of gas and certificates between Denmark and Sweden demonstrates the importance of considering not only vertical policy interaction within a country, but also horizontal interaction between nations and regions. Another example of this is the UK biodiesel market, where the domestic production decreased in 2007–2008 in favor of imported biodiesel from the US, as American producers received much better subsidies [Citation87].

Different forms of support for biogas production and use have proven successful for increasing biogas production in the studied countries. The outcome of an economic instrument seems to depend more on its size and its longevity than on its form and which part of the value chain it targets. In the end, all economic instruments that make biogas solutions more competitive can effectively stimulate growth of production and use, whether they are directed to the producer or are used to reduce the price for the customer. In line with these findings, several studies have observed the importance of economic support for the diffusion of biogas solutions (see, e.g. [Citation88–90]). Furthermore, many studies point at stability and continuity as one of the most important success factors of biogas policies (see, e.g. [Citation19, Citation21, Citation23, Citation24, Citation82, Citation91–94]). However, long-term policies—or, even more so, the combination of long-term and technology-specific policies—risk creating lock-in effects that impede transitions, e.g. from one area of use of biogas to another, as in the cases of Germany and Italy, where a transition to biomethane production may be delayed by the long-lasting electricity production contracts. Thus, a certain amount of agility and flexibility may be required to address future challenges and needs. Of the countries compared in this study, France has had the most stable development of biogas production in the last 20 years, owing to a policy framework with moderate but predictable subsidy levels.

It is evident that some European countries have been more successful than others in exploiting their domestic potential for biogas production. For example, Germany produces more than 1 MWh per person and year, while the corresponding figure for France, Norway and Sweden is around 0.2 MWh per person and year. The average for the EU-27 is nearly twice as high, just under 0.4 MWh per person and year (calculated based on [Citation20, Citation47]). This could indicate a larger untapped potential in these countries. For example, a national inquiry in Sweden proposed—based on previous estimates—a target to increase the production of renewable gases from 2 TWh/year to 10 TWh/year (corresponding to 1 MWh/capita) by 2030, and the long-term technical potential was estimated to be more than 30 TWh/year [Citation81]. However, even for countries that already have a relatively high production, like Germany and Denmark, there is room for further increasing the biogas production:

“The production potential for biogas in Germany is far from exhausted, especially from residual and waste materials” [Citation54]

For Denmark, the potential for biogas production has been estimated to 40–50 PJ/year [Citation95], which would correspond to over 2 MWh per person and year. Realizing this potential would make biogas significant from an energy perspective, and would at the same time bring additional perks in form of improved nutrient circulation, waste handling and reduced environmental impact. While not all countries have the same preconditions for biogas production as Denmark in terms of large-scale agriculture, population density and gas grid access, even 1 MWh per person and year would be a big step up for many European countries. On an aggregate level for the EU-27, that would correspond to about 450 TWh/year (calculated based on [Citation47]).

There is a great diversity of strategies and policy frameworks for biogas solutions in Europe. Until now, the policies influencing biogas solutions have mainly been present on the national level. The new EU strategies developed within the frame of the EU Green Deal can be a first step towards a more uniform policy framework for biogas solutions in the EU and more direct co-financing of biogas expansion from the EU. The fact that new EU policies increasingly acknowledge production and use of biogas as central for a sustainable development can hopefully stimulate a further positive development for biogas solutions, without inhibiting the varying sustainability strategies on the national level.

The type of comparison provided in the present study can serve to highlight differences and similarities between different countries. It is, however, not necessarily possible to draw conclusions about which effects a policy may have in one country based on the outcome of the same policy in another country. Every effective or ineffective biogas policy is effective or ineffective in its own way, in relation to its context, existing policy frameworks and traditional structures of a specific country. Thus, policies that prove successful for the biogas development in one country may not have the same effect in another country. For example, rewarding the feed-in of biomethane into the gas grid will most likely have a very limited effect in countries like Norway, Sweden and Finland, where only a minority of biogas producers are located near the gas grids. Likewise, the value of economic support must be seen in relation to local production costs—both investment and operational costs—energy prices and taxes. Czech Republic achieved a quick expansion of its domestic biogas production through a system with much lower FiT and FiP than in Italy, Germany or France. However, compared to other Eastern European countries, the subsidies given to Czech biogas producers were relatively large [Citation96].

Another way of using the policy model could be in case studies or comparisons of two or a few countries. This would give room for deeper analyses of biogas policies and their influence on the biogas development, as well as suggestions for future policy design and strategies, whereas a broader comparison such as the present one is better suited for a higher, less detail-oriented level of analysis. A country case study would therefore be a natural future step to test and evaluate the versatility of the policy model.

The policy model used for the comparison in this study was developed for describing the European policy landscape, and was based mainly on European policy literature [Citation39]. Nevertheless, the general characteristics of biogas policies described in this model seem recurrent in other regions as well. The multi-functionality of biogas solutions is most often reflected in the policy structure, with policies within many different administrative areas influencing the biogas conditions. This can be found in other studies on biogas policies in, e.g. China [Citation97], South Korea [Citation98], Canada [Citation99] and India [Citation89]. The strength and importance of different administrative levels vary between countries. In countries with strong federal governance, the regional level is often central, and often much more influential on the local biogas development than the national level. Typical examples of this are Canada [Citation100], USA [Citation101], Australia [Citation102] and Brazil [Citation103]. Thus, this model should be applicable—possibly with some modifications—in comparative studies and case studies outside Europe as well.

Conclusions

This paper has presented a comparison of the biogas development and biogas policies in eight European countries. The policy comparison was made using a model with five dimensions: type of policy; administrative area; administrative level; part of the value chain addressed; and temporal change and continuity. In addition, the relations between national policy frameworks and biogas development were analyzed. The analysis presented in this paper shows clear connections between biogas policies and development of biogas production in the studied countries. It is evident that policies—particularly economic instruments—can have a strong influence on the development of biogas production in a country, both in a positive and a negative direction. The studied countries show examples of both success and setbacks in biogas development, often strongly related to policy changes.

The effectiveness of economic instruments depends more on their relevance for the targeted actors and how long they can be expected to be valid than which part of the value chain they address. Hence, an increased production of biogas can be achieved either through production support or by incentivizing the use of biogas. However, policies targeting specific parts of the biogas value chain can be required to incorporate certain benefits that biogas solutions can bring, for example a manure digestion premium to reduce agricultural methane emissions and improve nutrient circulation. Moreover, a limited value chain perspective can lead to benefits related to other parts of the value chain to move across the border to another country, through trade of biogas and green certificates.

There is a large potential for producing and using more biogas in Europe, even in countries which already have a relatively high production. 1 MWh biogas per capita has already been achieved in Germany and similar or even higher levels are deemed possible to achieve in many countries. The agricultural sector has a central role and will continue to be increasingly important for biogas production, as a large share of the potential is found in agricultural substrates. In some countries, there is also a potential for increased anaerobic digestion of sewage sludge and municipal organic waste.

Long-term policies and policy instruments can be a good way of creating favorable conditions for the biogas sector, providing a stable and predictable framework for both producers and customers. However, there is a risk for lock-in effects if policies are directed towards specific technical solutions, feedstock or areas of use. Furthermore, it can be a challenge to design policies and set subsidy levels that are both effective and economically sustainable in a long-term perspective, as other factors may change that influence how well the policy works. In the last 20 years, France has been more successful than other countries when it comes to creating conditions for a stable biogas development.

Specific policies and policy instruments for stimulating the biogas development may not be directly transferable from one country to another, as they depend on the context in which they are applied. The lessons learned from a comparative analysis such as the one presented in this paper rather lies in the overarching, strategic level of policy design.

Acknowledgements

We would also like to thank the interviewees for providing valuable inputs to the study.

Disclosure statement

We declare that we have no competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Additional information

Funding

References

- Hagman L, Blumenthal A, Eklund M, et al. The role of biogas solutions in sustainable biorefineries. J Cleaner Prod . 2018;172:3982–3989.

- Richardson D. Farmers in rural Africa turn to biogas solutions to enable energy independence and cut deforestation rates. Gas Int. 2012:22–23.

- Lindfors A, Feiz R, Eklund M, et al. Assessing the potential, performance and feasibility of urban solutions: methodological considerations and learnings from biogas solutions. Sustainability. 2019;11(14):3756.

- Kiselev A, Magaril E, Magaril R, et al. Towards circular economy: evaluation of sewage sludge biogas solutions. Resources. 2019;8(2):91.

- Hagman L, Eklund M. The role of biogas solutions in the circular and bio-based economy. Biogas Research Center; 2016.

- Dada O, Mbohwa C. Energy from waste: a possible way of meeting goal 7 of the sustainable development goals. Mater. Today: Proc. 2018;5(4):10577–10584.

- World Biogas Association. Factsheet 3: how to achieve the sustainable development goals through biogas 2017.

- Scarlat N, Dallemand J-F, Fahl F. Biogas: developments and perspectives in Europe. Renew Energy. 2018;129:457–472.

- Conti C, Mancusi ML, Sanna-Randaccio F, et al. Transition towards a green economy in Europe: innovation and knowledge integration in the renewable energy sector. Res Policy. 2018;47(10):1996–2009.

- McCarty T, Sesmero J. Uncertainty, irreversibility, and investment in Second-Generation biofuels. Bioenerg Res. 2015;8(2):675–687.

- Hosseini SE, Wahid MA. Development of biogas combustion in combined heat and power generation. Renew Sustain Energy Rev. 2014;40:868–875.

- Salvador R, Barros MV, Rosário J, et al. Life cycle assessment of electricity from biogas: a systematic literature review. Environ Prog Sustain Energy. 2019;38(4):13133.

- Ahmadi Moghaddam E, Ahlgren S, Hulteberg C, et al. Energy balance and global warming potential of biogas-based fuels from a life cycle perspective. Fuel Process Technol . 2015;132:74–82.

- Lyng K-A, Brekke A. Environmental life cycle assessment of biogas as a fuel for transport compared with alternative fuels. Energies. 2019;12(3):532.

- Chen S, Chen B, Song D. Life-cycle energy production and emissions mitigation by comprehensive biogas-digestate utilization. Bioresour Technol. 2012;114:357–364.

- Yasar A, Nazir S, Tabinda AB, et al. Socio-economic, health and agriculture benefits of rural household biogas plants in energy scarce developing countries: a case study from Pakistan. Renew Energy. 2017;108:19–25.

- EurObserv’ER. Biogas Barometer. 2017.

- EurObserv’ER. Biogas Barometer. 2010.

- Kampman B, Leguijt C, Scholten T, et al. Optimal use of biogas from waste streams - An assessment of the potential of biogas from digestion in the EU beyond 2020. European Commission; 2016.

- Eurostat. Supply, transformation and consumption of renewables and wastes - Indigenous production (Biogases, Landfill gas, Sewage sludge gas and Other anaerobic digestion) 2021. Available from ec.europa.eu/eurostat/data/database. (accessed February 16, 2021).

- Huttunen S, Kivimaa P, Virkamäki V. The need for policy coherence to trigger a transition to biogas production. Environ Innov Soc Transit. 2014;12:14–30.

- Nilsson M, Zamparutti T, Petersen JE, et al. Understanding policy coherence: analytical framework and examples of Sector-Environment policy interactions in the EU: understanding policy coherence. Env Pol Gov. 2012;22(6):395–423.

- Hermann L, Hermann R. Report on regulations governing AD and NRR in EU member states SYSTEMIC, Grant Agreement no 730400; 2018.

- van Grinsven A, Leguijt C, Tallat-Kelpsaite J. Supporting mechanisms for the development of biomethane in transport CE Delft; 2017.

- Klackenberg L. Production and use of biogas and digestate in 2019 (Produktion och användning av biogas och rötrester år 2019). Energimyndigheten; 2020.

- European Commission. Directive 2018/851 of the European parliament and of the council amending directive 2008/98/EC on waste. Off J Eur Union. 2018:109–140.

- European Commission. Directive 2008/98/EC of the European parliament and of the council on waste and repealing certain directives. Off J Eur Union. 2008:3–30.

- European Commission. Communication from the commission to the European parliament, the council and the European economic and social committee of the Regions – A sustainable bioeconomy for Europe: strengthening the connection between economy, society and the environment Brussels, Belgium: 2018.

- European Commission. Directive 2018/2001 of the European parliament and of the council on the promotion of the use of energy from renewable sources (recast). Off J Eur Union. 2018:82–206.

- European Commission. Directive 2009/28/EC of the European parliament and of the council on the promotion of the use of energy from renwable sources. Off J Eur Union. 2009:16–62.

- European Commission. Directive 1999/31/EC of the European parliament and of the council on the landfill of waste. Off J Eur Union. 1999:1–19.

- European Commission. Regulation 1305/2013 of the European parliament and of the council of 17 december 2013 on support for rural development by the European agricultural fund for rural development (EAFRD) and repealing council regulation (EC) no 1698/2005. Off J Eur Union. 2013:487–548.

- European Commission. Regulation 1310/2013 of the european parliament and of the council of 17 december 2013 laying down certain transitional provisions on support for rural development by the european agricultural fund for rural development (EAFRD), amending regulation (EU) no 1305/2013 of the european parliament and of the council as regards resources and their distribution in respect of the year 2014 and amending council regulation (EC) no 73/2009 and regulations (EU) no 1307/2013, (EU) no 1306/2013 and (EU) no 1308/2013of the european parliament and of the council as regards their application in the year 2014. Off J Eur Union. 2013:865–883.

- European Commission. Communication from the commission to the european parliament, the council and the european economic and social committee of the regions on an EU strategy to reduce methane emissions Brussels, Belgium: 2020.

- European Commission. Communication from the commission to the european parliament, the council and the european economic and social committee of the Regions - Powering a climate-neutral economy: an EU strategy for energy system integration Brussels, Belgium: 2020.

- European Commission. Communication from the commission to the european parliament, the council and the european economic and social committee of the Regions - A farm to fork strategy for a fair, healthy and environmentally-friendly food system Brussels, Belgium: 2020.

- European Commission. Commission proposes new EU framework to decarbonise gas markets, promote hydrogen and reduce methane emissions. European Commission, Press Corner 2021. Available from https://ec.europa.eu/commission/presscorner/detail/en/IP_21_6682. (accessed December 20, 2021).

- Nevzorova T, Kutcherov V. Barriers to the wider implementation of biogas as a source of energy: a state-of-the-art review. Energy Strategy Rev. 2019;26:100414.

- Gustafsson M, Anderberg S. Dimensions and characteristics of biogas policies – modelling the european policy landscape. Renew Sustain Energy Rev. 2021;135:110200.

- Deremince B, Scheidl S, Stambasky J, et al. Data bank with existing incentives and subsequent development of biogas plants compared to national targets Biogas Action, Grant Agreement no 691755; 2017.

- Barré C, Przadka A, Kovacs A, et al. Inventory and analysis of the EU and national regulatory framework BIOSURF, Grant agreement no 646533; 2016.

- Rogstrand G. Overview on administrative and legal conditions as well as on financial and other support programs, for small to medium scale biomethane production and supply Record Biomap, Grant Agreement no 691911; 2018.

- Decorte M, Tessens S, Fernández D, et al. Mapping the state of play of renewable gases in Europe. REGATRACE; 2020.

- Spijker E, Jepma C, Hofman E, et al. A level playing field for the European biogas and biomethane markets – Case of The Netherlands and Germany: policy environment, key differences and harmonisation issues. 2015.

- Gustafsson M, Anderberg S, Fredriksson Möller B, et al. The institutional conditions of biogas (biogasens institutionella villkor). Biogas Research Center; 2020.

- RES LEGAL Europe. RES LEGAL Europe - Legal sources on renewable energy 2021. Available from http://www.res-legal.eu/en/comparison-tool/. (accessed March 19, 2021).

- Eurostat. Population on 1 January by age and sex 2020. Available from ec.europa.eu/eurostat/data/database. (accessed February 16, 2021).

- NGVA Europe. CNG/LNG map 2020. Available from https://www.ngva.eu/stations-map/. (accessed August 13, 2020).

- CzBA. Česká Bioplynová Asociace (Czech Biogas Association) 2020.

- Club Biogaz. Club Biogaz de l’Association Technique Énergie Environnement (French Biogas Association) 2020.

- Måge J. Avfall Norge (Norwegian Waste Association) 2020.

- EBA. European biogas association statistical report: 2019 European overivew Brussels, Belgium: 2020.

- EBA. New German Renewable Energy Act (EEG) shoots biogas in Germany (Press Release) 2014.

- Stolpp S. Fachverband Biogas (German Biogas Association) 2021.

- Stubholt LM, Grønnbakk MT. EØS-avtalens betydning for norsk regelutvikling – passiv resepsjon av fremmed rett eller aktiv europapolitikk? IP. 2019;77(4):350.

- Thrän D, Schaubach K, Majer S, et al. Governance of sustainability in the german biogas sector—adaptive management of the renewable energy act between agriculture and the energy sector. Energ Sustain Soc. 2020;10(1):3.

- Stürmer B. Biogas – part of austria’s future energy supply or political experiment? Renew Sustain Energy Rev. 2017;79:525–532.

- Lundmark R, Anderson S, Hjort A, et al. Establishing local biogas transport systems: policy incentives and actor networks in swedish regions. Biomass Bioenergy. 2021;145:105953.

- Eden A. Bio-Methane support policy in France. Federal Ministriy for the Environment, Nature Conservation and Nuclear Safety (BMU); 2018.

- Finnish Biocycle and Biogas Association (Suomen Biokierto ja Biokaasu ry). Association (Yhdistys) 2019. Available from https://biokierto.fi/yhdistys/. (accessed January 11, 2021).

- Swedish Ministry of Environment. Förordning (2015:517) om stöd till lokala klimatinvesteringar. 2015.

- Swedish Environmental Protection Agency. Om Klimatklivet 2021. Available from https://www.naturvardsverket.se/Miljoarbete-i-samhallet/Miljoarbete-i-Sverige/Uppdelat-efter-omrade/Klimat/Om-Klimatklivet/. (accessed January 11, 2021).

- Maggioni L, Iperoni C, Pezzaglia M. The biogas and biomethane market in Italy. Gas for Energy 2018.

- Government of France. LOI no. 2015-992. vol. LOI no. 2015-992. 2015.

- GRDF. Gaz Réseau Distribution France - Découvrir les untiés d’injection 2020. Available from https://www.grdf.fr/institutionnel/actualite/dossiers/biomethane-biogaz/unites-injection-gaz-vert. (accessed April 15, 2020).

- Energinet. Biogas via gasnettet. energinet.dk 2021. Available from https://energinet.dk/Gas/Biogas. (accessed February 17, 2021).

- Folketinget. Fremtiden for olie- og gasinvinding i Nordsøen 2020.

- Government of Germany (Deutscher Bundestag). Gesetz zur Neuregelung des Rechts der Erneuerbarer Energien im Strombereich und zur Änderung damit zusammenhängender Vorschriften. Bundesgesetzblatt 2008.

- CIB. Consorzio Italiano Biogas (Italian Biogas Consortium) 2019.

- Swedish Ministry of Enterprise and Innovation. Förordning (2014:1528) om statligt stöd till produktion av biogas. 2014.

- Luostarinen S, Tampio E, Niskanen O, et al. Lantabiokaasutuen toteuttamisvaihtoehdot. Helsinki: Luke Luonnonvarakeskus; 2019.

- Virolainen-Hynnä A. Suomen Biokierto ja Biokaasu ry (Finnish Biocycle and Biogas Association) 2019.

- Swedish Board of Agriculture. Gödselgasstöd 2020. Available from https://jordbruksverket.se/stod/fornybar-energi/godselgasstod#h-Forfattningar. (accessed January 11, 2021).

- Mozgovoy A. Fachverband Biogas (German Biogas Association) 2020.

- Nielsen BS. Biogas Danmark (Danish Biogas Association) 2020.

- Government of Denmark, Ministry of Climate, Energy and Utilities. Energiaftale af 29. juni 2018.

- Finnish Energy Agency. Information about the Power Plants Accepted to the Feed- In-Tariff System 2018 (Syöttötariffijärjestelmään Hyväksyttyjen Voimalaitoksien Tietoja 2018) 2019.

- Rabetsimamanga O, de Singly B, Barneto M, et al. Panorama du gaz renouvable en 2018. GRDF/GRTgaz/SER/SPEGNIN/Teréga; 2019.

- Government of Germany (Deutscher Bundestag). Gesetz zur Einführung von Ausschreibungen für Strom aus erneuerbaren Energien und zu weiteren Änderungen des Rechts der erneuerbaren Energien. Bundesgesetzblatt 2016.

- Remøy TD. Virkemidler for økt bruk og produksjon av biogass. Miljødirektoratet; 2020.

- Westlund Å. Mer biogas! För ett hållbart Sverige. Biogasmarknadsutredningen; 2019.

- Torrijos M. State of development of biogas production in Europe. Procedia Environ Sci . 2016;35:881–889.

- Government of Denmark, Ministry of Climate, Energy and Utilities. Energiaftale af 22. marts 2012.

- Gustafsson M, Ammenberg J, Murphy JD. IEA bioenergy task 37 - Country reports summaries 2019 IEA Bioenergy; 2020.

- Eyl-Mazzega M-A, Mathieu C. Biogas and biomethane in Europe: lessons from Denmark, Germany and Italy. Paris: Ifri; 2019.

- European Commission. Directive 2003/96/EC restructuring the community framework for the taxation of energy products and electricity. Off J Eur Union. 2003.

- Lieu J, Spyridaki N, Alvarez-Tinoco R, et al. Evaluating consistency in environmental policy mixes through policy, stakeholder, and contextual interactions. Sustainability. 2018;10(6):1896.

- Hasan ASMM, Kabir MA, Hoq MT, et al. Drivers and barriers to the implementation of biogas technologies in Bangladesh. Biofuels. 2020(11):1–13.

- Mittal S, Ahlgren EO, Shukla PR. Barriers to biogas dissemination in India: a review. Energy Policy. 2018;112:361–370.

- Patinvoh RJ, Taherzadeh MJ. Challenges of biogas implementation in developing countries. Curr Opin Environ Sci Health. 2019;12:30–37.

- Ammenberg J, Anderberg S, Lönnqvist T, et al. Biogas in the transport sector—actor and policy analysis focusing on the demand side in the Stockholm region. Resour Conserv Recycl. 2018;129:70–80.

- Capodaglio A, Callegari A, Lopez M. European framework for the diffusion of biogas uses: emerging technologies, acceptance, incentive strategies, and Institutional-Regulatory support. Sustainability. 2016;8(4):298.

- Dahlgren S, Kanda W, Anderberg S. Drivers for and barriers to biogas use in manufacturing, road transport and shipping: a demand-side perspective. Biofuels. 2022;13(2):177–188.

- Lönnqvist T, Anderberg S, Ammenberg J, et al. Stimulating biogas in the transport sector in a swedish region – an actor and policy analysis with supply side focus. Renew Sustain Energy Rev. 2019;113:109269.

- Danish Energy Agency (Energistyrelsen). Perspektiver for produktion og anvendelse af biogas i Danmark. 2018.

- Chodkowska-Miszczuk J, Kulla M, Novotný L. The role of energy policy in agricultural biogas energy production in visegrad countries. Bull Geogr Socio-Econ Ser. 2017;35(35):19–34.

- Xue S, Song J, Wang X, et al. A systematic comparison of biogas development and related policies between China and Europe and corresponding insights. Renew Sustain Energy Rev. 2020;117:109474.

- Kim Y-S, Yoon Y-M, Kim C-H, et al. Status of biogas technologies and policies in South Korea. Renew Sustain Energy Rev. 2012;16(5):3430–3438.

- Canadian Biogas Association. Current Status and Future Potential of Biogas Production from Canada’s Agriculture and Agri-Food Sector. 2018.

- Green J. Canadian Biogas Association 2019.

- Cuellar AD, Webber ME. Policy incentives, barriers and recommendations for biogas production. San Francisco: 2009.

- Edwards J, Othman M, Burn S. A review of policy drivers and barriers for the use of anaerobic digestion in Europe, the United States and Australia. Renew Sustain Energy Rev . 2015;52:815–828.

- Kanda W, Zanatta H Magnusson T, Hjelm O, Larsson M Policy coherence in a fragmented context: the case of biogas systems in Brazil. Energy Res Social Sci. 2022;87.

Appendix –

interview form

Introduction

Interview with representative for [organization] in [country].

Please describe the role of [the organization] in [the country].

Please describe your role within [the organization].

General questions

Which sector/-s is/are the most important for [the country’s]:

Biogas production?

Use of biogas?

Why is it like that? Has it been an intended strategy, or are there other explanations?

Does [the country] have any official goals for production and use of biogas?

If ‘yes’: What do these goals mean in practice?

If ‘no’: Why is that?

How are the EU directives and regulations of waste and renewable energy implemented?

Does [the country] have more ambitious goals than that, or do they stick to the common levels and goals of the EU?

What do you think have been the most driving factors behind [the country’s] development within:

Biogas production?

Use of biogas?

Have there been any financial incentives involved?

What regulatory incentives are there for biogas production/use?

Which factors, in your opinion, have been the most inhibiting for such developments?

How could/should the development of biogas production and use in [the country] be accelerated even more?

What type of efforts are needed?

Where should these efforts be concentrated? Production/use/both/other?

What does the competition for biogas look like in [the country]?

Other fuels/energy carriers? Fossil/renewable?

Other waste treatment methods?

Which factors are important on the market/-s where biogas competes? Financial/technology/policy/knowledge/other?

What role does natural gas have in the development of biogas production and use in [the country]?

Is it a competitor or a bridge for biogas?

Is there a gas infrastructure in place that facilitates the introduction of biogas?

Specific questions regarding biogas in the agricultural sector

How would you describe the role of the agricultural sector in the development of biogas solutions in [the country]?

Has it been important historically? Will it be important in the future? Which substrates from the agricultural sector are important?

How would you describe the significance of biogas for the agricultural sector in [the country]?

Economically: Biogas production as an extra source of income for farmers?

Ecologically: Increased nutrient recirculation by use of biofertilizers from biogas production, reduced GHG emissions, and so on.

In what ways are biogas solutions within the agricultural sector supported by the authorities in [the country]?

Are there regulations which facilitate and encourage production and/or use of biogas and/or biofertilizers?

Are there economic incentives for agricultural production and/or use of biogas and/or biofertilizers?

On what levels do these things exist? National, regional and/or local?

Which regulations or incentives have been the most important ones for developing agricultural biogas solutions?

Are there any significant barriers to production and/or use of biogas and/or biofertilizers within the agricultural sector in [the country]?

Do you think that the authorities could or should do more to support biogas solutions within the agricultural sector in [the country]?

To your knowledge, how do farmers in [the country] look upon biogas solutions?

Is it attractive to be or to become a biogas producer?

Are farmers in [the country] aware of the environmental benefits of anaerobic digestion and use of biofertilizer?