ABSTRACT

This paper provides a theoretical discourse linking traditional market failure literature and the recent research around potential stranded assets risks associated with the transition to a low-carbon economy (defined here as ‘transition risks’). While it does not seek to prove a mispricing in practical terms, it demonstrates the extent to which the market failure literature provides theoretical evidence of a potential mispricing of these risks, as a result of the design and interpretation of financial risk models, and the practices and institutions linked to economic agents. The evidence supports a growing body of practical literature highlighting transition risks in financial markets. It suggests that there may be a case for policy intervention to address the market failures and associated potential mispricing of risk. It also suggests however that this intervention will likely need to address both the design of financial risk models and associated transparency around their results, and the actual institutions governing risk management. A key challenge in this regard involves resolving the principal–agent problem in financial markets and the associated ‘tragedy of the horizons’.

1. Introduction

The past few years have seen a growing narrative around potential financial risks associated with the transition to a low-carbon economy, largely focused on the future of fossil fuels and the power sector (Meinshausen et al. Citation2009; Robins, Chan, and Knight Citation2012; Leaton Citation2013; Caldecott, derricks, and Mitchell Citation2015).Footnote1 This body of research argues that the transition to a low-carbon economy leads to value creation and destruction that can potentially impact the financial viability of assets on corporate and government balance sheets, a situation that can in turn impact the credit-worthiness and valuation of financial assets (e.g. equities and bonds). These risks are usually labelled ‘transition risks’, a short form this paper will use to describe this family of risks.

A key underlying assumption, either explicit or implicit, of this literature is that financial markets currently misprice the risks associated with the transition to a low-carbon economy. A consequence of this could be the creation of a bubble in valuation of assets and companies dependent on fossil-fuel energy. This is the concept of ‘transition risk’, which could – in theory – have system-wide impact and affect financial stability. ‘Transition risks’ and the ‘carbon bubble’ thesis are referenced across publications on the topic. The Financial Stability Board, on the initiative of Mark Carney – Governor of the Bank of England – and the French Treasury, has started assessing the issue. The French Parliament has passed a law mandating climate-related risk disclosure. The Swiss and German governments have both launched research inquiries on the potential financial stability risks arising from the transition to a low-carbon economy.

To date, the research around these risks has primarily focused on examining the potential materiality of these types of risks to financial market assets and actors. Notable examples include research on transition risk to physical assets (Fulton et al. Citation2015; McGlade and Ekins Citation2015; Caldecott et al. Citation2016), financial assets (Robins, Chan, and Knight Citation2012) and financial portfolios (Mercer Citation2015). Less explored in this debate is the question of whether financial market actors are already correctly pricing these risks, challenging the ‘bubble’ assumption. For example, research from organizations highlight risks to physical assets and capital expenditure plans, noting for example potential $2 trillion worth of capital expenditure that may not be profitable under a 2°C transition (Fulton et al. Citation2015). Robins, Chan, and Knight (Citation2012) suggest impact on share prices of fossil-fuel companies of 30–50%. Mercer (Citation2015) in turn shows little cross-asset impact, but some significant impacts within asset classes.

While there is growing consensus that these risks may materialize, it is unclear whether they are already priced into current asset prices. This is particularly the case for fossil-fuel companies that have lost in some cases upwards of 50% of their market capitalization in the past 2 years or even coal mining companies that have seen growing bankruptcies in the United States. Similarly, high-carbon European utilities have also suffered. While there is academic evidence of a sudden tipping point in climate policies that can create sudden, unexpected transition risks (Aghion et al. Citation2014), such literally does not directly question how actors may or may not already be pricing probabilities of such ‘surprises’.

The question of asset mispricing is key for two objectives. First, it is important from a financial stability perspective, as asset mispricing can lead to asset bubbles that may have systemic effects or at the very least create financial risks for some actors and asset classes. Second, and linked to the first, asset mispricing is also relevant from a policy and social perspective. Asset mispricing can lead to inefficient capital allocation, which in turn may inhibit growth as capital does not go to its best use. In this particular case, this may be even more problematic insofar as such inefficient capital misallocation may exacerbate economic inefficiencies that relate to the mispricing of the social cost of carbon. Thus, mispricing not only inhibits growth, but also has an additional negative impact on public welfare more generally, through negative health impacts (Lancet Citation2015) and other social and political costs.

The objective of this paper is to link the theoretical literature around market failure associated with correctly pricing risk with the literature on transition risk in order to test the premise that financial market actors currently misprice potential risks associated with the transition to a low-carbon economy. The paper will thus not contribute to the question of whether the transition to a low-carbon economy will be material for financial market actors. Rather, it seeks to build the theoretical basis as to why, should these risks be material, financial market actors may misprice these risks. In this sense, the paper provides the complementary analysis to the existing risk literature on this topic.

The paper reviews the existing literature on market failures and seeks to link it to the risk characteristics commonly associated with transition risks. Crucially, the paper only focuses on transition risks and does not address mispricing related to other climate-related risks (e.g. physical risks, litigation risks). The analysis demonstrates that transition risks exhibit a number of characteristics that, according to the market failure literature, are likely to lead to mispricing. This can be linked to the theoretical evidence on market failure as it applies to financial market models and economic agents. Developing transition risk models and associated evidence of the presence of these risks, according to the results of this paper, thus only addresses one side of the equation and needs to be complemented by activities related to tackling the broader market infrastructure and the actions of economic agents within.

The paper thus provides concrete input as to the potential for the existing body of research to improve the efficient pricing of these risks in financial markets. In addition, it suggests that there is at least theoretical evidence that these types of transition risks may be mispriced, suggesting the potential for the presence of capital misallocation related to investments associated with the transition to a low-carbon economy, both in high-carbon and low-carbon assets. This may be material for policymakers and regulators exploring the question of efficient capital allocation. It may also be material for the broader debate about achieving global climate goals. It also points the way for needed future research avenues.

The paper is organized as follows. Section 2 briefly introduces the efficient market hypothesis (EMH). Section 3 connects the market failure literature to financial market models and transition risks. Section 4 focuses on the market failure literature as it informs the assessment of economic agents. Here too the discussion is then linked to transition risks. Section 5 provides some concluding remarks.

2. A short history of the EMH

The starting point for any analysis on market failure is the EMH. Fama (Citation1970) and Samuelson (Citation1965) developed the EMH more or less in parallel.Footnote2 The EMH is based on the notion that ‘a market in which prices always “fully reflect” available information is called efficient’ (Fama Citation1970, 383). In such a scenario, information is fully available to all market participants equally and integrated into price formation instantly (Fama Citation1970).Footnote3 According to Jensen (Citation1978, 95), ‘there is no other proposition in economics which has more empirical support than the EMH’.

Whether a financial market is informationally efficient or not matters in two ways: ‘First, investors care about whether various trading strategies can earn excess returns (i.e. “beat the market”). Second, if stock prices accurately reflect all information, new investment capital goes to its highest-valued use’ (Jones and Netter Citation2014). In order for the EMH to exist, two conditions are crucial. Firstly, as highlighted above, prices need to fully (and equitably) reflect available information, allowing market participants to distinguish between different investments. Second, market participants need to operate as rational, utility-maximizing agents, an assumption also known as the ‘rational choice theory’.

The idea of the self-interested, utility-maximizing individual entered the economic discourse with the early Classical economists, notable among them being Smith (Citation1776, 105), who coined the famous adage that ‘it is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own interest’. In the nineteenth century, Mill (Citation1844, 48) then linked this self-interest to utility and rationality, arguing that political economy ‘concerned with [man] solely as a being who desires to possess wealth, and who is capable of judging the comparative efficacy of means for obtaining that end’.Footnote4 The concept of rational, utility-maximizing entered today’s discourse, on the shoulders of Walras, Pareto, Jevons and others, in the form of the Rational Choice Theory, pioneered by Robbins (Citation1938) at the London School of Economics. At the heart of the rational choice theory is the ‘homo oeconomicus’, the economic man.Footnote5

Today, the EMH forms a core tenet of finance, both as it is taught at universities (Krugman Citation2009) and increasingly thought of in practice. The growth of passive investing (PWC Citation2014) is arguably a function of the growing consensus that market actors cannot beat the market, given its ‘random walk’ characteristics. Modern portfolio theory, as developed by Markowitz (Citation1952), Tobin (Citation1958), Sharpe (Citation1964) and others relies on the assumption that optimal investing strategies involve adopting market assumptions around prices and diversifying portfolios accordingly.

At the same time, a growing literature is starting to challenge the EMH, suggesting the presence of a number of ‘market failures’ that market actors can exploit and that may lead to the mispricing of financial risk. Market failures can be defined as:

the failure of a more or less idealized system of price-market institutions to sustain ‘desirable’ activities or to stop ‘undesirable’ activities. The desirability of an activity, in turn, is evaluated relative to the solution values of some explicit or implied maximum-welfare problem. (Bator Citation1958, 351)

3. Transition risks and the design of risk models

This section will review elements of the market failure literature that can inform on the design and interpretation of financial market risk models. It will emphasize in particular the treatment of ‘tail risks’ in these models, the distribution assumed therein, and the extent to which financial market models can capture complexity, in particular as it relates to risk and uncertainty.

One of the strongest theoretical criticisms of the utility-maximization model comes from Simon (Citation1957), who coined the term ‘bounded rationality’. Simon (Citation1957, 198) argues, and it is worth quoting him at length, that:

the capacity of the human mind for formulating and solving complex problems is very small compared with the size of the problems whose solution is required for objectively rational behaviour in the real world [ … ] The first consequence of the principle of bounded rationality is that the intended rationality of an actor requires him to construct a simplified model of the real situation in order to deal with it. He behaves rationally with respect to this model, and such behaviour is not even approximately optimal with respect to the real world.

From an agent’s perspective, this may be ‘optimal’. Equally, from an investment perspective, this means that agents may not realize (or even attempt to realize) maximum returns. In this case, price formation does not reflect all information, given that agents have not attempted to optimize.Footnote7 As a result, prices may become skewed, leading potentially to capital misallocation.Footnote8

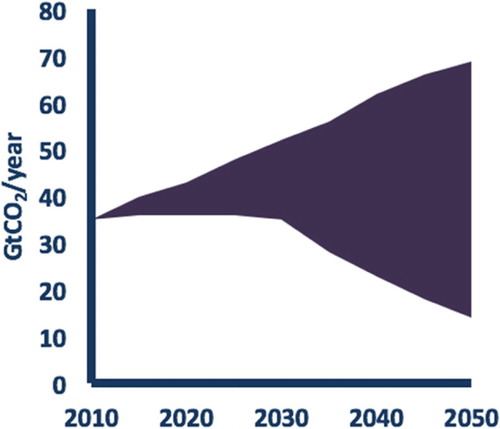

The issue of model is core to the question of transition risks. Transition risks are unlikely to be captured by traditional risk models – models which are equated to be representatives of real-world risks. There are a number of reasons for this, most notably perhaps the breakdown of the normal distribution principle associated with these risks and the lack of historical data (Simon 1957). As suggested in , the distribution of transition scenarios is not normal insofar as it exhibits a weight in one direction – there seems to be a visual weight that drags the bottom part of the curve downward. The chart thus suggests a skewed distribution in one direction – in this case in the direction of the probability related to a 2°C decarbonization pathway. Naturally, this distribution is somewhat ‘artificial’, perhaps more of a ‘social distribution’ than a quantified one – the number of 2°C scenario is not necessarily testament to its probability. But nevertheless, as a proxy for distribution, it shows a skew.

Figure 1. Range of IPCC scenarios. Source: Modified from IPCC 2014.

While the normal distribution assumption is no longer as core to finance as it used to be,Footnote9 it still forms the basis of all core models, including the models introduced by Markowitz (Citation1952) in the context of modern portfolio theory, Arrow-Debreu models (1954), Black-Scholes Options Pricing Model (1973) and more recent models of credit risk (Vasicek).Footnote10 It is also used by the International Monetary Fund stress-testing models for example (Ong Citation2014).

One core reason of using the normal distribution is the additional complexity a non-normal distribution introduces in the models – a complexity potentially avoided at least in part as a result of the bounded rationality principle. Agents satisfice by using simplified assumptions to reduce complexity. This may make sense for an agent that does not seek to optimize. It may however create systematic biases in models that lead to sub-optimal pricing of risks.

The bounded rationality thesis related to the nature of models would thus potentially apply to transition risks, as evidence suggests these risks are unlikely to be distributed in a normal manner – if the mean is a transition pathway of for example 5°C the probability of under-shooting that pathway (i.e. achieving less than 5°C warming) is significantly higher than over-shooting that pathway – based on the ‘social distribution’ logic defined above where 2°C is the official goal. Normal distribution assumptions may systematically bias against the skewed risks related to the transition to a low-carbon economy.

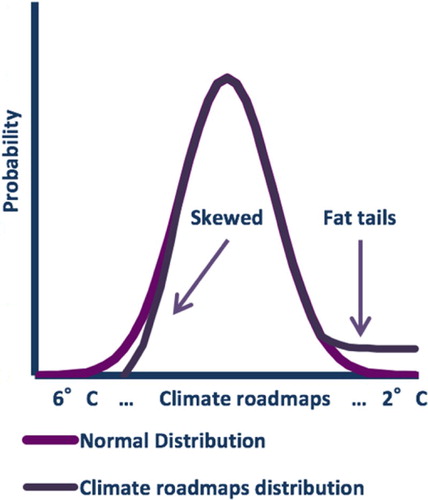

There are other ways agents may not optimize, notably in terms of dealing with tail risks. The idea that investors do not deal with risks equitably finds its roots in the Prospect Theory, developed by Kahnemann and Tsversky (Citation1979) and Tsversky and Fox (Citation1995). Tsversky argues that investors appear risk-averse for small losses, but indifferent to, or at the very least less impacted by large losses. In other words, the level of risk aversion is at least partly a function of the size of the loss, where investors are willing to take larger bets with a higher risk of loss. More recently this literature has been popularized in its application to models by Taleb (Citation2007) and his work on tail risks, which he describes as ‘black swans’ or ‘fat tails’. Taleb (2007) highlights the extent to which financial market models under-weight probabilities at the tail end of the distribution.

As outlined above, the skewed nature of climate roadmaps suggests risks associated with this transition are not normally distributed. Another way the risks are not normally distributed is potentially their characteristic as involving ‘fat tails’. While 2°C is seen as unlikely,Footnote11 it remains the global policy commitment. The extreme end of the tail may thus be more likely than in a normal distribution – where the probability of an event outside two standard deviations is about 5%. While possible and perhaps probable, it is not clear whether transition risks will indeed have fat tails. visualizes the joint impact of a skew and fat tail on a distribution function.

Figure 2. Illustrative example of the normal and climate roadmap distribution. Source: Authors.

At the same time, what does appear apparent is that the 2°C event can be seen as extreme. It is on the lower end of the spectrum of climate roadmaps and far removed from the current business as usual – defined for example by the International Energy Agency as the ‘Current Policy Scenario’ associated with roughly 6°C global warming. What is thus possible is that financial markets collectively are willing to take risks associated with the 2°C transition in the vein of Prospect Theory. In other words, even if the probability of the tail event is not over-stated, its ramifications in models are under-stated as a result of the cognitive bias of market actors vis-à-vis these tail risks.

The discussion here in a way pre-empts the subsequent discussion in the next section on cognitive biases related to market actors’ actions, beyond models. It also has a place here however, insofar as financial market models may reflect this bias in two ways. First, inputs chosen in the analysis, for example, the scenarios around cash flows and so on tend to congregate around the mean or median assumption, in particular when it comes to climate transition questions.Footnote12 Second, the emphasis on single indicator outputs for example in discounted cash flow models highlights mean results without creating transparency around potential tail risks.

Appropriate at this stage then is the reference to a strand of literature that, while having its origin in the traditional classical and neoclassical economics, has been picked up by the market failure literature as well. This relates to the distinction between risk and uncertainty, a distinction first introduced in the economic debate by Frank Knight in 1921 and then further developed by Keynes in the General Theory (Citation1936).Footnote13 According to Knight (Citation1921, 19–20),

risk means in some cases a quantity susceptible of measurement, while at other times it is something distinctly not of this character [ … ] It will appear that a measurable uncertainty, or ‘risk’ proper, as we shall use the term, is so far different from an unmeasurable (sic!) one that it is not in effect an uncertainty at all. We shall accordingly restrict the term ‘uncertainty’ to cases of the non-quantitative type.

The idea of risk and uncertainty was particularly made relevant in the context of the financial sector by Minsky (Citation1992), who argued that the inability to quantify all future risk scenarios was one of the factors that led to financial crises. Simon (Citation1957) argued that uncertainty, unlike risk, implies that contingencies cannot be assigned probability distributions and hence cannot be fully insured against. This is particularly the case in future-oriented decisions such as investment. Thus economic agents might fall back on rules-of-thumbs. The key idea then is that, in the presence of both risk and uncertainty, investors may not be able to make optimal decisions.

Transition risk is likely to be particularly subject to this constraint. As outlined above, climate change models and associated roadmaps are highly complex and subject to a wide range of assumptions. Data to input models is not necessarily available or available at affordable costs to investors. Already quantifying the possibilities associated with each degree of warming is a particular challenge, which is also why the ‘fat tail’ assumption cannot be validated at this stage. In addition, even if these probabilities could be quantified, each degree of warming is associated with a range of different technological roadmaps, some emphasizing one technology over another. There are over a 100 different roadmaps (Caldecott, Tilbury, and Carey Citation2014). For example, given the potential deployment of carbon capture and storage, a range of different fossil-fuel production volumes can be linked to a specific climate outcome. All of these of course pre-supposes capacity to assess and quantify these challenges, which the bounded rationality literature suggests is lacking. There is no reason to believe climate literacy is particularly high among financial sector actors – given that climate change related risks do not involve a historical precedent at a sufficient scale – and thus relevant historical data – that would have formed part of the education of individuals working in financial markets and their ability to integrate these challenges into models.

4. Transition risks and economic agents

There are two key characteristics of the market failure literature on economic agents relevant from a transition risk perspective that fall outside the scope of models, namely the role of time-inconsistent preferences and the role of institutions. Each of these aspects will be discussed in turn and linked to the analysis of the expected characteristics of transition risks.

One of the main tenets of the rational choice theory in terms of utility-maximization is the time-consistency of preferences by economic agents – in other words a ‘no regret’ position at point t + 1 relative to their choices at point t.Footnote14 If this was not the case, utility would not be maximized inter-temporally. Mathematically, this can be described as individuals having an exponential discount function, implying that we discount the future at a steady rate.Footnote15 Most economic modelling and analysis has been founded on the premise that ‘we do not suppose time to be allowed for any alteration in the character or tastes of the man himself’ (Marshall Citation1967). ‘What is assumed is that consumers are fairly consistent in their tastes and actions – that they do not flail around in unpredictable ways, making themselves miserable by persistent errors of judgement or arithmetic’ (Samuelson Citation1937).

As crucial as this condition for the theory of utility-maximizing agents, as weak is its theoretical and empirical foundation. In practice, economic agents discounting usually resembles hyperbolic discount function (Thaler Citation1981; Laibson Citation1997).Footnote16 The hyperbolic discount function suggests economic agents have ‘present-biased preferences’, where the immediate future is discounted highly, but the long-term future progressively at a lower rate.

In terms of finance, this is important because it suggests that investors may not optimize inter-temporal returns.Footnote17 In the case of transition risks, inter-temporal inconsistency is particularly important because transition risks are likely to be long-term and thus heavily discounted over the short-term. Transition risks may thus be mispriced in the context of hyperbolic discount functions not because investors do not believe the risks will materialize, but that their financial impact is discounted. In the same vein, from a broader capital allocation perspective, this may also suggest more long-term pay offs from ‘climate-friendly’ investments may similarly be discounted. Discounting is obviously visible in financial risk models as well, although here the issue is probably the practice of extrapolating current trends rather than the discounting. Beyond models however, hyperbolic discount functions lead economic agents to ignore long-term trends. Thus even where models can integrate long-term risks, these are not considered by the economic agent because the cash flows associated with these events are discounted by the actors themselves. By extension, there is no incentive to engage in an exercise beyond extrapolation given that potential hits to long-term cash flows are not material to the economic agent.

There may be another reason long-term risks are not integrated and this relates to externalities and principal–agent problems. The discussion on market failures has thus far focused on whether agents are rational and maximize their utility. It is important to also address the other part of the equation highlighted in the beginning, namely the extent to which financial markets are informationally efficient, independent of the rational nature of actors. This other side of the literature focuses on questions of market design creating inefficiencies, notably through transaction costs, agency costs in the context of the principal–agent problem and asymmetric information, and externalities.Footnote18

Principal–agent problems describe a situation where both the incentives and the information of a principal (for example an owner of assets or a voter) and the agent (the asset manager or politician, respectively) are not aligned.Footnote19 Whereas the differences in incentives and interests for the two parties are likely to be a frequent (if not omnipresent) characteristic of these types of transactions, they become problematic in the context of asymmetric information, allowing the agent to capitalize on superior information to the principal.Footnote20 The associated costs of this information asymmetry are called ‘agency costs’ (Jensen and Meckling Citation1976).

Externalities in turn are ‘the cost or benefit that affects a party who did not choose to incur that cost or benefit’ (Buchanan and Craig Stubblebine Citation1962, 200). The presence of externalities will lead to prices that are sub-optimal as they do not integrate the full range of cost and benefits associated with an asset (Greenwald and Stiglitz Citation1986).

The externalities associated with climate and the environment are usually referred to as the ‘tragedy of the commons’, after a seminal essay of the same name published by Garret Hardin in Citation1968. Interestingly, the analysis of externalities usually does not distinguish between inter-temporal externalities, where the affected party is somebody in the future and geographic externalities, where the affected party is in the same geography (analytically speaking). In terms of climate change, the question of externality has usually focused on the extent to which the costs of climate change are externalized by those who are responsible for it (Stern Citation2006).

Costs associated with climate change are socialized across the economy and will likely in some way impact all economic actors negatively, more or less.Footnote21 Costs associated with the transition to a low-carbon economy will be more focused however. These types of costs are likely to impact only a few sectors, industries or even just a select number of companies within industries. Similar to physical risks, these costs can also be externalized.

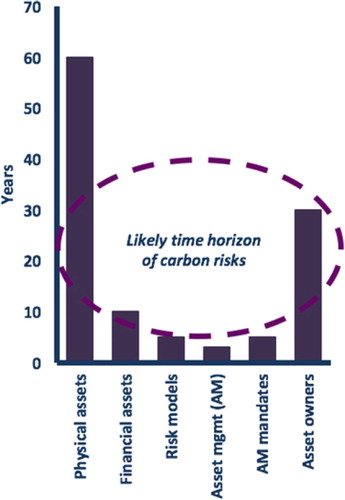

In financial markets, this may be the case in the presence of principal–agent problems. In such a scenario, short-term asset managers externalize long-term costs associated with their investments to asset owners. They are able to do this given the challenges around measuring long-term performance and risk of asset managers (WEF Citation2012). Asset managers may thus, even if financial models reveal long-term risks, ignore this risk as it is externalized to asset owners over the long-run – at some potential assumed short-term benefit. Part of this externalization happens in the models and use of data and thus can be linked to the first part of the discussion above. Even when these models are adjusted however, it does not respond to the principal–agent, externality, and time-inconsistency problem; this is the reason the discussion here focuses on the economic agent rather than the model itself. To reiterate, short-termism may be a problem in particular when discussing transition risks given the long-term nature of these risks ().

Figure 3. Illustrative time horizons across the investment chain. Source: Thomä, Dupré, and Chenet (Citation2014).

Beyond time horizons, institutions can also play a role for transition risk assessment in financial markets. The role of institutions is marginalized in the individual’s rational, utility-maximizing behaviour.Footnote22 The most obvious evidence for this lies in the fact that the actual preferences determining utility are treated as exogenous variables in neoclassical models (Savage Citation1950). According to North (Citation1993, 360), ‘history demonstrates that ideas, ideologies, myths, dogmas, and prejudices matter. [ … ] [Institutions] are made up of formal constraints (e.g. rules, laws, constitutions), and informal constraints (e.g. norms of behaviour, conventions, self-imposed codes of conduct), and their enforcement characteristics)’. Hence, the idea of an embedded economy: the economy functions in a specific social-historical context.

To the extent that rational choice theory acknowledges this, it is argued that rational individuals in the context of competitive market ensures the formation of efficient institution (i.e. minimizing transaction cost etc.), including incidentally cultural institutions.Footnote23 This ignores a number of behavioural elements however, notably path-dependency, where existing economic institutions are the contingent result of particular historical developments and therefore have no a priori claim to optimality or efficiency. Perhaps the most famous example in this regard is the QWERTY-keyboard, which is said to have been established for optimal typewriter typing (to avoid bunching of keys), but no longer being optimal for computers (David Citation1985).Footnote24 This has also been described as ‘evolutionary economics’ (Nelson and Winter Citation1982).

One important aspect to highlight in this regard is that institutions can create decision-making parameters that are ‘rational’ for the individual, but where the rationality is specific to the institutional context. For example, it is rational for asset managers to maximize short-term value given the institution of short-term remuneration to which that asset manager is subject to. It would naturally be irrational from a profit-maximization perspective to do the same if their remuneration was tied to more long-term performance and value.

The ‘atomism’ of the rational choice theory falls short in other respects as well, beyond a discussion of institutions. The key here is that individuals in a group will be confronted with a different utility function (and a different desire to satisfy that utility function) relative to being in isolation. Bikhchandani and Sharma (Citation2001) for example argues that herding behaviour partly explains booms and busts, where market participants exhibit ‘irrational exuberance’ and move as a crowd into a sector, overvalue their prices and ultimately move out, leading to a crash.Footnote25 It is better to be wrong in a group (Brennan and Li Citation2008).Footnote26

While it is difficult to find evidence on herding behaviour related to climate change, there is evidence that the transition to a low-carbon economy, despite success in recent years, is not fully on the radar screen of investors. The NGO Asset Owner Disclosure Project (AODP) finds that about half of all surveyed asset owners have a ‘no score’ on climate change issues and another 35% score a D.Footnote27 At the same time, other surveys (Mercer Citation2013; Novethic Citation2015) do identify action on climate change. Evidence is thus not unequivocal.

5. Conclusion

The previous section emphasized two ways the market failure literature influences risk management practices in financial markets. Section 3 focused on the insights financial market failure literature provides in terms of the assessment of the design of financial risk and valuation models. It then sought to show how these design features could create barriers to transition risk assessment, notably in their treatment of skewed, tail risks, and challenges around turning uncertainty into quantifiable risk. Section 4 then emphasized issues around the conduct of economic agents, notably the presence of time-inconsistent preferences, principal–agent problems and externalities. While these three features naturally also inform the design of models, they were identified as primarily as challenges in the market failure literature that related to the interpretation and use of models.

This study admits freely that the distinction between these two categories (i.e. models and economic agents) can be challenged, given the overlap and interplay between the two factors. At the same time, the key take-away from the review of the theoretical literature relates to the fact that transition risk assessment challenges may not be confined to the models. In other words, there is a case to be made that there is a mis-assessment of transition risks in financial markets and that this mis-assessment relates at least in part to the institutions around risk assessment. This suggests that solving this challenge requires not just better, smarter risk models, but in equal measure addressing key features of market design – notably the principal–agent problem and externalities – and potential ‘irrationality’ of market actors – notably their time-inconsistent preferences.

To date, the narrative and literature on transition risks has primarily focused on the issue of models. A review by Chenet, Thomä, and Janci (Citation2015) identifies over 30 different reports integrating transition risk into traditional financial market models and risk assessment. Many of these models address the key challenges defined in Section 3, notably the use of tail-end scenario assumptions and addressing issues around uncertainty. While they do not necessarily challenge the models themselves, they show that these models can capture transition risks. These models also at least in part tackle questions explored in Section 4, notably in the form of looking at more long-term time horizons or bringing events forward to today, visible in the work of Mercer and Profundo for the Green European Foundation (Chenet, Thomä, and Janci 2015).

This work however is only starting to address the structural challenges. Notable examples in this regard are research by Caldecott, derricks, and Mitchell (Citation2015) on investment consultants and a new research initiative by the 2° Investing Initiative on the ‘Tragedy of the horizons’. There are other examples in this space, for example the UK initiative ‘Preventable Suprises’. Key open questions remain, namely whether the way forward is an ‘integration’ approach, where these risks are integrated into traditional models to improve pricing, or a ‘stress-test’ approach where financial market actors use traditional risk tools for ‘business-as-usual’ assumptions, but are shown potential downside risks and resilience implications under extreme scenarios through models utilizing long-term scenario analysis. The way forward here will require further research. To date, the discussion on what approach works best has been limited.

The discussion here involved a theoretical discourse designed to inform research work on the question of the potential mispricing of transition risks. It is worth reiterating that the authors do not provide evidence as to the scale or materiality of these risks in and of themselves. Rather, the vantage point of the paper is on how, if these risks do exist, one could assume for them to be properly priced, based on the large theoretical literature on asset mispricing. It thus equally does not contend that transition risks deserve more or less attention than other risks, from a pure financial perspective. Rather, it suggests that mispricing of these risks, if they occur, are particularly damaging versus other types of risks because of the dual negative impact highlighted in the introduction, that is both the inefficient allocation of capital from a financial perspective and the associated potential increased costs of the transition to a low-carbon economy, which implies capital misallocation from a social perspective.

While the methodological design in terms of focusing on a theoretical analysis versus quantitative tools limits the explanatory power, the analysis does point to a few key conclusions.

First, the particular characteristic of transition risks suggest that they are susceptible to market failure. This relates to the likelihood that these risks are likely to be long-term, non-normally distributed, tail-end risks. There is thus reason to believe that an intervention may be needed from long-term asset owners and/ or regulators likely exposed to the potential capital misallocation associated with this market failure. Naturally, taking a more societal view, this call for action also appears justified given the global objective of limiting global warming to 2°C and the role investments play in realizing this objective.

It should be noted that, perhaps obviously, the toolbox of financial analysis may in itself provide some of the solutions to the problems described in this paper. This relates notably to the Real Options analysis or valuation, which allows investors to price options related to actual physical investment decisions and potential adverse impacts under various socio-economic scenarios.

At the same time, their long-term nature also suggests that there are institutional barriers linked to economic agents. Responses thus should not be limited to a focus on design of models and potential linked activities around risk transparency, for example in the form of expanded disclosure, but also address the broader institutional barriers – in effect, in the words of Carney (Citation2015), responding to the ‘tragedy of time horizons’ that grips climate change more generally.

Acknowledgements

The authors would like to acknowledge the inputs of Didier Janci and Catherine Karyotis to this paper.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1. These types of risks should be distinguished from physical risks associated with climate change itself (e.g. droughts, floods, storms etc.). This paper also does not cover legal risks. It thus only focuses on one of the three risks first identified in the taxonomy developed by Dupre and Chenet (Citation2013) and since then picked up by the Financial Stability Board (Citation2015).

2. Although Fama and Samuelson introduced the term to today’s economic discourse, modern economics now traces the origins of the efficient market hypothesis to the Ph.D. of Louis Bachelier and the idea of a ‘random walk’ of financial markets (Citation1900).

3. Fama in fact differentiated between weak, semi-strong and strong efficiency, a distinction, while relevant in general, is not relevant for the review in this study.

4. Interestingly, contrary to popular belief, not all of the Classical economists relied on this assumption, Ricardo being a notable exception.

5. Despite the apparent worship of the economic man, this man is treated with some ambivalence, like Frankenstein, who rejected his own monster. The political economist Fukuyama (Citation1992, 314) thus concluded that ‘the life of rational consumption is [ … ] in the end, boring.’

6. Related to this concept is the idea of ‘selective rationality’, articulated by Leibenstein (Citation1966) in the context of his work on ‘x-efficiency’.

7. This is not to be confused with agents not integrating all information as a result of costs. Here, allocative efficiency according to the rational actor still exists because the costs associated with the acquisition of information are seen to be higher than the associated benefits. In the scenario presented here however, actors do not integrate all information, even if this is profitable because they do not seek maximum profits. The distinction will be revisited later.

8. A scenario could be envisioned where agent satisficing has an equal effect on all financial assets and thus not lead to a skewing of prices. While possible, the ‘zero error’ hypothesis seems unlikely given that there is no good reason why an unconstrained decision-making process should have a distribution with a mean of zero. Such a scenario, while worthy of further research, will not be explored in further detail in this paper.

9. See for example a review by Alloway (Citation2012) in the Financial Times, although this review simply caveats that normal distribution is not always the norm.

10. Haldane and Nelson (Citation2012) provides a review of the history of normal distribution in financial market models, from which this paper borrows heavily.

11. See for example Pidcock (Citation2012) and Iacurci (Citation2014).

12. These assumptions may be more diverse in the case of economic stress-tests now part of the standard toolbox of regulators.

13. Knight arguably holds the economists crown for under-statement, in particular in hindsight, by beginning the book with the line: ‘There is little that is fundamentally new in this book’ (Knight Citation1921, vii).

14. Of course, rational choice theory does not assume we do not regret our decisions given 20/20 hindsight. Rather, it assumes that we do not disagree with our ‘former’ self’s decision, given the information set available at the time the decision was made.

15. While the discussion here focuses on the market failure associated with time-inconsistency in terms of allocative efficiency, the same problem obviously persists for policy, where it is more frequently labelled the dynamic-inconsistency problem (Kydland and Prescott Citation1977; Barro 1983).

16. While the hyperbolic discount function has achieved popularity with the rise of behavioural economics, the notion of time-inconsistent preferences is obviously not new and can be, at least in the field of economics, traced back to Smith and Hume (Palacios-Huerta Citation2003).

17. Hyperbolic discount functions may be rational from an individual’s perspective. If long-term paybacks are more uncertain, for example due to trust issues or external uncertainties, it may be rational to prefer a short-term payoff. Uncertainty may also exist about the ability to capture that payoff, particularly in finance. Equally, uncertainty is only one factor in explaining the hyperbolic discount function. Moreover, uncertainty is not an exogenous variable, but will be a function of a range of endogenous factors.

18. A range of other factors have been purposefully excluded in this debate, notably the presence of incomplete markets (Magill and Quinzii Citation1996), the literature on transaction costs (Coase Citation1937; Dahlman Citation1979) and the role of power in determining prices (Bowles Citation1985). While other factors may also play a role, the discussion is limited to these factors that seem immediately material for the questions around transition risk. Other factors which may prove to be equally material over time, were excluded however at this point, given the lack of immediately obvious link.

19. The term ‘Principal’ and ‘Agent’ have their origin in law, where it refers to two parties of a contractual agreement.

20. The concept of information asymmetry has been developed most prominently by Akerlof (Citation1970), who won the 2001 Nobel Prize in Economics for his work in this field.

21. That is not to say all economic actors will face the same costs, nor that all geographies will be affected the same. Rather, that some economy-wide costs at global scale and across most countries will affect most actors in some way.

22. Institutions in this study are understood in the political economy tradition (North Citation1993).

23. The origin of this analysis is with Coase (Citation1960), who applied this logic to law, where modern common law is frequently said to be driven by economic ‘efficiency’ considerations, as opposed to ‘natural rights’ considerations. See also Medema (Citation2010).

24. It is an open question as to whether other keyboards would be more optimal in terms of typing on a computer. In any event, however, the legacy of the QWERTY-keyboard, having established its pre-dominance largely independent of efficiency considerations, cannot be denied.

25. Keynes (Citation1936) famously called the financial markets ‘a beauty contest’.

26. Much of the literature here is inspired by Mackay (Citation1841)

27. The AODP ranks based on credit ratings from AAA to D and an ‘X’ for when no evidence/response was identified.

References

- Aghion, P., C. Hepburn, A. Teytelboym, and D. Zenghelis. 2014. “Path-dependency, Innovation and the Economics of Climate Change.” New Climate Economy Report: The Global Commission on the Economy and Climate.

- Akerlof, George A. 1970. “The Market for ‘Lemons’: Quality Uncertainty and the Market Mechanism.” Quarterly Journal of Economics 84 (3): 488–500. http://socsci2.ucsd.edu/~aronatas/project/academic/Akerlof%20on%20Lemons.pdf. doi: 10.2307/1879431

- Alloway, Tracy. 2012. “Modelling: Normal Distribution Is Not Always the Norm.” Financial Times Online, April 13.

- Bachelier, Louis. 1900. “La Théorie de la Speculation.” Annales scientifiques de l’E'cole Normale Superieure 3 (17): 21–86.

- Bator, Francis M. 1958. “The Anatomy of Market Failure.” The Quarterly Journal of Economics 72 (3): 351–379. doi: 10.2307/1882231

- Bikhchandani, Sushil, and Sunil Sharma. 2001. “Herd Behavior in Financial Markets.” IMF Staff Papers 47 (3): 279–310.

- Bowles, S. 1985. “The Production Process in a Competitive Economy: Walrasian, Neo-Hobbesian, and Marxian Models.” American Economic Review 75: 16–36.

- Brennan, Michael J., and Feifei Li. 2008. “Agency and Asset Pricing.” UCLA Finance Working Papers.

- Buchanan, James, and W. M. Craig Stubblebine. 1962. “Externality.” Economica 29 (116): 371–384. doi: 10.2307/2551386

- Caldecott, Ben, Gerard derricks, and James Mitchell. 2015. “Stranded Assets and Subcritical Coal: The Risk to Companies and Investors.” Oxford University Smith School of Enterprise and the Environment Stranded Assets Programme Working Paper.

- Caldecott, Ben, Lucas Kruitwagen, Gerard Dericks, Daniel Tulloch, Irem Kok, and James Mitchell. 2016. “Stranded Assets and Thermal Coal: An Analysis of Environment-related Risk Exposure.” Oxford University Smith School of Enterprise and the Environment Stranded Assets Programme Report.

- Caldecott, Ben, James Tilbury, and Christian Carey. 2014. “Stranded Assets and Scenarios.” Oxford University Smith School of Enterprise and the Environment Stranded Assets Programme Discussion Paper.

- Carney, Mark. 2015. “Breaking the Tragedy of the Horizon – Climate Change and Financial Stability.” Speech given at Lloyd’s of London, September 29.

- Chenet, Hugues, Jakob Thomä, and Didier Janci. 2015. “Financial Risk and the Transition to a Low-Carbon Economy: Towards a Carbon Stress-testing Framework.” 2° Investing Initiative / UNEP Inquiry Working Paper.

- Coase, Ronald. 1937. “The Nature of the Firm.” Economica 4 (16): 386–405. doi: 10.1111/j.1468-0335.1937.tb00002.x

- Coase, R. H. 1960. “The Problem of Social Cost.” The Journal of Law and Economics III: 1–44. doi: 10.1086/466560

- Dahlman, Carl J. 1979. “The Problem of Externality.” Journal of Law and Economics 22 (1): 141–162. doi: 10.1086/466936

- David, Paul. 1985. “Clio and the Economics of QWERTY.” American Economic Review 75 (2): 332–337.

- Dupre, Stanislas, and Hugues Chenet. 2013. “Landscaping Carbon Risk for Financial Intermediaries” 2° Investing Initiative Working Paper. Accessed July 9, 2016. http://2degrees-investing.org/IMG/pdf/landscaping_carbon_risk_website.pdf.

- Fama, Eugene. 1970. “Efficient Capital Markets: A Review of Theory and Empirical Work.” Journal of Finance 25 (2): 383–417. doi: 10.2307/2325486

- Financial Stability Board. 2015. “Task Force on Climate-Related Financial Disclosures.”

- Fukuyama. 1992. End of History and the Last Man. New York: First Free Press.

- Fulton, Mark, James Leaton, Paul Spedding, Andrew Grant, Reid Capalino, Luke Sussams, and Margherita Gagliardi. 2015. “The $2 Trillion Stranded Assets Danger Zone: How Fossil Fuel Firms Risk Destroying Investor Returns.”

- Greenwald, Bruce, and Joseph E. Stiglitz. 1986. Externalities in Economies with Imperfect Information and Incomplete Markets. Quarterly Journal of Economics 101 (2): 229–264. http://qje.oxfordjournals.org/content/101/2/229.short. doi: 10.2307/1891114

- Haldane, Andrew, and Benjamin Nelson. 2012. “Tails of the Unexpected.” Speech given at “The Credit Crisis Five Years On: Unpacking the Crisis.” conference held at the University of Edinburgh Business School, June 8–9.

- Hardin, Garett. 1968. “The Tragedy of the Commons.” Sciences 162 (3859): 1243–1248. doi: 10.1126/science.162.3859.1243

- Iacurci, Jenna. 2014. “Global Warming Goal of 2 Degrees Dwindling.” Nature World News, September 22. Accessed November 11, 2015. http://www.natureworldnews.com/articles/9139/20140922/global-warming-goal-of-2-degrees-dwindling.htm.

- Jensen, Michael C. 1978. “Some Anomalous Evidence Regarding Market Efficiency.” Journal of Financial Economics 6 (2): 95–101. doi: 10.1016/0304-405X(78)90025-9

- Jensen, Michael C., and William H. Meckling. 1976. “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure.” Journal of Financial Economics 3 (4): 305–360. doi: 10.1016/0304-405X(76)90026-X

- Jones, Steven, and Jeffrey M. Netter. 2014. “Efficient Capital Markets.” Library of Economics and Liberty.

- Kahnemman, Daniel, and Amos Tsversky. 1979. “Prospect Theory: An Analysis of Decision Under Risk.” Econometrica 47 (2): 263–292. doi: 10.2307/1914185

- Keynes, John Maynard. 1936. The General Theory of Employment, Interest and Money. Cambridge: Macmillan University Press.

- Knight, Frank. 1921. Risk, Uncertainty, and Profit. Boston, MA: Hart, Schaffner and Marx.

- Krugman, Paul. 2009. “How Did Economists Get It so Wrong?” NY Times, September 6.

- Kydland, F. E., and E. C. Prescott. 1977. “Rules Rather than Discretion: The Inconsistency of Optimal Plans.” Journal of Political Economy 85 (3): 473–491. doi: 10.1086/260580

- Laibson, David. 1997. “Golden Eggs and Hyperbolic Discounting.” Quarterly Journal of Economics 112 (2): 443–478. doi: 10.1162/003355397555253

- Lancet. 2015. “Health and Climate Change: Policy Responses to Protect Public Health.” 2015 Lancet Commission on Health and Climate Change.

- Leaton, James. 2013. “Unburnable Carbon 2013: Wasted Capital and Stranded Assets.” Carbon Tracker Initiative report.

- Leibenstein, Harvey. 1966. “Allocative Efficiency vs. ‘X-Efficiency’.” The American Economic Review 56 (3): 392–415.

- Mackay, Charles. 1841. Memoirs of Extraordinary Popular Delusions and the Madness of Crowds. London: Richard Bentley. https://vantagepointtrading.com/wp-content/uploads/2010/05/Charles_Mackay-Extraordinary_Popular_Delusions_and_the_Madness_of_Crowds.pdf.

- Magill, Michael J. P., and Martine Quinzii. 1996. Theory of Incomplete Markets. Vol. I. Cambridge: MIT Press.

- Markowitz, H. M. 1952. “Portfolio Selection.” Journal of Finance 7 (1): 77–91.

- Marshall, Alfred. 1967. Principles of Economics. London: Macmillan for the Royal Economic Society.

- McGlade, Christophe, and Paul Ekins. 2015. “The Geographical Distribution of Fossil Fuels Unused When Limiting Global Warming to 2°C.” Nature 517: 187–190. doi: 10.1038/nature14016

- Medema, Steven. 2010. The Hesitant Hand: Taming Self-interest in the History of Economic Ideas. Princeton, NJ: Princteon University Press.

- Meinshausen, M., N. Meinshausen, W. Hare, S. C. B. Raper, K. Frieler, R. Knutti, D. J. Frame, and M. R. Allen. 2009. “Greenhouse-gas Emission Targets for Limiting Global Warming to 2°C.” Nature 458: 1158–1162. doi: 10.1038/nature08017

- Mercer. 2013. “Global Investor Survey on Climate Change.” 3rd Annual Report on Actions and Progress – Commissioned by the networks of the global investor coalition on climate change.

- Mercer. 2015. “Investing in a Time of Climate Change.” Mercer report.

- Mill, Jon Stuart. 1844. Essays on Some Unsettled Questions of Political Economy. London: Longmans, Green, Reader and Dyer.

- Minsky, Hyman. 1992. “The Financial Instability Hypothesis.” Levy Economics Institute of Bard College Working Paper No. 74.

- Nelson, Richard, and Sidney G. Winter. 1982. An Evolutionary Theory of Economic Change. Harvard: Harvard University Press.

- North, Douglass. 1993. “Economic Performance through Time.” Nobel Prize Lecture 1993.

- Novethic. 2015. “Responsible Investors Acting on Climate Change.” Novethic report.

- Ong, Li. 2014. A Guide to IMF Stress Testing: Methods and Models. Washington, DC: International Monetary Fund.

- Palacios-Huerta, Ignacio. 2003. “Time-inconsistent Preferences in Adam Smith and David Hume.” History of Political Economy 35 (2): 241–268. doi: 10.1215/00182702-35-2-241

- Pidcock, Roz. 2012. “Can We Still Limit Warming to Two Degrees?” Carbon Brief, December 12.

- PWC. 2014. “Asset Management in 2020: A Brave New World.” PWC report.

- Robbins, Lionel. 1938. “Interpersonal Comparison of Utility: A Comment.” The Economic Journal 48 (192): 635–641. doi: 10.2307/2225051

- Robins, Nick, Wai-Shin Chan, and Zoe Knight. 2012. “Coal and Carbon.” HSCB investor report.

- Samuelson, Paul. 1937. “A Note on Measurement of Utility.” Review of Economic Studies 4: 155–161. doi: 10.2307/2967612

- Samuelson, Paul. 1965. “Proof that Properly Anticipated Prices Fluctuate Randomly.” Industrial Management Review 6 (2): 41–49.

- Savage, L. J. 1950. The Foundations of Statistics. New York: Wiley Press.

- Sharpe, William F. 1964. “Capital Asset Prices: A Theory of Market Equilibrium under the Conditions of Risk.” The Journal of Finance 19 (3): 425–442.

- Simon, Herbert. 1957. Models of Man: Social and Rational. New York: John Wiley and Sons.

- Smith, Adam. 1776. An Inquiry into the Nature and Causes of the Wealth of Nations. London: Methuen.

- Stern, Nicholas. 2006. “What is the Economics of Climate Change?” World Economics 7 (2): 1–10.

- Taleb, Nassim. 2007. Black Swans: The Impact of the Highly Improbable. New York: Random House Publishing Group.

- Thaler, R. H. 1981. “Some Empirical Evidence on Dynamic Inconsistency.” Economic Letters 8 (3): 201–207. doi: 10.1016/0165-1765(81)90067-7

- Thomä, Jakob, Stan Dupré, and Hugues Chenet. 2014. “The Turtle becomes the Hare: Short-termism in Financial Markets.” 2° Investing Initiative Working Paper.

- Tobin, J. 1958. “Liquidity Preferences as Behavior Towards Risk.” Review of Economic Studies 25 (2): 65–86. doi: 10.2307/2296205

- Tsversky, Amos, and Craig R. Fox. 1995. “Ambiguity Aversion and Comparative Ignorance.” The Quarterly Journal of Economics 110 (3): 585–603. doi: 10.2307/2946693

- WEF (World Economic Forum). 2012. “Measurement, Governance and Long-Term Investing.” World Economic Forum report.