Abstract

Private companies and investors can profit from the enhancement of nature in general and from specific investments allocated to improve biodiversity and ecosystem services (BES). The question is: What is the incentive, from a private sector point of view, to invest in nature, and what are the barriers and opportunities? This article demonstrates that new markets and business models are developing which are based on BES, thereby offering investment opportunities and contributing to nature conservation at the same time. Emerging BES markets include (i) sustainable forestry; (ii) ecotourism; (iii) carbon sequestration through forestry, agricultural projects and REDD (Reducing Emissions through Deforestation and Forest Degradation); (iv) watershed management; and (v) nature conservation and restoration such as wetland banking and biodiversity offset programmes. This article gives an analysis of the various business models and the factors that support a proper functioning thereof, including the dependence on public regulation and the necessity to collaborate with local communities, authorities, NGOs or other stakeholders. In the analysis, barriers for attracting mainstream capital from institutional investors into ‘BES business’ are identified and addressed.

Introduction

Biodiversity loss is a reality of the twenty-first century. The fight against biodiversity loss has become a priority for governments and nature conservation organisations worldwide. However, despite the fact that most states are a party to the Convention on Biological Diversity (CBD) and the Convention on International Trade in Endangered Species of Wild Fauna and Flora (CITES), their efforts have proved to be insufficient. Apparently, not only governments and environmentalists need to be engaged, but the private sector also appears to be a key player. Activities of companies have an immense impact on nature, that is, on the state of the world's biodiversity and ecosystems. Consequently, it would make a substantial difference if companies were to reduce their negative impacts and contribute to the restoration and conservation of the natural world. This ambition has been set out in many of the mainstream private regulatory regimes in the field of corporate social responsibility (CSR) and socially responsible investment (SRI).Footnote 1 The view that business and society share a joint responsibility for the conservation of biodiversity (B) and manage the use of ecosystem services (ES) in such a way that they can supply services on a sustainable basis is widely supported. For example, the EU has commissioned an extensive study on the value of biodiversity and ecosystem services (BES) that consists of different reports: The Economics of Ecosystem and Biodiversity (TEEB) Interim Report (TEEB Citation2008); TEEB Climate Issues Update (TEEB Citation2009a); TEEB for National and International Policy Makers (TEEB Citation2009b); TEEB Ecological and Economic Foundations (TEEB Citation2010b); and TEEB for Business (TEEB Citation2010a). Furthermore, the year 2010 was designated by the UN as the ‘International Biodiversity Year’ (UN General Assembly 2010) and the Nagoya Protocol to the CBD was adopted in 2010.

Besides impacting the ecological balance, companies also depend on ES for the continuity of raw material supplies and for regulatory services. ‘Ecological balance’ refers to ‘the state of dynamic equilibrium within a community of organisms in which genetic, species and ecosystem diversity remain relatively stable, subject to gradual changes through natural succession’. Hence, it considers both biodiversity and ecosystems as ecosystems (Boreal Forest Citation2011). This dependency of business will be explained in more detail later in the paper. The decline of quality and/or quantity of ecosystems impacts businesses and their investments in a negative way. It would thus seem logical for the private sector to invest in the conservation of nature. However, the dilemma is that the contribution of a single private sector participant to nature conservation in general will not help this company or investor directly. And as most business operations are set up to make a financial profit for themselves, the question is: What is the incentive from a private point of view to invest in nature?

In this article, we shed light on new business models that contribute to biodiversity and operate on a commercial basis (pro-biodiversity business). In particular, we analyse to what extent such models depend on government regulation or involvement. We describe the methodology of the research project that formed the basis for this article. Next, we provide background information on the various links between business and biodiversity, from both the entrepreneur and the investor perspective. Following that, we will present results and findings of the research project. We will elaborate on two pro-biodiversity business models: sustainable forestry and ecotourism. We will also present another approach, that is, to build a business case on the concept of ‘paying for ecosystem services’ (PES), such as water. We will evaluate which factors support private sector investment in BES. Finally, we point out common barriers for investors and entrepreneurs engaged in pro-biodiversity business.

Methodology

We conducted an empirical research project in which the question how the private sector can be encouraged to invest in biodiversity was the focal point. The original study was conducted in 2009 by the Center for Sustainability (CfS) of Nyenrode Business University (Citation2010) in collaboration with the International Union for the Conservation of Nature – Netherlands Committee (Citation2004); the European Centre for Nature Conservation (ECNC); the Dutch institutional investor APG; and financed by the Dutch Department for Environmental Affairs (http://www.nyenrode.nl/biodiversityfinance). Subsequently, CfS has performed two follow-up studies in this field in 2010 and 2011. To the extent that the information obtained in those studies did not support the results of the original study, this article has been updated to reflect the most recent insights (for more information on the CfS ongoing research in the area of investing in sustainable forestry and forest carbon, see the following link: http://www.nyenrode.nl/FacultyResearch/LSE/CS/Pages/Default.aspx).

The methodology of the original research project consisted of first conducting desk research and interviews in order to compile a database of pro-biodiversity business projects and investment funds in various parts of the world. Next, a number of large European investors were interviewed regarding their appetite to invest in these types of funds. Subsequently, an international working conference was organised in which a number of such pro-biodiversity business projects and investors participated. The purpose of the conference was twofold: (i) to bring project managers and investors into contact with each other; and (ii) to analyse – together with the pro-biodiversity business managers, investors, various nature conservation NGOs and public regulators – which barriers may keep investors from investing in pro-biodiversity business and what solutions can be found.

In this study, ‘pro-biodiversity business’ was defined as business projects aimed to contribute to biodiversity and a sustainable use of ecosystems services, with the objective to be financially profitable. Under ‘ecological health’, both the occurrence of certain attributes that are deemed to be present in a healthy, sustainable resource and the absence of conditions that result from known stresses or problems affecting the resource are understood (Boreal Forest 2011). In compiling the data base of pro-biodiversity business projects, the IUCN-NL representatives evaluated whether a particular project was capable of making a positive contribution to BES. The Nyenrode Business School representatives, among which the authors, considered whether a project was suitable and ready for private sector investment. The resulting collection of 35 projects was contacted for in-depth research. A number of them were invited to present themselves to investors in the working conference. In their presentations, it became apparent that the incorporators and/or the managers of the selected projects had a strong personal motivation to restore or conserve nature. They clearly wished to realise that ambition through setting up an economically viable business model.

The innovative way of performing this study, which included desk research as well as action research together with the pertinent business actors and regulators, assisted the authors in analysing which incentives can stimulate private actors to invest in nature, which pro-biodiversity business models are developing today and to what extent they rely on government interference.

Background information on the links between the private sector and the protection of biodiversity

First, it is essential to define BES and to understand in which way the business sector and investors interact with BES. ‘Biodiversity’ is a central element of sustainable development that affects the life of every living organism on the earth. It is a term used to describe a variety of genetically distinct populations within species and the natural communities and ecosystems of which they are a part (United Nations Convention on Biological Diversity Citation1993). ‘Ecosystems’ are defined as ‘a dynamic complex of plant, animal and micro-organism communities and their non-living environment interacting as a functional unit’ (United Nations Convention on Biological Diversity 1993). An ecosystem can be of any size – a log, pond, field, forest or the Earth's biosphere – but it always functions as a whole unit. Ecosystems deliver the so-called ES, which are ‘the benefits that people obtain from ecosystems. Examples include food, freshwater, timber, climate regulation, protection from natural hazards’ (TEEB 2008). A ‘sustainable ecosystem’ is a system that survives, functions and is renewed over time; a system in which people can continue to live and flourish for many generations.

The decline in the quality and/or quantity of BES undermines the richness and variety of species and therewith the functioning of ecosystems. This can have a significant impact on the private sector, because companies depend on BES for the provision of water and raw materials (Fauna and Flora International Citation2008; Grigg, Cullen, Foxall et al. Citation2009; Grigg, Cullen, Foxall, Strumpf Citation2009). Business also contributes to the change in BES, that is, (i) negatively due to the impact of their economic activities on BES and (ii) positively when they engage in pro-biodiversity business (UNEP FI 2008).

Business activities and BES

With regard to the dependence of business on BES, it is still difficult to concretely quantify the financial link between ES and companies. The EU TEEB studies are working on defining the value of BES (Economics of Ecosystem and Biodiversity 2010c), but mainly from a macroeconomic perspective. Research concerning the microeconomic perspective suggests that business profits and a good condition of biodiversity are often correlated (Tilman et al. Citation2006; Worm and Barbier Citation2006; Bishop et al. Citation2008), because (i) biologically diverse soils (i.e. the variability among living organisms in the soil – ranging from the myriad of invisible microbes, bacteria and fungi to the more familiar macro-fauna such as earthworms and termites (Scialabba Citation2010)) are generally more productive for agriculture; (ii) various tropical forests are the main locations in which to discover novel genes and compounds for agricultural, industrial and pharmaceutical uses; (iii) tourists prefer more diverse ecosystems; and (iv) marine biodiversity is associated with the increased productivity of fisheries (Naidoo and Adamowicz Citation2005; Millennium Ecosystem Assessment Citation2010). Concrete examples of the dependence of business on ES are, for instance, the Atlantic cod stocks fishery, which collapsed in 1992 after hundreds of years of exploitation. Coca-Cola, for example, has nearly 900 bottling plants around the world which depend on the availability of water to produce soft drinks (Coca-Cola Citation2006–2011). And ice cream producer Haagen-Dazs communicated in 2009 that nearly 50% of their all-natural super-premium flavours depend on bee pollination (www.haagen-dazs.com). Consequently, dependent on the sector, it is very likely that a company's activities depend on the sustainability and resilience of ecosystems. A decline thereof can threaten business opportunities and reduce profits (Vorosmarty and Leveque Citation2005; Fauna and Flora International 2008; Grigg, Cullen, Foxall, et al. Citation2009; Grigg, Cullen, Foxall, Strumpf Citation2009; Barcellos Harris Citation2010).

Besides the fact that many business activities are dependent on BES, companies can also impact BES. The negative impact has been described often: the transformation of natural areas into production areas or into industrial sites; the pollution of water, air and soil resulting from economic activities; and the hunt for animals for food, for example, fishing, and for rare species of flora and fauna. Climate change is an additional factor that threatens the continued existence of BES. However, companies can also have a positive impact on nature as will be demonstrated in the following sections.

An additional factor in the relation between companies and BES is the reputation of a company. The reputation of a company is often influenced by its attitude towards biodiversity and the environment in general (EU Initiative 2007). Being good for nature can uplift the reputation of a company and put it in a better position (Covalence Citation2008). Furthermore, as a developing trend, companies risk being delisted by supermarket chains and boycotted by consumers in case of unsustainable production methods (Eurosif Citation2009).

Investment activities and BES

The importance of the continued existence of ES for business also implies that investors are dependent thereon for a positive return on investment. An institutional investor is an entity, such as pension fund or insurance company, that pools a large amount of money which they invest into the companies. They typically adopt a mid- or long-term investment strategy. This approach seems compatible with the pro-biodiversity business models that typically also build their business case on a long-term strategy. In particular, when an institutional investor strives for a diversification of its investments in order to minimise the risk of losing invested capital in the long term, it would be prudent for it not only to invest in business activities that negatively impact BES, but also to invest in companies and funds that positively impact BES. Only in that way, the institutional investor can contribute to restoring the (global) ecological balance. This is important for an investor as sustainable ecosystems are ultimately relevant to many industries as they rely on the continued supply of ES.

Furthermore, the current capital market trends indicate that the acknowledgement of the importance of BES is growing. Capital markets show signs of becoming aware of sustainability issues. Over 600 of the world's largest asset owners and asset managers, responsible for investments exceeding in total USD 19 trillion in 2009, have endorsed the Principles for Responsible Investment (PRI Citation2010), thereby communicating their ambition to pay more attention to the environmental (E) and social behaviour (S) of the companies in which they invest and to address governance issues (‘G’, together ‘ESG’). The ‘E’ includes BES. Another sign is that various stock exchanges and other institutions have established sustainability indices, such as the Dow Jones Sustainability Indices, FTSE4GOOD, Domini 400 Social Index and ETHIBEL (UNEP FI, AMWG, UK SIF, SPP 2007). According to a recent study of the UN Global Compact and Accenture, 86% of CEO's globally are calling on investors to price the sustainability element in their valuations in a better way. CEO's are encouraging the investors to move capital markets ‘towards something of a sustainability “tipping point” where companies are fully rewarded for their sustainability efforts’ (Lacy et al. Citation2010). Another survey showed that more than 70% of the institutional investors in the Netherlands, France and the United Kingdom believed it to be their responsibility as a shareholder to pay attention to the ESG policies of a company in which they invest (Novethic Citation2009). Although this sounds promising, another survey, however, showed that only a few investors rank biodiversity conservation as a main concern (Thomson Extel and UKSif Citation2006). Reasons are that investors seem to have little knowledge of investment possibilities linked to biodiversity and that there is a lack of understanding that ecosystem degradation and species loss are directly interlinked with the stability of ‘normal’ business activities.

Concluding this section, the interaction between the private sector and BES has received new attention. Whereas ‘the environment’ was long perceived by the business community as something only related to burdensome and restrictive environmental law regulations, this perception is now changing. Both business and investors realise that they need sustainable ecosystems. Moreover, it has been discovered that enhancing BES offers entrepreneurial and investment opportunities (Earthwatch et al. Citation2002; UNEP 2008). New markets are emerging, among others through the creation of new property rights, such as carbon emission rights and water rights. In the next sections, new business models that support conservation and a sustainable use of ecosystems services will be explored.

Results: (i) investing in forests and national parks

Despite certain scepticism regarding the profitability of investing in biodiversity, which will be addressed when analysing the various pro-biodiversity business models, the research project demonstrated that there are indications that private sector actors are willing to invest in the protection of habitats, thereby contributing to the conservation of biodiversity. So far, interesting business models for forestry management and eco-tourism projects have been developed.

Investing in forests

For biodiversity conservation, it is essential to protect the forests and to only harvest timber in a sustainable manner. Forest degradation and deforestation is a day-to-day occurrence. In particular, tropical rain forests are disappearing from the face of the earth with immense speed (Biodiversity Indicators Partnership Citation2010). In the short term, deforestation results in the loss of the ecological services including the reduced access to renewable resources, like medical plants and timber, and the loss of valuable rainforest services, such as water treatment and flood control (Dykstra and Henrich Citation1992, FAO Citation2009). Over the longer term, deforestation has an impact on climate and biodiversity. Although rainforests cover less than 2% of the planet's surface, they provide habitat for 50% of the variety of life on the planet (Nature Conservancy Citation2010). One of the ways to halt deforestation is to invest in forests.

Typically, the timber business concerns the logging of all trees in a certain area or, in the case of plantation forestry, it concerns the activity of planting a single fast growing species for production. A more difficult approach is to manage naturally growing ‘natural’ forests, consisting of many different species of trees, which forests are the home for a large number of other species too (biodiversity). This type of forestry requires more time to grow and more specialised knowledge concerning ecology. Other challenges often mentioned are: the lack of secured ownership or concession rights of the area, the uncertainty regarding use rights of others, a failing rule of law, especially in developing countries (Mulder Citation2007). However, despite the challenges, the sustainable forestry market is probably the most developed market of the pro-biodiversity business. In the research project, a number of sustainable forestry and reforestation projects have been characterised as positively impacting biodiversity as well as suitable for private investment.

Investments in the asset class of sustainable forestry have clearly become more popular over the past few years: the volumes have increased and the spectrum of investors has widened (Suria Citation2008). Not only direct investments, that is, in forestry funds, but also indirect investments are increasing in significance. An example of an indirect investment product is a forest-backed security (Forum for the Future Citation2009). The value of these securities relates to expected future profits from commercial forest activities. For example, in Brazil, the Environmental and Social Stock Exchange (BVS&A) was established aimed at bringing together NGOs that require funds and social investors willing to support their programmes (FAO Citation2008). Today, socially and green investment funds are an important source of private sector finance (Forest Policy Brief Citation2009).

The research project revealed that a sustainable forest manager makes financial returns by selling timber and wood products, generally certified. He can also sell non-timber forest products (NTFP), such as fibre for biofuels and nuts. In addition, he can make use of PES mechanisms for generating other types of returns, for example, selling water rights to downstream users. Furthermore, he can offer eco-tourism services and he can tap into the emerging markets for environmental credits for carbon and biodiversity offsets. Financial results thus come from a mix of income streams. Sustainable forestry projects can be set up in different organisational and legal forms. Two innovative business models will be briefly discussed below.

Sustainable forestry business model: timber and related products

Usually, a sustainable forestry fund can be described as an investment fund which focuses on sustainable forestry, including the planting and managing of natural forests, combined with forest-based carbon certificates.

There are various examples of how forestry funds can be organised. This article provides an example of an actual forestry fund (hereafter: “forestry fund”) and describes its structure. Due to the confidentiality considerations, expressed by the fund mangers, the name of the fund will not be disclosed. This forestry fund depicts an innovative setup of the fund structure and possible activities of such a business case. The forestry fund is a closed-end ‘Specialized Investment Fund’ (SIF) regulated by Commission de Surveillance du Secteur Financier (CSSF) in Luxembourg. The forestry fund invests in projects in Panama, Costa Rica and Argentina. The forestry fund is set up as is a joint venture between a forestry management company and an investment company. The fund structure is presented in

Figure 1. Structure and business organisation of an example forestry fund.

The business case of the forestry fund is based on revenues coming from a mix of activities – all sustainable timber projects – that generate income, including:

| - | timber concessions, which give the right to harvest (usually 20 years). Concessions require less capital than the purchase of forest. A mix of low initial investment and fast cash flow can result in attractive returns. The forestry fund commits to forest certification according to sustainability standards; | ||||

| - | natural grown forest, which provides fast financial returns, but requires more capital. The certified ownership of land offers more security and no time limits; | ||||

| - | avoided deforestation projects, revenues can be generated from the emerging market for forest-based carbon certificates. Appropriate schemes that are ‘REDD ready’ (i.e. Reducing Emissions through Deforestation and Forest Degradation) are being developed; and | ||||

| - | reforestation projects, long-term investments with negative cash flow in the first years. Revenues from sustainable forest management during the growth phase would secure a higher return in the longer run in comparison to natural forests or timber concessions. Other advantages are secured land ownership and potential capital appreciation of the forest and the land. | ||||

The communications claim that the success rate of the investment will be determined by the following factors: (i) the clear focus (Latin America); (ii) a substantial number of pipeline projects (volume > USD 500 million); (iii) high standards regarding biodiversity and sustainable forestry; and (iv) the combination of local ground forestry management experience and expertise in capital markets, private equity and portfolio management (Timber Opportunities Fund 2009).

The aim of the forestry fund is to protect tropical forests, to regenerate local forest with a variety of endemic species and to collaborate with the local communities in order to incentivise them to use forestry-based activities in a new and smart way in order to positively contribute to BES. In addition, the forestry fund combines the forestry activities with REDD projects for extra revenues.

Forest investment business model: biodiversity certificates

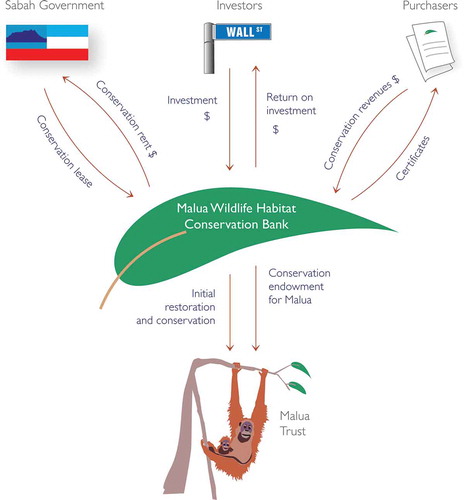

A different approach has been developed by ‘Malua Wildlife Habitat Conservation Bank’ (Citation2008) (Malua Biobank), which offers ‘Biodiversity Conservation Certificates’. The Malua Biobank was commenced as a public–private partnership. It combines forest conservation with efforts to protect wildlife and to restore natural forest. The resulting conservation benefits have been unitised for sale via biodiversity conservation certificates. It is an innovative project (New Forests Citation2008).

The organisational setup is as follows: Malua Biobank is an investment of the Eco Products Fund LP (EPF), a fund jointly managed by an Australian investment management firm, New Forests Pty Ltd (New Forests) and a New York-based investment firm, Equator LLC.

In 2007, the Sabah Government in Malaysia signed a ‘memorandum of understanding’ with New Forests to set up the Malua Biobank. The project aims at restoring and protecting the Malua Forest Reserve (Citation2008), home to some of the rarest species of animals, birds and plants, such as the orangutan. However, extensive logging has taken place in Malua in the past and palm oil plantations border some areas of the forest. Subsequently, EPF established the Malua Biobank via a partnership with the Sabah Government (Malua Forest Reserve 2008) (). Malua Biobank received its start capital from EPF to restore and to protect an area of 34,000 hectares of previously logged forest in the Malua Forest Reserve.

Figure 2. Structure of Malua Biobank (credit to Malua Wildlife Habitat Conservation Bank; see for an overview: http://www.maluabiobank.com/ and see for further information: www.newforest.com.au).

The Malua Biobank business model is as follows: (i) in 2007, the company that holds the concession licences to the Malua Forest Reserve (owned by the Sabah Government) had ceased all logging operations; (ii) EPF commited up to USD 10 million in Malua Biobank to protect and rehabilitate the Malua Forest Reserve. (iii) Malua Biobank has obtained the right to create, market and sell so-called ‘Biodiversity Conservation Certificates’ to parties that are interested in balancing or compensating their negative impacts on BES with positive impacts (e.g. cosmetics, energy and food companies, Malaysian companies; and palm oil growers and processors); each Certificate represents 100 square meters of rainforest restoration and protection; and (iv) the Malua Trust, which is managed by a bank (HSBC), is to manage the conservation of the forest over the remaining 44-year period of the license issued by the Malaysian government. The revenues from the sale of Biodiversity Conservation Certificates will be shared as follows: (i) an endowment will be made to Malua Trust to fund the long-term conservation management by Malua Biobank and; (ii) profits are to be shared between the Malua Biobank and the Sabah Government.

The aim of this inventive business model is to ‘translate’ rainforest protection into a market product so that biodiversity conservation can compete with other land uses on a commercial basis. In practice however, a bottleneck for Malua Biobank is market development. The expectation that companies (e.g. palm oil producers) will buy the Biodiversity Conservation Certificates on a voluntary basis still largely has to materialise.Footnote 2

To evaluate this, investments in sustainable forest management can assist public authorities in their strategies to reduce deforestation. The case studies show that a close collaboration between the private investors and the local communities and authorities is indispensable. Another precondition is a reliable investment environment, supported by the rule of law. In the example of Malua Biobank, the Sabah government has facilitated an effective regulatory environment for this business. Still, it appears to be a challenge to attract buyers for the Malua Biodiversity Certificates. It would help if Malua Biobank could rely on regulation stipulating mandatory biodiversity offsets. Management expects that there are potential opportunities for this to take place in the future.

Another observation is that investments in forestry and forests have a unique investment profile that aligns with the concerns of pension funds. Forestry by nature – like pension funds – have a long-term business profile. Moreover, it has been advocated that investing in sustainable forestry could be especially attractive for pension funds because of the strong physical asset backing in the form of land, standing timber and milling assets (Forum for the Future 2009).

However, even though an increased popularity can be observed,Footnote 3 it still appears difficult to attract substantial financing. In practice, asset managers who are tasked with investing the capital of pension funds, generally do not invest on the basis of long-term prospects but wish to see financial results as soon as possible. This is partly due to concerns related to receiving an annual bonus and partly due to the fact that asset managers often have a fixed-term contract with the pension fund which pushes for a short-term focus. Moreover, following the financial crisis, pension funds are generally encouraged or mandated by their national central bank or pension authorities to maintain ‘liquid’ investments, that is, which can be sold on a short-term notice.

Investing in national parks

Eco-tourism is a fast growing sector, with annual exports up to USD 100 billion (Bishop et al. Citation2008). Eco-tourism is a tool that can help to minimise the environmental effects of regular tourism (Gössling Citation1999). There is a direct link with biodiversity conservation. The collected revenues from visiting a protected areas can support its preservation. In addition, local communities can benefit from tourism by offering lodging, food, guiding and transportation to tourists. According to The International Ecotourism Society (TIES), eco-tourism can be defined as ‘responsible travel to natural areas that conserves the environment and improves the well-being of local people’ (International Ecotourism Society Citation2006). Eco-tourism can be considered an emerging market as more and more people wish to visit beautiful nature and habitats. It is concentrated in a small number of regions and facilities and depends on ‘caring’ consumers (United Nations World Tourism Organization Citation2011). Till recently, eco-tourism lagged behind, in comparison to other sectors, in establishing industry sustainability standards or certification schemes. However, the Tourism Sustainability Council, which was formed in 2009, has the potential to provide a global accreditation body for eco-tourism programmes that meet agreed standards (TEEB Citation2010c).

Ecotourism business case: adaptation of conservation activities to business reality

A novel approach of ecotourism is presented by the Pan (Protected Area Network) Parks Foundation (Pan Parks Foundation Citation2009). Pan Parks is an example of a fast growing semi-business enterprise, which focuses on protection of nature areas in the Eastern Europe, by developing nature parks attractive for tourists.

The organisational setup is as follows. Pan Parks is a joint creation of the nature conservation organisation WWF and the Dutch tourism company Molecaten B.V and was established in 1997. By 2011 it manages 11 projects. The main goal is to establish a network in which protected areas and businesses can work together to conserve nature and support local communities (Pan Parks Foundation 2009).

The business case works as follows. Pan Parks develops partnerships with the private sector and investors who wish to promote ecotourism with a focus on the European natural landscape. It allocates resources through the ‘Pan Parks Small Grants Fund’ to support ‘Certified Pan Parks’. Interesting elements of the Pan Parks concept are first that it has a WWF sub-branding which adds value from a business point of view. Second, Pan Parks follows the ‘wilderness management concept’, that is, an area can only qualify as a ‘protected area’ if it exceeds 10,000 hectares designated for untouched nature. Third, Pan Parks offers high-quality tourism which includes services provided by local business partners and expertise by NGOs. The idea is that the protected areas will stimulate tourism and therewith the business of local entrepreneurs. Pan Parks has begun to shift from a non-profit conservation organisation towards adopting a more business model structure.Footnote 4

To conclude this section, the network idea combined with the strategy to setup partnerships makes the business case innovative.Footnote 5 Collaboration with local communities and authorities is a crucial success factor. Putting this concept into practice requires good management skills and capacity to align all stakeholders. In addition, is a precondition that the legal and political framework provides for a reliable and economic investment environment. Pan Parks seems to be an example of a successful and enduring business case with an efficient structure, however, it also frequently faces the problem of obtaining permits from governments in the park areas.Footnote 6

Results: (ii) innovative finance models

Another way in which private sector parties are becoming more involved in investing in habitat conservation is the PES business model. PES represents a flexible compensation mechanism in which ES providers are compensated by service users (Katoomba Group et al. Citation2008). It concerns a new finance model. Over the last decade, we have seen various PES systems develop, such as paying for water management services, carbon sequestration, biodiversity conservation and landscape protection (Katoomba et al. 2008; Verweij and De Man Citation2002; Verweij Citation2004). Often, payments are bundled securing all or a combination of carbon, water and biodiversity services (Katoomba Group et al. 2008). Bundled payments also include those in which the ES payment is built into the price of the product, such as certified timber or certified products.

PES markets can be distinguished as: (i) compliance markets, that is, public regulation requires the payment for the use of ES (e.g. mandatory carbon emission trading for certain industries); (ii) government-mediated markets, that is, where the government is the intermediate party that collects payments from users and distributes them to the service providers (e.g. PES markets based on water services); and (iii) voluntary markets, that is, in which companies voluntarily decide to compensate their impact on BES by purchasing compensatory credits (e.g. voluntary carbon emission credits and biodiversity offsets as discussed above regarding the Malua Biobank) (Katoomba Group et al. 2008). After discussing the mandatory and voluntary carbon sequestration markets, two case studies involving the private sector in watershed management will be presented below. The first regards predominantly the volume of the water supply, the second concerns the quality of the water supply.

Financing carbon sequestration services

The global demand for carbon sequestration is motivated by the Kyoto Protocol (Kyoto Protocol Citation1997). The market for carbon sequestration services has two bases: legislationFootnote 7 and voluntary initiatives.

The legislative framework requires companies to reduce their carbon emissions to the level of the permits annually allocated to them (credits). If a company exceeds such levels, it has to buy additional carbon credits on the carbon credit market. Carbon credits can be created and obtained by completing projects that lead to a reduction of carbon emissions. The company that needs the credits can initiate such projects itself or, alternatively, can buy credits from another company that has generated credits. Both the regulated and the voluntary dimension of the market for carbon sequestration services can entail either a bilateral project-based transaction between the company-buyer and the carbon credit-producer, or the offset can take place through trading credits in a carbon sequestration market (Ashford et al. Citation2008).

The voluntary market for carbon sequestration develops between private parties on a voluntary basis (Hamilton et al. Citation2008). To exemplify, one of the voluntary systems in use is the Verified Carbon Standard ([VCS] Voluntary Carbon Standard Programme Citation2011), which is a greenhouse gas accounting programme used by projects around the world to verify and issue carbon credits in voluntary markets. Originally, VCS was initiated in 2005 by the Climate Group, the International Emissions Trading Association and the World Economic Forum. As forests and agriculture play an important role in carbon storage by storing carbon in plant matter and the soil, they can produce carbon credits. In 2008, VCS introduced a standardised approach for forestry and agriculture. REDD then became accessible to all market players (UN 2008–REDD Programme). Land use projects including forestry and agriculture can now be validated and verified against VCS. Noticeably, the voluntary carbon sequestration markets have been growing substantially in the past years, although it seems fair to say that these voluntary markets emerged alongside mandatory carbon sequestration markets, hence they profited from existing regulatory models. The overall market share, occupied by voluntary markets, is small and has to further be developed.

Financing watershed management services

A PES system can be set up to protect a watershed, that is, ‘the area of land where all the water that drains off goes into the same stream, lake or other water body’. Establishing a watershed payment system serves as a mechanism for protecting a lake, river or stream by managing the entire watershed that drains into it. Typically, it concerns financial mechanisms to compensate upstream landowners so as to maintain a certain land use in order to positively affect the quality and availability of the downstream water resources. For example, the upstream landowners can be paid to keep a forest intact, which can imply not to build roads or not to log trees. It can also concern a commitment to plant trees or perform other activities that have a positive impact on the quality and quantity of water (Kiersch et al. Citation2005). The farmers, water companies or power companies in a downstream area can then benefit from a continuous and regular supply of clean water. If the forest would be logged, the downstream users bear the risk of suffering from dirty water due to erosion, and from a less secure supply of water (no forest means less regular rainfall and less water; Carroll and Jenkins Citation2008).

PES systems vary; they can regard payments by private water users to environmental agencies and NGOs (which contribute to ensuring the watershed protection), and/or direct payments by the central or local government (which acts as user, provider or seller of the water) to the private landowners who protect a watershed (Bishop et al. Citation2008).

The scarcity of water and water-related conflicts have played a role in setting up PES water schemes in Costa Rica and Colombia (Kiersch et al. 2005). In Latin America, PES for watershed protection has gained popularity. In 2002, in Latin America 18 PES water–related schemes were in place (Landell-Mills and Porras Citation2002). The projects are usually public schemes and supported by external financing by way of loans, grants and the expertise of international organisations, development agencies and NGOs. Some are constructed in the form of public–private partnerships (Martinez and Dimas Citation2007; Martinez and Reyes Citation2007; Tresierra Citation2008).Footnote 8

The involvement of the private sector in the PES schemes for watershed management has not yet developed on a large scale. In fact, only 5% of global private investments were directed towards the water sector, which of course also comprises many water-related business activities other than PES. The SNS REAAL Water Fund explains that a lack of involvement is related to the presumptions of investors about water investments, such as that water issues are very complex and that investments have a high-risk and low-return profile, combined with high overhead and transaction costs.Footnote 9 High transaction costs should be understood in relation to the acquisition of legal title or use rights and capacity building with local communities in order to change unsustainable land-use practices. In order to improve the financial capacity of watershed protection businesses, private water users have to be involved. Examples are energy companies that need stability of the water volume in a river or artificial lake for the generation of electricity and water companies, breweries and soft drink companies that depend on the availability and the quality of water near their production sites. The examples of Costa Rica PES and Vittel PES below illustrate how companies can participate in or set up a PES scheme, thereby explaining the role of the local public authorities.

Costa Rica PES

The government of Costa Rica has developed a nationwide PES programme as a response to the country's rapidly increasing rates of deforestation. The ES providers, that is, private owners of forest lands, are paid by the State and GEF funds (Global Environmental Facility Citation2011) as well as by water users including hydropower companies, for the maintenance of forest cover in watersheds. In 1996, Forest Law No. 7575 was enacted in order to legally set up PES schemes (Bennet and Henninger Citation2008). The law provides a regulatory framework for the adoption of financial incentives for maintaining forest lands and a legal basis for the government to enter into contracts with property owners to provide services originating from their land. One PES scheme involving a private company is ‘Energia Global’ (Russo and Candela Citation2006).

The organisational setup is as follows. This initiative consists of a public–private partnership between the hydropower company Energia Global (the main investor), the ‘Government of Costa Rica Fund’ (income source: mostly fuel tax revenues) and the National Fund for Forestry Financing (acts as intermediary).

The business model regards the financing of two types of ES: (i) the continuity of water flow for hydroelectricity generation; and (ii) biodiversity protection. Energia Global is heavily dependent on the storage of water. Two small reservoirs can only store an amount of water sufficient for 5 hours' generation. It is therefore fundamental for the company to increase the stream flow regularity (quantity), especially in the dry season, when prices for electricity production are highest. It is also important to reduce reservoir sedimentation (Watershed Markets Citation2008).

It was estimated that an increase in forest cover upstream will provide for these services. Energia Global's first focus was on water quantity increase; this was followed by water quality concerns. The company's ambition became to protect the basins that drain into the Rio San Fernando (1818 hectares) and Rio Volcan (2493 hectares), which feed their plants. Energia Gobal had calculated that its investment in watershed management would be a profitable venture if it would be able to obtain an extra 460,000 cubic meters of water. There are no records as to whether this goal was achieved.

Vittel PES

Perrier Vittel S.A. (Vittel) is one of the world's largest bottlers of natural mineral water. The maintenance of water quality is vital for a water bottling business.

The Vittel PES business case is as follows. Vittel had calculated that the protection of an existing water source is more cost-effective than building a new filtration plant or transferring its operations to new sources (Perrot-Maitre and Davis Citation2001). Vittel therefore decided to finance ‘quality drinking water’ through compensation for services of landholders located around the springs. The farmers agreed to adopt less intensive farming practices in order to reduce agricultural run-off of herbicides and other pollutants. Vittel financed the programme with the support of the French National Agricultural Institute (INRA) and the French Water Agencies. The level of non-point-source pollutionFootnote 10 was reduced significantly and, according to a cost-benefit analysis study of the Vittel case by INRA, the project was economically justifiable (Perrot-Maitre Citation2007). The Vittel model might however be difficult to implement in a large geographical area, or in a region with many farmers without government support.

As an observation, it has to be noted that despite these business examples of watershed protection business, the potential to finance nature conservation through payments for water services has not yet been fully developed. Finding willing buyers appears to be a challenge. However, as water becomes scarcer, it is assumed that watershed management will become more profitable (UNEP FI 2008). Furthermore, the case studies affirmed that a water-related scheme needs a certain degree of government involvement and, preferably, regulation in order to support the scheme. This is due to the complex legal and social situation in which PES water business models have to operate and to the often large number of participants. Further research regarding the impact of land use on hydrological services would also be welcome.

To conclude, PES schemes have been initially designed by governments as an incentive for engaging the business sector into financing conservation activities. As was demonstrated above, public regulation generally formed the basis of setting up PES schemes although in the Vittel case, this was not the case. Furthermore, regulation is usually also necessary for the implementation of a PES mechanism. Since there are often a large number of providers and/or a large number of users of those ES involved, it is more practicable to publicly regulate the transfer of the payments than to manage the same through concluding individual contracts between all those parties.

Results: (iii) factors that support private investment in BES

General analysis

The business models set out here show various innovative approaches of private sector involvement into BES protection. These are interesting because they managed to reach the stage of scaling-up. However, many others failed in becoming financially viable. The business models and case studies analysed above reveal certain preconditions for making the private sector participate in BES ventures, which will be discussed in this section.

First, in order for a BES project to evolve steadily, the support and involvement of a local governmental body is often required. This was highlighted in the case of the sustainable forestry projects and watershed PES programmes. As regards the PES business model, new public regulation introduced by the local government is usually an additional factor for success. However, as the Vittel PES scheme has demonstrated, when a company is at risk to loose a certain ES on which it depends, it is motivated to invest into the conservation of this particular ES.

Second, large biodiversity projects routinely involve various stakeholders, such as the government, NGOs, entrepreneurs and private investors. In the case of ecotourism, support of local communities is a necessity. These factors imply that the entrepreneur must be willing to take the time to research the interests of all stakeholders and must have effective management skills for convening these parties and interests. This was demonstrated in the forestry fund case study and the Malua Biobank case.

Moreover, capacity building with local communities is a process that requires time. It will be evident that such a BES business case needs significant up-front capital for its development. The capital is needed for the management time to set up the business model, for local capacity building, for obtaining sustainability certification (e.g. FSC), for acquiring land, permits or concessions to start the ecotourism project or the sustainable forestry project. The ability to attract the up-front capital usually requires a track record of previous projects to prove the entrepreneurial skills of the manager. Also, a good understanding of the market and the ability to define a biodiversity product or ES in monetary terms are factors that are essential to set up a successful and investable BES project (Levashova and Jonkers Citation2010).

Additionally, a BES project needs to be set-up in an ‘investment-ready’ legal and operational structure. The fund managers should be able to communicate with financiers and investors in order to attract capital. As the language of BES entrepreneurs does not necessarily align with the jargon of financial experts, this might form a barrier.

Another factor is that, for institutional investors, an investment object should attain a certain volume and show a promising track record. Both conditions can constitute a challenge. Only when various projects have been bundled, like what we saw for example in the case studies of the forestry fund and the Pan Parks ecotourism projects (and also the African Parks Network (Citation2009)), do investors recognise it as an investable object.

Some business models transpired due to legislation. An example thereof is ‘wetland banking’ as developed in the United States. It is a variation of a mitigation scheme. This mechanism has been developed to cope with environmental liabilities and ultimately serves the purpose of avoiding damage to nature. Our research demonstrates that this business model is well developed in the United States. Later in this paper we will elaborate on wetland banking. Subsequently, we will introduce the ‘like-for-like’ compensation mechanism which also forms a motivation for companies to invest in a compensatory biodiversity programme. In some cases programmes have been established pursuant legislation, in other cases they have been set up on a voluntary basis (Hamilton et al. 2008).

Legislative framework as a stimulus for wetland banking business

Although wetlands only cover 6% of the total world surface, they form hotspots for biodiversity and deliver ES to billions of people (Wetlands International Citation2009). One of the ways to maintain the volume intact and generate biodiversity benefits is by means of ‘mitigation banking’. A mitigation bank is a wetland, stream or other aquatic resource area that has been restored, established, enhanced or preserved for the purpose of providing compensation for unavoidable impacts to wetlands elsewhere, that is, impacts comprise mostly drain and fill actions (Silverstein Citation1994; Robertson Citation2004; Carroll et al. Citation2008).

The main objectives of wetland banking are to preserve wetlands and to provide a habitat for endangered species. The mechanism is as follows: (i) a real estate developer who intends to initiate a project that can damage a wetland, must first assess how to avoid or minimise impacts on such wetland; (ii) in instances where impacts cannot be avoided or minimised and the real estate development plan will nonetheless be approved, the wetlands have to be replaced; (iii) replacement can take place through ensuring the restoration of prior wetlands, the enhancement of other low quality wetlands or the creation of new wetlands by the developer or by a third party, for example, a private company; and (iv) it will be ascertained that each hectare of wetland damaged or destroyed will be replaced (the mitigation ratio can vary, generally more than 1:1).

The business model of wetland banking originated under the US Federal Clean Water Act 1972 of the US Army Corps of Engineers regulations (Clean Water Act). The purpose was to protect America's rivers, lakes, swamps and other wetlands from disappearing. The Clean Water Act established limits on economic development, it became illegal to fill, dredge or in any other way to damage a wetland without a permit from the US authorities (i.e. US Army Corps of Engineers and the EPA). The authorities determine whether the damage can be avoided and, in cases where the damage is unavoidable, whether it can be mitigated or minimised (Bayon Citation2004).

Different actors, for example, private companies and public entities, can establish and maintain wetland banks. Usually, a third-party entrepreneur, the so-called mitigation banker, gains authorisation to create or restore a wetland area. When this task has been performed, this wetland can be used as a ‘bank’ of credits. The bank's value is defined in ‘compensatory mitigation credits’, the number thereof as decided by the authorities (Washington Department of Ecology Report Citation2006). The mitigation bankers can sell these credits to third parties, that is, real estate developers that use them to satisfy their mitigation obligations towards regulators (Bendor Citation2007) or use them themselves. Wetland mitigation banking in the United States is now largely an entrepreneurial activity: ‘77% of 454 approved or proposed banks identified in a 2006 report by the US Army Corps of Engineers involve the private third-party production of wetland credits for sale’ (Bishop et al. Citation2008; Robertson Citation2009).

Wetland banking can be considered the first successful environmental credit market that sells products certified using metrics of ecological function. It is quite distinct from carbon markets. What ‘is being traded isn't so much the right to pollute, but rather (…) the right to develop’ economic activities in a nature area (Robertson Citation2009). This system has been copied by several countries. Puerto Rico has created a market in the right to develop beachfront property and New Zealand has established a market for the right to exploit fisheries (Robertson Citation2009).

US wetland banking case study

A concrete example of the US wetland banking business is the ‘Nanticoke Headwaters Project’ managed by Ecosystem Investment Partners (Citation2007).

The organisational setup and the business case are as follows. EIP is a private equity fund manager that acquires and manages high priority conservation properties across the United States. It invested USD 27.5 million in wetland, stream mitigation banking and conservation (endangered species) banking across a variety of landscapes. EIP claims that the investments generate multiple revenue flows. In 2007, together with The Conservation Fund (TCF) and the State of Delaware (United States), EIP developed a project that aims at the conservation of the last-remaining massive forest area in Delaware. The impact of intensive agriculture and the development of monoculture pine plantations had resulted there in the loss of over 50% of the wetlands. By using private investment capital, market-based conservation mechanisms and the support of conservationists, the project claims to have saved 2300 acres of the forest area that otherwise would be converted into residential subdivision. EIP utilises the demand for ES credits found in Southern Delaware to pay for wetland conservation and restoration as well as to generate a financial return for EIP's investors.

Other like-for-like mechanisms involving business to compensate biodiversity damage

Environmental mitigation is a concept that is currently on the rise. New forms are being developed such as ‘nature credits’. Nature credit frameworks include wetland banking, habitat banking and biodiversity offsets. ‘Habitat’ refers to the environment or the place where organism or a biological population normally live. Biodiversity offsets are based on the ‘like-for-like’ compensation concept. A ‘biodiversity offset’ is a piece of land that is set aside to maintain its biodiversity values and thereby to offset the negative effects of economic development on a piece of land with biodiversity values elsewhere. They compensate for unavoidable, residual impacts, where avoidance, mitigation and restoration activities are insufficient to protect the resident biodiversity (BBOP 2009b). Biodiversity offsets are best applied near to where the development takes place (in situ). Ultimately, the goal is ‘no net loss’, and if possible a net gain.

The US-based non-profit organisation Forest Trends researched existing compensatory mitigation programmes around the world and found 39 in 2010 (Madsen and Carroll Citation2010).Footnote 11 The conservation impact of this market includes at least 86,000 hectares of land under some sort of conservation management or permanent legal protection per year. Biodiversity offset programmes can be discerned between ‘regulatory biodiversity offsets’ and ‘voluntary biodiversity offsets’ (Forest Trends and Ecosystem Marketplace Citation2008). Both categories will be elaborated on below.

In the United States, the Clean Water Act and the Endangered Species Act regulate biodiversity offsets. In the EU, the Habitats Directive (92/43/EEC Citation1992) and the Environmental Liability Directive (2004/35/EC Citation2004) set the scene. The Habitats Directive applies before damage has occurred. A Member State may only proceed with the development of a project that has negative ecological implications if there is ‘an overriding public interest’ and if the State takes compensatory measures (European Communities Citation2007). The measures are independent of the project and are intended to offset the negative effects so that the overall ecological coherence of the ‘Natura 2000 Network’ is maintained. The Environmental Liability Directive applies after the damage has occurred. This Directive is based on the ‘polluter pays’ principle and regulates the prevention and remedies for damage caused to animals, plants, natural habitats, water resources and land.

The measures introduced by these EU Directives serve as an incentive for businesses not to pollute or destroy nature. Moreover, they have stimulated new developments in the insurance market, which has introduced a differentiated premium system, a further stimulus to minimise ecological risks. Furthermore, the legislation indirectly encourages the development of voluntary markets for biodiversity offsets and wetland or habitat banking (Bräuer et al. Citation2006). Private companies take part therein by providing the compensational measures, that is, creating new nature or conserving high value existing nature that can be put forward by another company as compensation for its economic activities.

Mainstream investors such as Caisse des Dépôt, ABN-AMRO, Henderson Investors, BNP Paribas Bank, ISIS Asset Management, the World Bank Group and the International Finance Corporation (Citation2009) consider biodiversity offsets as a business opportunity (Howard Citation2007). Certain multinational companies, for example, BHP Billiton and Rio Tinto, are investing in voluntary biodiversity offset programmes and have communicated the ambition that their economic activities have no negative impact on biodiversity.Footnote 12 In 2006, Wal-Mart has made a 10-year commitment, totalling USD 35 million, to the National Fish and Wildlife Foundation for the creation of permanently protected reserves. Wal-Mart's ‘Acres for America’ project is intended to ensure that the company preserves one acre of priority wildlife habitat for every acre developed by the company.Footnote 13

Various voluntary biodiversity offsets programmes have been developed, such as the BBOP (Citation2009b). This was launched in 2004 by Forest Trends with support from the NGOs Conservation International and the Wildlife Conservation Society. BBOP developed guidelines for offset design and implementation, which were tested in pilot projects (BBOP case studies Citation2009a).

BBOP case study Australia

One BBOP pilot project concerned the Australian company Basslink Pty Ltd. (Basslink). Basslink was constructing an electricity cable to link Tasmania with Victoria State in the mainland Australia, thereby impacting an area located within the Special Protection Zone of a State Forest. The ‘habitat hectares approach’ was adopted, which constitutes a precise, quantitative method for assessing the type, quality and conservation significance of the vegetation at stake. The initial amounts of habitat hectares were combined with an additional multiplier to address risks and other factors to indicate the total number of habitat hectares needed to compensate for impact. Basslink purchased a property with similar, albeit degraded vegetation adjacent to the main impact site of the project, for purposes of restoration, maintenance and improvement of the habitat. A management plan for restoration was prepared before the construction of the project began. The developer will manage the offset area for a 10-year period. The land is to be given protective tenure by its inclusion in the Crown estate. Basslink's objective was to achieve a ‘net gain’ for native vegetation.

To conclude, the example of the US Clean Water Act clearly demonstrates that a legislative framework requiring developers to offset biodiversity impacts effectively draws private sector parties into biodiversity like-for-like programmes. This offers a business case opportunity to other parties for creating or regenerating nature and selling the credits they generate. Interestingly, Brazil, Canada, the United States and Australia have introduced measures for biodiversity offsets (Madsen and Carroll Citation2010). EU Regulations also motivate compensatory measures in connection with biodiversity loss in a certain area.

Apart from mandatory programmes, why would companies commit to participate in voluntary biodiversity offset programmes? One driver is that they can show society that it can trust them when they need access to land or sea for their activities. In other words: that they are companies that conduct their business in a responsible way. The application of biodiversity offsets as part of economic development projects can be considered ‘best practice’. Moreover, participation in offset programmes can enhance a company's reputation because biodiversity appears to have a high symbolic value (Covalence 2008). Another reason is the tendency that banks increasingly demand guarantees from borrowers that their projects do not cause environmental damage. However, as you would expect, investing in biodiversity offsets programmes entails risks equivalent to other business ventures in an emerging market. Possible set-backs can include disappointment about the conservation outcomes or the resulting reputational benefits.

It is interesting to see that ES ‘brokers’ and investors recognise that the creation of biodiversity offsets is a business opportunity in itself, both in the case of mandatory and in voluntary offset programmes, as was demonstrated above in the Nanticoke and Malua Biobank case studies.

Results: (iv) barriers for private sector investments and suggested solutions

Barriers

This article has discussed various emerging markets in the field of PES and for investing in BES, and the factors that support private sector involvement. Some markets can be considered more mature (sustainable forestry, wetland banking and ecotourism) than others that are still in a developing phase (REDD and biodiversity offset credits). The literature review, the interviews and the discussions during the working conference that was organised as part of the research project, all revealed that the following factors obstruct mainstream business participation:

| 1. | Lack of exchange of information and knowledge between the business sector and conservationists: Investors suffer from a lack of information concerning existing and developing biodiversity business opportunities. Furthermore, BES project managers often lack expertise and experience in structuring their funds in such a way that they meet the strict investment criteria of institutional investors. There is a two-way need for information provision and training in order to encourage the further development of a market framework that facilitates biodiversity business opportunities (Biodiversity Technical Assistance Unit Citation2009). In addition, it appears that the biodiversity sector (including NGOs) – that possesses knowledge about biodiversity – is not effectively assisting commercial actors in the development of a portfolio of bankable biodiversity projects (Bishop et al. Citation2008). | ||||

| 2. | BES business projects face high risks: Multiple risks can materialise regarding BES investments. One is the lack of predictability concerning the outcome. This is related to the fact that only a few front runners have successfully engaged in the biodiversity business. For example, the involvement of the private sector in PES is still relatively limited. The lack of successful case studies prevents large investors from considering biodiversity business as an opportunity. Another risk relates to the fact that biodiversity projects sometimes are located in countries that have a weak government or an inadequate regulatory environment. In sustainable forest practices, land tenure and the enforcement of compliance often are not always properly handled. | ||||

| 3. | High transaction costs for investors: The relatively high cost of due diligence required to meet financial and biodiversity criteria also constitutes an impediment. As most biodiversity projects aim at a long-term life cycle, they require adequate assessments. It is important to make this cost issue transparant. | ||||

| 4. | Lack of management capacity and entrepreneurs: In order to manage biodiversity business – and especially to develop an effective PES system for forestry and water services – project management needs to be knowledgeable in order to be cost-efficient (Bräuer et al. 2006). | ||||

| 5. | Small projects/low revenues: Voluntary biodiversiy business projects tend to be small and have relatively high transaction costs (except for the voluntary carbon market). The projects need to be bundled to attract large investors as the latter generally look for a substantial volume. | ||||

| 6. | Lack of enabling environment: In order for a business to prosper, the environment in which it operates has to be favourable for commercial activities. This includes an effective regulatory structure that reflects public expectations about the rights and responsibilities of business and society (Bishop et al. Citation2008). In the context of business and biodiversity, the enabling regulatory framework is often underdeveloped. This barrier came up earlier in the paper. Based on the perception that biodiversity is a public good; businesses consider that all related problems are the responsibility of the government and society in general. For most financial institutions and fund managers, biodiversity is no more than an ‘environmental liability, responsibility or a resource that they can exploit’. The majority of the private sector does still not see biodiversity as a business asset that ought to be conserved and managed in its own right (Bishop et al. Citation2008). | ||||

| 7. | Inability to think ‘long term’: Financial institutions lack an understanding of what biodiversity loss means for them and to the companies in which they invest. Investing in biodiversity can mitigate those risks. The investment itself can generate long-term benefits. The financial returns and conservation benefits at the early stage, however, might not be as impressive. Strict short-term-driven return-on-investment criteria used by investors constitute a barrier to investing in BES funds. | ||||

Suggested solutions

The critical question is how to overcome these barriers. Despite the recent financial crisis and ecological crises, the key concern for entrepreneurs and investors of today still appears to be how to secure short-term financial returns. The business models and case studies discussed in this article have shown that well-structured biodiversity ventures can indeed be financially promising from a long-term perspective. The research project, including in-depth interviews with pro-biodiversity project managers and owners as well as with institutional investors, and the structured discussions aimed at analysing the barriers and solutions with the participants at the working conference, suggested the following solutions to make the pro-biodiversity business successful:

| 1. | Encouragement of multi-stakeholder cooperation: All parties interested in habitat conservation have to share the responsibilities and collaborate to make it a priority issue. Governments, entrepreneurs, companies, NGOs, individuals, religious groups and local communities, who are usually initiators of biodiversity conservation projects, have to make use of each others' strengths. They have to work closely with investors, foundations, local authorities, farmers, forest landholders, consultants and universities to make conservation happen. Governments can provide finance for research in the field of biodiversity business and stimulate start-up biodiversity initiatives. They can also support the set up of a sound regulatory framework that activates BES markets (property rights, cap and trade liabilities). On the part of investors, clarification has to be achieved regarding companies' BES dependence and impacts. This need be linked with lending and investment requirements addressing these concerns. Investors have to become familiar with the opportunities and risks related to BES markets. Other actors could share their expertise on BES, actively develop initiatives and monitor projects on biodiversity value. | ||||

| 2. | Sharing information: One of the main barriers that prevents investment in biodiversity is lack of information. Companies do not produce sufficient and detailed public information on their impact and dependency on BES. Business risks arising from a company's dependence and impact on ES have to be clearly mapped. Transparency on these subjects will help companies and investors to produce sound business planning that promotes investing in sustainable ecosystems and response strategies in regard of restoring affected ecosystems. | ||||

| 3. | New tools to innovate BES business mechanisms: New tools that can help businesses to manage ecosystems can facilitate the recognition of the true value of the BES and to internalise the costs of public goods and service usage in business operations (Business and Ecosystems 2006). Investors could incorporate BES risks as a factor in their risk assessment mechanisms. Profound due diligence can assist. Institutional investors could encourage sell-side analysts to consider BES issues besides financial issues, when making investment recommendations (UNEP FI 2008).Footnote 14 | ||||

| 4. | Creating a good investment climate: This is primarily a task for (inter)national governments. Innovative biodiversity initiatives are usually successful in countries that have a favourable investment climate, which includes good governance, a well-developed legal system and supportive policies and institutions. | ||||

Conclusion

The loss of biodiversity comprises a major threat to the sustainability of our society. Presently, despite the popularity of the PRI, the vast majority of financial decision-makers is not aware of biodiversity-related problems or does not know how to address them in their practice. In particular, investment fund managers have limited ideas about the concept of biodiversity and as a result most of them do not consider it relevant enough for incorporating these concerns in investment decisions nor to actively invest in pro-biodiversity business.Footnote 15

The question addressed in this article was: What is the incentive from a private point of view to invest in nature and what are the barriers and opportunities? This article was to explore which incentives can motivate private sector investment in nature conservation by investigating various forms in which such investment can take place. An analysis was offered of different business models and cases that have been developed or that are in a developing stage. As a result, it has offered an insight into the possibilities for the private sector to engage in new market based approaches of nature conservation. ‘Biodiversity business’ is commonly explained as business conducted by a commercial enterprise that generates profits through the activities which conserve biodiversity and ecosystems, use biological resources sustainably and share the benefits arising from this use equitably. It was demonstrated that innovative mechanisms are being explored for channelling private funds to ensure the protection of BES. Various emerging ‘BES markets’ offer new opportunities to business entrepreneurs and investors and in particular to institutional investors with a long-term perspective. Although the business case for biodiversity is still developing, certain sectors like forestry-related products, eco-tourism, watershed management and wetland banking are already being marked as prospective business opportunities. The authors pointed out that in some cases, public regulation formed the basis on which a business case was built (wetland and habitat banking and carbon sequestration credits). In other cases, public involvement is required for the implementation of the business model (watershed management), and yet in other cases, it appears to be necessary to establish a public–private partnership with local communities and/or authorities (large ecotourism projects and nature conservation certificates).

The preconditions and the main barriers to set up and invest in pro-biodiversity business have been identified in a general way. Further research would be necessary to identify sector-specific constraints. The obstacles mentioned are mostly related to lack of knowledge, high transaction costs and a lack of entrepreneurial spirit. Examination of the innovative approaches presented in this article and engagement in partnerships with other stakeholders can help to overcome such obstacles. If the financial sector would succeed in seeing biodiversity as a business opportunity and not only as a risk and as a liability problem, this could increase value not only with respect to Profit, but also in the other two dimensions: Planet and People.

Acknowledgements

The research closed on 23 March 2011. In particular, Joshua Bishop of IUCN and the Journal's reviewers are thanked for their valuable comments to the earlier versions of this article. The authors also thank the BES fund managers who were willing to share information. The information in this article is provided for general informational purposes only and should not be construed to contain legal, business, accounting, tax or other professional advice.

Notes

1. For example, Global Compact, Principles 7–9; the OECD Guidelines for Multinational Enterprises, Chapter V; the Earth Charter, Chapter II (Principle 5); the Principles for Responsible Investment (PRI Citation2010); the Global Reporting Initiative G3 Sustainability Reporting Guidelines; the Equator Principles.

2. This last information is based on the research results conducted via interviews with fund managers of BES funds in another project, that is, the ‘Business Cases for Biodiversity’ 2010–2011 project, conducted by the authors of this article together with the Copernicus Institute of Utrecht University, the Netherlands.

3. The major Dutch pension funds, ABP and PGGM, invest substantial amounts in sustainable forestry. Investments & Pensions Europe, ABP makes first timber allocation, 13 July 2007, available online at http://www.ipe.com/articles/print.php?id=22547; APG Sustainability Report 2008, available online at: http://www.apg.nl/apgsite/pages/images/VVB%20APG%202008%20ENG_tcm124-91870.pdf, p. 18; sites visited on 23 March 2011.

4. According to its Annual Report, Pan Parks aims to pursue a financially sustainable approach and to seek diverse sources of income, including from institutional investors. See http://www.panparks.org/sites/default/files/upload/aboutus_publications/panparks_corp_publications/panparks_annualreport_2009.pdf accessed on 25 March 2011.

5. African Parks Networks, www.african-parks.org follows a similar business strategy.

6. This last piece of information is based on the research results conducted via interviews with fund managers of BES funds in one of the follow-up projects i.e. the ‘Biodiversity and Business Cases’ 2010–2011 project, conducted by the authors of this article together with the Copernicus Institute of Utrecht University, the Netherlands.

7. The EU Greenhouse Gas Emission Trading System is based on Directive 2003/87/EC (Citation2003). In the United States, the American Clean Energy and Security Act of 2009 was proposed in order to establish a similar cap-and-trade plan, but has been not adopted. See http://www.govtrackinsider.com/articles/2010-04-27/climate-change, accessed on 23 March 2011. In the United States, various voluntary carbon sequestration initiatives are already in place. Australia is also developing cap and trade legislation.

8. WWF has implemented a number of ‘payment for watershed services’ projects, for example, in Guatemala, Peru, Indonesia and Tanzania. Source: Information Exchange Meeting WNF, the Netherlands, 3 March 2010.