ABSTRACT

This study investigates whether the use of housing charges is an innovative or traditional instrument in financing bulk infrastructure. It develops a conceptual framework to demonstrate how housing charges are perceived as an innovative model of financing and funding bulk infrastructure. Research focuses on a case study policy pilot infrastructure project in New Zealand, with primary evidence gathered from informed professional stakeholder interviews. The findings highlight that revenue streams are the most common concern when applying the infrastructure funding and financing (IFF) model to deal with bulk infrastructure. Further, as housing charges are a new instrument generating cash flows to finance bulk infrastructure, it is found that financing infrastructure development is only innovative in terms of its mechanics, legislation and policy setting.

INTRODUCTION

Infrastructure development is critical to social and economic development, and provides the most basic human needs, such as water, electricity, transportation and communications. Hence, financing infrastructure systems is one of the most challenging aspects, and under-investment in infrastructure is the current tendency worldwide, even with developed countries that have strong institutions (Estache et al., Citation2015; Global Infrastructure Hub, Citation2016; Hutchison et al., Citation2016). It is argued that the world needs an annual investment of US$3.3 trillion, equivalent to 3.8% of gross domestic product (GDP) just to support economic growth between 2016 and 2030 (Woetzel et al., Citation2016). Infrastructure projects often require a considerable amount of up-front capital investments from investors, while revenue streams (cash flows) generated from the projects are uncertain to payback the capital investments. For example, the evidence is unclear as to whether infrastructure charges can stimulate property prices for financial payback in the future (Bryant, Citation2017). Several studies investigate innovation metrics, new mechanisms, technology, urbanization and the impacts of financialization on infrastructure development (Ersoy, Citation2017; Ersoy & Alberto, Citation2019; Grafe, Citation2020; Grafe & Mieg, Citation2019); however, no recent study has examined the use of housing charges in financing bulk infrastructure, leaving a knowledge gap in the field. Therefore, this study explores the role of housing charges to finance bulk infrastructure, and investigates whether they are an innovative instrument for financing infrastructure development. Moreover, it provides conceptual thinking on the term ‘innovative’ when looking at bulk infrastructure finance.

We determine the term ‘bulk infrastructure’ in this study, which is in terms of transport and water – excluding energy, waste, information and communication, and public capital/services. The case study looking into this issue focuses on New Zealand, especially Auckland City as its most populous city and the region of Auckland in general. A case of international appeal given that there is a considerable housing ‘crisis’ in terms of affordability and that bridging the infrastructure finance gap is seen as critical by many scholars (Andrés et al., Citation2014; Hutchison et al., Citation2016; Woetzel et al., Citation2016). The institutional and geographical case of Milldale, situated north of the city of Auckland, involves a large-scale new greenfield housing development. The case study uses a loan to fund the infrastructure, and is financed against a long-term private housing charge paid by those who will reside in the site’s properties (Orsman, Citation2018; Twyford, Citation2018). This research looks at multi-stakeholder thinking and practitioner development to explore a more profound conceptual question of what is meant by ‘innovative finance’ in infrastructure development when used quite arbitrarily during the process. For instance, we discuss whether the models are ‘innovations’ in dealing with ‘the problem’ of infrastructure finance and funding?

Using semi-structured interviews with experts from non-governmental organizations (NGOs), local and central government, the study qualitatively provides insightful contributions and critical discussion on the role of housing charges in financing bulk infrastructure in New Zealand.

The remainder of the paper is structured as follows. The next section presents a literature review of infrastructure funding and financing (IFF). This is followed by the research methods and content analysis theory as applied to the research. After presenting the main qualitative findings and data visualization from the semi-structured interviews, the paper provides a critical discussion on the several innovative approaches of the IFF model using the quotations extracted from the semi-structured interviews. We provide conclusions as well as various limitations, implications and further research options.

LITERATURE REVIEW: INFRASTRUCTURE FUNDING AND FINANCE AS INNOVATION?

One important distinction that must be established is the difference between funding and financing. According to Ernst & Young (Citation2014), funding is the allocation of ultimate cash flows that support the construction and operation of infrastructure (i.e., general taxation revenue, user charges or specific value-capture levies), whereby financing is described as selecting the immediate source of cash that will physically develop the assets with the repayment of this investment over the life of the asset (i.e., the full range of procurement approaches). The funding and financing of the infrastructure is a complex mix of deals that include tolls, taxes and metered user fees. Funding of infrastructure can be drawn against the person or place. For the person, income taxes are an excellent example of contributing to public infrastructure funds. For place, infrastructure projects that are built out (such as a road or a bridge) could be paid by the user consuming the benefits of the infrastructure (Koh, Citation2018). O’Brien et al. (Citation2019) argue that the way we fund, finance and govern infrastructure is critical to interpreting socially and spatially imbalanced infrastructural supplies. They also present that various methods of contemporary financialization engaged with urban infrastructure have become extremely important; hence, future research works are needed. The analysis framework of urban infrastructure financialization, especially determining accurately the ways and how much revenue infrastructure assets can generate, has been a central issue among other aspects such as capital structure, organizational structure and regulatory process (O’Brien et al., Citation2019; O’Neill, Citation2019). Financialization is also reviewed under built environments, which are determined as an extensive partial process, shaping social relations that are constructive to geographical change, urban governance and its sustainability (Clark et al., Citation2015). Besides the various works of financialization, and like other income-generating asset classes, Aalbers (Citation2017) aggregates housing as a key object of financialization, arguing that housing systems fluctuate across regions in which the financialization of housing will be uneven and path dependent.

Taxes and fees are known as an established traditional instrument, while newer instruments such as grants, bond-based finance, tax incentives or different kinds of infrastructure levies and developer fees are classified as the recent ‘innovative’ financing vehicles (Hutchison et al., Citation2016; Strickland, Citation2016). O’Brien and Pike (Citation2019) investigate the City Deals as a new form of funding, financing and governing urban infrastructure in the UK, which is based upon the agreed negotiations between local and central governments on decentralized powers, resources and responsibilities. The managerialist institutions and conservative/risk-averse administrative culture of the continued authority of the highly centralized UK national state have restricted the financialization of urban infrastructure and its entrepreneurial governance in the UK City Deals (O’Brien & Pike, Citation2019). Previous research provides a theoretical background for a better understanding of the importance of financialization as well as ‘innovative finance’ in urban infrastructure funding, financing and governing practices. In short, newer and ‘innovative’ instruments to forecast and generate sufficient revenue streams (cash flows) to payback large up-front capital investments have become a major concern in financing infrastructure development.

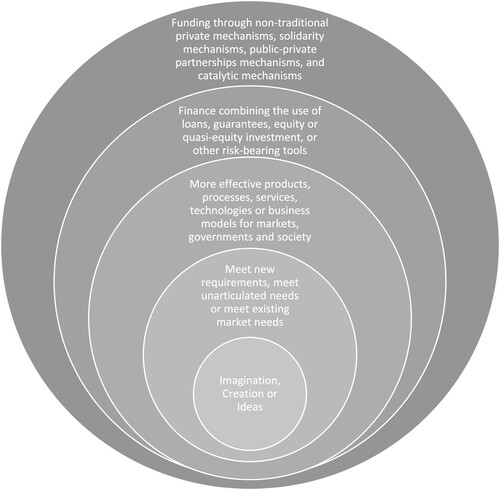

At the outset of the study through the theoretical background provided in the literature, we introduce the use of ‘housing charges’ as a new ‘innovative’ vehicle to fund bulk infrastructure using a case study of the Auckland region of New Zealand. Besides the work of O’Brien and Pike (Citation2019) that explores the City Deals as a new model of infrastructure finance and urban governance based on central–local government agreements in the UK, Bryant (Citation2017) provides empirical evidence showing that infrastructure charges are a critical factor contributing to decreased housing affordability and increasing house prices in Australia. These newer infrastructure financing vehicles somehow provide a clearer understanding of ‘financial innovation’ in infrastructure finance, especially the introduction of ‘housing charges’ in the study. puts forward the nature of innovation by bringing together the central tenets and how they have transcended to embrace more in-depth requirements, operational needs, financing types and funding mechanisms. The central tenets of innovation consider ‘new’ things that are imagination, creation or ideas based. Particularly those that apply better practical implementable solutions to meet new requirements, meet unarticulated needs or meet existing market needs (Maranville, Citation1992). Therefore, for ‘innovative finance’ we are looking at possible future financing solutions that suit new requirements, whether known or unknown. Hence, different geographical and temporal contexts in applying existing solutions could potentially be innovative – especially if there are more effective products, processes, services, technologies or business models for markets, governments and society (Addie et al., Citation2020; Cantafio & Ryan, Citation2020; Ersoy, Citation2017; Ersoy & Alberto, Citation2019).

Figure 1. The nature of innovation in infrastructure funding and financing.

Source: Authors.

‘Innovations’ in infrastructure finance are those non-traditional forms of funding infrastructure. Non-traditional forms include solidarity mechanisms, catalytic mechanisms and partnerships (Grishankar, Citation2009). This innovation of infrastructure finance is different from what is defined as more broad ‘innovative finance’, which covers a multitude of technical risk-bearing packages. For instance, there could be a combination of guarantees, equity and loans. This combination of risk-bearing packages blended with basic (public) grants that can boost infrastructure investment in large real estate development projects (Spence et al., Citation2012). As well as blending, this more contemporary innovation is more flexible (Carter, Citation2006). However, a drawback to such blend and flexibility is that some risks are undetected or redistributed. For example, private finance risk can be passed to public sector project groups that may not be able to manage effectively due to inadequate resources, knowledge and capabilities (Ng & Loosemore, Citation2007).

The nature of financial innovation for IFF is therefore exemplified by the innovative tools and mechanisms being used, but we are not focusing on the financial product innovations themselves. More so, we are looking here at ‘innovations in infrastructure finance and funding’, not ‘financial innovation’. Financial innovation more specifically concerns itself with new financial products, institutions and markets that can change the way in which the financial landscape is conducted (Miller, Citation1986). The relatively recent introduction of derivatives, hedge funds and the market for crypto-currencies would be good examples of these types of ‘financial innovation’. We are similarly not considering ‘financial innovation’ around approaches using a ‘regulatory dialectic’, a situation where rapid changes in the financial environment lead to banking regulation becoming overwhelmed by technological and regulation-induced innovation (Kane, Citation1981).

In terms of ‘innovation’ in funding and financing infrastructure, we contrast here some of the more traditional ‘non-innovative’ products/services, such as those traditional approaches that can be classified as general taxes. General tax attributes could include contributions, agreements, fees, levies and rates to fund an infrastructure project. For contributions in this development context, we consider the appropriation of funds via ‘developer contributions’ (Gielen & van der Krabben, Citation2019). Developer contributions (alternatively developer charges or planning gain) are a type of impact fee where a proportion of the impact is paid for the developer making the impact. Community benefits agreements (CBAs) in the United States are one such development contribution policy that a community and developer stakeholder consortium pays for some of the public and private infrastructure (Laing, Citation2009). In the UK, this type of developer contribution is by Section 106 agreements (Morrison & Burgess, Citation2014), where a proportion of payment is given by the housing developer towards any external impacts. By extension, the UK looked to supersede the Section 106 payment with an ‘infrastructure levy’ that took the policy form of a community infrastructure levy (CIL), where the infrastructure payment may be for both bulk infrastructure and more soft service provision needs such as playgrounds (Lord, Citation2009; Squires & Lord, Citation2017).

The developer contributions and infrastructure levies will often be in addition to traditional (non-innovative) public rates, which are paid as local authority rate tax by householders, or by businesses collected as taxes at the local and national governance level. Some of the initiatives mentioned above are also grant programmes implemented at differing spatial scales and levels of governance – supranational, national, regional, city/city-region, local. Programmes that include urban infrastructure from a block grant payment are arguably traditional. For the European Union supranational institution, the commission of a large-scale grant programme involving infrastructure has been via the European Regional Development Fund (ERDF) which encourages many transnational cooperation projects (Spilanis et al., Citation2016; Squires et al., Citation2016).

Debt finance approaches to financing urban infrastructure are also arguably traditional and non-innovative in type. Typical debt finance for infrastructure orchestrated by the government include bonds such as ‘general obligation bonds’ – a type of local authority loan secured by a larger geographical administrative institution (e.g., territorial state or national) which is paid back by property taxpayers. Any shortfall is often guaranteed by the local authority, plus the rate of tax rise/fall can be limited to a certain percentage, or on occasion an unlimited percentage backed by a public vote – as exemplified by the Proposition 13 ruling in California (Martin, Citation2006). Conduit bonds are another type of government traditional debt finance, where a governmental entity issues bonds to finance a project managed as a special-purpose vehicle (SPV) which may include non-profit corporations, private companies or other governmental bodies (Hargreaves, Citation2018; Walker, Citation2018).

Innovations are held where a catalysing effect is created to renew or regenerate an area that would not have done so ‘but for’ some intervention. This renewal extends to create new markets that would not have existed but for the tax-incentivizing intervention. Property tax relief and the encouragement of business districts through the enterprise zone and empowerment zone initiatives are notable cases (Squires & Hall, Citation2013). Tax credits, as well as tax relief, are also innovative ways with which urban infrastructure is funded. The low-income housing tax credit (LIHTC) is used by the federal guarantee as a credit scheme to leverage housing tax credit from commercial and not-for-profit institutions to finance district-wide urban development projects including infrastructure (Baum-Snow & Marion, Citation2009; Eriksen, Citation2009; Woo et al., Citation2016). Even more layered in innovation are tax credit bonds that not only match credits to other institutional funds but also float these credits as bonds to investors that are paid back by the issuing authority (mainly paying the premium rate and not the coupon rate) (Klein, Citation2009).

Therefore, the ‘innovations’ in IFF can be perceived as an update of the established mechanisms such as user fees and tolls, taxes and fees, as well as the proposal of newer ‘innovative’ vehicles including a mix of grants, debt finance, tax incentives and other infrastructure levies (O’Brien et al., Citation2019; Strickland, Citation2016). Especially, ‘housing charges’ are being explored in this study. With patient capital from pension funds and insurance companies being able to be part of the finance mix, new debt–equity packages are becoming more prominent (Squires et al., Citation2016). Further, more specialized banks and funds are able to evolve for the purposes of infrastructure development, such as state infrastructure banks and sovereign wealth funds (Yusuf et al., Citation2010). This is in addition to new specialized companies that would focus on infrastructure such as national and regional infrastructure companies (CIP, Citation2019a). Plus, the ability to raise capital for infrastructure via regular companies share issuance via these companies, as well as the proliferation of real estate investment trusts (REITs), which are effectively real estate-backed funds that are tradeable investment commodities in the financial marketplace (Giliberto, Citation1990). In a similar vein, emerging infrastructure project finance also encapsulates the creation of funding from bonds that are asset backed against projects or often infrastructure based. These bonds are traded as investment products and becoming more popular with over 400 project bonds recorded in China by 2013 (Hutchison et al., Citation2016).

With several newer instruments that have been discussed, the value-captured and income-generating mechanisms have become a central focus on the ‘innovations’ of IFF practices (Medda et al., Citation2011; Merk et al., Citation2012). Land value-capture finance, to fund infrastructure, has a long tradition in public finance. Particularly because land value capture is seen to stimulate further land development, increasing property values and economic growth (Medda, Citation2012; Starrett, Citation1981), examples in this value-capture sphere include tax increment financing (TIFs) which fund different projects including infrastructure projects (Squires, Citation2012; Squires & Hutchison, Citation2014; Squires & Lord, Citation2012). TIFs in California have morphed into what is known as infrastructure financing districts (IFDs), where the focus of the bond is more on infrastructure and even more spatially targeted within a district. Specific US approaches with the targeted districts and zoning features spatially to land value capture in infrastructure when considering different policies to deal with unique development parcels, such as special assessment districts (SPD), community facilities districts (CFD) and accelerated development zones (ADZ) for urban economic development (Squires, Citation2017; Squires et al., Citation2017). These spatial boundaries of funding connect to each other geographically and thus consider transport in their connectedness. More recent transit-oriented development funds (TOAF) within priority development areas are a testament to this more innovative funding approach with value capture (Knowles, Citation2012; Li et al., Citation2013), as money can be ported over space (e.g., with districts/zones and infrastructure connections) as well as time (e.g., with bonds) (Squires, Citation2014). Value-capture funding within the infrastructure sector is also possible when we consider the ability for transportation sales tax revenues to fund some infrastructure projects (Crabbe et al., Citation2005).

Innovations around asset leverage and leasing to enable infrastructure funds to involve those ways in which (often local) assets can be specifically utilized to evoke financial capital. Local asset-backed vehicles (LABV) could be consortiums that are looking to develop areas and see the realization of a physical piece of infrastructure to self-finance over a period of time. Greenhalgh and Purewal (Citation2015) argue that the difference to the approaches of the local authority municipal bonds is that real estate is increasingly transferred from public sectors to the LABV vehicles in which the private sectors can match the value of those assets with cash. As a variation on this LABV approach, there could be a leasing of assets by a public (or private) institution, which means that asset ownership remains with the leaseholder, as agreed in the contract between the different institutions (Ashton et al., Citation2012).

A potentially ‘innovative’ infrastructure financing model of public–private partnership (PPP) is with the private finance initiatives (PFI) (Abdel Aziz, Citation2007; Cui et al., Citation2018). PFI involves the transfer of substantial risk in building and operation to the private sector. It is structured to ensure a consortium receives a return on costs, payback of interest on the borrowed capital and a return on investment (Greenhalgh & Squires, Citation2011). One perceived advantage of this is that the private sector is better placed to manage the risk (Hutchison et al., Citation2016). Further advantages of PFI centre on value for money, as well as the ability to share the risk, and on arguments of efficiency in the private sector (Wall & Connolly, Citation2009). PFI difficulties occur and include insufficient flexibility during the operational period. To address deficiencies, governments have introduced changes such as non-profit distributing (NPD) that have capped returns and can reinvestment any financial surplus (Hutchison et al., Citation2016). Appendix A in the supplemental data online provides a summary of key selected previous studies on different traditional, innovative and blended approaches to infrastructure finance.

RESEARCH METHOD

Analytical framework of this study

The research methodology involved both primary data collected from the semi-structured interviews and secondary data from desk-based study. First, a secondary desk-based study enabled some understanding of infrastructure finance and funding. We explored the academic literature on these fields of enquiry, and reviewed reports and policies by consultants and government involved with the case study of the Milldale (Auckland Region, New Zealand) project and broader regulatory setting. The primary data collection was conducted during 2018–19. Key institutions were selected, and a comprehensive list of interviewees was purposefully selected as a sample, especially because expert sampling (i.e., purposive sampling approach) has been widely used and been effective in research studies of this nature (Hwang et al., Citation2013; Osei-Kyei et al., Citation2017; Tang et al., Citation2010). A range of professions and roles were interviewed due to their in-depth understanding of the case study and the wider strategic and intellectual knowledge of infrastructure charging. Professions were largely from a ‘top-down’ informed perspective, and they ranged from financiers, policy-makers, bankers, investors, authorities at various governance levels (national, regional, municipal), developers, planners, academics and consultants. Roles ranged from directors, chief executive officers (CEOs), senior officers, executives, and professors.

A snow-ball technique was adopted whilst being mindful of the drawbacks in bias and breath of informants, and the snow-ball technique also helped to increase the number of high-quality interviewees (Denzin & Lincoln, Citation2007; Hutchison et al., Citation2016). The depth of quality and range of perspectives and professions was seen to hold rigour, as convergence and divergence of points and themes presented themselves in the analysis (Denzin & Lincoln, Citation2007). We selected the sample size not only using the expert sampling approach that has been widely employed in research studies (Ameyaw & Albert, Citation2015; Osei-Kyei et al., Citation2017) but also purposively narrowing the study sample to leading people that come from the selected institutions, as shown in . This purposive approach assisted the study by providing both expert-level implications and insightful exclusive information extracted from the semi-structured interviews; hence, this method somehow led to a smaller sample size than normal. Also, the low response rate is not uncommon in the literature (Akintoye & Fitzgerald, Citation2000), and it is within a range of figures obtained in similar studies. For instance, Effiong (Citation2015) obtained 38 questionnaires; Abidoye et al. (Citation2018) obtained a total of 21 interviewees; especially Wilkinson et al. (Citation2017) obtained a lower response rate of 25 responses out of over 8000 valuers sampled in Australia. Although a low response rate of approximately 14% is recorded, the sample size of 42 is considered reasonable when compared with similar studies (Zhang, Citation2005, Citation2006) with 46 responses (Osei-Kyei et al., Citation2017) with 42 responses. Nonetheless, small samples are not uncommon in an international email/web-survey based research in PPP studies; for instance, Ernest and Albert (Citation2015) acquired 35 responses out of 326; and Sachs et al. (Citation2007) acquired 29 responses. In addition, the number of industrial and/or research years of experience in PPPs and diverse cultural backgrounds of experts contribute to the reliability and genuineness of the survey responses (Osei-Kyei et al., Citation2017). A detailed background of experts is shown in and in Appendix A in the supplemental data online.

Table 1. Institutions that contributed to the primary data collection.

Hence, this study implemented a final sample size of 19 semi-structured interviews with leading senior experts, key stakeholders and policy-makers, from both public and private sectors, who have the long-run experience to provide insightful perspective exclusively to the development of infrastructure finance in the country. The 19 formal and informal interviews were undertaken in a deductive process whereby answers to the questions were semi-structured and open to illicit richer qualitative understanding (Mason, Citation2017). To investigate qualitatively the relation between bulk infrastructure and housing charges, the researchers used semi-structured interviews with experts from NGOs, local to central government who have long-run experience in infrastructure development and investment in terms of the policy, regulation and direct decision-making. All interviewees were in senior positions at the time of interviewing; the roles of the selected interviewees include senior investment strategist, central government minister(s), director(s), portfolio manager, general manager(s) in development and financing planning, executive director(s), senior executive, chief executive(s), chair, partner, deputy chief executive and principal researcher. To be effective in collecting opinions from the interviewed experts, the researchers adopted open questions around the main themes, such as bulk infrastructure and innovative finance.

Content theme analysis of the terms of being ‘innovative’ when using housing charges to finance bulk infrastructure

After completing semi-structured interviews, the interview transcripts were coded by the main themes based on the information provided by the experts using QSR NVivo 10 software (QSR International, Citation2020) as the qualitative research software. The percentage results of each theme were then visualized by each interviewed expert. For instance, for each interview transcript, the response percentage of interviewees on a discussed theme is coded; the higher the response percentage of a specific theme, the higher the concern recorded from the experts. presents the interviewees’ institutions that contributed to the primary data collection through the semi-structured interviews. These interviewees also represent the ‘organizational elite’ and possessed substantial experience in the public and private sector working at top management-level positions.

Further, semi-structured interview questions provide a practical understanding of the case and widened answers to discuss how the housing charge financing approach was ‘innovative’. It was important at a broad level to bring out respondents’ thoughts as to what innovation meant, and how innovation was enabled. Analysis of the interview data involved categorizing key issues and themes that emerged and highlighting relevant quotations to evidence of the narrative.

Like any research method, there are various limitations and drawbacks that need to be highlighted. A single in-depth case study will have some contextual considerations, and bias, if applied and generalized to other cases in Auckland, New Zealand and elsewhere. Given the greenfield nature of the case study, views of the potential residents were unable to capture. Future studies could investigate residents’ concerns in proximity to the site or those residents directly gaining or losing from the site development. However, the large scale and high profile of the pilot raises some desires by stakeholders to replicate the model, so will need some practical and theoretical reflection from this research. Data visualization was based on the response parentage of the interviewees on each theme discussed; however, when coding the interviewed transcripts, it may lead to some unexpected mistakes in terms of recording, transcription and converting the transcript in word to numeric for data visualization.

CASE STUDY: A SITE-BASED MULTI-INSTITUTIONAL FINANCIAL MODEL

The case study of the geographical site and financial model was used to identify and interrogate key issues in policy and practice of housing charges to finance infrastructure. We used a case study of the Milldale development in the Auckland region. Milldale is selected as a pilot project that uses housing charges to pay back infrastructure costs. This approach is something new and novel for New Zealand. The site is to support approximately 4000 sections, plus an additional 5000 dwellings in the surrounding area (CIP, Citation2019a). The large site case of Milldale operates in part with the Auckland housing market, albeit at a distance to the central core in the northern suburbs on a greenfield land. Auckland city is the dominant housing and commercial market in New Zealand. It has the largest population of residents in New Zealand at 1,534,700 people, which is 34% of the population (Statistics, Citation2020).

To give some introduction to the financial model of the case study, the principal legal entity is managed by the central government called the Crown Infrastructure Partnership (CIP). The estimated total cost of the bulk housing infrastructure in the case study is NZ$91.3 million (CIP, Citation2019b). The case has a cost contribution by Auckland City Council of NZ$33.5 million, which is to be recouped by future developer contributions in the site and future urban zone (Orsman, Citation2018). A further cost contribution of NZ$48.9 million is contributed by the SPV established by the CIP largely containing Accident Compensation Corporation (ACC) debt and CIP equity provision (CIP, Citation2019a). The remaining cost contribution of NZ$8.9 million is provided by the developer Fulton Hogan Land Development. The repayment of these contributions (beyond the developer contributions and CIP equity provision of NZ$3.7 million) is by section owner purchasers at a prescribed rate over 30 years. The payments are the responsibility of the developers until the legal right (encumbrance) is transferred to the section owner purchasers, and the owners of new homes in North of Auckland will pay an ‘infrastructure fee’ collected by Auckland City Council to payback the roading and water work (Orsman, Citation2018).

DATA VISUALIZATION OF INFRASTRUCTURE FUNDING AND FINANCING THEMES

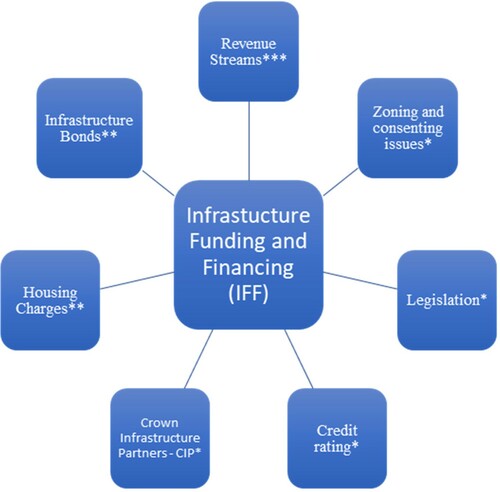

Based on given insightful information from the experts through semi-structured interviews, the study provided several key findings in terms of pressing themes put forward. First, presents the key themes discussed by the interviewees regarding IFF models. The concerns included a range of related issues such as revenue streams, credit rating, legislation and consenting/zoning issues. The study selected the main important themes that were indicated by the informants regarding the finance and funding models. The star characters of ***, ** and * present the highest, medium, and the lowest level of concern on each theme indicated by the interviewees, respectively. For example, revenue streams have attached a character of *** presenting that the interviewees showed the most serious concern about revenue streams regarding the infrastructure finance and funding models; in other words, it was implied by respondents that revenue streams are a very important component to finance infrastructure projects. Infrastructure bonds and housing charges both received a character of ** indicating that they had a good concern from the experts regarding the IFF models. The interviewees also gave concern to other aspects associated with the IFF models, and they were credit rating, CIP, legislation, zoning and consenting issues in which they received a character of * for the concern level.

Figure 2. Key themes of the infrastructure funding and financing (IFF) model.

Note: The symbols ***, ** and * indicate the concern level of the interviewed experts from the highest, medium, to the lowest regarding the IFF model, respectively.Source: Authors; extracted from the semi-structured interviews.

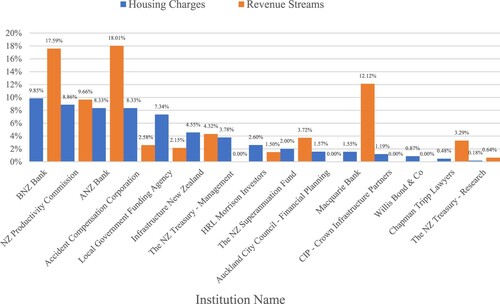

The findings turned their attention on the three key main findings in the content analysis, and these include housing charges, revenue streams and infrastructure bonds. For housing charges, highlights the percentage coverage of using housing charges in bulk infrastructure from the experts during the interviews. Each column presents the response of the interviewed expert(s) from the selected institution. indicates the percentage coverage of housing charges and revenue streams in bulk infrastructure by each selected institution during the semi-structured interviews. To understand the chart, the higher the percentage coverage given, the higher the concern about using housing charges from the interviewed experts to generate revenue streams to payback infrastructure bonds for long-term infrastructure projects.

Figure 3. Percentage coverage of housing charges and revenue streams by institution.

shows that experts from BNZ Bank, the Productivity Commission, ANZ Bank and the ACC have the greatest concern about using housing charges as an effective instrument to generate a revenue stream to payback infrastructure projects. The coverage percentages are 9.85%, 8.86% and 8.33%, respectively. For example, for the semi-structured interview with BNZ Bank’s experts, shows that the experts spent 9.85% of the time during the interview discussing housing charges in bulk infrastructure finance, implying their great concern for using housing charges. Especially, some experts indicated that housing charges are only innovative in terms of mechanics, legislation and political settings, while other experts argued that housing charges are a traditional mechanism to generate cash flows from private funds to finance bulk infrastructure. In general, from the example of the Milldale project, the experts imply that using housing charges is currently an effective instrument to attract revenue streams from private funds to finance long-term infrastructure projects.

Besides an array of factors to determine whether housing charges are an innovation in financing bulk infrastructure, the primary data collected from the semi-structured interviews imply that they are known as an innovative instrument in New Zealand, but they have been used around the globe for financing infrastructure development. Also, experts are greatly concerned about the issues of credit rating, zoning, consenting and legislative settings for bulk infrastructure in New Zealand, implying that local and central government play a crucial role in generating a facilitating environment when attracting private funds using housing charges ().

For revenue stream considerations, highlights the percentage coverage of revenue streams in the IFF model from the experts during the interviews. Each column presents the response of the expert(s) from the selected institution. shows that experts from the banking sector are greatly concerned about revenue streams as the main financing constraints in bulk infrastructure development. In other words, they argue that having sufficient revenue streams (future cash flow) is one of the most concerning issues within the infrastructure finance and funding model to payback infrastructure bonds. shows that the experts of the ANZ Bank and BNZ Bank discussed revenue streams in the development of bulk infrastructure with a coverage rate of 18% of the interview time. The high coverage percentage during the semi-structured interviews shows that revenue streams are very crucial when using IFF in bulk infrastructure and housing.

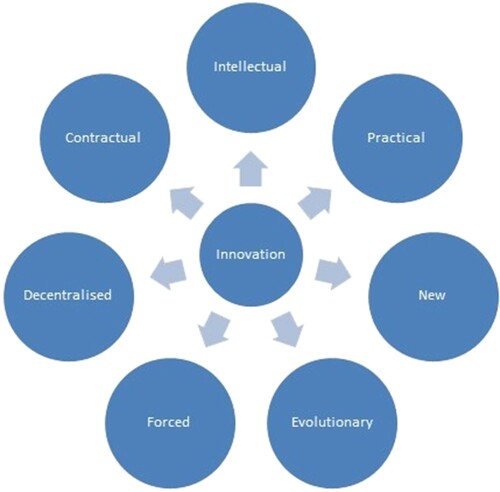

The main findings shown in indicate that banking experts have the greatest concern about using housing charges to generate revenue streams to payback bulk infrastructure and to produce more housing for the next generations in New Zealand. It also shows a general positive relationship between housing charges and revenue streams in financing bulk infrastructure in the context of New Zealand, indicating that experts with a high concern for revenue streams show a relative higher percentage coverage of using housing charges during the interviews. By extracting the quotations of the experts, the following section provides a conceptual framework for innovative approaches in the IFF as presented in . The section further supports the visualized content themes and contributes a better understanding of the IFF model being piloted.

Figure 4. The innovative approach to the funding and financing infrastructure.

Source: Authors.

INNOVATION FRAMEWORK FOR FUNDING AND FINANCING INFRASTRUCTURE

This section now develops a relational framework that draws out several innovation approaches when studying IFF (). First, the funding model was perceived as innovative in that the model was never fixed and evolved through negotiations. In this sense, the case study exemplified what we term here ‘evolutionary innovation’, particularly as the model evolved as discussions took place on the best course of policy development. Findings during the study clarified who was involved in the case study and what finance model evolved as the financial ‘package’ and policy took root. The evolution led to a high debt model, but one that included a high level of low-interest patient capital lending, as one of the interviewees stated:

With the debt though, we decided that we would have a significant amount in debt in our first deal. We decided that we would leverage it quite high. … The ACC [Accident Compensation Corporation – a National Insurance Health Provider] solution worked really well, because it was a long-term solution for us. Completely locked in. There was no exposure for us required. The total cost of the transaction was enormously attractive. It was the longest-term money raised in New Zealand, and the total rate would’ve been one of the best-priced transactions in New Zealand … it’s less than 6%. (Crown Infrastructure Partners)

Third, for the case study more generally, it was found that the eventual settling of a contractual model was still to some extent considered by interviewees as innovative. As such, despite the idea of a contact being nothing new or creative over millennia, we can put forward for this study the use of a ‘contractual innovation’. Contractual innovation in this case study included two key pillars. The first was over who puts in what debt or equity amount, and what the returns and ownerships would be expected over a set period. The second pillar of the contractual model was the certainty of the income stream. With which the local authority can invoice the partnership a charge on their rating invoice to the household.

As such, the conceptual model case in focus had a level of imagination and creative ideas (), whilst also transcending this level to apply a better practical implementable solution, as well as a more effective business model for the New Zealand infrastructure and housing market. We also see in this ‘contractual model’ a finance vehicle that engages with a combination of risk-bearing tools.

It was found that bulk-infrastructure finance was targeted to be the best possible way to ‘force through’ new developments at scale. What we describe is a type of ‘forced innovation’. These new developments of guaranteed road and water services could then connect physically and financially to ‘other’ integrated infrastructure needs and requirements. Further, the less visible raising of public money via a user charge on housing (similar to rates) rather than road (e.g., toll roads) was important to getting the infrastructure financed and built. Some of the partners are forthright about the end goal of ‘any development’ justifying the means through a forced funding and financing model for bulk infrastructure, namely providing water and transport. For instance, ‘Transport’s particularly problematic because, to date, there has been not any willingness for anyone to take the risk on particularly bulk transport infrastructure’ (Infrastructure New Zealand). The larger conversation was articulated around the central government not being willing or able to directly fund major bulk infrastructure projects. Hence, the need to find more innovative funding and financing had been done traditionally. It was argued that the central public (crown) balance sheet is not large enough to pay for all the desired infrastructure requirements. Similarly, the local authority could also not have a balance sheet large enough to fund this infrastructure requirement, particularly as the local authority’s credit rating would be affected if too much debt were incurred.

This focus on ‘decentralized innovation’ in governance considers a financial risk, but with the de-risking of a project through regulatory powers rather than financial resource powers. Put another way, local authorities are given more of a stake in the project compared with central authorities. However, the local authority defers risk itself by being in a partnership, whilst de-risking the project by bringing in its regulatory powers to collect local rates as well as the local authority being able to keep the funding liability for any infrastructure being kept off the public balance sheet.

What is of greater constraint in this decentralization innovation new direction is that the local authority debt–revenue restrictions are set against the business model in developing a site, whereas central government restrictions will be set more against the growth of economic development more broadly. As such, debt–revenue restrictions are more of an issue for local authorities rather than central government. Local authority borrowing is undertaken against future rates and developer contributions, whereas central government borrowing is justified on future economic growth. For local authorities, compared with the central government, borrowing ‘cannot get too far in front’ of what economic growth will look like in the future, especially in realizing the development value once development is completed.

For this case study, debt ceilings may be more of a problem for Auckland City Council than for central government. This is particularly interesting as central government institutions (e.g., CIP) are paying less of a financial stake in the project. This means the case study model is not entirely a value-capture innovation that considers uplift in values over time, but more of a PPP arrangement that takes a traditional mix of partners, but with the public local authority provider underwriting rather than directly funding. To illustrate this decentralization of power and deferred risk by the local authority, some interviewees stated that:

but the Crown could never supply all the capital that is necessary for us to meet our aspirations in terms of the infrastructure and the development for urban growth. (New Zealand Central Government)

We would say the financing constraint is a mix of technical and behavioural issues. Technical issues around things like covenants or restrictions; and then behavioural willingness for councils to have higher levels of debt. Typically, people don’t like that. (New Zealand Treasury)

I don’t think it’s a rocket science what we’re doing here, we’re trying to find practical solutions. There are a lot of other sophisticated models used around the world. I look at it, it’s an innovative model in the sense that it’s different to the traditional approach. (Auckland City Council)

Also, the pandemic unfolds a concern about policy responses to the sustainability of urban infrastructure financing and regional economies in overall, for instance, climate changes, new deals and sustainable revolution (Gibbs, Citation2018), political and governance dimensions of the pandemic (Dodds et al., Citation2020), or in terms of growth opportunities, social responsibilities, economic productivity, housing, industry and land-development reform (Milani, Citation2021; Queensland Policy Forum, Citation2020). The financial innovation in infrastructure as well as other asset classes in general, also needs a further elaboration of other related factors, including asset price volatility, expected returns and pricing (Henderson & Pearson, Citation2011; Kubler & Schmedders, Citation2012), neglected risk, financial and technological evolution (Hsu et al., Citation2014; Rooney et al., Citation2013), political, public and other barriers (Badu et al., Citation2012; Christophers, Citation2018; Fostel & Geanakoplos, Citation2016), especially regulation and its role during a global crisis (Kim et al., Citation2013).

CONCLUSIONS

The question of using housing charges to fund and finance housing and bulk infrastructure projects has not been fully investigated around the world, and particularly in New Zealand, until now, at least not to consider whether this is anything innovative. This paper has discussed how bulk infrastructure development using housing charges is innovative by being a newly adopted instrument. This study theoretically contributes to the recent studies of O’Brien et al. (Citation2019), O’Neill (Citation2019) and O’Brien and Pike (Citation2019) by adding ‘housing charges’ as the newer ‘innovative’ vehicle in infrastructure funding, financing and financialization. It also implies the recent trend in using ‘housing charges’ along with ‘infrastructure charges’ of Bryant (Citation2017) for financing infrastructure development in Australasia.

The study qualitatively contributes to the literature with three main findings. First, housing charges are only innovative in terms of mechanics, legislation and policy settings. However, housing charges are newly used and somewhat known as an innovation to generate sufficient cash flows to finance bulk infrastructure in New Zealand. Second, the high performance of bulk infrastructure accelerates the growing supplies of housing from the experts’ perspective, leading to a consequential concern implied by the experts about the development of transportation and water infrastructure. Third, the experts indicate that sufficient revenue streams are one of the most concerning issues when long-term infrastructure projects often require large up-front capital amounts from investors, while there is a lack or no guarantee that a constant stream of future cash flows is generated by the projects sufficiently to pay back the investors using the IFF approach in bulk infrastructure.

In terms of limitations and future research, this study was held at the national level due to the exclusive expert sampling approach leading to the small sample size, but appropriate for the final sample of 19 semi-structured interviews with leading senior experts and policy-makers in New Zealand. However, to fulfil this sample limitation, an empirical examination at a multinational or cross-regional level in using housing charges to finance bulk infrastructure is expected to investigate in future studies contributing to the literature. Moreover, combining secondary data from various research databases with qualitative interviews is promising in order to have a more quantitative examination using a mixed method to examine the role of housing charges in infrastructure financing. Finally, given the existing Covid-19 pandemic, there will be a multitude of economic and regional impacts (Bailey et al., Citation2020). Therefore, the sustainability and resilience of innovation to Infrastructure Funding and Financing (IFF) will need to adapt to any future shocks.

ACKNOWLEDGEMENTS

The authors acknowledge and thank all the interviewees who participated in this study and gave freely of their time.

DISCLOSURE STATEMENT

No potential conflict of interest was reported by the authors.

REFERENCES

- Aalbers, M. B. (2017). The variegated financialization of housing. International Journal of Urban and Regional Research, 41(4), 542–554. https://doi.org/https://doi.org/10.1111/1468-2427.12522

- Abdel Aziz, A. M. (2007). Successful delivery of public–private partnerships for infrastructure development. Journal of Construction Engineering and Management, 133(12), 918–931. https://doi.org/https://doi.org/10.1061/(ASCE)0733-9364(2007)133:12(918)

- Abidoye, R., Chan, A., & Oppong, D. (2018) Property valuation practice in developed countries: A case of Hong Kong’. Proc., RICS COBRA Conference, London, 23–24.

- Addie, J.-P. D., Glass, M. R., and Nelles, J. (2020). Regionalizing the infrastructure turn: A research agenda. Regional Studies, Regional Science, 7(1), 10–26. https://doi.org/https://doi.org/10.1080/21681376.2019.1701543

- Akintoye, A., & Fitzgerald, E. (2000). A survey of current cost estimating practices in the UK. Construction Management and Economics, 18(2), 161–172. https://doi.org/https://doi.org/10.1080/014461900370799

- Ameyaw, E., & Albert, P. C. (2015). Risk ranking and analysis in PPP water supply infrastructure projects: An international survey of industry experts. Facilities, 33(7/8), 428–453. https://doi.org/https://doi.org/10.1108/F-12-2013-0091

- Andrés, L., Biller, D., & Dappe, M. H. (2014). Infrastructure gap in South Asia: Infrastructure needs, prioritization, and financing. The World Bank.

- Ashton, P., Doussard, M., & Weber, R. (2012). The financial engineering of infrastructure privatization: What are public assets worth to private investors? Journal of the American Planning Association, 78(3), 300–312. https://doi.org/https://doi.org/10.1080/01944363.2012.715540

- Badu, E., Edwards, D. J., Owusu-Manu, D., & Brown, D. M. (2012). Barriers to the implementation of innovative financing (IF) of infrastructure. Journal of Financial Management of Property and Construction, 17(3), 253–273. https://doi.org/https://doi.org/10.1108/13664381211274362

- Bailey, D., Clark, J., Colombelli, A., Corradini, C., De Propris, L., Derudder, B., Fratesi, U., Fritsch, M., Harrison, J., Hatfield, M., Kemeny, T., Kogler, D. F., Lagendijk, A., Lawton, P., Ortega-Argilés, R., Otero, C. I., & Usai, S. (2020). Regions in a time of pandemic. Regional Studies, 54(9), 1163–1174. https://doi.org/https://doi.org/10.1080/00343404.2020.1798611

- Baum-Snow, N., & Marion, J. (2009). The effects of low income housing tax credit developments on neighborhoods. Journal of Public Economics, 93(5–6), 654–666. https://doi.org/https://doi.org/10.1016/j.jpubeco.2009.01.001

- Bryant, L. (2017). Housing affordability in Australia: An empirical study of the impact of infrastructure charges. Journal of Housing and the Built Environment, 32(3), 559–579. https://doi.org/https://doi.org/10.1007/s10901-016-9527-0

- Cantafio, G. U., and Ryan, S. (2020). Incorporating innovation metrics in urban indices: The Sustain-LED Index. Regional Studies, Regional Science, 7(1), 133–163. https://doi.org/https://doi.org/10.1080/21681376.2020.1760731

- Carter, A. (2006). Building an investment market for economic development. Local Economy: The Journal of the Local Economy Policy Unit, 21(1), 65–72. https://doi.org/https://doi.org/10.1080/02690940500478084

- Christophers, B. (2018). Risking value theory in the political economy of finance and nature. Progress in Human Geography, 42(3), 330–349. https://doi.org/https://doi.org/10.1177/0309132516679268

- CIP. (2019a). Crown infrastructure partners – Milldale development bulk housing infrastructure – questions and answers. https://www.crowninfrastructure.govt.nz/wp-content/uploads/2018/11/Milldale-QA-FINAL-12-Nov.pdf

- CIP. (2019b). Building together–annual report 2019. Crown Infrastructure Partners (CIP) Limited.

- Clark, E., Larsen, H. G., & Hansen, A. L. (2015). Financialisation of built environments: A literature review.

- Crabbe, A. E., Hiatt, R., Poliwka, S. D., & Wachs, M. (2005). Local transportation sales taxes: California's experiment in transportation finance. Public Budgeting & Finance, 25(3), 91–121. https://doi.org/https://doi.org/10.1111/j.1540-5850.2005.00369.x

- Cui, C., Liu, Y., Hope, A., & Wang, J. (2018). Review of studies on the public–private partnerships (PPP) for infrastructure projects. International Journal of Project Management, 36(5), 773–794. https://doi.org/https://doi.org/10.1016/j.ijproman.2018.03.004

- Denzin, N. K., & Lincoln, Y. (2007). Strategies of qualitative inquiry (3ed ed.). Sage.

- Dodds, K., Broto, V. C., Detterbeck, K., Jones, M., Mamadouh, V., Ramutsindela, M., Varsanyi, M., Wachsmuth, D., & Woon, C. Y. (2020). The COVID-19 pandemic: Territorial, political and governance dimensions of the crisis. Taylor & Francis.

- Effiong, J. B. (2015). A comparative study of valuation variance and accuracy between Nigeria and UK. International Letters of Social and Humanistic Sciences, 57, 94–105. https://doi.org/https://doi.org/10.18052/www.scipress.com/ILSHS.57.94

- Eriksen, M. D. (2009). The market price of low-income housing tax credits. Journal of Urban Economics, 66(2), 141–149. https://doi.org/https://doi.org/10.1016/j.jue.2009.06.001

- Ernst & Young. (2014). Superannuation investment in infrastructure: Steps to further efficiency. Financial Services Council.

- Ersoy, A. (2017). Smart cities as a mechanism towards a broader understanding of infrastructure interdependencies. Regional Studies, Regional Science, 4(1), 26–31. https://doi.org/https://doi.org/10.1080/21681376.2017.1281154

- Ersoy, A., and Alberto, K. C. (2019). Understanding urban infrastructure via big data: The case of Belo Horizonte. Regional Studies, Regional Science, 6(1), 374–379. https://doi.org/https://doi.org/10.1080/21681376.2019.1623068

- Estache, A., Serebrisky, T., & Wren-Lewis, L. (2015). Financing infrastructure in developing countries. Oxford Review of Economic Policy, 31(3–4), 279–304. https://doi.org/https://doi.org/10.1093/oxrep/grv037

- Fostel, A., & Geanakoplos, J. (2016). Financial innovation, collateral, and investment. American Economic Journal: Macroeconomics, 8(1), 242–284. https://doi.org/https://doi.org/10.1257/mac.20130183

- Gibbs, D. (2018). Sustainability transitions and green regional economies. Regions.

- Gielen, D. M., & van der Krabben, E. (2019). Public infrastructure, private finance: Developer obligations and responsibilities. Routledge.

- Giliberto, M. (1990). Equity real estate investment trusts and real estate returns. Journal of Real Estate Research, 5(2), 259–263. https://doi.org/https://doi.org/10.1080/10835547.1990.12090615

- Global Infrastructure Hub. (2016). Global infrastructure outlook. Oxford Economics and Global Infrastructure Hub A G20 Initiative.

- Grafe, F.-J. (2020). Finance, water infrastructure, and the city: Comparing impacts of financialization in London and Mumbai. Regional Studies, Regional Science, 7(1), 214–231. https://doi.org/https://doi.org/10.1080/21681376.2020.1778515

- Grafe, F.-J., & Mieg, H. A. (2019). Connecting financialization and urbanization: The changing financial ecology of urban infrastructure in the UK. Regional Studies, Regional Science, 6(1), 496–511. https://doi.org/https://doi.org/10.1080/21681376.2019.1668291

- Greenhalgh, P., & Purewal, B. (2015). Challenging the Myths: An investigation of the barriers to wider use of local asset backed vehicles in the UK. Journal of Urban Regeneration & Renewal, 8(3), 260–278.

- Greenhalgh, B., & Squires, G. (2011). Introduction to building procurement. Routledge.

- Grishankar, N. (2009). Innovating development finance: From financing Sources to financial solutions [online]. The World Bank.

- Hargreaves, D. (2018). Special purpose vehicle will fund $91 mln of infrastructure to support building of 9,000 homes at Wainui, north of Auckland. https://bit.ly/3fIdMTD.

- Henderson, B. J., & Pearson, N. D. (2011). The dark side of financial innovation: A case study of the pricing of a retail financial product. Journal of Financial Economics, 100(2), 227–247. https://doi.org/https://doi.org/10.1016/j.jfineco.2010.12.006

- Hsu, P.-H., Tian, X., & Xu, Y. (2014). Financial development and innovation: Cross-country evidence. Journal of Financial Economics, 112(1), 116–135. https://doi.org/https://doi.org/10.1016/j.jfineco.2013.12.002

- Hutchison, N., Squires, G., Adair, A., Berry, J., Lo, D., McGreal, S., and Organ, S. (2016). Financing infrastructure development: Time to unshackle the bonds? Journal of Property Investment & Finance, 34(3), 208–224. https://doi.org/https://doi.org/10.1108/JPIF-07-2015-0047

- Hwang, B.-G., Zhao, X., & Gay, M. J. S. (2013). Public private partnership projects in Singapore: Factors, critical risks and preferred risk allocation from the perspective of contractors. International Journal of Project Management, 31(3), 424–433. https://doi.org/https://doi.org/10.1016/j.ijproman.2012.08.003

- Kane, E. J. (1981). Accelerating inflation, technological innovation, and the decreasing effectiveness of banking regulation. The Journal of Finance, 36(2), 355–367. https://doi.org/https://doi.org/10.1111/j.1540-6261.1981.tb00449.x

- Kim, T., Koo, B., & Park, M. (2013). Role of financial regulation and innovation in the financial crisis. Journal of Financial Stability, 9(4), 662–672. https://doi.org/https://doi.org/10.1016/j.jfs.2012.07.002

- Klein, M. (2009). Tax credit bonds. CitiBank Investment Management Review, 11, 27–31.

- Knowles, R. D. (2012). Transit oriented development in Copenhagen, Denmark: From the finger plan to Ørestad. Journal of Transport Geography, 22, 251–261. https://doi.org/https://doi.org/10.1016/j.jtrangeo.2012.01.009

- Koh, J. M. (2018). Green infrastructure financing. Springer Books.

- Kubler, F., and Schmedders, K. (2012). Financial innovation and asset price volatility. American Economic Review., 102(3), 147–151. https://doi.org/https://doi.org/10.1257/aer.102.3.147

- Laing, B. Y. (2009). Organizing community and labor coalitions for community benefits agreements in African American communities: Ensuring successful partnerships. Journal of Community Practice, 17(1–2), 120–139. https://doi.org/https://doi.org/10.1080/10705420902862124

- Li, G., Luan, X., Yang, J., & Lin, X. (2013). Value capture beyond municipalities: Transit-oriented development and inter-city passenger rail investment in China’s Pearl River Delta. Journal of Transport Geography, 33, 268–277. https://doi.org/https://doi.org/10.1016/j.jtrangeo.2013.08.015

- Lord, A. (2009). The community infrastructure levy: An information economics approach to understanding infrastructure provision under England's reformed spatial planning system. Planning Theory & Practice, 10(3), 333–349. https://doi.org/https://doi.org/10.1080/14649350903229778

- Maranville, S. (1992). Entrepreneurship in the business curriculum. Journal of Education for Business, 68(1), 27–31. https://doi.org/https://doi.org/10.1080/08832323.1992.10117582

- Martin, I. (2006). Does school finance litigation cause taxpayer revolt? Serrano and Proposition 13. Law & Society Review, 40(3), 525–558. https://doi.org/https://doi.org/10.1111/j.1540-5893.2006.00272.x

- Mason, J. (2017). Qualitative researching. Sage.

- Medda, F. (2012). Evaluation of value capture mechanisms as a funding source for urban transport: The case of London's Crossrail. Procedia – Social and Behavioral Sciences, 48, 2393–2404. https://doi.org/https://doi.org/10.1016/j.sbspro.2012.06.1210

- Medda, F. R., Caschili, S., & Modelewska, M. (2011). Innovative financial mechanisms for urban heritage brownfields. Journal of Financial Management Practices, 11(2), 245–255.

- Merk, O., Saussier, S., Staropoli, C., Slack, E., & Kim, J.-H. (2012). Financing green urban infrastructure.

- Milani, F. (2021). COVID-19 outbreak, social response, and early economic effects: A global VAR analysis of cross-country interdependencies. Journal of Population Economics, 34(1), 223–252. https://doi.org/https://doi.org/10.1007/s00148-020-00792-4

- Miller, M. H. (1986). Financial innovation: The last twenty years and the next. The Journal of Financial and Quantitative Analysis, 21, 459–471. https://doi.org/https://doi.org/10.2307/2330693

- Morrison, N., & Burgess, G. (2014). Inclusionary housing policy in England: The impact of the downturn on the delivery of affordable housing through section 106. Journal of Housing and the Built Environment, 29(3), 423–438. https://doi.org/https://doi.org/10.1007/s10901-013-9360-7

- Ng, A., & Loosemore, M. (2007). Risk allocation in the private provision of public infrastructure. International Journal of Project Management, 25(1), 66–76. https://doi.org/https://doi.org/10.1016/j.ijproman.2006.06.005

- O’Brien, P., O’Neill, P., & Pike, A. (2019). Funding, financing and governing urban infrastructures. Urban Studies, 56(7), 1291–1303. https://doi.org/https://doi.org/10.1177/0042098018824014

- O’Brien, P., & Pike, A. (2019). ‘Deal or no deal?’ Governing urban infrastructure funding and financing in the UK City Deals. Urban Studies, 56(7), 1448–1476. https://doi.org/https://doi.org/10.1177/0042098018757394

- O’Neill, P. (2019). The financialisation of urban infrastructure: A framework of analysis. Urban Studies, 56(7), 1304–1325. https://doi.org/https://doi.org/10.1177/0042098017751983

- Orsman, B. (2018). Buying a section in a new development north of Auckland will come with an ‘infrastructure payment’ tagged onto rates bill. The New Zealand Herald.

- Osei-Kyei, R., Chan, A. P., Javed, A. A., & Ameyaw, E. E. (2017). Critical success criteria for public–private partnership projects: International experts’ opinion. International Journal of Strategic Property Management, 21(1), 87–100. https://doi.org/https://doi.org/10.3846/1648715X.2016.1246388

- QSR International. (2020). NVivo 10 for Windows. https://bit.ly/39g6Pa9.

- Queensland Policy Forum. (2020). Making the Change–New thinking and bold ideas: Long-term post COVID-19 strategy and policy initiatives for the development of Queensland and its regions, Supporting document, Brisbane.

- Rooney, D., Mandeville, T., & Kastelle, T. (2013). Abstract knowledge and reified financial innovation: Building wisdom and ethics into financial innovation networks. Journal of Business Ethics, 118(3), 447–459. https://doi.org/https://doi.org/10.1007/s10551-012-1595-9

- Sachs, T., Tiong, R., & Wang, S. Q. (2007). Analysis of political risks and opportunities in public–private partnerships (PPP) in China and selected Asian countries. Chinese Management Studies.

- Spence, J., Smith, J., & Dardier, P. (2012). Overview of financial instruments used in the EU multiannual financial framework period 2007–2013 and the Commission’s proposals for 2014–2020. In Directorate-General for Internal Policies – Analytical Study. Brussels: European Parliament.

- Spilanis, I., Kizos, T., & Giordano, B. (2016). The effectiveness of European regional development fund projects in Greece: Views from planners, management staff and beneficiaries. European Urban and Regional Studies, 23(2), 182–197. https://doi.org/https://doi.org/10.1177/0969776413498761

- Squires, G. (2012). A review of Tax Increment financing (TIF) for regeneration and renewal. Journal of Urban Regeneration and Renewal, 5(4), 356–366.

- Squires, G. (2014). Future financing of Cities for real estate development. RICS (Royal Institution of Chartered Surveyors).

- Squires, G. (2017). Mechanisms for financing affordable housing development. Routledge Companion to Real Estate Development.

- Squires, G., & Hall, S. (2013). Lesson (un) learning in spatially targeted fiscal incentive policy: Enterprise zones (England) and Empowerment zones (United States). Land use Policy, 33, 81–89. https://doi.org/https://doi.org/10.1016/j.landusepol.2012.12.010

- Squires, G., Heurkens, E., & Peiser, R. (2017). Routledge Companion to real estate development. Routledge.

- Squires, G., & Hutchison, N. (2014). The life and death of Tax Increment Financing (TIF) for redevelopment: Lessons in affordable housing and implementation. Journal of Property Management, 32(5), 368–377. https://doi.org/https://doi.org/10.1108/PM-07-2013-0037

- Squires, G., Hutchison, N., Berry, J., Adair, A., McGreal, S., & Organ, S. (2016). Innovative real estate development finance – Evidence from Europe. Journal of Financial Management of Property and Construction, 21(1), 54–72. https://doi.org/https://doi.org/10.1108/JFMPC-09-2015-0036

- Squires, G., & Lord, A. (2017). The uneven Geography of financing cities through a betterment tax: Using the Community Infrastructure Levy (CIL) in England. Delft, Netherlands: European Real Estate Society (ERES).

- Squires, G., & Lord, A. D. (2012). The transfer of Tax Increment Financing (TIF) as an urban policy for spatially targeted economic development. Land Use Policy, 29(4), 817–826. https://doi.org/https://doi.org/10.1016/j.landusepol.2011.12.007

- Starrett, D. A. (1981). Land value capitalization in local public finance. Journal of Political Economy, 89(2), 306–327. https://doi.org/https://doi.org/10.1086/260967

- Statistics, N. Z. (2020). Subnational population estimates. https://www.stats.govt.nz/topics/population/

- Strickland, T. C. (2016). Funding and financing urban infrastructure: A UK–US comparison. Newcastle University.

- Tang, L., Shen, Q., & Cheng, E. W. (2010). A review of studies on public–private partnership projects in the construction industry. International Journal of Project Management, 28(7), 683–694. https://doi.org/https://doi.org/10.1016/j.ijproman.2009.11.009

- Twyford, H. P. (2018). Major infrastructure partnership for North Auckland.

- Walker, M. (2018). New funding mechanisms for growth. The New Zealand Herald.

- Wall, A., & Connolly, C. (2009). The private finance initiative: An evolving research agenda? Public Management Review, 11(5), 707–724. https://doi.org/https://doi.org/10.1080/14719030902798172

- Wilkinson, S., Antoniades, H., & Halvitigala, D. (2017). The future of the valuation profession.

- Woetzel, J., Garemo, N., Mischke, J., Hjerpe, M., & Palter, R. (2016). Bridging global infrastructure gaps. McKinsey Global Institute, 199–217.

- Woo, A., Joh, K., & Van Zandt, S. (2016). Unpacking the impacts of the low-income housing tax credit program on nearby property values. Urban Studies, 53(12), 2488–2510. https://doi.org/https://doi.org/10.1177/0042098015593448

- Yusuf, J.-E., O’Connell, L., Hackbart, M., & Liu, G. (2010). State infrastructure banks and borrowing costs for transportation projects. Public Finance Review, 38(6), 682–709. https://doi.org/https://doi.org/10.1177/1091142110373606

- Zhang, X. (2005). Critical success factors for public–private partnerships in infrastructure development. Journal of Construction Engineering and Management, 131(1), 3–14. https://doi.org/https://doi.org/10.1061/(ASCE)0733-9364(2005)131:1(3)

- Zhang, X. (2006). Public clients’ best value perspectives of public private partnerships in infrastructure development. Journal of Construction Engineering and Management, 132(2), 107–114. https://doi.org/https://doi.org/10.1061/(ASCE)0733-9364(2006)132:2(107)