Abstract

This study aims to determine the factors that influence an individual’s continuance usage of mobile payment. This study proposed a research model that combines two well-known theories, namely Technological Personal Environmental (TPE) model and Technology Continuance Theory (TCT) to examine the impact of environmental factors in mobile payment continuance usage. The data were obtained empirically from 443 respondents by using an online questionnaire. Then, the data were used to test the research model by using covariance-based SEM (CB-SEM). The results of data processing showed that user satisfaction was a factor that positively influenced the continuance usage of mobile payment. Furthermore, user satisfaction was directly influenced by environmental factors, consisting of Additional Value (VA), Payment Culture (PC), Lifestyle Compatibility (LC), and Facilitating Conditions (FC). Thus, this research is useful for mobile payment service providers in Indonesia to help them engage with their customers to use mobile payment for the long term. This research provides an explanation of the relationship among environmental aspects used as research models to understand the phenomenon of mobile payments sustainable use in Indonesian customers who have a cultural tendency to use cash as the payment method. By understanding factors that influence continuance usage of mobile payment in Indonesia, the mobile payment providers can evaluate then improve their services and determine the right strategy by emphasizing various environmental aspects in developing and promoting mobile payment services.

PUBLIC INTEREST STATEMENT

Continuance usage is a crucial aspect of mobile payment adoption that can be used to determine the user’s long-term relationship with the technology services. User’s decision to continue using a service is based on an overall evaluation of product or service experience. This study investigated the continuance usage of mobile payments accessed by Indonesian users. In addition, this study also identifies environmental factors, such as competitive values, regulations, social factors, social conditions, and availability of support. A questionnaire was created and distributed to users who have used mobile payment service with at least one transaction. The results of the study showed that environmental factors, including additional value, payment culture, lifestyle compatibility, and facilitating conditions increased user satisfaction in order to form a positive continuance usage of mobile payment. This study signifies that environmental characteristics, including socio-culture, could influence the continuance behavior of mobile payment technologies among Indonesian users.

1. Introduction

Data fromAPJII (2018) survey showed that the number of internet users grew to 27.9 million (10.12%) when compared to the previous year. This growth is in accordance with the high mobile phone users in Indonesia reaching 355.5 million, this is greater than the total population of Indonesia totaling 268.2 million (We Are Social & Hootsuite, Citation2019). The increasing number of mobile devices all over the world and high-speed cellular networks encourages the use of mobile payment transactions. In 2016, market size of mobile payment reached at 601 USD billion and is projected to be worth 4.574 USD billion by 2023. The growth of mobile payment transactions is supported by the PricewaterhouseCoopers reporting that globally, up to 34% of consumers did in-store mobile payment. The highest mobile payment usage was in Asia, proven by eight Asian countries were among the top ten countries for mobile payments in the world. Six of them are in Southeast Asia, namely Thailand, Vietnam, Indonesia, Singapore, Philippines, and Malaysia (PricewaterhouseCoopers, Citation2019). One positive impact arising with the rapid growth of the internet is in the economic sector, with the increased presence of various financial technologies. Data from Bank Indonesia (Citation2019) showed the growth of digital (non-cash) payment transactions in 2018 was four times compared to the previous year which reached 49.19 trillion IDR. The large number of internet and smart phone users compared to account holders in financial institutions (banked people) accompanied by the increasing volume of digital payment transactions encouraged the use of smartphone technology-based financial services to accelerate financial inclusion and reach unbanked people (Nugroho, Citation2017).

Mobile payment allowed customers to make transactions anytime and from anywhere in real-time, offering convenience and speed, performance, and secure transfer of information among devices (Oliveira et al., Citation2016). The use of mobile payments encourages the economy to shift toward the movement of non-cash transactions or less cash society (Chakraborty & Mitra, Citation2018). This is in accordance with one of the Indonesian Payment System visions in 2025 to encourage the use of mobile fast payments that are real-time, efficient, and available 24/7. A survey conducted by DS Research & BRI (Citation2019) towards public attitudes in understanding financial technology products showed that 82.7% of the public had an understanding and familiarity with mobile payment products and became the most widely used fintech product in Indonesia during 2019 with a percentage of 80%.

There is a considerable research that discussed the adoption of mobile payment using various technology acceptance theories, such as Technology Acceptance Model (TAM), The Theory of Reasoned Action (TRA), The Theory of Planned Behavior (TPB), Dissemination of Innovations (DOI), and The Unified Theory of Acceptance and Use of Technology (UTAUT). As the mobile payments have spread globally in various countries, it should not be ignored that environmental characteristics, including socio-culture, can influence customer behavior (Zhang et al., Citation2011). However, most mobile payments research ignored environmental factors. Therefore, elaborating environmental factors that include socio-culture into the mobile payment adoption model is necessary. Research conducted by Hofstede (Citation1984) showed that socio-culture affected the behavior of societies and organizations over time. The research results by Sundqvist et al. (Citation2005) showed that the country’s wealth and cultural similarity positively affected the adoption of the technology.

This study gives contributions to fill the gaps to the prior research conducted by Karsen et al. (Citation2019) which showed that prior research on mobile payments mostly focused on the technology and characteristics of individuals, while only limited research focused on exploring the environmental context of the intention to use mobile payments. Previous studies of mobile payments investigated adoption and initial usage behavior, but did not analyze the long-term use of mobile payments (Chawla & Joshi, Citation2019; Hunafa et al., Citation2017; Leiva et al., Citation2017; Shaw & Kesharwani, Citation2019). Unfortunately, previous research only focused on identifying sustainable use factors for users in South Africa and China (Humbani & Wiese, Citation2019; Khayer & Bao, Citation2019). In addition, the characteristics of Indonesian culture are different from other countries so that there will be different factors that encourage Indonesian users to use mobile payments.

External influences have the greatest impact on intentions to use and become a determining element for establishing the usage of digital payment systems (Cabanillas & Fernandez, Citation2014). This study focuses on environmental aspects of the continuance usage in mobile payments, including service provider industries, competitive values, regulations, social influence, social conditions, and availability of support related to mobile payment services (Karsen et al., Citation2019). Environmental factors become one of the critical success factors that encourages the adoption of mobile payment. Research by Sahu & Singh (Citation2018) stated that cultural factors, government policy, compatibility, and infrastructure as elements in the context of environment are some of the critical success factors that influence the adoption of mobile payments.

Based on the above conditions, this study aims to identify environmental factors that influence individuals to continue using mobile payments in the context of users in Indonesia. This study proposed a robust model incorporating Technological Personal Environmental (TPE) and Technology Continuance Theory (TCT). TPE framework provides an explanation about the acceptance of technology for an individual context which consists of three categories, including technology, personal, and environment. The environment context in the TPE framework includes social circumstances and the availability of support on the object under investigation. Technology Continuance Theory (TCT) has constructs to explain continuance usage intention of the technology. This theory has been developed by integrating technology acceptance model (TAM), expectation-confirmation model, and cognitive model to capture continuance behavior of innovative technologies. This research applied covariance-based structural equation modeling (CB-SEM) approach to analyze and confirm the research model. This research enriches the environmental aspect in previous study conducted by Hunafa et al. (Citation2017) that examined technological, personal, and environmental factors to understand mobile payment adoption in Indonesia. Additionally, this study also complements research result by Azizah et al. (Citation2018) that identified satisfaction factors formed by confirming user expectations based on usage experience.

2. Literature review

2.1. Mobile payment

Mobile payment is a transaction process that is carried out using a mobile device that is able to process financial transactions securely through mobile networks or through various wireless technologies (Ghezzi et al., Citation2010). The mobile payment process involves three parties among users, merchants, and service providers both bank and non-bank (Oliveira et al., Citation2016). Mobile payment in Indonesia uses server-based electronic money for offering services, such as bill payment, telecom top-ups, virtual transfer, on-site retail payment, on-site dining payment, and public transport ticketing. Research conducted by MDI Ventures (2019) showed in 2017, QR-code-based mobile payments in Indonesia became a payment technology that had the potential to compete with the other digital banking channels. The QR payment supports mobile payment services to penetrate the micro, small, and medium size in the F&B, groceries, and retail segments. QR Code on mobile payment services helps accelerate the nation’s progress towards a cashless society. Therefore, the QR Code service based on mobile payments developed by banks and non-banks was included in the scope of this research. Mobile payment based on QR Code only needed static QR code stickers at merchant points to start facilitating payments (Agusta & Hutabarat, Citation2019).

2.2. Technological personal environmental (TPE)

The Technological Personal Environmental model is a framework adapted from TOE (Technological Organizational Environment) which is used as a theoretical basis for the acceptance of technology for individuals (Hunafa et al., Citation2017). The TPE framework consists of three categories, namely technology, individuals, and the environment (Jiang & Lai, Citation2010). Technologies context related to internal and external technology consists of equipment and processes. The personal context related to an individual’s personalities and properties consists of risk aversion and values. The environmental context consists of service provider industries, competitive values, regulations, social factors, social conditions, and availability of support (Jiang & Lai, Citation2010).

2.3. Technology continuance theory (TCT)

In Technology Continuance Theory, Liao et al. (Citation2009) explained that individuals would build expectations of a technology after a period of usage. They would compare expectations with user experience. User experience in using technology services would be compared with user expectations that result in the form of confirmation or disconfirmation of services that would affect the level of individual satisfaction. The level of satisfaction would affect the user’s decision to continue or discontinue the use of technology (Bhattacherjee, Citation2001). Satisfaction was reflected in the user’s perception as a positive, indifferent, or negative result after the user evaluates the use of technology (Mouakket & Bettayeb, Citation2015). Confirmation of expectation or adoption refers to the user’s perception of the compatibility between their expectations and the real performance of the technology.

3. Conceptual model

Research conducted by Sahu & Singh (2018) showed that the environmental factor was one of the critical success factors that drives the adoption of mobile payments. The factors found were cultural factors, government policy, compatibility, and infrastructure. Environmental factors are factors that are located at research sites so they are unique and specific to each case study (Karsen et al., Citation2019). Research by Karsen et al. (Citation2019) showed that previous research on mobile payment focused only on technology and characteristics of individuals, while there is only one study that focused on the environmental context. Previous researches on mobile payments investigated adoption and initial usage behavior, but did not analyze the continuance usage of mobile payment (Chawla & Joshi, Citation2019; Hunafa et al., Citation2017; Leiva et al., Citation2017; Shaw & Kesharwani, Citation2019).

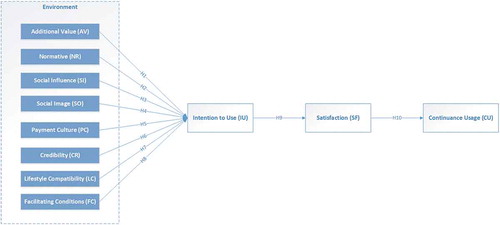

Figure shows the theoretical framework used in the study. The behavior of users after the initial adoption might change based on actual experiences perceived, and at the end of the experience, they might intensify or reduce the future use (Khayer & Bao, Citation2019). According to Humbani and Wiese (Citation2019), adoption and the continuing intention to use technology are important to study since adoption cannot be classified as a success if the sustainable use of the technology has not been measured. Therefore, this study seeks to complement previous research by focusing on the influence of the environmental side. In this study, to determine the intention to use mobile payments continuously, the Technology Continuance Theory (TCT) model was integrated with the Technological Personal Environmental (TPE) model framework. The Technological Personal Environmental (TPE) framework is suitable for explaining phenomena in the acceptance of technology from the environmental side. In addition, Technology Continuance Theory (TCT) was chosen because it provides the prediction of satisfaction based on consumer confirmation of previous usage and tests its effect on the continued use of mobile payments. Thus, this study used TCT adopted from research conducted by Khayer and Bao (Citation2019) to provide an understanding of user adoption and post-adoption behavior of mobile payment. Table explains the research variables in the environmental context obtained from the variables that existed in previous studies.

Figure 1. The proposed research model

Table 1. The proposed Variables

Additional value is often used in the promotion of digital payments to attract and retain customers (Sierzchula et al., Citation2014). Promotions in the form of discounts and offers given to customers in digital payment methods could attract customers to convert to new payment methods. In a study by Pham and Ho (Citation2015), service providers offered value-added to their digital payment products that led users more likely to use this payment method. Carbó-Valverde and Liñares-Zegarra (Citation2011) research showed that financial incentives, such as cashbacks, points, and discounts had a positive influence in promoting the use of non-cash payments. The study by Zhao et al. (Citation2018) revealed that points and prizes were the main drivers of consumer payment choices.

H1: Additional Value (AV) has a significant positive effect on the intention to use (IU) the mobile payment

Normative occurs when individuals voluntarily and unconsciously imitate the same attitudes, behaviors, and practices from others. Attitudes, behaviors, and practices are the right things to do. Normative pressure caused individuals who have not adopted technology to feel uncomfortable (Jiang & Lai, Citation2010). Other individuals could build legitimacy which forces non-adopters to adopt the same behavior even when this behavior is not necessarily suitable (Jiang & Lai, Citation2010). Zhu & Chen’s research (Zhu & Chen, Citation2016) showed the normative effect of creating social pressure for people to use a product or service. If they do not use the product or service, they will be considered as old-fashioned. People choose to take an action when someone in their social circle forces them to do even though they may not like or believe it. Research by Ting et al. (Citation2016) found that normative influence on the use of mobile payment in Malaysia was indicated by the concern possessed by the Malays in social relations and received approval from other groups related to technology adoption.

H2: Normative (NR) has a significant positive effect on the intention to use (IU) the mobile payment

Social influence is the extent to which consumers feel that others who are influential to them (such as family and friends) believe that they must use certain technologies (Chawla & Joshi, Citation2019). When others are considered influential for those adopting a service, then it can encourage them to adopt mobile payment services. Previous research suggested that social influence significantly affected the desire to use mobile payment (Hunafa et al., Citation2017; Oliveira et al., Citation2016; Park et al., Citation2019). These results however contradict with the research by Baabdullah et al. (Citation2018) who found that social influence did not affect the use of mobile payment technology

H3: Social Influence (SI) has a significant positive effect on the intention to use (IU) the mobile payment

Research by Karsen et al. (Citation2019) stated that social image as one of the environmental factors had an influence on the use of mobile payment. Social image is defined as the desired social value that everyone creates through interaction with others (Liu & Li, Citation2011). The purpose of social image is to gain respect and admiration from colleagues in their social networks as a result of using their information (Leiva et al., Citation2017). In achieving the goal of maintaining a social image, the presence of others around the user becomes necessary to strengthen or reject that image. Leiva et al. (Citation2017) research showed that social image had a positive influence on the attitude of using mobile payment.

H4: Social Image (SO) has a significant positive effect on the intention to use (IU) the mobile payment

The way of person uses information systems is influenced by cultural values that act as important moderators in technology acceptance (Baptista & Oliveira, Citation2015). Payment culture is defined as a set of values, attitudes, opinions, and beliefs that characterize a group and direct their behavior in transactions (Tam & Oliveira , Citation2017). Uncertainty avoidance is one of the indicators in payment culture that becomes the focus of this research referring to the extent to which users are willing to follow formal rules and regulations created by service provider platforms to minimize uncertainty (Fan et al., Citation2018; Baptista & Oliveira, Citation2015; Zhang et al., Citation2011). Individuals who avoided uncertainty felt uncomfortable with ambiguity and tended to refuse to take risks (Baptista & Oliveira, Citation2015). Research by Fan et al. (Citation2018) and Baptista & Oliveira (Citation2015) showed that payment culture had a significant influence on the intention to adopt mobile payment.

H5: Payment Culture (PC) has a significant positive effect on the intention to use (IU) the mobile payment

Financial transactions through mobile phones connected to the internet network are vulnerable to fraud, therefore trust and integrity of mobile payment service providers play an important role in encouraging consumers to use mobile payment services (Shaw & Kesharwani, Citation2019). An individual’s perception of credibility was influenced by the security and confidentiality guaranteed by the service provider in online transactions (Lewis et al., Citation2010). Shaw & Kesharwani research (Shaw & Kesharwani, Citation2019) showed that credibility had no influence on behavioral intentions to use digital payment services. This contrasts with the research results by Luarn & Lin (Citation2005) which stated that credibility as the strongest factor influencing behavioral intention to use mobile banking. The results of Luarn & Lin’s (2005) research are in line with the research results conducted by Yu (Citation2012) and Al Khasawneh (Citation2015) who validated that credibility is a factor driving the adoption of mobile banking.

H6: Credibility (CR) has a significant positive effect on the intention to use (IU) the mobile payment

Lifestyle Compatibility (LC) is the adoption of a product, service, or idea by consumers through a process of knowledge, persuasion, decision, and confirmation (Chawla & Joshi, Citation2019). Lifestyle Compatibility can be defined as the suitability of choices and lifestyle values among individuals. Lin (Citation2011) study explained LC as the extent to which mobile payment services were aligned with user values, experience, lifestyle, and preferences. In another study by Mohammadi (Citation2015) revealed that LC was the main factor influencing user attitudes towards the use of mobile payment. Previous studies have shown that lifestyle compatibility had a positive influence on the use of mobile payments (Chawla & Joshi, Citation2019; Singh & Srivastava, Citation2014). One of the requirements of mobile payment usage did not change the way users behave in the transaction, so that it might encourage the user’s desire to use mobile payment (Ozturk, Bilgihan, Esfahani, & Hua, Understanding the mobile payment technology acceptance based on valence theory, Ozturk et al., Citation2017).

H7: Lifestyle Compatibility (LC) has a significant positive effect on the intention to use (IU) the mobile payment

Facilitating conditions (FC) is defined as the ease of access to resources needed to be able to run services (Hunafa et al., Citation2017). Facilitating conditions in mobile payment refers to the availability of mobile devices, internet connections, knowledge, or procedures regarding the use of services, security, and privacy laws. The research by Baabdullah et al. (Citation2018) explained that the ability of people to surf the internet and get access to online payment facilities has influenced their intention to use the technology. Research by Hunafa et al. (Citation2017) showed that the more complete the supporting facilities available, the higher the individual’s perception about the use of mobile payment.

H8: Facilitating Conditions (FC) has a significant positive effect on the intention to use (IU) the mobile payment

Research by Straub (2009) showed that confirmation and adoption were similar terms as both measured consumer experience after using new technology. Adoption of technology reflected confirmation of expectations that served as elements that supported continuance usage (Baabdullah et al., Citation2018). Khayer & Bao’s research (Khayer & Bao, Citation2019) found that confirmation determining the level of user satisfaction and initial expectations of fulfilled services formed the level of satisfaction in using mobile payment. Previous research showed that user expectations that were met in the use of services positively increased customer satisfaction (Baabdullah et al., Citation2018; Humbani & Wiese, Citation2019). When the user was satisfied with the service, the user would tend to show the behavior of continuance use of the service (Cao et al., Citation2018). The continuance usage is described as the extent to which a person will consciously continue to use a service for a long period of time (Mouakket & Bettayeb, Citation2015). Previous research has shown that satisfaction is a fundamental driving force in the continuance usage of mobile payments (Azizah et al., Citation2018; Humbani & Wiese, Citation2019; Khayer & Bao, Citation2019).

H9: Intention to Use (IU) has a positive effect on the satisfaction (SF) of using a mobile payment

H10: Satisfaction (SF) has a positive influence on the continuance usage (CU) of the mobile payment

4. Methodology

This study applied a quantitative approach using survey targetted at the mobile payment users in Indonesia. Quantitative method was used to test objective theories by examining the relationships among variables in the research model (Creswell, Citation2013). Hypothesis testing was done through research survey by collecting data using a questionnaire distributed online through social media and considering the availability of the number of respondents needed for data processing with Structural Equation Modeling (SEM) methods. Data processing method used in this study was Covariance-based SEM (CB-SEM) as this research has strong theoretical bases, such as Technological Personal Environmental and Technology Continuance theory (TCT) (Wijanto, Citation2015). The questionnaire was distributed for three weeks in November 2019 to mobile payment users in Indonesia, especially those who had experienced at least one transaction using mobile payment-based services. Respondents were asked to answer statements in the form of scale to measure respondents’ attitudes toward some statements in the questionnaire. The scale used was a Likert scale with a range of 1 to 5 with scale 1 shows strongly disagree and 5 demonstrates strongly agree. The result of data collection through a survey managed to collect 443 responses as shown in Table .

Table 2. Demographics

5. Results

5.1. Measurement model

Measurement models were conducted to examine the relationship between the indicator and its construct through three measurements, including loading factor, validity test, and reliability test. Loading factor showed the indicator had a strong relationship with its construct and was used as an indication in the validity test. The recommendation for the loading factor value was >0.7 (Santoso, Citation2018). Reliability and validity tests on the model were performed by calculating the value of Construct Reliability (CR), Cronbach’s Alpha (CA), and Average Variance Extracted (AVE). The recommended CR value was >0.7, while the recommended CA value was >0.5, and the recommended AVE value was ≥0.5 (Hair et al., Citation2009).

In this study, the number of latent variables used was 11 units with a total of 36 indicators and 443 data samples obtained. Outlier evaluation process was carried out to eliminate all observation numbers that had p1 and p1 values as p1 < 0.001 and p2 < 0.001. The final data that were used to test the measurement model and the structural model were 404 data with 39 data were not included because the data were declared as an outlier. The results of the multicollinearity test showed that in the research model there was no correlation value between the indicators which had a value of ≥0.9, so the data were declared to meet the requirements of the multicollinearity test. The offending estimate test showed that all variance on the variables in the model was positive. This indicates that there was no estimation error in the model. The loading factor test showed that at the beginning, there were six indicators (AV1, NR1, CR4, LC4, IU3, CU3) which had a value of <0.7, so that it was necessary to eliminate them. After removing the indicator, it was found that each indicator had a loading factor value of >0,7 which indicates each indicator had a strong relationship with the construct. Reliability test was done by calculating the Construct Reliability (CR) and Cronbach Alpha. The results showed that all the indicators were qualified, so that the data on the research model were valid and reliable (Table ).

Table 3. Confirmatory analysis results

5.2. Structural model

Structural model test was performed to determine the correlation that shows relationships among constructs. The structural model was tested by measuring the relationship between the dependent and independent variables in the model. Hypothesis test was the final stage of the SEM analysis conducted to test the research hypothesis by looking at the significance of the p-value.

Based on the results of the Goodness of Fit test, Table shows that almost all of the criteria tested have a value that meets the good fit criteria, except AGFI as is stated as marginal fit. In the measurement model, the value of AGFI needs to be increased to achieve good fit. Therefore, modifications were made by looking at AMOS recommendations on Modification Indices with a cut-off value for the M.I ≥ 10,000 and having a positive Par Change value (Byrne, Citation2016). After modifying the model, the Goodness of Fit test results showed an increase in the value for the AGFI criteria to 0.908, so that all criteria had a good fit value. Therefore, the result of the GOF test in the modified measurement model is in line with the data.

Table 4. Model evaluation overall fit measurement

Hypothesis testing by comparing the p-value with a significance level of 5% and the coefficient of Critical Ratio (C.R.) >1.96 was generated by AMOS by looking at the value of regression weights (Bahri & Zamzam, Citation2014). Basis for a decision to test the hypothesis was seen from the p-value (probability) and Critical Ratio (C.R.). If the value of p < 0.05 and Critical Ratio (C.R.) >1.96, the hypothesis is accepted. Table shows six hypotheses accepted and four hypotheses rejected.

Table 5. Results of the hypothesis testing

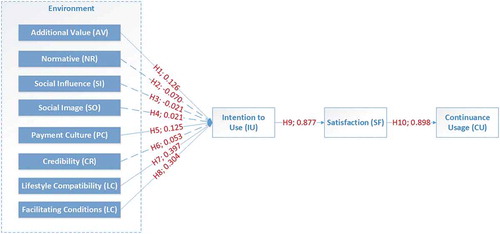

Figure shows the relationship between endogenous variables. Satisfaction (SF) variable significantly influences Continuance Usage (CU) with a coefficient value of 0.898. While the value that mostly influences the Intention to Use (IU) variable is the Lifestyle Compatibility (LC) variable with a coefficient value of 0.397 and Facilitating Conditions with a coefficient value of 0.304.

Figure 2. The final model

To obtain the depth of analysis in the research model, an analysis of the quadratic correlation value (R2) was carried out to determine the strength of the structural model on the data used in the study. According to Santoso (Citation2018), a value of R2 > 0.5 indicates the closeness of the relationship or correlation between variables or constructs, the greater value of R2, the stronger or tighter the correlation between variables in the research model. The results showed that the satisfaction and continuance usage variables in the research model had a value of 76.9% and 80.6%. The R2 value for the Continuance Usage (CU) variable is 0.806 which indicates that the continuous use of mobile payment services can be explained by all exogenous variables up to 80.6%, while the remaining 19.4% is explained by other variables that are outside the research model and not measured.

6. Discussion

Based on the hypothesis results, factors that influence the continuance usage of mobile payment services are additional value, payment culture, lifestyle compatibility, facilitating conditions, intention to use, and satisfaction. This is in line with the results of a survey conducted by Jakpat (2018) that 59.9% of the main reasons users used non-cash transactions were because of promotional programs offered by service providers. Customers would not switch to a new payment service without additional services as a reason for customers to try (Pham & Ho, Citation2015). Normative did not influence the decision to use mobile payment. It indicates that individual behavior in adopting mobile payment technology tends not to be easily influenced by other individual behavior. In line with the research of Ting et al. (Citation2016) in the ethnic Chinese group, the results showed that normative factors did not influence the adoption of mobile payments. Chinese ethnic groups avoided uncertainty and were willing to adopt a payment system if security was guaranteed or enhanced. Similar characteristics are also shown by the Indonesian people. This study revealed that users of mobile payment services in Indonesia had the characteristics to avoid uncertainty, ambiguity, and tend to refuse to take risks in the use of mobile payment services as evidenced by the acceptance of the payment culture hypothesis influencing the desire to use mobile payment services. This research showed that users tended to obey the rules and regulations provided by service providers to minimize uncertainty and risk. These results align with the previous studies which showed that payment culture significantly influenced on the use of mobile payment (Fan et al., Citation2018; Baptista & Oliveira, Citation2015; Zhang et al., Citation2011). Consumers showed concern and were reluctant to make transactions through services that provide a higher risk than perceived benefits (Park et al., Citation2019).

Social influence and social image did not influence the use of mobile payments. It indicates that Indonesians are not easily influenced by the opinions or behavior of individuals or figures they consider famous, influential, or successful. Mobile payment users in Indonesia tended not to rely on information and advice originating from their social environment in forming the decision to use mobile payment. There is a possibility that individuals pay less attention to social environmental support if they already have good experience in using technology. Research by Revels et al. (Citation2010) explained the difference in the role of social image in technology adoption, currently gadgets or smartphones considered as common things that almost everyone has. It revealed that the use of mobile applications was common because it can be easily replicated through the use of different media, such as computers and the internet. The results showed that credibility had no influence on the use of mobile payment. The results of this study contradict with the research results conducted by Yu (Citation2012) and Al Khasawneh (Citation2015) who validated that credibility was a factor that drove the adoption of payment technology. User experience utilizing various other mobile-based applications, such as mobile banking and e-commerce increased trust in users, so that it can be the reason for users not paying attention to the credibility factor (Shaw & Kesharwani, Citation2019). This can indicate that longer experience can increase user confidence in mobile payment services, so that credibility is no longer the main factor driving the desire to use mobile payment.

The results of this study are in line with the research results by Chawla and Joshi (Citation2019) and Singh and Srivastava (Citation2014). They showed that lifestyle compatibility plays an important and significant role in influencing users’ intention to adopt mobile payment. The user will use mobile payment as a payment method if the user believes that it is a lifestyle. Users would align their values, experiences, personalities, and preferences with technology and generated positive intentions to adopt the technology (Liu & Li, Citation2011). Hypothesis testing showed that the facilitating conditions affected the use of mobile payment. It indicates that the user believes the availability of access to the resources needed to facilitate the service will affect the intention to use the service. The availability of resources needed by conducting transactions with mobile payments, such as necessary knowledge, internet-enabled smartphone, a mobile network with good network speeds had a significant influence on user intentions to use mobile payments (Madan & Yadav, Citation2016). In line with the research results by Chawla and Joshi (Citation2019) and Baabdullah et al. (Citation2018), this study proved that facilitating condition was one of the factors that significantly influenced behavioral intentions to adopt mobile payment.

Based on real experience using mobile payment, users form expectations regarding the benefits of mobile payment. The user’s fulfilled expectations led to satisfaction in using mobile payments (Khayer & Bao, Citation2019). The results of this study indicate that user satisfaction influenced the continuance usage of mobile payment services. The fulfillment of the expectations of consumers towards a technology would directly support continuance usage of mobile payment services. Previous research has shown that satisfaction is the main driving force affecting sustainable use (Azizah et al., Citation2018; Humbani & Wiese, Citation2019; Khayer & Bao, Citation2019).

7. Implications

This study confirms the environmental factors that influence individual’s decision to continue using mobile payment services, namely perceptions of economic benefits, availability of terms and conditions of service, lifestyle, and supporting facilities. Additional value of mobile payment services can be adjusted to the characteristics of users by offering or recommending promos or discounts based on consumer behavior. Recommendations of promo or discount are displayed to consumers in the form of notifications, reminders by message or email to encourage the intention to continue using the mobile payment services (Zhao et al., Citation2018). This study proved that payment culture became one of the important environmental factors and influenced on the intention to use mobile payment services. This indicates that users will tend to obey the rules and regulations provided by service providers to minimize uncertainty and risk. Consumers showed concern and were reluctant to make transactions through a service that provides a higher risk than the perceived benefits (Park et al., Citation2019). The government and regulators need to improve public perception and regulatory readiness for financial technology services, especially mobile payment services. In addition, socialization and education programs through seminars and roadshows to the public and merchants or MSMEs are needed to improve equality in understanding digital payment products. In order to increase consumer understanding of mobile payment features and regulations, service providers can provide customer care that works 24/7 by utilizing support systems, such as livechat or chatbots and using social media, such as Youtube to explain the functionality and regulations applied in mobile payments.

Service providers need to pay attention to the suitability of services with social values and user preferences, thereby giving satisfaction for users and lead to continued use of the mobile payment application (Ozturk, Bilgihan, Esfahani, & Hua, Understanding the mobile payment technology acceptance based on valence theory, Ozturk et al., Citation2016). Service providers need to add features that allow users to adjust themselves, so that it leads to the user’s perception that the technology is appropriate and useful (Chawla & Joshi, Citation2019). By considering the characteristics of individuals who have high mobility, service providers need to provide features that can enhance user experience and provide payments that integrate various mobile payment services into one application to meet a variety of needs (Shao et al., Citation2019). Service providers can present automated transaction features and personalized reminders that allow users to set reminders for transactions and make it easier for users to schedule payment transactions, such as electricity payments, insurance, cable TV, and data packages on scheduled dates.

Research by Lin. H. (2011) proved that users put trust in the ability of governments, telecommunications companies, and financial institutions in providing adequate service support to facilitate access to mobile payment services. The limited number of merchants who serve mobile payment transactions, unstable internet quality, weak data security, and information confidentiality are some of the obstacles faced by users when using mobile payment services in Indonesia. Government should cooperate with the service providers and network operators in providing infrastructure ecosystem, instruments, and mechanisms of mobile payment services and encourage the strengthening of internet networks to ensure network connectivity and reliability needed to be able to access mobile payment services (Humbani & Wiese, Citation2019).

Meanwhile, this study showed that individual behavior in Indonesia in adopting mobile payment technology tended not to be easily influenced by the social environment and other individual behaviors. Individuals did not consider others who use the mobile payment application as someone who has a high social status as technology can be easily replicated and obtained. This also indicates that the use of mobile payment cannot be used to maintain or strengthen the image of individuals in their environment. Individuals pay less attention to the support of the social environment if they already have good experience in dealing with technology. Respondents’ responses to the experience of using mobile payment showed that 28% or 124 respondents had used mobile payment services for more than two years and 23.3% or 103 respondents said they had used mobile payment services for 7–12 months. This indicates that longer experience can increase user confidence in mobile payment services, so that the credibility factor is no longer the main factor that drives the desire to use mobile payment.

8. Conclusion and future works

This study found the environmental factors that influenced the continuance usage of mobile payment services were additional value, payment culture, lifestyle compatibility, and facilitating conditions. This shows that consumers’ decision to use mobile payment was influenced by the added value in the form of gifts or rewards given by mobile payment service providers. This study also found that consumers were influenced by trust to follow formal regulations made by service providers in using mobile payments. Consumer lifestyle preferences that were influenced by their environment also encouraged consumers to use mobile payments. Other environmental factors that influenced consumers in the use of mobile payments were the availability of resources and supporting facilities. This research supports the theory of Technology continuance theory (TCT), where consumer experience during service use can be used to predict satisfaction and continuance usage of new technologies. This is indicated by the value of satisfaction and continuous usage in the research model that had a value of 76.9% and 80.6%, which implies the correlation between the two variables is close or strong.

Service providers are expected to develop features that are in accordance with the preferences, history, and transaction habits of users, so that the program provided can be in line with user needs and can provide added value. Government, service providers, and network operators are expected to be able to build a mobile payment ecosystem that includes the availability of infrastructure and network connectivity to support equal distribution of network quality and expand locations and businesses that can serve transactions using mobile payment services. Future studies can explore other environmental factors that encourage individuals’ intention to use sustainable mobile payment services.

Acknowledgements

We want to convey our gratitude to the University of Indonesia for the Grant PUTI Q2, grant No. NKB-1472/UN2.RST/HKP.05.00.2020.

Additional information

Funding

Notes on contributors

Arifianita Febrina Putri

Arifianita Febrina Putri received her master's degree in Information Technology from Universitas Indonesia. She has written paper on topics of business transformation and information quality. Recently she has taken a keen interest in research on technology adoption. Now she is working at central banking services project as a business analyst. Putu Wuri Handayani, Msc is a lecture in the Faculty of Computer Science Universitas Indonesia. She obtained her master's degree in electronic business from University of Applied Science Fulda, Germany. She obtained her doctoral study at the Faculty of Computer Science Universitas Indonesia. Her research interest is related to information system/information technology such as e-commerce, enterprise resource planning, supply chain management, customer relationship management, and healthcare information system. Muhammad Rifki Shihab is a lecturer and researcher at the Faculty of Computer Science, Universitas Indonesia. His research interests include information management, eParticipation, and electronic commerce.

References

- Agusta, J., & Hutabarat, K. (2019). Mobile payment in Indonesia. MDI Ventures and Mandiri Sekuritas.

- Al Khasawneh, M. (2015). An empirical examination of consumer adoption of mobile banking (M-Banking) in Jordan. Journal of Internet Commerce, 14(3), 341–18. https://doi.org/10.1080/15332861.2015.1045288

- APJII. (2018). Penetrasi dan Profil Perilaku Pengguna Internet Indonesia: Survey 2018.

- Azizah, N., Handayani, P. W., & Azzahro, F. (2018). Factors Influencing Continuance Usage of Mobile Wallets in Indonesia. 2018 International Conference on Information Management and Technology (ICIMTech) (pp. 92–97). Jakarta : IEEE doi:10.1109/ICIMTech.2018.8528157

- Baabdullah, M. A., Alalwan, A. A., Rana, N. P., & Kizgin, H. (2018). Consumer use of mobile banking (M-Banking) in Saudi Arabia: Towards an integrated model. International Journal of Information Management, 44, 38–52. https://doi.org/10.1016/j.ijinfomgt.2018.09.002

- Bahri, S., & Zamzam, F. (2014). Model Penelitian Kuantitatif Berbasis SEM-AMOS. Deepublish.

- Baptista, G., & Oliveira, T. (2015). Understanding mobile banking: The unified theory of acceptance and use of technology combined with cultural moderators. Computers in Human Behavior, 50, 418–430. https://doi.org/10.1016/j.chb.2015.04.024

- Bhattacherjee, A. (2001). Understanding information systems continuance: An expectation-confirmation model. MIS Quarterly, 25(3), 351–370. https://doi.org/10.2307/3250921

- Byrne, B. M. (2016). Structural Equation Modeling with Amos. Routledge.

- Cabanillas, F. J., & Fernandez, J. S. (2014). Role of gender on acceptance of mobile payment. Industrial Management & Data Systems, 114(2), 220–240. https://doi.org/10.1108/IMDS-03-2013-0137

- Cao, X., Yu, L., Liu, Z., Gong, M., & Adeel, L. (2018). Understanding mobile payment users’ continuance intention: Atrust transfer perspective. Internet Research, 28(2), 456–476. https://doi.org/10.1108/IntR-11-2016-0359

- Carbó-Valverde, S., & Liñares-Zegarra, J. (2011). How effective are rewards programs in promoting payment card usage? Empirical evidence. Journal of Banking & Finance, 35(12), 3275–3291. https://doi.org/10.1016/j.jbankfin.2011.05.008

- Chakraborty, S., & Mitra, D. (2018). A Study on Consumers’ Adoption Intention for Digital Wallets in Indonesia. International Journal on Customer Relations, 6(1), 38–56. https://search.proquest.com/docview/2024116193?accountid=44927

- Chawla, D., & Joshi, H. (2019). Consumer attitude and intention to adopt mobile wallet in India – An empirical study. International Journal of Bank Marketing, 37(7), 1590–1618. https://doi.org/10.1108/IJBM-09-2018-0256

- Creswell, C. (2013). Research design: Qualitative, quantitative, and mixed methods approaches. SAGE Publications.

- DS Research, & BRI. (2019). Fintech Report 2019 : Moving Towards A New Era In Indonesia's Financial Industry. Jakarta: DS Research & BRI

- Fan, J., Shao, M., Li, Y., & Huang, X. (2018). Understanding users’ attitude toward mobile payment use: A comparative study between China and the USA. Industrial Management & Data Systems, 118(3), 524–540. https://doi.org/10.1108/IMDS-06-2017-0268

- Ghezzi, A., Renga, F., Balocco, R., & Pescetto, P. (2010). Mobile payment applications: Offer state of the art in the Italian market. info, 12(5), 3–22. https://doi.org/10.1108/14636691011071130

- Hair, J., Black, W., Babin, B., & Anderson, R. (2009). Multivariate Data Analysis. Prentice Hall.

- Hofstede, G. (1984). Culture’s consequences: International differences in work-related values. SAGE Publications.

- Humbani, M., & Wiese, M. (2019). An integrated framework for the adoption and continuance intention to use mobile payment apps. International Journal of Bank Marketing, 37(2), 646–664. https://doi.org/10.1108/IJBM-03-2018-0072

- Hunafa, K., Hidayanto, A. N., & Sandhy, P. (2017). Investigating Mobile Payment Acceptance Using Technological- Personal-Environmental (TPE) Framework: A Case of Indonesia. 2017 International Conference on Advanced Computer Science and Information Systems (ICACSIS), (pp. 159–165). Bali : IEEE doi:10.1109/ICACSIS.2017.8355027

- Indonesia, B. (2019, May 27). Bank Indonesia Paparkan 5 Visi Sistem Pembayaran Indonesia 2025. Siaran Pers Bank Indonesia. https://www.bi.go.id/id/ruang-media/siaran-pers/Pages/SP_214019.aspx

- Jiang, Y., & Lai, F. (2010). Technological-Personal-Environmental (TPE) Framework: A Conceptual Model for Technology Acceptance at the Individual Level. Journal of International Technology and Information Management, 19(3), 89–98. https://scholarworks.lib.csusb.edu/jitim/vol19/iss3/5

- Karsen, M., Chandra, Y. U., & Juwitasary, H. (2019). Technological Factors of Mobile Payment: A Systematic Literature Review. 4th International Conference on Computer Science and Computational Intelligence 2019. 157, pp. 489–498. Yogyakarta: Procedia Computer Science 157 doi:10.1016/j.procs.2019.09.004

- Khayer, A., & Bao, Y. (2019). The continuance usage intention of Alipay: Integrating context-awareness and technology continuance theory (TCT). The Bottom Line, 32(3), 211–229. https://doi.org/10.1108/BL-07-2019-0097

- Leiva, F. M., Climent, S. C., & Cabanillas, F. L. (2017). Determinants of Intention to Use the Mobile Banking Apps: An Extension of the Classic TAM Model. Spanish Journal of Marketing - ESIC, 21(1), 25–38.https://doi.org/10.1016/j.sjme.2016.12.001

- Lewis, K., Nicole, P., Adrian, M., & Alexander. (2010). Predicting young consumers’ take up of mobile banking services. International Journal of Bank Marketing, 28(5), 410–432. https://doi.org/10.1108/02652321011064917

- Liao, C., Palvia, P., & Chen, J.-L. (2009). Information technology adoption behavior life cycle: Toward a Technology Continuance Theory (TCT). International Journal of Information Management, 29(4), 309–320. https://doi.org/10.1016/j.ijinfomgt.2009.03.004

- Lin, H-F.. (2011). An empirical investigation of mobile banking adoption: The effect of innovation attributes and knowledge-based trust.International Journal of Information Management.2010(07). doi:10.1016/j.ijinfomgt.2010.07.006

- Liu, Y., & Li, H. (2011). Exploring the impact of use context on mobile hedonic services adoption: An empirical study on mobile gaming in China. Computers in Human Behavior, 27(2), 163–181. https://doi.org/10.1016/j.chb.2010.11.014

- Luarn, P., & Lin, H. (2005). Toward an understanding of the behavioral intention to use mobile banking. Computers in Human Behavior, 21(6), 873–891. doi:10.1016/j.chb.2004.03.003

- Madan, K., & Yadav, R. (2016). Behavioural intention to adopt mobile wallet: A developing country perspective. Journal of Indian Business Research, 8(3), 227–244. https://doi.org/10.1108/JIBR-10-2015-0112

- Mohammadi, H. (2015). A study of mobile banking usage in Iran. International Journal of Bank Marketing, 33(6), 733–759. https://doi.org/10.1108/IJBM-08-2014-0114

- Mouakket, S., & Bettayeb, A. (2015). Investigating the factors influencing continuance usage intention of learning management systems by university instructors. International Journal of Web Information Systems, 11(4), 1–24. https://doi.org/10.1108/IJWIS-03-2015-0008

- Nugroho, A. (2017, February 14). Financial Technology, Solusi Menjangkau Unbanked People Indonesia. Kompasiana: https://www.kompasiana.com/nodiharahap/58a2fcc7d47e61f33dbdfd0a/financial-technology-solusi-menjangkau-unbanked-people-indonesia

- Oliveira, T., Thomas, M., Baptista, G., & Campos, F. (2016). Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Computers in Human Behavior, 61, 404–414. https://doi.org/10.1016/j.chb.2016.03.030

- Ozturk, A., Bilgihan, A., Esfahani, S., & Hua, N. (2016). Understanding the mobile payment technology acceptance based on valence theory. International Journal of Contemporary Hospitality Management, 29(8), 2027–2049. https://doi.org/10.1108/IJCHM-04-2016-0192

- Ozturk, A., Bilgihan, A., Esfahani, S., & Hua, N. (2017). Understanding the mobile payment technology acceptance based on valence theory. International Journal of Contemporary Hospitality Management, 29(8), 2027–2049. https://doi.org/10.1108/IJCHM-04-2017-0192

- Park, J., Ahn, J., Thavisay, T., & Ren, T. (2019). Examining the role of anxiety and social influence in multi-benefits of mobile payment service. Journal of Retailing and Consumer Services, 47, 140–149. https://doi.org/10.1016/j.jretconser.2018.11.015

- Pham, -T.-T.-T., & Ho, J. C. (2015). The effects of product-related, personal-related factors and attractiveness of alternatives on consumer adoption of NFC-based mobile payments. Technology in Society, 43, 159–172. https://doi.org/10.1016/j.techsoc.2015.05.004

- PricewaterhouseCoopers. (2019) . Global consumer insights survey.

- Revels, J., Tojib, D., & Tsarenko, Y. (2010). Understanding consumer intention to use mobile services. Australasian Marketing Journal (AMJ), 18(2), 74-80. https://doi.org/10.1016/j.Australasian Marketing Journal (AMJ).

- Sahu, G., & Singh, N. (2018). Identifying Critical Success Factor (CSFs) for the Adoption of Digital Payment Systems: A Study of Indian National Banks. Emerging Markets from a Multidisciplinary Perspective, 61–73. https://doi.org/10.1007/978-3-319-75013-2_6

- Santoso, S. (2018). Konsep Dasar dan Aplikasi SEM dengan AMOS 24. Elex Media Komputindo.

- Shao, Z., Zhang, L., Li, X., & Guo, Y. (2019). Antecedents of trust and continuance intention in mobile payment platforms: The moderating effect of gender. Electronic Commerce Research and Applications, 33, 100823. https://doi.org/10.1016/j.elerap.2018.100823

- Shaw, B., & Kesharwani, A. (2019). Moderating Effect of Smartphone Addiction on Mobile Wallet Payment Adoption. Journal of Internet Commerce, 18(3), 291–309. https://doi.org/10.1080/15332861.2019.1620045

- Sierzchula, W., Bakker, S., Maat, K., & Van Wee, B. (2014). The influence of financial incentives and other socio-economic factors on electric vehicle adoption. Energy Policy, 68, 183–194. https://doi.org/10.1016/j.enpol.2014.01.043

- Singh, S., & Srivastava, R. (2014). Factors Influencing the adoption of mobile banking in India. International Journal of E-Services and mobile applications, 6(4), 1–15. https://doi.org/10.4018/ijesma.2014100101

- Sundqvist, S., Frank, L., & Puumalainen, K. (2005). The effects of country characteristics, cultural similarity and adoption timing on the diffusion of wireless communications. Journal of Business Research, 58(1), 107–110. https://doi.org/10.1016/S0148-2963(02)00480-0

- Tam, C., & Oliveira, T. (2017). Understanding mobile banking individual performance: The DeLone & McLean model and the moderating effects of individual culture. Internet Research, 27(3), 538–562. https://doi.org/10.1108/IntR-05-2016-0117

- Ting, H., Yacob, Y., Liew, L., & Lau, W. M. (2016). Intention to Use Mobile Payment System: A Case of Developing Market by Ethnicity. Procedia - Social and Behavioral Sciences, 224(5). https://doi.org/10.1016/j.sbspro.2016.05.390

- We Are Social & Hootsuite. (2019). Digital 2019: Indonesia. We are social.

- Wijanto, S. (2015). Metode Penelitian Menggunakan Structural Equation Modeling dengan Lisrel 9. Lembaga Penerbit Fakultas Ekonomi Universitas Indonesia.

- Yu, C. (2012). Factors affecting individuals to adopt mobile banking: Empirical evidence from the UTAUT model. Journal of Electronic Commerce Research, 13(2), 104–121. http://www.jecr.org/node/48

- Zhang, A., Yue, X., & Kong, Y. (2011). Exploring Culture Factors Affecting the Adoption of Mobile Payment. International Conference on Mobile Business (pp. 263–267). Como : IEEE doi:10.1109/ICMB.2011.32

- Zhao, H., Anong, S. T., & Lini, Z. (2018). Understanding the impact of financial incentives on NFC mobile payment adoption. International Journal of Bank Marketing, 37(5), 1296–1312. https://doi.org/10.1108/IJBM-08-2018-0229

- Zhu, S., & Chen, J. (2016). E-commerce use in urbanising China: the role of normative social influence. Behaviour & Information Technology, 35(5), 357–367. https://doi.org/10.1080/0144929X.2016.1160286