Abstract

To improve the electricity services in Nigeria, the government has embarked on a total reform of the Nigerian Electricity Supply Industry. The reform started with rehabilitating the government-owned electricity infrastructures in 1999 and implementing the 2010 Power Sector Reform. While some stakeholders have seen these reforms benefit the industry, others have yet to see the positive impact of the reforms. Based on this premise, this work presents a synopsis of the Nigerian power sector’s past, present, and future. A review of its state of the art is explored and presented using documents and recent literature on the Nigerian electricity sector. Findings from the study show that infrastructural deficits and administrative lapses dominated the pre-liberation era. The privatization of electricity led to organizational structure and infrastructure improvements. The sector was unbundled into the GenCos, TransCo, Discos, and the regulatory bodies assigned well-defined tasks. The generation capacity has increased to 16,384 MW against the pre-liberation figure of approximately 6000 MW. As against the approximate figure of 10,000 km covered by the transmission infrastructure, an additional 10,000 km has been added to the existing transmission facilities. Although there have been improvements in service deliveries, there are still more grounds to cover to stabilize the Nigerian electricity sector. It is proposed that stakeholders harmonize the various policies and structural changes to make the necessary improvements.

Public interest statement

For more than a decade, various African countries have adopted power sector reforms to enhance their electricity industry. However, some have failed to deliver the various targets that were promised. The outcome of this research evaluates the successes and challenges of power sector reform in Nigeria. This would help decision-makers identify areas that need modifications.

1. Introduction

In the last three decades, many developed and developing economies have directed intense efforts at various electricity sector reforms to stabilize the sector. These reforms are necessary due to the different emerging themes that have emanated from the electricity market. Some of these include the inclusion of renewable energy in the electricity mix, change of ownership structure, market competition, and the sector’s decentralization to meet SDG 7 (Babatunde et al., Citation2018). With a specific emphasis on developing economies, these reforms are triggered by consumers’ dissatisfaction in countries whose electricity sectors are based on the inefficient, traditional model (monopolistic). Also, successes recorded in many developed countries’ electricity sectors are another motivation behind adopting electricity reforms in developing economies. However, although electricity reforms in developed countries aim to improve comparatively efficient market performance, the narrative is totally different in developing countries (especially the global south). In developing countries, many electricity sectors are plagued with vandalization, weak networks, non-cost reflective tariffs, high technical and non-technical losses, and inadequate coverage (Eberhard & Shkaratan, Citation2012; Babatunde et al., Citation2020). Moreover, in the wake of global economic recessions, the budgets of many governments of developing economies are no longer capable of the state-supported electricity sector. In addition, significant reforms will open up and suitably position a monopolistic government-funded electricity sector in developing countries for much-needed competition and investments (Rehermann & Shi, Citation2016). As such, many power sector reforms in Africa are stimulated by the states’ needs in accessing credits from international financing institutions (Wamukonya, Citation2003).

Nigeria’s federal government enacted a decree as part of efforts intended to improve the Nigerian power sector in the early 1970s. This decree led to the merger of the Niger Dams Authority (NDA) and the Electricity Corporation of Nigeria (ECN) to create National Electric Power Authority (Oluseyi et al., Citation2012). Until deregulation, the public-owned utility company operated a vertically integrated government-funded model. With a considerable transmission and distribution infrastructure deficit, it could only generate a total power of about 6200 MW (four thermal and two hydropower plants). The deficit in the generation, transmission, and distribution infrastructures ensured that the market’s demand side was severely underserved, with commodities characterized by brownouts, blackouts, and unscheduled load shedding. The utility could not reduce technical and non-technical losses on the supply side, adequate maintenance, timely expansion, and a reasonable collection rate. Seeing the underfunded state-owned Nigerian power sector’s poor condition and the need for significant restructuring for increased efficiency, the FGN promulgated the National Electric Power Policy in 2001 (Ayamolowo et al., Citation2019b). The policy aimed to unbundle the Nigerian power sector for private sector participation and create enabling structures to sustain the Nigerian electricity market. This was followed by the enactment of the Electric Power Sector Reform (EPSR) and the creation of the Nigerian Electricity Regulatory Commission (NERC) in 2005 (Ayamolowo et al., Citation2019b). Based on the EPSR, the Nigerian electricity sector was finally unbundled and allowed private sector participation in 2013. However, the much-expected service delivery improvements are far from being achieved, with electrification rates in Nigeria standing at 45% (Rural: 36% Urban: 55%; USAID-United States Agency for International Development, Citation2019). Apart from the fact that electricity demand far exceeds the installed and available capacity, the transmission and distribution capacity is also grossly below the required capacity.

With the privatization of the last distribution facility concluded in 2014, various milestones and drawbacks have been experienced within the Nigerian electricity sector. Passed as a law almost 20 years ago, the Electric Power Sector Reforms Bill was expected to, among other issues, develop and guarantee an efficient, reliable, affordable, safe, and cost-effective system of electricity generation, transmission, distribution, and marketing in the NESI (Isola, Citation2016). Various works of literature have been dedicated to appraising the progress or otherwise of Nigeria’s deregulated electricity market. (E. Ogunleye, Citation2017) presented a political economy aspect of the Nigerian power sector reform. The author identified regulatory uncertainty and policy inconsistencies as major challenges in the industry. The challenges and possible solutions to the challenges of power sector reforms in Nigeria have also been discussed in the literature (Oladipo et al., Citation2018; Onochie et al., Citation2015). While (Oladipo et al., Citation2018) suggested proper funding of GENCOs as a key solution to improving power generation in Nigeria, (Onochie et al., Citation2015) opined that implementing the existing policies would go a long way in improving the NESI. Also (Gatugel Usman et al., Citation2015) concludes that transforming the NESI for sustainable growth and development mitigation of energy poverty and corruption is critical and must be pursued. Other aspects of the NESI that have been discussed in the literature include power sector laws (Usman & Abbasoglu, Citation2014), decentralization of the grid (Alao & Awodele, Citation2018), policy analysis (Audu et al., Citation2017), and productivity analysis (Barros et al., Citation2014). Based on this literature, the efficacy of the reforms in improving the Nigerian power sector has remained ambiguous. Although the network capacities have been relatively increased, the electrification access (percentage) post-liberation era has not significantly improved. Many consumers are still exposed to long hours and multiple national blackouts. This paper summarizes the Nigerian power sector by improving the existing literature, emphasizing the trends, challenges, and future perspectives. The contribution of the paper includes the following

Aggregation, comprehensive review of state-of-the-art and documentation of the NESI. The current power sector market structure, market regulations, and policies and reforms were aggregated and discussed

Identification of the various challenges of the Nigerian Power Sector and discussion of potential solutions to the challenges; a unique approach for improving the Nigerian Electricity Sector was proposed in this study

This review is expected to act as a navigating compass for stakeholders in the industry in terms of the present state of the sector and what needs to be done to improve the sustainability of the Nigerian Electricity Supply Industry (NESI). Accordingly, the review is organized as follows: Section 2 focuses on the current power sector market structure, Section 3 discusses market regulations available in the NESI, Section 4 is dedicated to government-motivated policies and reforms, and Section 5 highlights the present challenges in the NESI, Section offer some solutions to the challenges identified in the study, while Section 7 concludes the study by discussing the various findings drawn from the review.

2. Current power sector market structure

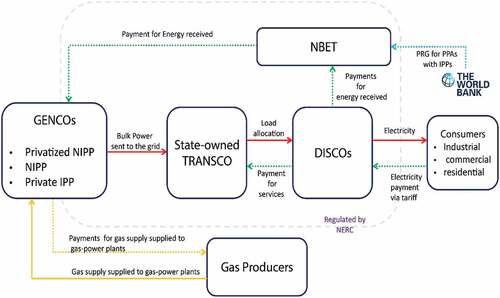

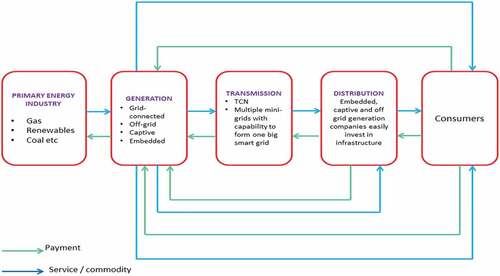

The Nigerian power sector is one of the electricity markets that have been vertically unbundled to allow private sector participation in Africa. Other countries with vertically unbundled markets that allow the private sector’s participation include Ethiopia, Angola, Sudan, Uganda, Algeria, Ghana, Zimbabwe, and Kenya (Trimble et al., Citation2016). Concerning Nigeria, private sector participation is only allowed in the market’s generation and distribution sections. At the same time, the transmission is operated and financed using a public-owned utility company. The Structure of the Power Sector Post-Privatization is presented in Figure . It consists of the Generation Companies (GenCos), the transmission company (TransCo), also known as the Transmission Company of Nigeria (TCN), the distribution companies (DISCOs), the Nigerian bulk electricity trading company, the gas producers, and the consumers. The interactions between these major operators (GenCos, TransCo, DisCos, and NBET) are regulated by the Nigerian Electricity Regulatory Commission (Nigerian Electricity Regulatory Commission, Citation2020). The power generated by the GenCos is transferred to the DisCos, and spread across the country through the transmission infrastructures of the TCN. The DisCos then sell the consumers’ power to industrial, commercial, or residential consumers. In addition, the DisCos are responsible for distributing electricity and collecting energy tariffs served to the various customers. The payments are forwarded to the GenCos through the NBET, while the TCN is also paid to use its infrastructures. The NBET was established as a tool for bulk procurement to compensate for any payment shortfall in the network through subsidies (Nigerian Electricity Regulatory Commission, Citation2020).

Figure 1. Structure of the power sector post-privatization (Nigerian Electricity Regulatory Commission, Citation2020).

2.1. Generation

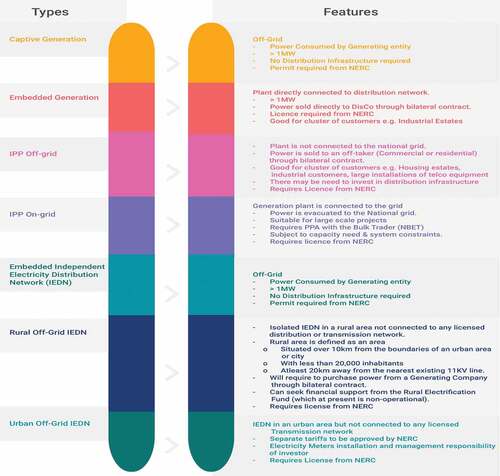

There are four major categories of power generation in Nigeria; these include (a) transmission-grid connected generation, (b) embedded generation (usually connected to the distribution line), (c) off-grid generation, and (d) captive generation (Nigerian Electricity Regulatory Commission, Citation2020). To operate the first three categories of generation options, a valid license is required from NERC. In contrast, the last power generation option only involves obtaining a permit from NERC. With the implementation of the EPSR Act of 2005, the generation part of the former state-owned PHCH was unbundled into six privatized GenCos, National Integrated Power Project (NIPP), and Independent Power Producers (IPPs; Nigerian Electricity Regulatory Commission, Citation2020). From these three sources, the Nigerian electricity network has 23 grid-connected generators with a total installed capacity of 12,522 MW (Hydro: 19%, Thermal: 81%; USAID-United States Agency for International Development, Citation2019). However, due to various challenges, only about 58% of the total installed capacity is available (Hydro: 1,060 MW, Thermal: 4,996 MW; Bamisile et al., Citation2020). Therefore, NERC periodically licenses IPPs who meet the specified conditions to improve electricity generation. Also, the commission proposed Bulk Procurement Guidelines to systematically and effectively procure bulk power.

Furthermore, a guideline targeted at connecting to and evacuating power from embedded generations via the distribution networks has also been developed by NERC. This particular guideline is proposed to encourage communities, private properties, state and local governments, investors, and DisCos to generate and sell or consume electricity without the rigours (technical and financial) of wheeling power through the transmission lines. Although these ideas are directed at increasing the Nigerian electricity market’s generation capacity to 40GW by 2020, it is obvious that this is not attainable, with the present total installed capacity still standing at less than 13GW (Nigerian Electricity Regulatory Commission, Citation2020). The opportunities for generation in the Nigerian power sector are summarized in Figure .

Figure 2. Opportunities in the generation sub-sector (Adopted from https://nerc.gov.ng/index.php/home/nesi/403-generation).

2.2. Transmission

Nigeria’s transmission network is managed and operated by the state-owned Transmission Company of Nigeria (TCN). TCN, incorporated in 2005, is responsible for expanding and improving the transmission network’s reliability. TCN serves as a transmission service provider, system operator, and market operator. The TCN is saddled with providing the necessary infrastructure for wheeling electric power generated by the GENCOs to the DISCOs. The Nigerian transmission network consists of approximately 20,000 km of 132kV lines, 330kV lines, and high voltage substations with a theoretical wheeling capacity of about 7.5GW (Nigerian Electricity Regulatory Commission, Citation2020). At present, the operational generation capacity (3,879.MW) is less than the transmission wheeling capacity (5,300 MW); however, if the total installed generation capacity (12,522 MW) were to be evacuated into the transmission network, there is likely to be a system collapse. The network is also reported to suffer from transmission losses (7.4%), which are above the average (figure –6%) for emerging countries (Nigerian Electricity Regulatory Commission, Citation2020). The highest power to be evacuated to the transmission grid to date is 5,420.3 MW; this was achieved in August 2020–7 years after the privatisation process was completed (Okafor, Citation2020). Without redundancies, the Nigerian transmission network is radial and as such susceptible to poor reliability and frequent collapse.

2.3. Distribution

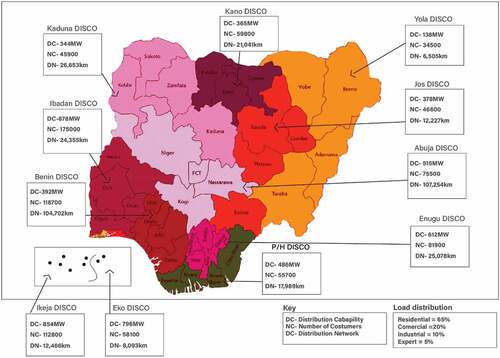

Nigeria’s power distribution network operates majorly on low voltage (11kV) and medium voltage (33kV). The distribution network spans approximately 366,363 km serving more than 8,645,000 customers across the 36 states of Nigeria (Ley et al., Citation2015).

The distribution network is radial, grossly under-maintained, and records an average technical loss of approximately 13% (Ley et al., Citation2015). With few customers being metered, the non-technical loss on the Nigerian distribution network is very high. In addition, Nigeria’s electricity sector’s privatization in 2013 gave rise to 11 privately run (DisCos), which serve consumers across the country’s six geo-political zones, as shown in Figure .

Figure 3. 11 Distribution Companies (DisCos).

2.4. Off-grid electrification

A 2013 study reported that about 80% of Nigerian have and use off-grid backup power sources such as fossil-powered generators and solar PV with inverters (Ley et al., Citation2015). The report further stated that a decentralized diesel generator’s contribution to electrification is worth between 8 and 14 GW. Nigeria leads Africa as a generator importer and is one of the highest importers worldwide, spending approximately $14 billion annually on installing, operating, and maintaining fossil-powered captive generators (Nigerians spend $14 billion on generators, fuel | Nairametrics, Citation2020). Apart from individual and corporate efforts in the off-grid generation, governments at various levels are also dedicated to improving electricity access through several off-grid electrification schemes. Through the Nigerian Rural Electrification Agency (REA), Nigeria’s federal government is responsible for remote and unserved communities’ electrification through the Nigeria Electrification Project (NEP). The REA is also responsible for administering the rural electrification fund and coordinating rural electrification programs through various private and public sector participation. The NEP includes the Energizing Education Programme (EEP), which targets clean and affordable energy for 7 University Teaching Hospitals and 37 federal universities across Nigeria. Apart from this, REA also has the responsibility of providing clean electricity access for clusters of economic hubs (shopping malls, agricultural and agro-processing, and markets) through private sector partnerships (The Nigeria Electrification Project (NEP)—Rural Electrification Agency, Citation2020).

2.5. Regional participation

Nigeria is a member of the West African Power Pool (WAPP), an arm of the Economic Community of West African States (ECOWAS) responsible for integrating member states’ national power grids into a unified regional electricity market. WAPP’s target is to provide a framework to ensure cost-effective, stable, and reliable electricity for ECOWAS region citizens at both long-term and medium-term timescales. It covers the public and private generation, transmission, and distribution companies. Nigeria contributes 53.98% of the pool’s total viable capacity (Benin ICC | WAPP Information and Coordination Centre, Citationn.d.). Though not adequately documented, there is a level of electricity trading between Nigeria and some members of the WAAP (Togo, Benin Republic, and Niger). In 2020, Togo, Benin Republic, and Niger were indebted to Nigeria up to a total sum of N29.97 billion for the electricity supplied to them between January and September 2019 (Togo, Citation2020).

3. Market regulation

3.1. Regulatory agencies and functions

Several agencies of government define regulatory policies regarding the power sector in Nigeria. These are the Nigerian Electricity Regulatory Commission (NERC), Federal Ministry of Power, Works and Housing (FMPWH), Nigerian Electricity Management Services Authority (NEMSA), and Energy Commission of Nigeria (ECN). The others are Nigerian Transmission Company (TCN) and Bulk Electricity Trading (NBET) Plc. NERC is the statutory body responsible for regulating the electricity industry in Nigeria. NERC initiates economic and technical regulation of the electricity sector via the governing statute as a regulator. These regulations include setting tariffs while considering fair pricing, promotion of competition, and investment, especially the private sector’s involvement, among several other responsibilities. FMPWH stipulates government policy direction and coordinates the activities of the rest of the regulatory agencies. The Ministry aims to establish and promote electricity sector policies and programs to ensure a reliable electricity supply across all energy sources. The technical standards and requirements in this sector are regulated and enforced by the NEMSA. The ECN was formed with the legal provisions of the systemic management and scheduling of national energy policies and programs. ECN promotes energy diversification and strategically plays advisory roles, primarily regarding adequate energy funding for federal and regional governments. The TCN operates the country’s electrical transmission system. It was unbundled in April 2004 from the former PHCN formed by a merger of PHCN’s transmission and system operations. The NBET manages and supervises the Nigerian electricity pool in the Nigerian Electricity Supply Industry (NESI).

3.2. Electricity tariff

Electricity tariff methodology has evolved in Nigeria over the years, with a non-cost-reflective tariff already in place. NERC, on 31 March 2020, issued the Order on the transition to Cost Reflective Tariffs in NESI (Analysing the Recent Nigerian Electricity Regulatory Commission Order on the Transition to Cost Reflective Tariffs in the Nigerian Electricity Supply Industry | Nigeria | ICLG.com Online Updates, Citation2020). The cost-reflective tariff is proposed to be replaced by the future service-reflective tariff. NERC regulates and sets electricity tariffs, emphasizing the achievement of cost-reflective tariffs over a given period. At the dawn of electricity industry privatization, tariffs were ordinarily non-cost-reflective, implying the initial under-recovering investment. However, the tariffs were intended to increase to an economic level that eventually led investors to over-recover their initial and generate significant profit needed to promote competition and continuous investment. The NERC aims to migrate from a solely cost-reflective tariff approach and sculpting idea to a service-reflective method in the nearest future. Consequently, NERC’s emphasis on ensuring that tariffs are enough to meet costs and provide fair investment returns will ensure that tariffs reflect service delivery quality.

3.2.1. Multi-year tariff order (MYTO)

Multi-year tariff order (MYTO) is the incentive-based tariff model that aims to recompense all system operators’ performance improvements above specific requirements, decrease technical and non-technical losses, and contributes to cost recovery and enhanced standards. It is a standardized tool for calculating the overall sectoral revenue requirement with observable changes in performance and standards in wholesale and retail prices for electricity in the industry (Arowolo & Perez, Citation2020). The MYTO aims to set cost-reflective tariffs representing the efficient financing and functioning of the sector. The approach allows tariffs to be shaped over the regulatory price control period to “sculpt” tariffs to avoid customer price shock. This sets out a fifteen-year electricity industry tariff roadmap with specific slight revisions every year, considering certain parameters like inflation, interest rates, exchange rates, and production capacity. Furthermore, significant revisions are made in consultation with stakeholders every five years when all the feedback is analyzed. That permits the tariff upgrade to reflect new macroeconomic and sectoral factors, for example, inflation, exchange rate variation(USD to NGN), and grid generation capacities (Adeniyi, Citation2019).

The MYTO implements a building block technique to set distribution and transmission tariffs that offer price controls and incentives advantages by integrating all associated electricity costs into a standardized financial system. The first two blocks are the return on invested capital (ROIC): market and asset depreciation-based. The last is the overhead and resourceful running cost. Finally, long-run marginal cost (LRMC) is the incremental cost incurred by a generating station when all inputs are variable. Hence, The generation tariff is estimated with the most financially viable new market entrants’ LRMC standard.

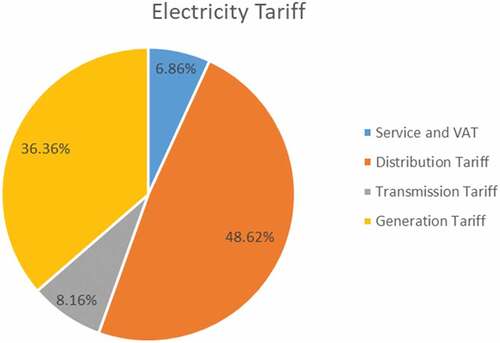

The retail electricity price to consumers consists of four units, as shown in Figure . MYTO provides a simple segmentation and evaluation of required operational expenses, overhead, and a real investment return to create transparent tariffs with credibility and widespread acceptance.

Figure 4. Four units of retail electricity price to consumers consists.

3.2.2. Service-reflective tariff

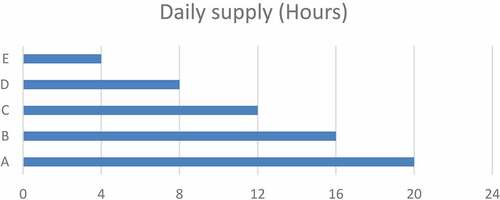

The new tariff determination is proportionate to the electricity supply to the respective customers in compliance with service criteria (more extended and more stable supply hours and less frequent interruptions or supply at the required voltage). The tariff model simultaneously implies cost recovery and ensures that customers always get value for their pay. Consequently, DisCos are now disaggregating and grouping customers into various bands (A, B, C, D, and E, as shown in Figure , concerning their daily electricity supply meeting the different service criteria (including the number of supply hours). This helps DisCos to charge customers according to the service quality parameters.

Figure 5. DisCos’ grouping of customers.

DisCos service evaluation criteria include hours of electricity supply, supply reliability determined by disruption frequency and length, and power quality (operating voltage magnitude and frequency specified by grid code). Future tariff adjustments will be based now on negotiations and agreements between DisCos and consumer clusters. If DisCos not meet performance goals, incentives will be used to reimburse consumers.

3.3. Bulk electricity procurement

The NBET engages in the purchase and resale of power and associated ancillary services from independent power producers (IPP) and the now privatised Generation Companies (GenCos) to Distribution Companies (Discos; Longe, Citation2016). NBET, as a bulk electricity dealer, acts as a broker by initiating viable power purchase agreements (PPA) with the IPPs and the GenCos, as shown in Figure .

Figure 6. Bulk electricity purchase.

MYTO regime specifies wholesale and retail tariff services, including charges for power transmission. The base cost of the electricity tariff defined by the generation cost module is 36.36% of the retail tariff, as shown in Figure . This is the wholesale price that the bulk buyer, NBET, purchased electricity from GenCos and IPP before selling to DisCos. GenCos and IPPs can recover their capital return, operating, and overhead costs under the cost generation module. The GenCos decide their respective wholesale electricity price with NBET through a PPA authorised by NERC. However, the IPPs are prohibited from recovering their capital or capital return. This is because the IPPs are paid only for their cost of operation and not for investment in gas power plants. This module is critical as it determines the generation lucrativeness to private investment. The government also considers it significant, as it is, in reality, among the few tools to encourage competition in the market hitherto dominated by natural monopolies. As inflation shifts, exchange rates, and gas prices changes, the wholesale tariff is also adjusted.

The transmission cost module, also known as the “grid charge” or Transmission Use of System (TUoS) Charge, is the second layer of the electricity tariff in Nigeria, contributing 8.16 % of the retail tariff by the DisCos to TCN. Using the TCN’s transmission infrastructure to transmit power to substations under DisCo ownership for distribution is the cost. The TUoS enables TCN to recover current and projected capital costs and effective operational costs and make capital return and maintenance provisions. However, NERC controls the TUoS, which is uniform across the country and susceptible to inflation and the exchange rate.

The smallest and third module of the electricity tariff is the service and VAT, which amounts to 6.86%. The service and VAT consist of the agency running cost of NERC and NBET regulating and operating the NESI.

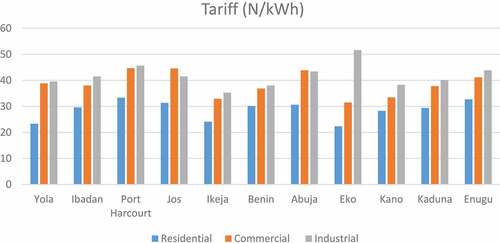

The distribution cost is the highest and last layer and accounts for 48,62% of the overall price for electricity which is charged by the DisCos. The cost is different in the eleven DisCo networks, as shown in the year 2020 average tariff depicted in Figure . Hence the tariff at the distribution level depends on the type of customer: residential, commercial, industrial, street lighting, and special tariff. The customer categories are further subdivided into groups based on the number of phases, voltage level, and demands.

Figure 7. Tariff charged by the DisCos in 2020.

4. Government-motivated policies and reforms

4.1. Need for reforms

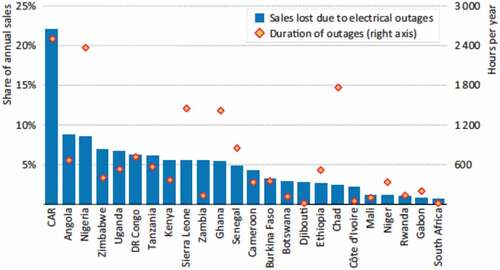

The protracted non-performance compels the Electric Power Sector Reform Act 2005 and the Roadmap for Power Sector Reform 2010 in the power sector. The reform’s implementation led to significant developments, including disaggregating and privatizing the power sector (E. K. Ogunleye, Citation2016). The Act gives legal support to the reform. At the same time, the road maps are used as a mechanism to quickly track and ensure that the proposed structural changes in the ownership, control, and management of the sector are enforced and enforced, particularly to the benefit of electricity users. The Act focuses on establishing a regulatory body to ensure efficient regulation and compliance with the electricity sector laws. The privatization of the market is underlined. In the same vein, the concept of a feed-in tariff system is being implemented. It allows renewable energy companies to sell electricity to the grid at prices significantly above those producing energy via traditional gas, coal, and hydro sources: the NBET’s assured electricity procurement and a five-year exclusion from renewable energy investment tax. As shown in Figure , the apparent challenges negatively affecting businesses have necessitated the reform’s conception as depicted.

Figure 8. Electricity outage duration and impact on business sales in certain selected countries in Africa. (Africa Energy Outlook Citation2019—Analysis—IEA, 2019).

It must be noted that moderate progress was made in executing the power sector reform. First of all, the former NEPA and later PHCN were unbundled, and 11 distribution firms, six generating firms, and one transmission company were born. Secondly, a cost-reflective tariff (MYTO) is introduced to make the industry attractive to domestic and international investors. Third, many IPPs with 2,500 MW aggregated capacity have been added to the system. Fourthly, NERC was created. Fifthly, considerable efforts are underway to develop the gas-to-power plan, the country’s biggest electricity supply bottleneck amidst pipeline vandalism and gas pricing policies. Finally, many policies and market rules have been formulated to govern the evolving privatised electricity sector at various reform phases.

4.2. Key policies

Some rationales for the unbundling of policy are the industry’s strategic importance, uniformity, economies of scale, and efficient communication. The recent restructuring of Nigeria’s power sector is traced to September 1990, when the former NEPA was partially commercialised (Okoro & Chikuni, Citation2007). With the creation of the National Electric Power Policy in 2001, the change was given a further policy drive. This policy resulted from a survey conducted by the government in 1999 to identify the power sector’s challenges and provide guidelines to transform the sector. This policy provided the foundation for the reform plan and signified the birth of Nigeria’s modern power sector. In 2005, the reform was given great impetus by the Electric Power Sector Reform Act (EPSRA), introduced to provide legal support for the reform and implement the strategy. The reform’s overall purpose is to improve the productivity, transparency, reliability, standard, and affordability of electricity supply to spur economic transformation, growth, and development. The former NEPA was transformed into PHCN and subsequently unbundled following the procedures drawn in the EPSRA. Key policies since 2001 are shown in Figure .

Figure 9. Timeline of key policies.

The system has designed many policy measures, proclamations, and reports to steer the power sector’s reform process. The Nigeria Energy Commission established and adopted the 2003 National Energy Policy (NEP) for the energy sector. The target of 75% electrification by 2020 encompasses all forms of electricity, including renewable energy, energy conservation, and rural electrification. The 2007 National Energy Master Plan (NEMP) lays out the National Energy Policy (NEP) structure for implementation. The government approved the National Electric Power Policy (NEPP) in 2001 to set out the power sector’s basic structure. Roadmap for Power Sector Reform in 2010 was leveraged on the Electricity Master Plan (EMP) of 2008 and 2013 to identify the critical barriers affecting the power sector’s full liberalisation and energy sufficiency. The 2015 National Renewable Energy and Energy Efficiency Policy (NREEEP) conceptualizes energy efficiency and renewable energy strategy. The Energy Commission of Nigeria (ECN), along with the United Nations Development Programme (UNDP) 2006, developed the Renewable Energy Master Plan (REMP), which was reviewed in 2012. The structure and goals for the rural electrification program are set out in the Rural Electrification Policy Paper (REPP), approved by the government in 2009, which targets 10% of the energy mix for renewable sources by 2025. The Electric Power Sector Reform Act (EPSRA) empowers the Rural Electrification Agency (REA) to develop its operational plan and strategy. However, this must be done in consultation with the NERC and ratified by the government.

The NREEEP, which was officially approved in 2015, is the power sector policy pool. The policy seeks to implement programs to achieve sustainable and inclusive development by effectively using energy resources in the country. The policy seeks to tackle various renewable energy concerns: planning and policy implementation, regulations, research and innovation; enforcement and rules; supply and use; funding and pricing; training and technical; performance and sustainability; execution of initiatives; gender; and climate change.

5. Main challenges of the Nigerian power sector

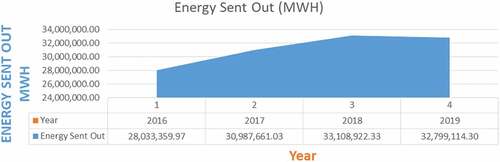

Nigeria’s power sector has been through a difficult period necessitated by diverse infrastructure issues, inadequate generation capacity, system collapse, government and foreign policy, inadequate funding, and corruption. As a result, electricity consumers have largely experienced frustration as basic electricity cannot be provided for citizens to contribute actively to our nation’s economic growth. According to the Bureau of Statistics, Figure shows the eneggy generation and distribution in Nigeria between the years 2016 and 2019.

Figure 10. Power sector report: energy generated and sent out and consumed and load allocation (2019; NATIONAL BUREAU OF STATISTICS, Citation2020).

Over the past two decades, the successive government has tried to find a solution to generation capacity issues by assuming a monopoly role in generating, transmitting, and distributing power where billions of the country’s hard-earned resources have been invested in power with meagre improvement.

In August 2010, the power sector reform roadmap was launched to lay the groundwork for transferring the private sector’s power utilities’ operations. Finally, in 2013, six (6) power-generation plants and 11 distribution companies unbundled from Nigeria’s power holding company were sold to private investors. (Challenges facing the Nigerian power sector, Citation2016), (Ayamolowo et al., Citation2019a). This new transformation raised expectations as it was assumed that the new investors would rapidly end frequent power outages and meet up with the populace’s power demands. However, the initiative has brought little improvement as numerous issues still hamper the electricity growth in Nigeria. Below is the graph shows the energy sent out from 2016 to 2019. The analysis shows that there is still a large deficit. This write-up aims to look at the challenges hampering the power sector fulfillment and resolve this deficit.

5.1. Absence of bankable gas supply agreement

The bulk of power generated in Nigeria has its source mainly from thermal and hydro, with the estimated percentage at 80% thermal and 20% hydro http://cseaafrica.org/challenges-and-interventions-needs-in-the-nigerian-electricity-supply-industry-nesi/. The thermal plants require natural gas to fire its turbines to generate power. However, it is unfortunate that the gas is either unavailable or in short supply. A large part of the issue is the absence of a robust gas network to efficiently run this plant and an inactive service level agreement, i.e., a gas supply agreement to drive efficiency. Nigeria’s power sector is a critical institution with diverse interdependencies that must be carefully aligned to deliver the Nigerian populace’s power demand consistently. Running a large institution such as the power sector with significant dependency on other sectors without a service level agreement will run into chaos. Its operations will be unstable; value creation will be limited or nonexistent.

The Nigerian national grid’s design capacity is about 7500 MW, and power generated and supplied to the grid instantly has never been up to 6000 MW. (Nigerian Electricity Regulatory Commission, Citation2020). One tends to ask the question, why? The shortage of gas has rendered most of the thermal power plants idle. There is no accountability because there is no agreement and, therefore, no efficiency in service delivery. This has hampered our economy. Table below shows the status of the Gas Supply Agreement for the various power plants.

Table 1. PPA power plants statuses (Nigerian Electricity Regulatory Commission, Citation2020)

5.2. Power purchase agreement

The power purchase agreement is a contractual obligation between the privately-owned power plant and the state or government-owned electric utility like the Nigerian Bulk Electricity Trading (NBET) in the Nigerian power sector. NBET is 100% owned by Nigeria’s Federal government and is referred to as the “manager and administrator of the electricity pool” in the electricity supply industry. The power purchase agreement is a powerful document that provides the guidelines and contractual obligations of both the private power investor and NBET. It is disheartening to note that this agreement is not yet active for most power plants. (Arowolo & Perez, Citation2020. This document’s inactive nature has created a gap that makes the investor reluctant to commit more resources to an existing investment. Most of the power infrastructure is dilapidated and requires repair, replacement, or upgrade. This has hampered the growth of the power sector. The GIZ study estimated electricity demand in Nigeria to rise to 45,490 MW by 2020 and 213,122 MW by 2040 (Challenges and Interventions Needs in the Nigerian Electricity Supply Industry (NESI), Citation2020). With the rate we are handling the critical issues affecting electricity in Nigeria, it might just be a lofty and unattainable foot to achieve the power demand. The economy will be the recipient. A little wonder, our power sector reflects our economy, and unless we get this right, our economy will remain stunted. The power purchase agreement documents include the following;

Duration of PPA is a 20 years tenor by NBET standard and provides clauses to take care of early termination due to either party’s default.

Tariff Structure—makes available the guide on how NBET will make payment for the duration of PPA

Resolution of Conflict—defines the processes for resolving conflict as regards disputes or issues on the invoice.

Metering—clarify the metering and metering code rules supersedes the conflict between PPA provision and metering code.

Allocation of Risk—captures all the risk related to the project and allocate these risks to the best party who can bear them.

Testing and Commissioning—gives detail of the testing and commissioning of the power plant.

Operation and Maintenance—provides the details of the private investor’s operation and maintenance responsibilities throughout the PPA duration.

Precedent Conditions—indicates all the prerequisite conditions that either party must fulfill before the PPA can become active.

Liability and indemnity—highlight the parties responsible for specific types of failures and provide both parties’ indemnity.

Project Document—states all the documents connected to the PPA, such as the design, procurement, construction, Gas Transport Agreement, Gas Supply Agreement, and Finance documents.

Force Majeure—Provides the scenario’s details to be considered a force majeure and the payments to be made in the occurrence. https://nbet.com.ng/our-customers/generation/key-parts-of-ppa/

Furthermore, this essential document’s absence is counterproductive and tantamount to the inefficiencies the country currently experiences in our power sector. Table shows the status of the PPA for the various power plants.

5.3. Shallow domestic finance

Power generation, transmission, and distribution are not cheap. Significant investments are required to keep the infrastructure top-notch. Nigeria’s transmission company, which is 100% owned by the federal government, is responsible for providing the power sector’s enabling environment and critical infrastructure. The yearly power budget is still insufficient to eradicate the years of neglect and dilapidation the power infrastructures have been subjected to. It will require massive investment, and the government is handicapped due to limited resources and the many facets of the economy competing for national resources. Attracting private investors is also a big issue because the investors are not sure of making profitable returns due to the business environment and the state of the current infrastructure. The current investors also have limited access to the loan facility and guarantees due to the Nigerian banks’ conservative nature and fear of investment going down the drain. Most privatised power companies’ financial statements also show consistent losses over the years, even when revenue increases. Table below shows a sample financial statement of one privatised sector.

Table 2. Privatised sectors’ sample financial statement

5.4. Adequate transmission and distribution facilities

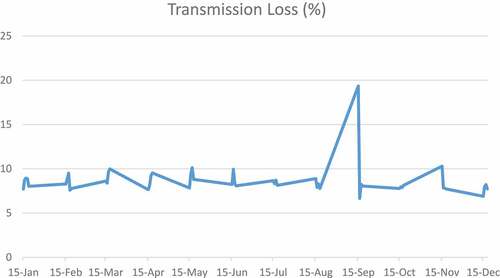

The Nigeria transmission network spans about 20,000 km with a wheeling capacity of about 7,500 MW. It is a radial network without redundancies and hence unreliable. A healthy part of the network can easily experience power failure due to faults from the network’s parts. The losses estimated on this transmission network are 7.4%, which is relatively high than the acceptable threshold of 2 to 3%. Figure shows the yearly transmission losses. As the population continues to rise, the power demand increases. Studies estimated that the power demand in 2020 will be 45,490 MW and 213,122 MW by 2040. Suppose the transmission network currently has a capacity of 7,500 MW. That case shows that the transmission network’s current capacity can not address the present and future demands. Hence, massive investment is required in the expansion of the network capacity. The distribution lines, transformers, and feeder pillars are in no way better as years of neglect, and lack of maintenance and upgrade has caught up with them. The higher losses on the lines portend a rise in the bill to reconcile power sent and power received.

Figure 11. Transmission losses (Nigerian Electricity Regulatory Commission, Citation2020).

5.5. Fear of policy reversal

The government is responsible for providing an enabling environment to investors through established policies to aid the business and instill sustainability confidence. Policy change or reversal changes the dynamics and might negatively affect the business’s future and profitability. Over the years, the government has had to reverse policies due to foreign or local directions to achieve a specific purpose. The power equipment used in the power sector is import-dependent, and monetary policy changes considerably affect purchasing power. They could be detrimental to investments needed to upgrade critical power infrastructure. In May 2020, the senate recently requested that the government suspend the proposed increase in electricity tariff, scheduled to take off on 1 July 2020. It also moved the motion for the immediate reversal of the power sector privatisation completed by the government due to what they termed “failure to deliver.”This could lead to undesirable consequences and revenue loss for current private investors. Due to this unstable environment that the policymakers and the government have created, the fear of policy reversal creates serious fear in private investors to commit huge resources to improve our current power systems. Government and policymakers must invest their energy in setting regulations encouraging investors to channel more of their resources into the power sector rather than regulating to suffocate it.

5.6. Non-cost reflective tariffs

Due to the poor state of the power infrastructures before privatisation, there is a shortfall in the private investment for required deliverables and expected reliability. Due to importation duties on parts, gas pricing, exchange rates, and inflation, the ever-changing cost of running the generating plants has made it very difficult for investors to balance their books. As a result, most of them have been declaring losses in their end-of-year financial statements. The tariff is currently not reflective of the cost of generating power. Hence, the loss has been declared by the investors. This will only make the electricity sector stagnant and unsustainable with limited investment and the system’s eventual collapse.

The Nigeria Electricity Regulation Commission ensures that the investor’s tariff is fair and adequate to finance their operations while still making sensible profits from efficient operations. NERC developed a system known as the Multi-year Tariff Order. It is a tool meant for setting cost-reflective tariffs to enable funding and functioning of the power sector. The minor review is twice a year, considering ± 5% changes in a defined parameter such as generation capacity, gas prices, inflation, and exchange rates corresponding to tariff implementation adjustment. Similarly, a series of significant reviews in 5 years is expected to cover the costs of generating electricity, transmission system usage, regulation, market operation, and distribution charges. However, MYTO 2015 is based on specific parameters and assumptions that have seriously affected other factors and have become unrealistic. Moreover, the economic parameters used have also changed rapidly and in no correlation to the 5 years duration of the review. As a result, there has been a tariff shortfall, meaning Discos’ allowable revenue has fallen short of what the real revenue is supposed to be. Table shows the difference in the MYTO Tariff assumption.

Table 3. MYTO Tariff assumption and variations

(Cost-reflective tariff in the Nigerian electricity supply industry (NESI)—Businessday NG, Citation2020)

The table clearly shows a huge difference between the forecast and the reality of December 2019. The overall effect of this is the tariff shortfall that the private investors are experiencing. It is non-cost reflective of their operations and a dangerous omen for the power sector’s future.

5.7. Vandalisation

The vandalisation of gas pipelines, transmission, and distribution lines is rampant and poses a serious threat to private investors. There is also colossal revenue loss associated with this due to the plant’s risk and cost of non-operation. The vandalisation of gas pipelines and power infrastructure has limited the development of the power sector. Table captures some of the vandalisation recorded

Table 4. Recorded vandalisations

6. Way forward

Like other sectors of Nigeria’s economy, the policies directed at improving Nigeria’s electricity sector have been largely imported, with few homegrown policies addressing Nigeria’s peculiarities. In this work, we put forward a proposed power sector structure that can solve the sector’s many protracted problems; the structure will, in turn, substantially turn around the national economy. This proposed structure is wholly deregulated, liberalised, and subject strictly to demand and supply. Figure shows that the subsector’s generation, transmission, and distribution freely and flexibly, without regulatory restrictions, interact with one another and the consumer. The key differences between this model and the existing structure are;

Generation companies of different categories and sizes freely and directly trade with distribution companies and consumers while trading with the transmission grid operators.

The exchange of services/product for revenue is a two-way interaction among all sectors driven solely by the free-market force of demand and supply.

Multiple transmission grid operators with government-licensed trade associations enforce a framework for an operation that makes these grids easy to integrate into a single, smart national grid.

Figure 12. Proposed approach for improving the Nigerian electricity sector.

6.1. Generation

The most discussed topic in Nigeria’s electricity sector is the sector’s generation capacity; as stated earlier in this work, the national grid’s transmission capacity is less than the total operational capacity of available grid power plants. This capacity shortage shows that generation capacity shortage is not the sector’s most critical challenge, contrary to popular belief. Frequent grid collapse and power rejection by distribution companies (Discos reject 17,657MW as power outage persists—Punch Newspapers, Citation2020) show that even if more power is generated, these capacities cannot be wheeled to the consumers. This notwithstanding, Nigeria is in dire shortage of generation capacity. The solution to this shortage is not more budget to deliver more power plants (as most socio-political analysts believe). However, the solution lies in the right economic policies that can attract needed investment from private investors who can key into the model described above for opportunities.

If supported with the right policies, this model will promote a wide range of investors. Most importantly, medium-scale investors will come into the sector as off-grid generation, captive, and embedded generation operators; these solutions can be delivered without the hindrance of the national grid capacity shortage. Many value chains in the electricity sector and sectors in primary energy sources will also take a new life of their own from these activities. Typically the proliferation of these embedded, captive, and off-grid plants will spur investment opportunities in sectors like natural gas distribution; these are definite progressions driven by free-market forces and opportunities.

6.2. Transmission

In the model proposed, less emphasis is on the national grid as it is currently operated. Total deregulation and liberalisation of Nigeria’s electricity market will attract investors into the national grid sector. The current grid capacity cannot handle the capacities this model can deliver hence the investors’ involvement in driving toward a smarter grid. The smart grid comprises as many mini-grids of various sizes and capacities as there can be across the nation, developing as described under generation in the last paragraph; a privatised TCN only becomes a major player in this free market scheme through it is existing vast infrastructure.

The main policy objective that the national grid regulations would seek to achieve would be a framework for integration/interlinking of these mini-grids with sizeable capacities into a new smart national grid. Today, there are technologies to achieve these interlinks. However, only investors in a deregulated and liberalised market can bring them to bear. The government’s core objective and responsibilities in this model are national security, not pricing or other economic decisions. They only set the framework for regulating a deregulated electricity sector to preserve national security, public safety, and consumer rights.

6.3. Distribution

Contrary to the most popular public opinion in Nigeria, the weakest link in the Nigeria electricity sector is the distribution sub-sector because infrastructure is most deficient in this subsector. The deficiency impacts the sectors’ entire value chains. Most studies and public discourse have been about generation capacity deficiency. The alarming and worse deficit in the distribution system is rarely discussed; hence the public’s public perception sadly influences political and economic decisions, especially by the government. In the model proposed in this work, the government is expected to go further than its recent efforts, including privatising the distribution companies and, most recently, the service-reflective tariff by NERC. Policies that totally deregulate and liberalise the sector are needed to attract the right investment to bridge the distribution system’s infrastructure gap.

Understandably, deregulation/liberalisation of the distribution sub-sector will particularly face the most opposition from the public, given how many Nigerians see electricity as a social right owed to them as against it being a commodity to be traded. This is particularly substantiated by (Babatunde et al., Citation2020), showing how much it costs homes and small businesses to generate captured power. Therefore, a government with the will to deregulate and liberalise the electricity sector is what it takes to make a difference. The case modelled in this work is the totally deregulated and liberalised electricity sector. As indicated in Figure , the value chains best drive one another when the market force is allowed to play out. Consumers will pay more initially, but as the sector evolves and grows, the tariff will come crashing; this is already evident in the telecommunication sector. Therefore, it goes that popular say from most socio-economic pundits to the government that; “Fix electricity, and the economy is fixed” should be “hand off electricity, and a liberalised viable electricity sector will fix the economy”.

7. Conclusion

In the Nigerian Government, 1999 proposed implementing diverse reforms that would transform the state-owned vertically operated electricity industry to a more efficient unbundled market consisting of various agencies and companies coordinated by an independent regulator. The restructuring has improved the infrastructure capacity and service deliveries across the market’s value chain. Based on the discussions from the previous sections, the actors in the NESI pay attention must propose effective ways of addressing the various challenges highlighted in this study. Although the NESI is now deregulated and the private sector is driven, its significance to industrial development and economic growth will entail strategic intervention from the government. The following are the findings of this study:

Various reforms have been aimed at raising the Nigerian electricity sector’s generation capacity to 40 GW by 2020, and it is clear that this is not achievable, with the current total installed capacity still below 13 GW. Operational 3,879.MW generation capacity is smaller than the 5,300 MW transmission wheeling capacity; nevertheless, a system failure is likely to occur if the total installed 12,522 MW capacity were transferred into the transmission network. The transmission network is radial and, as such, vulnerable to low reliability and frequent failure. Nevertheless, about 80% of Nigerians have decentralized off-grid 8–14 GW backup power sources such as fossil-powered generators and inverter solar PVs and use them. Still, there is electricity trade between Nigeria and some West African Power Pool members amidst Nigeria’s lack of electricity supply to the extent that member countries owed Nigeria a total amount of N29.97 billion.

The framework for electricity tariffs has grown over the years in Nigeria, with a non-cost-reflective tariff. Cost-reflective tariffs are proposed to replace non-cost-reflective tariffs with potential service-reflective tariffs. MYTO comprehensively optimises and analyses the necessary operating expenses, overhead, and a real return on investment to build straightforward tariffs with integrity and widespread adoption. Non-cost-reflective MYTO 2015 is focused on essential criteria and projections, which have become impractical and have seriously affected other variables. Future changes to tariffs will now be focused on deals and agreements between DisCos and groups of customers. If DisCos fails to achieve performance targets, bonuses may be used to repay customers. The IPPs are only charged for their running expenses and not for investments. This module is significant as it establishes the viability of the generation for private investment. It is also considered critical by the government. It is one of the few instruments to promote competition in a market previously controlled by natural monopolies.

The bulk of electricity produced in Nigeria comes predominantly from thermal and hydropower, with an approximate percentage of 80 percent thermal and 20 percent hydropower. Running an extensive system such as the power industry with substantial reliance on other sectors without a service level agreement would create frustration with unpredictable services. The power purchase agreement’s ineffectiveness has created a void that prevents the investor from investing more capital. The annual power budget is inadequate to eliminate the years of mismanagement and decrepitude of power infrastructures. Furthermore, the existing transmission network cannot transmit the installed 7,500 MW capacity, implying that the present transmission will not handle future generations and demand. Thus, the expansion of the network capacity is inevitable with massive investment. Policy shift or reversal affects the dynamics and may adversely impact the future and profitability. The government has had to reverse policies due to international or local directions to accomplish a particular goal. The tariff is currently not reflective of the cost of generating power, and the investors have therefore declared the loss. Thereby making the electricity industry unstable, with narrow investment unprofitable, and the system’s eventual collapse. The malicious destruction of gas pipelines and power networks has restricted the power industry’s growth.

Policies to promote the electricity industry in Nigeria have been mostly exported with few indigenous solutions that address Nigeria’s particularities, like other sectors of the economy. This work proposed a structure for the power sector with the potential to solve the many unresolved challenges of the sector; in turn, the structure would significantly revolve around the national economy. However, this proposed system is absolutely deregulated, liberalized, and solely subject to demand and supply.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Olubayo Babatunde

Olubayo Babatunde completed a doctoral degree in Electrical Engineering at the Tshwane University of Technology South Africa in 2020. He is a registered Engineer in Nigeria and also a member of the American Energy Association.

Elutunji Buraimoh

Elutunji Buraimoh is a member of IEEE. He completed his Doctor of Engineering at Durban University of Technology, South Africa. His research interests include inverter-based microgrids, renewable energy, power systems control, and FACTS devices.

Oluwatobi Tinuoye

Oluwatobi Tinuoye finished his master’s degree in Electrical Electronic Engineering, University of Lagos. He is a registered Power System Engineer.

Clement Ayegbusi

Clement Ayegbusi finished his master’s degree in the Department of Electrical Electronic Engineering, University of Lagos. He is currently with Clema Engineering Consultants, Lagos, Nigeria

Innocent Davidson

Innocent Davidson is currently a Full Professor and the Chair of the Department of Electrical Power Engineering, Durban University of Technology, Durban. His research interests include grid integration of renewable energy using HVDC technologies and innovation for smart cities. He holds a Ph.D. in Electrical Engineering from the University of Cape Town, South Africa, in 1998. He is also a fellow of IET, U.K., and SAIEE, a Chartered Engineer in the U.K., and a registered ECSA Professional Engineer.

Desmond Eseoghene Ighravwe

Desmond Eseoghene Ighravwe is a professor of mechanical engineering at the Bells University of Technology, Ota, Nigeria. He holds a Ph.D. degree from Ladoke Akintola University of Technology, Nigeria. His research interests include Artificial intelligence, Operations research, Production & Maintenance engineering, Decision Analysis, and Energy and Waste

References

- Adeniyi, F. (2019). Overcoming the market constraints to on-grid renewable energy investments in Nigeria. Oxford Institute for Energy Studies. Issue November https://doi.org/10.26889/9781784671495

- Africa Energy Outlook 2019 – Analysis - IEA. (2019). https://www.iea.org/reports/africa-energy-outlook-2019

- Alao, O., & Awodele, K. (2018). An overview of the Nigerian power sector, the challenges of its national grid and off-grid development as a proposed solution. 2018 IEEE PES/IAS PowerAfrica, PowerAfrica 2018, 178–24. https://doi.org/10.1109/POWERAFRICA.2018.8521154

- Analysing the Recent Nigerian Electricity Regulatory Commission Order on the Transition to Cost Reflective Tariffs in the Nigerian Electricity Supply Industry | Nigeria | ICLG.com Online Updates. (2020). https://iclg.com/briefing/14459-analysing-the-recent-nigerian-electricity-regulatory-commission-order-on-the-transition-to-cost-reflective-tariffs-in-the-nigerian-electricity-supply-industry-nigeria

- Arowolo, W., & Perez, Y. (2020). Market reform in the Nigeria power sector: A review of the issues and potential solutions. Energy Policy, 144, 111580. https://doi.org/10.1016/j.enpol.2020.111580

- Audu, E., Paul, S. O., & Ameh, A. (2017). Privitisation of power sector and poverty of power supply in Nigeria: A policy analysis. International Journal of Development and Sustainability, 6(10), 1218–1231. www.isdsnet.com/ijds

- Ayamolowo, O. J., Buraimoh, E., Salau, A. O., & Dada, J. O. (2019a). Nigeria electricity power supply system : The past, present and the future. 2019 IEEE PES/IAS PowerAfrica, 64–69.

- Ayamolowo, O. J., Buraimoh, E., Salau, A. O., & Dada, J. O. (2019b). Nigeria electricity power supply system: The past, present and the future. IEEE PES/IAS PowerAfrica Conference: Power Economics and Energy Innovation in Africa, PowerAfrica 2019, 64–69. https://doi.org/10.1109/PowerAfrica.2019.8928767

- Babatunde, O. M., Ayegbusi, C. O., Babatunde, D. E., Oluseyi, P. O., & Somefun, T. E. (2020). Electricity supply in Nigeria : Cost comparison between grid power tariff and fossil-powered generator. International Journal of Energy Economics and Policy, 10(2), 160–164. https://doi.org/10.32479/ijeep.8590

- Babatunde, O. M., Munda, J. L., & Hamam, Y. (2018). Generation expansion planning : A survey. 2018 IEEE PES/IAS PowerAfrica Generation, 307–312.

- Bamisile, O., Huang, Q., Ayambire, P., Anane, P. O. K., Abbasoglu, S., & Hu, W. (2020). Analysis of solar PV and wind power penetration into Nigeria electricity system. Conference Record - Industrial and Commercial Power Systems Technical Conference, 6, 1–5. https://doi.org/10.1109/ICPS48389.2020.9176822

- Barros, C. P., Ibiowie, A., & Managi, S. (2014). Nigeria’s power sector: Analysis of productivity. Economic Analysis and Policy, 44(1), 65–73. https://doi.org/10.1016/J.EAP.2014.02.003

- Benin ICC | WAPP Information and Coordination Centre. (n.d.). Retrieved January 3, 2021, http://icc.ecowapp.org/

- Challenges and Interventions Needs in the Nigerian Electricity Supply Industry (NESI). (2020). http://cseaafrica.org/challenges-and-interventions-needs-in-the-nigerian-electricity-supply-industry-nesi/

- Challenges facing the Nigerian power sector. (2016). http://country.eiu.com/article.aspx?articleid=1003980684&Country=Nigeria&topic=Economy_1

- Cost-reflective tariff in the Nigerian electricity supply industry (NESI) - Businessday NG. (2020). https://businessday.ng/energy/power/article/cost-reflective-tariff-in-the-nigerian-electricity-supply-industry-nesi/

- Discos reject 17,657MW as power outage persists – Punch Newspapers. (2020). https://punchng.com/discos-reject-17657mw-as-power-outage-persists/

- Eberhard, A., & Shkaratan, M. (2012). Powering Africa : Meeting the financing and reform challenges. Energy Policy, 42(1), 9–18.

- Gatugel Usman, Z., Abbasoglu, S., Tekbiyik Ersoy, N., & Fahrioglu, M. (2015). Transforming the Nigerian power sector for sustainable development. Energy Policy, 87, 429–437. https://doi.org/10.1016/J.ENPOL.2015.09.004

- Isola, W. (2016). Power Sector reforms in Nigeria: Challenges and the way forward. Unilag Journal of Humanities, 4(1), 47–62. http://ujp.unilag.edu.ng/index.php/ujh/article/view/228

- Ley, K., Gaines, J., & Ghatikar, A. (2015). The Nigerian energy sector: An overview with a special emphasis on renewable energy, energy efficiency and rural electrification. Deutsche Gesellschaft Für Internationale Zusammenarbeit (GIZ) GmbH, 151(1), 10–17.

- Longe, Y. (2016). Opportunities in the on-Grid Re Sector in Nigeria. https://www.africa-eu-renewables.org/wp-content/uploads/2016/11/NBET-Opportunities-in-the-on-grid-RE-section-in-Nigeria.pdf

- NATIONAL BUREAU OF STATISTICS. (2020). https://nigerianstat.gov.ng/elibrary

- The Nigeria Electrification Project (NEP) — Rural Electrification Agency. (2020). https://rea.gov.ng/nigeria-electrification-project-nep/

- Nigerian Electricity Regulatory Commission. (2020). Nigerian Electricity Supply Industry. https://nerc.gov.ng/index.php/home/nesi

- Nigerians spend $14 billion on generators, fuel | Nairametrics. (2020). https://nairametrics.com/2020/03/17/nigerians-spend-14-billion-on-generators-fuel-as-senators-seek-ban-on-generator-use/

- Ogunleye, E. K. (2016). Political economy of Nigerian power sector reform. In World institute for development economics research. UNU-WIDER.

- Ogunleye, E. (2017). Political economy of Nigerian power sector reform. In D. Arent, C. Arndt, M. Miller, F. Tarp, & O. Zinaman (Eds.), The political economy of clean energy transitions (1st) ed., pp. 391–409). Oxford University Press.

- Okafor, P. (2020). Electricity: Nigeria records highest grid transmission.

- Okoro, O. I., & Chikuni, E. (2007). Power sector reforms in Nigeria: Opportunities and challenges. Journal of Energy in Southern Africa, 18(3), 52–57. https://doi.org/10.17159/2413-3051/2007/v18i3a3386

- Oladipo, K., Felix, A. A., Bango, O., Chukwuemeka, O., & Olawale, F. (2018). Power sector reform in Nigeria: Challenges and solutions. IOP Conference Series: Materials Science and Engineering, 413(1), 012037. https://doi.org/10.1088/1757-899X/413/1/012037

- Oluseyi, P. O., Akinbulire, T. O., & Awosope, C. O. A. (2012). Evaluation of the roadmap to power sector reforms in a developing economy. 9th International Conference on the European Electricity Market (EEM 12), 12, 8–14.

- Onochie, U. P., Egware, H. O., & Eyakwanor, T. O. (2015). The Nigeria electric power sector (Opportunities and Challenges). Journal of Multidisciplinary Engineering Science and Technology, 2(4), 3159. www.jmest.org

- An Overview with a Special Emphasis on Renewable Energy, Energy Efficiency and Rural Electrification. (2015). https://www.get-invest.eu/market-information/nigeria/energy-sector/

- Rehermann, T., & Shi, L. (2016). Attracting private investment through power sector reforms. International Finance Corporation.

- Togo, N. Benin owing Nigeria N30bn for electricity – Commission | Africa Energy Portal. (2020). https://africa-energy-portal.org/news/togo-niger-benin-owing-nigeria-n30bn-electricity-commission

- Trimble, C., Kojima, M., Perez Arroyo, I., & Mohammadzadeh, F. (2016). Financial viability of electricity sectors in Sub-Saharan Africa: Quasi-fiscal deficits and hidden costs. World Bank. https://doi.org/10.1596/1813-9450-7788

- USAID-United States Agency for International Development. (2019). NIGERIA POWER AFRICA FACT SHEET. https://www.usaid.gov/powerafrica/nigeria

- Usman, Z. G., & Abbasoglu, S. (2014). An overview of power sector laws, policies and reforms in Nigeria. Asian Transactions on Engineering, 4(2), 6–12.

- Wamukonya, N. (2003). African power sector reforms : Some emerging lessons. Energy for Sustainable Development, 7(1), 7–15. https://doi.org/10.1016/S0973-0826(08)60344-0