Abstract

Ethiopia is one of the African countries that produce and export cotton. It has a long tradition of cotton cultivation with an estimated area of 2.6 million hectares suitable for this product. Of these 65% is found in 38 high potential cotton-producing areas and the remaining 0.9 million ha or 35% is in 75 medium potential districts. Of the total land under cotton cultivation, 33% is cultivated by small holders, 45% by private farms and 22% are state-owned farms. But, Ethiopia shares only 5% of total cotton produced in Africa. This is because it recently cultivates only 3% of the total suitable land for cotton production. Ethiopia produces an average of 33,842.11 metric tonnes in the year 2000–2018. The production trend shows some declining stage since 2012. Natural and technological constraints were existed for cotton production in this country. The country also participates on the export market and earned an average of $14,336,667 especially in the last decade. Currently the country exports with an average price of $1.45. Cotton market has also some constraints like price disincentives and lack of market information. Despite its inefficiency the cotton sector still has its own vital economic role on textile industry and employment creation. It employs about 52,754 smallholder farmers. Therefore, it is recommended that the government, the producers and other relevant stakeholders should work in collaboration to solve the constraints.

PUBLIC INTEREST STATEMENT

Ethiopia has a long tradition of cotton cultivation with an estimated area of 3 million hectares. Though its role on textile industries, the current level of cotton production and marketing is not at its optimum level due to immense internal and external factors. Therefore, the author is Highly interested to recommend a collaborated work between the government and farm Households to encourage this product.

Competing Interests

The authors declare no competing interests.

1. Introduction

1.1. Background and justification

Cotton is an important cash crop to a number of both developed and developing countries. It has a strong poverty reduction impact, because it is cultivated in small family farms in areas where opportunity for growing other crops are very limited and per capita income very low (Goreux, Citation2004).

In 2007, cotton was grown in 90 countries. Cotton cultivation cost is lower in Africa as compared to other countries. But, the share of African countries in the world market is only 12% (USDA, Citation2010). In this continent, cotton is typically a smallholder crop, and the main cash crop grown in rain-fed land where the use of purchased inputs such as chemicals and fertilizer is minimal (Bosena, Bekabil, Berhanu, & Dirk, Citation2011).

According to Sneyd (Citation2006), production of cotton in sub-Saharan Africa raised by a factor of 8.5 from 200,000 tonnes per year to over 1,700,000 in 2004/05 while during the same period the world production volume only tripled. However, over the past decade yields have stagnated at roughly half due to lack of irrigation and due to inconsistency in the provision of inputs and advice across the region. Additionally, the author showed that the land covered by cotton is increasing while the productivity of cotton is still only half of the world’s production in Africa (Ibid).

Ethiopia is also part of sub-Saharan African countries that produce and export cotton. It has a long tradition of cotton cultivation with an estimated area of above 2.6 million hectares suitable for the cultivation. The major markets for Ethiopian cotton are Africa, Asia and Europe, with Asia alone accounting for 67% of the total exports (EIA, Citation2012). Currently, the price of Ethiopian cotton is determined by textile industry development institute as Grade “A” ($1.47/kg), Grade “B” ($1.43/kg) and Grade “C” ($1.40/kg). But Ethiopia shares only 5% of total production in Africa (Ethiopian Investment Agency [EIA], Citation2012; ESTC, Citation2006). Going through these reports, despite its available land to produce abundant cotton, Ethiopia performed weakly in its production and marketing of cotton products. Therefore, these contradicting issues on the production and its marketing of cotton product enhanced us to review different literatures.

1.2. Objectives

The overall objective of this paper was to assess cotton production and marketing circumstances in Ethiopia, and it specifically reviewed;

Cotton production trend in Ethiopia especially in the millennium

The cotton production constraints

The cotton marketing trend and

The economic role of cotton production in Ethiopia.

2. Methodology

The design of this review study is involved a quantitative analysis. Intensive review of both published and unpublished documents from websites of governmental and nongovernmental organizations was undertaken. Therefore, the data collected, organized, analysed, interpreted and evaluated here are obtained from secondary sources. Different authors and researchers have written on this issue; all the available sources have been used to assess the current production and market situations and the major constraints of cotton produce in Ethiopia. Therefore, descriptive statistics followed by its interpretation of the raw data obtained from organizational sources were employed for the justification of the results.

3. Result and discussion

3.1. Cotton production trend in Ethiopia

Ethiopia possesses 2,697,640 million hectares of land suitable for growing cotton; an area that equals the cotton land in Pakistan, the world’s fourth largest producer (EIA, Citation2012). Sixty-five percent (65%) is found in 38 high potential cotton-producing areas while the remaining 35% is in 75 medium potential districts. Of the total land under cotton cultivation, 33% is cultivated by small holders, 45% by private farms and 22% are state-owned farms (Admassie, Seid, May, Megquier, & Moreland, Citation2015).

Ethiopia recently cultivates 3% of the total suitable area for cotton production (EIA, Citation2012). The annual production of seed cotton was approximately 120,000 tons in the year 2011 to 2013 with an overall yield of 1.42 ton/hectare (Alebel, Firew, Berihu, & Mezgebe, Citation2014). Currently, majority of the cotton cultivation takes place in the Awash Valley, with some cultivation also taking place in Gambella, Humera and Metema. Ethiopia can also produce irrigated cotton. Out of 84,000 hectares of land that is under cotton cultivation, only 35,000 hectares is irrigated. The major potential cotton-growing areas include Omo, Ghibe, Wabi-Shebelle, Awash, Baro-Akobo, Blue Nile and Tekeze river basins (ICAC, Citation2014).

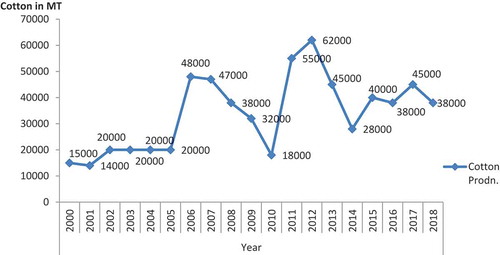

Figure 1. Lint Cotton production trend in Ethiopia (2000–2018).

Source: FAOSTAT (Citation2011) and USDA (Citation2018)

As shown in Figure , Ethiopia produces an average of 33,842.10 metric tons of cotton in the year 2000–2018. With these year durations, Ethiopia produces a minimum of 14,000 in the year 2001 and a maximum of 62,000 metric tonnes in the year 2012.

3.2. Cotton production constraints

For the last several decades, Ethiopian cotton farmers have primarily been using one major seed variety which is becoming increasingly vulnerable to pests and diseases. According to Textile Industry Development Institute (TIDI) report in 2015, the cottonseed that currently being used varieties are (e.g. California and Delta); that were sourced from the United States more than 20 years ago (TIDI, Citation2015).

During the most recent crop season, farmers reported sizeable losses resulting from bacterial blight, Flea Beetle, Pink Bollworm and Mealy bug. In some cases, these losses came after unfavourable weather conditions occurred through several rounds of pesticide application. Meanwhile, the cotton bollworm is one of the pest challenges farmers struggle to manage. Commercial cotton farms are said to be experiencing a serious shortage of labour to help with planting, weeding and harvesting. Many labourers are reportedly choosing to work at the state-owned sugar plantations where they receive better wages and benefit packages which include housing, transport and medical care. In other instances, labour is scarce because of the seasonal demand for workers to help with the coinciding cereal harvest. These labour shortages have occasionally led to delays in some farms harvesting their cotton which has impacted the quality of the harvested cotton.

In addition to the challenge of finding enough labour, some farmers are holding back growing more cotton, switching to other crops, or quitting the business altogether due to the increasingly erratic weather conditions, difficulty accessing inputs, lack of credit, rising production costs and an inefficient marketing system. GOE has placed considerable emphasis on ramping up sugar production with the intent of making the country one of the world’s top 10 sugar producers. The Tendaho cotton farm, which previously was one of the country’s largest cotton-producing farms, was converted to sugar several years ago. In addition to Tendaho, several other smaller cotton operations have switched to sugar production.

Second, the limited availability of quality inputs, including seed and fertilizer, and pest challenges have restricted the potential expansion in cotton production. Land tenure rights as well as natural disasters, such as floods, especially along the Awash River have also negatively impacted growth in cotton production. The third oft-cited reason for stagnation in the country’s cotton production is the previous restriction from 2010–12 on exporting surplus cotton along with the fact that other crops, like sesame, were more profitable to grow. As a consequence of the export restrictions, farmers planted less cotton, opting for the more profitable sesame or other cash crops. In general factors that constrain the production of cotton is shortage of improved seed varieties, shortage of technical inputs including labour, absence of extension service and limited irrigation practices.

3.3. Cotton marketing trend in Ethiopia

Cotton is a major cash crop. From the 1940s to 1970s, Ethiopia was importing raw cotton to satisfy the domestic demand of its textile factories. Following the establishment of state farms and large-scale private farms in 1970s, the country started exporting cotton. However, due to the drought in the 1980s, the country discontinued the export of cotton. Then, in 1994/95, the country resumed exporting lint cotton (MoARD, Citation2005).

At an extraction rate of 37%, the average yearly domestic production of lint cotton during the period 1996/97-2000/01 was about 29,849.7; of which about 24,861.0 metric tons or nearly 83% was domestically consumed. The respective share of textile mills and handlooms and handcrafts was 86% and 14% of the annual domestic sales of lint cotton, respectively (Mulat, Tewodros, Solomon, Asefa, & Temesgen, Citation2004).

According to data obtained from the Ethiopian Revenue and Customs Authority (ERCA, Citation2016), Ethiopia earned an average of 10.08 million USD in the year 2006/07-2010/11. There were dramatically decline of cotton export from 10.6 million USD in 2009/2010 and 0.5 million USD in 2010/2011. It had faced continuous difficulty in exporting cotton since USA exports cotton with high subsidy. The export declined because Ethiopia banned exports of cotton in 2010 to protect domestic textile firms from high international cotton prices. The ban did not yield its intended result of encouraging textile and apparel manufacturers to use locally produced cotton for at least two reasons. First, some factories faced financial difficulties in purchasing the desired amounts of local cotton.

Second, some factories needed higher grade cotton, which was not available in the local marketplace, and therefore, had to import. After considerable discussion with commercial cotton growers, the government decided to lift its cotton export ban which had been in place since 2013 (Global Agricultural Information Network [GAIN], Annual, Citation2015).

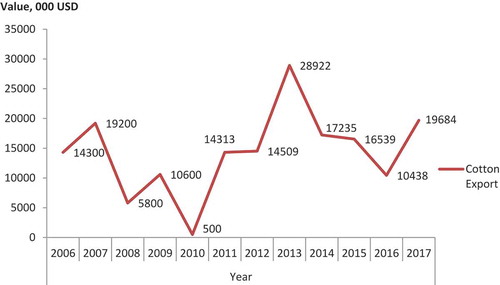

However, after the ban was left at the end of 2012, despite rising local demand for cotton, Ethiopia recently started exporting small volumes of cotton to Indonesia and few EU-member countries. Tight local supplies, small export margins and price/quality competitiveness suggest future exports will remain small. In early 2015, the GOE announced that it was going to resume price controls on cotton in order to minimize the markups charged by middlemen. The price is set by a government committee made up of the MOA, TIDI and MOT. This committee made the price concerning the quality of the product and inflation rate of Ethiopian currency. In 2015, the farm gate price for cotton was 30–38 birr per quintal, while the textile and apparel firms were purchasing it for 50–60 birr per quintal and the average export price of Ethiopian cotton was $1.62/kg (GAIN, Citation2015). Therefore, the prices of cotton were mostly steady with the cotton grade level. As described in the background section in 2018 the average price of export cotton (Figure ) was $1.45 following October 2017/18 devaluation of Ethiopian currency (USDA, Citation2018).

Figure 2. Value of export cotton in 2006–2017.

Source: Alebel et al. (Citation2014) and USDA (Citation2018)

3.4. Economic role of cotton in Ethiopia

Cotton as Industrial input: Cotton crop has direct connections with various agro-processing industries like textile, oil mills and the livestock sub sector. In other words, the crop has a direct linkage with the industrial sector. It is a major industrial input for textile firms. Currently, Ethiopia has about 14 textile factories and 50 medium-to-large garment manufacturers. There is a relatively better FDI flow in the textile and garment sector; especially many Turkish textile firms are relocating to Ethiopia. Hence, the demand for raw cotton and fabric continues to expand as existing textile firms expand and new domestic and FDI firms join the sector. While cotton produced by the state farms and private commercial farms is mainly used in the modern textile manufacturing sector and to some extent exported to foreign countries, cotton produced by peasant farms is for the large part used by the handloom sector (Berihu, Mezgebe, & Alebel, Citation2015). The high-quality cotton yarn produced would be packaged and supplied primarily into Ethiopia’s growing textile industry (80%), with surplus production exported to the global textile and garment manufacturing market (20%) (EIA, Citation2014).

Employment creation: In 2016, about 30 textile companies and brands including the Bonprix or OTTO, Rewe group, Tchibo, Ernsting’s family, Engelbert Strauss, Asos, Besteller, Dibella or AldiSüd put about 50 million cotton made in Africa (CmiA) textiles on the market. More than 695,000 smallholder farmers and their family members included more than 5,7 million people from Cameroon, Ethiopia, Ghana, Ivory Coast, Mozambique as well as Zambia, Zimbabwe, Tanzania and Uganda are currently part of the Cotton made in Africa program (Cotton made in Africa [CmiA], Citation2017).

Similarly, Ethiopian textile and garment sectors are relatively labour-intensive. According to Ethiopian development research institute (EDRI), the cotton sector employs about 52,754 smallholder farmers, 408 mechanized rain-fed farms and 107 mechanized irrigated farms in 2015 (Berihu et al., Citation2015). Additionally, huge temporary employment opportunities are also generated from both private commercial and state farms that are engaged in cotton production.

4. Conclusion and recommendations

4.1. Conclusion

Cotton is an important cash crop to a number of both developed and developing countries. Ethiopia is also one of the African countries that produce and export cotton. It has a long tradition of cotton cultivation. Therefore, the review concluded that though Ethiopia has a huge potential capacity to produce both rain-fed and irrigated cotton it performed weakly. This is due to different production and marketing constraints. These constraints can be derived from physical constraints, lack of technology and agricultural inputs and lack of government support and development services. Hence, erratic weather conditions, difficulty in accessing inputs like fertilizer and improved quality seeds, pest challenges, absence of extension services on irrigation practices, shortage of seasonal labour, lack of credit or financial constraints and rising production costs are identified as production constraints. Similarly, an inefficient marketing system like inadequate knowledge about market standard, lack of market information, absence of a system for contractual production and marketing arrangements, inefficient communication and pricing inefficiencies are identified as marketing constraints.

4.2. Recommendations

Extension service should be improved for the seed sector including the fertilizer provision, pest management and irrigation services.

Additionally, Ethiopian seed sector have to consider the cottonseed quality improvement.

The government should give great emphasis on standardized grading in line with price incentives. In addition, the government must work with business development services and financial institutions to solve financial problems and bureaucratic requirements and to deliver better producing and marketing information.

Ethiopian commodity marketing institutions should work in collaboration to all actors to disseminate market information to all producers and traders throughout the year.

Also, producers must aware themselves that the cotton is a highly demanded product both in the domestic as well as international market and should motivate themselves to solve production and marketing constraints.

Additional information

Funding

Notes on contributors

Habtamu Mossie

Habtamu Mossie was born Deber Elias Woreda, East Gojjam Zone of Amhara Regional State in Semepetebr 1993. He also attended his elementary, secondary and preparatory school education at Deber Elias Secondary and Preparatory High School in East Gojjam zone. After completion of his high school education, he joined Jimma University College of Agriculture and Veterinary Medicine (JUCAVM) in October 2013 and graduated with BSc Degree in Agricultural Economics in June 25/2015. Soon after his graduation, Assistance Lecturer I employed him at Wolkite University. After two year experience the author joined Bahir Dar University College of Agriculture and Environmental since in October 2018 to pursue of his MSc degree in Agricultural Economics in regular program. After the accumulation of my master degree I joined Injibar University College of agriculture, food and climate as Lecturer in department of Agricultural Economics.

References

- Admassie, A., Seid, N., May, J. F., Megquier, S., & Moreland, S. (2015). The demographic dividend: An opportunity for Ethiopia‘s transformation. Washington, DC: Population Reference Bureau and Ethiopian Economics Association.

- Alebel, B., Firew, B., Berihu, A., & Mezgebe, M. (2014). Assessment of the cotton and sugarcane commodities in Ethiopia: The climate change perspective. Addis Ababa, Ethiopia: Ethiopian Development Research Institute (EDRI).

- Annual, E. B. Gain report number nl5028 Annual, E. B. (2015). The hague, The Netherlands: United States Department of Agriculture-Foreign Agriculture Service (USDA-FAS), Global Agricultural Information Network (GAIN).

- Berihu, A., Mezgebe, M., & Alebel, B. (2015). Value chain analyses for a climate resilient production of cotton and sugarcane commodities in Ethiopia. Addis Ababa, Ethiopia: Ethiopian Development Research Institute.

- Bosena, F., Bekabil, G., Berhanu, & Dirk, H. (2011). Factors affecting cotton supply at the farm level in metema district of Ethiopia.

- Cotton made in Africa (CmiA). (2017).Cotton made in Africa; Impacts and scope. Released on 02/2017.

- EIA. (2014). Investment opportunity profile for cotton Production and Ginning in Ethiopia. Addis Ababa, Ethiopia.

- EIA (Ethiopian Investment Agency). (2012). Investment opportunity profile for cotton production and ginning In Ethiopia. Updated Report on Cotton Ginning. Addis Ababa, Ethiopia. doi:10.1094/PDIS-11-11-0999-PDN

- ERCA. (2016). Ethiopian Revenue and Customs Authority.

- Ethiopian Science and Technology Commission (ESTC). (2006). R and D and innovation in the textile sub sector: Training Course on R and Capacity Building in the Industry Sector. June 02, 2006, Bahir Dar, Ethiopia. 77.

- Faostat, F. (2011). Production-crops.

- Goreux, L., 2004. Cotton after cancun: Draft discussion paper to inform debate. March [Online]. Retrieved from http://www.acp-eu-trade.org/pdf

- International cotton advisory committee (ICAC) (2014). Production and Trade Policies Affecting the Cotton Industry. A Report by the Secretariat. Washington, DC: International Cotton Advisory Committee.

- Ministry of Agriculture and Rural Development (MoARD). (2005). Towards increasing benefits from cotton. PP 10-15. Managing Natural Resources Secures from Soil Erosion and Degradation (Amharic Version Publication). Second Year, No.5. October 2005.

- Mulat, D., Tewodros, N., Solomon, D., Asefa, B., & Temesgen, A. (2004, October). Decent work deficits in the Ethiopian cotton sector. Retrieved from http://www.ilo.org/public/english/regional/afpro/addisababa/sro/pub/cottoncasestudy.pdf

- Sneyd, A. (2006). Cotton and poverty in Sub-Saharan Africa: A review of the factors (PhD Qualification Paper). Department of Political Science McMaster University, Hamilton.

- TIDI. (2015). Textile Industry Development Institute (TIDI): Supervises the performance of both the cotton production and textile manufacturing industries.

- USDA. (2010). The Progress of West African Cotton Production and Trade Presented by H.E Tièna COULIBALY. Ambassador of Mali to the USA, unpublished.

- USDA. (2018). USDA Foreign Agriculture Service Global Agricultural Information Network Report on Ethiopian Cotton Production. Addis Ababa, Ethiopia.