Abstract

The objective behind this research is to determine the influence of board size (BSZ), board independence (BID), board diversity (BDV), board meetings (BM), and a number of board committees (NBCM) on organizational performance with the use of innovation as mediating variable in Pakistan textile companies. Innovative culture uses as a moderating variable between innovation and organizational performance. Data were collected from top management and 550 questionnaires distributed among respondents.

Only 407 questionnaires returned back and 384 questionnaires use for final analysis and remaining 23 questionnaires excluded due to missing values. PLS-SEM used for analysis purpose and data collected by using simple random sampling technique. Findings reveal that BSZ and BDV have a positive influence on organizational performance. Despite this, BID, NBCM, and BM have no influence on organizational performance. BSZ, BID, BDV, BM, and NBCM have a significant and positive influence on innovation. Innovation also significantly mediates between independent variables and organizational performance. Innovation has a positive influence on organizational performance. Moreover, innovative culture significantly moderates between innovation and organizational performance. Innovation and innovative culture is an important construct in determining organizational performance. It is beneficial for textile organizations to uses these two constructs in measuring organizational performance through corporate governance.

PUBLIC INTEREST STATEMENT

Corporate governance is an important area for organizations and most of the prior studies focus on secondary data and less attention has been paid on the questionnaire-based study, this study fulfills this gap. This study also uses innovation as a mediating variable that explains the relationship between corporate governance dimensions well with organizational performance because out of five direct relationships with organizational performance three hypotheses show insignificant influence. By using innovation as mediating variable all hypotheses show significant influence with the dependent variable. 384 questionnaires use for analysis and data were collected from the top management of textile companies in Pakistan. This study contributes theoretically and practically that will provide benefits for academicians and textiles companies.

1. Introduction

This study determines the mediating role of innovation between corporate governance and organizational performance. In addition, this study also investigates the moderating role of innovative culture between innovation and organizational performance. Organizational performance is considered the most significant factor for the organizations in measuring their objectives and for gaining success in a competitive market (Rehman, Mohamed, & Ayoup, Citation2018a, Citation2019). Moreover, it is an important indicator for investors, shareholders, stakeholders, and for economic development (Khan & Ali, Citation2017). Organizational performance measured in two dimensions such as financial performance and non-financial performance (Rehman, Mohamed, & Ayoup, Citation2018b; Rehman et al., Citation2019). It depends upon the nature of organizational objectives that which indicator used to measure organizational performance. The literature demonstrates that there are some studies that use both financial and non-financial indicators to compute their performance (Hofmann, Citation2001; Kaplan & Norton, Citation1996). On the other hand, few of the researchers use only financial performance indicator to measure organizational performance (Henri, Citation2006; Kariyawasam, Citation2014) and ignores non-financial performance. However, one of the latest study authors recommends that non-financial performance is essential for organizations if they want to enhance their performance in long-range (Rehman et al., Citation2018a). In this study, we are focusing on both indicators to compute performance.

Corporate governance (CG) system plays a significant role in the betterment of organization wealth. CG refers to a system by which organizations controlled as well as directed. CG takes much attention in the eyes of researchers and organizations after a big scandal in WorldCom and Enron (Ali, Citation2018). In the developing countries, proper governance structure serves as a key objective in the organizational success that decreases the possibility of monetary crises and the management conflicts (Gompers, Ishii, & Metrick, Citation2003). One of the studies elucidated that protect organizations as well as their stakeholders, the authoritarian agencies attempted to discourage the immoral practices by implementing rules and regulations that forbid these immoral practices; and most importantly practice or rule is CG (Rankin, Ferlauto, McGowan, & Stanton, Citation2012). CG structure identifies the sharing of responsibilities and rights within various participants in the organization like an external auditor, the board of directors (BOD’s), management, and shareholders (Mansur & Tangl, Citation2018). In relation to the organizational shareholder’s, CG identifies the shareholder’s rights and give confidence the cooperation between organization and shareholders In relation to management and BOD’s the CG provides the structure through which organizations goals set. In relations to external auditors, organizations that have good CG structure facilitate the work of an auditor, if auditor works with honesty and diligence.

Organizations going to face failure due to weak CG system and there is a need to develop CG structure in the organizations for their betterment (Arora & Sharma, Citation2016). According to Berkman, Zou, and Geng (Citation2009), good CG structure plays a significant role to reduce accounting as compared to weak CG structure. Another study revealed that with weak CG structure organizations faces lots of agency problems and in these organizations managers get more personal advantages (Core, Holthausen, & Larcker, Citation1999). Agency theory elucidated that BOD’s are much careful with their personal property or money as compared to other people funds (Letza, Sun, & Kirkbride, Citation2004). Moreover, this theory further elaborates that the basic objective of CG is to give assurance to organizational shareholders that managers play their role in obtaining results that give benefits to them (Shleifer & Vishny, Citation1997). There is another theory related to this construct like Stewardship theory that assumes a significant association between the achievement of corporation and satisfaction of shareholders. Steward looks after as well as enhance the wealth of shareholders by the organizational performance because by doing this activity utility functions of steward’s enhanced (Arora & Sharma, Citation2016). Significantly, the stakeholder theory recommends that an organization search for in providing a balance between its stakeholders (Abrams, Citation1951). All the theories regarding CG recommends for an effective system of governance that involves the board appointment that consists of the executive as well as non-executive directors.

Literature shows that within the last twenty years researchers paid much attention in determining the association between CG and organizational performance. As much work done on this area in developed economies and less attention has been paid in developing economies (Barnhart, Marr, & Rosenstein, Citation1994; Gompers et al., Citation2003; Judge, Naoumova, & Koutzevol, Citation2003; Pass, Citation2004). Above-mentioned studies determine the influence of CG on organizational performance, findings elucidated that relationship exists between these constructs. In developed countries, the results are different as compared to developing countries even though with the same theory and framework (Arora & Sharma, Citation2016). The relationship between CG and organizational performance is a crucial area and these constructs not conclusive and there is needs to further study (Mardnly, Mouselli, & Abdulraouf, Citation2018). However, CG is more significant factors for less developed markets as compared to developed markets.

This study focus to examine the influence of CG dimensions such as board size (BSZ), board independence (BID), board diversity (BDV), number of board committees (NBCM), and board meetings held in a year (BM) on organizational performance with the mediation role of innovation in the context of Pakistan. Innovative culture uses as a moderating variable between innovation and organizational performance. Figure demonstre the theoretical framework of the current study. Findings of this study help policymakers and they can develop the different governance policies particularly BSZ, BID, BDV, NBCM, and BM. Moreover, policymakers focus on innovative culture and innovation in determining organizational performance. This study majorly contributes that introducing innovation as a mediating effect and innovative culture as a moderating effect that largely ignored in previous studies of corporate governance and organizational performance.

Figure 1. Theoretical Framework.

The current research consists of seven sections that follow; Introduction, background, theory, empirical literature review and hypotheses development, research methodology, empirical results and discussion, and conclusion and future directions.

2. Background

Textile sector of Pakistan is the largest manufacturing sector of Pakistan and considered the backbone of the economy (Ahmad, Hussain, Ahmad, & Islam, Citation2017). Pakistan is the leading exporter and manufacturer of textile products and earns Rs. 1446.86 billion annually from the sale of textile products (Rehman et al., Citation2019). Moreover, this sector contributes 8.5% in the gross domestic product and more than 63% of Pakistan exports comes from the textile sector (Rehman et al., Citation2019). Ataullah, Sajid, and Khan (Citation2014) reveal that the textile sector of Pakistan has below 1% of world market share and researchers recognize that this sector will grow in the future. In Pakistan 954 organizations registered under All Pakistan Textile Mills Association and All Pakistan Bedsheets and Upholstery Manufacturers Association (APBUMA).

Corporate governance and organizational performance is still a debatable area for the believers of agency theory and stewardship theory. Corporate governance was commenced in Pakistan by Security and Exchange Commission of Pakistan (SECP) in the 2002 and researchers conclude that very limited literature contribution in the corporate governance mechanism (Javid & Iqbal, Citation2008). Corporate governance in the context of Pakistan has recently started scratching the surface (Ameer, Citation2013). On the other hand, most of the undocumented economy not in favors of promoting accountability and transparency within organizations (Ameer, Citation2013). Hence, there is still an enormous gap exist in the area to work in the context of Pakistan.

Innovation and innovative culture two different things cover this study. Innovation refers to the firm’s tendency and receptivity to implement ideas that diverge from the common course of business. While, innovative culture means creative, challenging work environment; result oriented and is depicted as being industrial ambitious, risk-taking, and stimulating (Wallach, Citation1983). In Pakistan, less attention has been paid on innovation and innovative culture in determining the organizational performance (Hussain, Hanif, & Hamid, Citation2018). This study covers this gap to focus on textile organizations in Pakistan to determine performance.

3. Theory

Agency theory (Jensen & Meckling, Citation1976) gives an argument that in most cases firms operate their business under conditions with the lack of uncertainty and information. Furthermore, it states that the separation of owners from control communicates that organizations are being controlled by some professionals. Kiel and Nicholson (Citation2003) reveal that professional managers closely work with their personal welfare rather than shareholders interests. Agency theory, presented by (Fama & Jensen, Citation1983) and (Jensen & Meckling, Citation1976), is the core of many explanations for the relationship between corporate governance and organizational performance. Resource dependency theory (RDT) recommends that firms depend on their outside actors in their surroundings for resources essential for organizational growth as well as their survival in the market (Pfeffer, Citation1972). Moreover, the dependency level is restrictive on the level of the resources required and also the number of sources from where organizations get resources (Thompson, Citation1967).

The stewardship theory is also called as stakeholders theory and recommends that management are reliable and not involved in the misappropriate organizations decision making (Shahwan, Citation2015). The stewardship theory assumes a significant relationship between organizations success and shareholder’s satisfaction. Arora and Sharma (Citation2016) argue that steward protects and enhances shareholders wealth by increasing organizational performance, as by performing this stewards utility functions are maximized. Some of the prior studies investigate the relationship between corporate governance and firm performance by using stewardship theory and concludes that corporate governance plays a significant role in determining firm performance

The stewardship theory is majorly related with the managerial behaviors as well as believes that primary inspiration factor for the management is getting satisfied after finishing the job within time and in the effective way (Khan & Abdul Subhan, Citation2019). Hence, the behavior of managers is pro-organizational and in line of mission and objectives of the specific organization (Madison, Holt, Kellermanns, & Ranft, Citation2016). The focus of stewardship theory around intrinsic rewards and motivations (Davis, Schoorman, & Donaldson, Citation1997). Few of the researchers demonstrate that intrinsic motivation is one of the significant sources of innovation and creativity (Amabile, Conti, Coon, Lazenby, & Herron, Citation1996; Tierney, Farmer, & Graen, Citation1999). The literature on stewardship theory reveals that innovation plays a vital role in determining organizational performance (Craig & Dibrell, Citation2006; Goel & de Jong).

4. Literature review and hypotheses development

4.1. Board size (BSZ)

According to O’connell and Cramer (Citation2010) board size defines the strength of both executive and non-executive directors. Agency theory demonstrates that smaller boards within organizations have more managerial controls as compared to larger boards (Jensen & Meckling, Citation1976). Furthermore, Jensen (Citation1993) reveals that smaller board can help organizations to enhance their performance, and also demonstrates that board size more than 7 members creates some issues such as moral hazard problems, inefficient operations, greater control by CEO, and lack of commitment. Researchers elucidated that the reasonable size of the board has much effective to control activities of organizations as compared to a larger board that reduces the performance of an organization (García-Ramos & García-Olalla, Citation2011).

One of the authors concludes that bigger board size decreases organizational performance because of its communications between them that results in late decisions (Guest, Citation2009). Meanwhile, larger board size increases the costs in terms of compensations and not provides effective monitoring that based on the organizational value in the market (Haniffa & Hudaib, Citation2006). Despite this, a larger board size likely to perform the monitoring role within organizations ineffective way because of a number of directors more involved in the decision making and process (Kiel & Nicholson, Citation2003; Ozcan & Ince, Citation2016). Board of directors operates to form different committees based on the board member expertise (Kiel & Blennerhasett, Citation1984). Board size plays a significant role in enhancing innovation (Galia & Zenou, Citation2018). Hence, a large number of boards have a variety of expertise that would help the board to perform their work well and enhance innovation and organizational performance. Hypotheses are proposed on the bases of the above studies.

H1: BSZ has a positive influence on organizational performance

H2: BSZ has a positive influence on innovation

H3: Innovation significantly mediates the relationship between BSZ and organizational performance

4.2. Board independence (BID)

Literature shows that board independence explained by two extensive theories such as stewardship theory and agency theory that elucidated that BID has an impact on organizational performance. Agency theory tells about objective conflicts between the principal (board) and agent (CEO) because of organizations agents’ works for the betterment of their personal benefits rather than work for principal betterment. According to Huse (Citation1994), there should be some independent members of a board that must monitor the performance of the CEO. As agency theory recommends that a large number of independent directors as compared to dependent members in the board enhance the organizational performance. The literature demonstrates that independent directors are beneficial for organizations and also cost associated by having a higher number of independent directors.

A meta-analysis on the topic of BID and organizational performance reveals that there are inconsistent results between these constructs (Dalton, Daily, Ellstrand, & Johnson, Citation1998). Some studies show that board independence increase organizational performance (Baysinger & Butler, Citation1985; Daily & Dalton, Citation1993). Despite this, there are some studies reveal that board independence decreases organizational performance (Bhagat & Bolton, Citation2008; Klein, Shapiro, & Young, Citation2005; Muth & Donaldson, Citation1998). While, there are some studies that elucidated that BID has no impact on organizational performance (Hermalin & Weisbach, Citation1991; Villalonga & Amit, Citation2006). Board independence also plays a significant role in innovation (Balsmeier, Fleming, & Manso, Citation2017). Hypotheses are proposed on the bases of the above studies.

H4: BID has a positive influence on organizational performance

H5: BID has a positive influence on innovation

H6: Innovation significantly mediates between the BID and organizational performance

4.3. Board diversity (BDV)

RDT and human capital theory (HCT) explained the association between BDV and organizational performance. The main character of BOD’s is to monitor and control organizations managers as well as provide resources. RDT recommends that organizations depend upon their surroundings (Pfeffer, Citation1972). Organizations have to protect their resources from the surroundings and this reduces the uncertainty as well as improves organizational performance (Taljaard, Ward, & Muller, Citation2015). Moreover, BDV formed by assorted board capital and supports the capability to protect resources from the surroundings that minimize uncertainty and enhance organizational performance (Hillman & Dalziel, Citation2003; Pfeffer, Citation1972). Assorted BOD’s is much superior to secure the resources as compared to less diverse BOD’s because the board has more access to both networks and information regarding organizational activities (Bryant & Davis, Citation2012; Taljaard et al., Citation2015). HCT tells that the skills and knowledge of BOD’s impact on the effectiveness of the implementation of resource provision and monitoring roles (Hillman & Dalziel, Citation2003). Skills and knowledge of BOD’s also known as the human capital of board members.

According to Fagan, Menéndez, and Ansón (Citation2012), decision making should be improved because of new and unique knowledge. The compatibility of HCT and RDT theory is on the assumptions that the diversity of board enhances organizational performance. HCT and RDT argue that inimitable human capital offers the BDV. Literature shows that board diversity increases organizational performance (Carter, Simkins, & Simpson, Citation2003; Kim, Pantzalis, & Park, Citation2013). Despite this, there are some studies that reveal that board diversity decreases organizational performance (Arena et al., Citation2015; Smith et al., Citation1994). As recommended by Miller and Del Carmen Triana (Citation2009), board diversity has a significant and positive influence on innovation. Hypotheses are proposed on the bases of the above studies.

H7: BDV has a positive influence on organizational performance

H8: BDV has a positive influence on innovation

H9: Innovation significantly mediates between BDV and organizational performance

4.4. Board meetings held in a year (BM)

Vafeas (Citation1999), was the first person that argues that a number of board meetings play an important role in enhancing organizational performance. Similarly, one of the authors recommends that board meetings frequency will possibly improve the performance of an organization since board meetings consider a measure of supervision efficacy and after that influence on overall organization outcomes (Lipton & Lorsch, Citation1992). The literature demonstrates that board activity has a significant influence on organizational performance (Brick & Chidambaran, Citation2010; Kaur & Vu, Citation2017). One of the recent studies reveals that board meetings play a significant role in examining innovation (Asensio López, Cabeza García, & González Álvarez, Citation2018). Hypotheses are proposed on the bases of the above studies.

H10: BM has a positive influence on organizational performance

H11: BM has a positive influence on innovation

H12: Innovation significantly mediates between the number of BM and organizational performance

4.5. Number of boards committees (NBCM)

BOD’s in usually regarded as the essential control mechanism that observes the decision-making activities (Lam & Lee, Citation2012). Moreover, board monitoring character can be enhanced to establish a board committee that enables the BOD’s responsibilities to be “‘rigorously discharged’”(Higgs, Citation2003). Additionally, the role of this board committee should be more efficient when this committee consists of non-executive directors and most of them should be independent (Lam & Lee, Citation2012). Board committees enhance the organizational performance but there are less empirical studies available on this relationship (McMullen, Citation1996). There are three types of board committees like nomination, audit, and remuneration committee (Anand, Citation2007). Literature shows that board committees have an influence on organizational performance but most of the studies conducted in developed economies and less work in developing economies (Puni, Citation2015). There are some studies that recommend that board committees linked with organizational performance (Carter, D’Souza, Simkins, & Simpson, Citation2010). Independent board committees play a significant character in innovation (Balsmeier et al., Citation2017). Hypotheses are proposed on the bases of the above studies.

H13: NBCM has a positive influence on organizational performance

H14: NBCM has a positive influence on innovation

H15: Innovation significantly mediates between NBCM and organizational performance

4.6. Innovation, innovative culture, and organizational performance

According to Menguc and Auh (Citation2006), innovation (INV) means the organization tendency as well as receptivity to implementing ideas that diverge from the common course of business. Innovation entails compliance to relinquish previous habits and try untried ideas (Tsai & Yang, Citation2014). INV plays an important character in determining organizational performance (Uzkurt, Kumar, Semih Kimzan, & Eminoğlu, Citation2013; Zaefarian, Forkmann, Mitręga, & Henneberg, Citation2017). Prior studies reveal that INV has a major impact on organizational performance (Naala, Nordin, & Omar, Citation2017; Turulja & Bajgoric, Citation2018). Despite this, the literature reveals that INV has insignificant influence on organizational performance (Darroch, Citation2005). There are inconclusive results between INV and organizational performance and there a need for another variable that moderates the relationship between these constructs. Innovative culture refers to a creative, challenging work environment; result oriented and is depicted as being industrial ambitious, risk-taking, and stimulating (Wallach, Citation1983). This study used innovative culture as a moderating variable that covers that organization culture is challenging, creative, enterprising, stimulating, driving, risk-taking, result oriented, and pressurize. Innovative culture plays an important role in examining organizational performance (Quy, Citation2017). Hypotheses are proposed on the bases of the above studies.

H16: INV has a positive influence on organizational performance

H17: Innovative culture moderate between INV and organizational performance

5. Research methodology

The research methodology is a significant part of research to determine the objectives of that research (Rehman et al., Citation2019). In achieving this, the appropriate analysis technique used to see the problem and objective of that specific research (Rehman et al., Citation2019). Hence, in this research, to see the nature, problem, and research objectives we employed a quantitative approach, the cross-sectional design used in collecting data from respondents by using questionnaire technique. This study is deductive in nature as a theoretical framework developed on the basis of existing theory.

5.1. Data collection procedure

In the current study, data were collected by using questionnaire technique and instruments were adapted from previous studies on BSZ, BID, BDV, NBCM, BM, INV, innovative culture, and organizational performance. Questionnaires were distributed to top management in textile companies under all Pakistan textile mills association (APTMA) and All Pakistan Bedsheets and Upholstery Manufacturers Association (APBUMA). Questionnaires send through postal as well as personally administered questionnaires.

5.2. Questionnaire development

Model of this research consists of eight variables. Each variable measured to use various items. Questionnaire of current research consists of two major portions. The first portion is regarding demographics characteristics consist of five questions. The second portion is regarding BSZ, BID, BDV, NBCM, BM, INV, innovative culture, and organizational performance consist of fifty-five items. Extensively, each item measured by using five-Likert scale (5 for strongly agree, and 1 for strongly disagree). This study used five-Likert scales because of some reasons such as it reduces the frustration or irritation level of respondents that ultimately enhances the quality of response and also enhance the response rate (Sachdev & Verma, Citation2004). Corporate governance five elements like board size (5 items), board independence (3 items), board diversity (6 items), number of board committees (5 items), board meetings held in a year (4 items) adapted from (Honghui, Citation2017). Innovation consists of 11 items and adapted from (Darroch & Jardine, Citation2002). Innovative culture consists of 8 items and adapted from (Wallach, Citation1983). The organizational performance consists of 11 items and adapted from (Henri, Citation2006; Teeratansirikool, Siengthai, Badir, & Charoenngam, Citation2013). After adapted the instruments, send to three field experts and three Ph.D. They confirm that questionnaire fulfills the face validity. Questionnaire attached in Appendix end of this paper.

5.3. Population, sampling, and sample size

Current research is based on 954 textile companies under APTMA and APBUMA in Pakistan and questionnaires distributed among 550 companies. Simple random sampling use to collect data from respondents as the technique is the most appropriate sampling technique in known population. The reason to use simple random sampling is that we know the whole population of textile companies that registered under APTMA and APBUMA in Pakistan. Some of the prior studies used this technique and get better results (Bhatt & Bhatt, Citation2017; Bhatti, Citation2018; Mudashiru, Bakare, Ishmael, & Babatunbe, Citation2014; Rehman et al., Citation2019). According to Comrey and Lee (Citation1992) there are various ranges of the sample size regarding the strength like sample size lower than 50 is considered weaker sample size, more than 50 and equals to 100 is considered weak sample, between 101 to 200 respondents is considered adequate sample size, sample size between 201 to 300 is considered a good sample size, sample size 500 is considered a very good sample size, and the sample size 1000 is considered excellent. However, this study used 550 sample sizes that are considered very good sample size. Questionnaires were distributed to top management in textile companies under APTMA and APBUMA in Pakistan. In this study, total 550 questionnaires distributed among top management, out of 550 questionnaires, only 407 questionnaires returned back, 23 questionnaires have missing values and these questionnaires not included in the analysis. Hence, 384 questionnaires were used for analysis purpose and it meets the sample selection criteria mentioned above. The response rate of this study is 69.81% that is less than a study that conducted in textile industries in Pakistan under APTMA only and that study has response rate 79.50% (Rehman et al., Citation2019).

5.4. Respondents profile

Respondents for this study were the top management of textile companies. The total number of questionnaires distributed among respondents was 550 and 384 used for analysis purpose that is 69.81% response rate. Table represents the organization profile of the respondents. Table show that 67.44% of the respondents have a master’s degree. Majority of the respondents are from the accounting and finance field that equals to 66.92% of total respondents. Regarding the experience of respondents, 76.03% of the respondents have experience at most 10 years. Regarding a number of employees, 48.70% of the organizations have employees within 401–650. Average annual revenue of 46.35% organizations is within 151 to 250 million Pakistani rupees.

Table 1. Respondents profile

5.5. Data analysis

In the current study, we used SmartPLS 3.2.8 to determine the study model because this is a fast-growing 2nd generation technique as suggested (Hair, Hult, Ringle, & Sarstedt, Citation2014). There are various reasons to choose partial least squares structural equation modeling (PLS-SEM) as compared to covariance-based structural equation modelings (CB-SEM) such as no need for normality assumption and Multicollinearity. Moreover, PLS-SEM is most appropriate analysis tool for simple as well as complex models. In the current study, our model is complex because we use both mediation and moderation. According to Hair, Hult, Ringle, and Sarstedt (Citation2017), finding considerable values of path coefficient as well as factor loadings, a bootstrapping of 5000 subsamples required. Two models such as measurement and structural model calculated in PLS-SEM.

5.6. Measurement model

To calculate measurement there is a need to compute convergent and Discriminant validity.

5.7. Convergent validity

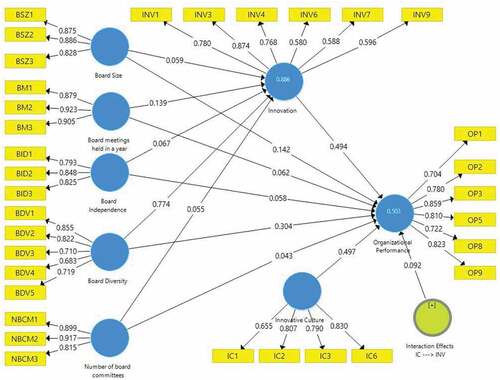

Zhou (Citation2013), convergent validity refers to a situation where items of specific variable reflect effectively to their linked indicator. According to Hair, Hult, Ringle, and Sarstedt (Citation2013), convergent validity requires three things like factor loadings, composite reliability (CR), and the last one is average variance extracted (AVE). Hair et al. (Citation2013), suggests that AVE and factor loadings value must be higher than 0.50 and CR value higher than 0.70. All the items that have a factor loading less than 0.50 must be deleted to an obtained better outcome of CR and AVE as suggested (Hayduk & Littvay, Citation2012). Nunnally (Citation1978), Cronbach’s alpha value should be more than 0.60. Figure demonstrates the measurement model. Table demonstrates that this study fulfill convergent validity criterion.

Figure 2. Measurement model.

5.8. Discriminant validity

Discriminant validity means the level to which all items make a distinction amongst constructs (Rehman et al., Citation2019). Discriminant validity computed by using two methods such as comparing AVE with squared correlation or comparing AVE square root with correlation. In the current research, the second method used to compute Discriminant validity as shown in Table . Diagonal upper values should be greater than other variables values in the same columns and rows as suggested (Fornell & Larcker, Citation1981).

Table 2. Factor loadings, Average Variance Extracted (AVE), and Composite Reliability (CR)

Table 3. Discriminant validity

5.8.1. Structural model and hypotheses testing

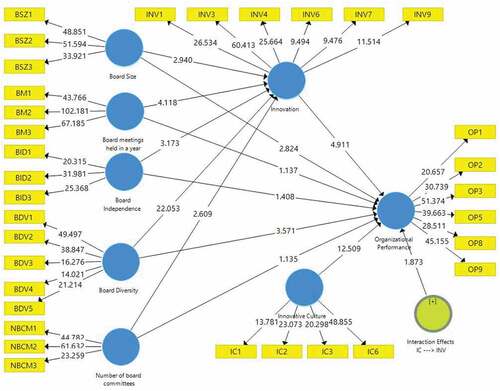

In the above part, we computed Discriminant validity and convergent validity to fulfill the requirement of measurement or outer model. In this section, examines the study proposed hypotheses by running algorithms technique and bootstrapping technique in SmartPLS 3.2.8. According to Hair et al. (Citation2017), finding considerable values of path coefficient as well as factor loadings, a bootstrapping of 5000 subsamples required. In the current research, we follow 5000 subsamples criteria. Figure and Table demonstrates that we have 17 hypotheses consist of 11 direct hypothesis, 5 mediating hypotheses, and 1 moderating hypothesis.

Table 4. Direct relationships

Figure 3. Structural model.

BSZ = Board size; BM = Board meetings held in a year; BID = Board independence; BDV = Board diversity; NBCM = Number of board committees; INV = Innovation; IC = Innovative culture; OP = Organizational performance

5.9. The predictive relevant of study model

In calculating predictive relevance of model there is a need for two things such as R-square (R2) and cross-validated redundancy (Q2). R2 refers to the variance of the dependent variable that all independent variables explained. Table demonstrates that 88.6% innovation explained by BSZ, BID, BDV, NBCM, and BM. While, 50.3% organizational performance explained due to BSZ, BID, BDV, NBCM, and BM, innovation, and innovative culture. According to Cohen (Citation1988), R2 considers weak (0.02 to 0.13), considers moderate (0.13 to 0.26), and considers substantial in case R2 higher than 0.26. In the current research, INV and OP consider substantial. Q2 computed to know the quality of the model in SmartPLS to use blindfolding technique. The value of Q2 must be greater than zero as recommended (Chin, Citation1998). However, the current research fulfills this criterion as Q2 of INV 0.412 and OP 0.273 as demonstrates in Table .

Table 5. The Predictive relevance of study model

6. Empirical results and discussion

The objective of the current study is to determine the mediating effect of INV between corporate governance (BSZ, BID, BDV, BM, and NBCM) and OP in Pakistan textile industry. Furthermore, determines the moderating effect of IC between INV and OP. Table shows BSZ has a positive influence on OP (β = 0.142, t = 2.824, p < 0.05) and accepted H1. The findings are consistent with the findings of (Ozcan & Ince, Citation2016). BSZ has a positive influence on INV (β = 0.059, t = 2.940, p < 0.05) and supported H2. The findings are similar to a prior study (Galia & Zenou, Citation2018). Furthermore, INV significantly and positively mediates the relationship between BSZ and OP (β = 0.029, t = 2.261, p < 0.05) and accepted H3. The results are in line with resource dependency theory that large BSZ, directly and indirectly, enhances OP (Pfeffer, Citation1972).

BID has no influence on OP (β = 0.058, t = 1.408, p > 0.05) and H4 not supported. BID has no influence on OP and consistent with (Villalonga & Amit, Citation2006). BID has a positive influence on INV (β = 0.067, t = 3.173, p < 0.05) and accept H5. BID has a significant and positive influence on INV and findings are similar with (Balsmeier et al., Citation2017). INV significantly and positively mediates the relationship between the BID and OP (β = 0.033, t = 2.600, p < 0.05) and H6 accepted. BID has no direct influence on OP but INV significantly explains the relationship between BID and OP and agency theory supports. BDV has a positive influence on OP (β = 0.304, t = 3.5714, p < 0.05) and supported H7. The outcomes are consistent with (Kim et al., Citation2013). The findings are in line with resource dependency theory and stewardship theory that BDV improves OP. BDV has a positive influence on INV (β = 0.774, t = 22.053, p < 0.05) and accept H8. The findings are consistent with (Miller & Del Carmen Triana, Citation2009). INV significantly and positively mediates between BDV and OP (β = 0.383, t = 4.822, p < 0.05) and accepted H9.

BM has no influence on OP (β = 0.062, t = 1.137, p > 0.05) and not supported H10. The results of this study consistent with (Makhlouf, Ali, & Ramli, Citation2017). BM has a positive influence on INV (β = 0.139, t = 4.118, p < 0.05) and supported H11. The results are in line with (Asensio López et al., Citation2018). INV significantly and positively mediates between BM and OP (β = 0.069, t = 3.092, p < 0.05) and accepted H12. The indirect results are in line with agency theory that BM significantly improves OP. NBCM has no influence on OP (β = 0.043, t = 1.135, p > 0.05) and not supported H13. The findings are similar finding with (Puni, Citation2015). NBCM has a positive influence on INV (β = 0.055, t = 2.609, p < 0.05) and accepted H14. The results are consistent with (Balsmeier et al., Citation2017). INV significantly and positive mediates between NBCM and OP (β = 0.027, t = 2.380, p < 0.05) and accepted H15. The indirect results are in line with agency theory that NBCM significantly influences OP. INV has a highly significant and positive influence on OP (β = 0.494, t = 5.022, p < 0.05) and supported H16. The results are in line with some prior studies (Uzkurt et al., Citation2013; Zaefarian et al., Citation2017). IC moderate the relationship between INV and OP (β = 0.092, t = 1.873, p < 0.05) and accepted H17. The results are similar to the stewardship theory that INV and IC play a significant role in enhancing OP.

7. Summary and conclusion

The study found that only two factors of corporate governance such as BSZ and BD have a significant positive influence on OP. Moreover, all five factors of corporate governance used in this study have a significant and positive influence on organizational performance. INV significantly mediate the relationship between BSZ, BID, BDV, BM, NBCM, and OP. moreover, IC significantly moderate the relationship between INV and OP. Hence, this study concludes that textile companies enhance organizational performance by focusing these five elements of corporate governance, innovation, and innovative culture.

The current research made some fabulous theoretical contributions by focusing on innovation and innovative culture as mediating and moderating variable with corporate governance elements and organizational performance. Most of the previous studies on corporate governance are based on secondary data and less attention has been paid on the questionnaire-based study. Furthermore, the current study incorporates BSZ, BID, BDV, BM, NBCM, IC, INV, and OP in a single study as ignored in previous literature corporate governance with innovative culture and innovation. In practical term, the findings of this study give various fabulous benefits in a practical sense to textile companies. This study elucidated that INV and IC plays a significant role in determining OP. Hence, textile companies can focus these two constructs with corporate governance and OP because BID, BM, and NBCM have no direct influence on OP but with the inclusion of INV, this insignificant relationship converted into a significant and positive term. This study suggests that corporate governance elements can increase OP only with the use of the third variable between these constructs that is INV. IC also plays a significant role in determining OP as suggested (Quy, Citation2017).

7.1. Limitations and suggestions

This study focuses on Pakistan textile companies and provides a significant contribution to the literature but the results of the current study cannot be generalized in the whole world. Hence, there is a need to explore further current study model in the manufacturing sector in Pakistan as well as in other countries. In addition, there is a need to study corporate governance with a performance by using some mediating variables such as organizational culture and organizational capabilities. Moreover, in future management controls systems and corporate governance both use an independent variable to measure organizational performance.

Additional information

Funding

Notes on contributors

Sajjad Nawaz Khan

Sajjad Nawaz Khan completed his Ph.D. in Accounting from Universiti Utara Malaysia. His research interest includes corporate [email protected]

Rai Imtiaz Hussain

Rai Imtiaz Hussain is working as a lecturer in University of [email protected]

Shafique -Ur-Rehman

Shafique-Ur-Rehman is doing a Ph.D. in Accounting from Universiti Utara Malaysia. His research interest includes a management control system, capabilities, corporate [email protected]

Muhammad Qasim Maqbool

Muhammad Qasim Maqbool is doing Ph.D. from Universiti Utara Malaysia. His research interest includes leadership, TQM, HR practices. [email protected]

Engku Ismail Engku Ali

Engku Ismail Engku ALI School of Accountancy (SOA), College of Business (COB), University Utara Malaysia (UUM), Sintok 06010 Kedah [email protected]

Muhammad Numan

Muhammad Noman [email protected], Ph.D. Scholar, (UUM)

Related Research Data

References

- Abrams, F. W. (1951). Management’s responsibilities in a complex world. Harvard Business Review, 29(3), 29–23.

- Ahmad, A., Hussain, A., Ahmad, Q. W., & Islam, B. U. (2017). Causes of workplace stress in the textile industry of developing countries: A case study from Pakistan. In Advances in social & occupational ergonomics (pp. 283–294). Springer.

- Ali, M. (2018). Impact of corporate governance on firm’s financial performance (A comparative study of developed and non developed markets). Economic Research, 2(1), 15–30.

- Amabile, T. M., Conti, R., Coon, H., Lazenby, J., & Herron, M. (1996). Assessing the work environment for creativity. Academy of Management Journal, 39(5), 1154-1184.

- Ameer, B. (2013). Corporate governance-issues and challenges in Pakistan. International Journal of Academic Research in Business and Social Sciences, 3(4), 79.

- Anand, S. (2007). Essentials of corporate governance (Vol. 36). John Wiley & Sons.

- Arena, C., Cirillo, A., Mussolino, D., Pulcinelli, I., Saggese, S., & Sarto, F. (2015). Women on board: Evidence from a masculine industry. Corporate Governance, 15(3), 339–356. doi:10.1108/CG-02-2014-0015

- Arora, A., & Sharma, C. (2016). Corporate governance and firm performance in developing countries: Evidence from India. Corporate Governance, 16(2), 420–436. doi:10.1108/CG-01-2016-0018

- Asensio López, D., Cabeza García, L., & González Álvarez, N. (2018). Corporate governance and innovation: A theoretical review. European Journal of Management and Business Economics. doi:10.1108/EJMBE-05-2018-0056

- Ataullah, M, Sajid, A, & Khan, M. (2014). Quality related issues and their effects on returns of Pakistan textile industry. Journal of Quality and Technology Managment, 10(I), 69-91.

- Balsmeier, B., Fleming, L., & Manso, G. (2017). Independent boards and innovation. Journal of Financial Economics, 123(3), 536–557. doi:10.1016/j.jfineco.2016.12.005

- Barnhart, S. W., Marr, M. W., & Rosenstein, S. (1994). Firm performance and board composition: Some new evidence. Managerial and Decision Economics, 15(4), 329–340. doi:10.1002/mde.v15:4

- Baysinger, B. D., & Butler, H. N. (1985). Corporate governance and the board of directors: Performance effects of changes in board composition. Journal of Law, Economics, & Organization, 1(1), 101–124.

- Berkman, H., Zou, L., & Geng, S. (2009). Corporate governance, profit manipulation and stock return. Journal of International Business and Economics, 9(2), 132–145.

- Bhagat, S., & Bolton, B. (2008). Corporate governance and firm performance. Journal of Corporate Finance, 14(3), 257–273. doi:10.1016/j.jcorpfin.2008.03.006

- Bhatt, P. R., & Bhatt, R. R. (2017). Corporate governance and firm performance in Malaysia. Corporate Governance: the International Journal of Business in Society, 17(5), 896–912. doi:10.1108/CG-03-2016-0054

- Bhatti, A. (2018). Factors effecting consumer purchase intention with the mediating role of corporate social responsibility in Pakistan. International Journal of Academic Management Science Research (IJAMSR), 2(8), 30-37.

- Brick, I. E., & Chidambaran, N. (2010). Board meetings, committee structure, and firm value. Journal of Corporate Finance, 16(4), 533–553. doi:10.1016/j.jcorpfin.2010.06.003

- Bryant, P., & Davis, C. (2012). Regulated change effects on boards of directors: A look at agency theory and resource dependency theory. Academy of Strategic Management Journal, 11(2), 1.

- Carter, D. A., D’Souza, F., Simkins, B. J., & Simpson, W. G. (2010). The gender and ethnic diversity of US boards and board committees and firm financial performance. Corporate Governance: An International Review, 18(5), 396–414. doi:10.1111/j.1467-8683.2010.00809.x

- Carter, D. A., Simkins, B. J., & Simpson, W. G. (2003). Corporate governance, board diversity, and firm value. Financial Review, 38(1), 33–53. doi:10.1111/fire.2003.38.issue-1

- Chin, W. W. (1998). Commentary: Issues and opinion on structural equation modeling. MIS Quarterly, 22(1).

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences. 2nd: Hillsdale, NJ: erlbaum.

- Comrey, A. L., & Lee, H. B. (1992). A first course in factor analysis (2nd Ed.). Hillsdale: Lawrence Erlbaum Associates.

- Core, J. E., Holthausen, R. W., & Larcker, D. F. (1999). Corporate governance, chief executive officer compensation, and firm performance1. Journal of Financial Economics, 51(3), 371–406. doi:10.1016/S0304-405X(98)00058-0

- Craig, J, & Dibrell, C. (2006). The natural environment, innovation, and firm performance: A comparative study. Family Business Review, 19(4), 275-288.

- Daily, C. M., & Dalton, D. R. (1993). Board of directors leadership and structure: Control and performance implications. Entrepreneurship Theory and Practice, 17(3), 65–81. doi:10.1177/104225879301700305

- Dalton, D. R., Daily, C. M., Ellstrand, A. E., & Johnson, J. L. (1998). Meta‐analytic reviews of board composition, leadership structure, and financial performance. Strategic Management Journal, 19(3), 269–290. doi:10.1002/(ISSN)1097-0266

- Darroch, J. (2005). Knowledge management, innovation and firm performance. Journal of Knowledge Management, 9(3), 101–115.

- Darroch, J., & Jardine, A. (2002). Combining firm-based and consumer-based perspectives to develop a new measure for innovation. Zhejiang: Zhejiang University Press.

- Davis, J. H, Schoorman, F. D, & Donaldson, L. (1997). Toward a stewardship theory of management. Academy of Management Review, 22(1), 20-47.

- Fagan, C., Menéndez, M. G., & Ansón, S. G. (2012). Women on corporate boards and in top management: European trends and policy (M. G. Menèndez & S. G. Ansón, Eds. illustrated ed.). UK: Palgrave Macmillan.

- Fama, E. F, & Jensen, M. C. (1983). Separation of ownership and control. The Journal Of Law and Economics, 26(2), 301-325.

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 39–50. doi:10.1177/002224378101800104

- Galia, F., & Zenou, E. (2018). Board composition and forms of innovation, does diversity make a difference? European Journal of International Management Decision, 6(6), 630–650.

- García-Ramos, R., & García-Olalla, M. (2011). Board characteristics and firm performance in public founder-and nonfounder-led family businesses. Journal of Family Business Strategy, 2(4), 220–231. doi:10.1016/j.jfbs.2011.09.001

- Gompers, P., Ishii, J., & Metrick, A. (2003). Corporate governance and equity prices. The Quarterly Journal of Economics, 118(1), 107–156. doi:10.1162/00335530360535162

- Guest, P. M. (2009). The impact of board size on firm performance: Evidence from the UK. The European Journal of Finance, 15(4), 385–404. doi:10.1080/13518470802466121

- Hair, J. F., Jr, Hult, G. T. M., Ringle, C., & Sarstedt, M. (2013). A primer on partial least squares structural equation modeling (PLS-SEM). Thousand Oaks, CA: Sage Publications.

- Hair, J. F., Jr, Hult, G. T. M., Ringle, C., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS-SEM). Thousand Oaks: Sage Publications.

- Hair, J. F., Jr, Hult, G. T. M., Ringle, C., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling (PLS-SEM) (2nd edition ed.). Thousand Oaks: Sage Publications.

- Haniffa, R., & Hudaib, M. (2006). Corporate governance structure and performance of Malaysian listed companies. Journal of Business Finance & Accounting, 33(7‐8), 1034–1062.

- Hayduk, L. A., & Littvay, L. (2012). Should researchers use single indicators, best indicators, or multiple indicators in structural equation models? BMC Medical Research Methodology, 12(1), 159. doi:10.1186/1471-2288-12-159

- Henri, J.-F. (2006). Management control systems and strategy: A resource-based perspective. Accounting, Organizations and Society, 31(6), 529–558. doi:10.1016/j.aos.2005.07.001

- Hermalin, B. E., & Weisbach, M. S. (1991). The effects of board composition and direct incentives on firm performance. Financial Management, 101–112. doi:10.2307/3665716

- Higgs, D. (2003). Review of the role and effectiveness of non-executive directors. London: Stationery Office.

- Hillman, A. J., & Dalziel, T. (2003). Boards of directors and firm performance: Integrating agency and resource dependence perspectives. Academy of Management Review, 28(3), 383–396. doi:10.5465/amr.2003.10196729

- Hofmann, C. (2001). Balancing financial and non-financial performance measures (pp. 30167). Koenigsworther Platz, 1: University of Hannover.

- Honghui, L. (2017). The effect of corporate governance on performance of firms listed on the Nairobi securities exchange. Nairobi: School of business, University of Nairobi.

- Huse, M. (1994). Board-management relations in small firms: The paradox of simultaneous independence and interdependence. Small Business Economics, 6(1), 55–72. doi:10.1007/BF01066112

- Hussain, G, Hanif, M. I, & Hamid, A. B. A. (2018). The effect of organizational innovation and organizational culture on the market performance of SMES in Pakistan. International Journal of Research and Innovation in Social Science (IJRISS), 2(5).

- Javid, A. Y, & Iqbal, R. (2008). Ownership concentration, corporate governance and firm performance: Evidence from Pakistan. The Pakistan Development Review, 47(4–II), 643-659.

- Jensen, M. C. (1993). The modern industrial revolution, exit, and the failure of internal control systems. The Journal of Finance, 48(3), 831–880. doi:10.1111/j.1540-6261.1993.tb04022.x

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. doi:10.1016/0304-405X(76)90026-X

- Judge, W. Q., Naoumova, I., & Koutzevol, N. (2003). Corporate governance and firm performance in Russia: An empirical study. Journal of World Business, 38(4), 385–396. doi:10.1016/j.jwb.2003.08.023

- Kaplan, R., & Norton, D. P. (1996). Using the balanced scorecard as a strategic management system. Harvard Business Review, 74 (January–February), 75–85.

- Kariyawasam, A. (2014). Impact of management control systems on the return on sales of manufacturing companies in Sri Lanka. Journal of Business and Retail Management Research, 8(2), 110-118.

- Kaur, M., & Vu, M. (2017). Board characteristics and firm performance: Evidence from banking industry in India. Asian Journal of Accounting and Governance, 8, 39–53. doi:10.17576/AJAG-2017-08-04

- Khan, A. W., & Abdul Subhan, Q. (2019). Impact of board diversity and audit on firm performance. Cogent Business & Management.

- Khan, S. N., & Ali, E. I. E. (2017). The moderating role of intellectual capital between enterprise risk management and firm performance: A conceptual review. American Journal of Social Sciences and Humanities, 2(1), 9–15.

- Kiel, G. C., & Blennerhasett, P. (1984). The board of directors in large Australian companies. Management Decision, 22(1), 40–44. doi:10.1108/eb001338

- Kiel, G. C., & Nicholson, G. J. (2003). Board composition and corporate performance: How the Australian experience informs contrasting theories of corporate governance. Corporate Governance: An International Review, 11(3), 189–205.

- Kim, I., Pantzalis, C., & Park, J. C. (2013). Corporate boards’ political ideology diversity and firm performance. Journal of Empirical Finance, 21, 223–240.

- Klein, P., Shapiro, D., & Young, J. (2005). Corporate governance, family ownership and firm value: The Canadian evidence. Corporate Governance: An International Review, 13(6), 769–784.

- Lam, T.-Y., & Lee, S.-K. (2012). Family ownership, board committees and firm performance: Evidence from Hong Kong. Corporate Governance: the International Journal of Business in Society, 12(3), 353–366. doi:10.1108/14720701211234609

- Letza, S., Sun, X., & Kirkbride, J. (2004). Shareholding versus stakeholding: A critical review of corporate governance. Corporate Governance: An International Review, 12(3), 242–262.

- Lipton, M., & Lorsch, J. W. (1992). A modest proposal for improved corporate governance. The Business Lawyer, 48(1), 59–77.

- Madison, K, Holt, D. T, Kellermanns, F. W, & Ranft, A. L. (2016). Viewing family firm behavior and governance through the lens of agency and stewardship theories. Family Business Review, 29(1), 65-93.

- Makhlouf, M. H., Ali, N. H. L. M. Y., & Ramli, B. N. A. (2017). Board of directors’ effectiveness and firm performance: Evidence from Jordan. Research Journal of Finance and Accounting, 8(18), 23–34.

- Mansur, H., & Tangl, A. (2018). The effect of corporate governance on the financial performance of listed companies in Amman stock exchange (Jordan). Journal of Advanced Management Science Vol, 6(2), 97–102.

- Mardnly, Z., Mouselli, S., & Abdulraouf, R. (2018). Corporate governance and firm performance: An empirical evidence from Syria. International Journal of Islamic and Middle Eastern Finance and Management. doi:10.1108/IMEFM-05-2017-0107

- McMullen, D. A. (1996). Audit committee performance: An investigation of the consequences associated with audit committees. Auditing, 15(1), 87.

- Menguc, B., & Auh, S. (2006). Creating a firm-level dynamic capability through capitalizing on market orientation and innovativeness. Journal of the Academy of Marketing Science, 34(1), 63–73.

- Miller, T., & del Carmen Triana, M. (2009). Demographic diversity in the boardroom: Mediators of the board diversity–Firm performance relationship. Journal of Management Studies, 46(5), 755–786. doi:10.1111/joms.2009.46.issue-5

- Mudashiru, A., Bakare, A., Ishmael, Y., & Babatunbe, Y. (2014). Good corporate governance and organisational performance: An empirical analysis. International Journal of Humanities and Social Science, 4(7), 1.

- Muth, M., & Donaldson, L. (1998). Stewardship theory and board structure: A contingency approach. Corporate Governance: An International Review, 6(1), 5–28. doi:10.1111/corg.1998.6.issue-1

- Naala, M., Nordin, N., & Omar, W. (2017). Innovation capability and firm performance relationship: A study of pls-structural equation modeling (Pls-Sem). International Journal of Organization & Business Excellence, 2(1), 39–50.

- Nunnally, J. C. (1978). Psychometric theory (Vol. 226). New York: McGraw-Hill.

- O’connell, V., & Cramer, N. (2010). The relationship between firm performance and board characteristics in Ireland. European Management Journal, 28(5), 387–399. doi:10.1016/j.emj.2009.11.002

- Ozcan, I., & Ince, A. R. (2016). Board size, board composition and performance: An investigation on Turkish banks. International Business Research, 9(2), 74. doi:10.5539/ibr.v9n2p74

- Pass, C. (2004). Corporate governance and the role of non-executive directors in large UK companies: An empirical study. Corporate Governance: the International Journal of Business in Society, 4(2), 52–63. doi:10.1108/14720700410534976

- Pfeffer, J. (1972). Size and composition of corporate boards of directors: The organization and its environment. Administrative Science Quarterly, 218–228. doi:10.2307/2393956

- Puni, A. (2015). Do board committees affect corporate financial performance? Evidence from listed companies in Ghana. International Journal of Business and Management Review, 3(5), 14–25.

- Quy, V. T. (2017). organizational culture and firm performance–A comparative study between local and foreign companies located in Ho Chi Minh City. Paper presented at the Proceedings of NIDA International Business Conference 2017–Innovative Management: Bridging, Thailand.

- Rankin, M., Ferlauto, K., McGowan, S. C., & Stanton, P. A. (2012). Contemporary issues in accounting. Australia: Wiley Milton.

- Rehman, S.-U., Mohamed, R., & Ayoup, H. (2018a). Cybernetic controls, and rewards and compensation controls influence on organizational performance. Mediating role of organizational capabilities in Pakistan. International Journal of Academic Management Science Research (IJAMSR), 2(8), 1–10.

- Rehman, S.-U., Mohamed, R., & Ayoup, H. (2018b). Management Control System (MCS) as a package elements influence on organizational performance in the Pakistani context. Pakistan Journal of Humanities and Social Sciences, 6(3), 280–295.

- Rehman, S.-U., Mohamed, R., & Ayoup, H. (2019). The mediating role of organizational capabilities between organizational performance and its determinants. Journal of Global Entrepreneurship Research, 9(1), 30. doi:10.1186/s40497-019-0155-5

- Sachdev, S. B., & Verma, H. V. (2004). Relative importance of service quality dimensions: A multisectoral study. Journal of Services Research, 4, 1.

- Shahwan, T. M. (2015). The effects of corporate governance on financial performance and financial distress: Evidence from Egypt. Corporate Governance, 15(5), 641-662.

- Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. The Journal of Finance, 52(2), 737–783. doi:10.1111/j.1540-6261.1997.tb04820.x

- Smith, K. G., Smith, K. A., Olian, J. D., Sims, H. P., Jr, O’Bannon, D. P., & Scully, J. A. (1994). Top management team demography and process: The role of social integration and communication. Administrative Science Quarterly, 412–438. doi:10.2307/2393297

- Taljaard, C. C., Ward, M. J., & Muller, C. J. (2015). Board diversity and financial performance: A graphical time-series approach. South African Journal of Economic and Management Sciences, 18(3), 425–447. doi:10.4102/sajems.v18i3.926

- Teeratansirikool, L., Siengthai, S., Badir, Y., & Charoenngam, C. (2013). Competitive strategies and firm performance: The mediating role of performance measurement. International Journal of Productivity and Performance Management, 62(2), 168–184.

- Thompson, J. D. (1967). Organizations in action: Social science bases of administration. New York: McGraw-Hill.

- Tierney, P, Farmer, S. M, & Graen, G. B. (1999). An examination of leadership and employee creativity: The relevance of traits and relationships. Personnel Psychology, 52(3), 591-620.

- Tsai, K.-H., & Yang, S.-Y. (2014). The contingent value of firm innovativeness for business performance under environmental turbulence. International Entrepreneurship and Management Journal, 10(2), 343–366. doi:10.1007/s11365-012-0225-4

- Turulja, L., & Bajgoric, N. (2018). Innovation, firms’ performance and environmental turbulence: Is there a moderator or mediator?. European Journal of Innovation Management, 22(1), 213-232.

- Uzkurt, C., Kumar, R., Semih Kimzan, H., & Eminoğlu, G. (2013). Role of innovation in the relationship between organizational culture and firm performance: A study of the banking sector in Turkey. European Journal of Innovation Management, 16(1), 92–117.

- Vafeas, N. (1999). Board meeting frequency and firm performance. Journal of Financial Economics, 53(1), 113–142. doi:10.1016/S0304-405X(99)00018-5

- Villalonga, B., & Amit, R. (2006). How do family ownership, control and management affect firm value? Journal of Financial Economics, 80(2), 385–417. doi:10.1016/j.jfineco.2004.12.005

- Wallach, E. J. (1983). Individuals and organizations: The cultural match. Training & Development Journal, 37(2), 28-36.

- Zaefarian, G., Forkmann, S., Mitręga, M., & Henneberg, S. C. (2017). A capability perspective on relationship ending and its impact on product innovation success and firm performance. Long Range Planning, 50(2), 184–199. doi:10.1016/j.lrp.2015.12.023

- Zhou, T. (2013). Understanding continuance usage of mobile sites. Industrial Management & Data Systems, 113(9), 1286–1299.