Abstract

Banking segment is one of the ultimate key segments that support the sustainable economic progress in Jordan. Hence, banks in Jordan are considered as tremendously significant financial establishments that pursue profit by providing various financial services to various customers through dealing with different kinds of risk. Therefore, loan decisions for such institutions are crucial because they can avert credit risk. However, loan sanction assessment at Jordanian banks is particularly based on credit officer’s intuition and sometimes a combination of credit officer’s judgment and traditional credit scoring models. Consequently, it is important to assess the riskiness of the banking sector in Jordan. Then again, banks kept data regarding their clienteles in data warehouses that can be looked as concealed knowledge assets that can be read and exercised via data mining tools. Artificial Neural Networks (ANN) denote a recent development of statistical techniques and promising tools of data mining and data processing. The current study attempts to develop an artificial neural network model as a decision support system to credit approval evaluation at Jordanian commercial banks based on applicant’s characteristics; the proposed model can be utilized to aid credit officers make better decisions when evaluating future loan applications. A real-world credit application of cases of both granted and rejected applications from different Jordanian banks was employed to develop the artificial neural model. The experimental outcomes showed that artificial neural networks area promising addition to the existing classification methods.

PUBLIC INTEREST STATEMENT

Banking segment is one of the ultimate sustainable economic progresses in Jordan. Hence, banks are considered as important financial corporations that pursue profit. Various financial services given to customers are crucial. Therefore, decisions and local sanctions are based on credit officials intuitions. It is important to assess the riskiness of banking sector in Jordan.

Artifical Neural networks (ANN) denote recent development of statistical techniques to credit approval evaluation at Jordan commercial banks.

The proposed model can be utilized to aid credit application of cases of both granted and rejected application form from different Jordanian Banks. The experimental outcomes reveal the artificial neural network is promising.

1. Introduction

The service economy acts as a significant character in the progress and social welfare of Jordan as an emerging nation with inadequate natural resources. Jordanian banks propose loan to individuals, manufacturing and agricultural enterprises to empower them to precede fruitful investments and, consequently advance the economic progress of Jordan. At what time banks maintain superior performance, it will add to the profitability of a bank additionally to the economic progress and improvement of a country.

Banks in Jordan are considered as extremely imperative financial organizations that look for profit by giving several services to clienteles while dealing with different kinds of risk. Risk taking is frequently seen as the simple carter for profitability and financial behavior. However, credit approval assessment at the Jordanian banks is idiosyncratic in sprit. This requires appraising individual loan application physically, imposing biases comprising knowledge, personal insights, and instinct of the credit executive. This technique has been substituted in a limited number of banks by credit scoring models to take appropriate credit decisions. Conversely, banks kept data regarding their clienteles in data warehouses which can be seen as concealed knowledge assets that can be read and exercised via data mining instruments. Therefore, credit management Jordanian banks required to progress more operative models to progress the predictive accurateness of credit risk judgements.

The determination of the current study is to build up a high-performance predictive model using artificial neural networks (ANN) for the Jordanian commercial banks. This model highlights the utmost substantial variables that effect the sanction of individual loan judgements in the Jordanian Banking sector. Furthermore, it would upgrade credit judgement and control loan office responsibilities, in addition to save investigation time and cost.

Credit forms a keystone of the banking sector as credit behaviour influences the success and firmness of a bank. Therefore, loan judgements are significant for financial organizations as they avert credit risk. Olokoyo (Citation2011) emphasizes that loaning is at the core of the banking business. Often, bank managers are faced with the problem of exasperating to upsurge credit volume while declining the possibility to non-payment (Huang, Chen, & Wang, Citation2007). On the other hand, credit scoring models enable bank mangers to ascertain those accounts that are likely to be creditworthy and those likely to default (bad credit risks) based on applicant’s characteristics taken from the application form.

Nowadays, the future of the banking business is extremely hooked on risk management subtleties. Banks are looking for more effective risk management instruments and decision support models supplemented by analytical techniques to endure in uncertain business environments. The basis of risk management is to launch a framework that outlines loan approval, credit risk rating system, risk-adjusted pricing system, and comprehensive reporting system (Arunkumar & Kotreshwar, Citation2006). In addition, Olszak and Ziemba (Citation2006) stress that decision-making is becoming more challenging. It needs using scattered information assets and engaging different parties (stakeholders, suppliers, customers, etc.) to improve decision-making in a scope of global nature. According to the author business intelligence (BI) systems can meet such challenges: support and increase proactive decision-making. Besides, BI contributes to optimizing business process and recourses leading to increased profits. A BI system is a combined set of tools and technologies used to collect data and analyse information to support making more improved decisions. Therefore, this study will help the policy makers to take a decision on implementation of ANN which is developed as an advanced data mining techniques and mimic the human brain on the computer. Moreover, this study helps to contribute to the Jordanian Banking sector as it shows the technique of minimizing the missing information by the ANN and which also helps to improve the performance. Furthermore, this study will help to guide the future researchers to explore ANN for getting better credit-risk management output as few studies have done research on it in the developed countries and more specially very few have done in the underdeveloped and developing countries.

2. Overview of Jordanian banking system

The banking industry in Jordan plays a decisive role in the progress of the country. Jordanian bank shares the support of economic action along with main providers to the countrywide economy as they play a foremost role in improving economic progress in the country (Kandah, Citation2009). According to the CBJ annual report (Citation2018), the number of working banks in Jordan stood at 30 by the end of 2022. Their services will be extended over all most all areas of Jordan with an index of banking density of 9,179 people for each branch at the end of 2022.

The rate of loans and advances to total credit facilities increased from 59.6% in 2000 to 86.1% by the end of 2020 (Central Bank of Jordan [CBJ], Citation2018 and figure 3). Simultaneously, the rate of overdrafts to total credit facilities and the rate of bills and discounted to total credit facilities witnessed a decline during the same period. This is evidence that retail banking is achieving extra base in the acts of banks in Jordan with an upsurge in economic activity also, since the upsurge in the volume of credits was distributed to all economic events. General trade, construction and industry are the main sectors accounting for the biggest part in the volume of credits.

To highlight the significant role of the Jordanian commercial banks, Table shows the percentages of some financial key signals taken from balance sheet items among banks operating in Jordan at the end of 2010. They are total assets, the outstanding credit extended by banks, total deposits, the total shareholders’ equity and the total capital. As shown, the five percentages affirm the soundness of the commercial banks as they record three quarter of share in each one. 74.87% of the total credit facilities extended by banks operating in Jordan are from commercial banks. This indicates the role of Jordanian commercial banks as well as their importance in enhancing economic and social development in Jordan.

Table 1. Some financial indicators of banks operating in Jordan

3. Literature review

The credit industry has gone through serious progress and development in the last decade. Banks’ officers have developed some credit scoring models to supplement traditional methods in order to classify loan applications to either good or bad based on the applicant’s attributes such as employment history, prior credit history, age, etc. Researchers are constantly searching for new algorithms to increase the accuracy of credit scoring simulations.

According to Ong, Huang, and Tzeng (Citation2005), a progress even to a fraction of a percent in credit accurateness will lead to substantial savings. Bensic, Sarlija, and Zekic-Susac (Citation2005) showed in their study that the probabilistic neural network model achieves the best results. They called for extending the methodology analysis by adding more neural network algorithms such as unsupervised classifiers as well as exploring other advanced statistical methods with AI techniques such as genetic algorithms in credit scoring modeling.

Basically, ANNs are the modeling of the human brain with the simplest definition and building blocks are neurons. In the human brain, there are approximately 100 billion neurons. Each neuron has between 1,000 and 100,000 connecting points. The information in the human brain is stored in a way that is distributed and, if necessary, we can parallel extract more than one piece of that information from our memory. We are not wrong to mention that there are thousands of very, very potent parallel computers in the human brain. There are also cells positioned similarly to the human brain in multi-layer artificial neural networks. Each neuron has certain coefficients linked to other cells. The data is allocated during instruction to these connecting points to enable the network to be taught.

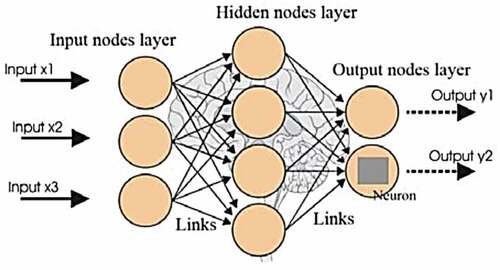

A neural network comprises three layers, as illustrated in Figure , an entry layer, a middle layer, and a yield layer. The red lines shown are the cells and the arrows are the points of association. The network displays the information collection that is ready for input layer practice. The network gives the weights of the activities to the intermediate part of the connecting lines. Not all points should be a value, and certain points could be null. A limit between these strata is introduced to ensure that the values of zero are not zero at the link points.

Figure 1. Layers of the artificial neural network.

Martens, Baesens, Gestel, and Vanthienen (Citation2007) use rule extraction techniques to create a grouping model. Boguslauskas and Mileris (Citation2009) argue that artificial neural networks and LR are the most efficient, widely used methods for CRM. They describe the rates of CR estimation models' accuracy and their counting for the analysis of Lithuanian enterprises credit risk. They confirm that neural network models enjoy upper rates of grouping accurateness.

Limsombunchai and Lee (Citation2005) developed a loaning decision model and shown that the PNN model was effectively used in grouping and screening agricultural loan in Thailand. Huang et al. (Citation2007)state that NN models are more accurate, adaptive and robust in bank failure prediction when compared with other techniques such as discriminant analysis, logistic regression, etc.

Raghavendra and Simha (Citation2010) utilized data mining feature selection algorithms on Australian, German, and Japanese, credit data so as to identify the ideal set of attributes for the classification model. The feature selection algorithm and classification accuracy were used to measure the performance of the predictive model with the neural network for risk classification. Results show that the classification accuracy and number of features selected algorithms with neural network were more efficient when compared with other methods. Lahsana, Ainon, and Wah (Citation2010) point out that to pursue even a small improvement in credit scoring accuracy, soft computing techniques have to be used to assist existing methods.

Keramati and Yousefi (Citation2011) suggest that credit executives need to use ML techniques to fulfil the growing demand on credit departments also to manage the huge amount of credit data in order to save time and reduce errors. Thus, neural networks are a rewarding alternative business intelligence tool that can be applied to credit scoring models as they provide better classification accuracy. Therefore, the main objective of the current study is to propose a high-performance predictive model capable of assisting credit managers in taking sound and safe personal loan decisions.

4. Data collection

A combined data of both accepted applications and rejected applications from different Jordanian banks for the 2010–2018 periods was used to achieve the objective of the current study. The number of opinions from each bank was hidden so as to protect the privacy of the banks. The data is composed of 492 cases. From the sample, 292 (59.3%) applications were creditworthy while 200 (40.3%) applications were not. A total of 13 variables were used: seven of them were scale while six were categorical. Also, there were 12 independent variables and 1 dependent categorical variable with two values, 1 for accepted applications and 0 for rejected ones. All scale variables were standardized so as to improve the network training. SPSS software (Version 22) was employed to perform the analysis.

5. Methodology

Artificial neural networks are considered a strong alternative to conventional forecasting and grouping methods due to their ability to capture nonlinear and complex relationships. According to Cao and Parry (Citation2009), these models have a biologically stimulated competence that satirists processing competences of the human brain. They have been used successfully in financial applications, a good ability in classification (e.g., credit scoring, corporate failure prediction and bond ratings) as well as in modeling tasks such as predicting share price movements and exchange rate fluctuations. The multi-layer perception (MLP) is the most popular FFNN model used in pattern recognition. Designing an artificial NN model successfully depends on a perfect understanding of the problem, and on determining upon most influential input variables.

A typical FFNN model is represented as some processing units called neurons cooperating across several linking layers (Lahsana et al., Citation2010). The information flows from origin to destination strictly in one direction through a system of weighted connections, without interconnections between the output of a neuron and the input of another neuron in the same layer or in a preceding layer. The output of each neuron is the outcome after applying the transfer function to the weighted sum of all inputs to that neuron (Limsombunchai & Lee, Citation2005).

A typical FFNN model is usually comprised of a three-layered architecture: input, hidden, and output layers. The input layer feeds the input variables (predictors) to the next layer. Each concealed neuron receives a weighted sum of entire efforts in the input layer, applies a transfer function such as log sigmoid, hyperbolic tangent, soft max to the weighted sum. Similarly, each hidden neuron transfers a weighted outcome to each neuron in the yield layer, i.e., each dependent variable neuron (Cao & Parry, Citation2009). The outcome of the output neuron is the solution to the problem. A learning algorithm is used to find the values of the connection weights where the network preserves its knowledge. During training when an input pair is fed to the network, the net calculates a temporary output, Y. Next, the net compares the actual output, Y, with the desired output, T, and if not satisfied then it adjusts the connection weights in proportion to error which is equal to the difference between its output and the target in an iterative process until a desirable result is reached. This is done mathematically by calculating delta ∆, where is: ∆ = T-Y. The training objective is to find the best set of weights that lessens the mean squared error (Malhorta & Malhorta, Citation2003). The network model is trained until it is able to recognize the input patterns and classify them to give corresponding outputs.

Furthermore, the current study will use a multilayer feed-forward (MLFF) algorithm to build a three-layer neural network model. The number of neurons in the first layer and the last layer should be set according to the number of independent variables and dependent variable, respectively. The middle layer is the hidden layer and the number of neurons in this layer will be set during model implementation using the automatic architecture selection in SPSS. Therefore, the neural network model will consist of three fully connected layers: an input layer, a hidden layer and an output layer in 12-9-1 architecture. Therefore, the input layer has 12 neurons equivalent to the independent variables, 9 hidden neurons with hyperbolic tangent function while the output layer represents the dependent variable with soft max activation function. Next, the training dataset will be used to train the neural network on mixed types of accepted and rejected applications. Throughout the training phase, the net will extract the pattern of accepted applications as well as the pattern of rejected applications. After training, the net will classify the training data correctly. Then, the net is ready for testing phase; a testing set (which includes cases that the net has not seen before) will be used to examine the model’s predictive power. This study uses the batch training method because it reduces total error more quickly.

6. Result analysis

To build the neural network model, the dataset was divided randomly using a partitioning variable created by SPSS into training, validation and testing subsets. A total of 359 (73%) cases were used for training, 64 (13%) for validation, and 69 (14%) for testing. The three subsets contain both accepted and rejected applications as seen in Table .

Table 2. Screening data

Using training set with the mentioned architecture, the network was able to conduct the training and learn the relationship between input attributes and credit decision. A training algorithm was used to adjust the connection weights in the neural network during the learning phase. A validation set was used during training as well to minimize overfitting. To measure the predictive performance of the developed model, a testing set was used to test the results. All classification results are shown in Table . Furthermore, the gradient descent optimization algorithm was used to estimate the synaptic weights of the neural network with learning rate and momentum 0.7 and 0.1, respectively. Table displays the training results of the neural network. The training is aimed to reduce the error between the network output and the actual output. As seen from Table the percentage of incorrect predictions was 7%, meaning the neural model was able to classify 93% of training cases correctly. Also, the percentages of false predictions for the testing and validations were 8.7% and 17.2%, respectively.

Table 3. Model summary

Table 4. Classification results

Table explains the analysis of the importance value of independent variables. The importance of an independent variable is a measure of how much the predicted value of the network’s model is influenced by different values of the independent variable. Large importance value means the variable has the strongest effect on the credit decision outcome. As seen, debt income ratio (DPR) has the highest concern in the model creation and the predicted value of the model (credit decision) is strongly influenced by the DPR while gender achieved the least importance level. Table also displays the normalized importance which is equal to the percentage of each variable importance value divided by the largest importance value (in this case, the DPR’s importance value).

Table 5. Independent variable importance

Debt income ratio, nationality, and TML seem to have the greatest effect on how the network classifies credit applications. The importance value of debt income ratio, nationality, and TML are 0.163, 0.127, and 0.113, respectively. The normalized importance of debt income ratio, nationality, and TML are 100%, 78.7%, and 72.3%, respectively. Whereas gender has the least influence on credit decision and the importance value of gender showed in Table is 0.029 as well as the normalized importance percentage is showing 16.7%. The importance value of variables age, loan purposes, guarantor, amount, income term, experience, loan period, and interest rate are 0.073, 0.062, 0.077, 0.046, 0.071, 0.059, 0.098, and 0.094, respectively. Moreover, the normalized importance percentage of variables age, loan purposes, guarantor, amount, income term, experience, loan period, and interest rate are 43.8%, 36.8%, 48.2%, 29.4%, 43.6%, 36.2%, 61.3%, and 59.9%, respectively. The way these variables are correlated to the predicted value of the credit decision is not obvious. From common-sense one could guess that a larger amount of DPR points to a greater likelihood of rejecting the credit application. Also, Jordanian applicants can get credit much easier than non-Jordanian applicants. Besides, banks are more flexible to extend credit to applicants working in companies accredited to the bank companies.

7. Conclusion

The results show the neural model could screen 95% of accepted applications correctly, and 89.9% of rejected applications correctly in an overall percent, 93%. In the holdout sample, the classification accuracy level was 92.3% for accepted applications and 76.3% for rejected applications with an overall percentage of 82.8. Furthermore, the testing set classification accuracy of accepted applications was 93.3% while for rejected applications was 87.5% with an overall percentage of 91.3%. However, type I error occurs when rejected applications are classified as accepted applications. On the other hand, type II error occurs when an accepted application is classified as rejected one. For a lending decision, creditors need to look for a classification tool that reduces type I error as much as possible to avoid the cost of default as possible. The percentage of type I error in the training data was 10.1%; while for the testing data it was 12.5%.

Although loan approval in the Jordanian banks has been up to the credit officer mostly or supported by credit scoring based on traditional statistical models, banks can improve loan approval methods by using artificial neural networks. This study proposes a new approach to evaluate loan applications as a decision support model to credit officer judgment. The proposed model uses the most important variables in Jordanian credit industry. Debt payment ratio highly influences the loan decision while gender has the least. The results show that a multilayer feed forward (MLFF) neural network successfully classified loan applications with 91.3% accuracy level. The benefit of using such method in the Jordanian commercial banks enfold improving credit decision effectiveness, saving analysis time and cost. Furthermore, this study proposes a further study that compares multilayer feed-forward neural networks and other types of artificial neural networks with different learning algorithms. Also, a study that compares the classification performance of artificial neural networks against tradition statistical techniques is suggested.

Additional information

Funding

Notes on contributors

Khaled Alzeaideen

Dr. Khaled Abdulwahab Helal Alzeaideen is an Associate Professor of Business Administration at the faculty of Economics and Business Administration at Zarqa University. Dr. Alzeaideen works as the dean of Registration and administrations office sice 2010, his reasearch inerests are related to the area of Business Administration, and his Professional Objectives are: - Contributing to the administrative processes of the university and in the design and planning of programs and committees and science at the university, and represent the university or its colleges. - Teaching, guiding, guiding and supervising student research, facilitating the learning process, facilitating the methods of achieving it, preparing the various educational materials needed for it, and using it in appropriate ways, times and places. - Provide students with cognitive skills and technical skills.

References

- Arunkumar, R., & Kotreshwar, G. (2006). Risk management in commercial banks: A case study of public and private sector banks. Indian institute of capital markets, 9th capital markets conference. Retrieved from SSRN http://ssrn.com/abstract=877812

- Bensic, M., Sarlija, N., & Zekic-Susac, M. (2005). Modeling small-business credit scoring by using logistic regression, neural networks and decision trees. Intellectual Systems Accounting and Financial Management, 13(3), 133–9. doi:10.1002/isaf.261

- Boguslauskas, V., & Mileris, R. (2009). Estimation of credit risk by artificial neural networks models. Izinerine EkonomikaEngineering Economics, 4, 1392–2785.

- Cao, Q., & Parry, M. (2009). Neural network earning per share forecasting models: A comparison of backward propagation and genetic algorithm. Decision Support Systems, 47, 32–41. doi:10.1016/j.dss.2008.12.011

- Central Bank of Jordan. 2018. Annual Repot. 47. Amman, Central Bank of Jordan: Jordan.

- Huang, C. L., Chen, M. C., & Wang, C. J. (2007). Credit scoring with a data mining approach based on support vector machines. Experts Systems with Applications, 33, 847–856. doi:10.1016/j.eswa.2006.07.007

- Kandah, A. (2009). Interviews with Jordanian bankers, association of banks in Jordan. Amman, Jordan.

- Keramati, A., & Yousefi, N. (2011). A proposed classification of data mining techniques in credit scoring.International conference on industrial engineering and operations management Kuala Lumpur, Malaysia.

- Lahsana, A., Ainon, R., & Wah, T. (2010). Credit scoring models using soft computing methods: A survey. The International Arab Journal of Information Technology, 7(2), 129–139.

- Limsombunchai, G. V. C., & Lee, M. (2005). Lending decision model for agricultural sector in Thailand,American. Journal of Applied Science, 2(8), 1198–1205.

- Malhorta, R., & Malhorta, D. K. (2003). Evaluating consumer loans using neural networks. Omega, 31(2), 83–96. doi:10.1016/S0305-0483(03)00016-1

- Martens, D., Baesens, B., Gestel, T., & Vanthienen, J. (2007). Comprehensible credit scoring models using rule extraction from support vector machines. European Journal of Operational Research, 183(3), 1466–1476. doi:10.1016/j.ejor.2006.04.051

- Olokoyo, F. (2011). Determinants of commercial banks lending in Nigeria. International of Financial Research, 2(2). doi:10.5430/ijfr.v2n2p61

- Olszak and Ziemba. (2006). Business intelligence systems in the holistic infrastructure development supporting decision-making in organizations. Interdisciplinary Journal of Information, Knowledge, and Management, 1, 47–58.

- Ong, C., Huang, J., & Tzeng, G. (2005). Building credit scoring models using genetic programming. Expert Systems with Applications, 2, 1–7.

- Raghavendra, B. K., & Simha, J. (2010). Evaluation of feature selection methods for predictive modeling using neural networks in credits scoring. The International Journal of Advanced Networking and Applications, 2(3), 714–718.