Abstract

This study aims to describe the intellectual capital disclosure practices in the biggest Indonesian universities and to empirically examine the impact of intellectual capital disclosure on prospective student interest. Data were drawn from official website of Indonesian universities. The result indicates that from 30 samples of universities, there are no university has fully disclosed their intellectual capital indicator. Actually, besides of human capital information, the universities tend to report their relational capital which indirectly describes university’s achievements and excellences. Based on Warp-PLS results shows that intellectual capital disclosure has a positive impact on prospective student interest. Regardless of its limitations, this study has practical implications for the decisions taken by universities in choosing what information will be presented on their website.

PUBLIC INTEREST STATEMENT

The study of intellectual capital (IC) in Indonesia only stretched in the early 2000s. At that time, research on IC mostly studied IC management in private entities (public companies). These studies can be grouped into two main categories, namely research on intellectual capital disclosure/reporting, and the second on intellectual capital performance (the impact resulting from good IC management).

In the same period, in Europe, scholars had begun to study IC management practices at universities. In fact, several countries in Europe have also issued guidelines for the preparation of university IC reports.

This paper is very interesting because it seeks to cover the impact of IC disclosure through the university’s website on the interests of prospective students.

1. Introduction

The ministry of research, technology, and higher education (Ristedikti)’s data shows in the last 5 years (2013–2018), the interest of writing tests to enter public and private universities continues to increase, universities that have many enthusiasts have an attractiveness and a good competence to compete from various sides. Universities are asked to get a competitive advantage for recruiting students and obtaining funds (Bisogno, Citro, & Tommasetti, Citation2014). They must compete better for teachers, researchers, students, and funds get used to managerial procedures and producing reports which allow internal and external bodies to evaluate their performance (Sànchez, Elena, & Castrillo, Citation2009). IC reporting allows comparability between different universities and allows quality assurance at a university (Leitner, Citation2002). Higher education institutions should use the intellectual capital framework as a heuristic tool to assist them in the challenges of new management and inform their resources and activities to stakeholders and the wider community (Sànchez et al., Citation2009).

Intellectual Capital and intellectual property are included in intangible assets (Mok, Sohn, & Ju, Citation2009). Although the IC concept was first developed as a framework to analyze the contributions of intellectual resources in for-profit enterprises, it has been soon taken over by public and non-for- profit organizations, due to it overall importance (Antonella & Stefania, Citation2011; Kong & Prior, Citation2007; Mouritsen, Thorbjørnsen, Bukh, & Johansen, Citation2004). Universities are examples of public and non-profit organizations. Universities and research institutions adopt many practices that companies use, in this context, the company should provide information that shows their true condition (Sànchez et al., Citation2009). This information are not only in the form of monetary numbers but also the intangible assets disclosure which cannot be presented in monetary figures, that is an intellectual capital disclosure as competitiveness among similar institutions. A major consequence was the introduction of IC reports recognizing that the “the efficient use of IC is essential for a university’s performance” (Karl‐Heinz Leitner, Schaffhauser‐Linzatti, Stowasser, & Wagner, Citation2005; Sànchez et al., Citation2009).

Universities should follow the basic principles of autonomy and accountability to better manage their internal affairs and satisfy societal needs (Sànchez et al., Citation2009). In Indonesia, educational institutions such as universities have not been obliged to make voluntary non-financial reports like IC reporting, whereas intellectual capital reporting will be a good mechanism for universities to satisfy users’ needs (Leandro Cañibano & M. Paloma Sánchez, 2009). In terms of their broad accountability to society, they should report on their activities (Coy, Fischer, & Gordon, Citation2001; Sordo, Farneti, Guthrie, Pazzi, & Siboni, Citation2016). IC as a part of a strategy to make universities accountable towards their stakeholders (Antonella & Stefania, Citation2011).

Bezhani (Citation2010) has found that the amount of IC information disclosed by UK universities in their annual reports is low and had low awareness of ICD. Even though the study results (Najim, Al-Naimi, & Alnaji, Citation2012) at Jordanian universities stating that the intellectual model has a positive impact on university performance in general. Regarding this research model that uses the university’s website as a data search source (Rossi, Nicolò, & Polcini, Citation2018) have been doing study in Italian universities about IC disclosures on universities’ websites and finds that extensive intellectual capital disclosure through the universities’ websites are for human and internal capital items, whereas external capital is still limited in this means.

The biggest universities in Indonesia have their attractiveness, annual reports, and data from accessible website. Universities’ websites are a medium of communication between customers (new students) and universities to show their IC components. Some researchers have previously taken objects in different countries, such as Jordan and countries in Europe, they take all universities in the country on average to be used as research objects. This study uses only 30 biggest universities in Indonesia and has been accredited taken from the 4ICU website as samples. The 4ICU website which utilizes access activity data visited by university websites to measure its ranking, the more frequently accessed, the higher its rank. In particular, Dumay (Citation2016) emphasizing the role of web-based disclosure of IC in the private sector context, stated that it is “dynamic” and “followed”. A similar investigation could be extended to public organizations devoted to research and teaching, as universities, to detect how web-based disclosure may improve ICD (Rossi et al., Citation2018).

This study describes the results of descriptive statistics analysis contents that reflect Intellectual Capital disclosure from the biggest universities in Indonesia and empirically examines the influence of Intellectual Capital disclosures on the universities’ official websites with changes in the interest of new students using Partial Least Square (PLS).

2. Intellectual capital disclosure and students in Indonesian Universities

There are more than 120 public universities and 3000 private universities in Indonesia. Therefore, it is not easy for prospective students to determine their choice of continuing education. In addition to the general characteristics and accreditation status, information related to how the university's “wealth” is something that prospective students also consider (Fathony & Ulum, Citation2018).

As a public sector entity, universities are also required to develop innovation (Moussa, McMurray, & Muenjohn, Citation2018). One important aspect in the current digital era is the ability of universities to communicate via websites. If the website is understood as a medium to act as a public relations function, then universities are even required to start adapting to the internet of things (IoT)(Amodu, Omojola, Okorie, Adeyeye, & Adesina, Citation2019). Website can also act as a medium to show the level of accountability of universities and their governance. Brender, Yzeiraj, and Dupuy (Citation2017) stated that in public governance, the network model emphasizes participatory and interactive organizations and co-production of services.

Through the website, the university can reveal information that is actually voluntary. For example information about the characteristics of lecturers, achievements that have been achieved by the academia, qualifications of education personnel, and others. More than that, through the website, universities can also report various types and results of cooperation carried out, both regional, national and international. Such information is actually aspects of intellectual capital.

Why does this information need to be disclosed through the website? Because until now, there are no regulations that govern the university's obligation to prepare annual reports as required to public companies. In addition, the website is a very user-friendly medium for prospective new students. This is important, because user knowledge has become a very important source of innovation in such organizations (Park, Cho, Jung, & Main, Citation2015).

3. Theoretical framework for intellectual capital disclosures

3.1. Intellectual capital

Stewart (Citation1997) stated that Intellectual Capital is a resource derived from knowledge, experience, and staff competencies that can be transferred, starting from the ability of the organization to innovate and manage change, from its infrastructure from the relationship between stakeholders and partners (Lee, Citation2010).

In general terms, all of the major players in the IC community share the idea that intellectual capital, from a qualitative point of view, can be divided into three categories (Figure ): structural (or organizational), human and relational capital (Antonella & Stefania, Citation2011). According to Stewart (Citation1997) human capital is an individual level of knowledge, such as professional skills, experience, and innovativeness that every employee possess (Lee, Citation2010). Structural Capital includes all non-human storehouses of knowledge in organizations (Bontis, Richardson, & Keow, Citation2000). Company vision, management philosophy, organizational culture, strategies, processes, work systems, and information technology can be categorized into these assets (Edvinsson & Malone, Citation1997). Relational capital is the totality of the relationship between the organization and its main stakeholders (Antonella & Stefania, Citation2011).

Figure 1. Intellectual capital framework.

3.2. Intellectual capital disclosure

Since the 2000s, academics and practitioners have begun to focus on the company’s IC (ICD) disclosure issues in their annual reports (see for examples: Goh & Lim, Citation2004; Guthrie & Petty, Citation2000; Guthrie, Petty, Ferrier, & Wells, Citation1999). The definition of IC disclosure has been fiercely debated among experts in various literatures.

Guthrie and Petty (Citation2000) did not offer an explicit definition of IC disclosure, but they allude to the fact that IC disclosure now provides greater benefits than in the past. Especially for sectors that have dominant industrial characteristics which then experience changes, such as from the manufacturing sector turned into high technology, financial and insurance services.

Bukh, Johansen, and Mouritsen (Citation2001), Petty and Guthrie (Citation2000) dan Mourtisen, Bukh, and Marr (Citation2005) identified that the IC literature in accounting mainly addresses external reporting. This can be understood because the capital market does want more reliable information related to knowledge resources owned by the company, and disclosure of IC will reduce transaction costs and uncertainty among related parties. (Tayles, Pike, & Sofian, Citation2007). Furthermore, Bukh (Citation2003) states that company disclosures about ICs are part of the framework of the value creation process in the company.

Most of the literature on IC in various countries focuses on the disclosure of IC in the company’s annual report (Goh & Lim, Citation2004; Guthrie & Petty, Citation2000). Several studies of efforts to explain the different levels of IC disclosure in annual reports (April, Bosma, & Deglon, Citation2003; Brennan, Citation2001; Ulum, Citation2011), but not many use statistical tests (Bontis, Citation2002; Bozzolan, Favotto, & Ricceri, Citation2003; Williams, Citation2001). The level of IC disclosure is generally assessed using content analysis of annual reports from a small number of samples (companies).

Mouritsen, Larsen, and Bukh (Citation2001) state that IC disclosure in a financial statement as a way to express that the report describes the company’s activities that are credible, integrated (cohesive) and “true and fair”. They refer to IC reports which show that much of the IC disclosure literature is based on textual analysis of financial statements. Very few companies make separate IC reports.

Furthermore, Mouritsen et al. (Citation2001) state that IC disclosure is communicated to internal and external stakeholders by combining numerical, visual and narrative reports aimed at creating value. Bukh et al. (Citation2001) also confirm the same thing, that IC reports in practice, contain various financial and non-financial information such as employee turnover, job satisfaction, in-service training, customer satisfaction, supply accuracy, and so on.

In particular, ICD can be very effective means for companies to signal quality excellence because of the importance of IC for wealth creation in the future (Guthrie & Petty, Citation2000). Especially for companies with a strong IC base, ICD can distinguish them from other low-quality companies (An, Davey, & Eggleton, Citation2011). Signals from IC attributes can bring many benefits to the company, such as improving the company’s image, attracting potential investors, lowering capital costs, decreasing stock volatility, creating understanding of products or services, and more importantly improving relationships with various stakeholders (Singh & Van-der-Zahn, Citation2008; Vergauwen, Citation2005). Voluntary disclosure of IC information is usually done through the company’s annual report media, or through an IPO prospectus (initial public offering).

As a form of voluntary disclosure, ICD depends on several factors, two of which are organizational culture and employee awareness (Iliya Nyahas, Munene, Orobia, & Kigongo Kaawaase, Citation2017). IC disclosure has become a new form of communication that controls “contracts” between management and workers. This allows managers to make strategies to meet the expectations of stakeholders such as investors, and to convince stakeholders of the advantages or benefits of company policy (Ulum, Citation2009).

3.3. Intellectual capital disclosure in university

Leandro Cañibano and M. Paloma Sánchez (2009) argue that universities can reflect the management and government processes followed by companies, learn from their experiences and benefit from the IC framework to cope with the external pressures for change they are facing. This study will describe the three items into 46 indicators. This description (Table ) follows Ulum (Citation2012)’s study where these indicator numbers have been adapted from the BAN-PT guidelines to adjust universities in Indonesia.

4. Empirical literature review and hypothesis development

4.1. Previous studies

Some researchers have revealed the facts of the benefits and importance of IC disclosures at universities like Sànchez et al. (Citation2009) and K.H Leitner (Citation2002), both of them used the same framework model from Austrian universities. More recently, some researchers conducted studies on intellectual capital disclosure on the universities’ websites which is preceded by Middleton, McConnell, and Davidson (Citation1998), such as Rossi et al. (Citation2018), Chatterjee and Hawkes (Citation2008), Bisogno et al. (Citation2014). Najim et al. (Citation2012) conducted a research by taking samples of three universities in Jordan tested three components of intellectual capital (human, structural, relational capital) and leadership and strategies to realize university goals and found that relational capital, human capital and leadership capital had a positive impact on attracting new students, while structural capital had no significant impact.

Sangiorgi and Siboni (Citation2017) used analysis content on voluntary social reports and survey the most popular university managers in Italy. They found that in voluntary social reports there were a large number of IC disclosures and top managers had an awareness of the benefits of IC management. Rossi et al. (Citation2018) explaining the way of IC disclosure through a website, this study aims to identify and provide new insights into the factors that enable IC disclosure through 58 universities in Italy. This study presents a new view of IC which is expressed through dynamic and timely communication tools, that is Italian universities’ websites. The results show that universities in Italy using IC reporting widely and the information categories most widely disclosed are Human Capital and Internal Capital, followed by information about External Capital.

4.2. Hypothesis development

The independent variable used is the percentage of IC disclosure through the official website of the 30 biggest universities in Indonesia based on the number of students. Few studies have investigated the relationship existing between the IC of the universities and their performance (Constantin, Citation2009; Cricelli, Greco, Grimaldi, & Dueñas, Citation2018; Secundo, Lombardi, & Dumay, Citation2018).

The dependent variable is the percentage of changes in the interest of new students’ public and private universities in Indonesia which indirectly describe the universities’ performance. IC disclosures help fulfil its accountability to stakeholders. IC is a collection of intangible assets that allow organizations to transfer material, financial and human resources to a system that can create value for stakeholders (Córcoles, Peñalver, & Ponce, Citation2011). Students are directly one of the biggest stakeholders in a university. The ability to disclose the intangible assets like indicator items of Intellectual Capital such as the achievements and completeness of university facilities is a special attraction for prospective students. The results of the Najim et al. (Citation2012)’s study supports the statement that intellectual capital is something which supports the university to attract new students. Therefore, it is hypothesized that:

Ha: The percentage of IC disclosure affects the changes in the interest of universities’ new students.

5. Research design

The object of this study is the universities that have the highest ranking at 4ICU in 2018, this website assesses it based on the flow of most web visits. The higher the visits to the website, the higher the ranking obtained by the university. The idea of a global economy signifies the availability of information that is accessible and equal on the company’s website (Chatterjee & Hawkes, Citation2008). With studies conducted by Rossi et al. (Citation2018) and Chatterjee and Hawkes (Citation2008) allows researchers to obtain data by collecting information describing 46 IC indicators through the official website of the largest universities in Indonesia.

Table of analysis content will be filled with number 0 if no information about IC indicator is found on the university web, number 1 for information in the form of narration, number 2 for information in the form of numbers, number 3 for information in the form of monetary or financial units, number 4 for information in the form of graphic images or table. The author will present and describe the results of the survey and content analysis according to the comparison of the disclosures between Human Capital, Structural Capital, and Relational Capital as well as the trend of the form of IC indicator disclosure by comparing the amount of narrative, number, monetary, and table graphs.

Hypothesis testing uses Partial Least Square (PLS), where independent variable (percentage of IC disclosure through the university’s official website) are divided into three constructs (human capital, structural capital, and relational capital). The separation of these three constructs follows the study (Najim et al., Citation2012). The three constructs have a different level of relation to the dependent variable including the variable “attracting students”. Dependent variable represents the interest of new students towards the university measured by processing data on written examinations for public and private taken from the university’s official website and the SBMPTN being a form of the percentage of interest changes in 2017 to 2018.

6. Empirical results and discussion

Samples of this research are the biggest universities in Indonesia which have a total of more than 24,000 students and have the highest rating at 4ICU in June 2018. This research will show the percentage of Intellectual Capital disclosures in these universities which are detailed in three constructs (HC, SC, and RC) Descriptive statistics tables will also show changes in the interest of universities’ new students for public and private universities in Indonesia with the highest number of students (Table ).

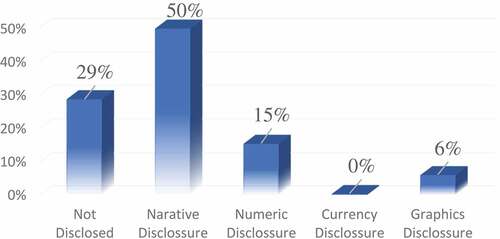

The content analysis shows monetary/financial disclosures occupy the lowest position. 0.0029 is a detail of the number 0% in the currency disclosure graph or there are only four disclosures with monetary figures from 1,378 indicators in 30 universities. This statement is supported by Leitner (Citation2002), in the industry, there is a strong demand for the valuation of intangible assets by financial figures, with mixed and successful solutions offered. In the case of universities, this call is not that loud, but existent.

The highest IC reporting is occupied by 50% narrative disclosure, especially for indicators of the university’s vision and mission and goals and objectives. Due to the limitations of a purely indicator-based method, IC reports should also integrate qualitative methods (best practice, narration, etc.) (Leitner, Citation2002). Qualitative information (narrative) is considered the easiest way to present IC indicator information on universities’ website.

Graph 1. Presentation of IC disclosure types.

The drop-out ratio ranks second in the least disclosure, with only 3 from 30 universities disclosing it. Institutes will not be willing to deliver information and especially intimate information if they have the fear that this will have negative consequences for their funding (Leitner, Citation2002). The ratio of drop-out students is considered as information that will convey the weaknesses of their performance (universities) and is considered to cause negative consequences that are not desired by stakeholders. Companies producing IC reports differentiate between the information needed for management purposes, not all of which needs to be diffused, and the information to be made available to stakeholders (Sànchez et al., Citation2009).

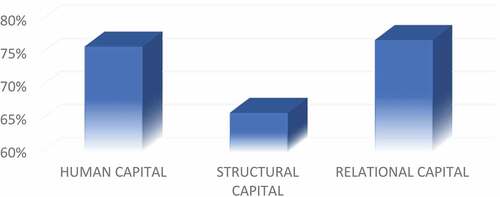

Content analysis shows that relational capital occupies the highest disclosure rate (77%), followed by a very thin difference by human capital (76%) and the smallest disclosure is Structural Capital (66%), the numbers of percentage are not too far apart. This fact proves that universities understand the importance of human capital (HC). Besides that HC is the most important element for universities, HC (for example, related to competence and attitude) is a determinant of financial performance (Iwamoto & Suzuki, Citation2019).

The greater amount of disclosure must involve aspects related to RC, this will encourage an increase in university performance comparability concerning the three university missions and ultimately improve the university’s overall performance in terms of IC (Sangiorgi & Siboni, Citation2017). Relational Capital is the most interesting item to be disclosed because the indicators in it indirectly reveal the competitive advantages of the university and attract students. Structural Capital occupies the lowest disclosure position, particularly structural capital has to be considered as a blind spot within universities (Leitner, Citation2002). In general structural capital is the most difficult to identify (as a blind spot) because most of it is in the form of a constructor of the organization.

Graph 2. Percentage of the three IC constructs.

Leadership, human and relational capital have in general a significant effect on realizing the majority of university goals, and more than structural capital (Najim et al., Citation2012). Furthermore, Najim et al. (Citation2012) state that universities attract students through developing relationships with local communities. This results in a greater impact on the disclosure of Relational Capital than on Structural Capital and leadership. This statement can be attributed to the fact that the sample universities are more revealing other IC categories besides structural capital.

The disclosure of IC is influenced by regulations from the local government, evidenced by “academic lecturer competency item” revealed by 28 of 30 universities. UU number 14 in 2014 concerning Teachers and Lecturers stated that the requirement to become a lecturer must have a minimum level of masters education (Indiyati, Citation2015). The University will display the related data to obey the regulations as a form of accountability such as for some IC items like data on the number of permanent lecturers, qualifications (number of positions) of academic lecturers and 98% of lecturers’ achievement disclosed by 30 universities samples.

Over the past decade, knowledge assets and IC have attracted more attention, not only among CEOs and academics but also national policymakers (Lin & Edvinsson, Citation2008). Among main barriers, we can list cultural barriers (fear of measurement and new systems, lack of understanding), lack of meaningful employees involvement, lack of common definitions of terms and IC indicators, vision and strategy poorly defined and understood (Antonella & Stefania, Citation2011). Whereas universities must have the autonomy that allows them to adopt the necessary changes (Constantin, Citation2009).

To complete the test through PLS, Table present fit and quality indices models that present indexes and p-values and compare them with the existing criteria.

Table 1. Intellectual capital indicators

Table 2. Descriptive statistics

Table 3. Model fit and quality indices

PLS test results show the dependent variable changes in the interest of new students’ R-square is 0.28, meaning that the three constructs of IC disclosure can explain this dependent variable by 28% significantly, another 72% is explained by other variables (Figure ). The existence of a significant positive influence shown by this test proves that the greater the disclosure of IC on the official website of the university will affect the increase in the level of changes in the interest of new students of the public and private universities.

Figure 2. The result of the PLS test.

This research is supported by the results of the Najim et al. (Citation2012)’s study, where Intellectual can attract the new students. The university’s ability to attract new students can be used as a material for performance evaluation, but a company performance evaluation that only bases on a periodic report will be very misleading (Suwardjono, Citation2014). This results reinforces the findings of Ulum, Septerina, Prasetyo, Mohamed, and Abdullah (Citation2017) which stated that the intellectual capital disclosure enhance organisational governance.

To complete the results of the study, we add the dependent variable data to 2 years. In theory, this is related to stakeholder theory where the different stakeholders of the university are the scientific community, students, citizens, industry, etc. (Leitner, Citation2002). In this study stakeholder focused on students as contributors to the largest development funds at the university. The more fulfilled the student’s need for information that is considered beneficial, the greater the ability of the university to attract the interest of its students.

7. Summary and conclusion

7.1. Findings

In general, there are no universities in Indonesia that disclose IC information in full in accordance with the instruments used in this study. During this observation period, the university seemed to try to influence prospective new students by disclosing information related to relational capital and of course information related to human capital aspects.

Statistical testing shows that the ICD constructed by three formative indicators (HC, SC, and RC) has a positive effect on the interest of prospective new students. This shows that in addition to the characteristics and accreditation status factors (Fathony & Ulum, Citation2018), disclosure of information about IC is also a concern for prospective students in determining the choice of their university.

7.2. Implications

This research has practical implications for the decisions taken by universities in choosing what information will be presented on their website. If they are aware of current issues needed by prospective new students, of course they will reveal more information about intellectual capital. Even though it is voluntary in nature, presenting as much information as possible will certainly have a positive impact on the university. This is of course if the information presented is the hidden “wealth” owned by the university, which so far has only been a matter of word of mouth between them. Of course, this does not mean we ignore the power of “traditional” marketing patterns by word of mouth (Ngoma & Ntale, Citation2019).

7.3. Contributions

An important contribution of this study is that it is proven that the ICD has a positive effect on the interests of prospective new students. In addition to describing the preference information needed by prospective students, this study also provides evidence that in general universities in Indonesia are quite good at presenting information about IC through their website. The percentage of disclosures which averaged above 60% shows that in public organizations (universities), concern for voluntary disclosure of the information is not left behind when compared to practices in the business sector (see for detail: Macagnan, Citation2009; Uyar, Kilic, & Bayyurt, Citation2013; Warad & Al-Debi’e, Citation2017; Yolanda & Setyawan, Citation2018).

7.4. Limitations

Subjectivity is an inherent limitation in the content approach. Likewise in this study using content analysis methods. But to minimize the limitations of inherent, we do cross-content analysis to mutually confirm the results. Thus, we hope that the level of subjectivity in the method we use can be reduced.

Besides, the existence of several university websites that are currently under construction makes this research not optimal in selecting the ideal sample. Some universities are forced to be unable to be observed because the website content cannot be accessed.

Additional information

Funding

Notes on contributors

Ihyaul Ulum

Ihyaul Ulum is an Associate Professor at Accounting Department, University of Muhammadiyah Malang (UMM), Indonesia. He currently holds the position as Director of Professional Certification Body at UMM. His main research interest include: intellectual capital, intellectual capital disclosure, intellectual capital performance, and public sector accounting.

Ratu Rahma Harviana

Ratu Rahma Harviana, Siti Zubaidah, and Ahmad Waluya Jati are scholars from Accounting Department, University of Muhammadiyah Malang. Their research interests are about good governance, transparency, and accountability in public and private entities in emerging countries.

Siti Zubaidah

Ratu Rahma Harviana, Siti Zubaidah, and Ahmad Waluya Jati are scholars from Accounting Department, University of Muhammadiyah Malang. Their research interests are about good governance, transparency, and accountability in public and private entities in emerging countries.

Ahmad Waluya Jati

Ratu Rahma Harviana, Siti Zubaidah, and Ahmad Waluya Jati are scholars from Accounting Department, University of Muhammadiyah Malang. Their research interests are about good governance, transparency, and accountability in public and private entities in emerging countries.

Related Research Data

References

- Amodu, L., Omojola, O., Okorie, N., Adeyeye, B., & Adesina, E. (2019). Potentials of Internet of Things for effective public relations activities: Are professionals ready? Cogent Business & Management, 6(1), 1683951. doi:10.1080/23311975.2019.1683951

- An, Y., Davey, H., & Eggleton, I. R. C. (2011). Towards a comprehensive theoretical framework for voluntary IC disclosure. Journal of Intellectual Capital, 12(4), 571–13. doi:10.1108/14691931111181733

- Antonella, S., & Stefania, V. (2011). The Intellectual Capital Report Within Universities: Comparing Experiences.

- April, K. A., Bosma, P., & Deglon, D. A. (2003). IC measurement and reporting: Establishing a practice in SA mining. Journal of Intellectual Capital, 4(2), 165–180. doi:10.1108/14691930310472794

- Bezhani, I. (2010). Intellectual capital reporting at UK universities. Journal of Intellectual Capital, 11(2), 179–207. doi:10.1108/14691931011039679

- Bisogno, M., Citro, F., & Tommasetti, A. (2014). Disclosure of university websites: Evidence from Italian data. Global Business and Economics Review, 16(4), 452. doi:10.1504/GBER.2014.065365

- Bontis, N. (2002). Intellectual capital disclosure in canadian corporations. McMaster University.

- Bontis, N., Richardson, S., & Keow, W. C. C. (2000). Intellectual capital and business performance in Malaysian industries. Journal of Intellectual Capital, 1(1), 85–100. doi:10.1108/14691930010324188

- Bozzolan, S., Favotto, F., & Ricceri, F. (2003). Italian annual intellectual capital disclosure: An empirical analysis. Journal of Intellectual Capital, 4(4), 543–558. doi:10.1108/14691930310504554

- Brender, N., Yzeiraj, B., & Dupuy, F. (2017). Risk and accountability: Drivers for change in network governance. The case of school restaurants governance in a Swiss city. Cogent Business & Management, 4(1), 1384636. doi:10.1080/23311975.2017.1384636

- Brennan, N. (2001). Reporting and managing intellectual capital: Evidence from Ireland. Paper presented at the International Symposium Measuring and Reporting Intellectual Capital: Experiences, Issues and Prospects, Amserdam.

- Bukh, P. N. (2003). Commentary, the relevance of intellectual capital disclosure: A paradox? Accounting, Auditing & Accountability Journal, 16(1), 49–56. doi:10.1108/09513570310464273

- Bukh, P. N., Johansen, M. R., & Mouritsen, J. (2001). Constructing intellectual capital statements. Scandinavian Journal of Management, 17, 87–108. doi:10.1016/S0956-5221(00)00034-8

- Chatterjee, B., & Hawkes, L. (2008). Does internet reporting improve the accessibility of financial information in a global world? A comparative study of New Zealand and Indian companies. Issue 4 Australasian Accounting Business and Finance Journal, 2, 93–104.

- Constantin, B. (2009). The intellectual capital of universities. Annals of the University of Oradea, Economic Science Series, 18(1), 63–70.

- Córcoles, Y. R., Peñalver, J. F. S., & Ponce, Á. T. (2011). Intellectual capital in Spanish public universities: Stakeholders’ information needs. Journal of Intellectual Capital, 12(3), 356–376. doi:10.1108/14691931111154689

- Coy, D., Fischer, M., & Gordon, T. (2001). Public accountability: A new paradigm for college and university annual reports. Critical Perspectives on Accounting, 12, 1–31. doi:10.1006/cpac.2000.0416

- Cricelli, L., Greco, M., Grimaldi, M., & Dueñas, L. P. L. (2018). Intellectual capital and university performance in emerging countries: Evidence from Colombian public universities. Journal of Intellectual Capital, 19(1), 71–95. doi:10.1108/JIC-02-2017-0037

- Dumay, J. (2016). A critical reflection on the future of intellectual capital: From reporting to disclosure. Journal of Intellectual Capital, 17(1), 168–184. doi:10.1108/JIC-08-2015-0072

- Edvinsson, L., & Malone, M. S. (1997). Intellectual capital: Realizing your company’s true value by finding its hidden brainpower. New York: Harper Collins Publishers.

- Fathony, M. M., & Ulum, I. (2018). University’characteristics, accreditation status, and intellectual capital disclosure: Evidence from Indonesia. International Journal of Economics and Research, 9(6), 23–36.

- Goh, P. C., & Lim, K. P. (2004). Disclosing intellectual capital in company annual reports: Evidence from Malaysia. Journal of Intellectual Capital, 5(3), 500–510. doi:10.1108/14691930410550426

- Guthrie, J., & Petty, R. (2000). Intellectual capital: Australian annual reporting practices. Journal of Intellectual Capital, 1(3), 241–251. doi:10.1108/14691930010350800

- Guthrie, J., Petty, R., Ferrier, F., & Wells, R. (1999). There is no accounting for intellectual capital in Australia: Review of annual reporting practices and the internal measurement of intangibles within Australian organisations. Paper presented at the International Symposium Measuring and Reporting Intellectual Capital: Experiences, Issues and Prospects, Amserdam

- Iliya Nyahas, S., Munene, J. C., Orobia, L., & Kigongo Kaawaase, T. (2017). Isomorphic influences and voluntary disclosure: The mediating role of organizational culture. Cogent Business & Management, 4(1), 1351144. doi:10.1080/23311975.2017.1351144

- Indiyati, D. (2015). Intellectual capital development in higher education in Indonesia. International Journal of Applied Business Economic Research, 13(7), 6033–6051.

- Iwamoto, H., & Suzuki, H. (2019). An empirical study on the relationship of corporate financial performance and human capital concerning corporate social responsibility: Applying SEM and Bayesian SEM. Cogent Business & Management, 6(1), 1656443. doi:10.1080/23311975.2019.1656443

- Kong, E., & Prior, D. (2007). An intellectual capital perspective of competitive advantage in nonprofit organisations. International Journal of Nonprofit and Voluntary Sector Marketing, 13(2), 119–128.

- Lee, S.-H. (2010). Using fuzzy AHP to develop intellectual capital evaluation model for assessing their performance contribution in a university.

- Leitner, K. H. (2002). Intellectual Capital Reporting for Universities: Conceptual background and application within the reorganisation of Austrian universities. Paper presented at the The Transparent Enterprise. Madrid, Spain: The Value of Intangibles.

- Leitner, K. H., Schaffhauser‐Linzatti, M., Stowasser, R., & Wagner, K. (2005). Data envelopment analysis as method for evaluating intellectual capital. Journal of Intellectual Capital, 6(4), 528–543. doi:10.1108/14691930510628807

- Lin, C.-Y.-Y., & Edvinsson, L. (2008). National intellectual capital: Comparison of the Nordic countries. Journal of Intellectual Capital, 9(4), 525–545.

- Macagnan, C. B. (2009). Voluntary disclosure of intangible resources and stock profitability. Intangible Capital, 5(1). doi:10.3926/ic.2009.v5n1.p1-32

- Middleton, I., McConnell, M., & Davidson, G. (1998). Presenting a model for the structure and content of a university World Wide Web site. Journal of Information Science, 25(3), 219–227.

- Mok, M. S., Sohn, S. Y., & Ju, Y. H. (2009). Conjoint analysis for intellectual property education.

- Mouritsen, J., Larsen, H. T., & Bukh, P. N. (2001). Intellectual capital and the ‘ capable firm’: Narrating, visualising and numbering for managing knowledge. Accounting, Organizations and Society, 26, 735–762. doi:10.1016/S0361-3682(01)00022-8

- Mouritsen, J., Thorbjørnsen, S., Bukh, P. N., & Johansen, M. R. (2004). Intellectual capital and new public management: Reintroducing enterprise. The Learning Organization, 11(4/5), 380–392. doi:10.1108/09696470410538279

- Mourtisen, J., Bukh, P. N., & Marr, B. (2005). A reporting perspective on intellectual capital. In B. Marr (Ed.), Perspectives on intellectual capital (pp.69–81). Jordan Hill, Oxford, UK: Elsevier Butterworth-Heinemann.

- Moussa, M., McMurray, A., & Muenjohn, N. (2018). Innovation in public sector organisations. Cogent Business & Management, 5(1), 1475047. doi:10.1080/23311975.2018.1475047

- Najim, N. A., Al-Naimi, M. A., & Alnaji, L. (2012). Impact of intellectual capital on realizing University goals in a sample of Jordanian Universities. European Journal of Business and Management, 4(14), 153–162.

- Ngoma, M., & Ntale, P. D. (2019). Word of mouth communication: A mediator of relationship marketing and customer loyalty. Cogent Business & Management, 6(1), 1580123. doi:10.1080/23311975.2019.1580123

- Park, H. Y., Cho, I.-H., Jung, S., & Main, D. (2015). Information and communication technology and user knowledge-driven innovation in services. Cogent Business & Management, 2(1), 1078869. doi:10.1080/23311975.2015.1078869

- Petty, R., & Guthrie, J. (2000). Intellectual capital literature review: Measurement, reporting and management. Journal of Intellectual Capital, 1(2), 155–176. doi:10.1108/14691930010348731

- Rossi, F. M., Nicolò, G., & Polcini, P. T. (2018). New trends in intellectual capital reporting Exploring online intellectual capital disclosure in Italian universities. Journal of Intellectual Capital, 19(4), 814–835.

- Sànchez, M. P., Elena, S., & Castrillo, R. (2009). Intellectual capital dynamics in universities: A reporting model. Journal of Intellectual Capital, 10(2), 307–324.

- Sangiorgi, D., & Siboni, B. (2017). The disclosure of Intellectual Capital in Italian Universities. What has been done and what should be done. Journal of Intellectual Capital, 18(2), 354–372.

- Secundo, G., Lombardi, R., & Dumay, J. (2018). Intellectual capital in education. Journal of Intellectual Capital, 19(1), 2–9. doi:10.1108/JIC-10-2017-0140

- Singh, I., & Van-der-Zahn, J. L. W. M. (2008). Determinants of intellectual capital disclosure in prospectuses of initial public offerings. Accounting and Business Research, 38(5), 409–431. doi:10.1080/00014788.2008.9665774

- Sordo, C. D., Farneti, F., Guthrie, J., Pazzi, S., & Siboni, B. (2016). Social Reports in Italian Universities: Disclosures and preparers’ perspective. Meditari Accountancy Research, 24(1), 91–110. doi:10.1108/MEDAR-09-2014-0054

- Stewart, T. A. (1997). Intellectual capital: The new wealth of organizations. New York: Doubleday.

- Suwardjono. (2014). Teori Akuntansi: Perekayasaan Pelaporan Keuangan.

- Tayles, M., Pike, R. H., & Sofian, S. (2007). Intellectual capital, management accounting practices and corporate performance. Accounting, Auditing & Accountability Journal, 20(4), 522–548. doi:10.1108/09513570710762575

- Ulum, I. (2009). Intellectual Capital; Konsep dan Kajian Empiris. Yogyakarta: PT. Graha Ilmu.

- Ulum, I. (2011). Analisis Praktek Pengungkapan Informasi Intellectual Capital dalam Laporan Tahunan Perusahaan Telekomunikasi di Indonesia. Jurnal Reviu Akuntansi Dan Keuangan (JRAK), 1(1), 49–56.

- Ulum, I. (2012). Konstruksi Komponen Intellectual Capital untuk Perguruan Tinggi di Indonesia. Jurnal Reviu Akuntansi Dan Keuangan, 2(2), Oktober 2012, 251–262.

- Ulum, I., Septerina, A. T., Prasetyo, A., Mohamed, N., & Abdullah, A. (2017). Does intellectual capital disclosure enhance organization governance? Evidence from Indonesian biggest organizations. Advanced Science Letters, 23(8), 7878–7881. doi:10.1166/asl.2017.9599

- Uyar, A., Kilic, M., & Bayyurt, N. (2013). Association between firm characteristics and corporate voluntary disclosure: Evidence from Turkish listed companies. Intangible Capital, 9(4). doi:10.3926/ic.439

- Vergauwen, P. G. M. C. (2005). Annual report IC disclosures in The Netherlands, France and Germany. Journal of Intellectual Capital, 6(1), 89–104. doi:10.1108/14691930510574681

- Warad, H. S., & Al-Debi’e, M. M. (2017). The impact of accounting conservatism and voluntary disclosure on the cost of capital of industrial companies in Jordan. Accounting and Finance Research, 6(1), 102. doi:10.5430/afr.v6n1p102

- Williams, S. M. (2001). Is a company’s intellectual capital performance and intellectual capital disclosure practices related?: Evidence from publicly listed companies from the FTSE 100. Journal of Intellectual Capital, 2(3), 192–203. doi:10.1108/14691930110399932

- Yolanda, U., & Setyawan, S. (2018). Enterprise risk management dan intellectual capital disclosure: Perspektif investor. Jurnal Reviu Akuntansi Dan Keuangan, 8(2), 83–92. doi:10.22219/jrak.v8i2.38