Abstract

This study compares the financial planning behavior of urban and rural citizens in China. Data from 399 urban citizens and 315 rural citizens were analyzed by applying the structural equation modeling (SEM) approach and the multi-group analysis (MGA) so that urban and rural citizens’ retirement behaviors were able to compare. We found that an individual’s retirement behavior is related to perceived retirement benefits, perceived health status, financial attainment capacity, and perceived parental burden. The SEM model also suggested the positive relationship between retirement behavior and individual short-term financial goals, which in turn influence long-term financial goals. Finally, the MGA indicated behavior differences between rural and urban citizens in terms of retirement benefit sufficiency and perceived parental burden.

PUBLIC INTEREST STATEMENT

Under the rapid growth of China’s floating population, several inequality issues between rural and urban areas have been presented in society. With different financial attainment capacity, urban and rural citizens may be required to manage expenditures and create retirement plans differently. This paper would let public policymakers comprehend how urban and rural citizens differ in terms of retirement behavior and how their financial goals are affected. The novelty in this paper is the formation of a structural relationship that explains and compares the retirement planning behavior of Chinese citizens residing in urban and rural areas.

1. Introduction

In the big picture, the problem of population implosion during the emergence and rise of developed countries has severe effects on retirement. Interestingly, China has previously undergone rapid economic growth, but this has recently slowed. Thirteen percent of the Chinese population is over the age of 60, three percentage points above the United Nations’ standard for severe aging. A crucial reason for the rapid decline of China’s economic growth is the labor force shortage due to the aging population; the pension shortfall is likely also a reflection of China’s aging population. The idea of a social pension is that the working population provides for the retired population (e.g., Social Security in the United States) according to the dialectical and logical design of statutory retirement age and thereby directly burdens and pressures the next generation to support the previous generation.

As the average life expectancy increased, populations have rapidly aged and extended the statutory retirement age worldwide. Ergo, a flood of pensioners appeared within a decade, straining the social security system and social safety nets. However, partial households seem to lack knowledge related to handling their financial decisions- including saving and investing during retirement life. Numerous prior empirical studies have addressed such a theme, but most are based on unilateral studies (Akgüç et al., Citation2014; Frazier, Citation2010; Giles et al., Citation2010; Shen & Williamson, Citation2010; D. Wang, Citation2006). We make a thorough inquiry into the differentiation between urban and rural citizens since the negatives effect of inadequate retirement financial planning not only affect individuals, but also their extended families and, ultimately, society.

Nevertheless, we found that the majority of research emphasizes the issue of an urban-rural cleavage in contemporary China as the most crucial, contradictory, and controversial aspect of China’s inequality. From the institutional perspective, under the rapid growth of China’s floating population, the reform of the household registration system still lags (K. W. Chan & Zhang, Citation1999). A recent research paper focused only on the financial literacy of Chinese citizens in urban areas and found that barely more than half of the citizens presented a low level of financial literacy (Niu et al., Citation2020). Another research article explores the differences between the willingness to pay for a farmland retirement project (FRP) of urban and rural residents (Yao et al., Citation2018); however, it employed a logit model that can hardly explain causal relationships among variables in more profound dimensions. Rethinking Chinese social security (pension coverage, medicare service, and provident fund) to pursue rural-urban harmonization, to rural citizens, reflects the continued unequal rights to employment and the infringement of legitimate rights and interests. However, the phenomenon could include lower-class urban citizens (i.e., under the middle-class), and therefore one cannot differentiate rural and urban citizens by how many benefits they obtained.

Due to variations in education levels, any stimulus could induce urban and rural citizens to manage expenditures as the result of making successful financial plans. The data on prosperity still inquired us to investigate. Therefore, to fill the research gaps, we probe into which financial planning behaviors are more successful between urban and rural citizens. In this paper, we use SEM modeling to analyze each factor’s relevance and interconnectedness. Ultimately, we find that retirement behavior is related to retirement benefits, health satisfaction, financial rewards, and parental satisfaction; citizens’ retirement behavior influences short-term goals and short-term goals influence the long-term goals of citizens’ retirement behavior. We also find that financial planning behavior can distinguish urban and rural citizens.

2. Literature review

This section discusses academic literature related to an individual’s retirement planning behavior and associated hypotheses, which will then be employed to develop the proposed structural model. Those literature and hypotheses were classified into different categories, for instance, retirement benefit sufficiency, perceived health status, financial attainment capacity, perceived parental burden, short-term financial goals, long-term financial goals, and rural vs. urban areas.

2.1. Retirement benefit sufficiency (RBS)

Though the issues surrounding retirement have been explored in-depth, there is wide-ranging opinion in the numerous studies about retirement behavior, from a variety of perspectives, and the results of contribution son ensuring post-retirement life and retiree well-being. One early study stated that pensioners’ health status shows noticeable improvements after annuity increases in pensions (Johnston & Lee, Citation2009); however, this finding is inconsistent with the statements that pension status does not have any critical effects on self-reported health (L. W. Li et al., Citation2016). Pensions are an essential growth factor for retirement satisfaction and increase health indexes. Nevertheless, the interval estimation of pension income is not considered and results in a lack of control over wealth (Panis, Citation2004). Though the variables of pension income and wealth are controlled, the otherness of individuals’ tendencies to choose social security investments and pensions are non-negligible. However, the treatise substantiated that self-reported pension data could identify retirement behavior, and beside the pension, incentives have a significant impact on retirement behavior (S. Chan & Stevens, Citation2008). One notable empirical study brings us to our next contemplation, which considered pensions as retirement income insurance (Bodie, Citation1989).

Regarding the provident fund in China, housing problems in massive cities in China are mainly left unsolved. In the absence of such institutions, the Chinese government has turned to savings augmentation plans, specifically the Housing Provident Fund (HPF), to help Chinese households’ transition to becoming homeowners (Tang & Coulson, Citation2017). Another study also agrees that the Chinese housing policy has moved away from a traditional welfare orientation to a monetized allocation system, which somewhat ensures residences for retirees (Burell, Citation2006). The government’s behavior is expected to be non-neutral in terms of the impacts on both welfare and inequality. The traditional public finance literature states that governments should provide public goods and services because the market either fails to do so or to supply them adequately (Samuelson, Citation1954). A government’s size and expenditure composition are expected to affect inequality, both directly and indirectly (Viegas & Ribeiro, Citation2013). While transfers, subsidies, and progressive tax systems are attempts to directly correct for inequality, expenditures on the provision of public services, such as education, health, or even R&D, may indirectly affect inequality via their effects on earning abilities (Galor & Moav, Citation2004).

Insurance is a crucial risk-sharing instrument that protects individuals from monetary losses that derive from health problems or natural catastrophes (Naruetharadhol & Ketkaew, Citation2018). Health insurance may also affect retirement benefits and behavior. A study demonstrated that health insurance has a small impact on retirement behavior (Lumsdaine et al., Citation1994). Nonetheless, we noticed that this ignored the risk of therapy costs. A dynamic programming model proved that health insurance is an essential determinant of retirement, in contrast to previous findings (Bailey, Citation2013). Moreover, they found that the age of medical insurance eligibility is equally crucial for understanding retirement behavior and the average retirement age of social security.

An understanding of the determinants of retirement behavior is critical from the points of individual well-being and policymaking. It is acknowledged in most studies that pension funds (H1a), insurance (H1b), employment benefits (H1c), and government welfare (H1d) influence retirement benefit. In Mao’s time, the government introduced the employment-based social security system, which guaranteed state employees a pension, living accommodations, and medical care after retirement, largely ensured that the urban elderly could be financially independent and guaranteed people’s retirement benefits (Sheng & Settles, Citation2006). Additionally, social insurance had a significant positive effect on rural citizens’ assessment of government performance (Huang & Gao, Citation2018). It has been well documented that differences in retirement behavior are potentially tied to the nature of pension wealth accumulation (Manchester, Citation2010). For employees, employee benefits work as a motivational tool; companies expanded the benefits as an alternative to wage increases (Dencker et al., Citation2007). The traditional public finance literature states that governments should provide public goods and services for employees to guarantee their retirement benefits (Samuelson, Citation1954).

H1a-RBS is related to pension. (RBS1)

H1b-RBS is related to insurance. (RBS2)

H1c-RBS is related to employee benefits. (RBS3)

H1d-RBS is related to government welfare. (RBS4)

2.2. Perceived health status (PHS)

Health status always plays an indispensable role in preretirement planning. Many retrospective studies have thoroughly inquired into the relationship between later-life well-being and retirement planning. An empirical study (Deaton & Paxson, Citation1998) suggested that the causality between income and health deserves further investigation. Nonetheless, Noone et al. (Citation2009) surveyed 1,008 American workers and retirees and found that higher levels of retirement satisfaction are interconnected with higher psychological health status and the importance of pre-retirement financial planning (Noone et al., Citation2009).

In another study, survey respondents with ill health showed deficient levels of happiness (Bender, Citation2012); however, several other studies utilized exogenous income shocks and sophisticated panel data models to probe into that causality and present many mixed results (Larrimore, Citation2011). Nevertheless, these previous researches did not consider the life cycle; by contemplating the life cycle, the cause-and-effect relationship among health and income could fluctuate as age increased (Cutler et al., Citation2008). With the duplicate finding, high levels of income are associated with health indexes for people aged 34–76 years but there was no significant effect for those aged 60 and above (Lindahl, Citation2005). In practice, one study found only a small positive correlation between income and health status (Meer et al., Citation2003), but other authors did not find any effect for people aged 51–61 years (Michaud & Van Soest, Citation2008) or those aged 70 and above (Adams et al., Citation2003). Further research on the impact of income on health status may be obfuscated because the >50 age group is partially driven by health shocks at prior ages and relies on the correlation between income and health to bias welfare analysis (Porr et al., Citation2006). Furthermore, due to errors associated with income, using the regularly available self-report to measure well-being would generate misconceptions of the income-health gradient (Johnston et al., Citation2009).

Importantly, to measure whether a correlation exists between health status and retirement behavior, one can use subjective well-being since it ordinarily used in well-being research and seems to be used as a substitute for happiness. In general, retirement satisfaction is considered a dependent variable and therefore is an attempt to estimate happiness in the analysis (Xiao et al., Citation2014). Many surveys found that most retirees have high satisfaction on a mental level, and yet the degree of that satisfaction fluctuates substantially because of multiple factors. Two factors are corroborated that have a significant effect on happiness: individuals’ sense of control over their lives and social relationships (Calvo et al., Citation2009; Gallo et al., Citation2006). Individuals’ sense of control over their lives was studied with people at the work-retirement transition, and that study showed that retirees who voluntarily retire from their jobs are happier than those who are reluctant to retire. The value of social relationships is embodied by the fact that people who made many acquaintances of other individuals are happier than those who had fewer such relationships during later life. In addition, well-being theory posits that positive psychological attributes are positively related to retirement satisfaction, with the precondition that happiness and well-being are the ideal outcomes of positive psychology (Seligman, Citation2012).

According to the literature, physical health (H2a) and mental health (H2b) are significant for employees’ health, which will directly influence their retirement behavior. In retirement, as seen through positive psychology, happiness is related to the concept of successful aging (Adams et al., Citation2003). The changes in lifestyle for people to be retired are devalued by society. This can occur when retirees have placed their work in the central position of their lives compared to other aspects, turning the end of working into a negative experience (Gallo et al., Citation2006). Retirement has been seen as a significant transition in adults’ lives, and if they do not plan for it early, this transition can traumatize their health (M. Wang, Citation2013). The daily routine of individuals requires a basic plan to obtain financial balance, avoid habits or lifestyles that compromise their health, and promote physical, emotional, and social integrity, causing, to some extent, the happiness status (Heybroek et al., Citation2015).

H2a-PHS is related to physical health. (PHS1)

H2b-PHS is related to mental health. (PHS2)

2.3. Financial attainment capacity (FAC)

To probe into retiree behavior, an unequivocal income resource is postulated. People with higher incomes are more hesitant and frustrated to become a social burden after retirement (Ketkaew, Van Wouwe et al., Citation2019). A prior study stated that retirement income satisfaction could be used as a controlled variable, based on the finding that perceptions of financial security have a positive relationship with retirement status (Talaga & Beehr, Citation1995). However, in another study, retirement income satisfaction was composed of three sources: employer-sponsored retirement accounts, social security, and personal investments and saving (Fisher et al., Citation2012). Another study defined an individual’s earnings from employment and investment as one’s financial attainment capacity (Ketkaew, Wouwe, Vichitthammaros et al., Citation2019)

Age, as an element, clearly has something to do with the importance of employee benefits, especially retirement benefits (Ketkaew et al., Citation2019). A study analyzed the effects of age on the amounts of savings in different financial retirement plans and concluded that the older age group had higher numbers of savings deposits in their thrift account (DeVaney & Zhang, Citation2001). Similarly, other studies have found that age and life expectancy were negatively correlated with retirement income satisfaction (Hsu, Citation2013; Hsu & Leech, Citation2010). In different circumstances, a strong correlation was found between planned retirement age, income, and saving regularly (Hsu, Citation2016). On the other hand, a pension provides a significant percentage of income for many retirees. Likewise, Bender and Jivan (Citation2005) intensified the standpoint that having a guaranteed pension income has a statistically significant impact on retirement satisfaction (Bender & Jivan, Citation2005). Panis (Citation2004) initially intended to measure the role of annuities and wealth with the 2000 HRS on retirement satisfaction, even though the determinants are limited, and the study does not control for other elements of the source of post-retirement income (Panis, Citation2004). Panis still had two findings: annuities from pensions significantly increase satisfaction and most retirees reported higher levels of retirement satisfaction when they had guaranteed income streams, as measured by data from defined benefit pension plans (DB plans). Sundali et al. (Citation2008) highlighted the significance of annuitized income streams and how life satisfaction would be enhanced if annuitized income streams existed (Sundali et al., Citation2008).

On the one hand, a prior study indicated that an overwhelming majority of respondents had basic financial knowledge, and roughly half of them were somewhat dramatically educated at an advanced level (BooN et al., Citation2011). However, we notice that the author solicited primary data only from a city in Malaysia. Such a geographically-confined study has limited persuasiveness, particularly for studying differences between rural and urban citizens. We should note that the results confirm previous arguments (Hilgert et al., Citation2003) that many do not possess sound with financial knowledge (regarding, e.g., the stock market and compound interest).

Employees have enough investment knowledge (H3a) and financial assets, e.g., investment/saving (H3b), which are essential for an individual’s financial attainment capacity (Ketkaew, Wouwe, Vichitthammaros et al., Citation2019). Based on previous work, as expected, the effect of investment knowledge on the belief in one’s future capability of orchestrating a plan to achieve investment goals was mediated by confidence (Forbes & Kara, Citation2010). Workers seek out formal planning methods to successfully plan retirements, such as retirement calculators, retirement seminars, and financial experts (Nicholas et al., Citation2011). In recent years, employers have increasingly transitioned from defined benefit pension plans, with payouts based on pay level and years of service, to retirement savings plans that require individuals to make complex, long-term investment decisions. However, a paper observed that most retired people did not have the opportunity to save enough for their old age due to having fewer financial instruments available to them (Njuguna, Citation2012). Though it is never too late to begin sound financial planning, one can avoid unnecessary difficulties in financial planning by starting to plan early.

H3a-FAC is related to investment knowledge. (FAC1)

H3b-FAC is related to financial assets (investment/saving). (FAC2)

2.4. Perceived Parental Burden (PPB)

Concerning parental status, urban China shows a representative environment where grown children are under compulsion to support their parents under failed pension systems. The amount of transfer is associated with the recipient’s level of income (Cai et al., Citation2006). A study provided a descriptive discussion of old-age support, whereas they did not premeditate the crucial intra-family transfers for old-age support in urban China (Saunders et al., Citation2003). Based on the affection for ancient Chinese religious thought, Confucian ideals instruct children to abide and serve parents. One Confucian teaching, filial piety, has been cited as a determinant that shaped traditional obligation in East Asia and became the dominating concept that regulates the connection between children and their parents (Goldin, Citation2014). Nonetheless, a research paper suggested that stimulating support for the elderly is not significantly related to filial piety in rural China (Liu et al., Citation2010). Moreover, it also emphasized that non-resident children frequently live near retired parents and provide non-financial condolences and assistance.

Retirees who have children often self-assess as individuals who feel lonely (often with a sense of humor), thereby further affecting their health status. In contrast, these characteristics are not embodied in those who lack children (Brajković et al., Citation2011). After the implementation of the two-child policy in 2011, each household probably considered the need more safety in case the eldest son had an accident. The one-child policy explicitly forced many households to give up on having children (Tsui, Citation1989); prior studies have examined the effects of the one-child policy in China (Ebenstein, Citation2010; Hesketh et al., Citation2005). Unsurprisingly, this would cause issues in data diversification regarding the ages and number of children in China today. Our sample was not restricted to respondents who had children while the one-child policy was in effect. Lastly, housing assets were an intermediary to help elderly retirees to negotiate with their children for support, shifting from dependence on their children to reduced dependence and even to having the financial capacity to support their children if the value of the housing assets grew rapidly (B. Li & Shin, Citation2013).

In daily life, having a child puts pressure on parents regarding child living (H4a) and education (H4b). Older people, as heads of households, owned or controlled the productive resources upon which the younger people were dependent, and they had broader social connections with kinship support (Sheng & Settles, Citation2006). The growth in living standards, especially in improved housing conditions, made older and younger generations independent from each other (Sheng & Settles, Citation2006). The current situation is that more Chinese are working in the private sector, but private companies have been reluctant to take on more responsibility, and therefore the past retirement resources are no longer a dependable structure for the elderly of today or their adult children (Sheng & Settles, Citation2006).

H4a-PPB is related to financially supporting a child’s living. (PPB1)

H4b-PPB is related to financially supporting a child’s education. (PPB2)

2.5. Short-term financial goals (SFG)

Retirement planning is a process that consists of a series of cognitive stages and corresponding retirement scheme behavior. Before retirement, to better adapt to retirement and guarantee the quality of post-retirement life, individuals should save money (from the economic facet), develop leisure activities suitable for retirement well-being (from the lifestyle sphere), and prepare for retirement in advance (from the psychological dimension) (Muratore & Earl, Citation2010). One paper (Petkoska & Earl, Citation2009) notes that research papers concerning retirement planning are still focused on economics.

Moreover, previously, numerous studies (Ebenstein, Citation2010; Hesketh et al., Citation2005) have confirmed the fact that retirement planning can trigger positive outcomes, including good health, higher life satisfaction, and higher subjective happiness. On the other hand, specific goals in retirement planning seem to be a determinant to measure life satisfaction in post-retirement life (Hershey et al., Citation2002).

Recent studies emphasize that a real sense of the first step into retirement is needed to consider the retirement transition (Griffin et al., Citation2012). Adjustment outcomes of the retiree are associated with their work roles and how retirees change mentally and psychologically; some occur in retirees who are not ready to retire from those familiar surroundings (Barnett et al., Citation2012). Hence, as the leisure time increased, the positive effect of retirement is probably reversed; redefining the retiree’s role is crucial during the period of transition (Pinquart & Schindler, Citation2009). The paper (Noone et al., Citation2009) also confirmed these views and found that the individual who prepares for retirement financially and psychologically has a higher self-rated health level in later life.

It is acknowledged in most literature that short-term goals will be influenced by travel expenses (H5a), daily expenses (H5b), and saving accounts (H5c), annual vacation (H5d), and ability to track financial transactions (H5e). Short-term goals are essential for financial planning, and having a specific goal will help one to execute a financial plan. Before retirement, to better adapt to retirement, people should save money to guarantee the quality of post-retirement life and develop leisure activities suitable for retirement well-being, such as travel and daily activities (Muratore & Earl, Citation2010). If the short-term planning for retirement is inadequate, that will affect individuals, their extended families, and their homes, eventually producing a negative impact on the entire society. Other research has noted that retirement expenditures are not necessarily influenced by inflation on average, or by some otherwise static percentage, but that the actual “spending cure” of retired households changes by total consumption (Campbell & Weinberg, Citation2015). For many workers, whether they can have a comfortable retirement may depend on the savings decisions they make now; thus, a specific and successful goal will influence people’s financial planning. As people age, failing to save today can have very real consequences, i.e., reduces the comforts they get to enjoy during retirement and their ability to cope with health and financial shocks

H5a-SFG is related to travel expenses. (SFG1)

H5b-SFG is related to daily/weekly expenses. (SFG2)

H5c-SFG is related to setting up a savings account. (SFG3)

H5d-SFG is related to an annual vacation. (SFG4)

H5e-SFG is related to the ability to keep on track of financial transactions. (SFG5)

2.6. Long-term financial goals (LFG)

A study pointed out that Chinese citizens could not rely on China’s pension system to guarantee their later life. Hence, people have shifted more attention toward commodities that retain value (Pozen, Citation2013). Foremost, individual investment properties became popular to ensure retired life instead of paying for a monthly pension before retirement (Wu, Citation2013). Secondly, another study stated that intergenerational housing support is a universal phenomenon (B. Li & Shin, Citation2013). Nevertheless, in Asian cultures, parents generally support children through housing purchases or transfer their property and wealth unconditionally, which could be affected by filial piety as a result of the substantial obligation for parents (Helderman & Mulder, Citation2007).

On the other hand, the proportion and level of debt of people over 55 are showing an upward trend; an increasing number of Americans, both pre- and post-retirement, is now fighting with debt (Marshall, Citation2011). Furthermore, older Americans are burdened with more mortgage debts after retirement and meanwhile have accumulated less home equity and tackle paying their monthly mortgages with difficulty, which threatens retirement security (Seay et al., Citation2015).

Lacking financial knowledge has been substantiated as a universal phenomenon on a global scale and is gradually exposed in developed economies, for instance, the United States (Lusardi & Mitchell, Citation2011) and the United Kingdom (Ironfield-Smith et al., Citation2005). Learning and training are co-constitutive in playing a very significant role for individuals in developing behaviors and skills required to accomplish their financial goals (Phonthanukitithaworn et al., Citation2017). Those individuals who lack financial literacy no longer make informed financial planning decisions and do not participate in investing (Lusardi & Mitchell, Citation2011). Besides, the study found that educational level and ethnic status are significantly associated with stock ownership; however, another study illustrated that people with higher education have more open attitudes toward borrowing (Borden et al., Citation2008). Overall, such an adverse factor has increasingly evolved into a determinant that influences retirees’ financial behavior, especially financial planning. Due to the essential bilateral influence of filial piety on a household, borrowing generates significant tress and pressure on retirees, whether they are ready to retire or not.

In the long term, purchasing a house will influence long-term goals (H6a). After retirement, the Association of Retirement Housing Managers (ARHM) estimates that there to be some 105,000 leasehold retirement homes in the UK, that is, homes to purchase rather than rent (OFT investigation into retirement home transfer fee terms, Housing Care, Citation2013); more people will spend money purchasing houses, which leads to capital decreases, thus influencing their long-term goals. In our opinion, forming a family will influence long-term financial goals (H6b): forming a family leads to increased family expenses and, therefore, less money to achieve long-term goals. Finally, debt payment will also influence long-term goals (H6c). For retired people, they are not saving enough, which can have serious financial consequences for their long-term financial well-being (Montgomery et al., Citation2017). Compared to previous generations, they will face challenges which paying off debt and debt ranks as one of their top four retirement-planning challenges; before retirement, they are more focused on paying off debt as a prerequisite for retirement and as a result, they expect more mortgage debt to be carried into their retirement years, which will influence their long-term goals (Munnell et al., Citation2018).

H6a-LFG is related to readiness to own a house/property. (LFG1)

H6b-LFG is related to readiness to take care of a family financially. (LFG2)

H6c-LFG is related to readiness to pay back a long-term debt. (LFG3)h

2.7. Urban and rural

Based on the different contexts of their financial needs, financial needs, and financial plans differ for rural and urban citizens (Kumar & Mukhopadhyay, Citation2013). Among others, people’s knowledge, skills, fluid and crystallized intelligence, and psychological biases would likely influence their ability to execute a financial plan and save money (Resende & Zeidan, Citation2015).

H7-Urban citizens and rural citizens’ retirement behavior is distinguishable.

3. Research model and hypotheses

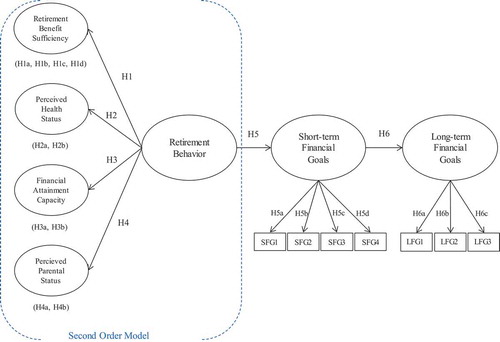

Based on the literature, a structural model is proposed (see Figure ). The retirement behavior construct was presented using the concept of Second-order Structural Equation Modeling (Gerbing et al., Citation1994). In the second-order part, the model proposes that retirement behavior is directly associated with retirement benefits sufficiency (RBS), perceived health status (PHS), financial attainment capacity (FAC), and perceived parental status(PPS), making retirement behavior (RB) a four-factor construct. The model also proposes that citizens’ retirement behavior will influence citizens’ short-term financial goals; therefore, short-term financial goals are a dependent construct of retirement behavior. Similarly, short-term financial goals are associated with long-term financial goals; therefore, long-term goals are a dependent construct of short-term financial goals. Derivation of the said relationships will be described in the next section.

Figure 1. Proposed model

4. Method

4.1. Survey items

The purpose of the survey was to compare urban and rural citizens’ retirement behavior; a questionnaire was developed for this purpose. The questionnaire included six items (see the Annexure 1): retirement benefit sufficiency (RBS), perceived health status (PHS), financial attainment capacity (FAC), perceived parental burden (PPB), short-term financial goals (SFG), and long-term financial goals (LFG). A 5-point Likert-type scale ranging from 1 (lowest) to 5 (highest) was used. The questionnaire was developed in English and translated into Chinese to collect data from Chinese people.

4.2. Sampling and data collection

The research used the independent control quota sampling method to collect data. Three representative cities in China were chosen: a new first-tier city (Chengdu), an old industrial city (Shenyang), and a second-tier city (Nanning). Chengdu includes important high-tech industrial bases, commercial and trade logistics centers, and comprehensive transportation hubs, making it a crucial central city in the western region. Shenyang is an old industrial city with industrial production as its primary function, and it was a central city in northeast China with economic, financial, cultural, transportation, information, and business centers. Nanning’s economic, financial, and transportation are not better than those of a first-tier city, but it functions as a representative second-tier city.

The research involved quota sampling according to urban and rural areas. In Chengdu, there were about 14,353,000 people, 8,512,000 urban people and 5,841,000 rural people. In Shenyang, there were about 12,007,200 people, 6,732,000 urban people and 5,275,200 rural people. In Nanning, there were about 8,351,400 people, 4,208,200 urban people and 4,143,200 rural people. Therefore, in Chengdu, Shenyang, and Nanning, the total population was 34,711,600, the total urban population was 19,452,200, and the total rural population was 15,259,400. Therefore, the calculated ratio between urban and rural people was 1.27:1. This proportion was applied based on the stratified sampling approach using geographical regions as a stratum.

Based on the stratified sampling approach, we expected to collect 700 respondents from 392 urban citizens and 308 rural citizens. At the end of the survey, the research team collected 750 questionnaires, which were more than enough. We used the self-filling method to collect questionnaires. Of the 750 respondents, 238 questionnaires were distributed electronically, and 512 were surveyed manually. Finally, we received 714 responded questionnaires; 227 from online questionnaires and 487 from issued questionnaires. According to the 1.27:1 (urban: rural) ratio, we ultimately came up with 399 urban citizens and 315 rural citizens for a total of 714 questionnaires. A response bias test to validate perceptual indifferences between the respondents answering online and drop-off questionnaires was performed using the measurement invariance approach (Steenkamp & Baumgartner, Citation1998) after an examination of the measurement model (see Annexure 2). The results from the measurement invariance test found that the respondents from both groups perceived the questions in this questionnaire the same way because CFI, IFI, and RMSEA of both unconstrained and measurement weights models did not pass the thresholds of >0.90, >0.90 and <0.10, respectively. Therefore, the measurement invariance between the online and offline respondents holds, relaxing the response bias issue between two groups of respondents.

Respondents’ demographics were expressed in Table below.

Table 1. The descriptive statistics of demographic variables

4.3. Measurement of variables

A self-administered survey is one where respondents read the questionnaire, record their responses themselves, and do not require the use of an interview to administer the survey. Self-administered surveys are likely to cause a biasing effect on the measurement of constructs (Podsakoff et al., Citation2012). Therefore, before testing, we used 200 responses to conduct pre-tests by using SEM to measure whether the result is feasible for the constructs, the constructs are accurately assessed by the study, and it is suitable to use the framework in future tests. Our SEM pre-test with 200 data points revealed that the framework was feasible and could be used on a future test.

4.4. Data analysis

The study’s data analysis was based on the SEM approach. SEM encompasses such diverse statistical techniques as path analysis, confirmatory factor analysis, causal modeling with latent variables, and even analysis of variance and multiple linear regression. In this research, the SPSS-AMOS software was employed for statistical analysis.

The SEM approach was applied to examine the model’s estimation in three steps: 1) to validate the outer (CFA) model in order to measure the relationship between each indicator and its variable, whether it is truthful and reliable; 2) to examine the inner structural model in order to measure whether the full structure is reliable and that the relationship between dependent variables and independent variables is like the full structure of Table ; 3) to conduct multi-group analysis (MGA) to compare the results between urban and rural citizens.

In the multi-group analysis (MGA) of the study, firstly, the evaluation of the measurement model focused on indicating the study’s reliability, convergent validity, and discriminant validity. Secondly, the structural model was assessed based on heuristic criteria that are determined by the model’s predictive capabilities. The most critical metrics present the significance of the path coefficients. We followed Hair et al.’s (Citation2006) recommendation to examine and evaluate the full structure of the study (Hair et al., Citation2006). Third, the full structure is examined separately for the groups of urban citizens and rural citizens by using the MGA approach to test hypotheses, i.e., identify and compare the differences between urban and rural financial planning behaviors. MGA was examined by restricting measurement residuals in three steps: 1) the configural invariance assessment (unconstrained model); 2) the metric invariant assessment (equal factor loading model); 3) the scalar invariance assessment (equal intercepts model). This approach is used to measure differences between the path’s coefficients of two groups, that is, reliability. Thus, the acceptability of the measurement models and measurement invariances were established before exploring any structural variances between the models of urban citizens and rural citizens.

Bentler and Chou (Citation1987) noted that researchers might go as low as five cases per parameter estimate in SEM analysis, but only if the data are perfectly well-behaved, i.e., normally distributed, no missing data or outlying cases (Bentler & Chou, Citation1987). Typically, measured variables have at least one path coefficient associated with another variable in the analysis, as well as a residual term or variance estimate (A Reasonable Sample Size. March 2015). For this class of model with two to four factors, the researcher should plan on collecting at least 100 cases; using smaller samples will lead to convergence failures (the software cannot reach a satisfactory solution), improper solutions (including negative error variance estimates for the measured variables), and lowered accuracy of parameter estimates and, in particular, standard errors because SEM program standard errors are computed under the assumption of large sample sizes (Hair et al., Citation2006).

5. Results and discussion

5.1. Measurement model assessment

CFA (confirmatory factor analysis) starts from the dependence relationship within the correlation matrix of research indicators and refers to a multivariate statistical analysis method that combines some overlapping information and intricate relationships into a few unrelated comprehensive factors. CFA helps us understand the relationship(s) between indicators.

The requirement for SEM is acceptable model fit, which is indicated by a CFI and NFI value of 0.90 or higher (Suhr, Citationn.d.), AGFI and GFI values of 0.7 or higher (Abedi et al., Citation2015). Also, for SEM, sample sizes above 200 as considered large; we had 713 samples in this analysis, and therefore the CMIN value higher than three is accepted (Hair et al., Citation2006).

We also require the AVEs and the standardized estimates, which should be 0.7 or above, and the CR (composite reliability) should be 0.5 or above (Alarcón et al., Citation2015).

The results showed that the structural model fits the data well, suggesting that the data are truthful (df = 110, GFI = 0.856, NFI = 0.929, CFI = 0.937, RMSEA = 0.111). All the hypotheses were tested by examining the path significance.

As we can see in Table , all the standardized estimates are higher than 0.7, and especially those of RBS2, RBS4, PPB1, PPB2, SFG1, SFG4, SFG5, and LFG3 are above 0.9, which showed that those eight indicators have high reliability. The AVE values are all above 0.5, which means that all the indicators in this measurement model satisfactorily passed convergent validity criteria.

Table 2. Confirmatory factor analysis of the measurement items

As we can find in Table , the AVE met the requirements, confirming that all the indicators are good enough and are different from one another, satisfying discriminant validity criteria.

Table 3. The AVE and squared correlation estimates

5.2. Structural model and hypothesis testing

After achieving the requirements for reliability and the dimensionality of the measurement scales, we proceeded to the SEM analysis.

Viewing with caution the significance of the global contrast, which is sensitive to sample size (Hair et al., Citation2006), according to Table the goodness of fit was acceptable (df = 110; RMSEA = 0.128; GFI = 0.796; AGFI = 0.73) although RMSEA of 0.128 is slightly higher than the threshold of < 0.10 (Browne & Cudeck, Citation1993). Six variables or dimensions reached the level of reliability and internal consistency.

Concerning the estimated coefficients of causal relationships (See Table ), there are significant effects from the constructs. Perceived health status (0.965) and financial attainment capacity (0.93) provide potent explanations for retirement behavior, and long-term financial goals (0.955) were strongly influenced by short-term financial goals. Also, we can find that retirement benefit sufficiency is slightly weaker than perceived health status and financial attainment capacity as an explanation. Similarly, perceived parental burden significantly influences (0.768) retirement behavior.

For the retirement benefit part, insurance is the most critical indicator for a retirement benefit, but the other three indicators are as important as well since their numbers are almost 0.9 or above 0.9. These results show that the result is accepted for the first group of hypotheses, which are H1a to H1d. These results lead to the idea that self-reported pension data could help to identify retirement behavior and that incentives have a significant impact on retirement behavior (S. Chan & Stevens, Citation2008).

Health status has two support indicators, physical health and mental health. Both coefficients were higher than 0.8, which also means that they have strong influences on health status. These results show that we can also accept the second group hypotheses, H2a and H2b. This led us to understand what Noone et al. (Citation2009) found in their research, i.e., that a higher level of retirement satisfaction is interconnected with higher psychological health status and the importance of financial planning before retirement (Noone et al., Citation2009).

Financial attainment capacity has strong supporters as well; the coefficients for investment/saving and investment knowledge are both above 0.85. This shows that the third group of hypotheses (H3a and H3b) can be accepted. It also led us to understand that, as reported previously (Fisher et al., Citation2012), employer-sponsored retirement accounts, social security, and personal investments and savings are essential for retirement behavior.

Perceived parental burden also has two indicators to support it: Child’s living expense (0.932) and child’s educational expense (0.892). As before, these two indicators indicate that the hypotheses in group 4, H4a and H4b, can be accepted. Considered with the affection of ancient Chinese religious thought, Confucian ideals instruct children to abide and serve parents and vice versa, and thus filial piety has been cited as a determinant that shaped traditional obligations in East Asia as well as the dominating concept that regulates the connection between children and their parents (Miller et al., Citation1997). This result shows that traditional Chinese culture still heavily influences Chinese people today.

The short-term financial goal variable has five indicators to support it, and three of them have coefficients above 0.9, and the other two are higher than 0.85. These results show that group 5 of hypotheses, from H5a to H5e, can also be accepted. For the long-term financial goal variable, the indicators are purchasing a house (0.836), forming a family (0.888), and debt payment (0.924), leading us to accept the group 6 hypotheses, from H6a to H6c. Previous studies (Ebenstein, Citation2010; Hesketh et al., Citation2005) have confirmed that retirement planning can trigger positive outcomes, including good health, higher life satisfaction, and higher subjective happiness. On the other hand, achieving specific goals in retirement planning seem to be a determinant to measure life satisfaction in post-retirement life (Hershey et al., Citation2002).

The model examines every pair of models in which one model of the pair can be obtained by constraining the parameters of the other (Her et al., Citation2019). In order to understand the different financial behaviors between rural and urban citizens (H5), we estimated the MGA. To start, we began with an examination of measurement invariance following these steps: (a) establishing configural invariance (unconstrained model); (b) establishing metric invariance (equal factor loadings); and (c) establishing scalar invariance (equal intercepts). Table illustrates the establishment of full measurement invariance, where all the three models (unconstrained, equal factor loadings, and equal intercepts) were satisfied. Hence, both urban and rural Chinese citizens perceived questions in the assigned questionnaire the same way, allowing a comparison between the two groups in a further step.

Table 4. The goodness of fit for structural analysis

Table 5. Structural model of the causal relationships

Table 6. Differences between urban and rural citizens

Table shows the differences between the retirement behavior of urban and rural people resulted from the MGA. From the measurement weights, the P-value is less than 0.01, indicating statistically significant relationships among variables.

Table 7. Estimation of the multi-group analysis

According to Table , the most considerable differences between urban and rural areas were demonstrated by H1 and H4, the relationship between retirement behavior and retirement benefit sufficiency (RBS), and between retirement behavior and perceived health status (PHS) respectively. This implies that people in urban areas perceive that retirement benefits are more influential to their retirement lives than people in rural areas do. This is because urban people do receive better retirement benefits from either the government or employees than rural people. On the other hand, people in rural areas perceive more parental burdens than those living in cities due to lower ability to earn income to afford family expenditure such as child education and day-to-day living. As a result, those who sense parental burden will have to put more significant efforts for successful retirement lives.

We consider that Chinese rural areas have been highly developed from 1998 until now and that 2,817,100,000 rural citizens moved to urban areas for work. The total workforce is 7,850,000,000 and the total rural area is 47.7%. The total rural area has grown by around 5% every year since 2007 (China Labor Force Total, Citationn.d.). In 2017, the average income for Chinese rural people who migrate to work in the cities was 6,500 USD (China (Citationn.d.)), whereas the average income for Chinese urban workers was $12,475.12 (Income and Living Standards across China, (Citationn.d.)), i.e., the income of an urban worker is, on average, twice that of a migrant worker’s income. This strongly indicates why urban and rural citizens incur differences in perceived retirement benefits and perceived parental burden. Also, urban people have higher education levels and know more about investments, which is another reason for the differences that we observed.

6. Conclusion

The study discusses the retirement behavior of urban and rural citizens. In the study, we applied SEM and MGA to examine and analyze the consequences. We focused on explaining the retirement behavior of urban and rural citizens, identifying the factors that affect the retirement behavior of urban and rural citizens, and identifying the differences in retirement behavior between urban and rural citizens. In the course of analysis, we found that retirement is a phase of the lifecycle; retirement behavior is related by retirement benefit sufficiency, perceived health status, financial attainment capacity, perceived parental burden, short-term financial goals, and long-term financial goals, which positively influence retirement behavior. After we compared urban and rural citizens’ financial planning behavior, we found that their retirement behavior is distinguishable in terms of retirement benefits and parental burden in that the urban people demonstrated better retirement benefits and the parental burden than the rural due to the better level of income. In contemporary China, the most crucial, contradictory, and controversial aspect of China’s inequality is the issue of the urban-rural cleavage, which leads to different behavior among urban and rural citizens.

However, in recent fiscal years, the flourishing worldwide economic development and objective of embracing free trade has intensified inflation, exchange rates, and other economic factors that will influence the retirement and financial planning behavior of urban and rural citizens. As countries emerge and rise as developed countries, they will face the population aging problem, which leads to the absence of labor and, thus, a rapid decline of economic growth. Nowadays, the population aging problem has made the economic situation even more severe, which may alter citizens’ financial behavior, and, psychologically, the bandwagon effect may lead to retirement and financial planning behavior changes. Therefore, we are extending our analysis in this direction for future research arena.

Acknowledgements

The authors would like to thank the following research assistants: Miss Ziwen Huang, Miss Haodi Wang, and Mr. Ziyang Zhang.

Additional information

Funding

Notes on contributors

Chavis Ketkaew

Chavis Ketkaew is an assistant professor of management at the International College, Khon Kaen University, Thailand. He is the first author of this research project. His research interests include behavioral economics, consumer research, market research, and business models.

Chutima Sukitprapanon

Chutima Sukitprapanon is a lecturer in Business Administration Division, International College, Khon Kaen University, Thailand. Her research interests include e-Marketing, e-Business, e-Commerce, Management Information Systems, Enterprise Resource Planning.

Phaninee Naruetharadhol

Phaninee Naruetharadhol is an assistant professor of management at the International College, Khon Kaen University, Thailand. She is the principal investigator and plays a corresponding role in this research project. Her research interests involve organizational behavior, human resources management, financial planning, and innovation management.

References

- Abedi, G., Rostami, F., & Nadi, A. (2015). Analyzing the dimensions of the quality of life in Hepatitis B patients using confirmatory factor analysis. Global Journal of Health Science, 7(7), 22. https://doi.org/10.5539/gjhs.v7n7p22

- Adams, P., Hurd, M. D., McFadden, D., Merrill, A., & Ribeiro, T. (2003). Healthy, wealthy, and wise? Tests for direct causal paths between health and socioeconomic status. Journal of Econometrics, 112(1), 3–23.https://doi.org/10.1016/S0304-4076(02)00145-8

- Akgüç, M., Giulietti, C., & Zimmermann, K. F. (2014). The RUMiC longitudinal survey: Fostering research on labor markets in China. IZA Journal of Labor & Development, 3(1), 5. doi:10.1186/2193-9020-3-5

- Alarcón, D., Sánchez, J. A., & De Olavide, U. (2015). Assessing convergent and discriminant validity in the ADHD-R IV rating scale: User-written commands for Average Variance Extracted (AVE), Composite Reliability (CR), and Heterotrait-Monotrait ratio of correlations (HTMT). Spanish STATA Meeting (pp. 1–39).

- Bailey, J. (2013). Who pays for obesity? Evidence from health insurance benefit mandates. Economics Letters, 121(2), 287–289. https://doi.org/10.1016/j.econlet.2013.08.029

- Barnett, I., Guell, C., & Ogilvie, D. (2012). The experience of physical activity and the transition to retirement: A systematic review and integrative synthesis of qualitative and quantitative evidence. International Journal of Behavioral Nutrition and Physical Activity, 9(1), 97. https://doi.org/10.1186/1479-5868-9-97

- Bender, K. A. (2012). An analysis of well-being in retirement: The role of pensions, health, and ‘voluntariness’ of retirement. The Journal of Socio-economics, 41(4), 424–433. https://doi.org/10.1016/j.socec.2011.05.010

- Bender, K. A., & Jivan, N. A. (2005). What makes retirees happy? (Vol. 28). Center for Retirement Research at Boston College.

- Bentler, P. M., & Chou, C.-P. (1987). Practical issues in structural modeling. Sociological Methods & Research, 16(1), 78–117. https://doi.org/10.1177/0049124187016001004

- Bodie, Z. (1989). Pensions as retirement income insurance. National Bureau of Economic Research.

- BooN, T. H., Yee, H. S., & Ting, H. W. (2011). Financial literacy and personal financial planning in Klang Valley, Malaysia. International Journal of Economics and Management, 5(1), 149–168. http://0104.nccdn.net/1_5/1c2/228/3bd/Financial_Literacy_and_Personal_Financial_Planning_Malaysia.pdf

- Borden, L. M., Lee, S.-A., Serido, J., & Collins, D. (2008). Changing college students’ financial knowledge, attitudes, and behavior through seminar participation. Journal of Family and Economic Issues, 29(1), 23–40. https://doi.org/10.1007/s10834-007-9087-2

- Brajković, L., Gregurek, R., Kušević, Z., Ratković, A. S., Braš, M., & Dordević, V. (2011). Life satisfaction in persons of the third age after retirement. Collegium Antropologicum, 35(3), 665–671. Retrieved from Scopus.

- Browne, M. W., & Cudeck, R. (1993). Alternative ways of assessing model fit. In K. A. Bollen & J. S. Long (Eds.), Testing structural equation models (pp. 136–162). SAGE

- Burell, M. (2006). China’s housing provident fund: Its success and limitations. Housing Finance International, 20(3), 38.

- Cai, F., Giles, J., & Meng, X. (2006). How well do children ensure parents against low retirement income? An analysis using survey data from urban China. Journal of Public Economics, 90(12), 2229–2255. https://doi.org/10.1016/j.jpubeco.2006.03.004

- Calvo, E., Haverstick, K., & Sass, S. A. (2009). Gradual retirement, sense of control, and retirees’ happiness. Research on Aging, 31(1), 112–135. https://doi.org/10.1177/0164027508324704

- Campbell, D., & Weinberg, J. A. (2015). Are we saving enough? Households and retirement. Economic Quarterly, Q2, 99–123. http://doi.org/10.21144/eq1010202

- Chan, K. W., & Zhang, L. (1999). The hukou system and rural-urban migration in China: Processes and changes. The China Quarterly, 160, 818–855. https://doi.org/10.1017/S0305741000001351

- Chan, S., & Stevens, A. H. (2008). What you don’t know can’t help you: Pension knowledge and retirement decision-making. The Review of Economics and Statistics, 90(2), 253–266. https://doi.org/10.1162/rest.90.2.253

- China Labor Force Total. (n.d.). Retrieved November 12, 2018, Trading Economics, from https://tradingeconomics.com/china/labor-force-total-wb-data.html

- China: Migrant workers average monthly income 2017 | Statistic. (n.d.). Retrieved November 12, 2018, from Statista website https://www.statista.com/statistics/306686/china-monthly-income-of-migrant-workers/

- Cutler, D. M., Lleras-Muney, A., & Vogl, T. (2008). Socioeconomic status and health: Dimensions and mechanisms. National Bureau of Economic Research.

- Deaton, A. S., & Paxson, C. H. (1998). Aging and inequality in income and health. The American Economic Review, 88(2), 248–253. https://www.jstor.org/stable/116928.

- Dencker, J. C., Joshi, A., & Martocchio, J. J. (2007). Employee benefits as a context for intergenerational conflict. Human Resource Management Review, 17(2), 208–220. https://doi.org/10.1016/j.hrmr.2007.04.002

- DeVaney, S. A., & Zhang, T. C. (2001). A cohort analysis of the amount in defined contribution and individual retirement accounts. Journal of Financial Counseling and Planning, 12(1), 89. https://www.researchgate.net/profile/Sharon_Devaney/publication/228735215_A_cohort_analysis_of_the_amount_in_defined_contribution_and_Individual_Retirement_Accounts/links/09e41509c0a7439301000000.pdf

- Ebenstein, A. (2010). The “missing girls” of China and the unintended consequences of the one-child policy. Journal of Human Resources, 45(1), 87–115. https://doi.org/10.1353/jhr.2010.0003

- Fisher, J., Mello, M. C., De, Patel, V., Rahman, A., Tran, T., Holton, S., & Holmes, W. (2012). Prevalence and determinants of common perinatal mental disorders in women in low-and lower-middle-income countries: A systematic review. Bulletin of the World Health Organization, 90(2), 139–149. https://doi.org/10.2471/BLT.11.091850

- Forbes, J., & Kara, S. M. (2010). Confidence mediates how investment knowledge influences investing self-efficacy. Journal Of Economic Psychology, 31(3), 435–443. https://doi.org/10.1016/j.joep.2010.01.012

- Frazier, M. W. (2010). Socialist Insecurity: Pensions and the politics of uneven development in China. Cornell University Press.

- Gallo, W. T., Bradley, E. H., Dubin, J. A., Jones, R. N., Falba, T. A., Teng, H.-M., & Kasl, S. V. (2006). The persistence of depressive symptoms in older workers who experience involuntary job loss: Results from the health and retirement survey. The Journals of Gerontology Series B: Psychological Sciences and Social Sciences, 61(4), S221–S228. https://doi.org/10.1093/geronb/61.4.S221

- Galor, O., & Moav, O. (2004). From physical to human capital accumulation: Inequality and the process of development. The Review of Economic Studies, 71(4), 1001–1026. https://doi.org/10.1111/roes.2004.71.issue-4

- Gerbing, D. W., Hamilton, J. G., & Freeman, E. B. (1994). A large-scale second-order structural equation model of the influence of management participation on organizational planning benefits. Journal of Management, 20(4), 859–885. https://doi.org/10.1177/014920639402000408

- Giles, J., Wang, D., & Zhao, C. (2010). Can China’s rural elderly count on support from adult children? Implications of rural-to-urban migration. The World Bank.

- Goldin, P. R. (2014). Confucianism. Routledge.

- Griffin, B., Hesketh, B., & Loh, V. (2012). The influence of subjective life expectancy on retirement transition and planning: A longitudinal study. Journal of Vocational Behavior, 81(2), 129–137. https://doi.org/10.1016/j.jvb.2012.05.005

- Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E., & Tatham, R. L. (2006). Multivariate data analysis (Vol. 6). Pearson Prentice Hall.

- Helderman, A., & Mulder, C. (2007). Intergenerational transmission of homeownership: The roles of gifts and continuities in housing market characteristics. Urban Studies, 44(2), 231–247. https://doi.org/10.1080/00420980601075018

- Her, Y.-W., Shin, H., & Pae, S. (2019). A multigroup SEM analysis of moderating role of task uncertainty on budgetary participation-performance relationship: Evidence from Korea. Asia Pacific Management Review, 24(2), 140–153. https://doi.org/10.1016/j.apmrv.2018.02.001

- Hershey, D. A., Jacobs-Lawson, J. M., & Neukam, K. A. (2002). Influences of age and gender on workers’ goals for retirement. The International Journal of Aging and Human Development, 55(2), 163–179. https://doi.org/10.2190/6WCP-TMJR-AR8B-BFC6

- Hesketh, T., Lu, L., & Xing, Z. W. (2005). The effect of China’s one-child family policy after 25 years. Mass Medical Soc.

- Heybroek, L., Haynes, M., & Baxter, J. (2015). Life satisfaction and retirement in Australia: A longitudinal approach. Work, Aging and Retirement, 1(2), 166–180. https://doi.org/10.1093/workar/wav006

- Hilgert, M. A., Hogarth, J. M., & Beverly, S. G. (2003). Household financial management: The connection between knowledge and behavior. Federal Reserve Bulletin, 89, 309. https://heinonline.org/HOL/LandingPage?handle=hein.journals/fedred89&div=90&id=&page=

- HousingCare.org (2013). OFT investigation into retirement home transfer fee terms, pp. 68, Office of Fair Trading. http://www.housingcare.org/information/detail-3450-oft-investigation-into-retirement-home-transfer-fee-terms.aspx

- Hsu, C., & Leech, I. E. (2010). Retirement income satisfaction of American retired workers. In dissertation Virginia Polytechnic Institute and State University. https://www.fermascholar.org/wpcontent/uploads/2013/09/p6_retirement-income-satisfaction_hsu.pdf.

- Hsu, C. (2013). Women$\backslash$’s retirement income satisfaction and saving behaviors [Ph.D. Thesis]. Virginia Tech.

- Hsu, C. (2016). Information sources and retirement savings of working women. Journal of Financial Counseling and Planning, 27(2), 252–264. https://doi.org/10.1891/1052-3073.27.2.252

- Huang, X., & Gao, Q. (2018). Does social insurance enrollment improve citizen assessment of local government performance? Evidence from China. Social Science Research, 70, 28–40. https://doi.org/10.1016/j.ssresearch.2017.11.001

- Income and Living Standards across China. (n.d.). Retrieved November 12, 2018, Federal Researve Bank of St. Louis from https://www.stlouisfed.org/on-the-economy/2018/january/income-living-standards-china

- Ironfield-Smith, C., Keasey, K., Summers, B., Duxbury, D., & Hudson, R. (2005). Consumer debt in the UK: Attitudes and implications. Journal of Financial Regulation and Compliance, 13(2), 132–141. https://doi.org/10.1108/13581980510621910

- Johnston, D. W., & Lee, W.-S. (2009). Retiring to the good life? The short-term effects of retirement on health. Economics Letters, 103(1), 8–11. https://doi.org/10.1016/j.econlet.2009.01.015

- Johnston, D. W., Propper, C., & Shields, M. A. (2009). Comparing subjective and objective measures of health: Evidence from hypertension for the income/health gradient. Journal of Health Economics, 28(3), 540–552. https://doi.org/10.1016/j.jhealeco.2009.02.010

- Ketkaew, C., Van Wouwe, M., & Vichitthamaros, P. (2019). Perceptions of working versus becoming a societal burden after retirement: Demographic analyses of industrial workers in Thailand. Organizational Cultures: An International Journal, 19(1), 23–42. https://doi.org/10.18848/2327-8013/CGP/v19i01/23-42

- Ketkaew, C., Wouwe, M. V., Vichitthamaros, P., & Teerawanviwat, D. (2019). The effect of expected income on wealth accumulation and retirement contribution of Thai wageworkers. SAGE Open, 9(4), 215824401989824. https://doi.org/10.1177/2158244019898247

- Ketkaew, C., Wouwe, M. V., & Vichitthammaros, P. (2019). Exploring how an entrepreneur financially plans for retirement income: Evidence from Thailand. Cogent Business & Management, 6(1), 1668676. https://doi.org/10.1080/23311975.2019.1668676

- Kumar, L., & Mukhopadhyay, J. P. (2013). Patterns of financial behavior among rural and urban clients: Some evidence from Tamil Nadu, India. Institute for Financial Management and Research (IFMR), Working Paper, 9.

- Larrimore, J. (2011). Does a higher income have positive health effects? Using the earned income tax credit to explore the income-health gradient. The Milbank Quarterly, 89(4), 694–727. https://doi.org/10.1111/milq.2011.89.issue-4

- Li, B., & Shin, H. B. (2013). Intergenerational housing support between retired old parents and their children in urban China. Urban Studies, 50(16), 3225–3242. https://doi.org/10.1177/0042098013483602

- Li, L. W., Liu, J., Xu, H., & Zhang, Z. (2016). Understanding rural-urban differences in depressive symptoms among older adults in China. Journal of Aging and Health, 28(2), 341–362. https://doi.org/10.1177/0898264315591003

- Lindahl, M. (2005). Estimating the effect of income on health and mortality using lottery prizes as an exogenous source of variation in income. Journal of Human Resources, 40(1), 144–168. https://doi.org/10.3368/jhr.XL.1.144

- Liu, L., Dong, X., & Zheng, X. (2010). Parental care and married women’s labor supply in urban China. Feminist Economics, 16(3), 169–192. https://doi.org/10.1080/13545701.2010.493717

- Lumsdaine, R. L., Stock, J. H., & Wise, D. A. (1994). Pension plan provisions and retirement: Men and women, medicare, and models. In The National Bureau of Economic Research (Ed.), Studies in the economics of aging (pp. 183–222). University of Chicago Press.

- Lusardi, A., & Mitchell, O. S. (2011). Financial literacy and retirement planning in the United States. Journal of Pension Economics & Finance, 10(4), 509–525. https://doi.org/10.1017/S147474721100045X

- Manchester, C. F. (2010). The effect of pension plan type on retirement age: Distinguishing plan incentives from career length preferences. Southern Economic Journal, 77(1), 104–125. https://doi.org/10.4284/sej.2010.77.1.104

- Marshall, K. (2011). Retiring with debt. Statistics Canada.

- Meer, J., Miller, D. L., & Rosen, H. S. (2003). Exploring the health–wealth nexus. Journal of Health Economics, 22(5), 713–730. https://doi.org/10.1016/S0167-6296(03)00059-6

- Michaud, P.-C., & Van Soest, A. (2008). Health and wealth of elderly couples: Causality tests using dynamic panel data models. Journal of Health Economics, 27(5), 1312–1325. https://doi.org/10.1016/j.jhealeco.2008.04.002

- Miller, G., Yang, J., & Chen, M. (1997). Counseling Taiwan Chinese in America: Training issues for counselors. Counselor Education and Supervision, 37(1), 22. https://doi.org/10.1002/ceas.1997.37.issue-1

- Montgomery, N., Szykman, L., & Agnew, J. (2017). Saving for tomorrow today: How message framing can improve retirement saving rates for younger workers. Italy: CONSOB.

- Munnell, A. H., Sanzenbacher, G. T., & Rutledge, M. S. (2018). What causes workers to retire before they plan? The Journal of Retirement, 6(2), 35–52. https://doi.org/10.3905/jor.2018.6.2.035.

- Muratore, A. M., & Earl, J. K. (2010). Predicting retirement preparation through the design of a new measure. Australian Psychologist, 45(2), 98–111. https://doi.org/10.1080/00050060903524471

- Naruetharadhol, P., & Ketkaew, C. (2018). Managing claims from catastrophic events: An empirical study of claim management process practice and its assessment. Change Management: An International Journal, 17(4), 13–26. https://doi.org/10.18848/2327-798X/CGP/v17i04/13-26

- Nicholas, L. H., Langa, K. M., Iwashyna, T. J., & Weir, D. R. (2011). Regional variation in the association between advance directives and end-of-life Medicare expenditures. JAMA, 306(13), 1447–1453. https://doi.org/10.1001/jama.2011.1410

- Niu, G., Zhou, Y., & Gan, H. (2020). Financial literacy and retirement preparation in China. Pacific-Basin Finance Journal, 59, 101262. https://doi.org/10.1016/j.pacfin.2020.101262

- Njuguna, A. G. (2012). Critical success factors for a micro-pension plan: An exploratory study. Africa: United States International University.

- Noone, J. H., Stephens, C., & Alpass, F. M. (2009). Preretirement planning and well-being in later life: A prospective study. Research on Aging, 31(3), 295–317. https://doi.org/10.1177/0164027508330718

- Panis, C. W. (2004). Annuities and retirement well-being. Pension Design and Structure: New Lessons from Behavioral Finance, 259–274. https://pensionresearchcouncil.wharton.upenn.edu/publications/books/pension-design-and-structure-new-lessons-from-behavioral-finance/

- Petkoska, J., & Earl, J. K. (2009). Understanding the influence of demographic and psychological variables on retirement planning. Psychology and Aging, 24(1), 245–251. https://doi.org/10.1037/a0014096

- Phonthanukitithaworn, C., Naruetharadhol, P., & Ketkaew, C. (2017). Skill development and job satisfaction: Workers’ perspectives in Thailand’industrial sector. Knowledge Management: An International Journal, 17(2), 1–10. https:// doi.org/10.18848/2327-7998/CGP/v17i02/1-10

- Pinquart, M., & Schindler, I. (2009). Change of leisure satisfaction in the transition to retirement: A latent-class analysis. Leisure Sciences, 31(4), 311–329. https://doi.org/10.1080/01490400902988275

- Podsakoff, P. M., MacKenzie, S. B., & Podsakoff, N. P. (2012). Sources of method bias in social science research and recommendations on how to control it. Annual Review of Psychology, 63(1), 539–569. https://doi.org/10.1146/annurev-psych-120710-100452

- Porr, C., Drummond, J., & Richter, S. (2006). Health literacy as an empowerment tool for low-income mothers. Family & Community Health, 29(4), 328–335. https://doi.org/10.1097/00003727-200610000-00011

- Pozen, R. C. (2013). Tackling the Chinese pension system. Paulson Institute Chicago.

- Resende, M., & Zeidan, R. (2015). Psychological biases and economic expectations: Evidence on industry experts. Journal of Neuroscience, Psychology, and Economics, 8(3), 160. https://doi.org/10.1037/npe0000043

- Samuelson, P. A. (1954). The pure theory of public expenditure. The Review of Economics and Statistics, 36(4), 387–389. https://doi.org/10.2307/1925895

- Saunders, P., Shang, X., & Zhang, K. (2003). The structure and impact of formal and informal social support mechanisms for older people in China [Unpublished manuscript]. Social Policy Research Centre, University of New South Wales.

- Seay, M., Asebedo, S., Thompson, C., Stueve, C., & Russi, R. (2015). Mortgage holding and financial satisfaction in retirement. Journal of Financial Counseling & Planning, 26(2), 200–216. https://doi.org/10.1891/1052-3073.26.2.200

- Seligman, M. E. (2012). Positive psychology in practice. John Wiley & Sons.

- Shen, C., & Williamson, J. B. (2010). China’s new rural pension scheme: Can it be improved? International Journal of Sociology and Social Policy, 30(5/6), 239–250. https://doi.org/10.1108/01443331011054217

- Sheng, X., & Settles, B. H. (2006). Intergenerational relationships and elderly care in China: A global perspective. Current Sociology, 54(2), 293–313. https://doi.org/10.1177/0011392106056747

- Steenkamp, J.-B. E. M., & Baumgartner, H. (1998). Assessing measurement invariance in cross-national consumer research. Journal of Consumer Research, 25(1), 78–107. https://doi.org/10.1086/209528

- Suhr, D. (n.d.). 200-31: Exploratory or confirmatory factor analysis?, 17.

- Sundali, J., Westerman, J. W., & Stedham, Y. (2008). The importance of stable income sources in retirement: An exploratory study. Journal of Behavioral and Applied Management, 10(1), 18.

- Talaga, J. A., & Beehr, T. A. (1995). Are there gender differences in predicting retirement decisions? Journal of Applied Psychology, 80(1), 16. https://doi.org/10.1037/0021-9010.80.1.16

- Tang, M., & Coulson, N. E. (2017). The impact of China’s housing provident fund on homeownership, housing consumption and housing investment. Regional Science and Urban Economics, 63, 25–37. https://doi.org/10.1016/j.regsciurbeco.2016.11.002

- Tsui, M. (1989). Changes in Chinese urban family structure. Journal of Marriage and the Family, 51(3), 737–747. https://doi.org/10.2307/352172

- Viegas, M., & Ribeiro, A. P. (2013). Welfare-improving government behavior and inequality in a heterogeneous agents model. Journal of Macroeconomics, 37, 146–160. https://doi.org/10.1016/j.jmacro.2013.05.005

- Wang, D. (2006). China’s urban and rural old age security system: Challenges and options. China & World Economy, 14(1), 102–116. https://doi.org/10.1111/cwe.2006.14.issue-1

- Wang, M. (2013). The Oxford handbook of retirement. Oxford University Press.

- Wu, K. B. (2013). Sources of income for older Americans, 2012. AARP Public Policy Institute.

- Xiao, N., Sharman, R., Rao, H. R., & Upadhyaya, S. (2014). Factors influencing online health information search: An empirical analysis of a national cancer-related survey. Decision Support Systems, 57, 417–427. https://doi.org/10.1016/j.dss.2012.10.047

- Yao, L., Zhao, M., Cai, Y., & Yin, Z. (2018). Public preferences for the design of a farmland retirement project: Using choice experiments in urban and rural areas of Wuwei, China. Sustainability, 10(5), 1579. https://doi.org/10.3390/su10051579

Annexures

1. Questionnaire

(All the questions in this questionnaire are in the form of a 5-point Likert scale. 1 = lowest and 5 = highest)

Retirement Benefit Sufficiency (RBS)

RBS1 I believe that pension will be sufficient for my retirement.

RBS2 I believe that insurance will be sufficient for my retirement.

RBS3 I believe that employee benefit will be sufficient for my retirement.

RBS4 I believe that government benefit will be sufficient for my retirement.

Perceived Health Status (PHS)

PHS1 I believe that I am physically healthy.

PHS2 I believe that I am mentally healthy.

Financial Attainment Capacity (FAC)

FAC1 I believe that my investment knowledge is sufficient.

FAC2 I believe that my savings/investment in financial assets is sufficient.

Perceived Parental Burden (PPB)

PPB1 I believe that financially support a child’s day-to-day living is burdensome.

PPB2 I believe that financially support a child’s education is burdensome.

Short-term Financial Goals (SFG)

SFG1 I am prepared to meet travel expenses in the short term.

SFG2 I am prepared to meet daily/weekly budget.

SFG3 I am prepared to set up a savings account.

SFG4 I am prepared to spend on an annual vacation.

SFG5 I believe I can efficiently keep on track of financial transactions.

Long-term Financial Goals (LFG)

LFG1 I am ready to own a house/property.

LFG2 I am ready to have/take care of my family financially.

LFG3 I am well-prepared to pay off debt.

2. Measurement Invariance