Abstract

Since 2009, the Chinese government has committed itself to encourage Renminbi (RMB) internationalization. China has introduced various direct steps supporting the RMB internationalization, including the open capital market in Hugangtong, the growth of the offshore RMB, the launch of the Cross-Border Interbank Payment System (CIPS). The reform of the exchange rate structure for the RMB, developing crude oil futures. Incorporating the RMB into the SDR, BRI, and the establishment of AIIB contribute to further internationalization of the RMB. The BRI provides an opportunity, on the one hand, that the RMB becomes a foreign trade currency and strengthens the RMB’s position as an international currency. China must encourage RMB internationalization, including turning cross-border RMB trade as a payment currency, promoting RMB internationalization with ODI, enhancing the RMB exchange rate process, developing domestic financial system and financial infrastructure, and warning to expand capital account and develop offshore RMB.

PUBLIC INTEREST STATEMENT

Internationalization of RMB is a long-term strategy involving continuous commitment and perseverance. This paper analyses the emerging sources of control such as the economic mechanism, investments and trade dynamics and the exchange rate framework. China also introduced several new steps to promote RMB internationalization. The alignment between the BRI and the internationalization of the RMB could be practiced in order to extend the RMB trade settlement sector and the development and activity of an RMB offshore finance hub. There are some implications which China has to bear. However, China needs to involves in the internationalization of currencies and to continue improving domestic financial markets and continually increasing the ability to withstand risks at the same time.

Before 1978, China was only an underdeveloped country with poverty and food shortages. However, the US has retained its status as the largest economy in the world since 1871. The US GDP was nominally high at USD 20.58 trillion in 2018 and is projected to reach USD 22.32 trillion in 2020 (Silver, Citation2019). When economies are evaluated for purchasing power parity, the US loses its leading position in China. In 2019, the US economy was GDP (PPP) at USD 21.44 trillion, relative to the Chinese economy at USD 27.31 trillion. The US is forecast to grow to USD 24.88 trillion, and China will close to USD 19.41 trillion by 2023 (Silver, Citation2019).

Such remarkable economic successes show that China has gradually changed its foreign system role. In 1997, given the Asian financial crisis, the Chinese government did not depreciate its currency, effectively curbing its spread, bringing China with high recognition from neighbouring countries. In 2001, China participated in the World Trade Organization and dedicated itself to promoting economic system reform and domestic market liberalization. China retained its average annual growth rate of 8.26 percent from 2008 to 2017, during the global financial crisis and the severe condition both inside and outside (World Bank database, Citationn.d.), contributing to global economic stability and recovery. President Xi initiated the Belt and Road Initiative (BRI) in 2013 to encourage global development by deepened economic cooperation, which is based on the principle of multilateral free trade and should be developed together to fulfil the needs of all.

China’s influence in the world is continuously growing, with the rapid economic growth and shifts in the international system, and has therefore steadily acquired more considerable influence in international affairs. It can be seen that China also plays a crucial role in global and regional issues and the DPRK nuclear problem, the Iranian nuclear issue, climate change, and so forth. To accelerate renminbi internationalization (RMB), among them, China’s move toward an emerging power is an essential step in the financial sector.

Internationalization RMB is an internationally recognized global currency, becoming a prime currency for international trade, finance, funding, and a popular foreign reserve currency. Using RMB as an international currency is sophisticated. The whole cycle of RMB increasingly becomes a primary international currency. The present global currency system calls for the internationalization of the RMB to undergo a lengthy and tortuous period that eventually strives to be one of the major international currencies and reach China’s existing economic and commercial circumstances worldwide.

Following the financial crisis of 2008, the international currency system with the US dollar in its center was shocked and shook up the dollar’s dominance. The US Federal Reserve’s policy on quantitative easing (QE), which was followed by the financial crisis, greatly affected global investor confidence in the US dollar, which promoted RMB internationalization. The US creates trade deficits with financial resources. The US economy has a share of roughly one fifth, but trade has declined to about 10 percent. The US dollar represents approximately two-thirds of the global total official reserve and is the only super currency. Banking on a market deficit to sustain the US dollar’s superposition will only lead to problems like the shortage of US dollar stocks, the dollar asset bubble, the extension of America’s subprime domestic mortgage crisis transforming into a global crisis, and the spillover in US domestic monetary policy in the global economy.

Other countries are deeply concerned about the international monetary system, particularly in most developing countries. Such countries have experienced rapid economic and financial development and have thus built considerable foreign reserves in US dollars. The US economic and financial problems must be compensated for because of the dollar trap. It is therefore agreed that the international monetary system needs to be reformed. The Executive Board of the International Monetary Fund (IMF) agreed in November 2015 to include RMB with a weight of 10.92 percent, only third behind USD and the Euro in the Special Drawing Right (SDR) ’s currency basket (Kennedy, Citation2015). Since then, the RMB has formally become the primary foreign reserve currency in the internationalization of the RMB.

The growing international trade and investment also strengthen the role of RMB in the global market. A growing number of countries are adopting RMB as a cross-border exchange and pricing currency. So far, China has entered into trade swap deals with over 30 nations. The size and distribution of RMBs outside China are increasing through the frontier exchange, national monetary coordination, RMB foreign direct investment, and the Hong Kong RMB offshore hub.

To date, the Belt and Road Cooperation Agreements with China have been signed between 126 countries and 29 international organizations (Huaxia, Citation2019). The first International Cooperation Belt and Road Forum (BRF) took place in Beijing in 2017, with the emphasis on two issues: on enhancing cooperation in policy-making and development strategies and on fostering pragmatic collaboration in interdependencies. In Beijing, a second BRF, attended by representatives of 40 countries and international organizations, was conducted in 2019, while the Forum concluded with an unveiling of a joint communique of 283 concrete results in six categories (Belt and Road News, Citation2019). In other terms, the BRI has been influential in fostering regional economic growth by some international organizations or agencies. BRI has just improved trade and financial cooperation between China and its neighbouring countries, broadening the RMB’s circulation in these areas and creating favorable terms for RMB outsourcing and regionalization. However, RMB is still not an international currency for capital regulation, underdeveloped financial markets, and limited capital transactions. Also, the internationalization process of RMB has been substantially accelerated in the sense of the BRI. It means that the BRI offers an excellent opportunity for the internationalization of the RMB. Through the BRI, the Chinese government can thus broaden the scale and distribution of RMBs beyond China. Also, the Chinese national financial system and exchange reforms are essential and will further enhance financial market growth, which is an institutional basis for RMB internationalization. Thus, this work analyses the nexus of the BRI and the internationalization of RMB. Also, it seeks to identify the internationalization of RMB through the BRI as prospects and challenges.

The BRI is, thus, an essential analytical resource for this research. The primary method of addressing research questions will be the trade and investment details from the BRI countries and using indices, such as the economic interdependence measure. The AIIB and the Silk Road Fund are effective ways to help internationalize the RMB with the BRI. The AIIB was set up in 2015, which is China’s first multilateral financial institution and a cooperation body between governments. Since December 2019, AIIB has 102 representatives from around the globe (AIIB, Citation2019). It concentrates on constructing infrastructures aimed at improving interconnection and economic integration in Asia and strengthening cooperation between China and other Asian nations. Silk Road Fund was founded in 2014. The independent financial institution, solely sponsored by China, intends to assist the BRI’s cultural exchange and interconnection initiatives as an essential step in implementing the BRI. As a further example of comparative data for their investment projects outside China, the AIIB and Silk Road Fund will, therefore, be used in this study.

In order to address the issue, the study focuses primarily on the following research questions: What are the reasons for internationalizing RMB? What are the internal and external obstacles of the internationalization of RMB? Also, what are the prospects and challenges for RMB internationalization through the BRI? Upon addressing these concerns, the study is supposed to figure out the best way to accelerate the internationalization of the RMB within the BRI context.

According to Cohen (Citation1971) argues that the internationalization of currency that its function is consistent with that of the domestic currency, except that the use of currency extends to the entire world. Cohen argues that the internationalization of currencies relies on two sorts of subjects: one is state interference in internationalizing the currency, primarily expressed in the dominance of the state on the issue of currency rights and the control of the country’s monetary policies; the other is domestic and overseas market transaction networks (Cohen, Citation1971). Mundell (Citation1961) contends that the requirements of a truly internationalized currency require expanded participation of global trade, production, and finance for the issuer, a highly free market, the abolition of foreign exchange barriers, currency predictability and consistency, and the stability of the currency value. Economic strength is seen as the key variable that affects the degree to which a country’s currency is internationalized. Similarly, Grassman (Citation1976) states that developed industrialized nations have a high degree of decision-making power over exchange rates, influencing the allocation of the profits of imports and exports. Thus, it is easy for the currency of the country to be a stable currency and to become an increasingly international share in the international market (Grassman, Citation1976). Again, Kindleberger (Citation1967) indicated that a strong economy could have a sound economic base and a stronger domestic currency capital market potential. Eichengreen and Frankel (Citation1996) compared the share of international currencies in global foreign exchange reserves with the share of their currency issuers in world output and found that they were highly correlated. Global trade is also an essential element in currency internationalization. Kubarych (Citation1983) argued that the greater the volume of trade in a region, the greater the demand in foreign exchange transactions for local currency, which would further boost the pricing power of domestic currencies. From the perspective of trade, Shams (Citation2005) explores domestic currency internationalization, assuming that international currencies often exist in countries where international trade is the most substantial proportion of global trade. Some scholars also examine currency internationalization from a currency stability standpoint. Ozeki and Tavlas (Citation1992) pointed out that currency volatility would distort price signalling. When the information search cost of a currency holder rises, of course, it reduces currency demand (Ozeki & Tavlas, Citation1992). Also, the currency with an odd number should be replaced with the denominated value, which would result in a decline in market demand for the currency with an indefinite value (Calvo & Vegh, Citation1992; Li & Matsui, Citation2005).

Domestic scholars assume that the factors impacting the internationalization of the currency of a country include overall economic growth, inflation, real interest rates level, the exchange rate appreciation (depreciation), and volatility (Liu & Li, Citation2008). Que and Ma (Citation2013) concluded that trade integration is the primary catalyst to facilitate the internationalization of the RMB, based on the State-space model. Using the RMB settlement ratio as a measure of currency internationalization and using the VAR model to measure the factors affecting RMB internationalization, Yuan and Xu (Citation2014) found that the development of offshore financial markets and the RMB appreciation are conducive to the promotion of RMB internationalization.

Many studies have started to explore the issue of RMB internationalization based on the proposal of the BRI. Chen (Citation2014) explores the new mainline to further push RMB internationalization, including going global and outputting RMB capital. According to the study by Lin and Wang (Citation2015) assert that the economic scale, foreign direct investment, trade factor, and economic independence have a significant effect on the internationalization of the currency. Simultaneously, the BRI will boost the international scale of RMB substantially through an expansion in foreign investment and an active trade engagement with Europe and Asia (Lin & Wang, Citation2015). Also, the implementation of the BRI has helped to boost the export trade of China (Sun et al., Citation2017). The BRI nations allied with China form a significant currency bloc, and many recognize the Renminbi as payment of goods supplied to China and as payment means for goods supplied from China (Chamorro, Citation2017). At the end of June 2018, the total merchandise trade of China with countries associated with the BRI nations was USD 5 trillion–the RMB being the primary vehicle for this immense volume of trade (Olsson & Fei, Citation2018). Also, trade and investment through BRI in RMB, seek to foster Chinese soft power and act as a way to avoid US sanctions as a response to sanctions levied on those countries by the US, Russia, and Iran export oil to China and accepted payment in RMB. China also views the emergence of oil contracts denominated in RMB as an incentive for China to import oil and gas in its currency while removing exposure to fluctuation in the foreign currency. Since China is now the biggest importer of oil in the world, these policies are portraying the emergence of a multipolar system with an important role played by the RMB currency area.

Equally important, it would be one of the most significant foreign currencies in the future if we can make the RMB international in every aspect (Jianjun et al., Citation2013). With the growth of the Chinese economy, RMB has been continuously recognized and embraced around the world, with evident results in trade settlement and offshore markets (Jianjun et al., Citation2013). It is, therefore, of great theoretical and practical significance to further study its nexus and effect and seize advantage of the BRI opportunity.

This work is based primarily on a qualitative method. Also, economic data and relevant indexes are used to prove the argument and served as support. Based on secondary data sources, the study describes the causes, the structures, circumstances, processes, and obstacles to RMB internationalization, offering hypothetical help to examine RMB internationalization opportunities and challenges within the BRI context. The study will also use evidence from trade and investment, AIIB and Silk Road Fund projects, and other observational sources. To investigate their common interest, for example, the economic interdependence indexes between China and significant BRI countries shall be computed in the analysis. Neoliberal institutionalism, the theory of currency substitution, and the Ternary Paradox will be utilized for this paper.

Neoliberal institutionalism has a full analytical, conceptual structure, and it is one of the essential ideas in international relations. Neo-realism is the answer, yet neo-liberals contend that its significance and influence are overshadowed while they do not dispute the anarchic existence of the international system. The neoliberal institutional system will help examine how China can continue to expand trade and investment in cooperation between the BRI countries and enhance the RMB process of regionalization and internationalization. However, developing organizations like the Asian Infrastructure Investment Bank (AIIB) is a phenomenon not only of neoliberal institutionalism but also shows that neo-liberal institutionalism works well among its participants.

The Currency Substitution Theory and the Ternary Paradox are critical economic theories. The Theory of Currency Substitution indicates that foreign currencies are substituted for local currency in terms of value, the medium of exchange, value store, and other fields in the condition of free exchange. It contributes to understanding why RMBs should evolve into regional currencies instead of local currencies or US dollars by increasing trade and investments between China and the BRI nations and improving the RMB free trading mechanism. The RMB will also address the “Ternary Paradox” problem. As the world’s second-largest economy, China will maintain its monetary policy flexibility. Simultaneously, internationalizing the RMB includes a stable currency and free flow of capital (Park & Takagi, Citation2012). Therefore, the Chinese monetary authorities have a significant challenge of balancing the free flow of capital with a stable exchange rate.

1. Neoliberal institutionalism

Neo-liberal institutionalism is a major intellectual trend in the United States’ international relations in the 1980s. Neo-liberal institutions represent Robert Keohane and Joseph Nye, whose representative works, which were published in 1977, are Power and Interdependence and After Hegemony.

The objective of the external behaviour of states is to promote domestic interest, and states can decide reasonably (Modelski, Citation1986). Neoliberal institutions claim that collaboration will allow States to gain more considerable advantages in a world where external interdependence is high. However, there is anarchy among the international community, and cooperation is challenging to achieve. Parties that recognize common interests are prepared to agree on the same goal. It is the cornerstone of domestic partnership. The flow of international information and shared communication can be facilitated by international institutions, which will likely create opportunities for cooperation. International cooperation from this viewpoint requires international institutions. Developing a structure is an efficient way to promote cooperation if nations have common interests and will cooperate. The international institutions can provide for international cooperation with efficient frameworks and institutional guarantees. It is the crucial role of international institutions in maintaining global peace, security and order, and promoting functional interactions and active cooperation between States. States have to help international institutions agree to aim for the highest common interest (Keohane & Nye, Citation1977).

The AIIB is an international organization founded to support infrastructure construction in developing Asia due to the BRI. The establishment of the AIIB has these functions explicitly: first, to lower the interaction costs. If no process or protocol is to be practised, all things must be resolved from the outset, and parties have to pay too many expenses. Second, the legal framework should be laid down. While AIIB does not make mandatory orders for its members, it can help to agree with its member states through its principles, standards, rules, and decision-making procedures. Third, sufficient information should be provided. Lack of information represents an essential hindrance to international cooperation and leaves the international community in an unstable and suspicious environment. The settlements reached fear of fraud. To obtain adequate information and highly predict the expectations of each member, the AIIB can provide reliable, consistent, structured information to participating countries. As the information becomes more accessible and accurate, it stimulates international cooperation. Fourthly, exercising a supervisory role. The AIIB can evaluate its representatives’ actions. The AIIB may put effort into addressing infringement on people who violate the laws or violate their obligations.

The AIIB will provide Asian countries BRI countries, with much investment and cooperation opportunities. There will also be durable and more robust economic ties between China and these nations, and increased economic cooperation will be enhanced to promote RMB internationalism.

AIIB and BRI will expand the RMB value store function. Enhanced economic cooperation will form a solid basis for the swap agreement between the RMB and increase the RMB’s share in international reserves of Asian countries. It will promote global RMB’s status as an international reserve and encourage RMB internationalization. Another example of the value storage role of the RMB on the international stage is the use of RMB as a private-sector financial asset.

The creation of the AIIB will also encourage the internationalization of the RMB in the private sector. Asia’s development will require USD 1.7 trillion annually to sustain growth momentum. Businesses must increase infrastructure investment from 63 trillion dollars to up to 250 trillion dollars by 2020, which Government reforms could bridge up to 40 percent of the infrastructure gap in Asia, with the rest being done by the private sector (ADB, Citation2017). An organization, like AIIB, cannot fill such a broad gap, and large-scale fundraising is required, giving Chinese domestic investors great room for international trade and investment.

BRI and AIIB will extend the RMB pricing function. Developing AIIB will facilitate building infrastructure in Asia. Chinese companies have financial and development advantages and are actively involved in building the network. It will eventually improve economic and financial ties between China and BRI countries and will also increase transboundary trade and investment in the region. A reduction of US dollar dependence is essential to encourage cross-border business and lower the risk of currency fluctuations. For RMB, this will be excellent to become the BRI region’s prices and settlement currency.

2. Currency substitution theory

The concept of currency substitution was first proposed by the American economist Karuppan Chetty in his 1969 paper entitled Measuring the Nearness of Near-Moneys. Currency substitutions mean that a foreign currency replaces a domestic currency in its entirety, or part, if its residents lose faith, in local currency or if the return of local currency is low, and utilizes value storage, trade medium, and pricing functions (Chetty, Citation1969). “Good money expels bad one,” which is a significant phenomenon of the internationalization of currencies.

The collapse of the Bretton Woods system gradually resulted in economic liberalization and globalization, and the global trend to substitute currency emerged. The biggest is the US dollar. The dollar is still the world’s most widely accepted currency, and some nations, including Puerto Rico, Colombia, Ecuador, and other countries, also see it as the dominant currency. The Euro, the pound, and the Japanese yen can also be international currencies besides the US dollar.

Today, the reporting of Chinese RMB has grown significantly in recent years, and replacement has taken place in several Asian countries, such as Pakistan, Indonesia, Cambodia, Vietnam, Mongolia, and other nations. Thus, RMB acceptance progressively improves. Nevertheless, RMB cannot be deemed a foreign currency. The international rates of use and availability of RMB are still small, and the exchange rate of RMB is not steady. Most notably, China’s government continues to enforce capital account monetary restrictions that do not support the RMB replacement cycle in other areas outside China.

From the geographical viewpoint, the currency internationalization process includes three stages, including peripheralization, regionalization, and internationalization. This way, China should also encourage the RMB internationalization process. Throughout regions such as Hong Kong, Macao, and Taiwan, and nearby countries such as Vietnam and Laos, RMB is widely accepted. In the next move, China is expected to increase RMB standing in neighbouring countries, including Pakistan, Kazakhstan, Russia, and eventually become the main currency in the BRI zone. When RMB goes on the right path to regional currency, it will automatically become an international currency. RMB plays a multi-role role in RMB internationalization from the currency function, with the settlement currency, investment currency, and the reserve currency, respectively. By geographical extension and multiple roles, China would broaden RMB’s regional influence rapidly.

Currency substitution is affected by exchange rates, interest rates, inflation, national income earnings, and so forth. Of these, the exchange rate has the most impact on the internationalization of currencies. For illustration, in 2016, overall Chinese imports and exports, which use RMB as a settlement currency, decreased substantially. Several variables influence the preference of a trade-denominated currency. Also, economic growth, exchange rate, and the creation of financial markets are macro-factor factors. Micro factors include risk and trade prices, control bargaining, and product differentiation. If China’s economic status, such as developing the financial market, transaction costs, negotiating power, and other reasons have not changed significantly, fluctuating exchange rates should be mainly responsible for the sharp decline in the RMB settlement scale in 2016. It means that importers and exporters were reluctant to use RMB as a cross-border settlement curry, causing a significant decrease in their RMB settlement share due to RMB exchange rate depreciation and the expected RMB depreciation of the world market in 2016.

3. The ternary paradox

In the 1960s, in countries with various exchange-rate systems, Robert A. Mundell analyzed the effects of macroeconomic policies. He concluded that in the open-economy system with continuous capital flows, the balance of payments deficit would decrease domestic supplies, while the balance-of-payments surplus raises domestic supplies provided that the country adopts a fixed exchange rate regime. Any monetary policy adaptation or distribution of liquidity may lead to external imbalances if a country’s balance of payments is balanced. It is unsuccessful if the government takes monetary policy to fix the imbalance. It only works if the floating system of exchanges is implemented (Mundell, Citation1961).

Paul Krugman also suggested the ternary hypothesis in 1999 on the grounds of Mundell’s results. Krugman claims that in open economies, it is impossible to achieve free capital movement, monetary policy independence, and the fixed currency system. The monetary authority of a country can choose at most, only two. The ternary dilemma gives the monetary authorities three options: first, to surrender the stabilization of the currency to protect the freedom of the internal monetary policy and the free flow of capital. Instead, give up capital freedom and impose control of capital to preserve independence or the stability of the country’s monetary policy.

For an emerging power like China, and to become a monetary power, the independence of monetary policies is essential. The freedom of the monetary policy of a country is a prerequisite for monetary policy instruments to be effective. The monetary policy independence means that, regardless of other countries’ economic circumstances, the Central Bank can formulate the monetary policy according to its own will. Monetary policy instruments will play their full function only under the presumption of the independence of monetary policy to stimulate economic growth, guarantee full employment, preserve price stability, and achieve a long-term balance of payments.

In the same period, the free flow of capital is also an essential requirement for an international currency. The Chinese government, however, still has capital flow regulations. Although capital flows openly under the current foreign exchange system, capital accounts also include constraints. Considering the ongoing underdevelopment of China’s financial market, the blind opening of the Chinese private finance capital account without complete planning will lead to surprise in China’s domestic finance foreign hot-money market. It is reasonable to choose a policy to preserve capital account regulations. It does not imply, though, that China cannot continue to encourage the internationalization of the RMB. In some Asian countries and regions, RMB has been widely distributed and applied. Because of creating the AIIB and expanding RMB offshore markets, the RMB will be a significant currency in the BRI area. This chance should be taken by China to speed the RMB cycle.

China needs monetary policy stability and free capital movement. The floating exchange-rate mechanism has, therefore, been China’s only viable option, which is also under China’s current exchange-rate regime. In line with the announcement by China’s central bank, China is implementing a controlled floating exchange rate system, with a connection to a currency basket based on market demand and supply. It also reflects the desire of China to encourage the internationalization of RMB.

The RMB internationalization is not a single-stage activity but a systemic, time-consuming procedure. The launch of the capital account is also a continuous operation. It will be free to convert from the bank account to the sales, payment, and exchange currency used by other nations in the transaction and will then be free to convert to both the capital and current accounts. Only a few can become foreign currencies among the many national markets worldwide. It can be seen that currency internationalization cannot be accomplished by depending on our own will. Those who want monetary internationalization need to prepare themselves thoroughly and take advantage of the chance.

Therefore, RMB internationalization can be analyzed from various viewpoints. The research, considering integrity and reasoning, concerns primarily existing its status, China’s efforts to promote RMB internationalization, the impact on RMB internationalization of BRI and AIIB, and China’s decisions to enable RMB internationalization.

4. RMB internationalization status

China has made significant strides in recent years in encouraging the internationalization of the Renminbi, but it also faces a variety of difficulties. The status analysis for Renminbi internationalization consists of 5 components, RMB Internationalization Index and its influencing factors, cross-border trade as a settlement currency, financial transactions, global currency reserves (including RMB in SDR), and China’s reform of the Renminbi exchange rate system.

4.1. Internationalization index of RMB and its variables

The RMB internationalization index (RII) is used to assess the active practice of RMB in global economic activity. The RMB expansion may be viewed as an international currency for settlements in exchange, financial transactions, or official reserves. The basis of this analysis can be compared to other major international currencies. The RII in this study follows the measurement method reported by the International Monetary Institute of the Renmin University of China in the Annual Report on the RMB Internationalization. The vital statistics from the People’s Bank of China (PoBC), IMF, World Bank, and others are being compiled (International Monetary Institute, Renmin University of China [RUC], Citation2015).

The RII is not just a number; it also has economic significance. The higher the RII size, the more the RMB will be used on the global market. The RII meaning is RMB’s internationalization degree. The RII would be equal to 100 if RMB is the only foreign currency. The value of RMB should be zero if it is not used in any international economic transaction. When RII’s valuation continues to rise, the RMB will be gradually multinational. If RII is 10, for example, it implies that 10 percent of worldwide transactions use RMB for international trade, investment, finance, and official reserve purposes (RUC, Citation2015).

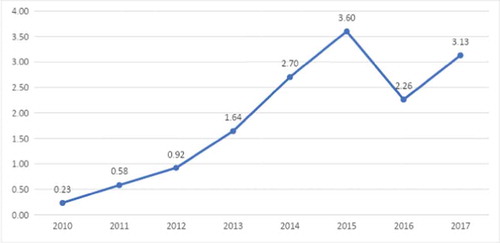

As shown in Figure , RII was only 0.23 in 2010, and RMB coverage on the international market was zero. By the end of 2017, the RII hit 3.13, and in just a few years, the RMB’s internationalization was increased. Between 2010 to 2015, China sustained steady economic growth despite high downward pressure. The RMB has been increased to include international trade, financial transactions, and world exchange rates through implementing the transnational RMB scheme, reforms of the clearing mechanism, and an extension of the RMB offshore market. The internationalization of the RMB is much enhanced, and RII has rapidly increased. RII experienced negative growth for the first time, owing to the impact of dual international and domestic pressures such as Brexit, the rise of international trading protectionism, the slowdown of China’s economic growth, declining exchange rates, and capital regulations. As the world economy improved in 2017, China’s economy’s output will strengthen, and the exchange rate of the RMB is expected to stabilize. Chinese trans-border RMB policies and infrastructures have been improved, and several major BRI projects have been launched. Therefore, the internationalization of RMB slowly digested and substantially repaired the past negative impacts in 2017. RMB has remained stable in the monetary system worldwide.

Figure 1. Internationalization index of RMB from 2010–2017.

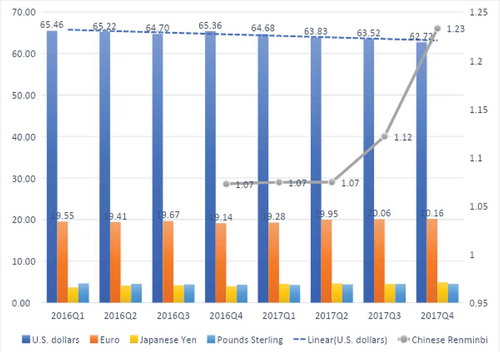

The US dollar share of central bank accounts in the last quarter of 2017 has fallen to a low of four years, but the buck does not lose its place at the top of the reserve (see Figure ). Data from the International Monetary Fund on the COFER showed that the dollar reserve share decreased to 62.72 percent and represented the lowest level than the buck was 65.36 percent of the reserves at the end of 2016. However, dollar reserves have not fallen as far as the IMF data suggests. Exchange rate changes and prime reserve valuation of debt securities denominated by prime reserve assets may cause a decrease in central bank cash in 2017, given the reduction in buck’s output. According to FactSet reports, the US dollar lost approximately 10 percent of its value compared to its peers in 2017, calculated according to the ICE US Dollar Index (Tappe, Citation2018). The growth in the Euro as a reserve currency was noted, which in the first three months of 2017 rose to USD 2.02 trillion, compared with USD 1.61 trillion a year ago. Although the dollar was weak in 2017, the Euro was high (IMF, Citation2019). The 14.1 percent increase against the greenback affected the funds, which are measured in dollars (Tappe, Citation2018).

Figure 2. World Currency Composition of Official Foreign Exchange Reserves (COFER).

However, with the increase in external demand, Japan’s economy grew strongly. Due to the uncertainty in financial markets, the Japanese Yen has become a typical foreign currency of haven internationally. As compared to 3.96 percent in the previous year, it rose to 4.90 percent in 2017. Though the internationalization index of RMB is still relatively low compared to the major international currencies, the gap is shrinking gradually. Faced with a trade war between China and the US and other economic growth uncertainties, China’s reforms and open policies persisted in 2018 and maintained stable and balanced economic perspectives. The currency of the RMB remained stable. It could effectively alleviate financial risks—this accomplishment supporting the internationalization of RMB. RMB was included in foreign exchange reserves in Germany, France, and an increasing number of emerging markets economies. The Shanghai International Energy Exchange Center lists RMB denominated crude oil futures. In foreign traders, Chinese iron ore prospects were introduced. Such encouraging messages also facilitated the internationalization of RMB.

4.2. Transboundary payment currency exchange with RMB

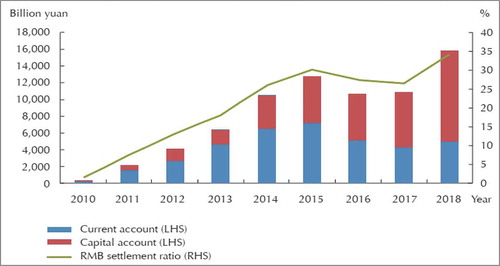

Ultimately, the size of China’s RMB cross-border exchange (see Figure ) is fluctuating. China’s cross-border trade decreased after the global financial crisis in 2009, owing to the weak global economic growth and the downward effect on the Chinese economy.

On the opposite, the transborder trade volume as a payment currency with RMB sustained a substantial growth from 2011 until 2015, given the harsh external environment. It is mainly because of the United States’ quantitative easing program, its deep confidence in China’s economy, its aggressive monetary and money strategies and Chinese accounts slowly opened up. The transboundary trade volume of RMB, as a settlement currency, has decreased significantly since 2015, affected by several factors including the return of funds from the economic recovery in the US, the withdrawal of quantitative easing policies, the continuing US dollar appreciation and the China-US trade war and other factors.

Figure 3. The proportion of RMB in total cross-border settlement during 2010–2018.

In 2018, the trust of investors in RMB increased significantly, and cross-border trade volumes with RMB as a currency boomed due to the influence of the BRI, the AIIB, and the inclusive RMB in SDR and other variables. Cross-border RMB payments amounted to 15.85 trillion yuan, which increased annually by 46.3 percent (People’s Bank of China, Citation2019). During this same period, cross-border RMB settlement accounted for 32.6 percent of the total cross-border settlement, a record high with a rise of approximately seven percentage points over the previous year. For eight years in a row, the RMB became the second-largest cross-border settlement currency (People’s Bank of China, Citation2019). RMB scope has substantially increased in bilateral trade settlement. Via collaboration on currency exchanges, China offered RMB liquidity to BRI countries. The geographical position of the RMB was strengthened.

4.3. Outward direct investment (ODI)

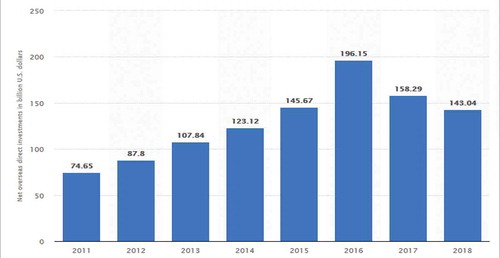

The scale of China’s ODI with RMB saw an increase in trend year after year from 2013 to 2016, but a significant decrease was observed in 2017 (see Figure ).

Figure 4. China net ODI from 2011–2018.

There are two primary explanations for this. First, China’s government has imposed capital outflow restrictions. Second, many Chinese companies have been delayed or prevented by the United States from acquiring US companies because of national security.

5. RMB’s inclusion in the global exchange reserve

On 30 November 2015, the Board agreed to add the RMB to the SDR and then extended the basket of SDR currencies to 5 currencies: the US dollar, Euro, Pound, and Japanese yen. Thus, the RMB is 10.92 percent weighted in the SDR currency pool, and the US dollar, Euro, Pound, and Japanese yen weights are 41.73 percent, 30.93 percent, 8.09 percent, and 8.33 percent respectively (Kennedy, Citation2015). On 1 October 2016, the new SDR basket came into force.

Including RMB in the SDR helps improve the SDR’s representativeness and the international currency system. The advantages are: (1) a diversified SDR set, a more flexible currency system, and more inclusive of the major currencies worldwide. (2) The incorporation of RMB in the SDR represents the support of the IMF for the internationalization of the RMB. With the more useful RMB, it can improve the international currency status, which relies heavily on the US dollar, and reduce the danger for surplus countries of the “dollar trap.” (3) RMB inclusion in SDRs will increase the hedging room among significant currencies, add to the smoothness of the SDR fluctuations, and improve SDR stability.

Adding RMB to SDR marks an integral part of the internationalization history of RMB. The IMF has stated that the RMB is a readily available currency. The widely available currency concept of the IMF means that the currency is generally used extensively for external financial transfers and is exchanged in the most relevant foreign exchange markets. Therefore, while the RMB exchange rate regime is still functioning openly and the RMB capital account is not convertible, the RMB is now one of IMF’s accepted, readily available currencies. It will contribute to enhancing RMB’s confidence in the world market, strengthening the RMB’s trading and reserve asset functions and encouraging internationalization. The PoBC concluded in 36 countries and regions at the end of March 2018 based on mutual currency exchange agreements with central banks or monetary authorities. Overall, the Agreement was above RMB 3.3 trillion (RUC International Monetary Institute, Citation2018).

However, it still has to understand that incorporating RMB into SDR does not imply that the Chinese capital account is open, nor does it indicate that the RMB has reached its internationalization target. Capital accounts are not enough to internalize the currency based on recent international experience and a necessary precondition, even in the early phase of monetary internationality (International Monetary Institute, Citation2018). In this respect, international market development and trade have fostered the internationalization of currencies, which has created capital account opening requirements in return. The situation is that the rapidly growing global offshore RMB market not fulfils the requirement for companies to use RMB for settlement only under capital account control but also meets the demand for non-residential investment for RMB assets and increases confidence in RMB. RMB offshore transactions have convertibility to a certain extent. This convertibility and the convenience of RMB have together contributed to rapidly developing RMB internationalization.

It is worth stressing that although the internationalization of the RMB has made some progress, the scale and share of the RMB as a global exchange reserve remains low. By including RMB in the SDR, the IMF has accepted the role of RMB as a reserve asset, but it still depends on RMB and on foreign reserves to decide if it can become a primary international currency.

6. The Internationalization of RMB by the BRI and AIIB

The BRI project helps promote the RMB’s internationalization. The core content of the BRI is, on the one hand, to promote economic cooperation among the countries in the region and to increase the demand for a unified currency, such as eurozone development, through strengthening regional economic cooperation. US dollars are the first currency option in the BRI, but many countries still try and use other alternative currencies to reduce risks by monetary diversification, after having learned the painful lessons of the financial crisis. It allows the RMB to be the regional currency for settlement.

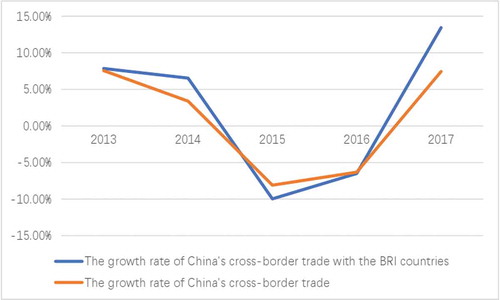

The BRI would, on the other side, further enhance the international currency status of the RMB. In the last years, many Chinese companies have increased their foreign direct investments in countries of the BRI. The supported by Chinese government policies to encourage the construction in BRI, and Silk Road countries have especially developed new foreign direct investment spots for Chinese companies like Pakistan economic, Yawan high-speed rail, Gwadar port, Sino-Russian oil and gas pipeline, Piraeus port construction, Greece and other projects. Between 2013 and 2018, China and the BRI countries had a combined import and export amount of up to USD 6.5 billion. After the downturn in the 2015 and 2016 global economy, cross-border trade growth between China and the BRI countries was 13.45 percent in 2017 (see Figure ).

Figure 5. The growth rate of China’s cross-border trade with the BRI countries.

However, China developed 82 economic and trade cooperation areas, and Chinese companies invested more than USD 80 billion directly in these countries. With the increasing investments of Chinese companies in the BRI in these countries and the RMB coverage, as shown in Figure , the RMB will be further expanding its scope and size, thus promoting further RMB internationalization.

6.1. RMB prospects to become the BRI region’s main currency

The main factors that shape the choice of significant regional currencies are economic development and risk, the stability of domestic financial markets, and exchange and foreign demand rates.

China is the most robust economy in the BRI region, with a view to economic development. While the double-digit growth rate of GDP in China is no longer maintained after the financial crisis, it retains the economic growth rate of 6–8 percent. However, the Chinese economy’s overall risk is relatively small from an economic risk viewpoint. In recent years China’s economic foundation has become more robust, and its prospects for growth have increased with China’s domestic structural supply-side reforms and implementing capability and deleveraging programs.

Again, the systems of financial organizations of China were continually developed and improved from the perspective of developing the domestic financial market. Several financial institutions and banks have developed quickly and have established a multi-level financial-market regime based on the money, equity, insurance, and foreign-exchange markets. The PoBC has improved its potential for macro-management and moved from direct supervision to indirect regulation, such as modification of the rediscount rate and open markets. China has increasingly matured in its domestic financial market.

The World Trade Organization (WTO) ’s most recent trade report issued in 2018 reveals that China’s trade in goods exceeded a gross import and export value of USD 4.6 trillion. China already places first on the globe for two consecutive years, although it faces the possibility of a Sino-US trade war. Again, China is increasing its openness, seeking to improve its domestic business climate and continuous exportation and the availability of imported products and services, in opposition to Trump’s America First approach and other types of protectionism.

As the economy of the country expands across boundaries, Chinese people now have more resources, more leisure, more energy and a more exceptional ability to travel and consume in other countries and the rise of disposable incomes per capita and the expansion of life expectancies. Simultaneously, Chinese students in foreign countries are an essential factor that cannot be overlooked. If Chinese students in foreign nations reside extended, so consumption is high, and consumer frequency is high. Such two factors have contributed to the need for a regional currency, which would further increase the RMB coverage and extend the RMB scale.

Hence, the RMB has excellent potential to become the main currency of the BRI region from its economic growth perspective, economic risks, development of the domestic market, trade scale, and cross-border consumption. The regionalization of the RMB will be further enhanced with the full extension of the significant projects of the BRI.

7. The RMB’s position in promoting BRI economic cooperation

China’s economic partnership with the BRI countries will play a greater significant role for the RMB. First, the RMB will encourage the growth of international trade in the BRI region. Massive capital outflows follow the RMB internationalization process. Different companies in the BRI have the opportunity not only to receive support for RMB in trading with China but also to accumulate assets of the RMB rapidly and create favorable conditions for further development of intra-regional trade cooperation. China has concluded reciprocal trade deals with many countries at the central bank level along with the basis of the BRI. Those countries that raise RMB funds via the backup credit channel and inject them in their domestic financial market, so their domestic entities or companies may borrow RMB conveniently to pay for imports from China, promoting bilateral trade and development cooperation. However, offshore industry growth has rendered the use of RMB simpler. The RMB offshore deposits have expanded to include multiple countries operated by international banks, creating sufficient RMB liquidity abroad to develop trade with China for countries part of the BRI. The internationalization of the RMB has resulted in over RMB liquidity, which may facilitate regional trade growth.

Utilizing RMB as a commodity and transfer money will decrease the risk of a currency like the US dollar being used by a third party. Different factors, such as the money available, exchange rate fluctuations, currency transaction cost, and interest rate return, affect the choice of the international trade currency. Currency costs are the most critical factor. For many years, the US dollar was number one in the world market. Such reasons are different, first, that the US dollar is a leading international currency, controls commodity goods like crude oil, and thus has the advantage of low exchange costs in terms of international trade in payments denominated by the dollar. Therefore, the US dollar is some high-quality international currency. The US’s national power is robust, and its economic and political development stable than any other country in the world. Therefore, the US dollar exchange rate is relatively stable, the currency value is high, the national interest rate is relatively large, and the US dollar’s retaining capital gains are considerable. Even if the US export share has fallen year after year since the 1970s, the US dollar is still the world trade’s most widely used third party currency and appears to be a dominant market price.

However, the US dollar exchange rate fluctuated tremendously after the 2008 financial crisis. The US Dollar is continuously depreciating under the Fed’s quantitative easing policy, and both sides have to face high exchange-rate risks with the US dollar as settlement money. Domestic economic reward policies in the US lead to economic and political instability, and declining asset yields often imply that US dollars are at considerable risk for official foreign reserves or wealth distributions for the private sector. It was evident at this point that the dangers of foreign currency in international trade were pricing and settlement currency.

The BRI represents a significant trading partner for China. Where international trade is priced and settled in RMB, the risk of a third-party currency can effectively be avoided. In recent years, it has gained more international recognition, and the advantage of using the RMB as a tradable currency is being demonstrated. The RMB’s stable market value has given it an excellent international reputation for its international expansion. The increase in RMB coverage in international markets can reduce the risk of the exchange rate of other currencies as a denomination and settlement currency. Thus, the returns on RMB assets continue to be high. Also, RMB holding can achieve a significant increase in asset value. It also has liquidity insurance for the RMB from China’s rising economic strength.

Increasing numbers of companies have used the RMB to settle trade prices. The results of a Bank of China survey in the White Paper for RMB Internationalization 2014 show that the cross-border coverage of RMB by surveyed companies is substantially higher than in 2013. The percentage of international companies with over 15 percent of total RMB payments rose by 10 percent relative to 2013 to 26 percent.

Furthermore, RMB funding for large BRI infrastructure projects may be supported by Chinese financial institutions. The BRI is built with several major national economic projects and public livelihoods, the main content being infrastructure construction. These major support projects are the basis on which a country can increase its potential for development and improve living standards and directly affect national economic development. Building costs by fees are challenging to cover, taking the example of a high-speed rail. However, high-speed rail building helps promote the migration of labour, resources, and technologies along the BRI, enhancing economic and trade connectivity and encouraging regional science and technological developments, growing cross-border trade and tourism growth.

The internationalization of the RMB facilitates the development of BRI infrastructure. Through building infrastructure, China has advantages. Via multilateral financial bodies such as IMF, AIIB, Silk Road Fund, and others, China can assist in facilitating the growth of Chinese infrastructure construction in other countries in terms of RMB bonds, loans, and direct investment to enhance regional economic cooperation and integration.

It can be seen that the US dollar and Euro control trading in the international financial system. Most of the payment is in the US dollar too. Though, the formation of the AIIB contributed to the international economic and financial system. In Asia and particularly China, it has increased the international influence of developing countries. After operations of the Asian Infrastructure Investment Bank, trade in goods and services will inevitably be strengthened between China and other Asian countries, thus enabling the BRI region to improve RMB coverage in international trade settlements and reduce US dollar reliance. Thus, RMB’s effect will be considerably improved.

8. Internationalization of RMB prospects

Theoretically, it can be concluded that: (1) From a geographical standpoint, the internationalization process of currency includes three steps: peripheralization, regionalization, and internationalization. This method of encouraging RMB internationalization is also to be used by China. From a currencies function viewpoint, RMB has a wide range of roles in RMB internationalization progress with the settlement, investment, and reserve currency. (2) Exchange rates, interest rates, inflation, and national income are the main factors influencing currency substitution. (3) Monetary policy flexibility and free capital flow in China are essential. Thus, for Chinese currencies, the floating exchange rate structure is the only feasible option. (4) In the internationalization of the RMB, international institutions, such as the International Monetary Fund and the AIIB, are playing an important role, facilitating monetary collaboration, in lowering trade and consulting costs between China and other countries.

On the grounds of neo-liberal institutionalism, currency replacement principle, and Ternary paradox, China will try to promote RMB internationalization: (1) Cross-border exchange with RMB as a settlement currency should be further expansion. (2) Encourage the internationalization of RMBs with large ODI. (3) Further, develop the exchange rate mechanism for RMB. (4) Further improve the domestic finance mechanism and financial infrastructure of China. (5) Further caution in free capital account and growth of the offshore RMB industry.

8.1. Cross-border exchange with RMB as a settlement currency should be further expansion

Over the last ten years, cross-border trade has increased rapidly, and RMB internationalization has become generally accepted. As cross-border trade develops, China will have more initiatives in the selection of cross-border price and settlement currencies. Through exchange with the countries of the BRI, the proportion of trade with RMB as rates and the payment currency must be more expanded and strengthened, and the scale and distribution of RMB must be enhanced, and RMB will thus be internationalized.

Also, China has rapidly evolved in the e-commerce area in recent years. To foster the growth of cross-border e-commerce and to use RMB as pricing and payment currency, China can use its accumulated experience and advantages in e-commerce, logistics, and express provision. The websites for cross-border e-commerce will turn from the current dollar rates into double-currency pricing for the Dollar-RMB prices. It will increasingly make the RMB the largest cross-border electronic trade denominational currency. Payment systems at home will take advantage of the opportunity to develop mobile payment apps and to provide services focused on cultural traditions and payment patterns of countries along the BRI. Mobile payment is convenient, safe, and efficient to promote RMB payment in cross-border e-commerce.

8.2. Encourage the internationalization of RMBs with large ODI

The rising Outward direct investments (ODIs) are not only beneficial to China’s economy in the new era of economic development, but also economic globalization and the internationalization of the RMB. ODI in China reached USD 129.83 billion in 2018 and grew by 4.2 percent year-on-year (Xinhua, Citation2019). The host country is prepared to accept the RMB due to the large amount. Providing businesses consistently continue to use the RMB as the foreign currency; the position of the RMB in global direct investment is likely to increase directly.

Most of the BRI countries have inadequate resources and substantial funding deficits, while China has a high potential for building infrastructure and a comparative abundance of capital and ample and required foreign investment conditions. In constructing infrastructure construction projects urgently needed along the BRI, China can use its competitive advantages to reduce building costs and risk at exchange rates by equipment, technology, management, and labour. Further private capital will also be drawn to participate in the BRI project, and eventually turn from the Dollar-RMB dual currency price to the RMB through financial institutions like the AIIB, the BRICS Development Bank, the Silk Road Fund (SRF), and the Shanghai Cooperation Organization Development Bank.

On 24 October 2014, the AIIB was jointly founded by China and 21 other nations, for which China contributed 50 percent (Sun, Citation2015). Also, President Xi announced on 8 November that China is spending USD 40 billion in setting up the SRF (Yang, Citation2016). The establishment of AIIB and SRF not only created a new model of regional financing cooperation but also fulfilled the enormous demand for Asian connectivity, which effectively addresses the investment gap in Asian infrastructure and encourages regional economic and financial inclusion. When AIIB issues RMB loans for developing nations in Asia, these loans will be used for acquiring Chinese machinery and equipment or paying for Chinese construction facilities, etc. This approach helps promote the settlement of RMB trade and decreases the cost of foreign currency clearing trades, and local investors can even hold certain RMB and financial assets purchased in RMB. Therefore, China has put out its internationalization policy for the RMB. The key goal is to facilitate the use of the RMB in settlements and RMB-denominated financial transactions and create a global RMB network, which will provide more impetus for the general use of RMB, thus continually creating a favorable environment for RMB internationalization.

8.3. Additional develop the exchange rate mechanism for RMB

The steady RMB exchange rate encourages RMB currency substitution and is, without a doubt, a significant assurance for fostering RMB internationalization.

First, the process for the exchange rate improvement must be strengthened, and the exchange rate of the RMB must be raised to become more stable and more visible to the market. The exchange rate fluctuation spectrum should also be broadened, market awareness of exchange-rate risk management should be strengthened, and businesses and organizations should be encouraged to adhere to the exchange rate index of the RMB.

Second, from managed floating systems to free-floating, and from direct interventions to indirect ones should gradually be transformed into an RMB exchange rate arrangement. The method of achieving the policy objective on exchange rates should be changed. Market arbitration would encourage a return to the exchange rate’s long-term equilibrium. China’s central bank would thus have to eliminate its conventional direct intervention but still have to prevent a broad range of adverse effects on the financial market and the real economy from the excessive exchange rate volatility.

Steps must be taken to stabilize RMB exchange rates, improve market participant engagement, enhance the legitimacy and productivity of government policy, and ensure the core stability of RMB exchange rates at a balanced level by mixing monetary policy, fiscal policy, and the revenue policy. Simultaneously, when the foreign exchange market is experiencing speculative shocks or financial crises, policies should be taken to intervene in the foreign exchange and capital markets, so the rate of exchange of the RMB is still stable.

8.4. Additional improve the domestic finance mechanism and financial infrastructure of China

It is focused on a relatively mature and established financial system for the complete opening of the capital account. From a national perspective, the Chinese government will develop China’s domestic financial system and build a multi-level, secure, competitive capital market quickly, provide RMB and instruments for company financing and payment transactions, and transaction costs and risks for companies and investors.

The RMB cross-border payment and settlement system must be improved and improved from an international perspective, and the convenience and attractiveness of RMB improved. China’s central bank should further extend bilateral trade agreements with the BRI, broaden the offshore RMB sector, develop an RMB winding-up system in investment and funding countries and regions where the RMB is involved, and encourage the use of RMB in trade and infrastructure project pricing and settlement through the BRI.

8.5. Further caution in free capital account and growth of the offshore RMB industry

If the domestic financial sector of Chinese finance has not been developed, the system of financial regulation remains flawless, and the capital account cannot be opened unnecessarily with the restricted way of addressing cross-border capital stocks. Maintaining effective management of the capital account will ensure an affordable range of capital shocks and prevent the recurrence of crises such as the Asian financial crisis of 1998.

The RMB offshore market’s central role must be maintained by freeing up the capital account. The global offshore market RMB is being further broadened, the RMB is being actively promoted in international multilateral financial bodies, and monetary integration is being stepped up in international bodies, such as AIIB, Silk Road Fund, and IMF. These measures will extend RMB trading coverage around the world and consolidate the RMB’s important international market position. Hugangtong must build the international capital market of RMB with the RMB must be formed, and Hong Kong must be the hub of financial exchange for its capital account.

9. Internationalization of RMB implication

Along with the above prospect, there are also some consequences of RMB internationalization. One of the adverse effects is that Chinese exports will be less competitive and relatively cheaper as Renminbi prone to revaluation if the currency is internationalized. Current accounts in China may deteriorate, with a decrease in trade surplus. Second, currency internationalization would change the monetary policy of the issuer and reduce the power of policymakers to manage the based currency and regulate the domestic economy. Given the dilemma between the internal and external balance in the different functions of the currency when it becomes international, the more RMB is held overseas, the more difficult is the implementation of domestic financial policies (Zou et al., Citation2015).

Similarly, the global downturn and inflation can be carried on to China at any time due to the absence of monetary barriers. According to Keynes, the demand for money is split up into three type—transactionary, precautionary and speculative (Agarwal, Citation2018), besides which, another is called investment motives in the RMB internationalization process. Such motives have resulted in rising demand for RMB, therefore, while its supply remains constant, the demand curve continuously shifts to the upper right, and the interest rate tends to rise. Additionally, it will affect domestic price level stability. Unless the central bank of China takes the increase in external demand for RMB fully into account in the supply of money, China’s price level will remain on the decline, and finally, there will be deflation. The internationalization of RMB could also have further potential drawbacks including the increase in the long-term appreciation of the RMB exchange rate, producing the imbalance of international payments, influencing the effect of regulation on capital projects, raising the risk of domestic financial institutions management, and so forth. To achieve the right to speak at global financial markets, China needs to take part in the internationalization of currencies and to continue improving domestic financial markets and continually increasing the ability to withstand risks at the same time.

10. Conclusion

This paper analyses the nexus of BRI and the internationalization of RMB. The BRI and affiliated financial entities such as the BRICS New Development Bank and the AIIB serve as an essential goal of China to encourage the use of the RMB as a tool for trade. China has long been a strategic goal for internationalizing RMBs, but in the past, trading volumes and the limited convertibility of the Renminbi worked against that. The internationalization conditions are now more favourable with the BRI.

The status of RMB internationalization is: (1) In just a few years, the RMB Internationalization index has grown considerably. Since 2010, the internationalization of RMB has expanded rapidly. The RMB internationalization measure is still at relatively low levels, well below the dollar and the pound, equivalent to the Japanese Yen and the Dollar, although compared to the major international currencies, the difference is slowly decreasing. (2) Generally, China’s settlement currency cross-border exchange with RMB has fluctuated mainly because of international economic growth, US economic policies, RMB’s participation in SDR, and BRI. At the international level, cross-border exchange in settlement currencies using RMB is low, but at the regional level, the share of the BRI countries is relatively high. (3) The financial transactions of RMB heavily influence Chinese government strategies. The Chinese Currency Authority’s capital regulations are apparent. The RMB exchange rate is another critical factor in RMB internationalization. The RMB depreciation predictions will reduce the confidence of investors and thus raise the RMB’s international coverage. (4) A significant milestone in history is RMB incorporation into SDR. It implies above all that the IMF has stated publicly that the RMB is a widely available currency. It will help strengthen RMB’s international confidence, further leverage RMB’s financial trading, and reserve asset functions, and promote RMB’s internationalization. While the RMB internationalization has made some progress, the RMB’s global foreign exchange reserve size and share remain limited. (5) The restructuring of the exchange rate system of RMB has proceeded, and in the last few years, the exchange rate index of RMB has remained stable.

Since 2009, the Chinese government has pledged to support RMB internationalization. China has taken several concrete steps to encourage RMB internationalization, including the launch of Hugangtong to open capital market, the expansion of the RMB offshore sector, the advent of CIPS, restructuring the RMB exchange rate structure, introducing RMB’s crude oil futures and so on. Incorporating RMB into SDR, the BRI, and developing AIIB both lead to further RMB internationalization.

On the one hand, the BRI allows the RMB to be a global trade currency, and RMB’s position as an international currency is further strengthened. The RMB has a great potentiality to be a significant currency in the BRI from the perspective of economic development, economic risks, development of the domestic market for the financial market, trade scale, and cross-border consumption. Meanwhile, the RMB will play a significant role in China’s BRI cooperation with countries to facilitate cross-border trade, minimize exchange rate risk, finance RMB financing for major BRI building projects and boost the credibility of the BRI area. There are some implications which China has to bear. However, China needs to involves in the internationalization of currencies and to continue improving domestic financial markets and continually increasing the ability to withstand risks at the same time.

Several theories can evaluate the internationalization of RMB. This study focuses primarily on structural institutionalism to explore how China should facilitate economic cooperation with the BRI countries aimed at accelerating the internationalization of RMB. Given its high explanatory potential for the position of the international system in promoting inter-State cooperation, the study focuses on neoliberal institutionalism to examine the possibilities and challenges of RMB internationalization by cooperation between China and BRI nations, and financial cooperation. The critical role of BRI and AIIB in the internationalization of the RMB is therefore needed to be demonstrated. However, the study is confined to the BRI countries and those with currency internationalization backgrounds, such as the US, UK, and Japan. Although the internationalization of RMB was innovative since the late-2000s, the research period was limited from 2008 onward as the 2008 global financial crisis was the official starting point for RMB internationalization.

Additional information

Funding

Notes on contributors

Bora Ly

Bora LY is a senior lecturer at the Paññāsāstra University of Cambodia. Recently graduated from Nanyang Technological University, Singapore. The research interests include Chinese political economy, Sino-EU, Foreign Policy of China, BRI, and global government.

References

- ADB. (2017). Meeting Asia’s infrastructure needs. Manila. Retrieved from https://www.adb.org/publications/asia-infrastructure-needs

- Agarwal, P. (2018). Liquidity preference theory. Retrieved 11 March 2020, from https://www.intelligenteconomist.com/liquidity-preference-theory/

- AIIB. (2019). Members and prospective members of the bank. Retrieved 11 January 2020, from https://www.aiib.org/en/about-aiib/governance/members-of-bank/index.html

- Belt and Road News. (2019). Joint communique of the leaders. Retrieved 11 January 2020, from https://www.beltandroad.news/2019/04/28/joint-communique-of-the-leaders/

- Calvo, G. A., & Vegh, C. (1992). Currency substitution in developing countries: An introduction.

- Chamorro, D. (2017). Belt and road: China’s strategy to capture supply chains from guangzhou to Greece. Retrieved 11 January 2020, from https://www.forbes.com/sites/riskmap/2017/12/21/belt-and-road-chinas-strategy-to-capture-supply-chains-from-guangzhou-to-greece/#fb09ef623708

- Chen, S. (2014). Open a new pattern of RMB internationalization. China Finance, 24, 14–21.

- Chetty, V. K. (1969). On measuring the nearness of near-moneys. The American Economic Review, 59(3), 270–281.

- Cohen, B. J. (1971). Future of sterling as an international currency.

- Eichengreen, B., & Frankel, J. A. (1996). On the SDR: reserve currencies and the future of the international monetary system (No. C96-068). University of California at Berkeley.

- Grassman, S. (1976). Currency distribution and forward cover in foreign trade: Sweden revisited, 1973. Journal of International Economics, 6(2), 215–221. https://doi.org/10.1016/0022-1996(76)90014-3

- Han, S. (2019). China: Net overseas direct investment volume 2018. Retrieved 13 January 2020, from https://www.statista.com/statistics/658742/china-net-overseas-direct-investment-odi-volume/

- Huaxia. (2019). Spotlight: BRI participating countries reap benefits after 6 years’ joint construction – Xinhua. Retrieved 11 January 2020, from http://www.xinhuanet.com/english/2019-09/14/c_138391095.htm

- IMF. (2019). Currency Composition of Official Foreign Exchange Reserves (COFER). International Financial Statistics (IFS).

- International Monetary Institute. (eds 2018). Currency Internationalization and macro-financial risk control. Palgrave Macmillan.

- International Monetary Institute, Renmin University of China (RUC). (2015). IMI Research Report No. 1501 [EN]. RMB Internationalization Report 2015 Press Release.

- International Monetary Institute, Renmin University of China (RUC). (2017). IMI Research Report No. 1702 [EN]. RMB Internationalization Report 2017 Press Release.

- Jianjun, L., Feng, Z., & Xiqiang, C. (2013). The status quo, development stages, and outlook evaluation for RMB internationalization. Studies of International Finance, 10.

- Kennedy, S. (2015). The RMB joins the SDR: Historic inch-stone in global financial system. Retrieved 13 January 2020, from https://www.csis.org/analysis/rmb-joins-sdr-historic-inch-stone-global-financial-system

- Keohane, R. O., & Nye, J. S. (1977). Power and interdependence.

- Kindleberger, C. P. (1967). The politics of international money and world language. International Finance Section, Department of Economics, Princeton University.

- Kubarych, R. M. (1983). Foreign exchange markets in the United States. Federal Reserve Bank of New York.

- Li, Y., & Matsui, A. (2005). A theory of international currency and seigniorage competition. CIRJE, discussion paper n. F–363.

- Lin, L., & Wang, S. (2015). Construction of the belt and road initiative and the internationalization of the RMB. International Political Economy, (15).

- Liu, L., & Li, D. D. (2008). RMB internationalization: An empirical and policy analysis. Journal of Financial Research, 11(4).

- Modelski, G. (1986). After hegemony: Cooperation and discord in the world political economy. By Robert O. Keohane. (Princeton: Princeton University Press, 1985. Pp. 290). American Political Science Review, 80(2), 724–726. https://doi.org/10.2307/1958347

- Mundell, R. A. (1961). A theory of optimum currency areas. The American Economic Review, 51(4), 657–665.

- Olsson, D., & Fei, A. (2018). Why international use of RMB is about to be propelled. Retrieved 11 January 2020, from https://www.kwm.com/en/au/knowledge/insights/why-international-use-rmb-will-increase-20180404

- Ozeki, Y., & Tavlas, G. S. (1992). The internationalization of currencies: an appraisal of the Japanese yen (No. 90). International Monetary Fund.

- Park, Y. C., & Takagi, S. (2012). Managing capital flows in an economic community: The case of ASEAN capital account liberalization.

- People’s Bank of China. (2019). RMB internationalization report 2019. Retrieved 11 January 2020, from http://www.pbc.gov.cn/en/3688241/3688636/3828468/3830455/3938217/index.html

- Que, C., & Ma, B. (2013). Has RMB been the anchor currency——Empirical evidence based on state space model. Finance & Trade Economics, (4), 7.

- Shams, R. (2005). Dollar-euro exchange rate 1999-2004-dollar and Euro as international currencies.

- Silver, C. (2019). Top 20 economies in the world. Investopedia. Retrieved 13 January 2020, from https://www.investopedia.com/insights/worlds-top-economies/

- Sun, C. R., Zhang, N., & Liu, Y. Y. (2017). The ‘Belt and Road’ initiative and China’s trade growth with countries along the route. Journal of International Trade, 2, 83–96.

- Sun, Y. (2015). China and the evolving Asian infrastructure investment bank. Asian Infrastructure Investment Bank: China as Responsible Stakeholder, 27–42.

- Tappe, A. (2018). Global dollar reserves slip to 4-year low in the 4th quarter of 2017, IMF data show. Retrieved 13 January 2020, from https://www.marketwatch.com/story/global-dollar-reserves-slip-to-4-year-low-in-4th-quarter-of-2017-imf-data-show-2018-04-02

- Xinhua. (2019). China’s ODI sees stable development in 2018. Retrieved 11 January 2020, from http://www.xinhuanet.com/english/2019-01/16/c_137749000.htm

- Yang, H. (2016). The Asian infrastructure investment bank and status-seeking: China’s foray into global economic governance. Chinese Political Science Review, 1(4), 754–778. https://doi.org/10.1007/s41111-016-0043-x

- Yuan, S. G., & Xu, D. M. (2014). An empirical analysis of influencing factors of RMB cross-border trade settlement under appreciation. Journal of Guangdong University of Finance & Economics, (1), 3.

- Zou, J., Liu, C., Yin, G. Q., & Tang, Z. (2015). Spatial patterns and economic effects of China’s trade with countries along the Belt and Road. Progress in Geography, 34(5), 598–605.

- World Bank Database. (n.d.). Retrieved 13 January 2020, from https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2017&slocations=CN&sstart=2008