?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the effect of bank-specific and macroeconomic key determinants of Islamic retail banks profitability in Bahrain. It used panel data of six Islamic retail banks from 2013 to 2019, and it employed an explanatory research with secondary financial data. Return on Assets (ROA) and Return on Equity (ROE) are two main profitability measures are used in this study. Random effect regression model and Fixed effect regression model are the two statistical models adopted in this study. Random effect regression model shows that Bank size is significantly positively related to banks’ ROA, while operating efficiency and GDP growth have significant and negative relationship with banks’ ROA. Fixed effect regression model shows that there are negative significant effects of credit risk, operating efficiency and GDP growth rate on banks’ ROE. Finally, inflation rate has positive and statistically significant effect on both ROA and ROE. The study recommends that Islamic banks in Bahrain should achieve full benefits form economics of scale, should concentrate on credit risk management, especially on the control and monitoring of non-performing loans. In addition, managers should focus more on modern credit risk management techniques. Finally, Bahraini policy makers must boost the development of the equity market in order to improve bank’s profitability.

STATEMENT OF PUBLIC INTEREST

It is very important to know the determinants of profitability position in any institution, especially banks. Previous researches show two main factors; internal factors related to the bank itself and external factors related to the economic performance of the state. In this paper, researchers attempt testing which factors have more effect on banks’ profitability. They selected data of six Islamic retail banks in Bahrain over the period 2013–2019. Because banks’ profitability is measured by financial ratios such as Return on Assets (ROA) and Return on Equity (ROE), the current study findings show that operating efficiency, credit risk (internal factors) and Gross Domestic Product (GDP) growth rate (an external factor) are significantly negatively related to banks’ ROA and ROE, while bank size and inflation rate are significantly positively effective.

1. Introduction

Profitability is one of the main indicators of Banks’ performance, where it reflects the quality of a bank’s management shareholders’ behaviour, the bank’s competitive strategies, efficiency and risk management capabilities (Samad, Citation2016). Banks’ profitability means the ability to generate revenues more than costs, in relation to bank’s capital base. Identifying the key determinants of bank’s profitability could help to evaluate bank operations and improve bank management (Masood et al., Citation2015).

There is a wealth of literature conducting in relation to bank profitability, some studies concerned on profitability measures (e.g. Masood et al., Citation2009; Al-Smadi and Al-Wabel, Citation2011).

Other studies aim the key factors affecting bank’s profitability. For instance, some studies investigated the relationship between capital adequacy ratio and ROE (e.g. Berger, Citation1995; Masood & Ashraf, Citation2013). While other studies focussed on the relationship between capital adequacy and bank size with ROA (e.g., Alshatti, Citation2016; Karim et al., Citation2010; Trujillo-Ponce, Citation2013) or tested the effect of operating efficiency, bank size and financial leverage on ROA (e.g. Ahmed et al., Citation2011; Mirzaei et al., Citation2013). Some researchers examined the impact of inflation on bank profitability (e.g. Revell, Citation1979; Al-Smadi and Al-Wabel, Citation2011); while other researchers tested the effect of macroeconomic factors on banks profitability (e.g. Wasiuzzaman & Tarmizi, Citation2010; Karim et al., Citation2010; Ramadan, Citation2011; Masood & Ashraf, Citation2013; Petria et al., Citation2015).

It could be argued that there is a shortcoming or limitations in these studies, where most of the them examined the relationship between one to three independent factors and banks’ profitability. These methods used by previous studies test the determinants of profitability from narrow or limited point of view. Moreover, these studies rely on one indicator of profitability, either ROA or ROE. Thus current study intends to fill the gap by studying the impact of a large set of internal and external factors (capital adequacy, bank size, credit risk, financial leverage, GDP growth rate and inflation rate) on banks’ profitability measured by both ROA and ROE. Furthermore, there is no study that tried to test all these factors on Islamic retail banks’ profitability in Bahrain, according to the authors’ knowledge. The banks under focus in this study will benefit from this research because it will provide a useful analysis of how they are functioning and what are they need to improve their future profitability’ rates.

Islamic banking is defined as “A method of banking or banking movement that is based on Shariah principles and Islamic principles” (Abduh & Idrees, Citation2013). Therefore, Islamic banks allocate most of their resources to contracts based on three different logics: the logic of sharing, the logic of commercial anchoring or participation, and finally the logic of beneficence. Among the financial products offered, the best known are the Murabaha, the mudaraba, the moucharaka and the ijara(Boukhatem & Moussa, Citation2018).

The Islamic banks have particularly advanced and developed in oil-exporting nations since 1975 to profit from surplus wealth that arises from significant increases in oil prices. Bahrain is one of the leading centres in the world banking sector, specifically in Islamic finance. Islamic banking in Bahrain was established in 1979, which makes Bahrain an important reprehensive of Islamic finance. The Bahraini banking system consists of conventional and Islamic financial institutions that include (29) retail banks, (70) wholesale banks (2) specialised banks in addition to representative offices of foreign banks. Sharia compliant products are offered by (6) retail banks and (18) wholesale banks. Financial markets of the country have moved towards growth mainly due the high performance of Islamic retail banks (Central Bank of Bahrain, Annual report,2019).

The motivation of this study is to understand the main exogenous and endogenous factors/determinants that led to the remarkable growth of Islamic banks in Bahrain, and directly impacted the overall economic performance of Bahrain.

Accordingly, the study attempts to examine the effect of endogenous and exogenous variables on Six Islamic retail banks’ profitability by employing panel data regression models over the period 2013–2019, the selected banks represent 35% of total Islamic banks in Bahrain.

The rest of the study is organized as follows: Section two reviewing the previous studies. Data, hypotheses and methodology are presented in section three. Empirical results and findings are provided in section four, conclusion and policy implications are discussed in section five.

2. Literature review

The analysis of the literature emphasizes the existence of a significant number of empirical studies that focus on investigating the factors that impact the bank profitability. Table illustrates various factors and variables used in literature review.

Table 1. Summary of key factors used to determine of Bank profitability in previous studies

The early study seeks to identify the profit determines conducted by Short (Citation1979) who collects data from (60) banks. The author concludes that banks’ assets growth and concentration at the domestic banking market have a significant positive effect on banks’ profitability. While Bourke (Citation1989) concludes that there is a direct relationship between capital ratio and bank profitability, where high capital ratio leads to an increase in bank’s profit.

Berger (Citation1995) studies a group of banks in the USA during the period (1983–1992) to investigate the relationship between ROE and capital adequacy ratio. Berger finds that there is a significant relationship between these two variables. The study of Duca and McLaughlin (Citation1990) finds that the fluctuations in bank profitability and its performance are highly correlated with the credit risk dissimilarity, where raising bank exposure to credit risk will decline the bank’s profitability.

Karim et al. (Citation2010) study a sample of (9) African Islamic banks over the period (1999–2009), their study points out that capital adequacy and bank size have positive and significant effects on ROA. The same results were obtained by Trujillo-Ponce (Citation2013) when they used a sample of (89) banks including (28) commercial banks, (45) savings banks and (16) credit cooperatives. The author concludes that capital adequacy directly affects banks’ profitability in the long term.

Ahmed et al. (Citation2011) investigate the profitability determinants of Pakistani commercial banks over the period (2006–2009). The regression outcomes show that operating efficiency, bank size and financial leverage have significant positive influences on profitability measured by ROA. Mirzaei et al. (Citation2013) find the same outcomes when they conduct a study on (26) banks listed on Dhaka Stock Exchange from 2008 to 2011. Al-Tamimi and Charif (Citation2011) discover a direct relationship between ROA and operating efficiency, when they use annual reports of (38) banks in the UAE during the period (1996–2005).

Masood and Ashraf (Citation2013) argue that the risk assessment could be performed using capital adequacy to determine the profitability position of Islamic banks in Asia and Africa. The authors use data from 2006 to 2010, and they find a positive relationship between capital adequacy and profitability of banks. Aggarwal (Citation2016) concludes that there is a significant positive relationship between financial leverage and ROA, when the author uses data of (27) Indian banks. Alshatti (Citation2016) uses balanced panel data set of (13) banks in Jordan over the period (2005–2014). The author finds that capital adequacy and financial leverage positively affect the profitability; therefore, rising bank’s profitability is associated with well-capitalized banks accompanied with high capital adequacy.

Revell (Citation1979) examines the relationship between inflation and bank profitability. The author concludes that the effect of inflation rate on bank profitability might be insignificant, if there is an accurate predicting of inflation, which will help banks to manage their operating expenses. Al-Smadi and Al-Wabel (Citation2011) collect data from (15) Jordanian banks during the period 2000–2010 in order to test the effect of inflation rate as an exogenous factor on the long-term performance and profitability. The authors conclude that high inflation rates adverse effects on profitability, due to declining in household savings.

Other authors use the annual data of Islamic banks operating in Malaysia and Jordan to test the effect of macroeconomic variables (e.g. Masood & Ashraf, Citation2013; Ramadan, Citation2011; Wasiuzzaman & Tarmizi, Citation2010). The regression’s outcomes show that macroeconomic variables have significant positive effects on profitability of Islamic banks. Petria et al. (Citation2015) apply quite a similar methodology to European banks. They state that there are external or macroeconomic factors having direct impact on profitability of commercial banks; therefore, the policy makers should focus on economic conditions of a country in which a particular bank is operating. Karim et al. (Citation2010) show that higher economic growth and inflation lead to an increase in the profitability of different Islamic banks operating in Africa during (1999–2009). In the same vein, Karim et al. (Citation2010) conclude similar findings in Islamic banks in African’s context.

Poposka and Trpkoski (Citation2016) use data from different financial reports of commercial banks in the Balkan region. The authors find that there is a significant and positive relationship between GDP growth and ROE of banks. On the contrary, other studies (e.g. Sufian & Parman, Citation2009; Abduh & Idrees, Citation2013) conducted on Malaysian banks find a significant negative effect of GDP growth on banks’ profitability due to the economy downturns, where the default risk is higher. Kohlscheen et al. (Citation2018) analyse key determinants of bank profitability based on the evolution of balance sheets of (534) banks from (19) emerging market economies. The authors find that higher long-run interest rates tend to boost profitability, while higher short-run interest rates reduce profits by raising funding costs. Moreover, during regular times credit growth tends to be more important for bank profitability than GDP growth.

3. Data, hypotheses and methodology

3.1. Data

The Bank-specific variables being examined in this study are derived from both income statements and balanced sheets of six Islamic banks (Ithmaar Bank (ITHB), Al Baraka Bank (ALBB), Kuwait Finance House (KFH), Bahrain Islamic Bank (BISB), Al Salam Bank (ASB) and Khaleeje Commercial Bank (KHCB)) that were published in the Bank-Scope database. The data set covers 7-year period from 2013 to 2019. Due to data availability issues, the study conducted on only six Islamic banks which represent 35% of Islamic banks in Bahrain. The country’s macroeconomic indicators including economic growth and inflation rate (2010 = 100) are obtained from the International Monetary Fund’s (IMF) website, in addition to the annual reports of Central Bank of Bahrain (CBB).

The study uses ROA and/or ROE as dependent variables and seven independent variables; namely capital adequacy, bank size, financial leverage, credit risk, operating efficiency, inflation and GDP growth rate. Table shows a brief description of these selected variables.

Table 2. Variables in this study

Descriptive statistics of different variables are shown in Table . It indicates the variability of most of the variables under study, where the value of standard deviation of bank size is the least followed by GDP growth rate. Platykurtic distribution (or negatively skewed) Leptokutic distributions and the results of Jarque-Bera normality test illustrate the non-normality of the study variables. Despite that the mean values of ROA and/or ROE were almost negative in different years during the study period, the time trend shows some improvement in its values.

Table 3. Statistical properties of the variables

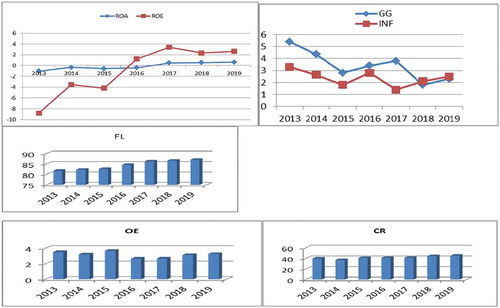

The profitability indices and bank-specific variables have different trends, where capital adequacy (CA) of retail Islamic banks declined and started to increase in year 2017. Bank size (BS), credit risk (CR) and financial leverage (FL) began to increase in 2015. GDP growth rate (GG) declined from 5.4% in 2013 to 2.3% in 2019, while the value of inflation rate (INF) was almost 2% over the study period. The trend of mean values of the variables is shown in Figure .

Figure 1. Mean values of the study variables over the period 2013–2016.

3.2. Hypotheses and methodology

The current study aims at testing the following two hypotheses:

H0: Profitability of Islamic retail banks operating in Bahrain is not affected by bank-specific variables and macroeconomic factors.

H1: Bank-specific variables and macroeconomic factors are expected to have significant relationship with Islamic banks’ Profitability.

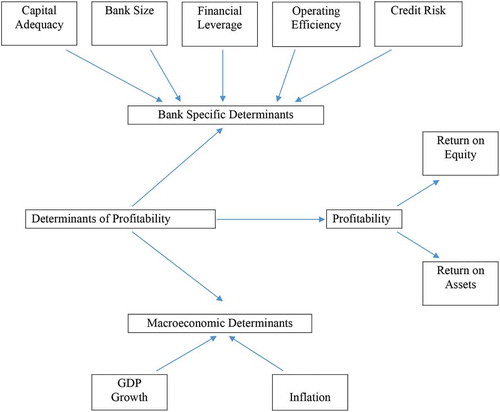

The hypotheses’ development is based on the following conceptual framework shown in Figure .

According to the above-cited literature and hypotheses, consider the following panel data model with unobserved bank-specific effects:

Where:

Yi.t: the profitability of bank (i) at time (t),

β: Vertical vector (K x1) of the estimated parameters for each independent variable,

Xi,t: the matrix (Tn x K) of the independent variables that affect the profitability of bank (i) at time (t),

€i,t: the vertical vector (Tn x 1) of the random error term of bank (i) at time (t).

This panel data are commonly used because it gives more informative data as it consists of both cross-sectional information, which captures individual variability, and the time series information, which captures dynamic adjustment. Moreover, it allows the studying of impact of macroeconomic and financial industry development on profitability after controlling bank-specific characteristics, with less collinearity among variables and more degree of freedom and greater efficiency. In panel data regression techniques, there are two models, Fixed effect model and Random effect model (Sarafidies & Wansbeek, Citation2020).

The study includes two dependent variables, which are ROA and ROE, in addition to seven independent variables which are: Capital adequacy (CA), bank size (BS), financial leverage (FL), credit risk (CR), operating efficiency (OE), inflation (INF) and GDP growth (GG). Accordingly, two regression equations estimated, namely:

The authors expect that capital adequacy, bank size, financial leverage, operating efficiency, and GDP growth affect banks’ profitability positively, while credit risk and inflation rate affect banks’ profitability negatively.

Before regressing Equationequations (2)(2)

(2) and (Equation3

(3)

(3) ), the study examines the properties of time series for each variable over the study period, and determine the order of integration by employing two panel data Unit Root tests which are Levin, Lin and Chu (Citation2002) test or (LLC test), and Im et al. (Citation2003) test or (IPS test). We briefly explain both as follows:

3.2.1. Levin, Lin and Chu (LLC) test

The LLC test includes three models for testing the existence of unit root, the first model does not have intercept, nor time trend, while the second one includes only intercept but no time trend, and finally the third one includes both intercept and time trend, as shown in Equationequations (4)(4)

(4) , (Equation5

(5)

(5) ) and (Equation6

(6)

(6) ) respectively (Jaroslava & Martin, Citation2005, pp. 7–8):

The three models assume the independence of error term. LLC suggests testing the following hypotheses:

H0: p = 0, H1: p < 0 (model 1)

H0: p = 0, αi = 0, for i = 1,2,3 … … N (model 2)

H1: p < 0, αi ϵ Ʀ, for i = 1,2,3 … … N

H0: p = 0, ßi = 0, for i = 1,2,3 … … N (model 3)

H1: p < 0, ßi ϵ Ʀ, for i = 1,2,3 … … N

3.2.2. Im, Pesaram and Shin (IPS) test

The IPS test uses a likelihood framework and it proposes a new flexible and simple computation procedure for panel unit root test by using the T-bar statistics. This procedure is approved for both stationary and non-stationary series. On the other hand, IPS allows for correlation of serial residual and heterogeneity of the dynamics in addition to variances of error cross groups (Im et al., Citation2003, pp. 53–74). The IPS test is based on the following formula:

IPS presents the individual-effects model with no time trend, and it examines the following hypotheses:

H0: pi = 0 for i = 1,2,3 … … N

H1: pi < 0 for i = 1,2,3 … … N

pi = 0 for i = Ni+1, Ni+2, … … N

After using both LLC and IPS tests to determine the degree of integration of selected variables, we estimate Equationequations (2)(2)

(2) and (Equation3

(3)

(3) ) by using Fixed Effect Model (FEM) and Random Effect Model (REM).

Hausman Test is employed to determine which model (FEM or REM) is more appropriate by identifying the endogeneity present in independent variables. The null hypothesis (H0) based on the appropriate model is REM, which means there is no correlation between independent variables and error terms in the panel data model. The alternative hypothesis (H1) assumes that the appropriate model is FEM, and there is a statistically significant correlation between independent variables and error term in panel data. (Bell et al., Citation2019)

After applying the Hausman test, the computed Hausman statistics are compared with the critical values for the X2 distribution for k degree of freedom. If the Hausman statistics are bigger than its critical value, or p-value < 0.05; the null hypothesis is rejected. Although random effect is preferred due to its higher efficiency, the Fixed effect method is more consistent and suitable when Error terms are not correlated with regressors (Paul et al., Citation2010).

4. Empirical results

4.1. Stationarity tests

The results of LLC and IPS tests are shown in Table . LLC test shows that all the study variables have no unit root at the level where the p value < 0.05. This means authors reject the null hypothesis and the variables time series are stationary at level and integrated at zero I(0). The IPS test implies that the time series are non-stationary at level, but it is stationary at first difference which means they are integrated of 1 or I (1).

Table 4. Results of panel unit root tests

Before conducting the regression analysis, the panel data for Islamic retail banks in Bahrain is tested for robustness and possible occurrence of multicollinearity. Correlation matrix checks the correlation between the independent variables. If the correlation coefficient between two variables is close to 1, then it is an indication of multicollinearity. The Variance Inflation Factor is also established, where the value for each independent variable is compared with the benchmark of five. If its value is greater than five; then there is multicollienerity in data and one independent variable should be excluded from the model.

Table shows that the correlation coefficient between financial leverage (FL) and capital adequacy (CA) is almost 1 and significant, whereas p value < 0.05. This suggests there is a high inverse correlation between them. Moreover, the value of Variance Inflation Factor (VIF) between (FL) and (CA) exceeds five, as shown in Table . When (FL) variable is excluded from the model, the (VIF) value of (CA) would be low; therefore, (FL) variable will be excluded from both models.

Table 5. Covariance analysis

Table 6. Variance inflation factor

4.2. Estimating models

Table shows the regression results of Fixed effect and Random effect models for Equationequations (2)(2)

(2) and (Equation3

(3)

(3) ). The appropriateness of each model is determined by means of the Hausman test. The p-value in Hausman test < 0.05 in ROA regression model, which means rejecting the null hypothesis; thus, Fixed effect model is the appropriate model for the panel data. In ROE regression model the Hausman test indicates that p> χ2 is higher than 0.05, which indicates that the coefficients estimated by Random effect regression are appropriate to show the relationship between ROE and the independent variables.

Table 7. Estimation of the model

According to the results shown in Table , the effect of growing bank size is significantly positively related to Islamic retail banks’ profitability at 5% significant level measured by ROA, while it has insignificant effect on ROE. This finding is consistent with the studies by Masood and Ashraf (Citation2013) and Eljelly (Citation2013). This implies that banks with high asset value are expected to achieve high profitability. However, high return is attributed to high-risk accepted by financial institutions. Therefore, an increase in bank size implies high risk involved in a bank as suggested by Al-Smadi and Al-Wabel (Citation2011).

Operating efficiency variable has a negative and significant relationship with banks’ profitability at the confidence level of 95% for both ROA and ROE. This means that the Islamic banks increased their operating costs to manage its total assets which negatively affect its profitability. The coefficients indicate that operating efficiency has greater effect on ROA compared to ROE. This finding is consistent with Karim et al. (Citation2010) and Eljelly (Citation2013).

The relationship between ROE and credit risk is significantly negative. This means improper credit risk management will increase the allowance for credit losses which reduces banks and stockholders’ profitability. The relationship between ROA and credit risk is negative and insignificant. This finding contradicts with the result obtained by Masood and Ashraf (Citation2013) who find a positive relationship between these two variables.

The study also finds a negative and significant relationship between banks’ profitability and GDP growth for both ROA and ROE. This finding coincides with Sufian and Parman (Citation2009) and Eljelly (Citation2013) studies, while it contradicts with the results obtained by Trujillo-Ponce (Citation2013) and Karim et al. (Citation2010) who concluded that economic growth enhances profits and that downturn adversely affects interest income. The negative relation between banks’ profitability and GDP growth in Bahrain during the study period might be due to Bahrain’s economy preferences, choice of depositing excess funds and taking loans, customers’ asymmetric information and lack of information regarding economic changes in Bahrain.

Finally, the study finds a significant positive relationship between Islamic retail banks’ profitability and inflation. The positive relationship implies that during inflation periods the income-increasing rate is higher than the cost-increasing rate which enhances profitability. This means that banks could more accurately forecast future change in inflation and they will be able to adjust both interest rates and margin at acceptable rates, which will increase their profits. However, when taking into consideration that Islamic finance does not deal with interest rates, authors assume that predicating the inflation rate will improve the banks’ decisions regarding the profit-sharing rates, loan quantity and asset quality.

Based on the findings above, Authors reject the null hypothesis (H0) which states that the profitability of Islamic banks is not affected by bank-specific and macroeconomic factors, and accept the alternative hypothesis (H1) at the confidence level of 95% which indicates that there is a joint effect of the independent variables on bank profitability, even though the capital adequacy variable is insignificant.

5. Conclusion and policy implications

This study investigates the profitability of Islamic retail banks and its determinants. Bank-specific and macroeconomic factors are considered to have influence on profitability. Two dependent variables were considered to measure banks’ profitability which are ROA and ROE. The study used the panel data of six banks over 7 years. The LLC and IPS panel unit root tests show that the time series are stationary and integrated at zero I (0) and one I (1) respectively.

The regression results of Fixed effect model and Random effect model show that bank size and inflation rate have direct and significant impact on ROA, while GDP growth rate has negative and significant effect on both ROA and ROE at the confidence level of 95% (α = 0.05). Credit risk and operating efficiency have insignificant negative effects on ROE, while capital adequacy has insignificant positive impact on both ROA and ROE. The findings of the study show that bank-specific and macroeconomic factors have significant effect on Islamic retail banks’ profitability during the study period.

In regards to policy implications, the study can draw some proposals. Since the bank size variable has signficant effect on profitability of Islamic retail banks; Islamic Banks in Bahrain should focus more on expanding the banks to achieve full the benefits of economics of scale. Due to the fact that inflation has positive significant impact on profitability; Islamic Banks should rely on more sophisticated forecasting models to predict future inflation in Bahrain. More accurate predictions of future inflation will help banks to improve their decisions regarding interest rates during inflation periods. Although Islamic finance does not adopt interest rates, more accurate prediction of inflation rates will enhance the rationality of decisions regarding profit sharing’s rates, loan quantity and assets quality. Moreover, Islamic Banks should concentrate on credit risk management, especially to control and monitor non-performing loans. In addition, managers should focus more on modern credit risk management techniques. Finally, Bahrain policy makers ought to recognize that improving banks’ profitability is associated with developing the Bahraini equity market.

This research faced several limitations such as the limited sample size due to data availability issues. Albeit the study relied on six banks representing 35% of Islamic banks in Bahrain across 7 years to increase the number of observations used for analysis. Lastly, the model adopted for this study focused on seven determinants of banks’ profitability determinants. Adding more bank’s profitability factors in the future research is highly recommended by authors to enhance and enrich the outcomes of their research.

Additional information

Funding

Notes on contributors

Mohamed Sayed Abou Elseoud

The authors’ research activities are economic policies, economic development, applied economics, financial markets, financial management, and organizations management. The purpose of the present study is identifying the determinants of profitability of Islamic banks in Bahrain. Since the performance of Islamic banks reveals a direct impact on the overall economic conditions of Bahrain, it is crucial to understand the reasons and factors that generate remarkable growth of Islamic banking in Bahrain. The banks under study will benefit from this research in that it provides analyses on how they are functioning at present and what they should do in the future. The adopted methodology and tools (e.g., panel data regression models) could be used for analyzing data of Islamic banks in other nations specially the Gulf Cooperative Council (GCC) countries. Meanwhile, the findings could be employed to make a comparison and contrasting Islamic and conventional banks.

References

- Abduh, M., & Idrees, Y. (2013). Determinants of Islamic banking profitability in Malaysia. Australian Journal of Basic and Applied Sciences, 7 (2), 04–16. http://irep.iium.edu.my/30037/1/Abduh_and_Yameen%2C_AJBAS_Feb_2013.pdf

- Abdullah, M., Parvez, K., & Ayreen, S. (2014). Bank specific, industry specific and macroeconomic determinants of commercial bank profitability: ACase of Bangladesh. World Journal of Social Sciences, 4(3), 82–96. https://www.researchgate.net/publication/320930850_Bank_Specific_Industry_Specific_and_Macroeconomic_Determinants_of_Commercial_Bank_Profitability_A_Case_of_Bangladesh

- Aggarwal, P. (2016). An empirical evidence determining profitability indicators of indian public sector banks. International Journal of Economic Perspectives, 10(2), 93–101. https://doi.org/10.5296/ijfar.v7i2.12211

- Ahmed, H., Ali, K., & Akhtar, M. (2011). Bank-specific and macroeconomic indicators of profitability: Empirical evidence from the commercial banks of Pakistan. International Journal of Business and Social Science, 2 (6), 235–242. Avaliable at http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.1065.7333&rep=rep1&type=pdf

- Alshatti, A. (2016). Determinants of banks’ profitability – The case of Jordan. Investment Management and Financial Innovations, 13(1), 84–91. https://doi.org/10.21511/imfi

- Al-Smadi, M., & Al-Wabel, S. (2011). The impact of e-banking on the performance of Jordanian Banks. The Journal of Internet Banking and Commerce, 1 (1), 1–16. http://www.icommercecentral.com/open-access/the-impact-of-e-banking-on-the-performance-of-jordanianbanks.php?aid=38255

- Al-Tamimi, H., & Charif, H. (2011). Multiple approaches in performance assessment of UAE commercial banks. International Journal of Islamic and Middle Eastern Finance and Management, 4(1), 74–82. https://doi.org/10.1108/17538391111122212

- Aslam, M., Inamullah, Ismail, M. (2016). Determinants Affecting the Profitability of Islamic Banks: Evidence from Pakistan. International Journal of Operations and Logistics Management, 5(2), 115–127. Retrieved from https://www.academia.edu/26943192/Determinants_Affecting_the_Profitability_of_Islamic_Banks_Evidence_from_Pakistan

- Bell, A., Fairbrother, M., & Jones, K. (2019). Fixed and random effects models: Making an informed choice. Quality & Quantity, 53(2), 1051–1074. https://doi.org/10.1007/s11135-018-0802-x

- Berger, A. (1995). The profit structure relationship in banking: Tests of market power and efficient structure hypotheses. Journal of Money, Credit, and Banking, 27(2), 404–431. https://doi.org/10.2307/2077876

- Boukhatem, J., & Moussa, F. (2018). The effect of Islamic banks on GDP growth: Some evidence from selected MENA countries. Borsa Istanbul Review, 18(3), 231–247. https://doi.org/10.1016/j.bir.2017.11.004

- Bourke, P. (1989). Concentration and other Determinants of Bank Profitability in Europe, North America and Australia. Journal of Banking and Finance, 13 (1), 65–79. https://doi.org/10.1016/0378-4266(89)90020-4

- Duca, J., & McLaughlin, M. (1990, July). Developments affecting the profitability of commercial banks. Federal Reserve Bulletin, 76(6), 477–499. https://EconPapers.repec.org/RePEc:fip:fedgrb:y:1990:i:jul:p:477-499:n:v.76no.7

- Eljelly, A. (2013). Internal and external determinants of profitability of Islamic banks in Sudan: Evidence from panel data. Afro-Asian Journal Of Finance and Accounting, 3(3), 222–240. https://doi.org/10.1504/AAJFA.2013.054424

- Ibrahim, S. (2017). The Impacts of Liquidity on Profitability in Banking Sectors of Iraq: A Case of Iraqi Commercial Banks. Journal of Finance & Banking Studies, 6(1), 113–121. doi: 10.20525/ijfbs.v6i1.650

- Idris, A., Hassan, F., Abdullah, N., Salim, N., Mustaffa, R., & Jusoff, K. (2011). Determinant of Islamic Banking Institutions’ Profitability in Malaysia. World Applied Sciences Journal, 12 (Special Issue on Bolstering Economic Sustainability), 1-7. Retrieved from http://citeseerx.ist.psu.edu/viewdoc/download?

- Im, K., Pesaran, M., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Economics, 115, 53–74. http://www.sciencedirect.com/science/article/pii/S0304-4076(03)00092-7

- Jaroslava, H., & Martin, W. (2005, April). The performance of panel unit root and stationarity tests: Results from a large scale simulation study. Working Paper, 5. European University Institute, Department of Economics.

- Karim, B., Sami, B., & Hichem, B. (2010). Bank-specific, Industry-specific and Macroeconomic Determinants of African Islamic Banks’ Profitability. International Journal of Business and Management Science, 3(1), 39–56. Retrieved from https://search.informit.com.au/documentSummary;dn=762462165033903;res=IELBUS,ISSN:1985-692X

- Karim, B., Sami, B., & Hichem, B. (2010). Bank-specific, industry-specific and macroeconomic determinants of African Islamic banks’ profitability. International Journal of Business and Management Science, 3(1), 39–56. http://www.safaworld.org/ijbms/abs/abs3.1/IJBMS03%20Ben%2039-56.pdf

- Kohlscheen, E., Murcia, A., & Contreras, J. (2018). Determinants of bank profitability in emerging markets. BIS Working Papers, Junary, 686. https://www.bis.org/publ/work686.htm

- Levin, A., Lin, C., & Chu, C. (2002). Unit root tests in panel data: asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1-24. Retrieved from http://www.sciencedirect.com/science/article/pii/S0304-4076(01)00098-7

- Masood, O., Aktan, B., & Chaudhary, S. (2009). An empirical study on Banks profitability in the KSA: A co-integration approach. African Journal of Business Management, 3(8), 374–382. https://doi.org/10.5897/AJBM09.112

- Masood, O., & Ashraf, M. (2013). Bank-specific and macroeconomic profitability determinants of Islamic banks: The case of different countries. Qualitative Research in Financial Markets, 4(2/3), 255–268. https://doi.org/10.1108/17554171211252565

- Masood, O., Ashraf, M., & Turen, S. Bank-specific and macroeconomic determinats of bank profitability: Evidence from member states of the OIC. (2015). Journal of Islamic Financial Studies, 1(1), 43–51. University of Bahrain. https://doi.org/10.12785/jifs/010104

- Mirzaei, A., Moore, T., & Liu, G. (2013). Does market structure matter on banks’ profitability and stability? Emerging vs. advanced economies. Journal of Banking & Finance, 37(8), 2920–2937. https://doi.org/10.1016/j.jbankfin.2013.04.031

- Paleckova, I. (2016). Determinants of the Profitability in the Czech Banking Industry. Economic Studies & Analyses / Acta VSFS., 10(2), 142–158. Retrieved from https://www.vsfs.cz/periodika/acta-2016-2-04.pdf

- Paul, C., et al. (2010, June). The choice between fixed and random effects models: Some considerations for educational research. Centre for Market and Public Organization, University of Bristol. Working Paper, 10 (240)

- Petria, N., Capraru, B., & Ihnatov, I.. (2015). Determinants of Banks’ Profitability: Evidence from EU 27 Banking Systems. Procedia Economics and Finance, 20, 518–524. doi:10.1016/S2212-5671(15)00104-5

- Poposka, K., & Trpkoski, M. (2016). Bank profitability prior and after the crisis: Evidence from selected Balkan transitional economies. Economic Development, 18 (1/2), 309–336. Available at https://www.ceeol.com/search/article-detail?id=411303

- Rachdi, H. (2013). What determines the profitability of banks during and before the international financial crisis? Evidence from Tunisia. International Journal of Economics, Finance and Management, 2(4), 2307–2466. http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.671.5105&rep=rep1&type=pdf

- Ramadan, I. Z. (2011). Bank specific determinants of Islamic banks profitability: An empirical study of the Jordanian market. International Journal of Academic Research, 3 (6), 73–80. Available at http://ijar.org.in/

- Rashid, A., & Jabeen, S. (2016). Analyzing performance determinants: Conventional versus Islamic Banks in Pakistan. Borsa Istanbul Review, 16(2), 92–107. https://doi.org/10.1016/j.bir.2016.03.002

- Revell, J. (1979). Inflation and Financial Institutions. Financial Times LTD. https://www.worldcat.org/title/inflation-financial-institutions/oclc/6310 151

- Samad, A. (2016). Are Islamic Banks’ non-bank deposits shock resistant? A comparison with conventional banks: Evidence from bahrain. Journal of Applied Finance & Banking, 6 (5), 1792–6599. http://www.scienpress.com/Upload/JAFB%2F Vol% 206_5_6.pdf

- Sarafidies, V., & Wansbeek, T. (2020). Celebrating 40 years for panel data analysis: Past, present and future. Monash Econometrics and Business Statistics Working Papers, Manash University 6 (20). https://EconPapers.repec. org/Re PEc: msh:ebswps:2020-6

- Short, B. K. (1979). The relation between commercial bank profit rates and banking concentration in Canada, Western Europe and Japan. Journal of Banking and Finance, 3 (3), 209–219. https://EconPapers.repec.org/RePEc:eee: jbfina: v:3: y:1979:i:3:p:209-219

- Sufian, F., & Parman, S. (2009). Specialization and other determinants of non-commercial bank financial institutions’ profitability: Empirical evidence from Malaysia. Studies in Economics and Finance, 26(2), 113–128. https://doi.org/10.1108/10867370910963046

- Trujillo-Ponce, A. (2013). What determines the profitability of banks? Evidence from Spain. Accounting and Finance, 53(2), 561–586. https://doi.org/10.1111/j.1467-629X.2011.00466.x

- Wasiuzzaman, S., & Tarmizi, H. A. (2010). Profitability of Islamic Banks in Malaysia: An empirical analysis. Journal of Islamic Economics, Banking and Finance, 6 (4), 51–68. https://ibtra.com/pdf/journal/v6_n4_article3.pdf