?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper investigates whether institutional quality determines the effect of inflation targeting (IT) on the banking risk of Islamic versus conventional banks, using an unbalanced panel data over the period 2007–2016. However, the use of the generalized method of moments (GMM) and two measures of institutional quality, namely the Corruption Perception Index and the Government Effectiveness Index, show that the institutional quality failures strengthens the negative impact of IT on conventional banking risk. For the Islamic banking business model, results suggest that corruption impair the good functioning of the price stability channel of financial stability. While IT have different impact on Islamic and conventional banking stability, the operation of these two types of banks in the same corrupt environment reduces the positive effects expected from such a monetary policy.

PUBLIC INTEREST STATEMENT

To stabilize the inflation rate close to the target value, the central bank uses its instruments, such the interest rates, to regulate the monetary aggregates, which are considered to be the main determinants of inflation in the long term. In fact the adjustment of the interest rate can have an impact on the stability of the banking system. Within this framework, our study focuses on the impact of an inflation-targeting monetary (IT) policy on the stability of both conventional and Islamic banks by stressing the role of the institutional quality. Our results also show that implementing an IT system in an economic environment characterized by the spread of corruption and government inefficiency can destroy the stability of the banking system. Moreover, although Islamic banks are immune from the interest rate risk, a fallen institutional quality impedes the positive effects of IT.

1. Introduction

Since the early 90s, IT has become the most suitable strategy for fighting inflationary pressures and therefore ensuring the proper conduct of monetary and exchange rate policies. This practice has been adopted by a large number of central banks around the world, particularly in emerging economies (Lucotte, Citation2015).

In fact, the growing enthusiasm of central banks in the emerging economies for IT is mainly explained by the difficulties encountered by the monetary authorities of these countries in conducting their monetary and exchange rate policies during periods of high inflation. In this sense, Lucotte (Citation2015) indicates that, for a central bank, an IT strategy does not consist only in announcing a target rate but also in implementing a whole framework based on three main characteristics. First, the central bank must assign a numerical inflation target and a precise horizon for achieving this target. Second, it must adjust its instruments on the basis of a set of macroeconomic and financial indicators (Bordes & Clerc, Citation2007). Finally, it must make vigorous efforts to improve transparency and communication with financial market participants.Footnote1

The traditional view of IT (the Schwartz, 1995 hypothesis) argues that price instability may lead to incorrect lending/borrowing decisions, increasing loan defaults, compromising the banking system loan portfolio, and increasing bankruptcies. In this context, De Guimarães e Souza et al. (Citation2016) confirm that the adoption of IT implies gains in economic growth. Moreover, in the case of developing economies, De Mendonça and De Guimarães e Souza (Citation2012) suggest that the IT is an effective monetary regime in reducing the volatility of inflation to internationally acceptable levels.

Despite the development of the IT strategy and the successful experiences of industrialized economies that have already adopted it, the global financial crisis has proven that this prospective is not always true. Indeed, the relatively low and stable inflation of the early 2000s did not prevent the global economy from experiencing a housing price bubble that burst in 2008. In this framework, Ftiti et al. (Citation2017) tested the efficiency of the IT regime in terms of economic performance. Their results showed that in some emerging countries where inflation is a topical challenge, this monetary policy ensures price stability with a sustainable growth (Ayres et al., Citation2014; Ftiti & Hichri, Citation2014; De Mendonça & De Guimarães e Souza, Citation2012; Öztürk et al., Citation2014). However, in the case of the industrialized countries, their results revealed that the monetary policy sacrifices economic growth despite price stability. This last result is important because it justifies the criticisms of Stiglitz (Citation2008) and Blanchard et al. (Citation2010) who pointed out that this monetary regime contributed to the Great Depression following the subprime crisis.

Among others, analysts showed that the commitment to low inflation levels makes the economic policy too loose in normal times. Thus, the policy rate approaches the zero lower-bound, reducing the margin for any adjustment of the interest policy rates should any economic downturn arise. Moreover, it is widely argued that central banks in the IT-countries have been less concerned with the development in the financial markets and therefore did not respond to financial imbalances. For their part, Giavazzi and Giovannini (Citation2010) illustrate this debate by noting that “[…] the crisis has taught to us that central banks, when they set interest rates, should also be concerned about the fragility of the financial system”. On the other hand, in a study of 70 countries over the 1998–2012 period, Fazio et al. (Citation2015) showed that the greater strength of banks operating in countries where inflation is a target is not essentially due to the implementation of such a monetary policy. In fact, the authors explain this finding by the pre-crisis dichotomy between the monetary policy and financial stability that led the authorities to conduct these two policies separately. Referring to the work of Mishkin (Citation2011), Fazio et al. (Citation2015) stated that central banks are not accustomed to including financial vulnerability in their general equilibrium models, which means that they do not believe that financial stability is a condition for the promotion of price stability. In the same context, Castro (Citation2011) studied the extent to which the Central Bank of England, the Fed, and the European Central Bank focus on the financial imbalance when adopting the IT strategy. His findings showed that only the European Central Bank seems to tighten its policy stance in the presence of increasing financial imbalances

Notwithstanding this criticism, the adoption of IT raises a number of questions, particularly in the emerging economies, among which is the institutional framework of these countries. Indeed, the emerging economies are generally characterized by relatively marked institutional weaknesses which can interfere with the conduct of the monetary policy. For this reason, the need for an institutional framework in line with the objective of price stability is crucial under penalty of tarnishing the credibility of the monetary policy, and therefore its effectiveness.

In this paper, we aim at revisiting the effect of IT and bank’s stability by highlighting the role of the quality of the institution and distinguishing between Islamic and conventional banks. More particularly, we seek to address the following fundamental questions; (i) to what extent is institutional quality involved in the relationship between IT and banking fragility? (ii) are Islamic banks immune from the harmful effects of IT? In fact, this paper, which is built upon these two issues, has to receive substantial attention in the academic literature, as it can fill the gap in the Islamic banking literature by examining whether IT affects the banking system stability and if so, is this effect caused by the quality of institutions.

To the best of our knowledge, this is the first survey to consider this pattern in the Islamic banking industry. Indeed, if both Islamic and conventional banks are part of the same financial system, then any instrument of monetary policy is expected to affect both types of banking systems (Raza, Shah et al., Citation2019). Therefore, our choice of the Islamic banking industry was not arbitrary since Islamic banks are commonly synonymous with interest-free banks operating in an interest-free system, which is one of the important things differentiate them from the conventional banks or the interest-based ones.

Therefore, the Central Bank uses its instruments, such as the interest rates, to regulate the monetary aggregates, which are considered to be the main determinants of long-term inflation. In fact, the control of the monetary aggregates should help stabilize the inflation rate at the target value. However, such practices may have repercussions on the state of health of conventional banks, which is something still ambiguous in the case of Islamic banks. Therefore, using a sample of two different types of commercial banks, Islamic and conventional banks, this paper is intended to find out if IT has an eventual effect on Islamic bank’s financial stability, to examine whether the quality of institutions has any effect on the IT-stability nexus.

According to the banking literature, financial stability and bank risk-taking are assessed through a variety of indicators. In fact, some studies, such as those of Pessarossi et al. (Citation2020), Cole and White (Citation2012) and Betz et al. (Citation2014), used profitability as a determinant variable of financial distress. In another study, Liang et al. (Citation2020) tested the theory of Wagner (Citation2010) to explore the impact of diversification on banking risk. For all what has been previously said, we included in our regression a set of bank and country-specific control variables to account for the characteristics that affect banking risk-taking behavior.

To achieve our purpose, we have employed two institutional quality measures, namely the corruption perception index of the international transparency, and the government effectiveness index of the World Bank’s Governance Indicators (WGI). Moreover, we specify an interaction term between these variables with dummies to check whether a specific country has adopted IT. Additionally, we used a split sample analysis to explore the differences between the two banking business models.

Thus, our results show that the implementation of a monetary policy based on IT can threaten the stability of conventional banks. This result can be explained by the credibility paradox according to which unsustainable booms take longer to be discovered by central banks that have adopted this strategy. Nevertheless, in the case of Islamic banks, IT can promote banking stability provided that institutional quality is strengthened.

The remainder of this paper proceeds as follows. Section 2 reviews the relevant literature, Section 3 describes the data and the methodological framework then, Section 4 discusses the results and finally, Section 5 concludes the paper.

2. Literature review

The literature offers a great number of studies that compared the financial characteristics of Islamic banks to those of their conventional peers, especially in terms of stability (Anginer et al., Citation2014; Beck et al., Citation2013; Berger et al., Citation2009; Ghosh, Citation2016; Louati et al., Citation2016), profitability (Alexakis et al., Citation2019; Kusumastuti & Alam, Citation2019; Mimouni et al., Citation2019; Rashid & Jabeen, Citation2016), efficiency (S. A. Srairi, Citation2010; Alqahtani et al., Citation2017; Bitar et al., Citation2017; Johnes et al., Citation2014, Citation2014; Saeed & Izzeldin, Citation2016) and credit risk (Ghenimi et al., Citation2017; Louhichi et al., Citation2019).

For instance, Beck et al. (Citation2013) used an array of different variables to compare Islamic and conventional banks’ soundness. More particularly, they employed an indicator of maturity matching the ratio of liquid assets to deposit and short-term funding to assess the sensitivity to bank runs. In fact, they found that Islamic banks are more stable than their conventional counterparts. The authors also showed that the good quality of Islamic bank’s assets and their well funding is behind this result. In addition, Abedifar et al. (Citation2015) indicated that small Islamic banks, as opposed to conventional banks, have higher stability rates. Similarly, in a recent survey, Alqahtani and Mayes (Citation2018) have added evidence that, during an economic downturn period, small Islamic banks can efficiently manage their insolvency. Within the same context, and using the E-GARCH and GJR-GARCH estimation techniques, Caby and Boumedienne (Citation2013) reported that Islamic banks’ stock returns are less volatile than those of conventional banks, suggesting that Islamic banks are more stable. Moreover, the study of Louhichi et al. (Citation2019) is along this line on this research as it combines the regulatory factors and market competition to explain Islamic and conventional banks’ stability. However, other studies, namely the one of Bourkhis and Nabi (Citation2013), have examined the financial soundness of Islamic and conventional banks. In addition to the measures related to banks’ capitalization, a number of indicators related to the asset quality and profitability provide complementary information about the health of the bank. However, the authors reported no significant differences between the two banking business models. Furthermore, Another strand of the literature considers competitiveness as an important indicator of banking stability. According to a comparative approach of Islamic and conventional banks, Kabir and Worthington (Citation2017) as well as Louhichi et al. (Citation2019) analyzed the trade-off between competition and financial stability. In fact, the authors supported the competition–fragility hypothesis by providing empirical evidence of a positive link between banking market concentration and bank’s risk taking incentives for both business models.

In the context of a comparative study opposing Islamic banks to conventional ones, and in another strand in the literature, among others, Abedifar et al. (Citation2013), Bitar et al. (Citation2016), Alqahtani et al. (Citation2017), Johnes et al. (Citation2014), S. Srairi (Citation2013, Citation2019)raised questions about efficiency using the cost to income ratio and efficiency scores.

While prior studies in the field of Islamic banking have been primarily concerned with identifying their risk, efficiency, and profitability, profiles and comparing them to those of conventional banks, little research has been conducted to examine whether IT has any effect on the banking system stability and risk and whether this relationship is affected by countries’ institutional quality. In fact, from a theoretical perspective, the adoption of IT driven by action on the interest rate cannot pass without effect on banking stability. In fact, raising the key rate risks eliminating the most solvent part of the customer’s base, which implies the deterioration of the banking portfolio quality and, consequently, the increase of risk.

In the context of Islamic banks, Bitar et al. (Citation2017) investigated whether and how political systems affect the financial soundness of the two banking system models. Their findings revealed that Islamic banks underperform their conventional counterparts in more democratic political systems but outperform them in hybrid and Sharia’a-based legal systems. In addition, Shah and Rashid (Citation2019) investigated the impact of monetary policy on the credit supply of Islamic versus conventional banks of Malaysia. The authors provide strong evidence on the existence of the credit channel of monetary policy transmission mechanism. They also suggested that Islamic banks are less vulnerable to changes in monetary policy instruments compared to their conventional counterparts.

In fact, an examination of the existing relevant literature clearly revealed that the research studies that dealt with the IT–financial stability nexus are very rare. To our knowledge, the study of Frappa and Mésonnier (Citation2010) is the only existing study that comparatively investigated the state of the financial system in targeting versus non-targeting countries. Relying on a sample of 17 advanced economies, their empirical analysis showed that IT is associated with higher real house prices and price-to-rent ratio. Considering the latter as indicators of financial instability implies that the financial sector is relatively less stable in countries implementing the IT regime

Actually, the closest paper to ours is the one of Fazio et al. (Citation2018). Using bank-level data from 66 countries over the 1998/2014 period, the authors showed that IT is found to have a stabilizing effect, especially for banks operating in countries where institutions are perceived to have average levels of quality.

Within this context, Fouejieu (Citation2017) investigated whether in the emerging markets inflation targeters are more financially vulnerable than their non-targeting peers. In fact, based on a sample of 26 emerging countries including 13 targeters, the author stated that the monetary policy in these targeting countries is relatively more sensitive to financial risks while Fazio et al. (Citation2015) compared the risk-taking behavior of banks in IT countries to that of their counterparts from non-IT countries. Their results revealed that banks operating in IT countries have an enhanced stability, which enables them protect themselves during global liquidity shortages Periods.

Simultaneously, Hove et al. (Citation2017) included other institutional quality variables, such as central banks’ independence, fiscal discipline and financial sector development, to investigate the extent to which these variables can influence the ability to achieve inflation target bands. They added that the improvement of institutional quality can bring about some important elements in favor of inflation target bands. Regarding the relationship between institutional quality and banking stability, Bermpei et al. (Citation2018) showed that regulatory instruments (with the exception of the supervisory power) can efficiently act on banking stability only if they are of good institutional quality.

As for Houa and Wang (Citation2016), they investigated the relationship between banking marketization and banking stability across different levels of institutional quality in China. Their results showed that an improvement of the institutional quality can reduce the adverse influence of banking marketization on banking stability. On a panel of 37 emerging markets and 21 advanced economies over the 2000/2015 period, Bui and Bui (Citation2019) argued that financial openness can force domestic banks to behave more prudently only when legal systems, market discipline, and transparency are reliable. In other words, the impact of financial openness on banks’ risk-taking behavior depends on the development of institutions.

3. Empirical approach

3.1. Data and variables description

The empirical analysis in this paper, which is based on a sample of 42 conventional banks and 15 Islamic ones, covers the 2007/2016 period. Therefore, since our main objective is to test the impact of IT on banking risk, we selected data from a cross-country sample that adopted IT and of which banking system includes both Islamic and conventional banks. A detailed description of these banks’ distribution per country and type is provided in the Appendix A (Table ). Moreover, the data related to financial information are extracted from DataStream while the information about the quality of institutions and the macroeconomic variables, which indicated in Table , are extracted from several sources.

Table 1. Variables description and data sources

3.2. Applied methodology

In this section, we explain the main empirical model, the employed variables and their sources. To scrutinize the “IT- Banking risk” nexus, we used a dynamic panel data. This approach enabled us to examine the joint endogeneity of the explanatory variables through the use of internal instruments, namely the Arellano and Bover (Citation1995), Blundell and Bond (Citation1998) system, the GMM estimator (Cooray & Schneider, Citation2016). With reference to previous literature (Belkhir et al., Citation2019; Fazio et al., Citation2018; Shah & Rashid, Citation2019), we constructed the following equation:

where is the stability or risk-taking proxy for the specific bank i that operates in country k at period t.

is a dummy variable that takes the value of one if the country k is an inflation targeter during period tand zero otherwise;

is a measure of the quality of institutions, then

is the quadratic term for the quality of institution measure which is introduced to capture a possible non linear relationship between this latter and the depended variable. While

is a vector of country- and bank-specific controls. And finally,

and

are bank and time fixed effects, respectively (Fazio et al., Citation2018).

4. Empirical analysis

4.1. Summary statistics

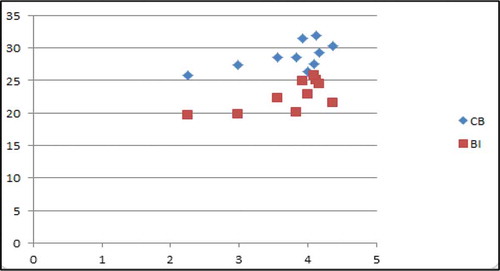

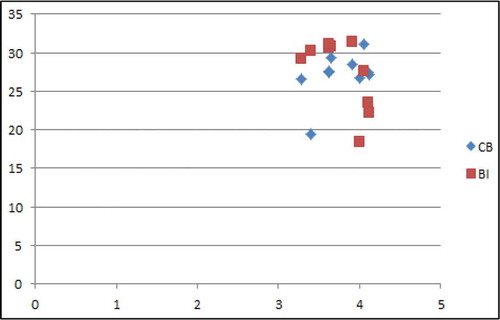

First, we present the scatter plots of Islamic and conventional bank’s average stability measures against the average corruption perception index for IT and non-IT countries, which are presented in Figures and , respectively. In fact, in both figures, we notice that the format of the scatter plots for both types of banking business models appears to suggest an inverse U-shaped relationship between banking stability and the quality of institutions. Furthermore, since the corruption perception index is inversely related to the level of the quality of institutions, we can conclude that low and high values of the corruption perception index usually have a lower Z-score, that is, a higher fragility. Moreover, we notice that the average financial stability of the conventional banks appears to be higher than that of their Islamic counterparts, but only in IT countries.

Figure 1. Scatter plots of the Islamic and conventional banks’ average stability measures against the average corruption perception index for IT countries

Figure 2. Scatter plots of the Islamic and conventional banks’ average stability measures against the average corruption perception index for non-IT countries

4.2. Empirical results

This paper investigates the extent to which the quality of institutions can alter the IT-banking stability nexus. Since IT coincides in the two banking business models, we mainly intend to test if one solution fits both of them. Therefore, to determine whether IT has an indirect effect on banking soundness, as channeled through institutional quality, we incorporate interaction terms between IT dummy and the corruption perception index. Moreover, we employ an alternative specification in which the IT dummy interacts with another institutional quality, namely the Government Effectiveness Index, which a variable that measures the government effectiveness of a country.

Following Louhichi et al. (Citation2020), and within the GMM framework, we use (i) the Sargan test, which is used for over identifying restrictions, to determine whether our instruments are valid or not, and (ii) the Arrelano and Bond (Citation1991) test for first-order autocorrelation (AR(1)) and second-order autocorrelation (AR(2)) (Arellano & Bover, Citation1995; Blundell & Bond, Citation1998). However, the Sargan test results rejected the null hypothesis of the validity of over identifying restrictions at 1% level for all the specifications, limiting the validity of exclusion restrictions. For their part, Cruces and Galianai (Citation2007) argued that the Sargan test is not very powerful in finite samples. In fact, the same conclusion was found by Athanasoglou et al. (Citation2008) and Tan and Floros (Citation2012). As for the second-order autocorrelation, it was rejected by the test for AR (2), indicating the consistency of the estimators. Moreover, the lagged dependent variables are positive, with highly significant coefficients across all the specifications, demonstrating the dynamic character of the model specification (Daher et al., Citation2015; Tan, Citation2016).

The regression results are presented in Tables and . In fact, Table shows the estimated results by taking into account the corruption as a proxy for a country’s quality of institution while Table presents the results with the WGI’s government effectiveness index instead of the corruption perception. These two measures, even though highly correlated with each other, may measure slightly different aspects of institutional quality. We first evaluate the IT-banking stability nexus without distinguishing between Islamic and conventional banks (regressions (1) and (2)) then, we perform a split sample analysis to detect potential differences between the two banking system models.

Table 2. IT + Corruption Perception Index: Z-score equation

Table 3. IT + Government Effectiveness Index: Z-score equation

In particular, regressions (3) and (4) report the results for conventional banks, while regressions (5) and (6) provide the results for Islamic banks.

The first column of Tables and shows the direct effect of IT and institutional quality on the financial stability. Moreover, both tables show that IT dummy has a significant negative relationship with the conventional banking stability, in other words, countries that adopt inflation targets have, on average, more fragile conventional banks. Therefore, our results are in conformity with those of Fouejieu (Citation2017) and Fazio et al. (Citation2015), which supports the hypothesis that a country’s choice to adopt and maintain an IT policy is exogenous to bank soundness considerations. This means that outside financial crisis periods, there is a consensus about the dichotomy between the monetary policy and financial stability (Mishkin, Citation2011). Among the IT critical arguments, there is a growing body of literature that shed light on the problem raised by the change of the short-term interest rates. They explain that lower short-term interest rates create incentives for investors to take more risks in order to obtain the returns promised to debtors. However, IT has not been implemented in many countries due to financial stability concerns.

Alternatively, the coefficient of IT dummy variable is predominantly positive and significant for the Islamic bank’s Z-score regression, indicating that Islamic banks are more stable under the IT policy. This result proves that despite the displaced commercial risk facing them Islamic banks are less sensitive to the interest rate changes compared to their conventional peers. Hence, by perceiving a higher interest rate, Islamic banks are considered to have a lower attitude towards risk (i.e., they are risk-averse). This outcome is to some extent evident given that, compared to their conventional counterparts, Islamic banks are mainly exposed to some additional specific, which, therefore, entails prudent behavior towards risk. Along the same line, Shah and Rashid (Citation2019) showed that Islamic banks respond considerably less to changes of the monetary policy instruments, compared to their conventional counterparts. In fact, the authors added that this result can be explained by the fact that Islamic banks’ financing is not entirely based on the interest rates as the IBOR (Islamic Banking Offered Rate) is determined in the Islamic Inter-bank Money Market (IIMM). Hence, by perceiving a higher interest rate, Islamic banks are considered to have a lower attitude towards risk (i.e., they are risk-averse).

In fact, the effect of the institutional quality, as measured by the Corruption Perception Index, on the banking stability is proved to be positive for both the Islamic and conventional bank sub-samples. It should be noted that higher values of the perception index reflect a lower corruption; we also notice that the fight against corruption improves the banking stability. This can be explained by the fact that decreasing the citizens’ skepticism about the policies of their own governments helps to create incentives to wiser strategies regarding the lending and investment decisions. Thus, this result is in line with those of Bermpei et al. (Citation2018) and Houa and Wang (2016) as well as with those of Bui and Bui (Citation2019) which proved that several factors such as banking regulation, banking marketization and financial openness can act effectively on the banking stability only if the institutional quality is developed.

The quadratic term of corruption shows that there is a non-linear relationship between institutional quality and banking stability. Interestingly, we obtain the same results when using government effectiveness as a measure of institutional quality.

Regarding the conventional banks’ sub-sample, we can see that the interaction between IT and corruption perception is negative and significant at 1% level. This finding indicates that institutional quality contributes to accentuating the negative effect of IT on the banking stability, which supports the “paradox of credibility”. In fact, this paradox explains the negative effect of IT on the banking stability for high levels of institutional quality. It also shows that central banks’ are committed to adopt an anti-inflationary policy in order to keep inflation low and stable and also maintain a high institutional quality, which may produce unsustainable price bubbles that may take longer to be identified and properly addressed (Fazio et al., Citation2018; Borio et al., Citation2003).

In the same vein, Amato and Shin (Citation2003) stated that the inflation index loses its informational character about the real state of the economy while the agents and authorities may not realize the building up of financial imbalances and price distortions. In this case, the building up of financial imbalances would be discovered only when it is too late for authorities to reverse it that is when financial stability is already undermined. As circumstances can lead to an increase of the bank’s default probability, some specialists, such as Bean (Citation2009), raised doubts about the achievement of both financial and price stability with only one instrument, which is Tinbergen’s Rule). In addition, the author argue that it may be difficult to identify (i) whether an increase of the asset prices is fundamentally justified or not; and (ii) whether the necessary (i.e., often large) increase of the interest rates to counter these financial imbalances will be socially desirable in terms of output loss.

In the case of Islamic banks, the coefficient of the interaction term with corruption is significantly negative. Therefore, the interaction between IT and corruption perception index hurts Islamic banking soundness. This finding implies that considering institutional quality undermines the positive effect of IT on Islamic banks’ stability, which confirms the validity of the credibility paradox even for the case of Islamic banks. With reference to Islamic banking theoretical model, which is based mainly on the prohibition of interest principle, this result is contradictory to our expectations.

As in several other cross-country studies, we are also aware that our results are due to some uncontrolled factors that explain both the quality of institutions and the banks’ risk-taking. Ideally, one could control such reforms by the use of country-year fixed effects. Nevertheless, this is not possible since such fixed effects would be collinear with the interaction between the IT dummy and the quality of institutional measure. For this reason, we performed a robustness test which consists of introducing variables specific to each country such as the annual gross domestic product growth rate and the financial freedom index. Nevertheless the same results are retained.

4.3. Robustness check

To check the validity of our results, we conducted a robustness test in which we substituted the Z-score variable with the ROA volatility since both variables are used in the literature as a proxy for the banking risk. The results about the corruption perception index and governance effectiveness are reported in Tables and , respectively.

Table 4. IT + Corruption Perception Index: σROA equation

Table 5. IT + Government Effectiveness Index: σROA equation

These results confirm the paradox of credibility for conventional banks. As for Islamic banks, the results remained approximately unchanged except for the interaction term between IT dummy and the quality of institutions as measured by the governance effectiveness index. In other words, Islamic banks’ asset volatility seems to be statistically insensitive, or immune from the quality of both public, civil services, and of policy formulation and implementation, as well as the extent of the government’s commitment to these policies.

5. Conclusion

It is well known that some of the cornerstones of Islamic finance are, among others, interest avoidance as well as the close relationship with the real economy. The positive aspects of these characteristics became evident during the last financial crisis of 2008. In addition, this crisis has shed light on the crucial role of the monetary policy, especially the price stability channel, which plays a crucial role in the banking risk management. Indeed, this impact is proportional to the countries’ quality of institutions in establishing IT policy. This paper aims at capturing the relationship between IT and banking risk while taking into account the behavior of highlighting the effect of the quality of institutions.

To carry out the empirical analysis, we used an unbalanced panel dataset of conventional and Islamic banks over the 2007/2016 period. We also applied the one-step GMM estimator method, which not only effectively controls for the possibility of endogeneity but also provides unbiased estimates in the presence of cross-section heteroskedasticity in the panels. In our empirical analysis, two banking risk proxies are adopted:the Z-score and the σROA. Furthermore, our analytical framework enables us to examine the prospective impact of the institutional quality on the IT-banking risk nexus. To do so, we used two alternative measures of the quality of the corruption perception and the government effectiveness index. We also controlled for several bank-specific and macroeconomic variables.

Initially, the results showed that the impact of IT differs per banking type. First, IT is found to have a destabilizing effect on conventional banks only. This effect is significantly stronger for banks operating in an economic environment characterized by corruption. Second, in Islamic banks, the direct effect of IT indicates that the predictability improvement of economic policy and the reduction of the degree of uncertainty about the price level are effective tools in enhancing Islamic banks’ stability and reducing their risk. However, when associated with the Corruption Perception Index, this monetary policy has an adverse effect on Islamic banks

Finally, it is worth noting that some policy conclusions can be drawn from our results. In a dualist financial system, the implementation of an IT strategy should be preceded by the preparation of an economic context based on the improvement of the institutional quality, particularly in the fight against corruption. In other words, we can readily note that the effectiveness of an IT strategy crucially depends on the agents’ trust levels on the government

Additional information

Funding

Notes on contributors

Salma Louati

Salma Louati holds a PhD in Finance and now she a student researcher in Applied Economics at the Research Unit of the Faculty of Economics and Management of Sfax, Tunisia. She is also a corresponding author, whose skills and expertise are developing around corporate finance and, more particularly, banking and finance, banking risk management and financial crises.

Younes Boujelbene

Younes Boujelbene is a Professor at the Faculty of Economics and Management of Sfax, Tunisia. He is specialized in financial economics, econometrics, risk management and insurance.

Notes

1. Papadamou et al. (Citation2015) stressed the crucial role of central banks’ transparency in the transmission mechanism of monetary policy through the interest rate channel for the emerging economies.

References

- Abedifar, P., Ebrahim, S. M., Molyneux, P., & Tarazi, A. (2015). Islamic banking and finance: Recent empirical literature and directions for future research. Journal of Economic Surveys, 29(4), 637–15. https://doi.org/10.1111/joes.12113

- Abedifar, P., Molyneux, P., & Tarazi, A. (2013). Risk in Islamic banking. Review of Finance, 17(6), 2035–2096. https://doi.org/10.1093/rof/rfs041

- Alexakis, C., Izzeldin, M., Johnes, J., & Pappas, V. (2019). Performance and productivity in Islamic and conventional banks: Evidence from the global financial crisis. Economic Modelling,79, 1–14. https://doi.org/10.1016/j.econmod.2018.09.030

- Alqahtani, F., & Mayes, D. G. (2018). Financial stability of Islamic banking and the global financial crisis: Evidence from the Gulf Cooperation Council. Economic Systems, 42(2), 346–360. https://doi.org/10.1016/j.ecosys.2017.09.001

- Alqahtani, F., Mayes, D. G., & Brown, K. (2017). Islamic bank efficiency compared to conventional banks during the global crisis in the GCC region. Journal of International Financial Markets, Institutions and Money, 51, 58–74. https://doi.org/10.1016/j.intfin.2017.08.010

- Amato, J. D., & Shin, H. S. (2003). Public and private information in monetary policy models.

- Anginer, D., Demirguc-Kunt, A., & Zhu, M. (2014). How does competition affect bank systemic risk? Journal of Financial Intermediation, 23(1), 1–26. https://doi.org/10.1016/j.jfi.2013.11.001

- Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error component models. Journal of Econometrics, 68(1), 29–51. https://doi.org/10.1016/0304-4076(94)01642-D

- Ariss, R. (2010). Competitive conditions in Islamic and conventional banking: A global perspective: Review of Financial Economics, 19, 101–108. doi:10.1016/j.rfe.2010.03.002

- Arrelano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297. https://doi.org/10.2307/2297968

- Athanasoglou, P. P., Brissimis, S. N., & Delis, M. D. (2008). Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of International Financial Markets, Institutions and Money, 18(2), 121–136. https://doi.org/10.1016/j.intfin.2006.07.001

- Ayres, K., Belasen, A. R., & Kutan, A. M. (2014). Does inflation targeting lower inflation and spur growth? Journal of Policy Modeling, 36(2), 373–388. https://doi.org/10.1016/j.jpolmod.2012.12.008

- Bean, C. (2009). ‘The Meaning of Internal Balance’Thirty Years On. The Economic Journal, 119(541), F442–F460. doi:10.1111/j.1468-0297.2009.02315.x

- Beck, T., Demirguk-Kunt, A., & Merrouche, O. (2013). Islamic vs. conventional banking: Business model, efficiency, and stability. Journal of Banking & Finance, 37(2), 433–477. https://doi.org/10.1016/j.jbankfin.2012.09.016

- Belkhir, M., Grira, J., Hassan, M. K., & Soumaré, I. (2019). Islamic banks and political risk: International evidence. The Quarterly Review of Economics and Finance, 74, 39–55. https://doi.org/10.1016/j.qref.2018.04.006

- Berger, A. N., Klapper, L. F., & Turk-Ariss, R. (2009). Bank competition and financial stability. Journal of Financial Services Research, 35(2), 99–118. https://doi.org/10.1007/s10693-008-0050-7

- Bermpei, T., Kalyvas, A., & Nguyen, T. C. (2018). Does institutional quality condition the effect of bank regulations and supervision on bank stability? Evidence from emerging and developing economies. International Review of Financial Analysis,59, 255–275. https://doi.org/10.1016/j.irfa.2018.06.002

- Betz, F., Oprică, S., Peltonen, T. A., & Sarlin, P. (2014). Predicting distress in European banks. Journal of Banking & Finance, 45, 225–241. https://doi.org/10.1016/j.jbankfin.2013.11.041

- Bitar, M., Hassan, M. K., Pukthuanthong, K., & Walker, T. (2016). The performance of Islamic vs. conventional banks: A note on the suitability of capital ratios (Working Paper). John Molson School of Business, Concordia University.

- Bitar, M., Hassan, M. K., & Walker, T. (2017). Political systems and the financial soundness of Islamic banks. Journal of Financial Stability, 31, 18–44. https://doi.org/10.1016/j.jfs.2017.06.002

- Blanchard, O., Dell’Ariccia, G., & Mauro, P. (2010). Rethinking macroeconomic policy. Journal of Money, Credit, and Banking, 42, 199–215. https://doi.org/10.1111/j.1538-4616.2010.00334.x

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8

- Bordes, C., & Clerc, L. (2007). Price stability and the ECB’S monetary policy strategy. Journal of Economic Surveys, 21(2), 268–326. https://doi.org/10.1111/j.1467-6419.2006.00504.x

- Borio, C. E., English, W. B., & Filardo, A. J. (2003). A tale of two perspectives: Old or new challenges for monetary policy? SSRN Electronic Journal. https://doi.org/10.2139/ssrn.844208

- Bourkhis, K., & Nabi, M. S. (2013). Islamic and conventional banks’ soundness during the 2007–2008 financial crisis. Review of Financial Economics, 22(2), 68–77. https://doi.org/10.1016/j.rfe.2013.01.001

- Bui, D. T., & Bui, T. M. H. (2019). How does institutional development shape bank risk-taking incentives in the context of financial openness? Pacific-Basin Finance Journal, 58, 101209. https://doi.org/10.1016/j.pacfin.2019.101209

- Caby, J., & Boumedienne, A. (2013). The financial volatility of Islamic banks during the subprime crisis ( No. halshs-02024729).

- Castro, V. (2011). Can central banks’ monetary policy be described by a linear (augmented) Taylor rule or by a nonlinear rule? Journal of Financial Stability, 7(4), 228–246. https://doi.org/10.1016/j.jfs.2010.06.002

- Clark, E., Radić, N., & Sharipova, A. (2018). Bank competition and stability in the CIS markets. Journal of International Financial Markets, Institutions and Money, 54, 190–203. https://doi.org/10.1016/j.intfin.2017.12.005

- Cole, R. A., & White, L. J. (2012). Déjà vu all over again: The causes of US commercial bank failures this time around. Journal of Financial Services Research, 42(1–2), 5–29. https://doi.org/10.1007/s10693-011-0116-9

- Cooray, A., & Schneider, F. (2016). Does corruption promote emigration? An empirical examination. Journal of Population Economics, 29(1), 293–310. https://doi.org/10.1007/s00148-015-0563-y

- Cruces, G., & Galianai, S. (2007). Fertility and female labor supply in Latin America: New causal evidence. Labour Economics, 14(3), 565–573. https://doi.org/10.1016/j.labeco.2005.10.006

- Daher, H., Masih, M., & Ibrahim, M. (2015). The unique risk exposures of Islamic banks’ capital buffers: A dynamic panel data analysis. Journal of International Financial Markets, Institutions and Money, 36, 36–52. https://doi.org/10.1016/j.intfin.2015.02.012

- De Guimarães e Souza, G. J., De Mendonça, H. F., & De Andrade, J. P. (2016). Inflation targeting on output growth: A pulse dummy analysis of dynamic macroeconomic panel data. Economic Systems, 40(1), 145–169. https://doi.org/10.1016/j.ecosys.2015.06.002

- De Mendonça, H. F., & De Guimarães e Souza, G. J. (2012). Is inflation targeting a good remedy to control inflation? Journal of Development Economics, 98(2), 178–191. https://doi.org/10.1016/j.jdeveco.2011.06.011

- Fazio, D. M., Silva, T. C., Tabak, B. M., & Cajueiro, D. O. (2018). IT and financial stability: Does the quality of institutions matter? Economic Modelling, 71, 1–15. https://doi.org/10.1016/j.econmod.2017.09.011

- Fazio, D. M., Tabak, B. M., & Cajueiro, D. O. (2015). IT: Is IT to blame for banking system instability? Journal of Banking & Finance, 59, 76–97. https://doi.org/10.1016/j.jbankfin.2015.05.016

- Fouejieu, A. (2017). IT and financial stability in emerging markets. Economic Modelling, 60, 51–70. https://doi.org/10.1016/j.econmod.2016.08.020

- Frappa, S., & Mésonnier, J. S. (2010). The housing price boom of the late 1990s: Did IT matter? Journal of Financial Stability, 6(4), 243–254. https://doi.org/10.1016/j.jfs.2010.06.001

- Ftiti, Z., Aguir, A., & Smida, M. (2017). Time-inconsistency and expansionary business cycle theories: What does matter for the central bank independence–inflation relationship? Economic Modelling, 67, 215–227.

- Ftiti, Z., & Hichri, W. (2014). The price stability under inflation targeting regime: An analysis with a new intermediate approach. Economic Modelling, 38, 23–32. https://doi.org/10.1016/j.econmod.2013.11.033

- Ghenimi, A., Chaibi, H., & Omri, Mohamed Ali Brahim.. (2017). The effects of liquidity risk and credit risk on bank stability: Evidence from the MENA region. Borsa Istanbul Review, 17(4), 238–248. doi:10.1016/j.bir.2017.05.002

- Ghosh, S. (2016). Political transition and bank performance: How important was the Arab Spring? Journal of Comparative Economics, 44(2), 372–382. https://doi.org/10.1016/j.jce.2015.02.001

- Giavazzi, F., & Giovannini, A. (2010). The low-interest-rate trap. VoxEU. org.

- Hou, X., & Wang, Q. (2016). Institutional quality, banking marketization, and bank stability: Evidence from China. Economic Systems, 40(4), 539–551. doi:10.1016/j.ecosys.2016.01.003

- Hove, S., Tchana, F. T., & Mama, A. T. (2017). Do monetary, fiscal and financial institutions really matter for IT in emerging market economies? Research in International Business and Finance, 39, 128–149. https://doi.org/10.1016/j.ribaf.2019.101074

- Johnes, J., Izzeldin, M., & Pappas, V. (2014). A comparison of performance of Islamic and conventional banks 2004–2009. Journal of Economic Behavior & Organization, 103, S93–S107. https://doi.org/10.1016/j.jebo.2013.07.016

- Kabir, M. N., & Worthington, A. C. (2017). The ‘competition–stability/fragility’nexus: A comparative analysis of Islamic and conventional banks. International Review of Financial Analysis, 50, 111–128. https://doi.org/10.1016/j.irfa.2017.02.006

- Kusumastuti, W. I., & Alam, A. (2019). Analysis of impact of CAR, NPF, BOPO on profitability of Islamic banks (Year 2015–2017). Journal of Islamic Economic Laws, 2(1), 30–59. https://doi.org/10.23917/jisel.v2i1.6370

- Liang, D., Tsai, C. F., Lu, H. Y. R., & Chang, L. S. (2020). Combining corporate governance indicators with stacking ensembles for financial distress prediction. Journal of Business Research, 120, 137–146. https://doi.org/10.1016/j.jbusres.2020.07.052

- Louati, S., Louhichi, A., & Boujelbene, Y. (2016). The risk-capital-efficiency trilogy. Managerial Finance, 42(2), 1226–1252. https://doi.org/10.1108/MF-01–2016-0009

- Louhichi, A., Louati, S., & Boujelbene, Y. (2019). Market power, stability and risk-taking: An analysis surrounding the Riba-free banking. Review of Accounting and Finance, 18(1), 2–24. https://doi.org/10.1108/RAF-07-2016-0114

- Louhichi, A., Louati, S., & Boujelbene, Y. (2020). The regulations–risk taking nexus under competitive pressure: What about the Islamic banking system? Research in International Business and Finance, 51, 101074. https://doi.org/10.1016/j.ribaf.2019.101074

- Lucotte, Y. (2015). Le ciblage d’inflation dans les économies émergentes. Revue française d’économie, 30(2), 93–128. https://doi.org/10.3917/rfe.152.0093

- Mimouni, K., Smaoui, H., & Temimi, A. (2019). The impact of sukuk on the performance of conventional and Islamic banks. Pacific-Basin Finance Journal, 54, 42–54. https://doi.org/10.1016/j.pacfin.2019.01.007

- Mishkin, F. S. (2011). Monetary policy strategy: Lessons from the crisis ( No. w16755). National Bureau of Economic Research.

- Öztürk, S., Sözdemir, A., & Ülger, Ö. (2014). The effects of inflation targeting strategy on the growing performance of developed and developing countries: Evaluation of pre and post stages of global financial crisis. Procedia-Social and Behavioral Sciences, 109, 57–64. https://doi.org/10.1016/j.sbspro.2013.12.421

- Papadamou, S., Sidiropoulos, M., & Spyromitros, E. (2015). Central bank transparency and the interest rate channel: Evidence from emerging economies. Economic Modelling, 48, 167–174. https://doi.org/10.1016/j.econmod.2014.10.016

- Pessarossi, P., Thevenon, J. L., & Weill, L. (2020). Does high profitability improve stability for European banks? Research in International Business and Finance, 53, 101220. https://doi.org/10.1016/j.ribaf.2020.101220

- Rashid, A., & Jabeen, S. (2016). Analyzing performance determinants: Conventional versus Islamic banks in Pakistan. Borsa Istanbul Review, 16(2), 92–107. https://doi.org/10.1016/j.bir.2016.03.002

- Raza, S. A., Ahmed, R., Ali, M., & Qureshi, M. A. (2019). Influential factors of Islamic insurance adoption: An extension of theory of planned behavior. Journal of Islamic Marketing, 11(6), 1497–1515. https://doi.org/10.1108/JIMA-03-2019-0047

- Raza, S. A., Shah, N., & Ali, M. (2019). Acceptance of mobile banking in Islamic banks: Evidence from modified UTAUT model. Journal of Islamic Marketing, 10(1), 357–376. https://doi.org/10.1108/JIMA-04-2017-0038

- Roger, S. (2010). Inflation targeting turns, 20. Finance & Development 47, 46–49.

- Saeed, M., & Izzeldin, M. (2016). Examining the relationship between default risk and efficiency in Islamic and conventional banks. Journal of Economic Behavior & Organization, 132, 127–154. https://doi.org/10.1016/j.jebo.2014.02.014

- Shah, S. M. A. R., & Rashid, A. (2019). The credit supply channel of monetary policy transmission mechanism: An empirical investigation of Islamic banks in Pakistan versus Malaysia. Journal of Islamic Monetary Economics and Finance, 5(1), 21–36. https://doi.org/10.21098/jimf.v5i1.1046

- Srairi, S. (2013). Ownership structure and risk-taking behaviour in conventional and Islamic banks: Evidence for MENA countries. Borsa Istanbul Review, 13(4), 115–127. https://doi.org/10.1016/j.bir.2013.10.010

- Srairi, S. (2019). Transparency and bank risk-taking in GCC Islamic banking. Borsa Istanbul Review, 19(Suppl. 1), 64–74. https://doi.org/10.1016/j.bir.2019.02.001

- Srairi, S. A. (2010). Cost and profit efficiency of conventional and Islamic banks in GCC countries. Journal of Productivity Analysis, 34(1), 45–62. https://doi.org/10.1007/s11123-009-0161-7

- Stiglitz, J. E. (2008). The failure of inflation targeting. Project Syndicate, 13.

- Tan, Y. (2016). The impact of risk and competition on bank profitability in China. Journal of International Financial Markets, Institutions and Money, 40, 85–110. https://doi.org/10.1016/j.intfin.2015.09.003

- Tan, Y., & Floros, C. (2012). Bank profitability and GDP growth in China: A note. Journal of Chinese Economic and Business Studies, 10(3), 267–273. https://doi.org/10.1080/14765284.2012.703541

- Wagner, W. (2010). Diversification at financial institutions and systemic crises. Journal of Financial Intermediation, 19(3), 373–386. https://doi.org/10.1016/j.jfi.2009.07.002

Appendix A.

Table A1. Sample banks distributed by IT country and bank type