Abstract

This present study aims to investigate the quality and scope of environmental disclosure (ED) in environmentally sensitive manufactures. It also analyzes the effect of media coverage, environmental award, and financial performance on the quality of environmental disclosure and the extent to which the implementation of corporate governance (CG) principles in moderating these factors. This study used 135 manufacturing companies listed in the Indonesian Stock Exchange during 2012–2016. Partial least squares–structural equation modeling (PLS-SEM) has been employed to test the research hypothesis. The results point out that media coverage and awards associated with the quality of environmental disclosure. The media coverage and environmental awards can improve the quality of environmental disclosure and the correlation will increase if the company pays attention to the implementation of CG principles. This finding supports a comprehensive view of corporate governance which includes disclosure. Empirical findings indicate that external pressures such as media coverage and competitions lead to an appreciation that can increase voluntary environmental disclosure, therefore highlighting the central role of community engagement, media, and non-governmental organizations. Government supervision is important in ensuring the implementation of environmental disclosure that aligns with applicable regulations.

PUBLIC INTEREST STATEMENT

Environmentally sensitive industries could potentially lead to pollution and environmental damage. This paper provides an insight into the environment disclosure quality in the developing countries, especially Indonesia. This study also provides empirical evidence of the relationship between media coverage, environmental award, financial performance with environmental disclosure. The implementation of corporate governance principles used as a moderating variable, this is what differentiates it from previous studies. This paper employs the corporate governance principles implementation index that includes transparency, accountability, responsibility, independence, fairness, and equality. Our findings confirm previous studies in both developed and developing countries which state that environmental disclosure remain low. This is encouraging news because there has been an increasing trend in the number of environmental reports. Most of the environmental disclosures are related to the company’s efforts to minimize environmental damage. The impact of environmental damage on environmentally sensitive industries will appear quickly in the short term.

1. Introduction

In developing countries, economic growth has been positively correlated with environmental destruction (Solikhah et al., Citation2020). This is due to industrial activities related to production such as the conversion of land for industrial development, environmental pollution (water, land, and air); and the impact on social and economic change. Over the last few decades, issues concerning environmental management have become a global concern (Barako & Brown, Citation2008) since the rise in geothermal temperatures (global warming) and natural disasters in various regions/countries. The increasing greenhouse gas emissions into the atmosphere, i.e. carbon dioxide (CO2), methane (CH4), dinitro oxide (N2O), and other gases have caused the earth temperature to rise. Carbon dioxide has a major contribution to climate change, especially to global warming (Levin & Fransen, Citation2017). Environmental damage is evident from the extent of greenhouse gas emissions that cause the earth’s temperature to rise. In 2016, based on data from the World Resources Institute Indonesia, global greenhouse gas emissions were around 52 gigatons/year, where carbon dioxide emissions from burning fossil, cement, and other processes contribute the most, which was around 70% of total emissions (Levin & Fransen, Citation2017). This means that the industrial sector plays a significant role in environmental degradation.

The various damages become the concern of all parties, e.g., the society, community, and government, including Indonesian government. To preserve the environment, the Indonesian government has made policies in the form of environmental regulations including 1) Law No. 23 year 1997 concerning environmental management, 2) Law No. 32 year 2009 concerning protection and environmental management, 3) Law No. 40 year 2007 concerning limited liability companies and 4) Government Regulation No. 47 year 2012 on mandatory corporate social and environmental responsibility. The Indonesian government also plays an active role in the international level in realizing the 2030 Sustainable Development Goals (SDGs) by involving SDGs indicators in the National Medium-Term Development Plan for 2015–2019 (www.bappenas.go.id, 2016).

The current regulations ensure the company’s responsibilities to abstain from damaging natural environment as well as responsible for any damages made to the environment. Meanwhile, guidelines for conducting and reporting social and environmental responsibility have not been issued explicitly by the Indonesian government so that the environmental reporting remains voluntary. This voluntary report causes the format, content, and disclosure of the report varies across the companies in Indonesia. Therefore, in terms of the environmental disclosure (ED) and its quality, Indonesia is considered to be in the low category. Compared with Malaysia, since 2010 companies listed on Bursa Malaysia are required to report their social and environmental activities in their annual reports (Fatima et al., Citation2015).

Environmental disclosure is a form of corporate responsibility for the environmental impacts caused by manufacturing activities. In practice, the preparation of sustainability reports or environmental disclosure still has considerable ambiguity (Bradford, Citation2017). Smith et al. (Citation2007) state that environmental disclosure information is material for stakeholders and is used to make various decisions. Many studies related to environmental disclosure take samples at high-profile companies (Rupley et al., Citation2012) or some studies call it environmentally sensitive industries (ESI) (Fatima et al., Citation2015; Radhouane et al., Citation2020). This kind of industry is characterized by its way of production process in removing residues including waste and pollution. Thus, ESI has the tendency to threaten the environment or has a high level of sensitivity to the environment. Companies under this category are those dealing with mining, energy, chemicals, pharmaceuticals, cosmetics, and food and beverages.

This paper demonstrates the quality of voluntary disclosure on the environment by investigating the driver’s aspect of the sustainability report. The current study also investigates the moderating variable, i.e corporate governance. Our study makes important contributions to existing literature by offering two insights. Firstly, this is a pilot study to observe the quality of environmental disclosure that develops a structural equation model that includes a moderating variable of corporate governance implementation. Secondly, this article also introduces a new measurement method for CG implementation by considering previous research and related regulations in a developing country.

To achieve this goal, this paper develops as follows. First, we briefly present the relevant literature both theoretical and empirical. Second, we describe our sample, explain the analytical method applied, and present the definitions of the relevant variables. Thirdly, we present and discuss our results, and finally, we summarize, conclude, and suggest possible future research extensions.

2. Theoretical literature review

The environmental disclosure can be examined through the theory of legitimacy and stakeholder theory. Ofoegbu et al. (Citation2018) argue that legitimacy theory and stakeholder theory are the main theories to explain the practice of disclosing social and environmental impacts. Both legitimacy theory and stakeholder theory predict that organizations will respond to the demands of various parties by aiming to legitimize their actions (Qu & Leung, Citation2006). Dowling and Pfeffer (Citation1975) state that legitimacy will become a problem for companies if they do not care to maintain their legitimacy. Shocker and Sethi (Citation1973) proposed two things that underlie the stability and development of companies: (1) the company’s final results can be socially given to the community, (2) distribution of economic, social, or political benefits to the group according to the power they have.

2.1. Legitimacy theory

Lindblom (Citation1994) defines legitimacy as a condition or status that exists when the entity’s value system matches the value system of the larger social system where it belongs to (Deegan, Citation2002). Disclosure of the environment as a form of corporate responsibility to the community regarding the environment can be a strategy to avoid the occurrence of legitimacy gaps or social and environmental conflicts. The legitimacy of a company can be obtained through various actions including communicating the company’s profiles to relevant stakeholders (Deegan, Citation2002).

The legitimacy theory explicitly recognizes that business is constrained by social contracts meaning that the company agrees to show a variety of corporate social activities (Solikhah & Winarsih, Citation2016). This implies that the company gains public acceptance of the company’s goals which will ultimately guarantee the survival of the company (Brown & Deegan, Citation1998). Organizations will operate within the boundaries and values that are acceptable to the surrounding society to gain the legitimacy from the society. The theory of legitimacy highlights the relationship between the organization and the society which is called as “social contract” (Choi et al., Citation2013). A social contract can be interpreted as an agreement between the organization and the surrounding society that the activities carried out by the organization are in line with the operating social values. Concern for environmental issues and environmental responsibility reports are one of the efforts to gain legitimacy from the public that the company is truly responsible for environmental sustainability due to the industrial activities it carries out.

2.2. Stakeholders theory

Freeman and Reed (Citation1983) argue that organizations would not exist without the support of groups. Therefore, the next theory that becomes a reference regarding the company’s efforts to make adequate disclosures is the stakeholder theory. Freeman (Citation1984) defines stakeholders as groups or individuals who have a relationship with the company and can influence the achievement of company goals. The theory of stakeholders also explains that the company is not an entity that only operates for its own sake but also must benefit its stakeholders (Ghozali & Chairi, Citation2007).

The relationship between the company and stakeholders has yielded a pressure on the company to accommodate the interests and needs of its stakeholders. Managers are obliged to explain themselves to stakeholders through disclosure to have sustainable access to critical resources that may be controlled in the future (Wakaisuka-Isingoma et al., Citation2016). The company should carry out strategies to accomplish its responsibilities to the environment, attempt to maintain good relations with stakeholders. This harmonious relationship allows the company to obtain support from stakeholders so that the company’s survival can be maintained. Environmental disclosure is a form of corporate responsibility to the society as a result of activities which emerging a negative impact on the environment. Meanwhile, ED is as the accountability of fulfilling the information needs of the company for investors, shareholders, customers, and other parties.

3. Empirical literature review and hypotheses development

3.1. Environmental disclosure

Studies in environmental reporting have increased in Indonesia in the last decade, but unfortunately, it does not indicate conclusive results. The results of the empirical literature review focusing on ED in Indonesia and several countries will be discussed in this section.

Two years since Malaysian Government announce that corporate social responsibility disclosure mandatory for all listed companies, Sulaiman et al. (Citation2014) examined 164 listed companies in Malaysia and found that there was a significant positive relationship between company level and leverage with the quality of environmental reporting. Meanwhile, the distribution of ownership and profitability is not significantly related to the quality of ED. Suttipun and Stanton (Citation2012) researched the top 50 listed companies listing on the Stock Exchange of Thailand (SET). They found a significant relationship between the type of industry, ownership status, and audit with environmental disclosure. The study also concluded that there was no significant relationship between company level, country of origin, company age, business type, risk and profitability on environmental disclosure. Carreira conducts a research that takes a sample of 24 firms listed on the Lisbon Euronext Stock Market. Carreira et al. (Citation2014) conclude that firm size and profitability significantly influence the ED but do not affect on the economic sector. A research in Italy and the US by Boesso and Kumar (Citation2007) on ED quality concluded that business complexity, volatility, award, and intangible asset significantly affect the volume of voluntary disclosure in Italy. Meanwhile, only the award variable has a significant effect on the volume of voluntary disclosures in USA companies.

Company success is determined by at least three factors, namely quality, profitability, and social and environmental responsibility. Environmental disclosure has several benefits for the company. O’Donovan (Citation2002) and Solikhah et al. (Citation2018) states that there are seven benefits for companies to report their environmental information to various stakeholders: (1) aligning management values with social values; (2) avoiding pressure from certain groups; (3) improving the company’s reputation; (4) providing an opportunity to lead the market; (5) acquiring support; (6) showing a strong management principle; (7) showing social responsibility.

There are several things that motivate companies to expose their environmental activities (Deegan, Citation2002). One of them is to win an award because it will have positive implications for the company’s reputation. Boesso and Kumar’s research (Boesso & Kumar, Citation2007) also proves that company’s pressure on stakeholder management as measured by the number of awards has a significant effect on the volume and quality of voluntary disclosures. Research by Anas et al. (Citation2015) supports the finding that the reward variable is positively correlated to CSR disclosure practices. Another motivation that encourages companies to make environmental disclosure is to convince the threat of organizational legitimacy. Environmental disclosure is used as a company’s response to negative media attention, certain environmental or social incidents, or as a result of bad ratings given by certain rating agencies (Deegan, Citation2002). This means that the presence of mass media can affect the company’s behavior in considering the environment. In carrying out operational activities, companies must apply the principles of corporate governance (CG). Good CG could potentially encourage the formation of clean, transparent, and professional management work patterns. The voluntary environmental disclosures will be optimally disclosed if the company applies the CG principles.

3.2. Hypothesis development

3.2.1. Media coverage

Media coverage of environmental issues can be informed through newspapers, magazines, televisions, websites, Facebook, Instagram, or other communication media. Brown and Deegan (Citation1998) argue that increasing media exposure is seen as a way to increase public attention on certain problems. Particularly in today’s digital era, the role of the media in disseminating information is very effective and strategic. Conveying information in the mass media (Rupley et al., Citation2012), is a way for companies to gain legitimacy from society through communication with relevant stakeholders (Ashforth & Gibbs, Citation1990). Empirical research by Brown and Deegan (Citation1998) found that companies with greater media coverage tend to disclose broader information. Media coverage can inform stakeholders about how much individual company concerns on the environment. This will encourage managers to expose the company’s environmental activities to maintain supports from the community. Aerts and Cormier’s research (Aerts & Cormier, Citation2009) has proven that environmental legitimacy has a positive effect on the quality of the economic segments of environmental disclosure of annual reports and environmental press releases that are reactive in nature. Reverte (Citation2009) also states that media exposure has a significant effect on CSR disclosure ratings. The study of Rupley et al. (Citation2012) reports that environmental media coverage has a positive relationship with the quality of environmental voluntary disclosure. The first hypothesis is articulated as:

H 1: The media coverage has a positive effect on environmental disclosure quality.

3.2.2. Environmental award

Regarding environmental management, various awards have been provided both from the government, NGOs, and environmental groups. It aims to encourage companies to take care the environment. Deegan (Citation2002) states that winning an award is a motivation for companies to oversee the environment. By getting an award, companies can overcome the legitimacy gap that can threaten the company’s sustainability (Anas et al., Citation2015). The assumption is that a company that receives an award means that the company has maintained the environment well according to certain criteria. Amran and Nabiha (Citation2009) also argue that what motivates managers in CSR disclosure is to win awards. Boesso and Kumar’s research (Boesso & Kumar, Citation2007) proves that company pressure on stakeholder management as measured by the number of awards has a significant effect on the volume and quality of voluntary disclosures. Based on the description, it can be assumed that the award has a positive effect on the quality of environmental disclosure. Hence, the second hypothesis is stated as follows:

H 2: Awards influence the environmental disclosure quality positively.

3.2.3. Financial performance

Companies with higher economic performance than the average have incentives to do different things compared with companies with lower profitability. One of the differences made is voluntary information disclosure (Frendy & Kusuma, Citation2011). It is necessary to consider the costs and the company’s financial condition before making a decision to carry out an environmental disclosure. Nasir et al. (Citation2014) opine that profitability is a factor that gives management freedom and flexibility to carry out and expose social responsibility broadly. Darus et al. (Citation2020) founded that the higher the level of corporate profitability, the greater disclosure of information on climate change initiatives. This is supported by research by Lu and Abeysekera (Citation2014) which found that financial performance has a significant positive effect on corporate social and environmental disclosure. Based on the previous studies, we propose the following hypothesis:

H 3: Financial performance has a positive effect on environmental disclosure quality.

3.2.4. Corporate governance principles

CG is a system and mechanism used to regulate, direct, and control the company’s operations under the expectations of the stakeholders. Wahyudin and Solikhah (Citation2017) argue that CG can generate goodwill and investor confidence. Suhardjanto and Permatasari (Citation2010) state that there are two important concepts in CG, namely (1) the rights of shareholders to obtain information correctly and timely, (2) the company’s obligation to disclose information about company performance, ownership, and stakeholders accurately, timely, transparently. The implementation of CG principles can influence decision making in quality environmental disclosure. The transparency principles enable the company to provide information that is substantial, relevant, accessible, and understandable for the stakeholders. Furthermore, transparency in company disclosure has become an important component of corporate governance principles issued by organizations throughout the world (The Organisation for Economic Co-operation and Development (OECD), Citation2003; ASX Corporate Governance Council, Citation2003). The second CG principle, namely accountability, is a prerequisite required to achieve sustainable performance. Being “responsible” is the third principle in CG that requires companies to comply with laws and regulations and to be responsible to the society and the environment. The fourth CG principle is independence to ensure companies do not dominate each other and cannot be intervened by other parties. In implementing the fifth principle of CG, in carrying out its activities, the company must always pay attention to the interests of shareholders and other stakeholders based on the principle of fairness.

Various cases due to weak governance in global companies such as Enron and WorldCom have highlighted the importance of corporate disclosure in playing a vital role as one of the external control mechanisms (Qu & Leung, Citation2006). Qu and Leung (Citation2006) argue that CG concerning transparency is the availability of company-specific information for those outside the public company and must go hand in hand with accountability.

The stakeholder theory also states that companies must be able to embrace the surrounding interests so that their interests can be achieved to the maximum. Conducting environmental disclosures can improve a company’s reputation (O’Donovan, Citation2002). This action is one of the applications of stakeholder theory. On the one hand, the needs of stakeholders for environmental information are met; and, on the other hand, the company’s reputation also increases. Companies that get awards will motivate companies to make quality environmental disclosures.

Previous study by Ntim et al. (Citation2017) conclude that the levels of voluntary disclosure (e.g., environmental disclosure) and the reasons underlying disclosure across companies and countries were found to vary. While some firm-level factors were consistently associated with disclosure, the results were more mixed when related to corporate governance factors.

Almaqtari et al. (Citation2020) recently reviewed 161 published articles related to CG in India, their recommendation that the next agenda for research includes the impact of corporate governance on environmental disclosure. Moses et al. (Citation2020) concluded that in most developed countries, effective board governance can improve sustainability performance and the quality of the sustainability report, there are mixed conclusions. The decision to make an environmental disclosure needs to consider the cost aspects and the company’s financial condition. Wahyudin and Solikhah (Citation2017) also argue that financial decisions can affect other financial decisions. If financial performance is good, then management will be more accessible to do environmental disclosure because the company has sufficient resources.

In sum, we argue that if CG principles are applied in the company, it will strengthen the relationships between media coverage, award, financial performance, and the quality of ED. The hypotheses are formulated as follows:

H 4 a: The implementation of the principles of CG strengthens the relationship between the media coverage of the environmental disclosure quality.

H 4b: The implementation of CG principles strengthens the relationship between respect for environmental disclosure quality.

H 4c: The implementation of CG principles strengthens the relationship between financial performance and environmental disclosure quality.

4. Research design

The samples in this research were high profile/environmentally sensitive manufactures listed in Indonesia Stock Exchange during 2012–2016. The high profile/environmentally sensitive manufactures company in this study following the category from Rupley et al. (Citation2012) comprising six types of industries, e.g., mining, energy, chemical, pharmaceutical, cosmetics as well as food and beverages. The sample in this study was selected by using a purposive sampling method by considering the social and environmental responsibility report in the annual report or sustainability report for at least one item. The sample comprised of 175 data for 5 years of observation. Data analysis techniques used Structural Equation Modeling (SEM) with an alternative method, namely Partial Least Square (PLS) using smart PLS 3.0 software.

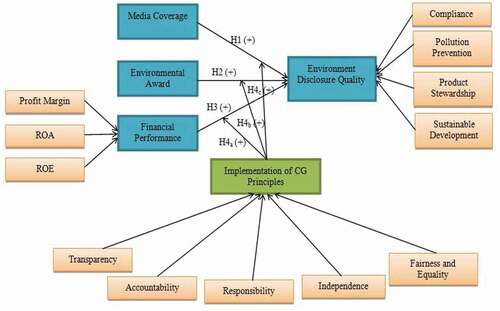

Figure 1. Research model

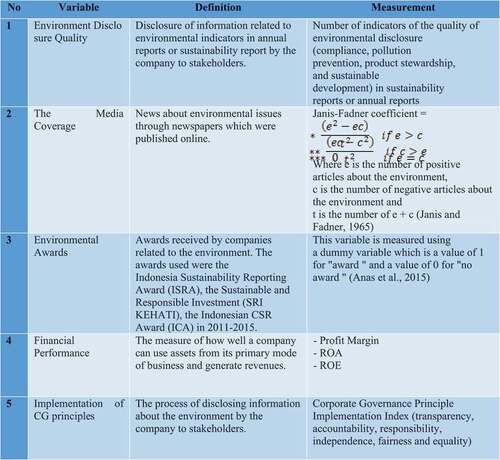

This study consists of three exogenous variables, namely media coverage, environmental award, financial performance, and one moderating variable, namely the implementation of CG principles to predict endogenous variables of environmental disclosure quality. The variables measurement avalable in the Appendix 1 and Appendix 2. The data used in this research were panel data. The data of ED quality were collected using content analysis from the Annual Report or Sustainability Report. The quality of measured environmental disclosure refers toRupley et al. (Citation2012) by dividing it into four levels of strategy groups consisting of compliance, pollution prevention, product stewardship, and sustainable development. Every change from the level of compliance to the level of sustainable development represents an improvement from environmental management into organizational processes, strategies, and culture in a better direction. The items were measured using the Global Reporting Initiative (GRI) guidelines which were broken down into 60 question items. Data related to media coverage were obtained from national newspapers in Indonesia which were published online, e.g., www.kompas.com, www.antaranews.com, SWA magazine www.swa.co.id), tempo newspapers (www.tempo.com) and each company’s official website. Meanwhile, environmental awards are measured from awards received by companies related to environmental management given by the government and non-profit institutions that focus on environmental issues. The awards include the Indonesia Sustainability Reporting Award (ISRA) organized by the National Center for Sustainability Reporting (NCSR) in collaboration with the Institute of Certified Sustainability Practitioners (ICSP) (https://www.ncsr-id.org/id), Kehati Sri Index (http://www.kehati.or.id/indeks-sri-kehati-2/), and the Indonesia CSR Award (ICA) (https://csr-indonesia.com/). Financial performance in this study was measured by ROA, ROE, and Profit Margin. Finally, five CG principles are measured based on the level of compliance with regulations related to CG implementation issued by the Indonesian government authorities.

Based on the description above, it can be illustrated in the theoretical framework shown in .

5. Empirical results and discussion

5.1. Descriptive statistics

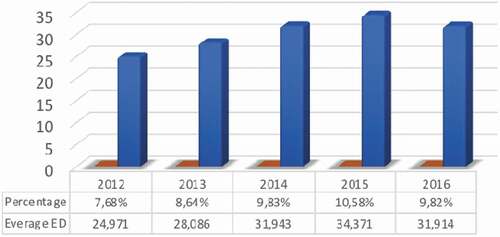

The descriptive statistics as shown in demonstrates that the quality of environmental responsibility disclosure in environmentally sensitive industries in the Indonesian Stock Exchange remains low with an average of 9.31% during 2012–2016. These results show that management awareness in reporting on social responsibility is low, as concluded by Solikhah et al. (Citation2018). This is confirmed by previous researchers who investigate ED in Indonesia. For example, Djajadikerta and Trireksani (Citation2012) who reveal that the extent of the Corporate Social and Environment Disclosure made by Indonesian listed companies on their corporate websites is low. Meanwhile, Yaya et al. (Citation2018) argue that ED in Indonesia has increased annually, 13.95% in 2011 then 25.25% in 2012 and 30.90% in 2013. The findings show an increase of environmental disclosure from 2012 to 2015 (see ). However, in 2016 there was a slight decrease of 0.76% because the companies were no longer competing to increase the quantity of ED items. The companies prioritized quality and focused on relevant and material issues in the context of economic, social, corporate environmental sustainability, and the surrounding stakeholders. The highest percentage of ED at the level of the Sustainable Development was 24.40% inferred that the companies sought to minimize the environmental damages to the companies’ growth by keeping competitive advantage for future positions. This finding is in line with the previous researchers that the practice of environmental reporting reflects an increased awareness of sustainability (Bouten & Everaert, Citation2014; Nasution & Adhariani, Citation2016).

Figure 2. Environment disclosure quality 2012–2016

Table 1. Descriptive statistic on environment disclosure quality

shows the descriptive statistics of exogenous variables and moderation variables. Media Coverage, Award Variables, and Financial Performance Variables (PM, ROA, ROE) show a high standard deviation, meaning that the cross-section data between companies has a fairly large range of differences. For example, for profit margins, where there were companies that are deficit, but on the other hand there were many companies that make large profits. Meanwhile, the variable of CG principle implementation that obtains the highest score is the ones who implement transparency-related disclosures in the annual reports of companies such as risk management system disclosure, overview of stock disclosure, the overview of financial statements disclosure, the system and the implementation of CG disclosure, and the information disclosure via the company’s website. Out of the five CG principles, accountability is the aspect that has the lowest value. Accountability here is associated with the transparency of the functions, structures, systems, and accountability of the company’s organs so that the company management run effectively among which are the number of audit committee, the audit committee from management or accounting graduates, the number of meetings of the audit committee, a system of award and punishment, as well as the internal control system implemented by the company.

Table 2. Descriptive statistics of exogenous and moderating variables

5.2. The results of partial least squares (PLS) test

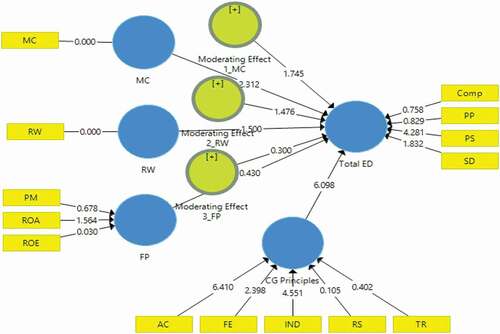

shows the outset test of whole formative indicators and variables. The next step, the assessment of outer loading factor to verify which factors are valid to form a proxy of the analyzed construct. The validity criteria for formative indicators are evaluated on the basis of substantive content and compare the statistical significance of the estimated weight values. The outer loading indicators <0.5 are eliminated from the model (ROE and RS) and re-adaptation of the factor structure. Final model testing is shown in .

Figure 3. Structural model for the initial test

Table 3. Direct and indirect effect test

5.3. Discussion

5.3.1. The effect of media coverage on the environmental disclosure quality

The test results demonstrate that media coverage has a significant positive effect on the quality of environmental disclosure. This result means that the more positive media coverage, the better quality of environmental disclosure. Media coverage in this study has proven to be able to increase the public attention to environmental issues. When the company under public scrutiny, the company will respond by making quality environmental disclosures. This environmental disclosure serves as a form of confirmation of news published by the media in order to re-gain public trust.

Legitimacy theory describes that the company should operate under norms and social values of the community in order to get legitimacy from the community. The way for companies to gain legitimacy from the public is to communicate with relevant stakeholders (Ashforth & Gibbs, Citation1990; Rupley et al., Citation2012). This will encourage company’s management to expose the company’s environmental activities in order to maintain their legitimacy from the society. Hassan and Lahyani (Citation2020) argue that disclosure delivered by companies to stakeholders through various media to convince the public that they are operating according to social expectations and to gain social legitimacy.

The results of this study are in line with research by Rupley et al. (Citation2012) that the existence of media coverage can inform stakeholders about how much the company concerns about environmental issues. Media coverage is assumed to be part of the stakeholders who will assess the company performance based on issues brought by media coverage rather than corporate finance. The existence of such media coverage encourages companies to make wider environmental disclosures.

5.3.2. The effect of environmental award on the environmental disclosure quality

Environmental awards have positive effects on the quality of environmental disclosure. In accordance with the theories of stakeholders (Freeman, Citation1984) which theorizes that awards will motivate companies to disclose a more transparent environment because transparent disclosures can meet the information needs of various interested parties. Based on the theory of legitimacy, the company will try to align its values with the operating social norms. If the company’s values are not in accordance with the values prevailing in the community, there will be a legitimacy gap that can threaten the company’s sustainability. One way to overcome the legitimacy gap is to win an environmental award.

The result of this study is consistent with the results of research from Anas et al. (Citation2015) which found that the most important factor in influencing CSR disclosure was the award received for doing CSR practices well. Companies that receive awards for having good CSR practices have an incentive to disclose quality information related to CSR activities. In accordance with Setiawan’s opinion (Citation2016), company that won the Indonesian Sustainability Reporting Award (ISRA) had more preparation in disclosing environmental performance in an integrated manner.

5.3.3. The effect of financial performance on the environmental disclosure quality

The test results show that financial performance has no significant effect on the quality of environmental disclosure. This is contrary to the theories and findings of previous studies (such as Nasir et al. (Citation2014); Lu and Abeysekera (Citation2014)) which mention that the company’s economic performance is a good incentive to perform and undertake social responsibility program widely. It is assumed that environmental disclosure will cover the company’s success information in its financial performance so that high profitability companies tend to do low environmental disclosure. The fact is the company will make a broad environmental disclosure when profitability is low as a way to establish a positive image of the company. Our research finds that the environmentally sensitive manufactures in Indonesia do not have a sufficient awareness of environmental disclosure, even if it was only to meet the regulations. This study concludes the companies that actively carry out social and environmental responsibility disclosures are government-owned companies.

5.3.4. The implementation of the CG principle moderates the influence between media coverage, award, and profitability on the environmental disclosure quality

The results of this study indicate that the implementation of the principle of CG would strengthen the influence of media coverage and environmental award on the quality of environmental disclosure. The role of CG in companies that have (positive) media coverage is very important since media coverage will shape public opinion. If the company receives negative media coverage, it will have negative impact on the company’s reputation. Thus, it requires the role of good corporate governance so that the company can overcome these problems through quality environmental disclosure. Likewise, if the company receives positive media coverage, if it is supported by the implementation of CG principles in the management of the company, the quality of environmental disclosure will be more extensive and qualified. Environmental disclosure is a form of implementing CG principles, namely transparency and responsibility. The implementation of CG principles is proven to be able to strengthen the relationship between media coverage on the quality of environmental disclosure which can be seen from the greater coefficient value on the indirect effect of 0.163 compared to the value of the direct effect coefficient of 0.148.

The theory and research results presented in developing hypotheses explain that getting an award will motivate companies to make quality environmental disclosures. The award is also a proof that in managing the environment the companies follow the criteria set by the awarding agent. The implementation of CG principles has an important role to get the award. Companies that have implemented the CG principle will have greater awareness regarding environmental concerns including disclosure as CG is a system that regulates and controls the company. The implementation of CG principles in this study moderate the relationship of award to the quality of environmental disclosure.

The implementation of CG principles in every company has different purposes. A company may only focus on financial performance, so that the disclosure of the environment is limited to comply with the regulations established by the government. There are also companies that focus on financial performance and disclose the environment in a quality manner so that they get an award as a company that has managed the environment well. Companies that have implemented the principles of good corporate governance (both high-profile and low-profile companies) will both disclose the environment in their annual reports in accordance with their respective risk levels Arifianata and Wahyudin (Citation2017).

Descriptive statistics demonstrate that companies in Indonesia that broadly disclose environmental performance are state-owned companies. More specifically, they are companies whose shares were mostly owned by the government. This result may be due to the fact that a government-owned company must be able to be a role model and a pioneer in environmental movement. In most companies, the decision to make environmental disclosure needs to consider the cost aspects and the financial condition of the company. Wahyudin and Solikhah (Citation2017) also state that when financial performance is good then the management will be free to carry out environmental disclosure. The implementation of CG principles has an important role in producing good financial performance because CG is a system or mechanism used to regulate, direct and control the company’s operations. However, the implementation of CG principles does not moderate the relationship of financial performance to the quality of environmental disclosure.

Based on stakeholder theory, companies must be able to embrace the surrounding interests through the implementation of CG principles. These interests include producing good financial performance and also carrying out environmental disclosure as a form of responsibility to the community for the activities carried out. Basically, the company will take actions to produce good financial performance in advance to meet the interests of shareholders as primary stakeholders. Frendy and Kusuma (Citation2011) also reveal that the company has enough funds to collect, classify, and process information to be more useful and can present more comprehensive disclosures with high profits.

6. Summary and conclusion

This paper explores voluntary environmental disclosure practices in developing countries, by taking the case of Indonesia. We observe that the low awareness of the company to compile a sustainability report is due to the fact that there is no government regulation that specifically requires environmental reporting. The observation of the quality of environmental disclosure is divided into four groups: compliance, pollution prevention, product stewardship, and sustainable development. Interestingly, the number of disclosures as well as the quality shows an increasing trend from time to time. In contrast to financial reports that have been in standard form and implemented in business and financial practices for centuries, sustainability reports have not yet reached the standard structure level.

The conclusion of this study is that media coverage and awards have a significant positive effect on the quality of environmental disclosure, while financial performance has no effect on the quality of environmental disclosure. The implementation of the principles of CG is able to strengthen the influence of media coverage and environmental award on the quality of environmental disclosure, but cannot moderate the relationship between environmental awards and financial performance of the quality of environmental disclosure. The consequence of this finding is that company management is absolutely required to implement the principles of CG i.e. transparency, accountability, responsibility, independence, fairness, and equality.

Environmental disclosure information in the annual report, sustainability report, and other forms of reports made to stakeholders needs to be improved. This is because the quantity and quality of environmental disclosure in Indonesia remains relatively low. Regulatory efforts through the formulation of policies and intensifying supervision are also needed to increase the awareness of private sectors to report environmental management. And finally, the involvement of all parties including the public, media, and non-governmental organizations is believed to be able to encourage awareness related to environmental management and reporting issues.

For future research, we suggest to improve the engagement of non-ESI companies, and to identify differences in the quality of disclosure. For future cross-border data research, common and civil law needs to be considered, as sustainability report has different rules and expectation between countries.

Additional information

Funding

Notes on contributors

Badingatus Solikhah

Badingatus Solikhah, a lecturer at Accounting Department, Universitas Negeri Semarang, Indonesia. Her major research interests are corporate governance, environmental disclosure, and intellectual capital. Her research has been published in various international journals and proceeding indexed in Scopus and SCI journals. She is experienced as a reviewer for several reputable international journals from Emerald and Inderscience publishers. She employs as an editor and reviewer for several national journals.

Ukhti Maulina, research assistant at Accounting Department, Universitas Negeri Semarang, Indonesia.

References

- Aerts, W., & Cormier, D. (2009). Media legitimacy and corporate environmental communication. Accounting, Organizations and Society, 34(1), 1–18. https://doi.org/https://doi.org/10.1016/j.aos.2008.02.005

- Almaqtari, F. A., Al-Hattami, H. M., Al-Nuzaili, K. M. E., & Al-Bukhrani, M. A. (2020). Corporate governance in India: A systematic review and synthesis for future research. Cogent Business & Management, 7(1), 1803579. https://doi.org/https://doi.org/10.1080/23311975.2020.1803579

- Amran, A., & Nabiha, S. A. (2009). Corporate social reporting in Malaysia: A case of mimicking the west or succumbing to local pressure. Social Responsibility Journal, 5(3), 358–375. https://doi.org/https://doi.org/10.1108/17471110910977285

- Anas, A., Majdi, H., Rashid, A., & Annuar, H. A. (2015). The effect of award on CSR disclosures in annual reports of Malaysian PLCs. Social Responsibility Journal, 11(4), 831–852. https://doi.org/https://doi.org/10.1108/SRJ-02-2013-0014

- Arifianata, A. F., & Wahyudin, A. (2017). Characteristics of firm and environmental disclosure, good corporate governance as moderating variables. Accounting Analysis Journal, 5(2), 47–56. https://doi.org/https://doi.org/10.15294/aaj.v5i2.14360

- Ashforth, B. E., & Gibbs, B. W. (1990). The double-edge of organizational legitimation. Organization Science, 1(2), 177–194. https://doi.org/https://doi.org/10.1287/orsc.1.2.177

- ASX Corporate Governance Council. (2003). Principles of good corporate governance and best practice recommendations. Australian Stock Exchange Corporate Governance Council.

- Barako, D., & Brown, A. (2008). Corporate social reporting and board representation: Evidence from the Kenyan banking sector. Journal of Management and Governance, 12(4), 309–324. https://doi.org/https://doi.org/10.1007/s10997-008-9053-x

- Boesso, G., & Kumar, K. (2007). Drivers of corporate voluntary disclosure: A framework and empirical evidence from Italy and the United States. Accounting, Auditing & Accountability Journal, 20(2), 269–296. https://doi.org/https://doi.org/10.1108/09513570710741028

- Bouten, L., & Everaert. (2014). Social and environmental reporting in Belgium: ‘Pour Vivre Heureux, Vivons Cachés’. Critical Perspectives on Accounting, 33(C), 24–43. https://doi.org/https://doi.org/10.1016/j.cpa.2014.10.002

- Bradford, M., Earp, J. B. & Williams, P. F. (2017). Understanding sustainability for socially responsible investing and reporting. Journal of Capital Markets Studies, 1(1), pp. 10-35. https://doi.org/https://doi.org/10.1108/JCMS-10-2017-005

- Brown, N., & Deegan, C. (1998). The public disclosure of environmental performance information-a dual test of media agenda setting theory and legitimacy theory. Accounting and Business Research, 29(1), 21–41. https://doi.org/https://doi.org/10.1080/00014788.1998.9729564

- Carreira, F., Damiao, A., Abreu, R., & David, F. (2014). Environmental disclosure: From the accounting to the report perspective. In Proceedings of the 16th International Conference on Enterprise Information System (pp. 496–501). https://doi.org/https://doi.org/10.5220/0004973604960501

- Choi, B. B., Lee, D., & Psaros, J. (2013). An analysis of Australian company carbon emission disclosures. Pacific Accounting Review, 25(1), 58–79. https://doi.org/https://doi.org/10.1108/01140581311318968

- Darus, F., Zuki, H. I. M., Yusoff, H. (2020). The Path to Sustainability, Understanding Organisations’ Environmental Initiatives and Climate Change in An Emerging Economy. European Journal of Management and Business Economics, Vol. 29 No. 1, pp. 84-96. https://doi.org/https://doi.org/10.1108/EJMBE-06-2019-0099

- Deegan, C. (2002). The legitimising effect of social and environmental disclosures - a theoretical foundation. Accounting, Auditing and Accountability Journal, 15(3), 282–311. https://doi.org/https://doi.org/10.1108/09513570210435852

- Djajadikerta, H. G., & Trireksani, T. (2012). Corporate social and environmental disclosure by Indonesian listed companies on their corporate web sites. Journal of Applied Accounting Research, 13(1), 21–36. https://doi.org/https://doi.org/10.1108/09675421211231899

- Dowling, J., & Pfeffer, J. (1975). Organizational legitimacy: Social values and organizational behavior. Pacific Sociological Review, 18(1), 122–136. https://doi.org/https://doi.org/10.2307/1388226

- Fatima, A. H., Sulaiman, M., & Abdullah, N. (2015). Environmental disclosure quality: Examining the impact of the stock exchange of Malaysia’s listing requirements. Social Responsibility Journal, 11(4), 904–922. https://doi.org/https://doi.org/10.1108/SRJ-03-2014-0041

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Cambridge University Press.

- Freeman, R. E., & Reed, D. L. (1983). Stockholders and stakeholders: A new perspective on corporate governance. California Management Review, 25(3), 88–106. https://doi.org/https://doi.org/10.2307/41165018

- Frendy, & Kusuma, I. W. (2011). The impact of financial, non-financial, and corporate governance attributes on the practice of global reporting initiative (GRI) based environmental disclosure. Gadjah Mada International Journal of Business, 13(2), 143–159. https://doi.org/https://doi.org/10.22146/gamaijb.5488

- Ghozali, I., & Chairi, A. (2007). Accounting theory. Universitas Diponegoro Press.

- Hassan, M. K., & Lahyani, F. E. (2020). Media, independent non-executive directors and strategy disclosure by non-financial listed firms in the UAE. Corporate Governance, 20(2), 216–239. https://doi.org/https://doi.org/10.1108/CG-01-2019-0032

- Janis, I., & Fadner, R. (1965). The coefficient of imbalance. In H. Lasswell, N. Leites, & Associates (Eds.), Language of politics (pp. 153–169). MIT Press.

- Levin, K., & Fransen, T. (2017). Understanding the “emissions gap” in 5 charts. Working Paper. World Resources Institute Indonesia. https://wri-indonesia.org/en/blog/understanding-%E2%80%9Cemissions-gap%E2%80%9D-5-charts

- Lindblom, C. K. (1994). The implications of organizational legitimacy for corporate social performance and disclosure [Paper presentation]. The critical perspectives on accounting conference, New York

- Lu, Y., & Abeysekera, I. (2014). Stakeholders’ power, corporate characteristics and social and environmental disclosure: Evidence from China. Journal of Cleaner Production, 64, 426–436. https://doi.org/https://doi.org/10.1016/j.jclepro.2013.10.005

- Moses, E., Che-Ahmad, A., & Abdulmalik, S. O. (2020). Board governance mechanisms and sustainability reporting quality: A theoretical framework. Cogent Business & Management, 7(1), 1771075. https://doi.org/https://doi.org/10.1080/23311975.2020.1771075

- Nasir, A., Ilham, E., & Utara, V. I. (2014). The effect of company characteristics and corporate governance on sustainability report disclosures on LQ45 registered companies. Jurnal Ekonomi, 22(1), 1–18. https://doi.org/http://dx.doi.org/10.31258/je.22.01.p.43-60

- Nasution, R. M., & Adhariani, D. (2016). Symbolic or substantive? Analysis of CSR reporting practices and disclosure quality. Jurnal Akuntansi Dan Keuangan Indonesia, 13(1), 23–51. https://doi.org/https://doi.org/10.21002/jaki.2016.02

- Ntim, C. G., Soobaroyen, T., & Broad, M. J. (2017). Governance structures, voluntary disclosures and public accountability the case of UK higher education institutions. Accounting, Auditing & Accountability Journal, 30(1), 65–118. https://doi.org/https://doi.org/10.1108/AAAJ-10-2014-1842

- O’Donovan, G. (2002). Environmental disclosures in the annual report: Extending the applicability and predictive power of legitimacy theory. Accounting, Auditing and Accountability Journal, 15(3), 344–371. https://doi.org/https://doi.org/10.1108/09513570210435870

- Ofoegbu, G. N., Odoemelam, N., & Okafor, R. G. (2018). Corporate board characteristics and environmental disclosure quantity: Evidence from South Africa (integrated reporting) and Nigeria (traditional reporting). Cogent Business & Management, 5(1), 1551510. https://doi.org/https://doi.org/10.1080/23311975.2018.1551510

- Qu, W., & Leung, P. (2006). Cultural impact on Chinese corporate disclosure – a corporate governance perspective. Managerial Auditing Journal, 21(3), 241–264. https://doi.org/https://doi.org/10.1108/02686900610652991

- Radhouane, I., Nekhili, M., Nagati, H., & Paché, G. (2020). Is voluntary external assurance relevant for the valuation of environmental reporting by firms in environmentally sensitive industries? Sustainability Accounting, Management and Policy Journal. 11(1). ahead-of-print No. ahead-of-print. https://doi.org/https://doi.org/10.1108/SAMPJ-06-2018-0158

- Reverte, C. (2009). Determinants of corporate social responsibility disclosure ratings by Spanish listed firms. Journal of Business Ethics, 88(2), 351–366. https://doi.org/https://doi.org/10.1007/s10551-008-9968-9

- Rupley, K. H., Brown, D., & Marshall, R. S. (2012). Governance, media and the quality of environmental disclosure. Journal of Accounting and Public Policy, 31(6), 610–640. https://doi.org/https://doi.org/10.1016/j.jaccpubpol.2012.09.002

- Setiawan, A. (2016). Integrated Reporting: Are Indonesian Companies Ready to Do It?. Asian Journal of Accounting Research, 1(1), pp. 62 –70. https://doi.org/https://doi.org/10.1108/AJAR-2016-01-02–B0042

- Shocker, A. D., & Sethi, S. P. (1973). An approach to incorporating social preferences in developing corporate action strategies. California Management Review, 15(4), 97–105. https://doi.org/https://doi.org/10.2307/41164466

- Smith, M., Yahya, K., & Amiruddin, A. M. (2007). Environmental disclosure and performance reporting in Malaysia. Asian Review of Accounting, 15(2), 185–199. https://doi.org/https://doi.org/10.1108/13217340710823387

- Solikhah, B., Wahyudin, A., & Subowo. (2020). Carbon emissions of manufacturing companies in Indonesia stock exchange: A sustainable business perspective. Journal of Physics: Conference Series, 1567(2020), 042086. https://doi.org/https://doi.org/10.1088/1742-6596/1567/4/042086

- Solikhah, B., Wahyudin, A., Yulianto, A., & Fathudin, M. I. (2018). Carbon emission disclosure on manufacturing companies in Indonesia. Proceeding of international conference: 3rd SHIELD, 2018, pp. 178–184. https://3rdshieldproceeding.uprci.org

- Solikhah, B., & Winarsih, A. M. (2016). Effects of media coverage, industry sensitivity, and corporate governance structure on the quality of environmental disclosure. Jurnal Akuntansi Dan Keuangan Indonesia, 13(1), 1–22. https://doi.org/https://doi.org/10.21002/jaki.2016.01

- Suhardjanto, D., & Permatasari, N. D. (2010). The effect of corporate governance, ethnicity, and educational background on environmental disclosure. KINERJA, Journal of Business and Economics, 14(2), 151–164. https://doi.org/https://doi.org/10.24002/kinerja.v14i2.45

- Sulaiman, M., Abdullah, N., & Fatima, A. H. (2014). Determinants of environmental reporting quality in Malaysia. International Journal of Economics, Management and Accounting, 22(1), 63–90. https://journals.iium.edu.my/enmjournal/index.php/enmj/article/view/253/179

- Suttipun, M., & Stanton, P. (2012). A study of environmental disclosures by Thai listed companies on websites. 2nd Annual International Conference on Accounting and Finance (AF 2012) 2(Af), pp. 9–15. https://doi.org/https://doi.org/10.1016/S2212-5671(12)00059-7

- The Organisation for Economic Co-operation and Development (OECD). (2003). White paper on corporate governance in Asia. Organisation for Economic Co-operation and Development.

- Wahyudin, A., & Solikhah, B. (2017). Corporate governance implementation rating in Indonesia and its effects on financial performance. Corporate Governance: The International Journal of Business in Society, 17(2), 250–265. https://doi.org/https://doi.org/10.1108/CG-02-2016-0034

- Wakaisuka-Isingoma, J., Aduda, J., Wainaina, G., & Mwangi, C. I. (2016). Corporate governance, firm characteristics, external environment and performance of financial institutions in Uganda: A review of literature. Cogent Business & Management, 3(1), 1261526. https://doi.org/https://doi.org/10.1080/23311975.2016.1261526

- Yaya, R., Wibowo, S. A., Ulfaturrahmah, & Jalaludin, D. (2018). Environmental disclosure practices after mandatory disclosure policy in Indonesia. Journal of Business and Retail Management Research (JBRMR), 12(4). https://doi.org/https://doi.org/10.24052/JBRMR/V12IS04/ART-09.

Appendix 1.

The Definition and Measurement of Variable

Appendix 2.

Corporate Governance Principle Implementation Index