?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Related Party Transactions (RPTs) are perceived as genuine transactions, which fulfill the economic needs of a company. However, the controlling shareholders may use RPTs as a tool for transferring the firm’s resources for their private benefit. The dual effect of RPTs, i.e., transaction efficiency and conflict of interest between the controlling shareholders and minority shareholders, increase audit risk and as a result, increases the audit fee. The Companies Act, 2013, and Clause 49 of the SEBI listing agreement mandate arm’s length principle of pricing of RPTs. However, there are situations in which the regulations are silent about the method of pricing, and this increases the risk of auditors for auditing RPTs. This study intends to examine the relationship between RPTs and audit risk in India, based on a sample of 1,182 firms covering a period from 31 March 2011 to 31 March 2018. Panel data methodology has been applied for empirical analysis and the results show that higher audit fee is an indication of resource transferring RPTs. The results prove that instead of reducing the complexity associated with RPTs, the new RPTs regulations increase audit fee as a result of the increases in audit risk.

JEL:

PUBLIC INTEREST STATEMENT

This paper examines the impact of Related Party Transactions (RPTs) on audit risk. RPTs include sale and purchase of goods, transfer of assets, liabilities, providing guarantee, etc. RPTs are considered as genuine business transactions, which reduce transaction costs and facilitate resource allocation between-group affiliated firms. However, the controlling shareholders may use RPTs as a tool for transferring the firm’s resources for their private benefit and manipulating firm’s earnings and assets. In India, Satyam scandal shows the consequences of RPTs, the Chairman inflated the profit figures and assets and the failed acquisitions was his last attempt to write off the inflated figures. The various consequences and effects of RPTs increase audit risk and it questions the effectiveness of governance mechanism. The results of the study show that the presence and volume of RPTs increase audit risk. The results of the study are useful to the investors and the regulators to know the effectiveness of the transparency of RPT regulations.

1. Introduction

This paper empirically examines the effect of Related Party Transactions (RPTs) on audit risk among 1,182 selected companies in India. Ind-AS 24 defines related party transaction (RPT) as “a transfer of resources, services, or obligations between related parties, regardless of whether a price is charged”. An entity’s transaction towards its managers, subsidiaries, directors, and affiliates is always a reason for concern because they may violate the principle of arm’s length pricing, which makes these types of transactions more complex and diverse. The transactions between related parties may expropriate the right of minority shareholders, and controlling shareholders may use RPTs as a tool to divert the firm’s resources for their private benefit (Henry et al., Citation2012). The efficiency-enhancing hypothesis says that RPTs increase the efficiency of a firm through the creation of an internal market within corporate groups (El-Helaly, Citation2016). The conflict of interest hypothesis says that RPTs are harmful to the firm’s interest because there is chance for expropriation of the interest of minority shareholders by the controlling shareholders (Cheung et al., Citation2009; Elkelish, Citation2017; Gordon et al., Citation2004; J. J. Chen et al., Citation2011). The expropriation of the interests of minority shareholders results in the violation of the principle of arm’s length pricing. Many publicized accounting frauds around the world involving firms Satyam (India), Enron (USA), and Tyco (Ireland) show the abusive nature of RPTs, but the law does not prohibit it because RPTs are normal business transactions, and within corporate groups, RPTs facilitate efficient allocation of resources. The governance mechanism must facilitate resource allocation between affiliates without losing the wealth of minority shareholders (Wong, and Kim, Citation2015; Wan & Wong, Citation2015; Wong, Kim, and Lo, 2015; Chauhan et al., Citation2016; Suhaily et al., Citation2016; Kohlbeck & Mayhew, Citation2004; Habib, Muhammadi, Jiang et al., Citation2017b).

In India, most of the companies engage in various types of RPTs to fulfil their economic needs. Srinivasan (Citation2013) find that more than 80% of Indian companies have transactions with their related parties, except for their KMP, and the major RPTs were income-related RPTs, expenses-related RPTs, and loans and deposits. The Companies Act, 2013, and LODR of SEBI are the major regulations of RPTs in India. After the Satyam scam, the Companies Act, 2013, came in place of the previous Act of 1956 with some improved measures for RPTs, and SEBI revised their Clause 49 of the listing agreement following the provisions of the company law. Board independence, audit committee independence, audit rotation, audit firm, etc. increase the quality of governance and disclosure. Jiang et al. (Citation2019) argue that big N auditors provide higher audit quality but capital market may not attach any informativeness to the audit quality of big N auditors. Widyaningsih et al. (Citation2019) find that audit rotation is effective without any coercive regulation and Almaqtari et al. (Citation2020) argue that board independence and audit committee independence, foreign ownership and institutional ownership have the majority focus of research in India. Yang et al. (Citation2020) find that auditors experience while examining RPTs moderate the effect of firms incentive to manage earnings and the likelihood of the auditor requesting additional evidence. The Companies Act, 2013, and LODR of SEBI mandate that RPTs must be on arm’s length basis, and the Board’s approval and the shareholders’ approval are required unless these are in the ordinary course of business. But the Companies Act, 2013, and LODR of SEBI loosely defined the two terms, i.e., arm’s length price and transactions in the ordinary course of business. Sec 92 C of the Income Tax Act, 1961 provides methods of arm’s length pricing but the determination of arm’s length price depends on the type and nature of transactions, it may vary between firms and industries. The Companies Act, 2013, fails to provide a comprehensive understanding of the concepts of arm’s length price and transactions in the ordinary course of business which increases the risk for auditors auditing RPTs.

1.1. Research gap

Many studies were examined the various consequences of RPTs, but a limited number of studies examined the various aspects of auditing and RPTs. The auditors believe that RPTs increase the risk of material misstatement or fraud and therefore, they charge a high fee to identify such kinds of misstatement. There is a positive relationship between audit fee and volume of RPTs because auditors make additional effort in auditing RPTs (Kohlbeck & Mayhew, Citation2004). This study examines whether the presence and magnitude of RPTs is likely to increase the audit fees or not by selecting a sample of 1,182 companies listed on the Bombay Stock Exchange (BSE) and covers a period from 31 March 2011 to 31 March 2018. Objectives and importance of the study

To examine whether RPTs increase audit risk or not.

To know the effect of new RPT regulations on the relationship between RPTs and audit risk.

The results of the study are useful to the regulators and investors. It is useful to the regulators to make sure that the regulatory measures are transparent and auditors do not face any difficulty while auditing RPTs. The study is important to the investors to know the quality of audit and complexities associated with RPTs.

2. RPTs in india

The presence of family businesses and large business houses strengthen the corporate sector of India, and companies allocate their resources within their affiliated firms via RPTs. The company law and capital market regulators allow the companies to transact with their related parties. In India, almost all companies have business dealings with their related parties in the form of sales, purchases, giving loans and advances etc. (Srinivasan, Citation2013). Sales of goods and purchase of raw materials and finished goods are the major RPTs in India. To control abusive RPTs and facilitate efficient RPTs, the Companies Act, 2013, came into force with some improved regulations. The Companies Act, 2013, implemented with an enhanced definition of RPTs, enhanced scope of related parties, prior approval process and disclosure requirements all these measures reduces the inconsistencies associated with related party transactions. As per the new Companies Act, 2013, special approval of the company by way of special resolution is required, instead of the Central Government approval, if the value of RPTs exceeded the threshold limit. This regulatory change increases the transparency of conducting RPTs. The Board and the audit committee approval are required for certain transactions, but RPTs in the ordinary course of business are exempted from both the audit committee and the Board approval. These changes make the new regulations simpler and facilitate transactions between related parties. However, the concept of arm’s length pricing and transactions in the ordinary course of business increase the complexity of RPTs.

3. Literature review and development of hypotheses

The impact of RPTs has been widely discussed in the existing literature. Studies examining the expropriation of minority shareholders’ rights and RPTs give contradictory findings because two conflicting views are associated with the impact of RPTs, i.e. transaction efficiency and conflict of interest. Louwers et al. (Citation2008) observed 83 SEC actions involving both fraud and RPTs and identified that related-party loans and guarantees are the most frequent type of transaction, which expropriate minority shareholders’ rights. Ullah and Shah (Citation2015) investigated the impact of corporate governance mechanism on RPTs and found that associated firm ownership, CEO duality, and managerial ownership act as agents for the expropriation of minority shareholders rights. Hu et al. (Citation2012) analyzed the determinants of RPTs and find that the size of cross-border RPTs positively associated with concentrated ownership, CEO duality, and imbalance of power among large shareholders, and their findings also prove that there is relationship between outside director’s compensation and cross-border RPTs. Gordon et al. (Citation2004) attempted to identify the determinants of RPTs and their impact on firm value. The results show that weaker corporate governance mechanism associated with more RPTs and there is a negative relationship between industries adjusted returns and RPTs. Group affiliated firms report a high level of RPTs compared with standalone firms because group affiliated firms fulfilled their economic needs through their affiliates (Ming and Wong, Citation2003; Hwang & Kim, Citation2016). Internal corporate governance structure and external monitoring mechanisms are major determinants of RPTs (Kohlbeck & Mayhew, Citation2004; Lo et al., Citation2010; Yeh et al. (Citation2012). Weaker corporate governance is associated with more RPTs, which badly affects firm value and operating performance (Gordon et al., Citation2004). An efficient governance mechanism consisting of diversified directors on the Board and a high proportion of outside directors can reduce the self-dealing transactions (Chauhan et al., Citation2016). Nekhili and Cherif (Citation2011) prove that RPTs can destroy the firm’s value, and Y. Chen et al. (Citation2009) find that only firms with worse operating performance engage RPTs to prop-up their earnings. Dahya et al. (Citation2008) and Jian and Wong (Citation2010) argue that controlling shareholders tunnel out firm’s resources for their personal purposes if their control right is more than their cash flow right and they divert the firm’s resources from where they have low cash flow right to where they have high cash flow right. Wan and Wong (Citation2015) argue that the type of ownership has a detrimental impact on RPTs, wherein state-owned firm engages in more tunnelling than privately controlled firms. Ariff and Hashim (Citation2013) find a statistically significant relationship between RPTs and accounting irregularities.

RPTs are the common cause of corporate scandals and major tool for financial reporting re-statement. Chalardpodjanaporn (Citation2008) examined the application of RPTs in earnings management among listed companies in the Thailand stock exchange. The result proves that RPTs are one of the ways that managers use to manage the firm’s earnings. Cheung et al. (Citation2009) is in line with Gordon, Henry and Palia (Citation2005) that firms’ prop-up their earnings via RPTs. Aharony et al. (Citation2010) and Marchini et al. (Citation2018) argue that firms use RPTs for opportunistic earnings management, and the parent company use related-party loans to tunnel out the resources of the affiliated firms. Apart from manipulation of accruals, RPTs are also used for real earnings management (Wang & Yuan, Citation2012). Khober Limanto and Herusetya (Citation2017) argue that RPTs are used for real earnings management and board commissioners strengthen the positive association between RPTs and real activity manipulations, but the effectiveness of audit committee can control this positive relationship. Firms manipulate their reported earnings to conceal their tunneling via RPTs, and there is a chance to manipulate firm’s earnings to conceal tunneling if firm diverts its resources for the private benefit of the controlling shareholders (Habib, Muhammadi, and Jiang, Citation2017a).

There are empirical and theoretical evidence to show that the presence of RPTs increases audit risk. Al-gmrh et al. (Citation2018) argue that the existence of RPTs can reduce the quality of financial reporting and increase audit risk resulting in increased audit fee. In this study, audit fee is taken as a measure of audit risk. Khan and Abdul Subhan (Citation2019) argue that a high audit fee is an indication of high audit quality due to extended audit hours and expert audit staff to conduct more detailed investigation and Shakhatreh et al. (Citation2020) find that audit fee has a significant effect on disclosure quality. The audit fee is higher for firms that undertook RPTs and internal audit function have a moderating effect on the relationship between RPTs and audit fee (Al-dhamari et al., 2018). Rahmat and Ali (Citation2016) argue that Big-4 auditors could reduce company engagement in RPTs even when they have a close relationship with the firm, and establishing a good relationship with the auditors is likely to create a conflicting opinion which will impair the auditors’ independent judgment. Gordon et al. (Citation2004) reported issues related to auditing of RPTs. Failure in the identification of RPTs is one of the major issues while auditing RPTs, and auditors failed to detect the abusive part of RPTs and are unable to cross-confirm the details of transactions with a third party. Louwers et al. (Citation2008) examined the efficiency of the existing auditing standards relating to RPTs. The results show that a combination of factors made the examination of RPTs difficult and suggested that audit teams should discuss the potential for RPTs abuse during their fraud awareness brainstorming sessions as required by SAS No. 99. Habib et al. (Citation2015) investigated the relationship between RPTs and audit fees in China, and find that the presence of RPTs increases audit risk, and identifying RPTs and verifying the nature and volume of transactions increase the risk of auditors and as a result, increase the audit fee. The audit fee is very high for RPTs involving loans and capital transfers (Habib et al., Citation2015). Based on the theories and the available empirical results, we developed the following hypothesis.

H1: There is a significant positive association between RPTs and audit fee.

In India, the Companies Act, 2013, and revised Clause 49 of the SEBI listing agreement was implemented in the year 2014. The two governance measures were implemented with some improved measures for RPTs to reduce abusive RPTs and to control the expropriation of the controlling shareholders via RPTs. The major criticisms for these regulatory measures are some of the concepts such as “arm’s length price” and “transactions in the ordinary course of business” are loosely defined. The new regulations also added some additional approval and disclosure requirements for RPTs, which could increase the risk of auditors while auditing RPTs. Based on this argument, the following hypothesis is developed:

H1: The revised RPT regulations have a positive moderating effect on the relationship between RPTs and audit fee.

4. Research design

4.1. Sample and data collection

A total of 5,309 companies listed on the BSE were considered for the study. These exclude banking and financial companies due to their specific nature of financial reporting and also those companies whose data are not available during the study period. A period of 8 years from 31 March 2011 to 31 March 2018 is considered for the study, 4 years before the changes in RPT regulations and 4 years after the changes in RPT regulations. Therefore, the final sample is 1182 companies consisting of 9456 firm-year observations. The data for the empirical investigation are taken from the Prowess database maintained by the Centre for Monitoring of Indian Economy Private Limited (CMIE).

4.2. Regression models

The primary interest of the study is to examine the relationship between RPTs and audit risk. Based on the findings of Khan and Abdul Subhan (Citation2019) and Shakhatreh et al. (Citation2020) we chose audit fee as a measure of audit risk. The following econometric model has been developed to examine the impact of RPTs on audit risk and the moderating effect of new RPT regulations on the relationship between RPTs and audit risk.

Here, AFEE is the audit fee. The RPTs have been split into six categories as Total Revenue Receipts (TRR) from related parties, Total Revenue Expenses (TRE) to related parties, Capital Receipts (CRRP) from related parties, Capital Payments (CPRP) to related parties, Borrowings (RPB) from related parties, and Loans and Advances (LARP) to related parties. The total volumes of RPTs are scaled by the total assets. A dummy variable “REG” is used to measure the effect of the new RPT regulations on the relationship between RPTs and audit fee. The dummy variable REG is coded as ‘1ʹ, if the observation is taken from the period 2015–2018, or otherwise is coded as ‘0ʹ. The interaction term “REG*RPT” is used to investigate the assumption that the new regulations increase the audit risk of the RPTs.

A set of controlled variables find in the literature by Mitra et al. (Citation2019), Qu et al. (Citation2020), Gul and Ng (Citation2018), Goncharov et al. (Citation2014), Mitra et al. (Citation2007), and Vafeas and Waegelein (Citation2007) are included. The Size is included to control the firm size, which is the natural log of the firm’s total operating assets. The LEV (debt to total assets) and CR (current assets to current liabilities) to control the liquidity risk is also included along with INV (inventory to total assets) and REC (receivables to total assets) to control the inherent risk. The ROA (profit before interests, tax and preference dividend to total assets) is included to control the profitability of the firm.

5. Results and discussions

5.1. Descriptive statistics

reports the summary statistics of audit fee, RPT variables, and other controlled variables. The mean audit fee is Rs.2.298 million with a standard deviation of 2.964 and the median is Rs.1 million. The natural log of the total assets represents the size of the firm, the mean and median size is 8.33 with a standard deviation of 1.8. The LEV average is 0.44 with a standard deviation of 0.373. LEV shows that the level of financial risk is low and CR is 2.26 indicates a high liquidity positions. ROA represents the profitability of firms, ROA is 0.132 with standard deviation of 0.943 and the median as 0.116. The average of BR is 0.172 with standard deviation of 0.142 and its maximum as 0.926, it shows that the average of BR constitutes 17% of the total assets. The average INV is 0.153 with standard deviation of 0.136 and its maximum as 0.940, it indicates that INV constitutes more than 15% of the total assets.

Table 1. Descriptive statistics of the variables

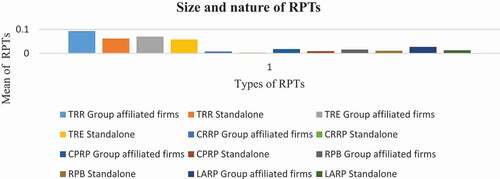

also reports the descriptive statistics of RPTs, which show that most Companies have operating RPTs (TRR and TRE). The average TRR is 0.076 with a standard deviation of 0.183 and its median as 0.007 showing that the average operating receipts (sales, services, etc.) from related parties is more than 7% of the total assets, and it proves that Indian companies have significant business relationship with their related parties. The average TRE is 0.063 with standard deviation of 0.126. The average TRE is less than the average of TRR, but its median is 0.018, which is more than the median of TRR. The reason for the massive change in the median is that the TRE includes the remuneration and incentives paid to Key Managerial Persons (KMPs) since almost all companies have transactions with their KMPs in the form of salaries and remunerations. The average of CRRP is 0.005 with a standard deviation of 0.049 showing that the average capital receipts from related parties is less than 1% of the total assets. The averages of CPRP, RPB, and LARP are 0.013, 0.013, and 0.019 showing that the average non-operating RPTs are less than 2% of the total assets. The descriptive statistics show that most of the RPTs in Indian firms are of an operating nature, and compared with operating RPTs, only few companies have non-operating RPTs (CRRP, CPRP, RPB, and LARP).

reports the descriptive statistics of the variables in group affiliated firms and standalone firms. It shows that the mean difference of all the variables is statistically significant at 1% level. The sample consists of 1159 firm-year observations, and of these, 4248 observations are of firms belonging to the business group and the remaining 5024 observations are of standalone firms. The mean AFEE is Rs.3.26 million in group affiliated firms and Rs 1.484 million in standalone firms showing that the average audit fee in group affiliated firms is twice that of the average of standalone firms, and the mean difference is 1.776, which is statistically significant at 1% level. The mean difference in the size of group affiliated firms compared with standalone firms is 1.09 and the mean difference of the LEV is 0.035, and both the figures are statistically significant. The mean difference of ROA in group affiliated firms to standalone firms is 0.009 and statistically significant showing that standalone firms underperformed compared with group affiliated firms. The mean differences of all the other controlled variables such as CR and BR are negative and statistically significant.

Table 2. Descriptive statistics in group affiliated firm and standalone firms

The average TRR is 0.093 in group affiliated firms and 0.062 in standalone firms. The average TRE is 0.070 in group affiliated firms and 0.058 in standalone firms. The mean differences of both TRR and the TRE are statistically significant showing that the level of operating RPTs in group affiliated firms is higher than the level of RPTs in standalone firms. The average CRRP is 0.008 in group affiliated firms and 0.003 in standalone firms, and the difference is more than twice of the average in standalone firms, which is statistically significant. The average CPRP is 0.018 in group affiliated firms and 0.009 in standalone firms, and the mean difference is twice of the average of standalone firms. The average of RPB is 0.016 in groups affiliated firms and 0.011 in standalone firms, and even though the values are less than 2% of the total assets, their mean difference is statistically significant. The descriptive statistics also show that group affiliated firms give more loans and advances to their affiliates. The average LARP is 0.027 in group affiliated firms and 0.013 in standalone firms, and the difference is twice of the average of standalone firms. The descriptive statistics and the associated two-sample independent t-tests show that the magnitude of various types of RPTs (both operating RPTs and non-operating RPTs) in group affiliated firms is higher than the magnitude of RPTs in standalone firms.

reports the correlation statistics of the variables used in the analysis. The correlation statistics show that there is no exact collinearity between the variables. The firm’s size has positive correlations with LEV, ROA, TRE, CRRP, and LARP and negative correlation with CR, BR, and RPB. LEV has a negative and significant correlation with ROA and CR and positive correlation with BR, INV, CRRP, CPRP, RPB, and LARP. It shows that there is a positive correlation between LEV and non-operating RPTs. ROA has a positive correlation with CR, TRR, TRE, CRRP, CPRP, and LARP and negative association with INV and RPB. CR has negative and significant correlations with BR, INV, TRE, and RPB. BR has a negative correlation with INV and LARP and positive correlation with TRR. INV has a negative correlation with TRR, CPRP, and LARP.

Table 3. Correlation statistics for variables used in the analysis

5.2. Empirical results

The panel data procedure is followed to estimate the regression coefficients. To identify the best estimators of the coefficients, three regression sets for each model, namely, pooled OLS, fixed-effect model, and random effect model are estimated. The Wald-statistic proves that there is individual heterogeneity in the models and the panel fixed effect is chosen to estimate the relationship between the variables. The Hausman-statistic is used to test whether the individual heterogeneity is random or not, and the null hypothesis of the Hausman test that individual heterogeneity is random is rejected, and fixed effect model is chosen to estimate the coefficients. Due to the problems of serial correlation and heteroskedasticity, the cluster-robust standard error is chosen. Three sets of regression models are estimated wherein the first set represents the full sample and the second and third sets represent group affiliated firms and standalone firms, respectively.

reports the empirical findings of the relationship between RPTs and audit fee of the selected firms. About 12 sets of regressions are performed from Model 1 to Model 12, wherein Model 1showes the empirical relationship between TRR and audit fee, Model 2 shows the interaction effect of new RPT regulations on the relationship between TRR and audit fee, and likewise, Model 3 onwards shows the impact of various types of RPTs such as TRE, CRRP, CPRP, RPB, and LARP on the audit fee. The RPT coefficient in Model 1is 0.56 and which is significant at 1% level of significance, showing that revenue receipts from related parties increase the audit fee. The results are consistent with the argument that the presence of RPTs increases the risk of auditors and consequently, audit risk premium. In Model 3, the coefficient of RPT is 0.96, which is statistically significant showing that the payment of revenue expenses to related parties increases the audit risk and consequently, the audit fee. The empirical results prove that both the revenue receipts from related parties and revenue payments to related parties increase audit risk and consequently, the audit fee. The results are consistent with Dhamari et al.(2018), who reported that firms that are involved in operating RPTs bore high audit fee to compensate for the risk and effort of auditors for auditing RPTs. also proves that except for TRR and TRE, none of the RPT variables are statistically significant. The coefficients of CRRP, RPB, and LARP are positive, but statistically insignificant which shows that only operating RPTs affect the audit fee. The results also show that the relationship between TRE and audit fee is very strong compared with the relationship between TRR and audit fee.

Table 4. Regression results

also reports the interaction effect of RPT regulations on the relationship between RPTs and audit fee. The interaction effects of new regulations on the relationship between various types of RPTs and audit fee is positive and statistically significant. The interaction terms are positive and significant even though the relationship between non-operating RPTs and audit fee is insignificant. The coefficient of the interaction effect of REG is 1.2 on the relationship between TRR and audit fee, and the coefficient is 2.4 on the relationship between TRE and audit fee; likewise, the coefficients of the interaction term “RPT*REG” in other models are 1.4, 2, 0.88 and 2.1. The statistically significant interaction effect of “REG” on the relationship between various types of RPTs and audit fee supports the argument that instead of reducing the complexity associated with RPTs, the new RPT regulations increase the risk of auditors of auditing RPTs. The interaction effect of “REG” is very strong on the relationship between TRE and audit fee compared with other RPTs; one possible explanation is that the amount of TRE is high compared with other types of RPTs. Another possible explanation for the positive association between operating RPTs (TRR and TRE) and audit fee is that the magnitude and number of operating RPTs is very high compared with non-operating RPTs, and the audit risk increase if the number and volume of the RPTs increase. The results of the regression models reported in are significant at 1% level, while the F-statistic varies between 21 and 28.7 and the R2varies between 0.41 and 0.43. Except for CR, all the controlled variables are statistically significant. The coefficients of Size are positive and significant showing that as size increases, the audit fee also increases. LEV is negatively significant in all the models showing that an increase in leverage reduces the audit fee. The coefficients of ROA are positive and significant, showing that the firm’s profitability has a positive association with the audit fee. The positive and significant effect of INV and BR show that the valuation and auditing of the books of accounts relating to inventory and bills receivables increase the audit risk of auditors and consequently, the audit fee.

reports the empirical evidence of the relationship between RPTs and audit fee in group affiliated firms. The results based on a sample of 4248 firm-year observations show that in group affiliated firms, operating RPTs have significant positive impact on audit fee. Compared with the estimates of the full sample, the relationships in group affiliated firms are strong and the coefficient of TRR increased from 0.56 to 0.68 and the coefficient of TRE increased from 0.97 to 1.4 in group affiliated firms. The results also show that there is no statistically significant association between non-operating RPTs and audit fee, and the results are in line with the results of the full sample. Most of the coefficients of non-operating RPTs are positive but statistically insignificant. The overall findings show that TRR and TRE have a positive impact on audit fee, and this relationship is very strong in-group affiliated firms. The moderating effect of “REG” on the relationship between various RPTs and audit fee also exists in group affiliated firms, and the coefficients of REG*RPT varies between 0.88 and 2.4 in various models which are almost similar to the results of the full sample.

Table 5. Regression results (business group)

also shows that the controlled variables Size, ROA, and BR are positive and significant; CR and LEV are negative but insignificant, and INV is positive and insignificant. The statistical significance of Size and ROA shows that audit risk increases as the profitability and size of the firm increases, and there is a positive impact of BR on audit fee. The R2varies between 0.45 and 0.47 and all the models are statistically significant at 1% level.

reports the empirical findings of the impact of RPTs on audit fee of standalone firms in India. The findings are similar to the findings of the full sample that operating RPTs have a significant positive impact on audit fee. The coefficient of TRR is 0.41 and the coefficient of TRE is 0.64 and both are statistically significant at 1% level. The relationship of RPTs and audit fee in standalone firms is similar to group affiliated firms, but the value of the coefficient is low in standalone firms. Similar to the findings of group affiliated firms, the non-operating RPTs in standalone firms do not have any impact on the audit fee. The coefficients of non-operating RPTs such as CRRP, CPRP, RPB and LARP are 0.20, −0.3, 0.15 and −0.4 and statistically insignificant. The interaction effect of “REG” on the relationship between RPTs and audit fee is positive and significant in all the models. The coefficients of the interaction term are 0.57, 2.17, 0.87, 1.3, 0.40 and 1.1. The interaction effect of “REG” is very strong on the relationship between TRE and audit fee and this relationship is consistent with the results of group affiliated firms. The statistical significance of the interaction effect of “REG” proves that the new RPT regulations increase the audit risk of all types of RPTs. The controlled variables used in the regression analysis reported in are partly significant; Size and INV are positively significant and LEV is negative and significant. The R2 value varies between 0.33 and 0.36 in various models and the F-statistic is more than 13 shows that the models are significant at 1% level of significance.

Table 6. Regression results (standalone firms)

5.3. Sensitivity analysis

A robustness check is conducted using the OLS method and the panel fixed-effect method. Separate year specific dummy variables are used to control the time effect in the panel OLS regressions, and most of the time, the dummy variables are insignificant, but the regression results were almost similar in panel fixed-effect model. Some additional variables such as founders’ holdings and board size were also added, but the additional variables do not bring any change in the regression results. The Wald-statistic suggests that the fixed effect model is appropriate than the pooled OLS and the Hausman-test prove that the entity effect is fixed and not random.

6. Conclusions

The dual effect of RPTs increases the audit risk of RPTs. A few studies examined the auditing aspect of RPTs. The present study aims to measure the impact of various types of RPTs on audit risk measured by the amount of audit fee in selected firms, which are listed in the BSE. The examinations associated with RPTs are value relevant in emerging countries, especially in India, where most of the firms use RPTs to fulfill their economic needs and the ownership structure of the corporate is concentrated. The study also intends to address an unanswered question of whether the new RPT regulations implemented in the year 2014 increases or reduces the risk of auditors. The new Companies Act, 2013, and the revised Clause 49 of the SEBI listing agreement were implemented with some improved measures for RPTs.

The empirical findings show that the types of RPTs such as TRR and TRE increase the audit risk and as a result, it increases the audit fee. TRR and TRE are the most frequent RPTs in Indian companies, and the frequency and volume of RPTs such as CRRP, CPRP, RPB and LARP is low. The positive effect of TRR and TRE on audit fee exists in group affiliated firms and standalone firms and the relationship is very strong in-group affiliated firms. The additional regression results, which measured the impact of new RPT regulations on the relationship between RPTs and audit fee, show a positive interaction effect proving that the new RPT regulations increase the complexity of auditing RPTs.

The results are useful to various stakeholders, especially standard setters and regulators. In India, majority of the RPTs represent usual business dealings such as sales, purchases, payment of wages, etc. and it would help in the efficient allocation of resources between affiliates. The frequency of operating RPTs and the complexity associated with RPTs increase the audit risk and consequently, the audit fee. The revised RPT regulations implemented in the year 2015 also increase the audit risk of all types of RPTs. The market regulators and company regulators should simplify the regulations associated with RPTs to facilitate the transfer of goods and services between affiliates, and at the same time, the regulators must ensure that the policy and governance measures are effective to control abusive RPTs.

Additional information

Funding

Notes on contributors

Abdul Rasheed P. C

Dr.Iqbal Thonse Hawaldar completed his Bachelor, Master and PhD degrees from India. He is a Professor of Finance at Kingdom University, Bahrain. He published more than 65 research papers in the field of Finance, banking, and management. He is the reviewer for many reputed journals and international conferences.

Iqbal Thonse Hawaldar

Abdul Rasheed P. C. is an Assistant Professor at Centre for Management Studies and Research, PA College of Engineering, Mangalore, India. He has successfully completed PhD in Commerce from the Department of Commerce, Mangalore University, India. His field of study is finance and corporate governance.

Mallikarjunappa T

T. Mallikarjunappa Professor and Head, Department of Commerce and International Business, Central University of Kerala, India. Before this he worked as professor of Business Administration, Mangalore University, India. He is an associate member of the Institute of Cost Accountants of India. His research areas are Accounting and Finance. He has published 135 papers and presented 375 papers.

References

- Aharony, J., Wang, J., & Yuan, H. (2010). Tunnelling as an incentive for earnings management during the IPO process in China. Journal of Accounting and Public Policy, 29(1), 1–17. https://doi.org/https://doi.org/10.1016/j.jaccpubpol.2009.10.003

- Al-gamrh, R. A. A. B. (2018). Related party transactions and audit fees : The role of the internal audit function. Journal of Management & Governance, 22(1), 187–212. https://doi.org/https://doi.org/10.1007/s10997-017-9376-6

- Almaqtari, F. A., Al-Hattami, H. M., Al-Nuzaili, K. M. E., & Al-Bukhrani, M. A. (2020). Corporate governance in India: A systematic review and synthesis for future research. Cogent Business and Management, 7(1), 1. https://doi.org/https://doi.org/10.1080/23311975.2020.1803579

- Ariff, A. M., & Hashim, H. A. (2013). The breadth and depth of related party transactions disclosures. International Journal of Trade, Economics, and Finance, 4(6), 388–392. https://doi.org/https://doi.org/10.7763/IJTEF.2013.V4.323

- Chalardpodjanaporn, (2008). Application of related party transactions in earnings management: An empirical evidence from the stock exchange of thailand. Doctoral Dissertation (joint doctoral programme), Thammasat University, Chulalongkorn University and National Institute of Development Administration.

- Chauhan, Y., Lakshmi, K. R., & De, D. K. (2016). Corporate governance practices, self-dealing, and firm performance: Evidence from India. Journal of Contemporary Accounting & Economics, 12(3), 274–289. https://doi.org/https://doi.org/10.1016/j.jcae.2016.10.002

- Chen, J. J., Chengb, P., & Xiao, X. (2011). Related party transactions as a source of earnings management. Applied Financial Economics, 21(3), 165–181. https://doi.org/https://doi.org/10.1080/09603107.2010.528361

- Chen, Y., Chen, C. H., & Chen, W. (2009). The impact of related party transactions on the operational performance of listed companies in China. Journal of Economic Policy Reform, 12(4), 285–297. https://doi.org/https://doi.org/10.1080/17487870903314575

- Cheung, Y. L., Jing, L., Lu, T., Rau, P. R., & Stouraitis, A. (2009). Tunneling and propping up: An analysis of related party transactions by Chinese listed companies. Pacific Basin Finance Journal, 17(3), 372–393. https://doi.org/https://doi.org/10.1016/j.pacfin.2008.10.001

- Dahya, J., Dimitrov, O., & McConnell, J. J. (2008). Dominant shareholders, corporate boards, and corporate value: A cross-country analysis. Journal of Financial Economics, 87(1), 73–100. https://doi.org/https://doi.org/10.1016/j.jfineco.2006.10.005

- El-Helaly, M. (2016). Related party transactions and accounting quality in Greece. International Journal of Accounting & Information Management, 24(4), 375–390. https://doi.org/https://doi.org/10.1108/IJAIM-04-2016-0044

- Elkelish, W. W. (2017). IFRS related party transactions disclosure and firm valuation in the United Arab Emirates emerging market. Journal of Accounting in Emerging Economies, 7(2), 173–189. https://doi.org/https://doi.org/10.1108/JAEE-05-2015-0035

- Goncharov, I., Riedl, E. J., & Sellhorn, T. (2014). Fair value and audit fees. Review of Accounting Studies, 19(1), 210–241. August 2013. https://doi.org/https://doi.org/10.1007/s11142-013-9248-5

- Gordon, E. A., Henry, E., & Darius, P. (2004). Determinants of related party transactions and their impact on firm value. In American Accounting Association 2004 Annual Conference Paper.USA, 1–60.

- Gordon, E. A., Henry, E., & Palia, D. (2005). Related Party Transactions: Associations with Corporate Governance and Firm Value. SSRN Electronic Journal. https://doi.org/https://doi.org/10.2139/ssrn.558983

- Gul, F. A., & Ng, A. C. (2018). Auditee Religiosity, External Monitoring, and the Pricing of Audit Services. Journal of Business Ethics, 152(2), 409–436. https://doi.org/https://doi.org/10.1007/s10551-016-3284-6

- Habib, A., Jiang, H., & Zhou, D. (2015). Related-Party Transactions and Audit Fees: Evidence from China. Journal of International Accounting Research, 14(1), 59–83. https://doi.org/https://doi.org/10.2308/jiar-51020

- Habib, A., Muhammadi, A. H., & Jiang, H. (2017a). Political connections and related party transactions: Evidence from Indonesia. International Journal of Accounting, 52(1), 45–63. https://doi.org/https://doi.org/10.1016/j.intacc.2017.01.004

- Habib, A., Muhammadi, A. H., & Jiang, H. (2017b). Political connections, related party transactions, and auditor choice: Evidence from Indonesia. Journal of Contemporary Accounting and Economics, 13(1), 1–19. https://doi.org/https://doi.org/10.1016/j.jcae.2017.01.004

- Henry, E., Gordon, E., Reed, B., & Louwers, T. (2012). The role of related party transactions in fraudulent financial reporting. Journal of Forensic & Investigative Accounting, 4(1), 186–213. https://doi.org/https://doi.org/10.2139/ssrn.993532

- Hu, S.-H., Li, G., Xu, Y.-H., & Fan, X.-A. (2012). Effects of internal governance factors on cross-border-related party transactions of chinese companies. Emerging Markets Finance and Trade, 48, 58–73. https://doi.org/https://doi.org/10.2753/REE1540-496X4801S105

- Hwang, S., & Kim, W. (2016). When heirs become major shareholders: Evidence on pyramiding financed by related-party sales. Journal of Corporate Finance, 41, 23–42. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2016.08.013

- Jian, M., & Wong, T. J. (2010). Propping through related party transactions. Review of Accounting Studies, 15(1), 70–105. https://doi.org/https://doi.org/10.1007/s11142-008-9081-4

- Jiang, J., Wang, I. Y., & Philip Wang, K. (2019). Big N auditors and audit quality: New evidence from quasi-experiments. Accounting Review, 94(1), 205–227. https://doi.org/https://doi.org/10.2308/accr-52106

- Khan, A. W., & Abdul Subhan, Q. (2019). Impact of board diversity and audit on firm performance. Cogent Business and Management, 6(1), 1. https://doi.org/https://doi.org/10.1080/23311975.2019.1611719

- Khober Limanto, G., & Herusetya, A. (2017). The Association between related party transactions and real earnings management: Internal governance mechanism as moderating variables. SHS Web of Conferences, 34, 04008. https://doi.org/https://doi.org/10.1051/shsconf/20173404008

- Kohlbeck, M. J., & Mayhew, B. W. (2004). Agency costs, contracting, and related party transactions. SSRN Electronic Journal, March 2017. https://doi.org/https://doi.org/10.2139/ssrn.592582.

- Lo, A. W. Y., Wong, R. M. K., & Firth, M. (2010). Can corporate governance deter management from manipulating earnings? Evidence from related-party sales transactions in China. Journal of Corporate Finance, 16(2), 225–235. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2009.11.002

- Louwers, T. J., Henry, E., Reed, B. J., & Gordon, E. A. (2008). Deficiencies in auditing related-party transactions: Insights from AAERs. Current Issues in Auditing, 2(2), A10–A16. https://doi.org/https://doi.org/10.2308/ciia.2008.2.2.A10

- Marchini, P. L., Mazza, T., & Medioli, A. (2018). The impact of related party transactions on earnings management: Some insights from the Italian context. Journal of Management and Governance, 22(6), 1–34. https://doi.org/https://doi.org/10.1007/s10997-018-9415-y

- Ming, J. J., & Wong, T. J. (2003). Earnings Management and Tunneling through Related Party Transactions: Evidence from Chinese Corporate Groups. SSRN Electronic Journal. https://doi.org/https://doi.org/10.2139/ssrn.424888

- Mitra, S., Hossain, M., & Deis, D. R. (2007). The empirical relationship between ownership characteristics and audit fees, Review of Quantitative Finance and Accounting 28 (3), 257–285. https://doi.org/https://doi.org/10.1007/s11156-006-0014-7

- Mitra, S., Jaggi, B., & Al-hayale, T. (2019). Managerial overconfidence, ability, firm-governance, and audit fees. Review of Quantitative Finance and Accounting. https://doi.org/https://doi.org/10.1007/s11156-018-0728-3

- Nekhili, M., & Cherif, M. (2011). Related parties transactions and the firm’s market value: The French case. Review of Accounting and Finance, 10(3), 291–315. https://doi.org/https://doi.org/10.1108/14757701111155806

- Qu, X., Yao, D., & Percy, M. (2020). How the Design of CEO Equity-Based compensation can lead to lower audit fees : Evidence from Australia. Journal of Business Ethics, 1(1), 281-308. https://doi.org/https://doi.org/10.1007/s10551-018-4031-y

- Rahmat, M. M., & Ali, S. H. A. (2016). Do managers reappoint auditor for related party transactions? Evidence from selected East Asian countries. Jurnal Pengurusan, 48(3), 1–22. https://doi.org/https://doi.org/10.17576/pengurusan-2016-48-04

- Shakhatreh, M. Z., Alsmadi, S. A., & Alkhataybeh, A. (2020). The effect of audit fees on disclosure quality in Jordan. Cogent Business and Management, 7(1), 1. https://doi.org/https://doi.org/10.1080/23311975.2020.1771076

- Srinivasan, P. (2013). An analysis of related party transactions in india. working paper No.402 IIMB, http://www.iimb.ernet.in/research/sites/default/files/WPNo.402_0.pdf

- Suhaily, H., Daie, R. M., & Hussain, M. R. A. (2016). Related party transactions and earnings quality : Does corporate governance matter? International Journal of Economics and Management, 10, 189–219. April 2015

- Ullah, H., & Shah, A. (2015). Related party transactions and corporate governance mechanisms : Evidence from firms listed on the karachi. Pakistan Business Review, 17(3), 663–680. http://www.masb.org.my/pdf.php?pdf=MFRS%20 124%20042015.pdf

- Vafeas, N., & Waegelein, J. F. (2007). The association between audit committees, compensation incentives, and corporate audit fees. Review of Quantitative Finance and Accounting, 2007(28), 241–255. https://doi.org/https://doi.org/10.1007/s11156-006-0012-9

- Wan, Y., & Wong, L. (2015). Ownership, related party transactions, and performance in China. Accounting Research Journal, 28(2), 143–159. https://doi.org/https://doi.org/10.1108/ARJ-08-2013-0053

- Wang, J., & Yuan, H. (2012). The impact of related party sales by listed Chinese firms on earnings informativeness and earnings forecasts. International Journal of Business, 17(3), 258–275. https://doi.org/https://doi.org/10.2139/ssrn.970873

- Widyaningsih, I. A., Harymawan, I., Mardijuwono, A. W., Ayuningtyas, E. S., & Larasati, D. A. (2019). Audit firm rotation and audit quality: Comparison before vs after the elimination of audit firm rotation regulations in Indonesia. Cogent Business and Management, 6(1), 1. https://doi.org/https://doi.org/10.1080/23311975.2019.1695403

- Wong, R. M. K., & Kim, J. (2015). Are Related-Party Sales Value-Adding or Value-Destroying ? Evidence from China. Journal of International Financial Management and Accounting, 26(1), 1–38

- Yang, L., Ruan, L., & Tang, F. (2020). The impact of disclosure level and client incentive on auditors’ judgments of related party transactions. International Journal of Accounting and Information Management, 28(4), 717–737. https://doi.org/https://doi.org/10.1108/IJAIM-02-2020-0016

- Yeh, Y. H., Shu, P. G., & Su, Y. H. (2012). Related-party transactions and corporate governance: The evidence from the Taiwan stock market. Pacific Basin Finance Journal, 20(5), 755–776. https://doi.org/https://doi.org/10.1016/j.pacfin.2012.02.003

Appendices