Abstract

Nigeria Deposit Insurance Corporation (NDIC) annual reports (2014–2017) suggest that the country’s deposit money banks (DMBs) have been exposed to escalating incidence of fraud and forgeries. This has hampered their capacity, efficiency and contribution to national economic growth and development. This study examines the capability and competence of DMB regulators to prevent and detect fraud and, at the same time, develop an effective mechanism to do so. The study employed quantitative methodology. Data was collected using questionnaires administered on 350 forensic accountants and bank examiners working with the Central Bank of Nigeria (CBN), NDIC and 15 randomly selected DMBs in Lagos. Data collected were analyzed using descriptive statistics and multivariate regression. Key results include significant positive relationship between the study variables and reduction in fraud incidence in DMBs. This result has implications for existing accounting literature on knowledge capability and competence as vehicles for fraud prevention and detection in DMBs in Nigeria. The study recommends an integrative approach to bank examination in which both forensic accountants and bank examiners are involved as permanent fixtures in fraud prevention and detection in DMBs. This will guarantee a fraud-free DMB sector.

Public interest statement

Fraud and forgeries remain a major impediment to efficient financial intermediation by deposit money banks (DMBs) and also deter the DMBs from making significant contribution to national economic development and growth. Subsequently, the research was undertaken in the quest to find solutions to the escalating incidence of fraud within Nigeria deposit money banking sector and reposition the DMBs for effective and efficient financial intermediation and contributions to national economic development and growth. The study applied quantitative methodology to answer the research questions. Key results include significant positive relationship between the study variables and reduction in fraud incidence in DMBs. The results has implications for existing literature on regulators knowledge capability and competence as vehicle for fraud prevention and detection. The study advocates the integration of both forensic accountants and bank examiners as permanent fixtures in fraud prevention and detection in DMBs. Further, the integration results, will aid the DMBs capacity to drastically reduce the incidence of fraud and forgeries not only in the DMBs but all other sectors of the finance industry.

1. Introduction

Globally, deposit money banks (DMBs) are considered critical to national economic growth and development. However, the DMBs cannot play this role unless they are prudently managed and properly regulated to sustain customer patronages (Ly, Citation2015; Nwoji et al., Citation2011; Okpara, Citation2009; Al Shaher et al., Citation2011). Furthermore, prior studies (Abata, Citation2015; Muoghalu et al., Citation2018; Okpara, Citation2009) have established that the ability to curtail fraud and ensure transparency in DMB transactions rests with effective banking regulation. These activities combined are presumed to guarantee sustainable development of DMBs and national economic performance. In Nigeria, the DMBs have failed to perform this crucial developmental role. This has been attributed to escalating incidence of fraud, forgeries, and weak capacity in the DMB sector. Consequently, Nigeria remains afflicted with escalating economic and financial insecurity, and its attendant effects on various sectors in the economy: power supply, communication, transport, infrastructure, education and social life (Lamorde, Citation2012; Nwankwo, Citation2013; Taiwo et al., Citation2016). This study strives to address the nexus between banking regulation and fraud in the DMBs.

Prior literature (Adeyemo, Citation2012; Akindele, Citation2011; Nwoji et al., Citation2011; Olatunji et al., Citation2014) have attributed the upsurge in fraud and forgers in Nigeria’s DMBs to problems of poor corporate governance practices, economic and political stability, policy implementation and regulatory laxity. These studies, and myriad others (Hogan et al., Citation2008; Houck et al., Citation2006; Popoola et al., Citation2015), have pointed to growing incidence of financial crimes, audit failures, and banking frauds as evidence of decline in audit standards, loss of confidence in existing regulatory capacity, and collapse in auditor’s professional ratings. These challenges have instigated the clamour for improvement in the quality of the auditor’s work to ensure proactive fraud prevention and detection as audit engagement sine qua non (Chui & Pike, Citation2013; Hogan et al., Citation2008; Nicolaisen, Citation2005; Popoola et al., Citation2015).

The drive towards proactive and ethical auditing practices through joint assurance and investigation by forensic accountants and auditors, as against the usual recourse to reactive investigations of frauds and forgeries in the DBM system, is anticipated in the literature that theorized the imminent replacement of auditors with forensic experts (Asare et al., Citation2015; Boritz et al., Citation2008, January; Chui, Citation2010; Chui & Pike, Citation2013; Hogan et al., Citation2008; Jenkins et al., Citation2018; O. Popoola et al., Citation2016).

This study therefore aligns with the findings of previous literature (Awolowo, Citation2016; Chui & Pike, Citation2013; DiGabriele, Citation2016) that argues that auditors are unable to detect fraud because they are not, by training and certification, fraud specialists. Besides, there is a difference between fraud examination and financial statement audit. Further, the study sought an integration of forensic accountants and bank examiners to ensure effective fraud risk assessment in Nigeria’s DMBs. Thus, the study proposed that bank examiners’ inability to stem escalating incidence of fraud in DMBs might be attributable to gaps in their knowledge capability (KC) and competence. In this regard, the study examined the mediating effect of fraud-related problem representation on KC (forensic accountants and bank examiners) and fraud risk assessment (task performance) in the DMBs.

The objective of the study is to establish an effective and enduring mechanism for preventing and detecting fraud within the Nigeria DMBs. The specific objectives include, to:

Examine the relationship between KC requirement (forensic accountants and bank examiners) and task performance fraud risk assessment within the Nigeria DMBs.

Examine the relationship between KC requirement (forensic accountants and bank examiners) and fraud related problem representation within the Nigeria DMBs.

Examine the relationship between fraud-related problem representation and fraud risk assessment of forensic accountants and bank examiners within the Nigeria DMBs.

Examine the mediating effect of fraud-related problem representation on KC requirement (forensic accountants and bank examiners) and fraud risk assessment within the Nigeria DMBs.

2. Contents

2.1. Banking sector review

In Nigeria, financial institutions are broadly classified into three categories, namely, DMBs, Specialised banks and Other financial institutions (CBN, Citation2016). This study is focused on DMBs based on the availability of credible information on fraud and forgeries within DMBs, its significance within the financial system value chain and tremendous impact on national economic growth and development when properly regulated and managed efficiently. In this regard, the Nigeria DMBs currently has 22 licensed banks which operate from 5,450 branch networks. Their total assets as at 31 December 2017 stood at N38.53 billion, total deposit liability, N19.38 billion, total loans and advances, N15.91 billion and total shareholders’ fund N2.66 billion (CBN, Citation2017).

In Nigeria, banking activities are regulated by both the Central Bank of Nigeria (CBN) and the Nigeria Deposit Insurance Corporation (NDIC). In this regard, regulation connotes the rules governing banking operations. Prior researches of Singh (Citation2016), Lucca et al. (Citation2014), and Liewellyn (Citation1986) established that banking regulation consist agreed behaviour based on distinct rules that are: self, government, or external agency imposed through implicit or explicit agreements of the industry, which restricts business operations within financial institutions. This study posit that the reviews and implementations of the various regulatory frameworks would appear not to have positive impact on fraud and forgeries in DMBs due to gaps in KC and competence of the bank examiners.

2.2. Fraud concept

Fraud entails deliberate concealment, misrepresentation, manipulation and exclusion of facts to the detriment of people and organisations including banks. Fraud also encompass theft, appropriation, obtaining illegally, misapplying and exposing organisational assets to harm (Adeduro, Citation1998; Bostley & Dover, Citation1972; Gilbert & Wakefield, Citation2018; Levi et al., Citation2007). Furthermore, prior studies assert that fraud prevention require the strengthening of internal controls by the management of DMBs and the regulators (Chui & Pike, Citation2013; W. D. Huber & DiGabriele, Citation2015; Pike, Citation2013). This study aligns with prior studies which affirmed that fraud erode customers’ confidence (Akinyomi, Citation2012; Alghamdi et al., Citation2015). It is therefore imminent that bank examination mechanism within the DMBs must be strengthened in order to curtail the current striking incidence of fraud and forgeries.

Furthermore, prior studies (Adetiloye et al., Citation2016; Chui & Pike, Citation2013; Adeyemo, Citation2012; Nwoji et al., Citation2011; Godwin Citation2009) on the origin of banking fraud highlighted the nature and dimensions of banking fraud as well as various means applicable towards its prevention and detection. Ultimately, their findings affirmed fraud as preventable, provided the regulators and managements constantly review and strengthens bank examination as well as internal control mechanism. In this regard, evidence from annual reports of both CBN and the NDIC confirmed escalating incidence of fraud in the Nigerian DMBs. In context, the NDIC annual report for 2017 showed a 246% increase in the incidence of Fraud and forgeries within the Nigeria DMBs between 2014 and 2017, as shown in .

Table 1 Total Number of Fraud and Forgeries in Banks (2014 to 2017)

Source: NDIC Annual Report 2017.

Concisely, this study aligns with prior literature (Agyemang, Citation2015; Baz et al., Citation2017; Cascarino, Citation2012; Daniel-Draz, Citation2011; Zaworski, Citation2005) on the origin of fraud in deposit money banks and identify ineffective examination structures, internal control weaknesses and governance ineptitude as contributing factors. This study proposed that this may be attributed to lack of KC by the forensic accountants and bank examiners. The study thus focuses on the KC and competence of the forensic accountants and bank examiners who constitute the human capital, deployed for bank examination and policy implementation towards fraud prevention and detection in DMBs. This study opined that forensic accountants and bank examiners, through the deployment of appropriate professional and technical KC complemented by effective and efficient implementation extant banking regulations, will be better equipped to prevent and detect fraud in DMBs.

2.3. Knowledge Capability Requirement

Prior studies (Popoola, Citation2014; Davis et al., 2010; Chui, Citation2010; DiGabriele, Citation2008) describe capability as competences; capacities; abilities; key, core and fundamental skills; ethics; values; and attitudes; distinguishing characteristics; pervasive qualities; and individual attributes deployed for task accomplishments. KC represents professional and technical attributes deployed by individuals for work station accomplishments. KC constitute attributes which propelled a professional with the opportunity to demonstrate competence. Thus, KC include: “professional knowledge, skills, values and ethics” exhibited to demonstrate competence (IFAC-IES 8, 2006).

Prior studies, Suleiman and Ahmi (Citation2018), Wuerges (Citation2011) and Chui (Citation2010), affirmed that the concept, fundamental forensic knowledge includes: “professional responsibilities and practice management, laws, courts and disputes resolution, planning and preparation, information gathering and preservation (documents, interviews or interrogations, electronic data), findings, reporting, experts and testimony”. According to IES No. 8, section 36–41, bank examiners knowledge being auditors comprises: historical banking information audit; banks’ financial accounting; and reporting and information technology (IFAC, Citation2006).

2.3.1. Definition of Forensic Accountant and Bank Examiner

Prior literature W. Huber and DiGabriele (Citation2014) define forensic accounting as “the application of specialised accounting knowledge, investigative and analytical skills to resolve financial matters in tandem with standards stipulated by the court of law. This study describes a forensic accountant (FA) as an accounting professional, equipped with the skills for investigative activities; criminality techniques; and ability to integrate accounting and legal procedures to detect and prevent fraud. FAs are currently engaged in DMBs when fraud occurs.

Bank Examiners (BE) are defined as professionals employed in the banking sector pursuant to section 29 of BOFIA (1991) to ensure that the banks are operating legally and safely in accordance with subsisting statutory banking regulations. BEs are currently engaged as the arrowhead of the bank’s fraud prevention and detection architecture and risk management. Bank Examiner’s knowledge consists attributes deployed in evaluating audit plans and procedures considered adequate to provide audit evidence and give reasonable assurance that the bank statements and periodic returns are error free.

2.4. Fraud Related Problem Representation (FRPR)

Problem representation is recognised by scholars (Glover et al., Citation2016; Mala & Chand, Citation2015; Bedard & Chi, Citation1993; Christ, Citation1993; Chi et al., 1981) as a structure for internal reasoning incorporating an individuals’ interpretation and understanding of problematic situations. Prior studies (Pitz & Sachs, Citation1984; O. Popoola et al., Citation2016) also establish that such individuals ultimately cultivate problem representation once there is need to make decisions. Prior literature, Larkin (2014), Nendaz and Bordage (Citation2002), Bedard and Chi (Citation1993), Christ (Citation1993) and Chi et al., (1981) define problem representation as the internal cognitive framework embodying people’s comprehension and interpretation of a problem situation.

In effect, an underlying motive of fraud-related problem representation is the encouragement of an individual’s understanding of a problem and the resolution (Ilse et al., Citation2018; Markman & Gentner, Citation2001; Reed, Citation2012; Tomasic & Akinbami, Citation2013). Fraud related problem representation thus permits individuals to establish the task significance beyond elementary specifications laid out at the commencement of the job (Mala & Chand, Citation2015; Thibodeau, Citation2003; Christ, Citation1993; Pitz & Sachs, Citation1984). For the study, fraud-related problem representation denotes the forensic accountant and bank examiner’s ability in accessing fraud risk prevalent within DMBs to define standards in order to facilitate fraud prevention and detection.

2.5. Task Performance Fraud Risk Assessment (TPFRA)

Fraud risk assessment (FRA) is a unique procedure for discerning and evaluating risk militating organisational goals’ achievements. As noted by Popoola et al. (Citation2015), Chui and Pike (Citation2013), Rezaee and Davani (Citation2013), Wuerges (Citation2011) and Chui (Citation2010), task performance fraud risk assessment facilitates the evaluation of an entity to establish its state of affairs, develop appropriate audit processes for risk identification and establish procedures for identifying the significance and possibility of fraud occurrence. Prior literature (Knapp & Knapp, Citation2001; Payments, Citation2015; Subramanian, Citation2014) affirmed and endorsed task performance fraud risk assessment as a strong tool for fraud prevention and enhancement of the auditor’s competence towards fraud prevention and detection.

This study aligns with prior literature Popoola (2015), Wuerges (Citation2011), Chui (Citation2010) which opine that task performance fraud risk assessment illuminate audit focus and aid auditors in ascertaining the organisation’s condition. TPFRA denotes stretches of audit procedures purposely required to establish the possibility and significance of fraud occurrence within the DMBs. The study presents task performance fraud risk assessment as the forensic accountant and bank examiner’s capacity to access fraud risk to a distinct standard towards fraud prevention and detection in DMBs.

2.6. Conceptual Framework and Hypotheses Development

The conceptual framework in this study examines the mediating effect of fraud-related problem representation on KC (forensic accountant and bank examiner) and competence that is, task performance fraud risk assessment and it is presented in .

Figure 1. Conceptual Framework

3. HYPOTHESIS DEVELOPMENT

3.0.1. The Influence of Knowledge Capability on Task Performance Fraud Risk Assessment in the Nigeria Deposit Money Banks

The first conceptual linkage in the study is the prediction that KC exerts direct positive influence on task perfomance fraud risk assessment. Previous literature (Popoola et al., Citation2015; Chui, Citation2010; Davis et al., 2010; DiGabriele, Citation2008; Brandstatter & Frank, Citation2002) confirmed that a modest change in KC would produce considerable changes in performance with an inclusive impact on a professional’s energy and drive to achieve set objectives. The study thus hypothesise based on the above discussion that:

H1: There is a significant positive relationship between KC (forensic accountants and bank examiners) and task performance fraud risk assessment in DMBs.

The findings indicate the significant contributions of knowledge requirement as a most important predictor of task performance fraud risk assessment by forensic accountants and bank examiners in the Nigeria DMBs.

3.0.2. Influence of Knowledge Capability on Fraud Related Problem Representation in the Nigeria Deposit Money Banks

The second conceptual linkage of the study is the relationship between knowledge and fraud-related problem representation. KC was found to have direct influence on fraud-related problem representation (Popoola, Citation2014; Davis et al., 2010; Christ, Citation1993; Chi et al., 1981). The association between KC and fraud-related problem representation is recognised by literature in accounting. Subsequently, this study asserts that a significant positive relationship exists between KC and fraud-related problem representation in Nigeria DMBs. Specifically, and for this reasoning the hypothesis is formulated thus:

H2: There is a significant positive relationship between KC and fraud related problem representation (forensic accountants and bank examiners) in DMBs.

More specifically, this study produced empirical evidence supporting the assertion that forensic accountants and bank examiners in DMBs required distinct content and technical knowledge in aid of their comprehension and interpretation of fraud-related problem representation situations.

3.0.3. Influence of Fraud Related Problem Representation on Fraud Risk Assessment in the Nigeria Deposit Money Banks

Prior studies (Denison, Citation2009; Kadous & Sedor, Citation2004; Mulia et al., Citation2015; Viscusi et al., Citation2011) have shown that fraud-related problem representation has a resultant influence on individual’s judgement and decision-making process. In addition, the study by Kadous and Sedor (Citation2004) collaborates Bierstaker et al. (Citation1999). Prior study, Popoola et al. (Citation2015b), found a significant direct relationship between fraud-related problem representation and task performance fraud risk assessment. This study aligns with findings in prior literature and formulates the hypothesis thus:

H3: There is a significant positive relationship between fraud related problem representation and task performance fraud risk assessment (forensic accountants and bank examiners) in DMBs.

The result revealed a significant direct relationship between the mediating construct of fraud-related problem representation and the endogenous construct of task performance fraud risk assessment.

3.0.4. Mediating influence of Fraud Related Problem Representation on Knowledge Capability Requirement and Task Performance Fraud Risk Assessment in the Nigeria Deposit Money Banks

Prior studies, Widhoyoko (Citation2017), Baz, Samsudin, Ayoib, and Popoola (Citation2016), affirmed a significant positive relationship between KC and fraud-related problem representation on one hand, and a positive significant relationship between fraud-related problem representation and task performance fraud risk assessment on the other. Prior literature (Baz et al., Citation2016; Popoola et al., Citation2015b) on empirical investigation of task performance fraud risk assessment and KC requirement on fraud-related problem representation affirmed a significant positive relationships between knowledge requirement and task performance fraud risk assessment, significant positive relationship between knowledge requirement and fraud-related problem representation and significant positive relationship between fraud related problem representation and task performance fraud risk assessment. Based on these studies, the hypothesis is thus formulated:

H4: Fraud- related problem representation positively mediate the relationship between KC and task performance fraud risk assessment in DMBs.

The result indicated the significance of fraud-related problem representation as mediator and assert its influence on KC and task performance fraud risk assessment within the DMBs.

3.1. Research Methods and Measurement of Variables

Cross-sectional design and survey methodology was deployed in this study (Creswell & Creswell, Citation2017). Questionnaires were administered on forensic accountants and bank examiners in CBN, NDIC and 15 randomly selected DMBs in Lagos, Nigeria which constitute the study scope. A total of 27 indicators were evaluated on a 5-point Likert scale of “Strongly Disagree to Strongly Agree”. The individual forensic accountant and bank examiner are the unit of analysis.

3.1.1. Data Collection

Prior to the administration of questionnaires, 11 experts in the field were contacted and inputs received were used to enhance the questionnaire before distribution. Subsequent to content validation, the final questionnaires were produced and administered (Sekaran & Bougie, Citation2010). In context, 350 questionnaires were distributed with 275 returned out of which 251 were found suitable and retained for analysis representing 72% useable response rate.

3.1.2. Data Analysis

IBM SPSS for windows version 26 and PLS-SEM software version 3.2.8 were used for data screening and analysis, respectively (Hair et al., Citation2017, Citation2014). Subsequently, the study deployed regression analysis technique for inferential statistics to evaluate the hypotheses whilst descriptive statistics entailed summary statistics.

4. RESULTS AND DISCUSSIONS

4.0.3. Response Rate

As shown in , 350 questionnaires were distributed out of which 275 were returned representing a return rate of 78%. A total of 24 questionnaires were removed for incomplete response and outliers (Hair et al., Citation2017). Subsequently, 251 questionnaires were found suitable for analysis, a useable rate of 72% (Tabachnick & Fidell, Citation2013). The response rate is higher than the 50% recommended for social science research in Nigeria (Linus, Citation2001) and also higher than the 30% advocated by Sekaran and Bougie (Citation2013, Citation2010).

Table 2. Response Rate

4.0.4. Descriptive Analysis of Constructs

Based on the results contained in , TPFRA construct revealed the highest mean score of 4.11 with a standard deviation of 0.718. KC construct disclosed a mean value of 4.10 and a standard deviation score of 0.605 whilst FRPR recorded a mean value of 3.79 and a standard deviation of 0.469. An indication of the symmetry in the distribution is provided by the skewness whilst the kurtosis provides information on the peakedness (Tabachnick & Fidell, Citation2013). The study applied both skewness and kurtosis to test the normality of the distribution. The criterion advocated by Tabachnick and Fidel ranged between ± 2.58 and the results shown in all fell within range, to confirm the data as normally distributed.

Table 3. Summary Statistics

4.0.5. Model Fit Assessment

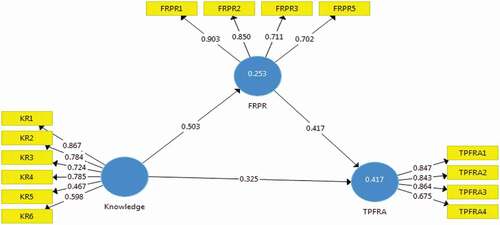

The measurement model of the study is presented in . Structural equation model was applied to ascertain the fitness of the model. According to prior literature (Hair et al., Citation2014), composite reliability should be higher than 0.7 whilst average variance extracted should be higher than 0.5. After discarding items that failed to meet the benchmark, the final measurement model is shown in .

Figure 2. Measurement Model (Algorithm)

4.0.6. Research Instrument Validity and Reliability

Prior literature, Sekaran and Bougie (Citation2013), affirmed validity as the extent to which a variable accurately and candidly represents the construct it is supposed to measure. The constructs of the study were evaluated for reliability and validity. This entails calculating composite reliability to evaluate internal consistency, individual reliability as well as average variance extracted (AVE). presents the results of the evaluation of the study constructs reliability and validity.

Table 4. Construct Reliability and Validity

Based on , the composite reliability and average variance extracted from the constructs are well above the thresholds of 0.7 and 0.5 as espoused by Hair et al. (2014). Furthermore, each factor load were retained as reported as their retention did not raise composite reliability and average variance extracted beyond the thresholds. Furthermore, the results of the assessment of the discriminant validity is presented in . The square root of AVE of each of the latent variable is presented in the bolded diagonal and each is higher than its corresponding correlation with another variable as espoused by the Fornell-Larker criterion. This is in tandem with stipulations that a construct should be unique and it should capture situations not represented by other constructs within the model .

Table 5. Discriminant Validity

Table 6. Structural Model (Direct effect)

Table 7. Mediating Effect (Indirect effect)

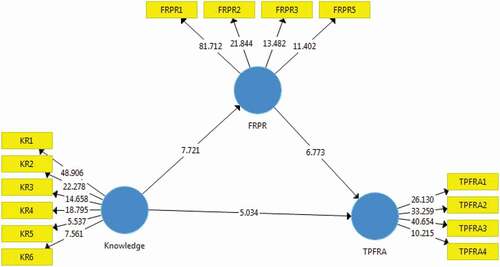

4.1. Bootstrapping Analysis

Sequel to the confirmation of the reliability and validity of the study construct measure, the assessment of the structural model’s predictive capabilities is presented in .

Figure 3. Structural Model (Bootstrapping @5000)

To determine the mediating effect of fraud-related problem representation on KC and task performance fraud risk assessment, bootstrapping analysis using 5000 samples was deployed. The results, as reflected in revealed the consistence, magnitude and significance of the structural paths (Henseler, Hubona, & Ray (2016). The result affirmed significant structural mediating effect of fraud-related problem representation on KC (forensic accountant and bank examiner) and task performance fraud risk assessment.

4.2. Test of Hypotheses

The direct effect hypotheses were evaluated and presents the results of the path coefficient indicating the beta value, standard error, t and p values and the decision on the tested hypotheses. The table showed that KC (forensic accountants and bank examiners) has positive significant effects on task performance fraud risk assessment in the Nigeria DMBs with a t-value of 5.034, beta of 0.325 and p = 0.000. The result supports hypothesis H1, that, there is a significant positive relationship between KC (forensic accountants and bank examiners) and task performance fraud risk assessment in DMBs. Furthermore, KC (forensic accountants and bank examiners) with a t-value of 7.721, beta coefficient of 0.503, and p = 0.000 has positive significant effect on fraud-related problem representation. This result supports hypothesis H2 that there is a significant positive relationship between KC and fraud-related problem representation (forensic accountants and bank examiners) in DMBs.

In addition, fraud-related problem representation with a t-value of 6.773, beta coefficient of 0.417, and p = 0.000 maintained a significant positive relationship on task performance fraud risk assessment thus confirming hypothesis H3 which states that there is a significant positive relationship between fraud-related problem representation and task performance fraud risk assessment (forensic accountants and bank examiners) in DMBs. In essence, to enhance forensic accountant and bank examiner’s competence within DMBs, a sound professional and technical KC is invaluable.

Furthermore, in relation to the mediating effect, Hypothesis H4 was developed and bootstrap method employed to evaluate fraud-related problem representation as a mediator of KC construct and the endogenous task performance fraud risk assessment. The result presented in with a t-value of 4.860**, beta of 0.210, and p = 0.000 revealed that FRPR effectively mediates the relationship between KC and TPFRA. The result thus confirmed the hypothesis that fraud-related problem representation positively mediates the relationship between KC and task performance fraud risk assessment in the discharge of their job specifications, with emphasis on prevention and detection of fraud in DMBs.

4.3. Contributions/implications of the study

Theoretically, the study enhanced the accounting literature on TPFRA within DMBs’ context in Nigeria, a developing economy. The study established a significant direct positive relationship of KC (forensic accountants and bank examiners) on TPFRA, affirmed the positive effect of FRPR on TPFRA and confirmed the positive influence of KC on FRPR in DMBs. The findings established the mediating influence of FRPR on the relationship between KC (forensic accountants and bank examiners) and TPFRA in DMBs.

Managerial and practical: the results provide justification for the proactive integration of forensic accountants and bank examiners to ensure effective fraud risk assessment in Nigeria’s DMBs. Fraud risk assessment prior to this intervention is a generally accepted principle in the auditing field, yet it is skewed in favour of bank examiners rather than forensic accountants, who under Nigerian practices, are generally invited to intervene after the act. Thus, required, as the results of the study show, is an integrative approach in which both forensic accountants and bank examiners are involved as permanent actors in the prevention and detection of fraud and forgeries in DMBs.

The study espoused the significance of KC to forensic accountants and bank examiners in organisations including DMBs. The study makes potential contributions to existing regulatory, legal and institutional frameworks in banking. The study affirmed FRPR as an effective and significant mediating construct and espoused TPFRA as a basic competence requirement for fraud prevention and detection.

4.4. Limitations and future research

Based on the recommendation for the integration of forensic accountants and bank examiners for bank examination engagements, harmony is fundamental to success in the union in view of the established differences between the two professionals (Davis et al., 2010; Durkin & Ueltzen, 2009). Future research could examine organisational climate and ethical values as mediator on the constructs examined in the study.

5. Conclusion

The study applied the developed conceptual framework, evaluated four hypotheses formulated and the results established significant positive relationships among the three constructs of the study. The results affirmed the clamour for the integration of the forensic accountants and bank examiners to create standing forensic audit teams in the CBN, NDIC and DMBs towards fraud prevention and detection in DMBs. The results ultimately would significantly enhance regulators’ efforts toward fraud prevention and detection in aid of the DMBs capacity to contribute to national economic growth and development.

This study contributes to the accounting literature on bank examination, KC, fraud-related problem representation and fraud risk assessment in the quest for prevention and detection of fraud in DMBs. The study thus develops a conceptual framework that can be deployed by forensic accountants and bank examiners working within DMBs to prevent and detect fraud.

Additional information

Funding

Notes on contributors

Olusoji Olumide Odukoya

Odukoya Olusoji Olumide the corresponding author is a PhD Accounting student of the Universiti Utara Malaysia (UUM). He also holds a Masters and Bachelor's degree in Accounting. A Chartered Accountant/Stockbroker/Tax Practitioner with over 35 years of varied professional practice experience. The PhD thesis of Mr Odukoya is supervised by Associate Professor (Dr) Rose Shamsiah Samsudin ORCID ID – 0000-0002-2149-1799), the current Dean of the Department of Accounting (TISSA) at the Universiti Utara Malaysia. The current research effort is further undertaken as part requirement for Viva that is, a Scopus journal publication is a major requirement for the consideration of PhD students for Viva in UUM. The paper is an integral part of the post data analysis results from my thesis and represents an effort in giving scholarly publicity to my research findings and obtaining feedbacks for further improvements of the thesis and also broaden my horizon.

References

- Abata, M. A. (2015). Impact of Asset Management Corporation of Nigeria (AMCON) on the securitization in the Nigerian banking sector. Global Journal of Contemporary Research in Accounting, Auditing and Business Ethics, 1(2), 282–15.

- Adeduro, A., . A. (1998). “An investigation into frauds in banks”. An unpublished thesis of University of Lagos. Administrative Sciences (UMAS) (), Vol 2, 01–05. University of Lagos, Research Unit/UniLag Press.

- Adetiloye, K. A., Olokoyo, F. O., & Taiwo, J. N. (2016). Fraud prevention and internal control in the Nigerian banking system. International Journal of Economics and Financial Issues, 6(3), 1172–1179.

- Adeyemo, K. A. (2012). “Fraud in Nigerian banks: Deep-seated causes. Alternative and probable remedies”. An unpublished thesis of Covenant University, Ogun state, Nigeria.

- Agyemang, J. (2015). Internal control and fraud prevention. International Journal of Management and Scientific Research, 1(1), 230–257.

- Akindele, R. I. (2011). Fraud as a negative catalyst in the Nigerian banking industry. Journal of Emerging Trends in Economics and Management Sciences (JETEMS), 2(5), 357–363.

- Akinyomi, O. J. (2012). Examination of fraud in the Nigerian banking sector and its prevention. Asian Journal of Management Research, 3(1), 182–194.

- Al Shaher, T., Kasawneh, O., & Salem, R. (2011). The major factors that affect banks’ performance in Middle Eastern countries. Journal of Money, Investment and Banking, 1(3), 27–41.

- Alghamdi, A., Flechais, I., & Jirotka, M., (2015), Security practices for households bank customers in the kingdom of Saudi Arabia. USENIX Association. https://www.usenix.org/

- Asare, S. K., Wright, A., & Zimbelman, M. F. (2015). Challenges facing auditors in detecting financial statement fraud: Insights from fraud investigations. Journal of Forensic & Investigative Accounting, 7(2), 63–112.

- Awolowo, I. F. (2016). Financial statement fraud: The need for a paradigm shift to Forensic accounting. International Journal of Economics and Management Engineering, 10(3), 987–991.

- Baz, R., Samsudin, R. S., & Che-Ahmad, A. (2017). The role of internal control and information sharing in preventing fraud in the Saudi banks. Journal of Accounting and Financial Management, 3(1), 7–13.

- Baz, R., Samsudin, R. S., Che-Ahmad, A., & Popoola, O. (2016). Capability component of fraud and fraud prevention in the Saudi Arabian banking sector. International Journal of Economics and Financial Issues, 6(S4), 68–71.

- Bedard, J., & Chi, M. T. H. (1993). Expertise in Auditing. Auditing: A Journal of Practice and Theory, 12(Supplement), 21–45.

- Bierstaker, J. L., Bedard, J. C., & Biggs, S. F. (1999). ‘The role of problem representation shifts in auditor decision processes in analytical procedures”. Auditing: A Journal of Practice and Theory, 18(1), 18–36. https://doi.org/https://doi.org/10.2308/aud.1999.18.1.18

- Boritz, J. E., Kotchetova, N., & Robinson, L. A. (2008, January). Planning fraud detection procedures: Forensic accountants vs auditors. In IFA conference, accessed July (Vol. 22, p. 2009). University of waterloo.

- Bostley, R. W. B., & Dover, C. B. (1972). Sheldon’s practice and the law of banking. In English language book society, Macdonald, and Evans (10th ed.). London.

- Brandstatter, V., & Frank, E. (2002). Effects of deliberative and implemental mindsets on persistence in goal-directed behaviour. Personality & Social Psychology Bulletin, 28(10), 1366–1378. https://doi.org/https://doi.org/10.1177/014616702236868

- Cascarino, R. E. (2012). Corporate fraud and internal control: A framework for prevention. John Wiley & Sons.

- CBN. (2016). Banking system regulation and supervision in Nigeria (1976-2016). Central Bank of Nigeria Bullion, 40(1), 27–36.

- CBN, (2017). Central Bank of Nigeria annual report and accounts, 2017. CBN Press Limited.

- Christ, M. Y. (1993). Evidence on the nature of audit planning problem representations: an examination of audit free recalls: the accounting review. European Journal of Applied Physiology and Occupational Physiology, 66(2), 304–322. https://doi.org/https://doi.org/10.1007/BF00237773

- Chui, L., (2010), An experimental examination of the effects of fraud specialist and audit mindsets on fraud risk assessment and on the development of fraud related problem representation, ProQuest LLC UMI 3456520, 789 East Eisenhower Parkway, USA.

- Chui, L., & Pike, B. (2013). Auditors’ responsibility for fraud detection: New wine in old bottles? Journal of Forensic and Investigative Accounting, 5(1).

- Creswell, J. W., & Creswell, J. D. (2017). Research design: Qualitative, quantitative and mixed methods approaches. Sage publications.

- Daniel-Draz, M. S., (2011), Fraud Prevention: Improving internal controls. June 7, 2015, at http://www.csoonline.com/article/2127917/fraud-prevention/fraud-prevention–improvinginternal-controls.html.

- Denison, C. A. (2009). Real options and escalation of commitment: A behavioural analysis of capital investment decisions. The Accounting Review, 84(1), 133–155. https://doi.org/https://doi.org/10.2308/accr.2009.84.1.133

- DiGabriele, J. A. (2008). An empirical investigation of the relevant skill of forensic accountants. Journal of Education for Business, 83(6), 331–338. https://doi.org/https://doi.org/10.3200/JOEB.83.6.331-338

- DiGabriele, J. A. (2016). The expectation differences among stakeholders in the financial valuation fitness of auditors. Journal of Applied Accounting Research, 17(1), 43–60. https://doi.org/https://doi.org/10.1108/JAAR-06-2013-0043

- Gilbert, M., & Wakefield, A. (2018). Tackling fraud effectively in central government departments: A review of the legal powers, skills and regulatory environment of UK central government counter fraud teams. Journal of Financial Crime, 25(2), 384–399. https://doi.org/https://doi.org/10.1108/JFC-01-2017-0006

- Glover, S. M., Taylor, M. H., & Wu, Y. J. (2016). Current practices and challenges in auditing fair value measurements and complex estimates: Implications for auditing standards and the academy. Auditing: A Journal of Practice & Theory, 36(1), 63–84. https://doi.org/https://doi.org/10.2308/ajpt-51514

- Godwin, O., (2009). A synthesis of the critical factors affecting performance of the Nigerian banking system. European Journal of Economics Finance & Admin Sciences. 171, 34–44.

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A primer on partial least squares structural equation modelling (PLSSEM). Sage.

- Hair, J. F., Hult, T. M., Ringle, C. M., & Sarstedt, M. (2017). A primer on partial least squares structural equation modelling (PLSSEM). Sage, Publications.

- Hogan, C., Rezaee, Z., Riley, R., & Velury, U. (2008). Financial statement fraud: Insights from the academic literature. Auditing: A Journal of Practice & Theory, 27(2), 2. https://doi.org/https://doi.org/10.2308/aud.2008.27.2.231

- Houck, M. M., Kranacher, M., Morris, B., Robertson, J., & Wells, J. T. (2006). Forensic accounting as an investigative tool. The CPA Journal, August 1.

- Huber, W., & DiGabriele, J. A. (2014). Research in forensic accounting-what matters? Journal of Theoretical Accounting Research, 10(1), 40–70.

- Huber, W. D., & DiGabriele, J. A. (2015). Topics and methods in forensic accounting research. Accounting Research Journal.

- IFAC. (2006). International education standard no. In Competence requirements for audit professionals (pp. 8). International Federation of Accountants.

- Ilse, M., Tomczak, J. M., & Welling, M. (2018). Attention-based deep multiple instance learning. In International conference on machine learning (pp. 2127-2136). PMLR.

- Jenkins, J. G., Negangard, E. M., & Oler, M. J. (2018). Getting comfortable on audits: Understanding firms’ usage of forensic specialists.. Contemporary Accounting Research, 35(4), 1766–1797. https://doi.org/https://doi.org/10.1111/1911-3846.12359

- Kadous, K., & Sedor, L. (2004). The efficacy of third-party consultation in preventing managerial escalation of commitment: the role of mental representations. Contemporary Accounting Research, 21(1), 55–82. https://doi.org/https://doi.org/10.1506/R0MH-W9H9-CQJD-1356

- Knapp, C. A., & Knapp, M. C. (2001). The effect of experience and explicit fraud risk assessment in detecting fraud with analytical procedures. Accounting Organisation and Society.

- Lamorde, I. (2012). Nigeria: More boost for corruption. A paper presentation on the EFCC Budget Defence at the Senate Chamber, Federal Republic of Nigeria. Vanguard Newspaper, November 27.

- Levi, M., Burrows, J., Fleming, M., Hopkins, M., & Matthews, K. G. P. (2007). The nature, extent and economic impact of fraud in the UK. Economic Crime Portfolio Group.

- Liewellyn, D. (1986). The regulation and supervision of financial institutions. Institute of bankers.

- Linus, O. (2001). Marketing strategy effectiveness in Nigerian banks. Academy of Marketing Studies Journal, 5(1), 23–30.

- Lucca, D., Seru, A., & Trebbi, F. (2014). The revolving door and worker flow in banking regulation. Journal of Monetary Economics, 65, 17–32. https://doi.org/https://doi.org/10.1016/j.jmoneco.2014.05.005

- Ly, K. C. (2015). Liquidity risk, regulation and bank performance: Evidence from European banks. Global Economy and Finance Journal, 8(1), 11–33. https://doi.org/https://doi.org/10.21102/gefj.2015.03.81.02

- Mala, R., & Chand, P. (2015). Judgment and decision‐making research in auditing and accounting: future research implications of person, task, and environment perspective. Accounting Perspectives, 14(1), 1–50. https://doi.org/https://doi.org/10.1111/1911-3838.12040

- Markman, A. B., & Gentner, D. (2001). Thinking. Annual Review of Psychology, 52(1), 223–247. https://doi.org/https://doi.org/10.1146/annurev.psych.52.1.223

- Mulia, T. W., Lasdi, L., & Widjanarko, T. A. (2015). Pengaruh hurdle rates dan framing terhadap eskalasi komitmen dalam penganggaran modal. Simposium Nasional Akuntansi, 18.

- Muoghalu, A. I., Okonkwo, J. J., & Ananwude, A. (2018). Effect of electronic banking related fraud on deposit money banks financial performance in Nigeria. Discovery, 54(276), 496–503.

- Nendaz, M. R., & Bordage, G. (2002). Promoting diagnostic problem representation. Medical Education, 36(8), 760–766. https://doi.org/https://doi.org/10.1046/j.1365-2923.2002.01279.x

- Nicolaisen, D. T. (2005). In the public interest. Journal of Accountancy, 199(1), 63–70.

- Nwankwo, O. (2013). Implications of fraud on commercial banks performance in Nigeria. International Journal of Business and Management, 8(15), 144. https://doi.org/https://doi.org/10.5539/ijbm.v8n15p144

- Nwoji, D. L., Adebayo, O., & David, A. O. (2011). Corporate governance and bank failure in Nigeria: Issues, challenges and opportunities. Research Journal of Finance and Accounting, 2(2), 2.

- Okpara, G. C. (2009). A synthesis of the critical factors affecting performance of the Nigerian banking system. European Journal of Economics, Finance and Administrative Sciences, 17(17), 34–44.

- Olatunji, O. C., Adekola, D. R., & Isaac, A. A. (2014). Analysis of frauds in banks: Nigeria’s experience. European Journal of Business Management, 6(31), 90–99.

- Payments, U. U. (2015). Preventing money laundering and bank fraud in the banking industry.

- Pike, B. (2013). Auditors’ responsibility for fraud detection: new wine in old bottles? Lawrence chui. Journal of Forensic & Investigative Accounting, 5, 1.

- Pitz, G. P., & Sachs, N. J. (1984). Judgement and decision: theory and application. Annual Review of Psychology, 35(1), 139–163. https://doi.org/https://doi.org/10.1146/annurev.ps.35.020184.001035

- Popoola, O., Che-Ahmad, A., Samsudin, R. S., Salleh, K., & Babatunde, A. (2016). Accountants’ capability requirements for fraud prevention and detection in Nigeria. International Journal of Economics and Financial Issues, 6, S4, 1–10.

- Popoola, O. M. J., (2014), Forensic accountants, auditors, and fraud: Capability and competence requirements in the Nigerian public sector. A thesis submitted to Othman Yeop Abdullah Graduate School of Business, Universiti Utara Malaysia, in fulfilment of the requirement for the Doctor of Philosophy. Universiti Utara Malaysia.

- Popoola, O. M. J., Che-Ahmad, A., & Samsudin, R. (2015). Forensic accounting and fraud: Capability and competence requirements in Malaysia. Journal of Modern Accounting and Auditing, 10(2), 825–834.

- Popoola, O. M. J., Che-Ahmad, A., & Samsudin, R. (2015b). An empirical investigation of fraud risk assessment and knowledge requirement on fraud related problem representation in Nigeria. Accounting Research Journal.

- Reed, S. K. (2012). Cognition: Theories and applications. Cengage learning.

- Rezaee, Z., & Davani, H. (2013). Does financial reporting fraud recognize borders? Evidence from bank fraud in Iran. Journal of Forensic & Investigative Accounting, 5, 2.

- Sekaran, U., & Bougie, R. (2010). Research methods for business: A skill building approach. John Willey & Sons.

- Sekaran, U., & Bougie, R. (2013). Research methods for business: A skill building approach (6th ed.). John Wiley & Sons.

- Singh, D. (2016). Banking regulation of UK and US financial markets. Routledge.

- Subramanian, R., (2014), Bank Fraud. Wiley. ttps://www.sas.com/

- Suleiman, N., & Ahmi, A. (2018). Mitigating corruption using forensic accounting investigation techniques. Indian-Pacific Journal of Accounting and Finance, 2(1), 4–25.

- Tabachnick, B. G., & Fidell, L. S. (2013). Using multivariate statistics: International edition. Pearson2012.

- Taiwo, J. N., Agwu, P. E., Babajide, A., & Isibor, A. A. (2016). Growth of bank frauds and the impact on the Nigerian banking industry. Journal of Business Management and Economics, 14(12), 01–10. https://doi.org/http://dx.doi.org/10.15520/jbme.2016.vol4.iss12.232.pp01-10

- Thibodeau, J. C. (2003). The development and transferability of task knowledge. Auditing: A Journal of Practice & Theory, 22(1), 47–67. https://doi.org/https://doi.org/10.2308/aud.2003.22.1.47

- Tomasic, R., & Akinbami, F. (2013). Shareholder activism and litigation against uk banks-the limits of company law and the desperate resort to human rights claims. In Directors’ duties and shareholder litigation in the wake of the financial crisis, joan loughrey (ed) (pp. 143–172). Edward Elgar.

- Viscusi, W. K., Phillips, O. R., & Kroll, S. (2011). Risky investment decisions: How are individuals influenced by their groups? Journal of Risk and Uncertainty, 43(2), 81. https://doi.org/https://doi.org/10.1007/s11166-011-9123-3

- Widhoyoko, S. A. (2017). Fraud in rights and contracts: a review of bankruptcy case of livent inc. based on governance, risk, and compliance (GRC) framework. Binus Business Review, 8(1), 31–39. https://doi.org/https://doi.org/10.21512/bbr.v8i1.1827

- Wuerges, A. (2011). Auditors’ responsibilities for fraud detection: New wine in old bottles? , University of St. Thomas, Minnesota: .Accounting Faculty Publications. Retrievedfromhttp://www.scrid.com/doc/63671899/Auditor-Responsibility-for-fraud-Detection.

- Zaworski, M. J., (2005), Assessing an automated, information sharing technology in the post “9-11” era -do local law enforcement officers think it meets their needs? A dissertation submitted in partial fulfilment of the requirements for the degree of Doctor of Philosophy in Public Administration. Florida International University Miami.