Abstract

The objective of this study is to investigate the influence of workplace learning, organisational culture, personal characteristics, such as motivation to learn and self-efficacy on the information technology (IT) competency of external auditors. This study also examines the role of organisational culture as a moderating variable between workplace learning and IT competency. Using a simple random sampling technique, a self-administered questionnaire was completed by 220 external auditors in Yemen. Partial least squares structural equation modelling (PLS-SEM) was applied to analyse the hypothesised relationships. The results show that workplace learning, motivation to learn, self-efficacy, and organisational culture are significant and positively influence the IT competency of the external auditors. Organisational culture also significantly moderates the relationship between workplace learning and IT competency. The study’s findings contribute greater insight into the importance of organisational culture, motivation to learn, self-efficacy of external auditors, and how learning in the workplace influence their IT competency.

PUBLIC INTEREST STATEMENT

Nowadays, most companies employ information technology in their daily business activities. This application has led to the creation of digital accounting records, which need to be inspected by the auditors. Despite the increase in business information technology incorporation, there is a low level of usage of IT auditing among external auditors. Digital records have placed pressure on audit firms to expand and improve their technical level as well as the IT knowledge and skills of their auditors to serve their clients. Information technology competency for auditors is required in regard to the set of IT skills, non-IT skills, and experiences that external auditors must have in order to use IT effectively in their duties. Therefore, this paper investigates the factors that influence IT competency among external auditors and the role of organisational culture in moderating the relationships between workplace learning activities and IT competency.

1. Introduction

The audit profession is one of the industries that should be more efficient and effective as a result of the digitisation process (Han et al., Citation2016). At present, the business environment is still being transformed into a digitalised area with more advanced technology to support business operations; this also applies to audit firms that need to adapt to the new environment (Tarek et al., Citation2017). The integration of IT into business processes has led to the creation of digital accounting records to be reviewed by auditors. Digital records put pressure on audit firms to develop and improve their level of technology and increase IT knowledge among auditors to serve their clients (Flowerday et al., Citation2006). The role of the auditor is to express the opinion that their clients’ accounting data as reported in the financial statements are presented with reasonable assurance and are free from material misstatement (Fakhfakh, Citation2016). Therefore, auditors need to use relevant IT tools to manage electronic and paperless accounting data (Ahmi & Kent, Citation2013).

Several professional bodies, such as the American Institute of Certified Public Accountants (AICPA) in 2001 and the Information Systems Audit and Control Associations in 2014, have issued IT auditing standards, they encourage auditors and audit firms to change their audit strategies to align with changes in the way their clients conduct their business using accounting information systems. However, auditors still prefer to apply traditional audit procedures when forming an audit opinion (Ahmi & Kent, Citation2013; Bierstaker et al., Citation2014; Siew et al., Citation2020). Previous studies reported a low level of IT competency among auditors (Al-Duwaila & Abdullah, Citation2017; Greenstein & McKee, Citation2004; Strong & Portz, Citation2015). Particularly in Yemen, external auditors face the deficiency of knowledge and skills related to IT audit processes, contributing to their inefficiency in using technology effectively (Al-Ansi, Citation2015; Al-Sorihi, Citation2014). IT-based auditing practices among audit firms in Yemen are currently relatively low or at a basic level (Al-Ansi et al., Citation2017; Yemeni Association of Certified Public Accountants [YACPA], Citation2017). The value, importance and reputation of the auditing and accounting profession depend on the ability of members to provide suitable services to meet the needs of the specific operating environment and to meet the needs of stakeholders continuously (Wessels, Citation2005).

Information technology competency refers to IT knowledge, IT skills and attitudes or personal traits towards IT that determine the level of performance in a particular work context (Alkhaffaf et al., Citation2017; Ni & Chen, Citation2016). From the accounting profession viewpoint, IT competency defines as a set of IT skills, non-IT skills, and experiences that an accounting practitioner must possess to use IT effectively in his or her duties (Bahador et al., Citation2012). Auditors need to equip themselves with skills and knowledge on digital elements, data analytics, hardware, software and information system operations and other IT elements (Suhardianto & Leung, Citation2020). This principle was demonstrated by the International Accounting Education Standards Board (IAESB, Citation2018), which claimed that they must achieve a high level of competency in IT to perform their tasks effectively. It reflects the competency theory that individuals would be more effective if their competency for each task is enhanced, rather than merely relying on their skills and abilities (Taylor, Citation2016). Moreover, this theory further elaborates on the fact that individuals who lack IT skills, especially in high level skills, their level of competency is readily apparent and appears not to overvalue their capabilities (Gross, Citation2005). Therefore, it concludes that competence is gained by the development of skills and knowledge in a specific area (Kruger & Dunning, Citation1999).

Acknowledging the importance of IT competency among accounting practitioners, numbers of international accounting organisations have issued several competency frameworks to guide the development of skills and competencies in the accounting profession. For example, in 1995, the International Federation of Accountants (IFAC) published the International Education Guideline No. 11 (IEG11) “Information Technology for Professional Accountants” aimed at preparing accountants for work in the IT environment (IFAC, Citation2003). Similarly, in 1999, the AICPA issued a framework for core competencies for entry into the profession. This framework identifies the capacity and core competencies that accountants need to demonstrate at the entrance level, such as (personal, functional and broad business perspective). The AICPA framework focuses on the competencies and skills required of all accounting practitioners. It provides the basis for lifelong learning as accounting practitioners develop their skills at work (AICPA, Citation2017). Likewise, the Institute Management Accountants (IMA) has established a management accounting competence framework (IMA, Citation2020). This framework outlines six core areas of abilities, skills and knowledge that accounting, and finance professionals need to remain relevant in the digital age and to perform their current and future roles effectively, such as (technology & analysis, reporting & control, strategy, planning & performance, leadership and professional ethics & values and business acumen & operations) (IMA, Citation2020). In addition, Chartered Global Management Accountants (CGMA, Citation2020) designed the CGMA competency framework to help finance professionals, accountants and their employers recognise knowledge requirements and assess the skills needed for both existing and desired roles. The competence framework was first published in April 2014 and covered five knowledge areas: digital skills, people skills, business skills, technical skills and leadership skills.

Previous IT competency studies on accounting practitioners have focused on issues related to their level of IT knowledge, the importance of IT skills, the identification of IT skills requirements, the alignment of IT knowledge and IT importance, and the integration of IT competency into accounting curricula (Al-Duwaila & Abdullah, Citation2017; Bahador & Haider, Citation2017; Greenstein & McKee, Citation2004; Spraakman et al., Citation2015). However, only a few studies have examined the factors that impact the IT competency of accountants (Alkhaffaf et al., Citation2017, Citation2018; Bahador & Haider, Citation2020). For example, Bahador and Haider (Citation2020) discussed approaches to developing skills that enhance the competency of information technology among accounting practitioners, particularly those operating in Malaysian accounting firms. In their empirical qualitative study, they concluded that learning activities in the workplace impact their IT competency. To the best of the researcher’s knowledge, there is no empirical research investigating the impact of workplace learning activities on IT competency.

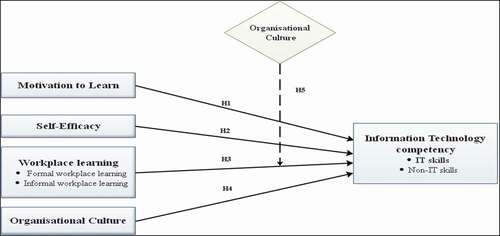

Alainati et al. (Citation2010) proposed that personal characteristics influence employee competency and should be considered when studying the factors that influence employees’ competency. Competency theory explains that personal characteristics (i.e. motivation to learn and self-efficacy) might affect external auditors’ competency. In line with Alkhaffaf et al. (Citation2017, Citation2018) studied some of the personal characteristics influencing accountants’ IT competency in Iraq, such as motivation and goal setting. They suggest that further work is required to identify different factors that might influence IT competency from different backgrounds and perspectives. To the best of the researcher’s knowledge, there is a scarcity of empirical studies examining the relationship between personal characteristics such as motivation to learn, self-efficacy and external auditors’ IT competency. Therefore, the present study seeks to resolve the theoretical gap in the relationship between workplace learning activities, personal characteristics such as motivation to learn, self-efficacy and external auditors’ IT competency in developing countries, such as Yemen. The aim of this study is to examine the influence of motivation to learn, self-efficacy, organisational culture and workplace learning on IT competency. Organisational culture is used as a moderating variable between workplace learning and IT competency. shows the theoretical framework of the present study.

Figure 1. Theoretical framework

The findings of this study suggest that IT competency is essential for external auditors to protect investors and create an attractive investment environment that will boost the overall growth of the economy, therefore, allow researchers to make new contributions to the existing literature. First, this study provides evidence for the first time on the connection between workplace learning, motivation to learn and self-efficacy and IT competency of external auditors, contributing to a better understanding of IT competency. Second, workplace learning is considered the best skill development factor for external auditors to enhance IT competency. Thus, audit firms in Yemen must create a workplace learning environment, whether formal or informal. Finally, the organisational culture mechanism as a moderator can strengthen the relationship between workplace learning activities and IT competency.

The current study consists of seven sections as follows: introduction, background, theoretical literature review, empirical literature review and hypotheses development, research design, empirical results and discussion as well as summary and conclusion.

2. Background

The lack of IT skills among auditors in Yemen has contributed to the inaccuracies in audit reports issued for companies (Al-Ansi, Citation2015). Many companies have gone bankrupt, such as Marib Poultry, National Bank for Trade and Investment, Paint Production Company, Alberh Cement Factory and the spinning and weaving factory (Al-Ansi, Citation2015; Central Organisation for Control and Auditing [COCA], Citation2007). These companies were mainly audited by external auditors, who follow conventional working practices where technology was not used efficiently (Al-Ansi, Citation2015; Al-Dois, Citation2010). For example, the collapse of the National Bank for Trade and Investment, one of the major banks in Yemen, was triggered by fraud committed by the bank’s board of directors. External auditors were faced with difficulties and challenges in accessing, interpreting, and analysing the bank clients’ data systems because of their lack of skills and knowledge in IT (Al-Ansi, Citation2015). Despite this, the auditors still issued a clean report (COCA, Citation2007). In this context, researchers such as Awolowo and Garrow (Citation2020), and Gibran (Citation2010) argued that external auditors should be responsible for corporate fraud and companies’ loss.

In seeking IT competency of external auditors, the Yemeni context was chosen for a number of reasons. First, there is a competition between companies in the private sector to use an information system in its daily operating. Additionally, 85% of Yemen’s public sector organisations use the electronic Accounting and Financial Management Information System (AFMIS) (World Bank, Citation2015). AFMIS is a financial management information system that integrates all financial management functions in one system. The using IT by companies requires the external auditors in Yemen to learn new IT audit skills to continue strengthening their procedures and conducting audits in a complex and rapidly evolving IT environment (World Bank, Citation2010). Second, empirical studies in IT auditing, especially on the IT competency of the external auditors in developing countries, especially in Yemen, have not received sufficient attention (Al-Ansi et al., Citation2017; Al-Hattami et al., Citation2021; Al-Sorihi, Citation2014). It is therefore important to recognise the factors that influence the IT competence of external auditors.

External auditors were chosen because the requirements of IT competency for external auditors are higher than the other accounting practitioners because they typically serve a wide variety of clients with diverse information systems (Greenstein-Prosch et al., Citation2008). An external auditor in Yemen is a person who has the permission of the public accountant from YACPA and in accordance with the provisions of the law in Yemen.

3. Theoretical literature review

3.1. Competency theory

The concept of competency is defined as a group of knowledge, attitudes and skills that affect a large part of a person’s activity and is correlated with performance, allowing an individual to excel in a particular field or task (Le Deist & Winterton, Citation2005). The concept has been used in many different areas of research, including education, psychology, management, information systems and human resources (Mulder et al., Citation2009). The theory of competency has shown that individuals who lack competency tend to overestimate what they can achieve and are unaware of their inability to do so (Kruger & Dunning, Citation1999). However, in the context of IT skills, particularly the high level of skills required by their environment, their level of competency is easily apparent and they tend not to overvalue their capabilities (Gross, Citation2005).

There are four stages of competency or learning new skills: conscious incompetency, unconscious incompetency, unconscious competency, and conscious competency (Robinson, Citation1974). In conscious incompetency, an individual does not know the right way to do or understand something. At this stage, an individual cannot identify this deficit and denies the importance of the skill and its usefulness (Flower, Citation1999; Robinson, Citation1974).

For unconscious incompetency, however, the individual understands and identifies the deficit along with the new skills needed to overcome this deficit (Robinson, Citation1974). This stage depends on learning from making mistakes, solving simple problems, and observing or discussing the topic with other employees in the workplace. Moreover, at this stage, an individual begins to judge whether he should continue or give up, and therefore the self-efficacy of the individual is essential in moving from this stage to the next. Furthermore, the length of time an individual spends at each stage depends on their motivation to learn (Cole et al., Citation2004).

In the third stage, unconscious competency, the individual understands the task that needs to be done and how to do it. Therefore, individuals should be given multiple opportunities to practise skills and internalise knowledge to enable them to develop these skills (Robinson, Citation1974). For conscious competency, the final stage, an individual can demonstrate skill while performing a task. The individual at this stage can also teach specific skills to others (Robinson, Citation1974). All of this can be done in the context of workplace learning activities.

There are also four stages in the skills development model developed by Schoonenboom et al. (Citation2007). The first stage is the orientation process in which employees determine what skills they want to develop. Second, moving towards skills development activities in the workplace or gathering evidence to indicate their current skills level through education or professional development. Third, this assessment is carried out by others and, finally, they move back to the development of skills in order to achieve a higher level of competency if the level at stage three is not sufficient; the development of skills in the workplace is iterative.

4. Empirical literature review and hypotheses development

4.1. Information technology competency

Information technology is a general concept that essentially refers to computers, programmes, and telecommunications, while the concept of IT competency is broader and representative of the use of these technologies to meet the organisation’s needs (Mithas et al., Citation2011).

Following Bahador and Haider (Citation2013), this research defines IT competency as a group of IT and non-IT skills that accounting practitioners must possess in order to use IT efficiently in their job. This research distinguishes between two dimensions of the concept: IT and non-IT skills. IT skills refer to an individual’s capability to utilise technology such as software applications, databases, computers and other technologies to achieve personal goals and accomplish a wide diversity of work-related tasks (Bahador & Haider, Citation2013).

Non-IT skills are defined as “the non-technical skills and knowledge necessary for effective participation in the workforce” (Department of Education Employment and Workplace Relations, Citation2012, p. 4). In the accounting field, IAESB (Citation2019) defines non-IT skills as the organisational, personal, intellectual, interpersonal and communication skills that the accountant combines with IT skills, professional attitudes, values, and ethics to demonstrate professional competency.

4.2. Motivation to learn and information technology competency

Motivation to learn can be described as an individual’s internal drive to acquire skills for their individual and professional benefit (Machin & Treloar, Citation2004; Noe, Citation2017). The motivation for learning can be assessed by learners’ ability to absorb content during the learning process (Maass, Citation2017). Motivation has thus been described as “the direction, intensity and persistence of learning-directed behaviour in training contexts” (Colquitt et al., Citation2000, p. 678).

From the point of view of competency theory, the length of time spent at each stage depends on the motivation to learn (Cole et al., Citation2004). Many researchers have recognised the critical need for motivation to improve the effectiveness of training and development activities. For example, Kontoghiorghes (Citation2001) argued that highly organised training could not achieve its objectives in the absence of motivation to learn. This means that if the motivation is lacking, the training will fail. On the other hand, Major et al. (Citation2006) and Tharenou (Citation2001) have indicated that the degree to which individuals engage in learning and training programmes depends on their motivation to learn. It has also been shown that the motivation to learn is related to the acquisition of skills, knowledge or training transfer behaviour (Lingappa et al., Citation2020; Noe, Citation2017). This is consistent with Sambrook’s (Citation2005) suggestion that employee motivation is a primary factor that makes an individual more decisive and knowledgeable at any place or time, particularly at work. The level of motivation for learning can be increased if the design of workplace learning programmes to improve job skills is appropriate (Baldwin & Magjuka, Citation1991).

Empirical studies have found a significant and positive relationship between motivation to learn and learning outcomes, such as skills acquisition and declarative knowledge (Colquitt et al., Citation2000; Klein et al., Citation2006; Liao & Tai, Citation2006). Another study found that learning motivation indicated transferable skills and provided the greatest amount of overall variance in transferable skills (Lau & McLean, Citation2013). From a performance perspective, highly motivated employees can produce better outputs than those with a low level of motivation (Noe, Citation2017). This was demonstrated in a study by Barba et al. (Citation2016), that motivation was the strongest predictor of performance.

Although earlier studies show a link between motivation to learn and employee competency, there is still a lack of studies to investigate the relationship between this motivation and IT competency. Accordingly, this study aims to investigate this relationship for auditors in Yemen. On this basis, the following hypothesis is formulated:

H1: There is a positive relationship between motivation to learn and IT competency.

4.3. Self-efficacy and information technology competency

Self-efficacy is defined as the assessment of an individual regarding his or her capabilities and effectiveness for better performing certain tasks and showing successful behaviour (Bandura, Citation2012). On the other hand, self-efficacy does not depend upon an individual’s skills but is related to one’s judgement of performing certain tasks regardless of their skills (Bandura, Citation1997, Citation2012).

Theoretically, according to the learning skills model in the competency theory, the second stage (unconscious incompetency) is where the employee makes their self-judgement about their deficit and inability to perform the new skills, due to the lack of self-efficacy; they withdraw themselves from the learning process. Consequently, at this stage, self-efficacy plays a key role in helping individuals to continue to learn, which eventually increases their competency.

In skill development activities, self-efficacy is linked positively to participation and intention (Kurbanoglu, Citation2010). The explanation is that individuals with a low perception of self-efficacy frequently underestimate their ability to deal with challenging circumstances and are less likely to acquire competencies, whereas individuals with a high perception of self-efficacy would make more effort to overcome challenges and improve those competencies (Artino, Citation2012; Kurbanoglu, Citation2010). Trainees with a higher level of self-efficiency are secure in their ability to acquire newly taught knowledge, skills, abilities and make extra efforts to achieve challenging objectives. In contrast, if the trainees have low self-efficacy, they tend to avoid attempting to transfer training to work (Nikandrou et al., Citation2009).

Complex IT poses cognitive burdens that challenge users (Gattiker & Goodhue, Citation2005), and several studies have revealed that self-efficacy can play an important role in understanding individual responses to IT (Chau & Lai, Citation2003; He et al., Citation2018). For example, Burton-Jones and Hubona (Citation2005), and Klopping and McKinney (Citation2004) studied the self-efficacy of computer usage and found that it had a significant impact on actual use.

While studies have recognised self-efficacy, research has not yet clearly examined the immediate effect of self-efficacy on IT competency. Therefore, the current study investigates the influence of self-efficacy on the IT competency of auditors in Yemen. Based on the stated arguments, the following hypothesis is put forth:

H2: There is a positive relationship between self-efficacy and IT competency.

4.4. Workplace learning and information technology competency

The importance of workplace learning is to contribute to the development of employees’ knowledge, skills and abilities (Doornbos et al., Citation2008). The workplace is considered as the best environment for individual learning, where people tend to work and learn via knowledge sharing between peers or the organisation; on-the-job training is also less costly to the organisation (Hamid et al., Citation2014).

Based on competency theory, in-house development programmes (workplace learning activities) are one of the steps in the competency development model to build up and improve employee skills (Schoonenboom et al., Citation2007). In order to develop skills in the workplace, simple problems, complex issues, and discussions with peers are addressed several times before the employees can gain and control specific skills (Azemikhah, Citation2006).

Empirically, Moon and Na (Citation2009) examined the interactions between learning in the workplace and psychological variables, such as learning competency. They found that the level of learning in the workplace in medium-sized and manufacturing companies was higher than the expected average and had a positive relationship with the competency of employees. Brandão et al. (Citation2012) found that workplace learning showed significant positive results with employees’ competency. Further, Kunjiapu and Yasin (Citation2015) examined the relationships between workplace learning and skill development in small and medium-sized tourism businesses in Malaysia. Their findings indicate that the correlation between workplace learning and skill development is moderate and positive. Daryoush et al. (Citation2016) investigated the power level of the relationship between types of workplace learning and task performance. The results of this study showed that two-way interactions were significant, and workplace learning was positively related to the performance of the task.

Organisations from various business sectors proclaim IT as the key reason for facilitating job change (Jacobs & Osman-Gani, Citation2005). The utilisation of IT, whether applied to enhance management or production capabilities, ultimately resulted in significant shifts in work arrangements and execution. As a result, many organisations are experiencing rapid change which, due to the importance of IT, requires them to promote continuous learning in the workplace (Cseh & Manikoth, Citation2011).

Previous studies have categorised workplace learning in several ways: unplanned versus planned learning, formal versus informal, incidental versus informal, and on-the-job versus off-the-job learning (Jacobs & Park, Citation2009; Malcolm et al., Citation2003). Formal and informal learning is generally seen as a major component of workplace learning, which can be achieved concurrently (Doyle & Young, Citation2004; Woodall & Winstanley, Citation1998). Thus, it may be difficult to observe the learning activity as either fully formal or entirely informal. Equally important, Choi and Jacobs (Citation2011) found evidence from the literature of learning at work that confirms the integrated nature of formal and informal learning in the improvement of individual knowledge and skills.

From the above discussion, workplace learning is an element that influences IT competency; it can assist in preparing accountants to face challenges in the workplace and therefore, is integrated into this theoretical study framework. The following hypothesis is formulated:

H3: There is a positive relationship between workplace learning and IT competency.

4.5. Organisational culture and information technology competency

Culture reflects common ways of thinking and behaving among individual. Organisational culture is a philosophy created by human beings themselves to enhance the harmony between individuals, which motivates them to enhance their efficiency and productivity by increasing their commitment to their work (Deal, Citation1985).

The literature has shown that organisational culture has a significant influence on various individual behaviours within an organisation such as job satisfaction, individual’s sense-making, collective efficacy, self-efficacy and organisational commitment (Lund, Citation2003; Walumbwa et al., Citation2005).

Organisational culture serves as the organisation’s genetic code in developing competencies. It is backstage for the organisation’s dynamics, which controls what it means to be competent in a specific organisation (McAuley, Citation1994; Prahalad & Hamel, Citation2006). Therefore, organisational culture influences the development of competencies (Fleury, Citation2009). It is found that organisational culture has a significant and positive effect on employee competency and employee job performance (Basmawi & Usop, Citation2016).

The literature of workplace learning studies reported a positive and significant influence in terms of employee competency and skills growth (Cacciattolo, Citation2015; Kunjiapu & Yasin, Citation2015; Plant et al., Citation2017). Despite this, learning at work and employee competency are marred with inconstant relationships. Brandão et al. (Citation2012) investigated the relationship of different workplace learning strategies with employee competency, and they found that learning through written material showed a weak relationship with employee competency.

The findings of workplace learning and IT competency are inconclusive and another variable is required to moderates the relationship between the variables. Daryoush et al. (Citation2013) argue that organisations’ culture activates workplace learning and focuses it more on high task and contextual performance. Therefore, the organisational culture effect may encourage or impede a firm’s knowledge activities and organisational learning (Lee et al., Citation2017). Organisational culture has been studied quite extensively as the moderator in various contexts, such as personality and managerial competency; workplace learning and performance; leadership competencies and job role performance (Chuttipattana & Shamsudin, Citation2011; Daryoush et al., Citation2013; Hamzah et al., Citation2013) and organisational culture has been approved to moderate the manager competency and workplace learning.

However, no study showed that the organisational culture is a moderating variable in the relationship between workplace learning activities and IT competency. The gap is still there and requires further investigation regarding the moderating effect of organisational culture on the relationship between workplace learning and IT competency, which can enhance the understanding of the role of organisational culture in the context of IT.

Therefore, the present study believes that organisational culture influences the learning process within a workplace and consequently, would increase IT competency among auditors. Based on the previous arguments, the following hypothesis is put forth:

H4: There is a positive relationship between organisational culture and IT competency.

H5: Organisational culture moderates the relationship between workplace learning and IT competency.

5. Research design

The current study uses a quantitative approach based on a cross-sectional survey to collect data from respondents using a questionnaire technique.

5.1. Data collection procedure

Data were collected using the questionnaire technique and the measurement of variables was adapted from previous studies. Questionnaires were distributed to the external auditors in public and private sectors in Yemen. External auditors were chosen because they audited many clients who use different information systems, so the external auditors’ IT competency standards are higher than those of other accountants (Greenstein-Prosch et al., Citation2008). To ensure elevated data quality and response rate, self-administered questionnaire was used.

5.2. Population, sampling, and sample size

The population of this study consists of 592 external auditors who meet the requirements of YACPA (Citation2018). Based on the table of Krejcie and Morgan (Citation1970), the sample size was 234 respondents. To minimise the error in sample size and to overcome the problem of non-response rate, this study followed the recommendations of Baruch and Holtom (Citation2008) by increasing sample size by 40%. Therefore, the sample size included 328 respondents. This study uses a simple random sampling technique to distribute questionnaires to respondents since this technique is the most appropriate sampling technique in the known population. Of the 233 questionnaires collected during the three months of January to March 2019, eight were excluded from the analysis due to incomplete (Keyton, Citation2015). Five questionnaires were also omitted from the analysis, following Tabachnick and Fidell (Citation2014) standards to eliminate outliers. The remaining 220 questionnaires were used for analysis, representing a 67% valid response rate.

5.3. Survey instrument and validation

This study adapts the measurements of variables from previous studies with validated survey instruments. Information technology competency was measured using 35items adapted from (Bahador, Citation2014; Greenstein & McKee, Citation2004). The scale reflects two dimensions, namely IT skills measured using 23 and non-IT skills measured using 12 items. The item taken as a sample for IT skills is “Generalised audit software—A computer program that helps the auditor access client computer data files, extract relevant data and perform some audit function such as addition or comparison”. Although the item of non-IT skills taken as a sample is “I have the ability to demonstrate cooperation (teamwork) while working towards organisational goals”. Workplace learning is assessed using a 20-items scale derived from Choi (Citation2009). The scale represents two dimensions, namely formal workplace learning measured using eight-items, “I received formal coaching from a peer or supervisors to help me improve on some aspect of my job” and informal workplace learning measured using 12-items, “I exchange ideas on how to solve a problem with peers during a break or after work”. Motivation to learn is measured using seven-items adapted from Tharenou (Citation2001). Sample items include “I would like to improve my IT skills through T&D programmes”. Self-efficacy was measured using six-items adapted from Chen et al. (Citation2001). Sample items include “I will be able to use IT successfully to overcome many challenges”. Organisational culture was measured using 16-items taken from Al-Swidi and Mahmood (Citation2012). These items were taken as a sample for organisational culture “In our organisation, the capabilities of people are viewed as an important source of competitive advantage”. A five-point Likert scale rated from 1 (Very poor) to 5 (Excellent) was used to assess the IT competency (dependent variable) and 1 (strongly disagree) to 5 (strongly agree) was used to measure all independent variables. Since the respondents are Arabic speakers, this study used a back-translation technique to translate survey forms from English into Arabic (Brislin, Citation1970). After translating the instruments, a pre-test and analysis of pilot study were carried out, and the results confirmed the reliability and validity of the measurements.

5.4. Respondents profile

Demographically, shows that 71.8% of the external auditors have a bachelor’s degree. The majority of external auditors do not have professional qualifications representing 76.8% of the total auditors. 47.7% of auditors have between 11 and 19 years of experience. Despite experience in the audit, 54.5% of external auditors have not experience in IT auditing. Regarding the category of firms where external auditors work, 40.9% of auditors work in public audit firms (Governmental organisations).

Table 1. Demographical profile

6. Empirical results

6.1. Descriptive statistics

Descriptive statistics of the variables are presented in . The information technology competency has a mean score of 3.786 with an associated standard deviation score of 0.640. This exhibit that the external auditors have knowledge and skills in the field of IT. The mean scores for workplace learning, motivation to learn, self-efficacy and organisational culture were 3.879, 4.176, 4.212, 3.806, respectively. This reflects that most external auditors agree that workplace learning, motivation to learn, self-efficacy and organisational culture are important to their IT competency.

Table 2. Results of the descriptive statistics of all the latent constructs (n = 220)

6.2. The empirical results

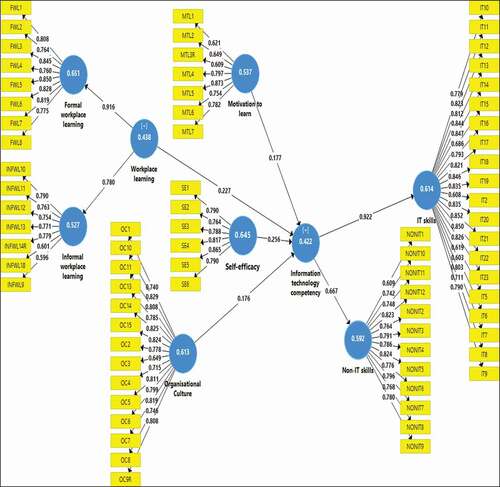

Cain et al. (Citation2017) suggested to use the web software to test multivariate normality when the data was obtained from the survey. Mardia’s multivariate skewness coefficient was 6.527 (t = 239.326, p < 0.00) and the kurtosis was 42.634 (t = 6.767, p < 1.31) indicating that the data were not normally multivariate. Therefore, the study uses Partial Least Square Equation Modelling (PLS-SEM). Moreover, this study applied a two-stage analytical approach through the SmartPLS 3.3.3 because the workplace learning and IT competency multidimensional and the items of each dimension are not equal (Ringle et al., Citation2012); this means that the model needs to use latent variable scores to evaluate the structural model (Cepeda-Carrion et al., Citation2019). There are two components of the PLS-SEM. The first is the measurement model, which measures each indicator’s contribution to the representation of each construct and assesses how well the combined indicators represent the construct (Hair, Black et al., Citation2019); see . The second component of SEM is the structural model, which assesses the constructs’ relationships (Henseler et al., Citation2009). More detailed information on the two components of the PLS-SEM in next sub-sections.

Figure 2. Measurement model

6.2.1. Measurement model

In order to establish the validity and reliability of the data, the measurement model is fundamental. The assessment involves determining discriminant validity, convergent validity, internal consistency reliability and indicators reliability (Hair, Black et al., Citation2019; Henseler et al., Citation2009).

Outer loadings are considered as criteria for assessing the reliability of the indicator. According to Hair et al. (Citation2017), loadings between 0.40 and 0.70 should be carefully inspected and should only be removed if their deletion improves the values of average variance extracted (AVE) and composite reliability (CR). Based on these criteria, eight-items out of the total of 68, (IT1, IT3, IT4, INFWL15, INFWL16, INFWL17, INFWL19, INFWL20), were removed as they have a loading of less than 0.50; by deleting them, the values of CR and AVE increase (see ).

Table 3. Construct reliability and validity

The internal consistency reliability is assessed using CR, which requires coefficient values of at least 0.70 (Hair, Risher et al., Citation2019). The CR for all constructs in the present study ranged from 0.796 to.0969, and therefore represented adequate internal consistency reliability (see Table ). The values of AVE were calculated to determine convergent validity and all were found to be more than 0.50, as indicated in , indicating satisfactory convergent validity (Hair et al., Citation2017).

Discriminant validity was then assessed; it shows the uniqueness of the constructs by measuring them in such a way that they cannot be captured by other constructs (Hair, Risher et al., Citation2019). Several researchers have criticised the approach of Fornell and Larker and cross-loading to assess discriminant validity, as these methods are insufficiently sensitive (Franke & Sarstedt, Citation2019; Henseler et al., Citation2015). Accordingly, this study used the criteria of HTMT for the evaluation of discriminant validity: values should be less than 0.85 (strict criteria), or less than 0.90 (lenient criteria) (Henseler et al., Citation2015). shows that all the values of HTMT are less than 0.85, indicating strict criteria distinguishing among the four constructs.

Table 4. Discriminant validity by HTMT

6.2.2. Structural model assessment

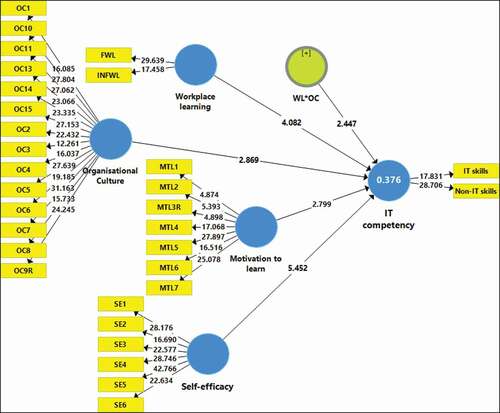

After establishing the reliability and validity of constructs through the measurement model, five steps are taken to assess the structural model. Since the data collected came from a single source, the common method bias problem was checked by the full collinearity inflation factor variance test (VIF) as suggested by Kock (Citation2015). All VIF values (motivation to learn1.275, self-efficacy 1.415, organisational culture 1.414, workplace learning 1.611) and IT competency 1.567) were less than 3.3, which means that there was no issue of a single source bias.

According to Hahn and Ang (Citation2017), to test the hypotheses, p-values alone are not sufficient as criteria, but a combination of effect sizes, confidence intervals and t-values should be used. A summary of the criteria used to test the hypotheses is presented in . The results revealed that motivation to learn (β = 0.118, t = 2.172, p < 0.015), self-efficacy (β = 0.340, t = 7.063, p < 0.000), workplace learning (β = 0.299, t = 5.949, p < 0.000), organisational culture (β = 0.170, t = 2.869, p < 0.002) and the moderating of organisational culture between workplace learning (β = 0.117, t = 2.447, p < 0.007) were positively and significantly related with IT competency (see ); hence, H1, H2,H3, H4 and H5 were supported.

Table 5. Hypothesis testing direct effects

Figure 3. Structural model

The value of the coefficient of determination (R2) was 0.376. This indicated that the independent variables, namely motivation to learn, self-efficacy workplace learning and organisational culture explain 37.6% of the IT competency. Further, the effect size (f2) was calculated for cross-checking the importance of every path. Each of the independent variables (motivation to learn, f 2 = 0.027, self-efficacy, f 2 = 0.101; workplace learning, f 2 = 0.055 and organisational culture, f2 = 0.034) had a small effect on IT competency (Cohen, Citation1988).

To assess the predictive relevance (Q2) of the study model, Shmueli et al. (Citation2019) proposed PLS-Predict as a new assessment criterion specifically designed for PLS-SEM’s predictive nature. PLS-Predict is “a holdout sample-based procedure that generates case-level predictions on an item or a construct level using the PLS-Predict with a 10-fold procedure to check for predictive relevance” (Shmueli et al., Citation2019, p. 2324). First, it was proposed to check the Q2 latent variable and only test items if Q2 was above zero. If all item differences (PLS-LM) are lower, then there is strong predictive power; if most are lower there is moderate predictive power and if the minority is lower than there is low predictive power (Shmueli et al., Citation2019). The Q2 for the latent variable IT competency was 0.207, that is above zero. This value shows the predictive relevance to be good at the construct level. As listed in , all values of Q2 are above zero, and the level error of all items of the PLS model is less than the LM model. Therefore, it is concluded that the model shows strong predictive power. In addition, model fit was also assessed using standardised root mean square residual (SRMR) criteria. The SRMR value should be below 0.10 (Hu & Bentler, Citation1998). As a result, the current study model is appropriate as the SRMR value is 0.083.

Table 6. PLS-Predict

6.3. Discussion

The findings indicate that workplace learning had a positive and significant influence on external auditors’ IT competency, supporting H1. This implies that workplace learning offers an ideal atmosphere for external auditors to learn and enhance their skills and competency. This is possible because the nature work of auditors encourages them to collaborate and learn through information exchange with colleagues in their workplace.

The relationship between learning in the workplace and IT competency is consistent with the theory of competency. The theory suggests that the process for competency development in the workplace is repeated many times using basic and simple problems, learning from making mistakes and discussion with peers (Azemikhah, Citation2006).

These findings are consistent with previous workplace learning studies that report positive and significant effects in terms of employee competency and skills growth (Brandão et al., Citation2012; Cacciattolo, Citation2015; Kunjiapu & Yasin, Citation2015). The inference that can be drawn from the result is, therefore, that learning in the workplace plays an important role in improving the level of IT competency of external auditors.

Motivation to learn had a positive and significant effect on external auditors’ IT competency, thereby supporting H2. The results indicate that, given the rapid change in IT environments, especially in accounting and auditing, external auditors are themselves attempting to learn as much as they can from training and development programmes. They are willing to exert effort in these programmes to enhance their skill. In fact, external auditors in Yemen have taken the initiative to engage in training and development programmes, although they may not be considered a top priority. They are motivated by the fact that training programmes will provide knowledge and skills that enable them to improve their competency level in line with evolving IT requirements.

The present finding is aligned with the theory of competency, which suggests that the degree to which external auditors participate in training and development and the length of time they spend on learning skills depend on the motivation to learn (Cole et al., Citation2004; Plant et al., Citation2017). Therefore, motivation to learn plays a key role in encouraging external auditors to participate in training and development to enhance their competency.

These findings are consistent with previous studies (Lau & McLean, Citation2013; Liao & Tai, Citation2006), which recorded a positive relationship between motivation and competency (i.e. skill acquisition and cumulative knowledge). Therefore, the motivation to learn is one of the essential variables that should be considered in order to increase the level of IT competency of external auditors.

The analysis shows that self-efficacy has a positive and significant influence on external auditors’ IT competency, supporting H3. This outcome means that if external auditors achieve the objectives set by themselves, they will fulfil the objectives of any challenging tasks they face in the future. They will also feel confident that they have acquired the required IT knowledge and skills that could help them to perform a variety of different tasks effectively.

According to competency theory, external auditors with a low level of self-efficacy frequently underestimate their ability to cope with difficult situations; thus, they are less likely to learn new skills. On the other hand, those with a strong sense of self-efficacy make greater efforts to resolve obstacles and develop competency (Robinson, Citation1974). Self-efficacy, therefore, plays a crucial role in encouraging external auditors to continue learning in order to improve quality, especially in the audit-related process.

The current results are aligned with most previous studies, which found a significant and positive relationship between self-efficacy and competency (Sanusi et al., Citation2018; Talsma et al., Citation2018; Velada et al., Citation2007). It can be said that self-efficacy is a key factor in assessing the intention to succeed in developmental activities.

In terms of organisational culture, it shows that organisational culture has a positive and significant influence on the external auditors’ IT competency, supporting H4. This means that organisational culture provides solutions to problems faced by the audit firm, external auditors and enhances harmony between them. These findings are consistent with previous studies (Basmawi & Usop, Citation2016; Shahzad, Citation2014), which found that organisational culture had a significant and positive effect on job performance and employee competency.

The result shows that organisational culture moderates the relationship between workplace learning and IT competency, supporting H5. This indicates that the organisational culture in audit firms in Yemen considers an individual’s skills and abilities as an essential source of competitive advantage and view failure as an opportunity to learn and improve.

The analysis of these findings suggests that the interaction between workplace learning activities and IT competency is higher among external auditors working in an audit firm enriched with a supportive culture. The findings of this study are consistent with previous studies (Freiling & Fichtner, Citation2010; McAuley, Citation1994), which found that organisational culture acts as an organisational genetic code for the create competencies and also a backstage for organisational dynamics, which determines what this means competent in a specific organisation.

7. Summary and conclusion

The results achieved the study’s objectives by demonstrating a positive and significant influence on IT competency of workplace learning, motivation to learn, self-efficacy and organisational culture. Moreover, it shows the moderating effect of organisational culture between workplace learning and IT competency. The analysis also shows that the study model has a good degree of precision and that it is important in resolving IT competency because the ability of auditors to do their job will protect investors and create an attractive investment climate that will boost the overall growth of the economy.

The current research made some theoretical contributions by examining workplace learning activities, motivation to learn, self-efficacy and organisational culture on external auditors’ IT competency. Most of the previous studies that have attempted to classify IT competency are descriptive and focus from an organisational perspective and use resource-based view theory to explain it. This study provides empirical evidence supporting competency theory, which assigns a specific function to workplace learning, motivation to learn, and self-efficacy as determinants of external auditors’ IT competency. As a result, this study’s findings contribute to broadening and complementing the knowledge body literature by unravelling and examining the variables that influence Yemen’s auditor’s IT competency. Moreover, the current study also expands the boundaries of established knowledge and information in literature by examining the moderating effect of organisational culture as a mechanism that can better explain the relationship between workplace learning activities and IT competency that enable external auditors to optimise technology utilisation to avoid being eliminated from their accounting and auditing profession. Therefore, the incorporation of organisational culture as a moderator was one of the key contributions of this study.

As a managerial contribution, this study’s findings will enable audit firms to improve their auditors’ competency to survive in a highly competitive environment; external auditors can have a high level of IT competency if they are motivated to learn IT and non-IT skills. Accordingly, the audit firms’ managers promote and stimulate their employees through policies, programmes and initiatives that boost their motivation. A further managerial implication of the current study relates to the fact that learning in the workplace is the best means of developing the required skills. Consequently, audit firms must build a workplace learning atmosphere, whether formal or informal, such as on-the-job training, coaching, mentoring, vendor training, in-house training, peer-to-peer learning self-experiment, which will lead to enhanced IT and non-IT skills and technical auditing skills. Furthermore, audit firms should be involved in cultivating an organisational culture between auditors, as organisational culture will strengthen the harmony of relationships and cooperation between auditors and will help auditors deal with numerous external and internal issues and enable them to understand the functioning of the organisation and encourage them to improve their productivity.

7.1. Limitations and suggestions

The current study is limited to a sample of external auditors who meet the YACPA membership requirements in 2018. Future studies might be expanded and generalised to include all external and internal auditors. Moreover, the study setting was cross-sectional and hence it is recommended for future researchers to incorporate longitudinal data collection. Information technology competency of auditors was assessed using self-reporting measures, which associated with standard method variance. Future researchers may use multiple sources to assess the IT competency of external auditors. Workplace learning can be studied as mediation to understand the individual’s IT competency. Future studies might also use leadership style as a moderator to enhance the relationships between variables. It is also suggested that future studies need to expand model with different variables, not only in Yemen but also in other countries.

Additional information

Funding

Notes on contributors

Mokhtar Abdulhakim Alsabahi

Mokhtar Abdulhakim Alsabahi received his PhD from Universiti Utara Malaysia and a Master’s degree from the University of Mysore - India. He is currently a lecturer in accounting department at the University of Ibb -Yemen. His research interests include accounting information system, information technology auditing, Blockchain, taxation and sustainability.

Ku Maisurah Ku Bahador

Ku Maisurah Ku Bahador received her PhD in Accounting Information Systems from the University of South Australia. She is currently the Academic Quality Assurance Coordinator at Universiti Utara Malaysia. Her research priorities include IT competency, information system auditing, and digital business. She has published in variety journals, including Scopus/WoS indexed journals.

Rafeah Mat Saat

Rafeah Mat Saat received her PhD from Universiti Utara Malaysia and her Master’s degree from the University of Alabama at Birmingham. Currently, she is the Head of Accounting Information System Unit. Her main research focuses are on corporate social responsibility, accounting information system, online business and social media.

References

- Ahmi, A., & Kent, S. (2013). The utilisation of generalized audit software (GAS) by external auditors. Managerial Auditing Journal, 28(2), 88–25. https://doi.org/https://doi.org/10.1108/02686901311284522

- Alainati, S., AlShawi, S., & Al-Karaghouli, W. (2010). The effect of education and training on competency. Paper presented at the European and mediterranean conference on information systems, UAE.

- Al-Ansi, A. A., Ismail, N. A., Senan, N. A. M., Al-Swidi, A. K., Al-Dhaafri, H. S., Faaeq, M. K., & Homaid, A. A. (2017). The effect of IT knowledge and IT training on IT utilization among Yemeni external auditors: The mediating role of IT importance. International Journal of Economic Research, 14(16), 413–432. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85045782585&partnerID=40&md5=2f6200a4c99a7fd2f84a1a0d174f6653

- Al-Ansi, A. A. M. (2015). IT fit on auditors’ performance in Yemen. (Doctoral dissertation, Universiti Utara Malaysia). Available from Universiti Utara Malaysian Electronic Theses and Dissertation

- Al-Dois, M. (2010). The extent of using information technology in the auditing process and its impact on external auditors’ efficiency and effectiveness in the Republic of Yemen. (Unpublished doctoral dissertation), Arab Academy for Banking and Financial Sciences, Amman, Jordan.

- Al-Duwaila, N., & Abdullah, A.-M. (2017). The opinion of auditors towards the importance and knowledge of information technology in Kuwait. International Journal of Business and Management, 12(3), 170–179. https://doi.org/https://doi.org/10.5539/ijbm.v12n3p170

- Al-Hattami, H. M., Hashed, A. A., Alnuzaili, K. M. E., Alsoufi, M. A. Z., Alnakeeb, A. A., & Rageh, H. (2021). Effect of risk of using computerized AIS on external auditor’s work quality in Yemen. International Journal of Advanced and Applied Sciences, 8(1), 75–81. https://doi.org/https://doi.org/10.21833/ijaas.2021.01.010

- Alkhaffaf, H. H. K., Idris, K. M., Abdullah, A., & Al-Aidaros, A.-H. (2017). The influence of cognitive factors on information technology competencies among accountants in civil conflict environment: The Iraqi perspective. Journal of Information System and Technology Management, 2(6), 13–30. http://www.jistm.com/archived.asm?dataid=41&iDisplayStart=0&aaSorting=&isSearchDetail=1&dataidExtend=217&iDisplayStartExtend=0&aaSortingExtend=&isSearchDetailExtend=1

- Alkhaffaf, H. H. K., Idris, K. M., Abdullah, A., & Al-Aidaros, A.-H. (2018). The influence of technology readiness on information technology competencies and civil conflict environment. Indian-Pacific Journal of Accounting and Finance, 2(2), 51–64. http://ipjaf.omjpalpha.com/index.php/ipjaf/article/view/48

- Al-Sorihi, S. A. A. F. (2014). The association of external auditor’s attributes with management fraud risk assessment in financial reporting: Empirical evidence from Yemen. (Doctoral dissertation, Universiti Utara Malaysia). Available from Universiti Utara Malaysian Electronic Theses and Dissertation

- Al-Swidi, A. K., & Mahmood, R. (2012). Total quality management, entrepreneurial orientation and organizational performance: The role of organizational culture. African Journal of Business Management, 6(13), 4717–4727. https://academicjournals.org/journal/AJBM/article-abstract/4D7F0B020506

- American Institute of Certified Public Accountants. (2017). AICPA Pre-certification core competency framework. https://www.aicpa.org/interestareas/accountingeducation/resources/corecompetency.html

- Artino, J., . A. R. (2012). Academic self-efficacy: From educational theory to instructional practice. Perspectives on Medical Education, 1(2), 76–85. https://doi.org/https://doi.org/10.1007/s40037-012-0012-5

- Awolowo, I. F., & Garrow, N. (2020). Audit keeps failing – Here’s why a fundamental change is needed. The ConversationAcademic rigour, journalistic flair. https://theconversation.com/audit-keeps-failing-heres-why-a-fundamental-change-is-needed-142598?

- Azemikhah, H. (2006). The 21st century, the competency era and competency theory. Paper presented at the global VET: challenges at the global, National and local levels, AVETRA 9th annual conference, Australia, 19-21. Wollongong.

- Bahador, K. (2014). Information technology competencies for accountants. (Unpublished doctoral dissertation), University of South Australia.

- Bahador, K., Haider, A., & Saman, W. (2012). Information technology and accountants-what skills and competencies are required? Paper presented at the European, mediterranean & middle eastern conference on information systems, Germany, 770–781.

- Bahador, K. M., & Haider, A. (2020). Enhancing information technology-related skills among accounting practitioners. International Journal of Business Information Systems, 35(1), 88–109. https://doi.org/https://doi.org/10.1504/IJBIS.2020.109554

- Bahador, K. M. K., & Haider, A. (2013). The maturity of information technology competencies: A professional accountants’ perspective. Paper presented at the proceedings of PICMET ‘13: Technology management in the IT-driven services (PICMET), San Jose, 2488–2497.

- Bahador, K. M. K., & Haider, A. (2017). Incorporating information technology competencies in accounting curriculum: A case study in Malaysian higher education institutions. Journal of Engineering and Applied Sciences, 12(21), 5508–5513. https://medwelljournals.com/abstract/?doi=jeasci.2017.5508.5513

- Baldwin, T. T., & Magjuka, R. J. (1991). Organizational training and signals of importance: Linking pretraining perceptions to intentions to transfer. Human Resource Development Quarterly, 2(1), 25–36. https://doi.org/https://doi.org/10.1002/hrdq.3920020106

- Bandura, A. (1997). Self-efficacy: The exercise of control. W. H. Freeman and Company.

- Bandura, A. (2012). Social cognitive theory. In P. A. VanLange, A. W. Kruglanski, & E. T. Higgins (Eds.), Handbook of social psychological theories (Vol. 1, pp. 349–374). SAGE Publications Ltd.

- Barba, P. D., Kennedy, G. E., & Ainley, M. (2016). The role of students’ motivation and participation in predicting performance in a MOOC. Journal of Computer Assisted Learning, 32(3), 218–231. https://doi.org/https://doi.org/10.1111/jcal.12130

- Baruch, Y., & Holtom, B. C. (2008). Survey response rate levels and trends in organizational research. Human Relations, 61(8), 1139–1160. https://doi.org/https://doi.org/10.1177/0018726708094863

- Basmawi, N. A. H., & Usop, H. (2016). Technological change as a mediator of employee competency profiling in selected industries in Kuching, Sarawak: A structural equation modeling approach. Journal of Cognitive Sciences and Human Development, 1(2), 56–70. https://doi.org/https://doi.org/10.33736/jcshd.198.2016

- Bierstaker, J., Janvrin, D., & Lowe, D. J. (2014). What factors influence auditors’ use of computer-assisted audit techniques? Advances in Accounting, 30(1), 67–74. https://doi.org/https://doi.org/10.1016/j.adiac.2013.12.005

- Brandão, H. P., Borges-Andrade, J. E., Puente-Palacios, K., & Laros, J. A. (2012). Relationships between learning, context and competency: A multilevel study. BAR-Brazilian Administration Review, 9(1), 1–22. https://doi.org/https://doi.org/10.1590/S1807-76922012000100002

- Brislin, R. W. (1970). Back-translation for cross-cultural research. Journal of Cross-Cultural Psychology, 1(3), 185–216. https://doi.org/https://doi.org/10.1177/135910457000100301

- Burton-Jones, A., & Hubona, G. S. (2005). Individual differences and usage behavior: Revisiting a technology acceptance model assumption. Special Interest Group on Management Information Systems, 36(2), 58–77. https://doi.org/https://doi.org/10.1145/1066149.1066155

- Cacciattolo, K. (2015). An analysis of how people learn at the place of work. European Scientific Journal, 11(22), 151–164. https://eujournal.org/index.php/esj/article/view/6051

- Cain, M. K., Zhang, Z., & Yuan, K.-H. (2017). Univariate and multivariate skewness and kurtosis for measuring nonnormality: Prevalence, influence and estimation. Behavior Research Methods, 49(5), 1716–1735. https://doi.org/https://doi.org/10.3758/s13428-016-0814-1

- Central Organization for Controlling and Accounting. (2007). Report of government for the first quarter. COCA. Retrieved from Yemen

- Cepeda-Carrion, G., Cegarra-Navarro, J.-G., & Cillo, V. (2019). Tips to use partial least squares structural equation modelling (PLS-SEM) in knowledge management. Journal of Knowledge Management, 23(1), 67–89. https://doi.org/https://doi.org/10.1108/JKM-05-2018-0322

- Chartered Global Management Accountant. (2020). CGMA competency framework 2019 edition. Chartered Global Management Accountant. https://www.cgma.org/resources/tools/cgma-competency-framework.html

- Chau, P. Y., & Lai, V. S. (2003). An empirical investigation of the determinants of user acceptance of internet banking. Journal of Organizational Computing and Electronic Commerce, 13(2), 123–145. https://doi.org/https://doi.org/10.1207/S15327744JOCE1302_3

- Chen, G., Gully, S. M., & Eden, D. (2001). Validation of a new general self-efficacy scale. Organizational Research Methods, 4(1), 62–83. https://doi.org/https://doi.org/10.1177/109442810141004

- Choi, W. (2009). Influences of formal learning, personal characteristics, and work environment characteristics on informal learning among middle managers in the Korean banking sector. (Doctoral dissertation, The Ohio State University). Available from ProQuest Dissertations & Theses Global

- Choi, W., & Jacobs, R. L. (2011). Influences of formal learning, personal learning orientation, and supportive learning environment on informal learning. Human Resource Development Quarterly, 22(3), 239–257. https://doi.org/https://doi.org/10.1002/hrdq.20078

- Chuttipattana, N., & Shamsudin, F. M. (2011). Organizational culture as a moderator of the personality-managerial competency relationship: A study of primary care managers in Southern Thailand. Leadership in Health Services, 24(2), 118–134. https://doi.org/https://doi.org/10.1108/17511871111125693

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Lawrence Erlbaum Associates.

- Cole, M. S., Harris, S. G., & Feild, H. S. (2004). Stages of learning motivation: Development and validation of a measure. Journal of Applied Social Psychology, 34(7), 1421–1456. https://doi.org/https://doi.org/10.1111/j.1559-1816.2004.tb02013.x

- Colquitt, J. A., LePine, J. A., & Noe, R. A. (2000). Toward an integrative theory of training motivation: Ameta-analytic path analysis of 20 years of research. Journal of Applied Psychology, 85(5), 678–707. https://doi.org/https://doi.org/10.1037/0021-9010.85.5.678

- Cseh, M., & Manikoth, N. N. (2011). Invited reaction: Influences of formal learning, personal learning orientation, and supportive learning environment on informal learning. Human Resource Development Quarterly, 22(3), 259–263. https://doi.org/https://doi.org/10.1002/hrdq.20084

- Daryoush, Y., Hassanzadeh, M., Silong, A. D., & Omar, Z. (2016). Workplace learning and task performance: The moderating role of innovation and communication oriented culture. International Journal of Current Research, 8(2), 26294–26302. http://www.journalcra.com/article/workplace-learning-and-task-performance-moderating-role-innovation-and-communication

- Daryoush, Y., Silong, A. D., Omar, Z., & Othman, J. (2013). Successful workplace learning: Moderating effect of organizational culture. International Journal of Human Resource Studies, 3(4), 1–19. https://doi.org/https://doi.org/10.5296/ijhrs.v3i4.4180

- Deal, T. E. (1985). Cultural change: Opportunity, silent killer, or metamorphosis. In R. H. Kilmann, M. J. Saxton, & R. Serpa (Eds.), Gaining control of the corporate culture (pp. 292–331). Business & Management, Wiley.

- Department of Education Employment and Workplace Relations. (2012). Employability skills framework stage 1-final report. National Centre for Vocational Education Research (NCVER). http://hdl.voced.edu.au/10707/219478.

- Doornbos, A. J., Simons, R. J., & Denessen, E. (2008). Relations between characteristics of workplace practices and types of informal work‐related learning: A survey study among Dutch Police. Human Resource Development Quarterly, 19(2), 129–151. https://doi.org/https://doi.org/10.1002/hrdq.1231

- Doyle, W., & Young, J. (2004). E-learning and small business: A nova scotia perspective. Paper presented at the Proceedings of the Atlantic Schools of Business Conference, Mount Saint Vincent University, Canada.

- Fakhfakh, M. (2016). Understandability of unmodified audit report on consolidated financial statements: A normative and advanced study of the international normalization. Cogent Business & Management, 3(1), 1258134. https://doi.org/https://doi.org/10.1080/23311975.2016.1258134

- Fleury, M. T. L. (2009). Organizational culture and the renewal of competences. BAR-Brazilian Administration Review, 6(1), 1–14. https://doi.org/https://doi.org/10.1590/S1807-76922009000100002

- Flower, J. (1999). In the mush. Physician Executive, 25(1), 64–67. https://pubmed.ncbi.nlm.nih.gov/10387273/

- Flowerday, S., Blundell, A. W., & Von Solms, R. (2006). Continuous auditing technologies and models: A discussion. Computers & Security, 25(5), 325–331. https://doi.org/https://doi.org/10.1016/j.cose.2006.06.004

- Franke, G., & Sarstedt, M. (2019). Heuristics versus statistics in discriminant validity testing: A comparison of four procedures. Internet Research, 29(3), 430–447. https://doi.org/https://doi.org/10.1108/IntR-12-2017-0515

- Freiling, J., & Fichtner, H. (2010). Organizational culture as the glue between people and organization: A competence-based view on learning and competence building. German Journal of Human Resource Management, 24(2), 152–172. https://doi.org/https://doi.org/10.1177/239700221002400204

- Gattiker, T. F., & Goodhue, D. L. (2005). What happens after ERP implementation: Understanding the impact of interdependence and differentiation on plant-level outcomes. MIS Quarterly, 29(3), 559–585. https://doi.org/https://doi.org/10.2307/25148695

- Gibran, M. (2010). Factors affecting the quality of the audit from the viewpoint of chartered accountants in Yemen. Paper presented at the The accounting profession in the Kingdom of Saudi Arabia and the challenges of the twenty-first century, Saudi Arabia

- Greenstein, M., & McKee, T. E. (2004). Assurance practitioners’ and educators’ self-perceived IT knowledge level: An empirical assessment. International Journal of Accounting Information Systems, 5(2), 213–243. https://doi.org/https://doi.org/10.1016/j.accinf.2004.04.002

- Greenstein-Prosch, M., McKee, T. E., & Quick, R. (2008). A comparison of the information technology knowledge of United States and German auditors. The International Journal of Digital Accounting Research, 8(14), 45–79. http://tubiblio.ulb.tu-darmstadt.de/35702/

- Gross, M. (2005). The impact of low-level skills on information-seeking behavior: Implications of competency theory for research and practice. Reference & User Services Quarterly, 45(2), 155–162. https://www.jstor.org/stable/20864481

- Hahn, E. D., & Ang, S. H. (2017). From the editors: New directions in the reporting of statistical results in the journal of world business. Journal of World Business, 52(2), 125–126. https://doi.org/https://doi.org/10.1016/j.jwb.2016.12.003

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2019). Multivariate data analysis (8th ed.). Cengage Learning.

- Hair, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling (PLS-SEM) (2nd ed.). Sage publications Inc.

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/https://doi.org/10.1108/EBR-11-2018-0203

- Hamid, M. S. A., Islam, R., & Manaf, N. H. A. (2014). Employability skills development approaches: An application of the analytic network process. Asian Academy of Management Journal, 19(1), 93–111. http://web.usm.my/aamj/19012014/Art%205%20(93-112).pdf

- Hamzah, M. I., Othman, A. K., Hashim, N., & Abd, M. H. (2013). Moderating effects of organizational culture on the link between leadership competencies and job role performance. Australian Journal of Basic and Applied Sciences, 7(10), 270–285. https://www.academia.edu/download/47354684/Moderating_effects_of_Organizational_Cul20160719-18317-ilplw5.pdf

- Han, S., Rezaee, Z., Xue, L., & Zhang, J. H. (2016). The association between information technology investments and audit risk. Journal of Information Systems, 30(1), 93–116. https://doi.org/https://doi.org/10.2308/isys-51317

- He, Y., Chen, Q., & Kitkuakul, S. (2018). Regulatory focus and technology acceptance: Perceived ease of use and usefulness as efficacy. Cogent Business & Management, 5(1), 1459006. https://doi.org/https://doi.org/10.1080/23311975.2018.1459006

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/https://doi.org/10.1007/s11747-014-0403-8

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. In R. R. Sinkovics & P. N. Ghauri (Eds.), New challenges to international marketing (Vol. 20, pp. 277–319). Emerald Group Publishing Limited.

- Hu, L.-T., & Bentler, P. M. (1998). Fit indices in covariance structure modeling: Sensitivity to underparameterized model misspecification. Psychological Methods, 3(4), 424–453. https://doi.org/https://doi.org/10.1037/1082-989X.3.4.424

- Institute of Management Accountants. (2020). Management accounting competency framework. https://www.imanet.org/career-resources/management-accounting-competencies?ssopc=1

- International Accounting Education Standards Board. (2018). Information and communications technology literature review. https://www.iaesb.org/publications/information-and-communications-technology-literature-review-0

- International Accounting Education Standards Board. (2019). Handbook of international education pronouncements. https://www.iaesb.org/publications/2019-handbook-international-education-standards

- International Federation of Accountants. (2003). Information technology for professional accountants. International education guideline 11. http://www.javeriana.edu.co/personales/hbermude/areacontable/particulares/IEG-11-Revised.pdf

- Jacobs, R., & Osman-Gani, A. (2005). Case studies in workplace training and learning: Across-cultural perspective. Pearson Prentice Hall.

- Jacobs, R. L., & Park, Y. (2009). A proposed conceptual framework of workplace learning: Implications for theory development and research in human resource development. Human Resource Development Review, 8(2), 133–150. https://doi.org/https://doi.org/10.1177/1534484309334269

- Keyton, J. (2015). Communication research: Asking questions, finding answers (4th ed.). McGraw-Hill Education.

- Klein, H. J., Noe, R. A., & Wang, C. (2006). Motivation to learn and course outcomes: The impact of delivery mode, learning goal orientation, and perceived barriers and enablers. Personnel Psychology, 59(3), 665–702. https://doi.org/https://doi.org/10.1111/j.1744-6570.2006.00050.x

- Klopping, I. M., & McKinney, E. (2004). Extending the technology acceptance model and the task-technology fit model to consumer e-commerce. Information Technology, Learning, and Performance Journal, 22(1), 35–48. https://search.proquest.com/docview/219841782?pq-origsite=gscholar&fromopenview=true

- Kock, N. (2015). Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e-Collaboration (Ijec), 11(4), 1–10. doi: https://doi.org/10.4018/ijec.2015100101

- Kontoghiorghes, C. (2001). A holistic approach toward motivation to learn in the workplace. Performance Improvement Quarterly, 14(4), 45–59. https://doi.org/https://doi.org/10.1111/j.1937-8327.2001.tb00229.x

- Krejcie, R. V., & Morgan, D. W. (1970). Determining sample size for research activities. Educational Psychological Measurement, 30(3), 607–610. https://doi.org/https://doi.org/10.1177/001316447003000308

- Kruger, J., & Dunning, D. (1999). Unskilled and unaware of it: How difficulties in recognizing one’s own incompetence lead to inflated self-assessments. Journal of Personality and Social Psychology, 77(6), 1121–1134. https://doi.org/https://doi.org/10.1037/0022-3514.77.6.1121

- Kunjiapu, S., & Yasin, R. M. (2015). Skills development and job satisfaction through workplace learning in small and medium tourism enterprises in Malaysia. Malaysian Journal of Chinese Studies, 4(1), 15–29. https://www.newera.edu.my/files/publication/MJCS_2015vol4no1-2.pdf

- Kurbanoglu, S. (2010). Self-efficacy: An alternative approach to the evaluation of information literacy. In A. Katsirikou & C. H. Skiadas (Eds.), Qualitative and quantitative methods in libraries: Theory and applications: Proceedings of the international conference on QQML2009 (pp. 323–328). World Scientific.

- Lau, P. Y. Y., & McLean, G. N. (2013). Factors influencing perceived learning transfer of an outdoor management development programme in Malaysia. Human Resource Development International, 16(2), 186–204. https://doi.org/https://doi.org/10.1080/13678868.2012.756157

- Le Deist, F. D., & Winterton, J. (2005). What is competence? Human Resource Development International, 8(1), 27–46. https://doi.org/https://doi.org/10.1080/1367886042000338227

- Lee, J.-C., Chen, C.-Y., & Shiue, Y.-C. (2017). The moderating effects of organisational culture on the relationship between absorptive capacity and software process improvement success. Information Technology & People, 30(1), 47–70. https://doi.org/https://doi.org/10.1108/ITP-09-2013-0171

- Liao, W.-C., & Tai, W.-T. (2006). Organizational justice, motivation to learn, and training outcomes. Social Behavior and Personality, 34(5), 545–556. https://doi.org/https://doi.org/10.2224/sbp.2006.34.5.545

- Lingappa, A. K., Kiran, K., . K., & Oommen Mathew, A. (2020). Safety training transfer in chemical manufacturing: The role of personality traits and learning motivation. Cogent Business & Management, 7(1), 1835335. https://doi.org/https://doi.org/10.1080/23311975.2020.1835335

- Lund, D. B. (2003). Organizational culture and job satisfaction. Journal of Business & Industrial Marketing, 18(3), 219–236. https://doi.org/https://doi.org/10.1108/0885862031047313

- Maass, S. A. (2017). Individual, organizational, and training design influences on supervision staff’s knowledge and use of evidence-based practices. (Doctoral dissertation, George Mason University). Available from ProQuest Dissertations & Theses Global. https://search.proquest.com/docview/1937522745/ECCB008BBCE746FBPQ/1?accountid=42599