?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Studies on green investment and corporate social responsibility (CSR) investment has been conducted by some researchers in the current and future trends of sustainable development. Many of them have focused on the relationship between CSR and financial performance, but only a few have examined how green investment, CSR investment, and sustainability are related to each other. Sustainable performance is based on three aspects: people-planet-profit, or also what is known as the triple bottom line concept. The sample for this study consisted of 132 manufacturing companies listed in the Indonesia Stock Exchange from 2016 to 2019. This study found that green investment and CSR investment positively affect financial performance and sustainable performance. Meanwhile, the financial performance has an insignificant effect on sustainable performance. Besides, financial performance cannot mediate the effect between green investment and CSR investment on sustainable performance.

PUBLIC INTEREST STATEMENT

Sustainable performance is a balanced performance based on three aspects; people, planet, and profit, or known as the triple bottom line concept. The company managers need to make decisions to invest and integrate it as a business strategy. To achieve sustainable performance, building a holistic and integrated environmental awareness is urgently needed by companies in all countries, including Indonesia. Manufacturing companies in Indonesia have contributed 20% of the environmental damage. Thus, high environmental awareness based on green investment and CSR investment should be included as a part of corporate responsibility to its stakeholders (i.e. society, investors, shareholders, customers, and other parties). Such investment can be a strategy to improve financial performance and sustainable performance as well as to avoid the legitimacy gap or social and environmental conflict. This study can be a reference for manufacturing companies in developing sustainable business strategy.

1. Introduction

Legitimacy has an important role in sustaining business. This has been emphasized by the finding by Dowling and Pfeffer (Citation1975), that an organization continues to seek legitimacy by aligning social values and norms with company values. The organization also maintains the harmony of these two values. As long as the company’s values or norms are in line with social values, the company will gain legitimacy and support from stakeholders (Ashforth & Gibbs, Citation1990; Dowling & Pfeffer, Citation1975; O’Donovan, Citation2002). One of the ways to improve company’s performance is corporate social responsibility activities. P.M. Clarkson et al. (Citation2011), Ganda et al. (Citation2015), and Kumarasiri and Jubb (Citation2016) believe that the activities will convince the investors to make sustainable investments. The investments are perceived as responsible and consistent with environmental ethics (such as reducing carbon emissions, green energy, and green technology).

Studies on the dynamics of sustainable performance involving green investment and CSR investment can create an interesting contribution to improving financial performance on sustainable performance. This study is also expected to reveal the reasons why manufacturing companies are committed to producing quality sustainability reports. Studies that consider green investment have been conducted by Chariri et al. (Citation2019), (Citation2018), and Cheema et al. (Citation2017); Zhu et al., (Citation2016); Eyraud et al. (Citation2013), Murovec et al. (Citation2012), Saxena and Khandelwal (Citation2012), and El Ghoul et al. (Citation2011). Meanwhile, studies on CSR aspects have only been conducted by Asogwa et al. (Citation2020), Eyasu et al. (Citation2020), and Nguyen et al. (Citation2020); Cupertino et al. (Citation2019); Ok and Kim (Citation2019), Viviani et al. (Citation2019), Jain and Winner (Citation2016), and Wahba and Elsayed (Citation2015), and Khojastehpour and Johns (Citation2014); Lanis and Richardson (Citation2012); Uadiale and Fagbemi (Citation2012).

Unfortunately, these research findings are contradictory, and most of the existing research ignores how green investment and CSR investment can improve financial performance on a sustainable performance of a company. Some researchers have found a positive relationship between environmental investments (Chariri et al., Citation2019) and green investment (Chariri et al., Citation2018) that could increase the company’s financial performance. Cheema et al. (Citation2017) believe that green environment provides social, ecological, and economic benefits. Zhu et al., (Citation2016) demonstrated that customer relational governance partially mediates the effect of green supply chain management practices on environmental performance. P. R. Martin and Moser (Citation2016) concluded that potential investors provide positive responses on firms that voluntarily disclose their green investment initiatives. Iatridis (Citation2013) stated that environmental disclosures contain relevant information value. Eyraud et al. (Citation2013) found that green investment is driven by economic growth and some green policy interventions. Murovec et al. (Citation2012) showed that environmental technologies have a positive effect on environmental investments. According to Saxena and Khandelwal (Citation2012), green investment will help industries gain a competitive advantage and sustainable growth. El Ghoul et al. (Citation2011) believe that corporate social responsibility (CSR) increases the investor base and reduces perceived risk. But other research has not identified a positive effect of environmental proactivity on financial performance (Cordeiro & Sarkis, Citation1997; Link & Naveh, Citation2006). Furthermore, P. M. Clarkson et al. (Citation2008), Iatridis (Citation2013), and Qiu et al. (Citation2016) concluded that good environmental performance consider changing to companies to prepare broader environmental disclosures, and this eventually leads to a higher corporate value (Iatridis, Citation2013; Lorraine et al., Citation2004).

In terms of CSR investment, Asogwa et al. (Citation2020) found that companies that engage in intensive social responsibility have positive effect on their companies’ stock value. Eyasu et al. (Citation2020) showed that separate stakeholders of CSR implementation have a positive effect on competitive advantage. According to Nguyen et al. (Citation2020), companies with CSR programs are more likely to receive unqualified opinions on the quality of their financial statements. Cupertino et al., (Citation2019) believed that a focus on environmental, social and governance standards may enhance a company’s long-term growth with a positive effect on its long-term value. Furthermore, Ok and Kim (Citation2019) implied that enhancing socially responsible management can increase company value. Viviani et al. (Citation2019) concluded that good socially responsible (SR) level reduces the downside risk level of stock returns. Jain and Winner (Citation2016) suggested that CSR climate shows the signs of positive reform. Moreover, Wahba and Elsayed (Citation2015) demonstrated that financial performance and CSR activities are the basis for making decisions related to investment by an investor. Khojastehpour and Johns (Citation2014) argue that environmental CSR has a positive effect on company/brand reputation and profitability. Lanis and Richardson, (Citation2012) stated that corporate social responsibility disclosure significantly strengthens the possibility of tax aggressiveness. Uadiale and Fagbemi (Citation2012) added that CSR has a positive and significant relationship with the financial performance measures. On the other hand, Brammer et al. (Citation2006) argued that the realized returns of firms with higher CSR performance are low, while Hamilton et al. (Citation1993); Nelling and Webb (Citation2009) found that CSR performance does not affect financial performance.

Currently, manufacturing companies in Indonesia contribute 20% of the environmental damage which triggers companies to disclose their sustainable performance (www.kemenperin.go.id). It is not only to gain maximum benefits but also to pay attention to the social impact of the investments. An environmentally friendly company will provide sustainable returns to investors. This is reflected by the Sustainable and Responsible Investment-KEHATI (SRI-KEHATI) stock index at the closing date of 2017–2020. It has better returns than the Composite Stock Price Index (IHSG) in recent years. The SRI-KEHATI index is a stock price index as a result of cooperation between the Indonesia Stock Exchange and the Indonesian Biodiversity Foundation (KEHATI Foundation). The SRI-KEHATI stock index is an indicator of stock price movements on the Indonesia Stock Exchange. This index uses the principles of sustainability, finance, good governance, and environmental concern as the benchmarks. The SRI-KEHATI stock index in 2017 and 2019 reached the levels of 395.56 and 400.56 respectively. However, in 2018 and August 2020, there was a decline to the level of 378.688 and 333.843 (www.idx.co.id) respectively. Based on this data, it can be concluded that the SRI-KEHATI stock index for manufacturing companies in Indonesia fluctuated during 2017–2020.

This study aims to find ways to build a holistic and integrative environmental awareness in improving financial performance and sustainable performance of manufacturing companies in Indonesia. High environmental concern based on green investment and CSR investment can create high financial and sustainable performance. Green investment, which consists of low carbon and climate resistance, is the crucial factor in the company’s sustainability to attract investor confidence in making a sustainable investment (Ganda et al., Citation2015). In other words, investment is responsible and consistent with environmental ethics (such as reducing carbon emissions, green energy, and green technology). Eyraud et al. (Citation2013), Mangla et al. (Citation2014), and Murovec et al. (Citation2012); and Zhu et al. (Citation2016) have shown that green investment can improve financial performance (Chariri et al., Citation2018, Citation2019) and create sustainable performance (Saxena & Khandelwal, Citation2012). This is due to the fact that the cost of green investment disclosure is lower than the cost for companies that do not disclose their environmental performance (Patrick R. Martin & Moser, Citation2012). Nevertheless, it is different from the findings by Munoz et al. (Citation2014) who found that green investment will decrease financial performance and sustainable performance because companies have to spend more on green investments (Ducassy, Citation2013; Lin et al., Citation2014).

Besides green investment, CSR investment may also increase financial performance and sustainable performance. Wahba and Elsayed (Citation2015) stated that CSR investment has the potential to positively contribute to the development of society and business. Thus, many organizations have begun to see the benefits of structuring CSR activities. Furthermore, Uadiale and Fagbemi (Citation2012) explained that CSR investment may improve reputation, profitability, and sustainable performance (Jain & Winner, Citation2016), so that further, it will enhance the company’s image. On the other hand, Menzel et al. (Citation2010); Newell and Lee (Citation2012) argued that CSR does not affect a company’s financial performance and its sustainable performance (Perez-Batres et al., Citation2010), because of the high additional costs of social responsibility. Lee et al. (Citation2017) found that there is no significant difference in the financial performance between companies that apply sustainability principles and companies that do not. CSR program is no longer considered the company’s responsibility to the public, but now it has become part of its investment to gain its growth and sustainable performance. CSR program is now shifted from spending budget orientation into profit orientation for the company.

Furthermore, financial performance is also becoming a measure of a company’s success in the operational activities (Lai & Wong, Citation2012). Many companies use the companies’ financial performance to make an investment decision in a sustainable environment. As a consequence, investors can predict their return through financial reports and sustainability reports that have been published by the company. The better the company’s financial performance, the higher the investors will invest their capital in the company. Therefore, it will increase sustainable performance (Bénabou & Tirole, Citation2010; Patrick R. Martin & Moser, Citation2012). In contrast, Dhaliwal et al. (Citation2011) and Karnani (Citation2010) found that financial performance has a negative effect on sustainable performance.

The previous studies only investigated the relationship between CSR and a company’s financial performance. Meanwhile, this study examined the role of green investment and CSR investment in improving the company’s financial performance and sustainable performance. Also, this study investigated how financial performance moderate the effect of green investment and CSR investment on sustainable performance. The pressure from green stakeholders and government policies has a profound impact on Indonesian business. This study contributes to assist the company’s decision-makers to respond positively to the environment. Besides, it helps the company in adopting green investment and CSR investment to increase profits without damaging the environment, and it can be a guide for investors in making investment decisions.

2. Literature review

Legitimacy theory highlights the importance of social consent in promoting a company’s sustainability. Therefore, companies must identify activities that are acceptable and in accordance with the beliefs, values, and norms of society. Burritt et al. (Citation2010) stated that legitimacy represents positive company externalities of the society regarding company practices in various social structures. Specifically, Gray et al. (Citation1995) explained that legitimacy depends on the fulfillment and alignment of social values and norms. It makes the company more acceptable to society. The company also continues to operate when the society is convinced that their interests have been addressed. As a result, the company implements environmental performance practices consistently to be accountable and gain the desired reputation. Based on Lindblom (Citation1994), there are four company legitimacy strategies. First, social reporting to communicate corporate efforts in addressing stakeholder interests. Second, public education and dissemination of information on relevant issues. Third, symbolic efforts to achieve legitimacy without changing performance and/or fulfilling the society demands. Finally, the fourth, incorporates popular perspectives according to business operations. Burritt et al. (Citation2010), Eyraud et al. (Citation2013), Ganda et al. (Citation2015), Khojastehpour and Johns (Citation2014), Kumarasiri and Jubb (Citation2016), and Mangla et al. (Citation2014), and Murovec et al. (Citation2012), and Uadiale and Fagbemi (Citation2012), and Wahba and Elsayed (Citation2015); and Zhu et al. (Citation2016) used this theory to describe how environmental performance affects the company’s financial performance.

Stakeholder theory indicates that companies are responsive to the demands of their internal and external partners in adopting policies and implementing strategic decisions. According to Freeman (Citation1984), stakeholder is any group or individual who can influence, or be influenced by, the implementation of company goals. Thus, stakeholder theory assumes that a company’s ability to operate lies in the strategic inclusion of stakeholder interests in decision making. Recently, stakeholder demands have reflected an increase in global concerns about weather conditions, natural disasters, and greenhouse gas emissions. Companies are morally obliged to adopt effective environmental performance initiatives to reduce environmental damage. Stakeholders play a major role in influencing the environmental performance of companies including (1) green government, through a strict carbon tax in addition to green laws; (2) green consumers, through a high preference for environmentally friendly products regardless of price; (3) environmentally friendly employees who prefer to work in companies with high carbon performance; and (4) green investors who give preference to green portfolios and independent environmental interest groups.

Financial performance is interpreted as how the company can earn income and growth (Selvarajah et al., Citation2018). The financial performance can be measured with several accounting methods such as return on assets, return on equity, and return on sales, and so on. Many companies use these whole methods to compare current performance with previous performance (to see if there is a decrease or increase) (Schniederjans, Citation2013; Waddock & Graves, Citation1997). Schniederjans (Citation2013) added that financial performance within a period could be used to measure performance achievements by the company, decision making by the investors, and capital augments for the company’s management.

The bank profitability ratio in Indonesia is still the highest compared to other South East Asia countries. Standard and Poor reported that the late 2018 Indonesian banks’ return on assets (ROA) industrially reached 2.55%. This achievement is higher compared to other South East Asia countries, which were only within a range of 1%-1.5%, such as the Philippines, Thailand, Malaysia, Singapore, and Vietnam (https://www.spglobal.com). By March 2019, the ROA of Indonesian Banks was recorded at 2.45%. It is higher compared to Thailand (1.24%), the Philippines (1.1%), Singapore (1.03%), and Malaysia (1.02%) (https://www.spglobal.com). Standard and Poor added that the capital adequacy ratio (CAR) of Indonesian banks within the same period was recorded at a level of 23.4%. It is higher compared to Malaysia (17.1%), Thailand (18.3%), Philippines (15.4%), and Singapore (16.5%). ROA in manufacturing companies listed in the Indonesian Stock Exchange within the 2016–2019 period tends to decline compared to ROA value on the highest point at 0.06 (in ratio units) in 2016. The lowest point was at 0.01 in the year 2014–2015. It was be affected by several troubled companies, such as PT. Polychem Indonesia Tbk. They listed their net profit after tax decreasing as Rp276.375.308.796 in 2016, -Rp 117.025.795.020 in 2017, and Rp18.891.637.461 in the year 2018. Other than that, PT. Eterindo Wahanatama Tbk has a deficit of -Rp68.488.774.415 in the year 2016 and -Rp127.520.042.125 in the year 2017.

There are three companies listed in Kuala Lumpur Composite Index in Malaysia that get in the high-performance category, which generate a detailed environment disclosure, while sixteen companies perform middle and low (Amran et al., Citation2010). Furthermore, when a financial or economic crisis occurs, most Malaysian companies are get affected. Whenever the economic condition not getting better, there is a probability that many of those companies will be forced to be dealing with liquidity (Yap et al., Citation2014). Meanwhile, in Singapore, two Companies listed in Strait Time Index Singapore were recorded to have a high-performance category that generates a detailed environment disclosure. It is lower than the total number of companies with middle and low performance (three and one companies) (Amran et al., Citation2010). In Thailand, the environmental disclosure practice by Companies listed in SET100 Thailand shows twelve companies have a low performance, and five companies have a high performance of environmental disclosure.

3. Hypothesis development

Green investment and CSR are forms of corporate responsibility to the stakeholder (public, investors, shareholders, customers, and other parties). There are also some strategies to improve financial performance and sustainable performance, as well as to avoid legitimacy gaps or social and environmental conflicts. According to Carnahan et al. (Citation2010); Little and Little (Citation2000), environmental accounting activities strengthen the reputation and legitimacy of a company as an intangible asset. This asset can produce sustainable benefits. Companies with low environmental performance tend to have a small shareholder base, low risk-sharing opportunities, and cheaper share prices than companies with high environmental activities (Hong & Kacperczyk, Citation2009). Moreover, companies with healthy relationship with stakeholders can mitigate market uncertainty, disruption, loss, or damage and unwanted events in the company operations (Ansong, Citation2017). Environmental and/or social accounting activities enhance a company’s ability to manage and reduce environmental and other risks including damage to brands, reputation, boycotts and government fines.

Green investment is a company strategy to gain and maintain legitimacy and support stakeholders. By doing so, the company manages the negative effect of operational activities on the environment by minimizing energy use and reducing carbon emissions (Berliner & Prakash, Citation2013; Minatti Ferreira et al., Citation2014; Testa et al., Citation2015). The company’s concern is stated in their annual report to illustrate their responsibility for the environment. Furthermore, the outcomes are decided by society and its stakeholders. Chariri et al. (Citation2018), (Citation2019), Cohen and Robbins (Citation2011), Mangla et al. (Citation2014), and Manrique and Ballester (Citation2017), and Murovec et al. (Citation2012), and Turcsanyi and Sisaye (Citation2013); and Zhu et al. (Citation2016) found a positive relationship between green investment and company’s financial performance. Saxena and Khandelwal (Citation2012) confirmed that there is a positive relationship between green investment and sustainable performance. This is due to the common goals shared by the company management and investors who want a green environment (Berliner & Prakash, Citation2013; Minatti Ferreira et al., Citation2014; Testa et al., Citation2015).

Meanwhile, CSR investment is an investment based on intangible resources such as innovation, human resources, reputation, and culture. It is realized by CSR initiatives in environmental preservation with the approval of shareholders, consumers, communities, and the government (Surroca et al., Citation2009). This CSR investment covers the organization’s economic, social and environmental impacts. There are also initiatives to provide stakeholders with better information on sustainability issues (GRI, Citation2013). Freeman (Citation1984) state that the company must provide benefits to its stakeholders, such as the welfare of employees, customers, and local communities. It aims to establish a good relationship between the company and the surrounding environment. De Klerk et al. (Citation2015); Khojastehpour and Johns (Citation2014); Mishra and Suar (Citation2013); Jain and Winner (Citation2016) state that CSR investment can improve reputation and a company’s performance. CSR creates a sustainable performance that can attract the attention of stakeholders to become part of the company by buying shares as proof of their ownership.

According to previous research, a positive correlation between CSR and financial performance can be interpreted as a means to increase financial benefits. It can be achieved through company reputation, brand image, customer loyalty, (Lee et al., Citation2017), cost reduction, operational flexibility, competitive advantage, and service (Galant & Cadez, Citation2017; Wahba & Elsayed, Citation2015). The success of environmental management will ultimately improve financial performance (Akisik & Gal, Citation2017; Chtourou & Triki, Citation2017; Devie et al., Citation2019; Feng et al., Citation2017; Mahrani & Soewarno, Citation2018; Nakamura, Citation2015; Nyeadi et al., Citation2018; Oware & Thathaiah, Citation2019; Salehi et al., Citation2018; Sun, Citation2012). Based on the description above, the hypotheses for this study are formulated as follows:

H1: Green investment has positive effect on financial performance

H2: CSR investment has positive effect on financial performance

H3: Green investment has positive effect on sustainable performance

H4: CSR investment has positive effect on sustainable performance

Based on the sustainability report with GRI standards, the implementation of green investment and CSR investment supports companies, both public and private, large and small, to protect the environment and improve social welfare. At the same time, it can also develop the economy by enhancing governance and stakeholder relations, improving reputation, and building trust. A good relationship with stakeholders can increase the investment potential. As a result, the company’s profit, in the form of productivity and sales, will increase. The increase in company profit or net income can be interpreted as an increase in the company’s financial performance. This illustrates the level of success of a company in generating profits which refers to the standards and policies that have been previously set (Cochran and Wood, Citation1984). The higher the profit of the company, the higher the rate of return to investors (Morea & Poggi, Citation2017).

The survival of the company also depends on the support of stakeholders. Therefore, the more powerful the stakeholders, the greater the company’s efforts to adapt (Artiach et al., Citation2010; Roberts, Citation1992; Ullman, Citation1985). The level of a company’s financial performance affects investment decisions in the future. For instance, when financial performance is high, the company faces urgent demands from financial and non-financial stakeholders. It provides the company with the financial resources to invest in social, environmental, and economic programs. High profitability allows the company to meet the expectations of financial stakeholders. It also maintains the company’s ability to fulfill the demands of social stakeholders through investment in social and environmental performance (Artiach et al., Citation2010).

Sustainable performance is a balanced performance based on three aspects: people-planet-profit, which is also known as the Triple Bottom Line concept. Therefore, company managers need to make decisions to invest. In other words, managers should not consider green investment and CSR investment activities as optional activities, but they can be integrated as a business strategy. When the implementation of green investment and CSR investment are closely integrated into company operations, it will ease the economic and social targets toward an improved social and financial performance of the company. Bénabou and Tirole (Citation2010) and Martin (Citation2012) showed that the company’s financial performance affects sustainable performance. This means that if the implementation of green investment and CSR investment are fulfilled, the company’s financial performance, as measured by return on assets, will increase. Thus, the hypothesis is formulated as:

H5: Financial performance has positive effect on sustainable performance

Based on the hypotheses above, the research model is described in below:

Figure 1. Research model

4. Research method

The sample frame of this study included all companies listed on the Indonesia Stock Exchange in 2016–2019. The sampling method used by this study was purposive sampling, with the following criteria: (1) manufacturing companies that published annual reports and sustainability reports from 31 December 2016 to 2019; (2) manufacturing companies that presented complete data related to research variables; and (3) manufacturing companies that presented annual reports in Indonesian rupiah (IDR). Based on these criteria, 132 manufacturing companies were selected as sample of this study.

This study has independent variables (green investment and CSR investment), an intervening variable (financial performance) and a dependent variable (sustainable performance). Green Investment is a company strategy to gain and maintain legitimacy. In this case, the company manages the business effects on the environment by minimizing energy use, reducing carbon emissions, and other negative effects (Berliner & Prakash, Citation2013; Minatti Ferreira et al., Citation2014; Testa et al., Citation2015). Green investment is measured by using PROPER (i.e Company Performance Assessment in Environmental Management). The Ministry of Environment and Forestry categorized the PROPER rating into five levels: five for Gold (very good), four for Green, three for Blue, two for Red, and one for Black (very poor) (Chariri et al., Citation2018; www.menlh.com).

CSR investment is an effort made by a company to be recognized as a socially wise entity to get support from stakeholders. As a result, it can build the company’s reputation, which in turn generates more profits (Surroca et al., Citation2009). The measurement of CSR investment (CSRINV) uses natural logs by including the cost spent on CSR activities (Oyewumi et al., Citation2018).

which:

CSRINC: CSR Investments

CSR Cost: Cost incurred by the company for CSR activities

Financial performance is used by companies to measure the level of success that the company has achieved in generating profits over a certain period. It refers to the standards or policies that have been previously set (Cochran and Wood, 1984). Financial performance is measured by the profitability ratio with the proxy of Return on Asset (ROA). ROA is the ratio of net income to total assets (Cochran and Wood, 1984).

Sustainable performance aims to improve investor confidence, employee loyalty, and maintain the company’s reputation in the eyes of the community (Ernst and Young, Citation2013). Sustainable performance is measured by using the Sustainability Report Disclosure Index (SRDI). It covers general and specific standards. General standards consist of disclosure strategy and analysis, and also organizational profile. It identifies the material aspects and boundaries, stakeholder relations, report profiles, governance, ethics, and integrity. Meanwhile, specific standards contain disclosures of the management approach, economic category indicators, environmental category indicators, and social category indicators (GRI, Citation2013). The SRDI calculation is determined by assigning a score of 1 if the item is disclosed, and a score of 0 if the item is not disclosed. The scores are then added up to obtain the score for each company. Sustainable performance is calculated by comparing the achieved disclosure score and the maximum score (Habek and Wolniak, Citation2015).

SEM-PLS (Structural Equation Modeling based on Partial Least Squares) with the SmartPLS 3.0 application was used to analyse the data in this study. SmartPLS 3.0 is designed to analyse latent variables using the manifest variable, multiple regression models, and path analysis using the observed variable (Ghozali and Latan, Citation2015). The research model of this study can be found below:

Information:

η1: Financial Performance

η2: Sustainable Performance

γ1-γ4: Coefficient

ξ1: Green Investment

ξ2: CSR Investment

ς1- ς2: Residual Value

5. Results

5.1. Descriptive statistic test

This study used several variables: CSR investment and green investment (as exogenous variables) and financial performance and sustainable performance (as endogenous variables). The results of descriptive statistics are presented in below:

Table 1. Descriptive statistic

As shown in , the green investment variable has a high mean value. In other words, the cross-section data between companies does not have a fairly large range of differences. It can be shown by PT. Astra Otoparts Tbk (AUTO) that disclosed the green investment activities well and consistently from 2016 to 2019. Based on the data, the PROPER rating of PT Astra Otoparts Tbk (AUTO) was at level 5 (Gold). Meanwhile, the CSR investment variable has a high mean value, which means that the cross-section data between companies does not have a fairly large range of differences. The next company that has implemented CSR investment well includes PT Semen Indonesia (Persero) Tbk (SMGR). In this company, the financial performance variable shows a low mean value. This means that the cross-section data between companies has a fairly large range of differences. For example, in terms of return on assets, when there is a deficit in a company, there is also profit in other companies this is as reflected in PT. Kertas Basuki Rachmat Indonesia Tbk (KBRI). The sustainable performance variable shows a high mean value. In other words, the cross-section data between companies does not have a fairly large range of differences. Furthermore, a company that has a good sustainable performance is PT Japfa Comfeed Indonesia Tbk (JPFA).

5.2. Measurement model results (outer Model)

5.2.1. Convergent validity and average variance extracted (AVE)

Convergent validity aims to determine the correlation between the indicator and its construct. It is categorized as valid and reliable if the correlation value is > 0.70 and the average variance extracted value is ≥ 0.50. The results of the outer model output are presented in and .

Table 2. Convergent validity

Table 3. Average variance extracted (AVE)

Based on the results of the convergent validity output above, the outer loading value is above 0.70. This proves that each variable has a good convergent validity value. Thus, the requirements for convergent validity have been fulfilled.

shows that the average variance extracted (AVE) output for each construct is >0.50. In conclusion, all variables have good AVE and fulfill the requirements.

5.3. Discriminant validity and composite reliability

Discriminant validity aims to measure the construct with its indicators by other constructs which can be seen from cross-loading. Meanwhile, the composite reliability test is used to assess the reliability of the indicators of a latent construct with Cronbach’s alpha value above 0.70. The results of the cross-loading output, composite reliability, and Cronbach’s alpha are presented below:

The value of cross-loadings in above shows that each construct and its indicator has a higher cross-loadings value than other constructs. Therefore, the constructs in this study can predict their indicators better than other indicators.

Table 4. Discriminant validity

above shows that the value of each construct is > 0.70. This means all constructs are good, and fulfill the reliability requirements.

Table 5. Composite reliability

5.4. Structural model test results (inner model)

5.4.1. Coefficient of determination (R2)

The R2 test was used to explain whether or not certain exogenous latent variables have a substantive effect on endogenous latent variables. If the value of endogenous variables is close to one, the R2 test is considered good. The following are the R-Square (R2) output results:

shows that the CSR investment and green investment variables explain only 8.7 percent of the financial performance variable, while the remaining 91.3 percent is explained by other variables. Similarly, the sustainable performance variable accounts for 34.6 percent of the explanation, while the remaining 65.4 percent is explained by other variables.

Table 6. R-Square (R)

5.5. Hypothesis result (t-Test)

The result of the hypothesis test can be determined by the P values obtained from the bootstrapping method in the Path Coefficient table. The hypothesis can be accepted if it has p-value of <0.05 and t-statistic of > 1.96. The t-test results are presented in below:

Table 7. Path coefficients

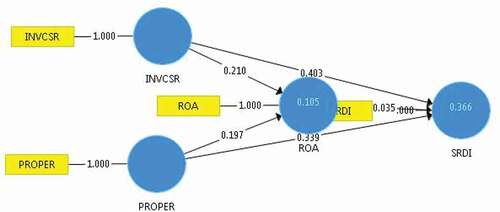

shows that the green investment variable has a parameter coefficient of 0.197, p value = 0.000 and a t-statistic 2,331 for financial performance. Meanwhile, for sustainable performance, the value of the parameter coefficient is 0.339, the p value = 0.001 and the t-statistic = 3.266. This means that the first hypothesis (H1), which states that green investment has a significant positive effect on financial performance, is accepted. Besides, the third hypothesis (H3), which states that green investment has a significant positive effect on sustainable performance, is accepted. CSR investment has a parameter coefficient of 0.210, p values of 0.027, and a t-statistic of 2,223 for financial performance. On the sustainable performance, the value of parameter coefficient is 0.403, p-value is 0.020 with t-statistic of 6,412. This means that the second hypothesis (H2), which states that CSR investment has a significant positive effect on financial performance, is accepted. Furthermore, the fourth hypothesis (H4), which states that CSR investment has a significant positive effect on sustainable performance, is accepted. The value of parameter coefficients, p values, and t-statistics for financial performance on sustainable performance are 0.035, 0.701 and 0.382 respectively. This means that the fifth hypothesis (H5), which states that financial performance has a significant positive effect on sustainable performance, is rejected.

indicates that financial performance has a t-statistic of 0.325 and 0.328, whereas the p-values are 0.745 and 0.743. In other words, financial performance cannot mediate the effect of green investment and CSR investment on sustainable performance.

Table 8. Specific indirect effect

6. Discussion

Green investment and CSR investment have a positive effect on financial performance and sustainable performance. This indicates that an increase or decrease in the number of green investment and CSR investment made by companies affects financial performance and sustainable performance. Furthermore, green investment and CSR investment in Indonesian manufacturing companies can persuade the public, management, and investors through the company’s environmental activities such as adopting new energy and company annual reports to reduce carbon emissions during the company’s manufacturing process. Thus, green investment and CSR investment have been proven to increase the company’s financial performance and sustainable performance.

The criteria for manufacturing companies used as samples in this study are companies that are responsible for their environment, and also companies that can convince internal and external stakeholders that the company is committed to environmental activities. The green investment activity is depicted in the PROPER rating. PT. Astra Otoparts Tbk. (AUTO) is at a rate of 5 (Gold/ 3.03%), PT. Ekadharma International Tbk (EKAD), PT. Industri Jamu dan Farmasi Sido Tbk (SIDO), PT. Semen Indonesia (Persero) Tbk (SMGR), PT. Indocement Tunggal Prakarsa Tbk (INTP), PT. JAPFA Comfeed Indonesia Tbk (JPFA), and PT. Kalbe Farma Tbk (KLBF) are at a rate of 4 (Green/21.21%) . Meanwhile, PT. Akasha Wira International Tbk (ADES), PT. Asahimas Flat Glass Tbk (AMFG), PT. Primarindo Asia Infrastructure Tbk (BIMA), PT. Berlina Tbk (BRNA), PT. Betonjaya Manunggal Tbk (BTON), and so forth are at a rate of 3 (Blue/75.76%).

The implementation of CSR in Indonesian manufacturing companies is shown by the reduction of the operating costs. This is because, after implementing CSR, the company will reduce the costs incurred for product marketing and replace them with CSR costs. Although the CSR costs incurred initially are the company’s responsibility costs to their environment, the CSR activities will affect company promotion activities and increase company sales. Therefore, the company will reduce its product promotion costs to reduce the company’s operating costs. The higher the CSR investment (the cost incurred for CSR activities), the more CSR activities conducted by the company. This indicates that manufacturing companies have changed their paradigm to view green investment and CSR investment as efforts to improve the welfare of society and companies.

The decision to invest in the environment can provide great benefits for the company. This is due to the fact that the main focus of social investment is not only attention on the environment, but also to obtain returns in the form of high profits. Accordingly, it can improve financial performance which in turn attracts investors to invest their shares. Moreover, the implementation of green investment and CSR investment in Indonesian manufacturing companies indicates a healthy and good relationship with stakeholders. It can reduce the risk of market uncertainty, disruption, loss, or damage to company operations and unwanted events (Ansong, Citation2017), because the green and CSR investment activities demonstrate the ability of a manufacturing company to manage and reduce environmental and other risks, such as brand damage, reputation, boycotts, and government fines.

The manufacturing companies in Indonesia have been active in maintaining their legitimacy by aligning policies and strategies according with environmental ethics. This is realized by managing the business effect on the environment (minimizing energy use, reducing carbon emissions, and other negative effects). The implementation of green investment and CSR investment can improve a company’s reputation and competitive advantage. Consequently, it also improves a company’s financial performance and sustainable performance. Thus, stakeholders will invest in the long term because they feel that manufacturing companies in Indonesia can survive for a long time. Furthermore, the green investment and CSR investment activities of the companies aim to respond to social needs in the sustainability reports used by companies. The sustainability reports are used by companies to communicate to the public and stakeholders. This helps in communicating the company’s contribution to environmental and/or social performance. As the result, it increases trust and maintains a good relationship between stakeholders in verifying the company’s social activities.

The results of this study are in line with the results of research by Chariri et al. (Citation2019), Cohen and Robbins (Citation2011), Mangla et al. (Citation2014), Manrique and Ballester (Citation2017), and Murovec et al. (Citation2012), and Turcsanyi and Sisaye (Citation2013), that green investment has a positive effect on financial performance. Saxena and Khandelwal (Citation2012) have proven that green investment has a positive effect on sustainable performance. Besides, Akisik and Gal (Citation2017), Chtourou and Triki (Citation2017), Devie et al. (Citation2019), Feng et al. (Citation2017), Mahrani and Soewarno (Citation2018), Nakamura (Citation2015), and Nyeadi et al. (Citation2018), and Oware and Thathaiah (Citation2019), and Salehi et al. (Citation2018), and Sun (Citation2012) also suggested that CSR investment has a positive and significant effect on financial performance. Furthermore, De Klerk et al. (Citation2015), Khojastehpour and Johns (Citation2014), Mishra and Suar (Citation2013), and Jain and Winner (Citation2016) believe that CSR investment can improve a company’s sustainable performance.

On the other hand, Munoz et al. (Citation2014) stated that green investment has a negative effect on financial performance. Oyewumi et al. (Citation2018) argued that CSR investment has a significant negative effect on financial performance because companies consider CSR investment as a cost. However, Ducassy (Citation2013) and Lin et al. (Citation2014) found that green investment has negative effect on sustainable performance. Menzel et al. (Citation2010); Newell and Lee (Citation2012) added that CSR investment does not affect improvement in financial performance. Furthermore, Perez-Batres et al. (Citation2010) stated that CSR investment does not affect sustainable performance.

Financial performance has no effect on sustainable performance. The results of this study show that financial performance does not play an important role in improving sustainable performance. The financial performance proxied by return on assets (ROA) shows that some of the ROA owned by manufacturing companies in Indonesia have decreased. This can be a sign that the company’s profits have decreased and the total asset of the company is big. Therefore, the comparison between profit and the total asset is small. The big total asset indicates that the components of the total assets are also big, such as receivables, loans, and financing. This is due to the fact that these components are the main percentage of the components that make up the total assets.

The sustainability aspect of manufacturing companies in Indonesia is still at the second or third level. Sustainable performance is still a “nice to have” thing. It has not reached the “great to have” thing, or a higher level, “mandatory to have”. The awareness and understanding of sustainable performance in Indonesia are still low. Consequently, the company’s financial performance is low as well. This indicates that high profitability does not necessarily fulfill the expectations and demands of the financial stakeholders. The level of financial performance produced by manufacturing companies in Indonesia cannot guarantee future investment decisions. When financial performance is high, companies face urgent demands from both financial and non-financial stakeholders and as such companies must have the financial capacity to invest in programs for social and environmental progress, as well as the economy.

Dhaliwal et al. (Citation2011) and Karnani (Citation2010) also found similar result and that is, financial performance has a negative effect on sustainable performance. Otherwise, Bénabou and Tirole (Citation2010) and Patrick R. Martin and Moser (Citation2012) believe that financial performance can improve the company’s sustainable performance. In other words, if green investment and CSR investment are applied, the company’s financial performance, as measured by Return on Assets, will increase.

7. Conclusion

Green investment and CSR investment activities of the 132 manufacturing companies in Indonesia were at the high category. This means that the majority of manufacturing companies have shown that their operational activities are consistent with the values and norms of community. Additionally, several stocks from manufacturing companies are listed in the SRI-KEHATI stock index, including PT. Japfa Comfeed Indonesia Tbk (JPFA), PT Kalbe Farma Tbk (KLBF), PT Industri Jamu dan Farmasi Sido Tbk (SIDO), and PT Semen Indonesia Persero Tbk (SMGR). This indicates that the manufacturing companies sampled in this study have good stock price performance as they are listed in 25 companies that have good performance in encouraging sustainable businesses. They also have the awareness of the environment, social, and good corporate governance.

Green investment and CSR investment have a positive and significant effect on financial performance and sustainable performance. This implies that the increase or decrease in the green investment and CSR investment affects financial performance and sustainable performance. Green investment and CSR investment are voluntary activities carried out by companies to achieve social goals and ethical motives. Previous research has revealed various CSR motivations, such as risk management and avoiding government penalties, although companies have to spend more to make green investment and CSR investment (Ducassy, Citation2013; Lin et al., Citation2014). Meanwhile, financial performance has a positive but insignificant effect on sustainable performance. Financial performance cannot mediate the effect of green investment and CSR investment on sustainable performance. Therefore, it can be concluded that financial performance is no longer an important factor in sustainable performance improvement.

This study has some implications for the role of green investment and corporate social responsibility investment on sustainable performance. First, this study can be a reference for manufacturing companies in Indonesia to adopt green investment and CSR investment. It can be a strategy to increase profits without damaging the environment. Second, for the government, this study can be a reference for formulating regulations related to business and the environment. Third, for investors, it can be used as a direction to create investment-related decisions. However, this study also has some limitations such as: first, the ability of green investment and CSR investment variables to explain the financial performance variable which is only 8.7% and the ability in explaining the sustainable performance variable is only 34.6%; second, these research results are limited to manufacturing companies in Indonesia; hence the results cannot be generalized to manufacturing companies in other countries. Therefore, future research needs to add other independent variables such as carbon price, company characteristics, good corporate governance, and adding samples for non-manufacturing companies.

Cover Image

Source: Author.

Additional information

Funding

Notes on contributors

Maya Indriastuti

Maya Indriastuti is a lecturer at the Faculty of Economics, Universitas Islam Sultan Agung. She is a PhD student at Faculty of Economics and Business, Universitas Diponegoro. Her areas of interest are in the fields of financial accounting, green accounting, corporate social responsibility, corporate governance, Islamic finance, banking and taxation.

Anis Chariri is a professor of accounting at the Faculty of Economics and Business at Universitas Diponegoro. His research interests are in the fields of qualitative and quantitative research concerning financial reporting, institutional aspect of accounting practice, and cultural perspective on accounting and corporate governance.

References

- Akisik, O., & Gal, G. (2017). The impact of corporate social responsibility and internal controls on stakeholders’ view of the firm and financial performance. Sustainability Accounting, Management and Policy Journal, 8(3), 246–21. https://doi.org/https://doi.org/10.1108/SAMPJ-06-2015-0044

- Amran, S. A. R., Yusoff, R., & Wan Mohamed, W. N. (2010). Environmental disclosure and financial performance: An empirical study of Malaysia, Thailand and Singapore. Social and Environmental Accountability Journal, 29(2), 46–58. https://doi.org/https://doi.org/10.1080/0969160X.2009.9651811

- Ansong, A. (2017). Corporate social responsibility and firm performance of Ghanaian SMEs: The role of stakeholder engagement. Cogent Business and Management, 4(1), 1–17. https://doi.org/https://doi.org/10.1080/23311975.2017.1333704

- Artiach, T., Lee, D., Nelson, D., & Walker, J. (2010). The determinants of corporate sustainability performance. Accounting and Finance, 50(1), 31–51. https://doi.org/https://doi.org/10.1111/j.1467-629X.2009.00315.x

- Ashforth, B. E., & Gibbs, B. W. (1990). The Double-Edge of organizational legitimation. Organization Science, 1(2), 177–194. https://doi.org/https://doi.org/10.1287/orsc.1.2.177

- Asogwa, C. I., Ugwu, O. C., Okereke, G. K. O., Samuel, A., Igbinedion, A., Uzuagu, A. U., Abolarinwa, S. I., & Ntim, C. G.. (2020). Corporate social responsibility intensity: Shareholders’ value adding or destroying? Cogent Business and Management, 7(1), 1. https://doi.org/https://doi.org/10.1080/23311975.2020.1826089

- Bénabou, R., & Tirole, J. (2010). Individual and corporate social responsibility. Economica, 77(305), 1–19. https://doi.org/https://doi.org/10.1111/j.1468-0335.2009.00843.x

- Berliner, D., & Prakash, A. (2013). Signaling environmental stewardship in the shadow of weak governance: The global diffusion of ISO14001. Law & Society Review, 47(2), 345–373. https://doi.org/https://doi.org/10.1111/lasr.12015

- Brammer, S., Brooks, C., & Pavelin, S. (2006). Performance and from returns : Disaggregate measures. Financial Management, 35(3), 97–116. https://doi.org/https://doi.org/10.1111/j.1755-053X.2006.tb00149.x

- Burritt, R. L., Schaltegger, S., & Burritt, R. L.. (2010). Sustainability accounting and reporting: Fad or trend? Accounting, Auditing & Accountability Journal, 23(7), 829–846. https://doi.org/https://doi.org/10.1108/09513571011080144

- Carnahan, S., Agarwal, R., & Campbell, B. (2010). The effect of firm compensation structures on the mobility and entrepreneurship of extreme performers. Business, 445(October2007), 1–43. https://doi.org/https://doi.org/10.1002/smj

- Chariri, A., Bukit, G. R., Eklesia, O. B., Christi, B. U., & Tarigan, D. M. (2018). Does green investment increase financial performance empirical evidence from Indonesia companies. E3S Web of Conferences. ICENIS, 1–7. https://doi.org/https://doi.org/10.1051/e3sconf/20183109001

- Chariri, A., Nasir, M., Januarti, I., & Daljono., D. (2019). Determinants and consequences of environmental investment: An empirical study of Indonesian firms. Journal of Asia Business Studies, 13(3), 433–449. https://doi.org/https://doi.org/10.1108/JABS-05-2017-0061

- Cheema, S., Javed, F., & Nisar, T.. (2017). The effects of corporate social responsibility toward green human resource management: The mediating role of sustainable environment. Cogent Business and Management, 4(1), 1310012. https://doi.org/https://doi.org/10.1080/23311975.2017.1310012

- Chtourou, H., & Triki, M. (2017). Commitment in corporate social responsibility and financial performance: A study in the Tunisian context. Social Responsibility Journal, 13(2), 370–389. https://doi.org/https://doi.org/10.1108/SRJ-05-2016-0079

- Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2008). Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations and Society, 33(4–5), 303–327. https://doi.org/https://doi.org/10.1016/j.aos.2007.05.003

- Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2011). Does it really pay to be green? Determinants and consequences of proactive environmental strategies. Journal of Accounting and Public Policy, 30(2), 122–144. https://doi.org/https://doi.org/10.1016/j.jaccpubpol.2010.09.013

- Cochran, P. L., & Robert, W. A. (1984). Corporate social responsibilityand financial performance. Academy of Management Journal, 27(1), 42–56. doi: https://doi.org/10.2307/255956

- Cohen, N., & Robbins, P. (2011). Green business: An A-to-Z guide, Thousand Oaks. In In green business: An A-to-Z guide. SAGE Publications Inc.

- Cordeiro, J., & Sarkis, J. (1997). Environmental proactism and firm performance: And, evidence from security analyst forecasts. Business Strategy Environment, 6(2), 104–114. https://doi.org/https://doi.org/10.1002/(SICI)1099-0836(199705)6:2<104::AID-BSE102>3.0.CO;2-T

- Cupertino, S., Consolandi, C., and Vercelli, A. (2019). Corporate Social Performance, Financialization, and Real Investment in US Manufacturing Firms. Sustainability, 11(7), 1836. doi:https://doi.org/10.3390/su11071836

- De Klerk, M., de Villiers, C., & van Staden, C. (2015). The influence of corporate social responsibility disclosure on share prices. Pacific Accounting Review, 27(2), 208–228. https://doi.org/https://doi.org/10.1108/PAR-05-2013-0047

- Devie, D., Liman, L., Tarigan, J., & Jie, F. (2019). Corporate social responsibility, financial performance and risk in Indonesian natural resources industry. Social Responsibility Journal, 16(9), 73-90. https://doi.org/https://doi.org/10.1108/SRJ-06-2018-0155

- Dhaliwal, D. S., Li, O. Z., Tsang, A., & Yang, Y. G. (2011). Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. The Accounting Review, 86(1), 59–100. https://doi.org/https://doi.org/10.2308/accr.00000005

- Dowling, J., & Pfeffer, J. (1975). Organizational legitimacy: Social values and organizational behavior. Pacific Sociological Review, 18(1), 122–136. https://doi.org/https://doi.org/10.2307/1388226

- Ducassy, I. (2013). Does corporate social responsibility pay off in times of crisis? An alternative perspective on the relation between financial and corporate social performance. Corporate Social Responsibility and Environmental Management, 20(3), 157–167. https://doi.org/https://doi.org/10.1002/csr.1282

- El Ghoul, S., Guedhami, O., Kwok, C. C. Y., & Mishra, D. R. (2011). Does corporate social responsibility affect the cost of capital? Journal of Banking and Finance, 35(9), 2388–2406. https://doi.org/https://doi.org/10.1016/j.jbankfin.2011.02.007

- Ernst and Young. (2013) . Value of Sustainability Reporting. Boston College Carroll School of Management.

- Eyasu, A. M., Arefayne, D., & Ntim, C. G.. (2020). The effect of corporate social responsibility on banks’ competitive advantage: Evidence from Ethiopian lion international bank S.C. Cogent Business and Management, 7(1), 1830473. https://doi.org/https://doi.org/10.1080/23311975.2020.1830473

- Eyraud, L., Clements, B., & Wane, A. (2013). Green investment trends and determinants. In Energy policy Elsevier, 60C (pp. 852–865). doi: https://doi.org/10.1016/j.enpol.2013.04.039

- Feng, M., Wang, X., & Kreuze, J. (2017). Corporate social responsibility and firm financial performance. American Journal of Business, 32(3–4), 106–133. https://doi.org/https://doi.org/10.1108/AJB-05-2016-0015

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Prentice-Hall.

- Galant, A., & Cadez, S. (2017). Corporate social responsibility and financial performance relationship: A review of measurement approaches. Economic Research Ekonomska Istraživanja, 30(1), 676–693. https://doi.org/https://doi.org/10.1080/1331677X.2017.1313122

- Ganda, F., Ngwakwe, C. C., & Ambe, C. M. (2015). Profitability as a factor that spurs corporate green investment practices in Johannesburg Stock Exchange (JSE) listed firms. Managing Global Transitions, 13(3), 231–252. http://www.fm-kp.si/zalozba//1581-6311/13_231-252.pdf

- Ghozali, I., and Latan. (2015). Concepts, Techniques, Applications Using Smart PLS 3.0 for Empirical Research. Diponegoro University Publisher. Semarang.

- Gray, R., Kouhy, R., Lavers, S. (1995). Corporate social and environmental reporting: A review of literature and a longitudinal study of UK disclosure. Accounting, Audiitng, and Accountability Journal, 8(2), 47–76. https://doi.org/https://doi.org/10.1108/09513579510146996

- GRI. (2013). Global reporting initiative G4. http://www.globalreporting.org

- Habek, P., and Wolniak, R. (2015). Assessing the quality of corporate social responsibility reports: the case of reporting practices in selected European Union member states. Quality & Quantity: International Journal of Methodology, 501, 399–420. doi:https://doi.org/10.1007/s11135-014-0155-z

- Hamilton, S., Jo, H., & Statman, M. (1993). Doing well while doing good? The investment performance of socially responsible mutual funds. Financial Analysts Journal, 49(6), 62–66. https://doi.org/https://doi.org/10.2469/faj.v49.n6.62

- Hong, H., & Kacperczyk, M. (2009). The price of sin: The effects of social norms on markets. Journal of Financial Economics, 93(1), 15–36. https://doi.org/https://doi.org/10.1016/j.jfineco.2008.09.001

- Iatridis, G. E. (2013). Environmental disclosure quality: Evidence on environmental performance, corporate governance and value relevance. Emerging Markets Review, 14(1), 55–75. https://doi.org/https://doi.org/10.1016/j.ememar.2012.11.003

- Jain, R., & Winner, L. H. (2016). CSR and sustainability reporting practices of top companies in India. Corporate Communications: An International Journal, 21(1), 36–55. https://doi.org/https://doi.org/10.1108/CCIJ-09-2014-0061

- Karnani, A. (2010). The case against corporate social responsibility. The Wall Street Journal, 23. https://www.wsj.com/articles/SB10001424052748703338004575230112664504890

- Khojastehpour, M., & Johns, R. (2014). The effect of environmental CSR issues on corporate/brand reputation and corporate profitability. European Business Review, 26(4), 330–339. https://doi.org/https://doi.org/10.1108/EBR-03-2014-0029

- Kumarasiri, J., & Jubb, C. (2016). Carbon emission risks and management accounting: Australian evidence. Accounting Research Journal, 29(2), 137–153. https://doi.org/https://doi.org/10.1108/ARJ-03-2015-0040

- Lai, K.-H., & Wong, C. W. Y. (2012). Green logistics management and performance : Some empiral evidence from Chinese manufacturing exporters. Omega, 40(3), 82–267. https://doi.org/https://doi.org/10.1016/j.omega.2011.07.002

- Lanis, R., and Richardson, G. (2012). Corporate social responsibility and tax aggressiveness: An empirical analysis. Journal of Accounting and Public Policy, 31(1), 86–108. doi:https://doi.org/10.1016/j.jaccpubpol.2011.10.006

- Lee, C., Chang, W., & Lee, H. (2017). An investigation of the effects of corporate social responsibility on corporate reputation and customer loyalty – Evidence from the Taiwan non-life insurance industry. Social Responsibility Journal, 13(2), 355–369. https://doi.org/https://doi.org/10.1108/SRJ-01-2016-0006

- Lin, I. H., Chang, O. H., & Chang, C. (2014). Importance of sustainability performance indicators as perceived by the users and preparers. Journal of Management and Sustainability, 4(1), 29–41. https://doi.org/https://doi.org/10.5539/jms.v4n1p29

- Lindblom, C. E. (1994). Success through inattention in school administration and elsewhere. Educational Administration Quarterly, 30(2), 199–213. https://doi.org/https://doi.org/10.1177/0013161X94030002006

- Link, S., & Naveh, E. (2006). Standardzation and discretion: Does the environmental standard ISO 14001 lead to performance benefits? IEEE Transactions on Engineering Management, 53(4), 508–519. https://doi.org/https://doi.org/10.1109/TEM.2006.883704

- Little, P. L., & Little, B. L. (2000). Do perceptions of corporate social responsibility contribute to explaining differences in corporate price-earnings ratios? A research note. Corporate Reputation Review, 3(2), 137–142. https://doi.org/https://doi.org/10.1057/palgrave.crr.1540108

- Lorraine, N. H. J., Collison, D. J., & Power, D. M. (2004). An analysis of the stock market impact of environmental performance information. Accounting Forum, 28(1), 7–26. https://doi.org/https://doi.org/10.1016/j.accfor.2004.04.002

- Mahrani, M., & Soewarno, N. (2018). The effect of good corporate governance mechanism and corporate social responsibility on financial performance with earnings management as mediating variable. Asian Journal of Accounting Research, 3(1), 41–60. https://doi.org/https://doi.org/10.1108/AJAR-06-2018-0008

- Mangla, S. M., Madaan, J., Sarma, P. R. S., & Gupta, M. P.. (2014). Multi objective decision modelling using interpretive structural modeling for green supply chains. International Journal of Logistics Systems, 17(2), 125. https://doi.org/https://doi.org/10.1504/IJLSM.2014.059113

- Manrique, S., & Ballester, C. (2017). Analyzing the effect of corporate environmental performance on corporate financial performance in developed and developing countries. Sustainability, 9(11), 1957. https://doi.org/https://doi.org/10.3390/su9111957

- Martin, P. (2012). Corporate social responsibility and managerial reporting. In Working Paper.

- Martin, P. R., & Moser, D. V. (2012). Managers’ green investment and related disclosure decisions. SSRN Electronic Journal. https://doi.org/https://doi.org/10.2139/ssrn.1911589

- Martin, P. R., & Moser, D. V. (2016). Managers’ green investment disclosures and investors’ reaction. Journal of Accounting and Economics, 61(1), 239–254. https://doi.org/https://doi.org/10.1016/j.jacceco.2015.08.004

- Menzel, V., Smagin, J., & David, F. (2010). Can companies profit from greener manufacturing? Measuring Business Excellence, 14(2), 22–31. https://doi.org/https://doi.org/10.1108/13683041011047830

- Minatti Ferreira, D. D., Borba, J. A., Rover, S., & Dal-Ri Murcia, F. (2014). Explaining environmental investments: A study of Brazilian companies. Environmental Quality Management, 23(4), 71–86. https://doi.org/https://doi.org/10.1002/tqem.21374

- Mishra, S., & Suar, D. (2013). Salience and corporate responsibility towards natural environment and financial performance of Indian manufacturing firms. Journal of Global Responsibility, 4(1), 44–61. https://doi.org/https://doi.org/10.1108/20412561311324069

- Morea, D., & Poggi, L. A. (2017). An innovative model for the sustainability of investment in the wind energy sector : The use of green Sukuk in an Italian case. International Journal of Energy Economics and Policy, 7(2), 53–60. https://www.researchgate.net/publication/316957398

- Munoz, F., Vagas, M., & Marco, I. (2014). Enviromental mutual funds : Finabncial performance and managerial abilities. Journal of Bussiness Ethics, 37(4), 551–569. https://doi.org/https://doi.org/10.1007/s10551-013-1893-x

- Murovec, N., Erker, R., & Prodan, I. (2012). Determinants of enviromental investment : Testing the structural model. Journal of Cleaner Production, 17, 265–277. https://doi.org/https://doi.org/10.1016/j.jclepro.2012.07.024

- Nakamura, E. (2015). The bidirectional CSR investment – Economic performance relationship. Journal of Global Responsibility, 6(1), 128–144. https://doi.org/http://dx.doi.org/10.1108/JGR-05-2014-0021

- Nelling, E., & Webb, E. (2009). Corporate social responsibility and financial performance: The “virtuous circle” revisited. Review of Quantitative Finance and Accounting, 32(2), 197–209. https://doi.org/https://doi.org/10.1007/s11156-008-0090-y

- Newell, G., & Lee, C. L. (2012). Influence of the corporate social responsibility factors and financial factors on REIT performance in Australia. Journal of Property Investment & Finance, 30(4), 389–403. https://doi.org/https://doi.org/10.1108/14635781211241789

- Nguyen, X. H., Trinh, H. T., & Ntim, C. G.. (2020). Corporate social responsibility and the non-linear effect on audit opinion for energy firms in Vietnam. Cogent Business and Management, 7(1), 1757841. https://doi.org/https://doi.org/10.1080/23311975.2020.1757841

- Nyeadi, J., Ibrahim, M., & Sare, Y. (2018). Corporate social responsibility and financial performance nexus. Journal of Global Responsibility, 9(3), 301–328. https://doi.org/https://doi.org/10.1108/JGR-01-2018-0004

- O’Donovan, G. (2002). Environmental disclosures in the annual report. Accounting, Auditing & Accountability Journal, 15(3), 344–371. https://doi.org/https://doi.org/10.1108/09513570210435870

- Ok, Y., & Kim, J. (2019). Which corporate social responsibility performance affects the cost of equity? Evidence from Korea. Sustainability (Switzerland), 11(10), 1–14. https://doi.org/https://doi.org/10.3390/su11102947

- Oware, K., & Thathaiah, M. (2019). Corporate social responsibility investment, third-party assurance and firm performance in India The moderating effect of financial leverage. Department of business administration, 303–324.

- Oyewumi, O., Ogunmeru, O., & Oboh, C. (2018). Investment in corporate social responsibility, disclosure practices, and financial performance of banks in Nigeria. Future Business Journal, 4(2), 195–205. https://doi.org/https://doi.org/10.1016/j.fbj.2018.06.004

- Perez-Batres, L. A., Miller, V. V., & Pisani, M. J. (2010). CSR, sustainability and the meaning of global reporting for Latin American corporations. Journal of Business Ethics, 91(2), 193–209. https://doi.org/https://doi.org/10.1007/s10551-010-0614-y

- Qinghua, Z., Feng, Y., & Choi, S.-B. (2016). The role of customer relational goverment in enviromental and economic performance improvement through green supply chain management. Journal of Cleaner Production, 155(2), 46–53. https://doi.org/https://doi.org/10.1016/j.jclepro.2016.02.124

- Qiu, Y., Shaukat, A., & Tharyan, R. (2016). Environmental and social disclosures: Link with corporate financial performance. British Accounting Review, 48(1), 102–116. https://doi.org/https://doi.org/10.1016/j.bar.2014.10.007

- Roberts, R. W. (1992). Determinants of Corporate social responsibilityDisclosure: An application of stakeholder theory. Accounting Organizations and Society, 17(6), 595–612. https://doi.org/https://doi.org/10.1016/0361-3682(92)90015-K

- Salehi, M., Lari Dashtbayaz, M., & Khorashadizadeh, S. (2018). Corporate social responsibility and future financial performance. EuroMed Journal of Business, 13(3), 351–371. https://doi.org/https://doi.org/10.1108/EMJB-11-2017-0044

- Saxena, R. P., & Khandelwal, P. K. (2012). Greening of industries for sustainable growth : An exploratory study on durable and service industries. International Journal of Social Economics, 39(8), 551–586. https://doi.org/https://doi.org/10.1108/03068291211238437

- Schniederjans, J. M. (2013). Information technology invesment: Decision making methodology. World Scientefic.

- Selvarajah, D., Murthy, D., & Massilamani, U., & Mathavi. (2018). The impact of corporate social responsibility on firm’s financial performance in Malaysia. International Journal of Business and Management, 13(3), 220. doi:https://doi.org/10.5539/ijbm.v13n3p220

- Sun, L. (2012). Further evidence on the association between corporate social responsibility and financial performance. International Journal of Law and Management, 54(6), 472–484. https://doi.org/https://doi.org/10.1108/17542431211281954

- Surroca, J., Tribó, J. A., & Waddock, S. (2009). Corporate responsibility and financial performance: The role of intangible resources. Strategic Management Journal, 31(5), 463–490. https://doi.org/https://doi.org/10.1002/smj.820

- Testa, F., Gusmerottia, N. M., Corsini, F., Passetti, E., & Iraldo, F. (2015). Factors affectingenvir onmental management by small and micro firms: The importance of entrepreneurs’ attitudes and environmental investment. Corporate Social Responsibility and Environmental Management, 23(6), 373–385. https://doi.org/https://doi.org/10.1002/csr.1382

- Turcsanyi, J., & Sisaye, S. (2013). Corporate social responsibility and its link to financial performance. World Journal of Science, Technology and Sustainable Development, 10(1), 4–18. https://doi.org/https://doi.org/10.1108/20425941311313065

- Uadiale, O., & Fagbemi, T. (2012). Corporate social responsibility and financial performance in developing economies: The Nigerian experience. Journal of Economics and Sustainable Development, 3(4), 44–54. https://core.ac.uk/download/pdf/234645537.pdf

- Ullman, A. A. (1985). Data in search of a theory: A critical axamination of the realtionship among social performance, social disclosure, and economic performance of U.S. firms. Academy of Management Review, 10(3), 540–557. doi: https://doi.org/10.2307/258135

- Viviani, J.-L., Revelli, C., & Fall, M. (2019). The Effects of A, CSR on Risk Dynamics and Risk Predictability: Value-at-risk Perspective 23(3), 141–157. https://doi.org/https://doi.org/10.7202/1062215ar

- Waddock, S. A., & Graves, S. B. (1997). The corporate social performance-financial performance link. Stategic Management Journal, 18(4), 303–319. https://doi.org/https://doi.org/10.1002/(sici)1097-0266(199704)18:4<303::aid-smj869>3.0.co;2-g

- Wahba, H., & Elsayed, K. (2015). The mediating effect of financial performance on the relationship between social responsibility and ownership structure. Future. Future Business Journal, 1(1), 1–12. https://doi.org/https://doi.org/10.1016/j.fbj.2015.02.001

- www.idx.co.id.

- www.kemenperin.go.id.

- www.menlh.com.

- Yap, B. C., Mohamed, Z., & Chong, K.-R. (2014). The effects of the crisis on the financial performance of Malaysian companies. The effects of the financial crisis on the financial performance of malaysian companies. Asian Journal of Finance & Accounting, 6(1), 236–248. https://doi.org/https://doi.org/10.5296/ajfa.v6i1.5314

- Zhu, Q., Feng, Y., and Choi, S. (2016). The Role of Customer Relational Goverment In Enviromental and Economic Performance Improvement Through Green Supply Chain Management. Journal of Cleaner Production, 155(2), 46–53. doi:https://doi.org/10.1016/j.jclepro.2016.02.124