?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study was conducted to investigate the determinants of bank’s stability in an emerging country. Data were collected from the commercial banks listed on Vietnam’s Stock Exchanges over the years from 2010 to 2018. Further, the generalized method of moments (GMM) regression technique to control for the three sources of endogeneity, namely, unobserved heterogeneity, simultaneity and dynamic endogeneity are concerned. Results demonstrate that there exists a positive effect from banking sector indicators such as equity-to-asset ratio, bank size, loans-to-assets ratio, revenue diversification on the stability of bank. In addition, a possible finding deals with the positive influence of macroeconomic factors in the banking sector on bank’s stability. Another possibility, bank’s stability in the previous year often goes hand in hand with this of the current year. Further investigated on every presence of foreign investment in the banking system, total assets- based foreign investment also correlates positively with bank’s stability. Finally, a negative effect from market share of mobilized capital, loan loss provisions, market structure on bank’s stability can be found.

Keywords:

Public interest statement

In recent years, bank’s stability has been focusing on the most economies worldwide. This concern is significantly increasing due to the global economic crisis and economic depression. The financial stability has become a key to global social and economic development. This study examines the determinants of bank’s stability in the case of Vietnam by employing the static analysis, and especially dynamic analysis based on the generalized method of moments (GMM) regression that is solved for endogeneity issue. The most important factors that can positively affect bank’s stability are equity-to-asset ratio, bank size, loans-to-assets ratio, revenue diversification, and total assets- based foreign investment.

1. Introduction

Banking sector in emerging economies has seen important transformations in the development of financial market. The recent financial crisis of 2007/2008 in the world was occurred and led a series of economic structural shifts. The banking system and financial institutions have faced difficulties how to maintain their operational activities, relieve losses and the need of liquidity. The financial stability and sustainable development have become a key to global social and economic development (Adusei & Elliott, Citation2015; Ali & Puah, Citation2018; Dao et al., Citation2020; Shair et al., Citation2021; Yin, Citation2019).

While there are several empirical studies that have investigated the determinants of bank’s stability, numerous empirical studies have focused on bank’s stability in both advanced and emerging economies (Ali & Puah, Citation2018; Lepetit et al., Citation2008; Sanya & Wolfe, Citation2011; Uhde & Heimeshoff, Citation2009). As theoretical models pointed out that banking system has played a significant role in human, social, and economic development (Tan & Floros, Citation2013). In fact, a healthy bank could predominantly promote more lending and reduce transaction fees, while a bank has a high cost of transactions as banking fees, overhead, and customer service that will reduce business’s profitability and economic performance (Nguyen, Citation2020).

This study contributes in three ways to the discussion about the determinants of banking’s stability. First, the study considers how the bank-specific banks could impact on banking’s stability in an emerging country since 2010, drawing insights from the discussion of Adusei (Citation2015); Ali & Puah (Citation2018). In addition, a foreign investment into the banking system will impact on market power (Manlagnit, Citation2011) and risk on the financial system (Klingelhöfer & Sun, Citation2019; Yin, Citation2019). On the asset side, the effects of macroeconomic factors on the stability of bank in the financial market can also be found (Adusei, Citation2015; Ali & Puah, Citation2018).

In Vietnam, the banking sector has been considered as an important engine to promote the development of financial system and well perform of the economic growth at roughly 7 per cent since political and economic reforms since 1986 (V.C. Nguyen & Do, Citation2020; Tran & Foroudi, Citation2020; Tran & Quang, Citation2019). However, the profit in the banking sector remarkably decreased in 2012–2015 period because of bad debts in lending and economic depression. Specifically, the bad debt ratio in on-balance sheet of commercial banks increased to 17.2% while the whole system should keep an acceptable level of bad debt ratio below 2%. In recent year, the Vietnam’s banking system has significantly changed at the uptrend development and stability level. A recent survey from the State bank of Vietnam (SBV) denoted that credit growth was maintained at 8–9% and capital mobilization rose by 9–10%. Further, Vietnam asset management company (VAMC) has been established to help the banking and financial system with the purpose to boost the debt purchase and the sale market. In reality, many commercial banks still face many difficulties in relation to the issue of handling collaterals and debt collection that may affect the stability of bank in the long run.

This current situation raised a new set of concerns for the central bank, policymakers, and researchers to study how to stabilize the banking and financial sector. In the previous studies, Adusei (Citation2015) just studied in the rural banking system in Ghana in which its economy is small and highly dependent on textiles sector and crude oil, gas exploration. In a study of Ali and Puah (Citation2018) who focus on the study how bank size and funding risk impact on bank stability in the case of Pakistan. In contrast to Vietnam, the shares of services are increasing and accounting for approximately 54% of GDP (Jalil et al., Citation2016). However, empirical studies on examining the impact of few factors as bank size, funding risk, and especially in a service driven economy on bank stability, with a particular emphasis on bank stability on a manufactured driven economy, have been largely ignored in the current state. In the context of Vietnam’s economy, the manufacturing sector has provided steadily support to the economy with contribution of 50.2% GDP while the smaller contribution for services and agricultural sector. Therefore, the objective of this study aims to examine important determinants of Vietnamese banking’s stability based on three factors, namely the bank-specific, competitive environment and macroeconomic factors. Specifically, the first group of bank-specific factors is related to the bank’s stability in the previous year, bank size, shareholders’ equity ratio, loan to asset ratio, bank share, loan loss provisions, revenue diversification, assets growth, and form of ownership. The second group of competitive environment factors is in association with the foreign investment in the banking sector. In addition, the third group of macroeconomic factors as GDP growth and inflation.

In order to analyze the objectives above, this study applies pooled ordinary least squares (pooled OLS), fixed effects model (FEM), random effects model (REM), and generalized least squares (GLS) because GLS may fix the common defects in the conventional model as multicollinearity, heteroscedasticity and autocorrelation. In addition, generalized method of moments (GMM) could be performed in order to treat the endogeneity in the analysis.

The remainder of this study is organized as follows. In Section 2, the study discusses the literature review the main determinants of bank’s stability. In Section 3, we present research methodology, research analysis, and descriptions of research variables, research samples, and data collection. In Section 4, we show our results. Section 5 discusses the results while conclusion referred in Sector 6.

2. Theoretical framework and literature review

In the current trend in the global financial system, many central banks and monetary authorities have concerned with financial stability and maintaining financial system safety. The financial stability and sustainable development have become a key to global social and economic development (Ali & Puah, Citation2018). The financial markets have always been concerned in both developing and developed countries, and countries in transition (Lepetit et al., Citation2013; Uhde & Heimeshoff, Citation2009; Sanya & Wolfe, Citation2011; Adusei, Citation2015; Ali & Puah, Citation2018; Dao et al., Citation2021). Referring to the study of the main determinants of bank’s stability, there have many types of researches in terms of both theoretical and empirical.

As suggested in the empirical previous studies of Adusei (Citation2015), Ali & Puah (Citation2018); Klingelhöfer and Sun (Citation2019), Zscore is the indicator denoting for bank’s stability and given as follows:

Where,

EATit, indicating for equity to asset ratio at the bank i and the time t

ROAit, indicating for return on assets at the bank i and the time t

, denoting for standard deviation of the sample

, denoting for bank’s stability

Previous studies suggest that there have given many empirical studies related to bank’s stability such as of (Adusei, Citation2015; Ali & Puah, Citation2018; Klingelhöfer and Sun, Citation2019; Lepetit et al. Citation2008; Nguyen et al., Citation2012; Sanya and Wolfe, Citation2011; Uhde and Heimeshoff, Citation2009; Yin, Citation2019). The studies aim to discuss the determinants of bank’s stability. Based on the assumptions of this, it is expected that the bank-specific factors (Lepetit et al., Citation2008; Sanya & Wolfe, Citation2011; Adusei,Citation2015; Ali & Puah, Citation2018), competitive environment factors (Uhde & Heimeshoff, Citation2009; Klingelhöfer & Sun, Citation2019; Yin, Citation2019), and macroeconomic factors (Adusei, Citation2015; Ali & Puah, Citation2018) have a statistically significant with the stability of bank.

Consistent with the literature on bank’s stability, Zscore measured for insolvency risk that is represented for bank’s stability (Adusei, Citation2015; Ali & Puah, Citation2018; Yin, Citation2019). It links a bank’s capitalization with returns with risk (volatility of returns) to estimate a bank’s solvency risk. Theoretically, a greater value of z-score describes a greater banking stability. A few number of empirical studies that used the z-score for analysis bank stability consists of Sanya and Wolfe (Citation2011), Adusei (Citation2015), Ali & Puah (Citation2018).

Regarding empirical research, numerous studies have concluded that bank-specific factors can influence bank’s bank. According to Adusei (Citation2015), bank stability has been typically supported by both bank size measured by natural logarithm of total assets or deposits, indicating that the aim of bank size expansion in relation to ensure stability in the financial market has to pursue. The contribution of bank size can also be investigated by Ali & Puah (Citation2018) over five Islamic and nineteen banks in Pakistan. In the context of credit risk measured by loans to asset ratio, that has a positive and statistically significant impact on stability of bank. Therefore, an increase in credit risk could expect better bank’s stability (Adusei, Citation2015; Ali & Puah, Citation2018)

Results also depict that revenue diversification has typically impacted on bank stability (Lepetit et al., Citation2008). Additionally, revenue diversification can create the role of the banks in the financial market in supervisory activities and enhance competitive pressures among banks, in particular in the participation of foreign banks in order to develop its business in a large kind of market segments, this channel can promote knowledge, technology and efficiency in the support process of services. According to Sanya and Wolfe (Citation2011) based on a sample of 226 listed banks in 11 emerging economies and the approach of system Generalized Method of Moments, diversification within and across interest and non-interest income generating activities can significantly decrease risk of insolvency and positively enhance bank performance. This is strongly supported by Baele et al. (Citation2007), revenue diversification can decrease bank’s stability in the case of European banks.

Drawing heavily on the bank-specific, macroeconomic, and institutional factors of the financial market and jointly covering the period of 1997–2005 in European banks, Uhde and Heimeshoff (Citation2009) discuss that concentration of banking sector has a negative effect on banks’ financial health as measured by stability level. In addition, banking markets in Eastern Europe displaying a lower level of income diversification, and competitive pressure, a higher proportion of state-owned banks will be more likely to decrease financial stability. In contrast, capital regulations from the central banks have significantly supported financial stability in the whole European Union.

As observed in the recent study in East Asian economies, Phan et al. (Citation2019) conclude that credit risk, bank size and market concentration can positively impact on bank’s stability. In contrast, a bank with a higher level of liquidity risk as well as revenue diversification can be less stable. Importantly, banking system stability is regularly decreased by financial crisis in the world. Further investigated in South Asia’s banking sectors such as Sri Lanka, Bangladesh, Pakistan, and India), Nguyen et al. (Citation2012) using generalized method of moments to correct the sources of endogeneity and also show that a bank with more revenue diversification in both interest income and non-interest income activities will result in an increase in stability. In addition, South Asia’s banking markets with greater competitive capacity can be related to the traditional interest income in operation.

Ozili and Outa (Citation2017) conduct on the review of loan loss provisions (LLPs) research in banks. In fact, LLPs in banking system plays an important role for financial stability and health in the process of acting lending function to their customers, therefore, the central banks have frequently requested banks have to keep optimal LLPs to relieve expected losses. To complement Tan and Floros (Citation2013) in a sample data of China’s commercial banks, and employing the link between efficiency, risk and capital, the empirical finding indicates that a positively statistically significant association between risk measured by LLPs and bank efficiency in China’s banking system, meanwhile the link between risk measured by Z-score and capitalization level is significant with a negative effect. By using a panel data of 565 commercial banks from 52 economies worldwide in the period of 2011–2015 and a dynamic analysis using the maximum likelihood with structural equation modelling, Siddika and Haron (Citation2019) found that an increase in capital ratio significantly decreases bank risk while a higher regulatory pressure is consistent with a higher level of bank risk. Further discussed on the concentration of ownership, a negative impact on bank risk can be found.

After the recent financial crisis of 2007/2008, in particular in the public debt crisis of 2012/2013 in European countries, the most important requirement in banking regulation is how to maintain minimum capital ratios and capital regulation in the specific bank and the banking system. The study of Shaddady and Moore (Citation2019) indicated their work on capital regulation and financial stability in the European banking industry. The empirical results confirmed that the significant relationship a higher level in capital regulation is positively and significantly correlated with stability of bank, while a decrease in restrictions, deposit insurance and oversupply of supervision will become to influence an inverse effect on bank’s stability. As suggested in Bouheni and Hasnaoui (Citation2017), financial stability is circular, in which, a higher in lending can increase a higher in risk-taking and therefore a higher in rising capital can mainly promote financial stability.

In terms of presence of foreign investment in the banking system, Yin (Citation2019) covering a sample of 129 countries in 1995–2013 period, the entry of foreign banks can badly affect the stability of bank because of more risk in loan and overall banking system in the host country. However, this relationship has been much dependent on regulation and legal framework, especially the negative impact from foreign banks on financial stability will be decreased in the case of more restrictions in its operation in fee generation, less strict capital requirements, asset diversification request, a lower level of barrier in market entry. This is consistent with results in Klingelhöfer and Sun (Citation2019), which find that the central banks may play a major role in protecting financial stability. In particular, macro-prudential policy can have prompt, determined effect on credit and sustain financial stability or a support to monetary policy to neutralize the accumulation of financial gaps occurring from monetary reducing.

Regarding macroeconomic factors, the effect of inflation and GDP on bank stability is negative in the case of Pakistan (Ali & Puah, Citation2018). This implies that an increase in either inflation or economic growth tend to decrease in bank’s stability. A possible explanation can be viewed that the banking system in Pakistan has been unable to predict the adjustment of price on its services while economic growth in relation to the financial crisis of 2007/2008 has not supported for bank’s stability. Nevertheless, Adusei (Citation2015) suggests that bank’s stability is more stable in the rising of inflation and economic growth. In specific, an increase in either economic growth rate or inflation in current quarter generates in an increase in bank’s stability in next quarter.

3. Data and methodology

3.1. Data

The sample used in this study includes yearly data from 2010 to 2018. Vietnam has two stock exchanges such as Ho Chi Minh City Stock Exchange (HOSE), and Hanoi Stock Exchange (HNX), therefore, this study has collected the secondary data in both HOSE and HNX. The data includes domestic-owned commercial banks. The data of top banks in Vietnam will be also collected in this analysis, such as Vietcombank, Vietinbank, and BIDV. In addition, approximately 31 domestic-owned commercial banks used in this study has mainly represented for 99.78% total Vietnamese bank’s assets.

The study is further collected macroeconomic factors such as GDP growth and inflation of Vietnam during the period of 2010–2018. These indicators are retrieved from World Bank and General Statistics Office of Ministry of Planning and Investment.

3.2. Methodology

We follow the panel data analysis used in this study in order to find out the factors influencing financial stability of commercial banks. Followed the empirical previous studies of Adusei (Citation2015), Ali & Puah (Citation2018); Klingelhöfer and Sun (Citation2019), this research model is to investigate the determinants of financial stability in financial system. In this study, the measure of the market structure is market share, which is a measure of relative market power. According to Mirzaei et al. (Citation2011), Wen et al. (Citation2015), market structure can be calculated as either the bank’s share of assets to total bank assets. It is evident that market share is positively associated with bank stability in the competitive environment of the financial market (Mirzaei et al., Citation2011).

The proposed model presents in as follows:

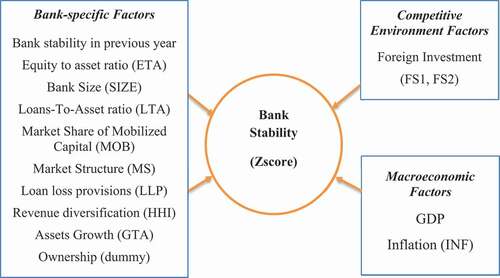

Figure 1. Research Model

The following equation is employed to examine the bank determinants of financial stability in the bank system listed on HOSE and HNX.

Where:

Ф1 … Ф13 are coefficients of regression;

εit is error term.

As suggested in the literature review, concludes the dependent and independent variables used in this study:

Table 1. Summaries of dependent and independent variables

Theoretically, the study analyzes based on pooled ordinary least squares (pooled OLS), fixed effects model (FEM), and random effects model (REM). In order to select the best model, F-test and Hausman test are preferred. It is perfectly reasonable to test multicollinearity heteroskedasticity and autocorrelation. According to Wooldridge (Citation2002), pooled OLS should be employed in the situation of a different sample for entities of the panel data. Fixed effects or random effects are employed when the study is going to observe the same sample of entities. Accordingly, generalized least squares (GLS) is ideally selected from three regression models (REM, FEM, pooled OLS) because GLS may fix the common defects in the conventional model as multicollinearity, heteroscedasticity and autocorrelation. Additionally, the POLS and FEM act as the robustness check for the regression coefficients. In the empirical studies of Arellano and Bond (Citation1991) the regression could be appeared the correlation between the observation matrix (the regressors) and the error terms. Furthermore, the POLS, FE and RE have problems to cater for dynamic model as compared to the generalized method of moments (GMM). To treat the endogeneity, GMM should be preferably performed. Further, the absence of defects in the model can enhance the research results more effective, unbiased, and normally distributed.

4. Results

4.1. Descriptive statistics

shows the descriptive statistics of the research variables. This research focuses on the sample of 31 commercial banks. It includes state-owned commercial banks and private joint-stock commercial banks in Vietnam.

Table 2. Descriptive statistics of research variables

depicts that Zscore has an average value of 12.66, but the standard deviation is 5.689 and quite large with the minimum value of 0.903 and the maximum value of 33.92. It shows that a significant gap in bank stability listed on HOSE and HNX in the period of 2010–2018. Further, bank’s size has an average value of 18.37 with the minimum value of 15.922 and the maximum value of 20.99. It indicates an insignificant gap in bank’s size in Vietnam. In addition, bank’s equity (ETA), revenue diversification (HHI), loans to assets ratio (LTA), and the market share of mobilized capital (MOB) have an average value of 0.094, 0.287, 0.543, and 0.636 respectively, with a major difference. Regarding foreign investment in the banking system, the portion of foreign-owned bank branches on the banking sector (FS1), the portion of foreign-owned banks’ assets on the banking sector’s assets (FS2) have an average value of 0.200, and 0.102 respectively, with a minor difference, indicating that foreign investment in the bank system has slightly fluctuated during this period. In addition, it has a huge range between 5.25% and 7.08% for GDP and between 0.19% and 21.26% for inflation.

shows the correlation matrix between variables used in the study. More specifically, the highest correlation (−0.79) obtained between ETA and Zscore1. As shown in V.C. Nguyen and Do (Citation2020), the absence of multicollinearity could be found if correlation coefficient is less than 0.8. It is therefore confirmed that there is no absence of multicollinearity in our regression analyses.

Table 3. Correlation Matrix

4.2. Regression results

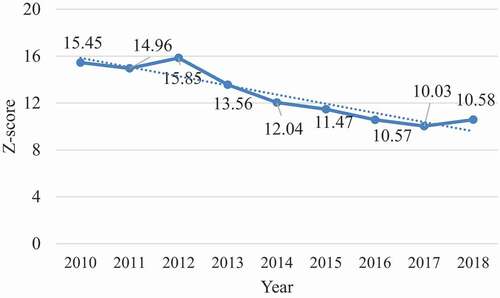

indicates the trends of Z-score index in the commercial banks in Vietnam in the period of 2010–2018, showing that Z-score index has been increasingly decreased between 15.45 and 10.58 in the period of 2010–2018. It is in relation to less stability in the bank system over time.

Figure 2. Average Z-score in Banks in the Period of 2010–2018

Z-score index can be represented for the stability of a bank. shows that Z-score index has been increasingly decreased between 15.45 and 10.58 in the period of 2010–2018. It is in relation to less stability in the bank system over time.

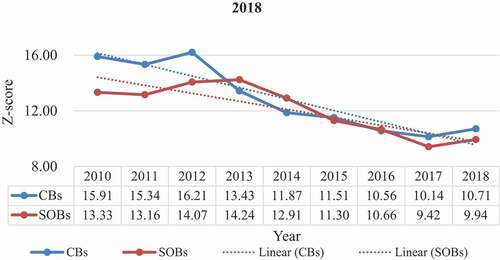

Figure 3. Z-score of Commercial Banks and State-Owned Banks in the Period of 2010–2018

Given that the variables are concerned. Factors influencing the bank stability can be estimated using pooled OLS, FEM and REM, especially to correct diagnostics problems by using GLS and GMM. The result has been reported in :

Table 4. Regression Results

shows the regression results and the test in the model. Firstly, through variance inflation factors (VIF), the value of VIF is 1.95 and less than 10 so that the multicollinearity is not existed. According to F-test, Prob > F = 0.0000, indicating that FEM is more appropriate than pooled OLS. In terms of Hausman test, it also indicates that FEM is better than REM because of Prob>chi2 = 0.000.

Breusch-Pagan test for heteroskedasticity with Prob>chi2 = 0.0000, and Wooldridge test serial correlation with Prob>F = 0.0000, indicating that there exist heteroskedasticity and autocorrelation in the model. To be correct the problems, generalized least square (GLS) is considered. Further, the correlation between the observation matrix (the regressors) and the error terms could be revealed, based on Hansen test with Prob > chi2 = 0.90, Sargent test with Prob > chi2 = 0.94 as well as the test of AR(2) with Pr > z = 0.719, it concludes that the absence of endogeneity is solved and GMM is more suitable in the model. As suggested in Bond et al. (Citation2001), the POLS estimate for Ф1 (coefficient of regression) should be considered an upper-bound estimate, while the corresponding fixed effects estimate should be considered a lower-bound estimate. In this case, the system GMM should be preferred due to the coefficient of regression Ф1 from system GMM is in the middle of the coefficient of regression Ф1 from POLS and FEM while the difference GMM estimate we obtained is below the fixed effects estimate.

5. Discussion

5.1. Bank-specific factors

5.1.1. Zscore in the previous year (Zscore_1)

The result shows that the coefficient of Zscore_1 is positive and significant. It is better to indicate that the impact of the bank’s stability in the previous year will positively impact on its bank in the current year. It is a noteworthy discussion that the bad debt ratio in on-balance sheet of Vietnamese commercial banks boosted to 17.2% while the bad debt ratio in the whole banking system should be an acceptable level of below 2%. In fact, during in the period of 2012–2015, Vietnam’s banking system has significantly faced difficulties in agreement with the issue of handling collaterals and bad debt collection, therefore, the stability of bank in this year can affect this in the coming year. Further, cross ownership in the Vietnam’s banking system had a problem in this period, credit institutions were not permitted to lend to major shareholders and their relatives in the case of holding less than 5% of another credit institution’s charter capital for the shareholders. In addition, shareholders and their relatives were also prohibited from increasing their stake holdings. Therefore, in the period of 2012–2017, the banking system has faced number of difficulties on their operation in the backdrop of solving bad debt and also cross-ownership issue (Le & Khuat, Citation2017).

5.1.2. Equity-To-Asset ratio (ETA)

This variable denotes for shareholder’s equity ratio and indicates the quotient of share’s equity on a bank’s assets. When a bank’s shareholder equity ratio increases, it means the bank has financed more equity on its assets instead of taking on debt. The coefficient of ETA is positive and significant, indicating that a bank with a higher level of equity in capital structure is positively consistent with a higher level of stability. This result supports with past studies of Juabin (Citation2019) in the commercial banks in Ghana. According to Juabin (Citation2019) banking system is a major player on the mediating role of stability in Ghana’s economy in which bank could not have been able to meet the demand of creditors because the tightening of supervisory and monitoring role in the banking system in order to detect early signs of non-performing banks. In Vietnam, the equity to asset ratio is still limited, in this case, State Bank of Vietnam (Citation2020) requests commercial banks that must increase their charter capital, therefore, most of commercial banks must find capital from either foreign investors or rising capital domestically. In addition, State Bank of Vietnam (Citation2020) suggests commercial banks have to keep profits and not pay dividends

5.1.3. Bank Size (SIZE)

The coefficient of SIZE is positive and significant. It reveals that a larger bank size will positively enhance its stability. It is associated with the finding of Nguyen (Citation2020) and in relation to micro-economic, a larger bank is frequently more efficient because of economies of scale. Further, a larger bank can own a lower bankruptcy cost and enhancement of a higher growth rate which is consistent with a better stability. This result supports with the past findings of Adusei (Citation2015) in Ghana, and contracts with the studies of Ali & Puah (Citation2018) in Pakistan. Adusei (Citation2015) suggests that in the context of global financial crisis, banking system is as the lifeblood in the economy, by demanding more capital and liquidity in the line of the requirements of Basel III is significantly necessary, and increasing bank size is more responsible for the global crisis. In agreement with a rising level of bank size, Nguyen (Citation2020) indicates that a larger size had a lower cost of bankruptcy and robustness of a higher growth rate which is connected with a greater performance. Therefore, it will help a bank less its risk-taking.

5.1.4. Loans to assets ratio (LTA)

LTA as an indicator measured for the level of bank liquidity that indicates the percentage of bank’s loans to total assets in a given year. shows that the variable of LTA has a positive and significant effect on bank’s stability. The positive and significant influence of LTA on bank’s stability indicates an increase of LAR will positively affect the stability of the bank in the short run. In fact, the income of commercial banks has been mostly contributed by loans. In the case of Vietnam, the NPL ratio of Vietnam’s banking system increased from 3% in 2012 to more than 8% in 2013, even at least 17.2% in regard to the evaluation of Moody. In the year of 2014–2018, a bank with lower rate of NPL could be allowed high credit growth as the request of State Bank of Vietnam (Citation2014). This research is supported by Phan et al. (Citation2019) conducting research in East Asian economies, and Ali & Puah (Citation2018) in Pakistan.

5.1.5. The market share of mobilized capital (MOB)

The market share of mobilized capital (MOB) has a negative and significant influence on the stability of bank. This indicates that the stability of a bank will be worsened if the market share of mobilized capital of that bank increases. This result is not in line with the opinion of Bouheni and Hasnaoui (Citation2017) when using an unbalanced panel of approximately 722 banks covering the years of 1999–2013 in European countries.

5.1.6. Loan loss provisions (LLP)

The LLP variable has a negative and significant influence on bank stability. If the loan loss provisions increase, the bank stability will decrease. This indicates that large loan loss provisions in the operational activities in a bank greatly impact on the stability of bank with a negative sign in the short run. In this study, the relationship between LLP and bank stability cannot be found in the long run. It is cornered by the discussion of Aristei and Gallo (Citation2019) that LLPs are predominantly impacted by non-discretionary factors in relation to the upcoming credit risk. Aristei and Gallo (Citation2019) further concluded that LLPs will be a higher level in regional banking sectors with a higher level in loan concentration and a lower level of competition degree. In addition, a bank facing increasing risk will be characterized by a higher level of LLPs in the case of Italy.

5.1.7. Revenue diversification (HHI)

shows that the revenue diversification (HHI) variable is statistically significant and negatively associated with the stability of a bank in the long run. The results depict that if increasing in the revenue diversification will harm bank’s stability in the long run. It is supported by the studies of Baele et al. (Citation2007), Sanya and Wolfe (Citation2011), and Lepetit et al. (Citation2008). More specifically, the market entry of foreign and privately owned banks in the banking sector, forcing other existing banks have to expand their products and services at low fees instead of focusing on traditional activities. This process can increase operating costs, and decrease in bank stability. Adversely, Nguyen et al. (Citation2012) conduct on a study in South Asian economies, a bank will be more stable when a bank can diversify revenue across from interest-income and non-interest income activities.

5.1.8. Market structure (MS)

indicates that the market structure has a negative and significant impact on bank stability, meaning that a bank with a higher market share will lead to that bank becoming less stability. As explained by Allen et al. (Citation2011) arguing that bank competition can encourage banks to have better capital levels because the competition can increase the effectiveness of monitoring in the bank, and attraction of creditworthy customers. In the case of Vietnam, according to Vietnam Stock Exchanges about major banks in the country, by the end of 31 December 2020, the total assets of banks reached more than 11 million billion VND, an increase of 11.3% compared to the end of 2019. But total assets of the four largest banks in Vietnam are VND 5.6 million billion, accounting for over 50% of the total assets of the system. That shows that the level of competition at Vietnamese banks is not really high. As shown by T.N. Nguyen and Pham (Citation2019), financial capacity is the weakest point of Vietnamese banking system, which will lead to limitations in competitiveness when integrating.

5.1.9. Growth of total assets (GTA) and form of ownership

The regression results show growth of total assets (GTA) has a negative and insignificant impact on bank’s stability. In fact, growth of total assets is in relation to increasing in liquidity of bank assets. It is for this reason that after the 2007/2008 global financial crisis and 2012/2015 Vietnam’s bad debt crisis, numerous commercial banks need to take care of its assets’ quality and liquidity in order to overcome shocks in the financial market. Adversely, Wagner (Citation2007) has another view on this relationship, a higher level in asset liquidity incontinently promotes bank’s stability by supporting banks to decrease its risks on the balance sheet and by relieving the payment of assets in the crisis. Regarding form of ownership, it has a negative and statistically significant effect on bank’s stability. A state-owned bank will be less stable than a private-owned bank. It is not in line with Uhde and Heimeshoff (Citation2009) on the study in European banks, and Klingelhöfer and Sun (Citation2019) on the study of Chinese financial market. More importantly, central banks can play a major role in sustaining financial stability. The well-designed combination of two policies such as targeted macroprudential policy, and harmonization with monetary policy can help to perform the objectives of financial stability.

5.2. Competitive environment factors

In terms of the contribution of foreign investment in the banking system, depicts that the coefficient of FS2 is statistically significant and positive effect on bank’s stability. This is justified by the fact that a larger proportion of foreign banks in terms of its total assets in the host country will make benefits for bank stability in the both short run and long run. Further discussed, Yin (Citation2019) concluded that for more improvement of financial stability, the host country needs to reduce converse effect of the entry of foreign investment in the banking system. This probably explains why the government should balance both demands and carefully circumstance prudential regulations to sustain financial stability and minimize the negative impact from foreign investment in the banking system.

5.3. Macroeconomic factors

Two macroeconomic factors such as GDP growth and inflation discussed in this study, GDP growth and inflation have positively affected bank stability at a significant level of 1%. This finding is supported by Phan et al. (Citation2019) conduct on study in East Asian countries. Further discussed, stability in banking sector was conversely impacted by financial crisis in the globe. During this crisis, global economic growth and local economic growth are likely to be the worst due to the interaction the financial market between Vietnam and the region. More importantly, Vietnam’s economy has been much dependent on foreign investment and trade openness (Nguyen, Citation2020), external shocks could affect macroeconomic performance and stability of bank.

6. Conclusions and implications

The aim of the study is to investigate the main determinants of bank’s stability with yearly data (2010–2018) from the banking sector in an emerging economy of Vietnam. The secondary data are collected from in Ho Chi Minh City Stock Exchange (HOSE) and Hanoi Stock Exchange (HNX) with panel generalized method of moments regression technique that has been used. Overall, we find a positive relationship between banking sector indicators such as equity-to-asset ratio, bank size, loans to assets ratio, revenue diversification, and the bank’s stability. At the same time, we find a negative relationship for market share of mobilized capital, loan loss provisions, market structure and the stability of bank.

A possible finding deals with the positive influence of macroeconomic factors in the banking sector on bank’s stability. In addition to its bank’s stability in the previous year, the study shows that bank’s stability in the previous year often goes hand in hand with this of the current year. Further investigated on every presence of foreign investment in the banking system, banking sector foreign investment also correlates positively with bank’s stability.

This study has some implications. Firstly, State Bank of Vietnam should keep banking system more stable, especially manage non-performing loans that largely comprise of mortgages, and personal business loans, and normally secured by property, but the bad debt could negatively harm economic development and the bank stable. Secondly, State Bank of Vietnam continue to solve cross-ownership problems by continuing to deploy Circular No 46/2018/TT-NHNN in which credit institutions and their relatives will be not allowed to hold more than 5 percent of charter capital in another credit institution in the financial and banking system in Vietnam. This policy could further deploy in future. Finally, credit institutions need to increase their charter capital in order to easily keep their operating activities and adapt requirements of Basel II and Basel III in the upcoming years. At present, State Bank of Vietnam has just requested some banks forbearance on Basel II implementation but many banks have delayed the requirements of Basel II.

Additional information

Funding

Notes on contributors

Van Chien Nguyen

Van Chien Nguyen is a graduate of doctoral study at the Department of Economics of University of Colombo, Sri Lanka. He works for Thu Dau Mot University and his research interests are financial economics, finance, and energy.

Le Kieu Oanh Dao is a graduate of doctoral study at the Banking University of Ho Chi Minh City, Vietnam. She works for Banking University of Ho Chi Minh City and specializes in macroeconomics, and banking. She has published some scientific papers on worldwide.

Thuy Tu Pham is a graduate of doctoral study at the Banking University of Ho Chi Minh City, Vietnam. She works for University of Finance - Marketing, Vietnam, and specializes in banking, and economics.

References

- Adusei, M. (2015). The impact of bank size and funding risk on bank stability. Cogent Economics & Finance, 3(1), 1111489. https://doi.org/https://doi.org/10.1080/23322039.2015.1111489

- Ali, M., & Puah, C. H. (2018). Does bank size and funding risk effect banks’ stability? A lesson from Pakistan. Global Business Review, 19(5), 1166–18. https://doi.org/https://doi.org/10.1177/0972150918788745

- Allen, F., Carletti, E., & Marquez, R. (2011). Credit market competition and capital regulation. The Review of Financial Studies, 24(4), 983–1018. https://doi.org/https://doi.org/10.1093/rfs/hhp089

- Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Review of Economic Studies, 58(2), 277–297. https://doi.org/https://doi.org/10.2307/2297968

- Aristei, D., & Gallo, M. (2019). Loan loss provisioning by Italian banks: Managerial discretion, relationship banking, functional distance and bank risk. International Review of Economics & Finance, 60(C), 238–256. https://doi.org/https://doi.org/10.1016/j.iref.2018.10.022

- Baele, L., De Jonghe, O., & Vennet, R. V. (2007). Does the Stock Market value bank diversification? Journal of Banking and Finance, 31(7), 1999–2023. https://doi.org/https://doi.org/10.1016/j.jbankfin.2006.08.003

- Bond, S., Hoeffler, A., & Temple, J. (2001). GMM Estimation of Empirical Growth Models. 2001-W21, Economics Group, Nuffield College, University of Oxford. Available on https://ideas.repec.org/p/nuf/econwp/0121.html

- Bouheni, F. B., & Hasnaoui, A. (2017). Cyclical behavior of the financial stability of eurozone commercial banks. Economic Modelling, 67, 392–408. https://doi.org/https://doi.org/10.1016/j.econmod.2017.02.018

- Dao, L. K. O., Loc, H. H., Nguyen, V. C., Hang, L. T. T., & Do, T. T. (2021). Factors affecting the choice of banks: Do bank’s interest rate, employee image and brand matter? Journal of Asian Finance, Economics and Business, 8(1), 457–470. https://doi.org/https://doi.org/10.13106/jafeb.2021.vol8.no1.457

- Dao, L. K. O., Nguyen, T. Y., Hussain, S., & Nguyen, V. C. (2020). Factors affecting non-performing loans of commercial banks: The role of bank performance and credit growth. Banks and Bank Systems, 15(3), 44–54. https://doi.org/http://dx.doi.org/10.21511/bbs.15(3).2020.05

- Jalil, A., Manan, S., & Saleemi, S. (2016). Estimating the growth effects of services sector: A cointegration analysis for Pakistan. Journal of Economic Structures, 5(6). https://doi.org/https://doi.org/10.1186/s40008-016-0037-8

- Juabin, M. (2019). Financial performance analysis of distressed banks in Ghana: Exploration of financial ratios and Z-score. MPRA Paper 97095, University Library of Munich, Germany.

- Klingelhöfer, J., & Sun, R. (2019). Macroprudential policy, central banks and financial stability: Evidence from China. Journal of International Money and Finance, 93, 19–41. https://doi.org/https://doi.org/10.1016/j.jimonfin.2018.12.015

- Le, V. L., & Khuat, D. T. (2017). Cross-ownership among commercial banks in Vietnam after the introduction of Circular 36. State Bank of Vietnam, Available at https://www.sbv.gov.vn/webcenter/portal/vi/menu/rm/apph/tcnh

- Lepetit, L., Nys, E., Rous, P., & Tarazi, A. (2008). Bank income structure and risk: An empirical analysis of European banks. Journal of Banking & Finance, 32(8), 1452–1467. https://doi.org/https://doi.org/10.1016/j.jbankfin.2007.12.002

- Manlagnit, M. C. V. (2011). Cost efficiency, determinants, and risk preferences in banking: A case of stochastic frontier analysis in the Philippines. Journal of Asian Economics, 22(1), 23–35. https://doi.org/https://doi.org/10.1016/j.asieco.2010.10.001

- Mirzaei, A., Liu, G., & Moore, T. (2011). Does Market Structure Matter on Banks’ Profitability and Stability? Emerging versus Advanced Economies. Working Paper No. 11-12. Brunel University London. Available at https://core.ac.uk/download/pdf/29139957.pdf

- Nguyen, M., Skully, M., & Perera, S. (2012). Market power, revenue diversification and bank stability: Evidence from selected South Asian countries. Journal of International Financial Markets, Institutions and Money, 22(4), 897–912. https://doi.org/https://doi.org/10.1016/j.intfin.2012.05.008

- Nguyen, T. N., & Pham, N. H. (2019). Assessing the competitiveness of Vietnamese banks in the context of ASEAN economic integration. Financial & Monetary Market Review. Available at https://thitruongtaichinhtiente.vn/danh-gia-nang-luc-canh-tranh-cua-cac-ngan-hang-viet-nam-trong-boi-canh-hoi-nhap-kinh-te-asean-23703.html

- Nguyen, V. (2020). Human capital, capital structure choice and firm profitability in developing countries: An empirical study in Vietnam. Accounting, 6(2), 127–136. https://doi.org/https://doi.org/10.5267/j.ac.2019.11.003

- Nguyen, V. C., & Do, T. T. (2020). Impact of exchange rate shocks, inward FDI and import on export performance: A cointegration analysis. The Journal of Asian Finance, Economics and Business, 7(4), 163–171. https://doi.org/https://doi.org/10.13106/jafeb.2020.vol7.no4.163

- Ozili, P. K., & Outa, E. (2017). Bank loan loss provisions research: A review. Borsa Istanbul Review, 17(3), 144–163. https://doi.org/https://doi.org/10.1016/j.bir.2017.05.001

- Phan, H. T., Anwar, S., Alexander, W. R. J., & Phan, T. M. H. (2019). Competition, efficiency and stability: An empirical study of East Asian commercial banks. The North American Journal of Economics and Finance, 50, 100990. https://doi.org/https://doi.org/10.1016/j.najef.2019.100990

- Sanya, S., & Wolfe, S. (2011). Can banks in emerging economies benefit from revenue diversification? Journal of Financial Services Research, 40(1–2), 79–101. https://doi.org/https://doi.org/10.1007/s10693-010-0098-z

- Shaddady, A., & Moore, T. (2019). Investigation of the effects of financial regulation and supervision on bank stability: The application of CAMELS-DEA to quantile regressions. Journal of International Financial Markets, Institutions and Money, 58(C), 96–116. https://doi.org/https://doi.org/10.1016/j.intfin.2018.09.006

- Shair, F., Shaorong, S., Kamran, H. W., Hussain, M. S., Nawaz, M. A., & Nguyen, V. C. (2021). Assessing the efficiency and total factor productivity growth of the banking industry: Do environmental concerns matters? Environmental Science and Pollution Research, 28(16), 20822–20838. https://doi.org/https://doi.org/10.1007/s11356-020-11938-y

- Siddika, A., & Haron, R. (2019). Capital regulation and ownership structure on bank risk. Journal of Financial Regulation and Compliance, 28(1), 39–56. https://doi.org/https://doi.org/10.1108/JFRC-02-2019-0015

- State Bank of Vietnam (2014). Press Release on SBV standpoint on NPL ratio of Vietnam’s banking sector. Available at Weekly information on banking operation details, on Feb 24th 2014.

- State Bank of Vietnam (2020). Increasing capital - an urgent need of state-owned commercial banks. Available at http://vnba.org.vn/index.php?option=com_k2&view=item&id=15092:tang-von-nhu-cau-cap-thiet-cua-ngan-hang-thuong-mai-nha-nuoc&lang=vi

- Tan, Y. A., & Floros, C. (2013). Risk, capital and efficiency in Chinese Banking. Journal of International Financial Markets Institutions and Money, 26, 378–393. https://doi.org/https://doi.org/10.1016/j.intfin.2013.07.009

- Tran, V. D., & Foroudi, P. (2020). Assessing the relationship between perceived crowding, excitement, stress, satisfaction, and impulse purchase at the retails in Vietnam. Cogent Business & Management, 7(1), 1858525. https://doi.org/https://doi.org/10.1080/23311975.2020.1858525

- Tran, V. D., & Quang, H. V. (2019). Inspecting the relationship among E-service quality, E-trust, E-customer satisfaction and behavioral intentions of online shopping customers. Global Business & Finance Review (GBFR), 24(3), 29–42. https://doi.org/https://doi.org/10.17549/gbfr.2019.24.3.29

- Uhde, A., & Heimeshoff, U. (2009). Consolidation in banking and financial stability in Europe: Empirical evidence. Journal of Banking & Finance, 33(7), 1299–1311. https://doi.org/https://doi.org/10.1016/j.jbankfin.2009.01.006

- Ullah, S., Akhtar, P., Zaefarian, G. (2018). Dealing with endogeneity bias: The generalized method of moments (GMM) for panel data. Industrial Marketing Management, 71, 69–78. https://doi.org/https://doi.org/10.1016/j.indmarman.2017.11.010

- Wagner, W. (2007). The liquidity of bank assets and banking stability. Journal of Banking & Finance, 31(1), 121–139. https://doi.org/https://doi.org/10.1016/j.jbankfin.2005.07.019

- Wen, S. Y., Yu, J., & Chan, C. H. (2015). Does market structure or financial deepening impact the banking stability? International evidence. Global Economy Journal, 15(3), 353–359. https://doi.org/https://doi.org/10.1515/gej-2014-0046

- Wooldridge, J. M. (2002). Econometric analysis of cross section and panel data. MIT Press.

- Yin, H. (2019). Bank globalization and financial stability: International evidence. Research in International Business and Finance, 49, 207–224. https://doi.org/https://doi.org/10.1016/j.ribaf.2019.03.009