Abstract

The focus of this review is to exhibit a thorough analysis of prominent aspects in bond funds literature and their conceptual developments employing the trending bibliometric analysis. The study was conducted using the Scopus database, which found 354 scholarly documents during a 40-year period spanning from 1982 to 2021, revealing that the amount of research within these fields has a limited presence in the academic literature. The authors, the publications, thematic groups, distribution of keywords, country of publication, trends, and the papers most frequently cited are examined to get an explicit view of the extant research. Thus, the present review identifies the existing knowledge base, examines it, and demonstrates the visualizing patterns to capture the fact-based insight into trending themes in the amphitheater of bond funds. The review further explicitly identifies three research fronts, i.e. performance measures, risk approaches, and bond fund flows. Finally, the findings of the study would be a virtue for researchers, practitioners, and academicians to proceed to further explore the area for an overview of trends and their empirical investigation.

Public Interest Statement

Over the years, the emergence of financial crisis has proven the instability of financial markets. Consequently, various researchers, policymakers, and academicians support the financial environment characterized by strong equity and debt markets. Furthermore, the financial system needs to recognize the importance of the equity and debt market as alternative financial systems so that adequate financial intermediation during financial crises could be handled with ease. It is important to note that the underdevelopment of the bond market threatens the effectiveness of the financial system and creates financial turmoil due to the core reliance on banks and equity markets. Therefore, the studies on the bond market have been a central topic of discussion in the academic literature. However, in the era of capital formation, the flow of funds from mutual funds helps to build strong and resilient bond markets. In this context, this review endeavors to demonstrate an overview of the extant literature on mutual funds that invest in bonds.

1. Introduction

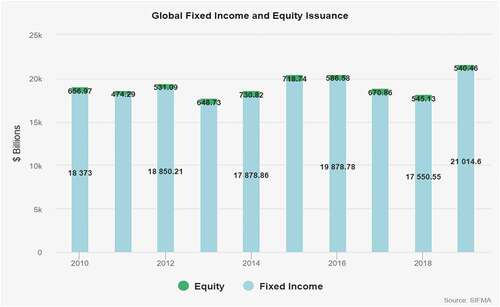

The bond market is a prominent theme in financial markets. The academicians, practitioners, and researchers have emphasized its vital role since the Asian Financial Crisis in 1997–98 (Bhattacharyay, Citation2013). ‘The lack of a spare tire is of no concern if you do not get a flat. East Asia had no spare tires’Footnote1 The Asian Financial crisis engendered a longer and deeper financial turmoil (Bhanoji Rao, Citation2000). One of the fundamental causes for this crisis was recognized as the excessive reliance on domestic banks. This persistent risk could be minimized if more corporate borrowers finance their capital needs through well-diversified portfolios, particularly through bonds. This entails the development of resilient and sustainable domestic local currency bond markets (Aman et al., Citation2020; Bhattacharyay, Citation2013). Data from the recent past demonstrate a significant increase in the long-term bond issuance from 2010 to 2019.Footnote2 Additionally, over a span of a year from 2018 to 2019, the global long-term bond market has witnessed a spur in the issuance by 19.7% to $21 trillion, while the issuance of global equity has decreased by 0.9% to $540.5 billion as shown in the .

Figure 1. Global fixed-income and equity issuance

Corporate bonds have been a topic of discussion for many decades, but the literature on mutual funds predominantly participating in the corporate bond market still stands at an embryonic stage (Bai et al., Citation2019; Choi & Kronlund, Citation2018; Huij & Derwall, Citation2008). There are two major grounds why this review is imperative. First, the potential significance of bond funds can be recognized by looking at some data in the recent past. Over the past three decades, financial data have demonstrated a spur in the growth of mutual funds in the bond market.Footnote3 Interestingly, mutual funds that invest in bonds (i.e., Government and Corporate) have experienced faster growth, and the net assets of bond funds have increased by 94% during the time period 2010 to 2019.Footnote4 Furthermore, 21% of the net assets of worldwide regulated funds are held by bond funds,Footnote5

Second, fund managers’ ability to anticipate future market conditions and timing the securities leave them unique in asset picking, and have a divergent approach towards risk (Alam & Ansari, Citation2020; Bai et al., Citation2019). Researchers and practitioners are of the opinion that mutual funds resort to increase their yields and attempt to surpass the benchmark by buying speculative-grade bonds that result in Reaching-For-YieldFootnote6 (Becker & Ivashina, Citation2015; Choi & Kronlund, Citation2018). These two reasons make this review practically relevant and academically essential.

This review divulges three research areas: a) holdings-based performance measures, b) risk approach of bond funds, and c) bond fund flows. Specifically, a key flow of research has emerged from the USA. However, strong collaborations from European countries are more apparent in the literature.

To analyze the research on bond funds, a bibliometric analytical technique is suggested in the present paper. Bibliometrics gives a more objective and reliable analysis (Aria & Cuccurullo, Citation2017). The goal of the analysis consists of conducting a bibliometric review of all documents in Scopus relevant to bond funds. Using R-tools for a thorough bibliometric analysis that offers a wide assortment of statistical and graphical techniques (R Core Team, Citation2020), this paper intends to identify potential research trends.

The second part includes a review of the literature, which wraps up the important studies on bond funds from diverse phases. The third section considers the objectives of the study. The fourth section discusses the research methodology. The fifth section presents the graphical visualizations, analysis, and interpretation. The sixth section comprises the discussions on the study. The seventh section concludes. The eighth section presents the future scope for research, while the ninth section is entailed with limitations. Finally, the tenth section ends the paper with the managerial implications.

2. Literature review

The study has been undertaken to comprehensively analyze the research work undertaken in the field of bonds. However, the bibliometric results reveal that the academic literature on bond funds is scant vis-à-vis their economic importance (Becker & Ivashina, Citation2015; Choi, Citation2020; Cici & Gibson, Citation2012; Goldstein et al., Citation2017). Furthermore, the results are endowed with the topics on the performance of bond funds, risk approach, and bond fund flows. Therefore, the extant literature on the bond funds presented below is in accordance with the bibliometric results, spread across three diverse disciplines i.e. performance of bond funds, risk approach, and bond fund flows.

The performance of bond mutual funds has been examined through timing and bond selection ability on the part of the bond fund managersFootnote7 (Y. Chen, Ferson, et al., Citation2010). Dietze et al. (Citation2009) empirically examined the performance of bond funds and show evidence that bond funds less exposed to speculative bonds act upon higher risk-adjusted returns. Additionally, bond funds underperform the passive benchmark portfolio post-expenses and this finding can be forerun to support the evidence shown by Christopher et al. (Citation1993), Cici and Gibson (Citation2012), and Y. Chen, Ferson, et al. (Citation2010). In contrast, previous studies on equity funds that support the stock-selection ability, fixed-income fund managers, on average, can not choose corporate bonds that perform better than other bonds with identical characteristics (Cici & Gibson, Citation2012). Polwitoon and Tawatnuntachai (Citation2008) studied the performance of bond mutual funds and showed evidence that bond funds act upon increasing their yield in a low-coupon-rate environment. These findings are consistent with Becker and Ivashina (Citation2015) and Choi and Kronlund (Citation2018), who empirically show that bond funds attempt to surpass the benchmark by buying speculative grade bonds given the above low coupon rate scenario. This act of mutual funds, tilting towards the bonds with higher yields, is termed as “Reaching-for-yield” (Choi & Kronlund, Citation2018). Unlike equity funds, bond funds hold illiquid assets, and their low-interest rate setting has pushed bond funds to “reach-for-yield” by holding illiquid assets (Anand et al., Citation2020; Y. Chen & Qin, Citation2017).

Further, bond funds that entail reaching for yield render comparatively superior returns, but their performance is determined by common risk factors and thus determined fundamentally by risk-taking rather than skill (Choi & Kronlund, Citation2018). However, the unique risk approach of bond mutual funds remains pivotal due to the switching ability of bond funds with regard to the state of the coupon rate (Becker & Ivashina, Citation2015). Thus, to the extent that the differential approach for risk in bond funds, an inclination for high risk or yield differentials stands owing to default and liquidity (Bai et al., Citation2019). It is highly acknowledged that fund flows respond positively to historical performance. In general, the behavior of risk shifting by bond funds deduces a convex flow–performance relationship (Goldstein et al., Citation2017). In contrast, for funds holding illiquid bonds, Q. Chen, Goldstein, et al. (Citation2010) show that the relationship between flow and performance is not always convex, the reason being bond funds have the tendency to possess greater sensitivity of outflows to poor performance when bonds with illiquidity are held, which exhibits a concave flow–performance relationship. Another strand of the literature supports the sensitivity of investor flows to macro frictions and it differs for funds with high yield and speculative-grade bonds (Y. Chen & Qin, Citation2017).

Based on the extant academic literature and practical relevance, this review attempts to answer the following questions:

RQ1. What are the most prominent facets of bond funds literature?

RQ2. What are the principal research topics in bond funds literature?

RQ3. What is the scope for future research in bond funds literature?

3. Objectives

This review endeavors to demonstrate an overview of the extant literature on bond funds. The main objective is disentangled into three categories and achieved. First, the most prominent facets in the bond funds literature are explored. Documents published, authors, affiliations, and sources are explored to demonstrate an overview of the most influential aspects of bond funds literature. As a snapshot of a global overview of the literature and annual scientific production over the sample period, documents with the most citations, the authors with the highest articles, citations and h-index, the most relevant sources and affiliations are analyzed descriptively to explore the prominent dimensions of bond funds literature. Second, the principal areas in the bond funds literature are examined. The conceptual structure, intellectual structure, and social structure are deeply delved into identifying the principal areas in bond funds literature (Aria & Cuccurullo, Citation2017). In particular, word-cloud, co-citation network, thematic map, conceptual structure map, co-occurrence network, and country collaboration map are investigated to attain the second objective. Finally, based on the descriptive, conceptual, intellectual, and social structure analyses, this review attempts to address the future scope and sets the tone for further research.

4. Research methodology

Bibliometrics is a discipline of library and information sciences that studies the characteristics of the research over diverse disciplines quantitatively (Broadus, Citation1987). The library and information sciences, otherwise known as scientometrics, delves into the statistical analysis of research articles, books, and other published works (Nicola, Citation2009). Since the coverage of documents and citations in the Scopus database are noticeably more (Boyack et al., Citation2018), the present bibliometric analysis uses Scopus multidisciplinary database (Okoli, Citation2015). We employ R for the bibliometric analysis to show visualizing patterns of relevant keywords related to bond funds.

4.1. Search strategy and selection criteria

To take into account all the relevant studies and lessen the omission of documents from bond funds, we have used keywords that are explicitly general to cover the overall documents. Keywords such as “Bond Funds” or “Bond Mutual Funds” or “Fixed-income funds” or “Debt Funds” are used to envelop the relevant literature. During the initial search, 364 documents were retrieved from all the fields of Scopus till March 2020. The time frame for the study includes the period between 1982 and 2021. Further, the inclusion criteria followed in the study were as follows:

a) Research documents on the subject areas such as “Business, Management, and Accounting” and “Economics, Econometrics, and Finance” in Scopus were considered.

b) Research documents in English were preferred for the analysis.

After following the inclusion criteria, 354 documents covering 40 years spanning from 1982 to 2021 were used for the bibliometric analysis.

Scientific communication is defined quantitatively in bibliometric analysis creating a framework for the research field with correlations and current themes, for example, in the category of clusters and networks (Small, Citation2006). In this context, a thorough study of research developments can lead to a cautious assessment of the various facets of the scientific environment inherent in bond funds (Biancone et al., Citation2020).

Biblioshiny is an open-source web-based graphical interface of bibliometrics for non-coders that provides interconnection with other R packages with evidence-based quantitative research insight into bond funds that is used in the study (Aria & Cuccurullo, Citation2017). exemplifies the bibliometrix workflow encompassing the data collection, data analysis, and data visualization supporting the science mapping workflow.

Figure 2. Bibliometrix workflow supporting the science mapping

5. Results, analysis, and discussion

Data analysis and interpretation of bond funds literature diverge into two branches, i.e. descriptive and evaluative. These segments explicitly cover all the significant research contributions and demonstrate an enriched visualization for the assessment (Tijssen, Citation2004).

5.1. Descriptive analysis

5.1.1. A global overview on bond funds

The keywords used are, “Bond Funds” or “Bond Mutual Funds” or “Fixed-income funds” or “Debt Funds”. These keywords are explicitly general to broaden the overall theme of the established research (Biancone et al., Citation2020) and results from the Scopus across diverse disciplines reveal paucity in the literature of bond funds. This bibliometric analysis provides a description of the findings in and gives a snapshot of the literature, with a total contribution of 323 publications which were published during the period 1982 and 2021, which includes 191 articles, 10 book chapters, 12 conference papers, and 6 review papers.

Table 1. ummary of bibliometric analysis based on Scopus

5.1.2. Annual scientific production

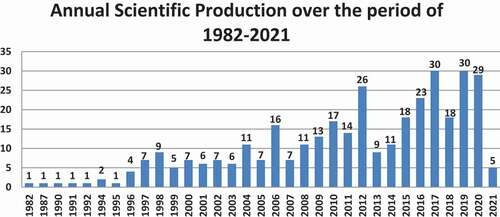

A trend of publications gathered as outlined in demonstrates an acquaintance of publications over time, and on average, there is an increasing trend between the period 1982 and 2021, particularly in 2017 and 2019, the years when 30 articles each were published vis-à-vis all fields of bond funds. Moreover, there are already 5 articles published across diverse fields of bond funds in 2021.

Figure 3. Annual scientific production

5.1.3. Research documents with most number of citations

A research document’s quality is determined by two major indicators (Duque Oliva et al., Citation2006; Rey-Martí et al., Citation2016), first, a number of citations a research document receives, and second, the studies cited in a research document. Among all the Scopus documents chosen shows the top five most cited documents with the name of the publishing house or journal. “The everyday life of global finance: Saving and borrowing in Anglo-America” published by Oxford University Press, authored by Langley (Citation2008) tops the list, with 533 citations in the Scopus database. This work establishes an entrepreneurial approach to the personal finances and concentrates on the unprecedented results that have developed between the society and the financial markets in which he depicts the significant role played by the funds with their popularity as an important avenue for investments, tilting more towards the behavioral approach of finance (Langley, Citation2008).

Table 2. Research documents with the highest number of citations

According to , most cited publications propose a substantial variability in the themes explored. Surprisingly, the results confirm that the top 10 most cited publications are not directly related to bond funds but dedicate a minuscule portion to bond funds in the literature. This demonstration exposes a dearth of the literature on bond funds (Choi & Kronlund, Citation2018).

5.1.4. Prominent authors with their h-index

shows the prominent authors in the bond funds literature and their h index. Hirsch (Citation2005) proposed a novel index for research performance at the micro level, which captures both the visibility and quantity of an author’s work. The Hirsch Index, or h-index, quantify the research output of an individual researcher in a single number (Bornmann & Daniel, Citation2007; Egghe, Citation2006; Egghe & Rousseau, Citation2006; Van Raan, Citation2006). An h index of 30 indicates that a researcher’s publications stand at 30, and each of them has received at least 30 citations. Therefore, the h-index of any researcher can never go down (Sidiropoulos et al., Citation2007); an increase in h-index is expected as new publications come up, as “sleeping beauties” come to life (Van Raan, Citation2004), and as the researcher’s papers attract citations (Hirsch, Citation2005). An h = 0 indicates the inactive authors and absence in the visible impact of their publications (Bornmann & Daniel, Citation2007).

Table 3. Scientific success thresholds based on h index

As stated by Hirsch (Citation2005) “A scientist has index h if h of his or her Np papers have at least h citations each and the other (Np-h) papers have no more than h citations each”. The threshold for the scientific success of researchers as mentioned by Hirsch (Citation2005) is stated in .

From it can be seen that there are five authors with the highest h-index, which means three publications of these authors have at least three citations and the remaining have either 3 or less than 3 citations. It is also evident that there are no prominent authors in this research area in terms of h-index.

Table 4. Authors who have published on bond funds and their h index

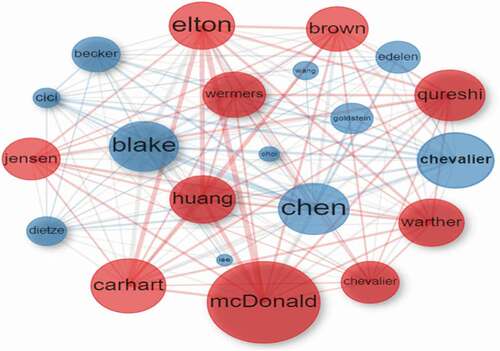

5.1.5. Co-citation network

Co-citation determines the frequency with which two documents are cited together by another research document (Small, Citation1973). The most influential research documents in a particular field determine the strength of the intellectual structure in the bibliometric analysis. Therefore, the more is the frequency of co-citation of two research documents, the more related they are in terms of the broad research arena (Culnan, Citation1987). According to Pilkington and Fitzgerald (Citation2006), the documents with only a few citations are new enough to make any significant impact on the research field; therefore, research documents with at least 10 citations were considered for the co-citation analysis. Further, we follow McCain (Citation1990) and establish a cut-off point for the most influential documents. Therefore, we limit the number of documents to the first 20.

The bubble size in the co-citation network demonstrates the normalized citations received by each research document and the thickness of the lines exemplifies the frequency with which two connected documents are cited together. Further, the color of the bubble indicates the cluster to which the bubble belongs, in particular, the bubbles with the same color belong to one identical cluster. The co-citation network visualizes the theoretical foundations and structures of the bond funds literature. Based on the color of the bubbles and the significance of the documents, we form two clusters and analyze them.

As presented in based on the co-citation network , the co-citation network forms two significant clusters and each cluster is broken down into two sub-clusters, based on the similarity of the references. In light of these clusters, the network demonstrates the battery of both the clusters under the broad umbrella “Mutual Funds”, pointing towards the theoretical background of bond funds research. The references in cluster 1 shred theoretical and empirical evidence on bond funds behavior, particularly, risk approach, bond fund flows, timing ability, and bond selection on the part of bond fund managers. The proposition is that the overall performance of the bond funds increases with an improvement in the ability of the managers to foresee the future. Furthermore, the bond funds literature also suggests the “Reaching-For-Yield” approach, exhibiting the linkage mechanism between speculative-grade bonds and bond funds performance.

Figure 4. Co-Citation network

Table 5. Co-Citation Clusters of representative citations

Similarly, cluster 2 identifies the broader area under which the literature on the bond funds falls. It comprehensively focuses on the references cited together in the bond funds literature focusing on fund flows, risk, and performance of mutual funds. Additionally, the relevant mutual funds literature suggests a theoretical underpinning for the literature on bond funds. However, mutual funds as an area for research has largely made a significant impact on the economy.

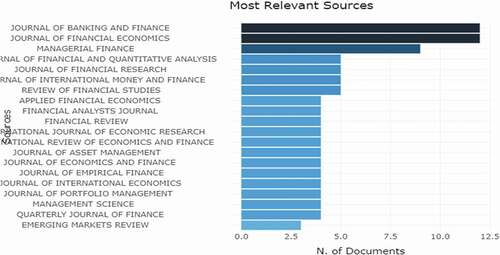

5.1.6. Most relevant sources

As part of the analysis of the prominent themes of bibliometric analysis, major journals with the highest publication of articles vis-à-vis bond funds are gathered and analyzed. presents the list of journals with the highest frequency of publications. This stands extremely vital for deciding which prominent journals to refer to during the review of the literature with a focus on bond funds. According to research influences by the Journal of Banking and Finance and Journal of Financial Economics are significant in bond funds with each having 12 publications. Additionally, the research work on bonds funds has majorly appeared in prominent first quartile journals that are most relevant (Rey-Martí et al., Citation2016).

Figure 5. Journals with the highest frequency of publications

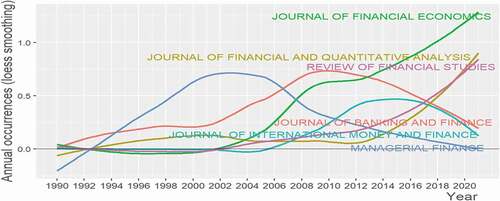

5.1.7. Growth in the journals publication

presents the growth in the publication of the journals from 1990 by employing Loess smoothing that sets the function to assume an unlimited distribution, and enables the function to consider the values below zero; it will demonstrate a better visualization of the results and display the discontinuity in the period of publications (Jacoby, Citation2000). Loess regression or Loess Smoothing shows that the growth in the publication of The Journal of Banking and Finance has declined. However, there has been a massive increase in growth in the Journal of Financial Economics from 2002 which has contributed equally vis-à-vis the Journal of Banking and Finance. Amidst the growth of the Journal of Financial and Quantitative Analysis and Review of Financial Studies, there is a sharp dip in the growth of Managerial Finance and Journal of International Money and Finance.

Figure 6. Growth in the publication of the journal

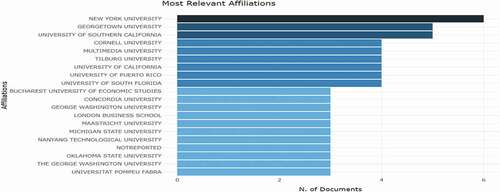

5.1.8. Most relevant affiliations

comprises the most relevant research affiliations in productivity in the identified sample. It can be observed that New York University tops the list with six publications, followed by Georgetown University and the University of Southern California with five publications each. It is evident from that bond funds as an area of research lack emphasis.

Figure 7. Most relevant research affiliations

5.2. Evaluative analysis

5.2.1. Word-cloud of the authors’ keywords

presents the authors’ keywords encircled in the word cloud. It comprises the frequent keywords used by the authors and depicts the trend over time as shown by the loess analysis (Secinaro & Calandra, Citation2021). This establishes the relationships among the major keywords used by the authors, and such keywords are scattered around the most significant keyword “bond funds”. Other vital keywords are endowed with a number of risk measurements, asset pricing, and market microstructure concepts within the nexus. The results are consistent with the major research themes exposed by MCA. However, it is likely to note that the field of bond funds encompasses frequent keywords in the category of performance, market timing, investment strategies, risk, fund flows, and alike. This study reveals the trending themes of research vis-à-vis bond funds and provides fertile ground for future research work.

Figure 8. Word-cloud of authors’ keywords

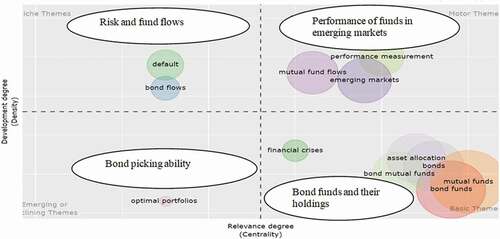

5.2.2. Thematic map of research streams in bond funds

presents the multiple research streams in bond funds literature through the thematic map. The major themes of bond funds are divided into four different quadrants in a two-dimensional graph, in which the x-axis and y-axis represent density and centrality, respectively. The themes placed in the upper-left quadrant (very specialized/niche themes) indicate strongly developed internal ties with insignificant external ties, but such themes lack central importance for the fields such as “default” and “bond flows”. These themes exhibit the risk in exchange for the bond as a tradable instrument in terms of inflows and outflows of bonds held by funds.

Figure 9. Thematic map of research streams in bond funds

Themes placed in the upper-right quadrant (motor-themes) present well-developed and significant structured research fields such as “performance measurement” and “mutual fund flows” and “emerging markets” and “investor redemption”. These themes explicitly cover funds’ performance in emerging markets.

Themes set in the lower-left quadrant (emerging or disappearing themes) indicate that the themes are at the infancy stage of development with marginal importance, majorly demonstrating either promising or disappearing themes such as “optimum portfolios”. Notably, these themes capture the bond picking ability of funds. Themes placed in the lower-right quadrant (basic themes) are significant for the research field but less developed; therefore, this quadrant assembles transversal and basic themes such as “bond funds” and “mutual funds” and “bond mutual funds” and “asset allocation” and “bonds” and “financial crises”. This quadrant in particular enfolds the significance of bond funds and their holdings.

The thematic map is highly intuitive and sets the basis for analysis of different quadrants in which themes are placed (Cobo et al., Citation2011; Esfahani et al., Citation2019). It demonstrates that for better outcomes researchers can merge their research focus with “performance measurement” and “mutual fund flows” and “emerging markets” and “investor redemption” that are important topics in this field but not well developed (Cobo et al., Citation2011; Esfahani et al., Citation2019; Nasir et al., Citation2021).

The net bond fund flows surpassed 2.0 trillion USD at the global level during the time period 2007–2006 and this dramatic increase has doubled the total Assets Under Management (AUM) of bond mutual funds.Footnote8 In this context, the performance of mutual funds in general and bond mutual funds, in particular, have been a central topic in academic research. A body of empirical literature examines the performance of bond funds and divides the drivers of performance into two parts. First, the bond picking ability of the fund managers is seen as an important driver of the performance of bond mutual funds. Additionally, it is empirically evident that the bond funds act upon Reaching-For-Yield (RFY), particularly, preference over speculative-grade bonds often results in the aforementioned scenario (Choi & Kronlund, Citation2018). Second, the timing ability plays a major role in the strengthening of the bond funds’ performance (Y. Chen, Ferson, et al., Citation2010). This strategic position makes the manager futuristic and thus the manager can maneuver superior information on the subject of the future realizations of common factors that affect bond market returns. Further, Zhu (Citation2021) proposes that the increasing presence of bond mutual funds and their effect on firms’ corporate finance decisions influence the soundness of the bond fund flows. Consequently, they show evidence that the issue policies of the corporate firms held in the portfolio of bond funds are majorly affected by the flow to bond funds. Yet, the academic literature on bond funds in light of these facts seems to have been neglected in emerging economies.

Cici and Gibson (Citation2012) delve deeper into examining the fund's performance employing security-level holdings. They observed that the active management cost, on average, was found to be greater than the benefits. However, this contrasts with the evidence shown in the extant literature on equity funds. Therefore, a possible future research gap would be to identify the key differences in the active management of bond funds and equity funds.

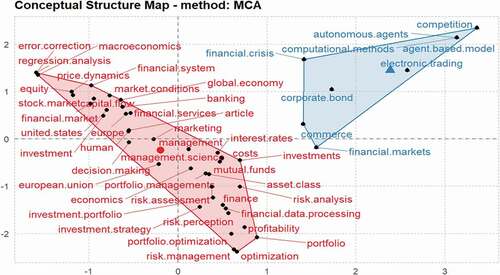

5.2.3. Structure map developed from the multiple correspondence analysis

Bibliometric analysis is not restricted to analyze merely the keywords, but also the important terms in the articles’ abstracts and titles. It does so utilizing either network analysis or Correspondence Analysis (CA) or Multiple Correspondence Analysis (MCA). CA and MCA present visualizations of the conceptual structure of a two-dimensional plot (Aria & Cuccurullo, Citation2017). Here, MCA is used to draw a conceptual structure of the field to discover clusters of documents that articulate common concepts, and the results are plotted on a two-dimensional map (Aria & Cuccurullo, Citation2017).

The conceptual structure map developed from the multiple correspondence analysis brings together the keywords, taking into consideration their homogeneity within the network. presents the division of the common keywords grouped into two clusters.

Figure 10. Structure map developed from the multiple correspondence analysis

Cluster 1 to the left of the conceptual structure map has shown the keywords that are most commonly used in the research articles with common research themes. Keywords such as “Capital flow” and “price dynamics” and “risk assessment” and “risk perception” and “interest rate” and “market conditions”. These articles with a broader phenomenon towards the bond funds discuss the need for a proper examination of pricing and risk assessment of bond funds based on the enormity of their impact on financial markets (L. Chen, Lesmond, et al., Citation2007; Gorton & Pennacchi, Citation1990; Longstaff, Citation2004; Mukherjee, Citation2019). On the other hand, cluster 2 to the right of the conceptual structure map presents the keywords such as “corporate bond” and “electronic trading” and “autonomous agents” and “financial crisis” and “agent-based model”. These keywords indicate that the market microstructure’s task is to provide insight and valuable information to traders and portfolio managers so that the best possible market prices are captured—thus reducing the performance drag and improving portfolio returns (Khandani & Lo, Citation2011; Tripathi et al., Citation2019).

The keywords that are close to the center within both the clusters point out that they have gained a high degree of research coverage in recent years; nearer are the keywords to the edge of the clusters, narrower is the research theme (Aria & Cuccurullo, Citation2017).

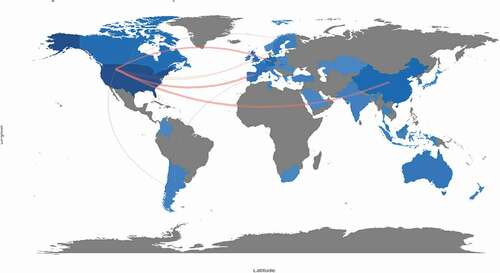

5.2.4. Country collaboration map

Collaboration network maps shown among countries resulted from bond funds bibliometric analysis. In light blue demonstrates the countries with low productivity, while dark blue denotes countries with high productivity, and the thickness of the red link represents the collaboration frequency; the thicker are the links from one country to the other, the more is the frequency of collaboration. The US has the most frequent research collaboration links with China, Spain, Germany, and Argentina and neutral research collaborations with Norway and Sweden. Argentina and Spain also show some research collaborations. Scientific production and research collaborations between Asian and European institutes are scant. The US authors collaborate more with European institutions but not with Asian institutions except China (Nasir et al., Citation2021).

Figure 11. Country collaboration map

6. Discussion

This review proposes a comprehensive overview of bond funds literature. The potential significance of bond mutual funds and their exponential development over many years is in fame in financial markets. However, the academic literature remains at a nascent stage. This study, particularly employing descriptive and evaluative bibliometric measures, throws light on the global overview of extant academic literature on bond funds. The descriptive analysis demonstrates paucity in the total academic contribution to bond funds. Interestingly, the results exhibit remarkable growth in the recent past since 2017, particularly, during the period 2017 and 2020, when there were 107 academic contributions to bond funds. The study further reveals that there is no prominent article/book that directly adds to bonds funds literature in terms of the highest number of citations. The most prominent articles on bond funds such as “The Performance of Bond Mutual Fund” (Christopher et al., Citation1993), “Reaching for Yield in the Bond Market” (Becker & Ivashina, Citation2015) have been precluded in the top 5 most cited documents in Scopus. It is evident that “Journal of Banking and Finance” and “Journal of Financial Economics” are the major sources that have been published on bond funds and these sources remain as the major gateways to explore further on bond funds. Additionally, results show that the highest h-index of authors who have contributed to the bond funds stands at three.

The evaluative analysis comprising word cloud, thematic map and conceptual structure map demonstrate the amount of research within bond funds fields. The development of a strong bond market would help in building a strong capitalist system for various financial activities which will help in managing risk at both micro and macro levels. In this context, the results also show the relevance of bond funds concerning the bond market development over time. It is likely to be noted that the field of bond funds encompasses subjects that connect performance, risk approach, and bond funds flow, and that these concepts remain identical in each type of evaluative analysis. However, anecdotal evidence reiterates that the majority of the emerging Asian economies’ corporate bond market capitalization lies between 20% and 33% or less than that of developed economies (Smaoui et al., Citation2017). Therefore, in the emerging Asian markets, fixed income markets in general and corporate bond markets, in particular, are in the initial development stage. Given the absence of well-developed bond markets, bond funds will not find good investment opportunities. Despite the magnitude of the financial and economic importance of bond funds, the literature is at an infancy stage in its understanding of the holdings of bond funds compared with the vast literature on equity funds (Choi & Kronlund, Citation2018; Cici & Gibson, Citation2012). A major reason behind this paucity of the literature many a time stands owing to the lack of comprehensive data on holdings and pricing of such holdings (Choi & Kronlund, Citation2018). Therefore, it is inferred that the field of bond funds is more niche than the field of equity funds, as both are the byproducts of mutual funds. Finally, a conclusion is then reached, demonstrating that the field of bond funds has turned into an important arena in research.

7. Conclusions

In the wake of bond funds’ vital role in financial markets, this study explores the diverse literature spread across different themes with a focus on 354 high-quality research contributions, covering the period from 1972 to 2021. The present review endeavors to uncover the different dimensions and presents an overview of the extant bond funds literature. All the selected documents are from Scopus with four keywords that are explicitly general to widen the overall picture of the established research. This study presents the visualization of the bibliometric network and classifies the research overview into an evaluative and analytical approach. An assessment of the trends in publications in a particular journal, theme, author, institution, and country are looked into and compared.

It is noted that the emerging literature on bond funds over the study period is dedicated to the developed markets, predominantly the US market. In the context of promising economies such as India and Russia, the literature on bond funds shows paucity. This review identifies the gaps in the established literature and provides future directions for research in bond funds. This includes the discussions on the holdings-based performance measures, risk approaches for bond funds, and bond fund flows and offers vivid directions for researchers to conjunct with the vacuum themes. Finally, a conclusion is then reached, despite its financial and economic importance; bond funds have a limited presence in the academic literature. Therefore, the area of bonds leaves a broader phenomenon for further research.

8. Scope for future research

8.1. Based on the descriptive and evaluative review

Based on the descriptive and evaluative bibliometric review, the significant themes revealed are analyzed and presented in line with the relevant extant literature. Therefore, the future scope for research is classified and addressed according to the prominent themes divulged by this review. Thus, the following research domains are proposed for the future:

The extant literature on the performance of bond funds lacks holdings-based measures at both aggregate and security levels, unlike studies in equity funds (K. J. M. Cremers & Petajisto, Citation2009; M. Cremers et al., Citation2016; Cici & Gibson, Citation2012). This presents an interesting opportunity to provide an appropriate holdings-based measure to understand the costs and benefits involved in the management of active bond funds.

The literature has prominent contributions towards the determinants of credit risk predominantly in the corporate bond market (L. L. Chen et al., Citation2007; Collin-Dufresne et al., Citation2001; Darwin et al., Citation2012; Elton et al., Citation2001; Haddad & Hakim, Citation2007; Landschoot, Citation2008; Mukherjee, Citation2019; Rodrigues & Agarwal, Citation2012; Thakur et al., Citation2018). The ability of the fund managers to predict the future market conditions and timing of the securities demonstrate a differential approach to bond funds towards the credit risk (Alam & Ansari, Citation2020; Bai et al., Citation2019). Thus, to the extent of the existence of a differential approach for risk in bond funds, it becomes imperative to determine the determinants of credit risk in the amphitheater of bond funds.

A constant change in the landscape across financial institutions, one of the leading trends of recent times is the increasing growth of assets under management by bond funds, i.e., mutual funds investing in bonds (Feroli et al., Citation2014). Further, poor performance caused by the outflows in the funds tends to outperform the performance rendered by inflows: outflows are more sensitive to bad performance (Y. Chen, Goldstein, et al., Citation2010). Therefore, funds can employ different mechanisms to alleviate the magnitude of outflows. These include maintaining the cash buffers (Chernenko & Sunderam, Citation2020), restricting redemptions, or altering the formula for net asset value (NAV) determinations when there are redemption requests. An understanding of the outline of outflows in bond funds in the financial system and their externalities to market prices and real economic activity calls for more research in the future (Goldstein et al., Citation2017).

Furthermore, a weakening performance of bond funds results in large investor outflows, and funds resort to fire sales by disposing the illiquid securities to meet the immediate redemption requests (Goldstein et al., Citation2017). Therefore, these numerous distinct features offer an advantageous setting to study the investor flows (Y. Chen & Qin, Citation2017). Additionally, a lack of cash holdings would have negative repercussions on the performance of funds. Whether poor performance can be overcome through mandated cash buffers would be a research opportunity (Choi et al., Citation2020).

The bond funds divulge in risk-taking particularly to recuperate from poor performance (Choi & Kronlund, Citation2018). In general, the flow–performance relationship is convex when bond funds engage in risk-shifting (Chevalier & Ellison, Citation1997). In contrast, some studies in the recent past show that bond funds with illiquid bonds tend to show a concave flow–performance relationship (Y. Chen, Goldstein, et al., Citation2010; Goldstein et al., Citation2017). Thus, shifting of risk may not be beneficial for the bond funds with poor performance if potential liquidation due to performance-driven outflows is costly (Choi & Kronlund, Citation2018). Whether corporate bond funds with poor performance take higher risk for high returns would be a potential area for research.

8.2. Based on the status of the corporate bond market

As stated, a developed corporate bond market is the key to attract investments from various sources. Additionally, developed bond markets are often associated with stronger macroeconomic fundamentals, stable financial systems, a strong institutional framework, and more open economies (Barry Eichengreen & Luengnaruemitchai, Citation2004). Further, corporate and sovereign bonds are highly demanded by Institutional Investors (Smaoui et al., Citation2017). However, in emerging markets, it looks no better. In this context, the paucity in the literature on bond funds can be attributed to the underdeveloped corporate bond markets. Therefore, this study identifies the following key research gaps to penetrate the growth of bond markets across the developing economies.

The extensive literature demonstrates that the developed bond markets help in diversifying the risk. This is because bond returns are either negatively correlated or uncorrelated to the returns of asset portfolios of stocks and other asset portfolios, which in turn, reduces the portfolio variance (Smaoui et al., Citation2017). Since the developed bond markets can pave the way for the development of fund houses, one closely related research gap is how to penetrate the growth of the bond market and identify the determinants to promote and develop the corporate bond market.

The domestic investors in bonds including bond fund houses—understand the domestic issuers better and are more comfortable with the examination of their credit and macroeconomic risk. Surprisingly, empirical shreds of evidence posit a deleveraging trend in which issuers barely choose to employ debt over internal and equity capital, particularly in Asia (Chauhan, Citation2017). A piece of forward-looking evidence for the following questions may contribute to the extant literature.

a) From the issuers’ perspective: Are there any constraints to substitute equity by raising debt?

b) From the investors’ perspective: What are the key impediments that govern the perceived behavior of investors towards investing in corporate bonds?

9. Limitations of the study

Nevertheless, this bibliometric review presents a snapshot of the research publications across the globe on bond funds, and a sincere attempt has been made to carry out the bibliometric analysis in the best manner possible; the review has some limitations. First, the results obtained from the review cannot be generalized as this study encompasses the research documents only in the Scopus database. For this reason, the Scopus database alone does not ensure the coverage of all relevant documents and the highest quality standards. Second, the analysis was carried out employing biblioshiny as an analytical tool. Therefore, the obtained results should be treated with caution for accuracy.

10. Managerial implications

The review was undertaken with the view that for the last 40 years, mutual funds investments in corporate bonds and other fixed-income securities have been exponentially increasing across the globe. Alongside contributing to the academic literature, the overall results of the study embrace various considerations that should be looked into by the managers and practitioners. The highlighted themes in the review show the nexus among the performance of bond funds and other related parameters such as risk, determinants of risk, and bond fund flows. The results reveal that the performance of bond funds can be enhanced by identifying the nature of flow of funds, risk due to illiquid bonds, and ameliorating the ability to time the securities.

Acknowledgements

The authors are grateful to the editors and reviewers for their constructive input.

Disclosure statement

The authors declare no conflict of interest.

Additional information

Funding

Notes on contributors

Suman Chakraborty

Mr. Lithin B M (First Author) is a Junior Research Fellow. His area of research is corporate finance and is currently pursuing his Ph.D. from the Manipal Academy of Higher Education, Manipal, India.

Dr. Suman Chakraborty (Corresponding Author) has over 20 years of experience in teaching and research in India. He is working as an Associate Professor at the Department of Commerce, Manipal Academy of Higher Education, India. Dr. Chakraborty’s research areas are Corporate Finance, Financial Markets, and Business Valuation.

Dr. Bidyut Kumar Ghosh (Co-Author) is an Associate Professor at the Department of Commerce, Manipal Academy of Higher Education, India. Dr. Ghosh’s research areas are Agricultural Economics, Financial Economics, Tourism Economics, and Development Economics.

Mr. Ravindra Shenoy (Co-Author) is an Assistant Professor (Senior Scale) at the Department of Commerce, Manipal Academy of Higher Education, India. His research areas are Corporate Finance, Vedic Management, Consumer Behaviour, and Marketing Management.

Notes

1. Remarks by Chairman Alen Greenspan at Financial Markets Conference of the Federal Reserve Bank of Atlanta on 19 October 1999.

2. Statistics from Securities Industry and Financial Markets Association’s (SIFMA) 2020 capital markets Factbook. SIFMA factbook 2019 shows the data on the significant growth in the size of the corporate bond market which accounted for an 80% increase between the period 2008 and 2018, alongside significant growth in the mutual funds and Exchange Traded Funds (ETFs) that invest in corporate bonds.

3. Investment Company Institute(ICI) data show that the total share of mutual funds and Exchange Traded funds in the corporate bond market has increased from 7.3% to 17.9% between the period 2006 and 2016 (Anand et al., Citation2020).

4. Investment Company Institute (ICI) data show that net assets of worldwide regulated funds have substantially increased from $6.1 trillion to $11.8 trillion between the time period 2010 and 2019.

5. Investment Company Institute data show that net assets in worldwide regulated funds increased by $8.2 trillion to $54.9 trillion of which the growth rate of bond funds from 2018 to 2019 stood at 17%.

6. Kirsten Grind, wall street journal 2012, Bond funds get aggressive.

7. Timing ability on the fund manager’s part is the preparedness to maneuver superior information on the subject of the future realizations of common factors that affect bond market returns. Bond picking ability refers to the utilizing of bond-specific information.

8. Investment Company Institute Factbook, 2017.

References

- Alam, M., & Ansari, V. A. (2020). Do mutual fund managers‘ possess style liquidity timing abilities? International Journal of Emerging Markets. Advance online publication. https://doi.org/https://doi.org/10.1108/IJOEM-02-2020-0195

- Aman, A., Isa, M. Y., & Naim, A. M. (2020). The role of macroeconomic and financial factors in bond market development in selected countries. Global Business Review, 097215092090720. Advance online publication. https://doi.org/https://doi.org/10.1177/0972150920907206

- Anand, A., Jotikasthira, C., & Venkataraman, K. (2020). Mutual fund trading style and bond market fragility. The Review of Financial Studies. Advance online publication. https://doi.org/https://doi.org/10.1093/rfs/hhaa120

- Aria, M., & Cuccurullo, C. (2017). bibliometrix : An R-tool for comprehensive science mapping analysis. Journal of Informetrics, 11(4), 959–21. https://doi.org/https://doi.org/10.1016/j.joi.2017.08.007

- Bai, J., Bali, T. G., & Wen, Q. (2019). Common risk factors in the cross-section of corporate bond returns. Journal of Financial Economics, 131(3), 619–642. https://doi.org/https://doi.org/10.1016/j.jfineco.2018.08.002

- Becker, B., & Ivashina, V. (2015). Reaching for yield in the bond market. The Journal of Finance, 70(5), 1863–1902. https://doi.org/https://doi.org/10.1111/jofi.12199

- Bhanoji Rao, V. V. (2000). The East Asian Crisis of 1997-98: Implications for India. Global Business Review, 1(1), 1–10. https://doi.org/https://doi.org/10.1177/097215090000100101

- Bhattacharyay, B. N. (2013). Determinants of bond market development in Asia. Journal of Asian Economics, 24, 124–137. https://doi.org/https://doi.org/10.1016/j.asieco.2012.11.002

- Biancone, P. P., Saiti, B., Petricean, D., & Chmet, F. (2020). The bibliometric analysis of Islamic banking and finance. Journal of Islamic Accounting and Business Research, 11(9), 2069–2086. https://doi.org/https://doi.org/10.1108/JIABR-08-2020-0235

- Bornmann, L., & Daniel, H. D. (2007). What do we know about the h index? Journal of the American Society for Information Science and Technology, 58(9), 1381–1385. https://doi.org/https://doi.org/10.1002/asi.20609

- Boyack, K. W., Jan, N., Eck, V., Colavizza, G., & Waltman, L. (2018). Characterizing in-text citations in scientific articles: A large-scale analysis. Journal of Informetrics, 12(1), 59–73. https://doi.org/https://doi.org/10.1016/j.joi.2017.11.005

- Broadus, R. N. (1987). Toward a definition of “bibliometrics”. Scientometrics, 12(5–6), 373–379. https://doi.org/https://doi.org/10.1007/BF02016680

- Brown, S. J., & Goetzmann, W. N. (1997). Mutual fund styles. Journal of Financial Economics, 43(3), 373–399. https://doi.org/https://doi.org/10.1016/S0304-405X(96)00898-7

- Carhart, M. M. (1997). On persistence in mutual fund performance. The Journal of Finance, 52(1), 57–82. https://doi.org/https://doi.org/10.1111/j.1540-6261.1997.tb03808.x

- Chauhan, G. S. (2017). Corporate financing and deleveraging of firms in India. IIMB Management Review, 29(3), 170–187. https://doi.org/https://doi.org/10.1016/j.iimb.2017.06.002

- Chen, L., Lesmond, D. A., & Wei, J. (2007). Corporate yield spreads and bond liquidity. The Journal of Finance, 62(1), 119–149. https://doi.org/https://doi.org/10.1111/j.1540-6261.2007.01203.x

- Chen, Q., Goldstein, I., & Jiang, W. (2010). Payoff complementarities and financial fragility: Evidence from mutual fund outflows. Journal of Financial Economics, 97(2), 239–262. https://doi.org/https://doi.org/10.1016/j.jfineco.2010.03.016

- Chen, Y., Ferson, W., & Peters, H. (2010). Measuring the timing ability and performance of bond mutual funds. Journal of Financial Economics, 98(1), 72–89. https://doi.org/https://doi.org/10.1016/j.jfineco.2010.05.009

- Chen, Y., & Qin, N. (2017). The behavior of investor flows in corporate bond mutual funds. Management Science, 63(5), 1365–1381. https://doi.org/https://doi.org/10.1287/mnsc.2015.2372

- Chernenko, S., & Sunderam, A. (2020). Measuring the perceived liquidity of the corporate bond market. SSRN Electronic Journal. https://doi.org/https://doi.org/10.2139/ssrn.3583872

- Chevalier, J., & Ellison, G. (1997). Risk taking by mutual funds as a response to incentives. Journal of Political Economy, 105(6), 1167–1200. https://doi.org/https://doi.org/10.1086/516389

- Choi, J., Hoseinzade, S., Shin, S. S., & Tehranian, H. (2020). Corporate bond mutual funds and asset fire sales. Journal of Financial Economics, 138(2), 432–457. https://doi.org/https://doi.org/10.1016/j.jfineco.2020.05.006

- Choi, J., & Kronlund, M. (2018). Reaching for yield in corporate bond mutual funds. The Review of Financial Studies, 31(5), 1930–1965. https://doi.org/https://doi.org/10.1093/rfs/hhx132

- Christelis, D., Jappelli, T., & Padula, M. (2010). Cognitive abilities and portfolio choice. European Economic Review, 54(1), 18–38. https://doi.org/https://doi.org/10.1016/j.euroecorev.2009.04.001

- Christopher, R., Blake, E. J. E., & G, M. J. (1993). The performance of bond mutual fund. The Journal of Business, 66(3), 371–403. https://www.jstor.org/stable/2353206

- Cici, G., & Gibson, S. (2012). The performance of corporate bond mutual funds: Evidence based on security-level holdings. The Journal of Financial and Quantitative Analysis, 47(1), 537–565. https://doi.org/https://doi.org/10.1017/S0022109011000640

- Cobo, M. J., López-Herrera, A. G., Herrera-Viedma, E., & Herrera, F. (2011). An approach for detecting, quantifying, and visualizing the evolution of a research field: A practical application to the Fuzzy Sets Theory field. Journal of Informetrics, 5(1), 146–166. https://doi.org/https://doi.org/10.1016/j.joi.2010.10.002

- Collin-Dufresne, P., Goldstein, R. S., & Martin, J. S. (2001). The determinants of credit spread changes. The Journal of Finance, 56(6), 2177–2207. https://doi.org/https://doi.org/10.1111/0022-1082.00402

- Core Team, R. (2020). R: A language and environment for statistical computing. R Foundation for Statistical Computing. https://www.r-project.org/.

- Cremers, K. J. M., & Petajisto, A. (2009). How active is your fund manager? A new measure that predicts performance. Review of Financial Studies, 22(9), 3329–3365. https://doi.org/https://doi.org/10.1093/rfs/hhp057

- Cremers, M., Ferreira, M. A., Matos, P., & Starks, L. (2016). Indexing and active fund management: International evidence. Journal of Financial Economics, 120(3), 539–560. https://doi.org/https://doi.org/10.1016/j.jfineco.2016.02.008

- Culnan, M. J. (1987). Mapping the intellectual structure of MIS, 1980-1985: A co-citation analysis. MIS Quarterly: Management Information Systems, 11(3), 341–350. https://doi.org/https://doi.org/10.2307/248680

- Da, Z., Engelberg, J., & Gao, P. (2015). The sum of all FEARS investor sentiment and asset prices. Review of Financial Studies, 28(1), 1–32. https://doi.org/https://doi.org/10.1093/rfs/hhu072

- Darwin, T., Treepongkaruna, S., & Faff, R. (2012). Determinants of bond spreads: Evidence from credit derivatives of Australian firms. Australian Journal of Management, 37(1), 29–46. https://doi.org/https://doi.org/10.1177/0312896211416137

- Dietze, L. H., Entrop, O., & Wilkens, M. (2009). The performance of investment grade corporate bond funds: Evidence from the European market. The European Journal of Finance, 15(2), 191–209. https://doi.org/https://doi.org/10.1080/13518470802588841

- Duque Oliva, E. J., Cervera Taulet, A., & Rodríguez Romero, C. (2006). A bibliometric analysis of models measuring the concept of perceived quality in providing internet service. Innovar, 16(28), 223–243. https://scholar.google.com/scholar_lookup?title=A%20bibliometric%20analysis%20of%20models%20measuring%20the%20concept%20of%20perceived%20quality%20inproviding%20internet%20service&author=E.J.%20Duque%20Oliva&publication_year=2006&pages=223-243

- Egghe, L. (2006). Theory and practise of the g-index. Scientometrics, 69(1), 131–152. https://doi.org/https://doi.org/10.1007/s11192-006-0144-7

- Egghe, L., & Rousseau, R. (2006). An informetric model for the Hirsch-index. Scientometrics, 69(1), 121–129. https://doi.org/https://doi.org/10.1007/s11192-006-0143-8

- Eichengreen, B., & Luengnaruemitchai, P. (2004). Why doesn’t Asia have bigger bond markets? In BIS Papers No 30 (2006) (Ed.), Asian bond markets: issues and prospects (pp. 40–77). Basel, Switzerland: Monetary and Economic Department, Bank of International Settlements.

- Elton, E. J., Gruber, M. J., Agrawal, D., & Mann, C. (2001). Explaining the rate spread on corporate bonds. The Journal of Finance, LVI(1), 21–51. https://doi.org/https://doi.org/10.1142/9789814335409_0003

- Elton, E. J., Gruber, M. J., & Blake, C. R. (1995). Fundamental economic variables, expected returns, and bond fund performance. The Journal of Finance, 50(4), 1229–1256. https://doi.org/https://doi.org/10.1111/j.1540-6261.1995.tb04056.x

- Esfahani, H. J., Tavasoli, K., & Jabbarzadeh, A. (2019). Big data and social media: A scientometrics analysis. International Journal of Data and Network Science, 3(3), 145–164. https://doi.org/https://doi.org/10.5267/j.ijdns.2019.2.007

- Feroli, M., Kashyap, A. K., Schoenholtz, K. L., & Shin, H. S. (2014). Market Tantrums and Monetary Policy (February 1, 2014) (Chicago Booth Research Paper No. 14-09). Retrieved from SSRN: https://doi.org/http://dx.doi.org/10.2139/ssrn.2409092

- Goldstein, I., Jiang, H., & Ng, D. T. (2017). Investor flows and fragility in corporate bond funds. Journal of Financial Economics, 126(3), 592–613. https://doi.org/https://doi.org/10.1016/j.jfineco.2016.11.007

- Gorton, G., & Pennacchi, G. (1990). Financial Intermediaries and Liquidity Creation. The Journal of Finance, 45(1), 49–71. https://doi.org/https://doi.org/10.1111/j.1540-6261.1990.tb05080.x

- Haddad, M. M., & Hakim, S. (2007). The cost of sovereign lending in the Middle East after September 11. Journal for Global Business Advancement, 1(1), 127–139. https://doi.org/https://doi.org/10.1504/JGBA.2007.012566

- Hirsch, J. E. (2005). An index to quantify an individual’s scientific research output. Proceedings of the National Academy of Sciences of the United States of America, 102(46), 16569–16572. https://doi.org/https://doi.org/10.1073/pnas.0507655102

- Huang, J., Wei, K. D., & Yan, H. (2007). Participation costs and the sensitivity of fund flows to past performance. The Journal of Finance, 62(3), 1273–1311. https://doi.org/https://doi.org/10.1111/j.1540-6261.2007.01236.x

- Huij, J., & Derwall, J. (2008). “Hot Hands” in bond funds. Journal of Banking & Finance, Elsevier, 32(4), 559–572. https://doi.org/https://doi.org/10.1016/j.jbankfin.2007.04.023

- Jacoby, W. G. (2000). Loess: - a nonparametric, graphical tool for depicting relationships between variables. Electoral Studies, 19(4), 577–613. https://doi.org/https://doi.org/10.1016/S0261-3794(99)00028-1

- Jensen, M. C. (1968). The performance of mutual funds in the period 1945–1964. The Journal of Finance, 23(2), 389–416. https://doi.org/https://doi.org/10.1111/j.1540-6261.1968.tb00815.x

- Khandani, A. E., & Lo, A. W. (2011). Illiquidity premia in asset returns: An empirical analysis of hedge funds, mutual funds, and US equity portfolios. Quarterly Journal of Finance, 1(2), 205–264. https://doi.org/https://doi.org/10.1142/S2010139211000080

- Landschoot, A. V. (2008). Determinants of yield spread dynamics: Euro versus US dollar corporate bonds. Journal of Banking and Finance, 32(12), 2597–2605. https://doi.org/https://doi.org/10.1016/j.jbankfin.2008.05.011

- Langley, P. (2008). The everyday life of global finance: Saving and borrowing in Anglo-America. Oxford University Press. https://doi.org/https://doi.org/10.1093/acprof:oso/9780199236596.001.0001

- Longstaff, F. A. (2004). The flight-to-liquidity premium in U.S. Treasury bond prices. The Journal of Business, 77(3), 511–526. https://doi.org/https://doi.org/10.1086/386528

- McCain, K. W. (1990). Mapping authors in intellectual space: A technical overview. Journal of the American Society for Information Science, 41(6), 433–443. https://doi.org/https://doi.org/10.1002/(SICI)1097-4571(199009)41:6<433::AID-ASI11>3.0.CO;2-Q

- McDonald, J. G. (1974). Objectives and performance of mutual funds, 1960-1969. The Journal of Financial and Quantitative Analysis, 9(3), 311–333. https://doi.org/https://doi.org/10.2307/2329866

- Mukherjee, K. N. (2019). Demystifying yield spread on corporate bonds trades in India. Asia-Pacific Financial Markets, 26(2), 253–284. Springer Japan. https://doi.org/https://doi.org/10.1007/s10690-018-09266-w

- Nasir, A., Farooq, U., & Khan, A. (2021). Conceptual and influential structure of Takaful literature: A bibliometric review. International Journal of Islamic and Middle Eastern Finance and Management, 14(3), 599–624. https://doi.org/https://doi.org/10.1108/IMEFM-04-2020-0192

- Nicola, D. B. (2009). Bibliometrics and citation analysis. USA: Scarecrow Press, Inc.

- Okoli, C. (2015). A guide to conducting a standalone systematic to cite this version : A guide to conducting a standalone systematic literature review. Communications of the Association for Information Systems, 37(1), 879–910. https://doi.org/https://doi.org/10.17705/1CAIS.03743

- Pilkington, A., & Fitzgerald, R. (2006). Operations management themes, concepts and relationships: A forward retrospective of IJOPM. International Journal of Operations & Production Management, 26(11), 1255–1275. https://doi.org/https://doi.org/10.1108/01443570610705854

- Polwitoon, S., & Tawatnuntachai, O. (2008). Emerging market bond funds: A comprehensive analysis. The Financial Review, 43(1), 51–84. https://doi.org/https://doi.org/10.1111/j.1540-6288.2007.00186.x

- Qureshi, F., Ismail, I., & Chan, S. G. (2017). Mutual funds and market performance: New evidence from ASEAN markets. Investment Analysts Journal, 46(1), 61–79. https://doi.org/https://doi.org/10.1080/10293523.2016.1253137

- Rey-Martí, A., Ribeiro-Soriano, D., & Palacios-Marqués, D. (2016). A bibliometric analysis of social entrepreneurship. Journal of Business Research, 69(5), 1651–1655. https://doi.org/https://doi.org/10.1016/j.jbusres.2015.10.033

- Rodrigues, M., & Agarwal, V. (2012). The performance of structural models in pricing credit spreads. SSRN Electronic Journal, 44. https://doi.org/https://doi.org/10.2139/ssrn.1929177

- Secinaro, S., & Calandra, D. (2021). Halal food: Structured literature review and research agenda. British Food Journal, 123(1), 225–243. https://doi.org/https://doi.org/10.1108/BFJ-03-2020-0234

- Sidiropoulos, A., Katsaros, D., & Manolopoulos, Y. (2007). Generalized Hirsch h-index for disclosing latent facts in citation networks. Scientometrics, 72(2), 253–280. https://doi.org/https://doi.org/10.1007/s11192-007-1722-z

- Small, H. (1973). Co-citation in the scientific literature: A new measure of the relationship between two documents. Journal of the American Society for Information Science, 24(4), 265–269. https://doi.org/https://doi.org/10.1002/asi.4630240406

- Small, H. (2006). Tracking and predicting growth areas in science. Scientometrics, 68(3), 595–610. https://doi.org/https://doi.org/10.1007/s11192-006-0132-y

- Smaoui, H., Grandes, M., & Akindele, A. (2017). The determinants of bond market development: Further evidence from emerging and developed countries. Emerging Markets Review, 32(September), 148–167. https://doi.org/https://doi.org/10.1016/j.ememar.2017.06.003

- Thakur, B. P. S., Kannadhasan, M., & Goyal, V. (2018). Determinants of corporate credit spread: Evidence from India. Decision, 45(1), 59–73. https://doi.org/https://doi.org/10.1007/s40622-018-0179-7

- Tijssen, R. J. W. (2004). Measuring and evaluating science—Technology connections and interactions. Handbook of Quantitative Science and Technology Research. https://doi.org/https://doi.org/10.1007/1-4020-2755-9_32

- Tripathi, A., Dixit, A., & Vipul, V. (2019). Liquidity of financial markets: A review. Studies in Economics and Finance, 37(2), 201–227. https://doi.org/https://doi.org/10.1108/SEF-10-2018-0319

- Van Raan, A. F. J. (2004). Sleeping Beauties in science. Scientometrics, 59(3), 467–472. https://doi.org/https://doi.org/10.1023/B:SCIE.0000018543.82441.f1

- Van Raan, A. F. J. (2006). Comparison of the hirsch-index with standard bibliometric indicators and with peer judgment for 147 chemistry research groups. Scientometrics, 67(3), 491–502. https://doi.org/https://doi.org/10.1556/Scient.67.2006.3.10

- Warther, V. A. (1995). Aggregate mutual fund flows and security returns. Journal of Financial Economics, 39(2–3), 209–235. https://doi.org/https://doi.org/10.1016/0304-405X(95)00827-2

- Wermers, R. (1997). Momentum investment strategies of mutual funds, performance persistence, and survivorship bias ( Unpublished Working Paper, University of Colorado [1996, 1–29]). http://jpkc.whu.edu.cn/jpkc2003/investment/kcwz/wxxd/art%5CM%5Cmomentuminvestmentstrategies,mutualfunds.pdf

- Zhu, Q. (2021). Capital supply and corporate bond issuances: Evidence from mutual fund flows. Journal of Financial Economics, 141(2), 551–572. https://doi.org/https://doi.org/10.1016/j.jfineco.2021.03.012