Abstract

Corporate governance is a field that is attracting great attention in the world due to its importance to the destiny of enterprises. More importantly, in the context of escalating environmental and social problems, how businesses are governed towards a balance of economic, social and environmental values receives significant concern by the stakeholders of the business in the globe. This study aims to understand intensively the impact of corporate governance on firm value by exploring the mediation mechanism of corporate social responsibility and organisational identification in the relationship between corporate governance and firm value. This study uses the covariance-based structural equation modelling (CB-SEM) analysis technique because of its suitability for organisational and management research such as the present study. This study focuses on the small and medium-sized enterprises (SMEs) in emerging economies due to its importance as outlined in the introduction below. The contribution of this study is the provision of the additional empirical evidence on the important role of corporate governance in increasing firm value. In addition, the empirical evidence on the mediating influence of corporate social responsibility and organisational identification in the relationship between corporate governance and firm value deserves the main interest of this study. Furthermore, its application to the SME context in emerging economies reinforces the novelty of this study. Based on the findings of this study, theoretical and managerial implications are also proposed. The findings of this study may be of interest to entrepreneurs, top management, academics and researchers.

PUBLIC INTEREST STATEMENT

Corporate governance is now a growing issue in emerging markets like Vietnam. It is a key technique to maintain the corporates’ operations effectively. There is very little research on corporate governance in the context of emerging economy like Vietnam. Thus, the authors want to contribute this research to consolidate the theoritical and practical contribution on this area. The findings suggest a positive and significant impact of corporate governance on firms’ value through mediating role of corporate social responsibility and organizational identification. This contribution has confirmed the role of corporate social responsibility and organizational identification affecting to the SMEs’ value in emerging markets. Besides, this study proved that corporate social responsibility has a positive and significant impact on organizational identification. This study contributes to the literature of corporate governance and firms’ value of SMEs in emerging country context. A mediating role of corporate social responsibility and organizational identification as a value-added contribution to this research.

1. Introduction

Corporate governance (CGV) and sustainability are two domains that are receiving increasing attention by scholars as illustrated by the recent increase in the amount of research in this field (Naciti et al., Citation2021). This, thereby, shows that both sustainability and the role of governance in sustainability are increasingly concerned (Naciti et al., Citation2021). CGV is defined as the set of rules, processes, ethic codes and organisational structures that underpin sound business practice geared towards the interests of different stakeholders (Du Plessis et al., Citation2018). CGV is important because it helps organisations to achieve their goals, control risks, and assists with formal decision-making to avoid risks (Ida Bagus et al., Citation2019).

Additionally, CGV is fundamentally concerned with a balance of stakeholders’ interests including shareholders, directors, employees, customers, suppliers, financiers, governments and communities. CGV differs from every country and every firm because it is related to economic, legal, social, cultural and ownership-structural contextual elements. Nikolić and Zlatanović (Citation2018) argue that CGV exists in relevant areas of research which create many dilemmas and disagreements in contemporary theory and practice. In addition to that, the Covid-19 emergency could affect the way that businesses self-govern, deal with socially responsible issues and carry sustainability practices (Eweje et al., Citation2021). In the context of the current dynamic environment, stakeholders are increasingly concerned with how businesses are governed to ensure a balance of the values of economy, society and the environment. Accordingly, the way in which the businesses create value for their stakeholders must be socially responsible and must not compromise on issues of society and the environment.

Corporate social responsibility (CSR) is approached in different way by current literature. CSR refers to the voluntary implementation of corporate responsibility towards stakeholders in a way that balances values of economy, society and the environment (Thanh Tiep et al., Citation2021). The importance of CSR for corporate competitive advantages, corporate performance and firm value (FV) is firmly demonstrated by the current literature (Butt et al., Citation2020; Fuadah & Kalsum, Citation2021; Hendratama & Huang, Citation2021; Thanh Tiep et al., Citation2021). Despite the growing importance of CSR globally, CSR in underdeveloped countries is not yet mandatory (Shu & Chiang, Citation2020). In addition, current literature on this domain focuses heavily on developed countries and the lack of empirical research on small and medium-sized enterprises (SMEs) in emerging countries (Butt et al., Citation2020; Fabeil et al., Citation2020). Meanwhile, this is a very important resource of the national and global economy. According to National Action Plan on Business and Human Rights (Citation2020), the SME force in the world is estimated at 400 million businesses. They represent about 90% of businesses and address more than 50% of employment around the world. Statistically, their contribution to the gross domestic product (GDP) in emerging economies is around 40% (The World Bank Group, Citation2020). This study takes some emerging economies such as Vietnam, which has around 518 thousand SMEs (Tuan, Citation2020) and Brazil, which has approximately 11.5 million SMEs into consideration (Organisation for Economic Co-operation and Development, Citation2018). In reality, the significant contribution of SMEs for economic and social development is well recognised. However, how to develop sustainably remains a hot topic. As a consequence of uncontrolled economic growth, it threatens the environmental sustainability, socio-economic development (Bekun et al., Citation2019) and quality of life (Badulescu et al., Citation2019) which effect sustainable development (Abdelhalim et al., Citation2019).

According to Kartika et al. (Citation2019), a firm should address the stakeholder’s interests, ensure ethical business practices and the legitimacy to maintain sustainable operations, and obtain investors’ trust to improve FV. According to Elkington (Citation1997), a so-called good business creates not only economic value but also environmental and social value towards sustainability. Additionally, Brigham and Houston (Citation2006) stated that the primary purpose of corporate incorporation is destined to address the interests of different stakeholders and maximise prosperity of stakeholders by improving FV. According to Ida Bagus et al. (Citation2019), FV is the value of a firm which is reflected by the company’s market price and closely related to the share price that investors need to make decisions regarding their investments. FV can maximise wealth for shareholders as its share value increases. A high stock price indicates a high FV. According to Kartika et al. (Citation2019), FV is closely associated with firm performance and corporate image which can be achieved by a good CGV and ethical behaviour. The current literature on this field indicates diverse approaches to the link between CGV and firms’ outcomes. For instance, research of Ida Bagus et al. (Citation2019) on India, China and Indonesia markets determined that CGV positively and significantly affects firm value with the mediating effect of CSR. Research of Kartika et al. (Citation2019) on the Indonesia market affirms that CGV and CSR positively and significantly affect FV directly and indirectly through the cost of capital. The study of Tarigan and Stacia (Citation2019) on Indonesia proves that CGV significantly and positively affects firm profitability.

It must be noted that the existing literature on CGV and FV still needs to be enriched in other contexts and involves other factors in order to diversify approaches. Although organisational identification (OID) is conceptually important for firm performance, it is rarely explored in relation to this relationship. As Miller et al. (Citation2000), OID can lead to employee loyalty that is formed and developed from affection for the organisation and belief in its normative values, leads to employee happiness and pride in contributing to the organisation. The above discussion shows that the relationship between CGV and FV needs to be explored further with the involvement of CSR and OID to mediate this relationship. Furthermore, in the context of the Covid-19 emergency, global businesses suffer heavy losses due to closures and business interruption (Alessandro & Marikka, Citation2021; Golubeva, Citation2021; Larcker et al., Citation2020; Nicola et al., Citation2020), simultaneously, and others, especially SMEs, are looking for ways to survive in the short and long term and recover from the Covid-19 crisis (Al-Fadly, Citation2020). Therefore, further empirical research on how, and the circumstances under which, CGV leads enterprises to overcome a crisis, enhance firm value and move towards sustainability for SMEs in specific emerging-based economy setting should be highly prioritised (Koutoupis et al., Citation2021).

Therefore, the focus of this study is an empirical research on the influence of CGV on FV with the mediation mechanism of CSR and OID in the link between CGV and FV for SMEs in an emerging economy. The objective of this study is to understand intensively how corporate governance is involved in enhancing FV towards sustainability for SMEs in emerging economies. The contributions of this study are twofold. First, this study expands existing literature on the domain of CGV and corporate outcomes by the development of an empirical model of the influence of CGV on FV through the mediating effects of CSR and OID. Second, this study provides an insight into how CGV improves FV with the mechanism of the mediation impact of CSR and OID on the link between CGV and FV. These contributions may be of great interest to owners, directors, managers and policy makers in terms of a value-adding mechanism for businesses on the basis of a balance of benefits for all different stakeholders towards sustainable economic, social and environmental values.

This study majorly uses stakeholder theory, resource-based view theory, social identity theory and stewardship theory as the theories which underpin the arguments in the research. It applies stakeholder theory in this context to explain the involvement of CSR as a mediator in this research. In addition to that, since CSR is conceptually oriented to drive the value of all stakeholders, not solely shareholders, it is often integrated as part of a good governance perspective (Shu & Chiang, Citation2020). Likewise, applying social identity theory aims to explain why OID is assumed to be involved in this study as a mediator. In addition, resource-based view and stewardship theories are to explain the how and the circumstance that CGV enhance a firm’s value. Further theoretical discussions are presented in the following theoretical framework under section 2.1 below. In order to address the research objective, the following questions need to be solved:

RQ1. How does CGV enhance FV for SMEs in an emerging economy?

RQ2. How do CSR and OID mediate the relationship between CGV and FV in this context?

This study uses the covariance-based structural equation modelling (CB-SEM) technique to analyse data because of its suitability for this research context. First, CB-SEM is popular for research in the field of organisational and management such as the present study. Second, CB-SEM has outstanding features that are suitable for multi-relationship and mediating influence models such as the model involved in this study. This research focuses on small- and medium-sized enterprises (SMEs) in the emerging economy of Vietnam. The analytical data for this study are primary data collected from the questionnaire-based survey. The target respondents are directorial and managerial levels, and entrepreneurs.

This study is structured into six sections. Section 1 introduces the background related to the research topic, and outlines the research problem, research objectives, research questions, theoretical application and applied methods. Section 2 presents the theoretical framework, reviews the relevant literature, outlines concepts and develops the research hypotheses. Section 3 describes the research model and methodology. Section 4 presents the research results and discussions. Section 5 concludes the study and Section 6 outlines the limitations of the present study, which provides the scope for future research.

2. Literature review and development of the hypotheses

This section includes subsections for the following contents, where subsection 2.1 presents the theoretical framework. Subsections from 2.2 to 2.5 present the hypothesis development. Section 2 ends with , which summarises the outcomes of a review of the literature relevant to this research topic.

Table 1. Summary of literature review of CGV related literature

2.1. Theoretical framework

In this study, stakeholder theory (Freeman, Citation1984), resource-based view (RBV) theory (Barney, Citation1991), social identity theory (Ashforth & Mael, Citation1989) and stewardship theory (Abdullah & Valentine, Citation2009; Rashid & Islam, Citation2013) are used as the underpinning theories. According to stakeholder theory, businesses cannot achieve so-called success if they only focus on their own economic benefits without regarding the interests of other stakeholders and a balance of values of economy, society and the environment. From the stakeholder theory perspective, a business’s stakeholders can be influenced by corporate outcome, which can simultaneously influence its corporate responsibility in a variety of ways, according to Freeman et al. (Citation2020). In this context, CSR is assumed to assist the relationship between CGV and FV, as CSR emphasises the requirement for businesses to behave and act responsibly towards society and the environment, especially in the context of globalisation. From this approach, it should be emphasised that businesses are expected by stakeholders to perform their responsibilities to increase stakeholders’ values without compromising on social and environmental issues.

In addition, OID deserves being coupled with CSR to mediate the relationship between CGV and FV in this setting. As social identity theory (Ashforth & Mael, Citation1989), OID refers to the situation in which employees in particular, and stakeholders in general, feel a similarity and affection for the business with which they are associated. This reflects the emotional link between businesses and their stakeholders. Thus, when they feel that the business cares about their interests in a sustainable way and addresses their concerns about the environment and society, they have a good impression of it, which motivates them to raise their awareness to the organisation and to be more attached to the organisation. Therefore, how the business is governed to be able to promote CSR efforts is very important in improving OID by stakeholders, in which the employee is an important stakeholder of the business. As a result, this ultimately leads to increased FV in various ways.

In addition, from the perspective of RBV theory, the structure and composition of the board is seen as a source of value creation for the business. RBV is linked to the characteristics of the board in terms of private resources that can be a source of competitive advantage for companies. Using this method for this study shows that CGV is the source of strategic resources for a firm’s competitive advantage. Therefore, a good CGV is considered to be an important resource to help enterprises improve their competitive advantage, which ultimately leads to the enhancement of the value of the enterprise. Moreover, this study uses stewardship theory to explain why business leaders strive towards the common good rather than individual interests. According to Rashid and Islam (Citation2013); Abdullah and Valentine (Citation2009), stewardship theory is mainly based on psychological and sociological aspects. Accordingly, it assumes that the board of directors is the head of the ship whose focus is on maximising the performance of the company rather than their own interests.

2.2. The involvement of CSR in mediating the link between CGV and FV

The involvement of CSR in mediating the link between CGV and FV is debated in line with the discussions of the relationship between CGV and CSR, and CSR and FV, based on current literature. The current literature demonstrates that CGV positively and significantly affects FV. For instance, good CGV has a positive and significant impact on a firm’s value (Ibrahimov & Omarova, Citation2020). CGV positively and significantly affects firm value with the mediating effect of CSR (Ida Bagus et al., Citation2019). CSR is perceived as associated with good governance. Better-governed businesses are often identified as having better social responsibility (Bolourian et al., Citation2021). In addition, according to Fahad and Rahman (Citation2020) and Ida Bagus et al. (Citation2019), CGV positively and significantly affects CSR. Accordingly, good CGV is about ensuring that businesses operate ethically, and behave and act responsibly towards all stakeholders, society and the environment. From this approach, the more advanced the CGV, the better the enterprises practice their CSR. Furthermore, the relationship between CSR and FV is demonstrated to be significant and positive by the existing literature. For instance, according to Tarigan and Stacia (Citation2019), CSR performance and CGV implementation are associated with greater profitability. CSR has a role to orient businesses to be more responsible to stakeholders, environment and society in the push towards sustainability that leads to enhanced firm value (Kartika et al., Citation2019). In addition, engaging in environmentally and socially responsible activities positively affects FV (Qureshi et al., Citation2020; Xie et al., Citation2019) (66-CGV). The higher the degree of corporate engagement in CSR, the higher the firm value is obtained (Fuadah & Kalsum, Citation2021).

Theoretically, this relationship is debated based on stakeholder theory, RBV theory and stewardship theory. From the stakeholder theory point of view, a company is well-governed when it ensures that its business activities run consistently on an ethical path and are aligned with the interests of its stakeholders towards sustainability. According to stakeholder theory, businesses cannot be successful if they only focus on their own economic benefits without regard for the interests of other stakeholders and a balance of values of economy, society and the environment. Besides, from the RBV theory perspective, a good CGV is considered an important resource that facilitates CSR efforts in practices and initiatives. As a result, this leads to the enhancement of the value of the enterprise. In addition, from the stewardship theory perspective, a board of directors is a group of top players whose focus is on maximising the performance of the company rather than their own interests.

The above discussions enable the assumption that enhancing CGV will help to optimise CSR efforts and enhance CSR outcomes, ultimately leading to increased FV. Therefore, the hypotheses involved in the mediating influence of CSR in the relationship between CGV and FV are reasonably assumed to be as follows:

H1a: CGV positively affects CSR.

H1b: CSR positively affects FV.

H1: CSR mediates the relationship between CGV and FV.

2.3. The involvement of OID as mediating the link between CGV and FV

The involvement of OID in the link between CGV and FV is debated in line with the discussions of the relationship between CGV and OID, OID and FV based the current literature. Current literature shows that CGV has a positive relationship with OID. For instance, according to Zollo et al. (Citation2019) CGV positively influences OID. In addition, according to Van Puyvelde et al. (Citation2012), through the lens of stakeholder theory, CGV tends to improve OID. Furthermore, Filatotchev and Nakajima (Citation2010) defined that CGV may have a profound impact on OID. With regard to the relationship between OID and FV, according to Ashforth and Mael (Citation1989), OID literature implies that individuals will become more engaged in activities that reinforce their organisational identity and value. According to Su et al. (Citation2019), OID levels positively affect the achievement levels of organisational goals and therefore affect the firm value as a result. When individuals have a high OID, this strengthens their emotional relationship with the organisation and simultaneously, they treat the firm’s success as their own success. Therefore, a higher level of OID can result in increasing the level of trust that leads to greater commitment and engagement between employees and the organisation. As a result, it will ultimately contribute to enhancing FV. In addition, according to Voss et al. (Citation2006), OID positively impacts on business performance metrics, ultimately leading to increased FV in a way that improves efficiency.

Theoretically, this relationship is debated based on RBV theory, stewardship theory and social identity theory. OID refers to the situation in which employees in particular, and stakeholders in general, feel a similarity and affection for the business with which they are associated. This reflects the emotional link between businesses and their stakeholders. Good CGV is when stakeholders, especially employees, perceive the actions and behaviours of governance to be consistent with the direction that the business is responsible to stakeholders, society and the environment. In addition, from the RBV and stewardship theories, the superior governance characteristics in terms of people, capacity-related factors, knowledge-related elements and diversity towards common interests are considered to be strategic resources that play a very important role in promoting employee organisational identity. In turn, it will increase employees’ positive perceptions of the organisation and motivate them to enhance their identity with the organisation. As a result, this ultimately leads to increased FV in various ways.

The above discussions enable the assumption that enhancing CGV will help enhance OID, ultimately leading to increased FV. Therefore, the hypotheses involved in the mediating influence of OID in the relationship between CGV and FV are reasonably assumed as follows:

H2a: CGV positively affects OID.

H2b: CSR positively affects FV.

H2: CSR mediates the relationship between CGV and FV.

2.4. CSR and OID

The current literature indicates that CSR has a positive relationship with OID. For instance, Nguyen et al. (Citation2020) demonstrate that CSR efforts towards different stakeholders such as employees, customers, suppliers, communities and the environment increase a positive awareness of the business by employees, leading to improved employee engagement and organisational identification. In addition, according to Muhammad et al. (Citation2017), CSR implementation towards customers, employees, shareholders, the environment and society positively affects OID. Accordingly, businesses which operate in an ethical and responsible manner towards stakeholders, the environment and society will return with benefits that help businesses to develop healthily. In addition, the relationship between CSR on OID is confirmed to be positive and significant by Kim et al. (Citation2010) and Su et al. (Citation2019).

Therefore, the hypothesis of the relationship between CSR and OID is assumed based on the above discussion, as follows:

H3: CSR positively affects OID.

2.5. CGV and FV

Tarigan and Stacia (Citation2019) define that a good CGV helps a company to improve its efficiency and effectiveness by reduced operational costs, increased margins and increased profitability. Firms with good CGV ensure socially responsible practices and ethical business practices that are consistent with the values and norms of the society in which they operate. In addition, Thomsen (Citation2005) contends that CGV has a positive and significant relationship with FV. This finding is consistently supported by the later studies of Ammann et al. (Citation2011), Lozano et al. (Citation2016), Li et al. (Citation2012), and Ararat et al. (Citation2017). In other words, an increase in firm value will necessarily require an increase in CGV efficiency and effectiveness.

Therefore, the hypothesis of the relationship between CGV and FV is assumed based on the above discussion, as follows

H4: CGV positively affects FV.

below summarises the outcomes of a literature review of CGV related literature.

3. Research model and methodology

3.1. Research model

A systematic review shows that the current literature on the field of CGV is approached from various angles and contexts as summarised in above. It, thereby, shows that none of the literature has an empirical study on the integration model to explore the relationship between CGV and FV deeply, with the involvement of CSR and OID mediating this relationship. In addition, there is a lack of empirical research for SMEs in emerging economies. Therefore, this suggests that the relationship between CGV and FV needs to be further experimentally investigated with the mediating mechanism of CSR and OID in the stated relationship between CGV and FV. The integrated model of CGV, FV, CSR and OID is shown in the following in which CGV is an independent variable having 5 items, FV is a dependent variable having 3 items, and CSR and OID are mediating variables that have 6 items and 4 items, respectively. These detailed items of each construct are presented in the following .

Figure 1. Proposed research model.

Table 2. Constructs

presents the detailed items of each construct.

3.2. Research methodology

This research employed a combined quantitative and qualitative method to optimise research efficiency. In particular, the advantage of the qualitative method gives us the opportunity to exploit insights into decisive elements of CGV and its association with FV. The target respondents are directorial and managerial levels, and entrepreneurs. The total number of participants is 50 people, including 20 managing directors, 22 managers and 8 entrepreneurs. The objective of this stage is to complete the survey questionnaire in accordance with the research context and quantitative research. The questionnaire was developed in accordance with a 7-point Likert scale (1 represents “strongly disagree”; 7 represents “strongly agree”).

Data was collected from 315 respondents from 225 companies in the south region of Vietnam. The sample size was computed based on the total number of items associated with the constructs under the guidance of J. Hair et al. (Citation2010) that should be 5 to 10 times the total determined items. Therefore, with a total of 18 items, as in this study, the sample size should be 180 samples. To avoid potential risks that could affect response rates such as missed or incomplete responses, the sample size was initially determined to be 325 samples collected by a simple random probability method. The selected respondents included managing directors (about 35%), managers (about 45%) and entrepreneurs (about 20%) in the south region of Vietnam, with no age restriction. The survey is conducted by combining direct form and online technology application, depending on the convenience of every participant in the survey. The obtained answer sheets are screened to select only the complete answer sheets. This resulted in 315 valid responses being collected which were then subjected for analysis using the covariance based structural equation model (CB-SEM).

CB-SEM was chosen to be used in this research for the following reasons. First, CB-SEM is known to possess feature advantages over other conventional analytical methods as a tool for data analysis suitable for the field of organisational and management research (Zhang et al., Citation2020). Second, CB-SEM is known as the most appropriate technique for analysing mediating effects compared to other methods due to its advantages such as the ability to be flexible in manipulation of analysis for mediation; the ability to analyse multiple indicators of the same construct in a latent variable model for mediation (Iacobucci et al., Citation2007); the ability to separate the measurement error from the manifest variable to ensure the most accurate factor loading estimate possible (McDonald, Citation1996); the ability to identify the multicollinearity problem well, thanks to the tool of modification index assigned to this application (McIntosh et al., Citation2014). With this approach, CB-SEM can assist the researcher in detecting which items have the potential to affect the construct meaning adversely, while this benefit cannot be found in other methods. Third, the CB-SEM estimate is more accurate than other quantitative analytical techniques (e.g., PLS-SEM) for a sample size of 50 and above (Jannoo et al., Citation2014). Fourth, the construct reliability may be more reliable for CB-SEM than other methods due to its ability to limit the bias of factor loading values (Afthanorhan et al., Citation2020). Fifth, the estimation technique of CB-SEM is preferred over others for parameter accuracy thanks to the use of the consistent estimator in CB-SEM which helps to render consistent attributes in different situations (Reinartz et al., Citation2009).

4. Results

This section presents the quantitative results of this study. Accordingly, it includes sub-sections presenting the evaluation of the scale (reliability, convergent and discriminant validity), assessments of the model fit, the measurement model, the structural model and the research hypotheses.

4.1. Assessing reliability of the scale

An assessment of reliability is necessary to check the degree of consistency between multiple measurements of a variable, according to J. Hair et al. (Citation2010). For this purpose, Cronbach’s Alpha and composite reliability (C.R) were used to evaluate the scale consistency and overall reliability. The analysis results show that Cronbach’s Alpha and C.R are all greater than 0.7. This result validates the measurement model, confirming that the scales are good and reliable (J. F. Hair et al., Citation2016). summarises the results of Cronbach’s Alpha and C.R to support the assessment and stated conclusion about the reliability of the scale involved in this study.

Table 3. Cronbach’s alpha and C.R results

The next step was taken to analyse factor prior to exploratory factor analysis (EFA). For this purpose, the KMO and Bartlett’s Test result indicators were assessed. The results presented in below show that the KMO coefficient > 0.5 and sig. < 0.05. This result reflects that the necessary conditions are met to perform EFA.

Table 4. KMO and Bartlett’s test

Exploratory factor analysis (EFA) was then taken. The result shows that most of the items converge on the appropriate factors according to the research model except for CSR5 whose factor loading is smaller than 0.5, so this variable does not satisfy convergence and needs to be eliminated. Thus, the CSR variable remains 5 items instead of 6 as initially proposed. below summarises the factor loading of items after eliminating CSR5 to assist in factor loading analysis.

Table 5. Factor loading

4.2. Convergent validity

Convergent validity was assessed as necessary to check the convergence of the measurement items onto the respective structures. For this purpose, Average Variance Extracted (AVE) values were evaluated (Götz et al., Citation2010). According to J. Hair et al. (Citation2010), AVE value is required to be equal to, or greater than, 0.5 to validate convergent validity. The result shows that the AVE values of all the variables in this study range from 0.505 to 0.560, which means that convergent validity is supported. below summarises the AVE values as stated.

Table 6. Convergent validity

4.3. Discriminant validity

Assessment of discriminant validity was performed by evaluating Maximum Shared Variance (MSV) and AVE values. In a scenario in which the MSV values are all smaller than the AVE values, discriminant validity is satisfied (J. Hair et al., Citation2010). The comparison of MSV and AVE values as shown in below indicates that MSV, with values from 0.146 to 0.237, is always smaller than AVE, with values from 0.505 to 0.560. This result affirms the discriminant validity of this study.

Table 7. Discriminant validity

4.4. Confirmatory factor analysis (CFA)

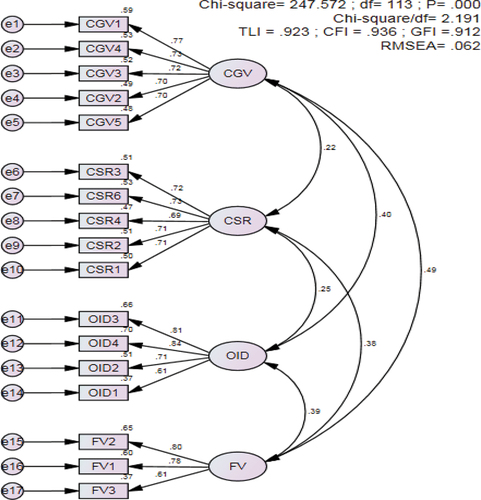

With Cronbach’s Alpha and AVE results being greater than 0.7 and 0.5, respectively, they satisfy the necessary requirements to perform the confirmatory factor analysis (CFA). below illustrates the exploratory factor analysis results showing the diagram between the factors and related variables in the research model.

Figure 2. Confirmatory factor analysis (CFA).

4.5. Evaluation of structural model

The model fit was assessed to determine its fitness and its validity through the evaluation indices such as RMSEA (root mean square error of approximation), GFI (goodness-of-fit statistics), CMIN/DF (Chi-square/df) and TLI (Tucker-Lewis index). The following presents the results corresponding to these indicators and concludes its validity against the proposed threshold. Therefore, the model involved in this study is fit and valid.

Table 8. Model fit analysis

In order to analyse the relationships in the structural model, p values were evaluated. Accordingly, with p-values less than 0.05, the corresponding relationships are concluded to be significant. below shows that all the p-values of the relationships in the research model are smaller than 0.05, which means that all relationships are significant.

Table 9. P-value

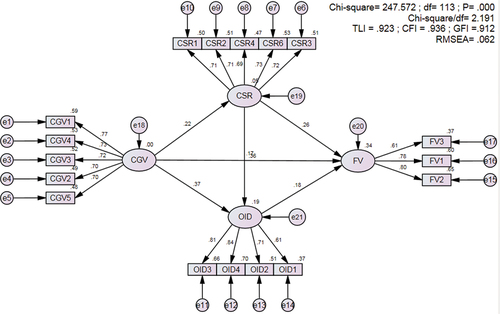

Regarding the analysis of the level of impact and the direction of impact in the relationship between the main variables in this research, SEM analysis results were used for this purpose. The results show that all path estimates are positive, indicating that the relationships between the variables of the respective path are positive. In addition, the p-values, all being less than 0.05, determine that these relationships are significant. Accordingly, the increase of the influencing variable will lead to the increase of the affected variable in the specific relationship. summarises the analysis results of SEM to support the analysis and stated conclusions. Besides, illustrates the SEM results of this study.

Figure 3. Analysis result of research model.Source: Authors’ analysis

Table 10. SEM analytical results

Analysis using the bootstrapping technique was performed with a 1,000 sample loop. According to Efron and Tibshirani (Citation1993) and Efron (Citation2003), bootstrapping assigns measures of accuracy (bias, variance, confidence intervals, prediction error, etc.) to sample estimates. The results show that all C.R. are smaller than 1.96, indicating that the results are reliable for sample-to-population prediction. below presents the bootstrapping results to reaffirm the robustness of the SEM analysis results as stated.

Table 11. Results of bootstrapping

The structural model and research hypotheses were assessed using SEM analysis results as presented in above. The results show that CGV positively and significantly affects CSR (β = 0.279, p < 0.05). This conclusion supports hypothesis H1a. Likewise, the relationship between CSR and FV is demonstrated to be positive and significant in this study (β = 0.198, p < 0.05). This conclusion shows that hypothesis H1b is accepted. This result supports the conclusion that CSR mediates the link between CGV and FV. Therefore, when the CGV is better, the CSR outcomes will be improved, leading to an increase in firm value.

In addition, the results indicate that CGV positively and significantly affects OID (β = 0.418, p < 0.05) which supports hypothesis H2a. Besides, the relationship between OID and FV is demonstrated to be positive and significant in this study (β = 0.155, p < 0.05). This result supports hypothesis H2b, so it is accepted. This result supports the conclusion that OID mediates the link between CGV and FV. Therefore, when CGV is better, the degree to which employees identify with the business is increased, which in turn benefits the business in various ways that the current literature has demonstrated regarding productivity and ultimately lead to an increase in firm value. In addition, the results show that CGV positively and significantly affects FV (β = 0.350, p < 0.05), which supports hypothesis 4. Likewise, the relationship between CSR and OID is demonstrated to be positive and significant (β = 0.149, p < 0.05) and this supports hypothesis 3 in this study.

5. Discussions and implications

This section includes subsections that include the discussions of the findings of this research, theoretical implications and managerial implications. The contents of these subsections are presented below.

5.1. Discussions

Throughout this study, a so-called good CGV for SMEs in an emerging market is considered to include board size, board independence, board interaction, managerial ownership and ownership structure. The board size should be small to be efficient because it offers flexibility in problem solving, therefore being more economical in operating costs (Diriba & Basumatary, Citation2019; Naushad & Malik, Citation2015), and having the ability to seize opportunities faster than the opponent (Lorsch & Maclver, Citation1990). As a result, this leads to increased firm value in such a way that it enhances efficiency. This finding supports the notion of Jensen (Citation1993) which implies that the board size should be small to be more efficient, so that proposes the proper size should be less than 7 people. In relation to board independence, the results imply that the more independent it is, the better the firm value, because independent directors can help to reduce agency problems and raise a manager’s compliance level with regard to his/her responsibilities with stakeholders. This finding supports the perception of Jain and Jamali (Citation2016). The board interaction itself is concerned with the meeting frequency in this study. The findings show that the meeting frequency is so-called suitable for efficiency when it is flexible enough based on the amount of work to be addressed. In relation to ownership structure, it is concerned with the share proportion of CEO, directors and immediate family members to total outstanding shares. The results show that the ratio of shares held by these components has a negative relationship with the CGV effectiveness towards CSR involvement. This finding supports the view that business owners and big inside shareholders tend not to favour long-term investment in CSR, while outside shareholders and other stakeholders expect long-term commitment to CSR activities from businesses towards sustainability (Shu & Chiang, Citation2020). In relation to ownership structure, it is considered to be effective and efficient when the ownership structure does not include a state element.

The findings of this study, based on its hypothetical relationships, have similarities and differences compared to the existing literature. Specifically, the affirmation of a positive and significant association between CGV and CSR advocates the studies of Ida Bagus et al. (Citation2019), Nikolić and Zlatanović (Citation2018), Bolourian et al. (Citation2021), and Fahad and Rahman (Citation2020). Besides, the results confirming the positive and significant impact of CSR on FV supports the findings of the studies of Fuadah and Kalsum (Citation2021), Tarigan and Stacia (Citation2019), and Kartika et al. (Citation2019); Qureshi et al. (Citation2020); Xie et al. (Citation2019). This result is different from Sameer (Citation2021) in that there is a negative and significant relationship between CSR and the firm outcomes. Likewise, the proven positive effects of CGV on OID supports the studies of Zollo et al. (Citation2019), Van Puyvelde et al. (Citation2012), and Filatotchev and Nakajima (Citation2010). Additionally, the relationship between OID and FV was shown to be positive and significant in this study, supporting the findings of studies by Su et al. (Citation2019); Voss et al. (Citation2006). Regarding the relationship between CSR and OID, the assertion of a significant and positive relationship between CSR and OID support the finding of Su et al. (Citation2019) and Muhammad et al. (Citation2017).

The relationship between CGV and FV is shown to be positive and significant in this study. This result supports the findings of Kartika et al. (Citation2019) and Tarigan and Stacia (Citation2019), although it is different from the findings of Berthelot et al. (Citation2012) and Zabri et al. (Citation2015), as they argue that CGV reduces FV. The results of the main interest of this study, which is the mediating role of CSR and OID in the relationship between CGV and FV, support the findings of Ida Bagus et al. (Citation2019) in that CSR mediates the stated relationship. This confirms that, in the context of SMEs in emerging economies, CGV plays a very important role in enhancing corporate value with the mediating influence of CSR and OID in this relationship. The results show that good CGV ensures that businesses operate ethically and responsibly to stakeholders, the environment and society. Good CGV orients businesses to work to address stakeholders’ interests towards balancing the values of economy, society and the environment. This confirms that a better CGV leads to better CSR and OID, which ultimately leads to better FV. Thereby, this shows that CGV plays a very important role in the outcomes of enterprises in the sustainability orientation. It is therefore no coincidence that there is a growing interest in CGV, CSR and sustainability (Naciti et al., Citation2021). The role of CGV in bringing businesses towards sustainability is the main interest. CSR serves as a strategic vehicle to help businesses drive their sustainability goals. Nonetheless, as outlined above, empirical research on the mediating influence of CSR and OID in the relationship between CGV and FV is rare in the current literature. Therefore, this contribution is considered as important, as well as the originality of this study. Based on the above discussion, the theoretical and managerial implications are proposed in the following section.

5.2. Theoretical implications

This study has some theoretical implications as discussed in this section. First, this study enriches the existing literature in the fields of CGV and FV that is inherently rare in the current literature and requires further empirical research in this specific setting. Second, this study provides additional evidence on the positive and significant relationship between CGV and FV for SMEs in an emerging market. Third, this study provides an extension to the extant literature in the domain of CGV and FV by the development of an empirical model of the impact of CGV on FV with the integration of CSR and OID to mediate this relationship. From the evidence-based view, this expands the empirical evidence on the importance of CGV in enhancing FV with the mediating mechanism of CSR and OID in this relationship. Fourth, this study contributes to the literature by developing the scale of CGV, CSR, OID and FV for SMEs in emerging economies. This is very important in clarifying each construct in the empirical model in the present study.

Fifth, this study supports the stakeholder theory, RBV theory, social identity theory and stewardship theory. Accordingly, it asserts that a well-governed enterprise is one that operates ethically and is geared towards addressing the interests of various stakeholders on the basis of balancing values of economy, society and the environment. When business stakeholders, especially employees, perceive that the business is governed in an ethical and responsible way to stakeholders, society and the environment, employees will improve their positive perception of the business, motivating them to stick around and enhance their contributions in a way that enhances efficiency, and ultimately leads to enhancing the firm value in a sustainable way. Good CGV is seen as an important source of resources to promote CSR efforts and enhance OID, ultimately leading to increased FV. Firm value is seen as a result of good CGV through the mediating influence of effective CSR efforts and positive OID.

5.3. Managerial implications

This study has some managerial contributions which are described in this section. The first contribution is the provision of the insight into how CGV components should be so that businesses can achieve so-called efficiency in the context of the involvement of CSR elements for SMEs in emerging economies. Therefore, business practitioners and SME owners are encouraged to give due concern to the findings of this study in considering the appropriate CGV for the business to achieve its sustainable development goals, where increasing firm value is seen as a result of good CGV. Furthermore, a good CGV is a prerequisite for business survival (Rehman & Hashim, Citation2021). This implication is important in the context of SMEs in Vietnam because the vast majority of SMEs govern their businesses with the use of nepotism. Accordingly, business owners and family members hold important positions on the board of directors, leading to a significant dominance in business orientation, mainly profit-driven and sporadic philanthropy rather than interest-driven for all stakeholders towards a balance of economic, social and environmental values. However, with pressure in the context of globalisation and increasing social and environmental problems nowadays, this method of governance cannot be continued or businesses are effectively destroying themselves.

The second contribution of this study is the provision of the insight into the mechanism of firm value enhancement. Through this study, business practitioners and owners can understand intensively how CGV increases firm value with the mediation mechanism of CSR and OID in the link between CGV and firm value. This thereby asserts that better CGV promotes better CSR, leading to better OID, which ultimately results in increasing firm value in a sustainable manner. Importantly, the connotation conveyed in this study is that CGV and CSR are seen to be a perfect couple in moving the organisation up towards sustainability. CGV is perceived as good when it ensures that the business operates ethically, and towards addressing the interests of various stakeholders, the environment and society. In order for CGV to be effective with the involvement of CSR elements, it is necessary to determine in advance an appropriate CGV in terms of governance structure and governance mechanism (Ibrahimov & Omarova, Citation2020, p. 48). In addition, OID is also an important factor in explaining that, when a business is governed in a way that is responsible to stakeholders, society and the environment, employees increase their positive perception of the business and this leads to increasing their organisational identity. In turn, this results in enhancing their contribution in a way that enhances efficiency and performance, which ultimately leads to increasing firm value in a sustainable way. This implication is very important for business practitioners and owners because it directly addresses the current problem of SMEs which is related to CGV, thereby, providing a mechanism to enhance firm value in a sustainable way that is highly applicable in the context of SMEs in emerging economies.

The third managerial contribution of this study is the recommendation of a long-term sustainable development strategy orientation for SMEs in emerging economies. Accordingly, businesses should integrate social and environmental issues into the CGV structure to ensure proactively that the company is always operated in a responsible and ethical manner (Spitzeck & Lenssen, Citation2009; Welford, Citation2007). Therefore, business practitioners and owners are encouraged to give due attention to the findings of this research in planning long-term development strategies for businesses because CGV, CSR and sustainability are highly correlated (Fahad & Rahman, Citation2020). Therefore, it is no coincidence that there is a growing interest in CGV, CSR and sustainability in the world (Ibrahimov & Omarova, Citation2020). In addition, through this study, it is implied that business leaders should use CSR as a strategic element for effective business development strategy and strengthening the competitive position of enterprises in the marketplaces, especially in the context of globalisation. This is because most of the SMEs in emerging markets do not consider CSR as a strategic element to improve their competitiveness, rather it is a charitable association. This could be due to many factors such as an inadequate approach to the concept of CSR, governance and resource constraint, motivation and others. Whatever the factor, the implication that this study conveys is that implementing CSR in accordance with standards is no longer an option, yet it is a responsibility that businesses must perform on a voluntary basis if they want to survive and develop sustainably, because this is an issue of growing concern among stakeholders around the globe.

6. Conclusions

This study provides a comprehensive examination of the association between CGV and FV with the mediating roles of CSR and OID for SMEs in an emerging country, in this case, Vietnam. This research provides significant contributions to theory and implementation as mentioned above. In this way, the major objectives of this study are achieved. In addition to the findings from our empirical research, this study provides interesting and useful insights into how businesses should be governed to increase value in a sustainable way. These insights may be very useful to business leaders, managers, entrepreneurs, investors and shareholders. Accordingly, the existing problem that most of the SMEs in an emerging economic context frequently face is the conflict related to the balance of interests of stakeholders. This is mainly because of the inconsistency between the views of the owner and the operator in operating the business, or it could be the ambiguity about business goals and organisation responsibility. It is also basically a matter of corporate governance which is majorly reflected by agency theory and stakeholder theory. Hence, the significance of this study’s results is reaffirmed for SMEs in an emerging economic context such as Vietnam.

7. Limitations

Despite the interesting contributions above, this study does have certain limitations. Firstly, this research focuses on SMEs from different segments, while differences in the nature of different industries might influence the essentials of governance characteristics for an effective CGV. Therefore, it might help future studies to refer to firms from a single segment to gain a deeper understanding of their knowledge and engagement with corporate social responsibility. Secondly, this study was conducted in the southern region of Vietnam. Thus, the results may not be the same in a different region, country or culture. Thus, future research may consider different contextual factors to diversify approaches to the background of the research in this area. These limitations present opportunities for future research to continue to leverage empirical studies to enrich the research literature in the field of CGV.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Thanh Tiep Le

Thanh Tiep Le has got PhD in Business Administration, is working at Ho Chi Minh City University of Economics and Finance (UEF), Vietnam. Besides, he has worked as role of part-time lecturer at University of Economics Ho Chi Minh City (UEH), Vietnam. His major research areas are International Business, Corporate Social Responsibility (CSR) related, Corporate Governance, Renewable Energy and Sustainability related.

Van Kha Nguyen is lecturer at Ho Chi Minh City University of Food Industry (HUFI), Vietnam. His major research areas are Business and Management, Corporate Governance, Corporate Social Responsibility (CSR) related, Sustainability related.

References

- Abdelhalim, K., & Amani, G. E. (2019). Can CSR help achieve sustainable development? applying a new assessment model to CSR cases from Egypt. The International Journal of Sociology and Social Policy, 39(9), 773–24. http://dx.doi.org/10.1108/IJSSP-06-2019-0120

- Abdullah, H., & Valentine, B. (2009). Fundamental and ethics theories of corporate governance. Middle Eastern Finance and Economics, 41, 88–96.

- Afthanorhan, A., Awang, Z., & Aimran, N. (2020). An extensive comparison of CB-SEM and PLS-SEM for reliability and validity. International Journal of Data and Network Science, 4(4), 357–364. http://dx.doi.org/10.5267/j.ijdns.2020.9.003

- Al-Fadly, A. (2020). Impact of COVID-19 on SMEs and employment. Entrepreneurship and Sustainability Issues, 8(2), 629–648. http://dx.doi.org/10.9770/jesi.2020.8.2(38)

- Alessandro, M., & Marikka, H. (2021). Business continuity in the COVID-19 emergency: A framework of actions undertaken by world-leading companies. Business Horizons 64(5), 683–695. https://doi.org/10.1016/j.bushor.2021.02.020

- Ammann, M., Oesch, D., & Schmid, M. M. (2011). Corporate governance and firm value: International evidence. Journal of Empirical Finance, 18(1), 36–55. https://doi.org/10.1016/j.jempfin.2010.10.003

- Ararat, M., Black, B. S., & Yurtoglu, B. B. (2017). The effect of corporate governance on firm value and profitability: Time-series evidence from Turkey. Emerging Markets Review, 30(2017), 113–132. http://dx.doi.org/10.1016/j.ememar.2016.10.001

- Arora, A., & Sharma, C. (2016). Corporate governance and firm performance in developing countries: Evidence from India. Corporate Governance, 16(2), 420–436. https://doi.org/10.1108/CG-01-2016-0018

- Ashforth, B. E., & Mael, F. (1989). Social identity theory and the organization. Academy of Management, 14(1), 20–39. https://www.jstor.org/stable/258189.

- Badulescu, D., Simut, R., Badulescu, A., & Badulescu, A.-V. (2019). The relative effects of economic growth, environmental pollution and non-communicable diseases on health expenditures in european union countries. International Journal of Environmental Research and Public Health, 16(24), 5115. http://dx.doi.org/10.3390/ijerph16245115

- Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/014920639101700108

- Bekun, F. V., Emir, F., & Sarkodie, S. A. (2019). Another look at the relationship between energy consumption, carbon dioxide emissions, and economic growth in South Africa. Science of the Total Environment, 655(2019), 759–765. https://doi.org/10.1016/j.scitotenv.2018.11.271

- Berthelot, S., Francoeur, C., & Labelle, R. (2012). Corporate governance mechanisms, accounting results and stock valuation in Canada. International Journal of Managerial Finance, 8(4), 332–343. https://doi.org/10.1108/17439131211261251

- Black, B., Love, I., & Rachinsky, A. (2006). Corporate governance indices and firms’ market values: Time series evidence from Russia. Emerging Markets Review, 7(4), 361–379. https://doi.org/10.1016/j.ememar.2006.09.004

- Bolourian, S., Angus, A., & Alinaghian, L. (2021). The impact of corporate governance on corporate social responsibility at the board-level: A critical assessment. Journal of Cleaner Production, 291(2021), 125752. https://doi.org/10.1016/j.jclepro.2020.125752

- Brigham, E., & Houston, J. (2006). Basics of financial management. Salemba Empat.

- Butt, A. A., Shahzad, A., & Ahmad, J. (2020). Impact of CSR on firm value: The moderating role of corporate governance. Indonesian Journal of Sustainability Accounting and Management, 4(2), 145–163. https://doi.org/10.28992/ijsam.v4i2.257

- Diriba, M., & Basumatary, D. (2019). Impact of corporate governance on firm performance: Evidence from indian leading companies. Parikalpana: KIIT Journal of Management, 15(1&2), 127–140. https://doi.org/10.23862/kiit-parikalpana/2019/v15/i1-2/190r78

- Du Plessis, J. J., Hargovan, A., & Harris, J. (2018). Principles of contemporary corporate governance. Cambridge University Press.

- Efron, B., & Tibshirani, R. (1993). An Introduction to the Bootstrap. Chapman & Hall.

- Efron, B. (2003). Robbins, empirical Bayes and microarrays. Annals of Statistics, 31(2), 366–378. https://doi.org/10.1214/aos/1051027871

- Elkington, J. (1997). Cannibals with forks: The triple bottom line of 21st century business. Oxford: Capstone Publishing Ltd.

- Eweje, G., Iona, A., Foley, M., & Nerantzidis, M. (2021). Guest editorial. Corporate Governance, 21(6), 961–968. https://doi.org/10.1108/CG-09-2021-555

- Fabeil, N. F., Pazim, K. H., & Langgat, J. (2020). The impact of Covid-19 pandemic crisis on micro-enterprises: Entrepreneurs’ perspective on business continuity and recovery strategy. Journal of Economics and Business, 3(2), 837–844. https://doi.org/10.31014/aior.1992.03.02.241

- Fahad, P., & Rahman, P. M. (2020). Impact of corporate governance on CSR disclosure. International Journal of Disclosure and Governance, 17(2–3), 155–167. https://doi.org/10.1057/s41310-020-00082-1

- Filatotchev, I., & Nakajima, C. (2010). Internal and external corporate governance: An interface between an organization and its environment. British Journal of Management, 21(3), 591–606. https://doi.org/10.1111/j.1467-8551.2010.00712.x

- Freeman, R. E., Phillips, R., & Sisodia, R. (2020). Tensions in stakeholder theory. Business and Society, 59(2), 213–231. https://doi.org/10.1177/0007650318773750

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Pitman.

- Fuadah, L. L., & Kalsum, U. (2021). The impact of corporate social responsibility on firm value: The role of tax aggressiveness in Indonesia. The Journal of Asian Finance, Economics and Business, 8(3), 209–216. https://doi.org/10.13106/JAFEB.2021.VOL8.NO3.0209

- Golubeva, O. (2021). Firms’ performance during the COVID-19 outbreak: International evidence from 13 countries. Corporate Governance, 21(6), 1011–1027. https://doi.org/10.1108/CG-09-2020-0405

- Götz, O., Liehr-Gobbers, K., & Krafft, M. (2010). Evaluation of structural equation models using the partial least squares (PLS) approach Vinzi, Vincenzo Esposito, W. Chin, Wynne, Henseler, Jörg, and Wang, Huiwen. In Handbook of partial least squares (pp. 691–711). Springer.

- Hair, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2016). A primer on partial least squares structural equation modeling (PLS-SEM) (2nd ed.). Sage Publications.

- Hair, J., Black, W., Babin, B., & Anderson, R. (2010). Multivariate data analysis (7th ed.). Prentice Hall.

- Harjoto, M., & Laksmana, I. (2018). The impact of corporate social responsibility on risk taking and firm value. Journal of Business Ethics, 151(2), 353–373. https://doi.org/10.1007/s10551-016-3202-y

- Hendratama, T. D., & Huang, Y.-C. (2021). Corporate social responsibility, firm value and life cycle: Evidence from Southeast Asian countries. Journal of Applied Accounting Research, 22(4), 577–597. https://doi.org/10.1108/JAAR-09-2020-0194

- Iacobucci, D., Saldanha, N., & Deng, X. (2007). A meditation on mediation: Evidence that structural equations models perform better than regressions. Journal of Consumer Psychology, 17(2), 139–153. https://doi.org/10.1016/S1057-7408(07)70020-7

- Ibrahimov, Z., & Omarova, U. (2020). Corporate governance and corporate social responsibility of enterprises. Varazdin: Varazdin Development and Entrepreneurship Agency (VADEA). https://search.proquest.com/conference-papers-proceedings/corporate-governance-social-responsibility/docview/2423564597/se-2?accountid=63189.

- Ida Bagus, A. P., Solimun, S., Adji Achmad, R. F., & Rahayu, S. M. (2019). Corporate governance, corporate profitability towards corporate social responsibility disclosure and corporate value (comparative study in Indonesia, China and India stock exchange in 2013–2016). Social Responsibility Journal, 16(7), 983–999. http://dx.doi.org/10.1108/SRJ-08-2017-0160

- Jain, T., & Jamali, D. (2016). Looking inside the black box: The effect of corporate governance on corporate social responsibility. Corporate Governance: An International Review, 24(3), 253–273. https://doi.org/10.1111/corg.12154

- Jannoo, Z., Yap, B. W., Auchoybur, N., & Lazim, M. A. (2014). The effect of nonnormality on CB-SEM and PLS-SEM path estimates. International Journal of Mathematical, Computational, Physical and Quantum Engineering, 8(2), 285–291. https://doi.org/10.5281/zenodo.1090631

- Jensen, M. C. (1993). The modern industrial revolution, exit, and the failure of internal control systems. The Journal of Finance, 48(3), 831–880. https://doi.org/10.1111/j.1540-6261.1993.tb04022.x

- Kartika, H. T., Moeljadi, M., Ratnawati, K., & Indrawati, N. K. (2019). The roles of cost of capital, corporate governance, and corporate social responsibility in improving firm value: Evidence from Indonesia. Investment Management & Financial Innovations, 16(4), 28–36. http://dx.doi.org/10.21511/imfi.16(4).2019.03

- Khatib, S. F. A., & Nour, A.-N. I. (2021). The impact of corporate governance on firm performance during the COVID-19 pandemic: Evidence from Malaysia. Journal of Asian Finance, Economics and Business, 8(2), 0943–0952. https://doi.org/10.13106/jafeb.2021.vol8.no2.0943

- Kim, H.-R., Lee, M., Lee, H.-T., & Kim, N.-M. (2010). Corporate social responsibility and employee–company identification. Journal of Business Ethics, 95(4), 557–569. https://doi.org/10.1007/s10551-010-0440-2

- Koutoupis, A., Kyriakogkonas, P., Pazarskis, M., & Davidopoulos, L. (2021). Corporate governance and COVID-19: A literature review. Corporate Governance, 21(6), 969–982. https://doi.org/10.1108/CG-10-2020-0447

- Larcker, D. F. L., Tayan, B., & Taylor, D. J. The spread of COVID-19 disclosure (2020). Rock Center for Corporate Governance at Stanford University. Stanford Closer Look Series, June https://ssrn.com/abstract=3636454, 1–15.

- Li, W. X., Chen, C. C. S., & Frech, J. J. (2012). The relationship between liquidity, corporate governance, and firm valuation: Evidence from Russia. Emerging Markets Review, 13(4), 465–477. http://dx.doi.org/10.1016/j.ememar.2012.07.004

- Lorsh, J., & Young, J. (1990). Pawns or potentates: The reality of America's corporate boards. The Academy of Management Perspectives, 4(4), 85–87. https://doi.org/10.5465/ame.1990.4277214 .

- Lozano, M. B., Martínez, B., & Pindado, J. (2016). Corporate governance, ownership and firm value: Drivers of ownership as a good corporate governance mechanism. International Business Review, 25(6), 1333–1343. http://dx.doi.org/10.1016/j.ibusrev.2016.04.005

- MacCallum, R. C., Browne, M. W., & Sugawara, H. M. (1996). Power analysis and determination of sample size for covariance structure modeling. Psychological Methods, 1(2), 130–149. https://doi.org/10.1037/1082-989X.1.2.130

- Mael, F. A., & Ashforth, B. E. (1992). Alumni and their alma mater: A partial test of the reformulated model of organizational identification. Journal of Organizational Behavior, 13(2), 103–123. https://doi.org/10.1002/job.4030130202

- McDonald, R. P. (1996). Path analysis with composite variables. Multivariate Behavioral Research, 31(2), 239–270. https://doi.org/10.1207/s15327906mbr3102_5

- McIntosh, C. N., Edwards, J. R., & Antonakis, J. (2014). Reflections on partial least squares path modeling. Organizational Research Methods, 17(2), 210–251. https://doi.org/10.1177/1094428114529165

- Miles, J., & Shevlin, M. (1998). Effects of sample size, model specification and factor loadings on the GFI in confirmatory factor analysis. Personality and Individual Differences, 25(1), 85–90. http://dx.doi.org/10.1016/S0191-8869(98)00055-5

- Miller, V. D., Allen, M., Casey, M. K., & Johnson, J. R. (2000). Reconsidering the organizational identification questionnaire. Management Communication Quarterly, 13(4), 626–658. https://doi.org/10.1177/0893318900134003

- Muhammad, I. A., Ashraf, S., & Sarfraz, M. (2017). The organizational identification perspective of CSR on creative performance: The moderating role of creative self-efficacy. Sustainability, 9(11), 2125. http://dx.doi.org/10.3390/su9112125

- Naciti, V., Cesaroni, F., & Pulejo, L. (2021). Corporate governance and sustainability: A review of the existing literature. Journal of Management and Governance,2021, 1–20. https://doi.org/10.1007/s10997-020-09554-6

- National Action Plan on Business and Human Rights (2020). https://globalnaps.org/issue/small-medium-enterprises-smes/

- Naushad, M., & Malik, S. A. (2015). Corporate governance and bank performance: A study of selected banks in gcc region. Asian Social Science, 11(9), 226. https://doi.org/10.5539/ass.v11n9p226

- Nguyen, T., Pham, T., Le, Q., Pham, T., Bui, T., & Nguyen, T. (2020). Impact of corporate social responsibility on organizational commitment through organizational trust and organizational identification. Management Science Letters, 10(14), 3453–3462. https://doi.org/10.5267/j.msl.2020.5.032

- Nicola, M., Alsafi, Z., Sohrabi, C., Kerwan, A., Al-Jabir, A., Iosifidis, C., Agha, R., & Agha, R. (2020). The socio-economic implications of the coronavirus pandemic (COVID-19): A review. International Journal of Surgery, 78(2020), 185–193. https://doi.org/10.1016/j.ijsu.2020.04.018

- Nikolić, J., & Zlatanović, D. (2018). Corporate governance and corporate social responsibility synergies: A systemic approach. Nase Gospodarstvo: NG, 64(3), 36–46. http://dx.doi.org/10.2478/ngoe-2018-0016

- Organisation for Economic Co-operation and Development. (2018). Financing SMEs and entrepreneurs 2018: An OECD scoreboard. OECD Publishing. https://doi.org/10.1787/fin_sme_ent-2018-16-en

- Porter, M., & Kramer, M. (2002). The competitive advantage of corporate philanthropy. Harvard Business Review, 80(12), 56–68.

- Qureshi, M. A., Kirkerud, S., Theresa, K., & Ahsan, T. (2020). The impact of sustainability (environmental, social, and governance) disclosure and board diversity on firm value: The moderating role of industry sensitivity. Business Strategy and the Environment, 29(3), 1199–1214. 10.1002/bse.2427

- Rashid, K., & Islam, S. M. N. (2013). Corporate governance, complementarities and the value of a firm in an emerging market: The effect of market imperfections. Corporate Governance: The International Journal of Business in Society, 13(1), 70–87. https://doi.org/10.1108/14720701311302422

- Rehman, A., & Hashim, F. (2021). Can forensic accounting impact sustainable corporate governance? Corporate Governance, 21(1), 212–227. https://doi.org/10.1108/CG-06-2020-0269

- Reinartz, W., Haenlein, M., & Henseler, J. (2009). An empirical comparison of the efficacy of covariance-based and variance-based SEM. International Journal of Research in Marketing, 26(4), 332–344. https://doi.org/10.1016/j.ijresmar.2009.08.001

- Sameer, I. (2021). Impact of corporate social responsibility on organization’s financial performance: Evidence from Maldives public limited companies. Future Business Journal, 7(1), 29. https://doi.org/10.1186/s43093-021-00075-8

- Shu, P.-G., & Chiang, S.-J. (2020). The impact of corporate governance on corporate social performance: Cases from listed firms in Taiwan. Pacific-Basin Finance Journal, 61(2020), 101332. https://doi.org/10.1016/j.pacfin.2020.101332

- Spitzeck, H., & Lenssen, G. (2009). The development of governance structures for corporate responsibility. Corporate Governance: The International Journal of Business in Society, 9(4), 495–505. https://doi.org/10.1108/14720700910985034

- Su, C., Lee, E. M., & Lee, Y. (2019). An empirical research of environment management strategy: Exploring The relationships among perceived corporate social responsibility, organizational trust, perceived external prestige and organizational identificatioN. International Journal of Organizational Innovation, 12(1), 245–260.

- Tarigan, J., & Stacia, L. (2019). Corporate social responsibility policies and value creation: Does corporate governance and profitability mediate that relationship? Investment Management & Financial Innovations, 16(2), 270–280. http://dx.doi.org/10.21511/imfi.16(2).2019.23

- Thanh Tiep, L., Quang Huan, N., Thi Thuy Hong, T., & Khoa Tran, D. (2021). The contribution of corporate social responsibility on SMEs performance in emerging country. Journal of Cleaner Production, 322(2021), 129103. https://doi.org/10.1016/j.jclepro.2021.129103

- The World Bank Group (2020). https://www.worldbank.org/en/topic/smefinance#

- Thomsen, S. (2005). Corporate governance as a determinant of corporate values. Corporate Governance, 5(4), 10–27. https://doi.org/10.1108/14720700510616569

- Tuan, V. K. (2020). Analysis of challenges and opportunities for Vietnamese SMEs in the globalization. Journal of Business Management and Economic Research, 4(2), 169‐185. https://doi.org/10.29226/TR1001.2020.192

- Turker, D. (2009). How corporate social responsibility influences organizational commitment. Journal of Business Ethics, 89(2), 189–204. https://doi.org/10.1007/s10551-008-9993-8

- Van Puyvelde, S., Caers, R., Du Bois, C., & Jegers, M. (2012). The governance of nonprofit organizations: Integrating agency theory with stakeholder and stewardship theories. Nonprofit and Voluntary Sector Quarterly, 41(3), 431–451. https://doi.org/10.1177/0899764011409757

- Voss, Z. G., Cable, D. M., & Voss, G. B. (2006). Organizational identity and firm performance: What happens when leaders disagree about “who we are? Organization Science, 17(6), 741–755. http://dx.doi.org/10.1287/orsc.1060.0218

- Warrad, L., & Khaddam, L. (2020). The effect of corporate governance characteristics on the performance of Jordanian banks. Accounting, 6(2), 117–126. http://dx.doi.org/10.5267/j.ac.2019.12.001

- Welford, R. (2007). Corporate governance and corporate social responsibility: Issues for Asia. Corporate Social Responsibility and Environmental Management, 14(1), 42–51. https://doi.org/10.1002/csr.139

- Xie, J., Nozawa, W., Yagi, M., Fujii, H., & Managi, S. (2019). Do environmental, social, and governance activities improve corporate financial performance? Business Strategy and the Environment, 28(2), 286–300. 10.1002/bse.2224

- Zabri, S. M., Ahmad, K., & Wah, K. K. (2015). Corporate governance practices and firm performance: Evidence from top 100 public listed companies in Malaysia. Procedia Economics and Finance, 35(2016), 287–296. http://dx.doi.org/10.1016/S2212-5671(16)00036-8

- Zhang, M. F., Dawson, J. F., & Kline, R. B. (2020). Evaluating the use of covariance-based structural equation modelling with reflective measurement in organizational and management research: A review and recommendations for best practice. British Journal of Management, 32(2), 257–272. https://doi.org/10.1111/1467-8551.12415

- Zollo, L., Laudano, M. C., Boccardi, A., & Ciappei, C. (2019). From governance to organizational effectiveness: The role of organizational identity and volunteers’ commitment. Journal of Management & Governance, 23(1), 111–137. http://dx.doi.org/10.1007/s10997-018-9439-3