?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to examine the market reaction to the Covid-19 pandemic using stocks listed on the LQ45 Index, by using the event study method to calculate and analyze the difference in Average Abnormal Return (AAR) and Trading Volume Trading (TVA) during the Covid-19 pandemic that occurred in Indonesia. The population for the study is companies listed on the LQ45 Index with a sample of 41 companies taken by purposive sampling technique. Statistical analysis was conducted by using events study with paired sample t-test in determining the abnormal return difference test for each event. The first finding was that the LQ45 stock market reacted positively since the confirmation of the Covid-19 outbreak in Wuhan, China, as investors did not consider this information bad news. Second, LQ45 shares have shown a decline since the first confirmed Covid-19 patients in Indonesia. Third, the announcement of a pandemic by the World Health Organization (WHO) continued until the Jakarta regional lockdown in April 2020 made LQ45 respond negatively. The market began to respond positively after the first vaccination in Indonesia in January 2021. Overall, the results show that the LQ45 stock market has responded quickly to the Covid-19 pandemic from the start events and responses vary over time depending on events during the pandemic. Investors tend to be quick to respond to any event so that stock movements are very difficult to project. This research concludes that the negative impact occurred on the stock market in Indonesia could be attributed to the Covid-19 pandemic.

PUBLIC INTEREST STATEMENT

Since being declared a global pandemic, Covid-19 has had a significant impact on all sectors of the world economy. This negative impact occurred after the World Health Organization (WHO) declared it a global pandemic, and lockdowns in various countries in particular this effect lowered the confidence of global stock markets, including in Indonesia. The increase in the LQ45 index shares in the Jakarta Composite Index (JCI) has occurred gradually since the vaccination was intensively carried out in January 2021. Companies in the LQ45 can maintain their performance in the midst of the Covid-19 pandemic by taking advantage of the role of digitalization, especially in marketing services, banking and telecommunication companies. Meanwhile, investors are advised to choose companies with a low risk level during the Covid-19 pandemic and choose investment instruments in telecommunication companies and food & beverage companies because of the increase in online-based jobs that encourage public consumption.

1. Introduction

The transmission of Covid-19 spread widely in China and to more than 190 countries and territories since its first confirmed case in Wuhan, China (Susilo et al., Citation2020; Zu et al., Citation2020). Formally, World Health Organization (WHO) announced Covid-19 as a global pandemic in March 2020. Since the announcement, the stock market has experienced a negative significant decline coupled with the increasing number of confirmed cases which is bad news for the stock market (Ashraf, Citation2020; Baker et al., Citation2020; Gherghina et al., Citation2020; Harjoto et al., Citation2021; Rahman et al., Citation2021; Wang & Wang, Citation2021; Xiong et al., Citation2020; Yong & Laing, Citation2021). The Covid-19 outbreak caused many problems, one of which was the health impact and indirectly had an impact on economic conditions (Putranti et al., Citation2020). Most of the countries affected are proof that there is instability in economic conditions even on a global scale (Burhanuddin & Abdi, Citation2020).

Many countries in preventing and reducing the rate of transmission of the Covid-19 outbreak have made efforts to lockdown, quarantine areas, to large-scale social curbs (PSBB/Pembatasan Sosial Berskala Besar). Indonesia, for example, has issued a warning regarding this outbreak. The government has comprehensively made efforts to suppress the spread of this outbreak with many areas imposing tight social curbs, land and sea transportation restricted and many flights being stopped in many countries. Many industries stopped producing and the human movement was also prevented between countries, provinces, districts, and cities. As a result of this government policy, it makes economic activity unstable. Bash (Citation2020), Ashraf (Citation2020), and Baker et al. (Citation2020), empirically proved that the stock market in the affected countries and several global indexes experienced a significant decline. They analyzed the increase in the number of confirmed Covid-19 patients globally with the result being that the market tends to decline on this information. As a result of the Covid-19 outbreak, there is uncertainty in the stock market in Australia, so the role of the government is needed in efforts to recover and restore confidence in the stock market (Rahman et al., Citation2021). The results of research conducted by Harjoto et al. (Citation2021) showed that there are differences in volatility and trading volume in developed and developing countries where investors react more to emerging markets. Other empirical evidences showed that market efficiency on the S&P 500 Index has decreased the most compared to the efficiency of the Bitcoin market during the extreme Covid-19 events (Wang & Wang, Citation2021).

Countries affected by the Covid-19 outbreak have shown poor economic conditions, especially in the stock market. This condition caused many investors to suffer losses, but on the other hand, they also benefited from issuers that performed well during the pandemic. The government as a regulator in making policies needs to pay close attention to the condition of the stock market. Without proper policy, it will result in a continuous outbreak. Cepaluni et al. (Citation2021) argue that countries with democratic political systems have less effective policy responses. The phenomenon of the Covid-19 outbreak caused a new, unexpected reaction so that the market response was unable to anticipate which resulted in stock investors reacting negatively. This can be seen in the decline in the volatility of stock returns. It was noted that the Jakarta Composite Index (JCI) experienced a significant decline in mid-March 2020 after the announcement of first case in Indonesia, where the lowest position JCI touched the level of 3,937.63. Until the end of 2020, the JCI has not been able to return to the level where it was before Covid-19 and is still at the level of 5,621.71. This affects the behavior of investors because they are concerned about their funds. The Covid-19 outbreak reflects negative information or bad news. Several times, Indonesia Stock Exchange took steps to suspend trading temporarily or trading halt because the JCI had depreciated by up to 4%.

This study aims to examine the market reaction to the Covid-19 pandemic using stocks listed on the LQ45 Index, by using the event study method to calculate and analyze the difference in Average Abnormal Return (AAR) and Trading Volume Trading (TVA) during the Covid-9 pandemic in Indonesia. By using purposive sampling technique with the analysis technique of events study, the contribution in this study will be a benchmark for comparison of existing research. More specifically, this research determined the formulations in this problem are, firstly, about the Abnormal Return and Trading Volume Activity that occurred during the Covid-19 pandemic event using stocks listed on the LQ45 Index, and secondly, about the differences in Abnormal Return and Trading Volume Activity that occurred during the Covid-19 Pandemic in stocks listed on the LQ45 Index.

2. Literature review

The capital market as a place for stock transactions is an avenue for investors. As for those who need funds, in this case, the company can invest without having to wait for funds from the company’s operations (Pratama et al., Citation2015). Tandelilin (Citation2010) believes that the capital market in trading securities is based on the party having excess funds as a source of proceeds for the company. In the event of a meeting between various parties, the company can sell shares and bonds. It can be interpreted that there are long-term and short-term financial instruments such as debt, equity, and other instruments in transactions on the capital market (Mansyur, Citation2021; Nupus & Ichwanudin, Citation2021).

Investors will behave when there is positive information as a good signal. Hartono (Citation2010) believes that a positive event direction is a good news in the hope that the market will react positively, while the negative event direction will be bad news so that the market responds negatively. This opinion implies that the market response to good news will likely provide economic value and vice versa, negative market response is more likely credited by bad news. Event studies were first introduced by Dolley (Citation1933) stating that most stock prices reacted positively to the stock split event. Ball and Brown (Citation1968), Beaver (Citation1968), and Fama et al. (Citation1969) stated that there are benefits from accounting profit figures by examining the information content and its timeliness. By publishing information on an event, there is a market reaction that occurs by studying the information content (Fakhimuddin et al., Citation2021; Hartono, Citation2010). Moreover, Strong (Citation1992) revealed that there is a relationship between the price of securities and economic growth. This method is used to measure the extent to which a certain event affects stock prices. Hartono (Citation2010) explained the reasons why event studies are widely used. First, event studies are used to analyze the effect of an event on firm value. The second reason is that the event study directly measures the effect of events on the company’s stock price at the time the event occurred.

Measuring the magnitude of the impact of an event by assessing the speed at which stock prices react to events is used as an assessment of market efficiency (Bodie et al., Citation2013). It is said to be an efficient market where the price of traded securities reflects all available information. Price changes in the market are influenced by information that is an opinion (Riswanto, Citation2021; Tandelilin, Citation2010). Fama (Citation1970) classifies three forms of an efficient market, including weak form, half strong, and strong efficient market. In the assumption of market efficiency, McWilliams and Siegel (Citation1997) found three assumptions of market efficiency namely market efficiency, unanticipated events, and no adverse effects along with the event window. Referring to the opinion on market efficiency, there is an element of the speed of adjustment of securities prices so that it reflects all available information.

Abnormal return is the difference from the actual return to the normal return which is a retraction of investors’ expectations, while the Cumulative Abnormal Return (CAR) is the amount of Abnormal Return from the first day to the last day (Hartono, Citation2010). Trading Volume Activity (TVA) is the sum of the volume of each trading transaction that occurs in securities within a certain time. According to Hamidi (Citation2008), to analyze stock price movements can use predictions of the trading volume.

3. Methodology

This research was conducted on stocks listed on the LQ45 Index during the research period, 2018 to 2021. The population of this study amounted to 45 stocks with sample selection criteria using purposive sampling with the following criteria:

1) The company has been listed on the LQ45 index as of the research period

2) The issuers publish complete closing price data during the research period

Based on those criteria, the final sample in this study amounted to 41 stocks. In this study, the data analysis technique uses descriptive analysis by looking at the graph of the movement of the average abnormal return and cumulative average abnormal return during the event period and statistical analysis using the paired sample T-test in determining the abnormal return difference test for each event.

The type of research used is an event study. According to Hartono (Citation2010), event study is also known as residual analyzes or abnormal performance index tests or market reaction tests by studying market reactions to the Covid-19 pandemic events. Using the estimated period of 300–400 days to calculate the estimated return, the study period during the Covid-19 pandemic, and to measure each event using the 11-day window period where 5 days before, 1 day of the event date, and 5 days after the event. This research was conducted using data on companies registered in the LQ45 index using the purposive sampling technique.

This study uses an estimated period of 300–400 days to calculate the estimated return. Furthermore, the research period during the Covid-19 pandemic to measure each event used a window period of 11 days where 5 days before, 1 day of the event date and 5 days after the event which can be depicted in .

Figure 1. Estimated and window period length.

Operational measurement of variables for this study refers to McWilliams and Siegel (Citation1997) and MacKinlay (Citation1997) in determining the actual return, mean-adjusted model, market model, abnormal return, and average abnormal return. Meanwhile, the measurement of trading volume refers to Foster (Citation1986) who calculated the trading volume and the average trading volume with the following formula:

Table

Abnormal Return

Average Abnormal Return

Data analysis techniques used descriptive analysis and statistical analysis paired sample t-test in determining the abnormal return difference test for each event.

4. Results

Descriptive statistics on each phenomenon that occurs when the Covid-19 pandemic is presented in .

Table 1. Descriptive Analysis AAR and ATVA before and after Wuhan first case of Covid19

From , there is an increase in the average AAR and TVA after the announcement of Covid-19 in Wuhan, China. Particularly in Indonesia, the first case of COVID-19 confirmed was on 2 March 2020. The descriptive results show that the data variants are heterogeneous with a high data distribution where the standard deviation value is greater than the average value.

Based on , there was a decrease in the average AAR and TVA after the first confirmed Covid-19 announcement in Indonesia with a high data distribution on share ownership. After the announcement, TVA has a homogeneous data distribution.

Table 2. AAR and ATVA before and after Indonesian first case of Covid-19

Based on , there is an average negative significant reduction in AAR after the announcement of the Covid-19 pandemic by WHO, there is high data deviation. Meanwhile, the average volume has an increase that is inversely proportional to stock returns, this is the effect of positive information that occurs both at home and abroad so that trade transactions have increased.

Table 3. Descriptive statistics of the Covid-19 pandemic announcement by WHO

Based on , there was a decrease in AAR and TVA after the announcement of the Jakarta Lockdown in April 2020. There was a high data deviation on AAR, low deviations occurred in trading volume. The companies with the lowest average occurred in the banking sector, and the health service sector company (Hakim, Citation2017), while the highest changes occurred in the mining sector company and the infrastructure sector.

Table 4. Descriptive statistics of Jakarta lockdown announcement

Based on , there is an increase in the average AAR and TVA after the first vaccination in Indonesia in January 2021, there is a high deviation with a standard deviation value of more than the average value. The existence of this information makes stock market conditions respond positively, as evidenced by the average trading volume increases by up to 190% every day. The companies with the lowest returns occurred in real estate companies and the highest change was in the mining sector.

Table 5. Descriptive statistics of the first time vaccination in Indonesia

showed that there is a difference in the Average Abnormal Return on 3–5 trading days on the stock exchange, where the average value increases after the event. This means that the stock market still responds positively and investors still have the opportunity to get the expected return. This condition also indicates the January effect on the LQ45 index. Trading Volume Activity test results show no difference in the average which is indicated by a significant value of more than 0.05. This means trading transactions are equally good before and after the event.

Table 6. Paired Sample T-Test Test Results Confirmed Covid-19 in Wuhan China

Based on the results of statistical tests in , there is no difference in the average abnormal return at the time of the announcement of the first confirmation of Covid-19 patients in Indonesia. This is evidenced by a significant value of more than 0.05. This means that investors tend to be careful in taking steps to transact on the stock market. The results are similar with Irmayani (Citation2021) and Khaulis (Citation2020). In another case with Trading Volume Activity, there is a significant difference between 1 and 4 trading days on the stock market. A decrease in the value of the transaction also decreases the trading volume, meaning that investors tend to sell their shares after the announcement event.

Table 7. Paired sample T-test after the first case of Covid-19 in Indonesia

The results of statistical tests presented in show that there is a significant negative Average Abnormal Return difference 2 days after trading on the stock exchange. The same result is shown by the average trading volume activity for 2 to 3 trading days on the exchange. The difference between the two instruments is due to the effect of the announcement of the global pandemic so that the market quickly responds negatively, in addition to that the decline in trading volume causes investors to be cautious in conducting transactions on the stock market. The increase in the number of confirmed cases and the number of deaths worldwide due to the Covid-19 outbreak resulted in a negative reaction to the stock market and a decline in investor confidence. These results are supported by some research (Ashraf, Citation2020; Baker et al., Citation2020; Bash, Citation2020; Sobar et al., Citation2021) demonstrating that since the announcement of a global pandemic by the World Health Organization the stock market has rapidly declined.

Table 8. Paired sample T-Test for WHO announcement of the Covid-19 pandemic

The results of statistical tests show that there are significant differences in Average Abnormal Return and Trading Volume Activity in 1–5 trading days on the stock exchange (). The fact is that the confirmed cases of Covid-19 in Indonesia, especially the Jakarta area, are increasing so that the Government has taken a stance to carry out a lockdown. The impact is proven to make the stock market corrected again. The unanticipated event made investors even more depressed because the lockdown was carried out in the Capital Region it would have a huge impact on the economy so that companies could not carry out their activities due to the policy.

Table 9. Paired samples T-Test after Jakarta lockdown

Statistical results using the Wilcoxon test on Average Abnormal Return show a significant difference (). It is known that the average score after the event showed an increase. This means that the information signal is positive so that it has a good impact on the stock market. The increasing volatility of returns has made investors believe in the government’s steps in making decisions to inject vaccines in Indonesia. On the other hand, the trading volume did not show any significant difference. This is due to the pattern of investors still waiting for 2nd vaccination, usually conducted 14 days after the 1st vaccination.

Table 10. Paired sample T-Test & Wilcoxon test for the first vaccination in Indonesia

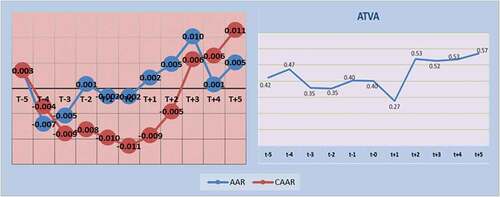

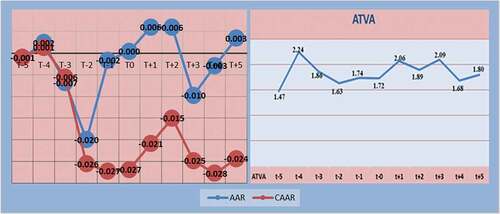

about the movement of the Average Abnormal return for LQ45 Index stocks showed a varied pattern that tends to be in a negative position. On 30 December 2019, China announced that it was confirmed that Covid-19 in Wuhan, the pattern of the AAR movement experienced an appreciation for up to 3 trading days. It is known that this effect occurs due to the January Effect where investors tend to buy shares at the beginning of the year as evidenced by the trading volume that tends to increase. With the information on Covid-19 in Wuhan China, the chances of getting the return that investors expect are still good.

Figure 2. AAR, CAAR & TVA after Wuhan’s first case of Covid-19. Source: data processing, 2021.

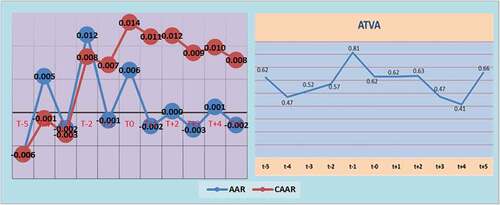

analyzing the Average Abnormal Return movement before the date of confirmation of Covid-19 patients in Indonesia tends to fluctuate highly. Until there is a negative drop after the date of the event. It can be seen that investors tend to be cautious in their transactions on the LQ45 index stock market. Moreover, this is the first case in Indonesia where investor concerns will continue if this outbreak continues to increase. The pattern of trading volume movements tends to fluctuate, which showed the decline in investor interest in making transactions on the stock market.

Figure 3. AAR, CAAR & ATVA after Announcement of Indonesian first case of Covid-19. Source: data processing, 2021.

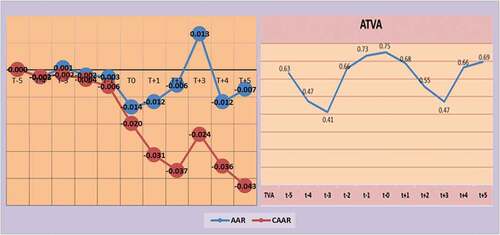

The increasing number of confirmed cases and cases of death due to the Covid-19 outbreak has made the World Health Organization take decisive steps in dealing with this, as evidenced by the fact that since it was announced as a global pandemic, the stock market has depreciated deeply (). Empirical evidence in this study supports previous studies showing significant declines in stock markets in several countries and in global indices (Ashraf, Citation2020; Baker et al., Citation2020; Bash, Citation2020; Wahyuni & Praninta, Citation2021). Harjoto et al. (Citation2021) revealed a decline in stock returns due to the increase in deaths, and the most influential was the stock market of developing countries. In addition, a more specific effect occurs in developing countries that are economically connected to several developed countries which makes the stock market experience pressure with an economic slowdown (Fernandez-Perez et al., Citation2021). Also, as a developing country that is economically connected to cooperation with several developed countries, the stock market is under pressure with a weakening economy (Fernandez-Perez et al., Citation2021). When viewed on the movement of the LQ45 index, the stock market responds very quickly to this information. The volatility of the decline occurs on the day the information is announced. This condition makes foreign investors choose not to transact on the stock market to protect their funds. However, the government quickly took several policies related to the handling of the Covid-19 outbreak by providing stage II stimulus assistance to provide employee tax incentives, import taxes, and relaxation of imports of incoming goods amounting to 147.9 trillion. Not only domestic policy, but the decline in US bank interest rates also caused the stock market to experience a significant increase. However, this condition did not last long, because this policy was only a temporary measure to safeguard the United States economy due to the Covid-19 outbreak. Foreigners recorded net sales of 258.5 trillion again on the 4th trading day. This is because Bank Indonesia did not respond to the FED policy of participating in lowering interest rates. So that investors tend to sell their shares.

Figure 4. AAR, CAAR & ATVA after WHO announcement of the Covid-19 pandemic. Source: data processing, 2021.

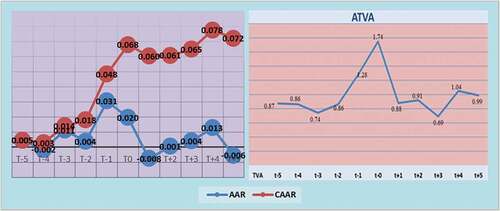

The increasing number of Covid-19 cases in Jakarta prompted the government to take steps to carry out a lockdown (). The return of the stock market responded negatively to this policy where quickly the response of investors was so bad that the stock market experienced a decline after 1 trading day. There was an increase in the volatility of stock returns up to 4 trading days where investors tend to be very quick in responding to any news so that movements are very difficult to predict. Stock volatility declined again on the 5th day of trading. This was due to Bank Indonesia still maintaining its 7day reverse repo rate of 4.5% ().

Figure 5. AAR, CAAR & ATVA after Jakarta Lockdown Announcement. Source: data processing, 2021.

Figure 6. AAR, CAAR & ATVA for the First Vaccination in Indonesia. Source: data processing, 2021.

The government announced that it had bought 2 million doses of the Sinovac vaccine from China, which investors welcomed the news to restore investor confidence in the stock market. Until 13 January 2021, the government officially injected vaccines in Indonesia, which made the stock market react positively (). The findings showed that where there is an increase in stock market volatility, there are still indicators of anxiety about the increase in the Covid-19 case. The weakening of the rupiah exchange rate against the US dollar was bad news for the stock market so that it experienced a significant decline on the 3rd day of trading. Investor patterns that are increasingly difficult to predict make stock market performance unstable. Overall, the findings are in line with previous studies demonstrating abnormal return in stock market during Covid-19 pandemic (Dang Ngoc et al., Citation2021; Fernandez-Perez et al., Citation2021; Gherghina et al., Citation2021; Rouatbi et al., Citation2021).

5. Conclusions

The results of the study found that there was AAR and ATVA at the beginning of the confirmation of Covid-19 in Wuhan China showed an upward trend, decreased volatility was seen at the time of the announcement of Covid-19 in Indonesia, a significant negative decline occurred when the World Health Organization (WHO) announced the Covid-19 outbreak. as a global pandemic. Until the announcement of the lockdown in Jakarta in April 2020, it was seen in the volatility of returns and fluctuating trade volume. The return of investor confidence in stocks occurred in January 2021 when the Indonesian government officially conducted the first vaccination. Statistically, the announcement of the Jakarta lockdown showed a significant negative difference, while the incidence of vaccination in Indonesia showed a significant and positive difference.

Some important points are needed to specify. First, this study empirically provides evidence that the LQ45 index stock market showed an increasing trend at the beginning of the confirmed Covid-19 in Wuhan China, the volatility of stock returns has decreased since the confirmation of Covid-19 patients in Indonesia, to concerns about the spread of the outbreak throughout the world. The negative impact occurred after the World Health Organization announced it was a global pandemic and continued until the Jakarta government carried out an area lockdown, resulting in the loss of investor confidence in the stock market. The increased mobility has been seen since the government gave the first vaccine in Indonesia in January 2021.

The conclusion of the study was obtained by analyzing five events from the initial confirmation of Covid-19 in Wuhan, China in December 2019 until the announcement of the first vaccine administration in Indonesia in January 2021. The results of the research can be elaborated on several important points. At first, the LQ45 stock market reacted positively since the confirmation of the Covid-19 outbreak in Wuhan. This reaction occurs because investors consider the information not likely to be bad news. A significant decline has occurred since the first confirmed Covid-19 patients in Indonesia, to concerns about the spread of the epidemic and the increase in confirmed patients in various countries.

The negative impact occurred after the World Health Organization (WHO) announced the Covid-19 outbreak as a global pandemic, and the implementation of a regional lockdown in Jakarta. in April 2020. This was marked by the loss of investor confidence in the stock market.

The limitation in this study is that it only uses stocks listed on the LQ45 index. As a theoretical recommendation, further research is expected to use all shares in JCI with a longer period. Managerially, companies included in the LQ45 are advised to maintain performance amid the Covid-19 pandemic, and take advantage of the role of digitalization, especially companies marketing services, banking, telecommunications or other industries. For investors, it is advisable to choose companies with a low level of risk during the Covid-19 pandemic and choose investment instruments in telecommunication companies and food & beverage companies in connection with increasing online-based services and people’s consumption needs.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Muhammad Yunus Kasim

Muhammad Yunus Kasim is lecturer of Master of Management Postgraduate Study Program at Tadulako University. His research interest include. His research interest includes financial management science. Muslimin is professor of financial management and lecturer of Master of Management Postgraduate Study Program at Tadulako University. His research interests are SMEs and Financial Performance. I Kadek Bellyoni Dwijaya is student of Master of Management Postgraduate Study Program at Tadulako University. His research interests are in economics and financial management.

References

- Ashraf, B. N. (2020). Stock Markets’ Reaction to COVID-19: Cases or Fatalities? Research in International Business and Finance, 54, 101249. https://doi.org/10.1016/j.ribaf.2020.101249

- Baker, S. R., Bloom, N., Davis, S. J., Kost, K., Sammon, M., & Viratyosin, T. (2020). The unprecedented stock market reaction to COVID-19. The Review of Asset Pricing Studies, 10(4), 742–15. https://doi.org/10.1093/rapstu/raaa008

- Ball, R., & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research, 6(2), 159–178. https://doi.org/10.2307/2490232

- Bash, A. (2020). International evidence of COVID-19 and stock market returns: An event study analysis. International Journal of Economics and Financial Issues, 10(4), 34–38. https://doi.org/10.32479/ijefi.9941

- Beaver, W. H. (1968). The information content of annual earnings announcements. Journal of Accounting Research, 6, 67–92. https://doi.org/10.2307/2490070

- Bodie, Z., Kane, A., & Marcus, A. (2013). EBOOK: Essentials of investments (Global Edition. McGraw-Hill Education (UK). ed.).

- Burhanuddin, C. I., & Abdi, M. N. (2020). Krisis ekonomi global dari dampak penyebaran virus corona (Covid19). AkMen Jurnal Ilmiah,17(1), 90–98. https://e-jurnal.nobel.ac.id/index.php/akmen/article/view/866/823.

- Cepaluni, G., Dorsch, M., & Branyiczki, R. (2021). Political regimes and deaths in the early stages of the COVID-19 pandemic. Journal of Public Finance and Public Choice. ahead-of-print. https://doi.org/10.1332/251569121X16268740317724.

- Dang Ngoc, H., Vu Thi Thuy, V., & Le Van, C. (2021). Covid 19 pandemic and abnormal stock returns of listed companies in Vietnam. Cogent Business & Management, 8(1), 1941587. https://doi.org/10.1080/23311975.2021.1941587

- Dolley, J. C. (1933). Characteristics and procedure of common stock split-ups. Harvard Business Review, 11(3), 316–326.

- Fakhimuddin, M., Khasanah, U., & Trimiyati, R. (2021). Database management system in accounting: assessing the role of internet service communication of accounting system information. Research Horizon, 1(3), 100–105. https://doi.org/10.54518/rh.1.3.2021.100-105

- Fama, E. F., Fisher, L., Jensen, M. C., & Roll, R. (1969). The adjustment of stock prices to new information. International Economic Review, 10(1), 1–21. https://doi.org/10.2307/2525569

- Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work. The Journal of Finance, 25(2), 383–417. https://doi.org/10.2307/2325486

- Fernandez-Perez, A., Gilbert, A., Indriawan, I., & Nguyen, N. H. (2021). COVID-19 pandemic and stock market response: A culture effect. Journal of Behavioral and Experimental Finance, 29, 100454. https://doi.org/10.1016/j.jbef.2020.100454

- Foster, G. (1986). Financial Statement Analysis. Prentice-Hall.

- Gherghina, Ș. C., Armeanu, D. Ș., & Joldeș, C. C. (2020). Stock market reactions to Covid19 pandemic outbreak: quantitative evidence from ARDL bounds tests and granger causality analysis. International Journal of Environmental Research and Public Health, 17(18), 6729. https://doi.org/10.3390/ijerph17186729

- Gherghina, Ș. C., Armeanu, D. Ș., & Joldeș, C. C. (2021). COVID-19 pandemic and Romanian stock market volatility: A GARCH approach. Journal of Risk and Financial Management, 14(8), 341. https://doi.org/10.3390/jrfm14080341

- Hakim, F. (2017). The Influence of non-performing loan and loan to deposit ratio on the level of conventional bank health in Indonesia. Arthatama, 1(1), 35–49. https://arthatamajournal.co.id/index.php/home/article/view/9

- Hamidi, M. (2008). Analisis Likuiditas Saham Sebelum, Saat dan Sesudah Bencana Banjir Antara Tahun 2007-2008 di Ibukota Jakarta (Studi Pada Industri Dasar dan Kimia di BEI) [Undergraduate thesis]. Faculty of Economics, Universitas Islam Negeri Malang.

- Harjoto, M. A., Rossi, F., Lee, R., & Sergi, B. S. (2021). How do equity markets react to COVID-19? Evidence from emerging and developed countries. Journal of Economics and Business, 115, 105966. https://doi.org/10.1016/j.jeconbus.2020.105966

- Hartono, J. (2010). Studi Peristiwa: Menguji Reaksi Pasar Modal Akibat Suatu Peristiwa. BPFE.

- Irmayani, N. W. D. (2021). Dampak Pandemic Covid 19 Terhadap Reaksi Pasar Pada Sektor consumer goods industry Di Bursa Efek Indonesia. E-Jurnal Ekonomi Dan Bisnis Universitas Udayana, 9(12), 1127–1240. https://doi.org/10.24843/EEB.2020.v09.i12.p05

- Khaulis, K. N. H. (2020). Reaksi pasar modal indonesia terhadap peristiwa virus corona. Jurnal Investasi Islam, 5(1), 43–58. https://doi.org/10.32505/jii.v5i1.1645

- MacKinlay, A. C. (1997). Event studies in economics and finance. Journal of Economic Literature, 35(1), 13–39. https://www.jstor.org/stable/2729691

- Mansyur, M. (2021). Marketing opportunities for bank syariah mandiri e-Banking services as a payment method. Research Horizon, 1(2), 71–80. https://doi.org/10.54518/rh.1.2.2021.71-80

- McWilliams, A., & Siegel, D. (1997). Event studies in management research: Theoretical and empirical issues. Academy of Management Journal, 40(3), 626–657. https://doi.org/10.5465/257056

- Nupus, H., & Ichwanudin, W. (2021). Business network accessibility, customer relationship management and value co-creation on family business performance. Research Horizon, 1(4), 126–135. https://doi.org/10.54518/rh.1.4.2021.126-135

- Pratama, I. G. B., Sinarwati, N. K., Darmawan, N. A. S., & Se, A. (2015). Reaksi Pasar Modal Indonesia Terhadap Peristiwa Politik (Event Study pada Peristiwa Pelantikan Joko Widodo Sebagai Presiden Republik Indonesia ke-7). JIMAT (Jurnal Ilmiah Mahasiswa Akuntansi) Undiksha, 3(1), 1–11. https://ejournal.undiksha.ac.id/index.php/S1ak/article/view/4754

- Putranti, H. R. D., Suparmi, S., & Susilo, A. (2020). Work life balance (WLB) complexity and performance of employees during Covid-19 pandemic. Arthatama, 4(1), 56–68. https://arthatamajournal.co.id/index.php/home/article/view/35

- Rahman, M. L., Amin, A., & Al Mamun, M. A. (2021). The COVID-19 outbreak and stock market reactions: Evidence from Australia. Finance Research Letters, 38, 101832. https://doi.org/10.1016/j.frl.2020.101832

- Riswanto, A. (2021). Competitive intensity, innovation capability and dynamic marketing capabilities. Research Horizon, 1(1), 7–15. https://doi.org/10.54518/rh.1.1.2021.7-15

- Rouatbi, W., Demir, E., Kizys, R., & Zaremba, A. (2021). Immunizing markets against the pandemic: COVID-19 vaccinations and stock volatility around the world. International Review of Financial Analysis, 77, 101819. https://doi.org/10.1016/j.irfa.2021.101819

- Sobar, A., Deni, A., Riswandi, R., Hamidi, D. Z., & Permadi, I. (2021). The effect of product turnover on company performance of SMEs. Research Horizon, 1(3), 115–119. https://doi.org/10.54518/rh.1.3.2021.115-119

- Strong, N. (1992). Modelling abnormal returns: A review article. Journal of Business Finance & Accounting, 19(4), 533–553. https://doi.org/10.1111/j.1468-5957.1992.tb00643.x

- Susilo, A., Rumende, C. M., Pitoyo, C. W., Santoso, W. D., Yulianti, M., Herikurniawan, H., Sinto, R., Singh, G., Nainggolan, L., Nelwan, E. J., & Chen, L. K. (2020). Coronavirus disease 2019: Tinjauan Literatur Terkini. Jurnal Penyakit Dalam Indonesia, 7(1), 45–67. https://doi.org/10.7454/jpdi.v7i1.415

- Tandelilin, E. (2010). Portofolio dan Investasi: Teori dan Aplikasi. Kanisius.

- Wahyuni, S., & Praninta, A. (2021). The influence of brand equity and service quality on purchase decisions on Garuda Indonesia airline services. Research Horizon, 1(1), 28–38. https://doi.org/10.54518/rh.1.1.2021.28-38

- Wang, J., & Wang, X. (2021). Covid-19 and financial market efficiency: Evidence from an entropy-based Analysis. Finance Research Letters, 42, 101888. https://doi.org/10.1016/j.frl.2020.101888

- Xiong, H., Wu, Z., Hou, F., & Zhang, J. (2020). Which Firm-specific characteristics affect the market reaction of Chinese listed companies to the COVID-19 Pandemic? Emerging Markets Finance and Trade, 56(10), 2231–2242. https://doi.org/10.1080/1540496X.2020.1787151

- Yong, H. H. A., & Laing, E. (2021). Stock market reaction to COVID-19: Evidence from US Firms’ international exposure. International Review of Financial Analysis, 76, 101656. https://doi.org/10.1016/j.irfa.2020.101656

- Zu, Z. Y., Jiang, M. D., Xu, P. P., Chen, W., Ni, Q. Q., Lu, G. M., & Zhang, L. J. (2020). Coronavirus disease 2019 (COVID-19): A perspective from China. Radiology, 296(2), E15–E25. https://doi.org/10.1148/radiol.2020200490