Abstract

An electronic wallet (e-wallet) is the digital equivalent of a physical wallet that can support cashless and contactless payment, thereby enabling consumers’ to meet the physical contact restrictions imposed to contain the spread of COVID-19. Hence, consistent with the increasing awareness of e-wallets, this study investigates consumers’ intention to use e-wallets. Drawing on the motivation-ability-opportunity (MAO) framework, we investigated the factors of consumers’ usage intention of e-wallets. The hypothesized model was tested using the survey data collected from 226 respondents in Malaysia. The results of partial modelling analysis of 226 respondents affirmed the significance of perceived COVID-19 risk, perceived government support, and facilitating conditions in influencing usage intention. However, effort expectancy was not a significant predictor. As hypothesized, facilitating conditions moderated the effects of effort expectancy and perceived government support on usage intention, but not that of perceived COVID-19 risk. Our findings demonstrated that motivation in terms of health risk avoidance and government incentives and opportunity in the form of facilitating conditions play significant roles in influencing the usage intention of e-wallets.

PUBLIC INTEREST STATEMENT

The outbreak of the COVID-19 pandemic and the enforced lockdown aimed at controlling movements have accelerated consumers’ adoption of electronic payments platforms. In Malaysia, for instance, there has been an 80% increase in electronic wallets transactions since the outbreak of the COVID-19 pandemic almost two years ago. This upsurge can be associated with the convenience of contactless payments in curbing the spread of COVID-19 by minimising physical cash transactions. Accordingly, our study investigates the continuous usage intention of electronic wallets among 226 consumers in Malaysia. We found that consumers who intend to continue to use e-wallets perceive the platforms as easy to use and are concerned about the risk of getting infected through physical cash transactions. Continuous usage intentions are also associated with their perceptions of sufficient government incentives for e-wallets adoption. Besides, their perceptions of ease of use are enhanced with adequate support by the e-wallets service providers. Interestingly, consumers’ perceptions of support from e-wallets service providers could neutralise the lack of government incentives.

1. Introduction

Cashless payment via electronic and digital platforms has contributed to exponential growth in e-commerce, and this trend has been accelerated with the outbreak of the COVID-19 pandemic. The virtual and contactless nature of e-wallet has made it a preferred payment platform in a period where physical distancing and movement restrictions have become normal (Ojo et al., Citation2021; Yang et al., Citation2021). Citing safety and cleanliness as critical factors, a global survey conducted by Mastercard during the March 2020 lockdown revealed a 25% growth in contactless payments at supermarkets, groceries, and pharmacies, with 79% and 91% of people globally and in the Asia Pacific region, respectively (Mastercard, Citation2020). Thus, the emerging consumption behavior toward the digitalization of services has gained traction amid the outbreak of COVID-19. This trend is likely to change most individuals’ hesitation for online purchases and transactions. Equally, consumers’ confidence and trust in electronic payment platforms has deepened with the increasing accessibility to the internet and enhanced security features, making services like electronic wallets (e-wallets) more accessible to consumers (Kassim et al., Citation2021; Li´ebana-cabanillas et al., Citation2015; Yang et al., Citation2021).

Several studies have investigated the adoption of mobile payment services (Kapoor et al., Citation2015; Li´ebana-cabanillas et al., Citation2015; Yang et al., Citation2021), yet the adoption rate of these platforms has remained low (De Kerviler et al., Citation2016; Teng & Khong, Citation2021). As a result, scholarly attention has shifted towards examining the barriers to e-wallets usage (Kaur et al., Citation2020; Leong et al., Citation2021; Teng & Khong, Citation2021). Kaur et al. (Citation2020) demonstrated value and risk barriers as the main inhibitors of usage intentions. Given the limited predictive relevance of the traditional survey methods, Teng and Khong (Citation2021) employed e-wallets’ actual usage data collected from social media platforms to clarify the adoption factors. The findings attributed the low adoption of e-wallets to the unfriendly interface and complexity of accessing incentives like cashback and rewards. Essentially, users need to commit more effort to navigate the unfriendly and complex interface. Not surprisingly, leading information systems (IS) models like the unified theory of acceptance and use of technology (UTAUT) and technology adoption model (TAM) have incorporated effort expectancy or perceived ease of use as one of the salient factors of usage intention and actual usage.

Drawing on the UTAUT model, previous studies have investigated usage intention from perceived ease of use, subjective norms, perceived security, perceived usefulness, social influence, satisfaction, self-efficacy, perceived trust (Soodan & Rana, Citation2020; Yang et al., Citation2021). Nevertheless, traditional IS models’ relevance and predictive power in explaining behavioral intention in different contexts have been questioned (Daragmeh et al., Citation2021; Macedo, Citation2017). Huterska et al. (Citation2021) noted that the traditional models posit the social characteristics, incentives, and network externality underlying usage intentions and behavior under stable conditions. However, different factors are likely to motivate consumers’ usage intention amid the COVID-19 pandemic. For example, in response to the outbreak of the COVID-19 pandemic, recent studies on usage intention of mobile payment have considered perceived health risk an essential factor (Aji et al., Citation2020; Daragmeh et al., Citation2021; Huterska et al., Citation2021).

Sequel to the above, the objective of this study is to address the call for more research on consumers’ usage intention of contactless payments like e-wallets amid the uncertainty associated with the COVID-19 pandemic (Daragmeh et al., Citation2021; Huterska et al., Citation2021). Further to the literature, we draw on the motivation-ability-opportunity (MAO) framework in investigating the usage intention of e-wallets. In particular, we posit that the usage intention of e-wallets is influenced by ability and motivation, while the opportunity is the situational determinant of the action. Hence, we conceptualized perceived COVID-19 health risks and incentives in the form of government support as motivational factors. At the same time, effort expectancy is considered the potential users’ awareness of the necessary skills required to use e-wallets. The opportunity reflects the facilitating conditions, which entails the necessary resources to facilitate the motivational and ability factors.

The subsequent sections of this manuscript are structured as follows. After the introduction, the relevant literature was discussed, resulting in the development of hypotheses. Then the methodology was examined, followed by the results of data analyses. Furthermore, we discussed the implications of findings for theory and practices, and the final section presents the conclusion and areas of future research.

2. Literature review

2.1. E-wallets in Malaysia

The proliferation of smartphones and network technologies has contributed to the evolution of e-wallets as convenient and efficient mobile payment solutions (Teng & Khong, Citation2021). E-wallets are the digital equivalent of physical wallets, which allow users to keep and draw out money to pay for goods or services at participating merchants or transfer money to fellow users. They are mainly deployed as apps on smartphones and appropriately funded to serve as means of payment. Hence, consumers can preload a certain amount of money through different channels like internet banking or card on their e-wallets and then make online or offline payments (Chawla & Joshi, Citation2019). Payment or money is transferred by using the e-wallets apps on the smartphone to scan a quick response (QR) code or through the near-field communication (NFC) technology (Lu, Citation2018). The NFC allows data to be shared between enabled digital devices, such as smartphones, and payment terminals like the point of sale (POS). Unlike the NFC-based POS like Apple Pay and Samsung Pay, the QR code service requires low infrastructural investment, i.e., retailers only need to print out the QR code for consumers to scan and make payments (Lu, Citation2018).

From the first e-wallet service launched in Malaysia in January 2017, service providers have increased to more than 20 by the second quarter of 2020, with Boost, GrabPay, and Touch n’ Go dominating the market (Oppotus, Citation2020). The appreciable growth in the e-wallets segment in Malaysia has been corroborated by a recent survey from Mastercard, which reveals that the 40% usage rate of e-wallets in Malaysia is the highest in the Southeast Asia region. This increasing usage rate of e-wallets is not surprising because the Malaysian government has invested in promoting and creating awareness of the utility of e-wallets through initiatives like e-Tunai Rakyat, which is the disbursement of RM30 e-wallet credit to 15 million eligible Malaysians (Balakrishnan & Shuib, Citation2021; Yeap, Citation2020). In addition, service providers have also offered customers several promotions like cashback, rebates, and credits to attract users.

Similarly, the high ownership rate of smartphones has created tremendous market opportunities for e-wallets in Malaysia. As a result, many start-up companies and incumbent financial service providers have ventured into the market, intensifying competition and pushing for market share. The higher customer acquisition cost has created an unlevel landscape, with the smaller firms exiting the market or being acquired by the larger firms (Soodan & Rana, Citation2020). Thus, to be successful in the e-wallets space, the service providers must prioritize the factors salient to customer adoption of their services. Consequently, an empirical investigation of consumers’ usage intention of e-wallets can offer valuable insights into developing competitive e-wallet platforms in Malaysia and other emerging markets.

2.2. Ability-Motivation-Opportunity framework

Many studies have employed either TAM or UTAUT models to explain consumers’ acceptance of mobile payment platforms (Kwateng et al., Citation2019; Soodan & Rana, Citation2020; Yang et al., Citation2021). Ajzen’s (Citation1991) theory of planned behavior (TPB) conceptualized usage intention as dependent on attitude, social influence, and perceived behavioral control. The UTAUT model extended the TPB by incorporating the contextual factors of technology usage intentions (Venkatesh et al., Citation2003). However, the proliferation of technological and innovative platforms both within and outside the organizational context has necessitated the inclusion of other motivating factors of consumers’ behavioral intention and usage (Kwateng et al., Citation2019). For example, amid the outbreak of COVID-19, the contactless and cashless options provided by e-wallets have become attractive to both retailers and consumers to limit physical interaction and exchange (Yang et al., Citation2021). Hence, the MAO framework is proposed in investigating the usage intention of e-wallets.

The MAO framework is a meta-theory based on the high-level abstraction of the factors of human behavior (Bigné et al., Citation2015). Motivation is the will to perform, and it captures the psychological and emotional factors that affect an individual’s disposition toward achieving a given task. Ability reflects capacity, and it measures one’s physiological and cognitive capability to perform a given task effectively. It includes knowledge, skills, competencies, and other related cognitive factors. Furthermore, (Blumberg & Pringle, Citation1982) suggested a third factor called opportunity, which captures the external elements that may constrain an individual’s motivation and ability to perform a given task. Opportunity includes factors like physical conditions, actions of supervisors, co-workers, and organizational policies and procedures. Thus, MAO posits that individuals’ actions are influenced by their possession of the necessary skills, adequate motivation, and the opportunity to perform the given activity (Ojo et al., Citation2019).

Several studies have adapted the MAO as a meta-theory to explain behavior in different domains, including information systems (Ojo et al., Citation2019), management (Reinholt et al., Citation2011; Siemsen et al., Citation2008), and environmental studies (Baumhof et al., Citation2018; Fawehinmi et al., Citation2020). Based on the MAO framework, we postulate that the usage intention of e-wallets necessitates the appropriate motivation to use it, the right skills and knowledge to operate it, and the adequate resources to use it.

Motivation is a driving force that allows people to partake in action. The influence of motivation on e-wallets usage has been researched (Daragmeh et al., Citation2021; Yang et al., Citation2021), likewise the effect of attitude on usage intention (Ojo et al., Citation2019). Accordingly, the health risk associated with contracting COVID-19 through physical interaction can motivate the adoption of contactless technology for transactions. Adequate skills and knowledge of technology are critical to the usage of the technology. Studies have examined the ease of technology use on consumers’ acceptance (Daragmeh et al., Citation2021; Yang et al., Citation2021). Opportunity reflects the degree to which an individual possesses the enabling conditions to use an e-wallet (Jesuthasan & Umakanth, Citation2021). Individuals with adequate ability and motivation but lacking the opportunity to perform a given task might not execute such a task. As a result, opportunity in this study can be related to the facilitating condition, which makes the adoption of e-wallet a possibility when the above factors are readily available and accessible.

Based on the above arguments, this study investigates the perceived COVID-19 health risk and incentives in the form of government support (motivation), effort expectancy (ability), and facilitating conditions (opportunities) as determinants of usage intention e-wallets. Given the importance of a conducive environment in carrying out tasks, the facilitating conditions could be a moderator of the links between perceived COVID-19 health risk, effort expectancy, government supports, and usage intention of e-wallets. The conceptual model is presented in Figure .

Figure 1. Conceptual model.

2.3. Hypotheses development

2.3.1. Perceived COVID-19 health risk and usage intention of e-wallets

Perceived COVID-19 health risk is defined as the perception of consumers toward the severity of contracting COVID-19. Perceived health risks entail both the perceived susceptibility to infection and its seriousness. Perceived susceptibility is a “person’s view of the likelihood of experiencing a potentially harmful condition,” and perceived seriousness refers to ”how threatening the condition is to the person” (Jesuthasan & Umakanth, Citation2021). The perceived risk of outdoor activities can cause exercise avoidance in urban parks (Khozaei et al., Citation2021; Sreelakshmi & Prathap, Citation2020). Similarly, individuals may avoid direct contact with others because of the fear of contracting COVID-19. The fear of contracting COVID-19 due to its perceived harmful effect may make consumers avoid direct contact while transacting. Such fear may translate to situations where individuals avoid physical exchange due to the anxiety of dealing with cash that could be virally contaminated (Wisniewski et al., Citation2021). Hence, they may use e-wallets instead. According to Daragmeh et al. (Citation2021), perceived COVID-19 health risks significantly influence individuals’ intention to use mobile payments. Puriwat and Tripopsakul (Citation2021) demonstrated that the perceived seriousness of COVID-19 positively influences an individual’s decision to continue using contactless payment technology, as cash poses a greater danger of viral transmission. Hence, it is hypothesized that;

H1. Perceived COVID-19 health risk is significantly and positively associated with the usage intention of e-wallets.

2.3.2. Effort Expectancy and usage intention of e-wallets

It refers to the belief that using a given technology will be free of effort (Davis, Citation1989). It reflects the ease of using new technology (Kaur et al., Citation2020). Thus, effort expectancy captures the perceived ease of use in the earlier technology acceptance model (Soodan & Rana, Citation2020). Regarding e-wallets adoption, ease of use reflects the degree to which consumers perceive that using e-Wallets will require a minimum level of effort. The practical usage of specific technology like e-wallets requires basic digital skills and knowledge, making effort expectancy an essential determinant of usage intention (Davis, Citation1989). Effort expectancy has been determined to significantly influence the intention to adopt mobile banking and payment platform (Alalwan et al., Citation2017; Islam & Khan, Citation2021; Tak & Panwar, Citation2017). Nevertheless, other studies have found effort expectancy not related to intention to use mobile payment services (Ooi & Tan, Citation2016; Soodan & Rana, Citation2020). Given the mixed findings, it is pertinent to examine the influence of effort expectancy on the usage intention of e-wallets.

H2. Effort expectancy is significantly and positively associated with the usage intention of e-wallets.

2.3.3. Perceived government support and usage intention to adopt e-wallets

Perceived Government support reflects the belief that the government is entirely in support of e-wallets usage to minimize physical contact between consumers and merchants (Aji et al., Citation2020). Such support could entail government investments in required infrastructures, collaboration with the industries, establishing regulations, and a framework that facilitates the usage of e-wallets (Mandari et al., Citation2017). Chen et al. (Citation2020) pointed out that government support could positively affect intention by increasing users’ willingness to use e-wallet services. Government support acts as a driving force for technology adoption because it assures the user that the technology will operate in an orderly and well-managed way. A study found that government backing encouraged Fintech adoption (Hu et al., Citation2019). Mandari et al. (Citation2017) also revealed that government support is essential in motivating the adoption of mobile government services. Government support for e-wallet services could entail policy, access speed, and security guarantees to boost consumers’ confidence. Thus, when customers perceive adequate government support, they could be more receptive to using e-wallets. Based on this postulation, it is hypothesized that;

H3. Perceived government support is significantly and positively associated with the usage intention of e-wallets.

2.3.4. Facilitating conditions and intention to adopt e-wallets

Facilitating conditions refers to the users’ belief about the availability of adequate resources to enable them to use a system in completing a given task (Taylor & Todd, Citation1995; Venkatesh et al., Citation2003). Such conditions could be a significant determinant of usage behavior, wherein relevant resources and support could ease an individual’s intention to use a new system. For example, using technology such as contactless payment allows users to maintain social distancing when making payments (Huterska et al., Citation2021). Even though these conditions are outside an individual’s control, they could affect the performance of behaviors (Ojo et al., Citation2019). As noted by Mahardika et al. (Citation2019), facilitating conditions could entail access to the operators’ resources (i.e., network coverage), manufacturers’ resources (i.e., platform and operating systems), developers’ resources (i.e. applications), and users’ resources (mobile device). Studies have validated the significant influence of facilitating conditions on the usage intention of mobile banking services (Kwateng et al., Citation2019; Tak & Panwar, Citation2017). Accordingly, we hypothesized the influence of facilitating conditions on the usage intention of e-wallets.

H4. Facilitating conditions is significantly and positively associated with the usage intention of e-wallets.

2.3.5. Moderating effects of facilitating conditions and usage intention of e-wallets

Facilitating conditions are critical in users’ acceptance of technology (Ojo et al., Citation2019). In the case of e-wallets, these conditions may include the availability of quality network service or the operating system and the device connected to the service network (Mahardika et al., Citation2019). The perceived health risk of contracting COVID-19 through physical interactions could better enhance consumers’ intention to use e-wallets when the facilitating conditions, such as the easy access to getting the e-wallets, the compatibility and features to keep transactions secure are favourable. In essence, notwithstanding the perceived risks of contacting COVID-19, it may be challenging to use e-wallets when insufficient resources exist.

An individual might be restrained from performing a behavior if the environment precludes it or the facilitating conditions make it impossible. By removing any barriers to usage, facilitating conditions can ensure the ongoing utilization of technologies (Rao and Troshani, Citation2007), such as e-wallets. Regarding e-wallets, conditions such as mobile networks and data connection speed might influence the desire to embrace the e-wallets by determining whether they are simple to use or not (Venkatesh et al., Citation2012). Users’ perceptions of enabling conditions have been found to positively moderate the relationship between uncertainty and resistance to adopting new technology (Kim & Lee, Citation2016).

Government support is considered adequate when the conditions for using and adopting e-wallets become favorable. In essence, the enabling facilities need to be in places such as fast internet, trusted operating systems, and reliable applications for government support to influence consumers’ usage intention of e-wallets. When the conditions to use e-wallets is seamless, government support can better stimulate the usage intention. Hence, consumer usage intention could be enhanced when the favourable conditions of secure and seamless services are complemented with government incentives, pricing regulations, policies, and subsidies for device ownership (Mandari et al., Citation2017). Based on this postulation, it is hypothesized that;

H5a. Facilitating conditions moderate the effect of perceived COVID-19 health risk on usage intention of e-wallets.

H5b. Facilitating conditions moderate the effect of effort expectancy on usage intention of e-wallets.

H5c. Facilitating conditions moderate the effect of perceived government support on usage intention of e-wallets

3. Research methods

3.1. Data collection procedure

We employed an online survey as the main instrument for collecting data to test the hypothesized model. The initial draft of the survey was pretested with four researchers and three practitioners in the finance technology sector. Based on their feedback, we revised the questionnaire to improve the clarity of the questions. Using Google Form, the online cross-sectional survey was distributed to the sampled respondents. The online questionnaire has several benefits: cost-effectiveness, time-saving, and broader reach (Ojo et al., Citation2021). Given the lack of a sampling frame, the non-probability convenience sampling technique was employed in collecting data. The link to the survey was shared through email and social media platforms like Facebook and WhatsApp to solicit participation from consumers across Malaysia. We enclosed with each questionnaire a cover letter explaining the study’s objective, the need for voluntary participation, and a promise to maintain anonymity. The respondents were also asked to recruit their friends and family members as survey participants.

A total of 237 questionnaires were completed, but 11 cases were excluded from the data analysis due to missing values. About 60% of respondents were male, and 40% were female. Regarding age, 44.7% of the respondents were between 30 and 39 years, 18.1% were between 20 and 29 years, and the remaining 37.2% were above 40 years. Besides, 73.9% were married, 21.2% were single, and 4.9% were divorced or widowed. Regarding educational attainment, 63.3% of the respondents had a bachelor’s degree, 20.4 had a postgraduate degree, and 16.3% had a diploma certificate. In terms of monthly income, 41.6% earned less than RM3000 (i.e., USD714), 32.7% earned between RM3000 to RM10000, and 25.7% earned more than RM10000. These are consistent with the three income groups in Malaysia—where B40 is the bottom 40%, M40 is the middle 40%, and T20 represents the top 20% (Balakrishnan & Shuib, Citation2021).

3.2. Operationalizations and measurement

The measurement items for performance expectancy, facilitating conditions, and usage intention of e-wallets were adapted from (Venkatesh et al., Citation2003). The perceived COVID-19 health risks items were adapted from Olya and Al-ansi (Citation2018). Four items were adapted from the literature to measure perceived government support (Aji et al., Citation2020). Moreover, all the scales were based on the five-point Likert scale ranging from “1“ (Strongly Disagree) to ”5” (Strongly Agree). The complete measurement items are summarised in Table 1. Consistent with the literature, we considered age, educational attainment, and income control variables (Huterska et al., Citation2021).

3.3. Data analyses techniques

Using the Smart-PLS 3 package, we employed the PLS-SEM technique to assess the measurement and structural models. This non-parametric technique maximizes the endogenous latent constructs’ variance while minimizing the unexplained variance (Leguina, Citation2015). PLS has gained wider acceptability in exploratory research because of its robustness in predicting parameter estimates for revised measurement models (Hair et al., Citation2017; Henseler et al., Citation2009). The present study incorporates additional variables into the MAO framework, making the PLS an appropriate technique for evaluating the hypothesized relationships.

We followed the appropriate methodical and procedural steps to minimize the likely effects of common method bias (CMB) associated with data collection from a single source. For the procedural remedy, a cover letter was enclosed with each of the questionnaires (Ojo, Citation2021). This letter stated the purpose of the survey and promised to guarantee the respondents’ anonymity. Besides, Harman’s single factor test was conducted to examine the likely effect of CMB. The result reveals that the largest single factor accounts for 42.34% of the variance, lower than the suggested value of 50% (Podsakoff et al., Citation2003). Thus, CMB has not significantly affected the self-reported data.

Moreover, in line with (Peng & Lai, Citation2012), we employed the two stages for model estimation. At stage one, the validity and reliability of the measurement model were assessed, then in the second stage, the structural model was evaluated to test the hypothesized relationships.

4. Results

4.1. Measurement model

We evaluated the reliability of the measurement model based on the Cronbach alpha (α) and composite reliability (CR) values. The convergent and discriminant validity were also assessed from the average variance extracted (AVE) values and correlation matrix between constructs, respectively (Ojo & Fauzi, Citation2020; Peng & Lai, Citation2012). As shown in Table 1, the reliability of the measurement model is ascertained with all the α and CR values greater than the cut-off value of 0.7. Besides, the conditions for convergent validity were met: except for an item in government support, all the factor loadings were above the minimum value of 0.6, and AVEs greater than the cut-off value 0.5 (Fornell & Larcker, Citation1981; Peng & Lai, Citation2012).

The result of discriminant validity is reported in Table 2, which represents the comparison of the values of correlations between paired constructs and the square root of the AVE of each construct (i.e., the main diagonal). The higher values of AVEs revealed the discriminant validity of the constructs (Fornell & Larcker, Citation1981).

4.2. Structural model

Unlike the covariance-based SEM, the PLS is not based on the assumption of normal distribution. As a result, the bootstrapping procedure is required to estimate the significance level of the beta coefficients of the hypothesized paths (Ojo & Fauzi, Citation2020; Peng & Lai, Citation2012). The beta values and corresponding p-values for the parameter estimates are summarized in Table 3.

As hypothesized, our data supports the significant effects of perceived COVID-19 health risk (β = 0.200 p < 0.05), perceived government support (β = 0.259 p < 0.05), and facilitating conditions (β = 0.392 p < 0.05) on the usage intention of e-wallets, but the effect of effort expectancy (β = −0.031 p > 0.05) was not supported. Thus, H1, H3, and H4 were supported, but not H2. Following Cohen’s (Citation1988) recommendations, we considered the effect sizes of 0.02, 0.15, and 0.35 as small, medium, and large, respectively. As shown in Table 3, facilitating conditions have a medium effect size, while the other significant predictors have small effect sizes. Regarding control variables, only age was significantly associated with usage intention of e-wallets, wherein younger consumers demonstrated higher intention to use e-wallets than older ones (see, Table 3).

Furthermore, the model’s explanatory power was examined based on the coefficient of determination (R2) value. The R2 value of 0.605 indicates that the predictors can explain 60.5% of the variance in intention to adopt e-wallets. Consistent with the literature, our model’s predictive capability was assessed using Stone-Geisser’s (Q2) criterion. The obtained Q2 value of 0.414 is greater than zero, indicating our model’s substantial predictive capability (Peng & Lai, Citation2012).

4.3. Moderation analysis

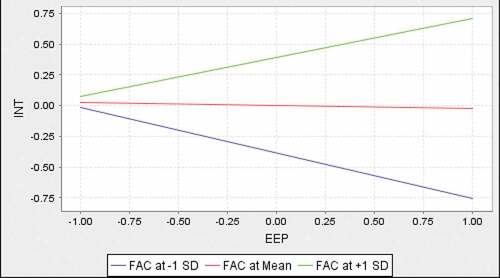

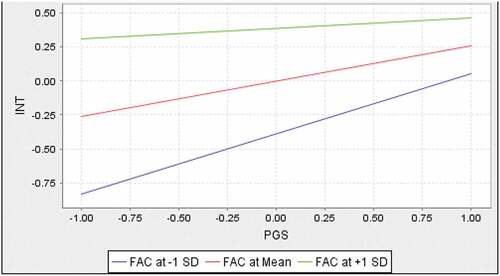

As hypothesized, the moderation analysis revealed that facilitating conditions does not significantly influence the link between perceived COVID-19 health risk and usage intention of e-wallets (β = −0197, p > 0.05), however facilitating conditions significantly influence the connections between effort expectancy and usage intention of e-wallets (β = 0.361, p < 0.05); and government support and usage intention (β = −0.197, p < 0.05). The interaction plot in Figure revealed that effort expectancy is positively associated with usage intention of e-wallets at higher levels of facilitating conditions. On the contrary, Figure revealed that government support is positively associated with usage intention of e-wallets at lower levels of facilitating conditions.

Figure 2. Effort expectancy by facilitating conditions interaction.

Figure 3. Government support by facilitating conditions interaction.

5. Discussion

Drawing on the MAO framework, this study investigates the factors of consumers’ usage intention of e-wallets among a sample of respondents in Malaysia. We contribute to knowledge by demonstrating the relevance of MAO in explaining the usage intention of e-wallets. In particular, we considered perceived COVID-19 health risk and government supports as motivation, effort expectancy as ability, and facilitating conditions as opportunity factors of consumers’ intention to adopt e-wallets. Furthermore, given the significance of a conducive environment in enabling actions, we examined the role of facilitating conditions in moderating the effects of perceived COVID-19 health risk, effort expectancy, and perceived government supports on intention to adopt e-wallet. The hypothesized model demonstrates appreciable predictive power with an R2 value of 0.605, which indicates that the variance explained by the significant factors, i.e., 60.5% is well above the acceptable level of 40% (Alalwan et al., Citation2017). The main theoretical implications of our findings are discussed in the next section.

5.1. Theoretical implications

As hypothesized, perceived COVID-19 health risk positively influences intention to adopt e-wallet. This result is in line with previous studies, which asserted that the health risk of contracting COVID-19 is a salient motivator for consumers to use contactless payment technology (Daragmeh et al., Citation2021; Jesuthasan & Umakanth, Citation2021; Puriwat & Tripopsakul, Citation2021). Also, this corroborates the IS literature, which demonstrated that the potential benefit of using a system, i.e., perceived usefulness, is a significant factor in usage intention (Alalwan et al., Citation2017; Islam & Khan, Citation2021). Hence, users who perceive e-wallets as valuable and essential in avoiding physical contact with cash prioritize health concerns and are more likely to be well disposed towards using them as a payment platform. For such users, intention stems from the e-wallets’ beneficial role in completing payment transactions by limiting contact, thereby affording touching likely COVID-19 droplets on physical cash.

Our data did not support the hypothesized effect of effort expectancy on usage intention of e-wallets. Nevertheless, this result is consistent with past studies, which revealed the lack of a significant relationship between perceived ease of use or effort expectancy and usage intention of mobile payment services (Daragmeh et al., Citation2021; Soodan & Rana, Citation2020). E-wallet is mainly available on handheld devices like smartphones, and their operation can be constrained by several factors, including internet access, operating speed, and interface display. However, e-wallets providers have continued to innovate their service delivery to minimize users’ effort in using their platforms. For example, recent advancements in user authentication like fingerprint and facial recognition have enhanced usage productivity by reducing effort. Accordingly, e-wallets have become easier to use, requiring little effort from potential users. Conversely, the lack of significance for effort expectancy could be due to the varying effort required in using a particular e-wallet service. Although there are more than 20 e-wallets in Malaysia, the three dominant players, i.e., Boost, GrabPay, and Touch’ n Go have similar functionalities. Yet, the respondents might have different experiences using them; therefore, effort expectancy for each e-wallet service requires further consideration.

Furthermore, the incentive provided through government support significantly influences the usage intention of e-wallets. This finding is in tandem with previous studies, which noted that consumers feel secure and safe to adopt e-wallets because they perceive the government is in full support of the initiative in terms of collaboration with the industry and favourable policies implementation (Aji et al., Citation2020; Hu et al., Citation2019; Mandari et al., Citation2017). In essence, the government has introduced relevant initiatives to support contactless payment by encouraging people to minimize physical interactions, thereby curtailing the spread of COVID-19.

The facilitating condition was also significantly related to the usage intention of e-wallets. This is consistent with previous studies, which assert that favourable conditions could allow consumers to have the propensity to adopt e-wallets (Hu et al., Citation2019; Rahman et al., Citation2020). The e-wallet services rely on network service providers and device manufacturers (Oppotus, Citation2020). In addition, a recent survey published by the Malaysian communications and multimedia commission revealed that 88.7% of the population are internet users, with 98.7% accessing the internet through their smartphones (MCMC, Citation2020). Therefore, the necessary resources like internet access and smartphone are widely available for users in Malaysia.

On the contrary, the moderating analysis showed that facilitating conditions did not significantly moderate the link between perceived COVID-19 health risk and usage intention of e-wallets. It is possible that with the fear of contracting the COVID-19 pandemic, the facilitating conditions become non-essential in influencing consumers’ usage intention. Thus, consumers’ intention to adopt e-wallets when there is a high likelihood of contacting COVID-19 is not impacted by the presence or absence of favorable conditions. Consumers will desperately use e-wallets because of the health risks of COVID-19. According to Paige et al. (Citation2018), a customer’s protective health change occurs when adopting a protective action reduces disease/health risk in addition to the perceived threat.

Also, facilitating conditions significantly moderate the link between effort expectancy and usage intention of e-wallets. As a result, effort expectancy depends on adequate facilitating conditions. The usage intention of e-wallets increases when it is easy to operate the technology due to the facilitating conditions (Mahardika et al., Citation2019). When the external conditions become favorable, the link between effort expectancy and usage intention becomes stronger. On the contrary, facilitating conditions have a negatively significant moderating effect on the link between government support and usage intention of e-wallets. The greater the facilitating conditions, the less effective the link between government support and usage intention of e-wallets. This may be because when individuals have access to the necessary resources, such as a good network, efficient operating system, secured and dependable application, their reliance on government support might be unnecessary. The incentive provided by the government might enhance consumers’ perception of support, but this might only have a significant effect on the usage intention when the external situations are unfavourable. In essence, our findings suggest that facilitating conditions could reduce the effect of perceived government support on the usage intention of e-wallets.

5.2. Practical implications

Our findings have several practical implications. Given the effect of perceived COVID-19 health risks, consumers’ awareness of the COVID-19 variants and their severity could influence their usage intention of e-wallets. Access to the relevant information will provide the consumers with the rationale to avoid being infected by COVID-19, including adopting e-wallets to prevent as many physical contacts as possible. Also, government support is an essential factor in encouraging e-wallets usage. The government should communicate the relevance of using e-wallets to curb physical contact, which reduces the risk of contracting COVID-19. Similarly, the government should facilitate appropriate regulations and procedures to enable seamless e-wallet operations, thereby deepening citizen’s confidence in e-wallets, which in turn could enhance their usage intention

Given the significant effect of facilitating conditions, the service providers must ensure that the appropriate features and services are incorporated to make e-wallets more convenient and valuable. These could include offering instant transfer between the consumers’ and merchants’ wallets, seamless transfer to bank accounts, and easy and fast self-registration. Also, e-wallet providers must invest in the necessary infrastructure to facilitate seamless operations, for example, by providing a robust back-end infrastructure that can manage multiple requests from mobile users. Equally, e-wallet providers should ensure that the user interface is easy to operate yet highly secured. The e-wallet service providers should also ensure that consumers can use the e-wallets without much effort. The ease of use could be enhanced by providing necessary training or a quick tutorial on using the e-wallets application. This tutorial should be available in multiple languages and text and audio formats. The interface of the e-wallets should also be user friendly and be easily understood with relevant, comprehensive symbols for ease in manoeuvring the e-wallets applications.

6. Conclusions and future research direction

The outbreak of the COVID-19 pandemic has increased awareness of e-wallets as an alternative payment method. Thus, this study draws from the MAO framework and identifies the drivers of consumer usage intention of e-wallets during the outbreak of the COVID-19 pandemic in Malaysia. We extend the MAO framework by demonstrating that motivation in terms of health risk avoidance and government incentives and ability in the form of effort expectancy and opportunity in the form facilitating condition play significant roles in influencing the adoption of e-wallets. Moreover, our findings confirmed the interaction effects of opportunity on the influence of effort expectancy and COVID-19 health risk on intention to adopt an e-wallet.

Despite the contributions of our study, the inherent limitations can be solved in future research. For instance, our study draws on convenience sampling of potential e-wallets users in Malaysia, thereby limiting the generalizability of our findings to the whole population. In addressing this, future research could employ a probability sampling technique to select respondents to enhance the generalizability of findings. Another issue in our study is the use of cross-sectional data, limiting the long-term applicability of our results. Individuals’ perceptions and beliefs about technology usage are temporal and could change over time. Therefore, subsequent studies should employ a longitudinal survey by assessing consumers’ intention to adopt e-wallets in the first instance and evaluate their usage behavior after a given period. Such studies will contribute to explaining how user behavior is shaped by behavioral intention. In addition, we encourage future research to consider the effect of effort expectancy for specific e-wallets to clarify differences in users’ experiences. Lastly, future studies could apply mixed methods and triangulation of data collection, which would provide a more robust perspective. In particular, qualitative and quantitative research designs are recommended for future researchers in this area. Such studies will explain the underlying mechanisms shaping behavioral intentions and usage of e-wallets.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Adedapo Oluwaseyi Ojo

Adedapo Oluwaseyi Ojo, PhD, is a senior lecturer at the Faculty of Management, Multimedia University Cyberjaya, Malaysia. He has extensive research and teaching experience in knowledge management, sustainability, operations management and technology management. His research agenda is driven by applying multidisciplinary perspectives in explaining behavioral and performance outcomes at the individual and organisational levels. He has published articles in WoS indexed journals like Journal of Cleaner Production, Review of Managerial Science, Industrial Systems and Data Management, Journal of Knowledge Management, Sustainable Production and Consumption, etc.

Olawole Fawehinmi

Olawole Fawehinmi, PhD., is a senior lecturer at the Faculty of Business, Economics and Social Development, Universiti Malaysia Terengganu, Malaysia. His research interests include organizational and behavioral studies, employee green behavior, employee engagement, human resource management (HRM), green HRM, and Employee empowerment. He has published in several top-ranking journals, including Journal of Cleaner Production, Benchmarking: An International Journal, International Journal of Manpower and SAGE Open. Olawole has received several prestigious academic rewards, including Pro-chancellor Award for Excellence.

Oluwayomi Toyin Ojo

Oluwayomi Toyin Ojo is currently a graduate research assistant (GRA) at the Faculty of Management, Multimedia University Cyberjaya, where she is also pursuing her Mphil in management. Her research interests are in entrepreneurship and information systems.

Chris Arasanmi

Chris Niyi Arasanmi, PhD is a senior lecturer at the Faculty of Business Management, Toi Ohomai Institute of Technology, Rotorua, New Zealand, where he teaches strategic HR management, information technology management, business intelligence, e-commerce, and research methods. He received a PhD from Auckland University of Technology (AACSB accredited), Auckland, New Zealand. His research interests are in enterprise systems and implementation training, enterprise resource planning, information systems adoption, e-commerce, HRD, and HRM. He has contributed articles to international refereed journals, like Enterprise Information Systems, Information Development, International Journal of Enterprise Information Systems, Industrial and Commercial training, European Journal of Training and Development, etc.

Christine Nya-Ling Tan

Christine Nya-Ling Tan, PhD, is a senior lecturer at the School of Business and Digital Technologies, Manukau Institute of Technologies, Manukau Campus, Auckland, New Zealand. She received her PhD in Knowledge Management from the Universiti Sains Malaysia, Penang, Malaysia. Her current research interests include knowledge management, knowledge sharing, business intelligence, big data analytics, and machine learning.

References

- Aji, H. M., Berakon, I., & Md Husin, M. (2020). COVID-19 and e-wallet usage intention: A multigroup analysis between Indonesia and Malaysia. Cogent Business and Management, Cogent, 7(1), 1–15. available at. https://doi.org/10.1080/23311975.2020.1804181.

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. https://doi.org/10.1016/0749-5978(91)90020-T

- Alalwan, A. A., Dwivedi, Y. K., & Rana, N. P. (2017). Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. International Journal of Information Management, Elsevier Ltd, 37(3), 99–110. https://doi.org/10.1016/j.ijinfomgt.2017.01.002

- Balakrishnan, V., & Shuib, N. L. M. (2021). Drivers and inhibitors for digital payment adoption using the Cashless Society Readiness-Adoption model in Malaysia. Technology in Society, Elsevier Ltd, 65(February), 101554. https://doi.org/10.1016/j.techsoc.2021.101554

- Baumhof, R., Decker, T., Röder, H., & Menrad, K. (2018). Which factors determine the extent of house owners’ energy-related refurbishment projects? A Motivation-Opportunity-Ability Approach. Sustainable Cities and Society, Elsevier, 36(July), 33–41. https://doi.org/10.1016/j.scs.2017.09.025

- Bigné, E., Ruiz, C., Andreu, L., & Hernandez, B. (2015). The role of social motivations, ability, and opportunity in online know-how exchanges: Evidence from the airline services industry. Service Business, 9(2), 209–232. https://doi.org/10.1007/s11628-013-0224-8

- Blumberg, M., & Pringle, C. D. (1982). The missing opportunity in organizational research: Some implications for a theory of work performance. Academy of Management Review, 7(4), 560–569. https://doi.org/10.2307/257222

- Chawla, D., & Joshi, H. (2019). Consumer attitude and intention to adopt mobile wallet in India – An empirical study. International Journal of Bank Marketing, 37(7), 1590–1618. https://doi.org/10.1108/IJBM-09-2018-0256

- Chen, W. K., Siburian, E. M., & Chen, C. W. (2020). The impacts of facilitating and inhibiting factors on usage intention of mobile payment services. International Journal of Applied Science and Engineering, 17(1), 107–120 doi:10.6703/IJASE.202003_17(1).107.

- Cohen, J. (1988). Statistical Power Analysis for the Behavioral Sciences (2nd ed.). Routledge. available at. https://doi.org/10.4324/9780203771587

- Daragmeh, A., Sági, J., & Zéman, Z. Continuous intention to use e-wallet in the context of the covid-19 pandemic: Integrating the health belief model (hbm) and technology continuous theory (tct). (2021). Journal of Open Innovation: Technology, Market, and Complexity, 7(2), 132. available at. https://doi.org/10.3390/joitmc7020132

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340. https://doi.org/10.2307/249008

- de Kerviler, G., Demoulin, N. T., & P, Z. (2016). Adoption of in-store mobile payment: Are perceived risk and convenience the only drivers? Journal of Retailing & Consumer Services, 31(1), 334–344. https://doi.org/10.1016/j.jretconser.2016.04.011

- Fawehinmi, O., Yusliza, M. Y., Mohamad, Z., Noor Faezah, J., & Muhammad, Z. Assessing the green behaviour of academics: The role of green human resource management and environmental knowledge. (2020). International Journal of Manpower, 41(7), 879–900. available at. https://doi.org/10.1108/IJM-07-2019-0347

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurements error. Journal of Marketing Research, 18(4), 39–50. https://doi.org/10.1177/002224378101800104

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2017). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM) (2nd ed.). SAGE Publications.

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. Advances in International Marketing, 20(2009), 277–319 https://doi.org/10.1108/S1474-7979(2009)0000020014.

- Hu, Z., Ding, S., Li, S., Chen, L., & Yang, S. Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model. (2019). Symmetry, 11(3), 340. available at. https://doi.org/10.3390/sym11030340

- Huterska, A., Piotrowska, A. I., & Szalacha-Jarmużek, J. Fear of the covid-19 pandemic and social distancing as factors determining the change in consumer payment behavior at retail and service outlets. (2021). Energies, 14(14), 4191. available at. https://doi.org/10.3390/en14144191

- Islam, M. T., & Khan, M. T. A. (2021). Factors influencing the adoption of crowdfunding in Bangladesh: A study of start-up entrepreneurs. Information Development, 37(1), 72–89. https://doi.org/10.1177/0266666919895554

- Jesuthasan, S., & Umakanth, N. Impact of behavioural intention on e-wallet usage during Covid-19 period: A study from Sri Lanka. (2021). Sri Lanka Journal of Marketing, 7(24), 24. available at. https://doi.org/10.4038/sljmuok.v7i2.63

- Kapoor, K., Dwivedi, Y., & Williams, M. D. (2015). Examining the role of three sets of innovation attributes for determining adoption of the interbank mobile payment service. Information Systems Frontiers, 17(1), 1039–1056. https://doi.org/10.1007/s10796-014-9484-7

- Kassim, N. M., Ramayah, T., Mohamad, W. N., & Shabbir, M. S. (2021). Battling COVID-19: The Effectiveness of Biometrics Towards Enhancing Security of Internet Banking in Malaysia. International Journal of Enterprise Information Systems, 17(2), 71–91. https://doi.org/10.4018/IJEIS.2021040104

- Kaur, P., Dhir, A., Singh, N., Sahu, G., & Almotairi, M. (2020). An innovation resistance theory perspective on mobile payment solutions. Journal of Retailing & Consumer Services, 55(1), 102059. https://doi.org/10.1016/j.jretconser.2020.102059

- Khozaei, F., Kim, M. J., Nematipour, N., & Ali, A. The impact of perceived risk and disease prevention efficiency on outdoor activities and avoidance behaviors in the urban parks during COVID 19 pandemic. (2021). Journal of Facilities Management, 19(5), 553–568. available at. https://doi.org/10.1108/JFM-09-2020-0065

- Kim, D. H., & Lee, H. (2016). Effects of user experience on user resistance to change to the voice user interface of an in-vehicle infotainment system: Implications for platform and standards competition. International Journal of Information Management, 36(4), 653–667. https://doi.org/10.1016/j.ijinfomgt.2016.04.011

- Kwateng, O. K., Osei Atiemo, K. A., & Appiah, C. (2019). Acceptance and use of mobile banking: An application of UTAUT2. Journal of Enterprise Information Management, 32(1), 118–151. https://doi.org/10.1108/JEIM-03-2018-0055

- Leguina, A. (2015). A primer on partial least squares structural equation modeling (PLS- SEM). International Journal of Research & Method in Education, 38(2), 220–221. https://doi.org/10.1080/1743727X.2015.1005806

- Leong, C. M., Tan, K. L., Puah, C. H., & Chong, S. M. (2021). Predicting mobile network operators users m-payment intention. European Business Review, 33(1), 104–126. available at. https://doi.org/10.1108/EBR-10-2019-0263.

- Li´ebana-cabanillas, F., Luna, I., & Montoro-Ríos, F. (2015). User behaviour in QR mobile payment system: The QR payment acceptance model. Technology Analysis & Strategic Management, 27(9), 1031–1049. https://doi.org/10.1080/09537325.2015.1047757

- Lu, L. (2018). Decoding Alipay: Mobile payments, a cashless society and regulatory challenges. Butterworths Journal of International Banking and Financial Law, January, 40–43 https://ssrn.com/abstract=3103751.

- Macedo, I. M. (2017). Predicting the acceptance and use of information and communication technology by older adults: An empirical examination of the revised UTAUT2. Computers in Human Behavior, 75 (October 2017) , 935–948. https://doi.org/10.1016/j.chb.2017.06.013

- Mahardika, H., Thomas, D., Ewing, M. T., & Japutra, A. (2019). Experience and facilitating conditions as impediments to consumers’ new technology adoption. International Review of Retail, Distribution and Consumer Research, 29 (1) , 79–98 https://doi.org/10.1080/09593969.2018.1556181.

- Mandari, H. E., Chong, Y. L., & Wye, C. K. (2017). The influence of government support and awareness on rural farmers’ intention to adopt mobile government services in Tanzania. Journal of Systems and Information Technology, 19(1/2), 42–64. https://doi.org/10.1108/JSIT-01-2017-0005

- Mastercard. (2020), “Contactless payments will be the new normal for shoppers in the post Covid-19 world”, Mastercard, available at: https://newsroom.mastercard.com/asia-pacific/2020/05/20/contactless-payments-will-be-the-new-normal-for-shoppers-in-the-post-covid-19-world/

- MCMC. (2020), Internet Users Survey 2020, available at: 1823-2523

- Ojo, A. O. (2021). Motivational factors of pro-environmental behaviors among information technology professionals. Review of Managerial Science. Springer Berlin Heidelberg(123456789). available at. https://doi.org/10.1007/s11846-021-00497-2.

- Ojo, A. O., Arasanmi, C. N., Raman, M., & Tan, C. N. L. (2019). Ability, motivation, opportunity and sociodemographic determinants of Internet usage in Malaysia. Information Development, 35(5), 819–830. https://doi.org/10.1177/0266666918804859

- Ojo, A. O., & Fauzi, M. A. (2020). Environmental awareness and leadership commitment as determinants of IT professionals engagement in GreenIT practices for environmental performance. Sustainable Production and Consumption, 24 (October 2020) , 298–307. https://doi.org/10.1016/j.spc.2020.07.017

- Ojo, A. O., Fawehinmi, O., & Yusliza, M. Y. (2021). Examining the predictors of resilience and work engagement during the covid-19 pandemic. Sustainability (Switzerland), 13(5), 1–18 https://doi.org/10.3390/su13052902.

- Olya, H. G. T., & Al-ansi, A. (2018). Risk assessment of halal products and services: Implication for tourism industry. Tourism Management, Elsevier Ltd, 65 (April 2018) , 279–291. https://doi.org/10.1016/j.tourman.2017.10.015

- Ooi, K. B., & Tan, G. W. H. (2016). Mobile technology acceptance model: An investigation using mobile users to explore smartphone credit card. Expert Systems with Applications, 59 (October 2016) , 33–46. https://doi.org/10.1016/j.eswa.2016.04.015

- Oppotus. (2020), “E-Wallet usage in Malaysia 2020: Thriving in lockdown”, Oppotus, available at: https://www.oppotus.com/e-wallet-usage-in-malaysia-2020/

- Paige, S. R., Bonnar, K. K., Black, D. R., & Coster, D. C. (2018). Risk factor knowledge, perceived threat, and protective health behaviors: Implications for type 2 diabetes control in rural communities. The Diabetes Educator, 44(1), 63–71. https://doi.org/10.1177/0145721717747228

- Peng, D. X., & Lai, F. (2012). Using partial least squares in operations management research: A practical guideline and summary of past research. Journal of Operations Management, 30(6), 467–480. https://doi.org/10.1016/j.jom.2012.06.002

- Podsakoff, P.M., MacKenzie, S.B., Lee, J.-Y., & Podsakoff, N.P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5), 879–903.

- Puriwat, W., & Tripopsakul, S. (2021). Explaining an adoption and continuance intention to use contactless payment technologies: During the Covid-19 pandemic. Emerging Science Journal, 5(1), 85–95. https://doi.org/10.28991/esj-2021-01260

- Rahman, M., Ismail, I., & Bahri, S. (2020). Analysing consumer adoption of cashless payment in Malaysia. Digital Business, 1(1), 100004. https://doi.org/10.1016/j.digbus.2021.100004

- Rao, S., & Troshani, I. (2017). A conceptual framework and propositions for the acceptance of mobile services, Journal of Theoretical and Applied Electronic Commerce Research, 2(2), 61–73. https://doi.org/10.3390/jtaer2020014

- Reinholt, M., Pedersen, T., & Foss, N. J. (2011). Why a central network position isn’t enough: The role of motivation and ability for knowledge sharing in employee networks. Academy of Management Journal, 54(6), 1277–1297. https://doi.org/10.5465/amj.2009.0007

- Siemsen, E., Roth, A. V., & Balasubramanian, S. (2008). How motivation, opportunity, and ability drive knowledge sharing: The constraining-factor model. Journal of Operations Management, 26(3), 426–445. https://doi.org/10.1016/j.jom.2007.09.001

- Soodan, V., & Rana, A. (2020). Modeling customers’ intention to use e-wallet in a developing nation: Extending UTAUT2 with security, privacy and savings. Journal of Electronic Commerce in Organizations, 18(1), 89–114. https://doi.org/10.4018/JECO.2020010105

- Sreelakshmi, C. C., & Prathap, S. K. (2020). Continuance adoption of mobile-based payments in Covid-19 context: An integrated framework of health belief model and expectation confirmation model. International Journal of Pervasive Computing and Communications, 16(4), 351–369. https://doi.org/10.1108/IJPCC-06-2020-0069

- Tak, P., & Panwar, S. (2017). Using UTAUT 2 model to predict mobile app based shopping: Evidences from India. Journal of Indian Business Research, 9(3), 248–264. https://doi.org/10.1108/JIBR-11-2016-0132

- Taylor, S., & Todd, P. A. (1995). Understanding information technology usage: A test of competing models. Information Systems Research, 6(2), 144–176. https://doi.org/10.1287/isre.6.2.144

- Teng, S., & Khong, K. W. (2021). Examining actual consumer usage of E-wallet: A case study of big data analytics. Computers in Human Behavior, Elsevier Ltd, 121(February), 106778. https://doi.org/10.1016/j.chb.2021.106778

- Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. Source: MIS Quarterly, 27(3), 425–478 https://doi.org/10.2307/30036540.

- Venkatesh, V., Thong, J. Y. L., & Xu, X. (2012). Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly, 36(1), 157–178. https://doi.org/10.2307/41410412

- Wisniewski, T. P., Polasik, M., Kotkowski, R., & Moro, A. (2021). Switching from Cash to Cashless Payments during the COVID-19 Pandemic and Beyond. NBP Working Papers 337 , Narodowy Bank Polski, Economic Research Department. available at. https://doi.org/10.2139/ssrn.3794790

- Yang, M., Al Mamun, A., Mohiuddin, M., Nawi, N. C., & Zainol, N. R. (2021). Cashless transactions: A study on intention and adoption of e-wallets. Sustainability (Switzerland), 13(2), 1–18 https://doi.org/10.3390/su13020831.

- Yeap, C. (2020). “Seizing opportunities beyond the RM30 e-wallet credit “,Edge Weekly, The Edge Market. available at: https://www.theedgemarkets.com/article/seizing-opportunities-beyond-rm30-ewallet-credit