Abstract

The purpose of this study is to explain the development of scientific publications on Islamic banking based on year, country, authors, and fields of science that are focused on mapping topics. This study used a qualitative method to review 696 articles published in Scopus indexed scientific journals and the collection of data was carried out in stages. Furthermore, this study reveals that the development of scientific publications on Islamic banking in the last ten years has shown an increase in the number of article because it increases yearly. However, it is both the Muslim majority and the Muslim minority countries that focus on the issue of Islamic banking. Also, the articles have clustering authors that have the same focus but discussed it with different issues. There are three important issues in the study of Islamic banking and they include the governance, auditing and supervision, and problems of Islamic banking. Also, there are dominant and other topics that are frequently discussed and have not been discussed by authors, respectively. The result showed that the sustainability of Islamic Bank Governance is for the benefit of concept development and Islamic banking practices. The limitation of this study is that it used only a qualitative method to review articles from scientific journals indexed by Scopus. Therefore, the next study needs to use scientific articles sourced from journals, books, and proceedings indexed by Scopus and Web of Science (WoS).

PUBLIC INTEREST STATEMENT

This research is a response to publications on Islamic banking governance that have received much attention from scholars in various countries, both developed and developing countries, and both Muslim-majority and Muslim-minority countries. The main finding of this research is that previous studies are related to the concept of Islamic banking governance, banking auditing and supervision approaches, and banking governance issues. Moreover, these three concepts are interrelated with each other, in which each has sub-concepts that are also interrelated. The relationship between the concepts emphasizes that the study of Islamic banking is a discipline that is related to many fields of science, study materials, and banking issues. These findings provide an essential picture for scholars that the concept of the study of Islamic banking governance is related to many concepts that can be formulated into a sustainable study concept in the issue of Islamic banking governance.

1. Introduction

Islamic banking studies received serious attention from scholars, researchers, research institutes, universities, and Islamic banking practitioners in the last ten years (Biancone et al., Citation2020). Therefore, many factors including the Islamic banking becomes a global issue that is widely discussed and studied by many parties, most especially the Muslim-majority countries. This factors are meant for developing Islamic banking science, conceptualization, and practical purposes such as service innovation, the role of banking organizational structures, and optimizing the role of Islamic banking in the country’s economic growth and community empowerment (Khan et al., Citation2020). However, the concept of Islamic banking as the object of debate by many parties, most especially within the Muslim community is another factor to be examined. The Muslim community has a Sharia law that is related to profit-sharing systems, banking ownership, and management relations between Islamic banking and their stakeholders (Riaz et al., Citation2017).

Several previous studies reveal the performances and challenges of Islamic banking, banking supervision and auditing systems, service innovation, strategies to increase stakeholder trust, and implementation of Corporate Social Responsibility (CSR) programs (Smolo et al., Citation2020). Therefore, an empirical method was used to explain the problems of Islamic banking practice (Narayan & Phan, Citation2019). Furthermore, these previous studies focused on literature to formulate Islamic banking concepts, models, theories, and frameworks (Algabry et al., Citation2020; Alshammary, Citation2014). However, this literature expatiated more on the conceptualization of the economy, a comparative review, and conventional banking. Also, it focused on the corporate financial systems, transformation, growth, the CSR programs, company capital market frameworks, and Islamic Governance Framework (Al-Magharem et al., Citation2019; El-Galfy & Khiyar, Citation2012; Sakti, Tareq, et al., Citation2017a).

This study aims to explain the development of publications on Islamic Bank Governance in the last ten years. It is focused on exploring Islamic banking studies to produce a clear picture of Islamic Bank Governance, which includes concepts, topics, and issues of Islamic banking studies, which then contribute to the study of Islamic Banks. Governance, both on the theoretical/conceptual aspect and the empirical aspect.

The main contribution of this research is to review 696 scientific articles on Islamic banking governance sourced from Scopus indexed scientific journals published from 2012 to 2020. Qualitative approaches to content analysis and systematic literature review methods are applied to this study. The retrieval of 696 articles was carried out in stages. The stages are subscribing to Scopus, entering the keyword “Islamic Bank Governance” in the article search column in the Scopus database, selecting articles with restrictions on the publication period between 2012 and 2020 and restrictions based on the type of scientific journal article document; and download 696 selected articles for review. The software review paper in this study uses VOSVIEWER, WORDSTAT 8, and NVIVO 12 Plus.

This research contributes to the presentation of scientific information about trends in Islamic banking studies in the last ten years. These countries focus on studies of Islamic banking governance, concept maps of Islamic banking studies, and presentation of research topics and themes on Islamic banking governance. This contribution can support the sustainability of Islamic Bank Governance studies as part of the Islamic banking study area, both for concept development and for the benefit of Islamic banking practices. Previous studies have not used a systematic literature review approach with data analysis software, namely VOSVIEWER, WORDSTAT 8, and NVIVO 12 Plus. The urgency of using the data analysis approach and software is to facilitate the conceptualization of the study of Islamic banking governance.

1.1. Islamic Bank Governance concepts

The Islamic banking governance model is formulated based on the economic concept in the Islamic law which is sourced from the Al-Qur’an and Sunnah (Algabry et al., Citation2020). This economic system emphasizes the principles of justice, openness, income distribution, welfare goals, and accountability to God Almighty. Cheteni (Citation2014) formulated two principles of Islamic economics and they include the profit and loss sharing and the prohibiting usury. However, the principle of profit sharing and loss is related to the economic system, which involves many stakeholders who run the Islamic banking business (Alam, Mustafa et al., Citation2020). Therefore, the management of the bank is not owned individually or by a group of people but by many parties so that the profits and losses of the company are jointly accounted for. Meanwhile, the principle of prohibiting Riba is the taking of profits from the customers financial transactions by the bank management (Ben Bouheni et al., Citation2016). However, the management is not allowed to take profit or interest from financial transactions because there is no economic activity that shows the business between the two parties (Louhichi et al., Citation2019).

There are several studies that have attempted to conceptualize economics, corporate governance, and Islamic banking simultaneously (Mansour, Citation2020; Zaki et al., Citation2019). This emphasizes that economics specifically discusses its principles that are implemented in corporate governance and Islamic banking. These principles are implemented through the Islamic corporate governance system and they include profit and loss sharing and prohibiting usury. Furthermore, Obid and Naysary (Citation2014) compiled five principles of Islamic Corporate Governance (ICGP), and they include accountability, openness and transparency, competence, the confidentiality of information, and management independence. These five principles are compiled based on the integration of agency, stakeholder, and stewardship theory that are associated with Islamic economic principles (Obid & Naysary, Citation2014). Also, these researchers explained that these five principles guarantee the companies’ compliances which include the Islamic banking and economic principles formalized in Sharia law (Alam, Mustafa et al., Citation2020).

The principle of accountability in Islamic banking management is related to stakeholders who are part of the partners of an organization as investors and customers (Mansour, Citation2020). Also, it is addressed to the Sharia Supervisory Board which is Islamic trading law formulated directly from the Al-Quran and Al-Hadith. Therefore, accountability to the Sharia Supervisory Board is part of the actualization of Islamic banking management’s towards Allah Sulub et al., Citation2020a). This principle is the accountability of Islamic banking management towards humans who act as partners and Allah which is source of the Islamic law that is included in Al-Quran (Meslier et al., Citation2020).

Furthermore, the principle of openness and transparency is related to information and Islamic banking management policies that are conveyed openly to all partners (Kasim et al., Citation2016). However, this principle includes information and policies on cooperation agreements, profit and loss sharing, forms of all parties’ roles, and commitment to compliance with Sharia law (Saha & Kabra, Citation2020). The disclosure of information and banking management policies affect the formation of trust and banking cooperation networks which have an impact on the sustainability of the bank. Furthermore, the disclosure of information and banking management is followed by the principle of professionalism and competence that relates to the ability of human resources to carry out the functions of an organization based on Islamic values and muamalah Syariah law (Mohd Noor et al., Citation2019). Therefore, this principle are the actualizations of Islamic economic activities that avoid usury, interest, or profits that are not obtained through a banking cooperation with customers.

Also, the Islamic banking prioritizes the principle of confidentiality or secrecy that is related to internal banking matters such as auditing, resource management, and Sharia decision-making (Algabry et al., Citation2020). However, several studies emphasize that this principle causes problems such as corruption, collusion, and nepotism. Also, some studies explained that this principle maintain the stability and compliance of Islamic banking to Sharia law. Therefore, the principle of confidentiality is strengthened by the application of the independence of banking management. Furthermore, the Islamic banking management is an autonomous right of each Islamic banks that are under the supervision of the Sharia Supervisory Board (Mukhibad et al., Citation2020).

Moreover, several literature studies emphasize that Islamic economic principles help in achieving or creating prosperity and justice for all parties. Furthermore, welfare and justice are the main objectives of Islamic banking management thereby allowing it to be prohibited from making a profit like conventional bank management (Algabry et al., Citation2020). However, the compliance of Islamic banking management with Sharia law is a determining factor for the achievement of this objective. Furthermore, the increase in the compliance of Islamic bank management to Sharia law makes the bank to achieve prosperity and justice (Hassan, Citation2019). However, several empirical studies reveal that the success factor of Islamic banking is influenced by the compliance of banking management to Sharia law. Meanwhile, the failure of the bank is caused by the lack of compliance of Islamic banking management with the muamalah law.

1.2. Current studies of Islamic Bank Governance

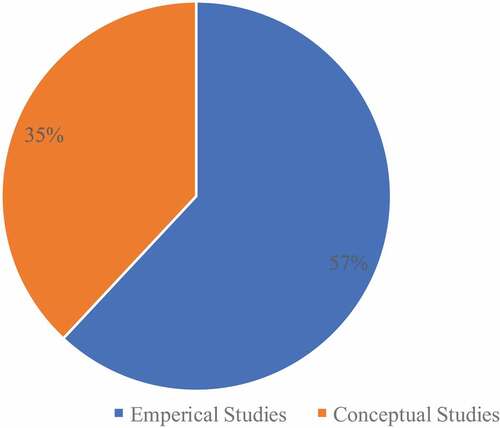

The study of Islamic Corporate Governance (ICG) or Shariah Governance (SG) is a study that has been in great demand in the last ten years (Grira & Labidi, Citation2020). Previous research on Islamic banking governance was carried out using many research approaches, including empirical and article review research approaches. The empirical research approach in Islamic banking governance research is related to research activities in the form of observation, case studies, and hypothesis testing about the problems that are the object of research on Islamic banking governance issues, including the success and failure factors of Islamic banking, the relationship between Islamic values and banking success, the determinants of banking success and failure, the relationship between service and public trust in Islamic banking, and other issues. Temporary, conceptual research approach or the popular term is library research, which is related to research activities in the form of reviewing articles, books, or other secondary sources that are directly related to the object of research. In general, the purpose of using a conceptual research approach in Islamic banking governance research is to develop a concept or theory based on articles, books, and scientific references that discuss the theme of Islamic banking governance, including the Islamic banking governance model, framework think the study of Islamic banking, the adaptation model of Islamic banking to change, the cooperative model of Islamic banking, and the development of other concepts.

Based on the identification of scientific publications on Islamic banking governance, especially scientific article documents from Scopus indexed journals, the use of an empirical approach is more dominant than the use of a conceptual approach in the study of Islamic banking governance. This illustrates that previous research has mostly explained and revealed problems based on field data such as surveys, observations, and experiments aimed at testing hypotheses on issues regarding Islamic banking. The dominance of the use of empirical research approaches in the study of Islamic banking has an impact on the lack of availability of literature on the concept or model of banking governance, which is built based on scientific articles, books, and other secondary references. Therefore, the urgency of this research is to contribute to conceptual research that produces an overview of publication trends, concept mapping, and conceptualization of Islamic banking governance research.

Figure shows that the empirical method is widely used to reveal the determinants that affect the performance of Islamic banking (Atanga Ondoa & Seabrook, Citation2020; Rozzani et al., Citation2016; Sutrisno & Widarjono, Citation2018). Furthermore, this method reveal that the performance of Islamic banking most especially in terms of credit ratings, is much better than conventional banking (Mansoor et al., Citation2020). Empirically, the openness and a system that ensures a fair distribution of income between banking management and bank customers are one of the factors that influence the performance of Islamic banking in the comfort of stakeholders or the public (Oladapo et al., Citation2019). Also, several empirical studies reveal that the Islamic banking system that prioritizes openness and profit-sharing affect public trust in the management of the bank. Therefore, this encourages them to invest in Islamic banking, which in turn affects the sustainability of banking business activities (Lahrech et al., Citation2014; Srairi, Citation2019). More so, orientation which emphasizes the welfare and empowerment of partners is another factor that affects public trust in Islamic banking (Akbar et al., Citation2012; Bukair & Abdul Rahman, Citation2015; Hassan & Saleem, Citation2017).

Figure 1. Gap Penelitian emperis dan Penelitian literature tentang Perbankkan Islam dalam sepuluh tahun tahun terakhir pada database scopus.

Furthermore, empirical studies with several methods such as surveys and analysis of organizational culture reveal that Islamic banking focuses on organizational management. However, this organizational management focused on the development of human resources, which includes knowledge, skills, and the cultivation of Islamic values (Cheteni, Citation2014; Salman & Nobanee, Citation2019).The attention of Islamic banking management significantly affects the performance of an organization in carrying out functions that are oriented towards achieving corporate goals (Mansoor et al., Citation2020). The results of other studies showed that Islamic banking management which focuses on the development of human resources and knowledge positively affect the compliance of an organizations with the Shari’ah. However, this is established and implemented by the Sharia Supervisory Board, which plays a role in supervising and monitoring Islamic banking (Ahmed et al., Citation2017). Furthermore, the compliance of an organization to Sharia is one of the factors that significantly affects the performance of Islamic banking in various countries. This is because it can increase stakeholder confidence, reduce the risk of violating business ethics, and strengthen stakeholder cooperation networks (Abdelhak et al., Citation2019; Mansori et al., Citation2015; Musleh Al-Sartawi, Citation2020).

The conceptual research approach is related to research on Islamic Bank Governance based on scientific articles, literature, and theories on Islamic economics, Islamic economic governance, and Islamic economic management models.(Handayati et al., Citation2017; Kabir et al., Citation2019). The use of a conceptual research approach in the study of Islamic banking is divided into two forms of research approach, namely a qualitative conceptual approach and a quantitative conceptual approach, both of which are used at the same time and are also used separately in a study of Islamic Bank Governance. In general, the use of a conceptual research approach in the topic of Islamic Bank Governance is related to the researchers’ efforts to conceptualize the Islamic Corporate Governance Framework. (Khan et al., Citation2020), reviewing the problems and challenges of Islamic Bank (Sulub et al., Citation2018), explain the effectiveness of the role of the Shari’ah Supervisory Board (Alam, Ahmad et al., Citation2020b), Islamic banking internal auditing analysis (Ballester et al., Citation2020), and formulate Islamic banking programs and policies (Al-Magharem et al., Citation2019; Zafar & Sulaiman, Citation2019), analysis of the challenges of Islamic banking in the era of information technology (Husseini et al., Citation2019a), and theoretical analysis of Islamic banking capital (Sakti et al., Citation2017a).

Also, several empirical and literature studies reveal that the success of Islamic banking is inseparable from the role of its institutions. However, this role include the principles of organizational governance that emphasize openness and transparency, independence, and accountability (Istrefi, Citation2020; Khalid et al., Citation2018; Sulub et al., Citation2020a). Therefore, the factor of openness is when stakeholders involved themselves in the development and business as a shareholders and banking partners (Neifar et al., Citation2020; Srairi, Citation2019). Also, this involvement is based on a profit-sharing agreement under a Sharia law established and monitored by the Sharia Supervisory Board (Lahrech et al., Citation2014). The transparency of Islamic banking organizations is related to bank income and assets (Hartanto et al., Citation2021; Naysary et al., Citation2020). Furthermore, independence as one of the factors focused on compliance with the law that is formulated by the Shari’ah Supervisory Board (Alam, Ahmad et al., Citation2020b; Musleh Al-Sartawi, Citation2020). Thus, Islamic banking has greater flexibility than the conventional own and it is directly tied to a state law (Alam, Ahmad et al., Citation2020b). Also, the accountability as one of the factors is directly addressed to Allah and stakeholders in which there are divine values as controllers of the bank management (Alam, Ahmad et al., Citation2020b).

However, several studies explain that the organizational activities of Islamic banking is based on Sharia law which is formulated and monitored by the Sharia Supervisory Board. Also, other studies reveal that Sharia law is Islamic values that is formalized in the banking business world and has links with other organizational governance principles. However, the non-Sharia law include the principles of openness and empowerment of the social environment through the Corporate Social Responsibility (CSR) Program (Husseini et al., Citation2019a). Therefore, the success of Islamic banks is inseparable from the efforts of its management that maximize organizational values, which are directly related to the principles of conventional governance (Parsa, Citation2020). Furthermore, several empirical studies reveal that some Islamic bank applies a conventional organizational governance structures such as internal and external audits, which are positively correlated and significantly affect the efficiency of the bank (Aslam et al., Citation2019; Hasan et al., Citation2020). The application of conventional organizational governance enables more efficient Islamic banking management. Therefore, this affects the good performances of Islamic banking following the Sharia standards (Samori et al., Citation2017).

Also, Islamic banking succeeded in contributing to the country’s economic growth. Several studies that focus on the role of Islamic banking in-state development reveal that it has made a positive contribution to the economic growth of society, most especially for the growth of Small and Medium Enterprises. However, this plays an important role in the economic growth of developing countries such as Malaysia and Indonesia (Husseini, Fam, et al., Citation2019a). The Islamic banking in Malaysia is a source of state finance that supports the country’s development in all aspects, most especially infrastructure and community empowerment. Therefore, the contribution of Islamic bank does not only focus on economic affairs, but also help in strengthening the understanding of business actors of the Islamic banking system. This understanding include the covering human resource governance, empowering business actors, and strengthening Sharia-based business networks (Shahar et al., Citation2020).

Recent studies related to the stability and competition of Islamic banking reveal that Islamic banking tends to be more stable than conventional banking (Albaity et al., Citation2019). On the one hand, the stability of Islamic banking shows that Islamic banking governance is better than conventional banking. But on the other hand, Islamic banking stability is influenced by Islamic banking management, which avoids banking competition in the financial market sector, which shows that Islamic banking does not dare to take risks in the banking sector which does not rule out the possibility that on the one hand, it will affect on the slow growth of Islamic banking in the financial sector, but on the other hand stability is a condition that must be maintained to ensure the sustainability of Islamic banking (Albaity et al., Citation2021). Basically, banking competition does not always make banking stability decrease or increase, and it is very dependent on government regulatory intervention to regulate banking competition (Kanas et al., Citation2019). Government regulations can determine a competitive code of ethics that guarantees healthy competition between banks so that the financial sector is not monopolized by large banks with access and large capital.

Furthermore, several studies reveal the success of Islamic banking, while others reveal that it was faced with many problems including the inconsistency, global market competition, and a decline in public trust while carrying out its business activities (Alhammadi et al., Citation2020). Also, several studies reveal that there is a tendency of inconsistency in Islamic banking towards Islamic-based corporate values (muamalah law), most especially in terms of empowerment and public welfare objectives (Yunan, Citation2021). However, both in the empirical studies and literature reviews, the respondents consider that Islamic banking goals not to be different from that of conventional that emphasize corporate profits. In addition, this inconsistency towards the value of an organization is inseparable from the minimal role of monitoring and evaluation of Islamic banking sharia boards (Hassan & Haridan, Citation2019). The findings of this empirical study need to be strengthened by other method to illustrate some public opinions and perceptions that tend to be negative towards Islamic banking.

Moreover, another study revealed that Islamic banking had not paid much attention to good and clean banking governance. Also, the Islamic banking has not paid attention to investigations, audits, and monitoring but support the disclosure of internal authority such as corruption, collusion, and nepotism in the internal banking management. Meanwhile, the Islamic banking tends to ignore anti-corruption programs in banks’ internal management (Salman & Nobanee, Citation2019). However, another study revealed that the Sharia Supervisory Board have a role in supervising and monitoring Islamic banking management. This supervisory board, has not shown a maximum role in shaping good banking governance and free from corruption, collusion, and nepotism practices (Nomran & Haron, Citation2019). Therefore, the Sharia Supervisory Board plays an important role in the aspects of regulatory formulation and formalization of Islamic values in business affairs. Meanwhile, the role of monitoring, auditing, and investigating bank management related to compliance with Shari’ah tends to be ignored to make internal problems to be difficult in disclosing Sulub, Salleh, et al., Citation2020a). Also, the internal problems in Islamic banking management, such as corruption, collusion, and nepotism, are a threat to the failure of the bank in the future (Darmadi, Citation2013).

2. Review methods

This study used a qualitative method with systematic literature review approach to analyzed 696 articles from scientific journals indexed by Scopus. Furthermore, this method is used in understanding text, content, and documents that are directly related to the problem of the study (Khatib et al., Citation2021). The flexibility of the researchers to translate and interpret text is one of the strengths of the qualitative method to content analysis. However, the interpretation of text can be categorized into concepts, themes, and topics to make the distribution of structured and non-structured texts to be well organized so that research questions can be answered properly. Therefore, this study can classified, categorized, and place text from the 690 articles reviewed to reveal issues and topics that have not been or have been the attention of previous Islamic banking studies. The stages of qualitative systematic literaure review method to content analysis are illustrated in Figure .

Figure 2. Stages of content analysis on articles sourced from the Scopus database.

First, the article identification stage. Article searches are carried out on the paid SCOPUS database by entering the keyword “Islamic Bank Governance“ in the search column by selecting the search type “Reference”. Furthermore, after the keywords have been entered, the next step is to run a search by pressing the ”Search” menu. Then, the search process produces a list of 876 articles with various topics and titles from all years and types of documents. Therefore, the next step is to limit the number of documents by selecting article for the publication period of 2012–2020 and journal article which then produce 696 articles.The second, the article selection stage. This study produced 696 articles that were selected as the unit of analysis through the search process. Furthermore, this articles was selected based on the criteria for the publication period of 2012–2020, the publication of the articles in the scientific indexed journals in Scopus, relevance of topics, themes, and titles with Islamic Bank Governance. Also, it was selected base on the quality of document files that facilitate the coding and classifying process of text as well as readability by the used data analysis software.Third, the article search stage. The 696 selected articles was searched for the purpose of publication thereby making it to be downloaded and placed in a computer folder. Furthermore, after the articles were downloaded and stored in a computer folder, they were all entered into the ”Mendeley” article management software. However, the articles that have been entered into Mendeley are exported as a RIS file type. The RIS file is entered into the data analysis software that includes VOSVIEVER, WORDSTAT 8, and NVIVO 12 Plus.

Fourth, the data analysis stage. This study used data analysis software that includes VOSVIEWER, NVivo 12 Plus, and WORDSTAT 8. However, VOSVIEWER is one of the popular software used for reviewing paper purposes that includes the mapping authors, visualizing author networks, mapping topics or concepts, visualizing topic networks, and grouping topics based on similar topics and related concepts. Meanwhile, the VOSVIER software is used to list authors, topics, and issues in Islamic banking studies based on the 696 reviewed articles. The weakness of the VOSVIEWER software is that its analysis results cannot show the topic or concept of the study based on the author’s name thereby making the researcher not to understand the topics discussed by each author. Therefore, this study uses NVivo 12 Plus software to obtain data on topics, concepts, or issues discussed by authors. The ability to connect authors with topics or issues is one of the strengths of the NVivo 12 Plus software. Furthermore, the topics and authors generated from the VOSVIEWER software are further analyzed with the NVivo 12 Plus to make the relationship between the topic and the author to be explained properly. Moreover, WORDSTAT 8 software is used to classify and map topics and concepts that are resulted from the VOSVIEWER and NVivo 12 Plus analysis to produce topic classifications based on issues in the studies of Islamic banking.

3. Results and discussion

3.1. Publication trends on Islamic Bank Governance studies

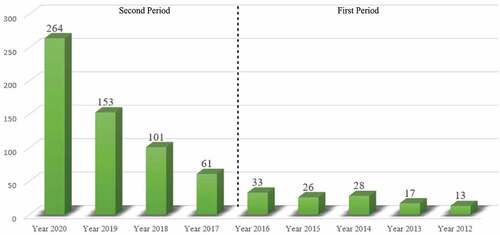

The publications on Islamic Bank Governance (IBG) experienced a positive increase between 2012 to 2020, with 696 articles that is sourced from scientific journals indexed by Scopus. However, these articles were published in stages which are divided into two periods that includes between 2012 to 2016 and 2017 to 2020. The number of articles published on Islamic banking in the first period ranged from 13 to 33. Furthermore, the number of articles published are 13, 17, 28, 26, and 33 in the year 2012, 2013, 2014, 2015, and 2016 respectively. Meanwhile, the number of articles published in the second period are 61, 101, 153, 264 in the year 2017, 2018, 2019, and 2020, respectively (Graph 1).

Graph 1. There are publication trends on Islamic banking in scopus indexed journals in the last nine years.

The trend of increasing the number of published scientific articles in the first period shows that scholars, researchers, and practitioners began to pay attention to the issues of Islamic banking. However, this issues were caused by many factors that includes this period to be after the crisis of global monetary faced by many developing and Muslim countries around the world. Furthermore, it is after this crisis that several studies revealed that Islamic banking is able to withstand an economic crisis situation. In fact, it was disclosed that Islamic banking is capable of playing a maximum role in restoring the country’s economy and increasing economic growth. Therefore, scholars, researchers, and practitioners began to focus on the issues of Islamic banking. However, they examined the factors that affect the performance of Islamic banking, governance models, the role of Sharia law, the design of the organizations, and comparison of the management and conventional banking.

Also, the trend of increasing the number of published scientific articles in the second period confirms that scholars, researchers, and practitioners continue to focus their studies on the issues of Islamic banking. The publication in this period experienced a 100% increase from the number of articles published in the first period. However, the first period shows that scholars, researchers, and practitioners continue to expand the issues for the benefit of theory development, the concept or model of the bank, and the Islamic banking practices. The issues that the researchers and publications attend to in the second period include the development of banking organizations, innovation in governance, an adaptation of Sharia law, auditing, and the role of the Sharia supervisory board. Furthermore, the ongoing studies in the first period are the number of issues in Islamic banking.

The increase in the number of publications both in the first and second period shows a consistent increase in the number of publications on Islamic Bank Governance. This confirms that the study of Islamic Bank Governance is becoming an attractive object for researchers, scholars, and practitioners in the field of Islamic banking. Furthermore, it is for the purposes of developing theories, concepts, models, and conceptual frameworks. Also, it is for the purpose of practical such as making government policies on Islamic banking, service innovation and developing governance models, adopting Sharia law, and formulating strategies to increase customer satisfaction and stakeholders. Furthermore, the consistent increase in the number of publications shows that the topic of Islamic Bank Governance will continue to receive serious attention from scholars, researchers, and practitioners. This has an impact on the development and expansion of the study area related to Islamic banking issues, which in turn contributes to the increase in the number of publications and high public interest on the studies in all developing and Muslim countries.

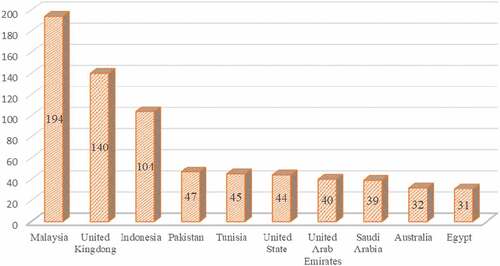

Furthermore, the graph shows that the study of Islamic Bank Governance in the last ten years has received attention from many countries, including Malaysia, United Kingdom, Indonesia, Pakistan, Tunisia, United States, United Arab Emirates, Saudi Arabia, Australia, and Egypt. This study classified all these countries into two clusters based on the trend in the number of publications produced. The first cluster includes Malaysia, United Kingdom, and Indonesia while the second cluster includes Pakistan, Tunisia, United State, United Arab Emirates, Saudi Arabia, Australia, and Egypt. However, in the first cluster, Malaysia is the country that publishes the most scientific articles on Islamic banking. The articles are published by Malaysia, United Kingdom, and Indonesia as 194, 140, and 104 respectively. Meanwhile, the articles are published in the second cluster by Pakistan, Tunisia, United States, United Arab Emirates, Saudi Arabia, Australia, and Egypt as 47, 45, 44, 40, 39, 32, and 31 respectively. This indicates that the Pakistan is the country with the highest number of published scientific articles on Islamic banking.

Moreover, the large number of scientific articles published by the Malaysian state cannot be separated from the existence of Malaysia as a Muslim majority country. This country has many scholars and researchers who focus on studies in the field of Islamic banking. Also, this confirms that Malaysia has the highest focus on Islamic banking compared to other Muslim countries, such as Indonesia and Saudi Arabia. However, the United Kingdom is the second country that produces the most scientific articles on Islamic banking. This shows that the study of this bank is not always the domain of Muslim majority countries. The United Kingdom as a Muslim minority country pay high attention to the issues of Islamic banking. This issues are caused by many factors, including the high interest of Muslim scholars and researchers towards the issue of Islamic banking. Also, this shows that the United Kingdom Kingdom is open to the study of Islamic banking. Furthermore, Indonesia as a Muslim-majority country is the third-largest to produce scientific articles on Islamic banking. This shows that scholars, researchers, and practitioners have a high interest in Islamic banking issues. However, this issues are caused by many factors including the Indonesian government policy that implements Sharia law in the state sector and private banking. Also, the number of universities that have opened Islamic banking economics study programs, high public interest, demands for innovative practices of the bank governance, and problems of governance are part of the factors that caused this issues.

Graph 2. The number of document articles on Islamic banking in Scopus indexed journals based on country names in the last ten years.

Countries in the second cluster produced a proportional number of scientific article and this means that the article produced are almost the same in number. The United State and Australia are Muslim minority countries and they produced almost the same number of articles that the Muslim-majority countries published. The Muslim-majority countries including the Tunisia, United Arab Emirates, Saudi Arabia, and Egypt confirms that the study of Islamic banking does not always depend on the religious existence of the state. However, it likely depends on the openness of the local government, the growth of the bank, the high number of studies on the comparison of the Islamic banking system and conventional banking, several problems that arises in governance, and the strategic role of Islamic banking on the economic growth of a country. Also, it depends on the strength of the role of the Sharia board in the sustainability of Islamic banking in several countries, high interest in undergraduate, and research studies in the economy and banking sector. The number of publications produced by both Muslim minority and Muslim majority countries in the second cluster strengthens the assumptions and findings of previous study. Therefore, the previous study explained that the Islamic Bank Governance has received a lot of attention from scholars and researchers in countries around the world. This makes it possible that the studies of Islamic Bank Governance will continue to develop and get a lot of responses from many countries.

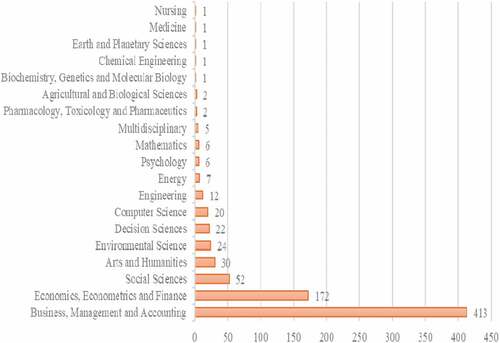

Furthermore, the study of Islamic bank governance is related to various fields of science that includes Business, Management, Accounting, Economics, Econometrics, Finance, Social Sciences, Arts and Humanities, Environmental Science, Decision Sciences, Computer Science, Engineering, and Energy. Also, it is related to Psychology, Mathematics, Multidisciplinary Pharmacology, Toxicology, Pharmaceutics, Agricultural and Biological Sciences, Biochemistry, Genetics, Molecular Biology, Chemical Engineering, Earth and Planetary Sciences, Medicine, and Nursing. Several fields of science are grouped into three clusters where the first one played a dominant role in the study of Islamic Bank Governance in the last 10 years and it includes economics, social sciences, and arts and humanities. Meanwhile, the second cluster includes environmental science, computers, information systems, engineering, and energy science. The third cluster includes psychology, mathematics, biology, medicine, and health sciences. Furthermore, the study of Islamic Bank Governance is part of the object of the first, second, and third cluster studies. This confirms that the study of Islamic Bank Governance does not only have a connection with the field of economics and social sciences, but also related to other fields of science, such as environmental science, computers, engineering, and health.

Graph 3. The number of articles on Islamic banking in Scopus indexed journals based on scientific fields in the last ten years.

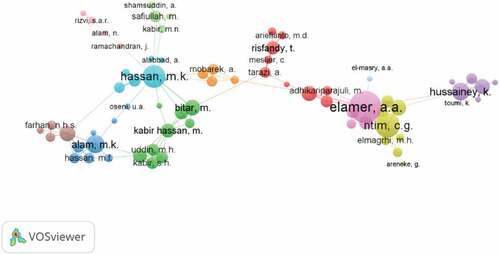

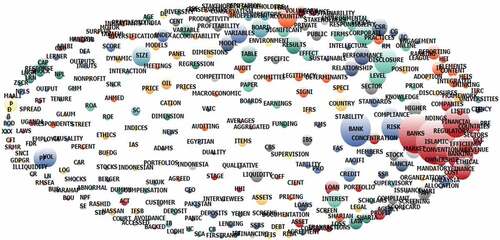

The above previous analysis revealed that scholars and researchers from various countries and fields of science had focused on the study of Islamic Bank Governance. There are ten clusters of authors based on the article generated from the VOSVIEWER analysis. However, the first, second, third, fourth, fifth, sixth, seventh, eighth, ninth, and tenth cluster are represented by Elamer, Hasan, Hussaeney, Alam, Bitar, Kabir, Mubarak, Risfandy, Ntim C.G respectively.

The ten clusters of writers in the Islamic Bank Governance in Figure have the same field of study, but focuses on differnt factors related to Islamic banking issues. The Natural Cluster focuses more on the auditing and controlling aspects, compliance, and efficiency while, the Alamer cluster focuses on the aspects of disclosure, auditing and controlling, and reporting. Furthermore, the Bitar cluster focuses on the aspects of assets, capital, and efficiency while, the Farhan’s cluster focuses on efficiency, governance, and disclosure. The Hasan cluster focuses on the aspects of assets, compliance, and governance while the Hussainey cluster focuses on studies in the fields of disclosure, auditing and controlling, and reporting. Also, the Kabir cluster focuses on assets, compliance, efficiency, and governance while Mubarak cluster focuses on studies in the fields of assets, efficiency, and performance. Furthermore, the Ntim C.G cluster focuses on the issues of auditing and controlling, governance, and reporting. The Risfandy, T is the author’s cluster that discusses all topics of Islamic banking studies (Table ).

Figure 3. Clusterization of writers on Islamic banking.

Table 1. The focus of studies in Islamic banking is based on the author cluster

The focus of the study and intensity of the author’s attention to the bank issues are different because all author clusters discuss topics that are directly related to Islamic banking. Therefore, each cluster is related to one another, both in terms of topics, issues, and concepts. These findings indicate that the study of Islamic banking can be carried out with a variety of perspectives, issues, topics, approaches, and concepts that enable its governance to contributes to the development of Islamic banking concepts and practices.

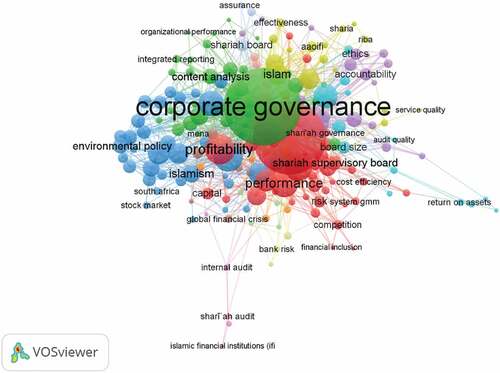

3.2. Dominant topics of Islamic Bank Governance Studies

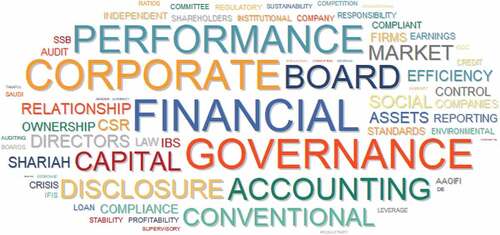

The content analysis with WORDSTAT 8 on 696 articles revealed that there were ten dominant topics in the study of Islamic Bank Governance in the last ten years. They include performance, company (corporate), organization (board), finance (governance), Capital (capital), financial management (accounting), management openness (disclosure), conventional banking (conventional), markets (market), assets (assets), management of Islamic banking organizations (director). Also, these topics include organizational ownership model (ownership), organizational efficiency (efficiency), corporate social responsibility (CSR) programs, shari’ah adaptation (compliance), supervision (control), reporting (reporting), and banking organization and finance audits (SSB-Audit). The performance, company, finance, and governance are the most dominant topics in the study of Islamic banking. Therefore, these four topics are the main concern of scholars and researchers in the study of Islamic bank governance in the last ten years.

Although it was stated above that the performance, company, finance, and governance are the most dominant topics from other dominant topics in the study of Islamic Bank Governance. These four topics are related to regulatory, institutional, market, CSR, auditing, controlling, others that have not yet become the center of important attention of the scholars and researchers in the last ten years. The topic mapping with WORDSTAT 8 confirms that there is a relationship between the dominant topic and others thereby making them to be interrelated in the study of Islamic Bank Governance. Furthermore, this relationship shows that the dominant topics has been and is being the concern of many scholars and researchers. Meanwhile, other topics are starting to become the attention of scholars and researchers in the study of Islamic Bank Governance. Also, they are needed to be further discussed in subsequent studies to reveal the relationship and important influence of the study of Islamic Bank Governance.

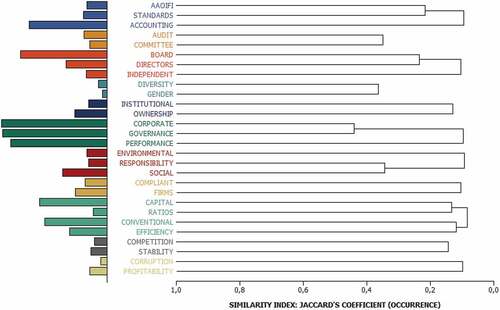

The dominant topics and others in the picture mapping are distributed into eleven clusters where the first cluster include Accounting which correlates with standards and AAOIFI. Meanwhile, the second cluster is the Audit that is correlated with the Committee while the third cluster involve the Board which correlates with the Director and the Independent. Furthermore, the fourth cluster include Diversity which is related to gender issues; the fifth one is Institutional that is related to Ownership. Moreover, the sixth cluster is Corporate and it is related to Governance and Performance, while the seventh cluster is Environmental that is related to Social Responsibility and Responsibility. The eighth cluster include Compliant topics that is related to Firm; the ninth one is Capital that is related to Ratios, Conventional, and Efficiency. More so, the tenth cluster is Competition which correlates with Stability; and the eleventh one include the issue of Corruption that is related to Profitability. This clustering of topics confirms that the dominant and other topics in the study of Islamic Bank Governance are related to one another.

Graph 4. Relation of topics in Islamic banking studies.

The relationship between topics is still very weak and this is shown by the Jaccard value ranging from 0.01 to 0.4. Therefore, several topics that have emerged in the Islamic Bank Governance study in the last ten years still need a more in-depth explanation to reveal the coherence and relevance of the topic.

3.3. Issues of Islamic Bank Government studies

Based on the results of content analysis with VOSVIEWER, the eleven topics cluster by following the WORDSTAT 8 in Figures are a unitary study of Islamic Bank Governance. However, this is broken down into three important issues where the first one is related to corporate, financial, governance, performance, accounting, and other governance issues. The second issue is related to the development of banking organizations, boards, directors, ownership, and other topics. Furthermore, the third issue is related to auditing and supervision of Islamic banking, such as controlling, disclosure, standards, reporting, independence, corruption, and other topics. Also, the issues or problems related to Islamic banking are needed to be explained in-depth in the study of Islamic Bank Governance.

Figure 4. The dominant topic in Islamic banking studies.

Figure 5. Mapping and clustering of dominant topics in Islamic banking studies.

Figure 6. Clusterization of issues in Islamic banking studies.

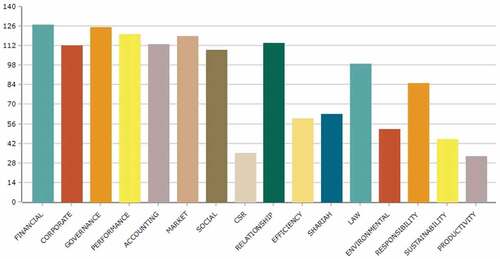

The results of content analysis with WORDSTAT 8 reveal that governance issues in the Islamic Bank Governance study are related to several issues. These several issues include financial which is mostly discussed by the previous study, governance, performance, market, stakeholder relations, corporate, performance, law, and the responsibility of Islamic banking. A number of these issues are related to governance affairs in Islamic banking thereby making it to become an important objects in the last ten years. Also, there are other issues related to governance in Islamic Bank Governance and they include Sharia, Sustainability, Productivity, Efficiency, and CSR. Although several issues have not been widely discussed in the last ten years, but they are still an important object in the study of Islamic Bank Governance. The main conclusion in is that the dominant topic has been the object of study in the last ten years and will continue to develop in line with the development of the study of the governance. Meanwhile, the issue that has not been widely discussed are needs to be used as a novelty in the study of Islamic bank Governance in subsequent research and publications.

Graph 5. Governance issues in the studies of Islamic banking.

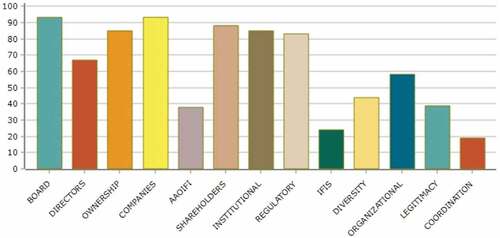

There are further analysis with WORDSTAT 8 that reveals other issues in the study of Islamic Bank Governance such as the organizational, Shariah Supervisory Board (Boards) as the most central issue, Shareholders, company management, institutional, regulatory, ownership, and directors. Several organizational issues have become the center of attention for scholars and researchers in the study of Islamic Bank Governance on organizational and institutional aspects. Furthermore, researchers and scholars in the last ten years have focused on the role of the Sharia Board in relation to the performance of an organization, models of shareholders, ownership, and the arrangement of the directors. Moreover, other issues such as behavior of Islamic banking organizations, diversity, legitimacy, stakeholder coordination, the role of IFIS, and the existence of AAOIFI in Islamic banking are not been widely discussed in the organizational issues.

Graph 6. Organizational issues in the study of Islamic banking.

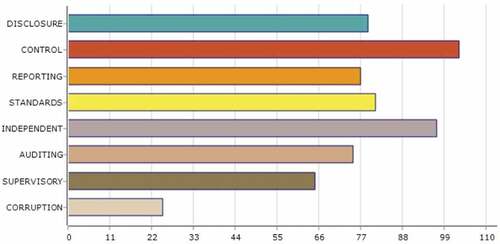

The issues of auditing and supervision of Islamic banking have now been discussed frequently in study and publications in the last ten years. The internal supervision relates to the role of the organization, Sharia auditing, the effectiveness and impact of the role of auditing on the performance of Islamic banking. The topic of internal supervision in auditing has become an issue that is often discussed in Islamic Bank Governance studies followed by other issues such as transparency, reporting, auditing standardization, independent auditing, and supervisory. Furthermore, these issues are directly related to the auditing activities and internal supervision which have been the object of Islamic banking studies for the past ten years. In general, the purpose of the study of auditing and supervision is to explain the role of auditing institutions and their impact on the performance of Islamic banking and management of an organization. However, the management reflects the principles of Sharia in muamalah affairs, including justice, openness, and welfare.

Graph 7. Auditing issues in the study of Islamic banking.

The topic of banking auditing and supervision which is the issue of corruption has not yet be the concern of the authors. However, the issue of corruption shows the explanation of the researchers and scholars on the performance and achievements of Islamic banking. Also, it reveal other problems such as corruption and collusion which has an impact on the sustainability of Islamic banking. The issue of corruption has started to be explained in more depth, such as forms and impact of corruption practices, corrupt relations of stakeholders in Islamic banking governance, collusive relationships and the impact of the independence on corruption practices. and other issues related to banking corruption practices.

The important finding in the study is that scientific publications on Islamic banking have shown positive developments in the last ten years. However, the Muslim-majority countries such as Malaysia, Saudi Arabia, Indonesia, Pakistan, and others and Muslim minority countries such as the United Kingdom and the United State have contributed to the increase in the number of scientific publications on Islamic banking. The findings of this study confirm that the Islamic Bank Governance has received a lot of attention from scholars and researchers in various countries and will continue developing the concept and complexity of problems (González et al., Citation2019; Ifada et al., Citation2019). However, the development of the Islamic Bank Governance is related to the increase in the number of countries, perspectives, approaches, and publications yearly. This shows that the study of Islamic banking is not only explained from the perspective of economics, accounting, sharia, but also from the social sciences, humanities, computers, and other disciplines. Therefore, the diversity of perspectives shows that Islamic Bank Governance are an object of study which are explained by various disciplines that allow Islamic banking issues to be well-expressed and conceptualized.

Furthermore, the diversity of perspectives and approaches in the study of Islamic Bank Governance are followed by the diversity of clusters of authors and researchers studying Islamic banking. This study reveals that there are eight clusters of authors, and each of them has a different object. Also, the clustering of authors are related to one another with regard to the citations of scientific publications. Therefore, the researchers and scholars in Islamic banking studies have the same focus on the area of Islamic Bank Governance. This study reveals that research and publications on Islamic banking in the last ten years are related to many topics, which are classified into three issues. These include the issue of governance, organizations, and auditing and supervision of Islamic banking. However, each of these issues is described in many topics, among which some are frequently discussed, and some have not been discussed by many researchers in the last ten years. The topics that are frequently discussed are performance, financial governance, organizational structure, accounting systems, the Islamic banking market, regulation, shareholders, supervision, and auditing. Moreover, this study reveal that research and publications in the last ten years have focused on topics that plays an important role in Islamic banking thereby making it to be directly related to organizational affairs. Also, some topics have not been discussed much and they include CSR programs and corruption. These two topics have not received much attention from researchers in the last ten years, thereby making the issues to be important in subsequent study.

4. Conclusions

Islamic banking studies in the last ten years show that Islamic Bank Governance is the concern of many researchers in several countries, both Muslim majority and Muslim minority countries. These study indicate that Islamic banking is related to two important issues such as the needs to be developed as a banking model that contributes to economic growth and several problems that hinder the sustainability. These problems include corruption, diversity of organizational structures, independence of the Sharia supervisory board, and others. The two important issues in the study of Islamic Bank Governance are continuous in subsequent studies. Moreover, this study has systematically laid out the Islamic Bank Governance related to the number and distribution of publications by country, year, study area, dominant topics, topic mapping, and important issues.

The limitations of this study is that it is only sourced from the Scopus database which is focused on articles published in scientific journals and also used only a qualitative method. This limitations allow the results not to clearly describe the studies ofIslamic Bank Governance. Also, this study was able to produce numerical visual data with the help of data analysis software. Therefore, the next study needs to use the source of articles from the Scopus database and the Web of Science which are published in journals, books, and proceedings. Also, this study had the limitation of using only a qualitative method and use qualitative and quantitative research approaches to content analysis. Thus, the next study needs to use both the qualitative and quantitative method and also produce a developing findings.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Idah Zuhroh

Idah Zuhroh has research interests in Islamic finance and banking field. Currently, Idah Zuhroh works at the Faculty of Economics and Business, Universitas Muhammadiyah Malang as Associate Professor.

References

- Abdelhak, E. E., Elamer, A. A., AlHares, A., & McLaughlin, C. (2019). Auditors’ ethical reasoning in developing countries: The case of Egypt. International Journal of Ethics and Systems, 35(4), 558–22. https://doi.org/10.1108/IJOES-02-2019-0041

- Ahmed, I., Nawaz, M. M., Danish, R. Q., Usman, A., & Shaukat, M. Z. (2017). Objectives of Islamic banks: A missive from mission statements and stakeholders’ perceptions. Journal of Islamic Accounting and Business Research, 8(3), 284–303. https://doi.org/10.1108/JIABR-08-2014-0028

- Akbar, S., Zulfiqar Ali Shah, S., & Kalmadi, S. (2012). An investigation of user perceptions of Islamic banking practices in the United Kingdom. International Journal of Islamic and Middle Eastern Finance and Management, 5(4), 353–370. https://doi.org/10.1108/17538391211282845.

- Al-Magharem, A. A. S., Haat, M. H. C., Hashim, H. A., & Ismail, S. (2019). Corporate governance and loan loss provisions: A review. Journal of Sustainability Science and Management 14(4), 228–241. . https://www.scopus.com/inward/record.uri?eid=2-s2.0-85075649041&partnerID=40&md5=44a3e98b59a2a994474c5a85260dd907.

- Alam, M. K., Ahmad, A. U. F., & Muneeza, A. (2020b). External Sharī‘ah audit and review committee Vis-a-Vis Sharī‘ah compliance quality and accountability: A case of Islamic banks in Bangladesh. Journal of Public Affairs, 22(1), 1–10 . https://doi.org/10.1002/pa.2364.

- Alam, M. K., Mustafa, H., Uddin, M. S., ISLAM, M. J., Mohua, M. J., & HASSAN, M. F. (2020). Problems of Shariah governance framework and different bodies: An empirical investigation of Islamic Banks in Bangladesh. The Journal of Asian Finance, Economics and Business, 7(3), 265–276. https://doi.org/10.13106/jafeb.2020.vol7.no3.265.

- Albaity, M., Mallek, R. S., & Noman, A. H. M. (2019). Competition and bank stability in the MENA region: The moderating effect of Islamic versus conventional banks. Emerging Markets Review, 38, 310–325. https://doi.org/10.1016/j.ememar.2019.01.003

- Albaity, M., Md Noman, A. H., & Mallek, R. S. (2021). Trustworthiness, good governance and risk taking in MENA countries. Borsa Istanbul Review, 21(4), 359–374. https://doi.org/10.1016/j.bir.2020.12.002

- Algabry, L., Alhabshi, S. M., Soualhi, Y., & Alaeddin, O. (2020). Conceptual framework of internal Sharīʿah audit effectiveness factors in Islamic banks. ISRA International Journal of Islamic Finance, 12(2), 171–193. https://doi.org/10.1108/IJIF-09-2018-0097

- Alhammadi, S., Alotaibi, K. O., & Hakam, D. F. (2020). Analysing Islamic banking ethical performance from Maqāṣid al-Sharī‘ah perspective: Evidence from Indonesia. Journal of Sustainable Finance & Investment, 1–23. https://doi.org/10.1080/20430795.2020.1848179

- Alshammary, M. J. (2014). An alternative conceptual corporate governance framework for high-context cultures: A case for the Islamic & Arabian Middle East. Corporate Board: Role, Duties and Composition. https://doi.org/10.22495/cbv10i3art3.

- Aslam, E., Haron, R., & Tahir, M. N. (2019). How director remuneration impacts firm performance: An empirical analysis of executive director remuneration in Pakistan. Borsa Istanbul Review, 19(2), 186–196. https://doi.org/10.1016/j.bir.2019.01.003

- Atanga Ondoa, H., & Seabrook, A. M. (2020, March). Governance and financial development: Evidence from a global sample of 120 countries. International Journal of Finance and Economics, 1–16. https://doi.org/10.1002/ijfe.2327

- Ballester, L., González-Urteaga, A., & Martínez, B. (2020). The role of internal corporate governance mechanisms on default risk: A systematic review for different institutional settings. Research in International Business and Finance, 54, 101293. https://doi.org/10.1016/j.ribaf.2020.101293

- Ben Bouheni, F., Ammi, C., & Levy, A. (2016). Banking Governance. Banking Governance, Performance and Risk-Taking, 31(4), 29–50. https://doi.org/10.1002/9781119361480.ch2

- Biancone, P. P., Saiti, B., Petricean, D., & Chmet, F. (2020). The bibliometric analysis of Islamic banking and finance. Journal of Islamic Accounting and Business Research, 11(9), 2069–2086. https://doi.org/10.1108/JIABR-08-2020-0235

- Bukair, A. A., & Abdul Rahman, A. (2015). Bank performance and board of directors attributes by Islamic banks. International Journal of Islamic and Middle Eastern Finance and Management, 8(3), 291–309. https://doi.org/10.1108/IMEFM-10-2013-0111.

- Cheteni, P. (2014). Awareness of Islamic banking products and services among consumers in South Africa. Mediterranean Journal of Social Sciences. https://doi.org/10.5901/mjss.2014.v5n9p96

- Darmadi, S. (2013). Corporate governance disclosure in the annual report: An exploratory study on Indonesian Islamic banks. Humanomics, 29(1), 4–23. https://doi.org/10.1108/08288661311299295

- El-Galfy, A., & Khiyar, K. A. (2012). Islamic banking and economic growth: A review. Journal of Applied Business Research (JABR), 28(5), 943. https://doi.org/10.19030/jabr.v28i5.7236

- González, L. O., Razia, A., Búa, M. V., & Sestayo, R. L. (2019). Market structure, performance, and efficiency: Evidence from the MENA banking sector. International Review of Economics and Finance, 64(May), 84–101. https://doi.org/10.1016/j.iref.2019.05.013

- Grira, J., & Labidi, C. (2020). Banks, Funds, and risks in Islamic finance: Literature & future research avenues. Finance Research Letters. Elsevier Ltd. https://doi.org/10.1016/j.frl.2020.101815

- Handayati, P., Krisnawati, D., Soetjipto, B. E., & Sudarmiatin, S. (2017). The shariah enterprise theory: Implementation of corporate social responsibility disclosure for Islamic Banking in Indonesia and Malaysia. International Journal of Economic Research, 14(13), 195–206.

- Hartanto, D., Agussani, A., & Dalle, J. (2021). Antecedents of public trust in government during the COVID-19 pandemic in Indonesia: Mediation of perceived religious values. Journal of Ethnic and Cultural Studies, 8(4), 321–341. https://doi.org/10.29333/EJECS/975

- Hasan, R., Hassan, M. K., & Aliyu, S. (2020). Fintech and Islamic finance: Literature review and research agenda. International Journal of Islamic Economics and Finance (IJIEF), 3(1), 75–94. https://doi.org/10.18196/ijief.2122

- Hassan, S. (2019). An empirical investigation of regulatory framework for Islamic banking system in Saudi Arabia. International Journal of Innovation, Creativity and Change, 7(3), 129–142.

- Hassan, A., & Haridan, N. (2019). Shariah auditing and Shariah compliance assurance in Malaysian Islamic banks. Global Journal Al Thaqafah, SI, 61–72. https://doi.org/10.7187/GJATSI112019-6

- Hassan, A., & Saleem, S. (2017). An Islamic microfinance business model in Bangladesh: Its role in alleviation of poverty and socio-economic well-being of women. Humanomics, 33(1), 15–37. https://doi.org/10.1108/H-08-2016-0066

- Husseini, S. A., Fam, S.-F., Ahmat, N. N., Azmi, F. R., Prastyo, D. D., & Yanto, H. (2019a). Islamic banking revolution in Malaysia: A review. Humanities and Social Sciences Reviews, 7(4), 267–275. https://doi.org/10.18510/hssr.2019.7434

- Ifada, L. M., Ghozali, I., & Faisal, F. (2019). Islamic organizational culture, Islamic corporate social responsibility, and corporate performance: Evidence from Sharia Bank in Indonesia. International Journal of Financial Research, 10(6), 118. https://doi.org/10.5430/ijfr.v10n6p118

- Istrefi, V. (2020). Corporate governance in Islamic financial institutions. Journal of Governance and Regulation, 9(2), 75–82. https://doi.org/10.22495/jgrv9i2art5

- Kabir, M. R., Sobhani, F. A., Omar, N., & Mohamad, N. (2019). Corporate governance and risk disclosures: A comparative analysis between Bangladeshi and Malaysian Islamic Banks. International Journal of Financial Research, 10(5), 110. https://doi.org/10.5430/ijfr.v10n5p110

- Kanas, A., Hassan Al-Tamimi, H. A., Albaity, M., & Mallek, R. S. (2019). Bank competition, stability, and intervention quality. International Journal of Finance and Economics, 24(1), 568–587. https://doi.org/10.1002/ijfe.1680

- Kasim, N., Hashim, N. A. B., & Salman, S. A. (2016). Conceptual relationship between corporate governance and audit quality in Shari’ah compliant companies listed on Bursa Malaysia. Modern Applied Science, 10(7), 106. https://doi.org/10.5539/mas.v10n7p106

- Khalid, A. A., Haron, H., & Masron, T. A. (2018). Competency and effectiveness of internal Shariah audit in Islamic financial institutions. Journal of Islamic Accounting and Business Research, 9(2), 201–221. https://doi.org/10.1108/JIABR-01-2016-0009

- Khan, A., Hassan, M. K., Paltrinieri, A., Dreassi, A., & Bahoo, S. (2020). A bibliometric review of takaful literature. International Review of Economics and Finance, 69, 389–405. https://doi.org/10.1016/j.iref.2020.05.013

- Khatib, S. F. A., Abdullah, D. F., Elamer, A. A., & Abueid, R. (2021). Nudging toward diversity in the boardroom: A systematic literature review of board diversity of financial institutions. Business Strategy and the Environment, 30(2), 985–1002. https://doi.org/10.1002/bse.2665

- Lahrech, N., Lahrech, A., & Boulaksil, Y. (2014). Transparency and performance in Islamic banking: Implications on profit distribution. International Journal of Islamic and Middle Eastern Finance and Management, 7(1), 61–88. https://doi.org/10.1108/IMEFM-06-2012-0047

- Louhichi, A., Louati, S., & Boujelbene, Y. (2019). Market-power, stability and risk-taking: An analysis surrounding the riba -free banking. Review of Accounting and Finance, 18(1), 2–24. https://doi.org/10.1108/RAF-07-2016-0114

- Mansoor, M., Ellahi, N., Hassan, A., Malik, Q. A., Waheed, A., & Ullah, N. (2020). Corporate governance, Shariah governance, and credit rating: A cross-country analysis from asian Islamic banks. Journal of Open Innovation: Technology, Market, and Complexity, 6(4), 170. https://doi.org/10.3390/joitmc6040170

- Mansori, S., Kim, C. S., & Safari, M. (2015). A Shariah perspective review on Islamic microfinance. Asian Social Science, 11(9), 273–280. https://doi.org/10.5539/ass.v11n9p273

- Mansour, W. (2020). Toward new strategies of Islamic financial products development. Journal of Islamic Accounting and Business Research, 11(9), 2053–2067. https://doi.org/10.1108/JIABR-09-2018-0135

- Meslier, C., Risfandy, T., & Tarazi, A. (2020). Islamic banks’ equity financing, Shariah supervisory board, and banking environments. Pacific-Basin Finance Journal, 62, 101354. https://doi.org/10.1016/j.pacfin.2020.101354

- Mohd Noor, N. S., Mohd. Shafiai, M. H., & Ismail, A. G. (2019). The derivation of Shariah risk in Islamic finance: A theoretical approach. Journal of Islamic Accounting and Business Research, 10(5), 663–678. https://doi.org/10.1108/JIABR-08-2017-0112

- Mukhibad, H., Nurkhin, A., & Rohman, A. (2020). Corporate governance mechanism and risk disclosure by Islamic banks in Indonesia. Banks and Bank Systems, 15(1), 1–11. https://doi.org/10.21511/bbs.15(1).2020.01

- Musleh Al-Sartawi, A. M. A. (2020) ‘Shariah disclosure and the performance of Islamic financial institutions’, Asian Journal of Business and Accountinghttps://www.scopus.com/inward/record.uri?eid=2-s2.0-85089016068&partnerID=40&md5=9b0d5b1b82a8db3006144a31a4d327b1

- Narayan, P. K., & Phan, D. H. B. (2019). A survey of Islamic banking and finance literature: Issues, challenges and future directions. Pacific-Basin Finance Journal, 53, 484–496. https://doi.org/10.1016/j.pacfin.2017.06.006

- Naysary, B., Salleh, M. C. M., & Abdullah, N. I. (2020). A comprehensive appraisal of Sharīʿah governance practices in Malaysian Islamic banks. ISRA International Journal of Islamic Finance, 12(3), 381–400. https://doi.org/10.1108/IJIF-09-2018-0104

- Neifar, S., Salhi, B., & Jarboui, A. (2020). The moderating role of Shariah supervisory board on the relationship between board effectiveness, operational risk transparency and bank performance. International Journal of Ethics and Systems, 36(3), 325–349. https://doi.org/10.1108/IJOES-09-2019-0155

- Nomran, N. M., & Haron, R. (2019). Dual board governance structure and multi-bank performance: A comparative analysis between Islamic banks in Southeast Asia and GCC countries. Corporate Governance: The International Journal of Business in Society, 19(6), 1377–1402. https://doi.org/10.1108/CG-10-2018-0329

- Obid, S. N. S., & Naysary, B. (2014). Toward a comprehensive theoretical framework for Shariah governance in Islamic financial institutions. Journal of Financial Services Marketing, 19(4), 304–318. https://doi.org/10.1057/fsm.2014.26

- Oladapo, I. A., Arshad, R., Muda, R., & Hamoudah, M. M. (2019). Perception of stakeholders on governance dimensions of the Islamic banking sector. International Journal of Emerging Markets, 14(4), 601–619. https://doi.org/10.1108/IJOEM-12-2017-0510

- Parsa, M. (2020). Efficiency and stability of Islamic vs. conventional banking models: A meta frontier analysis. Journal of Sustainable Finance and Investment, 1–21. https://doi.org/10.1080/20430795.2020.1803665

- Riaz, U., Burton, B., & Monk, L. (2017). Perceptions on Islamic banking in the UK—Potentialities for empowerment, challenges and the role of scholars. Critical Perspectives on Accounting, 47, 39–60. https://doi.org/10.1016/j.cpa.2016.11.002

- Rozzani, N., Mohamed, I. S., & Yusuf, S. N. S. (2016). Technology for Islamic microfinance’s disbursement and repayment system. International Journal of Social Economics, 43(12), 1271–1283. https://doi.org/10.1108/IJSE-05-2015-0115

- Saha, R., & Kabra, K. C. (2020). Corporate governance and voluntary disclosure: A synthesis of empirical studies. Business Perspectives and Research, 8(2), 117–138. https://doi.org/10.1177/2278533719886998

- Sakti, M. R. P., Tareq, M. A., Saiti, B., & Akhtar, T. (2017a). Capital structure of Islamic banks: A critical review of theoretical and empirical research. Qualitative Research in Financial Markets, 9(3), 292–308. https://doi.org/10.1108/QRFM-01-2017-0007

- Salman, M. H. A., & Nobanee, H. (2019). Recent developments in corporate governance codes in the GCC region. Research in World Economy, 10(3), 108. https://doi.org/10.5430/rwe.v10n3p108

- Samori, Z., Rahman, F. A., & Zahari, M. S. M. (2017). Adoption of Shari’ah governance framework of Islamic financial institution industry into the Muslim friendly hospitality industry in Malaysia: Is it possible? Journal of Engineering and Applied Sciences. https://doi.org/10.3923/jeasci.2017.3665.3671

- Shahar, N. A., Nawawi, A., & Salin, A. S. A. (2020). Shari’a corporate governance disclosure of Malaysian IFIS. Journal of Islamic Accounting and Business Research, 11(4), 846–868. https://doi.org/10.1108/JIABR-05-2016-0057

- Smolo, E., Šeho, M., & Kabir Hassan, M. (2020). Development of Islamic finance in Bosnia and Herzegovina. Journal of Economic Cooperation and Development, 41(1), 121–144. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85088046500&partnerID=40&md5=b4b4ef8706401542ee5d0029025f5a35

- Srairi, S. (2019). Transparency and bank risk-taking in GCC Islamic banking. Borsa Istanbul Review, 19, S64–S74. https://doi.org/10.1016/j.bir.2019.02.001

- Sulub, S. A., Salleh, Z., & Hashim, H. A. (2018). A review of corporate governance and corporate social responsibility disclosure of Islamic banks: A call for additional transparency. Journal of Sustainability Science and Management. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85052878596&partnerID=40&md5=92f76f24942bdc986f022f378c871a18

- Sulub, S. A., Salleh, Z., & Hashim, H. A. (2020a). Corporate governance, SSB strength and the use of internal audit function by Islamic banks: Evidence from Sudan. Journal of Islamic Accounting and Business Research, 11(1), 152–167. https://doi.org/10.1108/JIABR-12-2016-0148

- Sutrisno, & Widarjono, A. (2018). Maqasid sharia index, banking risk and performance cases in Indonesian Islamic banks. Asian Economic and Financial Review. https://doi.org/10.18488/journal.aefr.2018.89.1175.1184

- Yunan, Z. Y. (2021). Does corruption affect Islamic banking? Empirical evidence from the OIC countries. Journal of Financial Crime, 28(1), 170–186. https://doi.org/10.1108/JFC-06-2020-0101

- Zafar, M. B., & Sulaiman, A. A. (2019). Corporate social responsibility and Islamic banks: A systematic literature review. Management Review Quarterly, 69(2), 159–206. https://doi.org/10.1007/s11301-018-0150-x

- Zaki, I., Mawardi, I., Widiastuti, T., Hendratmi, A., & Anova, D. F. (2019). Business network strategy in Islamic micro finance institution of Islamic boarding school. Humanities and Social Sciences Reviews, 7(4), 276–279. https://doi.org/10.18510/hssr.2019.7435