?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We aim to investigate the sustainable growth rate that mediate the relationship between the firm specific factors and share price performance. The existing literature provides inadequate findings on the relationship between the firm specific factors and share price performance; there is an implicit assumption that this relationship is direct. An alternative perspective that has received less attention in the literature posits that this relationship can be mediated by the sustainable growth rate, especially from the perspective of Shariah-compliant companies. Using STATA software, we conducted structural equation model (SEM) to analyse data from 181 Shariah-compliant companies in Malaysia collected from 2007 to 2016. According to our results, the Shariah-compliant sample meets SEM requirements, such that the sustainable growth rate shows a significant relationship with share price performance. According to mediation effect results, capital structure, dividend policy, profitability and firm size are considered “indirect-only mediator”. These results demonstrate that certain factors influence the sustainable growth rate, including the planning and managing of a firm’s financial and operational activities. The sustainable growth rate is important for helping firms to manage, guide, control and plan their operating and financial strategies. The sustainable growth rate can also improve financial performance and assist managers with financing decisions. The findings of this study can be used as a reference for future studies that examine other aspects of the sustainable growth rate, especially across sectors, to determine how firms can more successfully manage financial and operating activities.

PUBLIC INTEREST STATEMENT

Issues of sustainability are among the areas that have been receiving more comprehensive attention from managers and investors when handling their business investment. Handling financial (capital structure and dividend policy) and operating activities (profitability and company efficiency) becomes an important factor that can influence the sustainable growth of the company. The role of the sustainable growth rate (SGR) must be considered, as it is a future-oriented measure of firm performance that may have a significant impact on firm share price performance (SPP). Due to the potential ability of SGR to act as a mediator, this study investigated the mediating effect of SGR between firm specific factors (capital structure, dividend policy, profitability, company efficiency and firm size) and the SPP of firms. The findings showed indirect-only mediators for capital structure, dividend policy, profitability and firm size. The result indicated that an increase or decrease in firm specific factors can increase the SGR and lead to an increase in SPP.

1. Introduction

The sustainable growth rate (SGR) is considered a factor that is strongly related to firm performance and that plays an important role in maximizing growth rates without increasing firm debt or issuing new equity. SGR is a key indicator that firms use to gauge their business profitability performance. According to Higgins (Citation1977), sustainable growth in a business context is the maximum platform or benchmark required for a company to grow its revenue without reducing its financial resources. It depends on the earnings retention rate (R) and the return on equity (SGR = ROE × RR). The combination of a company’s operating elements (i.e., profit margin and company efficiency) and financial elements (i.e., capital structure and retention ratio) into a single measurement is a very valuable financial performance measurement for every company. Based on a previous study by Srinivasa (Citation2011), the combination of operating and financial elements in a comprehensive measurement is of great importance to sustainable growth because this can increase the value of a firm. According to pecking order theory, a company is required to fund financial resources by retaining earnings at first. However, when the company experiences financial problems, it must raise funds on debt, followed by equity. Based on the trade-off theory, growth causes firms to shift their financing from new equity to debt to reduce agency problems. Handling financial leverage, dividend policy, profitability, and company efficiency become important and can influence the sustainable growth of a company. Therefore, the monitoring of firm performance is very important and can solve a company’s financial problems to sustain its growth.

According to Johnson and Soenen (Citation2003), a company’s strategic planning in handling its limitations and policy constraints (referring to leverage and dividend payouts) can help the company to sustain its growth. A higher profit margin, a higher debt-to-equity ratio, a lower dividend payout ratio, and a lower assets-to-sales ratio can increase the SGR (Arellano & Higgins, Citation2007). Amouzesh et al. (Citation2011) noted that the combination of operating and financial elements, such as profit margin, company efficiency, and capital structure and retention rate, are associated with SGR. The four main factors that influence the SGR are (1) financial leverage, (2) dividend policy, (3) profitability, and (4) asset efficiency (Higgins, Citation1977). However, the firm specific factors are unclear.

A new revised Shariah screening methodology of two-tier quantitative assessment for activity-based screening benchmarks and the newly- formulated financial ratio benchmarks, while the qualitative assessment remains the same has been formulated by Shariah Advisory Council (SAC) of Securities Commission (SC). The efficient of the system in the equity market could generate better income to the country’s economy when the screening methodology has classifies the Shariah and non-Shariah stocks. Due to that fact, one of the important elements to ensure the possible income to the economy is that the classification of the particular stock would affect the performance of the volume of the stock trading and as well as the share prices (Fauzias et al., Citation2019). In Malaysia, particularly as a Muslim country, the status of a particular stock would affect Muslim investor’s decision to invest in Shariah stocks.

In addition to focusing on factors that influence the SGR, it is also unclear whether the SGR mediates the relationship between firm specific factors and share price performance (SPP). Based on a previous study, the role of the SGR must be considered, as it is a future-oriented measure of firm performance that may have a significant impact on firm stock price (Arora, Kumar, Verma et al., Citation2018a). Moreover, increased costs are not limited to the usual cost variety but also include the impact on the share price of employing what management believes to be excessive debt or distributing what is believed to be too little in dividends (Higgins, Citation1977). Thus, managing a company’s financial and operating activities can increase its value and SPP. However, it is unclear whether firm specific factors directly affect SPP and whether SGR is significantly related with SPP?

Several studies have also investigated the relationships between capital structure (Welch, Citation2004), dividend policy (Hashemijoo et al., Citation2012; Hussainey et al., Citation2011; Khan, Citation2012; Sharif et al., Citation2015), profitability (Buzzell et al., Citation1975) and asset efficiency (Beccalli et al., Citation2006) and SPP. To the best of our knowledge, only Sutjiati (Citation2017) has investigated how the SGR mediates the effect of investment in fixed assets and dividend policies on company value (price book value). However, no studies have studied the SGR as a mediator of the relationship between firm specific factors and SPP. Due to the potential ability for the SGR to act as a mediator, the present work examines the mediating effect of the SGR on firm specific factors (capital structure, dividend policy, profitability, and company efficiency) and the SPP of Malaysian Shariah-compliant firms. However, it is unclear whether SGR mediates the relationship between the firm specific factors and SPP. The four objectives of this research are as follows.

To examine the direct relationship between firm specific factors and SPP.

To examine the direct relationship between firm specific factors and the SGR.

To investigate the significant relationship between the SGR and SPP.

To determine mediating effects of the SGR on the relationship between firm specific factors and SPP.

To address the above research questions and research objectives, we use a quantitative approach to collect data from the Thomson Reuters Database. We study 181 Malaysian Shariah-compliant companies from 2007 to 2016. We apply a Structural Equation Model (SEM) using STATA software for our data analysis.

This paper is intended to contribute to the additional knowledge in the existing literature by focusing on the issues of mediation effect of sustainable growth rate between the firm specific factors and share price performance in the context of Malaysian public-listed Shariah-compliant firms. The research will provide understandings related to the issues and challenges that are faces by Malaysian Public-listed Shariah-compliant firms in the view of SGR and SPP. The research relevance for management teams of companies to monitor and efficiently manage financial and operating activities of the firms. The research can provide financial information concerning the usage of debt in a firm’s capital structure, the payment of dividend, firm’s profitability, company’s efficiency, and larger or smaller firms that could lead to a higher or lower SGR and SPP.

This paper is organized as follows. The following session provides a literature review of firm specific factors, the SGR and SPP. This is followed by the research methodology, sample and variable measurements used. The following section then analyses the research findings and provides conclusions and implications for future research.

2. Review of the literature

2.1. Sustainable growth rate

Sustainability is an issue that has attracted more attention from managers and investors in managing their business investment. In financial contexts, the term of sustainability refers to the SGR. The SGR is the maximum growth rate a firm can achieve without having to increase its financial leverage or sell new equity. According to Higgins (Citation1977), sustainable growth in a business context can be defined as the maximum platform or benchmark from which a company can grow its revenue without reducing its financial resources. The literature has identified several factors that influence the SGR. A widely known framework for the SGR was developed by Higgins (Citation1977) and identifies four main factors that influence the SGR: capital structure, dividend policy (under financial constraints), profitability, and asset efficiency. According to a previous study by Amouzesh et al. (Citation2011), a firm’s SGR depends only on its earnings’ retention rate (r) and return on equity. The calculation of the SGR refers to the retention ratio of multiple return on equity. Capital structure, profitability (profit margin), asset efficiency and the retention ratio are associated with the SGR and reflect a combination of operating and financial elements. The combination of a company’s operating (i.e., profit margin and asset efficiency) and financial elements (i.e., capital structure and retention ratio) into a single measure then becomes a very valuable financial performance measure for every company. Vasiu and Ilie (Citation2018) found that asset turnover has a negative effect on the SGR. They also claimed that an increase in revenue is measured by an increase in efficiency in the usage of its assets. This reduces the need to increase the asset base in order to support revenue growth, and thus leads to an increase in the SGR.

For firms, SGR results can guide the growth strategies of financially distressed firms and firms attempting to reduce their leverage. For firms with access to financial markets, the SGR formula indicates whether they will need to raise new funds to achieve a sales growth level in excess of their SGR (Platt et al., Citation1995). Moreover, Harkleroad (Citation1993) stated that the SGR serves as an analytical framework that helps identify which elements of a firm’s operating and financial structure management to focus on to improve its financial performance. SGR also enables analysts to compare performance over time to quickly identify the key elements of a competitor’s strategy so that they can focus on identifying the competitor’s strengths and weaknesses. The SGR is also an imperative tool in helping managers make major corporate financial decisions (Guilford, Citation1970). Arora, Kumar, Verma et al. (Citation2018a) noted that the SGR can be useful to managers in balancing their operational and financial strategies. The SGR has been cited as a practically applicable concept in modern financial management contexts that can be used as a strategic planning and controlling tool for a firm (Fonseka et al., Citation2012). Pham et al. (Citation2021) found that a positive relationship between corporate sustainability and financial performance (earnings yield, return on asset, return on equity and return on capital employed).

Higgins (Citation1977) also mentioned that the SGR model is a useful tool for evaluating alternatives and for ensuring that internal financial, operating, and growth strategies adopted are consistent. The final policies adopted by a firm and their implementation are dependent on firm management. Moreover, Kanani et al. (Citation2013) state that important factors shaping financial information include a firm’s growth and level of risk facing a company. In this case, the decision-making process and investment guidance are influenced by financial information. Sometimes, a growth rate that is too high places financial stress on a company, thereby subjecting a firm to higher costs, higher debt, bankruptcy, financial losses, and declining market shares (Fonseka et al., Citation2012). Therefore, the SGR is a very important tool in helping a firm manage, guide, control and plan operating and financial strategies to improve its financial performance and help its managers make financing decisions. This study focuses on the importance of the SGR for firms.

2.2. Firm specific factors, SGR and SPP

The SGR must be evaluated with specific measures of a company’s performance. This measurement can be described by determining the factors that affect a firm’s SGR to help stakeholders (either internal or external management teams or customers) make the right decisions. According to Hartono and Utami (Citation2016) and Rădăşanu (Citation2015), the SGR is influenced by four factors: (1) the profitability ratio, where an increase in the profitability ratio increases the generation of internal funds with direct impacts on achieving growth; (2) the asset turnover ratio, where an increase in this ratio causes an increase in sales generated per asset unit, which reduces the need for additional assets for an increase in sales and which results in an increase in the SGR; (3) financial policy, where an increase in total debt provides additional resources and increases the SGR; and (4) dividend policy, where an increase in the retention rate increases the growth of capital and implicitly the SGR. According to Vasiliou and Karkazis (Citation2002), the SGR is not only applicable to firms but can also be used for banks. The authors showed that banks must determine the maximum annual rate to increase total assets that can be supported by internally generated equity capital.

Hartono and Utami (Citation2016) and Rădăşanu (Citation2015) stated that the profitability ratio where an increase in the profitability ratio increases the generation of internal funds with direct impacts on achieving growth. Lim and Rokhim (Citation2021) found strong and positive relationship between liquidity and sustainable growth rate with profitability as measured by return on equity, return on assets and earning per share, except earnings per share for liquidity. Therefore, more profitable firms would give higher SGR? In relation between firm size and SGR, Wang et al. (Citation2019) measured the size of firm as its normal logarithm of total company assets. They found that the relationship between the sustainable growth rate and the size of the company is positive and significant. Xu and Wang (Citation2018) also found that firm size has a significant and positive impact on SGR. In contrast, Huang et al. (Citation2019) found that firm size is significantly negative and suggested that the higher of the value, the lower the sustainable growth of firm. Similarly, Mamilla (Citation2019) the results show that firm’s size and debt-equity ratio has significant negative relationship with SGR. Thus, firm’s size can have a positive and negative impact on the SGR of firm.

Moreover, Lockwood and Prombutr (Citation2010) investigate the association between sustainable growth and stock returns for 1964–2007 using monthly stock prices. They obtained significant results using Time-Series Regressions, Cross-Sectional Regressions, and Firm-Level Regression Tests. They found that firms experiencing high levels of sustainable growth tend to experience low default risk, book-to-market ratios, and subsequent returns. In addition, the net profit margin is a major determinant of subsequent returns relative to each SGR component. The SGR is maintained after controlling asset and capital expenditure growth. Another analysis stated that the sustainable growth effect is attributable to risk and not to mispricing. These results are consistent with a discussion on rational pricing by Fama and French (Citation1995), who found that low-profit firms tended to have high BE/ME ratios and high required returns. In this case, the authors mention that low profitability reflects a high level of distress risk, which in turn should be related to high required returns.

Furthermore, Chandra et al. (Citation2019) indicated that capital structure has no effect on the stock returns of companies listed on the compass index 100 in Indonesia. They stated that their results are not in line with the research conducted by Khan (Citation2012) who found a positive effect of capital structure on stock returns. Ali et al. (Citation2017) stated that dividend per share and retention ratio have an insignificant relationship with share market prices, but dividend payout ratio has a significant positive relationship with share prices. Similarly, Hashemijoo et al. (Citation2012), whose results did not show a significant relationship between stock price volatility and dividend policy in Malaysian consumer products firms. They also found a significant negative relationship between stock price and dividend yield and between stock price volatility and payout ratio. This is because dividend policies implemented across different industries tend to vary; hence, it is not surprising that different results are attained for Malaysian industrial product firms. Dzikevičius and Šaranda (Citation2011) found no significant relation between assets turnover and stock returns. The non-significant finding is consistent with the recent findings of Lyroudi (Citation2018), who stated that there was no evidence of a statistically significant strong linear relationship between the assets turnover ratio and stock returns. Yang et al. (Citation2010) indicated that small firms tended to earn higher average stock returns than large firms (Banz’s “size effect”, 1981). The results, consistent with Fama and French (Citation1995), stated that small firms may suffer a long earnings depression that bypasses big firms, thereby suggesting that size is associated with a common risk factor that leads to the negative relationship between size and stock return.

Several studies have investigated the relationship between capital structure (Welch, Citation2004), dividend policy (Hussainey et al., Citation2011; Hashemijoo et al., Citation2012; Khan, Citation2011; Sharif et al., Citation2015), profitability (Buzzell et al., Citation1975) and asset efficiency (Beccalli et al., Citation2006) and SPP. However, few studies have examined the SGR as a mediator of the relationship between firm specific factors and SPP. Therefore, the present work determines the mediating effect of the SGR on the relationship between firm specific factors and SPP. shows the summary sample of studies on the sustainable growth rate.

Table 1. Sample of studies on the sustainable growth rate

of the research framework shows that certain facets of the SGR (capital structure, dividend policy, profitability, and company efficiency) might influence SPP. In addition, it is hypothesized that the SGR may mediate the relationships between firm specific factors (capital structure, dividend policy, profitability and company efficiency) and SPP.

Figure 1. Research framework.

summarizes the hypotheses and steps of the data analysis. The research framework used for this study was developed based on gaps identified in the literature. The mediation effects analysis is based on the SEM procedure proposed by Zhao et al. (Citation2010).

Table 2. Hypotheses and step by step of analysis

3. Research methodology

Structural equation modeling (SEM) was applied to estimate direct and indirect effects with the STATA software (Hussain et al., Citation2017; Gu et al., Citation2019). We adopted this approach as a suitable means to answer our research questions.

We employed panel unit root tests to determine whether the variables included in the model are stationary. As the data series are in panel form and unbalance. We used Fisher (augmented Dickey-Fuller (ADF); Dickey & Fuller, Citation1979) and PP-Fisher methods (Philips & Perron, Citation1988) as the most appropriate methods for unbalanced data testing. We in turn test the null hypothesis of unit roots (or stationary) in panel datasets. After confirming that all of the variables are stationary and multicolinear, SEM is conducted. The stages of the analysis are illustrated in Equationequations (1(1)

(1) –Equation4

(4)

(4) ).

Step 1:

Step 1:

Step 1:

Step 1:

4. Sample and variable measurement

The data of Malaysian listed Shariah-compliant firms from 2007 to 2016 were collected from the Thomson Reuters Database. shows the full dataset used for the study, which includes 181 firms. Listed companies from financial sectors are excluded from the sample due to unique facets of their financial statements and business activities (M. M. Ali et al., Citation2009).

Table 3. No. of final observations by using cook’s distance test

In addition, outliers (i.e., observations with large residuals) are measured using Cook’s distance test. If D > 1, then there is a substantial outlier problem, and the outliers are removed from the dataset. After removing outliers, we are left with 1731 final observations (refer to ).

lists the variables used in this research with the measurements for each variable. In this study, SPP is defined as an endogenous variable, while the SGR is used as a mediating variable. Exogenous variables include financial leverage, dividend policy, profit margins, company efficiency, and firm size.

Table 4. Variables used in the measure of firm specific factors, SGR and SPP

Previous studies have used the Higgins model to calculate the SGR (Amouzesh et al., Citation2011; Cahyo Hartono & Rahmi Utami, Citation2016; Chen et al., Citation2013; Escalante et al., Citation2009; Fonseka et al., Citation2012; Hafid, Citation2016; Molly et al., Citation2012). We use the Higgins model equation to calculate the SGR of Shariah-compliant firms in Malaysia. The SGR is generally based on information provided in a firm’s annual report and takes the following form: SGR = ROE × (1-DPR). There are a range of alternative SGR measures (Higgins, Citation1977) with variations found in both the measurement of returns on equity and the measurement of the dividend payout ratio selected for calculation. SPP determined based on a previous study by Lockwood and Prombutr (Citation2010).

5. Empirical results

This section reports the results of our estimations of mediation effects based on an SEM employed using Stata Software for the datasets described above for 2006 to 2017. The following discussion describes our descriptive statistics, unit root tests and four-stage mediation effects analysis.

Descriptive statistics

presents the descriptive statistics for the Shariah-compliant firms. The average dividend policy (DPR), firm size (TA) and sustainable growth rate (SGR) for Shariah-compliant companies are 31.66%, 20.31 and 4.81%, respectively. The minimum SGR is −1.25% and the maximum is 55% with 8.79% as the standard deviation. The minimum DPR and TA are −774% and 17.42, respectively, while the maximum DPR and TA are 1453% and 25.61, respectively. The average capital structure (TDTE), net profit margin (NPM), company efficiency (STA) and share price performance (SPP) values are 37%, 8%, 2.29 and 8.6%, respectively. The minimum and maximum TDTE are −306% and 1296%, respectively. The standard deviation of NPM and STA are 20% and 51%, respectively, and the standard deviation of SPP is 39%.

Table 5. Descriptive statistics

5.1 Panel unit root test and goodness of fit test

Panel unit root tests were also adopted to confirm that the variables are stationary at I(0) to avoid making incorrect inferences should this condition not be met. shows the panel unit root tests of unbalanced data by using Fisher (augmented Dickey-Fuller (ADF; Dickey & Fuller, Citation1979) and PP-Fisher methods (Philips & Perron, Citation1988). We find that most of the variables are stationary at I(0) or have stationary characteristics since nulls of the unit root are rejected. This allows us to further estimate direct and indirect effects by performing SEM.

Table 6. Panel unit root tests

For the model fitness test, the results are reported in . With all of the model level fit measures considered together, the overall model fits well, meaning that the relationships among the variables as specified in the path model represent the patterns in the data well. Hence, the model is appropriated.

Table 7. Panel unit root tests

5.2. Mediation analysis

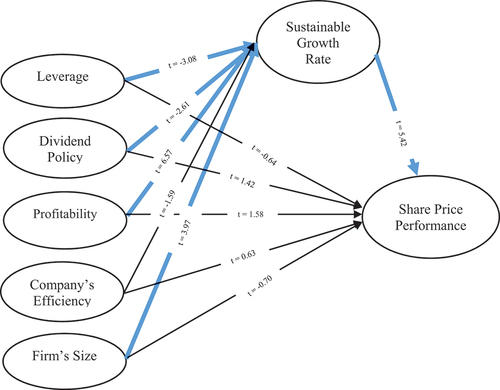

One of our main objectives is to examine mediating effects. Therefore, the following analyses examine (i) the relation between firm specific factors and SPP, (ii) the relation between firm specific factors and the SGR, (iii) the relation between the SGR and SPP, and (iv) the mediating effect (refer to ).

Table 8. Statistically significant value estimates for firm specific factors and SPP

5.1.1. Step 1: relation between firm specific factors and SPP

shows the relationships between firm specific factors and SPP (Hypothesis 1). The above results indicate that the direct relationship of all firm specific factors variables are not significant related with SPP. This finding is consistent with earlier findings for each exogenous variable, i.e., capital structure (Chandra et al., Citation2019), dividend policy (A. Ali et al., Citation2017; Hashemijoo et al., Citation2012), profitability (A. Ali et al., Citation2017), company’s efficiency (Dzikevičius & Šaranda, Citation2011; Lyroudi, Citation2018), and firm size (Ahmad et al., Citation2013). Capital structure has no effect on stock returns (Chandra et al., Citation2019). A. Ali et al. (Citation2017) found that dividends per share and the retention ratio are not significantly related to share market prices but the dividend payout ratio is significantly and positively related with share prices.

Table 9. The direct relationship between firm specific factors and SPP

Hashemijoo et al. (Citation2012) showed that there is no significant relationship between stock price volatility and dividend policy among Malaysian consumer products firms. With respect to profitability, profit after tax is not significantly related to stock prices, while earnings per share is significantly and positively related to stock prices (A. Ali et al., Citation2017). These findings suggest that firms should regularly pay dividends, as this will spur upward movement in stock market prices. Regarding a company’s efficiency, Dzikevičius and Šaranda (Citation2011) found no significant relation between asset turnover and stock returns. This finding of non-significance is consistent with the recent findings of Lyroudi (Citation2018), who found no evidence of a statistically significant, strong linear relationship between the asset turnover ratio and stock returns. However, firm size is not related to SPP. Ahmad et al. (Citation2013) found that firm size is not significant, indicating that is has no effect on stock returns. These findings is not consistent with the theoretical expectation that firm size affects stock returns. In this case, this result indicates that SPP would not necessarily increase regardless of higher or lower leverage, dividend policies, profitability levels, company efficiency or firm size.

5.1.2. Step 2: relation between firm specific factors and SGR

Hypothesis 2 examines the relationship between firm specific factors and the SGR. According to predicted sign and significance values for firm specific factors listed in , we find the same results for firm specific factors. All variables for Shariah-compliant firms have a significant relationship with the SGR except for company efficiency. Dividend policy is significantly and negatively related to the SGR. Theoretically, a negative relationship between the payout and growth ratios means that a high growth firm must reduce the payout ratio and retain more earnings to build up “precautionary reserves” but that low growth firms are likely to be more mature and to build up their reserves due to flexibility considerations (Lee et al., Citation2015).

Table 10. The direct relationship between firm specific factors and SGR

With respect to capital structure, profitability and firm size, the results show a significant relationship with the SGR. There is a significantly negative relationship between capital structure and the SGR. According to Fonseka et al. (Citation2012), a growth rate that is too high causes financial stress and subjects a company to higher costs, which may lead to bankruptcy, financial losses, and declining market share. Then, profitability and firm size show a significantly positive relationship with the SGR consistent with Higgins (Citation1977) who stated that more profitable firms have higher SGRs due to their effective investment in fixed assets, efficient working capital management, and higher taxes. Similarly with Wang et al. (Citation2019) and Xu and Wang (Citation2018) found that the relationship between the sustainable growth rate and the size of the company is positive and significant. In contrast, Huang et al. (Citation2019) and Mamilla (Citation2019) found that firm size is significantly negative and suggested that the higher of the value, the lower the sustainable growth of firm.

5.1.3. Step 3: relation between SGR and SPP

Hypothesis 3 predicts a positive relationship between the SGR of a firm and SPP. shows that among the Shariah-compliant sample, there is a significantly positive relationship between the SGR and SPP (z = 4.72, p < 0.01), indicating that a higher SGR tends to correspond with stronger SPP.

Table 11. The direct relationship between SGR and SPP

5.1.4. The mediation effect

shows whether the SGR has mediating effect on the relationship between firm specific factors and SPP. According to Ramli (Citation2014), Ramli and Nartea (Citation2016), and (Citation2018), certain requirements must be met to confirm mediation, as described by Baron and Kenny (Citation1986), Zhao et al. (Citation2010), and Iacobucci and Duhachek (Citation2003) and Maackinnon et al. (1995). Prerequisites to the mediation effect are shown in Figure and . First, the indirect path between “a” and “b” should be significant. Second, the relationship between path coefficients of firm specific factors and the SGR can be significant or non-significant (path c’). Finally, patch c (total direct effect) does not need to be significant.

Figure 2. Mediation effect.

Figure 3. Mediation effect on this research.

Table 12. SGR play as mediator between the firm specific factors and SPP

The sampled of Shariah-complaint companies incorporated into the mediation model show that the independent variable (firm specific factors) influences the mediator (the SGR), which in turn influences the dependent variable (SPP). According to , mediating effects of all of the variables reveal a significant mediation effect. The results are also confirmed via Sobel t-statistics.

The results of the mediation effect are based on the typology of mediation by Zhao et al. (Citation2010), Ramli (Citation2014), and (Citation2018); refer for details). shows summary results for mediation effect by type of mediation. From path c, none of the variables are significant. All variables are considered indirect-only mediator variable except for company efficiency. An indirect-only mediator variable denotes that an indirect effect (a × b) is significant while a direct effect (c) is not significant. Direct effects (c) for capital structure and dividend policy show an insignificant relationship, path a shows a negatively significant relationship, path b shows a positively significant relationship, and path c shows a significant relationship. Therefore, a decrease in capital structure can increase the SGR and lead to an increase in SPP. This result complies with trade off theory. Then, the direct effect (c) for profitability and firm’s size shows an insignificant relationship, path a shows a significantly positive relationship, path b shows significantly positive relationship, and path c shows a significant relationship.

Table 13. A typology of mediations

Table 14. Summary results of mediation effect with the typology of mediation

These results indicate that enhanced company efficiency and a larger firm size result in a higher SGR for firms and stronger SPP. This finding also shows that an increase in profitability can increase the SGR and lead to improvements in SPP.

5.3. Robustness test

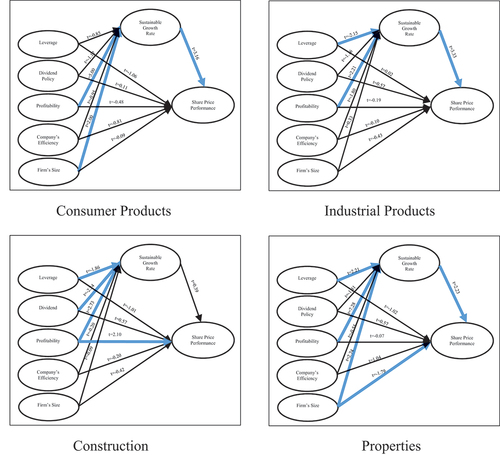

The following analysis discusses in details the empirical results for six industries such as consumer products, industrial products, construction, trading and services, properties, and plantation. Understanding the growth patterns of the industry is essential for establishing sustainable growth strategies (Park & Jang, Citation2010). In addition, the different industries have different characteristics and business activities. shows the results of the significant influence between the firm specific factors, SGR, and SPP by each industry.

Table 15. Statistically significant value estimates of the firm specific factors, SGR and SPP by each industry

The results on the Step 1 (the relationships between the firm specific factors and SPP) indicate that leverage, dividend policy, profitability, company’s efficiency, and firm’s size are not significantly related to SPP for all industries, but that only certain variables have a significant influence on the SPP in certain industries. The findings show that profitability has a positive influence on SPP in Construction, while company’s efficiency influence the SPP in Trading and services. Moreover, firm size has a significant influence on the SPP in Properties. This finding indicates that higher or lower SPP would not necessarily be influenced by leverage, dividend policy, profitability, company’s efficiency, or firm’s size. These findings are consistent and support the earlier findings for each exogenous variable, i.e. capital structure has no effect on stock returns (Chandra et al., Citation2019); dividend policy has no effect on stock returns (A. Ali et al., Citation2017; Hashemijoo et al., Citation2012); profitability has no effect on stock returns (A. Ali et al., Citation2017); Company’s efficiency has no effect on stock returns (Dzikevičius & Šaranda, Citation2011; Lyroudi (Citation2018); and firm size has no effect on stock returns (Ahmad et al., Citation2013).

Regarding on the Step 2 (the relationships between the firm specific factors and SGR), profitability has a positive significant influence on the SGR for the firms in all the industries. Firm size is reported to be positively related to the SGR in Consumer products, Trading and services, and Properties. The finding consistent with Higgins (Citation1977) who mentioned that more profitable firms have a higher SGR due to effective investment in fixed assets, efficient working capital management, and higher taxes. Leverage is found to be negatively related to a SGR in Industrial products and Construction but the same factor is positively related to a SGR in Properties. The prosperity of companies is much related to how managers manage their capital structure. The use of debt is limited as companies will face the prospect of bankruptcy. Under the pecking order theory, a company requires funding, financial resources by retained earnings at the beginning, but, if it still has financial problems, it is necessary for the company to raise funds on debt followed by equity. Based on the trade-off theory, growth causes firms to shift financing from new equity to debt to reduce agency problems. This is also related to whether the manager borrows money under long-term debt, short-term or equity in addition to improving company’s growth. Moreover, the use of debt can have an impact on the company earnings.

As for company’s efficiency, it is negatively related to the SGR in Industrial products and dividend policy is negatively related to a SGR in Construction. Theoretically, to increase the SGR, a company will reduce the payment of dividend to its shareholders when real growth is higher than the SGR. Then, the reduction in dividend payment can affect stock prices. Aligned with the signalling hypothesis, the effect of dividend policy will make changes to the stock prices, and the stock prices will go up or down. A negative relationship between the payout and growth ratios means that high growth firms need to reduce the payout ratio and retain more earnings to build up precautionary reserves, but low growth firms are likely to be more mature and build up their reserves for flexibility (Lee et al., Citation2015). Moreover, company’s efficiency has a positive significant relationship with a SGR. Higher asset efficiency tends to lead to a higher SGR. There is a significant negative relationship between leverage and SGR. According to Fonseka et al. (Citation2012), a growth rate that is too high causes financial stress, and, therefore, the company will face higher costs, which may lead to bankruptcy, financial losses, and a declining market share.

There is positive relationship between the SGR of the firm and SPP (under step 3) for all industries (p < 0.01) but insignificant results for Trading and services. The results indicate that a higher SGR tends to lead to higher SPP. This finding is consistent with the previous analysis by Fama and French (Citation1995) with rational pricing. The significant influence between the firm specific factors, SGR and SPP (under step 4) for each industry based on bootstrapping and the Sobel test in the mediation model is presented in . The results of Trading and services and Plantation shows that there is no-effect non-mediation for all variable. Table shows the summary results of the mediation effect with the typology of mediation only for Consumer products, Industrial products, Construction, and Properties.

Table 16. SGR as mediator between the firm specific factors and SPP by each sector

Table 17. Summary results of mediation effect with the typology of mediation for consumer products

Based on the results in , the mediation effect result indicates that firm size is considered as an “indirect-only mediator” in Consumer Products and “competitive mediation” in Properties. Competitive mediation means that the indirect effect (path: a × b) and direct effect (path c) are both significant, and the signs point in the opposite direction. For Consumer products, the direct effect (c) for firm size shows an insignificant relationship (a = −0.0023, z = −0.09, p > 0.10), path a shows a positive significant relationship (a = 0.0093, z = 2.00, p < 0.05), path b shows a positive significant relationship (a = 1.2336, z = 3.16, p < 0.01), and path c shows a significant relationship (a = 0.0115, z = 1.75, p < 0.10). This result indicates that larger firms would have a higher SGR and better SPP. Ahmad et al. (Citation2013) stated that firm size is not significant to the stock return, which means that the variable has no effect on stock returns; this result goes against the theoretical expectation that firm size affects stock returns.

Competitive mediation in Properties appears to cause a negative significant influence between firm size and SPP. This indicates that the larger the firm, the lower the SPP. This result is in line with Yang et al. (Citation2010) who indicated that small firms tended to earn higher average stock returns than large firms (Banz’s “size effect”, 1981). When the two hypotheses H2.2a (path a) and H3 (path b) are combined in one model (a × b) they have an indirect effect under the complex cause effect model. Hence, the combination of Hypotheses H2.1a and H3 is needed to develop a complete mediation model. The complete mediation model establishes hypotheses H2.4, which proposed that the relationship between firm size and SPP is mediated by the SGR. This result is consistent with Fama and French (Citation1992) who stated that small firms may suffer a long earnings depression that bypasses big firms, thereby suggesting that size is associated with a common risk factor that leads to the negative relationship between size and stock return.

As for the case of leverage in Industrial products (refer ), the mediation effect result in Industrial products shows that leverage is considered as an “indirect-only mediator”. The estimation on the relationship between the direct effects (c) for leverage shows an insignificant relationship (a = 0.0014, z = 0.20, p > 0.10), but path a shows a negative significant relationship (a = −0.0497, z = −2.15, p < 0.01), path b shows a positive significant relationship (a = 1.0578, z = 3.33, p < 0.01), and path c shows a significant relationship (a = −0.0525, z = −2.09, p < 0.01). Thus, this study provides important information in that higher or lower leverage does not directly influence the SPP, but that leverage may influence the SGR, and that an increase or decrease in the SGR might influence higher or lower SPP. Based on the trade-off theory, growth causes firms to shift their financing from new equity to debt in order to reduce agency issues. This is also dependent on whether the managers borrow long-term or short-term debt, or equity in addition to improving the companies’ growth. In conjunction, firms with high stock prices and high stock returns tend to use equity financing rather than debt financing, which is consistent with the market timing theory. However, the results of the positive influence between capital structure and stock return show that the more the firms use debt, the higher the stock returns they provide, which results from the leverage effect and leverage risk compensation (Yang et al., Citation2010).

Construction is considered for “Direct-only non-mediation” (refer ), the direct effects (c) for profitability show a positive significant relationship (a = 0.6955, z = 2.10, p < 0.05), and path a shows a positive significant relationship (a = 0.4756, z = 2.73, p < 0.01), but path b shows an insignificant relationship (a = 0.1145, z = 0.39, p > 0.10), and path c shows an insignificant relationship (a = 0.0545, z = 0.38, p > 0.10). Thus, profitability for Construction only has a direct significant influence on the SPP and SGR. This result is in line with Yang et al. (Citation2010) who reported that firms with higher profitability earned higher returns, and, thus, a positive relation between profitability and returns is expected.

Taken together, this finding shows that SGR plays an important role as the mediator variable for Malaysian Public-listed Shariah-compliant firms. Only three factors are strongly mediated by the SGR in each industry, and each type of mediation, i.e. profitability (Consumer Products, Industrial Products, and Properties resulted the indirect-only mediator while Construction is Direct-only non-mediation); leverage (Industrial products is indirect-only mediator); and, firm size (Properties is Competitive mediation). shows the framework for the mediation results for the relationship between the firm specific factors, SGR, and SPP.

Figure 4. Mediation analysis on the relationship between the firm specific factors, SGR, and SPP for each industry.

Practical Implications

The results presented could be useful to management and shareholders who are concerned with the financial and operating activities in the firms. The analysis can assist firms in terms of which area priority (firm specific factors) should be improve and lead to have higher SGR performance. In addition, higher SGR can improve SPP, thus, management should focus on SGR performance in order to have higher SPP. Lower capital structure, lower dividend policy, higher profitability and larger firms will increase SGR and lead to increase in SPP. The research uses SEM STATA techniques to estimate the analysis, and the findings confirm that the SGR is one of the important factors that influences SPP and also plays a role as a mediator variable for Malaysian Public-listed Shariah-compliant firms. Therefore, it is expected that research on the methodology debate will continue. The findings of this study can be used as a reference for future studies on other aspects of the SGR and can help guide sectors on ways to more successfully manage the financial and operating activities of firms.

6. Conclusions and recommendations

The objective of this study was to determine the influence of firm specific factors on SPP for 181 Shariah-compliant companies in Malaysia for 2007 to 2016. This study also investigated the significance of the SGR as a mediator of the relationship between firm specific factors and SPP. The existing literature provides inadequate information on the relationship between firm specific factors and SPP, as it implicitly assumes that this relationship is direct. An alternative perspective that has received less attention in the literature posits that this relationship can be mediated by the SGR. Moreover, no specific studies have explored the SGR as a mediator of the relationship between firm specific factors and SPP. Therefore, the present study determines the mediating effect of the SGR on the relationship between firm specific factors and SPP.

Based on our results, a mediation model hypothesizes that the independent variable (firm specific factors) influences the mediator (SGR), which in turn influences the endogenous variable (SPP). The mediation effect results appear to show that capital structure, dividend policy, profitability and firm size are “indirect-only mediators”. An indirect-only mediator variable denotes that an indirect effect (a × b) is significant, while a direct effect (c) is not significant. Only three factors are strongly mediated by the SGR in each industry, and each type of mediation, i.e. profitability (Consumer Products, Industrial Products, and Properties resulted the indirect-only mediator while Construction is Direct-only non-mediation); leverage (Industrial products is indirect-only mediator); and, firm size (Properties is Competitive mediation).

There are particular limitations that could potentially be addressed in future research such as the research only focus on Shariah-compliant firms, therefore, future research should focus overall firms and analyze the differences between Shariah-compliant and non-Shariah-compliant firms. The research investigate six sectors of Shariah-compliant firms as the sample of study which individual firm or one sector performance is less explored, therefore, future studies could focus only small group with longer period. As regards to literature review on sustainable growth rate, many countries started to focus on the sustainable growth rate performance analysis. Future research should aim to extend this research among ASEAN countries. In addition, this study focuses only capital structure, dividend policy, profitability, and company’s efficiency, therefore, future studies can investigate the internal and external factors (for example, macroeconomic factors) and also, focus on positive earnings or positive profitability of Shariah-compliant firms that affect the SGR and SPP.

The results demonstrate that certain factors influence the SGR, including the planning and managing of a firm’s financial and operational activities. The SGR is important in helping firms manage, guide, control and plan their operating and financial strategies. The SGR can also improve financial performance and help managers make financing decisions.

Acknowledgements

The authors would like to acknowledge The Research and Innovation Management Centre (RIMC) USIM, Nilai and Ministry of Higher Education Malaysia (MOHE) for the financial support of this research. This research is supported MOHE under the Fundamental Research Grant Scheme (FRGS) with reference code: FRGS/1/2018/SS01/USIM/01/2.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Nur Ainna Ramli

Dr. Nur Ainna Ramli, PhD, is a senior lecturer in the Faculty of Economics and Muamalat, USIM. She was awarded a PhD in Finance from Lincoln University, New Zealand. Her research interests are corporate performance, financial management.

Norfhadzilahwati Rahim

Dr. Norfhadzilahwati Rahim is a former lecturer at the College of Business Management and Accounting, Universiti Tenaga Nasional (UNITEN). She holds a Ph.D in Economics and Muamalat Administration from Universiti Sains Islam Malaysia (USIM). Her major research interest is in the areas of financial management, corporate finance and Islamic finance.

Fauzias Mat Nor

Prof. Dr. Fauzias Mat Nor is a professor of finance in the Faculty of Economics and Muamalat, USIM. She received her Ph.D. (Finance) from University College Dublin in 1991. Her research interest is on Corporate Finance and Banking.

Ainulashikin Marzuki

Dr. Ainulashikin Marzuki is an associate professor in the Faculty of Economics and Muamalat, USIM. She obtained her doctorate from the Griffith University. Her current research interest is in the fields of Islamic finance, fund management, corporate finance and disclosure.

References

- Ahmad, H., Fida, B. A., & Zakaria, M. (2013). The co-determinants of capital structure and stock returns: Evidence From The Karachi Stock Exchange, 1(Summer), 81–30. http://lahoreschoolofeconomics.edu.pk/EconomicsJournal/Journals/Volume%2018/Issue%201/04%20Ahmad,%20Fida,%20and%20Zakaria.pdf

- Ali, M. M., Ibrahim, M. K., Mohammad, R., Zain, M. M., & Alwi, M. R. (2009). Malaysia: Value relevance of accounting numbers. In Idowu, S.O., Filho, W.L. (eds) Global practices of corporate social responsibility. Berlin (pp. 201–231). Springer Berlin Heidelberg.

- Ali, A., Sharif, I., & Jan, F. (2017). Effect of dividend policy on stock prices. Journal of Management Info, 4(1), 19–28. https://doi.org/10.31580/jmi.v6i1.47

- Amouzesh, N., Zahra, M., & Zahra, M. (2011). Sustainable growth rate and firm performance: Evidence from Iran stock exchange. International Journal of Business and Social Science, 23(2), 249–255. https://api.semanticscholar.org/CorpusID:167421117

- Arellano, F., & Higgins, D. (2007). The sustainable growth rate and the short-run. Financial Decisions, 19(3), 1-9. http://www.financialdecisionsonline.org/current/ArellanoHiggins.pdf

- Arora, L., Kumar, S., & Verma, P. (2018a). The anatomy of sustainable growth rate of Indian manufacturing firms. Global Business Review, 19(4), 1050–1071. https://doi.org/10.1177/0972150918773002

- Baron, R. M., & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Beccalli, E., Casu, B., & Girardone, C. (2006). Efficiency and stock performance in European banking. Journal of Business Finance and Accounting, 33(1–2), 245–262. https://doi.org/10.1111/j.1468-5957.2006.01362.x

- Buzzell, R. D., Gale, B. T., & Sultan, R. G. M. (1975). Market share — A key to profitability. Harvard Business Review, 53(1), 97–106. https://hbr.org/1975/01/market-share-a-key-to-profitability

- Cahyo Hartono, G., & Rahmi Utami, S. (2016). The comparison of sustainable growth rate, firm’s performance and value among the firms in sri kehati index and Idx30 index in Indonesia stock exchange. International Journal of Advanced Research in Management Growth Rate, 284284(5). 68–81. https://garph.co.uk/IJARMSS/May2016/7.pdf

- Chandra, T., Junaedi, A. T., Wijaya, E., Suharti, S., Mimelientesa, I., Chandra, T., & Ng, M. (2019). The e ff ect of capital structure on profitability and stock returns: Empirical analysis of firms listed in Kompas 100. Journal of Chinese Economic and Foreign Trade Studies, 12(2), 74-89.

- Chen, H.-Y., Gupta, M. C., Lee, A. C., & Lee, C.-F. (2013). Sustainable growth rate, optimal growth rate, and optimal payout ratio: A joint optimization approach. Journal of Banking and Finance, 37(4), 1205–1222. https://doi.org/10.1016/j.jbankfin.2012.11.019

- Dickey, D. A., & Fuller, W. A. (1979). Distribution of the estimators for auto regression time series with a unit root. Journal of the American Statistical Association, 74(366), 427–432. https://doi.org/10.2307/2286348

- Dzikevičius, A., & Šaranda, S. (2011). Can financial ratios help to forecast stock prices? Journal of Security and Sustainability Issues, 1(2), 147–157. https://doi.org/10.9770/jssi.2011.1.2(7)

- Escalante, C. L., Turvey, C. G., & Barry, P. J. (2009). Farm business decisions and the sustainable growth challenge paradigm. Agricultural Finance Review, 69(2), 228–247. https://doi.org/10.1108/00021460910978706

- Fama, E., & French, K. (1995). Size and book to market factors in earnings and returns. The Journal of Finance, 50(1), 131–155. https://doi.org/10.1111/j.1540-6261.1995.tb05169.x

- Fauzias, M. N., Shaharuddin, A., Marzuki, A., & Ramli, N. A. (2019). Revised malaysian shariah screenning: its impact on islamic capital market. Research in World Economy, 10(1), 17–30. https://doi.org/10.5430/rwe.v10n1p17

- Fonseka, M. M., Ramos, C. G., & Tian, G. L. (2012). The most appropriate sustainable growth rate model for managers and researchers. Journal of Applied Business Research, 28(3), 481–500. https://doi.org/10.19030/jabr.v28i3.6963

- Gu, V., Cao, R., & Wang, J. (2019). Foreign ownership and performance: Mediating and moderating effects. Review of International Business and Strategy, 29(2), 86–102. https://doi.org/10.1108/RIBS-08-2018-0068

- Guilford, C. B. (1970). The concept of sustainable growth. Financial Analysts Journal, 11(2), 108–114. https://doi.org/10.2469/faj.v26.n3.108

- Hafid, I. (2016). The effect of margin profit and total assets towards sustainable growth rate of the distributor and trade company. International Business Management, 10(4), 423–428. https://medwelljournals.com/abstract/?doi=ibm.2016.423.428

- Harkleroad, D. (1993). Sustainable growth rate analysis: Evaluating worldwide competitors’ ability to grow profitably. Competitive Intelligence Review, 4(2–3), 36–45. https://doi.org/10.1002/cir.3880040209

- Hashemijoo, M., Ardekani, M. M., & Younesi, N. (2012). The impact of dividend policy on share price volatility in the Malaysian stock market. Journal of Business Studies Quarterly, 4(1), 111–129. http://citeseerx.ist.psu.edu/viewdoc/download?doi=10 .1.1.652.4019&rep=rep1&type=pdf

- Higgins, R. (1977). How much growth can a firm afford? Financial Management, 6(3), 7–16. https://doi.org/10.2307/3665251

- Huang, L., Ying, Q., Yang, S., & Hassan, H. (2019). Trade credit financing and sustainable growth of firms: Empirical evidence from China. Sustainability, 11(4), 1032. https://doi.org/10.3390/su11041032

- Hussain, S. T., Abbas, J., Lei, S., Jamal Haider, M., Akram, T., & Nisar, T. (2017). Transactional leadership and organizational creativity: Examining the mediating role of knowledge sharing behavior. Cogent Business & Management, 4(1), 1361663. https://doi.org/10.1080/23311975.2017.1361663

- Hussainey, K., Mgbame, C. O., & Chijoke-Mgbame, A. M. (2011). Dividend policy and share price volatility: UK evidence. Journal of Risk Finance, 12(1), 57–68. https://doi.org/10.1108/15265941111100076

- Iacobucci, D., & Duhachek, A. (2003), Mediating analysis. Paper Presented at the Round table of the ACR Conference, Toronto.

- Johnson, R., & Soenen, L. (2003). Indicators of successful companies. European Management Journal, 21(3), 364–369. https://doi.org/10.1016/S0263-2373(03)00050-1

- Kanani, M. A., Moradi, J., & Valipour, H. (2013). Sustainable growth and firm risk from the signaling perspective. Asian Economic and Financial Review, 3(5), 660–667. https://archive.aessweb.com/index.php/5002/article/view/1039

- Khan, K. I. (2012). Effect of dividends on stock prices–A case of chemical and pharmaceutical industry of Pakistan. Management, 2(5), 141–148. https://doi.org/10.5923/j.mm.20120205.02

- Lee, C.-F., Gupta, M. C., Chen, H.-Y., & Lee, A. C. (2015). Optimal payout ratio under uncertainty and the flexibility hypothesis: theory and empirical evidence. In Handbook of financial econometrics and statistics (pp. 2135–2176). Springer New York. https://doi.org/10.1007/978-1-4614-7750-1_79

- Lim, H., & Rokhim, R. (2021). Factors affecting profitability of pharmaceutical company: An Indonesian evidence. Journal of Economic Studies, 48(5), 981–995. https://doi.org/10.1108/JES-01–2020-0021

- Lockwood, L., & Prombutr, W. (2010). Sustainable growth and stock returns. Journal of Financial Research, 33(4), 519–538. https://doi.org/10.1111/j.1475-6803.2010.01281.x

- Lyroudi, K. (2018). Do financial ratios affect stock returns in the athens stock exchange ?. Economic Alternatives, 1(4), 497–516. https://www.unwe.bg/uploads/Alternatives/4_EA_4_2018_en.pdf

- Mamilla, R. (2019). A study on sustainable growth rate for firm survival. Strategic Change, 28(4), 273–277. https://doi.org/10.1002/jsc.2269

- Molly, V., Laveren, E., & Jorissen, A. (2012). Intergenerational differences in family firms: impact on capital structure and growth behavior. Entrepreneurship: Theory and Practice, 36(4), 703–725. https://doi.org/10.1111/j.1540-6520.2010.00429.x

- Park, K., & Jang, S. C. (2010). Firm growth patterns: Examining the associations with firm size and internationalization. International Journal of Hospitality Management, 29(3), 368–377. https://doi.org/10.1016/j.ijhm.2009.10.026

- Pham, D. C., Do, T. N. A., Doan, T. N., Nguyen, T. X. H., Pham, T. K. Y., & Tan, A. W. K. (2021). The impact of sustainability practices on financial performance: Empirical evidence from Sweden. Cogent Business & Management, 8(1), 1912526. https://doi.org/10.1080/23311975.2021.1912526

- Philips, P. C. B., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrica, 75(2), 335–346. https://doi.org/10.1093/biomet/75.2.335

- Platt, H. D., Platt, M. B., & Chen, G. (1995). Sustainable growth rate of firms in financial distress. Journal of Economics and Finance, 19(2), 147–151. https://doi.org/10.1007/BF02920515

- Rădăşanu, A. C. (2015). Cash-flow sustainable growth rate models. Journal of Public Administration. Finance and Law, 7, 62-70. https://www.jopafl.com/uploads/issue7/CASHFLOW_SUSTAINABLE_GROWTH_RATE_MODELS.pdf

- Ramli, N. A. (2014). Three essays on capital structure determinants [ Doctoral dissertation]. https://researcharchive.lincoln.ac.nz/handle/10182/6395.

- Ramli, N. A., & Nartea, G. V. (2016). Mediation effects of firm leverage in Malaysia:Partial least squares – Structural equation modeling. International Journal of Economics and Financial Issues, 6(1), 301–307. https://www.econjournals.com/index.php/ijefi/article/view/1490https://www.jopafl.com/uploads/issue7/CASHFLOW_SUSTAINABLE_GROWTH_RATE_MODELS.pdf

- Ramli, N. A., Latan, H., & Solovida, G. T. (2018). Determinants of capital structure and firm financial performance – A PLS-SEM approach: Evidence from Malaysia and Indonesia. Quarterly Review of Economics and Finance, 71, 148–160. https://doi.org/10.1016/j.qref.2018.07.001

- Ramli, N. A., Latan, H., & Nartea, G. V. (2018). Why should PLS-SEM be used ratherthan regression? Evidence from the capital structure perspective. In N.Avkiran & C. Ringle (Eds.), Partial least squares structural equation modeling (pp. 171–209). Springer International.

- Sharif, T., Purohit, H., & Pillai, R. (2015). Analysis of factors affecting share prices: The case of bahrain stock exchange. International Journal of Economics and Finance, 7(3), 207–216. https://doi.org/10.5539/ijef.v7n3p207

- Srinivasa, B. G. (2011). A Study on measuring the performance of indian banking sector in the event of recent global economic crisis- an empirical view. International Journal of Research in Commerce, Economics and Management, 1(10), 10-41.

- Sutjiati, R. (2017). Role of sustainable growth rate to increase company’s value. In: 14th International Annual Symposium on Management, Universitas Kristen Maranatha, March 3rd-4th, 2017, Riau.

- Vasiliou, D., & Karkazis, J. (2002). The sustainable growth model in banking: An application to the national bank of Greece. Managerial Finance, 28(5), 20–26. https://doi.org/10.1108/03074350210767843

- Vasiu, D. E., & Ilie, L. (2018). Sustainable growth rate: An analysis regarding the most traded companies on the bucharest stock exchange. In: S. Mărginean, C. Ogrean, & R. Orăștean (Eds.), Emerging issues in the global economy. Springer proceedings in business and economics. (pp. 1689–1699). Springer: Cham.

- Wang, L., Dai, Y., & Ding, Y. (2019). Internal control and SMEs’ sustainable growth: The moderating role of multiple large shareholders. Journal of Risk and Financial Management, 12(4), 182. https://doi.org/10.3390/jrfm12040182

- Welch, I. (2004). Capital structure and stock returns. Journal of Political Economy, 112(1), 106–132. https://doi.org/10.1086/379933

- Xu, J., & Wang, B. (2018). Intellectual capital, financial performance and companies’ sustainable growth: Evidence from the Korean manufacturing industry. Sustainability, 10(12), 4651. https://doi.org/10.3390/su10124651

- Yang, C., Lee, C., Gu, Y., & Lee, Y. (2010). Co-determination of capital structure and stock returns — A LISREL approach an empirical test of Taiwan stock markets. Quarterly Review of Economics and Finance, 50(2), 222–233. https://doi.org/10.1016/j.qref.2009.12.001

- Zhao, X., Lynch, J. G., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and Truths about mediation analysis. Journal of Consumer Research, 37(2), 197–206. https://doi.org/10.1086/651257