Abstract

Recent sustainability reporting (SR) has been of particular interest to stakeholders in developed countries but has begun to be studied in developing countries. The purpose of this study is to examine the relationship between SR and firm value (FV) of non-financial firms listed on the Vietnamese stock exchange. The authors used the combined method to measure the level of SR disclosure according to GRI standards of 360 enterprises in the period 2015–2019. The research results have revealed a positive relationship between SR and FV when measuring the SR by the aggregate indicator and components such as the general indicators, the economic dimension and the environmental and social dimensions. The research results suggest some recommendations to increase awareness and improve SR publication, which will help businesses add value.

PUBLIC INTEREST STATEMENT

Sustainability reporting (SR) refers to the disclosure, whether voluntary, solicited, or required, of non-financial performance information to outsiders of the organization. Sustainability reports help companies build consumer confidence and improve corporate reputations through social responsibility programs and transparent risk management. This communication aims at giving stakeholders broader access to relevant information outside the financial sphere that also influences the company’s performance. The research results suggest recommendations to increase awareness and improve SR publication, which will help businesses add value. The application of SR is very necessary for business organizations in the process of integrating with international markets because it brings benefits to both the organization and the society, especially increasing the competitiveness of the listed companies. Therefore, from now on, there should be actions and policies to facilitate listed companies to participate in SR activities.

1. Introduction

There are many views and models of economic development in the world throughout the history of human society. The first view is that resources are limited and therefore resources for economic development are limited and therefore economies cannot grow beyond their limits. In this view with the traditional economic model, economic development sooner or later leads to the collapse of the global ecological system and the solution of the problem is in no other way to limit decisively lists the consumption of all resources whether it is a renewable resource or a non-renewable resource. Only then will the next generation have access to the resources that cater to their needs. Another view is that resources are limited, but they are not limited in the absolute sense, but limited in the relative sense. When resources become scarce, humans will find alternative resources, on the one hand, and also take measures to effectively use available resources. This means that the level of environmental destruction will increase with the process of economic development, and when the economy develops to a certain extent, the level of destruction will decrease and the quality of the environment will be improved (Ishwaran et al., Citation2010). This means that in the early stages of development, people due to increased consumer demand have over-exploited the resources of physical production so the quality of the environment will decrease. As human material life increases, the need for quality of life also increases and now people have the material and technical conditions to offer solutions to both develop economy and reduce the level of environmental damage.

How to development the economy without harming the living environment? That is, the big question that the authors have for authors and the only possible solution is SR. At this stage, many businesses in developed countries tend to include social performance in their financial statements (Hahn & Kühnen, Citation2013). SR is an indispensable trend in the world today and is being promoted by big organizations such as the United Nations, the European Union, developed countries such as the United States, the United Kingdom and Germany. According to a Brundtland report presented at the World Environment Development Committee in 1987, SR is a development that meets the needs of the current businesses without affecting the development potential of future generations. This is considered one of the most commonly used and acknowledged concepts.

The firm’s SR includes the disclosure of information on the environment, energy, human resources, products and community issues (Hackston & Milne, Citation1996). Vietnam also has many businesses aware of the importance of information disclosure in SR. This information is for various reasons published in SR or published in annual reports and on the author’s bite of enterprises. Through SR, businesses can have many great opportunities in attracting investment capital from socially and environmentally responsible investors, strengthening the confidence of stakeholders in enterprises. According to the Ministry of Finance (2015) requires disclosure of information related to SR of listed companies to ensure “completeness, accuracy and timeliness”. SR is recognized as a means to minimize information asymmetry and thereby help investors to strengthen the supervision role for enterprises.

However, in underdeveloped or developing countries, the smaller businesses, the issues they are interested in are economic growth, the implementation of social responsibility or towards SR with them certain limitations. Therefore, should there be empirical studies, surveys and assessments between SR and how corporate values relate to Vietnam, a developing country? Research on SR and FV relationships in the world has been studied, attracting the attention of many leaders, managers and researchers in many countries around the world (McWilliams & Siegel, Citation2000; Nelling & Webb, Citation2009; Burhan & Rahmanti, Citation2012; Gnanaweera & Kunori, Citation2018). However, there is still much debate about the outcome of this relationship. In Vietnam, the issue of SR is still a very new issue, which is of little concern to enterprises. In 2015, the Ministry of Finance issued Circular 155, on the information disclosure on the stock market, the issue of SR has really been of interest to many researchers. However, the studies in Vietnam on this issue are just explanatory and clarifying studies on SR but not many empirical studies to examine the relationship between SR and FV. Previous studies (Hoang et al., Citation2018; H. T. V. H. T. v. Ha et al., Citation2019; Trang & Yekini, Citation2014; Phuong & Hung, Citation2020) only looking in one direction show that there is an impact of social responsibility (CSR) on performance; on the other hand, small research sample fund, short study duration, and previous research at a time when very few businesses made the announcement of SR.

Thus, on the basis of an overview of international and domestic studies, the authors found that the gap of previous studies as follows: (i) only focused on studying the effects of SR on FV; (ii) research on the relationship between SR and FV has heterogeneous results, there are studies that show a positive relationship but there are also studies that do not show relationship or negative relationship. (iii) What is new in this study is to consider the SR and FV relationships in a comprehensive way when considering SR according to both component indicators such as general indicators, economic indicators, environmental indicators and social indicators for enterprise value. Besides, we use the GLS regression method and follow the structural linear model (SEM) to consider the interaction between SR and FV.

2. Theoretical framework

Many researchers have studied the theoretical basis to explain the relationship between SR and FV in different contexts including stakeholder theory and legal theory.

2.1. Stakeholder theory

Stakeholder perspective (Freeman, Citation1984) proposes the idea that a company can exist only if it is able to meet the needs of stakeholders—who can significantly affect the company welfare. Because stakeholders can contribute to a firm’s ability to create the authors (Post et al., Citation2002), to maintain growth, companies should be concerned about the benefits of stakeholders (Van der Laan, Citation2009) and take into account their views and activities. This argument has two reasons. First, stakeholders provide resources such as capital, labor and revenue (Sweeney, Citation2009). If companies act irresponsibly to employees, customers and society, they risk losing these important resources. Second, stakeholders are both potential beneficiaries and high-risk recipients (Post et al., Citation2002). They often face risks associated with irresponsible social behaviors, such as poor quality products, excessive labor exploitation and the natural environment. According to the principle of fair distribution (Sweeney, Citation2009), corporate profits should be shared equally among the members at risk, including stakeholders. This theory is widely accepted among researchers and further developed in various ways. In other words, in addition to the goal of increasing profits for shareholders, companies should engage in social responsibility activities to meet non-financial stakeholders who can provide strong support for them. Jensen (Citation2002) introduced the concept of value maximization in line with stakeholder theory and firm value over the long term. In fact, value maximization shows that long-term market value is one of the company’s most important goals, while stakeholder theory advises managers to meet the interests and interests of all stakeholders. Jensen asserts that the company’s main goal is to maximize company value and prove that maximizing company value does not always conflict with a specific partner. This approach eliminates the practice of different corporate goals from the perspective of traditional stakeholders such as high salaries for employees, low prices for customers or charities for orphaned children. According to (Deegan et al., Citation2000), the stakeholder theory can be divided into two branches, ethical and management. The ethical branch is based on the premise “all stakeholders have the right to be treated fairly by an organization, and managers should manage the organization for the benefit of the stakeholders”; that is, all All stakeholders have the right to be provided with information about the activities of the company affecting them. Stakeholders need to know all the information, including information on hazardous waste, water pollution, social assistance, even information that is not directly relevant to them. The management branch is based on the argument that organizations will respond to society through stakeholder power to influence corporate governance. Based on this perspective, organizations will provide information that addresses the interests and expectations of specific groups or key stakeholders related to the organization. As a result, corporate information disclosure will be used as a strategy to maintain the support of key stakeholders (Islam & Deegan, Citation2010). In stakeholder theory, organizations aim to balance the expectations of all stakeholder groups through their activities. Organizations need to make sure their relationship with all stakeholders. Managers should consider and uphold the expectations of all stakeholder groups when making decisions about social responsibility. Stakeholder theory is used in this study to explain what motivates enterprises to practice SR publication.

2.2. Legal theory (jurisprudence)

Legal theory is widely used in social and accounting studies to explain why businesses need to disclose social and environmental information. Suchman (Citation1995) defined the legal theory of “the operation of an entity expected to be appropriate, or consistent with some social architectural systems in terms of standards, values, beliefs and concepts”. Legal theory is based on the idea that the rights and responsibilities of an organization must come from society. Business organizations must operate within the boundaries of society to meet society’s expectations, including providing better goods and services to society. Because organizations are part of a broad social system, organizations need to operate within the social system, without having any negative impact on society (Deegan, Citation2002). This can enable the organization to achieve stable goals and profits. Suchman (Citation1995) defined three forms of legitimacy: pragmatic (based on self-interest), ordinary (based on normative character), and awareness (based on inclusiveness and subsidy) it is used in terms of corruption and social support. These three forms are used to explain the relationship between social responsibility and legal theory (Guthrie & Parker, Citation1989), (O’donovan, Citation2002) argued, legal theory is based on the view that organizations are governed by society through a social contract. The agreement was made to obtain, based on a number of social requirements, in return for the organization’s own goals. Organizations need to behave and disclose enough information to society in order for society to assess it as a good citizen. Companies are recognized as a “good corporate citizen” when operating on social commitments. Because of the goal of “operating as a good corporate citizen,” many organizations may need to change their organizational processes. (Newson & Deegan, Citation2002) argued, legal theory is believed to be influenced by disclosure rather than by changes in business practices. As societal expectations change, organizations will be required to demonstrate change in their operational strategies accordingly. (O’donovan, Citation2002) argue, organizations try to change social expectations, perceptions and values through a number of approaches as part of the legal process. Lindblom () and Gray et al. (Citation1995) identified four strategies or approaches on how an organization achieves legality. First, an organization may need to educate and inform the public concerned about changes in its performance and actions. This method is used to determine the legal gap between the action and the actual failure of the organization. Second, to change society’s perceptions without changing the actual behavior of the organization. This method is used when the legal gap has increased between organization and society. Third, organizations may need to draw public attention away from current and other related issues. This method can deflect public expectations from an existing situation. Fourth, an organization may need to change public expectations when society has incorrect expectations about its performance. As such, legal theory can be used as motivation for companies to announce their social and environmental activities. However, this study does not focus on the legal process, but on the legal application to SR.

3. Overview and research hypotheses

Many studies considering SR and FV relationships have used SR as a dependent variable and the FV parameters are independent variables (McWilliams & Siegel, Citation2000; Nelling & Webb, Citation2009), while some other studies use SR as an independent variable and FV as a dependent variable (Aras et al., Citation2010; (Arayssi et al., Citation2016). The results of the studies mentioned above are mixed. Specifically, several studies found a positive correlation between the two variables (Waddock & Graves, Citation1997; Orlitzky et al., Citation2003). In summary, from the various results of the above studies and to better understand the nature of the SR and FV relationships, this study will examine the FR and FV relationships according to the following contents.

3.1. Research on the impact of sustainability reporting on the value of a business

There have been many studies in the past with conflicting results suggesting relationships with negative, positive or even negative correlations between social responsibility and performance, as study researches of (Aupperle et al., Citation1985; Waddock & Graves, Citation1997; Preston & O’bannon, Citation1997; Nelling & Webb, Citation2009). Thus, it can be divided into three research groups as follows:

- The first group: the research suggests that the relationship between social responsibility and performance is inversely opposite (Friedman, Citation2007). (Rhou et al., Citation2016) would like to emphasize the strategic operations of the business as the authors as the management need to rely on their resources to increase profits for shareholders and investors. In addition, studies emphasizing the use and seeking of optimal distribution of scarce resources will have a negative impact on performance. The importance of communication in social responsibility activities should be considered and focused on stakeholders.

- The second group: Based on the stakeholder theory of Freeman (Citation1984), there is a positive relationship between SR and FV including studies of Cochran and Wood (Citation1984), Wood (Citation2010), McWilliams and Siegel (Citation2000), Aupperle et al. (Citation1985), Waddock and Graves (Citation1997), Preston and O’bannon (Citation1997) and H. T. v. Ha et al. (Citation2019). In the interests of shareholders, when the company decides to carry out social activities, it is necessary to pay attention to the objects and other stakeholders such as customers, employees, suppliers, and communities. Social responsibility activities will help the company increase its financial performance by increasing sales, increasing the company’s image, brand and reputation.

- The third group: does not have the same research opinion as the two groups above, the third group thinks that there is no specific relationship between social responsibility and performance such as (Teoh et al., Citation1999). In these studies, the reason for not finding a link between social responsibility and performance is because there are too many factors affecting performance (Burhan & Rahmanti, Citation2012).

3.2. Research on the impact of corporate value on sustainability reporting

According to profit motive theory, businesses investing in sustainable development activities will change the future financial results of businesses in a positive direction. For example, investing in sustainable development will increase the image of the business with the community, thereby increasing sales, market share, or attracting good employees to work at the firm, or reducing unwanted conflicts with stakeholders, or to avoid legal problems. Therefore, the value of the business will be related to the extent to which the business invests in sustainable development. Many studies have investigated the relationship between corporate value and the performance of sustainable development such as Holbrook (Citation2010) and Cho et al. (Citation2012) or the relationship between business value and sustainable activities (Galdeano-Gómez, Citation2008; He & Loftus, Citation2014; Arayssi et al., Citation2016; Van Linh et al., Citation2019), thinking that increasing enterprise value will increase the disclosure of environmental, social and governance information. However, the research results show that corporate value has a positive influence on the level of disclosure of information in sustainability report. Morhardt (Citation2010) conducted an overview study based on a review of 101 articles related to sustainable development and business performance during 1992–2011, showing that in the first phase of the research most of the research is focused on development, but since 2000, research has been started in developing countries, and additional research is needed on this topic.

3.3. Study on the coming sustainability reporting relationship and business value

Investigates a two-way relationship between sustainability reporting and business value, the authors suited. Specifically, several studies have found a positive correlation between the two variables (Waddock & Graves, Citation1997; Orlitzky et al., Citation2003), but some studies have found no relationship between the two variables (McWilliams & Siegel, Citation2000). There are also studies that find negative correlations between the two variables. Jones et al. (Citation2007), Crisóstomo et al. (Citation2011), and Trang and Yekini (Citation2014) investigated the relationship between social responsibility and financial performance of the 20 largest companies listed on both stock exchanges in Hanoi and Ho Chi Minh City (2010–2012). The results show the relationship between social responsibility and the financial performance of 20 Vietnamese listed companies. The study of (Long, Citation2015) examines the relationship between SCR and market orientation (MO) with firm performance. The results show that both CSR and MO operations have a positive impact on company performance. The study also shows that senior managers, CEOs, and company owners of Vietnamese companies should upgrade their awareness of the importance of social responsibility, so that they can improve their high competitiveness in market-driven economy. (Hoang et al., Citation2018) investigates the impact of diversity on the board on the social disclosure of listed companies in Vietnam. The CSR is collected from the annual report and is measured based on GRI 3.1 guidelines. The board diversity variable was measured through four questionnaires for four different stakeholders (workers, products, local communities and social justice). The results show that there are significant positive effects of board diversity (differences between directors in a board, for example, the demographic attributes of board members) on social responsibility, while board diversity (differences between boards, such as board structure) has no effect on SR.

Based on the theories, the review of the study with the arguments and the real results on the relationship between SR and FV, the authors formulated the following research hypotheses:

Hypothesis H1: There is a positive and statistically significant relationship between the SR difference and FV.

Hypothesis H2: There is a positive and statistically significant relationship between the FV difference and the SR.

A lot of controversy in several studies (Branco & Rodrigues, Citation2008; Nelling & Webb, Citation2009; Margaritis & Psillaki, Citation2010; Vu, Citation2012; Jennifer Ho & Taylor, Citation2007; Kakani et al., Citation2001; T. v. Ha et al., Citation2019; Platonova et al., Citation2018; Zhang, Citation2013; Hung et al., Citation2018; Nguyen et al., Citation2020; Tran et al., Citation2020) show that the relationship between SR and FV affected by a number of factors. In this study, the authors use a number of control variables that can be considered to have an effect on the relationship between SR and FV such as (1) firm size, (2) financial leverage, (3) audit quality.

4. Research methodology

4.1. Research models

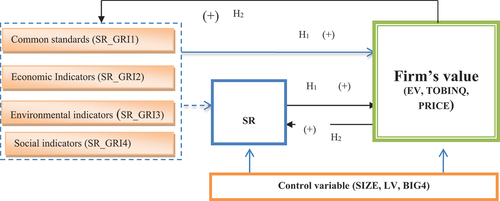

On the basis of a review of studies, research hypotheses the authors intend to export are as follows ().

Figure 1. Business value and sustainability reporting relationship model.

In this study, the authors measure SR according to GRI4 standards, including criteria for common standards (SR_GRI.1), economic indicators (SR_GRI.2), environmental indicators (SR_GRI. 3) and social indicators (SR_GRI.4). The authors measure CSR according to GRI4 because the indicators in the GRI Sustainability Reporting Standards help businesses to make reporting more convenient, transparent and efficient. GRI standards are clearly structured and easy to understand with (4) main contents: (1) GRI 101 General information (2) GRI 200 Economic problem (3) GRI 300 Social problem (4) GRI 400 Environmental problems. This structure makes it easy for businesses to see, understand and follow. The indicators are described in a specific and clear manner with a specific description and the language communicated more easily understood. The set of standards can be used flexibly, companies can use the direction of “full compliance” or “partial compliance” with the key contents of the Code. On the basis of interviews with experts’ opinions, in order to match the conditions of Vietnam, the authors use 86 criteria detailed in the section.

The dependent and independent variables in the research model are presented in .

Table 1. Variables in the research model

4.2. Research data

In this study, the author has collected from annual report data of 330 companies listed on the stock exchange of Vietnam in the 5 years from 2015 to 2019 which means there will be 1,650 observations. In the final step, the calculated variables are stored and processed, analyzed and verified through STATA 13.

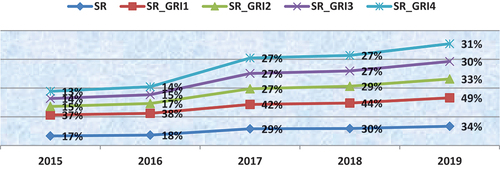

shows that the level of SR information disclosure has increased year by year; in 2015, it was 17% and increased to 34% in 2019, and the level of SR information disclosure increased steadily according to the aggregate indicator and component indicators in SR such as general indicator, economic indicator, environmental indicator and social indicator. However, the average level of publication and SR quality remains low.

Figure 2. Disclosure of sustainability reporting.

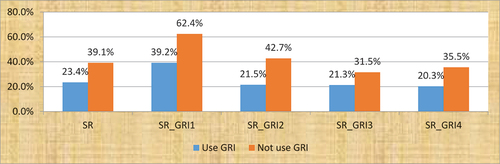

When measuring the publication of SRs, in Vietnam initially, 11% of enterprises have correctly used the GRI guidelines in the publication of SRs, the rest mainly rely on the guidance of Circular 155 of the Ministry of Finance. shows that firms using GRI guidelines are more likely to report SR than firms that do not use GRI in SR preparation.

Figure 3. Level of information disclosure between the two groups applying GRI.

5. Research results and discussion

The statistical data in shows that, among the surveyed enterprises, the firms whose average EV measured by EV is 27,596, the average Tobin’Q indicator is 1,179, the price of the stock, and the average vote is 25,817. EQ is measured in terms of mean profit management (EQ_EM) of −0.195, and the measure of stability of return (EQ_SM) is −0.031. The rate of SR disclosure for firms averaged 25.4%, with the lowest is 1% and the highest is 97%, and the standard deviation of 21%. The size of the business (SIZE) is measured by the total asset value after being logarithmic with the average value of 28,083, the average financial leverage ratio (Liabilities to Total Assets—LV), the enterprise is 49.9% and the financial statements made by Big4 auditing companies are 34.5%.

Table 2. Descriptive statistics

shows the results of the correlation coefficient between the variables, with the purpose of testing the close correlation between the independent variables and the dependent variable to eliminate the factors that may lead to multicollinearity before running regression model. Correlation coefficient between the independent variables in the model without pair has absolute value greater than 0.8. Therefore, when using the regression model, it is less likely to have the phenomenon of multi-collinearity.

Table 3. Correlation matrix

The research results in show that SR has an effect on FV with a statistically significant level of 1%, with all three models measuring FV by EV, Tobin’Q indicator and stock price (PRICE). Also, components in the SR, such as general indicators (SR_GRI1), economic criteria (SR_GRI2), environmental criteria (SR_GRI3), and social criteria (SR_GRI4), have a positive influence and are statistically significant to FV.

Table 4. Regression results affecting sustainability reporting and firm value

As described in section 3, several studies have found a relationship between SR and FV and many studies have shown that the relationship between SR and FV is significant, so hypothesis H1 is accepted. This study has provided evidence to confirm the results of many previous studies on the effects of SR and FV. These results are consistent with previous studies, such as Carroll (Citation1991), Deegan (Citation2002), Haniffa and Cooke (Citation2005), Waddock and Graves (Citation1997), and Nelling and Webb (Citation2009), and H. T. v. Ha et al. (Citation2019), and Hung et al. (Citation2020). These studies demonstrate that companies that spend on environmental protection activities or social activities or have information about environmental policy, social activity is more likely to lead to FV. However, through a product/customer accountability initiative, a company can expand its market to better respond to consumer needs, thereby enhancing its efficiency by minimizing fees and increasing profits.

On the contrary, in the second research model, the authors consider the effect of FV on SR. Research results in show that FV measured in different aspects has a positive influence on the overall SR and measured by each component indicator, with statistical significance of 1%. The results of this study are consistent with the study by Holbrook (Citation2010), Cho et al. (Citation2012), Galdeano-Gómez (Citation2008), He and Loftus (Citation2014), Arayssi et al. (Citation2016), Van Linh et al. (Citation2019), and Dang et al. (Citation2020) and consistent with the perspective of legal theory and stakeholder theory. When considering control variables, the results show that the factors of audit size and quality positively affect both SR and FV, whereas financial leverage variables negatively affect both SR and FV at 1% significance level.

Table 5. Regression results of the effect of firm value on sustainability reporting

The authors continue to classify the research sample into two industry groups, which are the studies of the manufacturing industry and the non-manufacturing industry to examine how the relationship between SR and FV is? Does industry factors influence this relationship? The research results in show that SR and FV have a positive and statistically significant relationship, in which the influence level in the relationship between SR and FV of non-manufacturing firms is higher than that of non-manufacturing firms.

Table 6. Regression of sustainability reporting effects on firm value by industry

Table 7. Regression of firm value effect on sustainability reporting by industry

For control variables, firm size (SIZE), financial leverage (LV), and audit quality (BIG4) can affect SR and FV at the same time. Therefore, the authors use linear structure model (SEM) to test the relationship between SR and FV. Regression results in and show that there exists a positive relationship between SR and FV and is statistically significant. For control variables, firm size and audit quality are positively related to SR and FV, while financial leverage is inversely related to SR and FV.

Table 8. Regression results of the effect of firm value on the linear structure sustainability report (SEM)

Table 9. Regression results of the impact of sustainability reports on firm’s linear structure (SEM)

Test results of the models’ indicators are given in . The model to measure the relationship between SR and FV satisfies the testing criteria of the estimation model, and the level of factor explanation is 79.7%, 21.5% and 23%. Thus, the hypothesis is accepted.

Table 10. Results of tests

6. Conclusions and recommendations

From the above results, the study assessed the impact of the SR and the components of the SR on the firm’s FV as measured by EV, Tobin’Q and PRICE. It is clear that there is a positive influence relationship between SR and FV of firms, which also contributes to reducing corporate risk in the Vietnamese context. Thus, in addition to traditional measures that management is often used to increase company’s value and efficiency, SR is a new trend attracting a lot of attention from organizations. Therefore, the application of social responsibility is very necessary for business organizations in the process of integrating with international markets because it brings benefits to both the organization and the society, especially increases the competitiveness of the listed companies. Therefore, from now on, there should be actions and policies to facilitate listed companies to participate in SR activities. Based on experimental results, this study proposes a number of recommendations to improve SR practice in Vietnam:

- Enterprises need to develop a long-term strategy to apply SR with appropriate steps in different phases. Companies need to have a long-term strategy in developing and implementing SR standards. Implementing CSR in the full and authentic sense is not a simple problem and is in the immediate resolution of the majority of companies because of perception constraints and resource factors, including financial, technical and highly qualified human resources.

- Sustainability reporting plays an important role for related parties and internal businesses. Through public reporting, transparency, accountability and its efforts in specific activities for sustainable development, the company strengthens the trust of stakeholders and increases credibility and brand name of the company.

In the context of Vietnam, the publication of the organization’s SR to stakeholders (domestic and foreign investors, authorities, local authorities, consumers …) is mainly voluntary and the freedom does not follow any general format (other than the GRI4 guidelines), only large firms produce SR reporting, and the number of firms preparing SR reporting is very small. The world’s most popular sustainability reporting framework developed by the GRI Initiative. The GRI Initiative’s Sustainability Report is considered to be the most useful because of its widespread use and recognition. The GRI framework addresses core sustainability issues including economic, social and environmental impacts with technical guidance on how to measure and report these issues.

- The Government should continue to supplement and improve the current legal system in Vietnam to create a solid legal basis for the implementation of SR. Because the legal system will be the framework for organizations to do business in general and to implement SR in particular. However, the current legal framework of Vietnam still has many shortcomings, enabling organizations to take advantage of legal loopholes to avoid ethical obligations and CSR.

- Strengthen communication to raise awareness about SR and adopt policies to encourage and support the implementation of SR in the organization’s business activities. Recognizing business ethics and SR is essential because the right perception can lead to the right action for every organization. The implementation of CSR will help organizations to develop sustainably, through activities such as compliance with the law on food safety and hygiene, environmental protection, pollution control, waste recycling and resource saving.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Dang Ngoc Hung

Nguyen Van Linh Master’s degree, PhD student is working at the Finance and accounting department, Hanoi University of Industry, Vietnam. His research interest includes accounting. He has published in the high ranked journals.

Dang Ngoc Hung is working and teaching at the Faculty of Accounting & Auditing, Hanoi University of Industry, Vietnam. His research interests include accounting and finance. He has published in the high ranked international journals.

Ta Quang Binh had his Master and PhD degrees in Accounting System from Kobe University, Japan. He is the Director of the Center for Research and Training in Professional Skills (CPS), Thuongmai University, Hanoi, Vietnam. His research interests include but are not limited to, financial statement analysis, management accounting and auditing.

References

- Aras, G., Aybars, A., & Kutlu, O. (2010). Managing corporate performance: Investigating the relationship between corporate social responsibility and financial performance in emerging markets. International Journal of Productivity and Performance Management, 59(3), 229–20. https://doi.org/10.1108/17410401011023573

- Arayssi, M., Dah, M., & Jizi, M. (2016). Women on boards, sustainability reporting and firm performance. Sustainability Accounting, Management and Policy Journal, 7(3), 376–401. https://doi.org/10.1108/SAMPJ-07-2015-0055

- Aupperle, K. E., Carroll, A. B., & Hatfield, J. D. (1985). An empirical examination of the relationship between corporate social responsibility and profitability. Academy of Management Journal, 28(2), 446–463. https://doi.org/10.5465/256210

- Branco, M. C., & Rodrigues, L. L. (2008). Factors influencing social responsibility disclosure by Portuguese companies. Journal of Business Ethics, 83(4), 685–701. https://doi.org/10.1007/s10551-007-9658-z

- Burhan, A. H. N., & Rahmanti, W. (2012). The impact of sustainability reporting on company performance. Journal of Economics, Business, and Accountancy Ventura, 15(2), 257–272. https://doi.org/10.14414/jebav.v15i2.79

- Carroll, A. B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4), 39–48. https://doi.org/10.1016/0007-6813(91)90005-G

- Cho, C. H., Freedman, M., & Patten, D. M. (2012). Corporate disclosure of environmental capital expenditures. Accounting, Auditing & Accountability Journal, 25(3), 486–507. https://doi.org/10.1108/09513571211209617

- Cochran, P. L., & Wood, R. A. (1984). Corporate social responsibility and financial performance. Academy of Management Journal, 27(1), 42–56. https://doi.org/10.5465/255956

- Crisóstomo, V. L., de Souza Freire, F., & de Vasconcellos, F. C. (2011). Corporate social responsibility, firm value and financial performance in Brazil. Social Responsibility Journal, 90(3), 22–25. https://doi.org/10.1108/17471111111141549

- Dang, H. N., Pham, C. D., Nguyen, T. X., & Nguyen, H. T. T. (2020). Effects of corporate governance and earning quality on listed Vietnamese firm value. The Journal of Asian Finance, Economics and Business (JAFEB), 7(4), 71–80. https://doi.org/10.13106/jafeb.2020.vol7.no4.71

- Deegan, C., Rankin, M., & Voght, P. (2000). Firms’ disclosure reactions to major social incidents: Australian evidence. Paper presented at the Accounting forum, 24(1), 101–130. 10.1111/1467-6303.00031

- Deegan, C. (2002). The legitimising effect of social and environmental disclosures—A theoretical foundation. Accounting, Auditing & Accountability Journal, 15(3), 282–311. https://doi.org/10.1108/09513570210435852

- Freeman, R. E. (1984). Strategic management: A stakeholder approach. Pitman.

- Friedman, M. (2007). The Social Responsibility of Business is to Increase Its Profits. In W. C. Zimmerli, M. Holzinger, K. Richter (Eds.), Corporate Ethics and Corporate Governance. Berlin, Heidelberg: Springer. https://doi.org/10.1007/978-3-540-70818-6_14

- Galdeano-Gómez, E. (2008). Does an endogenous relationship exist between environmental and economic performance? A resource-based view on the horticultural sector. Environmental and Resource Economics, 40(1), 73–89. https://doi.org/10.1007/s10640-007-9141-4

- Gnanaweera, K., & Kunori, N. (2018). Corporate sustainability reporting: Linkage of corporate disclosure information and performance indicators. Cogent Business & Management, 5(1), 1423872. https://doi.org/10.1080/23311975.2018.1423872

- Gray, R., Kouhy, R., & Lavers, S. (1995). Corporate social and environmental reporting. Accounting, Auditing & Accountability Journal, 8(2), 47–77. https://doi.org/10.1108/09513579510146996

- Guthrie, J., & Parker, L. D. (1989). Corporate social reporting: A rebuttal of legitimacy theory. Accounting and Business Research, 19(76), 343–352. https://doi.org/10.1080/00014788.1989.9728863

- Ha, H. T. V., Van, V. T. T., & Hung, D. N. (2019). Impact of social responsibility information disclosure on the financial performance of enterprises in Vietnam. Indian Journal of Finance, 13(1), 20–36. https://doi.org/10.17010/ijf/2019/v13i1/141017

- Ha, T. V., Dang, N. H., Tran, M. D., Van Vu, T. T., & Trung, Q. (2019). Determinants influencing financial performance of listed firms: Quantile regression approach. Asian Economic and Financial Review, 9(1), 78–90. https://doi.org/10.18488/journal.aefr.2019.91.78.90

- Hackston, D., & Milne, M. J. (1996). Some determinants of social and environmental disclosures in New Zealand companies. Accounting, Auditing & Accountability Journal, 9(1), 77–108. https://doi.org/10.1108/09513579610109987

- Hahn, R., & Kühnen, M. (2013). Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. Journal of Cleaner Production, 59(1), 5–21. https://doi.org/10.1016/j.jclepro.2013.07.005

- Haniffa, R. M., & Cooke, T. E. (2005). The impact of culture and governance on corporate social reporting. Journal of Accounting and Public Policy, 24(5), 391–430. https://doi.org/10.1016/j.jaccpubpol.2005.06.001

- He, C., & Loftus, J. (2014). Does environmental reporting reflect environmental performance?: Evidence from China. Pacific Accounting Review, 26(1–2), 134–154. https://doi.org/10.1108/PAR-07-2013-0073

- Hoang, T. C., Abeysekera, I., & Ma, S. (2018). Board diversity and corporate social disclosure: Evidence from Vietnam. Journal of Business Ethics, 151(3), 833–852. https://doi.org/10.1007/s10551-016-3260-1

- Holbrook, M. E. (2010). Corporate social responsibility and financial performance: An examination of economic benefits and costs as manifested in accounting earnings. University of Kentucky.

- Hung, D. N., Pham, C. D., & Ha, V. T. B. (2018). Effects of financial statements information on firms’ value: Evidence from Vietnamese listed firms. Investment Management and Financial Innovations, 15(4), 210–218. http://dx.doi.org/10.21511/imfi.15(4).2018.17

- Hung, D. N., Van, V. T. T., & Hung, N. D. (2020). The sensitivity of cash flows to cash holdings: Case studies at Vietnamese enterprises. Investment Management & Financial Innovations, 17(1), 266–276. https://doi.org/10.21511/imfi.17(1).2020.23

- Ishwaran, M., Paolo Ansaloni, G., & Rubin, A. (2010), Economic growth and the environment Tim Everett, defra evidence and analysis series, Paper 2. https://econpapers.repec.org/paper/pramprapa/23585.htm

- Islam, M. A., & Deegan, C. (2010). Media pressures and corporate disclosure of social responsibility performance information: A study of two global clothing and sports retail companies. Accounting and Business Research, 40(2), 131–148. https://doi.org/10.1080/00014788.2010.9663388

- Jennifer Ho, L. C., & Taylor, M. E. (2007). An empirical analysis of triple bottom‐line reporting and its determinants: Evidence from the United States and Japan. Journal of International Financial Management & Accounting, 18(2), 123–150. https://doi.org/10.1111/j.1467-646X.2007.01010.x

- Jensen, M. C. (2002). Value maximization, stakeholder theory, and the corporate objective function. Business Ethics Quarterly, 12(2), 235–256. https://doi.org/10.2307/3857812

- Jones, S., Frost, G., Loftus, J., & van der Laan, S. (2007). An empirical examination of the market returns and financial performance of entities engaged in sustainability reporting. Australian Accounting Review, 17(41), 78–87. https://doi.org/10.1111/j.1835-2561.2007.tb00456.x

- Kakani, R. K., Saha, B., & Reddy, V. (2001). Determinants of financial performance of Indian corporate sector in the post-liberalization era: An exploratory study National Stock Exchange of India Limited, NSE Research Initiative Paper No. 5. http://dx.doi.org/10.2139/ssrn.904983

- Long, H. C. (2015). The impact of market orientation and corporate social responsibility on firm performance: Evidence from Vietnam. Academy of Marketing Studies Journal, 19(1), 265. https://www.proquest.com/docview/1693219482/fulltextPDF/467975332EA5433EPQ/1?accountid=201058

- Margaritis, D., & Psillaki, M. (2010). Capital structure, equity ownership and firm performance. Journal of Banking and Finance, 34(3), 621–632. https://doi.org/10.1016/j.jbankfin.2009.08.023

- McWilliams, A., & Siegel, D. (2000). Corporate social responsibility and financial performance: Correlation or misspecification? Strategic Management Journal, 21(5), 603–609. https://doi.org/10.1002/(SICI)1097-0266(200005)21:5<603::AID-SMJ101>3.0.CO;2-3

- Morhardt, J. E. (2010). Corporate social responsibility and sustainability reporting on the internet. Business Strategy and the Environment, 19(7), 436–452. https://doi.org/10.1002/bse.657

- Nelling, E., & Webb, E. (2009). Corporate social responsibility and financial performance: The “virtuous circle” revisited. Review of Quantitative Finance and Accounting, 32(2), 197–209. https://doi.org/10.1007/s11156-008-0090-y

- Newson, M., & Deegan, C. (2002). Global expectations and their association with corporate social disclosure practices in Australia, Singapore, and South Korea. The International Journal of Accounting, 37(2), 183–213. https://doi.org/10.1016/S0020-7063(02)00151-6

- Nguyen, T. T., Nguyen, V. C., & Tran, T. N. (2020). Oil price shocks against stock return of oil-and gas-related firms in the economic depression: A new evidence from a copula approach. Cogent Economics & Finance, 8(1), 1–20. https://doi.org/10.1080/23322039.2020.1799908

- O’donovan, G. (2002). Environmental disclosures in the annual report. Accounting, Auditing & Accountability Journal, 15(3), 344–371. https://doi.org/10.1108/09513570210435870

- Orlitzky, M., Schmidt, F. L., & Rynes, S. L. (2003). Corporate social and financial performance: A meta-analysis. Organization Studies, 24(3), 403–441. https://doi.org/10.1177/0170840603024003910

- Phuong, N. T. T., & Hung, D. N. (2020). impact of corporate governance on corporate value: Research in vietnam. research in world economy, 11(1), 161–170. https://doi.org/10.5430/rwe.v11n1p161

- Platonova, E., Asutay, M., Dixon, R., & Mohammad, S. (2018). The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector. Journal of Business Ethics, 151(2), 451–471. https://doi.org/10.1007/s10551-016-3229-0

- Post, J. E., Preston, L. E., & Sachs, S. (2002). Managing the extended enterprise: The new stakeholder view. California Management Review, 45(1), 6–28. https://doi.org/10.2307/41166151

- Preston, L. E., & O’bannon, D. P. (1997). The corporate social-financial performance relationship: A typology and analysis. Business & Society, 36(4), 419–429. https://doi.org/10.1177/000765039703600406

- Rhou, Y., Singal, M., & Koh, Y. (2016). CSR and financial performance: The role of CSR awareness in the restaurant industry. International Journal of Hospitality Management, 57(1), 30–39. https://doi.org/10.1016/j.ijhm.2016.05.007

- Suchman, M. C. (1995). Managing legitimacy: Strategic and institutional approaches. Academy of Management Review, 20(3), 571–610. https://doi.org/10.2307/258788

- Sweeney, L. (2009). A study of current practice of corporate social responsibility (CSR) and an examination of the relationship between CSR and financial performance using structural equation modelling (SEM). ( Doctoral Thesis), Dublin Institute of Technology,

- Teoh, S. H., Welch, I., & Wazzan, C. P. (1999). The effect of socially activist investment policies on the financial markets: Evidence from the South African boycott. The Journal of Business, 72(1), 35–89. https://www.jstor.org/stable/10 .1086/209602

- Tran, T. N., Nguyen, T. T., Nguyen, V. C., & Vu, T. T. H. (2020). Energy Consumption, economic growth and trade balance in East Asia: A panel data approach. International Journal of Energy Economics and Policy, 10(4), 443–449. https://www.econjournals.com/index.php/ijeep/article/view/9401/5184

- Trang, H. N. T., & Yekini, L. S. (2014). Investigating the link between CSR and financial performance: evidence from Vietnamese listed companies. British Journal of Arts and Social Sciences, 17(1), 85–101. http://hdl.handle.net/10545/624269

- Van der Laan, S. (2009). The role of theory in explaining motivation for corporate social disclosures: Voluntary disclosures vs ‘solicited’ disclosures. Australasian Accounting, Business and Finance Journal, 3(4), 14–29. https://ro.uow.edu.au/aabfj/vol3/iss4/2/

- Van Linh, N., Hung, D. N., Dang, T. B., Van, V. T. T., & Anh, N. T. M. (2019). The effects of business efficiency to disclose information of sustainable development: The case of Vietnam. Asian Economic and Financial Review, 9(4), 547–558. https://doi.org/10.18488/journal.aefr.2019.94.547.558

- Vu, K. B. A. H. (2012). Determinants of voluntary disclosure for Vietnamese listed firms. ( Ph.D.), Curtin University,

- Waddock, S. A., & Graves, S. B. (1997). The corporate social performance-financial performance link. Strategic Management Journal, 18(4), 303–319. https://doi.org/10.1002/(SICI)1097-0266(199704)18:4<303::AID-SMJ869>3.0.CO;2-G

- Wood, D. J. (2010). Measuring corporate social performance: A review. International Journal of Management Reviews, 12(1), 50–84. https://doi.org/10.1111/j.1468-2370.2009.00274.x

- Zhang, J. (2013). Determinants of corporate environmental and social disclosure in Chinese listed mining, electricity supply and chemical companies annual reports. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/69195/pb13390-economic-growth-100305.pdf