Abstract

The study explored the influence of accounting graduates’ competencies on their job performance and how continuing professional development (CPD) mediates such relationships. The explanatory correlational design, through the census technique, was used to draw and analyse data from 115 accounting graduates working in the big four firms and finance directorates of four universities in Ghana. The results revealed that technical competence, professional skills and professional values ethics and attitudes significantly influenced graduates job performance. Also except for professional skills, continuing professional development significantly mediated the influences of the professional competencies on the job performance of accounting graduates. The study, therefore, implores universities to adequately develop all the three competencies in accounting students. Accounting graduates and their employers should also engage CPD to boost competencies for improved job performance.

PUBLIC INTEREST STATEMENT

Universities are deemed to be the powerhouse that produces a highly skilled workforce for every nation. However, there have been railing accusations against universities of their inability to develop graduates who possess the required competencies for some time now. In response, International Accounting Education Standard Board (IAESB) has developed International Education Standards (IES) to guide competency development in accounting education. This study, therefore, explores what the curricula the relationship between competencies and job performance while assessing the mediating role of continuing professional development (CPD) on this relationship. The outcome of this study has implications on the education of accounting professionals as well as the recruitment, training and development of same.

1. Introduction

Researchers and stakeholders have advocated that Intuitions of Higher Learning (IHL) should endeavour to holistically develop competencies of accounting graduates, especially through the thorough application of International Education Standards (IES; Georgiou, Citation2018), because of the critical role accountancy plays in an economy (Fung, Citation2017; Nechita, Citation2019; Spencer et al., Citation2012; Vannatta, Citation2014). Though IES is designed primarily to guide professional accountancy training and development, it guides higher learning institutions in shaping their accounting education. Institute of Chartered Accountants (Ghana), the accountancy regulatory body in Ghana, has entreated IHL in Ghana to adapt their accounting curricula to the International Accounting Education Standard Board (IAESB Citation2017) pronouncements. However, the autonomy granted IHL impedes the complete compliance to the IES (Busuioc et al., Citation2019). The partial adoption or noncompliance of IESs has the potential influence on competences of accounting graduates and consequently their job performance. For example, Baah-Boateng Citation2015) criticised IHL for their failure in equipping students with the right skills to make them employable.

In almost every profession, some entry competencies and continuous training are needed to enable individuals perform their jobs to acceptable standards. In accountancy, the (IAESB Citation2017) has prescribed the need for three main competencies to be emphasised in developing the structure and content of accounting curriculum. For the avoidance of doubt the IESs spell out the expected learning outcomes of the prescribed competencies. The first dimension prescribes the Initial Professional Development (IPD) which consists of technical competencies (IES 2), professional skills (IES 3), and professional values, ethics, and attitudes (IES 4). The second dimension also prescribes the continuing professional development (CPD) (IES 7), which is the required learning experience for accounting graduates to maintain and enhance their professional competencies after they have completed the IPD (IAESB, Citation2017). All these have been put in place to enable accounting graduates and newly trained accountants deliver on the job regardless of where they are working and where they were trained. In fact, the human capital theory and Campbell’s model of job performance have both stressed the instrumental role that education needs to play to successfully develop graduates who will be useful to their organisations and countries at large through a good job performance (Campbell et al., Citation1996; Campbell & Wiernik, Citation2015; G.S. Becker, Citation1993; Mincer, Citation1974; T. Schultz, Citation1961; Tan, Citation2014). Accounting education also resonates that education must render accounting graduates competent enough to perform their job (Al-Hattami, Citation2021; Fung, Citation2017; Spencer et al., Citation2012; Vannatta, Citation2014).

Studies have explored the relationship between competencies and job performance both within and outside the accounting context. Outside of the accounting context, Abas and Imam (Citation2016), Hanafi and Ibrahim (Citation2018), and Wade and Parent (Citation2002) have established a positive relationship between competencies and job performance. A meta-analysis of research papers by Palmer et al. (Citation2004) identified knowledge, skills, and abilities as relevant for auditors’/accountants’ job performance. The studies of Ahmad et al. (Citation2019), Hadisantoso et al. (Citation2017) and Afifah et al. (Citation2015) also identified a positive influence of competencies on auditor job performance. With most of these studies analysed with mean and standard deviation, the findings were not statistically rigorous to be applied widely. In addition, the specific need to assess the influence of the competencies prescribed in the IES justified the need to use a rigorous statistical approach to determine the relationship between the various competencies and the job performance of accounting graduates.

The role of continuing professional development in workers’ job performance has been usually expressed as a direct relationship. To begin with, Barzegar and Farjad (Citation2011) explored the effect of continuing professional development on staff performance in a descriptive survey. The study revealed that on-the-job training has a positive impact on the performance of the employees. The relevance of continuing professional development to the job performance of accounting practitioners was also supported by other empirical studies (Kavanagh & Drennan, Citation2008; Murphy & Hassall, Citation2020). From their study, the essence of CPD to the career success of an accountant was established as it was rated as one of the essential requirements to be successful in performing accountancy. Nassazi (Citation2013) found that CPD had a direct effect on employee performance. Other studies (Khan, Citation2018; Oliveira & Da-Costa, Citation2014; Oliveira & Holland, Citation2007) have questioned the relationship between competencies and job performance. A strand of literature contends that beyond the skills acquired by people, there are other factors that enhance people’s ability to perform on the job (Khan, Citation2018; Oliveira & Da-Costa, Citation2014; Oliveira & Holland, Citation2007). Their position draws attention to provision of relevant factors, including on-the-job training/CPD, clarity, commitment, cooperation, connections, and circumstances, that could influence such a nexus. However, this study is delimited to the scope of the IAESB framework and, therefore, focuses only on the mediating role of CPD. The search for literature revealed no evidence about the mediating role of CPD in improving job performance. Even though the literature suggests a positive association between CPD and job performance (Barzegar & Farjad, Citation2011; Murphy & Hassall, Citation2020; Widayati et al., Citation2021), the mediating role of CPD has rarely been explored. This is despite the argument made by (IAESB Citation2017) that CPD cannot solely determine job performance. One cannot rely on the unscientific position of the (IAESB Citation2017) who hold that CPD is a potent mediator in the use of competencies already acquired to improve job performance.

The study, therefore, sought to ascertain whether:

competencies acquired in school are relevant to job performance in actual employment.

CPD (i.e., value addition to graduates’ skillset whilst employed) mediates the competencies acquired in school to boost job performance.

The contribution of this study, is bi-focal. First, it provides evidence and understanding about the relevant skills that accounting graduates need to have in order to improve productivity on the job. Second, it helps in putting the arguments raised about the potency of CPD in mediating skills acquired to improve job performance in perspective by providing scientific and more authentic evidence. This will provide grounds for training officers to employ CPD to capacitate workers for improved work output. The rest of the paper presents, among other things, the remaining components of the introduction which are the concepts and theories undergirding the paper and the eventual generation of the conceptual framework. The other thematic issues articulated include the method employed to execute the study which details the research design, and data processing, analysis and diagnostics; the results obtained following the data analysis; discussion of the findings; and the conclusions reached based on the findings obtained.

1.1. International education standards

Technical competence (IES 2) is the first professional competence prescribed by the IAESB. This IES establishes the learning outcome in terms of how accounting graduates should apply accounting knowledge to a required level (Busuioc et al., Citation2019; Crawford et al., Citation2014; (IAESB, Citation2017). The learning outcome of technical competence has been grouped into eleven main subjects/courses. These courses include financial accounting and reporting, management accounting, financial management, taxation, audit and assurance, governance, risk management and internal control, business laws and regulations, information technology, business/organisational environment, economics, and business strategy/management. The eleven subjects stated may not necessarily be the exact descriptions used by the various universities and jurisdictions, but the content must be the same (IAESB, Citation2017).

Professional skills (IES 3) specify the professional skill as the second competence to be provided through accounting education. After going through accounting education, the graduate is expected to exhibit professional skills in four main ways. According to (IAESB Citation2017), graduates should possess and apply intellectual, interpersonal/communication, personal, and organisational skills. These skills enable accounting graduates to perform their role as account officers to an acceptable level (Busuioc et al., Citation2019; Crawford et al., Citation2014; (IAESB, Citation2017).

Professional values, ethics and attitudes (IES 4) explains the characteristics that help identify an individual as a member of the accounting profession. The characteristics include the principles of conduct (e.g., ethical principles) generally associated with and considered essential in determining the distinctive features of professional behaviour (IAESB, Citation2017). This attitudinal competency, just like the other competencies, would help the accounting graduate/accountant discharge his/ her job duties. The competency requires that accounting graduates be able to first identify ethical issues in situations and then apply the appropriate attitude, values, and ethics in such situations (Busuioc et al., Citation2019). According to IFAC. International Ethics Standards Board for Accountants (IESBA; Citation2015), professional values, ethics, and attitudes can be summarised into one’s commitment to five main principles: integrity, objectivity, confidentiality, professional competence/due care, and professional behaviour.

CPD (IES 7) aims to maintain the professional competence required to continue providing high-quality services (job performance) to clients, employers and other stakeholders and consequently strengthen public trust in the profession and graduates (IAESB, Citation2017). The responsibility to maintain one’s professional competency lies with the graduates/accountant, even though the seventh IES is addressed to the IFAC member body. The CPD, as the name suggests, is the continuation of the IPD and this means that there should first be an IPD. Therefore, CPD cannot stand on its own to influence one’s job performance (IAESB, Citation2017). The framework explains that CPD sharpens and refines all the three main competencies and other competencies developed during the university’s accounting education process.

1.2. Related theories

The Human Capital Theory traces its source back to the empirical works of; Becker, (Citation1993); T. W. Schultz (Citation1960), and Mincer (Citation1974). The basic assumption of the theory is that education provides competencies while the competencies ensure returns in the form of financial benefits and productivity. Becker (Citation1993) and Gillies (Citation2017) assert that the provision of senior high or tertiary education is the most important investment that could be made in a person since it develops the competencies that make the individual resourceful contributing to productivity or economic growth. Consequently, for decades now, governments, families, and individuals have invested in education to reap the crucial benefits education brings to individuals, organisations, and the nation (Becker, Citation1993). Education, in HCT, was described in two primary forms, that is, education derived from schooling and education derived from on-the-job training (Becker, Citation1993).

The HCT, in its original form, conceptualised returns from investment in education in the form of wages and other financial benefits derived from employment (Becker, Citation1975; Becker, Citation1993; Schultz, Citation1960). However, the concept of returns on investment in education was broadened to include social productivity to capture the benefits the society (nation or organisation) in the subsequent publications of Becker (Citation1993). The underpinning assumption of the direct and sole effect of formal education investment on the returns of education has been challenged by the likes of Oliveira and Da-Costa (Citation2014), Oliveira and Holland (Citation2007), and Khan (Citation2018). They argue that the antecedent of job performance cannot be limited to the competencies gained in school hence, on-the-job training and experience create a competency (structural capital), which is crucial to employees’ job performance. Borrowing from HCT, accounting education is responsible for the competencies that are developed in accounting graduates. The concepts of IPD and CPD as used in this study represent the concept of education derived from schooling and education derived from on-the-job training, respectively. Finally, in line with the HCT, this study thrives on the assumption that investment into quality accounting education or the use of quality curriculum is likely to develop quality competencies that would eventually ensure productivity and good job performance among accounting graduates.

The theory of job performance was propounded by Campbell (Citation1990) and associates (Campbell et al., Citation1996, Citation1993). The theory was first developed through a study (Project A) designed for the US navy to serve as selection criteria into the service (Campbell et al., Citation1993; McCloy et al., Citation1994). According to Campbell et al. (Citation1996); (Citation1993), performance is a behaviour or action exclusively relevant to the organisation’s goals. In their argument, performance is not the consequence of action; it is the action itself. Campbell et al. (Citation1993) further postulated three determinants of an individual’s job performance. These are; declarative knowledge (i.e., knowledge about facts and things, representing the concept of technical competence as used in the IES 2); procedural knowledge and skill (i.e., cognitive skill, interpersonal skill, representing the concept of professional skills as used in the IES 3); and motivation (i.e., combined choice effect of expending effort, choice of effort level to be expended, and choice to persist in the expenditure of that level of effort, also resonating the concept of professional values, ethics and attitudes as used in the IES 3; Campbell & Wiernik, Citation2015; Motowidlo & Kell, Citation2013). An empirical study by McCloy et al. (Citation1994) validated these antecedents through confirmatory factor analysis.

According to Campbell et al. (Citation1993), the individual differences in personality and interests are presumed to combine and interact with education, training, and experience to shape declarative knowledge, procedural knowledge and skill, and motivation. Thus, education and individual differences in cognitive ability and personality should only indirectly affect performance through knowledge, skill, and motivation. The point here is that knowledge, skills, and motivation should influence job performance when individual differences and interests remain constant or treated as control variables. This study applies the postulation of the theory of job performance, which states that the three competencies (knowledge, skill, and motivation) could determine the job performance of individuals when their interests are held constant. This study delimited the population to graduates employed in accountancy-related jobs after school to control for graduates’ interest. The rationale is that pursuing accountancy after completing school means the graduates seem to have a steadfast interest in accountancy. This makes “interest” a homogenous factor among the population used for the study. Therefore, it is safe to explore the relationship between accounting graduates’ competencies and their job performance without worrying about the confounding impact of graduates’ interest on the relationship.

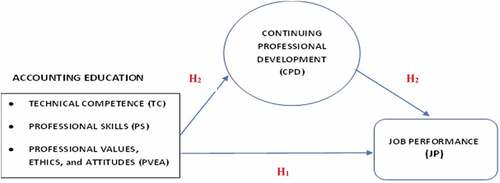

1.3. Conceptual framework

From the foregoing conceptual and theoretical literature (e.g., Busuioc et al., 2019; Crawford et al., Citation2014; IAESB, 2017; Campbell & Wiernik, Citation2015; Becker, Citation1993; Gillies, Citation2017) the conceptual framework (see, ) underpinning the study is formulated to guide the execution of the study. In , the conceptual framework depicts the general assumption and arguments of the study. It is understood from the framework that accounting education is the leading provider of the competencies required of accounting graduates. The universities would adequately develop the competencies of accounting graduates through their accounting curriculum that conforms to the requirement of IES. Another assumption is that higher competencies should lead to higher job performance. The competencies developed in the graduates in the form of technical competence, professional skills, and professional values, ethics, and attitudes would influence the graduates’ job performance. Finally, it is expected that the continuing professional development that accounting graduates achieve will mediate the relationship between their competencies and job performance. Therefore, the study hypothesised that:

H1: There is statistically significant influence of competencies on job performance.

H2: CPD (i.e., value addition to graduates’ skillset whilst employed) has a statistically significantly mediating role in the relationship between competencies and job performance.

Figure 1. Conceptual framework.

2. Method

2.1. Research design

The explanatory-correlational research design was employed to relate competencies and the job performance of 115 accounting graduates of universities in Ghana. The explanatory-correlational design was employed because it is economical and suitable for generalising the relationship between variables when cross-sectional data is rightly ascertained (Creswell & Creswell, Citation2017). These graduates were freshly employed or national service personnel in the audit or finance directorates of selected universities (UCC, UG, UPSA, and KNUST) and the big four accounting firms (KPMG, PWC, Ernst & Young, and Deloitte). Their respective supervisors were included to appraise the graduates job performance. The use of census of intangibles approach helped to avoid sampling bias as all 166 accounting graduates (2018, 2019 and 2020) in those firms and organisations were given opportunity to partake. The response rate was 69.3% of questionnaires distributed because three of the 118 responses were removed due to incomplete answers.

A questionnaire with multiple item scale was used to measure the latent constructs reflectively having relied on the pre-existing scales on job performance and IES pronouncements on IPD and CPD. Job performance (JP) was measured by adapting a scale developed by Williams and Anderson (Citation1991). To measure CPD, TC, PS, and PVEA, items were developed but solely guided by International Accounting Education Standard Board [IAESB] (Citation2017) pronouncements. TC, PS, and PVEA were measured on a 5-point Likert-type scale with; 1 = Lowly Developed, 2 = Moderately Developed, 3 = Highly Developed, 4 = Very Highly Developed, and 5 = Fully Developed. CPD and JP were also measured on a 5-point Likert-type scale with; 1 = Slightly Agree, 2 = Moderately Agree, 3 = Agree, 4 = Highly Agree, and 5 = Extremely Agree. To collect data, permission was sought from the institutions and respondents after ethical clearance was granted by the Institutional Review Board of the University of Cape Coast. Questionnaires were issued to respondents in person after the purpose of the study have been explained to them. The respondents were also assured of confidentiality and anonymity. Respondents were given up to two weeks to answer the questionnaires due to the fact that they were busy with work and would need ample time to provide candid answers to all the questions. Throughout the process, Covid 19 protocols prescribed by the World Health Organization (WHO), the Ghana Health Service (GHS), and the institutions involved in the study were strictly followed.

2.2. Data processing, analysis and diagnostics

The data were processed and managed with the use of SPSS (22) after being screened to remove incomplete responses. Frequency and percentage were used to check for data entry errors and produce results on the demographic characteristics of the respondents. PLS-SEM statistics was also employed to explore the hypothesised relationships. PLS-SEM is a rigorous nonparametric statistical approach that gives researchers the opportunity to explore the relationship and assess validity and reliability of unobservable latent variables concurrently (Abas & Imam, Citation2016). This is achieved through performance of a confirmatory factor analysis. However, the sample size criterion had to be satisfied before its use (Hair et al., Citation2011). The sample size must be equal to ten times the largest number of structural paths (5 in this study) directed at a latent construct. Therefore, the minimum sample required is 5 * 10 = 50. The variables used for the study were unobservable and latent in nature. Instrument validation diagnostics was also satisfied as presented subsequently. Hence, all these put together warranted the use of PLS-SEM.

2.3. Instrument validation and diagnostics

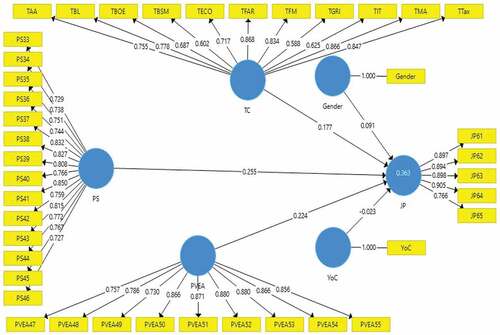

To perform partial least validate the instrument, indicator reliability, internal consistency reliability, convergent validity, and discriminant validity were assessed by observing results from PLS-SEM algorithm in . The outer loadings generally ranged between .588 and .906. This shows that all the indicators were reliable measures of their respective constructs, confirming the presence of indicator reliability (Wong, Citation2013). Cronbach’s alpha (CA), composite reliability (CR), and rho A values for all the latent constructs ranged above the minimum threshold of .7. This means that the models met the internal consistency reliability criteria (Hair, et. al., Citation2019). The least Average Variance Extracted (AVE) was .562, confirming the presence of convergent validity in all the measures used (Hair et al., Citation2011, p. 2019).

Table 1. Outer model specifications

To determine discriminant validity, the Heterotriat-Monotrait (HTMT) ratios together with their respective confidence intervals (CI) in were assessed. Recent studies (Hair et al., Citation2019; Henseler et al., Citation2015) have proven that HTMT ratios are more reliable than the Fornell-Larcker cross-loadings criterion. The results in suggested significant discriminant validity among the individual indicators of the various latent constructs because they were all lesser than .9 and had confidence interval ranging between 0 and 1.

Table 2. Heterotriat-monotrait (HTMT) ratios

Table 3. Objective three inner model specifications

2.4. Characteristics of respondents

The males (F = 80; 69.6%) dominated the distribution of the respondents while females (F = 35; 30.4%) were the minority of the two categories. Majority (F = 47; 40.9%) of the respondents were those who graduated in 2020. The second-highest representation (F = 39; 33.9%) were those who graduates in 2018. The cohort with least representation (F = 29; 25.2%) were those who graduated in 2019.

3. Results

This section presents the results obtained to address the objectives of the study. The results are presented in tables and figures to promote clarity and understanding.

3.1. Accounting graduates’ competencies and their job performance

The study explored the relationship between graduates’ competencies and their job performance. This helped to identify the competencies that are relevant to the job performance of graduates. Results from the inner model were discussed to assess the relationship. All VIFs were less than 5, indicating that the model was free of multicollinearity. The discussions excluded the control variables (gender and year of completion (Yoc)) as they had no significant impact on job performance and besides, they were not constructs of interest in the relationship. The results are subsequently shown in and .

Figure 2. Path model for competencies and job performance.

3.1.1. Path coefficient assessment

The results in and show that technical competence had a positive and significant influence on accounting graduates’ job performance (β = .177; t = 1.841; p = .033). This means that if accounting graduates’ technical competence is well developed, they are more likely to perform their jobs well as accountants. Additionally, as observed in , professional skills had a positive and significant influence on the job performance of accounting graduates (β = .255; t = 2.037; p = .021). This means that possessing higher professional skills will result in higher job performance among accounting graduates. Finally, the results as presented in suggest that professional values, ethics, and attitudes significantly and positively influences accounting graduates’ job performance (β = .224; t = 2.017; p = .022). This indicates that when accounting graduates possess higher professional values, ethics, and attitudes, they are more likely to perform their jobs well in accountancy or auditing. Consequently, all the hypothesis were supported.

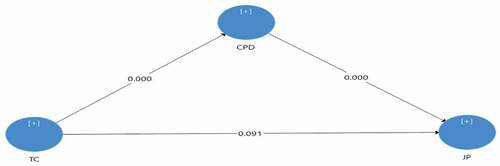

Figure 3. Mediating effect of CPD in TC-JP nexus.

3.1.2. Explanation of variance in endogenous variable

The variance in the endogenous construct was assessed by examining the coefficient of determination (R2). This also provided information on the predictive power of the model. The results in show that the exogenous constructs moderately and significantly explained the variance in the endogenous construct (R2 = .363). This means that about 36% of the variation in the job performance of accounting graduates (JP) was accounted for by the three professional competencies (TC, PS and PVEA). About 64% of the variations are probably explained by other factors not incorporated by this study.

3.1.3. Effect sizes of the exogenous constructs

Having identified the model’s predictive power, Cohen’s (Citation1988) f 2 criteria was used to determine the contribution of each exogenous variable to the predictive power. It was evident from that technical competence (.022), professional skills (.035), and professional values, ethics, and attitudes (.031) all had small effect sizes. This means that none of the exogenous constructs can singularly predict the job performance of accounting graduates. They would all have to be present concurrently to influence job performance effectively.

3.1.4. Predictive relevance (cross-validated redundancy)

Once the predictive power has been determined, it was equally pertinent to determine the predictive relevance of the model. Therefore, Stone-Geisser’s Q2 was used to assess predictive power, whereas q2 was used to assess the individual contribution of the exogenous constructs to the predictive relevance. As observed from , the model has predictive relevance since Stone-Geisser’s value (Q2 = .269) is higher than 0. Also, technical competence (q2 = .012), professional skills (q2 = .020), and professional values, ethics, and attitudes (q2 = .025) all had small effect sizes. The small effects on the predictive relevance confirms the concurrent need for all three professional competencies to significantly predict accounting graduates’ job performance.

3.2. Mediating role of CPD on the competencies and job performance nexus

Having identified the relationship between graduates’ competencies and their job performance, the study explored the mediating role of CPD on the relationship. The results from the structural equation model were used to evaluate the mediating roles of continuing professional development in each relationship. The results are presented in and and .

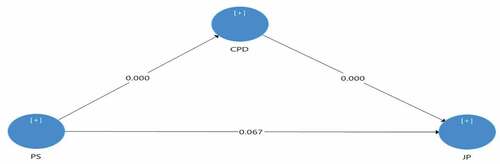

Figure 4. Mediating effect of CPD in the PS-JP nexus.

Figure 5. Mediating effect of CPD on PVEA-JP nexus.

Table 4. Mediation results

The results in shows that continuing professional development significantly and partially mediates the relationship between technical competence and job performance of accounting graduates (β = .091; t = 1.812; p = .035) since there is a direct relationship between technical competence and job performance. This partial mediating effect suggests that CPD strengthens the impact of technical competence on accounting graduates’ job performance.

The mediating effect of continuing professional development in the relationship between accounting graduates’ professional skills and their job performance was explored. Observations from and shows that the hypothesis was not supported because CPD does not significantly mediate the relationship (β = .067; t = 1.388; p = .083). However, there was a significant direct relationship between professional skills and job performance. This suggests that professional skills may not necessarily require CPD before they can be relevant for performing one’s job.

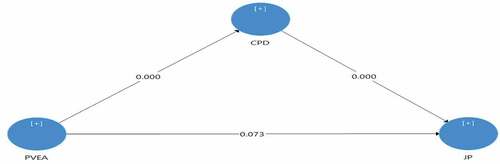

Finally, the mediating effect of continuing professional development in the relationship between professional values, ethics, and attitudes and job performance of accounting graduates was examined. The results from and show that CPD had a significant partial mediating effect in the relationship (β = .073; t = 2.042; p = .021). The hypothesis was supported. This suggests that if graduates are committed to developing their professional values, ethics, and attitudes through CPD, they are more likely to perform their job well.

4. Discussion

The general impression of the study is that the three competencies are relevant antecedents of the job performance of accounting graduates supporting the IAESB declaration. The findings obtained generally corroborate the arguments advanced by the theories and empirical findings that have been presented in the literature. Just as both human capital (G.S. Becker, Citation1993; Mincer, Citation1974; T. W. Schultz, Citation1960) and job performance (Campbell et al., Citation1996, Citation1993) theories postulated the influence of knowledge, skills, and attitude on the performance and productivity of workers; this study has also confirmed the relationship. Furthermore, the findings support empirical studies by Ahmad et al. (Citation2019), Hadisantoso et al. (Citation2017) and Palmer et al. (Citation2004) as they all revealed that competencies are significant predictors of job performance. Like the findings of this study, Ahmad et al., (Citation2019), observed that all the three competencies (skills, knowledge, and attitude) are relevant antecedents of auditors’ job performance. Even in a study outside the accounting context, the existence of the relationship between professional skills has been established by Wade and Parent (Citation2002). The findings of this study are also consistent with that of Abas and Imam (Citation2016). They found a significant and positive relationship between graduates’ employability skills and their job performance. The specific significant relationship between professional values, ethics, and attitudes also agrees with the finding of Afifah et al. (Citation2015). They realised a positive impact of ethical sensitivity on the job performance of auditors. They explain that the sensitivity directly informs their actions as auditors. These actions are their job performance. In the same vein, the professional values, ethics, and attitudes has the tendency to determine how graduates will perform their duties when they are employed. These findings affirm the need for universities to entirely focus on developing all the competencies of accounting graduates to make them efficient and effective when performing their duties as accountants, auditors, or tax officials. Not only would they need to have the technical know-how, but also, they would have to know the best way to relate and interact with colleagues while they predispose themselves to the best attitudes towards the job.

The mediating role of continuing professional development (CPD) has been established primarily in this study, as it was found to be significant in two of the three relationships. First, it significantly mediated the relationship between technical competence and job performance and the relationship between professional values, ethics, and attitudes and job performance. This validates the position of IAESB of CPD to be a mediating factor in the relationship between competencies and job performance of accounting practitioners. It also proves the need to engage in on-the-job training. The findings of Barzegar and Farjad (Citation2011) and Kavanagh and Drennan (Citation2008) suggested that CPD is a relevant contributor to workers’ job performance. Nassazi (Citation2013) also discovered a direct effect of CPD on the job performance of individuals. The finding of this study supports this position that exists in the existing literature. However, this finding gives new insight into how CPD can influence the job performance of accounting graduates. As argued by some critiques of the human capital theory (Khan, Citation2018; Oliveira & Da-Costa, Citation2014; Oliveira & Holland, Citation2007), CPD proved to be a factor that can influence the relationship between competencies and job performance of individuals. However, the mediating role of CPD in the relationship between professional skills is found to be insignificant. This may be accounted for by the fact that the study participants have had a maximum of three years, with the majority being below three years at the post. The experiences they may have gathered might not be significant enough to improve their existing competence in professional skills to mediate the relationship eventually. Although the mediating effect was not significant, the coefficient obtained suggested a positive mediating effect. Consequently, the importance associated with CPD by the (IAESB Citation2017) is vindicated by the findings of this study and therefore must be taken seriously.

5. Conclusions

The finding that all the competencies are significant determinants of accounting graduates’ job performance have both academic and practical implications. This finding was very conclusive, especially as it affirms the need for graduates to concurrently possess all the three competencies (technical competence, professional skills and professional values ethics and attitudes) to effectively perform their jobs. This implies that it would be impossible to bridge the gap between academia and the job market if some professional competencies are developed at the expense of the other competencies. IHL should consequently prioritize the development of competencies over merely teaching to the test. Accounting education should not in any way give students the impression that some competencies are more relevant than others. Therefore, academics should ensure that all the teaching and learning approaches that would be necessary to fully develop these competencies in accounting students should be adequately used by teachers and students. Specifically, relevant pedagogies that facilitate competency development such as cooperative learning and internships that focus on higher cognitive taxonomies should be employed by teachers and students. Therefore, academics need to empirically investigate the best pedagogical approaches to effectively develop the competencies of the accounting trainees.

Continuing professional development is proven to be relevant to the job performance of accounting graduates, therefore, the role it plays cannot be undermined in any way. The implication is that the overall development of an accounting graduate cannot be achieved and maintained only through higher education. Employers and graduates themselves have some crucial roles to play, judging by the fact that CPD is the responsibility of employees and employers. Therefore, the duty of accounting graduates being able to perform their job should not be solely ascribed to the IHL. Accounting graduates are advised to embrace lifelong learning through CPD. This will help keep their competencies relevant to the job market. They would be able to adapt to any form of change in administering their duties. Employers should also champion the course of CPD in their respective organisations to always keep their employees relevant. Employers should strategically organise periodic CPD programmes that are relevant to the respective roles of employees in the finance, account and audit departments of their organisations. This is critical to constantly capacitate them to execute their job roles up to the acceptable standard. Finally, schools, employers, and accounting students should periodically be up-to-date with any updates proposed by the IAESB to guide their IPD and CPD activities. To fully achieve the essence of CPD, practitioners would have to strategically, conduct regular evaluation of their CPD programmes to ensure it relevantly contributes to job performance. Even though the CPD has proven to be a potent mediator between competence and job performance, the response of specific population subgroups to the mediating role of the CPD in such nexus would be relevant to know whether the potency of the CPD in the relationship will differ amongst such population groups. For instance, there is a logical but yet to be established empirical relationship between length of study, familiarity with the job, history of similar job performance, length of service and job performance. However, it may be necessary to determine whether CPD may be indifferent to the competency of employees with varying length of their experience on their job performance. There is also the need to empirically explore effects of other mediating variables such as clarity, commitment, cooperation, connections, and circumstances.

6. Limitations

The study may suffer some limitations in terms of scope and research methodology. Given that there are other mediating factors (clarity, commitment, cooperation, connections; circumstances) that could influence the competencies and performance nexus, focusing on only CPD did not afford the opportunity to make comparisons among the other factors. Also, as with all quantitative studies conducted through questionnaire administration, this study may suffer the problem of different interpretations of questions by respondents and the lack of opportunity for the researcher to follow up ideas and clarify issues. Therefore, it is recommended that future studies should consider these other mediators to determine their contribution to job performance and employ a mixed-methods approach that would mitigate the shortfalls of either quantitative or qualitative research approaches.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abas, M. C., & Imam, O. A. (2016). Graduates’ competence on employability skills and job performance. International Journal of Evaluation and Research in Education, 5(2), 119–15 http://doi.org/10.11591/ijere.v5i2.

- Afifah, U., Sari, R. N., Anugerah, R., & Sanusi, Z. M. (2015). The effect of role conflict, self-efficacy, professional ethical sensitivity on auditor performance with emotional quotient as moderating variable. Procedia Economics and Finance, 31, 206–212. https://doi.org/10.1016/S2212-5671(15)01222-8

- Ahmad, S. R., Hariri, H., Zawawi, S. N. H. M., & Hassan, R. (2019). Determinants of auditors' work performance. International Journal of Financial Research, 10(3), 230–238 https://doi.org/10.5430/ijfr.v10n3p230.

- Al-Hattami, H. M. (2021). University accounting curriculum, it, and job market demands: Evidence from Yemen. SAGE Open, 11(2), 1–14. https://doi.org/10.1177/21582440211007111

- Baah-Boateng, W. (2015). Unemployment in Ghana: A cross-sectional analysis from demand and supply perspectives. African Journal of Economic and Management Studies, 6(4), 1–16. https://doi.org/10.1108/AJEMS-11-2014-0089

- Barzegar, N., & Farjad, S. (2011). A study on the impact of on-the-job training courses on the staff performance (A Case Study). Procedia - Social and Behavioural Sciences, 29, 1942–1949. https://doi.org/10.1016/j.sbspro.2011.11.444

- Becker, G. (1975). Human capital: A theoretical and empirical analysis (2nd ed.). Columbia University Press.

- Becker, G. S. (1993). Human capital: A theoretical and empirical analysis with special reference to education. University of Chicago Press.

- Busuioc, A., Borgonovo, A. J. M., & Mai, T. T. P. (2019). Vietnam corporate accounting education in universities. The World Bank: DC

- Campbell, J. P. (1990). Modeling the performance prediction problem in industrial and organizational psychology. Consulting Psychologists Press

- Campbell, J. P., McCloy, R. A., Oppler, S. H., & Sager, C. E. (1993). A theory of performance. In N. Schmit & W. C. Borman (Eds.), Personnel selection in organizations (pp. 35–70). Jossey-Bass.

- Campbell, J. P., Gasser, M. B., & Oswald, F. L. (1996). The substantive nature of job performance variability. In K. R. Murphy (Ed.), Individual differences and behavior in organizations (pp. 258–299). Jossey-Bass.

- Campbell, J. P., & Wiernik, B. M. (2015). The modeling and assessment of work performance. Annual Review of Organizational Psychology and Organizational Behavior, 2, 2(1), 47–74. https://doi.org/10.1146/annurev-orgpsych-032414-111427

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed. ed.). Erlbaum.

- Crawford, E. R., Rich, B. L., Buckman, B., & Bergeron, J. (2014). Antecedents and drivers of employee engagement. In C. Truss, R. Delbridge, K. Alfes, A. Shantz and E. Soane (Eds.), Employee engagement in theory and practice (pp. 57–81). Routledge.

- Creswell, J. W., & Creswell, J. D. (2017). Research design: Qualitative, quantitative, and mixed methods approach. Sage publications.

- Fung, D. (2017). Connecting academic learning with workplace learning. In connected curriculum for higher education. UCL Press.

- Georgiou, A. (2018). The accounting education of graduates: Is it meeting the needs of employers? Evidence from Cyprus. Iranian Journal of Accounting, Auditing, and Finance, 19(1–2), 23–50 doi:https://dx.doi.org/10.22067/ijaaf.v2i2.74113.

- Gillies, D. (2017). Human capital theory in education. In M. Peters (Ed.), Encyclopedia of Educational Philosophy and Theory (pp. 1–5). Springer.

- Hadisantoso, E., Sudarma, I. M., & Rura, Y. (2017). The influence of professionalism and competence of auditors towards the performance of auditors. Scientific Research Journal (SCIRJ), 1 V , 1–14.

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed, a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11–2018-0203

- Hanafi, H. M., & Ibrahim, S. B. (2018). Impact of employee skills on service performance. International Journal of Science and Research, 7(12), 587–600 https://www.ijsr.net/archive/v7i12/ART20193416.pdf.

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- IFAC. International Ethics Standards Board for Accountants (IESBA). (2015). International ethics standards board for accountants fact sheet. American Accounting Association

- International Accounting Education Standard Board [IAESB]. (2017). Handbook for international pronouncement (New York: International Federation of Accountants).

- Kavanagh, M., & Drennan, L. (2008). What skills and attributes does an accounting graduate need? Evidence from student perceptions and employer expectations. Accounting and Finance, 48(2), 279–300. https://doi.org/10.1111/j.1467-629X.2007.00245.x

- Khan, S. (2018). Demystifying the impact of university graduate’s core competencies on work performance: A Saudi industrial perspective. International Journal of Engineering Business Management, 10, 1–10. https://doi.org/10.1177/1847979018810043

- McCloy, R. A., Campbell, J. P., & Cudeck, R. (1994). A confirmatory test of a model of performance determinants. Journal of Applied Psychology, 79(4), 493–505. https://doi.org/10.1037/0021-9010.79.4.493

- Mincer, J. (1974). Progress in human capital analysis of the distribution of earnings. National Bureau of Economic Research.

- Motowidlo, S. J., & Kell, H. J. (2013). Job performance. In I. İçinde Weiner (Ed.) Handbook of psychology: Vol. 12.(pp. 82–103). https://www.routledge.com/Employee-Engagement-in-Theory-and-Practice/Truss-Alfes-Delbridge-Shantz-Soane/p/book/9780415657426

- Murphy, B., & Hassall, T. (2020). Developing accountants: From novice to expert. Accounting Education, 29(1), 1–31. https://doi.org/10.1080/09639284.2019.1682628

- Nassazi, A. (2013). Effects of Training on Employee Performance. Evidence from Uganda. [Thesis], University of Applied Sciences.

- Nechita, E. (2019). Analysis of the relationship between accounting and sustainable development. the role of accounting and accounting profession on sustainable development. Audit Financiar, 17(155), 520–536. https://doi.org/10.20869/AUDITF/2019/155/021

- Oliveira, T. C., & Holland, S. (2007). Beyond human and intellectual capital: Profiling the value of knowledge, skills, and experience. Comparimento Organizacionale Gestado, 13(2), 237–260 https://core.ac.uk/download/pdf/70656387.pdf.

- Oliveira, T. C., & Da-Costa, J. F. (2014). Gaining or losing? Projective identification, professional identities, and new public management. In C. Machado & J. P. Davim (Eds.), Work organization and human resource management. (pp. 135–152). Springer Publishing.

- Palmer, K. N., Ziegenfuss, D. E., & Pinsker, R. E. (2004). International knowledge, skills, and abilities of auditors/accountants. Managerial Auditing Journal, 19(7), 889–896. https://doi.org/10.1108/02686900410549411

- Schultz, T. W. (1960). Capital formation by education. Journal of Political Economy, 68(6), 571–583. https://doi.org/10.1086/258393

- Schultz, T. (1961). Investment in human capital. The American Economic Review, 51(1), 1 https://www.ssc.wisc.edu/~walker/wp/wp-content/uploads/2012/04/schultz61.pdf.

- Spencer, T. D., Detrich, R., & Slocum, T. A. (2012). Evidence-based practice: A framework for making effective decisions. Education and Treatment of Children, 35(2), 127–151. https://doi.org/10.1353/etc.2012.0013

- Tan, E. (2014). Human capital theory: A holistic criticism. Review of Educational Research, 84(3), 411–445. https://doi.org/10.3102/0034654314532696

- Vannatta, S. C. (2014). Teaching to the test: A pragmatic approach to teaching logic. Education and Culture, 30(1), 39–56. https://doi.org/10.1353/eac.2014.0000

- Wade, M. R., & Parent, M. (2002). Relationships between job skills and performance: A study of webmasters. Journal of Management Information Systems, 18(3), 71–96. https://doi.org/10.1080/07421222.2002.11045694

- Widayati, A., MacCallum, J., & Woods-McConney, A. (2021). Teachers’ perceptions of continuing professional development: A study of vocational high school teachers in Indonesia. Teacher Development, 25(5), 604–621. https://doi.org/10.1080/13664530.2021.1933159

- Williams, L. J., & Anderson, S. E. (1991). Job satisfaction and organizational commitment as predictors of organizational citizenship and in-role behaviors. Journal of Management, 17(3), 601–617. https://doi.org/10.1177/014920639101700305

- Wong, K. K. (2013). Partial least squares structural equation modeling (PLS-SEM) techniques using smartPLS. Marketing Bulletin, 24(1), 1–32 http://marketing-bulletin.massey.ac.nz/V24/MB_V24_T1_Wong.pdf.