Abstract

The Government of Ghana spends approximately seventy percent of its annual budget on the procurement of goods, services, and public works. The Public Procurement Acts (Act 663, and Act, 914) were established to regulate public procurement activities and ensure transparency, accountability, and Value for Money (VFM) in the procurement processes. Contrariwise, the extent of misappropriations of public funds in Ghana by public officials has reached an all-time high. To address this concern, our paper is aimed to develop a model to explain the extent to which Internal Audit Effectiveness (IAE) drives VFM, and Sustainable Public Procurement (SPP). This paper is a cross-sectional survey-based study involving public agencies in Ghana. The population of the study comprised 72 District Assemblies across the Greater Accra and Ashanti regions. Stratified sampling technique has been used to randomly select 200 participants comprising internal auditors, procurement officers, accountants, and finance officers for the study. Smart-PLS software and the Structural Equation Modelling (SEM) approach have been used to analyze the survey data, and test the hypotheses of the study. The study has revealed that internal audit competency, internal audit independence, external auditors’ role, and top management support are the main determinants of IAE. Again, our mediation analysis has revealed that IAE drives both VFM and SPP. The results have further shown that an increase in VFM positively affects SPP. These results have implications for the reinforcement of internal audit agency regulations of 2003 (Act 658) and public procurement act 2003 (Act 663) and the amended Act 2016 (Act 914). Again, the results have extended exciting knowledge on the IAE by linking it up with SPP and VFM in a developing country context where such studies still remain fuzzy.

1. Introduction

Sustainable Development Goals (SDGs) and the Paris Climate Agreement were adopted, recognizing the determination of UN member states to “take bold and transformative actions needed to put the world on a sustainable and resilient path.” The UN Agenda consists of 17 SDGs and 169 targets, with Goal 12 specifically addressing the need to “ensure sustainable consumption and production” through eleven different targets, one of which, Target 12.7, aims to “promote sustainable public procurement practices in accordance with national policies and priorities” (Islam et al., Citation2017; Chogo & Kitheka, Citation2019; (Barbanti et al., Citation2022; Khalid & Sarea, Citation2020). More and more companies are realizing that sustainability must be a priority for their business and are setting targets. This is not only because of increasing legislation and regulations, but also because consumers, shareholders, and their own employees are demanding it. Procurement, which more generally refers to the process or activity of providing services or goods to an organization, can play an important role in achieving these goals. For example, by contributing to the reduction of CO2 emissions and “net-zero” goals (Gormly, Citation2014; Grandia et al., Citation2015; Jermsittiparsert et al., Citation2019). According to the World Bank, governments today spend about $13 trillion on public procurement for goods, services, and works. Good public procurement can unlock trillions of dollars in annual savings that can be used to support a green, resilient and inclusive economy. At the same time, a quarter of this spending is lost to inefficiency (Josh & Karyawati, Citation2022; Murungi & Senelwa, Citation2019; Nsiah-Asare & Prempeh, Citation2016; Onumah & Yao Krah, Citation2012; Oyewobi et al., Citation2017; Prier et al., Citation2016).

In Ghana, the 2003 Public Procurement Act (Act 663) was amended in 2016 (Act 914) to include sustainable practices in the procurement of goods, services, and public works using all or part of public funds, as part of the government’s commitment towards Sustainable Development Goal 12.7 (SDG 12). By law, public agencies, institutions, and establishments are mandated to comply with these Acts. Despite these initiatives misappropriation of public funds in Ghana by public officials is hitherto a record high. To address this gap, our paper aims to develop a model to explain the extent to which IAE drives VFM, and SPP, and analyze the determinants of IAE and VFM with a focus on the Ghanaian public sector context. To address this puzzle, we have synthesized the contingency theory of management and institutional theory to develop a robust model. In addition, we argue that a credible IAE-SPP model could save millions of Ghana cedis each year, which could be used to support a green, resilient, and inclusive economy. This paper contributes to the existing empirical, practical, and theoretical knowledge stocks in five distinctive ways. First and foremost, this paper is among the very few to develop a robust and successful model for improving compliance with SPP in the Ghanaian context. Prior to this work, most existing studies (Gaosong & Leping, Citation2021; Ochieng et al., Citation2016; Oyewobi et al., Citation2017; Prier et al., Citation2016) examined the determinants of IAE and SPP practices in isolations.

The mechanism through which SPP could be achieved has been largely ignored. We, therefore, consider previous reports to be insufficient, inconclusive, and inconsistent. We have synthesized contingency theory of management and institutional theory as the main mechanism through which IAE drives VFM, and SP into a single model, with a strong workforce and a robust, powerful model. Secondly, this study provides a new perspective to accelerate Ghana’s commitment to Sustainable Development Goal 12.7. We argue that effective sustainable procurement is critical because it means an organization fulfills its mission and builds reputation and trust with its customers and partners. Sustainable procurement means that organizations commit to procuring goods and services in an ethical and environmentally responsible manner. Responsible procurement also aims to make effective and sustainable long-term decisions in the interests of the company, its customers, society, and the environment. This covers a range of issues beyond child labor or the use of harmful chemicals that can affect people or the environment. Thirdly, this paper draws on the synergy between contingency theory and institutional theory to predict SP which is a more vibrant and robust way as compared to the strengths of the individual theories. It is believed that the integrated model offers wider generality of the structural model beyond Ghana.

Fourthly, the study further contributes to conceptual factors such as IAE, VFM, and SPP in the context of Ghana’s public sector where such findings largely remained disjointed and vague (Chogo & Kitheka, Citation2019; Gaosong & Leping, Citation2021; Islam et al., Citation2017; Nsiah-Asare & Prempeh, Citation2016; Al Nuaimi et al., Citation2020; Onumah & Yao Krah, Citation2012). The outcome of this paper is therefore expected to renew policy and practitioners’ commitments towards the need to reinforce the existing legislative protocols to enhance best practices in public procurement. Finally, this paper has approached the issues raised with 2nd Generational Analysis (Structural Equation Modelling (SEM) and larger sample size from the Ghanaian public sector. The SEM is undoubtedly a robust form of the traditional regression analysis (1st Generational Analysis). Therefore, to be able to realize the needs and contributions of the study for the purpose of theory, practice, policy, and academics, the following research questions were raised and addressed:

What is the relationship between IAE and public procurement performance in Ghana?

To what extent do IEA mediate the relationships between its determinants and VFM in the context of public procurement performance in Ghana?

To what extent do IEA mediate the relationships between its determinants and SP in the context of public procurement performance in Ghana?

The rest of the paper has been structured into four sections as follows: The section B, discusses the theoretical review of the paper and the hypotheses development, the section C, discusses the materials and methods used in the paper, the Section D, discusses the results of the paper, the Section E, presents discussions of results, conclusions and implications.

2. Theoretical and conceptual Review

The study used both institutional theory and contingency theory to develop a robust model to explain SPP. According to the institutional theory (DiMaggio & Walter, Citation1983), the procurement process can be viewed as a set of institutions that have an unusual relationship between buyers and suppliers and also influence the economic development of a country. The institution of the procurement process consists of (i) formal procurement rules and relationships between suppliers and vendors, as well as informal relationships that influence joint agreements and economic development activities, (ii) enforcement measures to implement procurement rules, sanctions and severity for non-compliance with procurement laws. In the public sector, procurement plays a dominant role in the areas of public services, law enforcement, health, social services, education, defense, transportation, and the environment, which means that the scope of procurement by public agencies to achieve public policy objectives and meet the needs of civil society is much greater than in the private sector. Institutionalization allows for the identification of independent suppliers and vendors and distinguishes the network of public and private actors, groups and organizations. With respect to individual behavior and analysis of these theories, a new theory of institutional economics is developing. The study has adopted institutional theory to serve as one of the mechanisms to through which IAE drives SPP in Ghana. On the other hand, contingency theory argues external and internal factors influence the extent to which organization is managed and led, therefore no specific standard is adequate (Fiedler, Citation1964; Meyer & Rowan, Citation1977).

In the context of this paper, it can be argued that internal auditor’s role needs to be complemented by the other stakeholders’ such as top management and external auditors to be effective as showed in the research frame work in the Figure . Contingency theory is often used in the context of achieving efficiency. Previous studies, have used contingency theory in the context of achieving efficiency at the organizational level. Finally, it has been found that the effectiveness of such a system depends on three variables: standardization of the organization, interdependence of knowledge across functional areas of the organization, and interdependence of knowledge sharing with other organizations. Similarly, the effectiveness of proposed accounting systems depends on their ability to adapt to changes brought about by external and internal factors. Several studies (Chogo & Kitheka, Citation2019; Islam et al., Citation2017; Nsiah-Asare & Prempeh, Citation2016; Onumah & Yao Krah, Citation2012) on internal auditing have shown that internal auditors are important to the achievement of corporate goals, but there is still no consensus on what factors best influence internal audit effectiveness or what framework researchers believe best predicts. This covers a range of issues beyond child labor or the use of harmful chemicals that can affect people or the environment. Thirdly, this paper draws on the synergy between contingency theory and institutional theory to predict SPP which is more vibrant and robust way as compared to the strengths of the individual theories. It is believed that the integrated model offers wider generality of the structural model beyond Ghana.

Figure 1. Research framework.

While the presentations in this paper suggest that internal audit effectiveness (IAE) can play an important role in promoting sustainable public procurement (SPP) and value for money (VFM), the role of IAE in sustainable procurement has been largely ignored in previous studies. Procurement auditing is the process of reviewing and analyzing procurement process to ascertain areas of concerns in order to offer measures for improvements, enhance compliance with internal control, industry standards, and manage risk and fraud through optimization. In essence, the role of internal audit is to provide an independent and objective assurance and consulting process that adds value and improves an organization’s operations (Gormly, Citation2014; Grandia et al., Citation2015; Jermsittiparsert et al., Citation2019). In addition, an effective internal audit function provides three key elements of process assessment and improvement in the areas of risk management, control, and governance, using tools such as financial auditing, performance auditing, and research and advisory services to fulfill each role. Previous studies (Grandia et al., Citation2015; Murungi & Senelwa, Citation2019) have argued that IAE is a determinant of internal audit independent, internal audit competency, TMS for internal audit, internal—external auditors’ relationship, and quality of internal audit.

2.1. Empirical review and hypotheses development

2.1.1. IA competence as a determinant of IEA

We argue in this paper that IA competency relates to IAE. Accordingly, Hoffmann (Citation1999) defines competency as the specific knowledge, skills and attitudes required to apply certain standards in practice (International Federation of Accountants (IFAC), Citation2010). According to Baharud-din et al. (Citation2014) staff competence is defined as the ability of staff to perform tasks reliably and depends on training, experience of work and the development of continuous staff professionally. As asserted by the Institute of Internal Auditors (IIA) competencies and skills are basic requirements that internal auditors need to conduct an effective internal audit (Bailey, Citation2010). The IIA further averred that the skills and abilities that internal auditors need to do their job effectively (Bailey, Citation2010). Soft skills include the core competencies that there is a need for the auditors internally to do internal auditors need to do tasks specifically (Bailey, Citation2010). Behavioural skills are the interpersonal and technical skills needed to manage the work of internal auditors and their staff according to accepted standards (Bailey, Citation2010). The competence staff is a significance factor influencing IAE (Al-Twaijry et al., Citation2003; Alzeban & Gwilliam, Citation2014). The auditors internally should have education necessary for auditing, there should be qualifications in professions, there should be training and experience in order for improvement and also contribution towards organization performance (Ali & Owais, Citation2013; D.G. Mihret & Woldeyohannis, Citation2008). In view of the above presentation, the study hypothesizes that:

H1: Internal Audit staff competency has significant and positive relationship with IAE

2.1.2. IA Independence as a determinant of IEA

We argue in this paper that IA independence relates to IAE. Independence is the cornerstone of the auditing profession, but it is also very important for an audit firm. Although auditor independence is equated with the auditors externally, Alzeban and Gwilliam (Citation2014) argue that professional bodies and standard setters place more importance on the independence of the internal auditor, even if the auditor is an employee of the organisation. The independence of the internal auditor is considered an important element of effective internal auditing (Al-Akra et al., Citation2016; Baharud-din et al., Citation2014). In recent years, the association of the professional and the bodies of standard setting have made it clear on the significance of the independence of the internal auditors and objectivity in ensuring the quality of internal control, even if the internal auditor is an employee of the organisation. Independence and objectivity are important factors in improving the effectiveness of internal audit (Ahmad et al., Citation2009; Al-Akra et al., Citation2016; Mutchler, Citation2003). On the basis of the above, Institution of Internal Auditors (IIA; Citation2010) defines independence as “objective, honest independence, free from undue pressure from any authority”. Researchers assess organisational independence using three indicators: objectivity, legal basis and policies and procedures. Objectivity refers to the auditors’ ability to perform their duties as professionally and impartially as possible (Alzeban & Gwilliam, Citation2014). The legal framework defines the structure and organisation of the audit function and the influence and control of the internal auditor (Masika, Citation2013). Inferring from the arguments, the study hypothesizes as follows:

H2: Internal Audit independence has significant and positive relationship with IAE

H5: Internal Audit independence has significant and positive relationship with VFM

2.1.3. External auditors role as a determinant of IEA

We have argued further in this paper that the external auditor’s role relates to IAE. External auditors are an important part of public sector accountability and make an important contribution to the management of public resources and public services (Audit Commission, Citation2008). External auditors are appointed independently of the audited entity and their work focuses not only on the financial statements but also on the accuracy of expenditure and the efficiency of public service delivery. The audit of the financial statements aims to determine whether the organisation’s financial statements give a true and fair view. The audit process must follow established standards and provide the auditor with an opinion or other assessment of the quality of the audit and compliance with the standards. The main purpose of the audit is to ensure accountability of public funds (Azham et al., Citation2004). The Internal and External Auditing Standards stress the importance of cooperation between internal and external auditors. The Internal Auditing Standard (Standard 2050) stresses the importance of a professional relationship between internal and external auditors. The standard identifies the following benefits of cooperation between the two parties (Wu et al., Citation2017) Coordination ensures adequate audit coverage, reduces duplication of effort, and lowers external audit costs (Henderson et al.). Research shows that the auditors internally and external connection is very significant in order to ensure that there is benefit for stakeholders externally and the organization (Alzeban & Gwilliam, Citation2014; Alzeban & Sawan, Citation2013). Planning jointly and information sharing are the requirement for the connection between the auditors internally and externally, recommendations and reports to improve audit quality and avoid repetition of effort which are not necessary. Inferring from the presentation above, the study hypothesizes as follows:

H3: External auditor’s role has significant and positive relationship with IAE

H6: External auditor’s role has significant and positive relationship with VFM

2.1.4. Top management support as a determinant of IEA

Prior studies have argued that top management support relates to IAE. Management support facilitates the work of internal auditors, including resources, funding, travel when needed, training, introduction of auditors to new practices and procedures, and funding for certification (George et al., Citation2015). The support of senior management is critical to the success of internal audit (Dellai & Omri, Citation2016). The definition of internal audit includes good governance, which largely depends on management’s ability to ensure that the internal audit function is effective (Alzeban & Gwilliam, Citation2014). When internal auditors are supported by senior management, they have the resources that are adequate in order to fulfill the responsibility and the mandate, and the internal audit function can recruit staff who are qualified and give ongoing training and capacity building (Alzeban & Sawan, Citation2013; Cohen & Sayag, Citation2010). Management support for the audit process is critical to the success of the function of the audit internally. Many studies have shown that if there is no approval from the management, support and encouragement, the IA process often fails, resulting in lower standards, wasted time and money (D. Mihret & Yismaw, Citation2007). Management support is the time management spends defining values, building capacity, reviewing plans and monitoring performance (Lenz & Sarens, Citation2012). Inferring from the argument, the study hypothesizes as follows:

H4: Top management Support has significant and positive relationship with IAE

H7: Top management Support has significant and positive relationship with VFM

2.1.5. IAE as a determinant of VFM and SPP

We have argued that IAE drives VFM and SPP in the emerging economy context. Our position is that IAE can play an important role in promoting SPP and VFM, the role of IAE in sustainable procurement has been largely ignored in previous studies (Chogo & Kitheka, Citation2019; Islam et al., Citation2017; Nsiah-Asare & Prempeh, Citation2016; Onumah & Yao Krah, Citation2012). The SPP program enables organizations to review and analyze their procurement processes to identify areas for improvement; ensure compliance with internal controls, industry standards, and regulatory requirements; and reduce risk, fraud, and waste through procurement process optimization. In essence, the role of internal audit is to provide an independent and objective assurance and consulting process that adds value and improves an organization’s operations (Gormly, Citation2014; Grandia et al., Citation2015; Jermsittiparsert et al., Citation2019). In addition, an effective internal audit function provides three key elements of process assessment and improvement in the areas of risk management, control, and governance, using tools such as financial auditing, performance auditing, and research and advisory services to fulfill each role. Previous studies (Grandia et al., Citation2015; Murungi & Senelwa, Citation2019) have argued that IAE is a determinant organizational resilience. Therefore, we have hypothesized as follows:

H8: IAE has significant and positive relationship with VFM

H9: IAE has significant and positive relationship with SPP

H10-14: IAE determinants significantly mediate the relationship IAE and VFM

2.1.6. VFM as mediator between IAE and SPP

The final proposition of the study is that VFM is a significant contributor of SPP. VFM broadly defines the optimal ratio of total benefits to total costs. In this context, it does not necessarily mean that a contract is awarded to the lowest bidder (Nsia and Prempeh, Citation2016). VFM is usually characterised by a clear commitment to maximizing benefits. There is a clear commitment to best VFM. The public institutions use the VFM concept to ensure greater transparency and accountability in the use of public funds and to make the best use of available resources (Barnett et al., Citation2010). In public procurement, cost-effectiveness is achieved by achieving the lowest total life-cycle costs, clearly demonstrating the associated benefits and meeting deadlines (Glas et al., Citation2017; Nsiah-Asare & Prempeh, Citation2016). Jackson (Citation2012) explains that “VFM” is a balance between three aspects: economy (minimizing costs), efficiency (maximizing results) and effectiveness (achieving all desired outcomes). It is a qualitative indicator that measures the monetary value of the goods or services produced. Cost-effectiveness; cost-effectiveness shows how best to use resources to achieve a desired outcome. Cost effectiveness does not mean that the contract should be awarded to the cheapest bidder. In other words, it is not about the lowest initial price, but the best combination of cost and overall quality (Nsiah-Asare & Prempeh, Citation2016). It promotes the rational use of resources and emphasizes an organisation’s ability to reduce costs without compromising the scope, impact or quality of projects and services (Gelderman et al., Citation2015; McCrudden, Citation2004; Meehan & Bryde, Citation2011; Opiyo, Citation2015; Telgen et al., Citation2007). It examines whether resource-funded activities adequately achieve their objectives and whether the use of resources adds value. It also promotes transparency and accountability by providing decision-makers with comprehensive information on the performance of an organisation’s activities and decisions. In recent times, VFM has been linked to sustainable procurement. For instance, Brammer and Walker (Citation2011) argued that social and environmental objectives can be achieved directly through public procurement. Sustainable procurement is based on a bottom-up approach that aims to balance the economic, environmental and social aspects of the goods and services purchased (Gelderman et al., Citation2015; Meehan & Bryde, Citation2011). Therefore, we have hypothesized as follows:

H10: VFM has significant and positive relationship with SPP

H15-18: IAE determinants significantly mediate the relationship VFM and SPP

3. Materials and methods

3.1. Setting and research design

The setting of this paper is the Public Sector of Ghana. This sector comprises a portion of the Ghanaian economy entailing government-controlled enterprises and agencies at all levels of government. In principle, this sector does not include private companies’ voluntary organizations and individual households. This study focuses on internal audit effectiveness, value for money, and sustainable public procurement in Ghana. The Ministry of Finance has over the years reported that an estimated 70% of the Government’s annual budget passes through procurements of goods, services, and other works. This calls for vigilance, accountability, and transparency in the sector in order to ensure value for money, as a result, the procurement Acts 2003, and amendment Act 2016 were established by law to ensure the safety of public funds in the acquisition of goods and services. This paper is one of the very few to concurrently study IAE, VFM, and SPP among public agencies in Ghana since previous studies (Islam et al., Citation2017; Nsiah-Asare & Prempeh, Citation2016; Onumah & Yao Krah, Citation2012) partially addressed these three constructs. In order to develop a model to explain the relationship between IAE, VFM and SPP quantitative research approach has been employed in this paper. The quantitative approach involves the systematic study of phenomena by collecting measurable data and applying statistical, mathematical, or computer methods. Quantitative has been used because it is objective, comprehensive, and often explanatory in nature (causes-and-effects relationships), which usually leads to logical conclusions (Babbie, Citation2010; Brians & Leonard et al., Citation2011).

3.2. The population and sampling approach

The population of this paper compriseds government-controlled enterprises and agencies at all levels of government. In principle, target population of the study comprised 72 Metropolitans, Municipalities, and District Assemblies across the Greater Accra (29 districts) and Ashanti regions (43 districts). The estimated population of study comprised four representatives (internal auditors, procurement officers, accountants, and finance officers) from each of the 72 districts. These two regions were chosen for the study on the bases that the former is the administrative capital of the country while the latter serves as the second-largest region in terms of population, a number of districts, and commerce activities. As a result, the majority of the public agencies have their presence in these two regions. Studies involving SEM application have a varying approach to determining sample size (Hair et al., Citation2014). Inferring from Hair et al. (Citation2014), the rule often has been used to determine the number of participants. This rule stipulates that the minimum sample size should be equal to the total number of paths directed towards latent variables multiple by ten (10). In the current study 10 paths could be counted, suggesting that the minimum required sample size for the study is 100 (10*10). The paper adopted a sample size of 200 and received a usable 67.5 percent response rate. Stratified sampling technique has been used to randomly select 200 participants comprising internal auditors, procurement officers, accountants, and finance officers for the study. The paper adopted the functional classifications as strata, while the participants were selected from each stratum until the required sample size was attained. Stratified sampling approach has the potential to reduce sampling errors and ensure representativeness.

3.3. Constructs measurements and data collection instrument

The measurement tools have been adopted and modified from previous studies. In general, adopting is preferable to adapting for several reasons. Firstly, reliability and validity tests conducted with the tool can be used in research, so there is no need to collect evidence of validity. However, the tools have been modified, therefore new validity and reliability tests have been conducted. Secondly, using existing tools allow the study to be linked to other studies that have used the same tool. For instance, measurement scales for internal audit effectiveness and its determinants were adopted from D.G. Mihret and Woldeyohannis (Citation2008) and D. Mihret and Yismaw (Citation2007). The measurement scale for VFM was adopted from Nsiah-Asare and Prempeh (Citation2016) while the measurement scale for SPP was adopted from Meehan and Bryde (Citation2011). All the adopted scales were modified to meet the requirements of the current paper. The study used a 5-point Likert-type scale to measure all the constructs. Where 5-implies strongly agree and 1-implies strongly disagree. Again, a structured questionnaire was the main data collection instrument adopted for the study. Questionnaires are able to cover wider participants within a minimum time period at a relatively lower cost. Besides, in all survey-based studies including the current paper, the most appropriate instrument is always a questionnaire. The questionnaire was pretested using 20 respondents which were randomly selected from the Kumasi metropolis but the researchers did not find any significant issue with the instruments. The final questionnaire was structured into four sections. The first three sections focused respectively on IAE, VFM, and SPP while the last section focused on demographic questions such as age, education, experience, job designation, and sector/agency.

3.4. Ethical consideration

This study involved human participation as a result of ethical consideration have been duly followed. Among them are inform consent, respect for human right, protection of participants from harm, anonymity and professional integrity. The respondents have been given the free-will to decide their participation. None of the participant has been forced to partake in the study. The right and freedom of the participants have been respected throughout the study. The researchers have ensured that participants are not harmed in the process of participating in the survey. The responses received have been kept anonymously. The data shall be made available for other academic work upon request.

3.5. Data analyses

Prior to the data analysis, the field data were screened for omission, double-entry, and non-completions. The data was analyzed using PLS and SEM methods and SMART-PLS algorithm version 3.3.1. The first part of the analysis focused on scale validations. In this case, discriminant validity and convenience validity were conducted as evident in Tables . The second part of the analysis focused on the structural model (path coefficients). The original sample size was bootstrap using 500 resamples to generate T-values and path coefficients () which have been used to test the hypotheses of the study as shown in Table . There are steps recommended by Hair et al. (Citation2014) to evaluate the structural model. Namely: collinearity assessment, Path Coefficient, Coefficient of determination (R-square), effect size (f-square, predictive relevance (Q-square), and blindfolding. To conduct the mediation analysis, the SEM approach has been used as suggested by Hair et al. (Citation2014). The SEM is undoubted, a robust form of the traditional regression analysis (1st Generational Analysis). SEM has the capacity to support several exogenous variables mediators and outcome variables (endogenous variables) in just a single analysis (Cepeda et al., Citation2017; Nitzl et al., Citation2016).

Table 1. Respondent’s demographic characteristics

Table 2. Descriptive statistics

Table 3. Scale validation-reliability and validity Fornell–Larcker criterion

Table 4. Heterotrait-monotrait test ratio using Henseler et al., Citation2015)

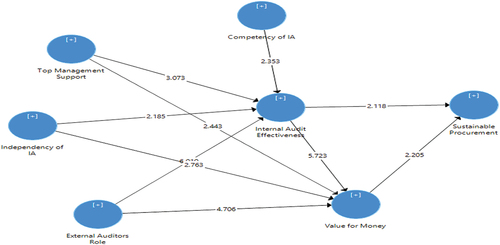

Figure 2. Path coefficients showing T-values.

4. Results and discussion

4.1. Respondent’s demographic characteristics

The results have showed that slightly above half (53%) of the participants are males while the rest (46.7%) are females. With respect to participants’ age ranges, slightly above one-third of the participants are aged between 30–39 years, 22.2% are aged between 20–29 years, 28.1% are aged between 40–49 years, and the least age group (8.9) are aged above 50 years. Concerning the participants education, the study has revealed that more than half (54.8%) of the participants have bachelor degrees, 37% have master’s degree, while the least participants have Higher National Diploma and other professional qualifications. The results have showed that majority of the participants had worked below 10 years while only 19.3% had worked for over 10 years. This is consistent with the age ranges of the participants who are predominantly youthful in nature. Regarding the participants job designation, the results have showed that 34.8% are internal auditors, 30.4% are procurement officers, 24.4% are finance officers and 14.4% are accountants. Table presents the details of the participants demographic information.

4.2. Descriptive statistics results

As showed in the Table , the descriptive analytics of each indicator has been examined using mean values, composite means values, standard deviation, minimum and maximum values. The highest mean score value was obtained for sustainable procurement with a composite mean value of 4.134 with standard deviation of 0.784. The second highest mean score was obtained for IAE variables independent of IA with a composite mean of 4.037 and a standard deviation of 0.918. Clearly, from the descriptive results it can be deduced that participants have varied opinions, experiences and perceptions of the issues been studied.

4.3. Validation: Convergent validity and discriminants validity (outer model measurement)

In the present study, convergent validity, and discriminant validity tests have been used to evaluate the reflexive structures of the measurement model (outer model). Convergent Validity (CV) measures the extent to which two or more constructs are related. The current study has assessed CV using composite reliability (CR). Hair et al. (Citation2014) suggested that for a construct to be acceptable it should have CR score of 0.70 or better. As should in the Table , CR scores ranged from 0.81 to 0.93 which suggest that all the construct meet the requirement threshold of 0.70. Again, Average Variance Extracted (AVE) scores have been used to assess CV. The minimum threshold of 0.50, has been exceeded by all the constructs used in the model. As indicated in the Table , the AVE scores ranged from 0.527 to 0.772 exceeding the minimum threshold of 0.50. Moreover, Cronbach Alpha (CA) scores have been assessed as part of the measures to determine convergence validity of the model. Like CR the minimum threshold of CA is 0.70, as showed in the Table , the CA scores for all the constructs ranged from 0.77 to 0.91, which exceeded the minimum threshold requirement 0 f 0.70.

Discriminant Validity (DV) is a statistical measure of the difference between two variables. DV is empirically use to analyse the extent to which one variable differs from another. Most prior studies relied on Fornell and Larcker’s (Citation1981) criteria for measuring DV. As showed in the , the Italics values in the diagonal row are square roots of the AVE which are higher than the intra-correlation among the variables suggesting that discriminant validity has been attained. Notwithstanding, Henseler et al. (Citation2015) have developed new criterion for assessing DV in structural modelling called Heterotrait-Monotrait Ratio (HTMT) which is a new method for calculating discriminant validity. For the model to attained DV, HTMT test score must be less than 0.85 for theoretically comparable structures and 0.90 for conceptually different structures. As depicted in the , the HTMT ratio for the constructs ranged from 0.146 to 0.711. Besides, the DV has been assessed using cross-loadings as showed in the clearly the items load into their respective construct which suggest that discriminant validity for the model has been further confirmed. These results confirm that the model has met the required convergent validity and discriminant validity thresholds, therefore, we can proceed to the structural model assessment.

Table 5. Cross-loadings

Table 6. Output of variance inflation factor (VIF) test

4.4. Structural model evaluation

There are five (5) steps approach recommended by Hair et al. (Citation2014) to evaluate structural model. Namely: collinearity assessment, Path Coefficient, Coefficient of determination (R-square), effect size (f-square, and predictive relevant (Q-square) and blindfolding. Each of the five steps has been elaborated below. First and foremost, each of the items has been assessed for possibly collinearity problem. As showed in the Table , Variance Inflation Factor (VIF) values for all the items in the structural model ranged between 1.281 to 3.36, which is below the minimum recommended threshold value of 5.0 (Hair et al., Citation2014). Therefore, the study finds insufficient evidence on collinearity.

4.5. Coefficient of determinants R-Square (R2) (path coefficient and hypotheses testing)

The R-square values have been used as the coefficient of determinants to quantify the extent to which a variance in a particular latent endogenous variable is explained by an exogenous latent variable. Three direct models have been presented in this paper. In model 1, exogenous variables such as CIA, IIA, TMS, and EAR have explained 65.7% variance in IAE as showed in the Table . In model 2, exogenous variables such as CIA, IIA, TMS, and EAR have accounted for 57.5% variability in VFM. Finally, in model 3, the result has showed that 73% variance in sustainable public procurement has been explained by VFM and IAE. All the ten (10) direct hypotheses have been supported in the model. Specifically, the hypothesized path has showed the following results. The model has revealed that CIA has significant and positive effect (Beta = 0.151, P-value = 0.019) on IAE. Moreover, EAR has positive and significant effect (Beta = 0.504, P-value = 0.000) on IAE. Additionally, IIA has positive and significant effect (Beta = 0.211, P-value = 0.029) on IAE. Also, TMS has negative and significant effect (Beta = −0.159, P-value = 0.002) on IAE. Further, the result reveals that EAR has positive and significant effect (Beta = 0.211, P-value = 0.000) on VFM. Likewise, IIA has positive effect (Beta = 0.223, P-value = 0.006) on VFM. Similarly, IAE has positive and significant effect (Beta = 0.411, P-value = 0.000) on VFM. Whereas TMS support has negative but significant effect (Beta = −0.119, P-value = 0.015) on VFM. In addition, the result reveals that IAE has positive and significant effect (Beta = 0.318, P-value = 0.035) on sustainable procurement. Furthermore, VFM has positive and significant effect (Beta = 0.314, P-value = 0.028) on sustainable procurement. These results imply that factors such as TMS, independency of IA, external auditors’ role and competency of IA have significant effect of VFM and SPP and furtherance VFM has a significant and positive effect on sustainable procurement.

Table 7. Structural model and hypotheses testing

As showed in the Tables the model examined two mediating roles. With respect to IAE as the mediator, the results have revealed a significant mediating role of IAE (Beta = 0.062, P-value = 0.033) on the relationship between competency of IA and VFM. Also, there is a significant mediation role of IAE (Beta = −0.065, P-value = 0.009) on the relationship between top management and VFM. Again, IAE significantly mediates (Beta = 0.087, P-value = 0.047) the relationship between independency of IA and VFM. Similarly, IAE significantly mediates (Beta = 0.207, P-value = 0.000) the relationship between EAR and VFM. Moreover, the result reveals a significant mediation role of VFM (Beta = 0.129, P-value = 0.029) on the relationship between IAE and sustainable procurement. Likewise, VFM significantly mediates (Beta = 0.092, P-value = 0.036) the relationship between EAR and sustainable procurement. Further, the result reveals a significant mediation role of VFM (Beta = 0.1070 P-value = 0.013) on the relationship between IIA and sustainable procurement. However, the result reveals that VFM insignificantly mediates (Beta = −0.037, P-value = 0.094) the relationship between TMS and sustainable procurement.

4.6. Structural model evaluation

There are five (5) steps approach recommended by Hair et al. (Citation2014) to evaluate structural model. Namely: collinearity assessment, Path Coefficient, Coefficient of determination (R-square), effect size (f-square, and predictive relevant Q-square) and blindfolding. Each of the five steps have been elaborated below. First and foremost, each of the items has been assessed for possibly collinearity problem. As showed in the Table Variance Inflation Factor (VIF) values for all the items in the structural model ranged between 1.281 to 3.36, which is below the minimum recommended threshold value of 5.0 (Hair et al., Citation2014). Therefore, the study finds insufficient evidence on collinearity.

4.7. Predictive relevance (Q2)

The Q-square measures the predictive relevance of a given model. It focuses on the value of the endogenous variable of the model where any value greater than zero implies that the model has predictive relevance. The predictive relevance of structural model could be assessed using Stone-Geisser Criteria (Hair et al., Citation2014). As showed in the Table , predictive relevance of the model was assessed using the PLS-SEM blindfolding approach by evaluating cross-validated redundancy. In model 1, the cross validated redundancy score for the endogenous variable (internal audit effectiveness) was greater than zero which implies the existence of predictive significance of the path model. In model 2, the cross-redundancy score for the endogenous variable (sustainable public procurement) was greater than zero suggesting the presence of predictive relevance of the path model. Finally, in the model 3, the cross-redundancy score for the endogenous variable (value for money) was greater than zero, implying that there is predictive relevance of the path model.

Table 8. Construct cross-validated redundancy

5. Discussions of results

The results emanating from the study have been further discussed in this section by comparing them with empirical literature. Our paper has developed a model to explain the extent to which IAE drives VFM and SPP. The study has revealed that internal audit competency, internal audit independence, external auditors’ role, and top management support are the main determinants of IAE. Again, our mediation analysis has revealed that IAE drives both VFM and SPP. The results have further should that an increase in VFM positively affects SPP. Prior to this work, most existing studies (Kannan, Citation2021; Nsiah-Asare & Prempeh, Citation2016; Onumah & Yao Krah, Citation2012) examined the determinants of IAE and SPP practices in isolations. Other mechanisms through which SPP could be achieved have been largely ignored. We, therefore, consider previous reports to be insufficient, inconclusive, and inconsistent. The paper has again discovered contextual factors such as internal audit competency, internal audit independence, external auditors’ role, and top management support. Again, our mediation analysis has revealed that IAE drives both VFM and SPP. The results have further should that an increase in VFM positively affects SPP. The paper has also revealed that the drive towards sustainable public procurement requires adequate investment in internal audit effectiveness and value for money which is consistent with prior related studies (Chogo & Kitheka, Citation2019; Islam et al., Citation2017; Kisiwili & Ismail, Citation2016; Nsiah-Asare & Prempeh, Citation2016). Again, the results have extended existing knowledge (Nsiah-Asare & Prempeh, Citation2016) on the IAE by linking it up with SPP and VFM in a developing country context where such studies still remain fuzzy. The outcome of this paper is therefore expected to renew policy and practitioners’ commitments towards the need to reinforce the existing legislative protocols to enhance best practices in public procurement. Prior to this work, most existing studies (Chogo & Kitheka, Citation2019; Kannan, Citation2021; Nsiah-Asare & Prempeh, Citation2016) examined the determinants of IAE and SPP practices in isolations. Other mechanisms through which SPP could be achieved have been largely ignored. We, therefore, consider previous reports to be insufficient, inconclusive, and inconsistent.

6. Conclusions and implications

The government of Ghana spends an approximately a larger portion of its annual budget on the procurement of goods, services, and public works. The Public Procurement Act (Act 663, Act, 914) was established to regulate public procurement activities and ensure transparency, accountability, and VFM in the process. Meanwhile, misappropriations of public funds in Ghana by public officials have reached an all-time high. To address this concern, our paper has developed a model to explain the extent to which IAE drives VFM and SPP. The study has revealed that internal audit competency, internal audit independence, external auditors’ role, and top management support are the main determinants of IAE. Again, our mediation analysis has revealed that IAE drives both VFM and SPP. The results have further should that an increase in VFM positively affects SPP. This study has implications for practices, policies, and theory.

6.1. Theoretical implications

This paper is among the very few to develop a robust and successful model for improving compliance with SPP in the Ghanaian context by integrating IAE, VFM, and SPP. have synthesized contingency theory of management and institutional theory as the main mechanism through which IAE drives VFM, and SP into a single model, with a strong workforce and a robust model. The integrated model has more coverage as compared to the strength of the individual theories. Besides, the paper has successfully applied the contingency theory of management and institutional theory in the context of developing countries. Secondly, this study provides a new perspective to accelerate Ghana’s commitment to Sustainable Development Goal 12.7. We have effectively established that SPP is critical because it means an organization fulfills its mission and builds reputation and trust with its stakeholders. Finally, this paper has approached the issues raised in the study with the 2nd Generational Analysis (SEM) from the Ghanaian public sector. The SEM is undoubted, a robust form of the traditional regression analysis (1st Generational Analysis).

6.2. Practical implications

The study has established a strategic model to guide sustainable procurement practices in the public sector of Ghana which could guide practitioners in managing public resources by ensuring effective internal controls and value for money. The paper has again discovered contextual factors such as internal audit competency, internal audit independence, external auditors’ role, and top management support. Again, our mediation analysis has revealed that IAE drives both VFM and SPP. The results have further should that an increase in VFM positively affects SPP. The paper has also revealed that the drive towards sustainable public procurement requires adequate investment in internal audit effectiveness and value for money which is consistent with prior related studies.

6.3. Policy implications

These results have implications for the reinforcement of internal audit agency regulations of 2003 (Act 658) and public procurement Act 2003 (Act 663) and the amended Act 2016 (Act 914). Procurement Authority should ensure that procurement officers, accountants, finance officers, and other stakeholders abide by the procurement regulations in order to enhance VFM. Sustainable public procurement should be seen as a means that organizations commit to procuring goods and services in an ethical and environmentally responsible manner. The outcome of this paper is therefore expected to renew policy and practitioners’ commitments towards the need to reinforce the existing legislative protocols to enhance best practices in public procurement. Again, the results have extended existing knowledge on the IAE by linking it up with SPP and VFM in a developing country context where such studies still remain fuzzy.

Correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Ahmad, N., Othman, R., Othman, R., & Jusoff, K. (2009). The effectiveness of internal audit in Malaysian public sector. Journal of Modern Accounting and Auditing, 5(9), 53–26.

- Al Nuaimi, B. K., Khan, M., & Ajmal, M. (2020). Implementing sustainable procurement in the United Arab emirates public sector. Journal of Public Procurement, 20(2), 97–117. https://doi.org/10.1108/JOPP-07-2019-0044

- Al-Akra, M.;., Abdel-Qader, W., & Billah, M. (2016). Internal auditing in the middle East and North Africa: A literature review. Journal of International Accounting, Auditing and Taxation, 26, 13–27. https://doi.org/10.1016/j.intaccaudtax.2016.02.004

- Al-Twaijry, A. A., Brierley, J. A., & Gwilliam, D. R. (2003). The development of internal audit in Saudi Arabia: An institutional theory perspective. Critical Perspectives on Accounting, 14(5), 507–531. https://doi.org/10.1016/S1045-2354(02)00158-2

- Ali, O. A., & Owais, W. O. 2013. Internal auditors’ intellectual (knowledge) dimension in creating value for companies empirical study of Jordanian industrial public shareholding companies. International Business Research. 6(1), 118–129. https://doi.org/10.5539/ibr.v6n1p118

- Alzeban, A., & Gwilliam, D. (2014). Factors affecting the IAE: A survey of the Saudi public sector. Journal of International Accounting, Auditing and Taxation, 23(2), 74–86. https://doi.org/10.1016/j.intaccaudtax.2014.06.001

- Alzeban, A., & Sawan, N. (2013). The role of internal audit function in the public sector context in Saudi Arabia. African Journal of Business Management, 7(6), 443.

- Audit Commission. (2008). Better outcomes, annual report and accounts

- Azham, M. A., Siti-Zabedah, S., Mohamad-Zulkurnai, G., Mohd-Syahrir, R., Mohd-Hadafi, S., Azharudin, A., & Aidi, A. 2004. Internal audit in the state and local governments of Malaysia: Problems and solutions. Paper presented at the ISF ALGAR, Universiti Utara Malaysia, MPSP and MPPP jointly organized PersidanganAkauntanPihakBerkuasaTempatan 2004 in Penang, 3-5 October, Penang.

- Babbie, E. R. (2010). The practice of social research (12th ed.). Wadsworth Cengage.

- Baharud-din, Z., Shokiyah, A., & Ibrahim, M. S. (2014). Factors that contribute to the effectiveness of internal audit in public sector. International Proceedings of Economics Development and Research, 70, 126.

- Bailey, J. A. (2010). Core competencies for today’s internal auditor. The Institute of Internal Auditors Research Foundation. Altamonte Springs.

- Barbanti, A. M., Anholon, R., Rampasso, I. S., Martins, V. W. B., Quelhas, O. L. G., & Leal Filho, W. (2022). Sustainable procurement practices in the supplier selection process: An exploratory study in the context of Brazilian manufacturing companies. Corporate Governance, 22(1), 114–127. https://doi.org/10.1108/CG-10-2020-0481

- Barnett, C., Barr, J., Christie, A., Duff, B., & Hext, S. (2010). Measuring the impact and value for money of governance & conflict programmes. ITAD.

- Brammer, S., & Walker, H. (2011). Sustainable procurement in the public sector: An international comparative study. International Journal of Operations & Production Management, 31(4), 452–476. https://doi.org/10.1108/01443571111119551

- Brians, C. L. (2011). Empirical political analysis: Quantitative and qualitative research methods (8th ed.). Longman.

- Cepeda, G., Nitzl, C., & Roldán, J. L. (2017). Mediation analyses in partial least squares structural equation modeling: guidelines and empirical examples., in partial least squares path modeling: basic concepts, methodological issues and applications. H. Latan & R. Noonaneds.Springer. https://doi.org/10.1007/978-3-319-64069-3_8

- Chogo, K. C., & Kitheka, S. (2019). Effect of sustainable procurement practices on organisation performance: A review of literature. International Journal of Economics & Business, 6(2), 21–34.

- Cohen, A., & Sayag, G. (2010). The effectiveness of internal auditing: An empirical examination of its determinants in Israeli organisations. Australian Accounting Review, 20(3), 296–307. https://doi.org/10.1111/j.1835-2561.2010.00092.x

- Dellai, H., & Omri, M. A. B. (2016). Factors affecting the IAE in Tunisian organizations. Research Journal of Finance and Accounting, 7(16), 208–211.

- DiMaggio, P. J., & Walter, W. P. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101

- Fiedler, F. E. (1964). A theory of leadership effectiveness. In L. Berkowitz (Ed.), Advances in experimental social psychology. Academic Press.

- Fornell, C., & Larcker, D. F. (1981). Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. Journal of Marketing Research, 18, 382–388. https://doi.org/10.1177/002224378101800313

- Gaosong, Q., & Leping, Y. (2021). Measurement of internal audit effectiveness: Construction of index system and empirical analysis. Microprocessors and Microsystems. https://doi.org/10.1016/j.micpro.2021.104046

- Gelderman, C. J., Semeijn, J., & Bouma, F. (2015). Implementing sustainability in public procurement: The limited role of procurement executives and party-political executives. Journal of Public Procurement, 15(1), 66–92. https://doi.org/10.1108/JOPP-15-01-2015-B003

- George, D., Theofanis, K., & Konstantinos, A. (2015). Factors associated with IAE : Evidence from Greece. Journal of Accounting and Taxation, 7(7), 113–122. https://doi.org/10.5897/JAT2015.0182

- Glas, A. H., Schaupp, M., & Essig, M. (2017). An organizational perspective on the implementation of strategic goals in public procurement. Journal of Public Procurement, 17(4), 572–605. https://doi.org/10.1108/JOPP-17-04-2017-B004

- Gormly, J. (2014). What are the challenges to sustainable procurement in commercial semi-state bodies in Ireland? Journal of Public Procurement, 14(3), 395–445. https://doi.org/10.1108/JOPP-14-03-2014-B004

- Grandia, J., Steijn, B., & Kuipers, B. (2015). It is not easy being green: Increasing sustainable public procurement behaviour. Innovation: The European Journal of Social Science Research, 28(3), 243–260. https://doi.org/10.1080/13511610.2015.1024639

- Hair, J., Hult, T., Ringle, C., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS-SEM). Sage Publications, Inc.

- Henseler, J., Ringle, M. C., & Sarstedt, M. (2015). A new criterion for assessing Discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hoffmann, T. (1999). The meanings of competency. Journal of European Industrial Training, 23(6), 275–285. https://doi.org/10.1108/03090599910284650

- Institution of Internal Auditors (IIA). (2010). International standards for the professional practice of internal auditing, standard 2120 risk management.

- International Federation of Accountants (IFAC). (2010). IFAC handbook of international public sector accounting pronouncements (2010 ed., Vols. 1-2). IFAC Publications.

- Islam, M., Turki, A., Murad, W., & Karim, A. (2017). Do sustainable procurement practices improve organisational performance? Sustainability, 9(12), 2281, 1–17. https://doi.org/10.3390/su9122281

- Jackson, P. (2012). VFM and international development. Deconstructing.

- Jermsittiparsert, K., Sutduean, J., & Sutduean, C. (2019). Sustainable procurement & sustainable distribution influence the organisational performance (economic, social and environmental): Moderating role of governance and collaboration at Thai food industry. Logistics & Supply Chain Management, 8(3), 83–94.

- Josh, L. P., & Karyawati, P. G. (2022). The institutional theory on the internal audit effectiveness: The case of India. Iranian Journal of Management Studies, 15(1), 35–48.

- Kannan, D. (2021). Sustainable procurement drivers for extended multi-tier context: A multi-theoretical perspective in the Danish supply chain. In Transportation research part E: Logistics and transportation review (Vol. 146(C)). Elsevier. https://doi.org/10.1016/j.tre.2020.102092

- Khalid, A. A., & Sarea, A. M. (2020). Independence and effectiveness in internal Shariah audit with insights drawn from Islamic agency theory. International Journal of Law and Management. ahead-of-print(ahead-of- print). https://doi.org/10.1108/IJLMA-02-2020-0056

- Kisiwili, E. N., & Ismail, N. S. (2016). Role of sustainable procurement practices on supply chain performance of manufacturing sector in Kenya: A case study of East African Portland cement company. European Journal of Logistics, Purchasing and Supply Chain Management, 4(3), 1–31.

- Lenz, R., & Sarens, G. (2012). Reflections on the internal auditing profession: What might have gone wrong? Managerial Auditing Journal, 27(6), 532–549. https://doi.org/10.1108/02686901211236382

- Masika, P. M. (2013). The effect of the quality of risk-based internal auditing on the effectiveness of internal audit in regulatory state corporations in Kenya. University of Nairobi.

- McCrudden, C. (2004). Using public procurement to achieve social outcomes. Natural Resources Forum, 28(4), 257–267. https://doi.org/10.1111/j.1477-8947.2004.00099.x

- Meehan, J., & Bryde, D. (2011). Sustainable procurement practice. Business Strategy and the Environment, 20(2), 94–106. https://doi.org/10.1002/bse.678

- Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83(2), 340–363. https://doi.org/10.1086/226550

- Mihret, D. G., & Woldeyohannis, G. Z. (2008). Value-added role of internal audit: An Ethiopian case study. Managerial Auditing Journal, 23(6), 567–595. https://doi.org/10.1108/02686900810882110

- Mihret, D., & Yismaw, A. (2007). Internal audit effectiveness: An Ethiopian public sector case study. Managerial Auditing Journal, 22(5), 470–484. https://doi.org/10.1108/02686900710750757

- Murungi, G. B., & Senelwa, W. A. (2019). Determinants of implementation of sustainable procurement practices in oil and gas sector in Kenya. (A case of Kenya pipeline). International Journal of Recent Research in Commerce Economics and Management, 6(4), 185–191.

- Mutchler, J. F. (2003). Independence and objectivity: A framework for research opportunities in internal auditing. The Institute of Internal Auditors.

- Nitzl, C., Roldán, J. L., & Cepeda Carrión, G. (2016). Mediation analysis in partial least squares path modeling: Helping researchers discuss more sophisticated models. Industrial Management & Data Systems, 119(9), 1849–1864. https://doi.org/10.1108/IMDS-07-2015-0302

- Nsiah-Asare, E., & Prempeh, K. B. (2016). Measures of ensuring VFM in public procurement: A case of selected polytechnics in Ghana. Munich Personal RePEc Archive.

- Ochieng, M. M., Oginda, M., & Oteki, B. E. (2016). Analysis of sustainable procurement practices and the extent of integration in Lake Victoria south water services board, Kenya. Journal of Business and Management, 18(3), 109–115.

- Onumah, J. M., & Yao Krah, R. (2012). Barriers and catalysts to effective internal audit in the Ghanaian public sector. In Accounting in Africa (pp. 177–207). Emerald Group Publishing Limited.https://doi.org/10.1108/S1479-3563(2012)000012A012

- Opiyo, P. (2015). VFM audits to ensure projects meet public expectations. Supreme Auditor. Feb - June, 3.

- Oyewobi, O. L., Ija, I. M., & Jimoh, A. R. (2017). Achieving sustainable procurement practices in the Nigerian construction industry: Examining potential barriers and strategies. ATBU Journal of Environmental Technology, 10(2), 63–84.

- Prier, E., Schwerin, E., & McCue, C. P. (2016). Implementation of sustainable public procurement practices and policies: A sorting framework. Journal of Public Procurement, 16(3), 312–346. https://doi.org/10.1108/JOPP-16-03-2016-B004

- Telgen, J., Harland, C., & Knight, L. (2007). Public procurement in perspective. In Public procurement: international cases and commentary (pp. 16–24). Routledge. https://doi.org/10.4324/NOE0415394048.ch2

- Wu, T. H., Huang, S. M., Huang, S. Y., & Yen, D. C. (2017). The effect of competencies, team problem-solving ability, and computer audit activity on internal audit performance. Information Systems Frontiers, 19(5), 1133–1148. https://doi.org/10.1007/s10796-015-9620-z

Appendix 1:

Survey Questionnaire

Demographics

Independence of IA

Indicate the extent to which you agree or disagree to these statements. There are five options to answer: Where 1 = strongly disagree; 2 = disagree; 3 = neutral; 4 = agree; 5 = strongly agree

Top management support

Indicate the extent to which you agree or disagree to these statements. There are five options to answer: Where 1 = strongly disagree; 2 = disagree; 3 = neutral; 4 = agree; 5 = strongly agree

Competency of internal audit

Indicate the extent to which you agree or disagree to these statements. There are five options to answer: Where 1 = strongly disagree; 2 = disagree; 3 = neutral; 4 = agree; 5 = strongly agree

External auditors role

Indicate the extent to which you agree or disagree to these statements. There are five options to answer: Where 1 = strongly disagree; 2 = disagree; 3 = neutral; 4 = agree; 5 = strongly agree

Internal audit effectiveness

Indicate the extent to which you agree or disagree to these statements. There are five options to answer: Where 1 = strongly disagree; 2 = disagree; 3 = neutral; 4 = agree; 5 = strongly agree

Sustainable procurement

Indicate the extent to which you agree or disagree to these statements. There are five options to answer: Where 1 = strongly disagree; 2 = disagree; 3 = neutral; 4 = agree; 5 = strongly agree

Value for money

Indicate the extent to which you agree or disagree to these statements. There are five options to answer: Where 1 = strongly disagree; 2 = disagree; 3 = neutral; 4 = agree; 5 = strongly agree