?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper provides the linkage between financial inclusion and welfare in Indonesia. This paper analyzes the level of financial inclusion Indonesian welfare using provincial data during 2015–2018. Index of Financial Inclusion (IFI) is calculated based on the dimensions of accessibility, availability, and usage of financial services. We employ the generalized least square (GLS) method for panel data estimation. Evidence showed that financial inclusion in Indonesia which mostly determined by the dimensions of the use and availability of financial services, while the accessibility dimension was relatively low in Indonesia. Based on the financial inclusion index, 25 provinces were grouped in the low financial inclusion, 8 provinces in the medium category and only DKI Jakarta Province categorized as high financial inclusion. The panel data estimation results show that the financial inclusion index has a positive and significant effect on the welfare of the Indonesian people as proxied by the human development index. The level of financial inclusion remains uneven between province in Indonesia. The lowest level of financial inclusion related to accessibility. The government should provide socialization and education of financial products to the public community, especially formal financial services such as banks. Financial literacy played an important role to improve welfare as a whole.

PUBLIC INTEREST STATEMENT

Financial inclusion has become an important topic to accelerate development in many countries. Several countries have showed that financial inclusion is related to community welfare. Evidence in Indonesia showed that financial inclusion was unevenly developed. Capitals such as DKI Jakarta were far more advanced than other regions in Indonesia. GLS showed that community welfare, which was proxied by Human Development Index (HDI), was positively related to FII. Thus, this paper suggested that Indonesia should improve FII to support HDI. The most important factor is to build accessibility of financial institutions such as Bank to society.

1. Introduction

Financial inclusion has been recognized as an important policy in many countries to accelerate development process (Bank Indonesia, Citation2019; Okello Candiya Bongomin et al., Citation2017). It is also believed that financial inclusion could help to achieve world’s sustainable development growths (SDGs) in several goals (Ofori-Abebrese et al., Citation2020). Empirical studies show a significant relationship between strengthening the financial sector, especially formal finance, with economic growth and improving people’s welfare (Chakrabarty & Mukherjee, Citation2021; Ratnawati, Citation2018). A good financial system may reduce information costs and transaction costs, increase capital allocation and asset liquidity, and can encourage investment in activities that have high added value (Beck et al., Citation2007; Levine, Citation1997).

The role of banking as an intermediary cannot be said to be successful when the availability of access and financial services is inadequate. This can be seen from the size of the financially excluded population. Financial exclusion signifies a lack of access to accurate, affordable, fair and secure financial products and services from service providers (Alonso et al., Citation2022; Ezzahid & Elouaourti, Citation2021). The causes of financial exclusion or the low use of formal financial products and services include limited access to products and services in the financial services sector, social-cultural society, and low levels of financial literacy (Otoritas Jasa Keuangan, Citation2016).

Financial inclusion is one of the characteristics of financial development that has received a lot of public attention. Financial inclusion, which is access to a variety of quality financial products and services, is an interesting topic for governments, researchers, and society in general (Domeher et al., Citation2022; Okello Candiya Bongomin et al., Citation2017). Currently, there is a large gap in financial inclusion worldwide, which presents challenges to achieving economic stability and development. The financial inclusion gap will result in differences in access to and use of financial products, inequality, poverty and low economic development (Cabeza-García et al., Citation2019; Duvendack & Mader, Citation2019). Formal financial inclusion begins with having a savings account or transaction at a bank or other financial service provider, with the aim of making and receiving payments and saving money. At a later stage, financial inclusion also involves access to credit from formal financial institutions, in addition to the use of insurance products that allow the public to reduce financial risk (Adrian & Mancini-Griffoli, Citation2019; Le et al., Citation2019).

Financial inclusion through intermediary groups such as women’s organizations is also gaining popularity in the community because it is believed to produce results in the form of financial profitability. In addition, because it is based on the spirit of gender equality and empowerment (Atiase et al., Citation2019; Swamy, Citation2014). Financial inclusion in some areas is driven through cooperative banks because they are considered an effective means for poverty alleviation, because cooperative financial access allows economic actors to carry out consumption activities, long-term investment, participation in productive activities and prevent unexpected economic shocks. This is because access to finance, especially by the poor, is a condition for employment, economic growth, poverty reduction and social cohesion, as it gives them the opportunity to have a bank account, to save and invest, to insure homes and to facilitate economic empowerment (Lal, Citation2018).

In general, the stage of financial development and the level of financial inclusion in a country are reflected in the ability of companies to access credit, the amount of collateral required for loans, and the ability of financial intermediaries to provide services at low costs. A more developed financial system is usually associated with a greater quantity of these three characteristics (Dabla-Norris et al., Citation2021).

The availability of financial services and ease of access are important aspects to increase the role of the financial sector and the involvement of the wider community in the economic system of a country. How big is the opportunity for the community to be able to access and use financial services can reflect the level of financial inclusion in an economy. Based on the results of surveys and research conducted by national and international institutions, it shows that financial inclusion in Indonesia is still relatively low compared to several countries in ASEAN. According to the global financial inclusion index created by the World Bank (Citation2015) it shows that only about 40 percent of Indonesians have access to formal financial institutions and this condition is still lower than Thailand and Malaysia which almost reached 80 percent.

The results of survey conducted by Indonesian Financial Services (Otoritas Jasa Keuangan, Citation2016) were quite encouraging, where the level of financial literacy increased from 21.84 percent in 2013 to 29.66 percent in 2016. Meanwhile, the level of financial inclusion also improved from 59.74 percent to 67.82 percent in 2016, the same period. This shows that financial inclusiveness in Indonesia is still low and mutually supportive that Indonesian people’s financial access to formal financial institutions is still relatively low so that the Indonesian population still has limited access to the financial service system. Therefore, considering the very important role of financial inclusion as an effort to accelerate the process of economic development in Indonesia, studies related to financial inclusion and its impact on community welfare are interesting to study.

2. Literature review

Financial inclusion refers to the access and use of quality, sustainable, and secure financial services by all economic actors in the community. Financial services may include a variety of products and services provided by banks and other financial institutions, including bank accounts, credit cards, ATM services, loans, and other forms of credit (Ezzahid & Elouaourti, Citation2021). A country is said to be financially inclusive when most of its population has access to these financial products. Financial inclusion can contribute to greater socioeconomic equity by reducing poverty and enabling the development of financial services and infrastructure. On the other hand, financial exclusion may result in lower investment in the economy due to the difficulty of accessing credit (Cabeza-García et al., Citation2019; Le et al., Citation2019).

Financial inclusion aims to provide public access to receive benefits from financial institutions. Ensuring that the financial system plays its part in promoting inclusive growth is one of the biggest challenges facing developing countries. Access to a well-functioning financial system enables economically marginalized people to better integrate and actively contribute to development (Swamy, Citation2014).

According to Ozili (Citation2020), financial inclusion by holding an account at a formal financial institution can be used for multiple purposes and will bring many benefits to individuals, businesses, and the economy. The importance of financial inclusion and its global spread revolve around the benefits of bringing the left-behind poor into the formal financial system. It helps reduce poverty and inequality by helping people invest in the future, improve consumption and better manage financial risk.

Financial inclusion is both pro-poor and pro-growth because it plays a role in helping low-income households to access basic financial services such as savings, credit and insurance, which can encourage financial independence. Financial inclusion can also be understood as a process of understanding the poor, their lives, their needs, their efficiency and powerlessness. So to involve the poor in participating in the country’s economic growth, they need to be given the opportunity to access various financial services (Lal, Citation2018).

Several meta-analyses-based studies have attempted to describe the impact of financial inclusion on the poor in low- and middle-income countries (Duvendack & Mader, Citation2019). Countries with low GDP per capita, high levels of income inequality, low literacy rates, low urbanization, and poor connectivity tend to be less financially inclusive. Meanwhile, countries with larger financial inclusion systems grow faster than those without (Atiase et al., Citation2019; Dabla-Norris et al., Citation2021).

Kumari (Citation2022) conducted research in several regions in India, which suggested that there was a positive correlation between financial inclusion and human development. Therefore, financial inclusion is an important driver for economic development through access to and use of the formal financial system, and contributes to human development. Moreover, it contributes to the economic development of India.

Ofori-Abebrese et al. (Citation2020) conducted a study on the impact of financial inclusion on people’s welfare in 33 countries. The results of his research state that there is a positive relationship between financial inclusion and welfare for certain countries. It is an obligation for stakeholders in the financial industry to ensure the availability of credit and expansion of ATM facilities, among others, to promote greater financial inclusion in the sub-region. Nonetheless, firm action must be taken to ensure that credit extended to potential borrowers is recoverable so as not to exacerbate the high incidence of default and non-performing loans. This is because, loan defaults and high non-performing loans have a tendency to bankrupt financial institutions and ultimately lead to bank failures which will further worsen individual welfare. The presence of wide cellular coverage and smartphones provide very broad access that can provide access to financial services electronically.

Financial inclusion has become a national strategy to encourage economic growth through equitable income distribution, poverty reduction, and financial system stability to Indonesian policy (Addury, Citation2019; Bank Indonesia, Citation2019; OJK, Citation2017). The right of every individual is guaranteed to be able to access the entire scope of quality financial services at an affordable cost. The target of this policy is to pay close attention to the low-income poor, the productive poor, migrant workers, and people living in remote areas (Bank Indonesia, Citation2019).

Financial inclusion is defined as all efforts to increase public access to financial services by eliminating all forms of barriers, both price and non-price. Study revealed that financial inclusion is an effort to incorporate the unbanked into the formal financial system so that they have the opportunity to enjoy financial services such as savings, payments, and transfers (Hannig & Jansen, Citation2010). In addition, Sarma (Citation2012) stated that financial inclusion is a process that ensures easy access, availability, and benefits from the formal financial system for all economic actors. So it can be concluded that financial inclusion is an effort to increase public access, especially the unbanked, to formal financial services by reducing various kinds of barriers to accessing them.

Previous study showed that financial inclusion in addition to being able to overcome income inequality also has the potential to increase financial stability (Hannig & Jansen, Citation2010). Poor people’s access to savings from formal financial institutions can increase household capacity in managing financial vulnerabilities caused by the adverse effects of the crisis, diversify the funding base of financial institutions that can reduce shocks during the global crisis, increase economic resilience by accelerating growth, diversification, and reducing poverty.

Meanwhile, related to research on the impact of financial inclusion on development, Sarma and Pais (Citation2008) used the OLS method and the results of their study found that the level of human development and financial inclusion had a positive relationship for several countries in the world. While the results of the study of (Gupta et al., Citation2014) which measured the Index for Financial Inclusion (IFI) in 28 states and 6 regions in India using the dimensions of penetration, availability and usage of banking services empirically found that the financial inclusion index and the human development index as a proxy for public welfare in India have positive correlation.

3. Research methodology

3.1. Research data and variables

This study uses secondary data with panel data types during the 2015–2018 period in 34 provinces in Indonesia sourced from the Central Statistics Agency (BPS), the Financial Services Authority (OJK), and Bank Indonesia (BI). This study uses the Financial Inclusion Index (FII) method developed by Sarma (Sarma, Citation2012) in analyzing and measuring financial inclusion in Indonesia. The research variables used refer to the FII measurement dimensions, namely accessibility (d1), availability (d2), and use (d3). As for the analysis of the impact of financial inclusion on welfare as proxied by the human development index (HDI), this study uses several variables as control variables, namely the number of poor people (PP) and population density (PD). For operational definitions of all these variables are summarized in .

Table 1. Definition of operational variables and research indicators

3.2 Analysis method

This study adopts the measurement of Financial Inclusion Index (FII) developed by Sarma (Sarma, Citation2012), where to calculate the financial inclusion index (IIK) using three dimensions, namely accessibility (d1), availability (d2), and use (d3). The accessibility indicator describes the penetration of formal financial institutions and the availability indicator is indicated by the number of banking branches. Meanwhile, usage indicators include the volume of credit disbursed by banks to the public. This method is used because it provides comprehensive measurements that are robust and can be compared between provinces.

Furthermore, this study also uses panel data to see the effect of financial inclusion on people’s welfare as proxied by the human development index and the estimation method used is Generalized Least Square (GLS). The specifications of the research model were formulated as follow:

where HDI is the human development index, FII is the financial inclusion index, PP is the number of poor people, and PD is population density.

In order to validate the use of GLS instead of pooled ordinary least square, we employ Breusch–Pagan Langrange multiplier test. If the null hypothesis (H0) is accepted, then the model used is the pooled ordinary least square through common effect model (CEM), and conversely if the null hypothesis (H0) is rejected, then the best model is panel data regression through GLS. The GLS method can be analyzed through two models, namely the fixed effects model (FEM) and the random effects model (REM). Furthermore, from the two models, the best model was chosen by conducting the Hausman test (Beyaztas et al., Citation2021; Hausman, Citation1978), where the provisions are that if the null hypothesis (H0) is accepted, then the model used is the random effect model (REM) and vice versa if the null hypothesis (H0) is rejected, then the model used is the fixed effect model (FEM). To process the data in this study, the Eviews version 10 program was used.

4. Results and discussion

4.1. Financial Inclusion Index (FII) in Indonesia

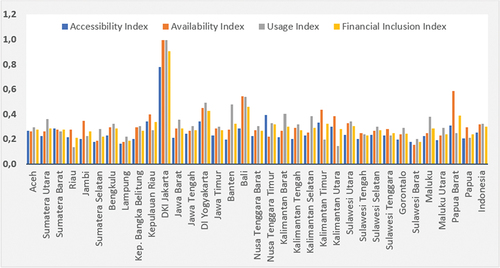

Based on the average value of the financial inclusion index (FII), Indonesia is included in the category of moderate financial inclusion because it has an average value of the financial inclusion index above 0.3 during the study period. For the grouping between provinces in Indonesia, there are 25 provinces that fall into the category of low financial inclusion (index value below 0.3). Meanwhile, there are 8 provinces that fall into the category of medium or medium financial inclusion (index value between 0.3 and 0.6) and only DKI Jakarta Province which is included in the category of high financial inclusion (index value above 0.6 which is 0.9052).

Provinces that fall into category of medium financial inclusion index category are the Riau Islands Province, DI Yogyakarta, Banten, Bali, East Nusa Tenggara, East Kalimantan, North Sulawesi, and West Papua Province. While the provinces that are included in the low financial inclusion category are 25 provinces with the lowest financial inclusion index values occurring in West Sulawesi Province (0.1782) and Lampung Province (0.1884).

The relatively low financial inclusion index in Indonesia shows that the distribution and utilization of banking services is still low as shown in . Likewise, the difference in the financial inclusion index between provinces in Indonesia also shows that there is still inequality or inequality in access to banking services between provinces. This condition occurs in the provinces of Banten, Bali, and North Sulawesi which have relatively high financial inclusion index (FII) values but relatively low accessibility dimension index (ADI) values. This indicates that there are still barriers for the community in the three provinces in terms of accessing banking institutions, even though the availability and use of banking services is relatively high.

Figure 1. Average Financial Inclusion Index (FII) in Indonesia.

Meanwhile, there are also several provinces that have relatively high financial inclusion index (FII) values but relatively low usage dimension index (UDI) values. This condition occurs in the Provinces of the Riau Islands, East Kalimantan, and West Papua which indicates that the utilization and use of banking services is not yet optimal, even though the accessibility and availability of banking services is relatively good. This is possible because in the three provinces the number of adults who have accessed and used banking services is relatively small but tends to have more than 1 bank account.

In addition, it was also found that the province has a relatively high financial inclusion index value but the value of the availability dimension index (ADI) of banking services is relatively low and this occurs in the Province of Nusa Tenggara Timur (NTT). These findings indicate that the province of East Nusa Tenggara is still facing the problem of the limited presence of bank branch offices in the region.

However, there are two provinces that have financial inclusion index values and dimension indexes that tend to be relatively evenly distributed, namely DKI Jakarta Province and DI Yogyakarta Province. This shows that the people in the two provinces already have a level of financial inclusion that tends to be evenly distributed, both in terms of the accessibility dimension, the availability dimension and the dimension of the use of banking services during the 2015–2018 study period. On the other hand, provinces that have an inclusion index value, relatively low financial and dimensional index occurred in Lampung Province and West Sulawesi Province. These findings indicate that people in these two provinces still experience obstacles to accessing and utilizing and using banking services in the area.

Based on these findings, it shows that on average the dimensions of banking availability tend to be higher than the dimensions of accessibility or banking penetration. This means that the number of bank branch offices is relatively large, but the number of adults with accounts is still very low. The low accessibility or penetration of banking may be possible even though banks do not have many customers, but relatively few customers carry out transactions with relatively large volumes. The size of the transaction volume can be seen from the dimensions of use which tend to be large.

In addition to availability, accessibility and penetration of financial services also need to be improved because it can not only increase economic growth, but also reduce poverty and income inequality, so that countries with a larger and more accessible number of financial institutions tend to grow faster (Lal, Citation2018). The existence of financial services such as banking that collaborates with each other can form an inclusive financial system while still taking into account the three core dimensions of financial inclusion, namely banking availability, banking penetration and the level of use of banking services (Le et al., Citation2019).

In addition, these findings also prove the low value of the accessibility dimension, but the high value of the availability dimension and the use dimension indicate that the community has not utilized it optimally to use formal financial services as the main source of financing. People are more likely to use informal financial services, such as cooperatives and moneylenders, rather than formal banking facilities. The dominant role of non-formal financial institutions in Indonesia, especially in remote areas, shows that the formal financial market in Indonesia is not functioning properly.

4.2. Data estimation results

First, we employ Breusch–Pagan Lagrange Multiplier test to select either to employ the pooled ordinary least square or the panel data regression model. The result of Lagrange test showed in .

Table 2. Lagrange multiplier test

shows that we reject the null hypothesis, thus we used panel data regression to evaluate the linkage between FII and HDI. To evaluate the effect of financial inclusion on people’s welfare as proxied by the human development index (HDI), an estimate was made for panel data using the Generalized Least Squares (GLS) method. The following are the estimation results using the GLS method for the fixed effect model (FEM) and random effect model (REM) as shown in the following .

Table 3. Estimation results with the GLS method

Furthermore, to choose the best statistically between the FEM and REM models for the Generalized Least Square (GLS) method, the Hausman test can be done (Gujarati, Citation2008) and the results can be seen based on the chi-square value as shown in .

Table 4. Hausman test for FEM vs REM

Based on the results of the Hausman test above, the chi-square value is 149.139 with a prob value of 0.0000 which means that the null hypothesis (H0) is rejected, then the best model in this study is the fixed effects model (FEM). From the estimation results with the FEM model as shown in , it shows that the coefficient of determination (R2) is 0.9914, which means that overall the independent variables in the model (FII, PP, PD) are quite able to explain the variation in community welfare (IPM) in Indonesia of 99.14 percent and the rest is explained by other variables not included in the equation model.

Table 5. Estimated results with Fixed Effects Model (FEM)

The estimation results show that the financial inclusion index (FII) has a positive and significant impact on the level of community welfare (IPM) in Indonesia at the 99% confidence level. The coefficient value is 0.089 which indicates that every time there is an increase in the financial inclusion index in Indonesia by 1 point, ceteris paribus, it will increase the welfare of the Indonesian people by 0.089 points. These empirical results support a study, where the level of human development and financial inclusion has a positive relationship for several countries in the world (Sarma & Pais, Citation2008). Likewise, the results of research conducted where the financial inclusion index and the human development index as a proxy for public welfare in India have a positive relationship or correlation (Gupta et al., Citation2014).

The results of the estimation of the number of poor people (PP) show a negative and significant effect on the level of community welfare (HDI) in Indonesia at the 99% confidence level. The coefficient value of 0.037 means that every 1 percent increase in the number of poor people in Indonesia, ceteris paribus, will cause the welfare level of the Indonesian people to decrease by 0.037 points. Meanwhile, the population density variable (PD) has a positive and significant effect on the level of community welfare (HDI) in Indonesia at the 99% confidence level. The coefficient value of 0.385 indicates that every time there is an increase in population density in Indonesia by 1 point, ceteris paribus, it will result in an increase in the welfare of the Indonesian people by 0.385 points. The estimation results are not in line with the hypothesis which states that there is a negative and significant effect between population density and the level of community welfare in Indonesia.

Financial inclusion is one of the effective means in overcoming the problems of poverty, unemployment, inequality and poor community welfare. This is because, through financial inclusion, access to basic financial services, such as savings, loans, insurance, credit, and others can have a positive impact on the lives of the poor and help them become more empowered (Lal, Citation2018). Several previous studies have shown that there is a better change in the level of welfare after the implementation of financial inclusion policies than before the policy was implemented (Dabla-Norris et al., Citation2021).

Financial inclusion programs such as improving access to financial services including credit, savings, insurance and money transfers enable poor people in low- and middle-income countries to improve their welfare, take advantage of opportunities, reduce shocks, and ultimately escape poverty (Duvendack & Mader, Citation2019). Evidence in Indonesia showed that financial inclusion were not evenly distributed. Only DKI Jakarta Province as capital of Indonesia was far more advanced than other regions. In rural area of Indonesia for example, such equipmet as electronic data capture (EDC) was rarely seen to support availability, access and usage of financial institution.

5. Conclusions and reccommendation

The results of this study indicate that Indonesia is included in the medium financial inclusion index category during the study period. In general, financial inclusion in Indonesia tends to be determined by the dimensions of use and availability, while the accessibility dimension has a relatively smaller proportion. The large proportion of the dimensions of use in supporting financial inclusion in Indonesia is indicated by the ability of the public to utilize and use banking services as savings and sources of financing.

For the availability dimension, it can be indicated by the increasing number of banking branch offices in the area, but the existence of these branch offices has not been able to serve all the people in the area. This condition causes the accessibility dimension to have a lower index value than other dimensions and this accessibility limitation makes many people still unable to access banking due to geographical barriers in Indonesia as an archipelagic country so that the cost of establishing branch offices is relatively expensive.

Furthermore, based on the results of panel data estimation, it shows that the financial inclusion index variable (FII) has a positive and significant effect on the level of community welfare as proxied by the human development index (HDI). Likewise, the population density variable (PD) has a positive and significant effect on the level of community welfare in Indonesia. While the variable number of poor people (PP) has a negative and significant effect on the level of welfare of the people in Indonesia during the study period.

Community welfare (HDI) can be improved significantly by furnishing Indonesian Financial Inclusion. FII can be improved through a better access to financial institution, more avaliablity financial services and more usage of financial institution. Our finding showed that Indonesian people access to financial institution relatively low. People's knowledge related to financial products needs to be improved. The government should provide socialization related to financial products to the public, especially from formal financial services such as Bank. People should be bankable. The socialization aims to provide an understanding of existing financial products, how to obtain them, and the benefits of these financial products, as well as to increase public awareness of using financial services.

The public in general did not want a difficult process to obtain access to financial services. Thus, providing an easy access to financial services is the right recommendation to improve increased financial inclusion. Ease access can be done by providing financial services, especially digital banking so that people do not need to go to the physical location of the bank, but can access it non-physically or digitally. The recommendation also help to reduce the cost of opening new branches.

6. Limitation and future research

This study only gives evidence of Indonesia based on secondary data sources. Our result should not be generalized to the whole South East Asia or the world. Thus, we would like to evaluate more evidence to support our findings of linkage between financial inclusion and community welfare.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Paidi Hidayat

Paidi Hidayat, S.E., M.Si., is currently working as lecturer at Department of Economics Development, Faculty of Economics and Business Universitas Sumatera Utara.

Raina Linda Sari

Raina Linda Sari S.E., M.Si., is a lecturer at Department of Economics Development, Faculty of Economics and Business Universitas Sumatera Utara.

References

- Addury, M. M. (2019). Impact of financial inclusion for welfare: Analyze to household level. Journal of Finance and Islamic Banking, 1(2), 90. https://doi.org/10.22515/jfib.v1i2.1450

- Adrian, T., & Mancini-Griffoli, T. (2019). The Rise of Digital Money. IMF FinTech Notes Note/19/01. Washington: International Monetary Fund.

- Alonso, S. L. N., Jorge-Vazquez, J., Forradellas, R. F. R., & Dochado, E. A. (2022). Solutions to financial exclusion in rural and depopulated areas: Evidence Based in Castilla y León (Spain). Land, 111, 74. https://doi.org/10.3390/land11010074

- Atiase, V. Y., Wang, Y., & Mahmood, S. (2019). FNGOs and financial inclusion: Investigating the impact of microcredit on employment growth in Ghana. International Journal of Entrepreneurship and Innovation, 20(2), 90–12. https://doi.org/10.1177/1465750319832478

- Bank Indonesia. (2019). Bank Indonesia, 1–49. https://www.bi.go.id/…/Indonesia-Payment-Systems-Blueprint-2025-Presentation.pdf

- Beck, T., Demirgüç-Kunt, A., & Levine, R. (2007). Finance, inequality and the poor. Journal of Economic Growth, 12(1), 27–49. https://doi.org/10.1007/s10887-007-9010-6

- Beyaztas, B. H., Bandyopadhyay, S., & Mandal, A. (2021). arXiv, 1–21. http://arxiv.org/abs/2104.07723

- Cabeza-García, L., Del Brio, E. B., & Oscanoa-Victorio, M. L. (2019). Female financial inclusion and its impacts on inclusive economic development. Women’s Studies International Forum, 77(October2018), 102300. https://doi.org/10.1016/j.wsif.2019.102300

- Chakrabarty, M., & Mukherjee, S. (2021). Financial inclusion and household welfare: An entropy-based consumption diversification approach. European Journal of Development Research, 34(3), 1486–1521. https://doi.org/10.1057/s41287-021-00431-y

- Dabla-Norris, E., Ji, Y., Townsend, R. M., & Filiz Unsal, D. (2021). Distinguishing constraints on financial inclusion and their impact on GDP, TFP, and the distribution of income. Journal of Monetary Economics, 117(1), 1–18. https://doi.org/10.1016/j.jmoneco.2020.01.003

- Domeher, D., Konadu-Yiadom, E., & Aawaar, G. (2022). Financial innovations and economic growth: Does financial inclusion play a mediating role? Cogent Business and Management, 9(1), 1. https://doi.org/10.1080/23311975.2022.2049670

- Duvendack, M., & Mader, P. (2019). Impact of financial inclusion in low‐ and middle‐income countries: A systematic review of reviews. Campbell Systematic Reviews, 15(1–2), 1–2. https://doi.org/10.4073/csr.2019.2

- Ezzahid, E., & Elouaourti, Z. (2021). Financial inclusion, mobile banking, informal finance and financial exclusion: Micro-level evidence from Morocco. International Journal of Social Economics, 48(7), 1060–1086. https://doi.org/10.1108/IJSE-11–2020-0747

- Gujarati, D. N. (2008). Basics of Econometrics. Jakarta: Erlangga.

- Gupta, A., Chotia, V., & Rao, N. M. (2014). Financial inclusion and human development: A state-wise analysis from India. International Journal of Economics, Commerce and Management, 2(5), 1–23. https://doi.org/10.37385/ijedr.v3i1.361

- Hannig, A., & Jansen, S. (2010). Tokyo: Asian Development Bank Institute. https://doi.org/10.2139/ssrn.1729122

- Hausman, J. A. (1978). Specification tests in econometrics. Econometrica, 46(6), 1251–1271. https://doi.org/10.2307/1913827

- Kumari, M. (2022). Financial inclusion and human development in India: An inter-state analysis. International Journal of Economics Development Research (IJEDR), 3(1), 1–12. https://doi.org/10.37385/ijedr.v3i1.361

- Lal, T. (2018). Impact of financial inclusion on poverty alleviation through cooperative banks. International Journal of Social Economics, 45(5), 807–827. https://doi.org/10.1108/IJSE-05-2017-0194

- Le, T. H., Chuc, A. T., & Taghizadeh-Hesary, F. (2019). Financial inclusion and its impact on financial efficiency and sustainability: Empirical evidence from Asia. Borsa Istanbul Review, 19(4), 310–322. https://doi.org/10.1016/j.bir.2019.07.002

- Levine, R. (1997). Financial development and economic growth: Views and agenda. Journal of Economic Literature, 35(2), 688–726. https://www.jstor.org/stable/2729790

- Ofori-Abebrese, G., Baidoo, S. T., & Essiam, E. (2020). Estimating the effects of financial inclusion on welfare in sub-Saharan Africa. Cogent Business and Management, 7(1), 1. https://doi.org/10.1080/23311975.2020.1839164

- OJK. (2017). Strategi Nasional Literasi Keuangan Indonesia (Revisit 2017). Otoritas Jasa Keuangan.

- Okello Candiya Bongomin, G., Munene, J. C., Ntayi Mpeera, J., & Malinga Akol, C. (2017). Financial inclusion in rural Uganda: The role of social capital and generational values. Cogent Business and Management, 4(1), 1302866. https://doi.org/10.1080/23311975.2017.1302866

- Otoritas Jasa Keuangan. (2016). Survey Nasional Literasi dan Inklusi Keuangan 2016. OJK.

- Ozili, P. K. (2020). Optimal Financial Inclusion. In B. N. Jeon & J. Wu (Eds.), Emerging Market Finance: New Challenges and Opportunities (Vol. 21, pp. 251–260). Emerald Publishing Limited. https://doi.org/10.1108/S1569-376720200000021014

- Ratnawati, T. (2018). Financial inclusion strategy to increase the welfare of regional community industry in Gresik regency of east Java. Archives of Business Research, 6(7), 86–93. https://doi.org/10.14738/abr.67.4859

- Sarma, M., & Pais, J. (2008). Financial inclusion and development: A cross country analysis. In Annual Conference of the Human Development and Capability Association, New Delhi, 168( 10–13), 1–30. https://doi.org/10.1002/jid

- Sarma, M. Competence Center “Money, Finance, Trade and Development“. (2012). Index of financial inclusion – A measure of financial sector. Berlin Working Papers on Money, Finance, Trade and Development Working.

- Swamy, V. (2014). Financial inclusion, gender dimension, and economic impact on poor households. World Development, 56(April), 1–15. https://doi.org/10.1016/j.worlddev.2013.10.019

- World Bank. (2015). Data from: Financial Inclusion Data / FINDEX. https://datatopics.worldbank.org/financialinclusion/country/indonesia