Abstract

Based primarily on agency theory, this study aims to examine the role of internal and external supervisory mechanisms in improving financial reporting quality by public non-business units in Vietnam. Quantitative research with a survey method was carried out on a sample of 362 public non-business units in Ha Noi, Da Nang, and Ho Chi Minh City, Vietnam. The data collection period spread from March to May 2021. The research hypotheses were tested by PLS-SEM. The research results show that all three factors independent audit, internal control effectiveness, and financial inspection frequency had positive impacts on the financial reporting quality; internal control effectiveness has a mediating role in the relationship between independent audit, financial inspection frequency, and financial reporting quality. This study is the first to examine the chain from independent audit, financial inspection frequency, internal control effectiveness, and financial reporting quality in the context of public non-business units in an emerging economy. Furthermore, the study is the basis for setting policies and regulations to improve financial reporting quality in public non-business units.

PUBLIC INTEREST STATEMENT

The current financial autonomy mechanism has required public entities to focus on quality and operational efficiency. Quality financial reporting information will help these units have many advantages in raising capital, investment, and increasing public confidence, thereby contributing to increasing operational efficiency of the unit. This study aims to understand the role of supervisory mechanism in improving the quality of financial reporting. Research results show that State agencies, independent audit and the effectiveness of internal control play important roles in ensuring financial reporting quality. We have proposed solutions from the supervisory mechanism to improve financial reporting quality in Vietnam public non-business units.

1. Introduction

The public sector plays an important role in every economy (Tran et al., Citation2021). Some experts and researchers highlight the creative and community-serving roles of public institutions, such as the public sector plays an active and stimulating role in the development and innovation of new industries and infrastructure (Burgmeijer, Citation2005); promotes knowledge sharing for the public interest (Chen & Hsieh, Citation2015). To most countries, public non-business units (PNUs) are seen as the main category that constitutes a system of public sector entities. PNUs are established and operate mainly on the state budget to perform the task of providing essential public services directly related to daily public life. Therefore, improving the quality and operational performance of PNUs is essential to maintain a key role in the transitional economy and ensure political-social stability. Many previous studies have demonstrated the essential role of the quality of financial information in decision-making and increasing operational performance. Financial reporting (FR) with high quality provides a transparent format to support the government’s public accountability in managing public resources (Steccolini, Citation2004); helps managers have more useful sources for their decision making to improve the performance of public entities (Tran et al., Citation2021); contributes to reducing corruption and increasing the operational performance of public organizations (Cuadrado-Ballesteros et al., Citation2019).

As can be seen, FRQ has always been a topic of interest to organizations in both the private and public sectors. However, the necessary question is what mechanisms and policies should be implemented to increase FRQ in public entities? Based on agency theory, previous private-sector studies have explained the role of internal and external supervisory mechanisms in ensuring FRQ. Krambia-Kapardis et al. (Citation2016), Pham et al. (Citation2021) argue that in the context of asymmetric information, the exploitation of accounting tools for self-interested behaviors on the leaders’ sides will be limited by the implementation of internal monitoring mechanisms of the enterprise. From these, the authors have argued the relationship between internal control and FRQ. Djama (Citation2010); Pham et al. (Citation2021) believe that the interests conflict resolution of stakeholders within the enterprise has led to the establishment of an internal and external control system as a mechanism to frame the actions of managers and minimize the costs arising from these conflicts. Based on this theoretical background, the above researchers have confirmed the role of independent audit (INA) and government agencies for FRQ. The relationship between supervisory mechanism and FRQ is also explained by institutional theory and contingency theory. Meyer and Rowan (Citation1977) argue that institution is a major determinant of an organization. Under external and internal pressure, the organization is forced to adhere to a set of expectations for achieving legitimacy so that the organization can survive in the long run. Applying this theory, Yến (Citation2021) argues that under the pressure of financial autonomy, public entities will have to make many changes to adapt, including improving FRQ. Therefore, organizations such as external audit companies and state agencies play their roles in forming a supervisory mechanism to help the entity increase FRQ. Thuan (Citation2022) on the basis of reviewing previous studies has concluded that contingency theory is widely applied to argue the role of contextual factors in the performance of entities. The author uses this theory to argue the relationship between factors in the internal and external environment (ICE, INA) and FRQ. Unlike research in the private sector, studies on the role of supervisory mechanisms for FRQ in public institutions are still very limited. Specifically, almost no studies have researched the role of INA in improving FRQ. This is explained as state agencies are the main users of accounting information of public institutions. Therefore, the need for financial statement audits by independent auditors for these organizations is almost very low. However, with the current financial autonomy mechanism implemented by many countries, PNUs have full rights in borrowing and mobilizing capital to ensure their operational efficiency. The question is then: do PNUs need an independent audit to help increase the FR reliability and quality?

Stemming from the above, we conclude that although FRQ plays an important role in operational efficiency and decision-making in public organizations, research on FRQ, especially on the FRQ increasing mechanism, is still very limited, not commensurate with its role in the economy and society. Besides, according to the World Bank 2017 report, a fraud survey conducted globally in 2016 by the Association of Certified Fraud Examiners found that government and the public sector are the represented second-largest areas after the banking and financial services industry. These frauds are broadly related to accounting frauds, including accounting or reporting manipulations. This has posed the need to learn more about the nature of FRQ in these units with a specific theoretical background.

This study applies agency theory, institutional theory, and contingency theory to develop the research model, specifically, explores the impact of internal and external monitoring mechanisms on ensuring FRQ in public entities. This study tests the direct effect of INA, FIF (financial inspection frequency), and ICE on FRQ and the indirect impact of INA and FIF on FRQ through ICE. The subjects of this study are PNUs, a common type of public organization that is strongly influenced by the innovation of financial mechanisms and accounting policy.

To our best knowledge, this research is the first to examine the chain from INA, FIF, ICE, and FRQ. It contributes to existing research on the FRQ in several aspects. Firstly, this study determines how to measure FRQ for public sector entities on the basis of full reference of components and qualitative characteristics identified by IPSASB Citation2013. Secondly, this study clarifies the role of INA and state inspection in improving ICE; provides empirical evidence on the influence of INA, state inspection, and ICE on FRQ in the public sector. Thirdly, this study explains the mediating role of ICE in the relationship between the INA, FIF, and FRQ. Furthermore, the study also explores improving ICE, enhancing state inspection, and performing audits of financial statements by INA as mechanisms for improving FRQ of the public sector in an emerging country like Vietnam; an effective internal control system will contribute to increasing the impact of INA and FIF on FRQ.

2. Literature review, theoretical framework and hypothesis

2.1. Institutional background

Public non-business units are organizations providing public services, serving state management in fields such as education, training, health care, scientific research, culture, physical training, and sports … With its role and importance, the quality and performance of PNUs have always been prime concerns of the government. In countries of emerging economies like Vietnam, the reform of financial mechanisms and accounting policy in public entities is impressively taking place and is considered the main solution to improve the quality and operational efficiency of the PNUs. In Vietnam, the Government Decree No. 16/2015/ND-CP stipulating the autonomy mechanism of PNUs is considered a breakthrough in the comprehensive reform roadmap of restructuring PNUs, aiming to increase PNUs’ autonomy and self-responsibility. This mechanism requires the entity to focus frequently on operational efficiency, considers it as one of the vital conditions of the entity, and subsequently emphasizes the role of accounting information. Financial statements in PNUs must be aimed at serving the accountability of the units and making decisions for users such as citizens, donors, and creditors. With the diversity of users of financial reporting information when implementing financial autonomy, questions for PNUs are whether information users have complete confidence in FR audited only by the state agencies or not? And, is INA necessary for FRQ enhancement of PNUs?

The role of internal control over FR is drawing strong attention from legislators and regulators following a series of financial scandals such as Enron and WorldCom. Most recent legislation emphasizes the link between ICE and the risk reduction of FR information. (Section 404 the Sarbanes—Oxley of the United States; Directive 2006/46 /EC in Europe …). In Viet Nam, Vietnam Accounting Law 2015 also requires accounting units to establish and operate an effective internal control system to ensure that the entity’s assets are safe, and not used for improper or ineffective purposes; transactions are approved with proper authority and are fully recorded as the basis for the preparation and presentation of true and fair financial statements. The current situation shows that the implementation of the above requirements is still difficult due to many reasons: inadequate attention from the unit leaders to the role of internal control; inappropriate number of personnel in the internal audit department comparing with the scale of operation; non-comprehensive content of the inspection leads to violations have not been prevented in time. In addition, the State has not yet issued specific regulations for the inspection, supervision and assessment of the compliance level of the units about assuring ICE. On that basis, we believe that studying the relationship between ICE and FRQ in PNUs is really necessary for state agencies to perfect the regulations on inspection and supervision of the implementation of internal control at PNUs; and for leaders at PNUs to ensure ICE rightfully in order to increase the entity’s operational efficiency at the same time.

Thus, along with the traditional role of state agencies, the above regulations have formed an important institutional foundation for us to propose a mechanism to inspect and supervise FRQ from state agencies, INA, and IC for this study.

2.2. FRQ

According to IASB (Citation2010), information quality is interpreted as the characteristics that make the information presented on the financial statements useful to the users of the information, including two fundamental attributes (relevant, faithful representation) and enhancing attributes (comparable, verifiability, timely, understandable). For the public sector, in 2006, the IASB issued IPSAS1 and outlined four key quality attributes of financial statements including understandability, relevance, reliability, and comparability. In 2013, IPSASB released The Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities, which outlined six qualitative characteristics including relevance, faithful representation, understandability, timeliness, comparability, and verifiability (IPSASB, Citation2013).

For studies in the field of accounting, the qualitative characteristics of IASB and IPSAS are considered as the main foundation for measuring FRQ. Bellanca and Vandernoot (Citation2014) in a study investigating the use of IPSAS by countries in the European Union found that the use of IPSAS will help increase transparency, clarity, and comparability of FR in the public sector of Europe and around the world. Based on IPSAS1 and Government Accounting Standards, the FRQ scale of Suwanda (Citation2015) has been built, including 4 components: relevance, reliability, understandability, and comparability. Tran Citation2021 bases on IPSASB Citation2013, measures FRQ in public organizations with 14 items. In a study aimed at measuring FRQ in enterprises in Vietnam, Pham et al. (Citation2021) measure FRQ in enterprises in Vietnam. Based on the point of view of IASB Citation2010, the FRQ scale of Pham et al. (Citation2021) is a third-order construct with three second-order dimensions: relevance, faithful representation, and enhancing qualitative characteristics.

Thus, in terms of content, the qualitative characteristics of FR applicable to businesses (according to IASB, Citation2010) and public sector entities (according to IPSASB, Citation2013) all include the following components: relevance, faithful representation, understandability, timeliness, comparability, and verifiability. However, in essence, there is a significant difference between IASB Citation2010 and IPSASB Citation2013. Specifically, IASB Citation2010 divides qualitative characteristics into three components: relevance, faithful representation, and enhancing qualitative characteristics (understandability, timeliness, comparability verifiability). Although there is no difference in the content of qualitative characteristics between IASB Citation2010 and IPSASB Citation2013, the measurement of FRQ between research targeting public sector entities and enterprises still has differences. For studies targeting enterprises, the FRQ attributes are considered quite adequate according to the guidelines of the 2010 IASB. Meanwhile, studies targeting public sector entities often measure FRQ on the reference of IPSAS1 and have not been updated according to the provisions of IPSASB Citation2013. Limitations of previous research on FRQ measurement in PNUs could be explained that the qualitative characteristics of IPSAS1 are much simpler than the qualitative characteristics of IPSASB Citation2013. Besides, the studies of FRQ measurement in public sector entities have just been paid attention to recently.

In summary, this study aims to measure FRQ based on full reference to the attributes of IPSASB Citation2013.

2.3. ICE and FRQ

Stemming from financial scandals that are increasingly common in the world, the role of internal control in the FRQ is increasingly emphasized. The 2015 Vietnamese Accounting Law requires accounting firms to establish an internal control system for their divisions as a basis for the preparation and presentation of true and fair financial statements. In the context of the public sector, researches on the relationship between internal control and FRQ have drawn interest from many scientists. Several empirical studies have shown that internal control is fundamental to the usefulness of financial information for decision-making. Hevesi (Citation2005) concludes that one of the reasons for the unreliability of FR originates from the internal control system in the organization. Yamamoto (Citation2008) analyzes the factors determining the relationship between the use and usefulness of financial information for the decision-making process of politicians in Japanese central and local governments. This research has noted the importance of internal control for the usefulness of financial information in their decisions. Afiah and Azwari (Citation2015) conclude that strengthening supervision of the internal control system becomes one of the main solutions for increasing FRQ. Kewo and Afiah (Citation2017) analyze the influence of internal control and internal audit systems on the FRQ of public sector entities in Indonesia. Research results show that establishing effective internal control and an internal audit system will lead to a positive impact on FRQ. Nogueira and Jorge (Citation2017) specifically emphasize the need to develop or improve internal control procedures to ensure financial information reliability, thereby increasing the usefulness of decision-making financial information. The primary objective of internal control in the public sector is to ensure the conformity of financial statements with standards and regulations, hence enhancing management’s accountability and transparency in the use of public resources. Gamayuni (Citation2018) aims to understand the impact of ICE on FRQ of public sector entities in districts, provinces, and cities in the Lampung region, Indonesia. The study result provides empirical evidence that ICE has a statistically significant positive effect on FRQ.

The impact of ICE on the FRQ is still controversial. Research by Simon et al. (Citation2016) finds that there is no evidence at a statistically significant level to show the impact of internal control on FRQ. This is explained by the fact that although the internal control system is operated by many firms, it is not fully monitored and enforced, so it cannot play its role in the FRQ. Ogneva et al. (Citation2007) did not confirm a decrease in information quality in entities with deficiencies in the effectiveness of internal control. Stemming from the relationship between internal control and FRQ based on the agency and contingency theory; the disagreement about the relationship between these two factors from previous studies, this study hypothesizes as follows:

H1: ICE has a positive effect on FRQ.

2.4. Audit and FRQ

As we know, it is imperative to comply with the basic provisions of the law on accounting, taxation, labor, etc. to ensure that the operation of an organization is not violating the law. In addition, depending on each business field and specific form of capital contributions the entity will be regulated by one or more other laws, which the law on auditing is also closely related to the operation of accounting and tax departments of organizations. In Vietnam, although the Law on independent auditing 2011 does not stipulate that PNUs are required to audit financial statements by independent auditors, the need comes from the diversity of both internal and external stakeholders for the publicity and transparency of financial information. Thus, more and more PNUs conduct audits of financial statements by independent auditors.

Stemming from the important role of audit, studying the impact of audit on FRQ has drawn the attention of many researchers. As Alijarde (Citation1997) concludes, the users of information appreciate the role and importance of auditing in the effectiveness of financial statements. López Hernández and Caba Pérez (Citation2004) stated that limitations related to the usefulness of financial information stem from many factors, including the lack of adequate audits. Kewo and Afiah (Citation2017) analyze the influence of internal control and internal audit systems on the FRQ of public sector entities in Indonesia. The results indicated that establishing an effective internal audit has a positive impact on FRQ. Recently, the research results of Abdulai et al. (Citation2021) find that internal audit is effective in detecting and preventing financial errors and frauds, thereby contributing to the increase of FRQ.

The review of the above studies shows that audit plays an important role in ensuring and maintaining FRQ in public sector entities. Different from the researches that focus on enterprises, where the role of independent auditors for FRQ has been confirmed, the researches aim at public sector entities and mainly consider the role of internal audit. The government’s policy towards renovating the operational and financial mechanism of PNUs in the direction of increasing autonomy and self-responsibility has set out the need for financial statements of PNUs to be audited by independent auditors. Deriving from the relationship between audit and FRQ based on the basis of agency and institutional theory; the lack of research on the role of independent audit on FRQ in public sector entities, the research hypothesis is established as follows:

H2: INA has a positive impact on FRQ.

2.5. State agencies and FRQ

The role of government agencies in inspecting and monitoring FRQ is explained on the basis of agency theory. Resolving conflict of interests of stakeholders in the organization has led to the establishment of control systems from the internal and external as a mechanism to frame the actions of managers and minimize the costs arising from these conflicts. This reflects the role of external monitoring factors, such as government agencies in ensuring the faithfulness of accounting information. López Hernández and Caba Pérez (Citation2004) indicate that one of the limitations related to the usefulness of financial information in Spanish local governments is caused by the lack of external control. Desai and Dharmapala (Citation2009) examine the role of government agencies in FRQ through the implementation of tax policy. The results show a positive impact of tax policy implementation on FRQ. Preobragenskaya et al. (Citation2018) explore that although accounting mostly serves management needs, the main purpose of FR is considered to be tax calculation and compliance with government reporting requirements, and the main users of financial statements are business owners and governments. Their study concluded that the usefulness of FR information in a transition economy like Russia is affected by regulations of state agencies such as the tax authorities and state audits.

Research on the relationship between the role of government agencies and the FRQ has only been focused on studies targeting businesses and is rarely mentioned in studies related to public sector entities. In Vietnam, the Revised Vietnam State Audit Law 2015 stipulates the power and responsibilities of the State Auditor to inspect and supervise the management and use of public finance, public assets, and other relevant activities related to the management and use of public finance and public assets of the unit. The state audit and inspection delegations, through the performance of their functions, have helped the inspected and examined units to promptly detect and get better understanding of errors related to financial statements and irregularities in complying with the law, contributing to improving the quality of financial statements through audits and inspections. Based on the research characteristics and the role of state inspection and testing for FRQ, the research hypothesis is determined:

H3: FIF has a positive impact on FRQ.

2.6. Audit and ICE

Internal control is a management tool built by the entities’ administrators for their management purposes. However, internal control also has a large influence on the auditor. An understanding of the entity’s internal control is an important foundation for the auditor to plan the audit and assess control risk. Through the process of understanding the internal control system at the entity, the auditors discover a lot of deficiencies and thus help managers provide solutions promptly to improve the effectiveness of the internal control system. International Standard on Auditing 265 also requires the auditors to be responsible for notifying management of deficiencies related to the internal control system.

Research on the relationship between audits to internal control has been confirmed by some previous studies. Y. Chen et al. (Citation2016); Haislip et al. (Citation2016) point out that the quality of internal control is influenced by the quality of the independent audit. Through the audit process and with the independent and objective assessment of the auditor, the weaknesses of the internal control system will be detected and reported to the management of the entity. Based on receiving and absorbing the opinions of the auditors, the management of the audited entity will make timely adjustments to improve the quality and effectiveness of their internal control system. However, the relationship between INA and ICE has only been noticed in studies targeting businesses and lacks studies fully exploring to PNUs. As for the previous researches related to PNUs, Unegbu and Kida (Citation2011), Safina (Citation2018) only discuss the role of internal audit and ICE. In Vietnam, to encourage, facilitate and establish an equal and competitive operating environment for organizations and individuals of all economic sectors, the Government has issued regulations to demand and encourage the implementation of financial autonomy mechanism for PNUs. This mechanism creates favorable conditions for the use of economic and financial resources, also puts a lot of pressure on PNUs. The mobilization of financial resources by the PNUs has set requirements for quality ensured financial statements. Therefore, more and more Vietnamese PNUs use the financial statement audit service from INA. Besides helping to ensure FRQ, INA is also expected to help PNUs improve ICE. On that basis, we propose hypothesis H4:

H4: INA has a positive impact on ICE.

2.7. State agencies and ICE

The state financial inspection for the public sector has the main objective of checking management responsibility for the effective use of public resources, the accuracy of accounting records, and the reliability of financial statements provided by the entity (Dikan et al., Citation2014). The subject of financial inspection at public institutions may vary from country to country, but it is usually the Ministry of Finance; Ministry of Public Finance, tax authorities, or specialized central bodies. Hurloiu et al. (Citation2014) finds that financial inspection with the function of checking financial efficiency in the use of public assets, checking compliance with current legal regulations contributes to increasing the effectiveness of the environment. Lusha et al. (Citation2015) argues that the monitoring of financial management in the public sector is important because this supervision not only directly affects the efficient and economic use of public funds but also significantly affects the establishment of a sustainability culture in the more efficient use of public funds. Vanchukhina et al. (Citation2020) finds that the relationship between tax inspections and ICE is explained by the concept of tax administration based on enhanced information interaction between tax authorities and taxpayers. Accordingly, taxpayers must provide more detailed information about accounting and tax-related transactions to tax authorities. This requirement has highlighted the role of the entity’s internal control system, which is considered an effective support tool for tax monitoring from tax authorities. Specifically, if the entity’s ICE is secured, the tax authority will reduce the administrative burden on taxpayers and may decide not to conduct some form of the complex and expensive tax audit. This shows that tax supervision from tax authorities has required businesses to focus on improving the effectiveness of the internal control system at their entities to provide assured-quality information. Although the relationship between state inspection and internal control has been mentioned in some previous studies, most of them are mentioned at the theoretical level and have not been tested by quantitative research. Based on the research characteristics and the role of state inspection and testing for ICE, the research hypothesis is determined:

H5: FIF has a positive impact on ICE

2.8. The mediating role of ICE

These two hypotheses H1 and H4 can be combined and expressed as the mediating role of ICE in the relationship between INA and FRQ:

H6: ICE mediates the relationship between INA and FRQ.

These two hypotheses H1 and H5 can be combined and expressed as the mediating role of ICE in the relationship between FIF and FRQ:

H7: ICE mediates the relationship between FIF and FRQ.

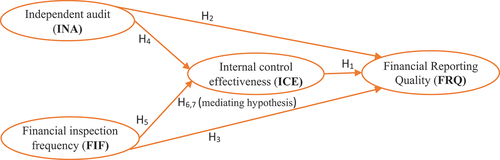

The research model and corresponding hypotheses are shown in .

Figure 1. Research model.

3. Methodology

3.1. Research method

The research was carried out through quantitative research and the convenience sampling method is used. The survey method was conducted through face-to-face interviews and email surveys.

3.2. Respondents

Survey respondents are deputy directors (in charge of finance), chief accountants, and accountants who have worked at PNUs for three years or more. The authors do not survey groups of subjects outside the public units such as public service users, investors, and state agencies that have the function of inspecting and supervising financial activities of public entities for two reasons: Firstly, in addition to FRQ, the research model considers a number of factors reflecting the unique characteristics of the entity (for example, the effectiveness of internal control, the situation of financial inspection and supervision acceptance from state agencies); Secondly, the selection of survey subjects within the unit was made on the basis of inheritance from previous studies (Pham et al., Citation2021; Tran et al., Citation2021).

3.3. Sample size

Hair et al. (Citation2021) suggested that when using PLS-SEM, the sample size should be large enough to ensure the implementation of the necessary estimations of the model. Accordingly, these authors give the ‘10-times rule”, specifically:

The sample size should be at least ten (10) times the maximum number of formative observations used to measure the single concept, or

The sample size should be at least ten (10) times the maximum number of structural paths directed at a particular concept in the structural model.

The model of this study () shows that the largest number of formative observations is 12 (belonging to the concept of ICE research—the number of observed variables of this factor is detailed in subsection 3.2) and the maximum number of structural paths is 3 (directed to the FRQ variable). Thus, the minimum number of samples needed for the study is 120.

3.4. Data collection tool and data description

A survey questionnaire with a 5-level Likert scale is used to collect data (except for INA called Dummy variable; two direct measured concepts are FIF and Timeliness quality characteristic). The survey period is from March to May 2021. We received 405 responses out of a total of 760 surveys sent with a response rate of 53.29%. For collected data, we screen and remove based on comparison with the conditions of the respondents’ job position as well as working experiences. The rejected samples mainly do not guarantee the job position as well as the working experience year conditions. After this screening step, we have 362 perfect responses. Compared with the minimum sample size in Subsection 3.3, the number of official samples is considered eligible to use in the PLS-SEM analysis.

Sampling characteristics presented in show that the number of PNUs in Hochiminh City accounts for 45.3%, Hanoi City is 33.15% and Danang City is 21.55%. This feature also accurately reflects the reality of economic scale by regions in Vietnam. Accordingly, Hochiminh city (Southern) is considered the largest economic center in the country, Hanoi city (Northern) is the political center and Danang City (Central region) is the 4th largest city in Vietnam. In terms of financial autonomy, the number of PNUs with financial autonomy accounts for 26.8% and 73.2% is not yet. Although the number of PNUs audited by INA accounts for a relatively low proportion (61 units, accounting for 16.85%), it is approximate to the reality in Vietnam where PNU financial statements are normally audited by the state auditors. Financial statements audited by INA normally occur only for PNUs that have conducted financial autonomy (55/97 self-financed PNUs have audited FR by independent auditors, accounting for 56.7%). Survey respondents include unit leaders—in charge of finance (14.09%), chief accountants (54.70%), and accountants (31.21%), most of whom have worked at the surveyed unit 5 years or more and have a bachelor degree at least. Regarding financial audit acceptance for the 2016–2020 period, 35.91% of PNUs received 5 financial audits from State agencies, 44.75% received 4 times and 19.34% received a relatively low number of financial audits (no more than 3 times).

Table 1. Sampling characteristics

3.5. Measurement scales

FRQ scale: FRQ is conceptualized as the achievement of quality attributes (relevance, faithful representation, verifiability, comparability, understandability, and timeliness) that make the information on the FR useful for accountability and decision-making (IPSASB, Citation2013). The FRQ scale is inherited from the FRQ scale of Pham et al. (Citation2021). This scale is the third-order construct comprising two-second order constructs that are Relevance (including predictive value, confirmatory value); faithful representation (including Complete, Neutral, and Free from material error), and four first-order constructs (understandability; timeliness; comparability; verifiability). The content, scale structure, and FRQ measurement method are presented in .

Table 2. Scale structure and measurement of FRQ

ICE scale: Effectiveness of internal control is defined as providing reasonable assurance to the board of directors about the achievement of the entity’s objectives or survival (INTOSAI, Citation2004). COSO (Citation2013) states three categories of objectives including efficiency and effectiveness of activities, reliability of FR, compliance with laws and regulations. This scale is inherited from research by Länsiluoto et al. (Citation2016), including three components: efficiency and effectiveness of activities (EFF: EFF1→EFF4); reliability of FR (REL: REL1→REL4); compliance with laws and regulations (LAW: LAW1→LAW4). Länsiluoto et al. (Citation2016) conducted a survey on CFO respondents, we made small editing on the content of the scale (about the label) to suit the survey respondents of this study (CFO, Chief accountant, and Accountant).

INA: Is defined as the FR of the entity audited by Audit firms. This scale is a Dummy variable with two values: This indicator variable has the value of 1 if the FR is audited by the INA and 0 for the remaining cases.

FIF: Is defined as the number of times receiving financial inspection and examination from state management units within a certain period of time. This study examines the number of state inspections and financial examinations received over a five-year period (from 2016 to 2020).

4. Research results

4.1. Quality of observed items

In this study, the FRQ scale is a third-order construct, composed of 9 first-order components; ICE is second-order construct, composed of 3 first-order components. Therefore, when performing testing steps, we conduct the implementation for the first-order components according to the guidance of Hair et al. (Citation2018). Hulland (Citation1999) states that an observed item is qualified when its outer loading coefficient is greater than the minimum threshold of 0.5. On that basis, after performing outer loading factor analysis using PLS-SEM software, we removed the observed item NEU1 due to its quality failure (outer loading is equal to 0.281). The remaining observed variables are qualified because they have outer loading values greater than 0.5 and are statistically significant (corresponding P values are all 0; ).

Table 3. Scale items and latent variable evaluation

4.2. Scale reliability

Dijkstra and Henseler (Citation2015) suggest that scale reliability is evaluated on three criteria, namely Cronbach’s Alpha, RhoA, and Composite Reliability (CR) and the scale is considered valid when the values of these three indexes are within the range of 0.7 to 0.95. Table presents the results of testing the scale value, showing the Cronbach’s Alpha values of all scales range from 0.736 to 0.900; RhoA values range from 0.748 to 0.901, and CR values also range from 0.850 to 0.938. Besides, the concepts of timeliness, INA, and FIF are directly measured by one item; the values of all three indicators above are equal to 1. Based on the results, we conclude that scale reliability is guaranteed.

4.3. Convergent validity

The scale is considered qualifying convergent validity when the Average Variance Extracted (AVE) value corresponding to each scale has a value of 0.5 or more (J. J. Hair et al., Citation2010). The test results in show that the scales used for this study all ensure Convergent validity because the AVE value corresponding to each scale ranges from 0.616 to 0.833.

4.4. Discriminant validity

HTMT index and square root index of AVE are used. Henseler et al. (Citation2015) suggest that the discriminant validity of the scale is guaranteed when the HTMT index is below 0.9. Fornell and Larcker (Citation1981) recommend that the discriminant validity of the scale is warranted when the square root of the AVE for each latent variable is higher than all correlations between the latent variables. shows that all coefficients of HTMT between two latent variables are less than 0.9. shows that the square root of the AVE of each latent variable (the number lying on the diagonal) is larger than its correlation coefficient with any other research concepts in the model. Besides, the highest value of the correlation coefficients between latent variables (the number below the diagonal) is 0.772 and lower than the lowest value of CR (by 0.850). The above results show that all the research model scales ensure discriminant validity.

Table 4. Heterotrait-Monotrait Ratio (HTMT)

Table 5. Fornell-Larcker Criterion

4.5. Multicollinearity test in the structural modeling

We use the VIF value to check this phenomenon. Thọ (Citation2011) said that if VIF is greater than 2, we need to be cautious in interpreting the regression weights. shows that the VIF value of each relationship arising between the independent variables and the dependent variable in the model has the highest value of 1.454, which is much lower than the threshold value suggested by Thọ (Citation2011). This result shows that there is no multicollinearity in this study.

Table 6. Inner VIF Values

4.6. Results and discussion

4.6.1. Research hypothesis test and the simple structural modeling

The research model hypotheses were tested using SmartPLS3 software. To provide evidence for testing the research hypotheses, we evaluate the standardized coefficients (Beta) and the level of statistical significance corresponding to each research hypothesis. Besides, to have a basis for assessing the fit of the model, we also evaluate adjusted R2 values for two dependent variables of the research model, FRQ and ICE. Basic bootstrapping was used with 500 bootstrap subsamples. The test results are presented in .

Table 7. PLS-SEM results

4.6.2. Structural model robustness checks

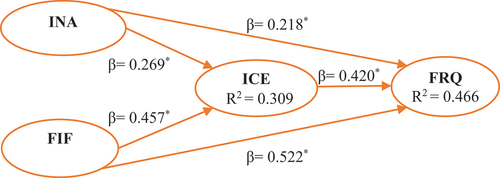

Hair et al. (Citation2019) argue that Robustness checks for PLS- SEM results should be performed. In terms of the structural model, these authors suggest the need to consider nonlinear effects, endogeneity, and unobserved heterogeneity. illustrates the path model used in our analyses for structural model robustness checks.

Figure 2. Present the simple structural modeling for the results.

4.6.2.1. Nonlinear effects

When the relationship between two variables is nonlinear, besides relying on the magnitude of the change in the exogenous variable, the effect size between two variables also depends on its value (Hair et al., Citation2018). This study used the quadratic effect in using bootstrapping with 5000 samples to test the nonlinear effect in the PLS-SEM model as recommended by Hair et al. (Citation2018). The model of this study includes four variables, of which INA is a qualitative variable, and then we included interaction terms to describe the quadratic effects between (1) FIF and ICE, (2) FIF and FRQ, (3) ICE and FRQ. The results in . show that the p-values of all interaction terms are greater than 0.05. Based on the above results, we conclude that there is no nonlinear relationship in the model of this study.

Table 8. Assessment of nonlinear effects

4.6.2.2. Endogeneity

Our endogeneity testing was performed according to the PLS-SEM endogeneity testing procedures of Hult et al. (Citation2018). The Gaussian copula instrument-free approaches introduced by Park and Gupta (Citation2012) was used. We examine if the endogenous variable has to be nonnormally distributed or not at first. To do so, the Kolmogorov-Smirnov (Lilliefors correction; Mooi & Sarstedt, Citation2019) test was run on the latent independent variable scores (i.e. INA, FIF, and ICE). The results indicated that all of the constructs’ score has nonnormally distributed. This allows us to take the next step of testing whether the Gaussian copula approaches detect endogeneity issues or not. With all p-value higher than 0.05, the results of the Gaussian copula approach in show that all of the Gaussian copulas (i.e. INA, FIF, and ICE) are insignificant (p-value > 0.05). On that basis, we conclude that endogeneity issues do not occur in this study.

Table 9. The Gaussian Copula approach results

4.6.2.3. Unobserved heterogeneity

Becker et al. (Citation2013) suggest that unobserved heterogeneity could be a significant threat to the validity of any SEM analysis. When using the PLS-SEM model, Finite mixture PLS (FIMIX-PLS) is considered to be a suitable method to evaluate unobserved heterogeneity (Sarstedt et al., Citation2011).

When performing unobserved heterogeneous data exploratory research, one of the most important tasks to do is to determine the potential number of segments in the dataset. The sample size for this study is 362, the minimum required sample size is 120 (Subsection 3.4). So we define the provisional number of segments as 3 (dividing the official sample number by the minimum sample size). Next, we run the FIMIX-PLS Procedures three times (first time with 1 segment, second time with 2 segments, and third time with 3 segments), utilizing a different potential number of segments to determine their corresponding Fit Indices.

Sarstedt et al. (Citation2011) have indicated that whenever AIC3 and CAIC point to the same segment number, the appropriate segment number will be identified. These authors further note that in FIMIX-PLS, the joint between AIC4 and BIC is well when used to identify the segment number. The optimal fit index value (the lowest absolute value) shown in clearly shows us both AIC3—CAIC and AIC4—BIC points together in segment 3. Besides, we easily see that segment 3 is big enough for the modeling (11% see the Segment sizes in the last row). Based on the above results, we conclude that the data of this study has three segments.

Table 10. Fit Indices based on number of segments

Unobserved heterogeneity does not significantly influence on the data if the criteria point to a specific segment solution or create various results (Sarstedt et al., Citation2020). shows that almost all indexes (AIC, AIC3, AIC4, BIC, CAIC, HQ) converge on segment 3; moreover the criteria values corresponding to each segment are also different. On that basis, we conclude that there is no significant effect of unobserved heterogeneity on our data.

4.6.3. Discussion

Robustness testing results in Section 4.6.2 show that nonlinear effects, endogeneity, and unobserved heterogeneity are not present in this research. This shows that the robustness of the structural model is guaranteed. On that basis, we conclude that the PLS-SEM results presented in this section are considered reliable for analysis.

The results of data analysis in show that the Adjusted R2 of the FRQ variable is 0.466. This shows that three factors ICE, FIF, and INA explain 46.6% of the variation of FRQ. The results of testing the research hypothesis show that all three hypotheses H1, H2, H3 are accepted with a statistical significance level of 0.01. The positive effect of ICE on FRQ is considered similar to previous studies by Yamamoto (Citation2008), Kewo and Afiah (Citation2017), Nogueira and Jorge (Citation2017), and Gamayuni (Citation2018). Regarding the role of audit for FRQ in PNUs, previous studies have mainly considered the role of internal audit. Therefore, with the approval of hypothesis H2, this study contributes to supplementing the important role of INA for FRQ in PNUs. With the approval of hypothesis H3, the study also shows that the inspection and examination by State agencies contribute to the increase of FRQ in PNUs. Through the process of inspection and examination at PNUs, State agencies promote the State supervisory role in the management and use of the state budget, as well as financial assets at PNUs; contribute to the fight against corruption; help detect the shortcomings of PNUs in complying with financial regulations and accounting regimes. Besides, the Adjusted R2 of the ICE variable of 0.309 shows that INA and FIF explain 30.9% of ICE variation. Similar to the above results, both hypotheses H4, H5 are accepted with statistical significance at the 0.01 level. The positive impact of INA on ICE is considered similar to previous studies in the business of Chen et al. (Citation2016); Haislip et al. (Citation2016). Accordingly, the purpose of evaluating the internal control system during an independent audit is to contribute to the improvement of the internal control system, thereby contributing to the increase of ICE at the audited entity. The positive impact of FIF on ICE is explained through agency theory. Consequently, the resolution of stakeholders’ conflicts of interests in the organization has led to the establishment of a control system from both inside and outside, including a monitoring mechanism from State management agencies through financial inspection. By using the process of inspection and control for the PNUs, the state financial inspectors also discover errors related to the operation of the internal control system; contribute to improving and enhancing the PNUs’ ICE.

This study also considers the mediating role of the ICE variable in the research model. Hair et al. (Citation2021) argue that a necessary condition to confirm an intermediate effect is that the directly related effects must be statistically significant. For the mediating role of the variable ICE on the impact of INA on the FRQ, the condition is that the direct impact of the INA on ICE and the direct effect of ICE on the FRQ must be statistically significant. The results of testing hypotheses H4 and H1 (Table ) show that both of these requirements are satisfied. Moreover, results in Table also point out that the indirect impact of INA on FRQ through ICE is confirmed with a statistical significance of 0% and β of 0.113. Based on the results, we conclude that the ICE variable acts as an intermediate variable between the INA and the FRQ. Similarly, ICE also acts as an intermediate variable between FIF and FRQ with a statistical significance of 0% and β of 0.192.

5. Conclusions and suggestions for future research directions

5.1. Conclusion

This study has contributed to the development of the research theory on FRQ towards the public sector entities in general and PNUs in particular. The study is also based on agency theory to explain the phenomenon of information asymmetry and conflicts of interests between the principal and the agent. Since then, it is necessary to have monitoring mechanisms from the internal and external of units to ensure and increase the FRQ.

Based on the results of PLS-SEM, the study has shown a positive impact of INA on FRQ. This shows that independent audit also plays an important role in ensuring FRQ even in public sector entities. Although the relationship between INA and FRQ has been mentioned many times in the studies targeting enterprises by Fargher et al. (Citation2001), Fathi (Citation2013), and Pham et al. (Citation2021), it is still relatively new to the researches in public sector entities. Limitations in the research on the role of independent auditors in these PNUs can be attributed to the fact that public sector entities have been subjected to state inspections and financial examinations by government agencies (state inspection agencies, state audits), so the role of independent audit for public sector entities is blurred and unnecessary. However, the current trend of implementing financial autonomy has posed many challenges for PNUs. This mechanism requires the PNUs to focus on exploiting revenue sources, build internal management solutions to save costs, use debt as capital, and mobilize capital sources to invest in expanding and improving the quality of non-business operations. To do so, accountants need to ensure the role of providing quality and reliable information to relevant stakeholders. This also explains the need for INA besides the traditional role of the state audit.

Besides, in the context that the role of internal control for FRQ is still being discussed, this study also helps confirm the role of internal control for FRQ. Effective internal control will contribute to increasing the sustainability of earnings and predictability of cash flows, minimizing fraud and errors, thereby increasing FRQ. Firms that fail to ensure FRQ often face internal control problems (Doyle et al., Citation2007). Therefore, strengthening the supervision of internal control systems becomes one of the main solutions for increasing FRQ in organizations (Afiah & Azwari, Citation2015). Although the current Vietnamese Accounting Law requires entities to set up internal control systems to ensure the fair presentation and qualified preparation of FR, the implementation is still facing difficulties due to the lack of specific legal documents for checking and monitoring this compliance. Major cases related to embezzlement and corruption in Vietnamese public institutions recently show that one of the main reasons is the ineffectiveness of the internal control system and the unqualified information on the FR. These are reflected in the fact that assets in the PNUs are not used properly and effectively; internal mechanisms, policies, processes, and regulations are not consistent with the provisions of the law, fail to prevent, detect and handle risks promptly then not meet the control requirements. Therefore, to ensure the effectiveness of internal control and improve the FRQ, we recommend that the Vietnamese State management agencies should promptly issue legal documents regulating the inspection, supervision, and ensuring the effectiveness of the internal control system in accounting units, especially PNUs.

The study also demonstrates the role of state inspections, financial examinations, and audits in increasing FRQ. The state inspection and examination agencies and state audit agencies, through their functional performance, help PNUs to promptly detect and better understand violations related to accounting, finance, and law compliance, contributing to improving FRQ. Through the survey results, we find that there are big differences in the frequency of state financial inspection between units. Specifically, 35.92% of the surveyed units receive 5 financial audits during the five-year period from 2016 to 2020, while 19.34% receive no more than three times during the same period. On that basis, we recommend that the state financial inspection at PNUs should be carried out regularly every year to help the unit promptly detect errors, including errors of misuse the accounting regulations, thereby contributing to improving FRQ.

ICE’s mediating role in the relationship between the INA and the FRQ; FIF and FRQ are also considered important findings of this study. The positive value of β indicates that ICE plays a positive role in the relationship between INA and FRQ (β = 0.113); FIF and FRQ (β = 0.192). This is interpreted that in PNUs with effective internal control systems, state agencies and independent audit recommendations for violations of the unit (including finance, accounting violations, etc.) will be seriously recognized and widely communicated to all relevant departments in the entity. The finance and accounting mechanisms and policies of the unit will be completed, and the reception of comments from state agencies and independent audits will also be closely supervised. On that basis, we conclude that increasing the effectiveness of internal control in PNUs will contribute to increasing the impact of INA and FIF on FRQ.

5.2. Limitations and suggestions for further researches

Our model with R2adj = 0.466 shows that the independent variables of the model explain 46.6% of the change in FRQ. This is explained by, besides the factors belonging to the supervisor mechanism, the FRQ is also affected by other factors (factors about corporate governance such as the support of managers, the diversity of capital owners; earnings management behavior; capacity of employees; level of application of internal control …).

The survey respondents of this study are internal subjects of PNUs, which may affect the objectivity of the collected data. Future studies may combine both internal and external survey subjects of public organizations to have more convincing assessments in their research.

The regression equation shows that 3 factors are affecting the FRQ, namely INA, ICE, FIF, in which two factors INA and FIF are considered discoveries of our research. Finally, it is necessary to have more application-oriented researches for analyzing detail of each factor’s nature to propose solutions for increasing FRQ in public sector entities in general and PNUs in particular.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Quoc Thuan Pham

Quoc Thuan Pham is a Head of Accounting Department, Faculty of Accounting and Audit, University of Economics and Law, VNU HCMC, Vietnam. His research interest could be found in accounting, audit, policy and finance.

Thi Hanh Dung Truong

Thi Hanh Dung Truong is a senior lecturer at Faculty of Accounting and Audit, University of Economics and Law, VNU HCMC, Vietnam with around 12 years of teaching and research in Accounting and Auditing. Her preferred research areas are international financial reporting standards, auditing, managerial accounting, and fraudulent financial reporting.

Xuan Thuy Ho

Xuan Thuy Ho is a Dean of the Faculty of Accounting and Audit, University of Economics and Law, VNU HCMC, Vietnam. Her preferred research areas are accounting, auditing, earning management and corporate social responsibility.

Quoc Thinh Nguyen

Quoc Thinh Nguyen is a lecturer at Department of Transport Economics, University of Transport of Ho Chi Minh City with more than 30 years of teaching and researching in the field of accounting. Almost research area are related to accounting, financial tax and shipping business management.

References

- Abdulai, I., Salakpi, A., & Nassè, T. B. (2021). Internal audit and quality of financial reporting in the public sector: The case of university for development studies. Finance & Accounting Research Journal, 3(1), 1–23. https://doi.org/10.51594/farj.v3i1.231

- Afiah, N. N., & Azwari, P. C. (2015). The effect of the implementation of government internal control system (GICS) on the quality of financial reporting of the local government and its impact on the principles of good governance: A research in district, city, and provincial government in South Sumatera. Procedia-Social and Behavioral Sciences, 211(2015), 811–818. https://doi.org/10.1016/j.sbspro.2015.11.172

- Alijarde, M. I. B. (1997). The usefulness of financial reporting in Spanish local governments. Financial Accountability & Management, 13(1), 17–34. https://doi.org/10.1111/1468-0408.00024

- Becker, J.-M., Rai, A., & Rigdon, E. (2013). Predictive validity and formative measurement in structural equation modeling: Embracing practical relevance. Proceedings of the International Conference on Information Systems (ICIS), Milan. https://aisel.aisnet.org/icis2013/proceedings/ResearchMethods/5

- Bellanca, S., & Vandernoot, J. (2014). International public sector accounting standards (IPSAS) implementation in the European Union (EU) member states. Journal of Modern Accounting and Auditing, 10(3), 257–269. http://www.davidpublisher.com/Public/uploads/Contribute/550a645f9b4c5.pdf

- Burgmeijer, J. (2005). Role of public organisations in the creation of new broadband access infrastructures. TNO, Delft. http://resolver.tudelft.nl/uuid:a50d6df2-1371-4fa8-a89d-fb187ae60e76 (Accessed: 1 June 2020)

- Chen, Y., Gul, F. A., Truong, C., & Veeraraghavan, M. (2016). Auditor client specific knowledge and internal control weakness: Some evidence on the role of auditor tenure and geographic distance. Journal of Contemporary Accounting & Economics, 12(2), 121–140. https://doi.org/10.1016/j.jcae.2016.03.001

- Chen, C. A., & Hsieh, C. W. (2015). Knowledge sharing motivation in the public sector: The role of public service motivation. International Review of Administrative Sciences, 81(4), 812–832. https://doi.org/10.1177/0020852314558032

- COSO. (2013). Internal control – Integrated framework 2013. https://www.coso.org/Shared%20Documents/Framework-Executive-Summary.pdf?web=1 16 April 2021)

- Cuadrado-Ballesteros, B., Citro, F., & Bisogno, M. (2019). The role of public-sector accounting in controlling corruption: An assessment of Organisation for Economic Co-operation and Development countries. International Review of Administrative Sciences, 86(4), 729–748. https://doi.org/10.1177/0020852318819756

- Desai, M. A., & Dharmapala, D. (2009). Earnings management, corporate tax shelters, and book-tax alignment. National Tax Journal, 62(1), 169–186. https://doi.org/10.17310/ntj.2009.1.08

- Dijkstra, T. K., & Henseler, J. (2015). Consistent partial least squares path modeling. MIS Quarterly, 39(2), 297–316. https://doi.org/10.25300/MISQ/2015/39.2.02

- Dikan, L. V., Synyuhina, N. V., & Deyneko, Y. V. (2014). Internal control under public financial control system reformation: The state of implementation and development prospects. Актуальні проблеми економіки, 154(4), 446–454. http://www.irbis-nbuv.gov.ua/cgi-bin/irbis_nbuv/cgiirbis_64.exe?C21COM=2&I21DBN=UJRN&P21DBN=UJRN&IMAGE_FILE_DOWNLOAD=1&Image_file_name=PDF/ape_2014_4_55.pdf

- Djama, C. (2010). Fraude A L’Information comptable et financiere: Le role des autorites de regulation. HAL archives-ouvertes. https://halshs.archives-ouvertes.fr/halshs-00522510 (Accessed: 1 June 2020)

- Doyle, J., Ge, W., & McVay, S. (2007). Determinants of weaknesses in internal control over financial reporting. Journal of Accounting and Economics, 44(1–2), 193–223. https://doi.org/10.1016/j.jacceco.2006.10.003

- Fargher, N., Taylor, M. H., & Simon, D. T. (2001). The demand for auditor reputation across international markets for audit services. The International Journal of Accounting, 36(4), 407–421. https://doi.org/10.1016/S0020-7063(01)00116-9

- Fathi, J. (2013). The determinants of the quality of financial information disclosed by French listed companies. Mediterranean Journal of Social Sciences, 4(2), 319. http://dx.doi.org/10.5901/mjss.2013.v4n2p319

- Fornell, C., & Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Sage Publications Sage CA.

- Gamayuni, R. R. (2018). The effect of internal audit function effectiveness and implementation of accrual based government accounting standard on financial reporting quality. Review of Integrative Business and Economics Research, 7(1), 46–58. http://repository.lppm.unila.ac.id/id/eprint/7430

- Hair, J., Black, B., Babin, B., & Anderson, R. (2010). Multivariate data analysis 7th Pearson prentice hall (pp. 816). Pearson; 7th edition (February 23, 2009).

- Hair, J. F., Jr, Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2021). A primer on partial least squares structural equation modeling (PLS-SEM) (Third Edition) ed.). Sage publications.

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11–2018-0203

- Hair, J. F., Jr, Sarstedt, M., Ringle, C. M., & Gudergan, S. P. (2018). Advanced issues in partial least squares structural equation modeling. saGe publications.

- Haislip, J. Z., Peters, G. F., & Richardson, V. J. (2016). The effect of auditor IT expertise on internal controls. International Journal of Accounting Information Systems, 20(2016), 1–15. https://doi.org/10.1016/j.accinf.2016.01.001

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hevesi, G. A. (2005). Standards for internal control in New York state government. (pp. 30). State Comptroller.

- Hulland, J. S. (1999). The effects of country-of-Brand and brand name on product evaluation and consideration. Journal of International Consumer Marketing, 11(1), 23–40. https://doi.org/10.1300/J046v11n01_03

- Hult, G. T. M., Hair, J. F., Proksch, D., Sarstedt, M., Pinkwart, A., & Ringle, C. M. (2018). Addressing endogeneity in international marketing applications of partial least squares structural equation modeling. Journal of International Marketing, 26(3), 1–21. https://doi.org/10.1509/jim.17.0151

- Hurloiu, L.-R., Burtea, E., & Preda, B.-F. (2014). Organizing inspections regarding managerial internal control and preventive financial control. Procedia Economics and Finance, 16(2014), 275–280. https://doi.org/10.1016/S2212-56711400801-6

- IASB. (2010). Conceptual framework for financial reporting. https://www.ifrs.org/projects/2010/conceptual-framework-2010/#published-documents 15 March 2018)

- INTOSAI. (2004). Guidelines for internal control standards for the public sector. Available at (Accessed: 2 May 2021).

- IPSASB. (2013). The conceptual framework for general purpose financial reporting by public sector entities. International Federation of Accountants.

- Kewo, C. L., & Afiah, N. N. (2017). Does quality of financial statement affected by internal control system and internal audit? International Journal of Economics and Financial Issues, 7(2), 568–573. https://dergipark.org.tr/en/pub/ijefi/issue/32035/354530

- Krambia-Kapardis, M., Clark, C., & Zopiatis, A. (2016). Satisfaction gap in public sector financial reporting. Journal of Accounting in Emerging Economies, 6(3), 232–253. https://doi.org/10.1108/JAEE-08-2013-0040

- Länsiluoto, A., Jokipii, A., & Eklund, T. (2016). Internal control effectiveness – A clustering approach. Managerial Auditing Journal, 31(1), 5–34. https://doi.org/10.1108/MAJ-08-2013-0910

- López Hernández, A. M., & Caba Pérez, C. (2004). The relevance of Spanish local financial reporting to credit institution decisions. International Journal of Public Sector Management, 17(2), 118–135. https://doi.org/10.1108/09513550410523250

- Lusha, A., Mziu, X., & Brahimi, F. (2015). Financial management in the public sector. European Scientific Journal, 11(7), 186–197. https://eujournal.org/index.php/esj/article/view/5315

- Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83(2), 340–363. https://doi.org/10.1086/226550

- Mooi, E., & Sarstedt, M. (2019). A concise guide to market research the process, data, and methods using IBM SPSS statistics (Third edition ed.). Springer.

- Nogueira, S. P. D. S., & Jorge, S. M. F. (2017). The perceived usefulness of financial information for decision making in Portuguese municipalities. Journal of Applied Accounting Research, 18(1), 116–136. https://doi.org/10.1108/JAAR-05-2014-0052

- Ogneva, M., Subramanyam, K. R., & Raghunandan, K. (2007). Internal control weakness and cost of equity: Evidence from SOX section 404 disclosures. The Accounting Review, 82(5), 1255–1297. https://doi.org/10.2308/accr.2007.82.5.1255

- Park, S., & Gupta, S. (2012). Handling endogenous regressors by joint estimation using copulas. Marketing Science, 31(4), 567–586. https://doi.org/10.1287/mksc.1120.0718

- Pham, Q. T., Ho, X. T., Nguyen, T. P. L., Pham, T. H. Q., & Bui, A. T. (2021). Financial reporting quality in pandemic era: Case analysis of Vietnamese enterprises. Journal of Sustainable Finance & Investment, 1–23. https://doi.org/10.1080/20430795.2021.1905411

- Preobragenskaya, G. G., McGee, R. W., & Komarev, I. (2018). Public perception of the role of accounting in a transition economy: The case of Russia. International Journal of Accounting, Auditing and Performance Evaluation, 14(4), 338–363. https://doi.org/10.1504/IJAAPE.2018.095110

- Safina, A. R. (2018). Internal control and audit of public sector organizations: Risk assessment. Revista SanGregorio, 25(Novembe), 151–157. https://dialnet.unirioja.es/servlet/articulo?codigo=6841032

- Sarstedt, M., Becker, J.-M., Ringle, C. M., & Schwaiger, M. (2011). Uncovering and treating unobserved heterogeneity with FIMIX-PLS: Which model selection criterion provides an appropriate number of segments? Schmalenbach Business Review, 63(1), 34–62. https://doi.org/10.1007/BF03396886

- Sarstedt, M., Ringle, C. M., Cheah, J.-H., Ting, H., Moisescu, O. I., & Radomir, L. (2020). Structural model robustness checks in PLS-SEM. Tourism Economics, 26(4), 531–554. https://doi.org/10.1177/1354816618823921

- Simon, Y., Mas’ Ud, M., & Su’un, M. (2016). The role of apparatus competence, internal control system on good governance and the quality of financial statement information. Researchers World, 7(4), 123–132. http://dx.doi.org/10.18843/rwjasc/v7i4/14

- Steccolini, I. (2004). Is the annual report an accountability medium? An empirical investigation into Italian local governments. Financial Accountability & Management, 20(3), 327–350. https://doi.org/10.1111/j.0267-4424.2004.00389.x

- Suwanda, D. (2015). Factors affecting quality of local government financial statements to get unqualified opinion (WTP) of audit board of the Republic of Indonesia (BPK). Research Journal of Finance and Accounting, 6(4), 139–157. https://www.iiste.org/Journals/index.php/RJFA/article/view/19978/20506

- Thọ, N. Đ. (2011). Phương pháp nghiên cứu khoa học trong kinh doanh (pp.593). Nhà xuất bản Lao động-Xã hội.

- Thuan, P. Q. (2022). Factors affecting the financial reporting quality in Vietnamese enterprises: A perspective from contingency theory. Science & Technology Development Journal-Economics-Law and Management, 6(2), 2486–2499. https://doi.org/10.32508/stdjelm.v6i2.907

- Tran, Y. T., Nguyen, N. P., & Hoang, T. C. (2021). How do innovation and financial reporting influence public sector performance in a transition market? Journal of Accounting in Emerging Economies, 12(4), 645-662. https://doi.org/10.1108/JAEE-06-2021-0180

- Unegbu, A. O., & Kida, M. I. (2011). Effectiveness of internal audit as instrument of improving public Sector management. Journal of Emerging Trends in Economics and Management Sciences, 2(4), 304–309. https://hdl.handle.net/10520/EJC134333

- Vanchukhina, L., Galeeva, N., Rogacheva, A., Rudneva, Y., & Shamonina, T. (2020). Development of the internal corporate control under conditions of tax monitoring. Revista Inclusiones, 7( Special September 2020), 358–374. https://revistainclusiones.org/index.php/inclu/article/view/1053/999

- Yamamoto, K. (2008). What matters in legislators’ information use for financial reporting: The case of Japan. In Susana Jorge (Ed.), Implementing reforms in public sector accounting (pp. 377–391). Uni Press. https://doi.org/10.14195/978-989-26-0422-0_19

- Yến, T. T. (2021). Tác động của năng lực kế toán và vai trò lãnh đạo đến chất lượng báo cáo tài chính, trách nhiệm giải trình và thành quả hoạt động trong các đơn vị công tại Việt Nam. (PhD). UEH University, Hochiminh City. https://digital.lib.ueh.edu.vn/handle/UEH/62796