Abstract

Audit fees are deemed as one of the factors that might influence the perceptions of public toward external auditors. The problem statement concentrated if there is a significant relationship between audit fees and audit quality through the mediators: total assets, origin of company, audit-firm size, complexity of operation in a company and auditor industry based on the perceptions of the external auditors. Therefore, this study aimed to investigate the perceptions of external auditors on the relationship between audit fees and audit quality. A survey questionnaire contains 18 items distributed to 90 external auditors, 73 were returned yielding 81% responses rate. Descriptive analysis and hierarchical regression were used to analyze data and test the hypotheses. The study revealed that there is insignificant relationship between audit fees and audit quality in case there is no mediators. Moreover, results revealed that after using five mediators (total assets, origin of a company, audit firm-size, complexity of operations, auditor industry) there is a significant relationship on the relationship between audit fees and audit quality in terms of audit firm-size as a mediator. In contrast, the study found that there are insignificant relationships between audit fees and audit quality in terms of the other mediators such total assets, origin of a company, complexity of operations, auditor industry. The results showed the audited companies/clients in Jordan are affected of the halo of big-4 audit firms regardless the factors that might play a big role in enhancing the quality of audit process.

1. Introduction

The global financial crisis has underlined the crucial need of reliable and high-quality financial reporting. Furthermore, it emphasized the need of addressing audit quality in the context of financial reporting quality, as obtaining high financial reporting quality is dependent on the integrity of each of the financial reporting liaisons (IAASB, Citation2019).

In spite of the fact that recent regulations have limited the breadth of audit services due to concerns about independence, it is possible to argue that audit quality will always be dubious if other services are supplied that are seen to jeopardize the auditor’s neutrality and skepticism (Francis, Citation2004).

Recent years have witnessed the emergence of many financial problems and the accompanying collapses of many large companies such as Enron, followed by the collapse Arther Andersen which was considered one of big-5 audit firms (De Fuentes et al., Citation2015).

External audit is one of such liaisons as it plays a critical role in ensuring the quality of financial reporting around the world, whether in the capital markets, the public sector, the private sector, or the non-public sector. It is a vital component of the regulatory and supervisory infrastructure and thus a public-interest activity. (IAASB, Citation2019).

Achieving a high level of audit quality helps to create trust and confidence in the audit profession. In spite the fact that there is no universally accepted definition of a quality audit, numerous factors influence audit quality. As a result, measuring audit quality can be difficult and subjective, but there are steps that can be taken to foster a high-quality auditing environment. (Chartered Accountants, Citation2019).

A high-quality of audit process is more expected to be completed when auditors have suitable values, integrity, attitudes, informed, skilled, experienced, and have sufficient time to complete the audit. These standards apply to the firm as a whole, as well as the quality of all audits performed. Individual auditors’ values, ethics, and attitudes are similarly influenced by their firm’s culture.(Chartered Accountants, Citation2019).

Stakeholders obtain helpful reports and information on time in a high-quality audit. The quality of the auditor’s outputs and audited entity’s outputs can both reflect and directly affect the audit quality (Chartered Accountants, Citation2019).

The client–auditor relationship, particularly the economic link that improves over time and may have an influence on auditor independence as because auditors’ fees are based on client firms. Therefore, there are lots of research in this topic to examine if auditors’ independence and audit quality are affected by their economic dependency (Firth, Citation1997).

Hoitash et al. (Citation2007) consider the following two implications of audit fees on audit quality; Higher fees paid to external auditors may indicate the complexity of the auditing process and raise the effort put in by auditors. Large audit fees provided to auditors, on the other hand, may make it easier for clients and auditors to form an economic tie, making it easier for auditors to compromise their audit independence due to the fear of losing much more fees.

The amount that a corporation pays an external auditor in exchange for doing an audit is known as audit fees. Audit fees have climbed dramatically in the United States since 2001 as a result of the Sarbanes-Oxley Act (SOX), which made audits more difficult. (Farlex Financial Dictionary, Citation2009). On the other hand, audit quality describes the input process and output factors that involve to audit quality, audit firm and audited financial statement (IFAC, Citation2019).

According to Abdul-Rahman et al. (Citation2017), the most important determinant the level of audit quality is audit fees. Audit fees are defined as the fees paid for audit services and reviews of financial statements. In contrast, Arens (Citation2012, p. 256) defined audit quality as “how well an audit detects and report material misstatements in financial statements, where the detection aspects are a reflection of auditor competence, while reporting is a reflection of ethics or auditor integrity, particularly independence”.

Accordingly, unlike the prior research that have investigated the effect of audit fees on audit quality, this study and will examine will which element/s (mediate) affect on the relationship between audit fees and audit quality based on the perception of the Jordan-certified public accountants (JCPA) to fill up the gap.

2. Problem statement and question

Several studies considered the effect of audit fees on audit quality (Hoitash et al., Citation2007; Nassar et al., Citation2017; Warrad, Citation2017, Citation2018). To mention but few, Cahan and Sun (Citation2015) showed how changing the external auditor affects on the audit fees and its relations with audit quality. Cahan and Sun (Citation2015) examined how auditor’s experience play a big role in determining the audit fees and its effect on audit quality. Corbella et al. (Citation2015) investigated how audit fees could be changed based on auditor’s tenure and its influence on audit quality. Choi et al. (Citation2010b) tested how the abnormally audit fees have an influence on audit quality. Kuntari et al. (Citation2017) examined the effect of audit fees and audit ethics on audit quality. While prior research as mentioned above focused on the perceptions of different financial statements’ using the mediators to determine the effect of audit fees on audit quality, this study will focus on the perception of the external auditors—as they are the provider of audit services—on the relationship between audit fees and audit quality. Therefore, the following research question is formulated to express about the topic of the study as follows:

Based on the perceptions of the external auditors, Is there a significant relationship between audit fees and audit quality through the mediators: total assets, origin of company, audit-firm size, complexity of operation in a company and auditor industry?

3. Literature review and hypotheses development

Several literatures from different contexts focused on the audit fees and audit quality. This study will highlight on the literatures that discussed audit fees and its effect on audit quality.

Jung et al. (Citation2016) aimed to examine how the association between abnormal audit fees and audit reporting quality improved after adoption of the International Financial Reporting Standards in South Korea. They used empirical data collected over the period from 2008 to 2013 where the study analyzed the relationship between unusually audit fees and audit reporting quality. The study used linear regression model to examine the proposed relation applying discretionary accrual as an indicator for audit reporting quality. The study showed that there is no significant association between unusually high audit fees and audit quality measured by the value of discretionary accruals in the pre-International Financial Reporting Standards adoption period. Although the association between unusually high audit process fees and the amount of discretionary accruals turns to be positive in the post-International Financial Reporting Standards adoption.

Hoitash et al. (Citation2007) aimed to examine if there was a link between auditor fees and audit quality from 2000 to 2003. The concept is based on the idea that effort and risk-adjusted fees, rather than the amount of fees collected from clients, impact auditor independence. Because risk and effort are unobservable, the authors estimated atypical fees using alternatives based on client size, complexity, and risk. Total fees were shown to have a statistically significant negative relationship with both audit quality proxies’ overall years in the study.

Ayoola (Citation2022) examined the relationship between audit fees and audit quality in Nigerian commercial banks. Moreover, the study used audit seasonality as a mediator, the study demonstrated how the audit fees affect on audit quality. The study found that there is a mediating role between audit fees and audit quality in Nigerian commercial banks.

The analysis discovered a statistically significant negative relationship between total fees and the overall years of both audit quality indicators. These results hold up to a range of further tests as well as various design standards. The findings (before and post SOX) support the hypothesis that economic situation, rather than the certified public accountant reputational interests, is a predictor of an external auditor demeanor.

Mitra et al. (Citation2009) aimed to report on audit quality variations amongst audit companies. They investigated the assumption of significant audit quality variations between big audit-firms (Big 4s) and small and medium enterprises. Based on qualitative data from certified public accountants, credit analysts, and board of directors as well they established scales for assessing perceived audit quality in the financial services sector. The authors used cross-case analysis to depict audit quality dimensions and scales based on the 13 recorded interviews. The authors then employed measurement scales to collect quantitative data in the financial services sector and used a MannWhitney U test to look for differences in perceived audit quality between audit firms. Findings showed that audit quality is a multi-dimensional construct that includes levels of discretionary accruals, audited account compliance with financial accounting standards, act, and rules, and audit fees. They concluded that Big-4 audit firms ensure better compliance with financial accounting standards, act, and other requirements than small and medium enterprises based on these measurements. When all three audit quality parameters are considered together, no major differences in audit reporting quality levels between Big-four and small and medium enterprises are found.

Fafatas and Sun (Citation2010) tested the association between country-level market shares of Big-4 audit firms and audit fees in nine emerging market economies. Audit Analytics is being utilized to acquire audit fee data for a group of foreign corporations which are listed on the United States exchange. The regression analysis was used on a final sample of 483 client. According to the survey, Big-4 auditors with large country-level market shares earn a fee premium of about 27% over competitors.

Mansur et al. (Citation2021) investigated the perceptions of external auditors in terms of the influences on audit fees. Findings revealed that there is a considerable positive association between firm origin and audit fees, where regional and international corporations paying greater audit fees than local ones. Furthermore, the findings demonstrated a significant positive association between overall assets, profitability, and audit fees. In contrast, the study demonstrated that no statistically significant association between audit fees and complex of operation.

Salehi et al. (Citation2019) examined the stickiness and changes of audit fees in Iran’s market using the influential factors such as auditor specialization, auditor tenure and auditor size. They used the multiple regression model and found that there is no significant relationship between audit quality and audit fees using the three mediators.

Campa (Citation2013) examined whether Big-4 audit firms showed a extra fees and, whether the extra fees are related to provide of better audit services. The authors used regressions such as univariate and multivariate analysis. Results offered consistent proof about the existence of an extra audit fee paid to Big-4 audit firms while they did not show any significant association between audit reporting quality and type of certified public accountants.

Lyubimov (Citation2019) examined the impact of audit firm-size and compliance on how audit fees have been changing over time. The study used regression model to analyze the relationship between audit fee changes and audit firm-size. The study found that compliant companies experience a higher external audit fees if they are audited by Big four audit-firms than.

In the United States external audit market, Nagy (Citation2014) investigated the effects of partner specialization on external audit fees. The author takes advantage of the one-of-a-kind situation produced by Andersen’s demise to investigate the impact of partner specialization on external audit fees. A sample of ex-Andersen clients who presumably followed their ex-Andersen audit partner to the new audit business was used to construct a least squares regression. The findings revealed a substantial positive relationship between external audit partner and office-level specialization, and external audit fees.

Choi et al. (Citation2010a) investigated whether and how the size of an audit firm is important, determining audit reporting quality and audit fees through audit firm-size and auditor industry. Findings revealed that the firm-size has significantly positive associations with both audit quality and audit fees. These positive relationships support the point of view that big local firms deliver higher quality audit compared with small ones, and that such prices for audit fees different for audit services.

Choi et al. (Citation2010b) investigated whether audit quality proxied by the amount of discretionary accruals is correlated with unusual external audit fees, The findings of regression analysis showed that the relationship between the two dimensions is asymmetric, depending on the unusual audit fees. Regarding the observations with negative unusual external audit fees, there is no significant relationship between audit reporting quality and unusual audit fees. In contrast, unusual audit fees are negatively correlated with audit reporting quality. Results proposed that external auditors’ incentives to prevent biased in the financial reporting quality, depending on in case their clients pay out more or less than the standard external audit fees.

Francis and Yu (Citation2009) examined a sample of The United States companies audited by Big four audit firms based on idea that Big four audit firms are expected to provide better quality audits Results were consistent with big firms delivering higher quality audits. Particularly, big firms are likely to issue going concern external audit reports, and clients in bigger firms evidence less violent in their behavior in terms of earnings management.

Zhoaan et al. (2022) examined how the relationship between audit fees and audit quality has changed after imposing penalties against uncommitted/ non-compliant audit firms. The study revealed that audit fees have been increased and audit quality has been improved by the suspended audit firms (compliant audit firms) relative to non-suspended audit firms in the two years of post-suspension.

Jensen and Payne (Citation2005) investigated the relationship between agency costs and audit services, and the relationship between audit services, audit quality, and audit fees. The researcher used a sample of municipal foundations. The authors noticed evidence that cities that depend more on their auditors to mitigate such costs, inclined to have better audit services. Furthermore, they noticed evidence that better audit services are correlated with the contracting of external auditors who have very good experience in a certain industry, reflective of higher audit quality. Finally, they found that well audit services have a marginal effect on audit fees; though, external audit services elements are related with external audit fees.

Azzam et al. (Citation2020) examined the effect of the relationship between external and internal audit on the quality of financial reporting. Findings demonstrated that Jordanian auditors viewed collaboration between internal and external auditors to improve financial reporting quality. Furthermore, the study showed that because of the favorable influence of technical expertise, the quality of financial reporting has improved.

Based on the related literature, hypotheses are formulated as follows:

H1: Audit fees have a positive effect on audit quality by using the total assets of an audited company as a mediate variable.

H2: Audit fees have a positive effect on audit quality by using the origin of an audited company as a mediate variable.

H3: Audit fees have a positive effect on audit quality by using the audit firm-size as a mediate variable.

H4: Audit fees have a positive effect on audit quality by using complexity of operation of an audited company as a mediate variable.

H5: Audit fees have a positive effect on audit quality by using the auditor industry as a mediate variable.

4. Materials and Methods

This paper is analytical, provides a literature review and discussion about the perceptions of external auditors on the relationship between audit fees and audit quality. It synthesizes the existing literatures between audit fees and audit quality. To attain the objective of research, the sample of the study was purposiveness. Bougie and Sekaran (Citation2019, p. 192) define sampling “process as selecting a sufficient number of elements from population”. Accordingly, the survey was distributed on licensed Jordan Certified Public Accountants (JCPA) who works in whether local or international audit firms in Jordan, 90 questionnaires were distributed through email, 73 questionnaires were returned, yield a percentage of 81 %. The main goal of this survey is to broaden the research in the same field for further studies in different context.

The questionnaire consists of 18 statements (as shown in the appendix). The first two statements represent the first mediate variable (total assets), statements 3 and 4 represent the second mediate variable (origin of a company), statements 5–7 represent the third mediate variable (audit firmsize), statements 8 and 9 refer to the complexity of operations, auditor industry represented in statements 10 and 11, statements 12–14 represents the independent variable (audit fees). Finally, the dependent variable (audit quality) was measured over the statements 15–18.

Fifth-Likert scale was used to weigh external auditors’ responses, where 1 represents strongly disagree and 5 represents strongly agree.

Descriptive analysis and multiple regression were used to analyze the collected data. The researchers used the hierarchical regression to specify the probability value with and without the five mediators.

Based on the above, Multiple-regression model was molded as the following:

4.1. AUDQUALITY = α + β1 TOTALAS + β2 OCOMP + β3 AUDFSIZE + β4 COMPlEX + β5 AUDINDUSTRY + β6 AUDFEES + ε

Where; α: Constant

AUDQUALITY: Audit Quality

TOTALAS: Total Assets

OCOMP: Origin of Company

AUDFSIZE: Audit Firm Size

COMLEX: Complexity of operations in a Company

AUDINDUSTRY: Auditor’s Industry AUDFEES: Audit Fees

ε: Error term

The authors prepared a model design to illustrate the association between independent variable, mediators and dependent variable as follows:

5. Results

A reliability test is used to check if the main six items are reliable through Cronbach’s alpha. According to Hair et al. (Citation2011), if Cronbach’s alpha is above 60 percent, the instrument of the study is deemed to be accepted. Before distributing the questionnaire, three academic professors were asked to give their feedbacks about the clarity of the items, which have been taken in to account.

shows the reliability coefficients for the items which exceeds than 70 percent as follows:

Table 1. Reliability coefficients

The next step in analysis, the authors entered the valid responses, analyzed data between independent variable and dependent variable without mediators to get the descriptive analysis, model summary, ANOVA and coefficient.

As shown in , descriptive analysis shows that the mean in term of audit quality and audit fees responses were 3.35 and 3.27 respectively which exceeds than the mean (3), where standard deviations were 0.55 and 0.59 respectively.

Table 2. Descriptive Statistics

As shown in , value of R square 0.012, which means that audit fees (alone) without mentioning other variables (mediators) can’t explain the relationship between audit fees and quality.

Table 3. Model Summary

In , ANOVA shows that significance value 0.348 which mean that there is no significant relationship between independent (audit fees) and dependent variable (audit quality) in case of testing the relationship without mediators.

Table 4. ANOVAa

As shown in , it confirms the previous result that there is insignificant relationship between audit fees and audit quality where Sig. 0.348 which exceeds than 0.05.

Table 5. Coefficients

To test the model, authors used a hierarchical regression model, where the five meditators entered between independent variable and dependent variable in order to test if there is any change in the relationship and the entire model through R square changed.

As shown in , R square in multiple-regression model increased to 0.164 after the authors had entered the five mediators to the model. This value (R square) means that it can predict and explain 0.164 from the relationship between independent and dependent variables. Shows that there is a statistically significant relationship when the five mediators had been entered to the regression model, where Sig. 0.045.

Table 6. Model Summary

Table 7. ANOVAa

Table 8. Coefficientsa

H1: Audit fees have a positive effect on audit quality by using the total assets of an audited company as a mediate variable.

The result shows that B value 0.43 (Sig. 0.57) which means that audit fees are insignificantly and don’t increase audit quality by using the total assets as a mediate variable. Based on the result, the first hypothesis is not supported and become “audit fees don’t have a positive effect on audit quality by using the total assets of an audited company as a mediate variable”.

H2: Audit fees have a positive effect on audit quality using the origin of an audited company as a mediate variable.

As shown in , B value 0.156 (Sig. 0.83) which means that audit fees are insignificantly and not positively increase audit quality by using the origin of company as a mediate variable. Based on the result, the second hypothesis also is not supported and become “audit fees don’t have a positive effect on audit quality by using the origin of an audited company as a mediate variable.

H3: audit fees have a positive effect on audit quality by using the audit firm-size as a mediate variable.

The result in shows that B value 0.349 (Sig. 0.003) which means that audit fees are significantly and positively increase audit quality by using audit firm-size as a mediate variable. Based on the result, the third hypothesis is supported.

H4: audit fees have a positive effect on audit quality by using complexity of operation of an audited company as a mediate variable.

As shown in , B value 0.36 (Sig. 0.785) which means that audit fees are insignificantly and not positively increase audit quality by using the complexity of operations as a mediate variable. Based on the result, the fourth hypothesis is not supported and become “audit fees don’t have a positive effect on audit quality using the complexity of operations as a mediate variable”.

H5: audit fees have a positive effect on audit quality by using the auditor industry as a mediate variable.

The result in exhibits B value 0.12 (Sig. 0.903) which means that audit fees are insignificantly and not positively increase audit quality by using audit industry as a mediate variable. Based on the result, the fifth hypothesis is not supported and become “audit fees don’t have a positive effect on audit quality by using the complexity of operations as a mediate variable”.

6. Discussion and conclusion

Where some studies mainly focused on the direct effect of audit fees on audit quality, other studies consider some of mediators such audit seasonality fees, audit tenure and auditor specialization. In contrast, this study focused on the factors that were expected to play a big role one the relationship between audit fees and audit quality.

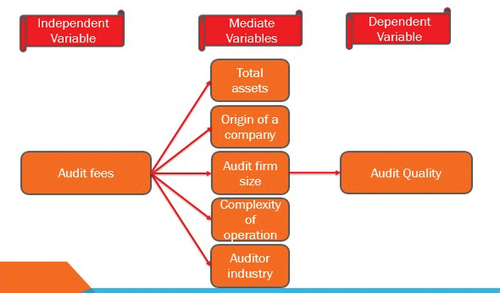

Accordingly, this study highlighted on the perceptions of external auditors on the relationship between audit fees and audit quality in Jordan, taking into consideration the effect of five mediate variables on this relationship: total assets origin of a company, audit firm-size, complexity of operation and auditor industry ().

Figure 1. The relationship between audit fees and audit quality through mediate variables.

The study found that the external auditors believes that audit fees are engaged more with audit firm-size, where this mediate variable has a significant influence on the relationship between audit fees and audit quality. In other words, the external auditors perceive that companies in Jordan are paying higher audit fees to big audit firm as they (companies) assume that they will get better audit quality.

The perceptions of Jordan certified public accountants didn’t agree that total assets, origin of a company, complexity of operations and auditor industry affect on the relationship between audit fees and audit quality.

Based on the above, the reason that audit fees are paid more to big audit firm-size could be explained that big audit firms have more reputation (whether local, regional or international firms), and provide better audit services, as clients (audited companies) prefer to get better audit quality as they believe that big audit firms are engaged with audit quality as well as they are ready to pay higher audit fees to the largest auditors’/audit firms only. This point could be explained that audited companies in Jordan are still affecting with the aura of big-four and other international audit firms regardless other the factors that might play a big role in enhancing the quality of audit process such as auditors’ industry/specialization and complexity of operations. In contrast, we have to take into account that big audit firms have certified auditors with professional certificates such as CPA, Chartered, etc. …, those professional and certified auditors mostly get higher salaries and remunerations. Hence, the big audit firms expect those certified external auditors to provide better audit services—which be reflected on its reputation—more than their counterparts who are not having professional certificates.

Furthermore, the big audit firms usually adopt and use audit software and audit tools to implement its audit processes. Using these audit software and tools need cost and time to qualify the professional auditors to have the technical expertise. In a nutshell, the big audit firms have higher operating expenses, especially these expenses which are devoted for audit process and qualifying their professional auditors.

Finally, it’s fair to mention that several Jordanian audited companies, especially multinational companies and those companies which look mainly for foreigner investors are obliged by their parent companies to have certified public accountants from big-four and other international audit firms.

correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

The authors report there are no competing interests to declare.

Additional information

Funding

Notes on contributors

Hasan Mansur

Hasan Mansur is an Assistant Professor at Accounting department, faculty of business - Applied Science Private University (ASU). Dr. Mansur holds PhD in accounting from Szent István University - Hungary by a scholarship from Tempus Public Foundation - European Union (TPF-EU).

[email protected], https://orcid.org/0000-0003-0806-4589

Abdul Aziz Abdul Rahman

Abdul Aziz Abdul Rahman is an Associate Professor and Chairperson of Finance & Accounting, College of Business Administration, Kingdom University, Bahrain. Dr. Abdul Rahman holds PhD in Economics/Accounting from Damascus University- Syria. [email protected], https://orcid.org/0000-0003-4967-6223

Abdelrhman Meero

Abdelrhman Meero is an Associate Professor and acting dean of Finance & Accounting, College of Business Administration, Kingdom University, Bahrain. Dr Meero holds PhD in Management Sciences-Finance and Banking 2007. University of Montesquieu Bordeaux/France. [email protected]

Ahmad Shatnawi

Ahmad Shatnawi is an Assistant Professor at Accounting department, faculty of business - Applied Science Private University (ASU). Dr. Shatnawi holds PhD in accounting from the Queensland University of Technology in Australia, awarded the commonwealth-funded postgraduate research scholarship to study PhD program. [email protected]

References

- Abdul-Rahman, O. A., Benjamin, A. O., & Olayinka, O. H. (2017). Effect of audit fees on audit quality: Evidence from cement manufacturing companies in Nigeria. European Journal of Accounting, Auditing and Finance Research, 5(1), 6–14.

- Arens, A. A. (2012). Auditing and assurance services: An integrated approach. Pearson Education, Inc. Pearson Prentice Hall, Upper Saddle River, New Jersey, 07458. 14 edition. ISBN 13: 978-0-13-257595-9.

- Ayoola, T. J. (2022). Audit fees, audit seasonality and audit quality in Nigeria: A mediation analysis. Journal of Financial Reporting and Accounting. (Ahead of print.). https://doi.org/10.1108/JFRA-01-2022-0010

- Azzam, M., Alrabba, H., AlQudah, A., & Mansur, H. (2020). A study on the relationship between internal and external audits on financial reporting quality. Management Science Letters, 10(4), 937–942. https://doi.org/10.5267/j.msl.2019.10.001

- Bougie, R., & Sekaran, U. (2019). Research methods for business: A skill building approach. John Wiley & Sons.

- Cahan, S. F., & Sun, J. (2015). The effect of audit experience on audit fees and audit quality. Journal of Accounting, Auditing & Finance, 30(1), 78–100. https://doi.org/10.1177/0148558X14544503

- Campa, D. (2013). “Big 4 fee premium” and audit quality: Latest evidence from UK listed companies. Managerial Auditing Journal, 28(8), 680–707. https://doi.org/10.1108/MAJ-112012-0784

- Chartered Accountants. (2019). Audit quality. https://www.charteredaccountantsanz.com/member-services/technical/audit-andhttps://www.charteredaccountantsanz.com/member-services/technical/audit-and-assurance/audit-qualityassurance/audit-quality

- Choi, J.-H., Kim, C., Kim, J.-B., & Zang, Y. (2010a). Audit office size, audit quality, and audit pricing. Auditing: A Journal of Practice & Theory, 29(1), 73–97. https://doi.org/10.2308/aud.2010.29.1.73

- Choi, J.-H., Kim, J.-B., & Zang, Y. (2010b). Do abnormally high audit fees impair audit quality? Auditing: A Journal of Practice & Theory, 29(2), 115–140. https://doi.org/10.2308/aud.2010.29.2.115

- Corbella, S., Florio, C., Gotti, G., & Mastrolia, S. A. (2015). Audit firm rotation, audit fees and audit quality: The experience of Italian public companies. Journal of International Accounting, Auditing and Taxation, 25, 46–66. https://doi.org/10.1016/j.intaccaudtax.2015.10.003

- De Fuentes, C., Illueca, M., & Pucheta-Martinez, M. C. (2015). External investigations and disciplinary sanctions against auditors: The impact on audit quality. SERIEs, 6(3), 313347. https://doi.org/10.1007/s13209-015-0127-0

- Fafatas, S. A., & Sun, K. J. (2010). The relationship between auditor size and audit fees: Further evidence from big four market shares in emerging economies. In M. Tsamenyi & S. Uddin (Eds.), Research in Accounting in Emerging Economies (Vol. 10, pp. 57–85). Emerald Group Publishing Limited.

- Farlex Financial Dictionary. (2009). Audit fees. https://financialhttps://financial-dictionary.thefreedictionary.com/Audit+Feesdictionary.thefreedictionary.com/Audit±Fees

- Feng, Z., Li, L. Z., Wong, H. Y., & Wong, J. (2022). Regulatory intervention and audit quality: New evidence from audit firm suspension. Meditari Accountancy Research. https://doi.org/10.1108/MEDAR-07-2021-1372

- Firth, M. (1997). The provision of non audit services and the pricing of audit fees. Journal of Business Finance & Accounting, 24(3), 511–525. https://doi.org/10.1111/1468-5957.00118

- Francis, J. R. (2004). What do we know about audit quality? The British Accounting Review, 36(4), 345–368. https://doi.org/10.1016/j.bar.2004.09.003

- Francis, J. R., & Yu, M. D. (2009). Big 4 office size and audit quality. The Accounting Review, 84(5), 1521–1552. https://doi.org/10.2308/accr.2009.84.5.1521

- Hair, J.,sJr, Celsi, M., Money, A., Samouel, P., & Page, M. (2011). Essentials of business research methods. Rouledge.

- Hoitash, R., Markelevich, A., & Barragato, C. A. (2007). Auditor fees and audit quality. Managerial Auditing Journal, 22(8), 761–786. https://doi.org/10.1108/02686900710819634

- IAASB. (2019). Audit quality https://www.ifac.org/system/files/meetings/files/6086_0.pdf

- IFAC. (2019). Focus on Audit Quality. https://www.iaasb.org/focus-audithttps://www.iaasb.org/focus-audit-qualityquality

- Jensen, K. L., & Payne, J. L. (2005). Audit procurement: Managing audit quality and audit fees in response to agency costs. Auditing: A Journal of Practice & Theory, 24(2), 27–48. https://doi.org/10.2308/aud.2005.24.2.27

- Jung, S.-J., Kim, B.-J., & Chung, J.-R. (2016). The association between abnormal audit fees and audit quality after IFRS adoption: Evidence from Korea. International Journal of Accounting & Information Management, 24(3), 252–271. https://doi.org/10.1108/IJAIM-072015-0044

- Kuntari, Y., Chariri, A., & Nurdhiana, N. (2017). The effect of auditor ethics, auditor experience, audit fees and auditor motivation on audit quality. Sriwijaya International Journal of Dynamic Economics and Business, 1(2), 203–218. https://doi.org/10.29259/sijdeb.v1i2.203-218

- Lyubimov,A. (2019). How do audit fees change? Effects of firm size and section 404(b) compliance. Managerial Auditing Journal, 34(4), 393–433. https://doi.org/10.1108/MAJ-072018-1938

- Mansur, H., AbdulRahman, A. A., Azzam, M., Meero, A., Alqudah, A., & Alrabba, H. (2021). The perceptions of external auditors about the influential factors on audit fees: An empirical study from Jordan. Journal of Legal, Ethical and Regulatory Issues, 24(1), 1–10.

- Mitra, S., Deis, D. R., & Hossain, M. (2009). The association between audit fees and reported earnings quality in pre and post Sarbanes Oxley regimes. Review of Accounting and Finance. 8(3), 232–252.

- Nagy, A. L. (2014). Audit partner specialization and audit fees. Managerial Auditing Journal. 29(6), 513–526.

- Nassar, M., Warrad, L. H., & Nassar, M. (2017). The Impact of the Practice of Earnings. Management on Financiers’ Decisions and the Role of Audit Quality as a Moderator Variable: Evidence from Manufacturing Companies Listed on Amman Stock Exchange. International Journal of Academic Research in Business and Social Sciences, 7(11), 2222–6990.

- Salehi, M., Komeili, F., & Gah, A. D. (2019). The impact of financial crisis on audit quality and audit fee stickiness: Evidence from Iran. Journal of Financial Reporting and Accounting, 17(2), 201–221. https://doi.org/10.1108/JFRA-04-2017-0025

- Warrad, L. H. (2017). Does listed jordanian manufacturing firms’ profitability and size affecting external audit fees? International Journal of Academic Research in Business and Social Sciences, 7(9), 2222–6990. https://doi.org/10.6007/IJARBSS/v7-i9/3312

- Warrad, L. H. (2018). Audit partner tenure, audit quality and audit fees: Evidence from Jordanian Firms. International Journal of Business and Social Science, 9(10), 163–172. https://doi.org/10.30845/ijbss.v9n10p16