Abstract

The present study endeavours to perform a systematic review of the literature related to the impact of corporate governance on dividend policy in the last two decades. This study uses the systematic literature review process . 143 articles were identified initially and subsequently further narrowed down to 66 most relevant articles for the scope of this study. This paper critically examines the influential studies in the literature related to the impact of corporate governance on dividend policy. The literature review related to corporate governance is analysed from two broad perspectives i.e. (a)Impact of Shareholder protection on dividend pay-out and (b) Impact of Controlling stakeholders on dividend pay-out. Our findings are as follows. Firstly, a vast majority of studies have found a positive relationship between better corporate governance practice and higher dividend pay-out. Secondly, the study finds that the majority of the research has been done in the USA and Europe while limited studies have focussed on emerging markets. Finally, our reviews show that there is a dearth of studies that evaluate the impact of the structural changes in corporate governance in various emerging markets. This study contributes to the extant literature in several ways. It highlights the research gaps in this field and provides a potential agenda for academicians and research organizations for future research.

1. Introduction

Dividend policy is the internal yardstick a company uses to decide how much of the company income it will distribute to the shareholders. Dividend policy is one of the core corporate finance decisions that firms must make. From the time of Lintner’s (Citation1956), there have been many studies to understand the importance of managed dividend policy in creating firm value, but dividend policy remains an unsolved puzzle.

There is no definitive answer to the perennial question “Whether dividend creates or destroys firm value”. Dividend policy has a pivotal role to play in corporate finance as it is a double-edged sword. While dividend distribution is a reward for the loyal shareholders who have invested in the company, at the same time it depletes the internal capital availabl to the company. Thus, dividend strategy is intertwined with other core investment and financing decisions of a firm and has a far-reaching impact on shareholders’ value maximization.

Lintner (Citation1956) is considered as the founder of modern empirical research on dividend theory. He stated that firms resort to longstanding, stable dividend pay-out ratios and managers avoid making dividend changes that might be reversed in near future. Thus, firms smoothen their dividends and dividends are sticky. Many empirical studies have demonstrated that dividends paid out in a year depend on two important parameters, namely the current earnings and the previous year’s lagged dividends. Some of the studies which have explored dividend policy from this angle are Fama and Babiak (Citation1968), Baker (Citation1999), Dhanani (Citation2005), and Brav et al. (Citation2005), Garrett and Priestley (Citation2012), and Gordon (Citation1959) proposed the “bird in hand” hypothesis. According to this hypothesis, shareholders prefer a certain current cash dividend as opposed to an uncertain future dividend. Shareholders will thus value current dividends higher than future capital gains which are uncertain.

Miller and Modigliani (Citation1961) were the first to question the notion of maximization of firm value through higher dividend pay-outs. They concluded that managed dividend policy cannot create additional firm value beyond the value created by the investment policy. In a perfect world without frictions like taxes or bankruptcy costs, dividend policy is immaterial and does not contribute to creating firm value. Investors can resort to homemade dividends to mimic the expected cash flow from the dividend stream.

Black (Citation1976) attempted to understand two basic questions: “Why do firms pay dividends at all?” and “Why do shareholders prefer stocks that pay dividends?” According to him, in the presence of a differential tax penalty for dividends compared to capital gains, it did not make sense for firms to pay dividends as it led to value destruction.

Jensen and Meckling (Citation1976) explored the various areas which give rise to agency conflicts. Even though managers are expected to act as agents to utilize the assets on the behalf of shareholders with the objective to maximize their wealth, many a time in real-world managers behave contrarily; they resort to resource tunnelling and divert the firm’s assets for their personal gains.

Rozeff (Citation1982) and Easterbrook (Citation1984) stated that dividends play a vital role in addressing the agency issue. Steady dividend pay-outs force managers to reach out to the capital market for external financing whenever more capital is needed. This enables the prospective shareholders and the existing shareholders to scrutinize the performance and the intentions of the management team.

Bhattacharya (Citation1979) constructed a two-period signalling model, which demonstrated that in the presence of information asymmetry, changes in dividend pay-out signal the firms’ future profitability and expected cash flows to the market. John and Williams (Citation1985) and M. E. Miller and Kevin (Citation1985) also constructed signalling models to analyse whether dividends signal the future. The assumption is that only financially sound firms can afford to declare dividends and firms which are not that well-off cannot use dividends as a signalling tool. Thus, shareholders put a premium on dividend-paying firms as they signal a better future.

Each firm has different stages in its life cycle. During the early stage of a newly incorporated firm, there exists ample scope for future growth and consequently, there is a significant requirement for capital. In such a scenario, it is prudent to retain earnings as capital rather than distribute them as dividends. As the firm enters the maturity stage, the demand for capital for investment reduces drastically, which helps in the accelerated build-up of free cash reserves. Some of the important studies related to the life cycle theory of dividend payment are Mueller (Citation1972), Fama and French (Citation2001), Grullon et al. (Citation2002), and DeAngelo et al. (Citation2006), and Coulton and Ruddock (Citation2011).

The behavioural dividend theory was first proposed by Shefrin and Statman (Citation1984) to explain the phenomenon of why shareholders prefer dividend-paying stocks. Many shareholders are not able to delay gratification and are forced to sell shares to fund their consumption requirements which can be avoided if the stocks pay dividends on a regular basis. Thus, they prefer to own stocks that pay steady dividends. Baker and Wurgler (Citation2004) further developed the catering theory by making it time-varying. They argued that shareholders’ demand for dividends varies with time.

1.1. Corporate governance and dividend policy

The term corporate governance can be interpreted in either a narrow sense or a broad sense. From the perspective of this study, corporate governance is defined in a broad sense, which basically encompasses a set of practices by which organizations are controlled, directed, and governed. The most important objective of corporate governance is to enable an environment whereby the organization’s top management acts in the interest of the organization and its stakeholders, thus mitigating the agency cost. Figure explains the reason for the agency cost which arises due to the divergence of objectives between the shareholders and the top management. Several studies over the past decades have explored the impact of corporate governance on the dividend policy of a firm.

Figure 1. Divergence of objectives.

The impact of the quality of corporate governance on dividend policy has been researched in detail over the years. While many studies found that a robust corporate governance culture acts as a catalyst for higher and increased dividend pay-outs (Michaely & Roberts, Citation2006; La Porta et al., Citation2000; Renneboog & Szilagyi, Citation2015), some contrasting studies have found the reverse to be true (Jo & Pan, Citation2009; Nielsen, Citation2006; Officer, Citation2007).

Studies have found evidence of minority stakeholders’ protection having a positive impact on higher dividend pay-out. La Porta et al. (Citation2000) did a pioneering study of dividend policy in 33 countries and found strong evidence of a direct link between larger dividend payments and stronger shareholder protection. They put forward and tested two agency models related to the payment of dividends. The first model, called the substitution model, suggests that firms with weaker shareholder protection and rights tend to pay a large amount as dividends to mask and protect their reputation in the market. To summarise, according to the substitution model, dividends act as a substitute for minority shareholder rights and firms use dividend payments to counter the perception of shareholder exploitation.

The second model, known as the outcome model, suggests just the opposite: dividends are paid as a by-product of stronger norms regarding minority shareholders’ protection which leads to shareholder activism pressurizing the firms to distribute large dividends.

La Porta et al. (Citation2000) demonstrated that well-managed firms with better shareholder protection culture, generally resort to higher pay-outs. Similar results favouring the outcome model were reported by Michaely and Roberts (Citation2006), who performed a comparative study on British firms. Their study found that public firms, which by regulations were mandated to adhere to tougher shareholder protection norms, paid significantly higher dividends as compared to private firms.

Similarly, an efficient and strong legal system is essential for shareholder protection and helps in ensuring dividend payments by reducing the scope for agency problems in the firms. Mitton (Citation2004) examined the cascading impact of corporate governance on dividend policy, first at country level and then at firm level. For the purpose of his study, he used a sample of 365 firms spread across 19 countries. He used the type of legal systems as the proxy or indicator of the level of shareholder protection prevalent in a country. He found that firms located in common law countries made larger dividend pay-outs compared to the firms located in civil law countries, which was in sync with the findings of La Porta et al. (Citation2000). Additionally, he found that firms within the same country, which followed a better corporate governance practice, paid higher dividends than their counterparts.

Subsequent studies by Von Eije and Megginson (Citation2008) and Denis and Osobov (Citation2008) also supported the “outcome hypothesis”. On the contrary,) Jo and Pan(Citation2009) in their study found evidence of “substitution model”, i.e., dividend was paid out as a substitute for weaker shareholder rights.

Thus, the contrasting impact of corporate governance on dividend pay-out makes it difficult to understand its scope and measurement from the dividend policy perspective. Hence, a detailed literature review is necessitated to better understand this important subject. The purpose of this research paper is to present a systematic literature review (SLR) of the impact of corporate governance on dividend pay-out. SLR methodology will be instrumental in creating a justifiable synthesis of the existing evidence related to the variables under study. Furthermore, this SLR will help to identify the existing research gaps and define the future area of research. The impact of corporate governance on dividend policy is primarily examined in this SLR through the prism of a) shareholders’ protection and b) controlling stakeholders (especially owners). The two important research questions of interest, addressed in our present study are as follows:

What is the impact of shareholder protection on dividend pay-out?

What is the impact of controlling stakeholders on dividend pay-out?

2. Review methodology

To evaluate the contributions of previous studies; a focussed analytical review strategy is of paramount importance. The present study uses the five-stage process for performing a systematic literature review (SLR) . The five steps are as below:

Define scope of SLR

Search strategy formulation

Screening/Filtering criteria

Quality assessment procedure

Data reporting and analysis

2.1. Scope and objectives of SLR

The primary purpose of the present study is to perform exploratory analysis followed by categorization and synthesis of the existing studies related to Corporate Governance and Dividend policy.

2.2. Search strategy (review protocols)

The keywords defined for the purpose of the Search strategy are “Corporate Governance”, “Dividend Policy”, “Minority Shareholders”, “Agency Cost” and “Ownership”. Different Boolean search operators were used to extract the required studies from the various databases. “AND” was used to connect different constructs and narrow down the search. “OR” was used to expand the search. Truncation was used for root word search. We conducted a structured electronic search of articles to explore existing literature. Reputed databases like SAGE, Taylor and Francis, Elsevier (ScienceDirect), and JSTOR were explored using search strings constructed from the keywords. We put a limit on the time period under consideration for the study and included those articles which were published from 2000 to 2021. We applied the process of forward (further cited articles) and backward (reference articles) search and finally the search resulted in 143 articles. explains in detail the Boolean search parameters.

Table 1. Boolean search

2.3. Screening

Only full papers published in academic journals were considered. Conference papers and workshop papers were excluded from the purview of the present study. The articles not published in English and paid articles were excluded. Initial screening of articles was done by reviewing the title, abstract, keywords, and findings to understand if it deals with the scope of this study, namely the impact of corporate governance on dividend policy. Finally, 66 articles were shortlisted to be analysed in the study.

2.4. Quality assessment

The quality assessment of the articles for inclusion in the literature review was based on two parameters. The first criterion was the publishing source, and the second criterion was the content relevancy. Only the articles published in journals ranked in either Q1 or Q2 quartiles according to Scimago Journal & Country Rank index are considered for further evaluation. The full text of all the 66 articles was thoroughly examined to determine whether the papers were eligible to be considered for this study. The authors individually assessed the relevance of the articles for inclusion and excluded irrelevant ones.

2.5. Data reporting and analysis

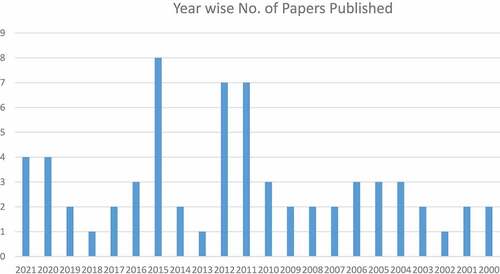

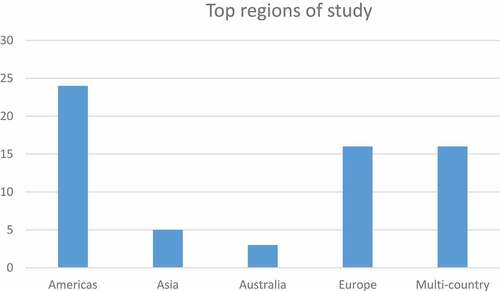

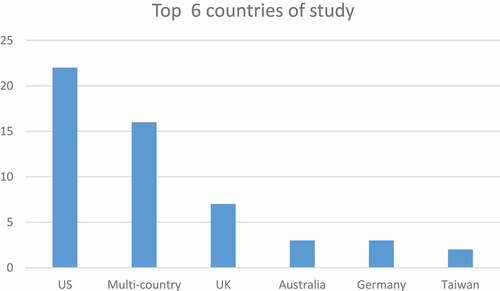

In depth analysis of the metadata for the selected papers was performed. Most of the papers are empirical in nature. The majority of the studies have used longitudinal data and are based on panel data analysis. There are two broad corporate governance spectra under which the majority of the studies have been undertaken. One major theme is evaluating the impact of agency cost including stakeholder protection on dividend policy and the other theme examines the effect of controlling stakeholders on dividend policy. We have also analysed the data from the year-wise publication perspective and countries where the sample was taken. As can be seen from Figure , a major portion of the papers have been published between 2010 to 2015 which appears to be a very productive phase. The Americas and Europe are the regions where the majority of the research has been conducted. Thus, it can be safely concluded that most of the research has happened in developed countries. Further, Figure demonstrates that the US is the top preferred choice as a country for the studies while there are hardly any studies in the ASEAN and other emerging market economies. provides a graphical view of the top six countries of study.

Figure 2. Year wise No. of papers published.

Figure 3. Top regions of study.

Figure 4. Top 6 countries of study.

3. Systematic literature review and findings

In the present study, the literature review related to corporate governance is analysed from two broad angles i.e. (a)Impact of Shareholder protection on dividend pay-out and (b) Impact of Controlling stakeholders on dividend pay-out. The SLR found that there was a steady increase in the number of published studies related to the impact of corporate governance on dividend pay-out after the financial crisis of 2007–2008. Most probably this was driven by the overall increase in interest to explore the mitigating role of corporate governance to prevent financial fraud.

3.1. Methodology and tools used

The three main methodologies used in the published articles are empirical, theoretical/conceptual, and survey-based. Out of these methodologies, the most dominant one is the empirical methodology which is used in more than 90% of the studies. SLR also reveals that Panel regression is the dominant tool used in the majority of empirical papers. Tobit, Logit, and Probit models are frequently used along with panel regression. Tran (Citation2020) while exploring the impact of corruption on dividend pay-out uses both Logit and Tobit, models. Alzahrani, & Lasfer (Citation2012), Atanassov & Mandell (Citation2018), Knyazeva, & Knyazeva (Citation2015), Martins & Novaes (Citation2012), and Renneboog and Szilagyi (Citation2015) are some other studies which have used Tobit or Logit models. Two important conceptual studies are by Allen et al. (Citation2000) and Mori and Ikeda (Citation2015). Both papers explored the impact of ownership structure on dividend pay-out. Chen, Leung, & Goergen (Citation2017) and Hossain, Hossain, & Kryzanowski (Citation2021) used Propensity score matching and Instrument variable approach in their studies while Barros et al. (Citation2021), Brockman, Tresl, & Unlu (Citation2014) and Michiels, Voordeckers, Lybaert, & Steijvers (Citation2015) have used mixed methodology for the research conducted by them. Some of the studies have used Simultaneous equation methods for their research (e.g., Balachandran et al., Citation2019; Gugler, Citation2003).

3.2. Themes researched

Some of the important papers which investigated the impact of shareholders protection on dividend pay-outs are Alzahrani, & Lasfer (Citation2012), Atanassov & Mandell (Citation2018), Gugler and Yurtoglu (Citation2003), La Porta et al. (Citation2000), Michaely & Roberts (Citation2012) and Mitton (Citation2021., Citation2004 found that the presence of activist shareholders increases the probability of a firm paying dividends. Petrasek (Citation2012) studied how cross-listing of various international firms in the USA impacted their dividend policy. He found that cross-listing on exchanges that mandated higher standards of shareholder protection and financial transparency leads firms to increase the dividend payments by 9% as a percentage of their earnings. Renneboog and Szilagyi (Citation2015) performed an empirical sample study of 150 Dutch firms and concluded that firms pay comparatively smaller dividends when they operate in an environment of a restrictive governance regime.

Several empirical studies have explored the relationship between controlling stakeholders and dividend pay-out. A controlling stockholder or group is present in many public firms. In most cases, the controlling stake is owned by the members of the family that founded the firm (Claessens et al., Citation2000; Faccio et al., Citation2001). Claessens et al. (Citation2000) found that family control of listed firms was widespread in Asia and in Western European countries. Perez-gonzalez (Citation2002) similarly found that a firm’s dividend policy is influenced by the tax position of the controlling shareholders. Goergen et al. (Citation2004) in their study of German firms found a strong and material relation between dividends and the percentage of voting rights held by the largest equity shareholder.

Amihud and Murgia (Citation1997) studied the effect of bank control in German firms and found that it increases the probability that a firm will reduce or omit dividend payments. Gugler (Citation2003) examined the impact of state control of firms in Austria on their dividend policy and observed that in comparison to “family-controlled” firms, “state-controlled” firms had higher pay-out ratios. The study by Attig et al. (Citation2016) found that dividend payments by a firm were inversely related to family control and ownership of the firm. Pindado et al. (Citation2012) investigated the use of dividend policy as a corporate governance mechanism to overcome agency problems between the controlling family and minority investors in a sample of family firms from nine eurozone countries and found a positive correlation. Balachandran et al. (Citation2019) performed an in-depth study of Australian firms and concluded that insider ownership positively influences dividend policy. On the contrary, Wu et al. (Citation2020) researched Taiwanese firms and found that family-controlled firms pay lesser cash dividends than non-family-controlled firms. A recent paper by Goyal et al. (Citation2020) examined the impact of significant state ownership in privatized firms on the corporate dividend policy. They found robust evidence that the extent of state ownership positively influences dividend pay-outs.

3.3. Geographic orientation

Majority of the studies have been performed in developed countries especially US (e.g., Atanassov & Mandell,Citation2018; Chen, Leung & Goergen,Citation2017; Jiraporn, Kim & Kim,Citation2011; Knyazeva & Knyazeva,Citation2015; Sharma,Citation2011). Very few studies have been done in the ASEAN countries or other emerging economies like China, India, and Latin American countries (e.g., Faccio et al., Citation2001; Li, Zhou, Yan & Zhang,Citation2020; Martins & Novaes,Citation2012). Germany and U.K. are the two countries in the European region where multiple relevant research has happened over the years(e.g., Geiler & Renneboog, Citation2016; Goergen et al., Citation2004; Khan, Citation2006; Michaely & Roberts,Citation2012; Renneboog & Trojanowski, Citation2007). Some of the studies have done research across multiple countries. Ye et al. (Citation2019) did a multi-country study in 22 countries and discovered a robust positive relationship between the degree of gender diversity on the board and dividend pay-out. Tran (Citation2020) performed cross-country research in 47 countries and found that level of corruption increases the agency cost and thus leads to a higher probability of dividend payment. Truong and Heaney (Citation2007) did multi-country research and found that insider ownership reduces dividend pay-out.

4. Scope for research in future

Although there have been many studies related to the impact of corporate governance on dividend policy globally, there are certain under-explored areas, which can be taken up in future studies. The SLR finds that there is limited theoretical and empirical study to evaluate the impact of structural changes in the Corporate governance on dividend policy, which have been implemented in the last two decades, for e.g., there are no studies exploring the impact of the modification to Singapore corporate governance code in 2012 which mandates that majority of directors must be independent if the chairman of the board is not independent or the UK corporate governance code (Citation2014) which requires that risk management and internal control system is monitored by the board and at least once a year a review is carried out and reported in the annual report.

Future studies can focus on analysing the impact of major corporate governance structural changes, especially in emerging markets. Do the changes in corporate governance solicit shareholder activism? Do the minority shareholders have more say in the dividend policy of a company now as compared to earlier? Is the management now being forced to distribute excess cash, which cannot be profitably redeployed in the business? These are some of the mute questions to be carefully examined in the backdrop of the corporate governance changes happening across the world in various countries.

5. Conclusion

Despite numerous academic studies, dividend policy remains a puzzle. In the last two decades, a significant attempt has been made to understand dividend policy through the framework of corporate governance. This article attempted to present a review of the important literature related to the impact of corporate governance on dividend policy. We reviewed both the conceptual and empirical studies relating to various facets of corporate governance and its impact on dividend policy.

This paper contributes to the area of corporate governance and dividend policy in multiple ways. After analysing the existing literature on the topic, we find that corporate governance practices across various countries have a positive impact on the dividend pay-out which is in sync with the ideas expressed in the pioneering paper by La Porta et al. (Citation2000). We analysed the various papers to understand the methodology and tools used for the research and find that very few studies have used theoretical model or survey method for the purpose of their research.

The corporate governance framework has evolved and become robust with time. Due to the rapid evolution of corporate governance standards globally, especially those related to minority shareholder protection, companies may be more positively inclined to pay higher dividends. However, the present Systematic Literature Review found that there are limited studies examining the dividend policy from the perspective of minority shareholder protection, especially in emerging markets. The focus of the studies has been biased towards the developed countries with very few noteworthy studies undertaken in emerging economies.

Although the present study provides significant insight into the existing body of knowledge and identifies the future research scope still it suffers from some limitations. Firstly, this study uses the systematic literature review process advocated by Opoku et al. (2015) but the Boolean keywords used by us for filtering the papers are not exhaustive so it is possible that we might have missed out on defining some keywords. Secondly, the study has used the top-rated electronic databases like SAGE, Taylor and Francis, Elsevier (ScienceDirect), and JSTOR but there may be other databases containing excellent articles which could not be analysed in the present study. Finally, the present study has explored in detail the impact of insider ownership or family ownership and institutional ownership while touching upon some of the papers related to director ownership, block ownership, etc. Although the authors have diligently followed a systematic approach for the literature review still due to the inherent challenges of classifying the sample studies based upon certain criteria, there is the probability of some loss of information.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Debadatta Das Mohapatra

Debadatta Das Mohapatra is a PHD scholar in management. He is pursuing his PHD in finance from Xavier institute of Management, Bhubaneswar. His research interest is corporate dividend policy. He is exploring various areas like impact of Corporate Governance and Dividend taxation on corporate dividend policy in the Indian context. He is also pursuing his CFA charter and is currently a CFA level-2 candidate.

Pradiptarathi Panda

Pradiptarathi Panda is working as an Assistant Professor at the National Institute of Securities Markets (NISM), Mumbai. His areas of research interest’s Include-International Capital Markets, Innovative financial instruments, and Financial Economics. His teaching interests are Financial Institutions and Markets (FIM), Research Methods and Data Analytics, Financial Computing using R and Python, and Trading in equity & derivatives. He has published a number of research papers in indexed journals. He is a Guest Editor for Asia Pacific Financial Markets and reviewer for a number of finance journals including World Finance Conferences.

References

- Abreu J Filipe and Gulamhussen M Azzim. (2013). The stock market reaction to the public announcement of a supranational list of too-big-to-fail banks during the financial crisis. Journal of International Financial Markets, Institutions and Money, 25, 49–18. 10.1016/j.intfin.2013.01.003

- Adjaoud, F., & Ben-Amar, W. (2010). Corporate governance and dividend policy: Shareholders’ protection or expropriation? Journal of Business Finance and Accounting, 37(5–6), 648–667. https://doi.org/10.1111/j.1468-5957.2010.02192.x

- Al-Najjar B and Belghitar Y. (2014). Do corporate governance mechanisms affect cash dividends? An empirical investigation of UK firms. International Review of Applied Economics, 28(4), 524–538. 10.1080/02692171.2014.884546

- Allen, F., Bernardo, A. E., & Welch, I. V. (2000). A theory of dividends based on tax clienteles. The Journal of Finance, 55(6), 2499–2536. https://doi.org/10.1111/0022-1082.00298

- Allen L, Gottesman A, Saunders A and Tang Y. (2012). The Role of Banks in Dividend Policy. Financial Management, 41(3), 591–613. 10.1111/j.1755-053X.2012.01207.x

- Alzahrani M and Lasfer M. (2012). Investor protection, taxation, and dividends. Journal of Corporate Finance, 18(4), 745–762. 10.1016/j.jcorpfin.2012.06.003

- Amihud, Y., & Li, K. (2006). The Declining Information Content of Dividend Announcements and the Effects of Institutional Holdings. The Journal of Financial and Quantitative Analysis, 41(3), 637–660. http://www.jstor.org/stable/27647264

- Amihud, Y., & Murgia, M. (1997). Dividends, taxes, and signaling: Evidence from Germany. The Journal of Finance, 52(1), 397–408. https://doi.org/10.1111/j.1540-6261.1997.tb03822.x

- Atanassov J and Mandell A J. (2018). Corporate governance and dividend policy: Evidence of tunneling from master limited partnerships. Journal of Corporate Finance, 53, 106–132. 10.1016/j.jcorpfin.2018.10.004

- Attig, N., Boubakri, N., El, S., & Guedhami, O. (2016). The global financial crisis, family control and dividend policy. Financial Management, 45(2), 291–313. https://doi.org/10.1111/fima.12115

- Baker, H. K, Powell, G. E. (1999). How corporate managers view dividend policy? Quarterly Journal of Business and Economics, 38 (2) , 17–35 http://www.jstor.org/stable/40473257.

- Baker, M., & Wurgler, J. (2004). A catering theory of dividends. Journal of Finance, 59(3), 1125–1165. https://doi.org/10.1111/j.1540-6261.2004.00658.x

- Balachandran, B., Khan, A., Mather, P., & Theobald, M. (2019). Insider ownership and dividend policy in an imputation tax environment. Journal of Corporate Finance, 54(C), 153–167. https://doi.org/10.1016/j.jcorpfin.2017.01.014

- Barros, V., Verga Matos, P., Miranda Sarmento, J., & Rino Vieira, P. (2021). Do activist shareholders influence a manager’s decisions on a firm’s dividend policy: A mixed-method study. Journal of Business Research, 122, 387–397. https://doi.org/10.1016/j.jbusres.2020.08.048

- Bhattacharya, S. (1979). Imperfect information, dividend policy, and “The bird in the hand” Fallacy. Source: The Bell Journal of Economics, 10 (1) , 259–270. https://doi.org/10.2307/3003330

- Black, F. (1976). The dividend puzzle. Journal of Portfolio Management, 2(2), 5–8. https://doi.org/10.3905/jpm.1976.408558

- Brav, A., Graham, J. R., Harvey, C. R., & Michaely, R. (2005). Payout policy in the 21st century. Journal of Financial Economics, 77(3), 483–527. https://doi.org/10.1016/j.jfineco.2004.07.004

- Brockman P, Tresl J and Unlu E. (2014). The impact of insider trading laws on dividend payout policy. Journal of Corporate Finance, 29, 263–287. 10.1016/j.jcorpfin.2014.09.002

- Burns N, McTier B C and Minnick K. (2015). Equity-incentive compensation and payout policy in Europe. Journal of Corporate Finance, 30, 85–97. 10.1016/j.jcorpfin.2014.10.019

- Chang K, Kang E and Li Y. (2016). Effect of institutional ownership on dividends: An agency-theory-based analysis. Journal of Business Research, 69(7), 2551–2559. 10.1016/j.jbusres.2015.10.088

- Chen J, Leung W Sau and Goergen M. (2017). The impact of board gender composition on dividend payouts. Journal of Corporate Finance, 43, 86–105. 10.1016/j.jcorpfin.2017.01.001

- Claessens, S., Djankov, S., & Lang, L. H. (2000). The separation of ownership and control in East Asian Corporations. Journal of Financial Economics, 581, 81–112. https://doi.org/10.1016/S0304-405X(00)00067-2

- Coulton, J. J., & Ruddock, C. (2011). Corporate payout policy in Australia and a test of the life-cycle theory. Accounting and Finance, 51(2), 381–407. https://doi.org/10.1111/j.1467-629X.2010.00356.x

- Deangelo, H., Deangelo, L., & Skinner, D. J. (2008). Corporate payout policy. Foundations and Trends in Finance, 3 (2–3), 95–287. http://ssrn.com/abstract=1400682.

- DeAngelo, H., DeAngelo, L., & Stulz, R. M. (2006). Dividend policy and the earned/contributed capital mix: A test of the life-cycle theory. Journal of Financial Economics, 81(2), 227–254. https://doi.org/10.1016/j.jfineco.2005.07.005

- Denis, D. J., & Osobov, I. (2008). Why do firms pay dividends? International evidence on the determinants of dividend policy. Journal of Financial Economics, 89(1), 62–82. https://doi.org/10.1016/j.jfineco.2007.06.006

- Dhanani, A. (2005). Corporate dividend policy: The views of British financial managers. Journal of Business Finance Accounting, 32(7–8), 1625–1672. https://doi.org/10.1111/j.0306-686X.2005.00643.x

- Easterbrook, F. H. (1984). Two agency-cost explanations of dividends. American Economic Review, 74 (4) , 650–659 https://www.jstor.org/stable/1805130.

- Eisdorfer A, Giaccotto C and White R. (2015). Do corporate managers skimp on shareholders' dividends to protect their own retirement funds?. Journal of Corporate Finance, 30 257–277. 10.1016/j.jcorpfin.2014.12.005

- Faccio, M., Lang, L. H., & Young, L. (2001). Dividends and expropriation. American Economic Review, 91(1), 54–78. https://doi.org/10.1257/aer.91.1.54

- Fama, E. F., & Babiak, H. (1968). Dividend policy: An empirical analysis. Journal of the American Statistical Association, 63(324), 1132–1161. https://doi.org/10.1080/01621459.1968.10480917

- Fama, E. F., & French, K. R. (2001). Disappearing dividends: Changing firm characteristics or lower propensity to pay? Journal of Financial Economics, 60(1), 3–43. https://doi.org/10.1016/S0304-405X(01)00038-1

- Fenn, G. W., & Liang, N. (2001). Corporate payout policy and managerial stock incentives. Journal of Financial Economics, 60(1), 45–72. https://doi.org/10.1016/S0304-405X(01)00039-3

- Francis B B, Hasan I, John K and Song L. (2011). Corporate Governance and Dividend Payout Policy: A Test Using Antitakeover Legislation. Financial Management, 40(1), 83–112. 10.1111/j.1755-053X.2010.01135.x

- Garrett, I., & Priestley, R. (2012). Dividend growth, cash flow, and discount rate news. Journal of Financial and Quantitative Analysis, 47(5), 1003–1028. https://doi.org/10.1017/S0022109012000427

- Geiler, P., & Renneboog, L. (2016). Executive remuneration and the payout decision. Corporate Governance (Oxford), 24(1), 42–63. https://doi.org/10.1111/corg.12127

- Goergen, M., Renneboog, L., Da Silva, Correia, L. (2004). Dividend policy of German firms. A dynamic panel data analysis of partial adjustment models. Working Paper, 31, 1–38. papers3://publication/uuid/92B1D23A-3253-4FA3-A96F-8D96EBCF7682

- Gonzalez M, Molina C A, Pablo E and Rosso J W. (2017). The effect of ownership concentration and composition on dividends: Evidence from Latin America. Emerging Markets Review, 30, 1–18. 10.1016/j.ememar.2016.08.018

- Gordon, M. J. (1959). DIVIDENDS, EARNINGS, AND STOCK PRICES. The Review of Economics and Statistics, 41(2), 99–105. https://doi.org/10.2307/1927792

- Gordon, R. H., & MacKie-Mason, J. K. (1990). Effects of the tax reform act of 1986 on corporate financial policy and organizational form. Do Taxes Matter? The Impact of the Tax Reform Act of 1986. http://ideas.repec.org/p/nbr/nberwo/3222.html

- Goyal, A., Jategaonkar, S. P., & Muckley, C. B. (2020). Why do privatized firms pay higher dividends? Journal of Corporate Finance. Elsevier, 60(C). 10.1016/j.jcorpfin.2019.101493

- GRINSTEIN Y and MICHAELY R. (2005). Institutional Holdings and Payout Policy. The Journal of Finance, 60(3), 1389–1426. 10.1111/j.1540-6261.2005.00765.x

- Grullon, G., Michaely, R., & Swaminathan, B. (2002). Are dividend changes a sign of firm maturity?. The Journal of Business, 75(3), 387–424. https://doi.org/10.1086/339889

- Gugler, K. (2003). Corporate governance, dividend payout policy, and the interrelation between dividends, R&D, and capital investment. Journal of Banking and Finance, 27(7), 1297–1321. https://doi.org/10.1016/S0378-4266(02)00258-3

- Gugler, K., & Yurtoglu, B. B. (2003). Corporate governance and dividend pay-out policy in Germany. European Economic Review, 47(4), 731–758. https://doi.org/10.1108/BSS-01-2013-0003

- Hossain A Tanvir, Hossain T and Kryzanowski L. (2021). Political corruption and corporate payouts. Journal of Banking & Finance, 123, 106016. 10.1016/j.jbankfin.2020.106016

- Hu, A., & Kumar, P. (2004). Managerial Entrenchment and Payout Policy. The Journal of Financial and Quantitative Analysis, 39(4), 759–790. http://www.jstor.org/stable/30031884

- Isakov D and Weisskopf J. (2015). Pay-out policies in founding family firms. Journal of Corporate Finance, 33, 330–344. 10.1016/j.jcorpfin.2015.01.003

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jeon J Q, Lee C and Moffett C M. (2011). Effects of foreign ownership on payout policy: Evidence from the Korean market. Journal of Financial Markets, 14(2), 344–375. 10.1016/j.finmar.2010.08.001

- Jiraporn P, Kim J and Kim Y Sang. (2011). Dividend Payouts and Corporate Governance Quality: An Empirical Investigation. Financial Review, 46(2), 251–279. 10.1111/j.1540-6288.2011.00299.x

- Jo, H., & Pan, C. (2009). Why are firms with entrenched managers more likely to pay dividends?. Review of Accounting and Finance, 8(1), 87–116. https://doi.org/10.1108/14757700910934256

- John K, Knyazeva A and Knyazeva D. (2015). Governance and Payout Precommitment. Journal of Corporate Finance, 33, 101–117. 10.1016/j.jcorpfin.2015.05.004

- John, K., & Williams, J. (1985). Dividends, dilution, and taxes: A signalling equilibrium. The Journal of Finance, 40(4), 1053–1070. https://doi.org/10.1111/j.1540-6261.1985.tb02363.x

- Khan, T. (2006). Company dividends and ownership structure: Evidence from UK panel data. The Economic Journal, 116(510), 172–189. https://doi.org/10.1111/j.1468-0297.2006.01082.x

- Oskar Kowalewski & Oleksandr Talavera, 2007. ”Corporate Governance and Dividend Policy in Poland,” Discussion Papers of DIW Berlin 702, DIW Berlin, German Institute for Economic Research

- La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. (2000). Agency problems and dividend policy around the world. Journal of Finance, 55(1), 1–33. https://doi.org/10.1111/0022-1082.00199

- Li W, Zhou J, Yan Z and Zhang H. (2020). Controlling shareholder share pledging and firm cash dividends. Emerging Markets Review, 42, 100671. 10.1016/j.ememar.2019.100671

- Lintner, J. (1956). Distribution of incomes of corporations among dividends, retained earnings and taxes. The American Economic Review, 46 (2) , 97–113 http://www.jstor.org/stable/1910664.

- Mancinelli L and Ozkan A. (2006). Ownership structure and dividend policy: Evidence from Italian firms. The European Journal of Finance, 12(3), 265–282. 10.1080/13518470500249365

- Martins T Cotrim and Novaes W. (2012). Mandatory dividend rules: Do they make it harder for firms to invest?. Journal of Corporate Finance, 18(4), 953–967. 10.1016/j.jcorpfin.2012.05.002

- Michaely, R., & Roberts, M. R. (2006). Dividend smoothing, agency costs, and information asymmetry: Lessons from the dividend policies of private firms. Working paper. https://faculty.fuqua.duke.edu/corpfinance/papers/Roberts_PrivatePayout-2006%20Aug%2031.pdf

- Michaely, R., & Roberts, M. R. (2012). Corporate Dividend Policies: Lessons from Private Firms. The Review of Financial Studies, 25(3), 711–746. http://www.jstor.org/stable/41407845

- Michiels, A., Voordeckers, W., Lybaert, N., & Steijvers, T. (2015). Dividends and family governance practices in private family firms. Small Business Economics, 44(2), 299–314. http://www.jstor.org/stable/43553051

- Miller, M. E., & Kevin, R. O. (1985). Dividend policy under asymmetric information. The Journal of Finance, 40(4), 1031–1051. https://doi.org/10.1111/j.1540-6261.1985.tb02362.x

- Miller, M. H., & Modigliani, F. (1961). Dividend policy, growth and the valuation of shares. The Journal of Business, 34(4), 411–433. https://doi.org/10.1086/294442

- Mitton, T. (2004). Corporate governance and dividend policy in emerging markets. Emerging Markets Review, 5(4), 409–426. https://doi.org/10.1016/j.ememar.2004.05.003

- Moh’d, M. A., Perry, L. G., & Rimbey, J. N. (1995). An investigation of the dynamic relationship between agency theory and dividend policy. Financial Review, 30 (2), 367—–385. http://onlinelibrary.wiley.com/doi/10 .1111/j.1540-6288.1995.tb00837.x/abstract.

- Mori N and Ikeda N. (2015). Majority support of shareholders, monitoring incentive, and dividend policy. Journal of Corporate Finance, 30, 1–10. 10.1016/j.jcorpfin.2014.10.015

- Mueller, D. C. (1972). A life cycle theory of the firm A LIFE CYCLE THEORY OF THE FIRM. The Journal of Industrial Economics, 20(3), 199–219. https://doi.org/10.2307/2098055

- Nielsen, A. E. B.(2006). Corporate governance, leverage, and dividend policy, Working paper, Princeton University

- Officer, M. S. (2007). Dividend policy, dividend initiations, and governance, Working paper, University of Southern California

- Perez-gonzalez, F. (2002). LARGE SHAREHOLDERS AND DIVIDENDS: EVIDENCE FROM U. S. TAX REFORMS. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.337640

- Petrasek, L. (2012). Do transparent firms pay out more cash to shareholders? Evidence from international cross-listings. Financial Management, 41(3), 615–636. https://doi.org/10.1111/j.1755-053X.2012.01192.x

- Pindado, J., Requejo, I., & Torre, C. (2012). Do family firms use dividend policy as a governance mechanism? Evidence from the Euro zone. Corporate Governance: An International Review, 20(5), 413–431. https://doi.org/10.1111/j.1467–8683.2012.00921.x

- Renneboog, L., & Szilagyi, P. G. (2015). How relevant is dividend policy under low shareholder protection?. Journal of International Financial Markets, Institutions and Money, 64(January 2020) . https://doi.org/10.1016/j.intfin.2015.01.006

- Renneboog, L., & Trojanowski, G. (2007). Control structures and payout policy. Managerial Finance, 33(1), 43–64. https://doi.org/10.1108/03074350710715809

- Rozeff, M. S. (1982). Growth, beta and agency costs as determinants of divided payout ratios. Journal of Financial Research, 5(3), 249–259. https://doi.org/10.1111/j.1475-6803.1982.tb00299.x

- Sawicki J. (2009). Corporate governance and dividend policy in Southeast Asia pre- and post-crisis. The European Journal of Finance, 15(2), 211–230. 10.1080/13518470802604440

- Setia‐Atmaja L. (2010). Dividend and debt policies of family controlled firms. International Journal of Managerial Finance, 6(2), 128–142. 10.1108/17439131011032059

- Sharma V. (2011). Independent directors and the propensity to pay dividends. Journal of Corporate Finance, 17(4), 1001–1015. 10.1016/j.jcorpfin.2011.05.003

- Shefrin, H. M., & Statman, M. (1984). Explaining investor preference for cash dividends. Journal of Financial Economics, 13(2), 253–282. https://doi.org/10.1016/0304-405X(84)90025-4

- Short H, Zhang H and Keasey K. (2002). The link between dividend policy and institutional ownership. Journal of Corporate Finance, 8(2), 105–122. 10.1016/S0929-1199(01)00030-X

- Teng C, Li S and Yang J Jimmy. (2021). Family control, external governance mechanisms, and dividend payouts. The Quarterly Review of Economics and Finance, 79, 198–209. 10.1016/j.qref.2020.05.012

- Tran, Q. T. (2020). Corruption, agency costs and dividend policy: International evidence. Quarterly Review of Economics and Finance, 76 (May 2020) , 325–334. https://doi.org/10.1016/j.qref.2019.09.010

- Trojanowski, G. (2004). Ownership structure and payout policy in the UK. EFMA 2004 Basel Meetings Paper. http://papers.ssrn.com/sol3/papers.cfm?abstractid=498023

- Truong, T., & Heaney, R. (2007). Largest shareholder and dividend policy around the world. Quarterly Review of Economics and Finance, 47(5), 667–687. https://doi.org/10.1016/j.qref.2007.09.002

- UK corporate governance code - financial reporting council. (n.d.). Retrieved August 27, from https://www.frc.org.uk/getattachment/59a5171d-4163-4fb2-9e9d-daefcd7153b5/UK-Corporate-Governance-Code-2014.pdf

- Von Eije, H., & Megginson, W. L. (2008). Dividends and share repurchases in the European Union. Journal of Financial Economics, 89(2), 347–374. https://doi.org/10.1016/j.jfineco.2007.11.002

- Wu, M., Ni, Y., & Huang, P. (2020). Dividend payouts and family-controlled firms—The effect of culture on business. The Quarterly Review of Economics and Finance, 75 (C) , 221–228. https://doi.org/10.1016/j.qref.2019.03.004

- Yarram S Reddy and Dollery B. (20152015). Corporate governance and financial policies. Managerial Finance, 41(3), 267–285. 10.1108/MF-03-2014-0086

- Ye, D., Deng, J., Liu, Y., Szewczyk, S. H., & Chen, X. (2019). Does board gender diversity increase dividend payouts? Analysis of global evidence. Journal of Corporate Finance, Elsevier, 58(C), 1–26. https://doi.org/10.1016/j.jcorpfin.2019.04.002

- Yoshikawa T and Rasheed A A. (2010). Family Control and Ownership Monitoring in Family-Controlled Firms in Japan. Journal of Management Studies, 47(2), 274–295. 10.1111/j.1467-6486.2009.00891.x