Abstract

This research work assesses the effects of tax revenue on the economic growth of Nigeria utilizing time series data spanning from year 2000 till 2021. The study’s specific goal is to evaluate the influence of hydrocarbon tax, corporation income tax and Value Added Tax on Nigeria’s economic growth. The study employs secondary form of data which have been sourced from CBN statistical bulletin and published Federal Inland Revenue Statement. Ex-post facto research design is used for this study. The data collected are analyzed and tested for unit root using Augmented Dickey Fuller method. The study variables which comprise GDP, PPT, CIT & VAT are found to be stationary at first difference. Thus, a Johansen co-integration test is also conducted and it reveals a long-run relationship. Consequently, the study utilizes the Vector Error Correction Model to evaluate the effects of PPT, CIT and VAT on GDP. The findings reveal that PPT and VAT have positive and significant effects on GDP. It also reveals that CIT has a negative and significant effect on GDP. Based on these findings, the inquiry suggests that trainings and workshops should be organized by government tax agencies to the Nigerian public and companies on the importance and benefits of tax revenue to the economy. The tax authorities should also endeavour to encourage companies to pay tax so as to improve the growth of the economy which the companies are meant to benefit from as part of government’s fulfilment of its social responsibilities.

1. Introduction

The government of any nation is saddled with enormous responsibilities which are influenced greatly by the income generated by the government from different sources one of which includes taxes. To finance its operations, the Nigerian government is primarily reliant on taxes. Individuals or companies must pay a tax to the government, which is normally levied by the government. Taxes are a significant source of revenue and a major source of income to the government. Taxes are considered different from other sources of government revenue because it is a compulsory charge. In the 19th century, the main purpose for which tax was imposed was for revenue to the government but today, it is seen to be used for different purposes other than fiscal purposes. Taxation being a major source of funding to all three tiers of government is highly important in helping the government achieve its macroeconomic objectives. According to Abomaye Nimenibo (Citation2017) Taxation is a process established by the government to exert control over tax and tax collection. It is thus considered as the redistribution of wealth from the private to the public sectors of the economy to help the nation in achieving some of its economic and social objectives which include providing essential facilities and services like proficient health care services, quality road, among others.

Taxation is the art of charging citizens with taxes, while tax itself is seen as a mandatory payment to be made by every citizen of a state. This payment of tax is called a civic duty (Abomaye-Nimenibo et al., Citation2018). Taxes are frequently levied to limit the creation of certain products and services, to protect new business and local businesses, and to reduce the level of income disparity in society, also to regulate business and to keep inflation under control (Edewusi & Ajayi, Citation2019). Due to the significance of tax in bringing revenue to the government for various uses, its ability to affect consumption patterns lead to the growth of the economy, exert influence on economic variables, and its ability to affect consumption patterns, the government of every nation will strive to maximize the revenues from tax (Asaolu et al., Citation2018). The effectiveness and efficiency in administering tax leads to an increment in the revenue generated which helps the government in the provision of amenities for citizens and even execution of capital projects in spite of this, the fraudulent affairs and schemes of tax authorities as well as incompetent tax personnel are seen to be threats and challenges that affect the revenues by channeling the funds from tax into their personal pockets (Asaolu et al., Citation2018).

The primary goal of a tax system is to produce adequate incomes to cover the government’s vital expenditures on commodities, and tax is widely regarded as the most effective instrument for improving the public sector’s capabilities and debt repayment (Okoye & Ezejiofor, Citation2014). Aside from the problems seen in the taxation system in present time, the purpose of charging tax has not only been for revenue generation for the state but also a means for reallocation of wealth as well as regulation of the economy (Ojo, Citation2008). As a result, a tax system is regarded as a powerful tool that the government can employ to aid socioeconomic development (Mathew, Citation2014).

Oil revenue forms a huge proportion of revenue generated in Nigeria because Nigeria significantly depends on oil. Nigeria’s over-reliance on oil as a key source of revenue is perilous and detrimental for its economic growth (Oladipupo & Oladipupo, Citation2015). Globally, the price of oil has dropped dramatically in recent years, therefore, affecting the government earnings and putting Nigeria in a precarious position as there is no sufficient funds to be allocated between the three tiers of governments. This was evident in April 2020 when the price of crude oil was as low as $38 per barrel and compounded with the outbreak of the COVID-19 pandemic (Gbeke & Nkak, Citation2021).

Economic growth is described as a constant increment in the production capacity of a country (as evaluated by reviewing the current year’s gross national product to the previous year’s), as well as an increment in per capita national output, measured by shifting the country’s production possibility frontier outwards (Salami et al., Citation2015). The government’s role in achieving economic growth for both established and developing countries is critical, and taxation, as an instrument of fiscal policy, can be a beneficial tool used by the government in stimulating economic growth (Edewusi & Ajayi, Citation2019). The correlation between taxation and economic growth is a contested subject as taxation has an impact on the economy, firms and individual decisions are also affected by tax (Mdanat et al., Citation2018).

According to the Economic Recovery and Growth Plan (ERGP, 2017), the 4.8 percent annual growth rate between 2011 and 2015 was mostly driven by high oil prices and was generally non-inclusive. Continuing, the majority of Nigerians are still suffering from severe poverty, inequality, and unemployment, according to this document (ERGP, 2017). Despite the revenue reported by the government over the years, the revenue has been insufficient in meeting its social and public spending which is important to enhance economic growth. Hence, the goal of this study which is to analyze the effects of tax income on economic growth by specifically unravelling the effect of direct taxes which include PPT and indirect taxes which include VAT has affected economic growth. The objective which this study intends to achieve is to examine the effects tax revenue has on economic growth in Nigeria. The specific objectives of the study include: to analyze the impact of petroleum profit tax on the economic growth of Nigeria; examine the effect of company income tax on economic growth of Nigeria and to determine the effect of Value added tax on the economic growth of Nigeria. The null hypotheses that will help to subject the objectives to test include: H01: Petroleum profit tax has no significant effect on economic growth in Nigeria; H02: Company income tax does not significantly affect economic growth in Nigeria; H03: Value added tax has no significant impact on economic growth in Nigeria.

2. Literature review

2.1. Conceptual clarifications

Taxation. Tax is a mandatory, non-repayable remittance made to the government for products and services intermittently. It is normally paid by private businesses and consumers to the government (Agunbiade & Idebi, Citation2020). The government is empowered to control, administer and make provisions for law, rules, regulations and policies that will regulate and guide tax system so as to ensure all taxes are properly administered and all revenue generated is reimbursed to the government (Abomaye-Nimenibo et al., Citation2018. Nigeria’s government being one of those countries that has the legal authority to impose any type of tax on its population at any rate it deems fit (Amadi & Alolote, Citation2019). Macek (Citation2014) opinionated that utilizing taxation as a fiscal policy tool to help attain economic development is complex for developing countries as there is a reduction in the rate of tax revenue generated.

Classification of Taxes. Taxes can be grouped into direct taxes and indirect taxes. Direct tax is a type of tax that is charged exactly on an individual or an organisation, and which the individual or organisation is required to pay by way of a notice known as an assessment notice. A taxpayer must have been informed of such tax payments. They are taxes that are remitted directly to the government by companies and individuals (Omodero et al., Citation2021). Types of taxes that fall under direct tax include Petroleum Profit Tax, Withholding Tax, Capital Gains Tax, Company Income Tax and Stamp Duties. Indirect tax are taxes whereby the tax burdens are not borne by the individuals or organisation imposed upon but are transferred to other individuals who will then bear the tax burdens. They are charged on goods and services where tax burden doesn’t fall on the initial buyer but on the final consumers (Abomaye Nimenibo, Citation2017b; Omodero, Citation2021). Indirect taxes include Value Added Tax, Custom and Excise Duties.

Economic Growth. Economy is a very important part of any nation. Salami et al. (Citation2015) view economic growth as a continuous rise in the net national product over a time frame. Peter and Adesina (Citation2015) believe that a rise in capital stock, an enhancement in the literacy level and an upgraded level of technology is a vital source of economic growth. They believe certain economic indicators will provide a view of the economy and an improved understanding of the economy some of which include Gross Domestic Product (GDP), Gross National Product (GNP) and Per Capita Income. Conceptually, economic growth is defined as a gradual upswing in national revenue or output as a direct consequence of the government’s deliberate manipulation of economic indicators via fiscal or monetary policy measures (Etim et al., Citation2021). However, it has been argued that economic growth is influenced by four essential indices: national resources, human resources, technological advancement, and wealth creation (Igbasan, Citation2017).

2.1.1. Conceptual framework

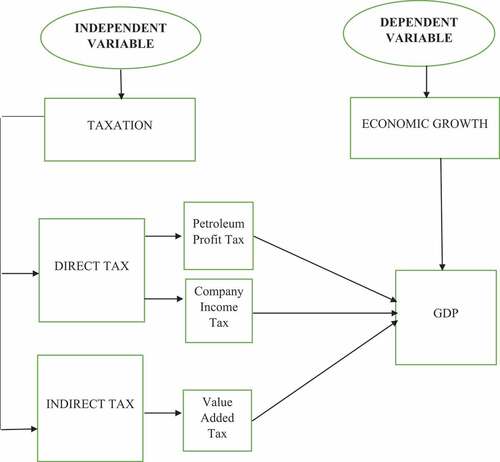

The conceptual framework of this study as shown below as , provides the pictorial demonstration of the study variables and their connections or possible effects.

Figure 1. Conceptual model.

2.2. Theoretical framework

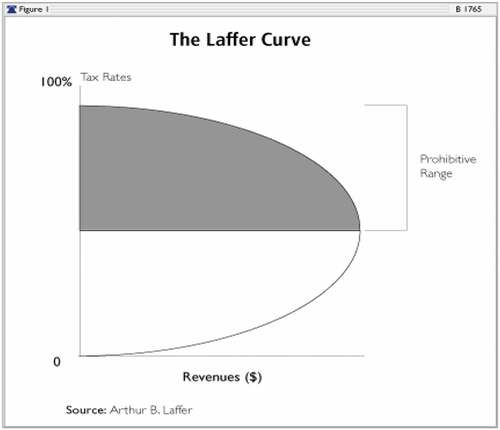

Laffer Curve Theory. Professor Arthur Laffer proposed the Laffer curve theory in 1974 which explicates the theoretical relationship between the tax rate and government revenue derived from taxation. The Laffer curve in , simply demonstrates the idea that a change in tax rate will have an effect on tax revenue in two different ways which are the Arithmetic Effect and the Economic Effect (Laffer, Citation2004). The Arithmetic Effect states that a depletion in tax rate will bring about a cutback in tax revenue (per currency of the tax base) proportionate to the reduction in tax rate, and vice versa. The Economic Effect, on the other hand, recognizes that a lower tax rate will have a favorable influence on work, output, employment, and, as a result, the tax base, by helping to grow activities through incentives. The Arithmetic Effect is the polar opposite of the Economic Effect. As a result, when the Economic and Arithmetic Effects of tax rate transposes are combined, the impact of a change in tax rates on total tax collection is less apparent.

Figure 2. Source: Laffer (Citation2004)

In the Laffer curve figure above, the bottom of the curve shows that there are no taxes which will bring about no government revenue thereby resulting in no government. In the beginning, when taxes are raised from 0 the tax revenue increases but as the government continues to raise taxes, tax revenue decreases, resulting in the steepness of the curve. Subsequently, increased taxes will pose a large burden on economic growth of any nation. The heavy tax burden makes consumers spend more money and thereby leading to a decrease in demand which makes, in the long term, the reduction in the tax base balance off the rapid increase in tax revenue. This is the shaded part of the Laffer curve called the Prohibitive Range where the curve moves backwards. A tax increase above the Prohibitive Range will result in a reduction in government revenue (Laffer, Citation2004).

Socio Political Theory. According to this taxation philosophy, the primary considerations in taxing should be social and political purposes. The ideology maintained that a tax structure should not be designed to benefit individuals, but rather to address societal issues (Chigbu et al., Citation2012). Wagner advocated for a modern welfare approach while deciding on a tax policy and using taxation to reduce income disparities (Chigbu et al., Citation2012). Adolph Wagner was not a believer in taking an individualistic approach to solving an issue, before an appropriate solution could be found, he believed that each economic issue needs to be analyzed in the context of its social and political environment (Etim et al., Citation2021).

Ability to Pay Theory. Taxation is also based on the basic premise that everyone in society should bear the burden of taxation in a fair and equitable manner (Ayeni et al., Citation2017). The theory was advocated by Adam Smith who is referred to as the Father of Economics, it is widely accepted as it is on the basis of the real meaning of “ability” of tax payer due to this many economies in the world believe that income is the best measurement of one’s ability to pay (Peter & Adesina, Citation2015). Benefit Received Theory. This theory establishes that government and tax payers have an exchange relationship in which the state supplies public goods and services and any other benefit to individuals in the society and these individuals in return pay for all goods and services supplied in proportion to the benefit received (Ayeni et al., Citation2017). Such benefits include: infrastructure, regularized labour, and capital markets, among other things (Amadi & Alolote, Citation2019).

Expediency Theory. This theory is of the idea that just about every tax plan meets the practicality test, which is the government’s single criterion for deciding on a tax policy (O. H. Otu & Adejumo, Citation2013). It must be the only factor taken into account by the authorities when deciding on a tax proposal. One should disregard the impact of a tax system as well as the state’s social and economic goals (Ayuba, Citation2014). According to Kiabel (2009), the state’s economic and social goal is to emplace an effective tax system that is relevant to a nation’s economic growth. The concept of expediency is based on a link among both tax liabilities and government actions. The state is expected to levy generally the societal members for the amenities it provides (Anyanfo, Citation1996).

2.3. Empirical findings

(Etim et al. Citation2021) Using a descriptive and inferential statistical technique, correlational and regression statistics, and an ex post facto research design, the study compared the effects of direct and indirect taxation on the growth of the Nigerian economy. The study demonstrated that indirect taxes have a greater detrimental impact on economic growth. Mukolu and Ogodor’s (Citation2021) study examined the impact of VAT on the Nigerian economic growth for the year 1994 till 2018 using an Augmented Dickey Fuller analysis method. Data gotten from Central Bank of Nigeria statistical bulletin and Federal Inland Revenue Service. The study showed that there is a positively significant impact of Value Added Tax on Gross Domestic Product. It also showed that VAT has to a great extent given rise to the total revenue of the nation and has helped in tax evasion by taxpayers.

John and Dickson (Citation2020) using Error Correction Models analyzed the influence of tax revenue on economic growth using both unadjusted and adjusted Gross Domestic Product from 1984 to 2018. When GDP was not adjusted for inflation, PPT had a minor but beneficial effect on economic growth, whereas VAT and CIT had a large but negative impact on GDP. PPT had a negative and insignificant impact on adjusted GDP, but VAT had a positive and considerable impact, and CIT had a negative and significant one. Yadawananda and Achal (Citation2020) investigated the long-run and short-run relationship between tax structure and state-level growth performance for the year 1991 till 2016 using the panel regression method. The findings revealed that commodity and service tax were bad for the economy and an increase in those taxes will lead to inflation while income taxes were found to be significant for the economy as it mostly impacts the savings and labour supply which is regarded as the drive for economic growth.

Adeusi et al. (Citation2020) investigated the impact of non-oil revenue of the economic growth of Nigeria where company income tax, value added tax, personal income tax and custom and excise duties where the non-oil revenue for the period 1994–2018 with data gotten from Federal Inland Revenue Service and National Bureau of Statistics. Ordinary Least Square Regression Techniques was used for data analysis. The study revealed that Value Added Tax and Custom and Excise duties have more significant positive impact on economic growth while Company Income Tax and Personal Income Tax have a negative but significant effect on economic growth.

Hieu (Citation2019) examined the impact of direct and indirect taxes on economic growth in Vietnam using ordinary linear regression from the year 2003 till 2017. Indirect tax is found to have a positive impact on the economic growth, it is seen to have a positive effect and aid economic growth while the effects of direct tax are discreet. Suna et al. (2019) studied the impact of direct and indirect tax on economic growth in Turkey using Autoregressive Distributed Lag (ADRL) method. The research found that indirect taxes had a positive and significant relationship on economic growth, direct taxes had a negative and significant impact on economic growth. It was found that an increase in direct taxes reduces disposable income which in turn affects the demand for goods and services which in turn also leads to a reduction in indirect taxes thereby affecting the economy negatively. Personal and corporate taxes collected in Turkey affects the economy negatively while VAT and excise duties affect it positively. Bruno and Emmanuel (Citation2019) used secondary data from the Central Bank of Nigeria statistical bulletin in several editions to look at tax income and the Nigerian economy from 2000 to 2017. They conducted the research using after the fact design. The statistical analyses were performed using the Ordinary Least Squares (OLS) regression approach. During the course of their analysis, their findings demonstrated that tax revenue had a little impact on economic growth.

Asaolu et al. (Citation2018) investigated the relationship between tax revenue and economic growth in Nigeria from the year 1994 till 2015, the study employed a descriptive and historical research design and an Auto Regressive Distributed Lag (ARDL) Regression. The study revealed a significant relationship between CED and VAT with economic growth, a negative and significant relationship with economic growth and an insignificant relationship with economic growth. Dladla and Khobai (Citation2018) used the Autoregressive Distribution Lag (ARDL) research method to look at the long- and short-term effects of taxation on economic development in South Africa from 1981 to 2016. The study’s results revealed a large and negative long- and short-term impact of taxes on economic growth as well as a long- and short-term favorable association between trade openness and economic growth.

Metri et al., (2018) examined the effect of tax structures on economic growth in Jordan for the year 1980 to 2015 using Error correction model. Consumption and tariffs positively impacted economic growth while income taxes negatively impacted economic growth and government is advised to focus on social justice rather than raising revenues and a shift from income tax to consumption and tariff taxes to help increase the per capita growth in the future. Abomaye-Nimenibo et al. (Citation2018) conducted Multiple Regression Analysis to conduct an empirical assessment of the influence of tax revenue on economic growth from 1980 to 2015. The analysis indicated that, in the short run, petroleum profit tax and corporate income tax had no major impact on economic growth, although customs and excise tariffs did. However, it is recommended that the government ensure that all companies are registered in Nigeria, limiting the risk of tax evasion.

Yahaya and Bakare (Citation2018) using data from the Federal Inland Revenue Service and the CBN statistical bulletin, analyzed the influence of petroleum profit tax and company income tax on Nigeria’s economic growth from 1981 to 2014. The researchers employed a time series study approach and ordinary least square regression analysis. Petroleum profit tax and firm income tax have a favorable significant impact on economic growth in Nigeria, according to the study. It was suggested that the government use the revenue earned by these tariffs for economic development and infrastructure improvements. Dang and Bala (2018) in Nigeria explored the importance of tax revenue in a nation’s development. The research explores how main tax revenue sources such as hydrocarbon tax, Corporation Income Tax (CIT), Customs and Excise Duties (CED), and Value Added Tax (VAT) affected Real Gross Domestic Product (RGDP). The Augmented Dickey Fuller unit root test, ECM and the Johansen Co-integration test were used by the researchers to evaluate series data for the period 1981 to 2013. Tax revenue in Nigeria contributes little to national development, according to the study’s findings, with some levies having a negative relationship with RDGP. Finally, they suggested stringent financial controls to limit income leakage in the system.

Udofot and Etim (Citation2017) from 1980 to 2015 looked into the relationship between SMEs’ tax revenue and economic growth in Nigeria. The study’s data came from several editions of the Central Bank of Nigeria (CBN) statistical reports and the Federal Inland Revenue Service (FIRS) yearly reports. Regression and correlation analyses were used to examine the data collected. The findings demonstrate that the variables are positively and strongly related, and they suggest redesigning the entire tax administration system to increase revenues collection. Ayeni et al. (Citation2017) using the Paired sample T-test looked at the effects of oil revenue and non-oil revenue on Nigerian economic growth 1986 to 2015. Oil revenue and non-oil revenue were both positive and highly associated with real GDP but there was a considerable difference between the effects of oil revenue and non-oil income on economic growth. Non-oil revenues were estimated to have contributed 2.5% to GDP growth while oil revenues contributed 7.7%.

Eyisi et al. (Citation2017) conducted a comparative analysis of Value Added Tax of developed and developing countries which in this case United Kingdom (UK) representing the developed economy and Nigeria the developing economy employing an Ordinary Linear Square regression for data analysis. The study showed that VAT of UK is of a small amount significant than Nigeria’s VAT in impacting economic growth but is greatly significant in economic development than Nigeria’s VAT in economic development. Inyiama et al. (2016) used regression analysis to examine the impact of VAT, customs, and excise levies on Nigeria’s economic growth. The outcome demonstrated a beneficial effect of value added tax, customs tariffs, and excise taxes on economic growth.

Previous studies as embedded in the empirical review of this literature reviewed reveal numerous works done on the subject of tax revenue and economic growth. Studies carried out in this area of concern have covered various geographical locations. However, there seems to be an absence of work exploring the revenue and economic growth based on the change of VAT rate. Most of the research work stops between 2017 and 2018 and there doesn’t include the most recent data on this topic. Also, that there is a conflicting number of results as to the effect of tax revenue on economic growth.

3. Methodology

An ex-post facto research design is a suitable research design for this project because it encompasses a technique in which concepts or categories with an already extant feature or element have been grouped and can be compared to a specific dependent variable. For this research the independent variable, tax revenue is divided into groups which are PPT, CIT, VAT, and it will be compared to the dependent variable which is Gross Domestic Product. The location of this study is Nigeria. The research focuses on the tax and economy of Nigeria. This research covers the time period from 2000 to 2021. This study research makes use of secondary data. This secondary data is obtained from the Central Bank of Nigeria Statistical Bulletin and Federal Inland Revenue Service (FIRS). Gross Domestic Product is obtained from the CBN Statistical Bulletin and the tax revenue data is derived from published statements of the Federal Inland Revenue Service. Secondary data is used as a source of data because the information that is needed for the study can only be obtained from published reports rather than a primary data. This study covers the effect of tax revenue on the economic growth of Nigeria. This study is on the taxation branch of accounting, it looks at the economic growth of Nigeria for a period of 20 years (2000–2021). The scope of this study covers three forms of taxes which are hydrocarbon tax, company income tax and value added tax, which are known to have the greatest impact on tax revenue in Nigeria as well as GDP for economic growth, which has been recognized to be the best indicator of economic growth. Revenue data is gotten from FIRS and GDP data is from CBN statistical bulletin.

3.1. Description and measurement of variables

Economic growth refers to a rise in the economic goods and service produced by a nation over a period of time.

Economic growth is measured by Gross Domestic Product, Gross National Income, Gross National Product and Consumer Price Index but for this research work Gross Domestic Product is being used. Tax revenue is the income received by the government in carrying out its activities coming from the taxation of individuals and organizations in a country. There are various measures of tax revenue which include, PPT, CIT, VAT, Stamp Duties, TET, CGT, Custom and Excise Duties but for the purpose of this research, PPT, CIT and VAT are used.

Tax revenue is the independent variable in this research study and it is measured using four selected groups of tax revenue. This selection is as a result of past literatures also they are considered by the most efficient and relevant in the generation of revenue for the government. The four selected measurements include Hydrocarbon Tax, Company Income Tax and Value Added Tax.

Economic growth as measured by Gross Domestic Product is the dependent variable in this study. The total market value of commodities produced by a country at any given time is referred to as its gross domestic product.

3.2. Method of Data Presentation and Analysis

The data gathered for this research will be subject to analysis and this study employed a time series data which is a sequence of data collected over time. The Vector Error Correction Model was the analytical technique employed in this research study. The VECM model was used because the cointegration existed between the variables after the Johansen Cointegration test. A Johansen Cointegration test was used to check whether or not cointegration existed. Unit root test was also employed in this study to so as to test for stationarity in the time series. It is to determine whether the variables are stationary or non-stationary. Descriptive analysis was also performed because it is a useful tool for assessing and summarizing vast amounts of raw data. The descriptive analysis focuses on displaying data sets in their most basic form to convey fundamental information about variables in the dataset. Correlation analysis will also be used to see if there were any plausible links between the variables. It is a statistical method for determining the strength of a link between variables. E-views 9 was used as the statistical package to perform the relevant data analysis.

3.3. Model specification

Gross Domestic Product is the overall dependent variable.

Linear specification:

GDP = f (PPT, CIT, VAT)———————————————(1)

From the above linear specification, the statistical model was derived

GDP = β1PPTt + β2CITt + β3VATt————————————(2)

The linear function was changed into log form for better interpretation of results

logGDPit = α + β1logPPTit + β2logCITit + β3logVATit + µit—————————(3)

Where:

GDP: Gross Domestic Product

PPT: Petroleum Profit Tax

CIT: Company Income Tax

VAT: Value Added Tax

α is a constant

β1, β2, β3 are the coefficients of the parameter estimate

µ is the error term

4. Data presentation and analysis

This chapter deals with the analysis and presentation of data as well as the interpretation of results. The econometric techniques used in the study to determine the effect of tax revenue on economic growth in Nigeria were the Augmented Dickey-Fuller unit root test, Johansen Cointegration test, and Vector Error Correction Model analysis.

4.1. Descriptive statistics

which represents the Descriptive statistics results showed the attributes and nature of the variable used in the study. It showed each variable’s median, mean, minimum and maximum values, standard deviations, kurtosis, skewness, probability and the sum of square deviations. The described variables were log of gross domestic product (LGDP) which was the dependent variable and, log of petroleum profit tax (LPPT), log of company income tax (LCIT), and log of value added tax (LVAT) which were the independent variables.

Table 1. Measurement of Variables

Both the mean and the median served as indicators of central tendency. The greatest values for the log of gross domestic product (LGDP) were 10.82193 and 10.93387, respectively. The greatest value for the log of value added tax (LVAT) was 13.24439, while the minimum value for the log of company income tax (LCIT) was 3.975936. The standard deviation displayed the summation of squared deviations from the mean and log of value added tax (LVAT) had the highest value of 2.736048. The skewness made the asymmetry of the data distributions around its mean apparent. The skewness of the normal distribution typically ranges from 0 to 1. As a result, a positive skewness indicated that the data distribution has a long right tail, while a negative skewness suggested that the distribution has a long-left tail. Due to their range of 0 to 1, all of the variables (LGDP, LCIT, LPPT, and LVAT) had a normal distribution skewness. Only LVAT was positively skewed, with a value of 0.233309, whereas the variables (LGDP, LCIT, and LPPT) were adversely skewed due to their negative values of −0.623309, −0.618258, and −0.893227.

Kurtosis showed if the data series’ spreads were flat or peaks. The variable is considered to have peaked to the normal if the kurtosis value is 3 or above, which is excellent because it indicates that the variable is uniformly distributed. The distribution is considered to be flat to the normal if the kurtosis is under 3. With kurtosis values of 2.989934, 2.944023, and 3.202724, respectively, the variables LCIT, LPPT, and LVAT were peaked to the normal distribution whereas the variable LGDP is flat to the normal distribution because its value of 2.458793 is below 3.

4.2. Correlation analysis

The type of relationship between the independent variable LOGGDP and all the independent variables LCIT, LPPT, and LVAT were tested using this. A positive or negative relationship could exist. In contrast to a negative relationship, which denotes an indirect or inverse relationship between the two variables, a positive relationship indicates a direct association between the dependent and independent variables.

According to the independent variables LPPT and LVAT and the dependent variable LGDP had positive correlations with values of 0.499365 and 0.064288, respectively. Only LCIT, with a value of −0.477703, had a negative correlation with LGDP. This demonstrated that the impact of the independent variables on the dependent variable was balanced.

Table 2. Descriptive Analysis of Variables

4.3. Unit root test

This was used to test for the stationarity of the variables so as to ascertain their order of integration. Using the Augmented Dickey Fuller (ADF) test, the ADF unit root test ascertains the presence of a unit root (non-stationary) tested against alternative hypothesis of the absence of a unit root (stationary). The ADF statistic (in absolute figure terms) must be greater than the standard critical value at 5% level of significance.

The ADF result demonstrated that all variables were stationary at the first difference, trend, and intercept since the ADF statistic’s value IS above the standard critical value at a significance level of 5%. The Johansen cointegration test was used to confirm the inference that the variables had a long-term relationship. The ADF test results are displayed in .

Table 3. Correlation Analysis Result

4.4. Johansen Co-integration

The long-run relationship was estimated adopting the Johansen co-integration test to ascertain the long-run relationship among the variables in the equation. The null and alternate hypothesis is:

H0: There is no long-run relationship among the variables in the model

H1: There is a long-run relationship among the variables in the model

From the Johansen co-integration analysis in , and using lag 1, there was a long-run relationship between log of GDP (LGDP) which was the dependent variable and log of company income tax (LCIT), log of petroleum profit tax (LPPT), and log of value added tax (LVAT) which were the independent variables. From the unrestricted cointegration rank test; using the trace statistics in , there existed four (4) cointegrating equation, with the probability value less than 0.05 level of significance and figures of 0.0000, 0.0346, 0.0289, and 0.0097. The maximum Eigen value on the other hand from indicated also four (4) cointegrating equations with figures of 0.0000, 0.0363, 0.0185, and 0.0097. Therefore, the result implies that using both the trace statistics and the maximum Eigen value statistics, there was a long-run relationship in the model. This also means that the null hypothesis was rejected, meaning that there is a long-run relationship among the variables in the model. Since a long-run relationship existed, the vector error correction model (VECM) was conducted to determine the long-run and short-run association and thus the corresponding speed of adjustment. The result is thus represented in .

Table 4. ADF unit root test results

Table 5. Vector error correction model result

4.5. Vector Error Correction Model (VECM)

VECM is used to calculate the speed at which short disequilibrium converge into long-run equilibrium relationship. It is constructed only if the variables are co-integrated which implied that there was evidence of a long-run relationship among the variables. Moreover, it is a restricted VAR model with co-integrating restrictions imputed into its specification. The coefficients in the co-integrating equation showed the estimated long-run relationship among the variables. The coefficient in the VECM revealed how deviations from that long-run relationship affect the changes in the variable in the next time-period. In summary, those coefficients across cointEq1 under the VECM show how each variable will move in the next period to get back to the long-run relationship. To confirm the Johansen co-integration conclusion, directs us to first look at the coefficient values of the cointeq1 to determine whether there is a long-term relationship among the model’s variables. The coefficient values of each independent variable are then scrutinized to determine whether they will quickly resume their long-term relationships with the dependent variable in the upcoming period.

From , the first figure under each variable was the coefficient. The second values in circle brackets represented the standard error, while the third value in square brackets represented the t-statistics. The cointeq1 value of −0.746375 indicated a long-run relationship between the independent variables and the dependent variable LGDP, representing a high percentage of about 75%, which is near to 100%. The next step is to determine how quickly the long-run relationship can converge in the following time frame. The coefficient value of log of company income tax (LCIT) was −0.140119 to prove that it has a short-run time period in having a long-run impact on the dependent variable log of GDP (LGDP) both now and in the next period. The short-run speed of adjustment was approximately 14%. This showed that it is a vital variable that affects economic growth now and would also affect it in the next period.

The coefficient of log of petroleum profit tax (LPPT) was 0.057789 proved that it also has a short-run time period in having a long-run effect on the dependent variable log of GDP (LGDP) both now and in the next period. The short-run speed of adjustment was approximately 6%. It also proved that it is an important variable that would impact the dependent variable both now and the next period in the long run. Finally, the coefficient of log of value added tax (LVAT) was −0.157526 and also proved that it also has a short-run time period in having a long-run effect on the dependent variable LGDP both now and in the next period. The short-run speed of adjustment was approximately 16%. This also proved that it is an important variable that would impact the dependent variable both now and the next period in the long run.

4.6. VECM Probability table

displayed how quickly the independent variables changed how the dependent variable changed both now and over the following period. The table confirmed that there was a long-run relationship between the dependent variable and all the independent variables. The following phase involved determining which variable was significant and which was not. This was investigated using the VECM probability table. A variable was significant if it falls below the 5% level of significance (0.05).

Table 6. VECM Probability Table

Using , C(2) represented the dependent variable. C(3) represented log of company income tax (LCIT) and its probability value of 0.0451 was statistically significant at 5% level of significance to prove that the variable was significant in impacting the dependent variable LGDP. The coefficient value was −0.078580 and carries a negative sign to show that the significance was a negative one. Summarily, LCIT has a negative and significant relationship with LGDP. C(4) represented LPPT and its significant figure was 0.0000 which was significant at 5% level of significance. Also the coefficient value of 0.016165 carries a positive sign. Therefore, LPPT was positively significant in impacting LGDP. C(5) measured LVAT and its significant value of 0.0174 was significant at 5% level of significance. Its coefficient value of 0.004902 carries a positive sign also. Hence, LVAT was positively significant in impacting LGDP. C(1) represented the error term.

4.7. Post-Estimation technique

4.7.1. VEC Residual heteroskedasticity test

Data with uneven variability (scatter) over a group of other predictor variables is known as heteroskedasticity, and it prevents the error term from having a constant variance. Due to this, the estimators may not be the Best Linear Unbiased Estimators and may produce results with Biased Coefficients. To test for heteroskedasticity in the VECM result, the probability value of the Chi-Square (Chi-sq) must be insignificant at 10% level of significance to confirm that there was no heteroskedasticity in the model.

To demonstrate that there was no heteroskedasticity in the model, the probability value from , 0.4724, was not significant at the 10% level of significance.

Table 7. Heteroskedasticity Test

4.7.2. VEC Residual serial correlation lm test

This test was used to determine whether the model contained serial correlation or autocorrelation. Each independent variable is not correlated with one another and stands alone in the case of autocorrelation. To demonstrate that there was no autocorrelation in the model, the probability values of the LM-stat must be non-significant at the 10% level of significance. To demonstrate that there was no autocorrelation in the model, s lag length of 1 and the probability values of the LM-Stat were not significant at a 10% level of significance.

Table 8. Residual Serial Correlation LM Test

4.8. Discussion of findings

The main goal of the study was to ascertain how tax income affected the economy of Nigeria and how it might contribute to its growth. In order to ascertain the relationship between the variables, descriptive statistics were first used. The unit root test showed that all the variables were stationary at first difference. As a result, the Johansen co-integration test was carried out, and the probability values of the result were significant, indicating that the variables in the model had a long-term relationship. The vector error correction model was performed, and it used the cointeq1 value of −0.746375 to confirm the long-run, substantial positive relationship between the dependent variable and all of the independent variables. The VECM study established the long-term link and demonstrated that each independent variable had a short-run rate of adjustment that would affect the dependent variable economic growth as it entered the subsequent period.

The probability table showed that log of company income tax was negatively significant in impacting economic growth of Nigeria in the long run. However, both petroleum profit tax and value added tax had positive and long-run significant impact on the dependent variable. The implication of the findings is that all the independent factors were crucial in improving economic growth both in the current time period and the next time period. Therefore, the importance of tax income cannot be over-emphasized in effecting and increasing economic growth in Nigeria. Therefore, tax income gives the government money for recurrent and capital expenses, which in turn assist the government gain a competitive edge that improves and increases economic activity, which in turn spurs economic growth and development.

4.9. Hypothesis testing

We previously stated three hypotheses for testing to analyze the effect of tax revenue on economic growth. To test the hypothesis, Vector Error Correction model was used to calculate the overall dependence of the dependent variable on the independent variable. The outcome of the vector error correction analysis will be used to test the hypothesis in this study. For the purpose of this study, a hypothesis is accepted at a 5% level of significance. A null hypothesis would only be rejected in favor of the alternate if the P-value (probability value) is less than 0.05. A p-value greater than 0.05 will see the null hypothesis is accepted. The results of the hypothesis tested are as follows;

H01: Petroleum profit tax has no significant effect on economic growth in Nigeria

Using the probability table in , petroleum profit tax was positively significant in impacting LGDP with significant value of 0.0000. Therefore, based on this finding, the null hypothesis was rejected and it was accepted that petroleum profit tax had a significant effect on economic growth in Nigeria.

H02: Company income tax does not significantly affect economic growth in Nigeria

Table 9. Summary of hypothesis result

Also based on the probability table in , company income tax was negatively significant in impacting LGDP with significant value of 0.04511. Hence, the null hypothesis was rejected and it was agreed that company income tax does have significantly affect economic growth in Nigeria.

H03: Value added tax has no significant impact on economic growth in Nigeria

Moreover, evaluating the probability table in , value added tax was positively significant in impacting LGDP with significant value of 0.0174. This means that the null hypothesis was also rejected and it was accepted that value added tax had a significant impact on economic growth in Nigeria.

5. Conclusion and recommendation

Tax revenue (measured by value added tax, company income tax, and petroleum profit tax were used as independent variables) against the dependent variable gross domestic product (GDP). The findings revealed that all the three variables were significantly influence economic growth although company income tax was negatively significant; petroleum profit tax and value added tax were positively significant. Based on this finding, the study concluded that the relevance of tax revenue to an improved Nigerian economy cannot be over-emphasized. Therefore, tax revenue is an avenue for the government to source for funds to use and improve the workings of the economy and this would lead to economic growth. The findings from the study supported the Laffer curve theory. The Laffer curve theory simply revealed that any change in tax rate will have economic effect in areas of work, output, employment, and in consequence the tax base by contributing to expand the activities through incentives. The findings showed that tax revenues variables of company tax, petroleum tax and value added tax had significant impact on the economy as a whole. Hence, any change in any of the variable would impact the GDP directly. The findings from the study also supported the endogenous growth model which explained that economic growth is influenced by internal factors rather than external factors. Tax was one of the internal factors as it is generated internally through the workings of human capital. The findings reveal tax revenue to be significant in impacting economic growth, hence, supporting the theory

5.1 Recommendation

Based on the findings, the study recommends trainings, seminars, and workshops should be organized by government tax agencies to the Nigerian public, students in higher institutions, and companies on the importance and benefits of tax revenue to the economy. There should be a more effective supervision of the tax revenue by the tax regulatory authorities. This would improve the safety and security of the purposes of tax revenue in Nigeria. Company income tax was negatively significant to the economy. Hence, tax authorities should encourage companies to pay tax so as to improve the growth of the economy which the companies would benefit from. Tax holidays or incentives should be given to companies and institutions and individuals who have been compliant to tax payment. This would encourage such institutions to keep paying tax as at when due. The Nigerian government should judiciously use the funds for the tax to improve the capital and recurrent expenditures and also improve on infrastructures. This would encourage the populace to benefit from the tax paid and continue to pay it.

This present study contributes to tax and economic growth literature by proving the importance of company income tax, petroleum profit tax, and value added tax to the growth of the Nigerian economy. Further researchers can examine other tax revenues like the import duties and excise duties and how they impact Nigerian economic growth. Other econometric techniques like regression can be used by further researchers to examine the same subject matter. There are notable drawbacks in the course of this study which includes lack of statistics to cover other sub-Saharan African nations for the period. Therefore, the study enjoins other researchers to consider studying other nations in African continent for a comparative result.

Contributors’ information

Ayeni Olasubomi Adefolake is a 2021/2022 graduating set from the Department of Accounting at Covenant University Ota in Ogun State, Nigeria. Her study focuses on taxes and economic growth in an emerging nation.

Dr. Cordelia Onyinyechi Omodero is an Associate member of the Institute of Chartered Accountants Nigeria and a full-time Lecturer in the Department of Accounting, College of Management and Social Sciences, Covenant University Ota, Ogun State, Nigeria. Her research interests include public finance, fiscal decentralization, taxes, and capital market analysis.

Acknowledgements

This paper is an excerpt from Ayeni Olasubomi Adefolake’s completed BSc Project from the Department of Accounting, Covenant University Ota, Ogun State, Nigeria. Ayeni Olasubomi Adefolake thanks the management of Covenant University for the privilege to conduct this research. She is grateful to her Supervisor (Dr. Cordelia Onyinyechi Omodero) for her dedication, time, patience, counseling, and professional guidance during the research period. She also expresses gratitude to all of her classmates for their countless contributions and assistance in finishing this project.

Disclosure Statement

The authors affirm that there are no conflicts of interest in this work.

Additional information

Funding

References

- Abomaye Nimenibo, W. A. S. (2017 b). The concept & practice of taxation in Nigeria. Port Harcourt, Nimehas Publishers.

- Abomaye-Nimenibo, W. A. S., Micheal, J. E. M., & Friday, H. C. (2018). An empirical analysis of tax revenue and economic growth in Nigeria from 1980 to 2015. Global Journal of Human Social Science: F Political Science, 18(3), 9–19.

- Adegbie, F., Olajumoke, J., & Kwarbai, J. (2016). Assessment of value added tax on the growth and development of Nigeria economy: Imperative for reform. Accounting and Finance Research, 5(4), 163–178. https://doi.org/10.5430/afr.v5n4p163

- Adeusi, A. S., Uniamikogbo, E., Erah, O. D., & Aggreh, M. (2020). Non-oil revenue and economic growth in Nigeria. Research Journal of Finance and Accounting, 11(8), 95–106. https://doi.org/10.7176/RJFA/11-8-10

- Agunbiade, O., & Idebi, A. A. (2020). Tax revenue and economic growth nexus: Empirical evidence from the Nigerian economy. European Journal of Economic and Financial Research, 4(2), 18–41. https://doi.org/10.46827/ejefr.v4i2.832

- Amadi, K. C., & Alolote, I. A. (2019). The Nomenclature of Taxation in Nigeria: Implications for Economic Development. Journal of International Business Research and Marketing, 4(4), 28–33. https://doi.org/10.18775/jibrm.1849-8558.2015.44.3004

- Anyandabu, J. O. (2004). Partnership taxation in Nigeria. ICAN Student Journal, 9(2), 15–17.

- Anyanfo, A. M. O. (1996). Public finance in a developing economy: The Nigerian case. The department of banking and finance. University of Nigeria.

- Appah, E. (2010). The problems of tax planning and administration in Nigeria: The federal and state governments experience. International Journal of Laboratory. Organic Psychology, 4(2), 1–14.

- Appah, E. (2014). Principles and practice of Nigerian taxation. Andy best publishers.

- Asaolu, T. O., Olabisi, J., Akinbode, S. O., & Alebiosu, O. N. (2018). Tax revenue and economic growth in Nigeria. Scholedge International Journal of Management & Development, 5 7 , 72–85. https://doi.org/10.19085/journal.sijmd050701

- Ayeni, A. P., Ibrahim, J., & Adeyemi, A. O. (2017). tax revenue and Nigerian economic growth. European Journal of Accounting, Auditing and Finance Research, 5(11), 75–85.

- Ayuba, A. J. (2014). Impact of non-oil revenue on economic growth: The Nigerian perspective. International Journal of Management Sciences and Business Research, 1(9), 12–22. https://doi.org/10.5923/j.ijfa.20140305.04

- Bruno, O. O., & Emmanuel, A. O. (2019). Tax revenue and the Nigerian Economy. International Journal of Academic Science Research, 3(2), 61–66.

- Chigbu, E. E., Akujuobi, L. E., & Appah, E. (2012). An empirical study on the casualty between economic growth and taxation in Nigeria. Curr. Res. J. Econ. Theory., 4(2), 29–38.

- Dladla, K., & Khobai, H. (2018). The impact of taxation on economic growth in South Africa. Nelson Mandela University.

- Edewusi, D. G., & Ajayi, I. E. (2019). The nexus between tax revenue and economic growth in Nigeria. International Journal of Applied Economics, Finance and Accounting, 4(2), 45–55. https://doi.org/10.33094/8.2017.2019.42.45.55

- Etim, O. E., Nsima, J. U., Austin, U. N., Samuel, S. C., & Anselem, M. U. (2020). Petroleum profit tax, company income tax and economic growth in Nigeria. Journal of Finance Accounting and Auditing Studies, 6(4), 164–187. https://doi.org/10.32602/JAFAS.2020.034

- Etim, O. E., Nsima, J. U., Austin, U. N., Samuel, S. C., & Anselem, M. U. (2021). Comparative analysis of the effect of direct and indirect taxation revenue on economic growth of Nigeria. Account and Financial Management Journal, 6(7), 2403–2418. https://doi.org/10.47191/afmj/v6i7.05

- Eyisi, A. S., Egiyi, M. A., & Okafor, V. I. (2017). A comparative analysis of the VAT system of developed and developing economies (UK and Nigeria). Research Journal of Finance and Accounting, 8(22), 66–72. https://core.ac.uk/download/pdf/234632171.pdf

- Gbeke, K. K., & Nkak, P. (2021). Tax reforms and economic growth of Nigeria. Journal of Business and Management, 23(6), 16–23. https://doi.org/10.9790/487X-2306051623

- Hieu, H. N. (2019). Impact of direct tax and indirect tax on economic growth in Vietnam. Journal of Asian Finance, Economics and Business, 6(4), 129–137. https://doi.org/10.13106/jafeb.2019.vol6.no4.29

- Igbasan, E. (2017) tax revenue and economic growth of Nigeria. An unpublished thesis, Babcock University.

- Inyiama, O. I., & Ubesie, M. C. (2016). Effect of value added tax, customs and excise duties on Nigeria economic growth. International Journal of Managerial Studies and Research, 4, 53–62. https://doi.org/10.20431/2329-0349.0410005

- James, A., & Moses, A. (2012). Impact of tax administration on government revenue in a developing economy: A case study of Nigeria. International Journal of Business and Social Science, 3(8), 99–113.

- John, O. A., & Dickson, O. E. (2020). Tax revenue and economic growth in Nigeria. Journal of Taxation and Economic Development, 19(1), 15–34.

- Karumba, A. K. (2016). Impact of taxation on economic growth in Kenya. An Unpublished Thesis, University of Cape Town.

- Khadijat, A. Y., & Taophic, O. B. (2018). Effect of petroleum profit tax and company income tax on economic growth in Nigeria. Journal of Public Administration, Finance and Law, 100–121.

- Korkmaz, S., Yilgor, M., & Aksoy, F. (2019). The impact of direct and indirect taxes on the growth of the Turkish economy. Public Sector Economics, 43(3), 311–323. https://doi.org/10.3326/pse.43.3.5

- Laffer, A. B. (2004). the laffer curve: past, present and future. The Heritage Foundation.

- Macek, R. (2014). The impact of taxation on economic growth: Case study of OECD countries, review of economic perspectives. 14(4), 309–328.

- Mathew, A. A. (2014). The impact of tax revenue on Nigerian economy (case of federal board of inland revenue). Journal of Policy and Development Studies, 9(1), 109–121. https://doi.org/10.12816/0011186

- Mdanat, M. F., Shotar, M., Samawi, G., Muloot, J., Arabiyat, T. S., & Alzyadat, M. A. (2018). Tax structure and economic growth in Jordan, 1980-2015. EuroMed Journal of Business, 1(1), 102–127. https://doi.org/10.1108/EMJB-11-2016-0030

- Mukolu, M. O., & Ogodor, B. N. (2021). The effect of value added tax on economic growth of Nigeria. IAR Journal of Business Management, 2(1), 203–210.

- Musgrave, R. A., & Musgrave, P. B. (2004). Public finance in theory and practice. Tata McGraw Hill.

- Nigeria’s aggregate earnings. Universal Journal of Accounting and Finance, 9(4),783–789. https://doi.org/10.13189/ujaf.2021.090424.

- Nwezeaku, N. C. (2015). Taxation challenges and revenue generation in Nigeria. International Journal of Accounting, Taxation and Management, 6(2), 114–128. https://core.ac.uk/download/pdf/234695079.pdf

- Ofoegbu, G. N., Akwu, D. O., & Olive, O. (2016). Empirical analysis of effect of tax revenue on economic development of Nigeria. “International Journal of Asian Social Science, 6(10), 604–613. https://doi.org/10.18488/journal.1/2016.6.10/1.10.604.613

- Ogbonna, G. N., & Appah, E. (2016). Effect of tax administration and revenue on economic growth in Nigeria. Research Journal of Finance and Accounting, 7(13), 49–58. https://core.ac.uk/download/pdf/234631498.pdf

- Ojo, S. (2008). Fundamental Principles of Nigerian Tax. Sagribra Tax Publications.

- Okafor, R. G. (2012). Tax revenue generation and Nigerian economic development. European Journal of Business and Management, 4(19), 49–56. https://core.ac.uk/download/pdf/234624448.pdf

- Okoye, P. V. C., & Ezejiofor, R. (2014). The impact of e-taxation on revenue generation in Enugu, Nigeria. International of Advanced Research, 2(2), 449–458. https://www.journalijar.com/article/948/the-impact-of-e-taxation-on-revenue-generation-in-enugu,-nigeria/

- Oladipupo, T. O., & Ibadin, C. S. (2015). Impact of tax revenue on economic growth in Nigeria. European Journal of Economics, Finance and Administrative Sciences, 48(12), 123–134.

- Olalekan, S., & Oyedokun, G. E. (2019). Relevance of Adam Smith canons of Taxation to the Modern Tax System. Journal of Taxation and Economic Development, 18(3), 14. https://ideas.repec.org/a/ris/jotaed/0028.html

- Omodero, C. O., Okafor, M. C., & Nmesirionye, J. A. (2021). Personal Income Tax Revenue and Nigeria’s aggregate earnings. Universal Journal of Accounting and Finance, 9(4), 783–789. https://doi.org/10.13189/ujaf.2021.090424

- Otu, O. H., & Adejumo, T. O. (2013). The effect of tax revenue on economic growth in Nigeria. International Journal of Humanities and Social Science Invention, 2(6), 16–26. https://www.academia.edu/20772705/The_Effects_of_Tax_Revenue_on_Economic_Growth_in_Nigeria_1970_2011

- Peter, O. I., & Adesina, O. O. (2015). Indirect taxes and economic growth in Nigeria. Department of Accounting, University of Benin, Edo State.

- Salami, G. O., Apelogun, K. H., Omidiya, O. M., & Ojoye, O. F. (2015). Taxation and Nigerian economic growth process. Research Journal of Finance and Accounting, 6(10), 93–101. https://www.iiste.org/Journals/index.php/RJFA/article/view/22574/23387

- Samuel, S. E., & Tyokoso, G. (2014). Taxation and revenue generation: An empirical investigation of selected states in Nigeria. Journal of Poverty, Investment and Development, 4(1), 102–114. https://core.ac.uk/download/pdf/234695079.pdf

- Shahzad, A., Maqbool, H. S., & Nisar, A. (2018). Indirect taxes and economic growth: An empirical analysis of Pakistan. Pakistan Journal of Applied Economics, 28(1), 65–81. http://www.aerc.edu.pk/wp-content/uploads/2018/04/Paper-653-SHAHZAD-V-1.pdf

- Udofot, P. O., & Etim, E. O. (2017). The effect of tax revenue components from SME’s and economic growth of Nigeria.

- Unegbu, A. O., & Irefin, D. (2011). Impact of VAT on economic development of emerging nations. Journal of Economics and International Finance, 3(8), 492–503.

- Yadawananda, N., & Achal, K. G. (2020). Tax structure and economic growth: A study of selected Indian states. Journal of Economic Structures, 9(38), 1–12. https://doi.org/10.1186/s40008-020-00215-3

- Yahaya, K. A., & Bakare, T. O. (2018). Effect of petroleum profit tax and company income tax on economic growth in Nigeria. Journal of Public Administration, Finance and Law, 13(1), 100–121. https://www.jopafl.com/uploads/issue13/EFFECT_OF_PETROLEUM_PROFIT_TAX_AND_COMPANIES_INCOME_TAX_ON_ECONOMIC_GROWTH_IN_NIGERIA.pdf

- Zakariya’u, G., & Abdurrahman, A. P. (2015). Tax evasion and Nigeria tax system: An overview. Research Journal of Finance and Accounting, 6(8), 203–211. http://repo.uum.edu.my/id/eprint/16182/1/88.pdf