Abstract

This paper sought to establish the competency skills required by accountants to utilise 4IR technologies at their work places. The following specific questions guided the study: What constitutes an accountant who is fit for purpose in the 4IR era? What needs to be done for accountants in Africa to remain relevant? To answer these questions the research adopted a qualitative research approach. A structured interview guide and document review was used to gather qualitative data. Telephone interviews were conducted with the selected members for the interview due to the covid-19 epidemic. Secondary data was gathered through desk research, which included analyzing various academic curricula of various institutions and syllabi of Professional Accounting Organisations. The results from the study on the first objective show that an African accountant needs mostly computer skills and critical thinking skills to effectively navigate in the technology driven era. Other skills identified were emotional intelligence, technical and analytical skills. The second research question indicated that African accountants are expected to have data management skills to effectively execute their duties in this digital era. These skills include information technology skills, data analytics, complex problem solving, specialised software, and business intelligence. These skills need to be fused in the curricula of training institutions. Professional Accounting Organizations, universities, and employers should structure their training curricula in such a way that they impart cutting-edge technology such as block chain and robotics as part of digital accounting so as to eliminate manual accounting and enhance quality financial reporting.

PUBLIC INTEREST STATEMENT

This article explores how the fourth industrial revolution has impacted on the accountancy profession in Africa, in particular on key competences required by an African accountant to fully embrace the digital world. A qualitative inquiry was conducted on the competency skills required by accountants to utilise 4IR technologies at their work places. The results from the study show that an African accountant needs mostly computer skills and critical thinking skills to effectively navigate in the technology driven era. The results also show that professional accountancy requires data management skills to effectively execute their duties in this digital era. These skills include information technology skills, data analytics, complex problem solving, specialised software, and business intelligence. As a result, Professional Accounting Organizations, universities, and employers should structure their training curricula in such a way that they impart cutting-edge technology such as block chain and robotics as part of digital accounting so as to eliminate manual accounting and enhance quality financial reporting.

1. Introduction

The accounting profession has been evolving since the discovery of debit and credit by Luca Decapolis in 15th century. However, the Fourth Industrial Revolution (4IR) has changed the ways of doing business and this has impacted on the accounting discipline (Blockgeeks, Citation2019; Hoffman, Citation2017). The 4IR was coined by Klaus Schwab as the “big idea” that builds on the previous digital revolution, but is very distinct in the sheer speed, magnitude and disruptive impact it potentially could have on current emerging business models based on a “sharing/on-demand” economy (Yang, Citation2018). 4IR requires the blending of the emergent technology of artificial intelligence, automation and robotics with the ever-increasing access and use of data and information learners have, due to developments in mobile device technologies.

Digitalization is affecting organisations on how they organise, process and evaluate the financial data which improves productivity and saves costs and time. In addition, it affects auditors and also helps them to uncover fraud, inconsistencies and other faults that affect organisations (Liffreing, Citation2018). 4IR has come with different technological innovations such as block chain—based distribution ledger, big data analytics, artificial intelligence and robotics that are likely to affect the accounting jobs (Hoffman, Citation2017). This type of innovation does not require intermediaries and this helps to minimize the costs. The block chain is changing the accounting and auditing processes in the world. It is creating new opportunities and challenges in accounting and auditing. Block chain technology can be applied in property records, banking, supply chain, auditing, anti-money laundering, customer survey, stock trading, smart customers (Blockgeeks, Citation2019). Information technology offers opportunities to accounting professionals and practitioners to explore the environment and claim the benefits related to digitalization (Liffreing, Citation2018). Digitalization is making machines perform accounting tasks better and faster than humans. This creates challenges on how humans are able to stay competitive and add value in the field of accounting and auditing (Blockgeeks, Citation2019).

Addaney (Citation2018) published a document explaining how accounting professionals could help in the realization of the Sustainable Development Goals (SDGs). The African Union Agenda 2063 is a continuation of the SDGs. The African Union Agenda 2063 is based on principles which include a prosperous Africa, based on inclusive growth and sustainable development; an integrated continent based on ideal Pan—Africanism and vision for African renaissance; an Africa of good governance, democracy, respect of justice and rule of law; an Africa with strong cultural identity, common heritage, values and ethics; an Africa whose development is driven by the potential of African people especially the youth and women. An Africa caring for its children and an Africa strong, united and an influential global player and partner (Addaney, Citation2018; Ndizera & Hannah, Citation2018). The 4IR era is changing the field of accounting (Blockgeeks, Citation2019). Therefore, the accounting academicians, practitioners and researchers need to broaden the boundaries of the accounting discipline in order to integrate the SDGs, African Union Agenda and the 4IR.

The accounting professional is endowed with many advantages which are direct while others are indirect. Konan (Citation2021) points out that accounting plays a very important role in ensuring accountability of the society and also enhancing planning and control which are major ingredients in the development of the country. Weak accounting and auditing are the major roots for corruption in many African states (P. Lassou, Citation2014; P.J.C Lassou, Citation2021).

In spite of the importance of the accounting profession in ensuring development and achieving the SDGs, the accounting professional in Africa is faced with a number of challenges. Previous research by Konan (Citation2021), P.J.C Lassou (Citation2021), (Tawiah & Tawiah, Citation2019) and Soobarayen et al. (Citation2017) show that the accounting professional in Africa is faced with a lack of capacity to implement accounting reforms, poor technological advancement as well as political and institutional interference at the workplace.

There was consensus among accountants that their very existence was being threatened by technologies that surround 4IR e.g., Smart Contracts through block chain technology, Artificial Intelligence and Machine Learning (Ryan, Citation2019). In order to accomplish accounting tasks, accountants had to possess both technical and social skills (Wahyuni, Citation2018). This study thus seeks to understand and inform the accounting profession by achieving the following research objectives two questions: What constitutes an accountant who is fit for purpose in the 4IR era? What needs to be done for accountants in Africa to remain relevant?

2. Literature review

2.1. Theoretical perspective

The theoretical framework selected for the study is the Diffusion of Innovations (DOI) by Rogers (Citation1995; Citation2003) and Technology Acceptance Model (TAM) by Davis (Citation1986). The two theories are well known in the information systems and technology literature. The theories are used in the accounting field to gain insights into the 4IR accounting technologies diffusion and the extent of accounting technology usage as a distribution channel for accounting services.

2.1.1. Diffusion of Innovations (DOI)

Rogers () posits that for diffusion to occur there must be a new thinking, a new idea or an innovation. Rogers (Citation2003) got challenged on the need to obtain a deep understanding on how a society accepts, adopts or rejects an innovation. Diffusion pervades an organization when a new idea or innovation has been embraced. Technology diffusion is affected by various factors within an environment. 4IR accounting technology adoption for instance, is dependent upon the level of advantage the technological advancement will bring to the association; the consistency of the development with the adopters’ current qualities and culture; the unpredictability or complexity of the advancement (ease of use); the capability of the thought for being executed on a preliminary premise (trialability), and the simplicity of watching the subsequent advantages (observability; Rogers, Citation1995). The factors mentioned above push for individuals within an organisation to be actively involved with their internal and external networks where these potential adopters find out about innovative developments that are applicable to their organisation’s necessitieshence effecting technology diffusion (Nguyen, Citation2019).

2.1.2. Technology Acceptance Model (TAM)

TAM postulates that the functionality of technological systems is related to interface characteristics and they affect adoption decisions (Davis, Citation1986). TAM as presented in has the following belief constructs:

perceived usefulness—use of technology should increase work output/job performance

perceived ease of use—minimum effort should be exerted to get work done through technology (free of effort)

Figure 1. Technology acceptance model: Davis (Citation1986).

The attitude or disposition towards utilizing the system in turn is also a key determinant of the behavioral intention to us which in turn determines the actual usage of the system as presented below:

TAM is one of the widely used technology acceptance model (Herweijer et al, Citation2005; Wang et al, Citation2003) In this study both TAM by Davis (Citation1986) and DOI by Rodgers (Citation1995) are combined and revised to determine 4IR accounting technology diffusion and adoption behavior. Hong and Seo (Citation2018) used TAM combined with Information Systems Success Models in Accountants in the republic of Turkey and concluded that strong external elements such as Service Quality and Experience had influence on both perceived ease of use (PEOU) and perceived usefulness (PU) of actual accounting software programs. Davis (Citation1986) postulates that any other variables that influence PEOU and PU are external and these are but not limited to technology usage procedures, involvement of users in technology design, computer technology viability (efficacy), the technology design characteristics, demographic characteristics of adopter population and potential adopter personal traits.

Despite TAM and DOI coming from different disciplines and authorities, the two theories are complimentary. Perceived Usefulness (PU) in Davis’s TAM is the relative advantage in Rodgers’s DOI and Perceived Ease of Use in TAM maps to DOI’s complexity attribute. Hence this study on 4IR for accountancy fuses the two theories. The changes in the complexities of 4IR is the basis of this research insofar as it tries to establish what an African accountant who is fit for purpose should be and the study also seeks to come up with a prescription of what needs to be done for African accountants in the face of a metamorphosing technological environment.

2.2. What is the fourth industrial revolution?

Liu and Xu (Citation2017) opines that 4IR it is the period from 2000 and beyond which relied more on cyber physical systems. 4IR centres on the connection of physical and cyber networks to allow actionable insights and real-time information flow (Olarewaju, Citation2021). It integrates manufacturing processes with innovative Information Communication Technologies (ICTs) and other intelligent technologies (Wang et al., Citation2003). These technologies lead to smart workplaces, quality services and products and business process efficiency. 4IR comes with tools such as Artificial Intelligence (AI), big data analytics, Virtual Reality (VR), Machine Learning (ML), robotics and Cloud Computing (CC) which are now widely used in the world. Herweijer et al. (Citation2005) examined how the fourth industrial revolution is offering huge opportunities to transform economies and societies. The study identified ten emerging 4IR technologies that were changing the society such as advanced materials, cloud technology, autonomous vehicles like drones, synthetic biology, virtual and augmented reality, artificial intelligence, robots, block chain technologies, 3D printing and internet of things.

2.3. Preparing an accountant in Africa who is fit for purpose in the 4IR technology era

There is a dearth of studies on the effects of 4IR on accountants in Africa. Many studies have been carried out in Asia and the developed world. For instance, a review in South Korea by Hong and Seo (Citation2018) concluded that 4IR pushes the need for accountants to focus on audit quality, reduce risk and promote audit innovation. These aspects are huge 4IR issues for accountants that should not be avoided. Financial and tax accountants have to improve their skills lest they are left behind by the advancing technology (Hong & Seo, Citation2018). When huge computational and routine tasks are handled by machines driven by 4IR technology, accountants are at risk of losing their relevance, unless they adapt and shift work focus to analytical work (Meinander & Soderling, Citation2020). Accountants might also face overwhelming amounts of data to process. A study by De Ruyter et al. (Citation2018) using evidence from UK and Australia established that new technologies would transform workplaces, displace jobs, create new jobs and change living conditions of accountants. How accountants would adapt especially in Africa, forms the basis of this study. However, a South African based review by Ackers (Citation2019) found little effects of 4IR on the role of accountants.

2.4. 4IR competency framework for an accountant in Africa in the face of a changing technological environment

Burritt and Christ (Citation2016) opine that there should be an upsurge of awareness on changes brought about by 4IR through continuous professional development education. Ndung’u and Signé (Citation2020) suggest that labour skills mismatch brought about by 4IR should be fixed because without basics like electricity and internet broadband that support 4IR, talk of becoming 4IR—compliant continues to become a pipe dream. Hong and Seo (Citation2018) propose that accountants should improve their skills in information technology (IT) by collaborating with IT professionals so that they can provide detailed and accurate information to their clients and various stakeholders who use accounting, financial and tax services.

Schwab (Citation2016) suggests that accountants will need to develop digital skills. Hence accountants have to keep abreast with the latest technology to be able to offer value-added services among them advising clients and proffering strategic insights on critical financial transactions (De Ruyter et al., Citation2018). This is supported by and Kruskopf et al. (Citation2019) who insist that accountants must adapt, shape and adjust the disruption caused by 4IR. Hamma-adama et al. (Citation2020) laments that not much is being done to adapt to 4IR thus he proposes that preparation is necessary in the area of right application (technology), legislative provision (regulation), and awareness/knowledge (social). The suggestions from Hamma-adama et al. (Citation2020) imply that accountants cannot go it alone. They have to be assisted by legislation while awareness of 4IR could be from the Professional Accountancy Organisations (PAOs) through development and provision of an effective Continuing Professional Development (CPD) program among other initiatives.

3. Methodology

This research is aimed at addressing two research questions namely, how has or how will 4IR technology affect the work of accountants in Africa? and what needs to be done for African accountants to remain relevant in the 4IR era (key competencies required for an African accountant to remain relevant)? With these questions, a qualitative inquiry grounded on interpretivism philosophical orientation has been preferred. Under this approach, researchers adopted a qualitative research design. Use of qualitative inquiry in research has been recommended by previous researchers (Burnard et al., Citation2020 & Grafton et al., Citation2011). This study adopted a qualitative research approach as it allows the researchers opportunity to gain an in-depth understanding of the fourth industrial revolution as it is applied to the accountancy processes. It gives room to researchers to interrogate the issues by engaging key experts in the filed across Africa.

3.1. Study population and Sampling

The population was chosen from the African continent and involved accounting professionals. There were 55 Professional Accounting Organizations (PAOs) representing 44 member nations (https://pafa.org.za), and there were 114,800 registered professional accounting members. The researchers noted that of the research unit some possessed superior information while others had inferior information and as such had to rely on key informants who were presumed to hold superior information. Telephone interviews were conducted with key informants across the African continent on how has the 4IR changed the accounting terrain and the competencies required for the african accountant to relain relevent. The interviews were administered to 48 accountants and auditors from Rwanda and Zimbabwe. Accountants from other nations were unable to be contacted through their PAOs since officers worked from home and obtaining personal phone numbers was difficult. Their business phone numbers, which we obtained on the internet, were unanswered. Interviews were performed with twelve (12) Rwandan accountants and thirty-six (36) Zimbabwean accountants. To identify those members who the researchers considered would be crucial informants for the study, the researchers utilized a snowball sampling technique. Some of those interviewed recommended other PAO members to the researchers. The researchers knew the majority of the interviews, and several were introduced to them by PAO workers.

3.2. Data collection

Interviews were used to collect primary data. A structured interview guide and document review were used to gather qualitative data. A telephone interview was conducted with the selected members for the interview due to the covid-19 epidemic. Interviews were utilized to obtain data by Marx et al. (Citation2020) and Surianti (Citation2020). Interviews allow research to gain an in-depth understanding of given phenomena as it allows further probing by researchers. Secondary data was gathered through desk research, which included analyzing various academic curricula of various institutions and syllabi of Professional Accounting Organisations.

3.3. Data analysis

One can utilize both inductive and deductive ways to analyse data (Burnad et al Citation2008). This paper used thematic analysis. Atlas- Ti. software was used in capturing data from interviews. Thematic analysis was used to understand the evolution of the fourth industrial revolution and how it has changed the accountancy profession as well as the key competencies required for the African accountant to remain relevant was thematic analysis. Such an approach, according to Burnard et al. (Citation2008), entails identifying themes and categories by looking at similarities and differences at various levels of abstraction.

4. Findings of the study

The study sought to establish the competency skills required by accountants to utilise 4IR technologies at their work places. The following main questions guided the study: What constitutes an accountant who is fit for purpose in the 4IR era? What needs to be done for accountants in Africa to remain relevant? Respondents were asked to identify the skills which make accountants in Africa fit for purpose. The major skills mentioned by respondents resulted in the following thematic areas and frequency of mention: computer skills (17), critical thinking (16), emotional intelligence (7), technical (2) and analytical skills (2). Respondents opined that the major skills revolved around the ability to use computers, critical thinking and emotional intelligence as shown by . This is evidenced by statements such as:

Figure 2. 4IR competency skills required by accountants (Source: Research data).

The skills needed to manage 4IR technologies are accounting computer-based skills need to be highly knowledgeable, critical thinking skills, technology use, problem solving.(Interviewee 8)

The skills needed to manage 4IR technologies are accounting computer-based knowledge where accountants will be able to Program, critical thinking skills, emotional intelligence.(Interviewee 9)

Analytical skills, technical skills and skills to adapt to fast technological changes. (Interviewee 27)

4.1. Data management skills required by accountants to succeed in the 4IR era

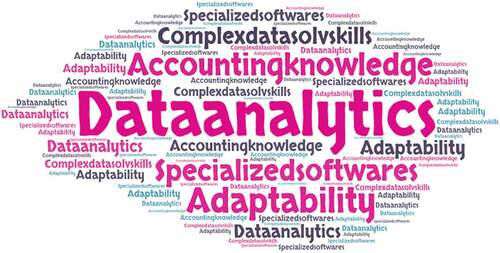

Respondents were asked to identify skills that are required in the efficient use and effective management of data. As illustrated by the word cloud in , the skills which prominently featured were data analytics (12) and accounting knowledge (6). Respondents showed that the two skills were pivotal in the life of an accountant by statements like:

Figure 3. Data management skills required by accountants to succeed in the 4IR era (Source: Research data).

… … . to be trained on data analytics skills so that they can analyse the data processed by specialized software(Interviewee 20)

… … . data analytics skills, and soft skills are the most important 4IR Technology skills need by accountants to remain relevant.(Interviewee 26)

… … . to learn a combined accounting knowledge and information system so as be familiar with digital accounting system.(Interviewee 3)

Due to the metamorphosis of technology, respondents were asked what would happen if they did not reskill to catch up with new 4IR trends. Respondents were of the view that accountants would become moribund if they did not reskill or do continuous professional development as one stated that:

The work of the accountants will be threatened, yes because 4IR technologies will be able to perform all duties which humans used to do.(Interviewee 6)

Another respondent pointed out that changing technologies in 4IR calls for accountants to also change. He said:

… …. (4IR) things in this world are changing quickly … … . accountants must keep learning new things to cope with new technology.(Interviewee 19)

A frightening statement by one respondent showed the seriousness accountants have to treat technological change. He stated that:

4.1.1. … accountants are threatened. They can become irrelevant … … … . If not reskilled.(Interviewee 22)

It also came to light that reskilling allows co-existence between accountants and 4IR technology as there would be job sharing. Computers would do routine tasks while accountants would do big data analysis and other high order tasks.

In light of the threats posed by the ever-changing technologies, respondents were asked the interventions expected from stakeholders so that accountants remain relevant in the 4IR era. As shown by the word cloud in , emerging themes centred on training (23), ICT infrastructure (12), affiliation to professional bodies (10) and aligning accounting curriculum (8). Respondents had this to say:

Doing accounting professional courses for being competent now and in the future.(Interviewee 3)

We have a lot of restrictions for Africa accountants such as ICT Infrastructure.(Interviewee 7)

They should subscribe on the accounting and finance professional bodies to have a chance of meeting other professionals around the world.(Interviewee 12)

… … there is need for curriculum review with main focus on practice. (Interviewee 14)

Figure 4. What needs to be done (Source: Research data).

Accounting is a profession found all over the world, thus respondents were asked what accountants should do to remain relevant and competitive internationally. Emerging themes as shown in , were continuous professional development (22), curriculum adaptation (19), international certification (8) and exchange programmes (6). Respondents had this to say:

Figure 5. Interventions to make accountants competitive internationally (Source: Research data).

Training programmes offered by international bodies offer relevant skills. (Interviewee 17)

Exchange programs may help.(Interviewee 8)

Acquire international certifications and competencies so as to standardise the accountants. International seminars and exposures also help.(Interviewee 10)

4.2. Discussion of results

The results of this qualitative inquiry show that the competencies required by an African accountant are basic computer skills, critical thinking, and emotional intelligences, technical and analytical skills. Computer skills were topping the least with analytical skills being the least. These results however contradicts Anshari and Hamdan (Citation2022) and Hoffman (Citation2017) whose findings in New Zealand pointed to soft skills as topping the most required skill competences by accountants to embrace fourth industrial revolution. Studies by Wahyuni (Citation2018) in China pointed to the need to have digital technology skills to effectively navigate the forth industrial revolution. The departure by the current results may be attributable to Africa lagging behind on basic information communication technologies such as computer applications, though their soft skills and confidence were found to be at par with their global peers. On data management skills results show big data analytics, Block chain technologies cloud computing and specialised softwares as mostly required and lacking among African accountants. The results dovetails with Olarewaju (Citation2021) and Lassou (Citation2021) findings who established that most accountants in the developing world are found wanting on big data analytics given the volumes which comes with digitisation of the accountancy profession. However, accountants in the European countries were found to be lacking soft skills in the mould of team playing, work ethic, growth mindset among others as noted by Anshari and Hamdan (Citation2022). Present results show that to address the skill deficit among African accountants, there is need to retrain accountants through continuous professional development and curriculum adaptation which contradicts Anshari and Hamdan (Citation2022) whose findings showed the need to incentivise Accountants in order to change their work ethic as well as team playing.

5. Conclusion

The research sought to address two research questions namely the competency skills required by accountants to effectively utilise the fourth industrial revolution technologies and data management skills to make the African accountant fit for purpose and policy interventions to make the African accountant a complete accountant the 4IR world.

The results from the study on the first objective show that an African accountant needs mostly computer skills and critical thinking skills to effectively navigate in the technology driven era. Other skills identified were emotional intelligence, technical and analytical skills. These form the backbone of competencies required by accountants to remain relevant in this knowledge community.

The results relating to the second research question indicated that accountants in Africa are expected to have data management skills to effectively execute their duties in this digital era. These skills include information technology skills, data analytics, complex problem solving, specialised software, and business intelligence. Information technology skills and data analytics were found to be topping the list on data management skills. These skills need to be fused in the curricula of training institutions.

5.1. Theoretical implications

This empirical study is one of the first qualitative inquiries into competencies required by accountants in Africa to fully embrace the fourth industrial revolution incorporating the whole of African continent. Few studies had interrogated the subject regionally and were focusing on secondary education accountancy curricula (Liu & Xu, Citation2017; Ndizere et al., Citation2018; Nguyen, Citation2019). Thus interrogating the issues at tertiary level and professional accountants adds a new and relevant paradigm to understanding key competencies needed for the industrial revolutions. The role of cloud computing in the covid-19 disruptions has been reviewed. The comprehensive inquiry of these technologies and key competencies required in the accountancy profession makes this research novel. This research also demonstrates the importance of cloud computing and big data analytics as well as internet of things in this digital era where every sector is looking at ways in which these disruptive technologies can be applied to their operations in a way that enhance their operations.

5.2. Practical implications

The study proffers recommendations that are meant to improve the readiness of accountants in Africa to use 4IR technologies to improve their work. The recommendations are as follows:

PAOs, universities, and employers should structure their training curricula in such a way that they impart cutting-edge technology such as block chain and robotics as part of digital accounting so as to eliminate manual accounting and enhance quality financial reporting. This helps addressing the competence gap on big data analytics use such as block chain technologies, cloud computing which are critical especial in the context of travel restrictions induced by covid-19 as such technologies allow accountants to work from home.

The second research objective examined the competencies required of African accountants in order to apply 4IR. The findings also reveal a lack of expertise in the areas of machine learning, robotics, and artificial intelligence. Accountants should be trained on how to use 4IR technology to increase audit quality and reduce audit risk. While universities train auditors to a basic level, PAOs should be on the lookout for new applicable technology that can be implemented and used by their employees. In addition, universities need to engage in exchange programs with PAOs so that learners can tap in the skills from professional accountancy. Cross pollination of ideas need to be fostered between instructors from universities and PAOs through exchange programs. Students are also encouraged to be subscribed to professional bodies. This is expected to keep university students and graduates up to date on professional accounting. Universities also need to invest in ICTs especially those that facilitate student learning on digital accounting technologies. On the part of the government tax reliefs on ICTs if adopted help on accessibility of gadgets that facilitate learning of digital accounting. The study recommends that employers should sponsor the retraining of accountants, improve network connectivity at their workplaces and governments should facilitate ICT infrastructural developments.

5.3. Limitations and future research directions

The research addressed key competencies required for an African accountant to effectively navigate the fourth industrial revolution terrain by studying the competences which accountants poses against what is required thus establishing the existing skills gap of the African accountant. This area on the skills and competencies required by African accountant is not cast in stone; the paper left out a lot on fourth industrial revolution which the researchers feel can add value to adaptability of fourth industrial revolution in the accounting profession. Future studies can focus on individual technologies for instance, block chain technologies on quality of final accounts, or alternatively, fourth industrial revolution technologies and audit quality. A quantitative research on the same area can be conducted in order to establish the effect of adoption of 4IR technologies on quality of financial reporting in the African continent. These areas if explored can add value to the accounting profession.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Rangarirai Mbizi

Rangarirai Mbizi is a senior lecturer and a well-known researcher at Chinhoyi University of Technology. In addition to the current manuscript, he has produced a number of peerreviewed research publications on the accounting profession, agricultural finance, technology, and financial inclusion. He is passionate about the role that Fintech (a fourth IR element) and the accounting profession may play in advancing Africa’s development aspirations. Rangarirai Mbizi has an academic experience that spans more than ten years in Finance including in the banking sector. My colleagues and I are focusing specifically on the accounting and finance professions as we examine a broader picture of the fourth industrial revolution.

References

- Retrieved (20 March 2021) From. https://pafa.org.za

- Ackers, B. (2019). Accounting for Rhinos – the case of South African National Parks. Social Responsibility Journal, 15(2), 186–13. https://doi.org/10.1108/SRJ-10-2017-0198

- Addaney, M. (2018). Education law, strategic policy and sustainable development in Africa. In Palgrave Macmillan.

- Anshari, M., & Hamdan, M. (2022). Understanding knowledge management and upskilling in fourth industrial revolution: Transformational shift and SECI model. VINE Journal of Information and Knowledge Management Systems, 52(3), 373–393.

- Blockgeeks. (2019). What is block chain technology? A step-by-step guide for beginners. Retrieved: https://blockgeeks.com/guides/what-is-blockchain-technology/

- Burnard, P., Gill, P., Stewart, K., Treasure, E., & Chadwick, B. (2008). Analysing and presenting qualitative data. British Dental Journal, 204(8), 429–432. https://doi.org/10.1038/sj.bdj.2008.292

- Burritt, R., & Christ, K. (2016). Industry 4.0 and environmental accounting: A new revolution? Asian Journal of Sustainability and Social Responsibility, 1(1), 23–38. https://doi.org/10.1186/s41180-016-0007-y

- Davis, F. D. (1986). A technology acceptance model for empirically testing new end-user information systems: Theory and results. [Doctoral dissertation]. Sloan School of Management, Massachusetts Institute of Technology.

- De Ruyter, A., Brown, M., & Burgess, J. (2018). GIG work and the fourth industrial revolution: Conceptual framework and regulatory challenges. Journal of International Affairs, 72(1), 37–50.

- Grafton, J., Lillis, A. M., Mahama, H., & Grafton, J. (2011). Mixed methods research in accounting. Qualitative Research in Accounting & Management, 1(1), 5–21. https://doi.org/10.1108/11766091111124676

- Hamma-adama, M., Salman, H., & Kouider, T. (2020). Blockchain in construction industry: Challenges and opportunities. 2020 International engineering conference and exhibition. https://rgu-repository.worktribe.com/output/828858.

- Herweijer, C., Combes, B., Johnson, L., McCargow, R., Bhardwaj, S., Jackson, B., & Ramchandani, P. (2005). Enabling a sustainable fourth industrial revolution: How G20 countries can create the conditions for emerging technologies to benefit people and the planet economics. Discussion Papers, No. 2018-32. Kiel Institute for the World Economy (IfW), Kiel.

- Hoffman, C. (2017). Accounting and auditing in the digital age. Retrieved 02 November 2020 From. http://xbrlsite.azurewebsites.net/2017/Library/AccountinandAuditinginTheDigitalAge.pdf

- Hong, S., & Seo, C. R. (2018). Developing a block chain based accounting and tax information in the 4th industrial revolution. Journal of the Korea Convergence Society, 9(3), 45–51.

- Konan, A. S. K. (2021). Accounting polycentric in Africa. Framing an accounting and development research agenda. Critical Perspective on Accounting, 78. Elsevier. https://doi.org/10.1016/j.cpa.2020.102234.

- Kruskopf, S. H. A. W. N. I. E., Lobbas, C. H. A. R. L. O. T. T. A., Meinander, H. A. N. N. A., Söderling, K. I. R. A., Martikainen, M. I. N. N. A., & Lehner, O. M. (2019). Digital accounting: Opportunities, threats and the human factor. ACRN Oxford Journal of Finance and Risk Perspectives, 8, 1–15.

- Lassou, P. (2014). Political economy of accounting and governance in Africa. Conference paper.

- Lassou, P. J. C. (2021). Accounting and development in Africa. Critical Perspective on Accounting, 78((2021).). 10.1016/j.cpa.2020.102168

- Liffreing, I. (2018). PwC launches 2-year digital skills course to train 1,000 employees on everything from drones to blockchain. Digiday UK. https://digiday.com/marketing/pwc-launches-two-year-digitalskills-course-train-1000-employees-everyth.

- Liu, Y., & Xu, X. (2017). Industry 4.0 and cloud manufacturing: A comparative analysis. Journal of Manufacturing Science and Engineering, 139(3), 3. https://doi.org/10.1115/1.4034667

- Marx, B., Mohammadali-Haji, A., & Lansdell, P. A. (2020). University accounting programmes and the development of Industry 4.0 soft skills. Journal of Economic and Financial Sciences, 13(1), 1–17. https://doi.org/10.4102/jef.v13i1.470

- Meinander, H., Söderling, K., Meinander, H., Söderling, K., Martikainen, M., & Lehner, O. (2020). Digital accounting and the human factor: Theory and practice. ACRN Journal of Finance and Risk Perspectives, 9(1), 78–98. https://doi.org/10.35944/jofrp.2020.9.1.006

- Ndizera, V. &., & Hannah, M. (2018). A critical review of Agenda 2063: Business as usual? African Journal of Political Science and International Relations, 12(8), 142–154. https://doi.org/10.5897/AJPSIR2018.1114

- Ndung’u, N. S., & Signé, L. (2020). Capturing the fourth industrial revolution: A regional and national agenda. https://media.africaportal.org/documents/ForesightAfrica2020Chapter5_20200110.pdf

- Nguyen, V. D. (2019). Determinants influencing the application of electronic invoice on accounting software in the Fourth Industrial Revolution Era. In Management Accounting Research, 13, 379-400.

- Olarewaju, O. M. (2021). Fourth industrial revolution, accounting profession well-being, and environmental well-being in South Africa. https://doi.org/10.4018/978-1-7998-3347-5.ch010

- Rogers, E. M. (1995). Diffusion of Innovations (4th ed.). The Free Press.

- Rogers, E. M. (2003). Diffusion of Innovations (5th ed.). The Free Press.

- Ryan, C. (2019). How the fourth industrial revolution is reshaping accounting. Retrieved 12 December 2020 Fom. https://accountingweekly.com/how-the-fourth-industrial-revolution-is-reshaping-accounting/

- Schwab, K. (2016). The fourth industrial revolution. https://www.weforum.org/about/the-fourth-industrial-revolution-by-klaus-schwab

- Soobarayen, T., Tsamenyi, M., & Sapra, H. (2017). Accounting and Governance in Africa. Contribution and Opportunities for Further Research. Journal of Accounting in Emerging Economies, 7(4), 422–427. https://doi.org/10.1108/JAEE-10-2017-0101

- Surianti, M. (2020). Development of accounting curriculum model based on industrial revolution approach. Research Journal of Finance and Accounting, 11(2), 116–123.

- Tawiah, & Tawiah, V. (2019). The State of IFRS in Africa. J. Journal of Financial Reporting and Accounting, 17(4), 635–649. https://doi.org/10.1108/JFRA-08-2018-0067

- Wahyuni, T. (2018). The role of information technology in supporting accountant profession in the era of industrial revolution 4.0. In 3rd International Conference on Vocational Higher Education (ICVHE 2018). Atlantis Press. (256–264)

- Wang, Y., Ma, H.-S., Yang, J.-H., & Wang, K.-S. (2003). Industry 4.0: A way from mass customization to mass personalization production. Advances in Manufacturing, 5(4), 311–320. https://doi.org/10.1007/s40436-017-0204-7

- Yang, P. A. (2018). Educational mobility and transnationalization. In N. W. Gleason (Ed.), Higher education in the era of the fourth industrial revolution (pp. 39‒65). Palgrave, Macmillan.