?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study examines the association between audit committee characteristics, namely audit committee independence, audit committee financial expertise, audit committee gender diversity, size of audit committee and frequency of audit committee meeting, and corporate governance disclosure (CGD). The paper develops a comprehensive literature review using a bibliometric analysis with Scopus database from 2004 to 2022 and offers insight into the relationship between audit committee attributes as independent variables and level of corporate governance disclosure as a dependent variable. The dependent variable is measured basing on a scorecard of Vietnam-Listed Company Awards (VLCA). The set of scorecard questionnaire is then Cronbach Alpha tested to assure the reliability and consistency. The result contributes to extant literature a measurement of CGD in Vietnam. The multiple regression is applied over a sample of 210 non-financial listed companies in 2021. The findings show that audit committee independence and size of audit committee are significantly associated with level of CGD. The empirical evidence also reveals that firm size is statistically linked to CGD indicating the capital demand of large companies. Overall, the study might be of interest to professionals, policymakers and regulators regarding the establishment of regulations concerning the audit committee structure.

1. Introduction

In recent years, corporate governance including issues of disclosure and transparency are important instruments to protect investors’ interest and performance of the capital market (Cadbury Committee, Citation1992; COSO, Citation2013; OECD, Citation2004). Vietnam, an emerging country where information disclosures lacks of accountability and transparency, have witnessed devastating stock market manipulation scandals of FLC group, Tan Hoang Minh group in the 2nd quarter of 2022. The corporate governance disclosure appears to be the biggest concern for the Government authorities and market regulators when the economy has been recovering after the COVID pandemic. From society’s perspectives, the increase in the number of corporate governance reports (CGR) that do not achieve expected level of community trust have been raising concerns over the reliability and credibility of corporate governance disclosure (CGD). In the context of Vietnam, the manipulated information on CGR have caused serious damage to investors and affected operations of Vietnam’s stock exchange. Current situations in emerging countries, typically in Vietnam, illustrates the need for investigation factors that affect CGD.

Agency theory depicts the situation that companies with high agency theory will try to reduce the costs of control mechanism and voluntary disclosure. The issue reflects information asymmetry between firm and outside investors (Akhtaruddin & Haron, Citation2010; Li et al., Citation2012). Although there are several methods for communicating important corporate information including official company website such as press releases (Healy & Palepu, Citation2001). However, the CGR remains the most important channel for communicating with the principals and outsider investors. The corporate governance report disclosure (CGRD) have been broadly analyzed in previous literature (Cheng & Courtenay, Citation2006; Dwekat et al., Citation2020; Simnett et al., Citation2009). The main reason is that the CGRD is subject to strict regulation and scrutinized by external regulators such as the State Securities Exchange Commission.

Current situation and extant literature have addressed concerns over corporate governance report disclosures, especially in the context of emerging countries.

The quality of corporate governance disclosure itself are affected by two underlying factors: external factors (macroeconomics, Government regulation) and internal factors (corporate governance, internal control). However, it is unclear from extant literature whether and how these underlying factors affect the level of corporate governance disclosure. Additionally, prior research are interested in corporate governance disclosure of developed countries in the Europe and the USA. Few evidences have come from developing economies such as Adelopo (Citation2011), Appiah et al. (Citation2016), and Boateng et al. (Citation2022) focused their studies on developing economies and have stated that the enhanced disclosures can attract foreign investment, reduce political and regulation intervention.

In the scope of the research, we choose audit committee characteristics as the setting for this study for two following reasons. Firstly, theoretical framework generally stated that audit committee as a sub—component of control environment which is considered as the foundation for all other components of internal control, and it has an influence on each of the three objectives and over all unit and entity activities (COSO, Citation2013). From this perspective, it is agreed that audit committee plays a key role in monitoring management disclosure and the effectiveness of internal control (Bilal et al., Citation2018; Kao & Chen, Citation2019). The explained reason is that control environment of internal control should begin with the board of directors and senior management, who establish what has come to be known as management’s “tone of the top” for every enterprise. Secondly, the extant literature on the relationship between CGD and audit committee characteristics (Haji, Citation2013; Shamil et al., Citation2014; Ahmed & Nicholls, Citation1994; Hossain et al. (Citation2017);; El-Bassiouny and El-Bassiouny (Citation2019); Hanen and Jamel (Citation2021); Girella et al., Citation2019); Ananzeh et al., Citation2022) employs variety of settings with mixed results.

In this study, we explore the relationship between corporate governance disclosure and features of audit committee characteristics. Although the current literature has addressed the existing inter-relationship between audit committee characteristics and CGD, this research is distinguished and rationale by the number of research condition. First, as an emerging country in South East Asia, Vietnam is plagued by low adherence to international benchmarks. The significant differences in financing, ownership and governance structures between developing and developed countries provides further rationale for this research. Two, we employ a scorecard for CGD based on the Annual Vietnam-Listed Company Awards (VLCA), which is permanently organised by Vietnam Investment Review (VIR) and the two biggest exchange stock markets are the Hanoi Stock Exchange (HNX) and the Ho Chi Minh city Stock Exchange (HSX). The advantage of this scorecard is that it provides objectively and regulated benchmark to evaluate the disclosure score. By using R to apply Exploratory Factor Analysis (EFA) and Confirmatory Factor Analysis (CFA), we aim to test whether the underlying structures of VLCA scorecard is consistent with collected observations.

In doing so, the study makes several significant contributions to the current literature. First, it develops and expands the current literature review by proposing a comprehensive understanding of the literature of audit committee characteristics and corporate governance disclosure by utilizing the recently popularized methods of bibliometric analysis. Second, the study further examines the reliability and structural equivalence of VLCA scorecard. The result test would be helpful to policy makers, the government, specialist in Vietnam to have an insight overview in corporate governance control mechanism. In addition, the governing parties may wish to improve their guidance concerning CGD and CGR. It is also helpful for international researchers and regulators in other emerging countries to acknowledge about corporate governance scorecard. Finally, the study focuses on investigating the relationship between audit committee characteristics and corporate governance disclosure with a sample of Vietnam-listed companies in 2021 that could contribute some evidence from emerging economy.

To address these issues, the research is structured as follows. The literature review provides a comprehensive and theoretical background explains the connection between CGD and audit committee characteristics. The following part is methodology section to describe data collection, variable measurement and empirical test model. The final section includes the empirical result and some discussion on findings.

2. Literature review and hypothesis development

2.1. Corporate governance disclosure background

The corporate governance disclosure is mandatory for Vietnam-listed companies and often published on an annual basis as a separate, standalone report containing nonfinancial information about a firm’s policies and practices. In the context of rebuilding the economy after the wake of the COVID-19 crisis, Vietnamese Government aims to maintain corporate governance as an essential role to promote stronger, cleaner and fairer economics growth. It fosters an environment of market confidence and business integrity that supports capital market development. Moreover, Vietnamese firms rely heavily on external sources of finance outside the stock market, the disclosure policy have been promoting via other channels apart from the traditional financial reports to disclose additional information that meet the expectation and requirement of stakeholders primarily outside of capital market (Gerayli et al., Citation2021; Nguyen et al., Citation2020; Tran & Tran Quoc Trung, Citation2020). Several researchers suggest that when the financial reporting does not provide relevant information, stakeholders should rely on nonfinancial disclosure (Allegrini & Greco, Citation2013; Boateng et al., Citation2022). Especially in almost all developing economies, including Vietnam have experienced poor implementation or enforcement of laws and regulations as the bane of a sound system of corporate governance, nonfinancial disclosure.

Corporate governance report is a form of nonfinancial disclosure. In the context of Vietnam, the VLCA is annually organized with the effort to enhance the transparency of information disclosure, improving corporate governance and sustainable development toward integration into regional and international capital market. The scorecard of VLCA to evaluate level disclosure of corporate governance reports include four main areas: Rights and fair treatment among shareholders, Role of stakeholders, Disclosure and transparency, Responsibilities of Board of Directors. Some examples of content that might be in a CGR are: the reliance on corporate code of conducts, information of shareholder’s structure, remuneration of board of directors and audit committee, disclosure of risk control mechanism, independent members of board of directors, the number of accounting and finance expertise in board of directors., The average score on CGR increased to 52.59 in comparison to the score of 49.67 in 2020. In detail, group of large companies illustrates higher score (64.89) on CGR than other groups of medium (57.30) and small companies (48.62). The result of VLCA (2021) also indicates a connection between level of corporate governance disclosure and score of corporate governance report. A company which is evaluated as good corporate governance disclosure, achieves high score of CGR. The same report also indicted audit committees for their lack of effectiveness in terms of independence, expertise knowledge and experience etc to function as expected.

2.2. Corporate governance disclosure and audit committee characteristics

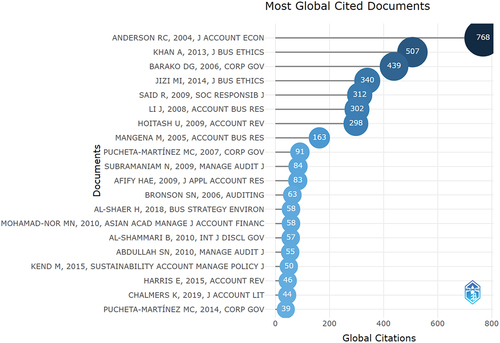

In order to present a comprehensive understanding of the literature on corporate governance and audit committee characteristics, the research utilizes the recently popularized methods of systematic literature review and bibliometric analysis. From the data of 112 publications sourced from the Scopus database from 2004 to 2022, the bibliometric mapping and citation analyses are graphically performed by R bibliometric.

Chart 1.1. The 20 articles that are most global cited documents.

Most cited documents provided evidence that audit committee are important elements affecting the quality of reporting process. Anderson et al. (Citation2004) examined the impact of audit committee characteristics on corporate yields spreads as audit committees are the direct mechanism that board use to monitor the financial accounting process. They used a sample of 252 industrial firms on the Lehman Brothers Fixed Income database and the S&P 500 and found that the committee independence is associated with a lower cost of debt financing. The research based on the creditors view audit committees and their characteristics as important elements in the financial accounting process. Magena and Pike (Citation2005) also tested the relationship between audit committee characteristics including audit committee independence, audit committee size and audit committee financial expertise and the level of disclosure in interim reports of a sample of 262 UK listed companies. The result provided a significant positive association between interim disclosure and audit committee expertise. There was also a significant negative association between shareholding of audit committee members (a proxy for audit committee independence) and interim disclosure. However, there was no significant relationship between audit committee size and the extent of disclosure.

In addition, Barako et al. (Citation2006) extended the literature by investigating the extent to which corporate governance attributes and company characteristics influence disclosure practices in developing countries, especially in Kenya. The study provided disclosure practices in annual reports of listed companies in Kenya from 1992 to 2001 and found that the presence of an audit committee is a significant factor associated with the level of voluntary disclosure, and the proportion of non—executive directors is found to be significantly negatively associated with the extent of voluntary disclosure.

Recently, legitimacy and political theories have been used to explain differences in the level of corporate governance disclosure. According to the theory, companies must ensure a decision-useful nonfinancial and financial disclosure strategy in alignment with stakeholders’ information needs. CGR as a supplement to financial disclosure, could be the first step to achieve legitimacy. In turn, organizations continually seek to ensure that they are perceived as operating within the bounds and norms of their respective societies, that is, they attempt to ensure that their activities are perceived by outside parties as being “legitimate”. In the context of accounting literature, many researchers conclude that corporate report disclosures can be generally employed by an organization to mitigate legitimacy threat and reduce the legitimacy gap (Chen et al., Citation2016; Deegan et al., Citation2000). Thus, the internal governance structure (such as board composition or audit committee) is likely to play a vital role in reducing legitimacy gap through extended corporate governance reports disclosures. In the light of the legitimacy theory perspective, firms have an implied social contract under the form of CGR with the community in which it works (Kend, Citation2015; Jizi et al., Citation2014); and the significant role of internal corporate governance enhance the CGR performance and disclosure (Dwekat et al., Citation2020; Alia & Mardawi, Citation2021; Jizi et al., Citation2014; Khan et al., Citation2013;). Martínez-Ferrero and García-Sánchez (Citation2017a) and Martinez-Ferrero et al. (Citation2017) indicate that size and the independence of the committee increase the level of disclosure of CGR. Furthermore, according to Liao et al. (Citation2018), gender diversity, size and frequent board meetings increase the implementation of CGD. Other studies reveal that gender diversity, especially a higher percentage of female members leads to better CGD implementation (Thi Thuy Anh & Phan Nha Khanh, Citation2017).

Additional explanation for information disclosure in CGR is offered by the agency theory. Corporate managers have incentives to withhold information to restrict the ability of the market to effectively monitor or access their performance, therefore creating an “information gap” between the principal and the agent. The problem between the principal and agent party which can be seen as “disclosure agency problem” could be reduced by a good corporate governance structure (Khan et al., Citation2013; Mustafa et al., Citation2018; Said et al., Citation2009). Pucheta Martinez and Garcia Meca (Citation2014) reveal that the principal agency conflict focuses on the expropriation of minority shareholders’ wealth by controlling shareholders. The research result also confirms that institutional audit committee members influence financial reporting quality. This result consistent with other research of Abdul Rahman et al. (Citation2006), Harris et al. (Citation2019).

2.3. Hypothesis development

2.3.1. Audit committee Independence

Agency theory addressed the phenomenon of “disclosure agency problem” between the shareholders, the principals and company executives, the agents. Therefore, the existence of corporate governance control function including external auditors, internal auditors and audit committee is stated to effectively monitor management’s behavior and reduce the asymmetric information situation. In order to enhance the quality of monitoring function, the audit committee is required to be independent by law and regulation. Specifically, since asymmetric information plays an important role to increase the share value of listed companies on stock exchange market, the independence of audit committee would enhance the benefit of investors (Adegboye et al., Citation2019; Holland, Citation2003; Li et al., Citation2012). The independence of the audit committee means that members of the audit committee have no economic financial interest, employment position or personal relationship with management. The threat of independence also could be eliminated if the non-executives of the committee do not have share ownership of company.

The UK Code (2010) suggests that an audit committee should be comprised of at least three members, who should be all be independent non-executive directors. In the case of Vietnam, Vietnam Ministry of Finance (2017) requires members of an audit committee in listed companies must not be executive directors, managers, accounting and finance staffs or members of external audit team. Members of audit committee are compulsorily approved by general meeting of shareholders. Several prior research in literature such as Cheng and Courtenay (Citation2006), Patelli and Prencipe (Citation2007), Akhtaruddin and Haron (Citation2010), Li et al. (Citation2012), and Madi et al. (Citation2014), and Almaskati and Hamdan (Citation2017) provide evidences that the presence of independent directors in audit committee is associated with more voluntary disclosure. In this research of Vietnam-listed companies, we expect independent audit committee to influence the level of corporate governance disclosure. The hypothesis is as following:

H1: There is a positive relationship between the level of corporate governance disclosure and the independence of audit committee.

2.3.2. Audit committee gender diversity

Even though prior research found mixed results, gender diversity on audit committee has been illustrated to enhance corporate productivity and the effectiveness of the committee (Aldamen et al., Citation2018; Green & Homroy, Citation2018). Almost all studies agreed that female executives performed better transformational leadership qualities than the male counterparts. Pathan and Faff (Citation2013) showed that female directorship tends to have high regards for their responsibilities by expending more effort on their tasks. In addition, Ibrahim and Al Harasees (Citation2019) confirmed that the conservative and ethical qualities of feminine improve the corporate governance and reduce the inherent risks and potential fraud risks. Din et al. (Citation2021) analyzed 302 listed firm on the Pakistan Stock Exchange and concluded that the female accounting expertise of audit committee enhance financial reporting quality. The study also stated that the female members improve corporate governance mechanisms and internal control. Thus, the second hypothesis is developed to assess the extent audit committee gender diversity affect annual report disclosure quality. The hypothesis is as following:

H2: There is a positive relationship between the level of corporate governance disclosure and the audit committee gender diversity.

2.3.3. Audit committee financial expertise

The requirement of financial expertises of an audit committee were not included in Vietnam regulations. However, according to Circular 155/2015 of Ministry of Finance, the annual reports consist of five main components namely: General corporate information, Operating and financial highlights, Letter to the shareholders from the chief executive officer, Management’s discussion and analysis (MD & A), Financial statements. Thus, the presence of financial expertises are expected to help the audit committee and managers to understand the nature of annual reports including financial statements and discern the substance of disagreement on daily accounting information process between management and external auditors (Bedard & Gendron, Citation2010; Bilal et al., Citation2018; Magena & Pike, Citation2005; Velte, Citation2018). In addition, in order to perform their role effectively, audit committee members should have relevant knowledge and competence to fulfill their tasks. Li et al. (Citation2012) confirmed the point that members with financial expertise will improve the quality of reporting and reduce the asymmetry of information. Such understanding by the audit committee should lead to the incentive of directors on information disclosure in order to communicate on firms’ value-creating processes and to support the valuation activities of the stock market participants (Li et al., Citation2012). Therefore, basing on the academic research and current situation analysis, the third hypothesis is as following:

H3: There is a positive relationship between the level of corporate governance disclosure and financial expertise of the audit committee.

2.3.4. Size of audit committee

Literature review reflect the mixed results on size of audit committee. Several studies supported for the resource dependency theory which argues that the larger audit committee are willing to devote greater resources and authority to effectively carry out their responsibilities (Allegrini & Greco, Citation2013). In accordance to this viewpoint, more directors on audit committee are more likely to bring diversity of views, expertise, experiences and skills to ensure effective monitoring (Bedard & Gendron, Citation2010; Li et al., Citation2012; Madi et al., Citation2014; Pearsons, Citation2009). However, some researchers argued that when the number of audit committee members increases, the performance is likely to suffer from process losses and diffusion of responsibility (Karamanou & Vafeas, Citation2005) and a larger committee will lack of room for flexibility (Afza & Nazair, Citation2014). Theories explains that organizations should set up a committee not so large to remain effectively, but reasonably large or large enough to fulfill the role (Allegrini & Greco, Citation2013). Although there is no standard for audit committee size, the Vietnam regulation prescribes a minimum of three executives. Due to the mixed results in literature review, the fourth hypothesis is as following:

H4: There is no relationship between the level of corporate governance disclosure and size the audit committee.

2.3.5. The frequency of audit committee meeting

The frequency of meetings refers to the number of meetings held by an audit committee during a financial year, with more meetings indicating high activity levels (Grandon et al., Citation2004). Prior research also considerably stated that the number of meetings held by the audit committee is a major determinant of committee’s effectiveness and efficiency as the more often the committee members meet the higher probability of achieving goals and organizational objectives (Raghunandan et al., Citation2003). Although studied in different areas, Li et al. (Citation2012) and Pearsons (Citation2009) found that when a committee meets more often, they have a tendency of making a higher voluntary disclosure. Additionally, empirical evidences in literature showed that there is a positive relationship between the number of audit committee meeting and voluntary disclosure. International regulation and standards recommend the frequency of meeting that should be a minimum of three or four meetings a year. Therefore, basing on the academic research and current situation analysis, the fifth hypothesis is as following:

H5: There is a positive relationship between the level of corporate governance disclosure and the frequency of the audit committee meeting.

3. Research methodology

3.1. Sample selection and data source

A criterion sampling technique is adopted for the study. According to Green (Citation1991), in order to evaluate the factor analysis of each independent variable such as t-test, regression coefficient, the minimum sample size should be 104 + m (m is the number of independent variables). According to Tauchen (Citation1986) condition for estimation of reliability for performing regression analysis is n > 200. Combined of two principles, the sample size chosen of 210 observations by authors is reasonable. The 210 observations are non-financial companies listed on the two Vietnam Stock Exchange that are the Ho Chi Minh City Stock Exchange (HOSE) and the Hanoi Stock Exchange (HNX) in 2021. The sample also includes 15 companies were awarded as the best corporate governance reports in 2021 (). Awarded companies illustrating high score of CGR that could demonstrate full and diversity characteristics of corporate governance. The representativeness of the awarded companies suggests the inclusion of selecting these typical economic entities in the sample to check the consistency and reliability of VLCA questionnaires.

Table 1. Awarded top 15 companies in term of size

We did not consider financial, banking and insurance companies because of their specific disclosure requirements and accounting regulations. The companies in initial sample are also in the VNX Allshare general index. VN Allshare is the Vietnamese third exchange index and issued after VN index at HOSE and HNX index at HNX, which cover nearly 90 percent of the combined market capitalization. The companies in the VNX Allshare need to meet three requirements namely: first, the company’s stocks must have been listed for at least six months without violating market rules; second, the company must have a stock return of at least 0.02 percent to ensure the company is eligible for business and finally, the minimum free-float rate must be no less than five percent.

The VLCA organizing committee develops a set of corporate governance marking criteria based on the principles of Organization for Economic Cooperation and Development (OECD). The set of marking criteria has been adjusted to be consistent with current regulations on corporate governance and in the context of Vietnamese enterprises. The criteria for evaluating the level of corporate governance disclosure by a company based on two main features:

Compliance with current Vietnamese laws on corporate governance for listed companies.

Good corporate governance practice based on the OECD/ G20 Corporate Governance Principles issued in 2015.

The VLCA set of scoring criteria includes 81 questions in four main parts:

Rights and Fair treatment of shareholders and basic ownership functions

The role of stakeholders

Disclosure and transparency

Responsibilities of the Board of Directors and Supervisory Board

Before examining the relationship between the corporate governance disclosure and audit committee characteristics, the study needs to confirm the reliability of marking criteria as well as internal consistency of the set of marking criteria in a group. We use Cronbach Alpha test to measure reliability or the consistency of VLCA scoring criteria.

3.2. Corporate governance disclosure and audit committee characteristics

The primary objective is to test the relationship between corporate governance disclosure a firm makes and features of audit committee characteristics of the firm. We begin by first documenting the overall association between corporate governance disclosure and audit committee characteristics. This provides a useful context within which to better understand the underlying relationship between different level of CGD and audit committee characteristics as well as to help situate this study within the extant literature. We use variation of the methodology which were used by Allegrini and Greco (Citation2013), Jizi et al. (Citation2014), Khan et al. (Citation2013), and Martínez-Ferrero and García-Sánchez (Citation2017a) to estimate the following model of corporate governance disclosure of firm i in the year 2021 using ordinary least square regression:

The model used in this study include year and industry fixed effects and heteroskedasticity-consistent standard errors clustered at firm level.

The model includes five audit committee characteristics variables representing characteristics of audit committee structures (AuditCommitteeIndependence, AuditCommitteeGenderDiversity, AuditCommitteeSize, FrequencyofAuditCommitteeMeetings. Other authors such as Jizi et al. (Citation2014), Khan et al. (Citation2013) also add several firm financial variables such as firm size, leverage ratio, profitability ratio, ownership diffusion to reflect an unresolved agency conflict. The financial variables are included in the proposed model in order to be control variables for the firm’s audit committee structure. Although, the study’s model is not identical to those in prior research, we expect that the tenor of existing results will be evident in our samples. In summary, the proposed model of our study as following:

Where:

i = firm 1 through n (n = 210); CGD = Corporate governance disclosure score, calculated by the scoring criteria of VLCA; ACI = Audit Committee Independence, measured by number of independent and non executive directors in audit committee; ACGD = Audit Committee Gender Diversity, measured by number of female directors in audit committee; ACFE = Audit Committee Financial Expertise, measured by number of directors with financial experience/ qualification in audit committee; COMSIZE = Size of Audit Committee, measured by total number directors in audit committee; FACM = Frequency of Audit Committee Meeting, measured by number of meetings held by audit committee in a year; LEV = Leverage, measured by the total book value of debt divided by total assets at the end of the year 2021; ROA = Return on Assets; SIZE = Firm size, measured by the natural logarithm of total revenue.

The regression model (1) shows relationship between CGD and audit committee characteristics using the ordinary least squares (OLS), however, to choose the most appropriate method, we also apply fixed effects model (FEM) and random effects model (REM). The paper then conduct the Breusch–Pagan Lagrange test to examine an alternative between OLS and REM, Hausman test to examine an alternative between REM and FEM, and finally conduct the Wald test to evaluate the most suitable model between OLS and FEM.

3.3. Dependent variable

Corporate governance disclosure is the independent variable and the construct of CGD is very complex, as illustrated by the numerous definitions found in the existing literature, therefore, it is not surprising that many different proxies have been employed to measure CGD. However, in the scope of this study, we use scoring index based on the VLCA set of marking criteria to measure the level of corporate governance disclosure by companies (see appendix for VLCA CGD scorecard).

There are two rounds of marking the CGD score. At the first round, an independent third party with experienced expertises conducts a preliminary assessment of the corporate governance content. Based on the shortlisted, Big4 auditing firms including: Deloitte, Ernst and Young, KPMG and PwC are invited to supervise the preliminary assessment result. After reviewing, Organizing Committee decide companies with good corporate governance to go to the final round. At final round, the Organizing Committee bases on the preliminary assessment result, the review result of auditing firms and internal evaluation discussion to award enterprises with highest corporate governance scores.

The set of criteria has 81 questions includes 29 questions assessing the compliance aspects, 35 questions assessing good governance practices and 17 additional questions. The questions are divided into 2 levels: level 1 questions evaluate general management requirements and maximum score for level 1 is 100; level 2 questions are additional questions and maximum score for level 2 is 10 (). Companies violates corporate governance regulations could be deducted up to 30 at level 2. The highest score a company could achieve for both level equivalents to 110. The value of dependent variable, CGD, therefore could range from 10 to 110 (Appendix 1).

Table 2. VLCA set of scoring criteria

Consistently with prior corporate governance disclosure index studies, we used the Cronbach’s coefficient alpha () to assess the internal consistency of VLCA scoring index. Internal consistency refers to the degree to which the items in a test measure the same construct. Tauchen(Citation1986) stated that “Cronbach’s alpha is a single correlation coefficient that is an estimate of the average of all the correlation coefficient of the items within a test. If alpha is higher than 0.6 then this suggests that all of the items are reliable and the entire test in internally consistent”.

3.4. Independent variables

The primary data on the corporate governance disclosure independent explanatory variables were manual collected from the annual corporate governance reports. Audit committee independence (ACI) is measured by number of non-executive directors in audit committee. Audit committee gender diversity (ACGD) is measured by number of female directors in audit committee. Audit committee financial expertise (ACFE) is measured by number of directors with financial experience/ qualification in audit committee. Size of audit committee (COMSIZE) is measured by overall number of directors in audit committee. Frequency of audit committee meeting (FACM) is measured by number of meeting held by audit committee in a year 2021 ().

Table 3. Definitions and measurement of variables

Other independent variables are selected on the basis of previous studies. Ahmed and Curtis (Citation1999), Allegrini and Greco (Citation2013), and Madi et al. (Citation2014), Zahd et al. (2020) and Boateng et al. (Citation2022) confirm significant and positive associations between disclosure levels and corporate size and leverage ratio. In accordance with Camfferman and Cooke (Citation2002), Allegrini and Greco (Citation2013), and Madi et al. (Citation2014), firm size (SIZE) also has been illustrated to be significantly and positively correlated with disclosure level. The result suggest that large sized companies tend to disclose more information than smaller companies. It could be explained that agency costs are associated with the separation of management from ownership which is likely to be greater in larger companies. In the study, the independent variable firm size (SIZE) is measured by the natural logarithm of the revenue in the year 2021. Alsaeed (Citation2006), Allegrini and Greco (Citation2013), and Alzeban (Citation2020) acknowledged that highly leveraged firms may deal with higher agency costs. Companies with a high level of debt try to reduce agency costs by disclosing more information. Leverage ration (LEV) is measured by the total book value of debt divided by total assets.

Profitability ratios are used in previous research on corporate disclosure (Khan et al., Citation2013; Mousa et al., Citation2018; Owusu Ansha & Ganguli, Citation2010). Therefore, we considered profitability ratio as an independent variable expecting that the ratio has a positive relationship with level of disclosure. In the study, the profitability ratio is measured by the ratio of net profit divided to total assets.

4. Empirical analysis and results

4.1. Cronbach alpha test

shows the alpha coefficient for the 81 items equivalents to 81 questions of VLCA scorecard. The alpha coefficient is 0.896 suggesting that the items have relatively high internal consistency with the specific sample (Henseler & Chin, Citation2010).

Table 4. Reliability statistics

Appendix 2 presents items-total statistics results, any item with total correlation less than 0.3 and Cronbach Alpha less than 0.6 should be eliminated from the scale. The final column “Cronbach Alpha if item deleted” shows the result that removal of any question would result in a lower Cronbach Alpha. Therefore, we would keep the set of questionnaires. Moreover, the Cronbach Alpha values above 0.6 and 0.7 are considered fitting in exploratory studies (Hair et al., Citation2014).

4.2. Descriptive statistics

Panel A of represents the descriptive statistics of corporate governance disclosure for the research sample. The mean disclosure score for overall sample is 52.69, with a range from a minimum of 12.37 to a maximum of 89.56. The evaluated result shows that the CGD of companies in research sample is relatively high with a small fluctuation of standard deviation. A clear indication that the research categories achieves average quality of corporate governance disclosure includes compliance and current practices.

Table 5. Descriptive statistics for dependent and independent variables (n = 210)

Panel B of presents the descriptive statistics of independent variables. The data revealed that the average number of non-executive member or independent member who do not engage in the day-to-day management of the company is approximately above 3 and the minimum number non executives in the board is 2. This figure reveals that at least 2 people remains independent in the audit committee.

The result also illustrates that the average audit committee size for the study is 4.68 with the minimum and maximum number of members range from 3 to 7. The analysis of statistic states that the larger size of a company is, a bigger audit committee size capture. In comparison to listed companies of developed countries, the size of audit committee in the research is relatively small. Prior research in existing literature review reported that board size members generally array from 7 to 20 with an average of 14 members (Velte, Citation2018; Din et al., Citation2021).

The average number of female executives in the audit committee was approximately above 1, whereas the largest comprised of four members and the smallest included only one female person. This figure indicates that make counterpart dominates the committee.

Additionally, the mean of audit committee members with financial expertise was 4.84, which illustrates the considerably high proportion of financial profession in the committee. In some companies 5 out of 6 audit committee members are financial expert with professional qualification.

On average, the frequency of audit committee meeting during a year is 4 meetings which indicates that audit committee meeting is normally organized once per quarter. There is only one case that audit committee meeting is held every six months.

4.3. Correlation analysis

examines the Pearson correlation matrix for the dependent variable (CGD) and independent variables (ACI, ACGD, ACFE, SIZE, FACM) applied in the study. The table generally illustrates low correlation among independent variables. It is evidence to state that there is no indication of material multicollinearity in the proposed model. When it comes to the relationship between CGD and independent variables, it reports that there is considerable connection between ACI, ACFE and SIZE and CGD. Firms that maintain large audit committee in term of size provide a higher level of corporate governance disclosure. The number of financial expertise (ACFE) and non-executive directors (ACI) represent in audit committee also have connection with CGD. Other variables of audit committee gender diversity and frequency of audit committee meeting appear not to have any relationship with CGD.

Table 6. Pearson correlation matrix

Table 7. Breusch and Pagan Lagrangian test result in random effects regression model

4.4. Multi-collinearity test

After conducting the OLS regression, we applied random effects GLS regression model (REM) and fixed effects model (FEM) to examine the relationship between CGD and audit committee characteristics. The result of REM and FEM model in appendix 3 and 4 respectively.

In the next step, the Breusch and Pagan Lagrangian multiplier test was conducted to examine the random effects. The following hypothesis is given for the Breusch and Pagan Lagrangian test:

H0: data is homoscedastic

H1: data is heteroscedastic

The Wald test is also applied to examine the heteroskedasticity phenomenon. The following hypothesis is given for the Wald test:

H0: data is homoscedastic

H1: data is heteroscedastic

Finally, we conducted the Hausman test to consider more suitable model between FEM and REM. The following hypothesis is given for the Hausman test:

H0: The difference in regression coefficient is not systematic

H1: The difference in regression coefficient is systematic

Finally, after conducting the Breusch and Pagan Lagrangian test, Hausman test and Wald test, the result shows that FEM is reasonable model to apply ().

4.5. Multiple regression result and discussion

The indicated the association between audit committee characteristics and corporate governance disclosure. Given the R-squared value, the result illustrates that 47.3% of the variations in the level of corporate governance disclosure can be explained by variations in explanatory variables. The model can be confirmed reliable by the significant F value of 13.686 (p-value = 0.000)

Table 8. Wald test result in fixed effect regression model

Table 9. Wald test result in fixed effect regression model

Table 10. Multiple regression analysis

For the explanatory variables, the independence of audit committee has a significant positive effect on the level of corporate governance disclosure at significant level of 5%. The hypothesis H1 is supported and consistent with prior finding of Akhtaruddin and Haron (Citation2010) The positive relationship exists for listed companies in Vietnam states the role of independent executives to enhance the CGD. The coefficient of awarded companies for ACI (β = 0.408) indicates a strong and positive association. The identification also confirm that independence is an important characteristic that help audit committee effectively monitors and motivate the CGD. In our research sample, audit committees are composed by a majority of independent directors and their diligence is found to be positively correlated with the level of corporate governance disclosure.

The hypothesis H2 is not supported as the result reflects no association between level of corporate governance disclosure and the number of female directors in the committee. The coefficient is low and more importantly, the P-value statistically illustrate insignificant at 1% level. This result is not consistent with prior research of Ghafran and Yasmin (Citation2018), Zalata et al. (Citation2018), and Din et al. (Citation2021) confirmed that female directors are cooperative towards subordinates, conservative towards financial disclosures and actively participate in board meetings. In the context of Vietnam-listed companies, this characteristic appears no important impact on CGD. Additionally, the perspective that more diversity in the audit committee is not equal to promote corporate governance disclosure. Hence, members in the audit committee are equally expected to be proficient to enhance the CGD.

When it comes to the audit committee financial expertise, the P—value statistically illustrate insignificantly impact at 5% level. The result indicates unimportant role of financial expertise in audit committee to promote CGD and that hypothesis H3 is not supported. The existing literature review addressed the result that financial expertise could enhance the quality of annual financial statements. However, the research study does not reflect the same phenomena in the case of corporate governance reports. The result implies that the availability of members with financial knowledge and experience do not lead to a promotion of CGD.

illustrates the positive and significant association of audit committee size (represented the number of AC members) and support the hypothesis H4. This result is different with prior research which specified that increased board size might not actually reflect a higher level of corporate governance disclosure. The prior research such as Omotoye et al. (Citation2021) explained that a large audit committee is equivalent to more opinions, which might cause conflicts, limit faster decision making and reduce performance. However, in the context of this study on Vietnam-listed companies, the research result suggests that firms with larger audit committee show greater transparency for outside shareholders. In addition, larger audit committee could contribute to mitigate agency conflicts among different types of shareholders Alzeban (Citation2020) by giving more opportunities for minority shareholders and improve the control environment.

The last characteristic is examined in the research is the Frequency of Audit Committee Meeting. The hypothesis H5 is proposed to test whether there exists a positive relationship between the number of audit committee meeting and the level of CGD. In addition, the Vietnamese regulation and standards recommend the frequency of meeting that should be a minimum of three or four meetings a year. However, the research result show that there is no association between CGD and FACM as the P-value is insignificant at 1% level. This result could indicate that meeting is formal appearance of the board, however, it does not promote the level of CGD as audit committee maintain ongoing oversee role on corporate practices.

With respect to other variables, only firm size (SIZE) is significantly positive for CGD indicating that it is a very important firm attribute associated with the CGD policy. The finding is consistent with previous studies such as Barako et al. (Citation2006), Khan et al. (Citation2013), and Raghunandan et al. (Citation2003), When it comes to leverage (LEV) and profitability ratio (ROA), the statistical result reflects no significant association suggesting that highly geared and profitability firms do not have any sign of corporate governance disclosure. It is probably not surprisingly because Vietnamese highly geared and profitability firms may demand disclose financial information which is primarily for shareholders rather than declare more internal corporate governance information.

In summary, the research result indicates the positive effect of audit committee independence, size of the committee and size of the firm on CGD of Vietnam-listed companies. The result is consistency with most previous studies such as Akhtaruddin and Haron (Citation2010), Elfeky (2016) found the audit committee characteristics and CGD linkage to be linear. In the context of Vietnam, the result also agree with almost all prior studies that there are two identified factors affecting level of disclosure, namely, the size of the committee and the ratio of foreign independent member to the total number of the board (Hoang et al., Citation2018;). However, the specific analysis is diversified when it comes to region area. Nguyen et al. (Citation2020) conducted a research on listed companies on Hanoi Stock Exchange (HNX) revealing that the proportion of female directors (gender diversity), deputy CEO (audit committee independence) and state holding had a significant correlation with corporate governance report publication. In contrast, the proportion of independent directors was found to be insignificant. This result could demonstrate the difference in policy setting across Vietnam.

5. Conclusion

A basic and fundamental concern is the association between the audit committee characteristics and corporate governance disclosure on corporate governance reports of listed companies in Vietnam. The study tests for correlations with a number of independent variables relating to audit committee characteristics and corporate governance disclosure. The independent variables including audit committee independence, audit committee gender diversity, audit committee financial expertise, size of audit committee and frequency of audit committee meeting are derived from previous research.

In order to achieve the fundamental objectives, the study first examines the reliability of the dependent variable (CGD) by assessing the VLCA scorecard with 81 questions across four categories. The result reveals that the set of questionnaires is internal consistent. In other words, the test items are considered to be valid and reliable for exploratory studies.

The study then tests the relationship between corporate governance disclosure and audit committee determinants. The result reveals a significant positive association between audit committee independence, size of audit committee and corporate governance disclosures. However, other variables including audit committee financial expertise, audit committee gender diversity, and the frequency of audit committee meeting illustrate no association with corporate governance disclosure. The findings suggest that independence and size of audit committee are important factors influencing corporate governance disclosure in the context of Vietnam. However, there is a research limitation in using non-executive directors as a proxy of audit committee independence. In fact, it is not reliable for non-executive directors to be independence.

Firm size is significantly positively associated with corporate governance disclosure indicating that larger firms provide more information. This could be explained by the greater incentives of financial capacity. On the other hands, leverage and profitability ratio have no impact on corporate governance disclosure.

In spite of several limitations, further research could expand sample size to other listed financial companies to test the level of corporate governance disclosures. Future research also examine the effect of other attributes to have more comprehensive explanation about corporate governance disclosure.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Hong Hanh Ha

Dr Hong Hanh Ha is a senior lecturer of Accounting and Auditing School, National Economics University (NEU), Hanoi, Vietnam. She has been teaching as a full-time lecturer at National Economics University for 12 years. Her major research focuses on accounting, auditing, accounting information system and internal control. She has published several research papers on these areas in national and international journals.

References

- Abdul Rahman, R., Haneem Mohamed Ali, F., & Haniffa, R. (2006). Board, audit committee, culture and earnings management: Malaysian evidence. Managerial Auditing Journal, 21(7), 783–31. https://doi.org/10.1108/02686900610680549

- Adegboye, A., Ojeka, S., Alabi, O., Alo, U., & Aina, A. (2019). Audit committee characteristics and sustainability performance in Nigerian listed banks. Business: Theory and Practice, 2(2), 469–476. https://doi.org/10.3846/btp.2020.10463

- Adelopo, I. (2011). Voluntary disclosure practices amongst listed companies in Nigeria. Advances in Accounting, 27(2), 338–345. https://doi.org/10.1016/j.adiac.2011.08.009

- Afza, T., & Nazair, M. (2014). Audit quality and firm value: A case of Pakistan. Research Journal of Applied Science, Engineering and Technology, 7(9), 1803–1810. https://doi.org/10.19026/rjaset.7.465

- Ahmed, K., & Curtis, J. K. (1999). Associations between corporate characteristics and disclosure levels in annual reports: A meta-analysis. The British Accounting Review, 31(1), 35–61. https://doi.org/10.1006/bare.1998.0082

- Ahmed, K., & Nicholls, D. (1994). The impact of non – Financial company characteristics on mandatory disclosure compliance in developing countries. The case of Bangladesh. The International Journal of Accounting, 29(1), 62–77.

- Akhtaruddin, M., & Haron, H. (2010). Board ownership, audit committees’ effectiveness and corporate voluntary disclosures. Asian Review of Accounting, 18(3), 245–259. https://doi.org/10.1108/13217341011089649

- Aldamen, H., Hollindale, J., & Ziegelmayer, J. (2018). Female audit committee members and their influence on audit fees. Accounting and Finance, 58(1), 57–89. https://doi.org/10.1111/acfi.12248

- Alia, M. J. A., & Mardawi, Z. M. (2021). The impact of ownership structure and board characteristics on corporate social responsibility disclosed by Palestinian companies. Jordan Journal of Business Administration, 17(2), 254–277.

- Allegrini, M., & Greco, G. (2013). Corporate boards, audit committees and voluntary disclosure: Evidence from Italian listed companies. Journal of Management Government, 17, 187–216.

- Almaskati, M. M., & Hamdan, A. M. M. (2017). Corporate governance and voluntary disclosure: Evidence from Bahrain. International Journal Economics and Accounting, 8(1), 1–26. https://doi.org/10.1504/IJEA.2017.084876

- Alsaeed, K. (2006). The association between firm specific characteristics and disclosure: The case of Saudi Arabia. Managerial Auditing Journal, 21(5), 476–479. https://doi.org/10.1108/02686900610667256

- Alzeban, A. (2020). The relationship between the audit committee, internal audit and firm performance. Journal of Applied Accounting Research, 21(3), 437–454. https://doi.org/10.1108/JAAR-03-2019-0054

- Ananzeh, H., Al Amosh, H., & Albitar, K. (2022). The effect of corporate governance quality and its mechanisms on firm philanthropic donations: Evidence from the UK. International Journal of Accounting and Information Management, 30(4), 477–501. https://doi.org/10.1108/IJAIM-12-2021-0248

- Anderson, R. C., Mansi, S. A., & Reeb, D. M. (2004). Board characteristics, accounting report integrity and the cost of debt. Journal of Accounting and Economics, 37(3), 315–342. https://doi.org/10.1016/j.jacceco.2004.01.004

- Appiah, K. O., Awunyo-Vitor, D., Mireku, K., & Ahiagbah, C. (2016). Compliance with international financial reporting standards: The case of listed firms in Ghana. Journal of Financial Reporting and Accounting, 14(1), 131–156. https://doi.org/10.1108/JFRA-01-2015-0003

- Barako, D. G., Handcock, P., & Izan, H. Y. (2006). Factors influencing voluntary corporate disclosure by Kenyan companies. Corporate Governance: An International Review, 14(2), 107–125. https://doi.org/10.1111/j.1467-8683.2006.00491.x

- Bedard, J., & Gendron, Y. (2010). Strengthening the financial reporting system: Can audit committees deliver? International Journal of Auditing, 14(2), 174–210. https://doi.org/10.1111/j.1099-1123.2009.00413.x

- Bilal, B., Chen, S., & Komal, B. (2018). Audit committee financial expertise and earnings quality: A meta-analysis. Journal of Business Research, 84 March 2018 , 253–270. https://doi.org/10.1016/j.jbusres.2017.11.048

- Boateng, R. N., Tawiah, V., & Tackie, G. (2022). Corporate governance and voluntary disclosures in annual reports: A post international financial reporting standard adoption evidence from an emerging capital market. International Journal of Accounting and Information Management, 30(2), 252–276. https://doi.org/10.1108/IJAIM-10-2021-0220

- Cadbury Committee (1992), Report of the committee on the financial aspects of corporate governance

- Camfferman, K., & Cooke, T. (2002). An analysis of disclosure in the annual reports of U.K and Dutch companies. Journal of International Accounting Research, 1(1), 3–30. https://doi.org/10.2308/jiar.2002.1.1.3

- Cheng, E. C., & Courtenay, S. M. (2006). Board composition, regulatory regime and voluntary disclosure. The International Journal of Accounting, 41(3), 262–289. https://doi.org/10.1016/j.intacc.2006.07.001

- Chen, L., Srinidhi, B., Tsang, A., & Yu, W. (2016). Audited financial reporting and voluntary disclosure of corporate social responsibility (CSR) reports. Journal of Management Accounting Research, 28(2), 53–76. https://doi.org/10.2308/jmar-51411

- COSO. (2013). Internal Control Integrated Framework. Committee of Sponsoring Organizations of the Treadway Commission.

- Deegan, C., Rankin, M., & Voght, P. (2000). Firms’ disclosure reactions to major social incidents: Australian evidence. Accounting Forum, 24(1), 101–130. https://doi.org/10.1111/1467-6303.00031

- Din, U. N., Cheng, X., Ahmad, B., Sheikh, F. M., Adedigba, G. O., Zhao, Y., & Nazneen, S. (2021). Gender diversity in the audit committee and the efficiency of internal control and financial reporting quality. Economics Research, 34(1), 1170–1189. https://doi.org/10.1080/1331677X.2020.1820357

- Dwekat, A., Segui-Mas, E., & Tormo-Carbo, G. (2020). The effect of the board on corporate social responsibility: Bibliometric and social network analysis. Economics Research, 33(1), 3580–3603. https://doi.org/10.1080/1331677X.2020.1776139

- El-Bassiouny, D., & El-Bassiouny, N. (2019). Diversity, Corporate Governance and CSR Reporting: A comparative analysis between top – Listed firms in Egypt, Germany and the USA. Management of Environmental Quality, 30(1), 116–136. https://doi.org/10.1108/MEQ-12-2017-0150

- Gerayli, S. M., Pitenoei, R. Y., & Ahmad, A. (2021). Do audit committee characteristics improve financial reporting quality in emerging markets? Evidence from Iran. Asian Review of Accounting, 29(2), 251–267. https://doi.org/10.1108/ARA-10-2020-0155

- Ghafran, C., & Yasmin, S. (2018). Audit committee chair and financial reporting timeliness: A focus on financial, experiential and monitoring expertise. International Journal of Auditing, 22(1), 13–24. https://doi.org/10.1111/ijau.12101

- Girella, L., Rossi, P., & Zambon, S. (2019). Exploring the firm and country determinants of the voluntary adoption of integrated reporting. Business Strategy and Environment, 28(1), 1323–1340. https://doi.org/10.1002/bse.2318

- Grandon, Y., Bedard, J., & Gosselin, M. (2004). Getting inside the black box: A field study of practices in “effective” audit committees. Auditing a Journal of Practice & Theory, 23(1), 153–171. https://doi.org/10.2308/aud.2004.23.1.153

- Green, B. S. (1991). How many subjects does it take to do a regression analysis. Mathematics and Statistics Journals, 26(3), 499–500. https://doi.org/10.1207/s15327906mbr2603_7

- Green, C. P., & Homroy, S. (2018). Female directors, board committees and firm performance. European Economic Review, 102, 19–38. https://doi.org/10.1016/j.euroecorev.2017.12.003

- Hair, J. F.,sJr., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS -SEM). In Journal of the Academy of Marketing Science 40 3 . Sage Publication 414–433 .

- Haji, A. A. (2013). Corporate social responsibility disclosures over time: Evidence from Malaysia. Managerial Auditing Journal, 28(7), 647–676. https://doi.org/10.1108/MAJ-07-2012-0729

- Hanen, B. F., & Jamel, C. (2021). Corporate governance and CSR disclosure: Evidence from European financial institutions. International Journal of Disclosure and Governance, 18(4), 346–361. https://doi.org/10.1057/s41310-021-00117-1

- Harris, M., Yao, H., Tariq, G., Javaid, H. M., & Ul Ain, Q. (2019). Corporate governance, political connections and bank performance. International Journal of Financial Studies, 7(4), 62. https://doi.org/10.3390/ijfs7040062.

- Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1–3), 405–440. https://doi.org/10.1016/S0165-4101(01)00018-0

- Henseler, J., & Chin, W. W. (2010). A comparison of approaches for the analysis of interaction effects between latent variables using partial least squares path modeling. Structural Equation Modeling, 17(1), 82–109. https://doi.org/10.1080/10705510903439003

- Hoang, T. C., Abeysekera, I., & Ma, S. (2018). Board diversity and corporate social disclosure: Evidence from Vietnam. Journal of Business Ethics, 151(3), 833–852. https://doi.org/10.1007/s10551-016-3260-1

- Holland, J. (2003). Intellectual capital and the capital market - organisation and competence. Accounting, Auditing and Accountability Journal, 16(1), 39–48. https://doi.org/10.1108/09513570310464264

- Hossain, M. T., Akter, A., & Li, X. (2017). Corporate governance and corporate social disclosures: A metal – Analytical review. International Journal of Accounting and Information Management, 25(4), 434–458. https://doi.org/10.1108/IJAIM-01-2017-0005

- Ibrahim, E., & Al Harasees, M. (2019). Gender attributes of audit committee members and the quality of financial reports. International Journal of Academic Research in Accounting, Finance and Management Sciences, 9(3), 24–37.

- Jizi, M. I., Salama, A., Dixon, R., & Stratling, R. (2014). Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. Journal of Business Ethics, 125(4), 601–615. https://doi.org/10.1007/s10551-013-1929-2

- Kao, L., & Chen, A. (2019). How a pre – IPO audit committee improves IPO pricing efficiency in an economy with little value uncertainty and information asymmetry. Journal of Banking and Finance, Elsevier, 110(C), 105688. https://doi.org/10.1016/j.jbankfin.2019.105688

- Karamanou, I., & Vafeas, N. (2005). The association between corporate boards, audit committees and management earnings forecasts: An empirical analysis. Journal of Accounting Research, 43(3), 453–486. https://doi.org/10.1111/j.1475-679X.2005.00177.x

- Kend, M. (2015). Governance, firm – Level characteristics and their impact on the client’s voluntary sustainability disclosures and assurance decisions. Sustainability Accounting, Management and Policy Journal, 56(1), 4–78 DOI: https://doi.org/10.1108/SAMPJ-12-2013-0061.

- Khan, A., Muttakin, M. B., & Siddiqui, J. (2013). Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. Journal of Business Ethics, 114(2), 207–223. https://doi.org/10.1007/s10551-012-1336-0

- Liao, L., Lin, T., & Zhang, Y. (2018). Corporate board and corporate social responsibility assurance: Evidence from China. Journal of Business Ethics, 150(1), 211–225. https://doi.org/10.1007/s10551-016-3176-9

- Li, J., Mangena, M., & Pike, R. (2012). The effect of audit committee characteristics on intellectual capital disclosure. The British Accounting Review, 44(2), 98–110. https://doi.org/10.1016/j.bar.2012.03.003

- Madi, K. H., Ishak, Z., & Manaf, A. A. N. (2014). The impact of audit committee characteristics on corporate voluntary disclosure. International Conference on Accounting Studies, ICAS 2014, 19

- Magena, M., & Pike, R. (2005). The effect of audit committee shareholding, financial expertise and size on interim financial disclosures. Accounting and Business Research, 35(4), 327–349. https://doi.org/10.1080/00014788.2005.9729998

- Martínez-Ferrero, J., & García-Sánchez, I. (2017a). Sustainability assurance and assurance providers: Corporate governance determinants in stakeholder-oriented countries. Journal of Management and Organization, 23(5), 647–670. https://doi.org/10.1017/jmo.2016.65

- Martinez-Ferrero, J., Rodriguez-Ariza, L., & Garcia-Sanchez, I. M. (2017). The strength of the board on sustainability assurance decisions. Journal of Small Business and Enterprise Development, 24(4), 863–886. https://doi.org/10.1108/JSBED-02-2017-0044

- Mousa, G. A., Desoky, A. M., & Khan, G. U. (2018). The association between corporate governance and corporate social responsibility disclosure – Evidence from Gulf cooperation council countries. Academy of Accounting and Financial Studies Journal, 22(4), 581–593.

- Mustafa, A. S., Che-Ahmad, A., & Chandren, S. (2018). Board diversity, audit committee characteristics and audit quality: The moderating role of control-ownership wedge. Business and Economic Horizons, 14(3), 587–614. https://doi.org/10.15208/beh.2018.42

- Nguyen, V. T., Le, T. H., & Pham, T. L. (2020). Impact of the board characteristic on earnings management of listed companies on Vietnam Stock Exchange. Journal of Finance, 1 27–38 .

- OECD. (2004). Principles of Corporate Governance (2nd ed.).

- Omotoye, O., Adeyemo, K., Omotoye, T., Okeme, F., & Leigh, A. (2021). Audit committee attributes, board attributes and market performance of listed deposit money banks in Nigeria. Banks and Bank Systems, 16(1), 168–181. https://doi.org/10.21511/bbs.16(1).2021.15

- Owusu Ansha, S., & Ganguli, G. (2010). Voluntary reporting on internal control systems and governance characteristics: An analysis of large U.S companies. Journal of Managerial Issues, 22(3), 383–408.

- Patelli, L., & Prencipe, A. (2007). The relationship between voluntary disclosure and independent directors in the presence of a dominant shareholder. European Accounting Review, 16(1), 5–33. https://doi.org/10.1080/09638180701265820

- Pathan, S., & Faff, R. (2013). Does board structure in banks really affect their performance? Journal of Banking and Finance, 37(5), 1573–1589. https://doi.org/10.1016/j.jbankfin.2012.12.016

- Pearsons, O. S. (2009). Audit committee characteristics and earlier voluntary ethics disclosure among fraud and no – Fraud firms. International Journal of Disclosure and Governance, 6(4), 284–297. https://doi.org/10.1057/jdg.2008.29

- Pucheta Martinez, M. C., & Garcia Meca, E. (2014). Institutional investors on boards and audit committees and their effects on financial reporting quality. Corporate Governance: An International Review, 22(4), 357–363.

- Raghunandan, K., Abbott, L. J., Parker, S., & Peters, F. G. (2003). The association between audit committee characterisitcs and audit fees. Auditing a Journal of Practice and Theory, 22(2), 17–32. https://doi.org/10.2308/aud.2003.22.2.17

- Said, R., Zainuddin, Y., & Haron, H. (2009). The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Social Responsibility Journal, 5(2), 212–226. https://doi.org/10.1108/17471110910964496

- Shamil, M., Shaikh, J., Ho, P.-L., & Krishnan, A. (2014). The influence of board characteristics on sustainability reporting: Empirical evidence from Sri Lanka firms. Asian Review of Accounting, 22(2), 78–97. https://doi.org/10.1108/ARA-09-2013-0060

- Simnett, R., Vanstraelen, A., & Chua, W. F. (2009). Assurance on sustainability reports: An international comparison. The Accounting Review, 84(3), 937–967. https://doi.org/10.2308/accr.2009.84.3.937

- Tauchen, G. (1986). Finite state Markov – Chain approximations to univariate and vector autoregressions. Economics Letters, 20(2), 177–181. https://doi.org/10.1016/0165-1765(86)90168-0

- Thi Thuy Anh, V., & Phan Nha Khanh, B. (2017). Impact of Board Gender Diversity on firm value: International evidence. Journal of Economics and Development, 19(1), 65–76. https://doi.org/10.33301/2017.19.01.05

- Tran, Q. T., & Tran Quoc Trung. (2020). Ownership structure and demand for independent directors: Evidence from an emerging market. Journal of Economics and Development, 22(2), 335–342. https://doi.org/10.1108/JED-03-2020-0022

- Velte, P. (2018). Is audit committee expertise connected with increased readability of integrated reports: Evidence from EU companies. Problems and Perspectives in Management, 16(2), 23–41. https://doi.org/10.21511/ppm.16(2).2018.03

- Zalata, A. M., Tauringana, V., & Tingbani, I. (2018). Audit committee financial expertise, gender and earning management: Does gender of the financial expert matter? International Review of Financial Analysis, 55(5), 170–183. https://doi.org/10.1016/j.irfa.2017.11.002