Abstract

This article aims to provide a visualization of the problems posed by board-diversity, review the latest developments in board members around the world and identify practical implications from innovative articles published in reputable-databases. By categorizing research on board-diversity to identify research gaps and trends and summarizing outcomes and explaining them based on claims in the literature. We reviewed previous literature on the findings of empirical and theoretical perspectives that support some of the claims about directors’ board-diversity in shaping the corporate-governance to provide recommendations for future research. To find distinguished researches from precise literature, the time point spans from 1988 to 2021 and the articles involved in this review are from Web-of-Science. The selection criteria used the tracking keywords: “Board Diversity” and “Diversity of Board”, it results with a total of 133 studies. Which are summarized and research gaps are revealed in the claims that need support through theoretical and pedagogical approaches. We are interested in what they note as one of the revised key findings, where they report that the relation between boardــdiversity and company performance is stronger in corporations that implemented reliable governance than their peers with inadequate governance. We recommend companies to appoint managers of different age groups to allow for greater diversity in values, cognitive abilities, and decision-making experience. Appointing female directors can improve board-diversity by providing a “check and balance” mechanism between different board members. The review saves writers, directors, researchers, and strategists time to research and read, by picking the most excellent and most relevant information on its own and attending it in a focused, easyــto-understand order.

1. Introduction

With the growing demand for stable companies, the current structure of many boards is inconsistent, where the same boards are the bigger rule than the exception. It contradicts the fact that different groups make better, longer and more stable decisions. While small and medium-sized businesses hold the majority of all board positions, they are customarily overlooked in negotiations to increase diversity on boards. As an alternative to the old-style principal-agent conflicts adopted in a comprehensive study of advanced economies, principal conflicts have been recognized as the main concern of Corporate Governance (CG) in emerging economies. The main conflicts between small shareholders and observant shareholders arise from extended family ownership, intense ownership and control, corporate group structures, and the pathetic legal shield of small shareholders. Such principal conflicts change the dynamics of the CG process and in turn require different refinements than those dealing with principal-agent conflicts (Young et al., Citation2008).

The need for CG arose as a result of the adoption of the economic systems of capitalism by many countries that rely on private sector companies for the development of their economies. This leads to the expansion of the size of the company and separation of ownership from management. Companies seek funding from cheaper sources to put their investments in the financial market with safe trade; leads to increased movement of capital across borders (BaLtaher & Bakhtah, Citation2019).

In times of distress and change, companies have realized that the “traditional” perspective is no longer adequate. Innovative voices are wantedــmost of them females (Zehnder, Citation2018). Globally, diversity at the board level is very current, both in the political sphere and in industries, making the wave of change in the corporate agenda similar to the effects caused by the emergence of “Industry 0.4”.

CG came as a response to solve the problem of ownership and management in companies and it is the same in the field of controlled products globally. CG has been instrumental in maintaining the company’s trajectory, affirming its credibility both now and in the future (Ghellab , Citation2019).The boardــofــdirectors is the highest power in the company. They are the legal representatives of the interests of the shareholders and are responsible for the interests and contributions of all kinds of shareholders through their participation in determining the vision and mission of the company. Therefore, it must be characterized by the diversity that gives it the ability to take care of these interests efficiently and effectively. In most countries, the definition of development across the board is heterogeneity of the senior management team; this means that there is a coalition of senior executives with differences in qualifications and values. In short, the diversity of the governing council can be of various aspects, including its characteristics, cultural and functional background.

The Middle East and North Africa comprehended the significance of varying company boards to expand business results (Jamali et al., Citation2007; Loukil & Yousfi, Citation2016; Salloum et al., Citation2019). There have been waves of economic, financial, and social governance in the Arab world, especially in 2010, even in conservative countries (Acemoglu et al., Citation2017; Hodler, Citation2018; Merrill, Citation2017). For example, the kingdom of Saudi Arabia, with the unprecedented expansion in the number of economic rights, and political and social such as financial and government, banking jobs, leadership and administrators (e.g., the appointment of women as managers). Now it is possible to obtain a Premium Residency with the two limited and unlimited sides of the kingdom, where they represent one of the biggest experiments within the Vision 2030 framework to promote the growth of the national economy and the diversity of its interests and opportunities (Kamrava, Citation2012; Merrill, Citation2017; Premium Residency Center, Citation2019; Salloum et al., Citation2019).

Moreover, in a study covering several countries, Terjesen and Singh (Citation2008) found that genderــdiversity in boards is affected by environmental, economic, political and social aspects at the macro level. Thus, national factors such as the legal framework, social norms, and the economy structure can consume a strong impact on preferences, incentives, chances and women’s capability to contribute in employment (Metcalfe, Citation2007; Salloum et al., Citation2019; Ullah et al., Citation2018; World Bank, Citation2013).

Diversification of company boards by gender, age, nationality, political problem of the universal key in accordance with the findings of several global studies (Adams & Ferreira, Citation2009; Gyapong et al., Citation2016; Mahadeo et al., Citation2012; Ullah et al., Citation2018). Some companies sometimes wish to achieve specific goals, which they pay providers for adhering to specific principles at the level of certain accounting policies and legal gaps that have had a significant impact on CG application and on property performance. With a diverse range of different genders, ages, nationalities, backgrounds and sciences, decisions can be made that reflect the rational positions of managers and ethical decisions of managers that are balanced and which in turn contribute to the enrichment of professional corporations’ governance practices. Adverse externalities include several cost-benefit aspects that have been taken into account in decision-making processes. Thereby ensuring the preservation of investor wealth and company value. The diversity of boards has become a feature of the success or failure of companies, resulting in an interest in the application of corporate governance, as in this overview we seek to explore the impact of different boards on the enrichment of the application and practice of CG mechanisms.

The core target of this paper is to review the issues raised by the diversity in the directorsــboard enriching the practice of CG mechanics. Through reviewing the current and historical literature along with the benefits and limitations of various aspects of the relation between boardــdiversity and CG. The research provides a comparative review of previous studies to prove the validity of the hypothesis of previous studies and compares them to prove the validity of the hypothesis, the diversity of scientific members of company boards in terms of age, gender, nationality, and background. Which will assist the board of directors in enriching the implementation of the CG mechanism.

Given the mature nature of this field of study, we have sought to adequately justify their motivation to conduct these researches. The review was made especially in terms of literature review and tried to be explained sufficiently. In addition, the review itself offered unlimited constructive and developmental criticism, explained in terms of analytical approaches and descriptive terms used. The scientific significance of paper from the standpoint of the importance of diversity in the boardsــofــdirectors of corporations, where there are many researches addressing the importance of diversity in the boards of directors in companies. As well as how to keeping abreast of modern trends in administrative thought and accounting to develop CG mechanisms in turn contribute to the establishment of the principle of disclosure both mandatory and voluntary that preserve the wealth of investors and the value of the company and the rights of shareholders.

The importance of search theory in the shadow of the growing interest of the authorities in the application of CG mechanisms to achieve a clear relationship between management and owners. To use the descriptive analysis approach based on the study of the phenomenon through the review of theoretical and empirical studies that have addressed the subject under study. In addition, extrapolation of the results of these studies and the use of comparative and scientific approach methods in the light of previous studies have been the development of what will increase the diversity of the boards and the implementation of CG.

The contribution of this paper is that we take stock of what we know about the board diversity and provide a review of advances in our understanding of the relevance studies. Then we discuss remaining gaps, and deliver an agenda for future research. In order to provide a comprehensiveــoverview and synthesis of current knowledge about board diversity, we performed a semi-structured literature review of 133 articles in the period 1988–2021. We map the existing literature on this topic and, based on our analysis, propose an integrated framework to illustrate current knowledge of theoretical mechanisms linking predecessors, results, and contextual impact, and identify research gaps and emerging topics that may advance fieldــdevelopment.

Our analysis reveals some key emerging topics that could advance the future development of the field. We first identify the need for a clearer conceptualization of diversity in the companies’ board and its aspects. Second, our analysis shows the need for a better understanding of the theoreticalــmechanisms that govern the presence of diversity on the board and shape its impact on the team and the results of the organization. In particular, more work is needed to figure out why the diversity of boards is important to organizations and how they work. Finally, our review exposes the dominance of the Western perspective on board-diversity. We urge future research to explore the concept of board diversity in Arabic societies, situations that do not use the role of the national institutional context in determining the influence of board diversity.

2. Methodology

We take into account for enclosure in this review researches published in top-tier-journals at Web of Science (WOS) database, figuring that articles that published in these journals can be considered authenticated-knowledge and utmost expected to have influence (Podsakoff et al., Citation2012; Tahai & Meyer, Citation1999). To find distinguished researches from precise literature, the time point spans from 1988 to 2021. The selection criteria used the tracking keywords: “Board Diversity” and “Diversity of Board”, it results with a total of 133 studies. We have adopted a board diversity definition as represented in the indices conducted and identified by various studies on how we can measure the level of diversity through corporates boards, as shown in Table below. We follow the methodology of the latest research by Ponomareva et al. (Citation2022).

Table 1. Board Diversity Measurements development over time

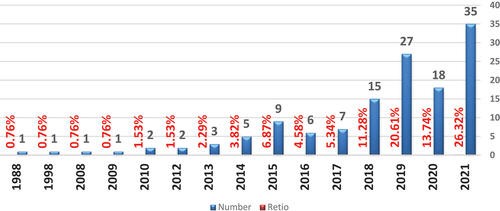

Depends on prior studies (e.g., Bodolica & Spraggon, Citation2018; Chakravarty et al., Citation2021; Hutzschenreuter et al., Citation2020; Kim & Aguilera, Citation2016; Koveshnikov et al., Citation2019; Nielsen et al., Citation2017; Wang et al., Citation2020) our review followed 3 phases: (a) choice of key academic journals, (b) detection and scrutiny of papers within those journals, and (c) search of paper-references to find further relevant articles. Based on the adopted definition, the first stage of data-collection was performed by searching the largest abstracts and citations databases of peer-reviewed documents in WOS. Along with similar reviews, and to ensure quality-control and capture-works with the greatest academic effect, we restricted our search to papers published in peer-reviewed journals. Since the purpose is to explore general developments in the field rather than presenting findings from a limited-number of journals, we did not limit our search to specific journals or publication years. The second stage of data-collection ensures that our search string process does not eliminate any related papers. This process continued until no further references were revealed and our final sample comprised 133 see articles in Figure .

Figure 1. Number of publications (Source: WOS).

3. Review and mapping the fieldFootnote1

Researchers have sought a causal relationship between board diversity and company performance for decades. Demographic diversity is often the focus, as there are different types of factors that can be seen by the audience, such as age, gender, race, etc. includes features which is manageable and manageable through data collection efforts. Studies on board diversity place great emphasis on quantitative approaches with minimal or mixed results, particularly with regard to organizational performance. Existing research has linked manager diversity to a number of important benefits beyond financial performance, such as higher company reputation, increased corporate social responsibility, higher levels of creativity and other performance characteristics. More diverse boards may be capable of thinking about a wider range of solutions and offer access to wider social capital and resources. Research has also shown that the advantages of a more gender-diverse board are only realized when managers move beyond a single female representative (Financial Reporting Council (FRC), Citation2021).

In economics, the theory that analyzes company boards is often found in the procedure of how board representatives come to a harmony. When managers behave differently, it is often because of their internal or external status. Accordingly, most current examination in economics concentrates unequally on the difference between independent and nonــindependent managers as the primary resource of direct heterogeneity (e.g., Adams & Ferreira, Citation2007; Adams et al., Citation2010; Hermalin & Weisbach, Citation1988, Citation1998; Raheja, Citation2005).

Contrasting economists, management professionals often create classifications to explain the different perspectives of boards. For instance, the idea that boards play a vital role in monitoring is often referred to as agency opinion. As an option, or a substitute, from the institution’s perspective, several management scholars are suggesting the idea of resource dependency (Pfeffer & Salancik, Citation1978). Managers are considered key service providers in the firm, such as key external liaison advisors and advisors (suppliers, regulators, financiers, etc.). The diversity of managerial diversity is clearly important when looking at managers as resource contributors. Therefore, utmost of the actual research on non-independent boardــcomposition has been accomplished by management students, experts in the resource dependency process (Ferreira, Citation2010).

The idea is that the approach taken by management professionals is wealthier than the approach taken by utmost economists. Management professionals have no problem employed with numerous theories at once. For instance, Hillman and Dalziel (Citation2003) discuss the potential relationship between board composition accounting and company performance of both resource dependencies. In contrast, economists often only examine the role of oversight boards (agency vision in the management jargon).

While there are still some doubts, the role that boards play has now become a prominent figure in economicsــliterature. For instance, Adams and Ferreira (Citation2007) developed a systematic boardsــmodel, carried into account the role boards play as auditors and management consultants. Critics of the economic approach will stress that the mathematicalــmodel of the dualــrole of boards is redundant. However, management professionals are constantly looking to boards to hold this dualــrole. Yet, economists believe differently. They could ask: Why cannot companies distinguish between the two roles? Why not hire a team to look after the CEO and someone else to offer advice and other resources?

To understand the main topic of the article and to identify notable studies from specific literature, the time point spans from 1988 to 2021. The documents included in this review are from the online database at Web of Science, with the following keywords: Board Diversity and Diversity of the Board, followed by a total of 133 studies. The first study, published in 1988, shows that the participation of diversity in boards/boards began to be a subject of study only 34 years ago.

Definitions of corporate governance have changed a lot, forcing researchers and international organizations as well as professionals to grasp some concepts. Following the Capital Markets Authority in the Kingdom of Saudi Arabia, CG are the rules through which they are promoting the company for thousands of families to organize the various relationships between the board of directors’ management and managers, the conditions that favor the owners. Through the development of procedures to help make resolutions and the nature of the basis therefor to protect the interests of the shareholders, achieving transparency and competitiveness in the market and business environment (Capital Market Authority, Citation2017; Mgammal, Citation2011, Citation2017).

Companies that adopt dialogue principles strengthen their trust and value their investments. This is an indicator of familiarity with the board and management of the governing body surrounding the company. Thus, the company’s capacity to manage and mitigate these risks, helping investors make investment decisions, taking into account the fundamentals of other investments. Cadbury Report 1992 CG is the system by which commercial institutions are monitored, and the IFCFootnote2 defines governance as the system through which a company and its business are managed (Cadbury, Citation1992).

Corporate governance processes attract investors and earn their trust as it provides fairness and transparency to stakeholders. Investors look to professionals to manage their investments due to the lack of time and expertise required to manage those investments. Consequently, there is a need to adopt dialogue to enhance owners’ confidence that the company’s board members and executive management are committed to achieving the company’s goals and upholding their rights (Capital Market Authority, Citation2017).

Boards are the mainstay of governance in companies and organizations in both the public and private sectors, and good governance ensures investors that their investments are being managed well. This ensures that they will not misuse capital or lose money, which is employed to determine the company economicــperformance, which in turn guides to better value for investors, and then to increase corporate value and social welfare. In a nutshell, corporate governance intends that the directors board, on behalf of investors and accountable to managers, holds them accountable for their performance to accomplish the corporation’s purposes.

A company’s directorsــboard has an important role in setting goals and implementing the strategies and policies that govern the company’s operations. As a result, board decisions have a weighty impact on the performance of any company. The rules of corporateــgovernance concentrate strongly on a number of issues interrelated to the boardــformation and the method the company is run, preserving assets and maximizing the wealth of shareholders are the most important of these issues. The board of directors of the company manages us under the authorization of the General Assembly. The ultimate responsibility for the company therefore remains with the board, and if the board establishes committees or authorized organizations or other individuals to carry out some of the work. Although the board of directors contains of representatives nominated from different shareholdersــgroups. When a person is appointed as a member of the board of directors, he would deliberate himself a representative of wholly shareholders who want to determine the interests of his company, not the interest group that voted to appoint to the board.

To highlight the relation between boardــdiversity and corporateــgovernance, Carter et al. (Citation2003) examined the relation between boardــdiversity and corporateــvalue for the Fortune 1000. They called for diversity of the board to include proportions of women, African-Americans, Asians, and Latinos. A pilot guide was presented to test whether boardــdiversity is connected with improving the financialــvalue of a company. After controlling size and industrial sector firms, corporateــgovernance standards have found a positive relationship between the proportion of females or minorities on the board and the value of the corporation. It also shows that the proportion of females & minorities on the board increases with the size of the corporation and the size of the directorsــboard, but the larger the sample size is reduced (Carter et al., Citation2003). This means that companies committed to rising the number of females on their boards similarly have more minorities on their boards and vice-versa. This is important evidence of a positive relation between corporate values and management.

Research conducted by Adeabah et al. (Citation2019) has contributed to the governance structure of banks, e.g., the genderــcomposition of the boards offers insight into the regulators and shareholders to assess the roles of men and females on boards in Ghana. They analyzed the performance of banks with gender diversity on their board of directors and examined the determinants of bank performance. Research shows that gender diversity enhances bank performance with up to two directors on a nineــmember board, showing an initial impact on bank performance. The size of the board of directors has enhanced the efficiency of the bank. Board independence is negative related to bankــperformance, and strong executive heads limit bank performance. Lastly, the authors found that ownershipــstructure, bankــsize, age of bank, ratio of loans to deposits are important factors that affect the efficiency of the bank (Adeabah et al., Citation2019).

Board diversity reflects diversity in corporate board structure in terms of specific features. Studies have described table variations in a number of ways based on specific characteristics (Kagzi & Guha, Citation2018). A. Intuitive and prominent criteria: Boardــdiversity can be described by perceived criteria for instance, age, nationality, gender, and less obvious criteria such as education, employment and job background for board members (Kang et al., Citation2007). B. Structural Diversity/Board Diversity: Structural diversity refers to the following characteristics: size, leadership structure, founder-led director is a director, presence of directors international and their number (Srivastava, Citation2015). C. Board Diversity/Demographic Diversity: Diversity based on people’s background, nationality, gender, age, education, employment and employment background (Ararat et al., Citation2015). D. Non-Taskــrelated/taskــrelated differences: Workــrelated differences are interrelated to educational or occupational background although nonــworkــrelated differences contain age, gender, race and race (Adams et al., Citation2015).

Companies can improve their performance by expanding the number of females on their boards (Unknown, Citation2019). In this context, the research results suggest that the presence of female directors in the meeting room has an important influence on the performance of the company. They show no indication that female directors are making an advance dividend (Arora, Citation2021). On the other hand, the results of other studies clearly show that an organization’s environmental performance has a significant influence on the level of gender diversity in the boardroom (Issa & Zaid, Citation2021). Furthermore, the Safari (Citation2021) results show a Uــshaped inverse association between the degree of board involvement of women and firm performance. The results also explain the presence of the hierarchical maze and the extremely large number of managerial positions (Safari, Citation2021). More, Hosny and Elgharbawy (Citation2021) argue that gender and skill diversity equally affects financialــperformance. Even so, the further diverse sizes, number, network, education and tenure of the board of directors do not affect financial performance. In contrast, race diversity negatively impacts financialــperformance, just as gender diversity of executives negatively affects market-basedــperformance (Hosny & Elgharbawy, Citation2021). Khatib et al. (Citation2021) argue that other diverse features of the board need to be discovered. Correspondingly, they focus on topics related to diversity on the boards of financial firms, such as the indirect effects of policy settings, knowledge capital, environmental performance, etc., innovation and earnings quality of financial institutions, as well as capital structure (Khatib et al., Citation2021). In this context, (Ludwig & Sassen, Citation2022) shows results for different internal CG-mechanisms for example, board independence, board diversity, the board size, the boardــlevel “sustainability committee”, ownership concentration, the role of the CEO, the disclosure and transparencyــpractice, which play a role in managing a company in a sustainableــdirection and accomplishing sustainability integration.

4. Practical cases of diversification of the board of directors

Recently, more and more researchers have focused on the need to diversify boards in terms of skills and gender. An effective board should include members from diverse cultural backgrounds to enhance decision-making, effective disclosure and reflection, shared values, perceptions and experiences. This can lead to heterogeneous organizations poorly coordinated with each other leading to unresolvable conflicts, making it difficult to achieve good governance.

In fact, a huge number of countries worldwide, particularly in EU, have lately taken some form of positive act to address the problem posed by diversification of corporate boards (Ullah et al., Citation2018). In this case, as seen in the Scandinavian countries, great attention was paid to the passage of national legislation to “strict (enforceable in a court of law)” the challenge of having a representative number of managers in trading companies, on stock exchanges and/or stateــowned enterprises (Rose, Citation2007; Terjesen et al., Citation2015). For instance, “Norway, Finland and Iceland” enacted laws in 2003, 2005 and 2010, correspondingly, demanding 40 percent of board members to be woman. The EuropeanــCommission similarly asks all publiclyــtraded European companies to include at least of 40 percent females on their boards of directors (European Union, Citation2012). There are similar “hard” or “soft” policies, laws and policies in other developedــcountries, for instance, “Australia, Belgium, Canada, France, Germany, Ireland, Israel, Italy, Japan, the Netherlands, Spain and Sweden”.

Other example, in Canada, Institut sur la gouvernance d'organisation privees et publiques- IGOPP (Citation2009) published an article on “The Status of Women on the Board of Directors in Canada: Calling for Change”. The issue of diversity in boards remains partially unresolved. To be sure, females’ representation on the directorsــboard has increased during this time [from 15% in 2008 to 29.58% in 2020], but the 40% gender diversity target remains unfulfilled. Today, a comprehensive definition of diversity has been developed, one that indicates the full representation of the many aggregates that make up the social community in which the organization is run. In response to this growing trend, the government of Canada amended the Canadian Business Corporations Act (CBCA) to promote increased diversity in the directorsــboard and upper management of civil society organizations. The reforms, effective on 1 January 2020, aimed at increasing representation of women but equally for Aboriginal people, people with disabilities and minority members. These new legal terms apply to incorporated companies listed on stock (François Dauphin et al., Citation2021).

Developingــcountries have as well identified the value of varied CG boards. Hence, these developing nations have similarly passed a “solid” national law similar to output shares or believe that corporate governance law requires the employment of a particular proportion of females to the firm board of directors (Terjesen et al., Citation2015). For example, in 2010, Kenya passed a law requiring 33 proportion of the directors of stateــowned companies to be females. In the same way, good governance codes in “Brazil, India, Malawi, Nigeria, and South Africa” contain recommendations for gender representation.

Countries in the “Middle East and North Africa”, including provincial states to a high degree, such as “Bahrain, Kuwait, Qatar, Saudi Arabia, Tunisia, the United Arab Emirates”, which have similar reforms aimed at authorizing females and increasing their representation at higher management’ levels (Salloum et al., Citation2019). Moreover, several earlier researches have discussed that the correlation between boardــdiversity and firmــvalue may not only be affected by changes at the organizational level (Baysinger & Butler, Citation1985; Baysinger & Hoskisson, Citation1990), but also by differences in organizational level with the state-level institutional structure (Byron & Post, Citation2016; Grosvold et al., Citation2016; Van der Walt & Ingley, Citation2003). It may therefore influence institutional factors at the state level in the trend and intensity of the relation between boardــdiversity and firm performance (Byron & Post, Citation2016; Estélyi & Nisar, Citation2016; Salloum et al., Citation2019). For example, Sarhan et al. (Citation2018) examined the effect of boardــdiversity on firm performance and executiveــcompensation in the Middle East and North African context. These include Saudi Arabia for the period 2009–2014. Its results are as follows, the influence of variety in the board of directors measuring gender nationality has a positive effect on the financialــperformance of companies. In addition, the relation between boardــdiversity and firm performance was stronger in corporations with good CG adoption than their peers.

However, the Diversity Panel, which measured by nationality, ethnicity and gender of directors, boosts pay sensitivity to performance, but not sensitivity of the executive pay compared to reality. The results of the study indicate that board diversity decisions are not solely affected by ethical values. They arise due to cost and advantage reflections due to the diversity of the corporation’s board of directors. The results are useful for evaluating different options to boardــdiversity measures, such as CG (Sarhan et al., Citation2018). Against this backdrop, a Catalyst report found that 500 wealth companies, including boards of three or more women, have outstripped the performance of boards, where the underrepresentation ratio of women is low, 84% on sales and 60 % return on investedــcapital and 46 % return on equity. In addition, when we examine gender-diverse companies, financial returns exceed the national industry average by 15% according to a study conducted by McKinsey. In 2012, a statistical study of 2360 companies around the world, conducted by Credit Suisse Bank, found that those with at least one woman on their board of directors achieved the best performance yield at stock price up to 26%. compared to the board, miss out on female representation (International Labour Organization, Citation2015).

In terms of social responsibility, Alshareef and Sandhu (Citation2015) determined the characteristics of board diversity that affect board of directors functions that expand the integration of corporateــsocialــresponsibility (C-S-R) in Saudi Arabia into the structure of CG. Alshareef and Sandhu (Citation2015) investigated how the effect of boardــdiversity characteristics on their roles vis-à-vis CSR adoption. As part of the caseــstudy of 2 corporations operating in KSA as a unique case through inــdepth interviews with partakers at different managementــlevels. The results indicate that characteristics of board diversity are necessary to advance the efficiency of board functions of directors (monitoring and information strategy) towards the integration of C-S-R in the governanceــstructure. Based on the results, they help to understand the characteristics of boardــdiversity and the roles that enhance CGــcodes in communicating with stakeholders. They highlights the need to strengthen the election criteria when it comes to the appointment of board members, exclusively in the case of an organizational transformation regarding a sociallyــresponsible company. Further highlights the need to improve the capacity of regulatory systems and the judiciary to build institutional pressures to increase the rate of adoption of corporate social responsibility in Saudi Arabia.

If we talk about the Malaysian board of public companies listed in the Bursa, Malaysia was weaker than expected. The minimum length of stay as a manager in Malaysia is four months and the maximum is 124 months. While the minimum and maximum age is 37 and 56, respectively; where the percentage of 74% of board members have attained the second cycle of higher education (i.e. after high school) as the highest level of education (AbdulWahab, Citation2018). However, if we talk about the board in terms of gender, we see that 91% of board members are male. This shows that it is clear that the boards of Malaysian companies have a strong gender bias. Although this has long been a phenomenon among Malaysian corporate boards, given the recent increase in government efforts to promote gender equality, it is expected to change the current scene in the near future.

According to AbdulWahab, Ntim, Mohd Adnan and Tye (Citation2018) from 2008 to 2015, the development of education level at the board level is down from a tenure on the board. Overall, in 2012, the change in education level is the highest, followed by owning the house, then labor member on the council and then comes the last change in gender. It experienced the post-2012 seesaw period where it became the diversity of possession of the department are the highest, followed by the diversity in the level of education and the development in the age of the members of the council and comes next gender development. This trend has identified challenges for boards to diversify their board membership members in terms of age and gender, taking into account that male managers in the same age group.

In this context, in a study in the United Arab Emirates, the proportion of women on company boards stood at 2.58% in 2018, compared to 1.6% in 2016. This means that the number of females in the directorsــboards of listed companies increased by 71.5% in 2018. Article 40 of corporate governance in terms of controlling candidacy for the board of directors stipulated that the representation of women is d at least 20% of the composition of the directorsــboards. The corporation is committed to disclosing the reasons for the achievement of these women and their commitment to the representation of women on the board of directors in its annual report on governance (Dabbas, Citation2018).

According to the report, which was published in an Egon ZehnderFootnote3 company that specializes in assessing and developing corporate leadership in a group of countries that are “reaching” a record that contains “Argentina, Chile, Hungary, Japan, Saudi Arabia, South Korea and the United Arab Emirates”. These have a proportion of board members of 55% women, below 10 % have 2 or further. But even in these nations, approximately companies are guiding the way with newfangled practices and mixed outcomes (Zehnder, Citation2018).

Harjoto et al. (Citation2019) studied the relationship between nationality, diversity, and the education of managers working on the boards of American companies and the American companies’ social performance (CSP). The measurement of the diversity of citizenship by nationality, of national managers and of the diversity of educational paths according to the countries which obtained them in license and post-diploma. CSP also assessed the companies using the MSCIESGFootnote4 classifications. The study found that diversity of board citizenship and diversity of educational background were positively correlated with CSP. The results indicate that the improving the diversity of nationality and the education of directors can improve the social performance of American companies. As explained, studying the growing trend of foreign citizens in the councils of America can re-focus American companies to be more oriented towards the stakeholders. On the other hand, Guest (Citation2019) research on whether ethnic diversity in the region makes control results more robust. The study explored a range of outcomes, such as executive director compensation, accounting errors, executive director turnover rate, performanceــsensitivity and vesting performance, nonetheless found no evidence to support. Correspondingly finds no evidence that ethnic diversity on boards progresses total corporation performance, even for firms with high agencyــproblems.

5. Diversity of the board of directors towards better corporate governance

Over the years, the Malaysian government and authorities have funded further reforms in the areas of photo management, which were based on the basic concepts of good governance and corporate responsibility and accountability. The diversity of the Board of Directors promotes good governance practices through the “Balance check” mechanism between the different members of the board of directors. The Diversity Council also enhances good governance practices through the sharing of values, experience and understanding between managers. For example, this could benefit the growing field in terms of work balance to avoid the risk of overlapping risks (managers old/or younger), and specialized expertise (the old customers) and technology partners (younger managers). For example, Lin et al. (Citation2018) found that acquired board diversity had a strong impact on innovation in high-tech firms, diverse organizations, firms with small tax problems, and low Tobin’s Q firms. The diversity of boards acquired has a strong influence on the effectiveness of high-tech business plans, emphasis companies, companies with monetary constraints, and Tobin’s Q companies. Likewise, a joint board can make decisions that reflect rational (male managers) and ethical (female) positions which, in turn, contribute to the enrichment of CG’s professional practices. Externalities of unfavorable characteristics include multiple aspects of costs and benefits that have been factored into decision-making processes, thereby ensuring that investors’ wealth and firm value are preserved.

Several studies have confirmed that there is a positive relationship between the presence of females on boards of directors and financialــperformance, which proves that the representation of women adds value to boards of directors as a part important in decision making. This representation is also important to enrich the discussion and its contribution to increasing the return on capital and assets. For example, in Jordan, the existence of female representation on boards of directors has led to a net growth in equity, so that the return on assets for companies where there is female representation of 3.3%, while the proportion is less than 1% in companies where there is no there is no female representation on their boardــofــdirectors. The presence of lady representation also contributes to reducing exposure to risks, attention to career development for women. Having women on gender diversity boards is important to having a board with a diversity of experiences, knowledge, perspectives and new ideas, and finding creative solutions in the shadows of the relationship symbiotic is not competitive between men and women within the competitive global market (Dabbas, Citation2018).

On the other hand, having a woman on the board of directors is progress in itself. Nonetheless it is faraway from a golden standard when the regular number of board members is between 9 and 13 members, while the number of members in each is up to 20 members. There is strong evidence to suggest that it takes lies than 3 females on the board to earn the advantages of Breathing Full. Zehnder (Citation2018) found one of the MSCIFootnote5 studies in 2011 that companies that have at least three women on the board saw an average rise in return-on-equity of 10% incomes per stake increased by 37% in 2016. This “critical mass” modifies together the way the board is operated and the way females can split their visions (Zehnder, Citation2018).

In conclusion, the presence of a woman on the board has no effect. The existence of two is part of a league, but when the number of them reaches three, everything changes. On average, women have more emotional intelligence, this enhances the board’s ability to look at angles and survey the horizon. Let us take a nearer look at the usual number of females on the board by nation. Foremost, leaders in “Australia, Belgium, Finland, France, Italy, Norway and Sweden” all average in excess of 30% women (highest proportion is France 42 per cent). The nation state with the smallest ratio of females on corporate boards are “Japan, South Korea and the United Arab Emirates”. No one of these nations has in excess of 6% females, in KSA equal 1%. If we tracked more women, we would see 13 states reach the magic number of three women where it has the biggest corporations, averagely, 3 or more females on the board, with the 5 nations being “Belgium, France, Germany, Italy, and Sweden” with an average of four or more. All these countries except Sweden are subject to the quota system in the distribution of members (Zehnder, Citation2018).

6. Board of directorsــdiversity and corporate tax planning

Business tax planning activities are necessary to achieve the best tax benefits, including improving after-tax returns and cash flow. These activities are considered beneficial for shareholders or more than tax planning for income investors. However, opponents of tax planning argue that this activity should be discouraged as it entails reputational risks to the business and excessive costs to the business. This varies depending on the terms that police officers may place on tax planning activities, suggesting that there are other factors, including board diversity, that play a role (Mgammal, Citation2015; Mgammal & Ku Ismail, Citation2015). In the relationship between board diversity and tax planning activities, AbdulWahab et al. (Citation2018) found that Malaysian companies responded to the change in governance rules. Additionally, AbdulWahab et al. (Citation2018) suggests that councils that cater in terms of member age and director tenure have lower activities available to this tax prior to the change in CG regimes in 2012, but the coefficient of homogeneity for both is no longer relevant to the interpretation of the level of corporate tax planning after reviewing the rules. This suggests that changing governance rules can be beneficial for the tax administration to limit tax planning activities.

Looking at our situation from a tax filing perspective, the board as well as the members have experience in their field and they have low social status who would engage in tax planning activities despite the risks inherent in the practice of activity planning. On the other hand, from the point of view of the risks inherent in the exercise of tax planning activities, the board of directors has homogenized the place of members who hate risk riding and have less cognitive abilities, they will engage in the activities tax planning to a lesser extent, although the ultimate interest is clear. A heterogeneous board of directors with diverse cognitive abilities, values, behavioral, psychological and social beliefs are expected to normalize the very high tax planning process to optimize costs and benefits. A diverse board is therefore strategically heavily involved in tax planning activities within specific institutions to reap the benefits of tax planning activities, taking into account the risks and costs associated with such activities (Mgammal et al., Citation2018).

7. Gender diversity and CSR assurance

The UK’s CG code indicates that panel efficiency is a function of special table properties, for instance, genderــdiversity (Elmagrhi et al., Citation2017). In addition, Brammer et al. (Citation2007) recorded a significant increase in female director meetings in FTSE 100 companies, to the point where they doubled between 1995 and 2003. Female representation in associations The UK’s GDP continues to grow, as evidenced by the proportion of women participating in the FTSE 100 enterprises to 32.4% in 2019, up from 12.5% in 2011 (International Labour Organization, Citation2020).

The variety of boards is consistent with the central structure of agencyــtheory (Hafsi & Turgut, Citation2013; Marquardt & Wiedman, Citation2016). As stated earlier, the main role of a corporation’s directorsــboard is to monitor the performance of executives and their activities to ensure that the board aims to maximize shareholders’ wealth not the interests of management. Similarly, given the view that boards with more internal managers will act as supervisors in a less effective way than independent boards, similarly it can be predicted that Boards with multiple genders are more effective in monitoring management activities (Marquardt & Wiedman, Citation2016). With this view, Adams Anderson and Augustyn (Citation2009) describe female directors who demonstrate a strong commitment to oversight and are farther likely to join boardــcommittees responsible for supervisory functions such as governance committees. In addition, Bernardi and Threadgill (Citation2011) have shown that diversity improves the decision making procedure because of different perspectives and opinions.

Likewise, Srinidhi et al. (Citation2011) claim that female directors may present different experience and knowledge than male directors in a way that can lead to more productive discussions by the board to reach higher decisions. Ahmad et al. (Citation2018) similarly say that forming a women’s and men’s board of directors will improve the board’s performance in fulfilling its roles for the sake of the portfolio. This fragmentation will address a holistic and comprehensive view of many processes, helping to improve company performance. The link between gender diversity and social activism and its consequences is of great interest in the relevant literature. Furthermore, in Malaysia, Abdullah et al. (Citation2016) found that female directors build the value of other companies and downplay the anthers. The effect is different between performance indicators, board structure, and corporate ownership are not the same. Their results require important feedback regarding the promotion of women in both government and companies.

Mangala (Citation2019) says that female directors are more interested in making decisions regarding ethical issues. In addition, using a sample of the Fortuneــ500 corporations by Bernardi and Threadgill (Citation2011), it was discovered that the greater the number of female directors on a corporation’s board, the greater their commitment to public accountability, which means that the declaration increases. Correspondingly, among other board variations, Hafsi and Turgut (Citation2013) have shown that gender is interrelated to organizationalــperformance. Dienes and Velte (Citation2016) argue that German corporations with a large percentage of lady directors are more likely to report CSR.

Nekhili et al. (Citation2017) have provided strong evidence based on a sample of “French” corporations that participation in CSR reporting can be more economical by improving market prices for companies with the potential to benefit from CSR reporting. Gay diversity instead of companies with male directors; female directors bring into full play the capacity of the sales department to record and manage CSR activities. According to a sample of Chinese firms, Liao et al. (Citation2018) reported that lady directors would enhance the reliability value of CSR reports because they hoped to relate the opportunity of their companies to participate in the CSR verification process. Therefore, because certified CSR will increase the reliability and consistency of integrated reports, we assume that UK companies’ tendency to increase representation of female directors on corporate boards is associated with a higher probability of CSR assurance.

8. Critical thoughts

While still has some doubts, the role of the directorsــboard has now become a major figure in economic literature. Consider the role of the directorsــboard as supervisor and management advisor. However, management professionals are constantly looking for boards to take on this dual role. However, economists think otherwise. They will ask: Why cannot companies split the two roles? Why not leasing a team of folks to take care of the CEO and someone else who will provide advice and other resources? Similarly, for most things, there is a full spectrum of behaviors and factors that merely determine how any organization is at the border. However, progress towards greater gender equality in senior roles has been unhurried. At the forefront of these are specific companies with women in top positions, like Apple or IBM, or with lady CEOs, for example, “Facebook &Yahoo”. Beneath these substantial numbers, however, there are yet limited corporations anywhere there is a 50:50 split across the board.

In United States, looking at the lack of board diversity among private companies, we spent a lot of time talking about diversity among publicly traded companies. But according to some new research by the coalition of diversity action, there are 4,700 board seats at companies funded by 18 leading private equity funds. Companies have gone public in the last two decades, only 49 of which have been held by black directors, just 1% of those thousands of positions since 2000. Research has focused on the issues around diversity and boards for a number of years and but they are increasingly interested in private companies because they do not have the same kind of regulatory accountability. This is really disheartened because as the numbers with regard to these directors is are extremely low just about one percent.

But that is not even the big picture because they also looked at the numbers as it relates to the C-suiteFootnote6 and looked at 843 companies that have listed stocks as part of our portfolio. These 18 companies. That has about 3,800 executives who are not just CEOs COFs general counsel chief human resources and in all those companies there are only 25 black executives. So, when we put that together, the combination of black people on the board and black people in the C-suite, the leadership of these companies, these companies have so much impact to the US economy. Additionally, over $10 trillion in market capitalization and companies are key innovators and disruptors and such key role models are indeed for the rest of tech in the rest of the Silicon Valley. Thus, the impact that these companies have cannot be underestimated and there is the diversity or the lack thereof both in the boards and the senior leadership really was of significant concern.

Hence, we often talk about what these publicly traded companies are doing but sometimes this is happening at the last-minute right before they go public. So, Nasdaq is demanding diversity, and so is Goldman. There are several private equity firms that are also trying to do this. But it all seems to be at the end not the beginning and I mean what is happening is people do business and take risks with people they know. So. if they start a new company or try to fundraise whatever they go to who they feel most comfortable with. They may not necessarily be the most skilled or the best, but they are the people they know. These data show exactly that few efforts are considered to reach far from their homes but they are staying very close to the homes of people they went to college with people they did business with in the past, etc. What we see is a pickup in women only for all white women exclusively still in the back where they have to be. But with a concerted effort, the numbers from the gender perspective of women are improving blacks, we must understand this, I have to say it all the time we have to affirm in our actions if we want to change these results.

To understand what is going on behind regulatory frameworks seems paradoxical and gender-sensitive. Researchers in Iceland observed at both quantitative & qualitative data to find factors that could explain the situation. The agenda of this approach has two main components. Foremost, numerous discuss that given the historical level of maleــdominance in corporations, achieving it to create an accurately egalitarian corporation will require considerable effort through time, and requires major and lasting variations in culture outstrip any organizational change.

Additionally, the interaction between these facilities and what goes on in workers’ homes is too an issue to consider, as such alterations must happen behind millions of households and thousands of facilities people work. It is difficult to examine these hypotheses and researchers wanted to do so with a survey of corporateــexecutives and CEOs. The CEOs of companies in Iceland with kids at home-81 of the CEOs responded to the inspection were male, but there were only 11 males. Women are among the initial jump outcomes. In terms of quality, an equal group of men and females were questioned and looked at workــlife balance in detail. Lastly, two sets of outcomes were combined and evaluated, and the researchers reported a goodــlevel of relevance and agreement with each other, confirming the authenticity of their results.

The first significant findings focused on working time, which suggests that men generally workــlonger times during their work. For example, while no female CEO works more than 70 hours weekly, 10% of CEOs and 6% of male CEOs do. Additionally, 58% of female CEOs work 41 to 50 hours a week, while 41% (the largest stake) of female directors work 51 to 60 hours a week. Digging deeper into the conversations helped confirm these findings, and many women criticized the exercise for longer hours than men, and related activities such as socializing and traveling they are far from home.

Furthermore, women report that their male colleagues tend to work longer hours, with 90% of CEOs saying their colleagues work more than 41 hours weekly competed with 52 % of male executives. Afterward, it is noted that the largest pay gap is between male CEOs and their partners, followed by maleــexecutives and their partners. The article now delves into what appears to be a gender inequality that persists, even in some of the greatest genderــneutral societies. The grouping of attitudes and persistent expectations in both work and home cultures can be blamed for increasing gender inequality. While it does not offer any solutions for these problems, in-depth research at least sheds light on how serious the problems are and where they come from, realizing that despite the variability in a businessــenvironment is culturally difficult and nationally nearly unfeasible to see easy way to get out. Where the rate of workــparticipation between females and men in Iceland is the uppermost in EU, with 85% of the world’s women, and accounting for 47% of the total workforce. Regardless of the almost equal division of employees, less than 10 % of big corporations have females as CEOs, and no one of the companies listed on the stock exchange do (Júlíusdóttir et al., Citation2018).

In the UK, corporate governance code has been around for a long time. One of the key issues around code rule is how do we create effective decision-making bodies for the board. That is not just the content of the law, the code that was revised in 2018 is much broader than that. But one of the central issues of the rule is the effectiveness of boards and how they make decisions. Because those decisions affect the company and of course they affect the economy. Furthermore, they affect the wider society and hopefully they improve the performance of companies. That enhances the importance of the wider economy and society and benefits the wider society as well as through sustainable long-term value creation.

Thus, that is why they think it is important to import diversity because diversity is absolutely at the heart of those issues. It is to effective boards effective companies and sustainable value creation now since 2010. The code has coordinated with what was then the Lord Davis review of gender diversity on boards. It later became the Hampton Alexander review and more recently Parker’s review of the MAC and minority representation on the council. Now that is the key to what is been done in the 2018 code, where they put forth a principle of diversity that aims to bring diversity to and to a much broader perspective. Gender and ethnicity are important but other forms of diversity and inclusion are important as well as socioeconomic background particularly important and different types of cognitive power are also important. That is why some researches are interested in a quantitative and a qualitative aspect of diversity.

Developing nations have too known the value of diverse governing boards. Hence, these developing nations have also passed national «solid» laws like to output shares or believe that corporate governance laws require the appointment of a certain percentage of women to the board of directors. Countries in the “Middle East and North Africa”, including the provincial states to a high degree, such as “Bahrain, Kuwait, Qatar, Saudi Arabia, Tunisia, the United Arab Emirates”, which have similar reforms aimed at authorizing females and increasing their representation at seniorــmanagement levels.

In some countries, there is a coalition of senior executives with differences in their qualities and values. Boardــdiversity dignified by directors’ gender and nationality which has a positive consequence on the financialــperformance of companies, such as KSA. In “Argentina, Chile, Hungary, Japan, Saudi Arabia, South Korea, and the United Arab Emirates”, 55 % of board members are women, and less than 10% are two or more. According to another study, the percentage of women on corporate boards in Saudi Arabia is one percent. The studies discussed the need to explore more diverse characteristics of the board rather than focusing on financial institutions on gender diversity in order to make sustained progress. For example, a number of studies show that corporate environmental performance is affected by the level of gender diversity on board. In addition, there are gender differences and abnormalities in the working environment and in the family.

Socially, the attendance of lady directors on the board of directors is meaningfully allied with organizational performance and there is no indication that female directors engage in complex dividend practices. For example, the influence of boardــdiversity measuring the gender of the directors’ nationality has a positive effect on the financialــperformance of companies. In addition, the relation between boardــdiversity and firm performance was solider in corporations with better computer adoption than their peers were the adoption of CG is least. Furthermore, companies that include at least one woman on their boards achieve better performance with stock prices of up to 26% compared to boards, which omits the underrepresentation of women. Equal diversity in skills and gender certainly affects financial performance. For example, several studies have confirmed that there is a positive relation between female representation on companies’ boards and financial performance, which demonstrates that female representation makes add value to the board as an important part of decision making. This representation is also important in enriching the discussion and its contribution in increasing capital and asset returns.

Even so, further diversities, including boardــtenure, education and networking, did not have a significant effect on financialــperformance. Boardــdiversity can be defined by perceived criteria for instance, nationality, age, gender, and less obvious criteria for example, education, employment and work background for members of board. If we talk about the Malaysian directorsــboard of public companies registered in the Bursa, Malaysia has been lower than expected. Of which, 74% of board members have the highest level of education in the second stage of higher education (e.g., after high school). In this regard, improving the diversity of nationalities and educational backgrounds of directors could improve the social performance of American companies.

9. Thoughts on COVID-19 and diversity

Another issue that some studies have shown is that assemblies that adopt diversity of thought at a slower rate have stronger long-term performance. So, there is a tendency to suggest that investors are favoring a gradual approach which is perhaps a bit unfair. But how the COVID-19 pandemic might have affected the thought process about diversity. As we know we have had to live with COVID-19 for a long time but as we emerge from it. In this context, we may have to take a more general look at the thought processes that may emerge from the pandemic and what we have experienced in terms of board diversity and how boards and companies can think about diversity on their boards.

Discuss this to answer the questions that have been raised, what changes have occurred over a period of time and with each type of right to diversify and change. There is something new, success in one variety does not necessarily lead to success in the next. So, it is not like there is only one magic pill to take, we all have our right to be included and suddenly that all changes. This is a long process, it will take time but we need to be patient. To do that, we have to set benefits and rewards and set a whole new set of priorities around resilience, adaptability, etc. In the study looked at, COVID-19 affected women and minorities more harshly than whites and men. But authors do not think at the board level that should be necessarily reflected in any pro anytime in terms of problem in terms of recruiting qualified candidates, thus in that sense it should that diversification should continue to provide increasing benefit. We think it is interesting to come out of the conversations, we guess to touch a little bit on the personality diversity we found and how now the pandemic has led us to switch to virtual platform. Certain board members feel that there is a different dynamic than virtual board meetings. So, members of the board of directors, need to think differently about how they run their meetings. How to include people how might even need to pay more attention to styles where people prefer to reflect before they speak.

To see how the pandemic might affect what happens in the virtual meeting room. There is no doubt that it is definitely affected. It greatly affects the way conversations on the chessboard, as some research results have confirmed. That is a good result in a way, because one of the things we know about working this way is that it tends to balance contributions. Because people who tend to be a little quiet want to assert themselves to make sure people know they are there and that they are engaged and talkative people tend to need a little more listening as they work in this way. Therefore, we think it may also have some positive results. However, we suggest further research on the link between individual diversity and personality and demographic diversity, we think that people from different backgrounds will generally have different views and that is the case. But in terms of actually measuring it and getting a more nuanced picture of it is quite essential, so to be able to say someone is of Asian descent or a woman from a similar socioeconomic status may have the same opinion as someone as the white counterpart for example. Therefore, the complex relationship between individual diversity and demographic diversity is also a key factor.

10. Results, comments and conclusions

In retrospect, boardــdiversity is an intriguing and important area of study in strategicــmanagement. The main objective of this study was to examine the problems posed by board diversity in companies around the world, especially in the selected studies. This has been done by examining the literature perspectives in studies on current and historical aspects of conceptual and psychological limitations and benefits, with respect to aspects of different practices of the board of directors in shaping the corporate governance agenda. Our review discovered several key emerging issues that could enhance the future development of the field. We recognize the need for a purer conceptualization of diversity in the corporations’ board and its features. Review displays the need for a better comprehending of the theoreticalــmechanisms that administrate the attendance of diversity on the board and figure its effect on the team and the outcomes of the business. Moreover, review reveals the dominance of the Western perception on board-diversity.

Thus, how, do we go about getting diverse boards in the broadest sense? How do those diverse boards actually improve decision making through constructive challenge in boardrooms and better discussion and what are the results of that? How does that lead to better corporate performance and the benefits that can bring to the economy and society? The study has several secondary purposes including a desire to help panels deepen their understanding of how they can move beyond the business case conceptualization process to stimulate diversity and discussion of a wide range of diversity categories exists. More importantly provide insights to help boards develop even more effective and impactful strategies to cultivate and maximize the value-add diversity can bring to the boardroom discussions and decisions.

On turning to the business case argument for diversity. Over the past 20 years, we have seen this happen many times over because of the value a diverse board of directors brings to an organization and its stakeholders. This is often referred to as the business case for diversity now. In the early days, this was seen as a way of doing business that focused on addressing the diversity and inclusion opportunities that present themselves. Research over the past 15 years has shown that promoting the business case argument can be a problem because it places an additional burden on disadvantaged groups, unlike those without inequality.

This fact is exacerbated by the fact that increasing the number of unrepresentative constituencies on board or within the organization does not automatically generate benefits. Thus, in order to reap the benefits from the many facets of diversity, one of the key elements required is the active and conscientious support of diverse groups to achieve those benefits. Turn to the question of whether diversity is helpful and moves towards the question of ways that diversity can be effectively facilitated or nurtured and added value in the boardroom. Diversity is a powerful force that can transform economies and societies where businesses manage it well, huge interests manage it poorly and it becomes a source of conflict or sometimes not in a good way.

At this point, we begin with the first question of how board performance and motivation have been affected by the gender and ethnicــdiversity of board members. Overall, we are in agreement with the findings in the current literature on the link between diversity and firm performance. In the sense that not every study we discuss suggests a statistically significant relationship. As we review their studies and findings tell us an absolutely fascinating story not only on the impact of diversity on board efficiency. But also on the path the board must take, implemented to realize those benefits and emphasize the importance of both inclusion and proactive management of diversity management.

For example, regarding actual effects, the research evidence suggests that more genderــdiversity have a positive influence on financialــperformance and it is measured by the EBITDAFootnote7 margin. However, that effect is not immediate, but must last from 3 to 5 years later. What is even more important is what we have found from some research analysis that the better performing companies are more likely to realize those benefits. This suggests that perhaps the management and leadership practices they adopt that enable them to succeed in general also benefit from the right to diversity. Where they observed significant benefits both short and long term that come from just starting the diversity journey. In this particular case, we are talking about the appointment of the first woman on the board. However, the important point is that the journey between just starting or starting to diversify the board and reaching critical mass, it is not a linear journey. In addition, research evidence suggests that simply increasing diversity without making a change to modern culture may not realize benefits or may in fact have some negative impact in both long and short term.

By looking at the stock returns of companies in a number of known related studies, stock returns reflect what’s happening in the boardroom. Based on these studies’ results we suggest that more diverse boards than gender-diverse councils place more emphasis on internal cooperation when they work together, and they also tend to put more emphasis on to engagement with external stakeholders. This helps in analyzing shareholder data that shows that boards of directors that become more diversified over time tend to attract fewer shareholders. We would also like to highlight the fact though that at the moment there are quite a few 350 footsie board in the UK have at least one woman on the board. It is also true that there are many much smaller companies that have not yet started and have yet to embrace diversity.

Several studies observe a weak positive relationship between an increase in ethnic diversity and a decrease in shareholder equity. They can certainly assert that gender diversity governance boards are not the same ethnic diversity laws as they are now. This shows that the code to unlock diversity allows it to be truly different from different types of diversity. The reports go into more detail on those specific characteristics. For example, some studies have found that boards that are more successful at achieving ethnic diversity have practices around establishing and maintaining practices around process monitoring and ratings only emphasize inclusion. This is very important to keep in mind that there are different types of diversity and achieving a true diversity in multiple directions or multiple game actions does take an additional effort.

The question here is, what are the skills and experience attributes that board members will need in the future? So, this broadly reflects what management considers most important for the future, such as strategy and strategic thinking, it makes sense, it is not surprising thing like the digital skill has become a necessity for most executives. Furthermore, what is interesting is that number one is adaptability and resilience to respond to all that has been happening. Thus again, this shows that boards are very aware of the need for diversity and its potential usefulness. Once again, reinforce the view that it is not that boards do not understand that it is important that they can sometimes struggle with the way they deliver diversity. It has a complicated task to arrange all the pieces when there are not many open positions and not many people to go with. Companies have to find the right people with the right skills and then as they add demographic diversity on top of that it becomes an even more complex challenge. We must then ask the question here, what can nominating committees do to implement a more diversity-friendly approach to recruitment? In this context, we think that in some studies, directors are not afraid to switch companies if the company you are working for does not fit that demographic within its niche or struggles with its own diversity. Intrinsically, they do not need outside support to help build the network, do not mind going to an additional network when needed and can work with two or three at the same time.

The next point in this discussion is diversity human resource management. It is important for companies to know their networks and what networks can be built into the network, how they can manage pipelines both within the company. So, when companies knew all that, they had some idea of who could be helpful here in filling a vacancy. In this regard, they must set three clear objectives and report regularly to the entire board, not just the nominating board. Furthermore, to discuss what we mean by diversity. The company should set specific goals for specific groups. So instead of talking broadly about diversity, talk about being very specific and set goals with a regular update. Through the importance of using skill assessment if they use the right experience. The traditional experience for board appointments is CFO or CEO on the board, in fact, if we go by experience, it is very difficult to diversify. So, define the skill sets you need to use or look for, and allow candidates who do not come from exactly this environment to explain why they have these skills that will be useful for your advice. The studies mentioned that it was a long-term game that does not happen overnight and requires perseverance over time, continuous efforts over a relatively long period of time to fully diversify the board. Finally, make sure that the nomination committee itself is sufficiently diverse. Many people have noticed that candidates are too often overlooked because the nomination committee itself does not have such a wide network and there may be reasons why a minority candidate or director does not necessarily want to be on the nomination committee. On the other hand, that those networks need to be picked up to be successful and run a more diversity friendly recruitment process.

Frankly, we note that some research findings reflect the experience many of them have had in working on more diverse boards or leadership teams. This diversity comes with a range of experience perspectives, ideas and solutions that can help improve decision making. But also, to create a truly inclusive culture, which we think is increasingly important for the challenges and levels of uncertainty that businesses face today. We can say that diversity is a long-term set of activities that are relatively complex and require perseverance and constant renewal and thinking and maintaining boards and board composition to ensure that companies continue to increase and improve their diversity at the board. However, chairing diverse councils can sometimes be a little more challenging to reconcile all these diverse perspectives and make decisions. But experts mentioned that the richness of that discussion and debate really does lead to improved decisions and the benefits, we think it helps all to reflect and challenge to continue to learn about diversity and what need to do to continue to improve diversity.

We are looking for new areas of research, especially where we can develop policies regarding the Code of Conduct and the Corporate Governance Code. It is therefore very interesting that some respondents to the one study survey stated that ensuring the diversity of the nomination committee was an important step in the recruitment. We think that few of the bulletin boards have a conversation about what we mean by mainstream diversity, and this is followed by the correct setting of some specific goals and their enforcement with data. In general, boards need to converse more about diversity and push less to ask who is ultimately responsible for the diversity on your board. If the board said that everyone is responsible, but we do not have specific goals, it means that no one is responsible. Things we are hoping that researches will do is stimulate perhaps some unconscious bias that may exist in boards about how they form committees who are on those committees, etc.